presentación de powerpoint -...

TRANSCRIPT

November 2010

[IR Web Site]

2

TELE

VISA

THIS IS

THE WORLD’S LARGEST SPANISH-LANGUAGE MEDIA COMPANYTelevisionBroadcasting

Major supplier of Spanish language programming throughout the world

3Q’10 sign-on to sign-off average audience share of 69.3 percent

21 pay television channels distributed through pay-tv platforms

Over 25 million pay-TV subscribers, as of September, 30, 2010

Pay-TV Networks

Exports programs and formats to television networks around the world

As of 2009, approximately57 countries worldwide

ProgrammingExports

Mexico’s most important DTH satellite television system based on number of DTH subscribers as of 2Q’10(1) and Central America ‘s only DTH platform

The subscriber base as of 3Q’10 reached 2.8 million

Sky

Cablevision, Cablemás and TVI offer triple play services in Mexico City, the surrounding metropolitan area, Monterrey and 49 cities around the country

As of 3Q’10, cable companies reached:• 1.9 million Video RGUs• 770 thousand Data RGUs• 470 thousand Voice RGUs

Cable andTelecom

The most important Spanish-language magazine publisher; as of December 2009 we produced 178 titles under 117 brands

2009 circulation of approximately 153 million magazines in 20 countries

Publishing

Gaming | Televisa Interactive Media | Soccer Teams & Azteca StadiumFeature-film Production and Distribution | Radio | Publishing Distribution

OtherbusinessesTelevisa also has a 40.5% unconsolidated equity stake in La Sexta, a free-to-air television channel in Spain.(1) Information as of June 30, 2010. The information for the third quarter was not available at the time this presentation was prepared.

• Operating Segment Income (1)

growth in• TV Broadcasting – 4.0%

• Cable & Telecom – 25.9%

• Sky – 29.3%

• Publishing – 160.7%

• Consolidated – 11.9%

• Pay TV Platforms• Cable companies reached 3.2 mm

RGUs

• 5.9 million video subscribers in our three cable companies and Sky

3Q’10HIGHLIGHTS

• Revenue growth in• TV Broadcasting – 7.1%

• Cable & Telecom – 37.1%

• Sky – 15.5%

• Pay TV – 17.7%

• Consolidated – 12.3%

• Net Debt Position: Ps.1,163 mm

(1) Operating segment income (loss) is defined as segment operating income (loss) before depreciation and amortization, and corporate expenses.

4

REVENUEBREAKDOWN BY SEGMENTFirst nine months 2010

(1)Equivalent in USD at the FX rate of 12.71947 Ps/US$ . The average of rates published by Mexico’s Central Bank for the first nine months of the year. (2) Growth calculated in peso terms.(3) Cablevision, Cablemás and Bestel grew 16.9%, 11% and 7.2%, respectively during the first nine months of 2010.

USD(1)

mmGrowth(2)

(YoY)

TV Broadcasting 1,247 7.1%

Cable and Telecom(3)

680 31.2%

Sky 658 13.6%

Other Businesses 218 -1.5%

Publishing 180 -5.2%

Pay-TV Networks 180 14.7%

ProgrammingExports

162 -0.8%

TV Broadcasting

38%

Cable and Telecom

20%

Sky20%

Other 7%

Publishing5%

Exports5%

Networks5%

5

OPERATING SEGMENTINCOME(1) - BREAKDOWN BY SEGMENTFirst nine months 2010

(1) Operating segment income (loss) is defined as segment operating income (loss) before depreciation and amortization, and corporate expenses. (2) Equivalent in USD at the FX rate of 12. 71947 Ps/US$ . The average of rates published by Mexico’s Central Bank for the first nine months of 2010. (3)Growth calculated in peso terms. (4) Cablevision, Cablemás, TVI and Bestel had Operating Segment Income margins of 39.5%, 36.8%, 35.1% and 12.2%, respectively during the first nine months of 2010. (5)Other Businesses reported a negative contribution to Operating Segment Income of US$6mm during first nine months of 2010.

