presentation by philip verleger at the forum

TRANSCRIPT

PRESENTATION BY PHILIP VERLEGER

AT THE FORUM:

"MARKET LEADERS AND SCENARIOS FOR THE 21ST CENTURY"

March 13, 14 and 15, 2009

“Villa d’Este” – Cernobbio (Como)

Reproduced by The European House-Ambrosetti for internal use only.

1

Oil Prices: Permanently Down or Cyclically Depressed?

Philip K. Verleger, Jr.Haskayne School of Business and PKVerleger LLCFlame 2009Amsterdam, March 10, 2009

Policy Blunders Caused $147/bbl Crude;Depression Could Bring Crude to $20/bbl

The surge in crude prices to $147 per barrel was caused by policy blunders, not resource constraints or growth in Asia.

The price rise resulted from environmental regulations and limits on the supply of sweet crude.

Crude prices collapsed when economic growth slowed.

A long recession could send crude below $20 per barrel for a while. Recovery will come.

2

2

Policy Blunders Caused $147 Crude

Strong global diesel fuel growth and refinery constraints set the stage for a crisis.

Untimely imposition of EU diesel sulfur regulations made the situation worse.

The regulations heightened the need for sweet crude.

Nigerian production losses and U.S. energy policy cut sweet crude supply.

The result was a classic commodity squeeze. 3

Industry Constraints and Economic Circumstances Contributed to $147/bbl Crude

Lack of capacity to remove sulfur made it impossible to use sour crude. It takes 30 barrels of sour crude to replace one lost barrel of sweet.

The euro added to upward pressure because Europe, not China, was the incremental buyer.

New U.S. ethanol regulations reduced refinery throughput and lowered global diesel output.

Higher prices solved the problem. Consumption dropped and prices followed.

4

3

Retail Gasoline and Diesel Prices in Germany and France, 2006-2008

0.800.901.001.101.201.301.401.501.601.70

Jan-06 Jul-06 Jan-07 Jul-07 Jan-08 Jul-08Mon

thly

Ave

rage

Pric

e in

Eur

os

Gasoline in France Gasoline in GermanyDiesel in France Diesel in Germany

Source: PKVerleger LLC.

Monthly NigerianCrude Production, 1999-2008

1.6

1.8

2.0

2.2

2.4

2.6

2.8

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Mill

ion

Bar

rels

per

Day

Source: Energy Intelligence Group.

Aug-07 to Jul-08

4

Monthly Net Distillate Imports/Exports to/fromthe U.S., January 1990-October 2008

-800

-600

-400

-200

0

200

400

600

800

1990 1993 1996 1999 2002 2005 2008

Impo

rts/

Expo

rts

(Tho

usan

d B

arre

ls p

er D

ay)

Source: U.S. DOE.

Exports

Imports

Euro/Dollar Exchange Rate, 2004-2008

1.151.201.251.301.351.401.451.501.551.60

Jan-

04A

pr-0

4Ju

l-04

Oct

-04

Jan-

05A

pr-0

5Ju

l-05

Oct

-05

Jan-

06A

pr-0

6Ju

l-06

Oct

-06

Jan-

07A

pr-0

7Ju

l-07

Oct

-07

Jan-

08A

pr-0

8Ju

l-08

Oct

-08

Dol

lars

per

Eur

o

Source: Platts.

Aug-07 toJul-08

5

Brent and Gasoil Spot Prices,January 2005-January 2009

200

400

600

800

1,000

1,200

1,400Ja

n-05

Jul-0

5

Jan-

06

Jul-0

6

Jan-

07

Jul-0

7

Jan-

08

Jul-0

8

Gas

oil P

rice

($/m

etric

ton)

20406080100120140160

Bre

nt P

rice

($/b

bl)

Gasoil Brent

Source: Platts.

