presentation on results q2 & h1 fy 2015-16 presentation on results q2 & h1 fy15-16 mssl...

TRANSCRIPT

Presentation on Results Q2 & H1 FY 2015-16

06th November 2015

Proud to be part of the world’s most admired automotive brands

MSSL Presentation on Results Q2 & H1 FY15-16 2

• Highlights

• MSSL performance

• SMRPBV performance

• Debt status

MSSL Presentation on Results Q2 & H1 FY15-16

Highlights Consolidated

3

Q2 vs Q2

29%

EBITDA

14%

11% 15%

176% 53%

Total Sales

Sales (outside

India)

Sales (within India)

PBT PAT

H1 vs H1

MSSL: Motherson Sumi Systems Ltd; SMRP BV : Samvardhana Motherson Automotive Systems Group BV, SMR: Samvardhana Motherson Reflectec; SMP: Samvardhana Motherson Peguform

21%

EBITDA

13%

08% 14%

106% 36%

Total Sales

Sales (outside

India)

Sales (within India)

PBT PAT

MSSL Presentation on Results Q2 & H1 FY15-16

Highlights Standalone

4

MSSL: Motherson Sumi Systems Ltd; SMRP BV : Samvardhana Motherson Automotive Systems Group BV, SMR: Samvardhana Motherson Reflectec; SMP: Samvardhana Motherson Peguform

Q2 vs Q2 H1 vs H1

18%

EBITDA

09%

09% 07%

36% 38%

Total Sales

Sales (outside

India)

Sales (within India)

PBT PAT

10%

EBITDA

05%

06% 03%

40% 38%

Total Sales

Sales (outside

India)

Sales (within India)

PBT PAT

MSSL Presentation on Results Q2 & H1 FY15-16

Highlights SMRP BV (in Euro Terms)

5

MSSL: Motherson Sumi Systems Ltd; SMRP BV : Samvardhana Motherson Automotive Systems Group BV, SMR: Samvardhana Motherson Reflectec; SMP: Samvardhana Motherson Peguform

Q2 vs Q2 H1 vs H1

33%

EBITDA

24%

267% 56%

Total Sales

PBT PAT

(concern share)

29%

EBITDA

25%

267% 40%

Total Sales

PBT PAT

(concern share)

MSSL Presentation on Results Q2 & H1 FY15-16

Highlights SMR & SMP (in Euro Terms)

6

MSSL: Motherson Sumi Systems Ltd; SMRP BV : Samvardhana Motherson Automotive Systems Group BV, SMR: Samvardhana Motherson Reflectec; SMP: Samvardhana Motherson Peguform

Q2 vs Q2 H1 vs H1

23%

EBITDA

14%

Sales

41%

EBITDA

31%

Sales

23%

EBITDA

19%

Sales

34%

EBITDA

28%

Sales

MSSL Presentation on Results Q2 & H1 FY15-16 7

• Highlights

• MSSL performance

• SMRPBV performance

• Debt status

MSSL Presentation on Results Q2 & H1 FY15-16

MSSL Consolidated : Q2 FY 2015-16 vs. Q2 FY 2014-15

(Rs. Crores) Q2 2014-15

Q2 2015-16

Exchange Loss / ( Gain ) on Long Term Facilities 15 39

Exceptional expenses - on Bond Issue and acquisition expenses 124 2

Notes :

1,333 1,479

6,589 7,558

7,922 9,037

-

2,000

4,000

6,000

8,000

10,000

Q2 FY 2014-15 Q2 FY 2015-16

Within India Outside India Total

724

935

9.1%

10.3%

0%

2%

4%

6%

8%

10%

12%

400

600

800

1,000

Q2 FY 2014-15 Q2 FY 2015-16

EBITDA % of Sales

396

605

104

287

-

100

200

300

400

500

600

700

Q2 FY 2014-15 Q2 FY 2015-16

PBT PAT

(Rs.

in C

rore

s)

(Rs.

in C

rore

s)

(Rs.

in C

rore

s)

{# concern share after exchange loss/(gain)exceptional expenses}

{* Before exchange loss/ (Gain) and exceptional expenses/(income)}

Sales EBITDA* / % to Sales PBT * & PAT#

8

14%

53%

176%

Currency (equal to Rs.)