USD(2)

MmMargin

(%)Growth(3)

(YoY)

TV Broadcasting 572 46% 4.3%

Sky 299 45% 14.0%

Cable and Telecom(4)

221 33% 28.8%

Pay TV Networks 87 48% -11.9%

Programming Exports

75 46% -9.3%

Publishing 20 11% 31.4%

TV Broadcasting

45%

Sky24%

Cable and Telecom

17%

Pay TVNetworks

7%

Exports6%

Publishing2%

6

Cash & Temporary Investments*Ps.40.6 bn

Total DebtPs.41.8 bn

*Including Ps.3,957.6 million of noncurrent held-to-maturity and available-for-sale investments

BALANCE SHEETONE OF THE STRONGEST IN THE INDUSTRYThird quarter 2010 – Net Debt Ps.1,163 mm*

USD76%

MXN24%

USD66%

MXN31%

Euro3%

7

Average maturity: 14.8 years Issued Ps.10,000 mm 7.38% notes on October

12,2010 due 2020 Issued US$600 mm bond on November 23, 2009

245 spread over treasuries Typically, coupon hedged for up to 30 months

Long-Term Foreign Currency RatingsMoody’s Standard &

Poor’sFitch

Baa1/Stable BBB+/Stable BBB+/Stable

6-Oct-10 19-Oct-10 6-Oct-10

MATURITY SCHEDULEEXCEPTIONALThird quarter 2010 – Total Debt Ps.41,821 mm

69 84

354

- -

175

277

-

500

- - - - - -

600

- - - - - -

300

- - - -

357

- -

600 20

1020

1120

1220

1320

1420

1520

1620

1720

1820

1920

2020

2120

2220

2320

2420

2520

2620

2720

2820

2920

3020

3120

3220

3320

3420

3520

3620

3720

3820

3920

40

US$m

8

WE CONTINUE TO RETURN CASHTO SHAREHOLDERS

*The dividend paid corresponds to the 2010 dividend pushed forward.** Amounts in pesos converted into US dollars at the exchange rate of each payment date.

In May 2009, Televisa paid a dividend of Ps.1.75 per CPO, equivalent to a yield of 4.5%

Additionally, in December 2009 Televisa paid a dividend of Ps.1.35 per CPO, equivalent to a yield of 2.5%

Over the last 6 years more than US$3bn** dollars in the form of dividends and share repurchases

333 387

96

400

214

394

309

2004 2005 2006 2007 2008 2009 2009*

(Dividends - USDmm)

9

DIVERSIFICATION…KEY TO OUR STRATEGYContribution to Operating Segment Income

(1 ) Other Businesses and Pay-TV Networks reported negative contributions to OSI of 1% each.(2) We began consolidating Sky on April 1, 2004 .(3) Other Businesses reported a negative contribution to OSI of (1.0)%. We began consolidating Cablemás in June 2008 and TVI in October 2009.

2000 (1)(2)

9M’10 (3)

