présentation powerpoint - engie.com · &oceania. strategy & transformation plan sectoral...

TRANSCRIPT

July 2017

2

SUMMARY

3 AT A GLANCE

4 ENGIE today

5 Low CO2 power generation

6 Leader in global infrastructure

7 Integrated customer solutions

8 ENGIE around the world

9 STRATEGY & TRANSFORMATION PLAN

10-13 Sectoral context

14 Strategy

15-18 Transformation plan

19 CSR Objectives

25 ENGIE AND YOU*

26-27 ENGIE stock

28 Bonus dividend

29 Actionaria 2017

30 Useful information

31 Agenda

20 2017 FINANCIAL HALF-YEAR RESULTS*21 Ahead of schedule on the transformation plan

22 Key figures

23 Understand 2017 half-year results

24 2017-2018 financial objectives

Navigation through this document is facilitated by an interactive summary that takes you directly to the pages you want and allows

you to return to the summary at any time, using the arrow in the bottom right-hand corner of each page. Clickable links also

provide more details about some subjects.

* Updated to 28 july 2017

AT A GLANCE

ENGIE today

Low Co2 power generation

Leader in global infrastructure

Integrated customer solutions

ENGIE around the world

3

4

ENGIE TODAY

Customer solutions Low CO2 power generation Global infrastructure

ENGIE is focused on its 3 core businesses to lead the global energy transition

5

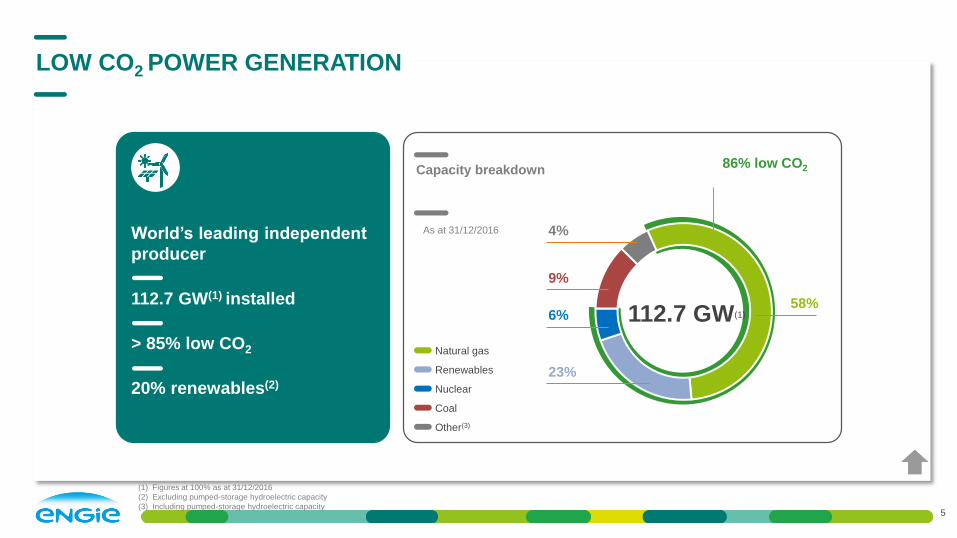

LOW CO2 POWER GENERATION

Natural gas

Renewables

Nuclear

Coal

Other(3)

4%

9%

6%

23%

58%

86% low CO2

112.7 GW(1)

World’s leading independent

producer

112.7 GW(1) installed

> 85% low CO2

20% renewables(2)

(1) Figures at 100% as at 31/12/2016

(2) Excluding pumped-storage hydroelectric capacity

(3) Including pumped-storage hydroelectric capacity

Capacity breakdown

As at 31/12/2016

6

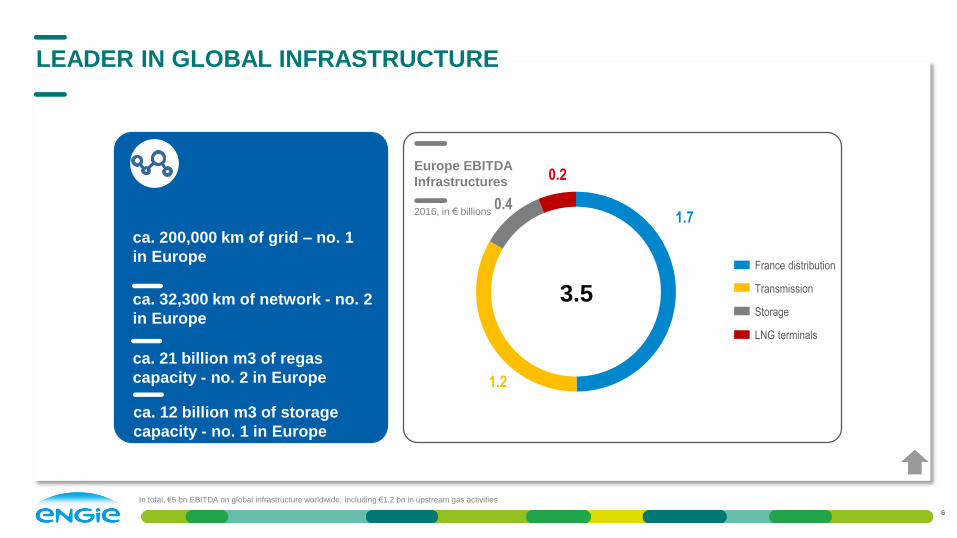

LEADER IN GLOBAL INFRASTRUCTURE

France distribution

Transmission

Storage

LNG terminals

3.5

0.2

1.7

1.2

0.4

Europe EBITDA

Infrastructures

2016, in € billions

ca. 32,300 km of network - no. 2

in Europe

ca. 21 billion m3 of regas

capacity - no. 2 in Europe

ca. 12 billion m3 of storage

capacity - no. 1 in Europe

ca. 200,000 km of grid – no. 1

in Europe

In total, €5 bn EBITDA on global infrastructure worldwide, including €1.2 bn in upstream gas activities

