presentation institutional 3q17 - bb · 2017-11-20 · institutional presentation 3q17. this...

TRANSCRIPT

Institutional

Presentation 3Q17

This presentation may include references and statements,

planned synergies, estimates, projections of results, and future

strategy for Banco do Brasil, its Associated and Affiliated

Companies, and Subsidiaries. Although these references and

statements reflect the management’s belief, they also involve

estimates and unforeseen risks. Consequently, results may

differ from those anticipated and discussed here. These

expectations are highly dependent on market conditions, on

Brazil’s economic and banking system performances, as well

as on international market conditions. Banco do Brasil is not

responsible for updating any estimate in this presentation.

Disclaimer

Index

Agenda 6

COMPANY PROFILE 7

Profile 8

Business diversification 9

Highlights 10

Ownership Structure 11

Presence in Brazil 12

Global Presence 13

Assets 14

Loan Portfolio 15

Total Loan Portfolio - Risk Level 16

Loan Portfolio (by closing date of the loan) 17

Disbursements 18

Loans to Individuals 19

Individuals Portfolio 20

Loans to Companies 21

Companies Portfolio by Macro-sector 22

Guarantees provided and Provisions 23

Agribusiness 24

Commercial Funding 25

Sources 26

Sources 27

Current Debt Issues Abroad 28

Uses 29

Ratings 30

Leaderships 31

Corporate Governance 32

Governance Timeline 33

Customer Segmentation 34

Digital Bank 35

Digital Strategy 36

Digital Strategy Evolution 37

Retail Relationship 38

B-Commerce 39

Service Digitalization 40

Credit Card / Digital Solutions 41

EARNINGS HIGHLIGHTS 42

Strategic Guidelines 43

Net Income 44

Earnings Breakdown 45

Market Indicators 46

Net Interest Income 47

Spread by Portfolio 48

Net Interest Margin 49

Earning Assets Breakdown 50

Assets and Liabilities Breakdown 51

BB’s Consolidated Net Position 52

Fee Income 53

Administrative Expenses 54

Delinquency Ratios 55

Delinquency Ratio by Segment 56

NPL Formation 57

NPL Formation by Segment 58

Vintages 59

ALL Balance and Coverage Ratio 60

Coverage Ratio by Segment 61

ALL Balance 62

Provision Expenses Flow / Loan Portfolio (%) 63

Average Risk and Loan Portfolio by Risk Level 64

Average Risk by Segment 65

Cost of Risk 66

Write-off 67

Renegotiated Overdue Loan Portfolio 68

Renegotiated Loan Portfolio 69

Index

BIS Ratio 70

Full Application of Basel III Rules 71

BIS III – Implementation Schedule 72

Guidance 2017 73

Banco Votorantim 74

MACROECONOMIC INFORMATION 75

Inflation and Selic Rate 76

Demographics: Population Pyramid 77

Population: Dependency Ratio 78

Social Security Deficit 79

Main Pillars of Brazilian Growth 80

Sustainable Growth 81

Brazilian Agribusiness 82

PPPs in Brazil 83

Brazilian Foreign Trade Balance 84

Summary Table 85

Summary Table 86

SUSTAINABILITY 87

Socio-environmental (SER) Policy 88

SER Governance 89

SER Strategy – Agenda 30 BB 90

SER Strategy – Agenda 30 BB 91

Socio-environmental Risk Management 92

Promotion of gender equity 93

Pacts and Voluntary Commitments 94

Market Indexes and Awards 95

Index

Agenda01 COMPANY

PROFILE

EARNINGS HIGHLIGHTS

SUSTAINABILITY

MACROECONOMIC INFORMATION

02

03

04

01COMPANY PROFILE

Founded in 1808

54.4%¹ controlled by the Federal Government

1st company listed on the stock exchange in Brazil

Access to a broad spectrum of clients

8

Profile

(1) Does not consider the treasury shares in the total capital.

Large, diversified and stable funding base

Business diversification including:

Banking

ServicesInsurance

Capital

Markets

Methods of

Payment

International

Franchise

Asset

Management

9

More than 200 years of solid performance

Market

Leaderships

Solid

Financial

Performance

Focus on

Services

Stable and

Diversified

Funding

1 2 3 4

Highlights

10

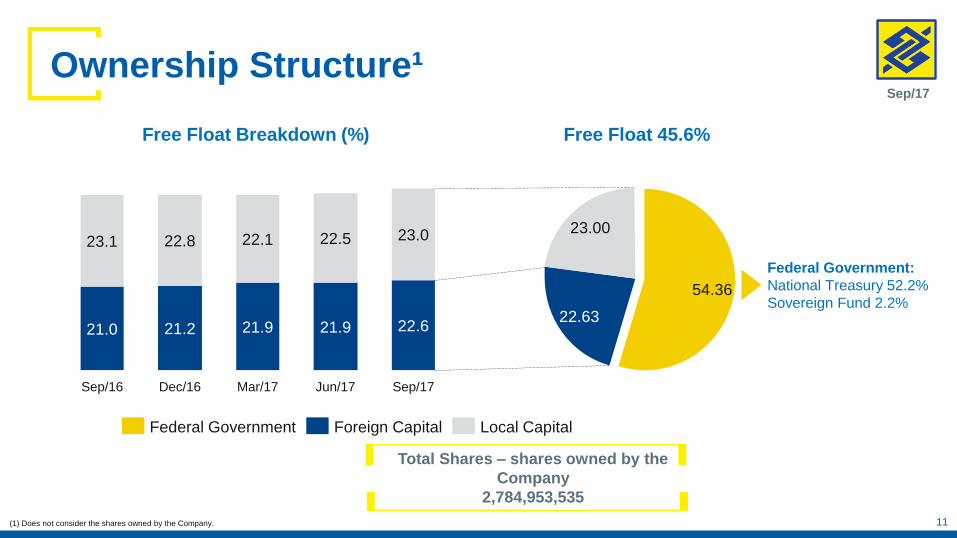

11

Free Float 45.6%

23.00

22.63

54.36

Local CapitalForeign CapitalFederal Government

Ownership Structure¹

11

Total Shares – shares owned by the

Company

2,784,953,535

Sep/17

Federal Government:

National Treasury 52.2%

Sovereign Fund 2.2%

Free Float Breakdown (%)

21.9

Dec/16

22.8

21.2

Sep/16

23.1

21.0

Sep/17

23.0

22.6

Jun/17

22.5

21.9

Mar/17

22.1

(1) Does not consider the shares owned by the Company.

Presence in BrazilBB at a Glance

Distribution Network

64,149

Branches

4,871

Customers

65,777 thousand

Employees

99,305

Market Share – 22.1%(Number of branches)

North 27.1%

Midwest 25.6%

Northeast 29.8%

Southeast 18.2%

South 23.2%

(1) Banking Agents and Postal Bank branches. (2) Shared Service Network: lotteries (CEF), Banco 24h e ATM (BRB+CEF).

$

Own Service Network

15,085

MaisBB Network¹

13,683Shared Service Network²

35,381

12

Sep/17

Points of Service

2,062$

Present in 99.8% of brazilian county

Banco do Brasil in the World

Branches

Sub-branches

Representative Offices

Subsidiaries, Affiliates and

Capital Markets Units

Shared Services Units

Global Presence

11

3

7

11

2

BB operates in 24

countries through a

network of 34 units. BB

also maintains

relationship with 889

correspondent banks in

107 countries.

13

Mar/17 Sep/17

1,445.61,399.9

Jun/17Dec/16

1,402.4

Sep/16

1,401.41,448.2

20.220.7 20.7

20.1

Market Share (%)¹Assets

Assets

14

2.2%

9.8%

13.3%

36.0%

38.7% • Loans

• Available Funds, Short-Term

Interbank Investments,

Interbank and Intrabank

Accounts

• Securities and Financial

Derivatives

• Other

• Permanent Assets

R$ billion

(1) Source: Brazilian Central Bank

Loan Portfolio – Expanded View¹R$ billion

(1) It includes private securities and guarantees provided. 15

-7.9-7.6-11.4-11.3

-6.9

Growth in 12 months (%)

Sep/17

677.0

267.7

187.5

180.7

41.2

Jun/17

696.1

277.2

185.9

188.2

44.9

Mar/17

688.7

280.8

185.1

180.1

42.7

Dec/16

708.1

294.7

187.8

179.8

45.7

Sep/16

735.4

316.8

187.6

179.6

51.5

CompaniesForeign Branches and Subsidiaries Agribusiness Individuals

7.0

43.1

25.5

24.4

39.5

6.1

26.7

27.7

%%

R$ million

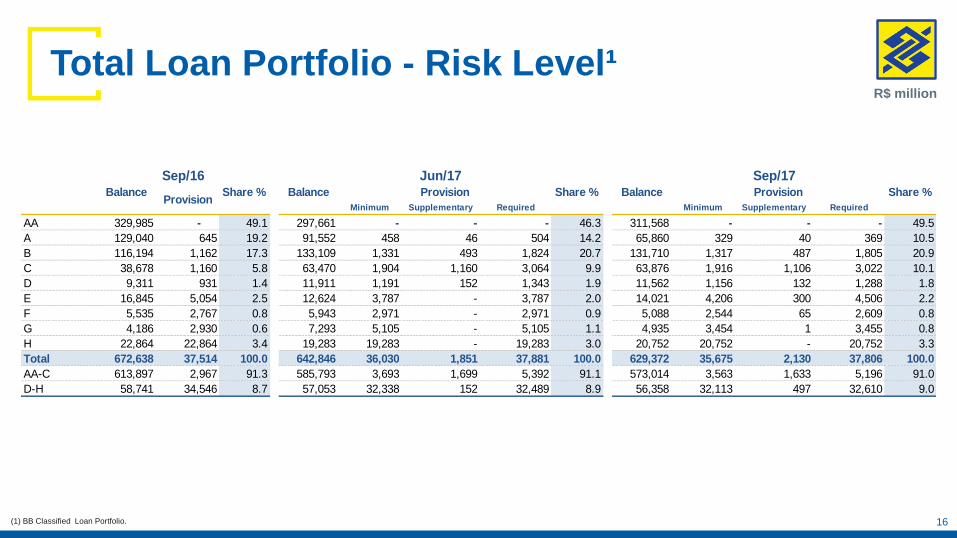

Total Loan Portfolio - Risk Level¹

16(1) BB Classified Loan Portfolio.

Minimum Supplementary Required Minimum Supplementary Required

AA 329,985 - 49.1 297,661 - - - 46.3 311,568 - - - 49.5

A 129,040 645 19.2 91,552 458 46 504 14.2 65,860 329 40 369 10.5

B 116,194 1,162 17.3 133,109 1,331 493 1,824 20.7 131,710 1,317 487 1,805 20.9

C 38,678 1,160 5.8 63,470 1,904 1,160 3,064 9.9 63,876 1,916 1,106 3,022 10.1

D 9,311 931 1.4 11,911 1,191 152 1,343 1.9 11,562 1,156 132 1,288 1.8

E 16,845 5,054 2.5 12,624 3,787 - 3,787 2.0 14,021 4,206 300 4,506 2.2

F 5,535 2,767 0.8 5,943 2,971 - 2,971 0.9 5,088 2,544 65 2,609 0.8

G 4,186 2,930 0.6 7,293 5,105 - 5,105 1.1 4,935 3,454 1 3,455 0.8

H 22,864 22,864 3.4 19,283 19,283 - 19,283 3.0 20,752 20,752 - 20,752 3.3

Total 672,638 37,514 100.0 642,846 36,030 1,851 37,881 100.0 629,372 35,675 2,130 37,806 100.0

AA-C 613,897 2,967 91.3 585,793 3,693 1,699 5,392 91.1 573,014 3,563 1,633 5,196 91.0

D-H 58,741 34,546 8.7 57,053 32,338 152 32,489 8.9 56,358 32,113 497 32,610 9.0

Sep/16 Jun/17 Sep/17Balance

ProvisionShare % Balance Share % Balance Provision Share %Provision

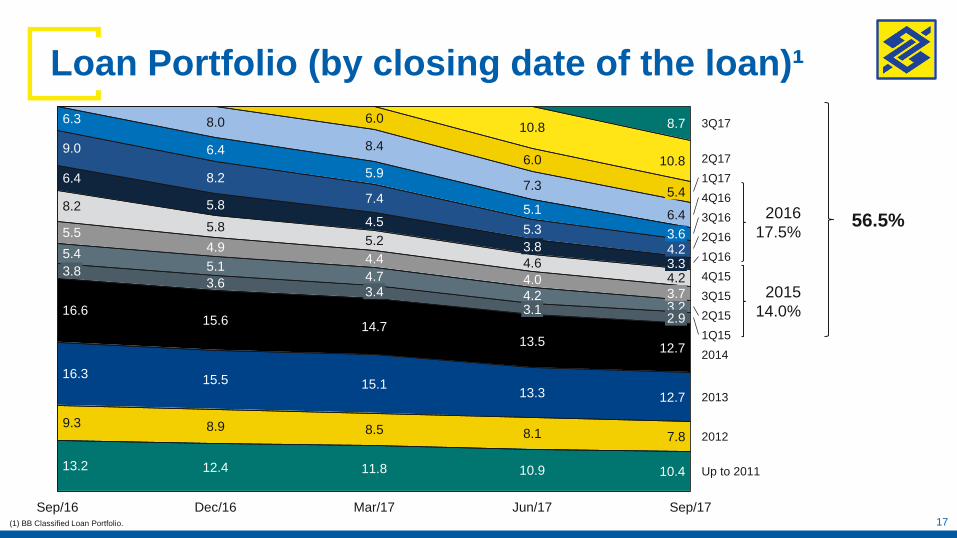

Loan Portfolio (by closing date of the loan)¹

17(1) BB Classified Loan Portfolio.