TV Broadcasting

86%

ProgrammingExports

6%

Publishing6%

Cable and Telecom 4%

TV Broadcasting

45%

Sky24%

Cable and Telecom

17%

Pay TVNetworks

7%

Exports6%

Publishing2%

Key Business Segments

11

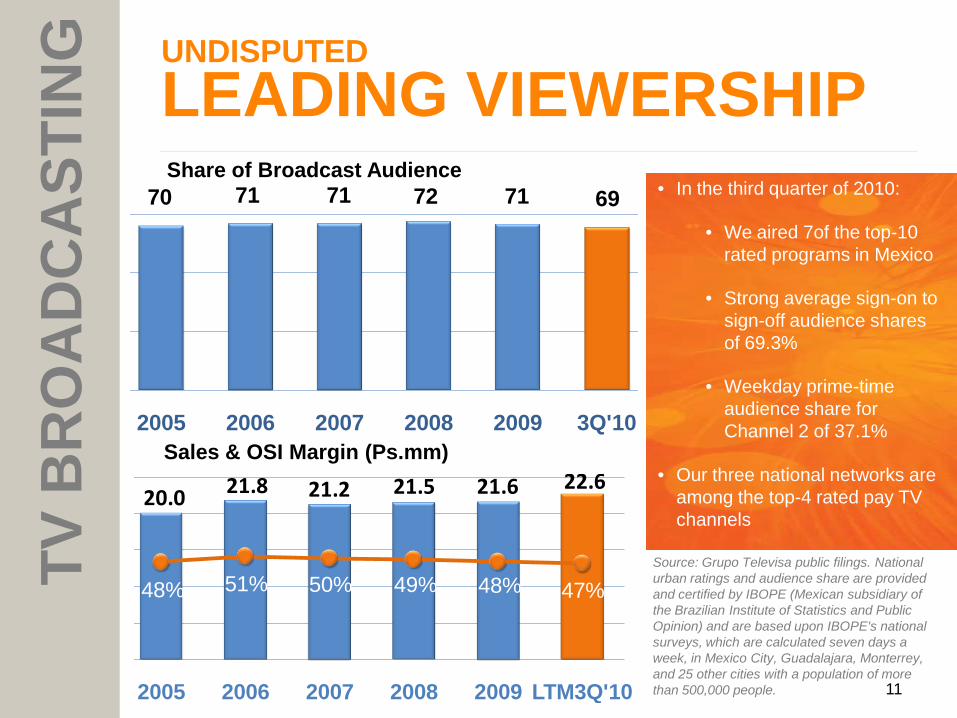

UNDISPUTED LEADING VIEWERSHIP

TV B

RO

AD

CA

STIN

GShare of Broadcast Audience

Sales & OSI Margin (Ps.mm)

• In the third quarter of 2010:

• We aired 7of the top-10 rated programs in Mexico

• Strong average sign-on to sign-off audience shares of 69.3%

• Weekday prime-time audience share for Channel 2 of 37.1%

• Our three national networks are among the top-4 rated pay TV channels

Source: Grupo Televisa public filings. National urban ratings and audience share are provided and certified by IBOPE (Mexican subsidiary of the Brazilian Institute of Statistics and Public Opinion) and are based upon IBOPE's national surveys, which are calculated seven days a week, in Mexico City, Guadalajara, Monterrey, and 25 other cities with a population of more than 500,000 people.

70 71 71 72 71 69

2005 2006 2007 2008 2009 3Q'10

20.0 21.8 21.2 21.5 21.6 22.6

48% 51% 50% 49% 48% 47%

2005 2006 2007 2008 2009 LTM3Q'10

12

CONTINUING OUR EFFORT TOPRODUCE HIGH QUALITY ANDATTRACTIVE CONTENT

In May 2010, we launched “Llena de Amor”, our 8PM telenovela, which delivered solid results, reaching an average audience share of 35.7%

In April 2010 we launched “Soy tu Dueña”, broadcasted at 9PM, achieving a strong 42.7% audience share during third-quarter 2010

Our 7PM Reality show, “Décadas”, aired on Sunday afternoonsdelivered solid audience shares of 24.6%

TV B

RO

AD

CA

STIN

G

Source: National urban ratings and audience share are provided and certified by IBOPE (Mexican subsidiary of the Brazilian Institute of Statistics and Public Opinion) and are based upon IBOPE's national surveys, which are calculated seven days a week, in Mexico City, Guadalajara, Monterrey, and 25 other cities with a population of more than 500,000 people.