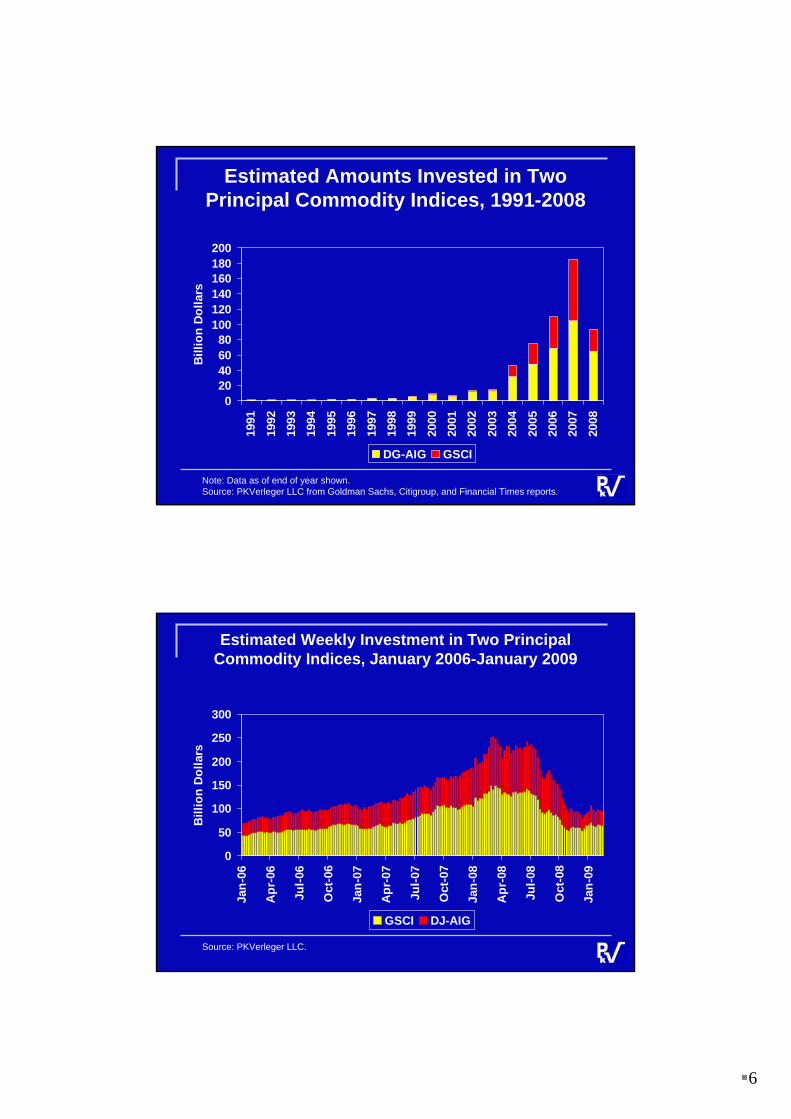

Speculation Did Not Cause the Price Rise

Speculators have been blamed for the price increase.

There is no evidence to substantiate the claim.

Commodities did become a passive investment vehicle. Billions were invested in them.

The investment did promote inventory accumulation.

However, OPEC and Saudi Arabia muted the impact.

10

6

Estimated Amounts Invested in Two Principal Commodity Indices, 1991-2008

020406080

100120140160180200

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

Bill

ion

Dol

lars

DG-AIG GSCI

Note: Data as of end of year shown.Source: PKVerleger LLC from Goldman Sachs, Citigroup, and Financial Times reports.

Estimated Weekly Investment in Two Principal Commodity Indices, January 2006-January 2009

0

50

100

150

200

250

300

Jan-

06

Apr

-06

Jul-0

6

Oct

-06

Jan-

07

Apr

-07

Jul-0

7

Oct

-07

Jan-

08

Apr

-08

Jul-0

8

Oct

-08

Jan-

09

Bill

ion

Dol

lars

GSCI DJ-AIG

Source: PKVerleger LLC.

7

Weekly WTI Price Spread (Third Futureless Cash), January 1986-November 2008

-6-4-202468

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

Dol

lars

per

Bar

rel

Source: PKVerleger LLC.