2016

17.5%

2015

14.0%

56.5%

4.7

4.4

5.2

7.4

4.5

4.9

5.1

5.85.5

9.3

16.3

16.6

5.4

3.8

5.8

8.2

6.4

Sep/16

8.0

8.5

4.23.1

2Q16

12.7

3Q16

1Q16

2Q15

3Q15

4Q15

2013

2014

1Q15

4.2

12.7

3Q17

Sep/17

7.8

4Q16

1Q17

2Q17

3.22.9

3.7

13.5

10.8

8.7

Jun/17

13.3

8.1

3.34.23.6

5.4

6.4

2012

4.0

Mar/17

7.3

6.0

10.8

3.8

9.0

5.1

4.6

6.3

3.6

15.6

6.4

8.2

14.7

15.1

3.4

15.5

5.3

5.9

8.4

6.0

8.9

Dec/16

Up to 201110.9 10.411.813.2 12.4

136168

12312091

117100

3Q172Q171Q174Q163Q162Q161Q16

195217

184

139

97106100

3Q162Q161Q16 3Q172Q171Q174Q16

126

171

86

140

91

157

100

4Q163Q162Q161Q16 3Q172Q171Q17

123157

12111199107100

3Q172Q171Q174Q163Q162Q161Q16

Brazil

Disbursements – quarterly average¹ (1Q16 base 100)

Agribusiness

Individuals

Companies

(1) Does not include revolving lines of credit and overdraft. 18

R$ million

Loans to Individuals¹

19(1) It considers the organic Loan Portfolio.

Sep/16 Jun/17 Sep/17

Payroll Loan 62,838 64,219 65,600

Mortgage 41,157 76.0% 43,049 76.2% 43,656 76.9%

Salary Loan 20,348 19,850 19,941

Auto Loan 6,799 5,432 5,091

Credit Card 22,844 23,627 23,612

Renegotiated Loan 7,236 8,139 8,288

Consumer Finance 7,010 6,110 5,144

Overdraft Account 2,830 2,425 2,333

Microcredit 757 538 480

Other 798 584 523

Total 172,617 173,972 174,669

+0.8%

Sep/17Jun/17

53.6

43.0

10.5

Sep/16

53.1

41.2

11.9

43.7

9.9

53.5

Mortgage - IndividualsMortgage -Companies

2.151.42 2.27

Individuals Mortgage NPL 90 (%)²

+4.4%

Sep/17Jun/17

64.2

87.8%

9.6% 2.6%

Sep/16

62.8

88.5%

8.5% 3.0%

87.7%

65.6

9.7% 2.6%

Civil ServantsINSS´s Retirees and PensionersPrivate Sector Employees

1.821.30 1.89

NPL +90 days (%)²

-2.0%

Sep/17Jun/17

19.8

Sep/16

20.3 19.9-25.1%

Sep/17Jun/17

5.4

Sep/16

6.8

5.1

4.942.78

4.86

NPL +90 days (%)²

1.290.97 1.06

NPL +90 days (%)²

R$ billion

Individuals Portfolio¹: Lower risk lines of credit

Individuals

Market

Share

7.8%

Market

Share

21.6%

(1) BB Organic Portfolio. (2) BB Classified Loan Portfolio.

PayrollMortgages

Auto LoansSalary Loans

20

6.1%

Chg. (%)

on

Sep/16

-3.4%-15.5%

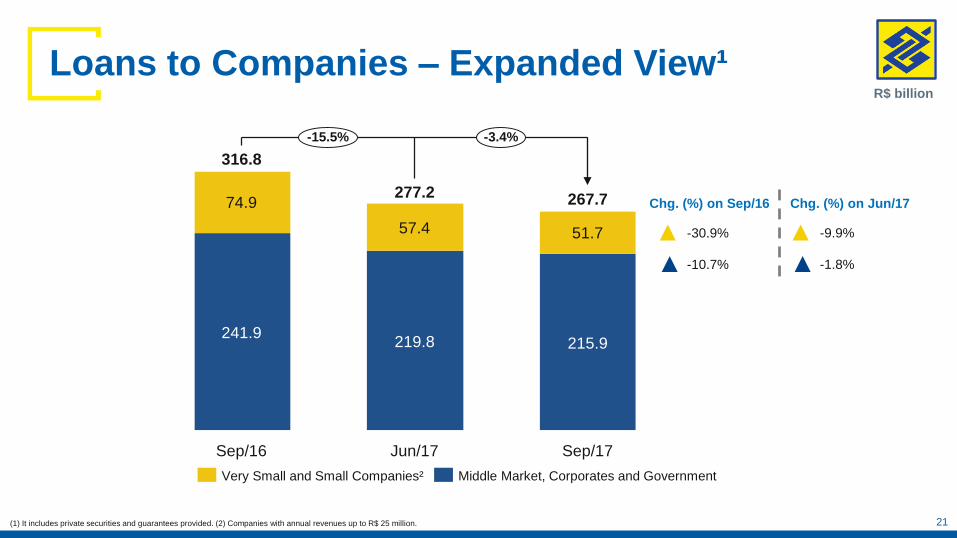

Sep/17

267.7

215.9

51.7

Jun/17

277.2

219.8

57.4

Sep/16

316.8

241.9

74.9

Middle Market, Corporates and GovernmentVery Small and Small Companies²

-30.9%

-10.7%

21

-9.9%

-1.8%

(1) It includes private securities and guarantees provided. (2) Companies with annual revenues up to R$ 25 million.

Chg. (%) on Sep/16 Chg. (%) on Jun/17

R$ billion

Loans to Companies – Expanded View¹

Companies Portfolio by Macro-sector¹

22

R$ million

(1) It includes Companies and Agro Companies Portfolio.

Macro-Sector¹ Sep/16 Share % Jun/17 Share % Sep/17 Share % Sep/16 Jun/17

Oil and Gas 43,618 10.7 38,660 10.8 38,752 11.4 (11.2) 0.2

Public Administration 38,647 9.5 39,225 10.9 37,832 11.1 (2.1) (3.6)

Metalworking and Steel 37,618 9.2 32,264 9.0 30,683 9.0 (18.4) (4.9)

Food products of Vegetable Origin 30,974 7.6 30,129 8.4 30,257 8.9 (2.3) 0.4

Eletric Utilities 37,250 9.1 29,416 8.2 28,121 8.2 (24.5) (4.4)

Transportation 27,520 6.8 25,099 7.0 24,080 7.1 (12.5) (4.1)

Services 19,978 4.9 20,729 5.8 18,973 5.6 (5.0) (8.5)

Housing 20,399 5.0 17,640 4.9 16,545 4.8 (18.9) (6.2)

Automobiles and Components 20,403 5.0 15,944 4.4 15,100 4.4 (26.0) (5.3)

Food products of Animal Origin 15,829 3.9 15,538 4.3 14,844 4.4 (6.2) (4.5)

Retail 16,173 4.0 11,828 3.3 11,138 3.3 (31.1) (5.8)

Construction Materials 13,191 3.2 11,190 3.1 10,444 3.1 (20.8) (6.7)

Financials 16,066 3.9 12,187 3.4 10,394 3.0 (35.3) (14.7)

Agricultural inputs 9,033 2.2 8,038 2.2 7,563 2.2 (16.3) (5.9)

Electrical and Electronic Goods 7,529 1.8 6,792 1.9 6,712 2.0 (10.9) (1.2)

Textiles 9,247 2.3 7,242 2.0 6,594 1.9 (28.7) (8.9)

Chemicals 6,306 1.5 5,586 1.6 5,875 1.7 (6.8) 5.2

Telecommunication Services 5,964 1.5 7,548 2.1 5,767 1.7 (3.3) (23.6)

Pulp and Paper 8,403 2.1 6,045 1.7 5,321 1.6 (36.7) (12.0)

Wholesale and Other Industries 6,188 1.5 4,720 1.3 4,763 1.4 (23.0) 0.9

Furniture and Forest products 5,904 1.4 4,639 1.3 4,336 1.3 (26.6) (6.5)

Heavy Construction 7,207 1.8 4,859 1.4 4,183 1.2 (42.0) (13.9)

Leather and Shoes 2,415 0.6 2,066 0.6 1,761 0.5 (27.1) (14.8)

Beverages 1,395 0.3 1,279 0.4 1,150 0.3 (17.6) (10.1)

Other Activities 19 0.0 15 0.0 26 0.0 42.4 79.0

Total 407,275 100 358,679 100 341,215 100 (16.2) (4.9)

Balance Chg. (%) on

Guarantees provided and Provisions

Sep/17

324

13,928

Jun/17

356

15,254

Mar/17

379

17,178

Dec/16

431

17,957

Sep/16

491

18,241

ProvisionsGuarantees Provided

2.32.32.2

2.4

2.7

Provisions/Guarantees

R$ million

23

%

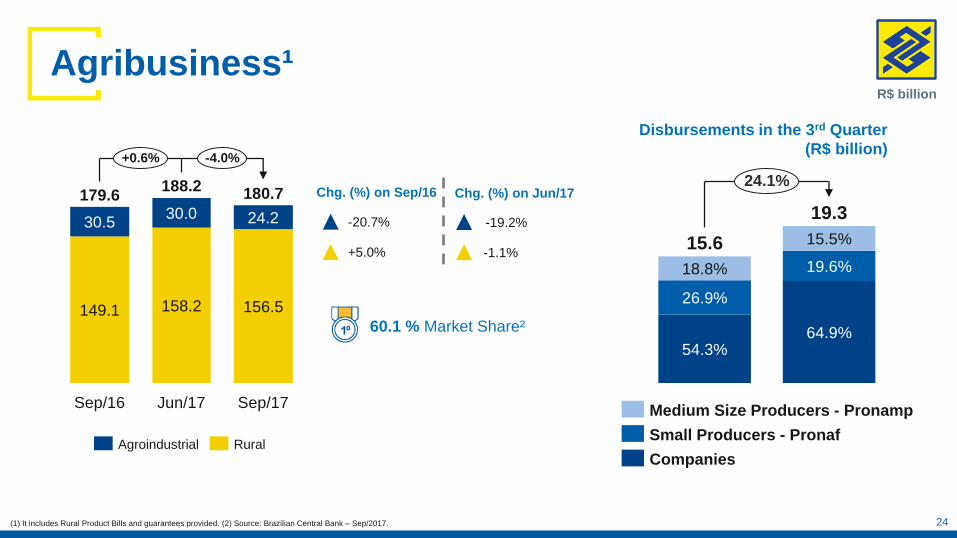

60.1 % Market Share²

+0.6%

Sep/17

180.7

156.5

24.2

Jun/17

188.2

158.2

30.0

Sep/16

179.6

149.1

30.5

-4.0%

RuralAgroindustrial

Agribusiness¹R$ billion

(1) It includes Rural Product Bills and guarantees provided. (2) Source: Brazilian Central Bank – Sep/2017. 24

+5.0%

-20.7%

Chg. (%) on Sep/16

-19.2%

-1.1%

Chg. (%) on Jun/17

54.3%64.9%

24.1%

19.3

15.5%

19.6%

15.6

18.8%

26.9%

Companies

Medium Size Producers - Pronamp

Small Producers - Pronaf

Disbursements in the 3rd Quarter

(R$ billion)

(1) Includes the balance of CRI (Certificates of Real Estate Receivables). (2) Includes part of the balances of the Private Securities shown on Notes to the Consolidated Financial Statements.