21 mio customers in Europe

Global leader in energy

solutions for cities

>250 DHC networks

worldwide

7

INTEGRATED CUSTOMER SOLUTIONS

EBITDA

by activity

2016, in € billions

0.6

0.4

0.9

1.9

B2B Business to Business

B2T Business to Territories

B2C Business to Customers

Breakdown of revenues by

geographic area

8

ENGIE AROUND THE WORLD

2016, in € bn

North America

Latin America

Europe

Africa

Asia, Middle East &Oceania

STRATEGY &

TRANSFORMATION

PLAN

Sectoral context

Strategy

Transformation plan

9

Pave the way for the future

CSR objectives

10

OPPORTUNITIES ARISING FROM A REVOLUTION

DECARBONISATION DECENTRALISATION DIGITALISATION

This energy revolution is intensifying and becoming global, structured by three major

trends

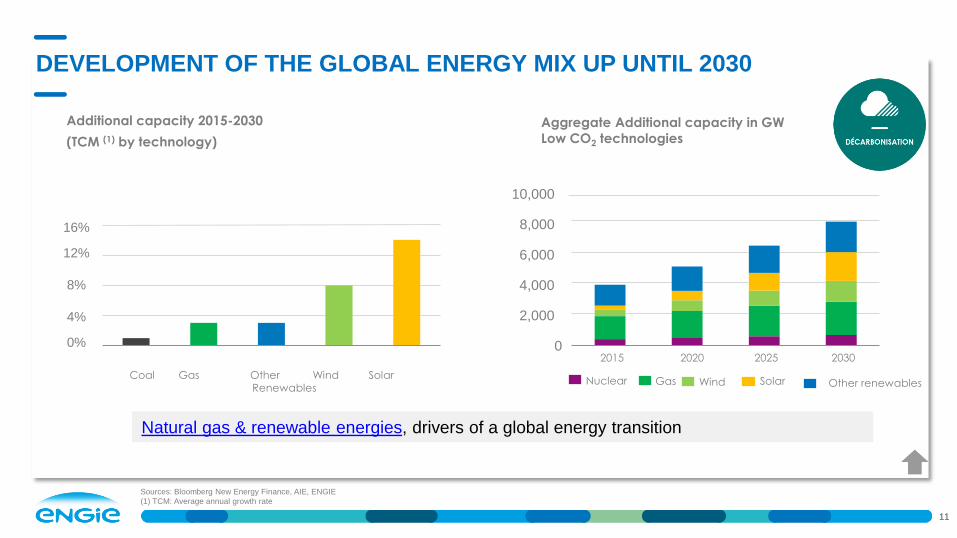

10,000

8,000

6,000

4,000

2,000

0

16%

12%

8%

4%

0%

Aggregate Additional capacity in GW

Low CO2 technologies

Coal Gas Other Wind SolarRenewables

Nuclear Gas Wind Solar Other renewables

2015 2020 2025 2030

Sources: Bloomberg New Energy Finance, AIE, ENGIE

(1) TCM: Average annual growth rate

11

DEVELOPMENT OF THE GLOBAL ENERGY MIX UP UNTIL 2030

Natural gas & renewable energies, drivers of a global energy transition

Additional capacity 2015-2030

(TCM (1) by technology)

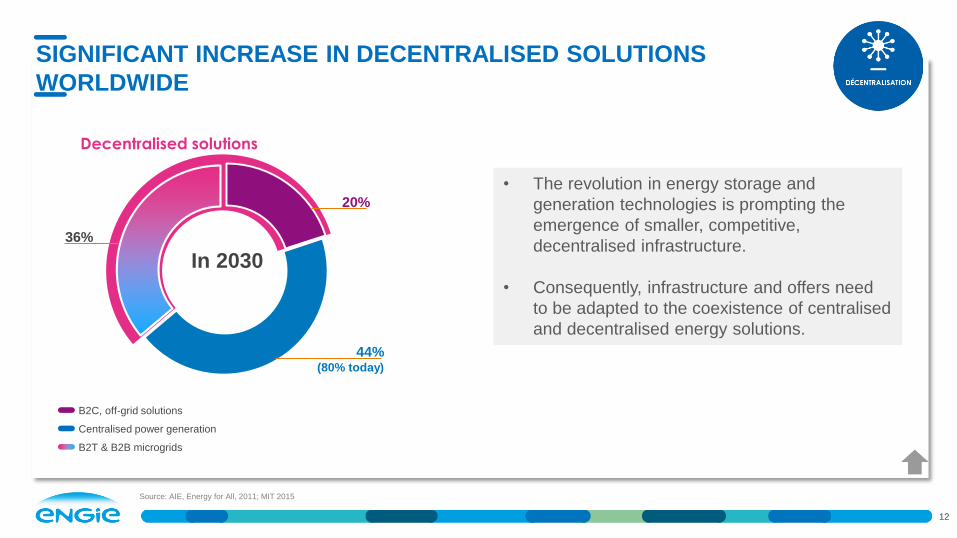

44%(80% today)

36%

20%

Decentralised solutions

In 2030

12

SIGNIFICANT INCREASE IN DECENTRALISED SOLUTIONS

WORLDWIDE

Source: AIE, Energy for All, 2011; MIT 2015

B2C, off-grid solutions

Centralised power generation

B2T & B2B microgrids

• The revolution in energy storage and

generation technologies is prompting the

emergence of smaller, competitive,

decentralised infrastructure.