13

1999 2006 2009 2003 1997 2001 1999 1999 2000 2002

31.7 29.3

26.0 25.9 25.4 25.0 24.9 24.1 23.9 23.1

Nunca te olvidaré

La fea más bella

Hasta que el dinero

nos separe

Niña amada mía

Esmeralda Salomé Laberintos de pasión

Por tu amor

Por un beso

La otra

Average National Rating (%)

TV B

RO

AD

CA

STIN

G

Three of the four

most successful

novelas ever

produced by

Televisa were

launched within

the last six years

The novela genre isHERE TO STAY

14

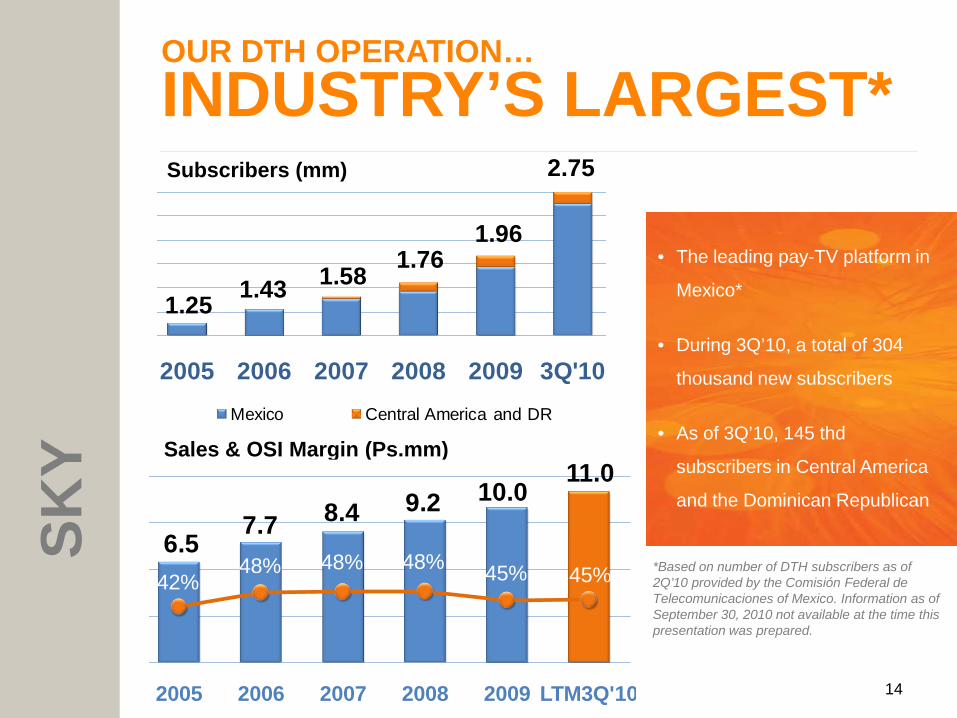

OUR DTH OPERATION…INDUSTRY’S LARGEST*SK

Y

• The leading pay-TV platform in

Mexico*

• During 3Q’10, a total of 304

thousand new subscribers

• As of 3Q’10, 145 thd

subscribers in Central America

and the Dominican Republican

Sales & OSI Margin (Ps.mm)

Subscribers (mm)

*Based on number of DTH subscribers as of 2Q’10 provided by the Comisión Federal de Telecomunicaciones of Mexico. Information as of September 30, 2010 not available at the time this presentation was prepared.

6.5 7.7 8.4 9.2 10.0

11.0

42%48% 48% 48% 45% 45%

2005 2006 2007 2008 2009 LTM3Q'10

1.25 1.43 1.58 1.76 1.96

2.75

2005 2006 2007 2008 2009 3Q'10Mexico Central America and DR

15

KEY COMPETITIVE ADVANTAGE:EXCLUSIVE CONTENT

A must have service for all sports fans due to Sky’s exclusive content

• 24 games of Soccer World Cup

• Key Mexican soccer matches

• Spain’s “La Liga”, and “Copa del Rey” soccer tournaments

• English soccer matches, including “Barclays Premier League”