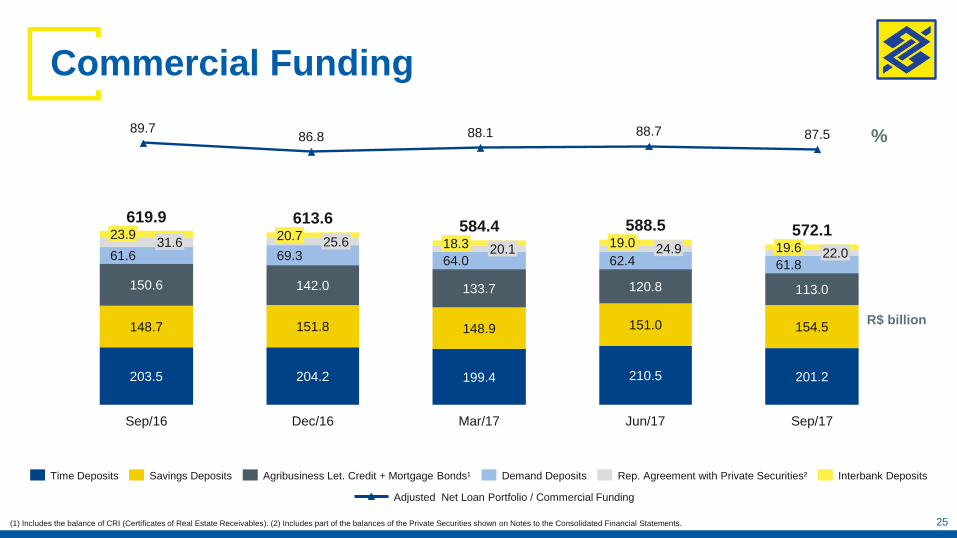

Sep/17

572.119.6 22.061.8

113.0

154.5

201.2

Jun/17

588.519.0 24.962.4

120.8

151.0

210.5

Mar/17

584.418.3 20.164.0

133.7

148.9

199.4

Dec/16

613.620.7

25.669.3

142.0

151.8

204.2

Sep/16

619.923.9

31.661.6

150.6

148.7

203.5

Interbank DepositsRep. Agreement with Private Securities²Demand DepositsAgribusiness Let. Credit + Mortgage Bonds¹Savings DepositsTime Deposits

R$ billion

25

87.588.788.186.889.7

Adjusted Net Loan Portfolio / Commercial Funding

%

Commercial Funding

Sources

26

R$ million

(1) Includes part of the balances of Private Securities on Notes to the Consolidated Financial Statements number 17.

(2) Includes Foreign Borrowing, Foreign Securities, Foreign Onlending and Subordinated Debt Abroad.

(3) Includes Financial Bonds and Debentures.

Mar/16 Jun/16 Sep/16 Dec/16 Mar/17 Jun/17 Sep/17

Commercial Funding¹ 638,611 624,778 619,944 613,611 584,445 588,506 572,091

Domestic Onlending 88,082 86,603 85,078 83,083 81,431 79,453 82,674

Subordinated Debt 58,049 58,648 60,027 61,976 61,123 62,306 62,943

Foreign Borrowing² 58,463 50,911 52,578 50,471 47,581 51,499 47,924

Hybrid Capital Instruments 34,806 31,068 31,825 31,466 31,206 31,753 31,253

Financial and Development Funds 14,781 13,741 14,620 14,791 14,817 14,837 14,842

Commercial Paper³ 2,309 2,384 2,673 2,734 2,812 3,088 3,899

Compulsory Deposits (62,613) (65,404) (63,637) (63,451) (61,619) (64,659) (69,442)

Total 832,489 802,728 803,107 794,680 761,795 766,782 746,184

Sources

27

Commercial Funding

Foreign

R$ million

(1) Includes part of the balances of the Private Securities shown on Notes to the Consolidated Financial Statements number 17. (2) Includes the balance of CRI (Certificates of Real Estate Receivables)

Mar/16 Jun/16 Sep/16 Dec/16 Mar/17 Jun/17 Sep/17

Foreign Securities 22,885 18,631 20,274 20,393 20,540 21,937 20,280

Foreign Borrowing 25,178 22,763 22,812 20,409 17,769 19,741 18,368

Subordinated Debt Abroad 10,400 9,517 9,491 9,668 9,271 9,821 9,275

Total 58,463 50,911 52,578 50,471 47,581 51,499 47,924

Cost Mar/16 Jun/16 Sep/16 Dec/16 Mar/17 Jun/17 Sep/17

Savings DepositsTR + (0.5% if Selic> 8.5%, or

70% of Selic)151,919 148,368 148,681 151,763 148,910 150,982 154,517

Judicial Deposits As Savings Deposits 114,140 116,655 119,281 121,969 121,931 130,514 124,782

Agribusiness Letters of Credits % of CDI 135,420 135,418 133,098 124,965 112,720 100,665 94,473

Time Deposits % of CDI 88,463 85,834 84,199 82,234 77,511 79,969 76,382

Demand Deposits - 62,631 62,550 61,623 69,349 63,960 62,385 61,793

Rep. Agreement with Private Securities¹ % of CDI 30,471 30,415 31,621 25,591 20,135 24,898 22,016

Interbank Deposits % of CDI 36,885 27,473 23,919 20,665 18,265 18,962 19,649

Mortgage Bonds² % of CDI 18,681 18,066 17,521 17,074 21,012 20,132 18,480

Total 638,611 624,778 619,944 613,611 584,445 588,506 572,091

Current Debt Issues Abroad

28(1) - A: annual; S: semiannual; Q: quarterly.

Issue Date Call Date Coupon (%)¹Term in

YearsMaturity

Amount issued

(US$ thousand)Currency

Rating

S&P/Moody's/FitchStructure

Outstanding

amount (US$

thousands)

04/29/2008 5,250 Q 10 06/15/2018 150.000 USD BBB / Ba1 / SR MT 100 18.000

10/20/2009 10/20/2020 8,500 S Perpetual Perpetual 1.500.000 USD SR / B2 / SR Stand Alone 1.498.500

01/22/2010 6,000 S 10 01/22/2020 500.000 USD BB / Ba2 / BB GMTN 500.000

10/05/2010 5,375 S 10 01/15/2021 660.000 USD SR / Ba3 / SR Stand Alone 660.000

05/26/2011 5,875 S 10 01/26/2022 1.500.000 USD SR / Ba3 / SR Stand Alone 1.500.000

01/20/2012 04/15/2023 9,250 S Perpetual Perpetual 1.000.000 USD B- / SR / SR Stand Alone 648.727

03/05/2012 04/15/2023 9,250 S Perpetual Perpetual 750.000 USD B- / SR / SR Stand Alone 750.000

06/19/2012 5,875 S 10 01/19/2023 750.000 USD B / Ba3 / SR Stand Alone 750.000

10/10/2012 3,875 S 10 10/10/2022 1.925.000 USD BB / Ba2 / BB Stand Alone 1.809.700

01/31/2013 04/15/2024 6,250 S Perpetual Perpetual 2.000.000 USD B- / SR / SR Stand Alone 1.988.000

07/25/2013 3,750 A 5 07/25/2018 929.775 EUR BB / Ba2 / BB GMTN 848.698

12/20/2013 2,500 A 5 06/20/2019 306.988 CHF BB / Ba2 / BB GMTN 283.886

03/26/2014 3,750 A 5 07/25/2018 417.210 EUR BB / Ba2 / BB GMTN 332.402

06/18/2014 06/18/2024 9,000 S Perpetual Perpetual 2.500.000 USD B- / B2 / SR Stand Alone 2.169.70010/23/2017 4,625 S 7 01/15/2025 1.000.000 USD BB / Ba2 / BB GMTN 1.000.000

Uses

29

Mar/16 Jun/16 Sep/16 Dec/16 Mar/17 Jun/17 Sep/17

Available Funds 116,384 106,045 122,741 139,059 124,617 123,694 120,660

Net Loan Portfolio (a) 716,105 696,683 680,366 655,621 637,178 643,088 625,524

Classified Loan Portfolio 703,878 691,832 672,638 653,591 638,336 642,846 629,372

Private Securities 47,625 41,819 45,242 38,100 35,256 38,124 33,958

Allowance for Loan Losses (35,398) (36,968) (37,514) (36,070) (36,414) (37,881) (37,806)

Adjusted Net Loan Portfolio (a) - (b) 589,982 572,451 556,270 532,435 514,963 522,162 500,789

Domestic Onlending Loans (b) 126,122 124,232 124,096 123,186 122,215 120,926 124,735

Total 832,489 802,728 803,107 794,680 761,795 766,782 746,184

R$ million

Banco do Brasil: Ratings

30

Sep/13 Sep/14 Sep/15 Sep/16 Sep/17

Standard & Poor's

Long-Term - Local Currency BBB BBB- BB+ BB BB

Long-Term - Foreign Currency BBB BBB- BB+ BB BB

Moody's

Long-Term Debt - Foreign Currency Baa1 Baa2 Baa3 Ba2 Ba2

Long-Term Deposits - Foreign Currency Baa2 Baa2 Baa3 Ba3 Ba3

Long-Term Deposits - Local Currency A3 Baa2 Baa3 Ba2 Ba2

Fitch Ratings

Long-Term - Local Currency BBB BBB BBB- BB BB

Long-Term - Foreign Currency BBB BBB BBB- BB BB

DepositsLoan PortfolioAssets under

Management²

(1) Comparison with the two largest Brazilian private banks. (2) It does not include Banco Votorantim. (3) Source: Anbima - Sep/17. (4) Source: Banco Central do Brasil - Sep/17. (5) Source: Banco Central do Brasil - Jun/17.

(6) Source: SUSEP – Year Accumulated up to Aug/17.

575.2

486.9

Bank A Bank BBB

677.0

259.6

Bank ABB

437.1

359.9

Bank B

852.3

Bank A

556.5

625.5

BB Bank B

19.5%

Market Share⁴

20.8%

Market Share⁵

22.9%

Market Share³

31

BB Seguridade6

Rural

Pension Plan

Life

Premium Bonds

Vehicle

Industry Leadership¹R$ billion

Corporate Governance

Decisions at any level of the Company are made in

Committees, involving several executives in the

definition of strategies and in the approval of

transactions and operations for the different

businesses lines of Banco do Brasil.

Customer Service and

Experience Executive

Committee

Credit Transactions

Committee

Human Resources

Appealing Committee

Information

Technology Committee

Risk, Asset and Liabilities, Liquidity and Capital Management Superior Committee

1 Superior Committee¹

14 Executive Committees¹

32(1) Base date: Septermber 30, 2017.

Profitability and

Performance Executive

Committee

Investor Relations

Executive Committee

Strategic Portfolio

Management Executive

Committee

Risk Management and

Internal Controls

Executive Committee

Asset and Liabilities,

Liquidity and Capital

Management Executive

Committee

Ethics and Discipline

Executive Committee

Prevention of Finan. and

Foreign Exch. Ilicit

transactions and Information

Security Exec. Committee

Products and Services

Executive Committee

Credit Transactions

Executive Committee

Human Resources

Executive Committee

Credit Limit Executive

Committee

Subsidiries and Affiliated Companies

Governance Executive Committee

Administrative and Operational

Executive Committee

Audit Commitee, Risk and Capital Committee, Compensation and Eligibility

Committee

3 Advisory Committees for the Board of Directors

The Only Brazilian Bank listed since 2006 in the

Novo Mercado segment which is comprised of

companies that voluntarily adopt the best

practices in corporate governance.

Other Committees

The Program for State-owned companies with

distinguished corporate governance was created by

B3 with the objective of encouraging state-owned

companies to improve their governance practices

and structures.

Governance Timeline

1st Brazilian

company listed on

the stock

exchange

BB Shares enter the

IBRX-50 portfolio

Bonus A

subscription

BB Shares enter

the B3 ITAG

portfolio

BB Shares enter the

ISE portfolio

Banco do Brasil

joined “Novo

Mercado” (B3)

BB Shares enter

Dow Jones

Sustainability

Index (DJSI) of NY

stock exchange

BB Seguridade

IPO

ADR Level I

Follow on

(secondary shares)

The Board of Directors of

BB approved the upgrade

of its program of

American Depositary

Receipt-ADR from level I

to level II

Inclusion of 100%

Tag Along clause

in the Bylaws.

Conversion of the

preferred shares to

common shares

Capitalization

and Restructuring

Plan

BB Shares enter the

IBrX portfolio

Private

placement of

common shares

linked to a public

offering for the

acquisition of

subscription

bonus

Follow on

(primary shares)

1995

1996

2002

1906

1998

20012003

2005

2006

2004

2009

2012

2013

2007

2010

2014

33

B3 Certification in the

Programa Destaque em

Governança de Estatais.

Maximum score in the IG-

SEST Governance

Indicator of the Ministry of

Planning, Development

and Management

2017

Customer Segmentation

34

Companies¹ Individuals

IndustrialCommerce and

Services

> R$ 1.5bn > R$ 2bn

> R$ 400mm

≤ R$ 1.5bn

> R$ 600mm

≤ R$ 2bn

> R$ 120mm

≤ R$ 400mm

> R$ 25mm

≤ R$ 120mm

> R$ 200mm

≤ R$ 600mm

> R$ 25mm

≤ R$ 200mm

Corporate

Empresarial Upper Middle

Empresarial Middle

> R$ 5mm ≤ R$ 25mm

> R$ 1mm ≤ R$ 5mm

≤ R$ 1mm

Empresa

Pequena Empresa

Microempresa

Large CorporatePrivate

Estilo²

Personalizado /

Exclusivo²

Varejo

Annual Income ≥ R$ 10mm

Investments ≥ R$ 2mm

Monthly Income ≥ R$ 10k

Investments > R$ 150k ≤ R$ 2mm

Monthly Income ≥ R$ 4k < R$ 10k

Investments > R$ 80k ≤ R$ 150k

Monthly Income ≥ R$ 2k < R$ 4k

Investments > R$ 5k ≤ R$ 80k

Mercado EmergenteMonthly Income < R$ 2k

Investments ≤ R$ 5k

(1) Based on Companies annual revenues. (2) Digital Service only.