Investors Begin PuttingMoney into Commodities

Environmental Authorities Beginto Squeeze Sweet Crude Market

Accumulation of GlobalCrude Oil Stocks, 1990-2008

-0.4

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

Bill

ion

Bar

rels

Source: PKVerleger LLC calculated from EIG data on supply and demand.

Date OPEC Actedto Cut Supply

8

OPEC and Saudi Arabia PreventComplete Market Adjustment

Saudi Arabia administers the price of sour crude by setting the price differential to sweet crude.

Sour crude prices could fall to a 50% discount absent such action, providing an incentive for refinery investment.

Instead sour crude supplies are left in tanks, on ships, or in the ground, even with $147 crude.

OPEC’s actions have laid the foundation for the next move in the price cycle.

15

Saudi Discount to Brent Offered to Buyers of Arab Heavy Destined for Europe, 2002-2009

-16

-14

-12

-10

-8

-6

-4

-2

0

Feb-02 Feb-03 Feb-04 Feb-05 Feb-06 Feb-07 Feb-08 Feb-09

Dol

lars

per

Bar

rel

Source: PKVerleger LLC.

9

Movement of OPEC Surplus Crude Capacity vs. Movement of Dated Brent Prices, 1997-2008

012345678

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

OPE

C S

urpl

us C

apac

ity

(Mill

ion

Bar

rels

)

0

20

40

60

80

100

120

140

Bre

nt P

rice

($/b

bl)

OPEC Surplus Capacity Dated Brent Price

Source: PKVerleger LLC.

Price Rise Reversed with Policy Adjustments and Beginning of Depression

Congress stopped DOE from filling the SPR.

Russian invasion of Georgia caused euro to fall.

Refiners changed catalysts, boosting distillate yield.

Economic slowdown began in Europe.

High retail prices cut use in United States.

Chinese use dropped due to end of Olympics and decline in manufacturing.

18

10

Spot WTI Price vs. Strategic Petroleum Reserve Inventory Level

19Source: Platts; U.S. DOE.

Onset of a Long Global Recession Will Keep Prices Low for Several Years

This economic cycle is different. It is a financial crisis.

Financial crises last longer, at least three years.

The loss in GDP is greater. Government debt can be expected to increase by more than 80 percent

Global oil use can be expected to drop at least ten percent by 2011. Recovery could be deferred to 2015.

20

11

Economic Forecasters Missed the Collapse

This is the first major financial collapse in 80 years. Economic models are based on data for the last 30 years and thus have no history.

Financial crises are hard to model. History books offer better lessons. No one reads history books.

Forecasting models cannot be relied upon to predict the end of the crisis. Without history one cannot forecast.