• Consequently, infrastructure and offers need

to be adapted to the coexistence of centralised

and decentralised energy solutions.

13

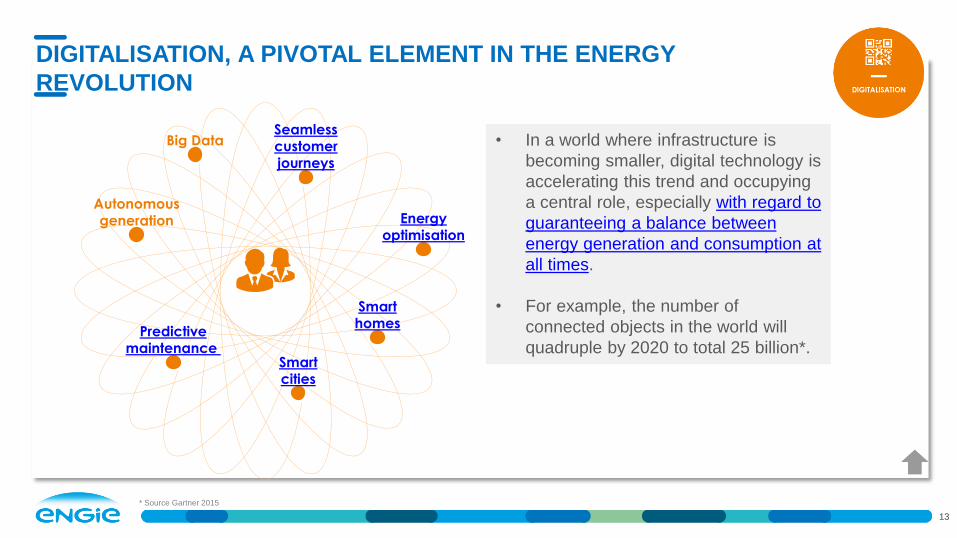

DIGITALISATION, A PIVOTAL ELEMENT IN THE ENERGY

REVOLUTION

• In a world where infrastructure is

becoming smaller, digital technology is

accelerating this trend and occupying

a central role, especially with regard to

guaranteeing a balance between

energy generation and consumption at

all times.

• For example, the number of

connected objects in the world will

quadruple by 2020 to total 25 billion*.