Digital

Bank

Digital Strategy – Improving customer experience

Branch

Relationship Manager

DIGITAL RELATIONSHIP

Manager

Specialized

Advisory

Human Solutions Digital Solutions

Telephone

Chat / messages

Videoconference

Documents Electronic Exchange

Double Confirmation

From 10am to 4pm From 8am to 6pm

From 10am to 4pmFrom 8am to 10pm

Ind

ivid

ua

lsC

om

pa

nie

s

36

(1) Refers to the customers in the Estilo, Exclusivo e Personalizado segments. (2) Refers to the customers in the Estilo e Exclusivo segments. (3) Refers to the customers in the Personalizado and traditional Estilo segments.(4) Since Jul/17, clients with monthly income ≥ R $ 10 thousand or investments > R$ 150 thousand ≤ R$ 2 million. (5) Since Jul/17, clients with monthly income ≥ R$ 4 thousand < R$ 10 thousand or investments > R$ 80 thousand ≤ R$ 150 thousand..

Digital Strategy Evolution

Until December 20173.3 million high income customers in the digital models

Sep/17Sep/16

4.6 MM4.1 MMHigh income customers ¹

2.3 MM1 MMH.I. customers in the digital model²

2.3 MM3.1 MMH.I. customers (traditional)³

ESTILO4

9

Digital service 249Branches

1.2 MMCustomers

Customers

EXCLUSIVO5

63Digital service

1 MM0.11 MM

11

Offices

216

0.9 MM

-

Offices

Customers

37

Dec/16

1,736

1,260

Jun/17

1,796

2,292

Mar/17 Sep/17 Dec/17

estimated

3,300

175

421

Sep/15 Dec/15 Mar/16

536 604

1,023

Jun/16 Sep/16

High income customers in

the digital model (million)

More than 1 millionof Conta Fácil¹,

representing 1/3 of the

accounts opened in BB

(1) From November 01, 2016 to September 30, 2017.

Retail Relationship: Conta Fácil

38

CRM /

ANALYTICS

CUSTOMER

EXPERIENCEDIGITAL SOLUTIONS+

Implementation of segmented market actions with volume of business over

R$ 3 billion¹, involving more than 2,000 clusters.

Conversion rate is seven times higher

(1) Since the beginning of the initiative in February/17 up to October/17.

B-Commerce

39

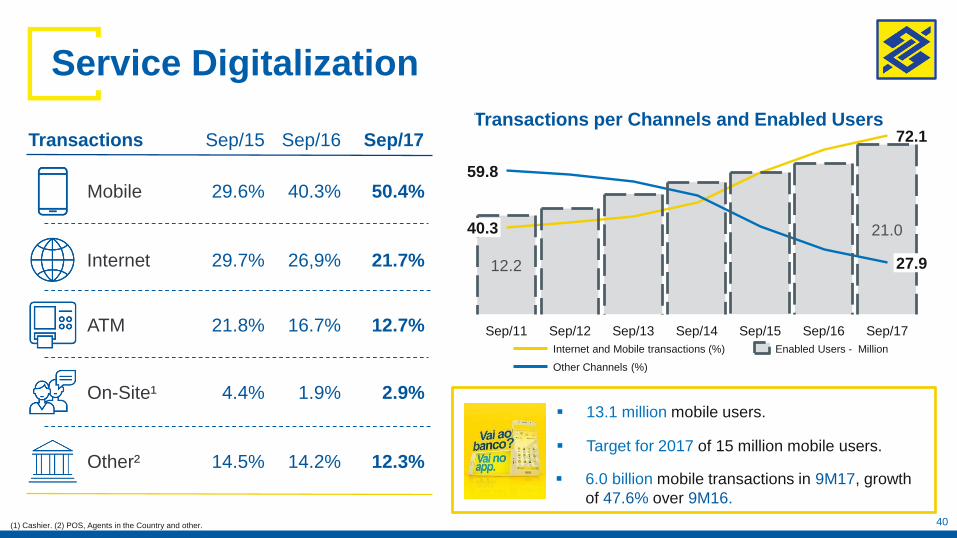

Service Digitalization

(1) Cashier. (2) POS, Agents in the Country and other.

Internet

Mobile

ATM

On-Site¹

Other²

26,9%

40.3%

16.7%

1.9%

14.2%

Transactions Sep/16

21.7%

50.4%

12.7%

2.9%

12.3%

Sep/17

29.7%

29.6%

21.8%

4.4%

14.5%

Sep/15

13.1 million mobile users.

6.0 billion mobile transactions in 9M17, growth

of 47.6% over 9M16.

Target for 2017 of 15 million mobile users.

Transactions per Channels and Enabled Users

21.0

Sep/16 Sep/17Sep/15

72.1

27.9

Sep/14Sep/13

12.2

40.3

59.8

Sep/12Sep/11

Internet and Mobile transactions (%) Enabled Users - Million

Other Channels (%)

40

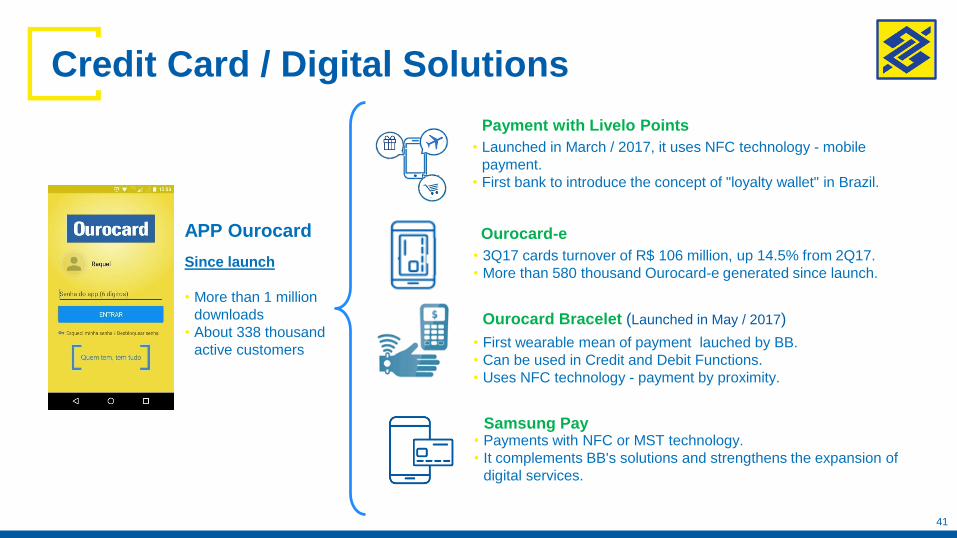

Credit Card / Digital Solutions

Payment with Livelo Points

APP Ourocard

Samsung Pay

Ourocard Bracelet (Launched in May / 2017)

Ourocard-e

Since launch

• More than 1 million

downloads

• About 338 thousand

active customers

• Launched in March / 2017, it uses NFC technology - mobile

payment.

• First bank to introduce the concept of "loyalty wallet" in Brazil.

• Payments with NFC or MST technology.

• It complements BB's solutions and strengthens the expansion of

digital services.

• First wearable mean of payment lauched by BB.

• Can be used in Credit and Debit Functions.

• Uses NFC technology - payment by proximity.

• 3Q17 cards turnover of R$ 106 million, up 14.5% from 2Q17.

• More than 580 thousand Ourocard-e generated since launch.

41

02EARNINGSHIGHLIGHTS

Profitability,

efficiency, control of

delinquency and

capital

Customer

Experience

Digital

Transformation

Str

ate

gic

Gu

ide

lin

esHighlights 9M17 / 9M16

Fee Income

9.9% growth.

Administrative Expenses

Under control, 2.7% decline.

Cost to income ratio¹

Reached 38.5%.

(1) Cost to Income Ratio: Administrative Expenses / Operating Revenues accumulated in 12 months in 3Q17. Data from the Income

Statement with Reallocations.43

Net Income

+45.1%

9M179M16

5.424

2.337

2.708

3.087

7.872

5.164

Adjusted Net Income 1HAdjusted Net Income 3Q

+11.8%

9M179M16

7.070

2.246

5.062

7.903

2.841

4.824

Net Income 1HNet Income 3Q

44

3Q16 2Q17 3Q17 9M16 9M17

Shareholders ROE % 13.4 14.1 14.1 10.1 13.5

Market ROE % 12.0 12.8 12.8 9.1 12.3

Profitability Ratios

R$ billion

Earnings Breakdown

45

(3.24)

(4.68)

6.56

(6.26)

14.25

2.840.132.71

(3.93)

(7.92)

Personnel

Expenses

(9.38)

(14.17)

Fee Income

19.21

ALL

(19.63)

NII

43.33

Net Income

7.90

One-Off Items

0.03

Adjusted

Net Income

7.87

Other

(11.48)

Administrative

Expenses

(23.55)

3Q17

9M17

R$ billion

Personnel

Expenses

Market IndicatorsDividend Yield² (%)Earnings per Share

Price/Book ValuePrice/Earnings 12 months

(1) Bloomberg estimative in November 14, 2017 based on analysts’ projections average. Banco do Brasil is not responsible for this information. (2) Dividends and Interest on Capital 12 months / Market Capitalization. Source: Economatica.

Source: Economatica.

2017E¹

7.96

3Q17

10.96

2Q17

9.02

1Q17

11.59

4Q16

9.74

3Q16

6.63

2018E¹

6.85

2Q17

0.82

1Q17

1.05

4Q16

0.90

3Q16

0.74

3Q17

1.04

2018E¹

0.86

2017E¹

0.95

2017E¹

3.46

3Q17

2.68

2Q17

3.26

1Q17

2.57

4Q16

3.01

3Q16

4.86

2018E¹

3.93

3Q17

0.971.01

2Q17

0.950.94

1Q17

0.900.86

4Q16

0.63

0.34

3Q16

0.840.80

Adjusted Earnings per Share - R$Earnings per Share - R$

2018E¹

4.474.59

2017E¹

3.853.97

2016

2.572.84

2015

4.12

5.05

Source: Economatica.

46

Net Interest Income

(1) It includes senior bonds, subordinated debt, and Hybrid Instruments in Brazil and abroad.

(2) It includes the result from interest, tax hedging, derivatives, and other financial instruments that offset the effects of the exchange rate variation on result.

(3) Series revised (Funding Expense for Institutional Funding to Treasury).

R$ million

47

Chg. (%) on

3Q16 2Q17 9M16

Net Interest Income 15,099 14,606 14,247 (5.6) (2.5) 44,008 43,330 (1.5)

Net Interest Income W/O Recovery 14,131 13,212 13,153 (6.9) (0.4) 40,796 39,886 (2.2)

Loan Operations 26,117 21,786 21,412 (18.0) (1.7) 76,506 66,809 (12.7)

Funding Expenses (11,366) (8,404) (7,814) (31.3) (7.0) (33,330) (25,972) (22.1)

Financial Expense for Institutional Funding¹ ³ (3,524) (3,040) (3,197) (9.3) 5.2 (10,358) (9,603) (7.3)

Treasury² ³ 2,904 2,870 2,753 (5.2) (4.1) 7,978 8,652 8.5

Recovery of Write-offs 968 1,394 1,094 13.0 (21.6) 3,212 3,444 7.2

9M16 9M173Q16 2Q17 3Q17Chg. (%) on

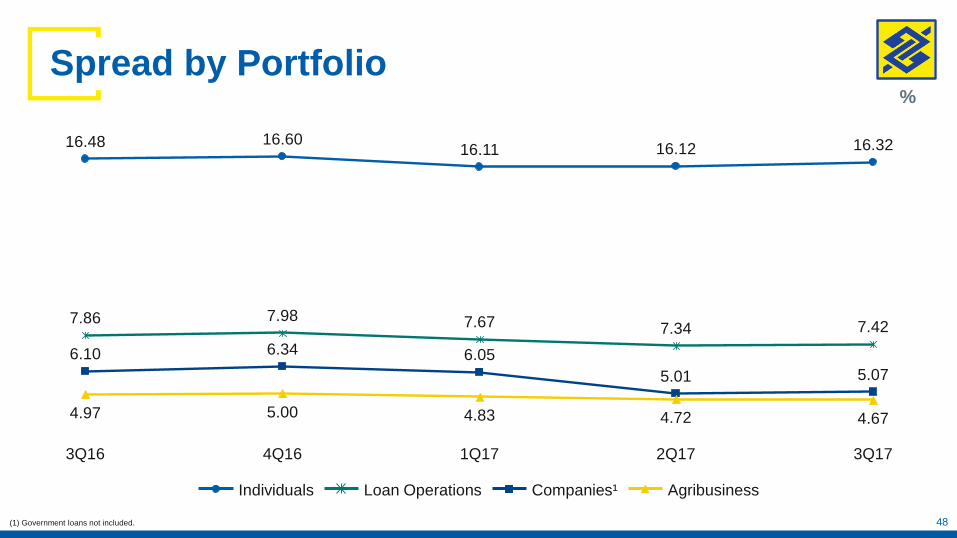

Spread by Portfolio

(1) Government loans not included.