Q2 2014-15

Q2 2015-16

% Change

EURO 80.26 72.38 -10%

Exchange rate for Euro

29%

MSSL Presentation on Results Q2 & H1 FY15-16

MSSL Standalone : Q2 FY 2015-16 vs. Q2 FY 2014-15

Notes :

(Rs.

in C

rore

s)

(Rs.

in C

rore

s)

(Rs.

in C

rore

s)

Sales EBITDA* / % to Sales

232 273

18.6% 20.1%

0%

4%

8%

12%

16%

20%

24%

50

100

150

200

250

300

Q2 FY 2014-15 Q2 FY 2015-16 EBITDA % of Sales

208

287

145

197

-

50

100

150

200

250

300

350

Q2 FY 2014-15 Q2 FY 2015-16 PBT PAT

1,057 1,156

190 203

1,247 1,359

-

300

600

900

1,200

1,500

Q2 FY 2014-15 Q2 FY 2015-16 Domestic Exports

(Rs. Crores) Q2 2014-15

Q2 2015-16

Exchange Loss / ( Gain ) on Long Term Facilities 13 13

Dividend Income 40 68

9

9% 18% 38%

{* Before exchange loss/ (Gain) and exceptional expenses/(income)} {# Before exchange loss/(Gain), exceptional expense/(income), including gain on sales of investment in JV and redemption of preference share and dividend income

36%

Average Q2 2014-15

Q2 2015-16

% Change

LME Copper (USD / Ton ) 6,993 5,251 -25%

INR to Euro 80.16 72.38 -10%

INR to YEN 0.583 0.532 -9%

Copper rate & exchange rates considered

PBT * & PAT#

MSSL Presentation on Results Q2 & H1 FY15-16

MSSL Consolidated : H1 FY 2015-16 vs. H1 FY 2014-15

(Rs. Crores) H1 2014-15

H1 2015-16

Exchange Loss / ( Gain ) on Long Term Facilities 26 47

Exceptional expenses- on Bond Issue and acquisition expenses 170 27

Gain on sale of investment in JV - 22

Notes :

2,581 2,783

13,638 15,506

16,219 18,289

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

H1 FY 2014-15 H1 FY 2015-16

Within India Outside India Total

1,462 1,776

9.0% 9.7%

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

H1 FY 2014-15 H1 FY 2015-16

EBITDA % of Sales

858

1,168

268 553

-

300

600

900

1,200

1,500

H1 FY 2014-15 H1 FY 2015-16

PBT PAT

(Rs.

in C

rore

s)

(Rs.

in C

rore

s)

(Rs.

in C

rore

s)

{* Before exchange loss/ (Gain) and exceptional expenses/(income)}

Sales EBITDA* / % to Sales

10

21% 36%

106%

{# Before exchange loss/(Gain), exceptional expense/(income), including gain on sales of investment in JV and redemption of preference share and dividend income

Exchange rate for Euro

Currency (equal to Rs.)

H1 2014-15

H1 2015-16

% Change

EURO 81.15 71.25 -12 %

13%

PBT * & PAT#

MSSL Presentation on Results Q2 & H1 FY15-16

MSSL Standalone : H1 FY 2015-16 vs. H1 FY 2014-15 (R

s. in

Cro

res)

(Rs.

in C

rore

s)

(Rs.

in C

rore

s)

{* Before exchange loss/ (Gain) and exceptional expenses/(income)}

Sales EBITDA* / % to Sales

450 494

18.4% 19.2%

50

100

150

200

250

300

350

400

450

500

550

H1 FY 2014-15 H1 FY 2015-16 EBITDA % of Sales

373

513

255 356

-

100

200

300

400

500

600

H1 FY 2014-15 H1 FY 2015-16 PBT PAT

2,060 2,174

388 401 2,448 2,575

-

500

1,000

1,500

2,000

2,500

3,000

H1 FY 2014-15 H1 FY 2015-16 Domestic Exports

(Rs. Crores) H1 2014-15

H1 2015-16

Exchange Loss / ( Gain ) on Long Term Facilities 16 20

Gain on sale of JV - 36

Gain on redemption of preference share - 9

Dividend Income 40 77

11

10% 38% 40%

{# Before exchange loss/(Gain), exceptional expense/(income), including gain on sales of investment in JV and redemption of preference share and dividend income

Notes :

PBT * & PAT#

5%

Average H1 2014-15

H1 2015-16

% Change

LME Copper (USD / Ton ) 6,890 5,653 -18%

INR to Euro 81.15 71.25 -12%

INR to YEN 0.584 0.527 -10%

Copper rate & exchange rates considered

MSSL Presentation on Results Q2 & H1 FY15-16 12

• Highlights

• MSSL performance

• SMRPBV performance

• Debt status

MSSL Presentation on Results Q2 & H1 FY15-16

SMRPBV : Q2 FY 2015-16 vs. Q2 FY 2014-15 (In Euro Terms**)

Notes :

(In M

illio

n Eu

ro)

(In M

illio

n Eu

ro)

(In M

illio

n Eu

ro)

