presentation: the capital markets introduction this lecture presents the basic ingredients of the...

TRANSCRIPT

1

THE CAPITAL MARKETS

February 2004

2

INTRODUCTION This lecture presents the basic ingredients of the capital m arkets –

their function, framework and implementation. It w ill define comm onm arket terms and survey the fram ew ork and structure of key m arket

sectors and components. It w ill discuss the significance and developmentof these sectors and their inter-relationships. Exam ples and exercises w illdemonstrate im portant characteristics of these sectors. The final goal is toutilize all the ingredients as tools to construct and to analyze the structure,planning and pricing of a capital m arket transaction.

A) BASICS

1) Jargon – let’s define some terms2)“Maturity” and “Security”

B) CAPITAL M ARKETS - (No M uni / No Equity)

1) The Firm- Bankers – Corporate Finance- Trading and Sales- Researc

2) Capital M arket The 415 Shelf

C) THE CURVES - A Fram ew ork

1) The Daily Page- The Curves- The Spreads- The Num bers

2) The Treasury M arket – Governm ents

- The 32nd

- The Curve1) The Money Market

- Libor- Swaps- Money Market Spreads

D) THE GOVERNMENT MARKET - Treasuries

1) The Curve - “on the run”2) T-Bills and Liquidity3) Comparables (“comps”) - “off the run”4) Benchmarks and Pricing5) “Did We Roll Yet” - the “WI” and Auctions

E) REPURCHASE AGREEMENTS – “REPO”

1) Ingredients- Collateral- Liquidity- Security and Maturity- “Mark to Market” Legal Test Financial Test

2) “Specials”3) Reverse Repo

F) INTEREST RATE SWAPS

1) Why Swaps ?- Efficiency / Risk Leverage vs “Notional”

2) Swap Spreads3) Swap Rates4) Swap Indices5) The Asset Swap

3

I)

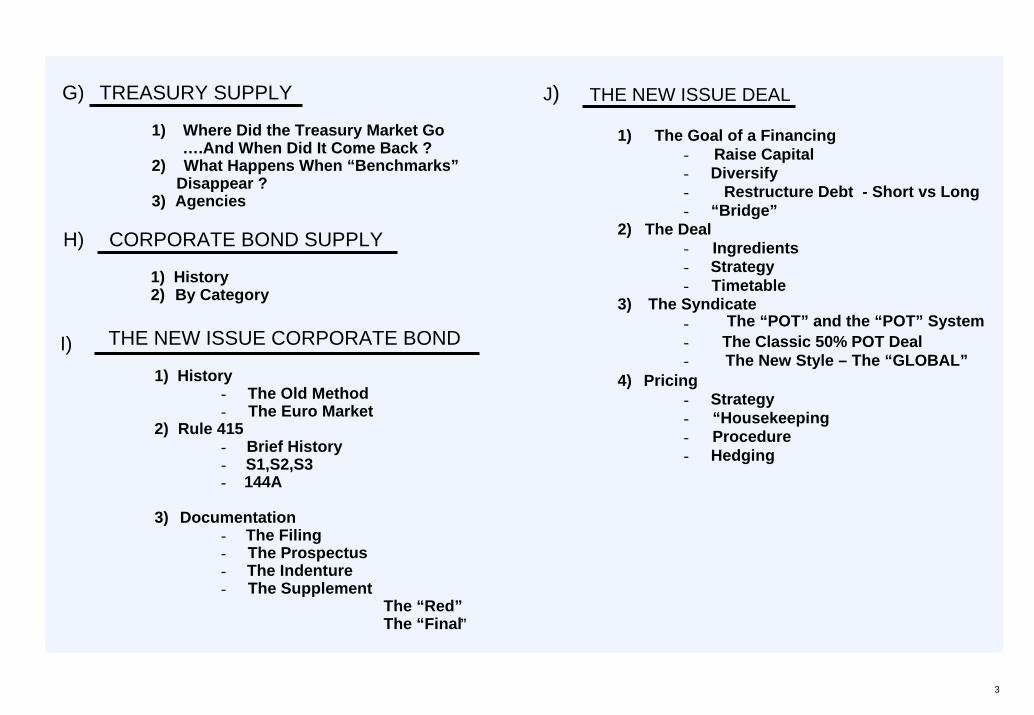

J) THE NEW ISSUE DEAL

1) The Goal of a Financing- Raise Capital- Diversify- Restructure Debt - Short vs Long- “Bridge”

2) The Deal- Ingredients- Strategy- Timetable

3) The Syndicate- The “POT” and the “POT” System- The Classic 50% POT Deal- The New Style – The “GLOBAL”

4) Pricing- Strategy- “Housekeeping- Procedure- Hedging

G) TREASURY SUPPLY

1) Where Did the Treasury Market Go….And When Did It Come Back ?

2) What Happens When “Benchmarks”Disappear ?

3) Agencies

H) CORPORATE BOND SUPPLY

1) History2) By Category

THE NEW ISSUE CORPORATE BOND

1) History- The Old Method- The Euro Market

2) Rule 415- Brief History- S1,S2,S3- 144A

3) Documentation- The Filing- The Prospectus- The Indenture- The Supplement

The “Red”The “Final”

4

TERMSand

CHRONOLOGY

5

COUNTING BONDS – $1000 = 1 bond / 1000 bonds $1,000,000.0

BASIS POINT – .0001 = .01% = 1 basis point / “running” vs “up front”

YIELD VALUE of 32nd = $312.50 per million – ALWAYS !!LIBOR – the “London inter-bank offered rate” / “libid” / “li-mean” / Sibor

EURIBOR – the “Euro” interbank offered rate / EONIA

SPREAD – “narrowing” “widening” “tightening” “credit”

Issue credit spread + benchmark yield = yield @ $ price

YIELD – “to maturity” “current” “DM” for FRN’s

DISCOUNT / COUPON – different expressions of YIELDDAY COUNT – 30/360 / actual/360 / actual/actual

COUPON PAYMENT TYPE – annual / semi-annual / quarterly / monthly

FIXED vs FLOATING – “variable” FRN vs FIXED COUPON

FED FUNDS – vs “clearinghouse” check vs cash “next day vs same day”

SETTLEMENT – time and type / “DVP” - delivery vs payment”

TYPE - physical / book-entry (BE) – global / DTC / Euro Clear

TIME - “cash” / “regular” / “skip” / “corporate” / (T + 1, 2 or 3 )

BOND / NOTE / BILL – Maturity reference CD, CP, BA

REPURCHASE AGREEMENT – “Repo” a “buy / sell” security agreement / a loan

Terms

6

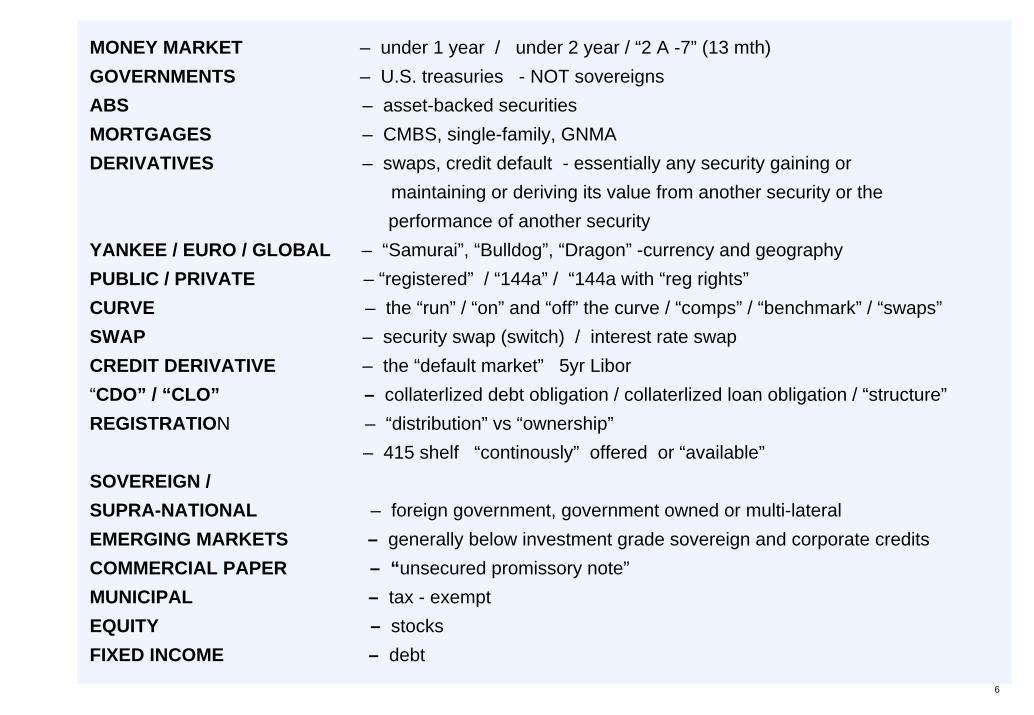

MONEY MARKET – under 1 year / under 2 year / “2 A -7” (13 mth)GOVERNMENTS – U.S. treasuries - NOT sovereignsABS – asset-backed securitiesMORTGAGES – CMBS, single-family, GNMADERIVATIVES – swaps, credit default - essentially any security gaining or

maintaining or deriving its value from another security or the performance of another security