2Q17

4.72

5.01

7.34

16.12

1Q17

4.83

6.05

7.67

16.11

4Q16

5.00

6.34

7.98

16.60

3Q16

4.97

6.10

7.86

16.48

3Q17

16.32

7.42

5.07

4.67

AgribusinessCompanies¹Loan OperationsIndividuals

48

%

49

3Q17

2.54

4.56

2Q17

2.54

4.70

1Q17

2.54

4.77

4Q16

2.54

5.00

3Q16

2.69

4.83

%

Risk Adjusted NIMNet Interest Margin (NIM)

(1) Net interest income / average balance of earnings assets, annualized.

Net Interest Margin¹

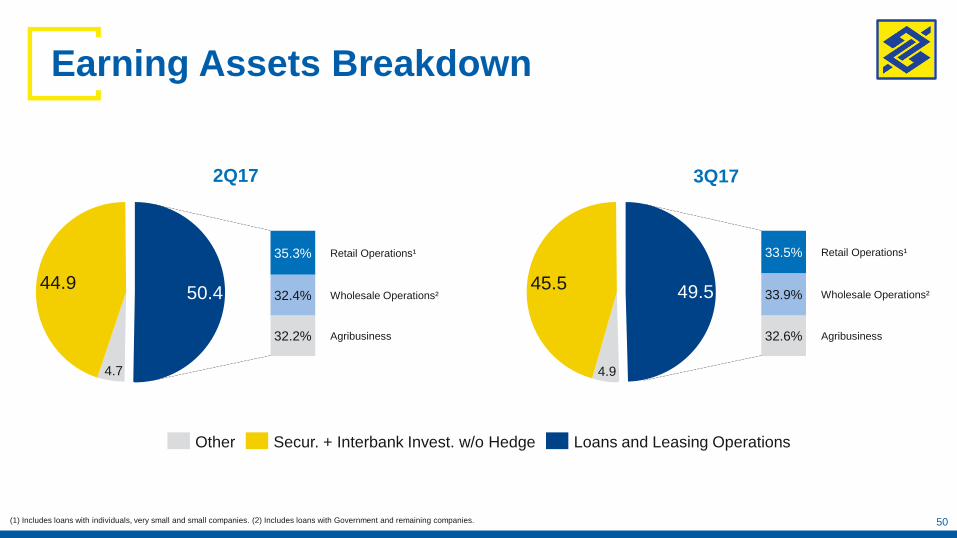

Earning Assets Breakdown

50

50.444.9

4.7

Other Loans and Leasing OperationsSecur. + Interbank Invest. w/o Hedge

49.545.5

4.9

35.3%

32.4%

Agribusiness

Wholesale Operations²

Retail Operations¹

32.2%

33.5%

33.9%

32.6% Agribusiness

Retail Operations¹

Wholesale Operations²

3Q172Q17

(1) Includes loans with individuals, very small and small companies. (2) Includes loans with Government and remaining companies.

Assets and Liabilities Breakdown

51

R$ billion

Liabilities

11.2%

0.3% 2.4%

19.6%

15.9%

25.9%

24.6%

Assets

4.7%1.3% 1.7%

10.7%

15.4%

16.5%

49.8%

W/O Index ⁵

Price Index ²

TJLP ⁴

IRP/TBF/TR ⁷

US$ / Gold ³

CDI / TMS / FACP ⁶

Fixed ¹

Sep/17

1,558

(1) Fixed rate (2) Inflation linked rate (3) Foreign Exchange rate and gold (4) Long term reference rate (5) W/O index: non-interest bearing liabilities (6) Short term rate (7) Savings reference rate

BB’s Consolidated Net Position

52

R$ billion

-8.1

15.0

391.2

-139.1-146.2

-101.3

-11.5

IRP/TBF/TR ⁷CDI / TMS / FACP ⁶W/O Index ⁵TJLP ⁴US$ / Gold ³Price Index ²Fixed ¹

Sep/17

(1) Fixed rate (2) Inflation linked rate (3) Foreign Exchange rate and gold (4) Long term reference rate (5) W/O index: non-interest bearing liabilities (6) Short term rate (7) Savings reference rate

R$ million

Fee Income

53

Chg. (%) on

3Q16 2Q17 9M16

Fee Income 5,972 6,432 6,562 9.9 2.0 17,476 19,207 9.9

Checking Account Fees 1,600 1,712 1,777 11.1 3.8 4,569 5,087 11.3

Asset Management Fees 1,119 1,336 1,419 26.9 6.2 3,198 4,051 26.6

Insurance, Pension and Premium Bonds 751 665 809 7.7 21.5 2,283 2,237 (2.0)

Credit / Debit Cards 460 486 487 5.9 0.1 1,342 1,460 8.8

Loan Fees 374 550 403 7.5 (26.8) 1,179 1,365 15.8

Collections 424 372 354 (16.3) (4.8) 1,264 1,109 (12.2)

Billings 254 270 270 6.4 0.0 771 813 5.4

Capital Market 165 180 198 20.1 10.4 485 548 13.0

Consortium 156 175 191 22.3 9.3 394 527 33.6

National Treasury and Manag. of Official Funds 151 171 177 17.7 3.8 432 515 19.2

Interbank 45 39 36 (18.6) (7.5) 134 117 (12.6)

Other 475 475 440 (7.3) (7.3) 1,424 1,377 (3.3)

3Q16 2Q17 3Q17 9M16 9M17Chg. (%) on

38.539.7

Cost to Income Ratio (12 months)

-2.7%

9M17

23,553

9,380

14,173

9M16

24,201

9,173

15,028

Other Administrative ExpensesPersonnel Expenses

R$ million

54

-6.0%

3Q17

7,915

3,236

4,679

2Q17

7,864

3,047

4,817

3Q16

8,419

3,137

5,283

38.538.939.7

(1) Cost to Income Ratio: Administrative Expenses / Operating Revenues. Data from the Income Statement with Reallocations. (2) Very Small and Small Companies.

Sep/16 Sep/17

Points of Service

Employees

Branches

109,159 99,305

5,430 4,871

1,736 2,062

Own Service Network 17,092 15,085

Exclusivo Office

216 249

Estilo Office - 9

Customer Service

Points326 762

Estilo Branch

11 63

MPE² Office 11 39

-0.3

-0.3

-2.6

-6.3

-0.4

200.0

-5.9

61.5

21.9

5,192 4,511Traditional Branches -1.1

238 360Digital Service 11.1

∆ Sep/17 (%)

on Sep/16 on Jun/17Jun/17

99,603

4,885

2,117

16,098

250

3

810

39

32

4,561

324

-9.0

-10.3

18.8

-11.7

15.3

133.7

472.7

254.5

-13.1

51.3

-

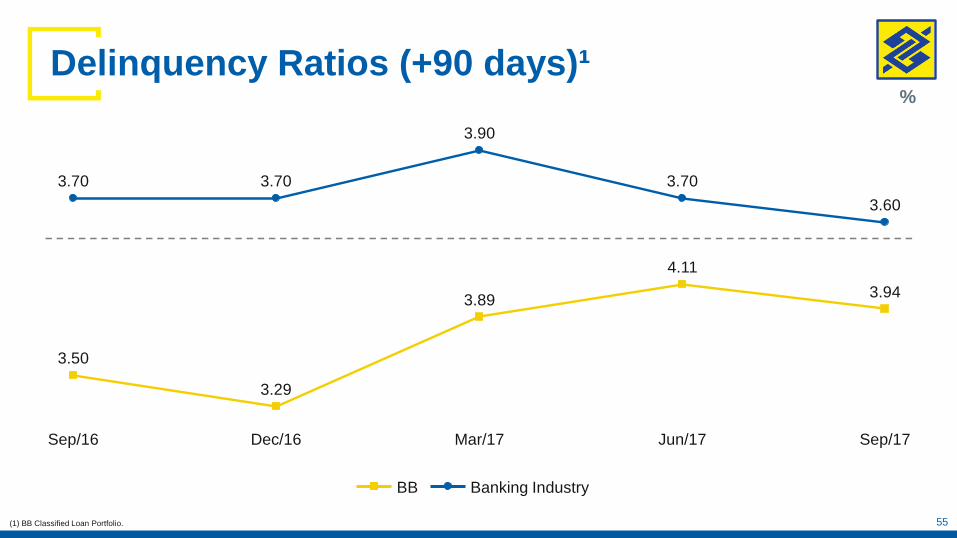

Administrative Expenses and Cost to Income Ratio¹

Sep/17

3.94

Jun/17

4.11

Mar/17Dec/16

3.29

Sep/16

3.50

3.89

BB

55

3.70

3.90

3.703.70

3.60

Banking Industry

Delinquency Ratios (+90 days)¹

(1) BB Classified Loan Portfolio.

%

Sep/17

2.59

8.93

6.58

Jun/17

2.24

9.41

6.46

Mar/17

2.30

11.09

6.94

Dec/16

1.81

9.29

5.26

Sep/16

1.79

8.47

5.97

6.83

Sep/17

1.61

6.70

3.49

Jun/17

1.39

7.35

3.34

Mar/17

1.28

3.09

Dec/16

0.99

5.83

2.67

Sep/16

0.96

5.26

2.56

NPL Ratio +90 days (%) NPL Ratio +15 days (%)

AgribusinessCompaniesIndividuals

Delinquency Ratio¹ by Segment

56(1) BB Classified Loan Portfolio.

NPL Formation

6.97

3Q16

7.12

2Q16

9.73

1Q16

7.39

4Q15

6.22

3Q15

5.59

2Q17

6.84

1Q17

9.75

4Q16

4.68

3Q17

0.731.07

1.49

1.041.031.38

1.030.870.81

133.6697.40

68.82107.4393.3285.05

123.80112.32104.30

2Q17

8.44

1Q17

10.10

4Q16

7.63

3Q16

7.55

2Q16

10.48

1Q16

7.93

4Q15

7.13

3Q15

6.16

3Q17

5.13

New NPL (R$ billion)¹

24.16% of the total

contracts in 3Q17were 90

days past due transactions.

Including the past

due renegotiated

loan portfolio³

57

78.94

121.90

78.8766.4798.1488.03

115.3498.1094.70

Quarterly ALL/New NPL (%)

0.801.32

1.551.13

1.09

1.491.101.000.89

New NPL / Loan Portfolio (%)²

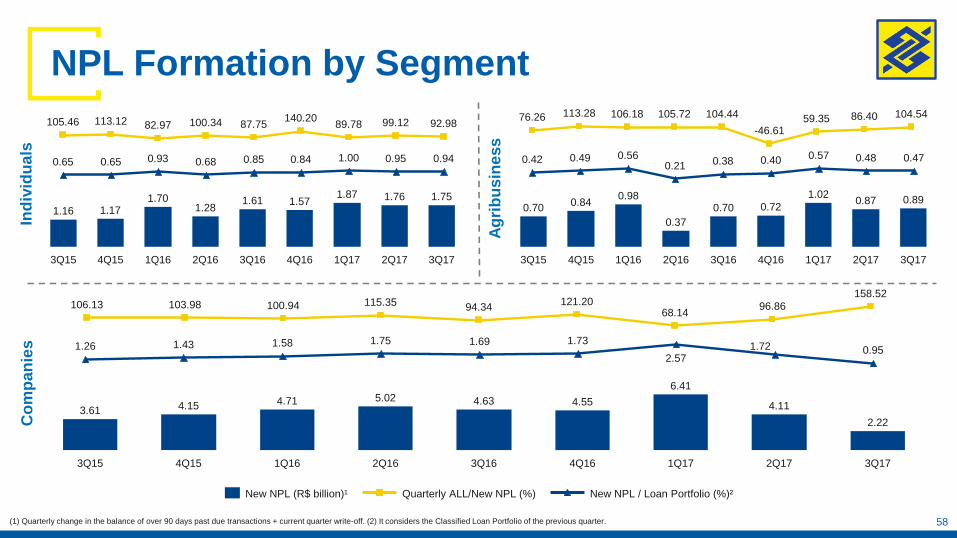

(1) Quarterly change in the balance of over 90 days past due transactions + current quarter write-off. (2) It considers the Classified Loan Portfolio of the previous quarter.

(3) Flow of the Renegotiated loan portfolio contracts of over 90 days past due transactions.

NPL Formation by Segment

2Q17

1.76

1Q17

1.87

4Q16

1.57

3Q16

1.61

2Q16

1.28

1Q16

1.70

4Q15

1.17

3Q15

1.16

3Q17

1.75

0.951.000.840.850.680.930.650.65 0.94

99.1289.78140.20

87.75100.3482.97113.12105.46 92.98

Ind

ivid

ua

ls

Ag

rib

us

ine

ss

2Q17

4.11

1Q17

6.41

4Q16

4.55

3Q16

4.63

2Q16

5.02

1Q16

4.71

4Q15

4.15

3Q15

3.61

3Q17

2.22

New NPL (R$ billion)¹

158.52

96.86121.2094.34115.35100.94103.98106.13

68.14

Quarterly ALL/New NPL (%)

0.951.721.731.691.751.581.431.26

2.57

58

Co

mp

an

ies

2Q17

0.87

1Q17

1.02

4Q16

0.72

3Q16

0.70

2Q16

0.37

1Q16

0.98

4Q15

0.84

3Q15

0.700.89

3Q17

86.4059.35-46.61

104.44105.72106.18113.2876.26 104.54

0.480.570.400.380.210.560.490.42 0.47

New NPL / Loan Portfolio (%)²

(1) Quarterly change in the balance of over 90 days past due transactions + current quarter write-off. (2) It considers the Classified Loan Portfolio of the previous quarter.