Big Data

Autonomousgeneration

Predictivemaintenance

Energyoptimisation

Smarthomes

Smartcities

Seamlesscustomerjourneys

* Source Gartner 2015

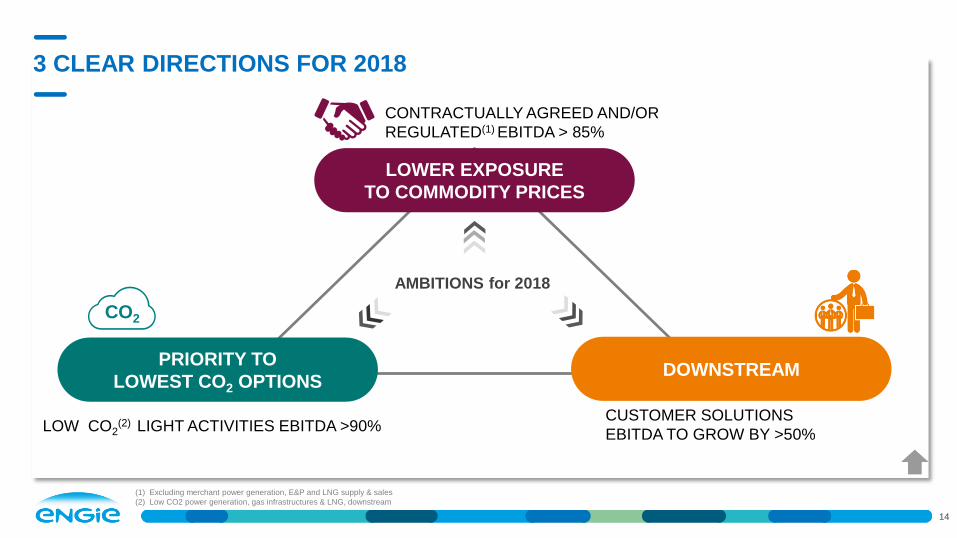

AMBITIONS for 2018

LOWER EXPOSURE

TO COMMODITY PRICES

DOWNSTREAMPRIORITY TO

LOWEST CO2 OPTIONS

LOW CO2(2) LIGHT ACTIVITIES EBITDA >90%

CO2

CONTRACTUALLY AGREED AND/OR

REGULATED(1) EBITDA > 85%

CUSTOMER SOLUTIONS

EBITDA TO GROW BY >50%

(1) Excluding merchant power generation, E&P and LNG supply & sales

(2) Low CO2 power generation, gas infrastructures & LNG, downstream

14

3 CLEAR DIRECTIONS FOR 2018

15

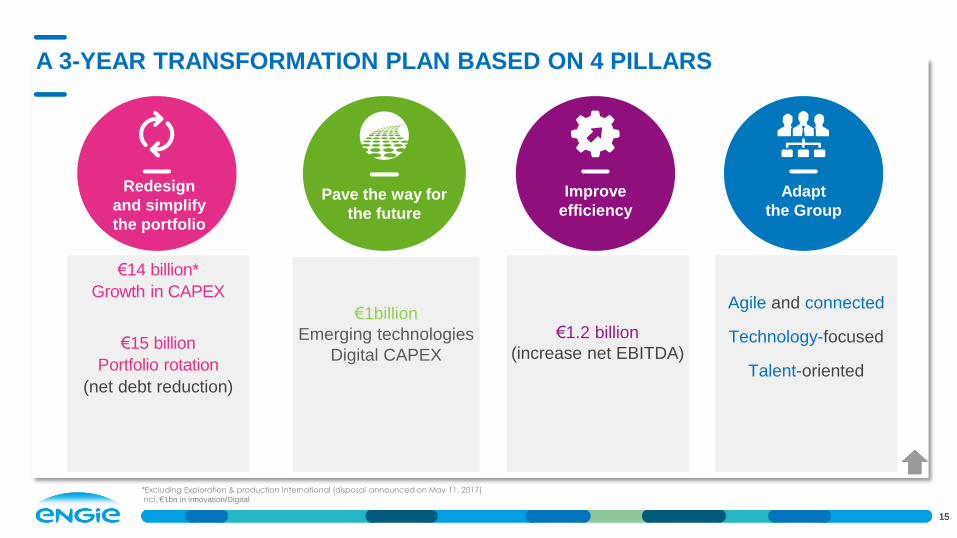

A 3-YEAR TRANSFORMATION PLAN BASED ON 4 PILLARS

*Excluding Exploration & production International (disposal announced on May 11, 2017)

ncl. €1bn in innovation/Digital

15

Agile and connected

Technology-focused

Talent-oriented

Adapt

the Group

Redesign

and simplify

the portfolio

€14 billion*

Growth in CAPEX

€15 billion

Portfolio rotation

(net debt reduction)

Pave the way for

the future

€1billion

Emerging technologies

Digital CAPEX

Improve

efficiency

€1.2 billion

(increase net EBITDA)

16

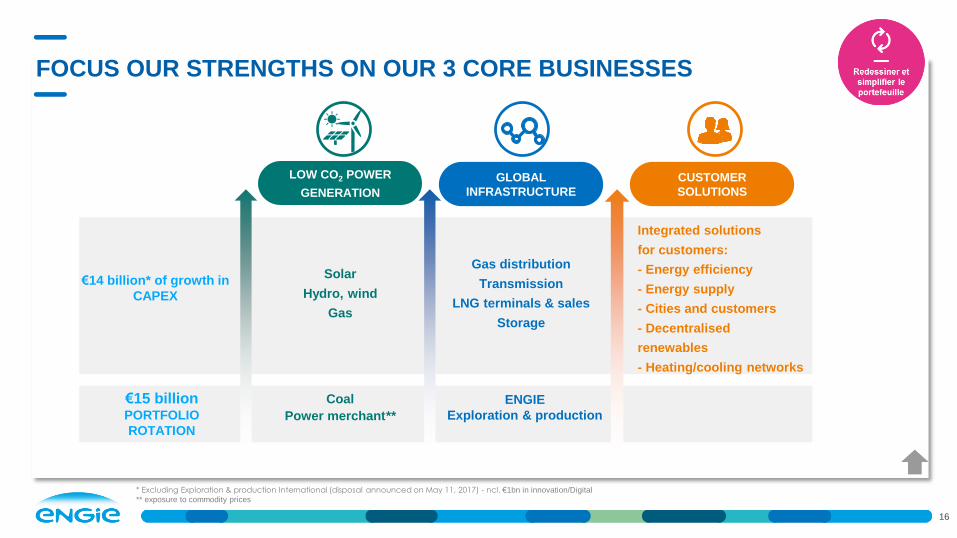

FOCUS OUR STRENGTHS ON OUR 3 CORE BUSINESSES

Coal

Power merchant**

ENGIE

Exploration & production

€14 billion* of growth in

CAPEX

€15 billionPORTFOLIO

ROTATION

Integrated solutions

for customers:

- Energy efficiency

- Energy supply

- Cities and customers

- Decentralised

renewables

- Heating/cooling networks

Gas distribution

Transmission

LNG terminals & sales

Storage

Solar

Hydro, wind

Gas

GLOBAL

INFRASTRUCTURE

LOW CO2 POWER

GENERATION

CUSTOMER

SOLUTIONS

* Excluding Exploration & production International (disposal announced on May 11, 2017) - ncl. €1bn in innovation/Digital