YANKEE / EURO / GLOBAL – “Samurai”, “Bulldog”, “Dragon” -currency and geographyPUBLIC / PRIVATE – “registered” / “144a” / “144a with “reg rights”CURVE – the “run” / “on” and “off” the curve / “comps” / “benchmark” / “swaps”SWAP – security swap (switch) / interest rate swapCREDIT DERIVATIVE – the “default market” 5yr Libor“CDO” / “CLO” – collaterlized debt obligation / collaterlized loan obligation / “structure”REGISTRATION – “distribution” vs “ownership”

– 415 shelf “continously” offered or “available”SOVEREIGN /SUPRA-NATIONAL – foreign government, government owned or multi-lateralEMERGING MARKETS – generally below investment grade sovereign and corporate creditsCOMMERCIAL PAPER – “unsecured promissory note”MUNICIPAL – tax - exemptEQUITY – stocksFIXED INCOME – debt

7

MATURITY - Chronology

1. FEDERAL FUNDS2. REPURCHASE AGREEMENTS - “overnights” “term”3. TIME DEPOSITS (Domestic and Euro) “TD’s”4. COMMERCIAL PAPER “CP”5. BANKER ACCEPTANCES “BA”6. CERTIFICATES of DEPOSIT “CD”7. EURO CD8. TREASURY BILLS9. 1 YR NOTES (MTN’s / FRN’s / FRA’s)

10. ASSET-BACKED SECURITIES11. SHORT NORES (2YR – 5YR) Gvt, Corps, Agencies12. INTERMEDIATES (5YR –10YR) Gvt, Agency, Corps, Mtgs13. LONG BONDS (12YR or longer…

SECURITY - Safety

1. FED FUNDS 2. T-BILLS3. GOVERNMENTS4. REPURCHASE AGREEMENTS “GC” ONLY5. BA’s6. CD’s (“Euro Question”)7. AGENCIES (not all)8. ASSET-BACKED SECURITIES9. MORTGAGES

10. CORPORATES11. COMMERCIAL PAPER

8

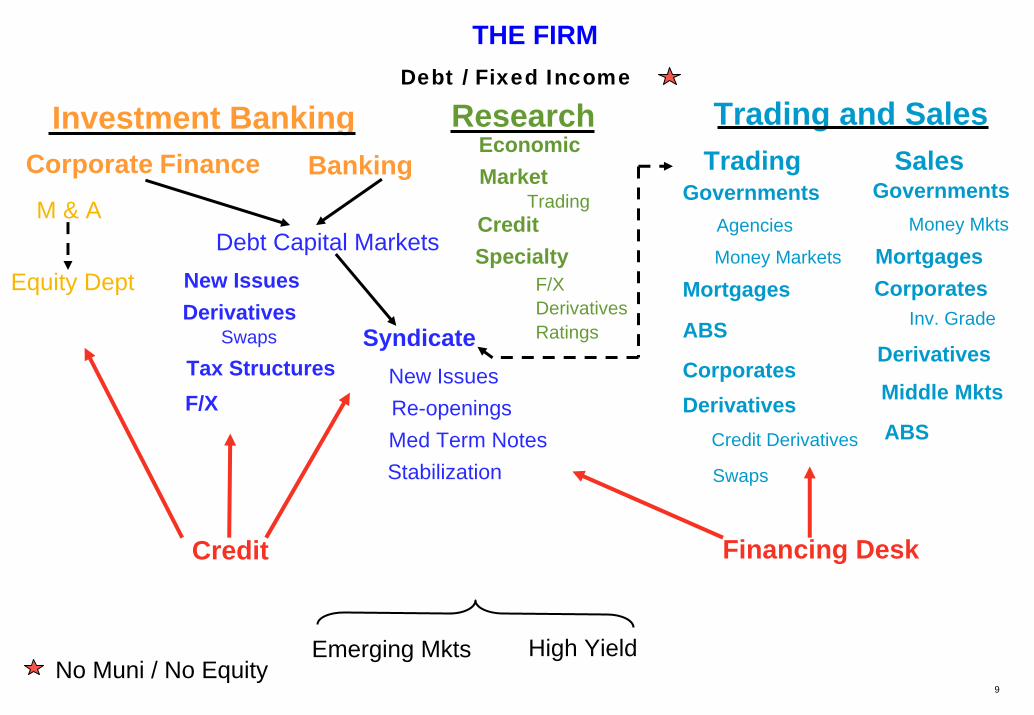

THE FIRM

9

THE FIRMDebt / Fixed Income

Investment Banking Trading and SalesResearch

Trading

SalesGovernments

M & A

Credit

Debt Capital Markets

Financing Desk

Swaps

SwapsDerivatives

Tax StructuresF/X

Syndicate

New Issues

TradingGovernments

Money Mkts

MortgagesCorporates

Inv. Grade

Corporate FinanceEconomicMarket

CreditSpecialty

F/XDerivatives

New Issues

Ratings

Equity Dept

Banking

Agencies

Money Markets

Mortgages

ABS

CorporatesDerivatives

Credit Derivatives

Emerging Mkts High Yield

Re-openingsMed Term NotesStabilization

Derivatives

ABS

Middle Mkts

No Muni / No Equity

10

THE CURVES

11

1 1.1418 1.43 2 1.703 2.234 2.655 3.01 (05)7 3.52

10 4.0330 4.89

1.38 1.70

2.00 – 04 30 – 342.58 – 62 34 – 383.03 – 07 41 – 453.39 – 43 38 – 423.91 – 95 50 – 534.41 – 44 38 – 425.18 – 22 30 – 33.

1 1.072 1.093 1.104 1.135 1.15 6 1.189 1.28

12 1,42 3 X 1.096 X 1.13

1.10

1.13

1 88 – 893 92 – 93 6 99 – 1.01 .

6. 3.298. 3.74 9. 3.88

2 – 5 + 1312 – 10 + 2332 – 30 + 3195 – 10 + 102

10 – 30 + 86

88 –1.00 – 981.02 – 99 1.03 – 00 1.03 – 00 1.03 – 00 .

98 –

1.36 –1.42 –1.42 –.

UST SWAP LIBOR

YLD CRV SPRDS

“BILLS”

FF 96 – 1.00 O/N 1.00 – 95

7 1.00 – 97 15 99 – 43 30 99 – 94 60 90

.

1.10 – 05

1.16 – 111.17 – 06 1.17 – 06 .

CPA-1 A-2

MMKT SWAPS

REPO

“THE DAILY”

12

TREASURER’S PAGE

13

Treasurer’s Page• Fed Funds• T- Bills• Repo Rates• Treasuries• Currencies• Swaps• Stock Indicies• LIBOR• Futures• MBS...

14

“DIRECT ISSUE”COMMERCIAL PAPER

A-1 / P-1

A-2 / P-2andA-3’s

15

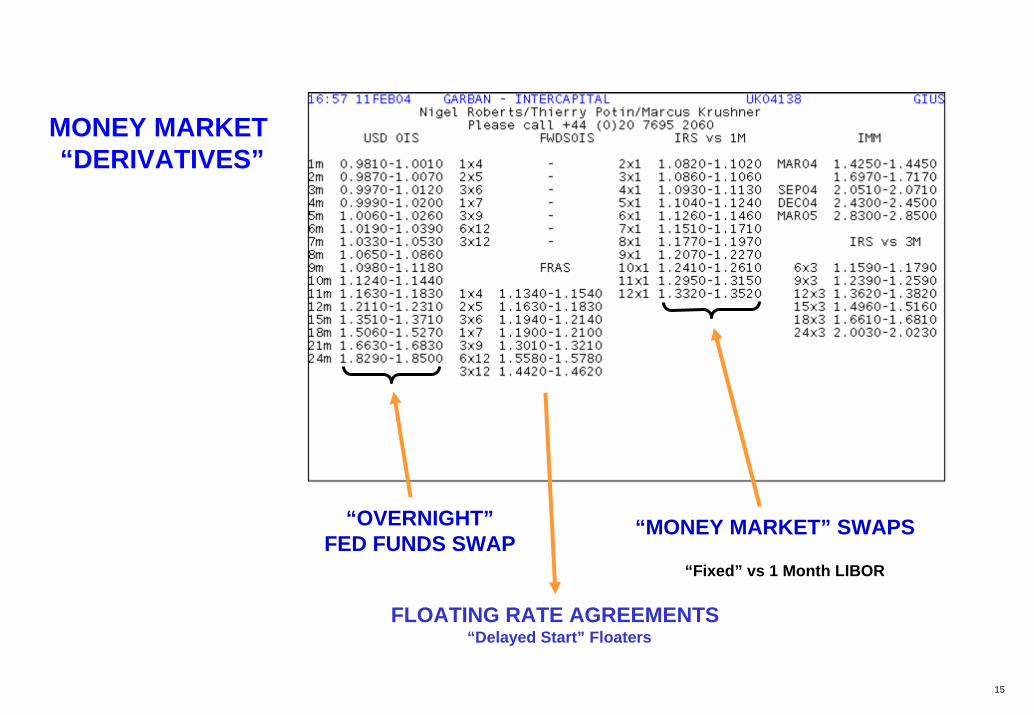

“MONEY MARKET” SWAPS“OVERNIGHT”FED FUNDS SWAP

MONEY MARKET “DERIVATIVES”