21

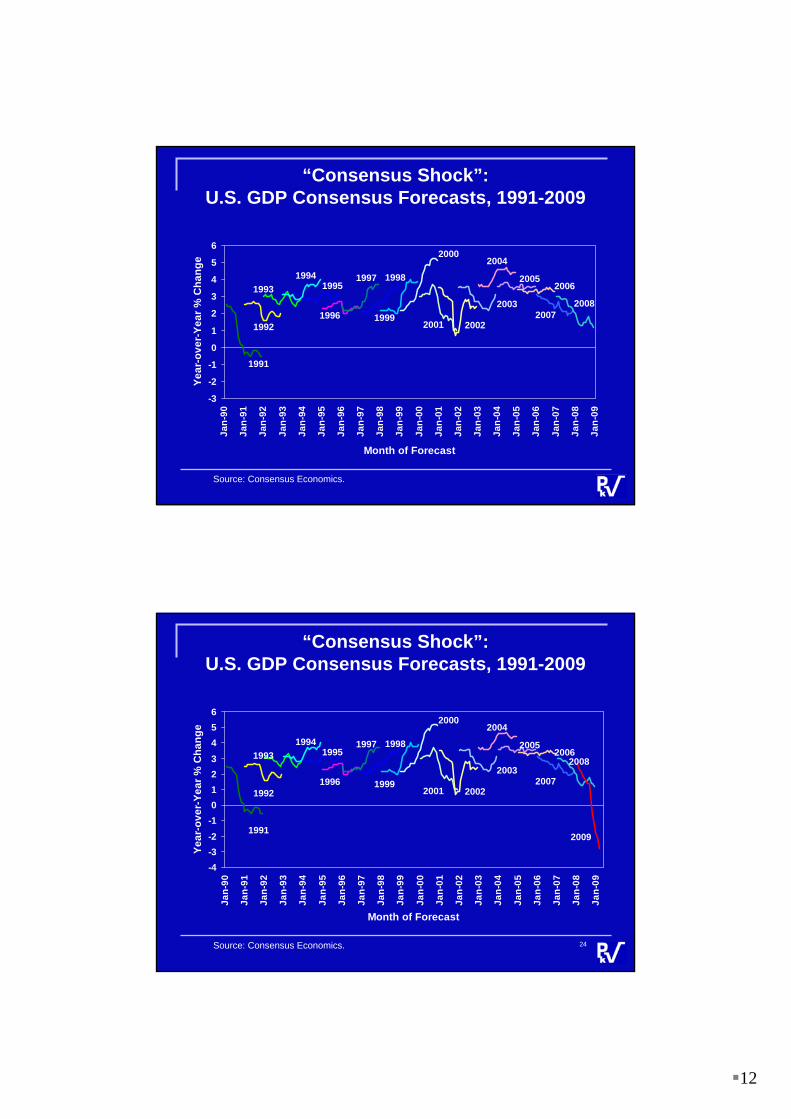

“Consensus Shock”:U.S. GDP Consensus Forecasts, 1991-2009

-3

-2

-1

0

1

2

3

4

5

6

Jan-

90

Jan-

91

Jan-

92

Jan-

93

Jan-

94

Jan-

95

Jan-

96

Jan-

97

Jan-

98

Jan-

99

Jan-

00

Jan-

01

Jan-

02

Jan-

03

Jan-

04

Jan-

05

Jan-

06

Jan-

07

Jan-

08

Jan-

09

Month of Forecast

Year

-ove

r-Ye

ar %

Cha

nge

1991

Source: Consensus Economics.

1992

12

“Consensus Shock”:U.S. GDP Consensus Forecasts, 1991-2009

-3

-2

-1

0

1

2

3

4

5

6

Jan-

90

Jan-

91

Jan-

92

Jan-

93

Jan-

94

Jan-

95

Jan-

96

Jan-

97

Jan-

98

Jan-

99

Jan-

00

Jan-

01

Jan-

02

Jan-

03

Jan-

04

Jan-

05

Jan-

06

Jan-

07

Jan-

08

Jan-

09

Month of Forecast

Year

-ove

r-Ye

ar %

Cha

nge

1991

Source: Consensus Economics.

1992

19931994

1995

1996

1997 1998

1999

2000

2001 2002

2003

2004

20052006

20072008

“Consensus Shock”:U.S. GDP Consensus Forecasts, 1991-2009

-4-3-2-10123456

Jan-

90

Jan-

91

Jan-

92

Jan-

93

Jan-

94

Jan-

95

Jan-

96

Jan-

97

Jan-

98

Jan-

99

Jan-

00

Jan-

01

Jan-

02

Jan-

03

Jan-

04

Jan-

05

Jan-

06

Jan-

07

Jan-

08

Jan-

09

Month of Forecast

Year

-ove

r-Ye

ar %

Cha

nge

1991

Source: Consensus Economics.

1992

19931994

1995

1996

1997 1998

1999

2000

2001 2002

2003

2004

20052006

2007

2008

2009

24

13

Global Economic Growth Rates, 1980 to 2008 andProjected to 2012 Based on Reinhart and Rogoff Results

-2-10123456

1980 1984 1988 1992 1996 2000 2004 2008 2012

% C

hang

e fr

om P

rior Y

ear

History Projection

Source: IMF (history); PKVerleger LLC (forecast).