** exposure to commodity prices

17

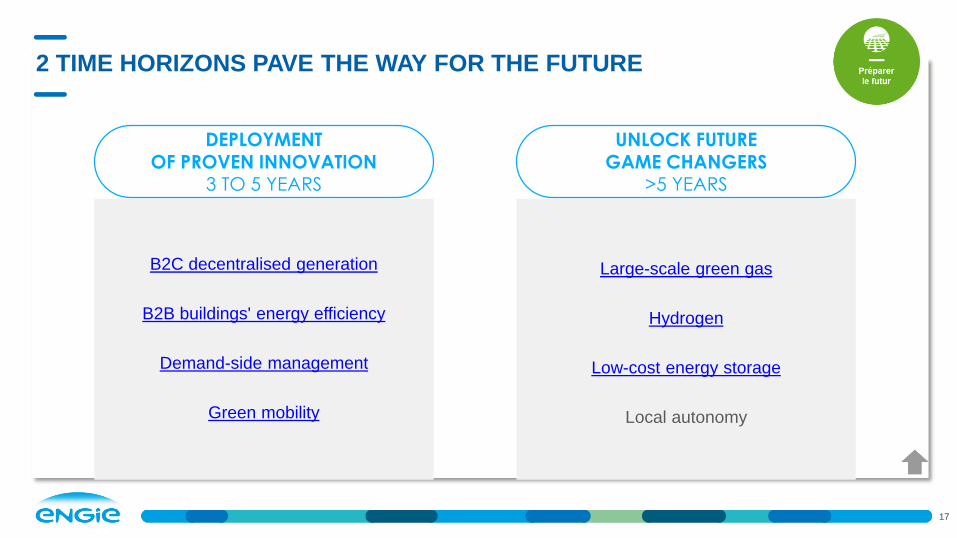

2 TIME HORIZONS PAVE THE WAY FOR THE FUTURE

B2C decentralised generation

B2B buildings' energy efficiency

Demand-side management

Green mobility

DEPLOYMENTOF PROVEN INNOVATION

3 TO 5 YEARS

Large-scale green gas

Hydrogen

Low-cost energy storage

Local autonomy

UNLOCK FUTUREGAME CHANGERS

>5 YEARS

18

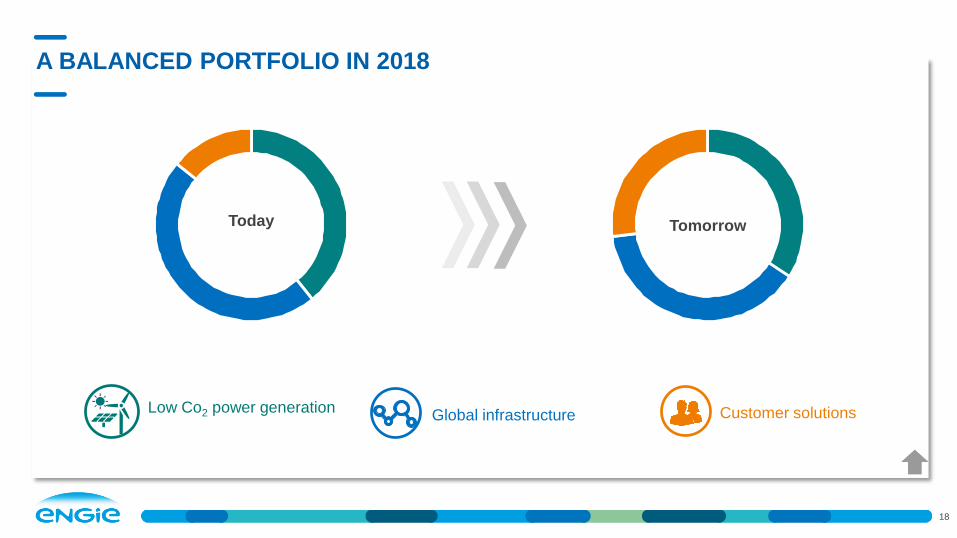

A BALANCED PORTFOLIO IN 2018

Global infrastructure Customer solutions

Today Tomorrow

Low Co2 power generation

19

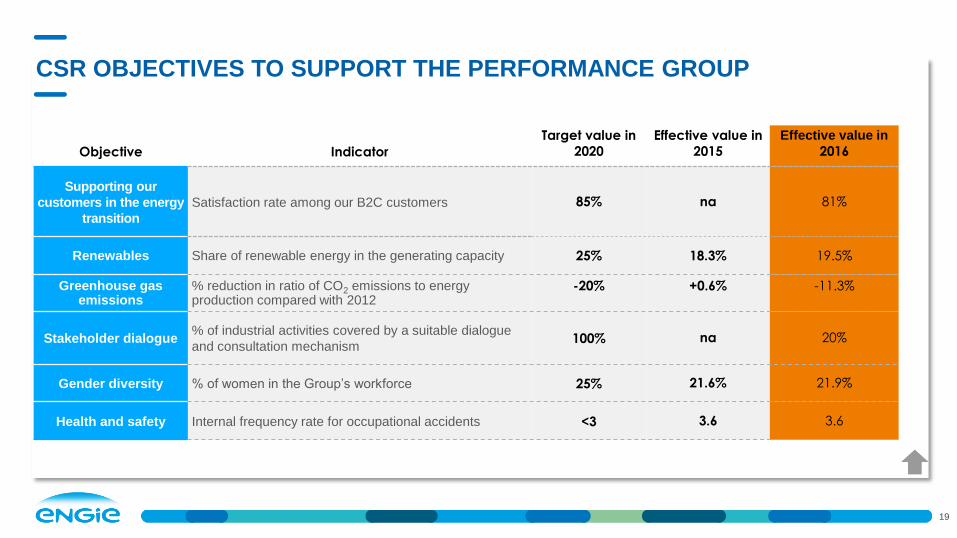

CSR OBJECTIVES TO SUPPORT THE PERFORMANCE GROUP

Objective Indicator

Target value in

2020

Effective value in

2015

Effective value in

2016

Supporting our

customers in the energy

transition

Satisfaction rate among our B2C customers 85% na 81%

Renewables Share of renewable energy in the generating capacity 25% 18.3% 19.5%

Greenhouse gasemissions

% reduction in ratio of CO2 emissions to energy production compared with 2012

-20% +0.6% -11.3%

Stakeholder dialogue% of industrial activities covered by a suitable dialogue

and consultation mechanism100% na 20%

Gender diversity % of women in the Group’s workforce 25% 21.6% 21.9%

Health and safety Internal frequency rate for occupational accidents <3 3.6 3.6

2017 HALF-YEAR

RESULTS

20

Understand the half-year results

Ahead of schedule on the transformation

plan

Key figures

2017-2018 financial objectives

21

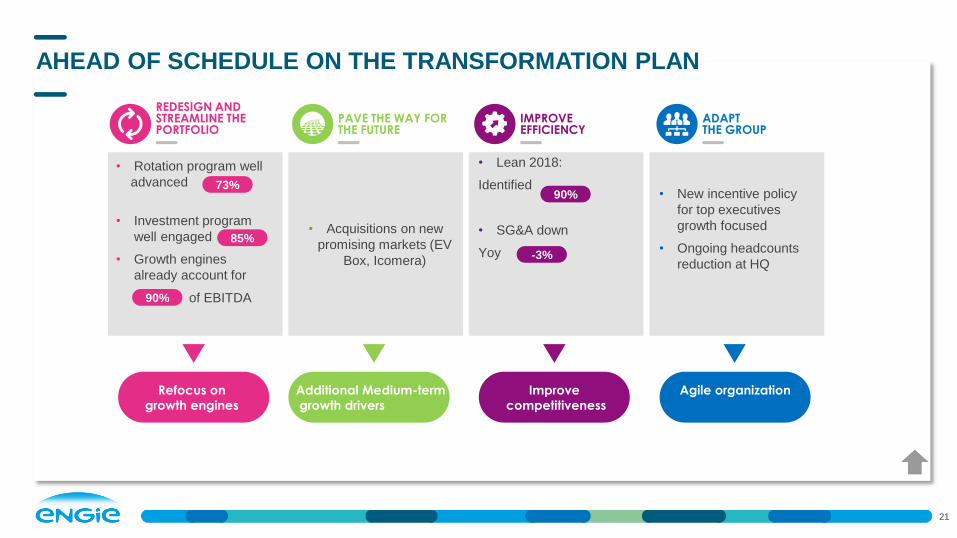

AHEAD OF SCHEDULE ON THE TRANSFORMATION PLAN

• Acquisitions on new

promising markets (EV

Box, Icomera)

• Lean 2018:

Identified

• SG&A down

Yoy

• New incentive policy

for top executives

growth focused

• Ongoing headcounts

reduction at HQ

PAVE THE WAY FOR THE FUTURE

IMPROVE EFFICIENCY