“Fixed” vs 1 Month LIBOR

FLOATING RATE AGREEMENTS“Delayed Start” Floaters

16

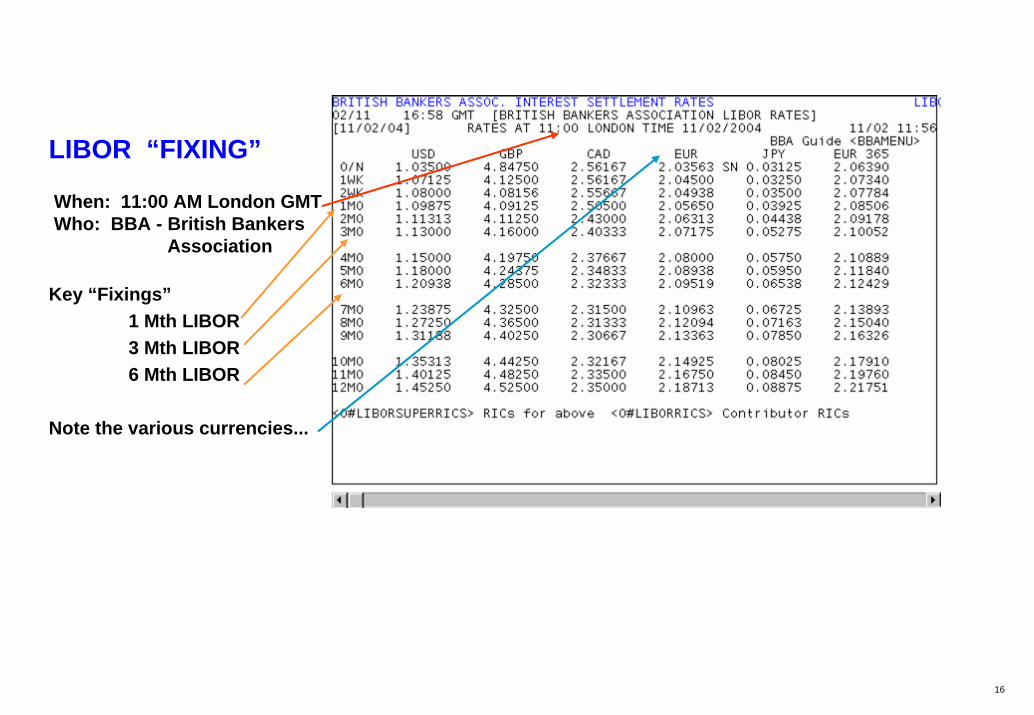

LIBOR “FIXING”

When: 11:00 AM London GMTWho: BBA - British Bankers

Association

Key “Fixings”1 Mth LIBOR3 Mth LIBOR6 Mth LIBOR

Note the various currencies...

17

LIBOR

LIBID LIBOR

18

1YEAR “LIBOR” orswap yield

18 Mth “LIBOR” orswap yield

30 /360 = “Bond Yield” ACT / 360 = Money Market semi–annual interest” paid on coupon dates Yield

“interest at maturity”

Combination“STRIPS”

19

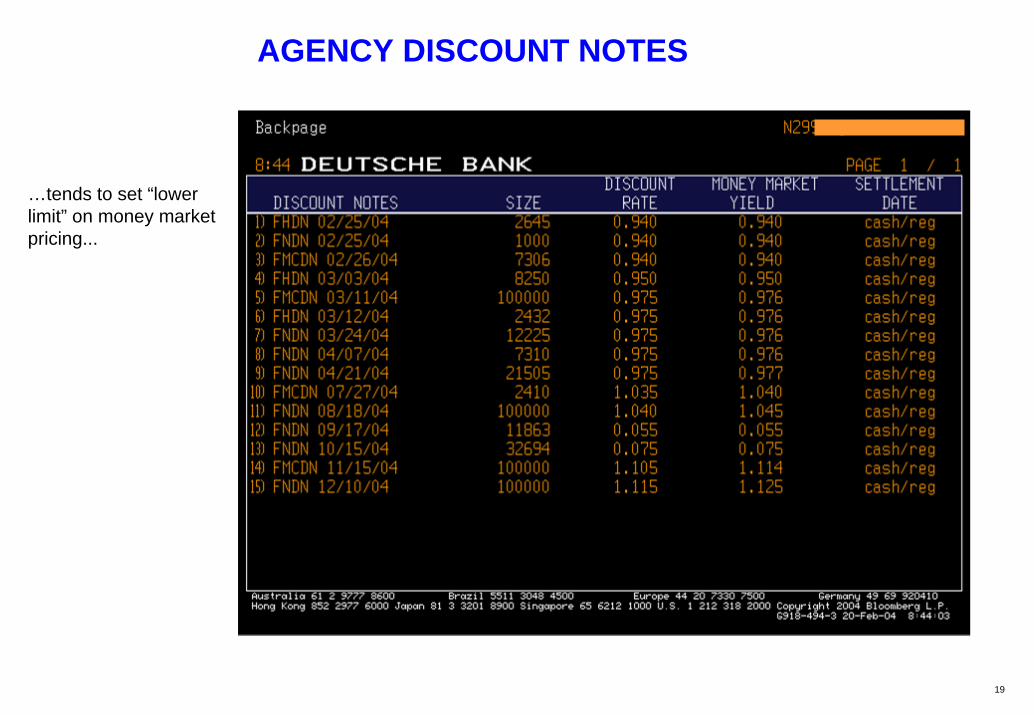

AGENCY DISCOUNT NOTES

…tends to set “lowerlimit” on money marketpricing...

20

T – BILLS1 MONTH3 MONTH6 MONTH

• Quoted on “discount”basis

• “bond equivalent” or“coupon yield” also quoted

NOTE: “WI”

21

T-BILLS(no coupons)

22

Low Rates…“liquidity preference”outweighed by yieldpreference..