Vintages

59

Annual Vintage – Individuals Loan Portfolio

0 10 20 30

5.00%

4.00%

3.00%

2.00%

1.00%

0.00%

Delin

quency

90 d

ays

Months

40 50 0

0%

Months

5%

10%

15%

20%

10 20 30 40 50

Annual Vintage – Very Small and Small Companies

Loan Portfolio

Delin

quency

90 d

ays

Vintage: 2010A 2011A 2012A 2013A 2014A 2015A 2016A 2017A Vintage: 2010A 2011A 2012A 2013A 2014A 2015A 2016A 2017A

186.5

174.4178.4175.7

186.1

152.3

143.3146.5

167.7

159.4

ALL Balance and Coverage Ratio

R$ million

(1) Banking Industry: Ratio created through Average Risk Index available at SGS (Time Series Management System) of the Brazilian Central Bank. 60

Jun/17

37,8811,851

36,030

Mar/17

36,4141,686

34,728

Dec/16

36,0701,535

34,535

Sep/16

37,514

Sep/17

37,8062,130

35,675

Supplementary ProvisionMinimum ProvisionRequired Provision

(%)

BB +90 days BI +90 days¹

Coverage Ratio by Segment

3Q17

161.7

137.8

171.2

2Q17

167.0

126.0

177.1

1Q17

181.7

128.3

183.9

4Q16

228.9

145.8

199.6

3Q16

295.6

141.0

190.9

AgribusinessCompaniesIndividuals

61

%

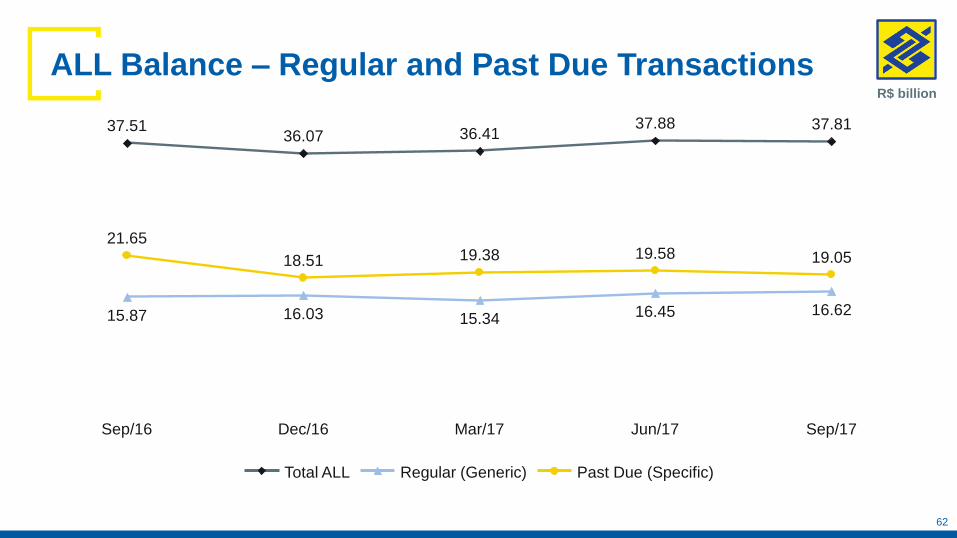

ALL Balance – Regular and Past Due Transactions

62

15.34

36.41

Dec/16

18.51

16.03

36.07

Sep/16

21.65

15.87

37.51

Sep/17

37.81

16.62

19.05

Jun/17

19.58

16.45

37.88

Mar/17

19.38

R$ billion

Past Due (Specific)Regular (Generic)Total ALL

Provision Expenses Flow / Loan Portfolio (%)

0.66

0.87

1.55

0.99

0.55

0.94

1.70

1.04

0.46

0.91

1.83

1.05

-0.24

1.18

2.21

1.15

0.55

0.75

1.66

0.99

2Q17

6,658

1,743

3,979

188 748

1Q17

6,713

1,677

4,370

60 606

4Q16

7,486

2,207

5,517

98

-336

3Q16

6,644

1,411

4,370

132 730

3Q17

6,257

1,627

3,526

175 929

Individuals

Companies

Foreign

Agribusiness

ALL by Segment (R$ million)¹

Agribusiness

Individuals

Companies

Total

63(1) Quartely ALL expenses, including write-off recovery.

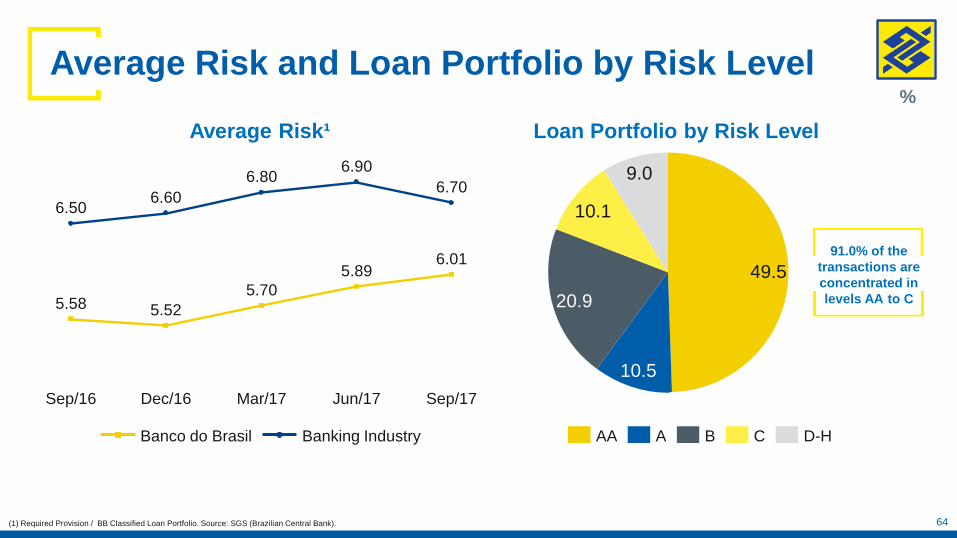

Average Risk and Loan Portfolio by Risk Level

Loan Portfolio by Risk Level

91.0% of the

transactions are

concentrated in

levels AA to C

(1) Required Provision / BB Classified Loan Portfolio. Source: SGS (Brazilian Central Bank). 64

9.0

10.1

20.9

10.5

49.5

D-HCBAAA

6.50

Sep/17

6.90

6.70

6.015.89

Jun/17Sep/16

5.58 5.52

Dec/16

6.60

5.70

6.80

Mar/17

Banco do Brasil Banking Industry

Average Risk¹

%

2Q17

5.98

3Q17

2.60

9.24

5.69

4Q16

7.42

9.278.76

3Q16

5.33

8.50

2.27

4.89

2.822.33

5.92

1Q17

2.32

AgribusinessIndividuals Companies

Average Risk by Segment¹

65

5.525.58 5.895.70 6.01

Classified Loan Portfolio

(1) Required Provision / BB Classified Loan Portfolio.

12 months Quarterly

4.204.184.334.584.43

ALL / Loan Portfolio¹

3Q17

6.3

634.2

2Q17

6.7

638.2

1Q17

6.7

644.4

4Q16

7.5

662.8

3Q16

6.6

682.0

Allowance for Loan LossesLoan Portfolio

3Q17

27.1

644.9

2Q17

27.5

657.3

1Q17

29.1

671.8

4Q16

31.6

688.8

3Q16

31.1

700.8

Allowance for Loan LossesLoan Portfolio

0.991.041.041.130.97

ALL / Loan Portfolio²

(1) ALL expenses accumulated in 12 months / 12 months Average Loan Portfolio. (2) Quarterly ALL Expenses / 3 months Average Loan Portfolio.

Cost of Risk

66

R$ billion

%

Jun/17

5.8

4.1

Mar/17

5.5

4.1

Dec/16

5.2

3.8

Sep/16

4.8

3.1

Sep/17

4.2

5.7

Peers Average²Banco do Brasil

Write-off – % of the Classified Loan Portfolio¹

67(1) Write-offs accumulated in 12 months / Classified loan Portfolio (12 months). (2) It corresponds to the three largest Brazilian private banks.

Renegotiated Past Due Loan Portfolio

68

3Q16 2Q17 3Q17

Credits Renegotiated When Past Due - Changes

Initial Balance 25,050 26,618 27,042

Contracts 2,758 3,622 1,870

Amortization Net of Interest¹ (744) (1,211) (773)

Write-Off (1,370) (1,986) (2,273)

Past due Renegotiated Loan Portfolio (A) 25,694 27,042 25,867

ALL Balance (B) 10,784 12,924 12,415

NPL + 90 days (C) 6,370 7,094 6,360

Indicators - %

ALL / Loan Portfolio (B/A) 42.0 47.8 48.0

NPL + 90 days / Loan Portfolio (C/A) 24.8 26.2 24.6

ALL Balance/NPL + 90 days (B/C) 169.3 182.2 195.2

Credits Renegotiated/Classified Loan Portfolio 3.8 4.2 4.1

2Q17

1.67

1Q17

1.97

4Q16

2.37

3Q16

2.10

3Q17

1.54

New NPL (R$ billion)²

6.277.289.248.37 5.69

New NPL / Loan Portfolio (%)³

NPL Formation

R$ million

(1) Principal and interest payments net of interest accrued in the period.

(2) Quarterly change in the balance of over 90 days past due transactions + current quarter write-off. (3) It considers the Classified Loan Portfolio of the previous quarter.

Credits Renegotiated Contracts %

0 to 14 days Past due 621 33.19

15 to 90 days Past due 588 31.43

Over 90 days Past due 452 24.16

Writen-Off Recovery 210 11.22

Total 1,870 100

Renegotiated Loan Portfolio

69

12,182 12,415

Sep/17Jun/17

12,92412,292

Mar/17

12,31411,692

Dec/16

11,92510,952

Sep/16

10,78410,734

BB - ALL BalancePeers Average - ALL Balance

24.6

21.6

26.2

22.4

27.8

24.7

27.2

24.524.8

26.8

BB - Renegotiated Portfolio NPL +90 days (%)Peers Average - Renegotiated Portfolio NPL +90 days (%)

BB x Peers¹R$ million

(1) It corresponds to the two large Brazilian private banks.

Renegotiated Loan

4.1

5.3

Renegotiated Loan Portfolio/Classified Loan Portfolio (%)

3Q17

25,86722,245

BB

Peers Average¹

%

BIS Ratio

70

17.5918.48 18.15 18.01

19.15

12.18 12.79 12.41 12.4213.29

9.07 9.59 9.20 9.18 10.04

Sep/16 Dec/16 Mar/17 Jun/17 Sep/17

Tier II Tier I Common Equity Tier I

Simulated BIS Ratio

under complete

Basel III Rules

18.6

Use of Tax Credits

0.4

BIS Ratio with Fully

Loaded Basel III Rules

18.2

RWA Rules Anticipation

-0.3

BIS Ratio with

full deductions

18.5

Deductions Schedule

Anticipation

-0.6

BIS Ratio

19.1

0.3

Use of Tax Credits

12.7

Simulated Tier 1

under complete

Basel III Rules

Tier 1 with Fully

Loaded Basel III Rules

12.4

RWA Rules Anticipation

-0.2

Tier 1 with full

deductions

12.6

Deductions Schedule

Anticipation

-0.7

Tier 1

13.3

BIS

Full Application of Basel III Rules

9.5

Use of Tax Credits

0.3

CET1 with Fully

Loaded Basel III Rules

9.1

RWA Rules Anticipation

-0.2

CET1 with full

deductions

9.3

Deductions Schedule

Anticipation

-0.7

Common Equity

Tier I (CET1)

10.0

Simulated CET1

under complete

Basel III Rules

Tie

r1

CE

T 1

%

71

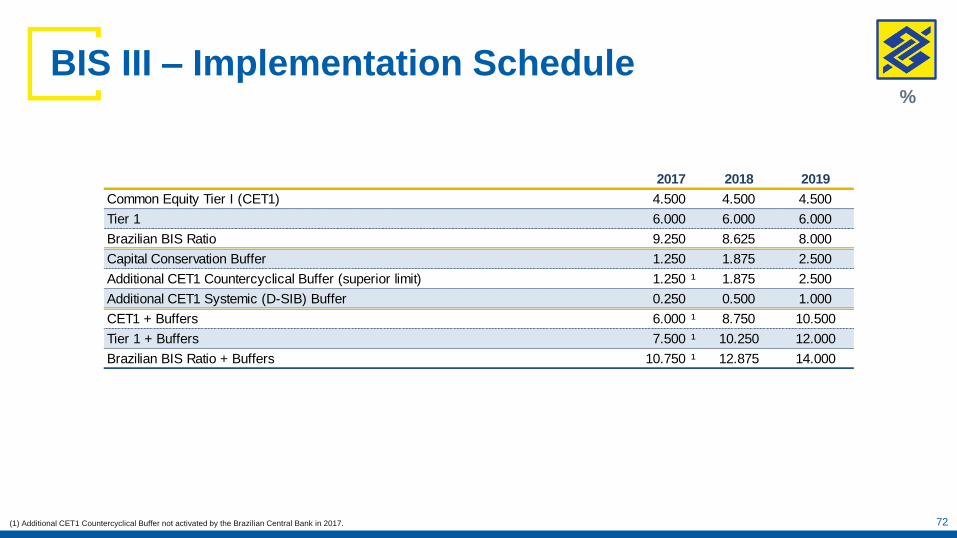

BIS III – Implementation Schedule

(1) Additional CET1 Countercyclical Buffer not activated by the Brazilian Central Bank in 2017.