History and Likely Trend in Global Oil Consumption, 1965-2008 and Forecast to 2012

20

30

40

50

60

70

80

90

1965

1968

1971

1974

1977

1980

1983

1986

1989

1992

1995

1998

2001

2004

2007

2010

Mill

ion

Bar

rels

per

Day

History Forecast

Source: BP Statistical Yearbook; PKVerleger LLC.

14

Year-to-Year Percentage Change in GlobalOil Use, 1966-2008 and Forecast to 2012

-6-4-202468

10

1966

1969

1972

1975

1978

1981

1984

1987

1990

1993

1996

1999

2002

2005

2008

2011

Perc

ent C

hang

e fr

om P

rior Y

ear

History Forecast

Source: PKVerleger LLC.

Oil Prices Will Recover and Surpass2008’s Peaks within Ten Years

Environmental regulations, not “Peak Oil Problems,” will likely send prices above $200/bbl by 2020.

New regulations on sulfur emissions from ships will again squeeze the light crude market. Refiners will be unable to satisfy demand. They will seek sweet crude.

Sweet crude prices will be pulled up. Sour crude will follow thanks to Saudi Arabia. The Depression will be prolonged.

28

15

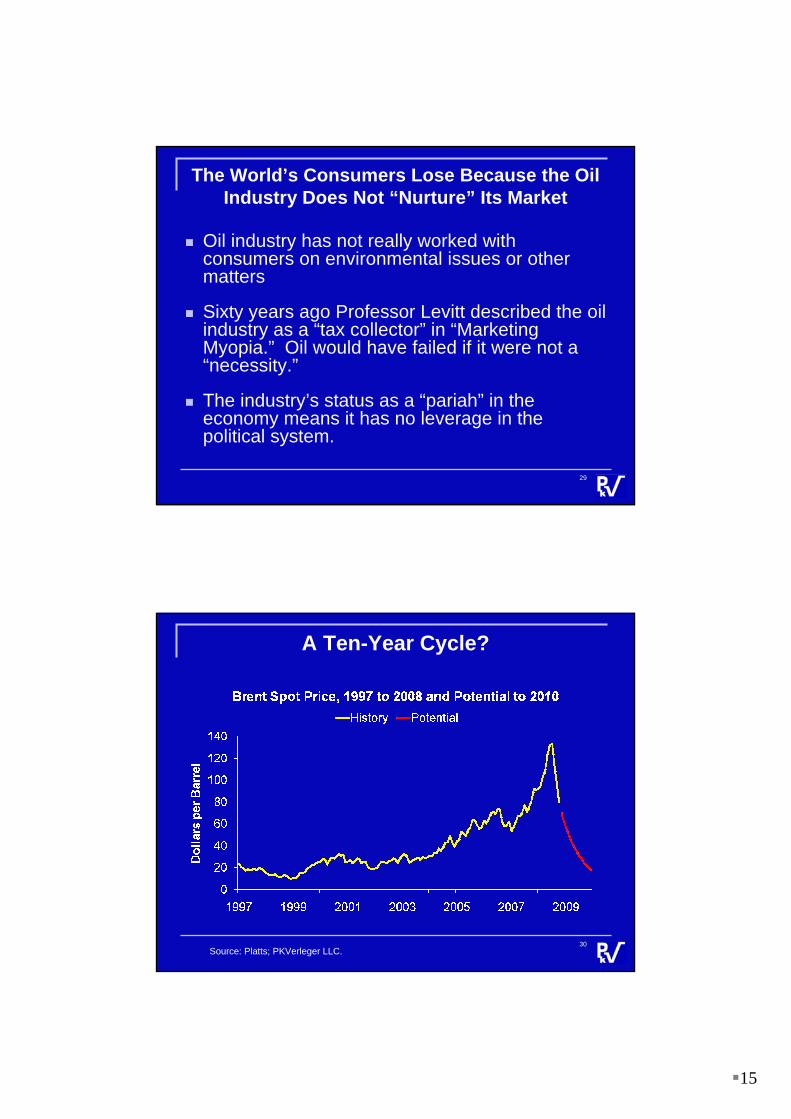

The World’s Consumers Lose Because the Oil Industry Does Not “Nurture” Its Market

Oil industry has not really worked with consumers on environmental issues or other matters

Sixty years ago Professor Levitt described the oil industry as a “tax collector” in “Marketing Myopia.” Oil would have failed if it were not a “necessity.”