23

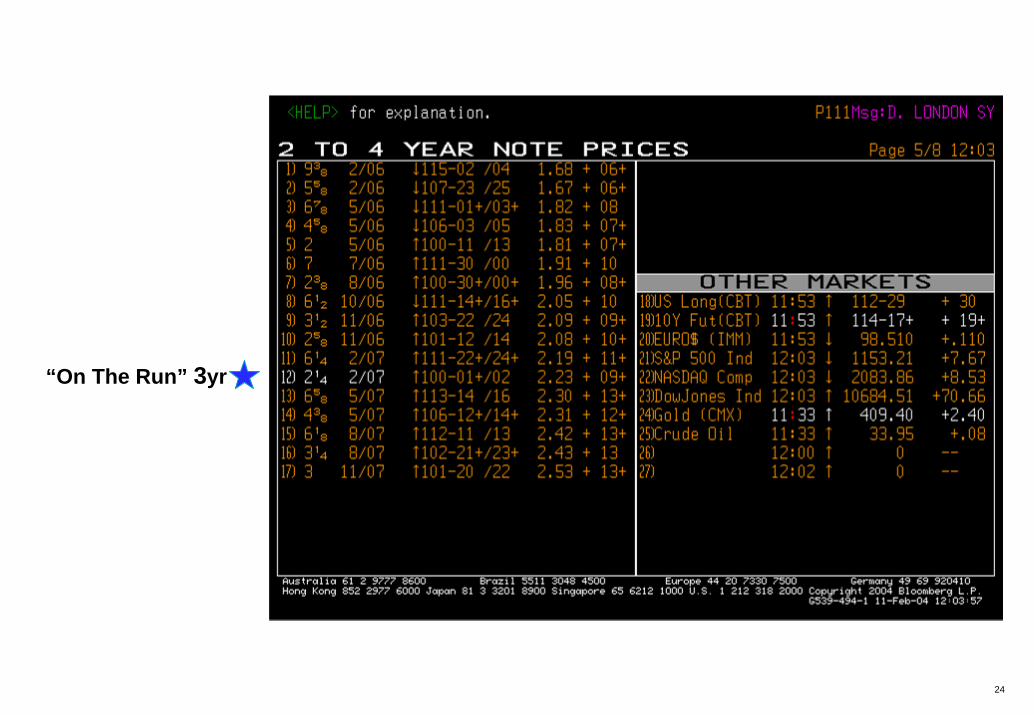

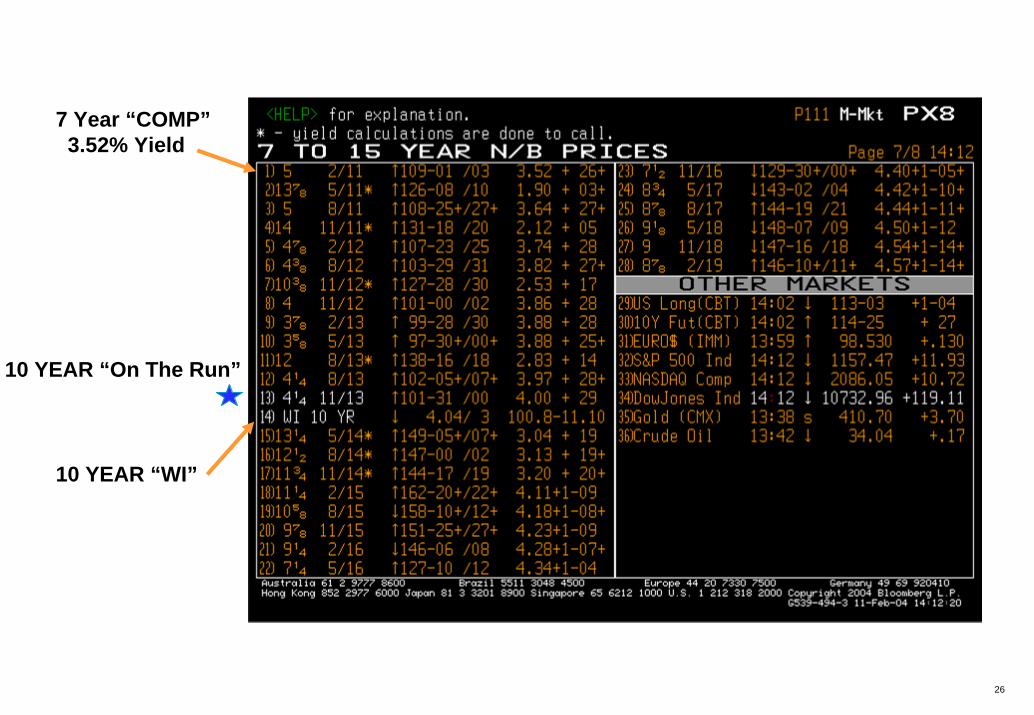

“On The Run” 2yr

24

“On The Run” 3yr

25

“On The Run” 5yr

4 YEAR “COMP”2.65 YIELD

“WI” 5 YEARTrades in “yield”

26

10 YEAR “On The Run”

10 YEAR “WI”

7 Year “COMP”3.52% Yield

27

THE TREASURY MARKET• “ON THE RUN”• “COMPS”• MY FRIEND THE “32nd” = $312.50 ALWAYS!!

28

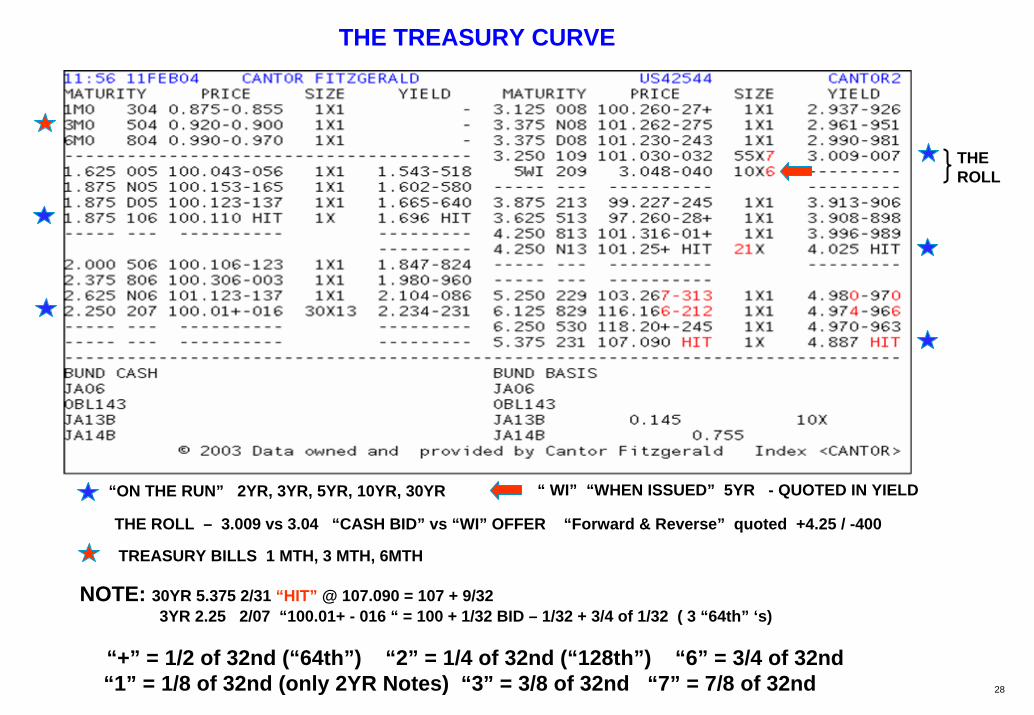

THE ROLL

“ON THE RUN” 2YR, 3YR, 5YR, 10YR, 30YR “ WI” “WHEN ISSUED” 5YR - QUOTED IN YIELD

THE ROLL – 3.009 vs 3.04 “CASH BID” vs “WI” OFFER “Forward & Reverse” quoted +4.25 / -400

NOTE: 30YR 5.375 2/31 “HIT” @ 107.090 = 107 + 9/323YR 2.25 2/07 “100.01+ - 016 “ = 100 + 1/32 BID – 1/32 + 3/4 of 1/32 ( 3 “64th” ‘s)

“+” = 1/2 of 32nd (“64th”) “2” = 1/4 of 32nd (“128th”) “6” = 3/4 of 32nd“1” = 1/8 of 32nd (only 2YR Notes) “3” = 3/8 of 32nd “7” = 7/8 of 32nd

TREASURY BILLS 1 MTH, 3 MTH, 6MTH

THE TREASURY CURVE

29

THE TREASURY CURVE

“OLD 3 YEAR” 101.123 “BID” = 101-12 and 3/8’s= 101 + 12 32nd’s + 3/8 of a 32nd= $1,010,000 + $3,750 + $117.19

1 MILLION BONDS = $1,013.867.19 + “accrued interest”

30

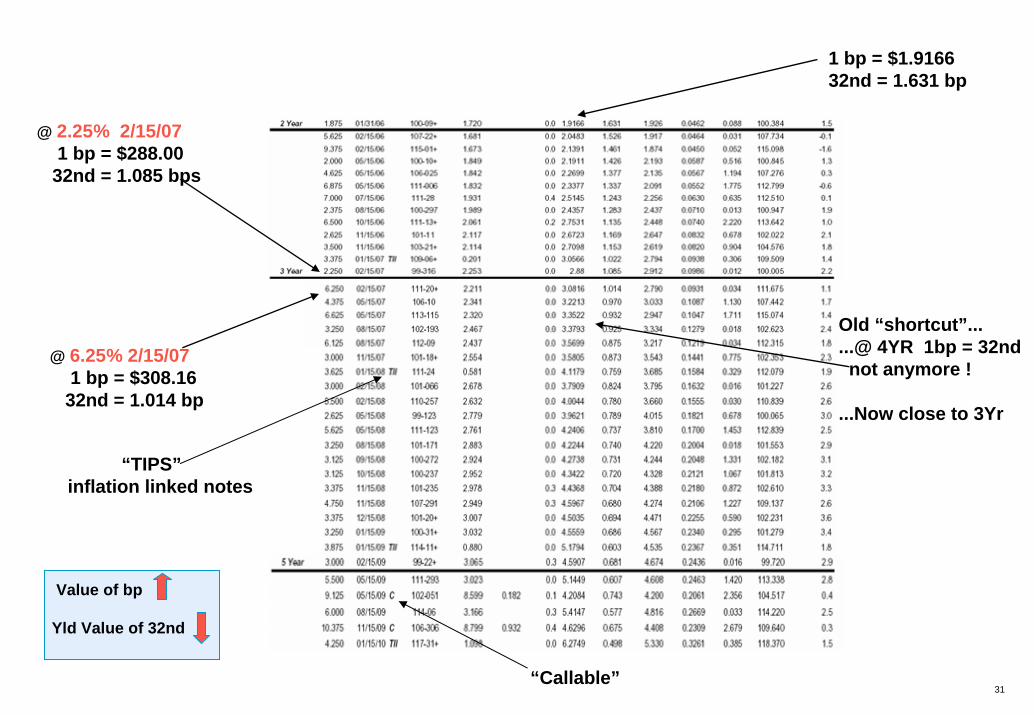

$ Value of a Basis Pointan (“01”) A 32nd always

equals $312.50ALWAYS !!

1 Year

1 YR bp = $1003 bps = $300

32nd = $312.50

@ 1YR…... 32nd = 3.046 bps

Value of bp

Yld Value of 32nd

31

Value of bp

Yld Value of 32nd

1 bp = $1.916632nd = 1.631 bp

@ 2.25% 2/15/071 bp = $288.00

32nd = 1.085 bps

@ 6.25% 2/15/071 bp = $308.16

32nd = 1.014 bp

Old “shortcut”......@ 4YR 1bp = 32nd

not anymore !