%

72

2017 2018 2019

Common Equity Tier I (CET1) 4.500 4.500 4.500

Tier 1 6.000 6.000 6.000

Brazilian BIS Ratio 9.250 8.625 8.000

Capital Conservation Buffer 1.250 1.875 2.500

Additional CET1 Countercyclical Buffer (superior limit) 1.250 ¹ 1.875 2.500

Additional CET1 Systemic (D-SIB) Buffer 0.250 0.500 1.000

CET1 + Buffers 6.000 ¹ 8.750 10.500

Tier 1 + Buffers 7.500 ¹ 10.250 12.000

Brazilian BIS Ratio + Buffers 10.750 ¹ 12.875 14.000

Guidance 2017

73

Guidance

2017

9M17

Performance

Adjusted Net Income - R$ billion 9.5 to 12.5 7.9

NII (Net of Recovery of Write-offs) - % -4 to 0 -2.2

Organic Domestic Loan Portfolio - Expanded View - % -4 to -1 -6.9

Individuals - % 2 to 5 1.1

Companies - % -11 to -8 -16.0

Rural Loans - % 6 to 9 5.0

ALL Expenses net of Recovery of Write-offs - R$ billion -23.5 to -20.5 -16.2

Fee Income - % 6 to 9 9.9

Administrative Expenses - % -2.5 to 0.5 -2.7

Net Income (R$ million)

Delinquency and Risk (%)

Banco Votorantim

2Q17

145.1

1Q17

127.4

4Q16

119.3

3Q16

112.1

3Q17

153.3

Jun/17

88.9

11.1

Mar/17

89.2

10.8

Dec/16

88.3

11.7

Sep/16

90.2

9.8

Sep/17

89.5

10.5

AA-CD-H

4.5 4.4

5.55.5

4.1

NPL +90 days / Loan Portfolio

74

03MACROECONOMIC INFORMATION

Inflation and Selic Rate

76

2012 2013 2014 2015 2016

7.28

8.49

2.172.50

5.84 5.91

8.21

10.67

6.41

10.91

13.28

4.23

14.03

2.36

6.29

Accumulated Selic (% YTD in 12 months) IPCA (acum. 12 months % a.a.) Real Interest Rate²

9.84

3.08

6.56

2017¹

6.88

4.02

2.75

2018¹

14.16

2.54

8.48

5.24

Sep/16

11.56

8.80

Sep/17

(1) Source: Banco Central do Brasil and IBGE. Projection for 2017 and 2018, according to Boletim Focus as of August 11, 2017. (2) Real Interest Rate = Selic / IPCA

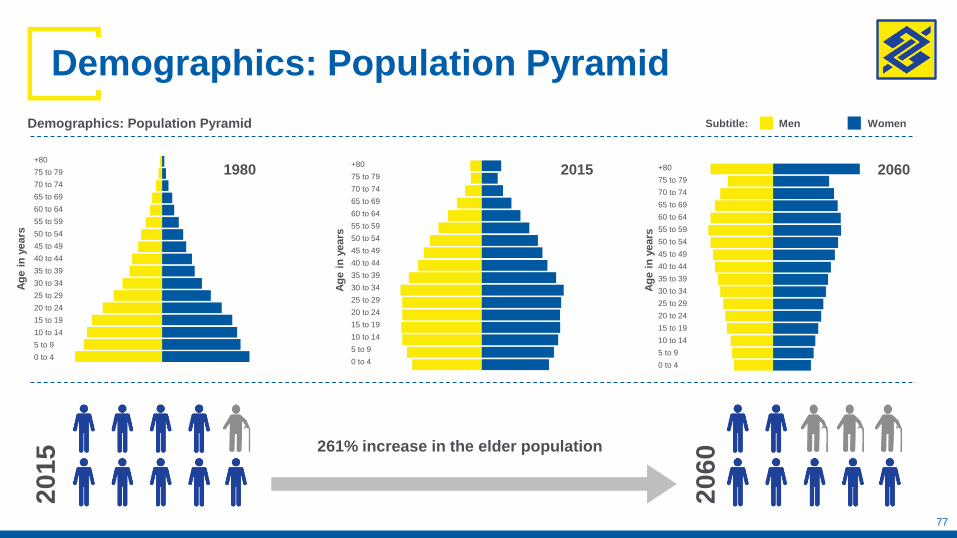

Demographics: Population Pyramid

0 to 4

5 to 9

10 to 14

15 to 19

20 to 24

25 to 29

30 to 34

35 to 39

40 to 44

45 to 49

50 to 54

55 to 59

60 to 64

65 to 69

70 to 74

75 to 79

+80

0 to 4

5 to 9

10 to 14

15 to 19

20 to 24

25 to 29

30 to 34

35 to 39

40 to 44

45 to 49

50 to 54

55 to 59

60 to 64

65 to 69

70 to 74

75 to 79

+80

0 to 4

5 to 9

10 to 14

15 to 19

20 to 24

25 to 29

30 to 34

35 to 39

40 to 44

45 to 49

50 to 54

55 to 59

60 to 64

65 to 69

70 to 74

75 to 79

+80

Demographics: Population Pyramid

206020151980

Subtitle: Men Women

20

15

20

60261% increase in the elder population

77

Ag

e i

n y

ears

Ag

e i

n y

ears

Ag

e i

n y

ears

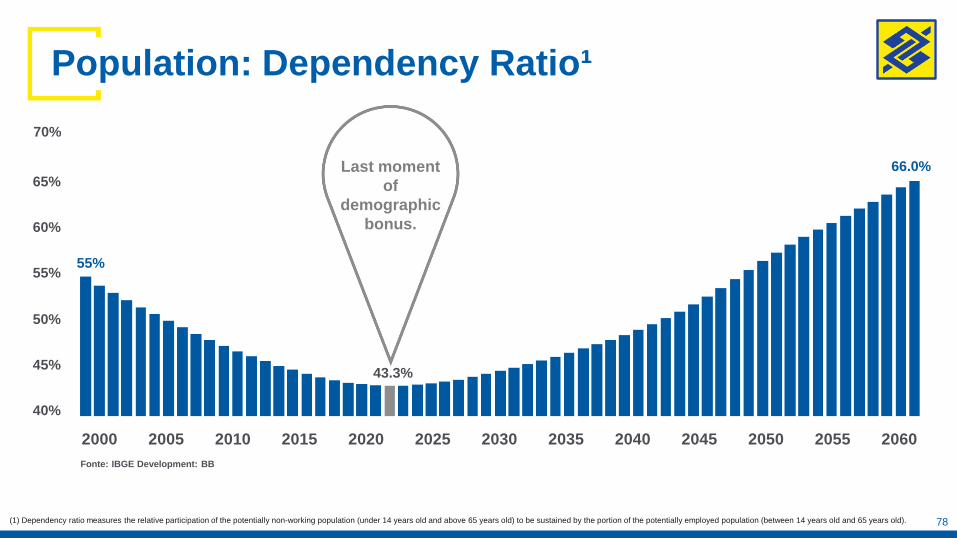

Population: Dependency Ratio¹

2000 2005 2010 2015 2020 2025 2030 2035 2040 2045 2050 2055 2060

55%

66.0%

40%

45%

50%

55%

60%

65%

70%

(1) Dependency ratio measures the relative participation of the potentially non-working population (under 14 years old and above 65 years old) to be sustained by the portion of the potentially employed population (between 14 years old and 65 years old).

Fonte: IBGE Development: BB

Last moment

of

demographic

bonus.

78

43.3%

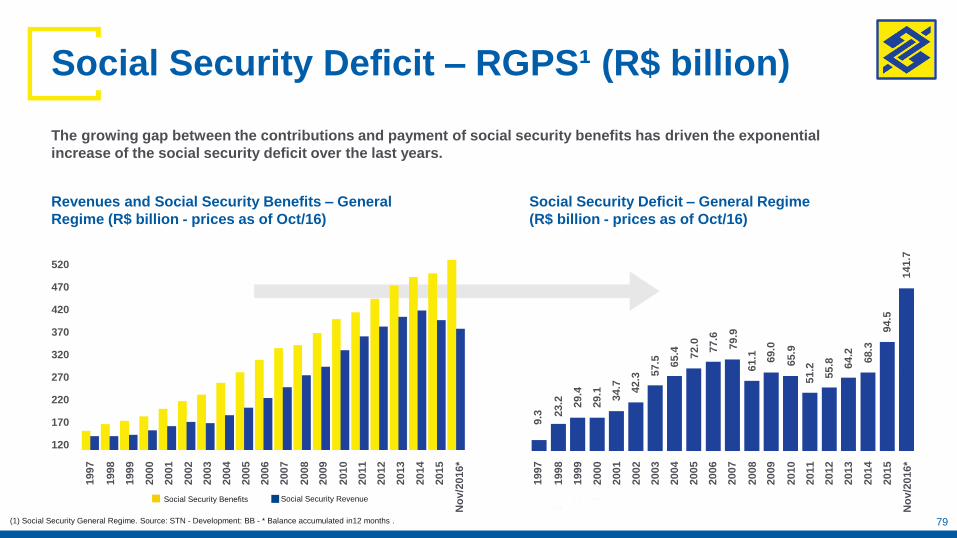

Social Security Deficit – RGPS¹ (R$ billion)

The growing gap between the contributions and payment of social security benefits has driven the exponential

increase of the social security deficit over the last years.

Social Security Deficit – General Regime

(R$ billion - prices as of Oct/16)

(1) Social Security General Regime. Source: STN - Development: BB - * Balance accumulated in12 months .

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

No

v/2

016*

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

No

v/2

016*

120

170

220

270

320

370

420

470

520

9.3 2

3.2 29.4

34.7

29.1 4

2.3

57.5 65.4 72.0

77.6

79.9

61.1 69.0

65.9

51.2

55.8 64.2

68.3

94.5

141.7

Revenues and Social Security Benefits – General

Regime (R$ billion - prices as of Oct/16)

79

Social Security Benefits Social Security Revenue

Main Pillars of Brazilian Growth

Agriculture InfrastructureForeign

Trade

80

81

Sustainable Growth

Brazil

USAChina

India Russia

Argentina

Kasakhstan

Australia Canada

Germany

UKFrance

Korea

Italy

Spain

Japan

Mexico

Indonesia

Planting Area

> 140 million há¹GDP > US$ 1 trillion¹

Brazil has the ideal conditions for sustainable growth.

Only a few countries have the same potential.

Urban Population

> 80 million people¹

Source: World Bank and FAO.(1) 2011.

Brazilian Agribusiness: Overview

Area

8.5 milllion Km²

Overview

Population (2016)

206 million

GDP (2Q17)

+0.2%¹

Agricultural GDP (1H17)

+15.0%¹

Source: Ministério da Agricultura and IBGE.(1) Change in Quarterly flow. 82

Production

Brazil: World Commodities Ranking

Exports

Coffee

Orange Juice

Sugar

Soybean

Poultry

Beef

Corn

Source: USDA – PSD online.

Sep/17

PPPs in Brazil can reach R$ 1.3 trillion (USD 395 billion CAPEX) over

the next years

R$ 324.8 billion in Logistics and Urban Mobility

Toll Roads

R$ 14.7billion

Toll Roads

R$ 11.81billion

Logistics: R$ 61.6 billion

Railroads

R$ 39.0billion

São Paulo Segue em Frente: R$ 13.4 billion

Bus Service

R$ 2.6billion

Ports

R$ 1.5billion

Metro Line

R$ 0.2billion

Airports

R$ 6.4billion

Regional

Airports

R$ 0.1 billion

BNDES – Expectation of investments in Urban Mobility: R$ 234 billion

R$ 688.1 billion in Water and Waste, Urbanization & Street Lighting

Water

R$ 158.7 billion

Plansab – National Plan for Sanitation: R$ 660.4 billion expected up to 2033

Street Lighting: R$ 27.8 billion

Sewage

R$ 236.2billion

Waste

R$ 30.3 billion

Drainage

R$ 89.2billion

Managment*

R$ 145.9billion

* Actions related to increase efficiency in the management and provision of services, to technical qualification of employees and to

implementation of educational campaigns, among others actions.

R$ 41.1 billion in Power Sector

Generation R$ 7.6 billion

Transmission Lines R$

33.2 billion (lot Out/16 +

2017 auctions)

R$ 263 billion* in Oil & Gas

Oil US$ 80 billion*

According to the Energy Ministry

Source: MPDG, MME, MCidades, MMA and SP Government.

Produced by: BB. ** USD = R$ 3.29 as of November 03, 2017.