{* Before exchange loss/ (Gain) and excep8onal expenses/(income)}

Sales EBITDA* / % to Sales

(In Million Euro) Q2 2014-15

Q2 2015-16

Exceptional expenses towards bonds issuance 11 0

Exchange Loss / (Gain) on Long Term Facilities

0 4

{# concern share}

55

73

7.2% 7.7%

0%

2%

4%

6%

8%

-

20

40

60

80

Q2 FY 2014-15 Q2 FY 2015-16 EBITDA % of Sales

12 16

745 926

757

942

-

200.00

400.00

600.00

800.00

1,000.00

1,200.00

Q2 FY 2014-15 Q2 FY 2015-16 Within India Outside India Total

25

39

3

11

-

10

20

30

40

50

Q2 FY 2014-15 Q2 FY 2015-16 PBT PAT- Concern Share

13

** Please refer to Note on last slide.

267%

Rs.6,067 Cr Rs.6,820 Cr Rs.438 Cr Rs.525 Cr Rs.202 Cr Rs.279 Cr

Rs.20 Cr

Rs.76 Cr

24%

PBT * & PAT#

33%

56%

MSSL Presentation on Results Q2 & H1 FY15-16

SMR : Q2 FY 2015-16 vs. Q2 FY 2014-15 (In Euro Terms**)

Sales EBITDA* / % to Sales

26 32

9.0% 9.6%

-

10

20

30

40

Q2 FY 2014-15 Q2 FY 2015-16 EBITDA % of Sales

12 16

281 319

293 335

-

50

100

150

200

250

300

350

400

Q2 FY 2014-15 Q2 FY 2015-16

Within India Outside India Total

*At exchange rate used for translation

Sales

14%

EBITDA

23%

14

(in M

illio

n Eu

ro)

Rs. 2,348 cr. Rs. 2,424 cr. Rs. 214 cr. Rs. 232 cr.

(in M

illio

n Eu

ro)

** Please refer to Note on last slide.

MSSL Presentation on Results Q2 & H1 FY15-16

SMP : Q2 FY 2015-16 vs. Q2 FY 2014-15 (In Euro Terms**)

Sales EBITDA* / % to Sales

(in M

illio

n Eu

ro)

(in M

illio

n Eu

ro)

*At exchange rate used for translation Sales

31%

EBITDA

41%

464 608

-

200

400

600

800

Q2 FY 2014-15 Q2 FY 2015-16

Rs. 3,719 cr.

29 41

6.3% 6.7%

-

5

10

15

20

25

30

35

40

45

50

Q2 FY 2014-15 Q2 FY 2015-16 EBITDA % of Sales

Rs. 4,399 cr. Rs. 224 cr. Rs. 295 cr.

15

** Please refer to Note on last slide.

MSSL Presentation on Results Q2 & H1 FY15-16

SMRPBV : H1 FY 2015-16 vs. H1 FY 2014-15 (In Euro Terms**)

Notes :

(In M

illio

n Eu

ro)

(In M

illio

n Eu

ro)

(In M

illio

n Eu

ro)

{* Before exchange loss/ (Gain) and excep8onal expenses/(income)}

Sales EBITDA* / % to Sales

(In Million Euro) H1 2014-15

H1 2015-16

Exceptional expenses towards bonds issuance 16 4

Exchange Loss / (Gain) on Long Term Facilities

1 4

{# concern share}

22 28

1,560 1,945

1,582

1,973

-

400.00

800.00

1,200.00

1,600.00

2,000.00

2,400.00

H1 FY 2014-15 H1 FY 2015-16 Within India Outside India Total

58

81

6

22

-

25

50

75

100

H1 FY 2014-15 H1 FY 2015-16 PBT PAT- Concern Share

Rs.1,041 cr. Rs.919 cr. Rs.12,842 cr. Rs. 14,059 cr. Rs.577 cr.

Rs.464 cr.

Rs.49 cr.

Rs.158 cr.