REDESIGN AND STREAMLINE THE PORTFOLIO

ADAPT THE GROUP

Additional Medium-term

growth drivers

Improve

competitiveness

Refocus on

growth engines

Agile organization

• Rotation program well

advanced

• Investment program

well engaged

• Growth engines

already account for

of EBITDA

73%

85%

90%

90%

-3%

22

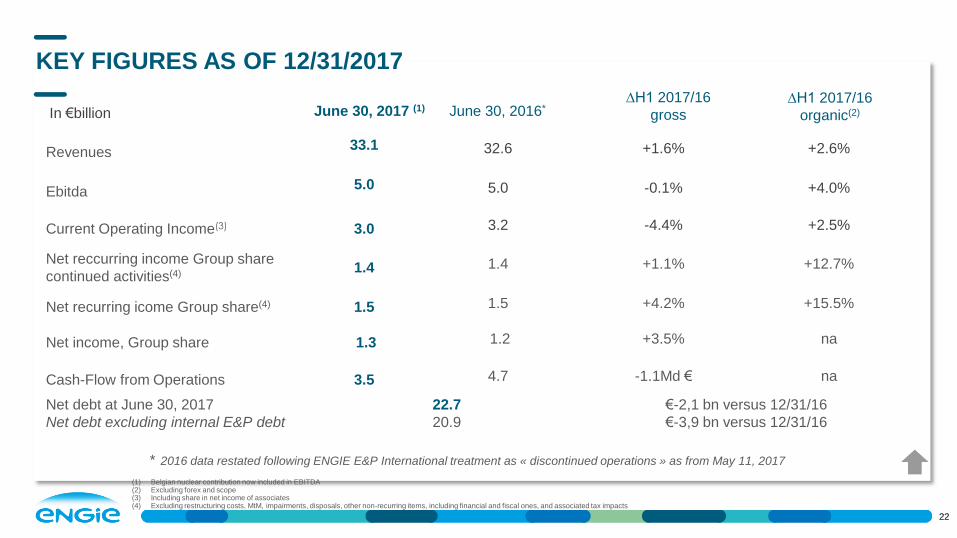

KEY FIGURES AS OF 12/31/2017

In €billion

Revenues33.1 32.6 +1.6% +2.6%

Ebitda5.0 5.0 -0.1% +4.0%

Current Operating Income(3) 3.0 3.2 -4.4% +2.5%

Net reccurring income Group share

continued activities(4) 1.4 1.4 +1.1% +12.7%

Net recurring icome Group share(4) 1.5 1.5 +4.2% +15.5%

Net income, Group share 1.3 1.2 +3.5% na

Cash-Flow from Operations 3.5 4.7 -1.1Md € na

Net debt at June 30, 2017

Net debt excluding internal E&P debt

22.7

20.9

€-2,1 bn versus 12/31/16

€-3,9 bn versus 12/31/16

* 2016 data restated following ENGIE E&P International treatment as « discontinued operations » as from May 11, 2017

22

June 30, 2016*∆H1 2017/16

organic(2)June 30, 2017 (1)∆H1 2017/16

gross

(1) Belgian nuclear contribution now included in EBITDA (2) Excluding forex and scope (3) Including share in net income of associates (4) Excluding restructuring costs, MtM, impairments, disposals, other non-recurring items, including financial and fiscal ones, and associated tax impacts

23

COMMENTS ON THE HALF-YEAR ACCOUNTS

Read the press release

Solid first half 2017 results, in line with our 2017 annual targets

Revenues increased by +1.6% on a reported basis to EUR 33.1 billion and by +2.6% on an organic basis compared with first half 2016. Adjusted for the

unfavorable evolution of temperatures in France, which have been less cold this semester compared to the same period last year, the organic growth

amounts to +3.0%.