83

36% 100%

50%

100%

98%

91%

84

Brazilian Foreign Trade Balance Evolution

47.7

19.7

-4.0

Trade Balance (US$ billion – year accumulated)

2016

137.6

185.3171.5

2015

191.1

2014

229.1225.1

Exports (US$ billion – year accumulated) Imports (US$ billion – year accumulated)

3Q16

139.4

103.2111.3

3Q17

164.6

36.2

53.3

Source: Ministério do Desenvolvimento, Indústria e Comércio Exterior.

Summary Table

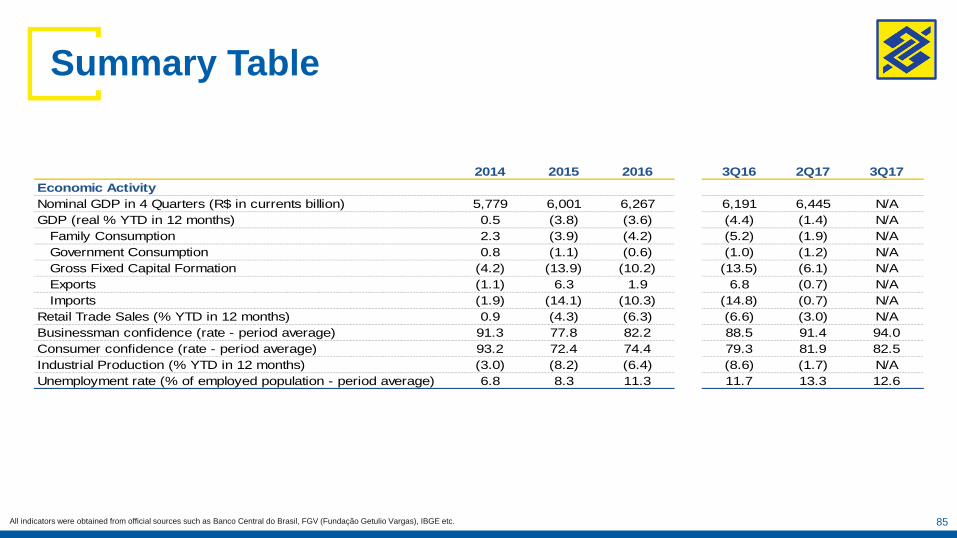

85All indicators were obtained from official sources such as Banco Central do Brasil, FGV (Fundação Getulio Vargas), IBGE etc.

2014 2015 2016 3Q16 2Q17 3Q17

Economic Activity

Nominal GDP in 4 Quarters (R$ in currents billion) 5,779 6,001 6,267 6,191 6,445 N/A

GDP (real % YTD in 12 months) 0.5 (3.8) (3.6) (4.4) (1.4) N/A

Family Consumption 2.3 (3.9) (4.2) (5.2) (1.9) N/A

Government Consumption 0.8 (1.1) (0.6) (1.0) (1.2) N/A

Gross Fixed Capital Formation (4.2) (13.9) (10.2) (13.5) (6.1) N/A

Exports (1.1) 6.3 1.9 6.8 (0.7) N/A

Imports (1.9) (14.1) (10.3) (14.8) (0.7) N/A

Retail Trade Sales (% YTD in 12 months) 0.9 (4.3) (6.3) (6.6) (3.0) N/A

Businessman confidence (rate - period average) 91.3 77.8 82.2 88.5 91.4 94.0

Consumer confidence (rate - period average) 93.2 72.4 74.4 79.3 81.9 82.5

Industrial Production (% YTD in 12 months) (3.0) (8.2) (6.4) (8.6) (1.7) N/A

Unemployment rate (% of employed population - period average) 6.8 8.3 11.3 11.7 13.3 12.6

Summary Table

86All indicators were obtained from official sources such as Banco Central do Brasil, FGV (Fundação Getulio Vargas), IBGE etc.

2014 2015 2016 3Q16 2Q17 3Q17

External Sector

Current Transactions (% GDP in 12 months) (4.2) (3.3) (1.3) (1.3) (0.8) (0.6)

Direct Foreign Investment (US$ billion - year accumulated) 97.2 74.7 78.2 46.5 36.2 51.8

Trade Balance (US$ billion – year accumulated) (4.0) 19.7 47.7 36.2 36.3 53.3

Exports (US$ billion – year accumulated) 225.1 191.1 185.3 139.4 107.7 164.6

Basic 109.6 87.2 79.2 62.1 52.5 78.3

Manufactured 80.2 72.8 73.9 53.5 37.7 59.2

Semi-manufactured 29.1 26.5 28.0 20.6 15.1 23.3

Special Operations 6.3 4.7 4.2 3.2 2.5 3.7

Imports (US$ billion – year accumulated) 229.1 171.5 137.6 103.2 71.5 111.3

Capital Goods 29.5 23.3 18.4 14.4 7.3 11.7

Intermediary Goods 126.9 99.5 84.9 63.3 45.0 70.1

Consumer Products 33.1 26.8 21.7 16.1 11.0 16.9

Fuels 39.5 21.7 12.4 9.3 8.2 12.6

Other 0.2 0.2 0.1 0.1 0.1 0.1

International Reserves (US$ billion – end of period) 375.8 361.2 367.5 369.3 374.9 381.0

Sovereign Risk (basis points – end of period) 259 523 328 319 289 247

CDS 10Y (In base points - end of period) 259 558 360 347 346 306

Exchange Rate (R$/US$ - end of period) 2.66 3.90 3.26 3.25 3.31 3.17

Public Finance

PSGD (% GDP) 56.3 65.5 69.9 69.9 72.5 73.9

Nominal Result (R$ billion - in 12 months) (343.9) (613.0) (562.8) (576.8) (607.5) (567.5)

Nominal Result (% GDP - in 12 months) (6.0) (10.2) (9.0) (9.3) (9.4) (8.8)

Monetary Ratios

Selic (end of period %) 11.75 14.25 13.75 14.25 10.25 8.25

Accumulated Selic (% YTD in 12 months) 10.91 13.28 14.03 14.16 12.89 11.56

04 SUSTAINABILITY

Socio-environmental (SER) Policy

Development of

responsible socio-

environmental

businesses and

Private Social

Investment

SER Governance

and socio-

environmental risk

management

Natural

resources

conscious

consumption

For us in Banco do Brasil, socio-

environmental responsibility

means: “to have Ethics as our

commitment and Respect as our

attitude in our interactions

with employees, stakeholders,

suppliers, partners,

customers, creditors,

shareholders, competitors,

community, government and the

environment”.

88

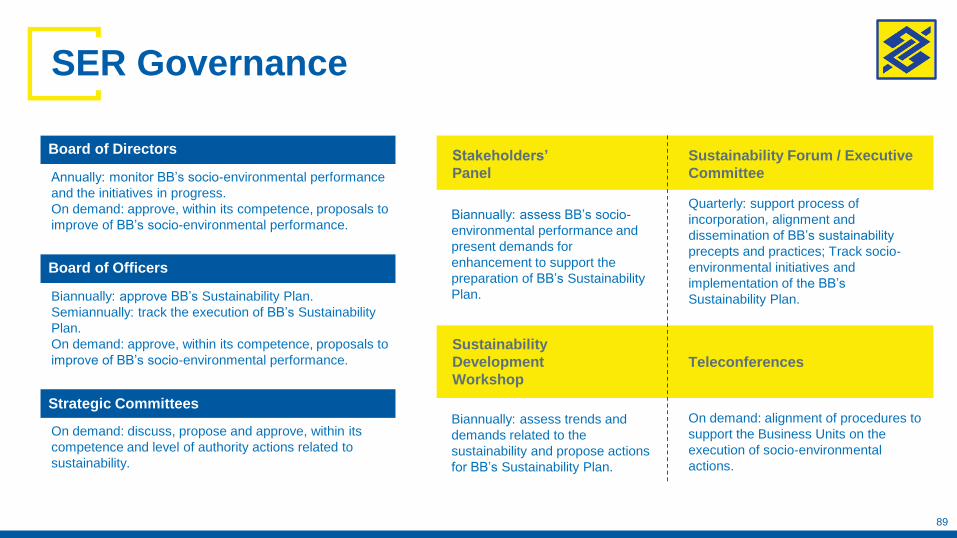

Board of Directors

Annually: monitor BB’s socio-environmental performance

and the initiatives in progress.

On demand: approve, within its competence, proposals to

improve of BB’s socio-environmental performance.

Board of Officers

Biannually: approve BB’s Sustainability Plan.

Semiannually: track the execution of BB’s Sustainability

Plan.

On demand: approve, within its competence, proposals to

improve of BB’s socio-environmental performance.

Strategic Committees

On demand: discuss, propose and approve, within its

competence and level of authority actions related to

sustainability.

Biannually: assess BB’s socio-

environmental performance and

present demands for

enhancement to support the

preparation of BB’s Sustainability

Plan.

Quarterly: support process of

incorporation, alignment and

dissemination of BB’s sustainability

precepts and practices; Track socio-

environmental initiatives and

implementation of the BB’s

Sustainability Plan.

Stakeholders’

Panel

Sustainability Forum / Executive

Committee

Sustainability

Development

Workshop

Teleconferences

Biannually: assess trends and

demands related to the

sustainability and propose actions

for BB’s Sustainability Plan.

On demand: alignment of procedures to

support the Business Units on the

execution of socio-environmental

actions.

SER Governance

89

SER Strategy – Agenda 30 BB

PROSPECTION

AND CONSULT REPORTS AND

TRANSPARENCY

FEEDBACK

SOCIO-ENVIRONMENTAL PERFORMANCE

Inductor Instruments

Legislation

Specific and General Policies

Internal rules

Board of Directors

Corporate Strategy and BB’s Sustainability Plan

Performance Evaluation

Instruments: Master Plan, Balance Scorecard,

Manager Radar

Metrics: Socio-environmental indexes,

Capital Markets indexes, such as DJSI and

ISE

Annual Report

Management

Report

Intranet/Internet

Campaigns

Market Trends and

Demands / Society

Stakeholders

Panel

Capital Markets

Indexes

Sustainability

Rankings

90

Updated every 2 years based on market and society demands

394 actions between 2005 and 2017 (5 editions)

Sixth version (2017-2019) – 82 actions

Inspired on UN Sustainable Development Goals

Followed by Sustainability Forum, Board of Officers and Board of Directors

Results presented in Annual Report

Capital Market awards: DJSI, ISE, ICO2

SER Strategy – Agenda 30 BB

Planet

Structured in 5 pillars:

Prosperity

Partnership

People

Peace

91

Socio-environmental Risk Management

Socio-environmental Risk

Potential Losses coming from social and / or environmental impacts generated by the

institution's activities, directly or indirectly.

The procedures to manage socio-environmental risk encompass exposures on credit,

investments, insurance, operational risks, strategy risk, reputation risk and administrative

activities.

Business

Management

92

1969

First public

contest

available for

women

1979

First woman

signed for a

lead position

in a branch

Promotion of gender equity

2006

BB signs the

“Programa

Pró-Equidade

de Gênero”

from the

Federal

Government

1987

First women

signed for a

lead position

abroad

1996

First three

woman in the

executive

manager

position

2003

First female

Senior

Director

(statutory

position)

2010

Signing up of

the UN

Women's

Empowerment

Principles

2017 Increase of gender

affirmative actions in the

programs of professional

ascent.

Extension to transgenders

of the exclusive Internal

Ombudsman channel for

women.

All executives sign up to

for the HeForShe

movement (from UN

Women).

93

Business Letter for

the Human Rights

and for Promotion of

Decent LaborPrinciples of

Equator

1995 1997 2003

BB Letter of Socio-environmental

Responsibility Principles

2004

AGENDA

21

2005 2006 2007 2008 2009 2010 2011 2012

Business Pact

for Integrity and

Against

Corruption

2013

Sustainable Animal

Husbandry

Working Group

2014

OECD Guidelines

for Multinational

Companies

20151991 2017

Green Protocol

Pacts and Voluntary Commitments

CORPORATE SUSTAINABILITY INDEX (ISE) – BM&F BOVESPA - 2017

12 CONSECUTIVE LISTING YEARS SINCE THE FIRST PORTFOLIO IN 2005

DOW JONES SUSTAINABILITY INDEX (DJSI) NEW YORK STOCK EXCHANGE – 2016, LISTED FOR

5 CONSECUTIVE YEARS.

BB IS A GLOBAL BENCHMARKING IN THE THEMES "CUSTOMER RELATIONSHIP MANAGEMENT",

"FINANCIAL STABILITY / SYSTEMIC RISK", "ANTICRIME POLICY & MEASURES“ "CORPORATE CITIZENSHIP

AND PHILANTHROPY", "FINANCIAL INCLUSION“ AND "CONTROVERSIAL ISSUES, DILEMMAS IN LENDING &

FINANCING."

CARBON EFFICIENT INDEX (ICO2) – BM&FBOVESPA - 2016

Market Indexes and Awards

95

Av. Paulista, 1230

18th. floor – Bela Vista

São Paulo/SP - Brasil - CEP 01310-100

www.bb.com.br/ir [email protected] +55 (11) 4298-8000