16

25% 29% 267%

** Please refer to Note on last slide.

PBT * & PAT#

113 146

7.2% 7.4%

-

40

80

120

160

H1 FY 2014-15 H1 FY 2015-16 EBITDA % of Sales

40%

MSSL Presentation on Results Q2 & H1 FY15-16

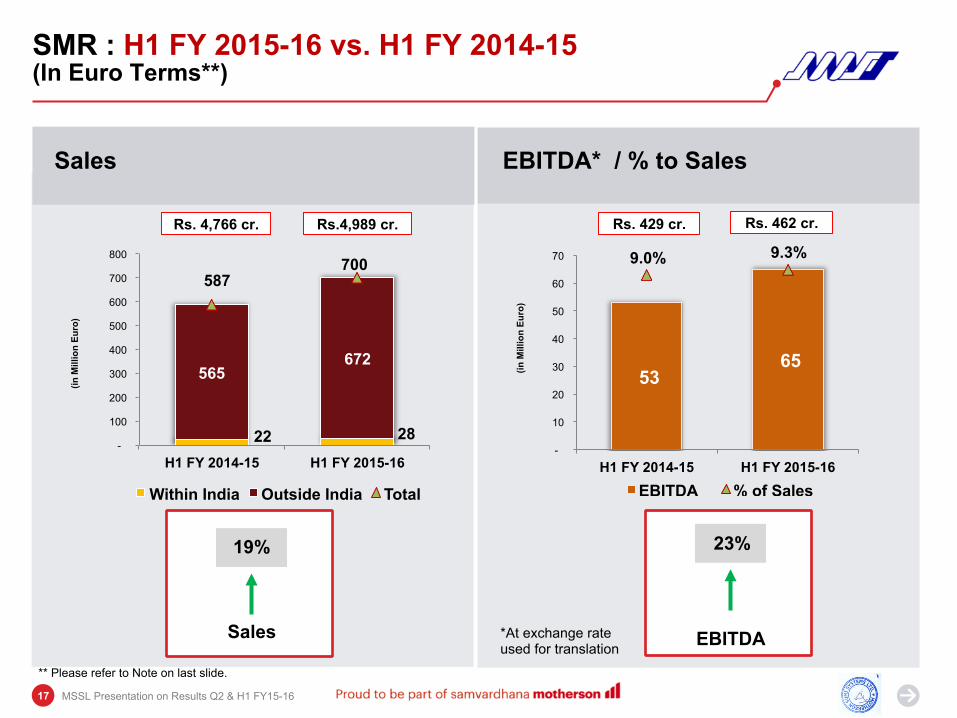

SMR : H1 FY 2015-16 vs. H1 FY 2014-15 (In Euro Terms**)

Sales EBITDA* / % to Sales

53 65

9.0% 9.3%

-

10

20

30

40

50

60

70

H1 FY 2014-15 H1 FY 2015-16 EBITDA % of Sales

22 28

565 672

587 700

-

100

200

300

400

500

600

700

800

H1 FY 2014-15 H1 FY 2015-16

Within India Outside India Total

*At exchange rate used for translation

Sales

19%

EBITDA

17

(in M

illio

n Eu

ro)

Rs. 4,766 cr. Rs.4,989 cr. Rs. 429 cr. Rs. 462 cr.

(in M

illio

n Eu

ro)

** Please refer to Note on last slide.

23%

MSSL Presentation on Results Q2 & H1 FY15-16

SMP : H1 FY 2015-16 vs. H1 FY 2014-15 (In Euro Terms**)

Sales EBITDA* / % to Sales

(in M

illio

n Eu

ro)

(in M

illio

n Eu

ro)

*At exchange rate used for translation Sales

28%

EBITDA

34%

995 1,274

-

200

400

600

800

1,000

1,200

1,400

H1 FY 2014-15 H1 FY 2015-16

Rs. 8,076 cr.

61 82

6.1% 6.4%

-

15

30

45

60

75

90

H1 FY 2014-15 H1 FY 2015-16 EBITDA % of Sales

Rs. 9,077 cr. Rs. 496 cr. Rs. 586 cr.

18

** Please refer to Note on last slide.

MSSL Presentation on Results Q2 & H1 FY15-16 19

• Highlights

• MSSL performance

• SMRPBV performance

• Debt status

MSSL Presentation on Results Q2 & H1 FY15-16

Debt status

20

Net Debt

Exchange rate used

Rs/Euro

Rs/USD

31.03.2015

67.06

62.50

30.06.2015

70.86

63.64

30.09.2015

73.30

65.58

(Rs. In crores)

387 275 303

3,241 3,794

4,566

31.03.2015 30.06.2015 30.09.2015

Standalone Consolidated

223

209

220

Debt due within 1 year

MSSL Presentation on Results Q2 & H1 FY15-16

Safe harbour & Note

Thank you

21

Safe harbour

This presentation contains forward-looking statements based on the currently held beliefs and assumptions of the management of the Company, which are expressed in good faith and, in their opinion, reasonable. Forward-looking statements involve known and unknown risks, uncertainties and other factors, which may cause the actual results, financial condition, performance, or achievements of the Company or industry results, to differ materially from the results, financial condition, performance or achievements expressed or implied by such forward-looking statements. Given these risks, uncertainties and other factors, recipients of this presentation are cautioned not to place undue reliance on these forward-looking statements. The Company disclaims any obligation to update these forward-looking statements to reflect future events or developments.

Note :

**SMRPBV, parent company for SMR & SMP prepares financial statements in Euro currency, hence comparative data is given in Euro terms. These results are consolidated in MSSL by using average year to-date exchange rates. The corresponding figures in Rupee terms have also been stated.