EBITDA amounted to EUR 5.0 billion, globally stable (-0.1%) on a reported basis but up +4.0% on an organic basis. On this organic basis, EBITDA is driven

by the positive impacts of (i) the Lean 2018 performance program, (ii) the sustained performance of the Group's growth engines, (iii) the commissioning of

new assets in Latin America and (iv) a good performance of thermal power generation activities in Europe and Australia.

Net recurring income Group share amounted to EUR 1.5 billion, stable compared with first half 2016. It includes EUR 103 million of net recurring income

Group share from ENGIE E&P International activities classified in "Discontinued operations".

Net recurring income Group share relating to continued operations amounted to EUR 1.4 billion for the six months ended June 30, 2017, up +1.1%

compared with first half 2016, driven by an improvement in recurring net financial result.

Net income Group share amounted to EUR 1.3 billion for first half 2017.

Net income Group share relating to continued operations amounted to EUR 1.3 billion for the six months ended June 30, 2017, stable compared with first

half 2016. It includes the negative impacts of fair value adjustments to hedges of commodity purchases and sales, and charges to restructuring provisions,

which were partially offset by the positive impacts of (i) a reduction in the cost of debt, (ii) lower net impairment losses than the previous year, and (iii) gains

on disposals.

Net debt stood at EUR 22.7 billion at June 30, 2017, down EUR 2.1 billion since December 31, 2016, mainly due to cash flow from operations and the

impacts of the portfolio rotation program.

24

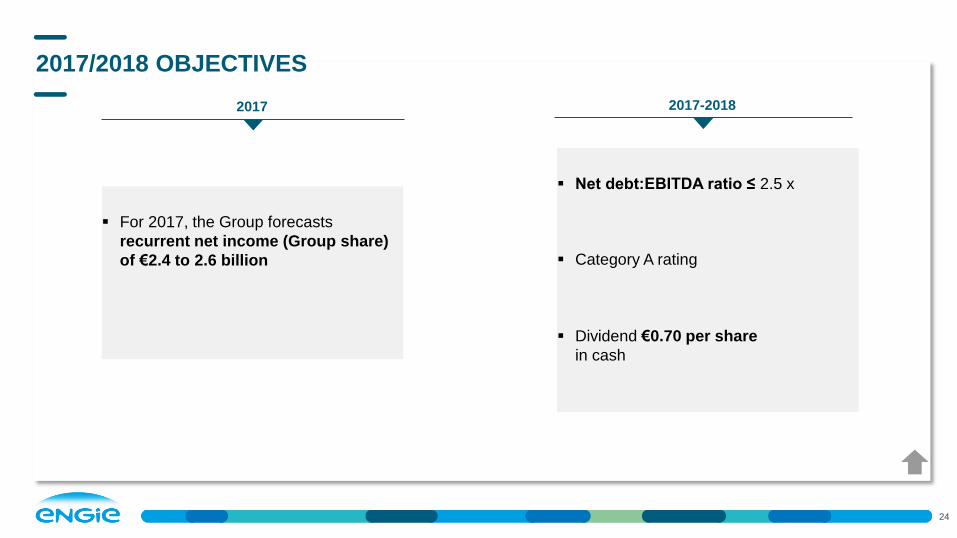

2017/2018 OBJECTIVES

Net debt:EBITDA ratio ≤ 2.5 x

Category A rating

Dividend €0.70 per share

in cash

2017-20182017

For 2017, the Group forecasts

recurrent net income (Group share)

of €2.4 to 2.6 billion

ENGIE

AND YOU

ENGIE stock

Bonus dividend

Actionaria

Useful information

Contents

25

IndicesMarketsStock market information

26

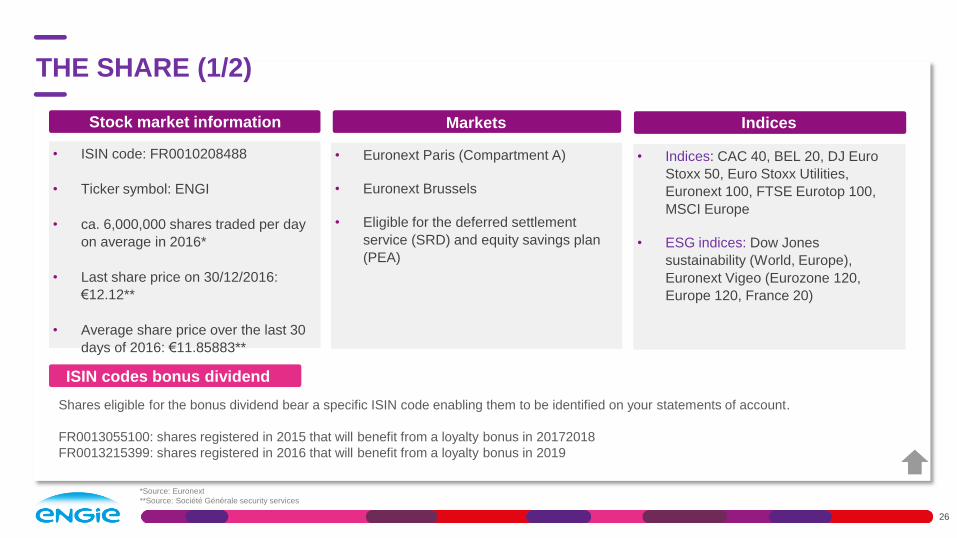

THE SHARE (1/2)

Shares eligible for the bonus dividend bear a specific ISIN code enabling them to be identified on your statements of account.