...Now close to 3Yr

“Callable”

“TIPS”inflation linked notes

32

Value of bp

Yld Value of 32nd

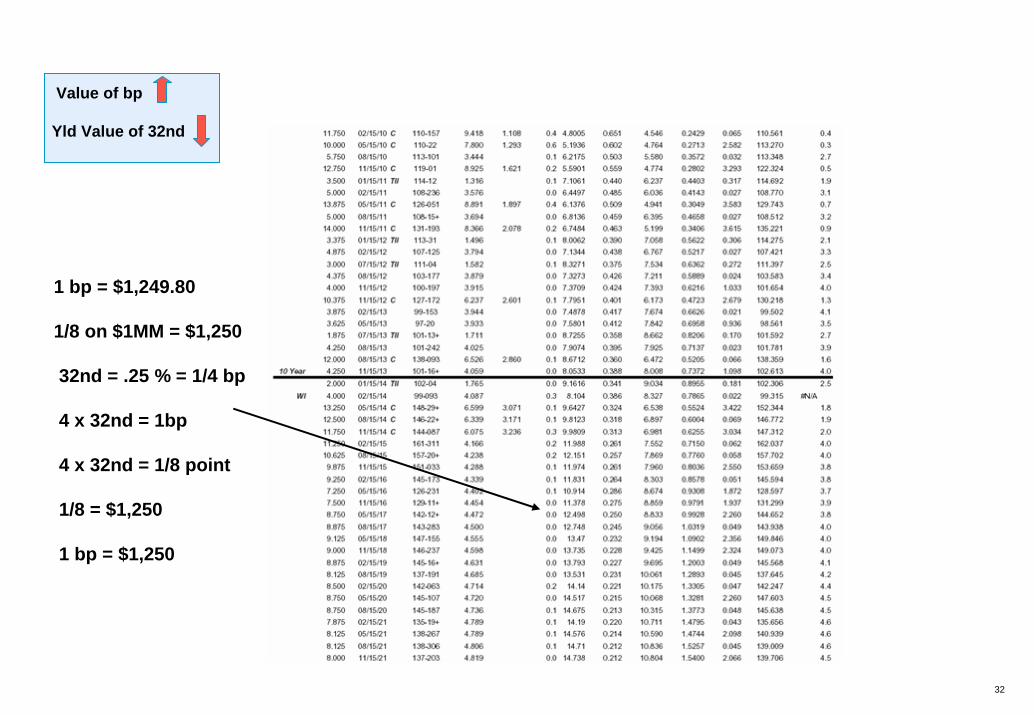

1 bp = $1,249.80

1/8 on $1MM = $1,250

32nd = .25 % = 1/4 bp

4 x 32nd = 1bp

4 x 32nd = 1/8 point

1/8 = $1,250

1 bp = $1,250

33

1 bp = $1,551.30

32nd = approx 1/5 of bp

1 bp = approx 5 X 32nd = 5 X $312.50 = $1,562.50

Value of bp

Yld Value of 32nd

34

THE REPO MARKET

“HOW A GUY NAMED VINNY AND HIS BUDDY SALCHANGED THE WORLD”

35

The Financing Desk• Insures liquidity of Firm by “funding” the Firm• Runs the “matched book”• Finances the “positions” of the Firm by using the “repo Market”

Debt – UST, agencies, ABS, mortgages, corporatesEquityForeign ExchangeMoney Markets – CP, CD’sBank Liquidity – Time deposits (TD’s, “depo’s”), CP, CD’s

Repurchase Agreement – “Repo” / “Reverse Repo”- “repo” market 1 wk “GC” = 1.01 / .95 - Dealer “buys collateral @ 1.01%

- Dealer “sells” collateral @ .95%

DEALER – “buys” collateral / “sells” money (receives) (delivers) earns 1.01% interest

CLIENT – “sells” collateral / “buys” money(delivers) (receives) pays 1.01% interest

DEALER – “sells” collateral / “buys” money (delivers) (receives) pays .95% interest

CLIENT – “buys” collateral / “sells” money(receives) (delivers) earns .95% interest

REPO

REVERSEREPO

“MATCHED BOOK”

FOLLOW THE

MONEY !!

36

“BID” for “GC”“general collateral”

THE “REVERSE REPO”

“OFFER OF “GC”THE “REPO”

Other types of collateral…agenciesmortgagescorporates

37

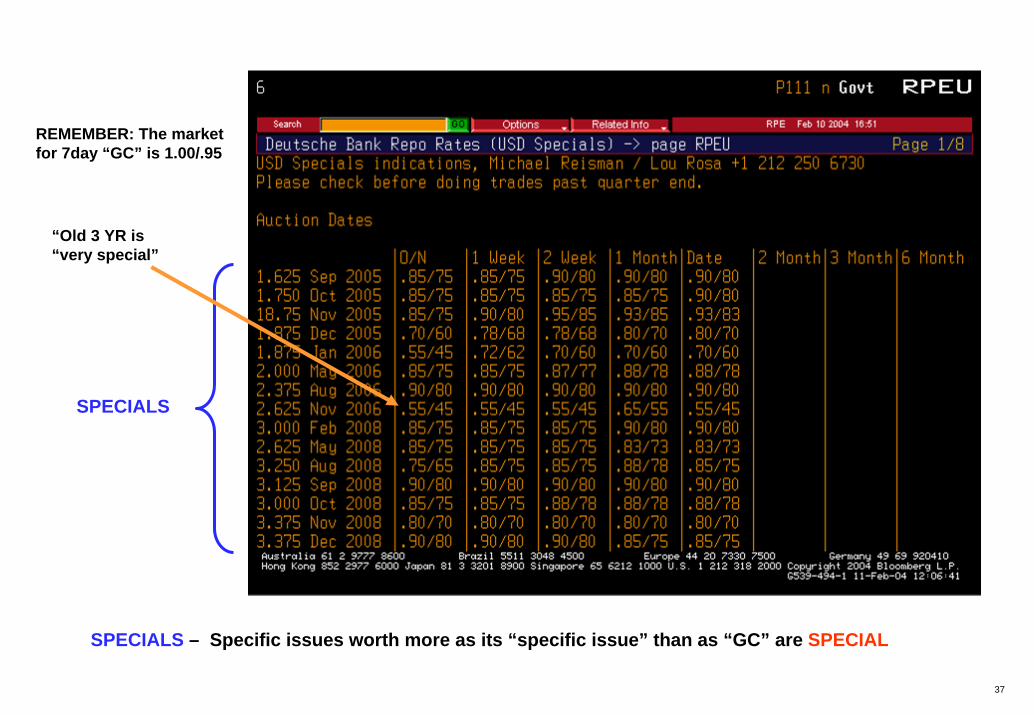

SPECIALS – Specific issues worth more as its “specific issue” than as “GC” are SPECIAL

SPECIALS

“Old 3 YR is “very special”

REMEMBER: The marketfor 7day “GC” is 1.00/.95

38

“SPECIALS”NOTE the large variationsin pricing…

Most of the pricing volatility is due to the auctions…

There is a scarcity of thesetwo issues going into theauctions…

Why ? Because they havebeen “shorted” as a resultof auction strategy and there is specific demandfor these issues

Must deliver to get paid….

VERY SPECIAL

39

DEALER:- 3.25% COUPON SHORT+ .15% REVERSE RATE- 3.10% COST OF SHORT

+ LOSS OF TIME / MONEY FORNUMBER OF SHORT DAYS

REPO

REVERSE REPO (“Special”)

DEALER

“pays interest”

CLIENT

“earns interest”CASH

“ COLLATERAL ”

UST 6.50 10/06

“GC” RATE .95%

DEALER EARNS “ CURRENT YIELD ” UST 6.50% @ 111- 14+ = 2.02 YTM CURRENT YIELD = approx 5.83%

REPO TRANSACTION DEALER EARNS “ CURRENT YIELD “ 5.83%LESS “ GC “ RATE .95% “ POSITIVE CARRY “ 3.88 bps

DEALER

“receives interest”

CLIENT

“pays interest’“ COLLATERAL ”

CASHDealer“short”

3.25% CPN

• UST 3.25% 1/09 @ 101-03 = 3.01% “YTM”• = CURRENT YIELD 3.19%• “REVERSE REPO” RATE = .15% (15 bps)

UST 3.25% 1/09

REVERSE RATE .15%

CLIENT:+3.19% CURRENT YIELD- .15% “COST OF MONEY”3.04%

+ .95% INVESTMENT RETURN (1wk “GC” rate = .95%)3.99% CLIENT RETURN

1 wk “GC” market = 1.01 / .95

Remember: DVP

“SPECIAL” MARKET3.25 1/09 = .15 / .05

40

New 3Y noteThe new 3Y note, maturing on 15-Feb-2007, will beauctioned on 10th February. We anticipate an issue size of$24 bn, and estimate a fair value for the roll at pick 15.75bp (for value as of announcement date).