• NFL Sunday Ticket, NBA Pass, MLB Extra Innings, NHL, Nascar, Golf Channel

In addition to some of Televisa-produced exclusive content

SKY

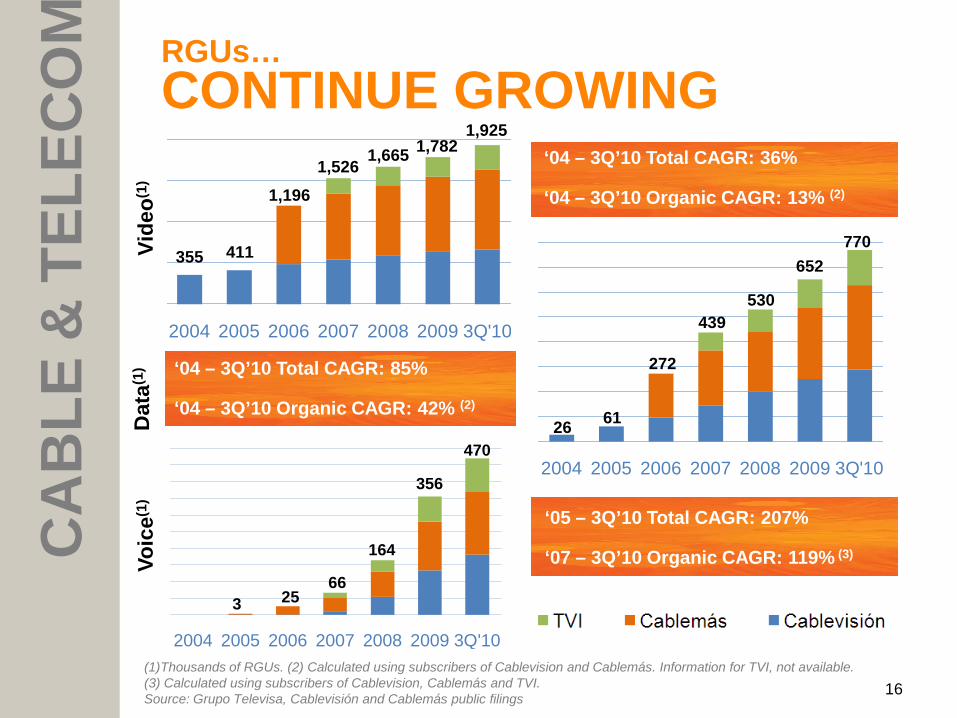

16(1)Thousands of RGUs. (2) Calculated using subscribers of Cablevision and Cablemás. Information for TVI, not available. (3) Calculated using subscribers of Cablevision, Cablemás and TVI.Source: Grupo Televisa, Cablevisión and Cablemás public filings

Vide

o(1)

Dat

a(1)

‘04-3Q’09 Total CAGR: 40%

‘04-3Q’09 Organic CAGR: 13%‘04-3Q’09 Total CAGR: 93%

‘04-3Q’09 Organic CAGR: 43%

Voic

e(1) ‘05 – 3Q’10 Total CAGR: 207%

‘07 – 3Q’10 Organic CAGR: 119% (3)

‘04 – 3Q’10 Total CAGR: 85%

‘04 – 3Q’10 Organic CAGR: 42% (2)

‘04 – 3Q’10 Total CAGR: 36%

‘04 – 3Q’10 Organic CAGR: 13% (2)

RGUs…CONTINUE GROWINGC

AB

LE &

TEL

ECO

M

2004 2005 2006 2007 2008 2009 3Q'10

356

164

6625

470

3

2004 2005 2006 2007 2008 2009 3Q'10

355

1,7821,6651,526

1,196

411

1,925

2004 2005 2006 2007 2008 2009 3Q'10

26

652

530439

272

61

770

17

SPANISH-LANGUAGE PROGRAMMER…TELEVISA NETWORKS

• A major producer of Spanish-language programming for pay TV. In 2009, we produced over 13,300 hours of programming and videos for broadcast on our pay-TV channels