FR0013055100: shares registered in 2015 that will benefit from a loyalty bonus in 20172018

FR0013215399: shares registered in 2016 that will benefit from a loyalty bonus in 2019

• ISIN code: FR0010208488

• Ticker symbol: ENGI

• ca. 6,000,000 shares traded per day

on average in 2016*

• Last share price on 30/12/2016:

€12.12**

• Average share price over the last 30

days of 2016: €11.85883**

• Euronext Paris (Compartment A)

• Euronext Brussels

• Eligible for the deferred settlement

service (SRD) and equity savings plan

(PEA)

• Indices: CAC 40, BEL 20, DJ Euro

Stoxx 50, Euro Stoxx Utilities,

Euronext 100, FTSE Eurotop 100,

MSCI Europe

• ESG indices: Dow Jones

sustainability (World, Europe),

Euronext Vigeo (Eurozone 120,

Europe 120, France 20)

ISIN codes bonus dividend

*Source: Euronext

**Source: Société Générale security services

27

THE SHARE (2/2)

Gross

change in %

Gross

change in %

Source: Factset, Bloomberg

Base ENGIE

Share price performance since 01/01/2017*

*Performance of reinvested dividends : ENGIE +16% - CAC 40 :+7.9 % - BEL20 : +10.5% - Eurostoxx utilities: +17.6%

ENGIE BEL 20 EUROStoxx utilities CAC 40

10,5

11,0

11,5

12,0

12,5

13,0

13,5

14,0

14,5

01/01/2017 01/03/2017 01/05/2017 01/07/2017

+12,0% +12,4%

+7,7%

+5,3%

10,5

11,0

11,5

12,0

12,5

13,0

13,5

14,0

14,5

01/03/2017 01/04/2017 01/05/2017 01/06/2017 01/07/2017

+16,5%

+11,6%

+6,1%

+3,2%

Share price performance since publication of year results

28

A BONUS DIVIDEND TO REWARD LOYALTY

Register your shares prior to December 31, 2017 to benefit in

2020 from the bonus dividend related to 2019.

29

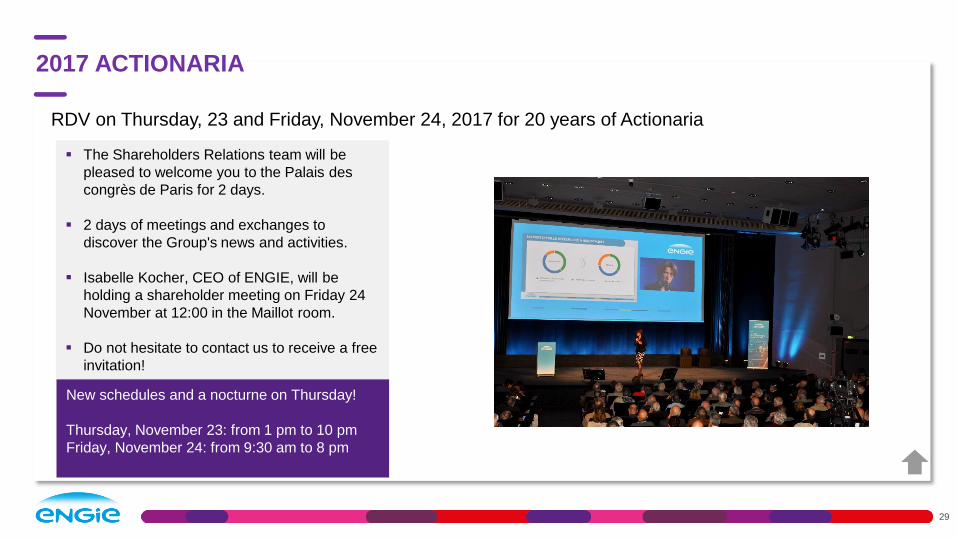

2017 ACTIONARIA

The Shareholders Relations team will be

pleased to welcome you to the Palais des

congrès de Paris for 2 days.

2 days of meetings and exchanges to

discover the Group's news and activities.

Isabelle Kocher, CEO of ENGIE, will be

holding a shareholder meeting on Friday 24

November at 12:00 in the Maillot room.

Do not hesitate to contact us to receive a free

invitation!

RDV on Thursday, 23 and Friday, November 24, 2017 for 20 years of Actionaria

New schedules and a nocturne on Thursday!

Thursday, November 23: from 1 pm to 10 pm

Friday, November 24: from 9:30 am to 8 pm

30

PRACTICAL INFORMATION

The ENGIE share price

Holding registered securities

The dividend

The loyalty bonus

General Meeting

The tax framework for your shares in

2017

Press releases

Publications by ENGIE

HOLDING ENGIE SECURITIESBEING AN ENGIE SHAREHOLDER

USEFUL LINKS

engie.com/shareholders

engie.com/club

Mes questions d’argent* (in French)

Euronext, Paris Stock Exchange

L’Ecole de la Bourse (in French)

placedesactionnaires.com (in French)

Salon Actionaria (in French)

Lexicon (in French)

CONTACT US

facebook.com/actionnairesengie

[email protected] (France)

(from France)

[email protected] (Belgium)

(from Belgium)

0 800 300 030

0 800 25 125

31

DATES TO NOTE IN 2017

Thursday, November 9

Results as of 30 September 2017

Thursday and Friday November 23&24

Salon Actionaria

Monday, October 2, 2017

Shareholders meeting in Nice

Friday, October 13

Payement of the interim dividend:

€ 0.35 per share

Saturday, September 30

Event VFB in Gand (Belgium)