We use our spline model to estimate a fair value for theroll, by first calculating a yield for the WI issue using thespline, and then fixing the amount of premium attributableto the WI issue (a spread to the spline). The amount ofthe premium factors in the benchmark status, as well ascurrent market supply and demand considerations. Usinga spline yield allows us to account for curve extension, aswell as coupon differences, and allows us to comparecycles of issuance in different yield curve and slopeenvironments, without the level distortions inherent inraw yield spreads.

Taking this analysis one step further, the spread to thespline for any particular issue incorporates a certainamount of premium, or financing-adjustment, driven bysupply and demand considerations in the market. We can

distortion, we need to strip out this financing-adjustmentto be able to compare previous cycles on a like-for-likebasis. This then gives us a cleaner estimate of how muchof a benchmark premium a new issue is likely tocommand. Note that in terms of actual valuation for WIissues though, we would need to add back a financingadjustmeestimate, based on where we believe the WIissue is likely to trade in the repo market.Exhibit 4 shows the financing-adjusted spline spread forthe current 3Y note, as well as the previous 2 issues

.

Estimated “roll”

“special”equals

demand

AUCTIONS

41

We see that the recent 3Y notes have been priced ataround 0.5-2.5 bp cheap to the spline, and have tended torichen in the following months. However, the current 3Ynote is currently slightly cheaper than the previous twoissues, for this point in the cycle, and as such we wouldexpect the WI 3Y note to trade on the cheaper side of therange. Hence, we estimate a financing-adjustedsplinespread for the WI of about 2 bp cheap to the curve. Also,we believe the WI issue is likely to trade about 25 bpthrough GC in the repo market, which equates to afinancing-adjustment of about 2.2 bp (to next auctionsettle date).Given the closing spline yield at 2.457%, we estimate afair roll of +15.75 bp, for value as of announcement date(with the forward yield on the current 3Y at 2.283%, as ofThursday’s close). Carry on the current 3Y note shouldnarrow the roll by about 2.6 bp to first settle.

New 5Y noteThe new 5Y note, maturing 15-Feb-2009, will beauctioned on 11th February. We anticipate an issue size of$16 bn, and estimate a fair value for the roll at pick 5.75bp (for value as of announcement date).Exhibit 5 shows that the recent 5Y notes have beenpriced at around 1-3 bp cheap to the spline model, on afinancing-adjusted basis. shows that the current issuance regime would result in an issuance shortfall of about

$119bn, if the CBO deficit projections are realized.

We estimate that the WI 5Y note will trade at afinancingadjustedspline spread of about 1.5 bp cheap to the curve.Also, we believe the WI issue is likely to trade about 35bp through GC in the repo market, which equates to afinancing-adjustment of about 0.6 bp (to next auctionsettle date).Given the closing spline yield at 3.262%, we estimate afair roll of +5.75 bp, for value as of announcement date(with the forward yield on the current 5Y at 3.213%, as ofThursday’s close). Carry on the current 5Y note shouldnarrow the roll by about 2.1 bp to first settle.

Adjusting for “repo” cost

“CARRY”

42

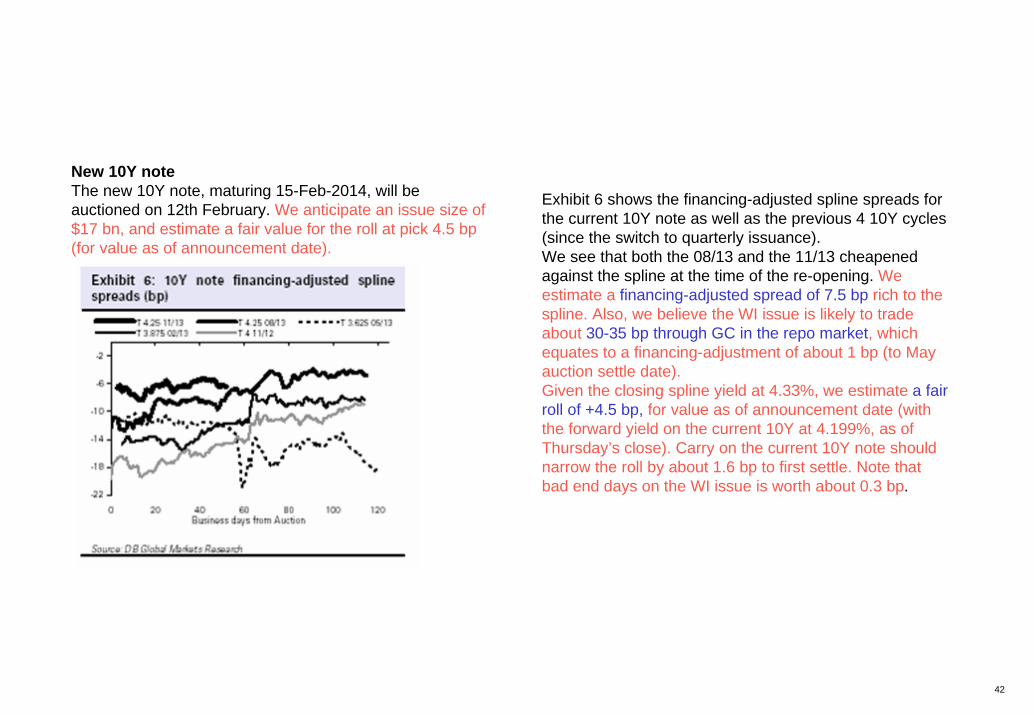

New 10Y noteThe new 10Y note, maturing 15-Feb-2014, will beauctioned on 12th February. We anticipate an issue size of$17 bn, and estimate a fair value for the roll at pick 4.5 bp(for value as of announcement date).

Exhibit 6 shows the financing-adjusted spline spreads forthe current 10Y note as well as the previous 4 10Y cycles(since the switch to quarterly issuance).We see that both the 08/13 and the 11/13 cheapenedagainst the spline at the time of the re-opening. Weestimate a financing-adjusted spread of 7.5 bp rich to thespline. Also, we believe the WI issue is likely to tradeabout 30-35 bp through GC in the repo market, whichequates to a financing-adjustment of about 1 bp (to Mayauction settle date).Given the closing spline yield at 4.33%, we estimate a fairroll of +4.5 bp, for value as of announcement date (withthe forward yield on the current 10Y at 4.199%, as ofThursday’s close). Carry on the current 10Y note shouldnarrow the roll by about 1.6 bp to first settle. Note thatbad end days on the WI issue is worth about 0.3 bp.

43

TREASURY SUPPLY

“WHO STOLE MY 3YR NOTE…AND BROUGHT ITBACK !”

44

TREASURY AUCTIONS

2 YR NOTES SINCE 1950 MONTHLY UNCHANGEDREDUCED / ENLARGED

3 YR NOTES SINCE 1950 QTLY GONE 5/98 – BACK 1/’03

4 YR NOTES SINCE 1950 QTLY GONE 12/90

5 YR NOTES SINCE 1950 QTLY QTLY TO ‘91

W / REOPENINGS MTHLY TO ’98QTLY TO ’00SEMI TO 1/03

7 YR NOTES SINCE 1966 QTLY GONE 4/93

10 YR NOTES SINCE 1950 QTLY SEMI-ANNUALW / REOPENINGS

15 YR NOTES 3 TIMES ONLY GONE 1980

20 YR NOTES SINCE 1981 QTLY GONE 1986

30 YR NOTES SINCE 1950 QTLY GONE 2002

1 YR T-BILL SINCE 1973 MTHLY GONE 2002

“Quarterly Refunding”

45

46

THE SWAP MARKET

“OBJECTS IN THE MIRROR ARE CLOSER THAN THEY APPEAR”

OR

“…PAY NO ATTENTION TO THAT MAN BEHIND THE CURTAIN”

47

SWAPS

SWAP YIELDS UST “interpolated curve”

+ SWAP SPREAD

TREASURY (UST) CURVE /YIELDthe “interpolated curve”

SWAP SPREADBID / ASK

“on the run”Benchmark Treasuries

NOTE:

7 YR UST 5.00% 2/15/11 YLD = 3.52%

7 YR “Comp Benchmark YLD = 3.52%

7 YR SWAP “interpolated” YLD = 3.418%

…This is a difference of 10 bps in YLD

MUST DEAL IN SWAP YIELDS NOT IN SWAP SPREADS

“bid” = “pay” fixed“ask” = “receive” fixed

…always 3mth LIBOR

48

ISSUER PAYS FLOATING RATE 3MTH LIBOR +50 3.89% - 3.39% = 50 bps

DEALERFIXED

3.39 (3.01 + 38)

Fixed 3.89%+85

“PAYS FIXED”

“RECEIVES FLOATING”

ISSUER“RECEIVES FIXED”

“PAYS FLOATING”FLOATING

3 Mth LIBOR “FLAT”

3 Mth LIBOR “FLAT”

DEALER ISSUERFLOATINGFIXED

3.43 (3.01 +42)

“RECEIVES FLOATING”

“PAYS FIXED”“RECEIVES FIXED”

“PAYS FLOATING”

3Mth LIBOR +55

ISSUER PAYS FIXED RATE 3.98% (3.43% +55bps = 3.98%)

ASSET SWAPBUYER OWNS 4.64% “Asset”