The industry’s status as a “pariah” in the economy means it has no leverage in the political system.

29

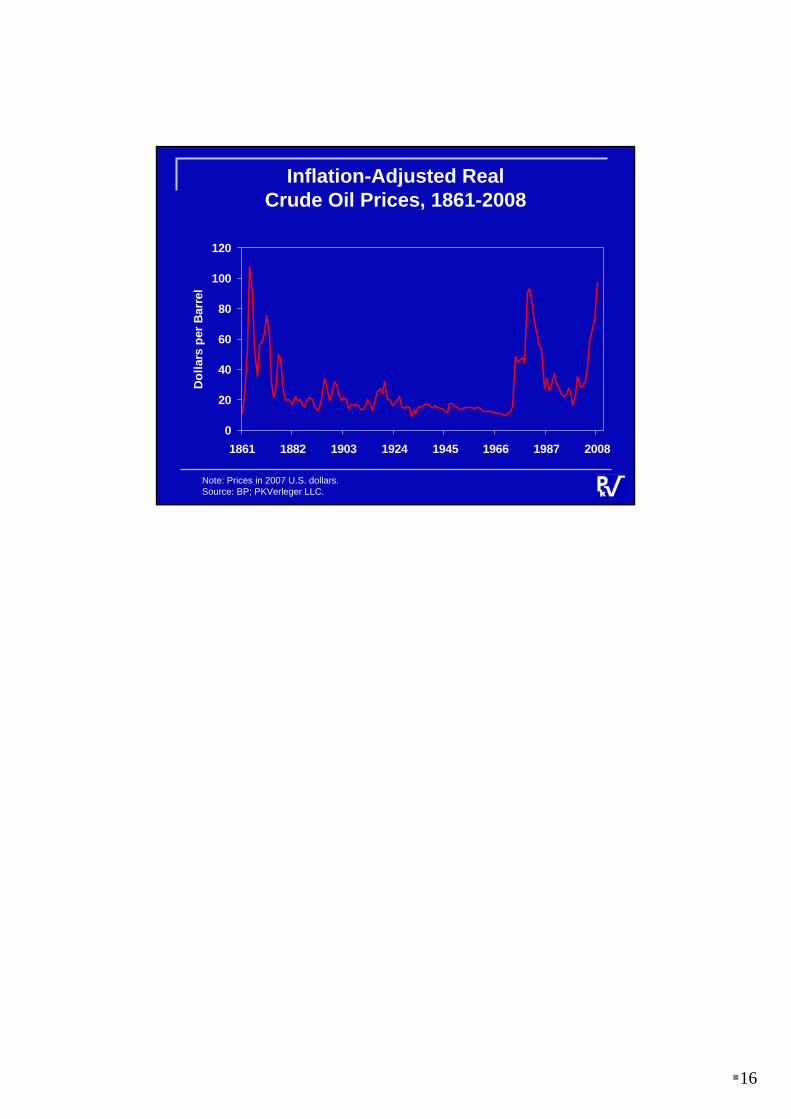

A Ten-Year Cycle?

30Source: Platts; PKVerleger LLC.

16

Inflation-Adjusted RealCrude Oil Prices, 1861-2008

0

20

40

60

80

100

120

1861 1882 1903 1924 1945 1966 1987 2008

Dol

lars

per

Bar

rel

Note: Prices in 2007 U.S. dollars.Source: BP; PKVerleger LLC.