• As of September 2010, our content reached close to 25million subscribers in 49 countries carrying an average of 5.2 pay-TV channels each

• New channel:• TDN – July 2009

Sales & OSI Margin (Ps.mm)

PAY

TV N

ETW

OR

KS

1hr delay

2hr delay

Source: Grupo Televisa public filings and publicly available information

1.2 1.41.9

2.2 2.7 3.047%

51% 62% 62% 61%50%

2005 2006 2007 2008 2009 LTM3Q'10

18

MAIN PROVIDER OF CONTENT FOR THEHISPANIC MARKET

• The transformation episode of the Brazilian version of La Fea Más Bella was among the highest rated shows in its time slot

• Programs in China:

• Destilando Amor• La Fea Más Bella

UVN Royalty Others

On October 5, 2010 we

signed an agreement with

Univision to expand our

strategic relationship in the

United States

Sales & OSI Margin (Ps.mm)

EXPO

RTS

Source: Grupo Televisa public filings and publicly available information

2.0 2.2 2.3 2.4

2.8 2.8

36%41%

46% 44%51% 47%

2005 2006 2007 2008 2009 LTM3Q'10

19

SPANISH-LANGUAGE MAGAZINE PUBLISHEREDITORIAL TELEVISA

• As of December 31, 2009, we published 178 titles under 117 different brands

• Over 153 million magazines distributed during 2009

• In 2009, we reached 20 countries and had a leading position in 18 of them

• More than 100,000 points of sale as of December 31, 2009

Revenue Breakdown LTM3Q’10

Sales & OSI Margin (Ps.mm)

PUB

LISH

ING 2.7 3.0 3.3

3.7 3.4 3.2

19% 19% 19% 18%6% 8%

2005 2006 2007 2008 2009 LTM3Q'10

Mexico43%

Abroad57%

Adverti-sing56%

Circula-tion44%

20

AN ENVIABLE POSITION OFSTRENGTH

Unparalleled production expertise as key differentiator

Resilient broadcasting business

Sky’s exclusive sports content and superior scale

Successful 3play offerings in our three cable TV operations

One of the strongest balance sheets in the industry

Over Ps.40.6 billion* in cash as of 3Q’10, a net debt position of approximately US$1,163 million*

Average debt maturity of 14.8 years

* Including Ps.3,957.6 million of held-to-maturity and available-for-sale investments.

21

This presentation contains statements that constitute forward-looking statements within themeaning of the U.S. Private Securities Litigation Reform Act of 1995. Forward-lookingstatements include statements regarding the current intent, belief or expectations of ourofficers or management with respect to future developments, including such important mattersas (1) our asset growth and financing plans, (2) trends affecting our financial condition orresults of operations, (3) the impact of competition and regulations, (4) projected capitalexpenditures and (5) liquidity. Forward-looking statements are not guarantees of futureperformance and involve risks and uncertainties, and actual results may differ materially fromthose described in forward-looking statements included in this presentation as a result ofvarious factors. These factors, many of which are beyond our control, include the actions ofcompetitors, future global economic conditions, market conditions, changes in interest ratesand foreign exchange rates, changes in legislation or regulations applicable to our business,operating and financial risks, the outcome of legal proceedings and the factors discussedunder “Risk Factors” in our annual report on Form 20-F for the year ended December 31,2009.

As required by Mexican FRS, 2005 – 2007 results presented in Mexican pesos in thispresentation are stated in Mexican pesos as of December 31, 2007, and 2008 – 2010 resultsare presented in nominal Mexican pesos.

FORWARD LOOKINGSTATEMENTS

Carlos MadrazoInvestor Relations Officer+ (52) 55 5261 2446Av. Vasco de Quiroga 2000, A4Col. Santa FeCP. [email protected]

María José CevallosInvestor Relations Manager+ (52) 55 5261 2445Av. Vasco de Quiroga 2000, A4Col. Santa FeCP. [email protected]