DEALER BUYER

FLOATING

FIXED“RECEIVES FIXED”

“PAYS FLOATING” “RECEIVES FLOATING”

“PAYS FIXED”3.43 = 3.01+ 42

BUYER “EARNS” FLOATING RATE LIBOR +121 bps (4.64% - 3.43% +121bps)

3Mth LIBOR +128

5 YR UST Yld = 3.015 YR Issue Sprd = 85 bps5 YR Security Yld = 4.01

5 YR LIBOR Swap Sprd = 38 / 425 YR Swap Yld = 3.39 / 3.433 Mth LIBOR = 1.13%

ISSUES

ISSUES

49

7 YR (UST 5.00% 2/11) Yld = 3.527 YR Issue Sprd = +1007 YR INTERPOLATED UST Yld = 3.418% (3.42)Difference = 10 bps

ISSUER PAYS FLOATING RATE

7 YR LIBOR Swap Sprd = 49.5 / 53.5 (49 /54)7 YR Swap Yld = 3.91 / 3.953 Mth LIBOR = 1.13%

3MTH LIBOR +61 4.52% - 3.91% = 61 bps

DEALERFIXED

3.91% (3.42 +49)

Fixed 4.52%+100

“PAYS FIXED”

“RECEIVES FLOATING”

ISSUER“RECEIVES FIXED”

“PAYS FLOATING”FLOATING

3 Mth LIBOR “FLAT”

ISSUES

ISSUER PAYS FLOATING RATE 3MTH LIBOR +51 4.52% - 4.01% = 51 bps

DEALERFIXED

4.01% (3.52 +49)

Fixed 4.52%+100

“PAYS FIXED”

“RECEIVES FLOATING”

ISSUER“RECEIVES FIXED”

“PAYS FLOATING”FLOATING

3 Mth LIBOR “FLAT”

ISSUES

WRONG Treasury + Swap Spread

“comps” vs “on the run”

50

SWAP AND FLOATING RATE TERMS

INDEX RESET PAYFED FUNDS DAILY (AVG) MONTHLY

“OPEN” (QUARTERLY)“EFFECTIVE”

LIBORMONTHLY MONTHLY MTHLY / QTLYQUARTERLY QUARTERLY QUARTERLYSEMI-ANNUAL SEMI-ANNUAL SEMI-ANNUAL

T-BILL WEEKLY (AVG) MTHLY/QTLY

PRIME RATE DAILY (AVG) MTHLY/QTLY

OTHERSCP – COMMERCIAL PAPER USUALLY “MTHLY RESET/ MTHLY PAY

COFI – “COSTT OF FUNDS” IDEX (11th DISTRICT)

CMT – “CONSTANT MATURITY TREASURY”

RESET and PAYMENT DATES

INTEREST DETERMINATION DATES - 2 LONDON BUSINESS DAYS- FED H15- TELERATE 3750- BBA PAGE

51

MONEY MARKET INDEXED SWAP RATES

PRIME RATE(4.00%)

T– BILLS LIBOR FED FUNDS

ALL INDICES ARE vs 3 MONTH LIBOR

52

CORPORATE BOND MARKET

SUPPLY SECTORSTRENDS

53

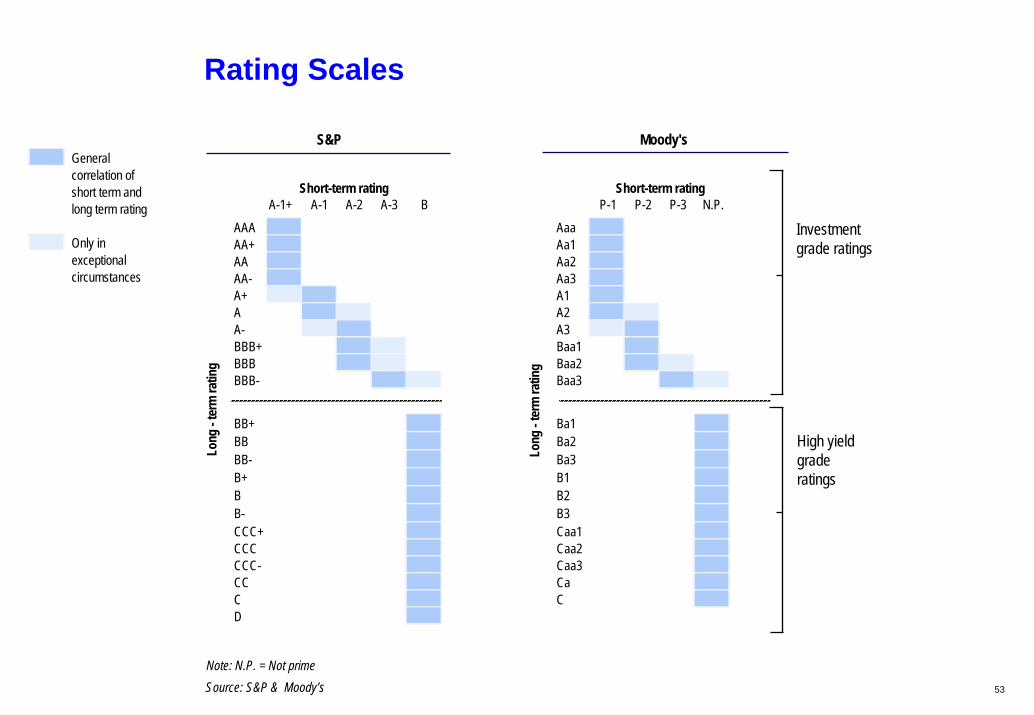

Rating Scales

Moody's

Long

-te

rm ra

ting

Short-term rating

High yield grade ratings

Investment grade ratings

Source: S&P & Moody’s

S&P

A-1+ A-1 A-2 A-3 BAAAAA+AAAA-A+AA-BBB+BBBBBB-

BB+BBBB-B+BB-CCC+CCCCCC-CCCD

Long

-te

rm ra

ting

Short-term rating

Note: N.P. = Not prime

Generalcorrelation ofshort term andlong term rating

Only inexceptionalcircumstances

P-1 P-2 P-3 N.P.AaaAa1Aa2Aa3A1A2A3Baa1Baa2Baa3

Ba1Ba2Ba3B1B2B3Caa1Caa2Caa3CaC

54

55

56

57

58

59

60

61

62

63

64

THE NEW ISSUE

CORPORATE BOND MARKET

• D0CUMENTATION

• REGISTRATION

• 414 SHELF “MTNs ”

• PUBLIC – PRIVATE (144A)

65

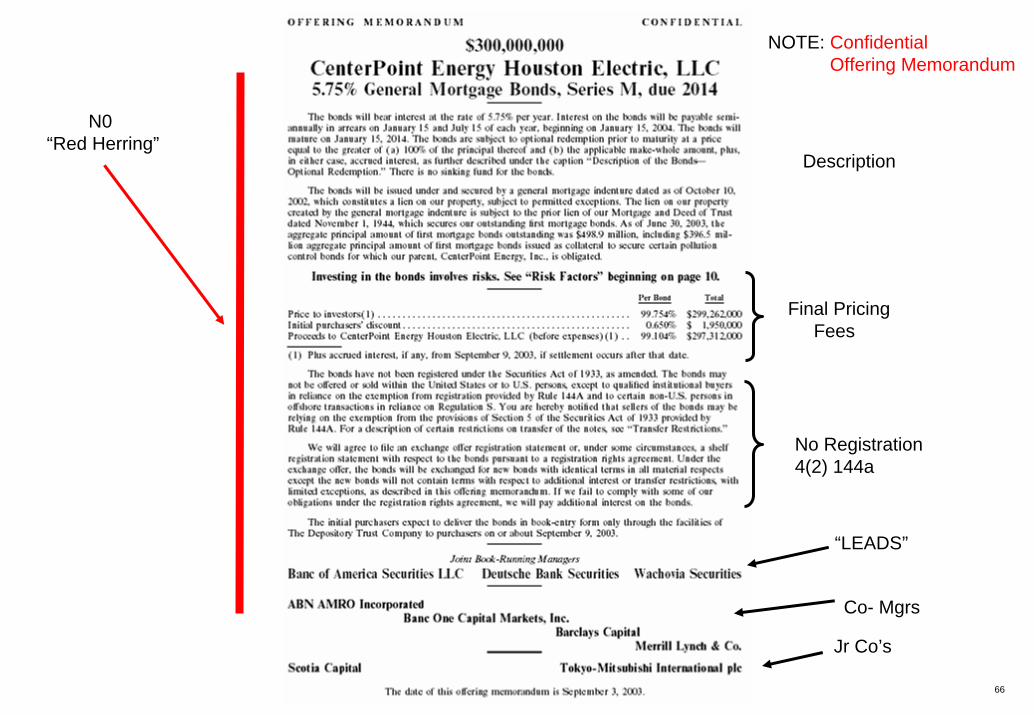

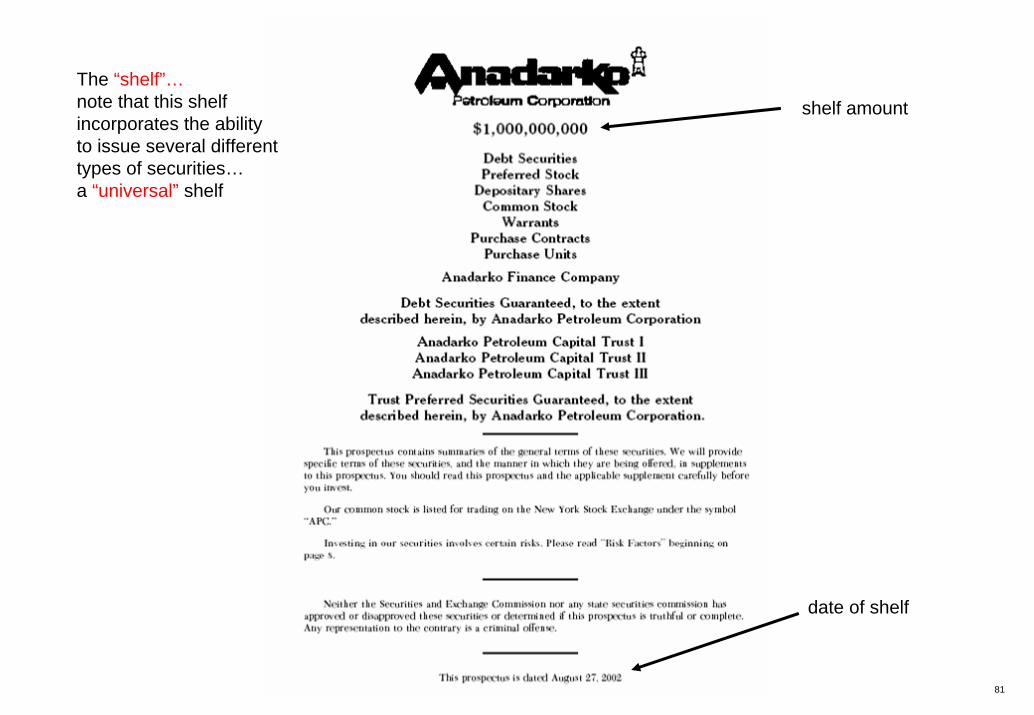

DEBT REGISTRATION and “OFFERING” MATERIALS

The 415 Shelf• 1981• S-1, S-2, S-3 (F-1, F-2, F-3) • “Schedule B”

•Basic Ingredients• Indenture – contract between issuer and trustee on behalf of

securities holders– creates the debt securities and “covenants” to

protect investors – filed with SEC / not distributed to investors

• Registration Statement – disclosure document– filed with the SEC and distributed to investo– Prospectus – the “base” / primary offering document

• Underwriting Agreement – purchase or distribution contract betweenissuer and underwriters

Underwritten Syndicate OfferingBase ProspectusPreliminary prospectus (“red herring”)The “final”

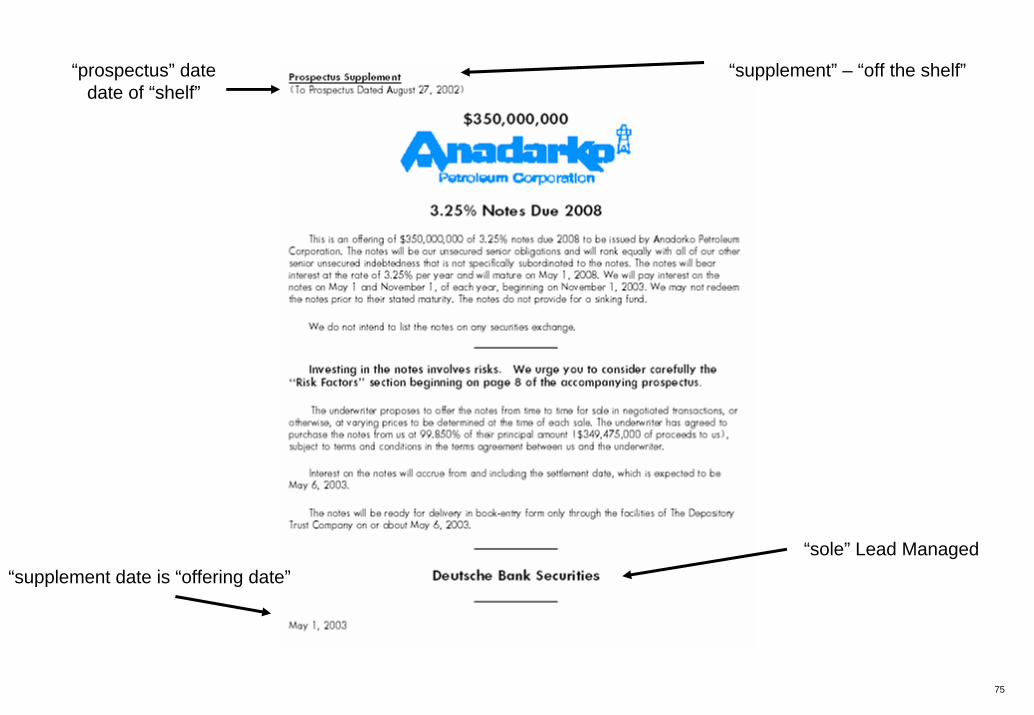

Medium-Term NotesBase prospectusProspectus supplementPricing supplement

(“pricing sticker”)

66

“LEADS”

Co- Mgrs

Final PricingFees

Description

No Registration4(2) 144a

N0 “Red Herring”

Jr Co’s

NOTE: ConfidentialOffering Memorandum

67

More Information than “registered” deal

68

“Boilerplate”…do’s and don’t’s

69

70

“make - whole”call

Using “144A” exemptionuntil “SHELF” filed... • Timing• Penalty

71

“denoms”

72

Syndicate participationbreakdown. Only in FINAL…not in preliminary or “redherring”

73

“Rule 144A “ sellingrestrictions - QIB’s

74

Last Page

75

“supplement” – “off the shelf”

“supplement date is “offering date”

“prospectus” datedate of “shelf”

“sole” Lead Managed

76

77

Company Information

78

NON-CALL

use of proceeds

79

“Company Disclosure”

80

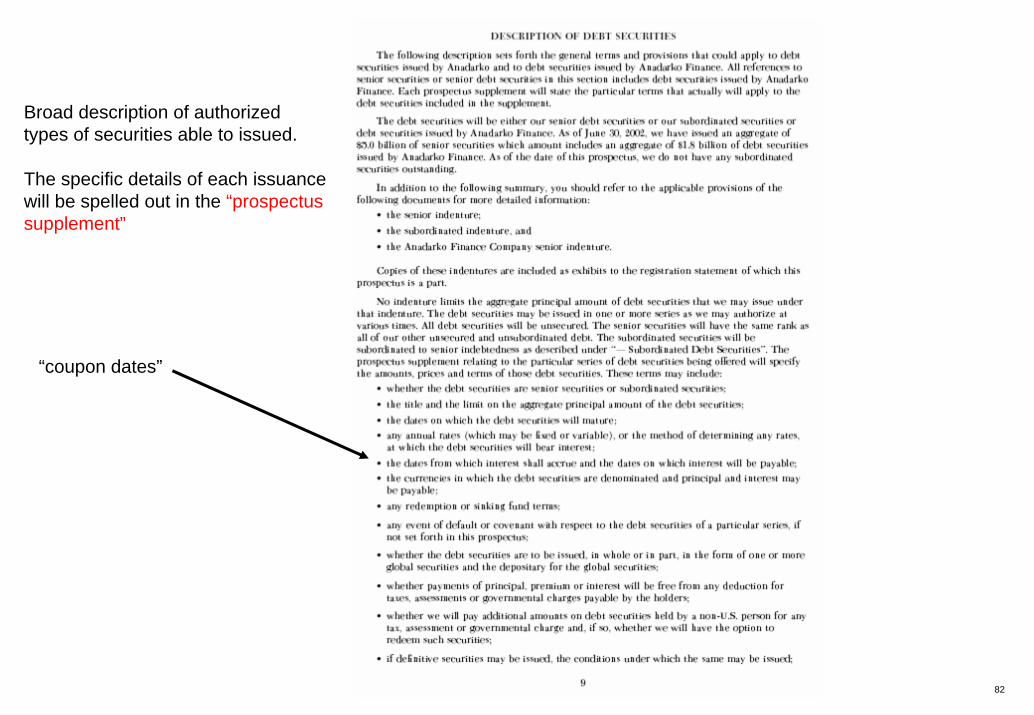

The ability to issue thesecurities is containedin the broad “description”in the “prospectus”

The details...

“Book-Entry”“global notes”

The amount of the offering…this amount will be subtractedfrom the registered amount of the “shelf”

“coupon dates’

“record dates”

81

The “shelf”…note that this shelf incorporates the abilityto issue several different types of securities…a “universal” shelf

shelf amount

date of shelf

82

Broad description of authorizedtypes of securities able to issued.

The specific details of each issuancewill be spelled out in the “prospectussupplement”

“coupon dates”

83

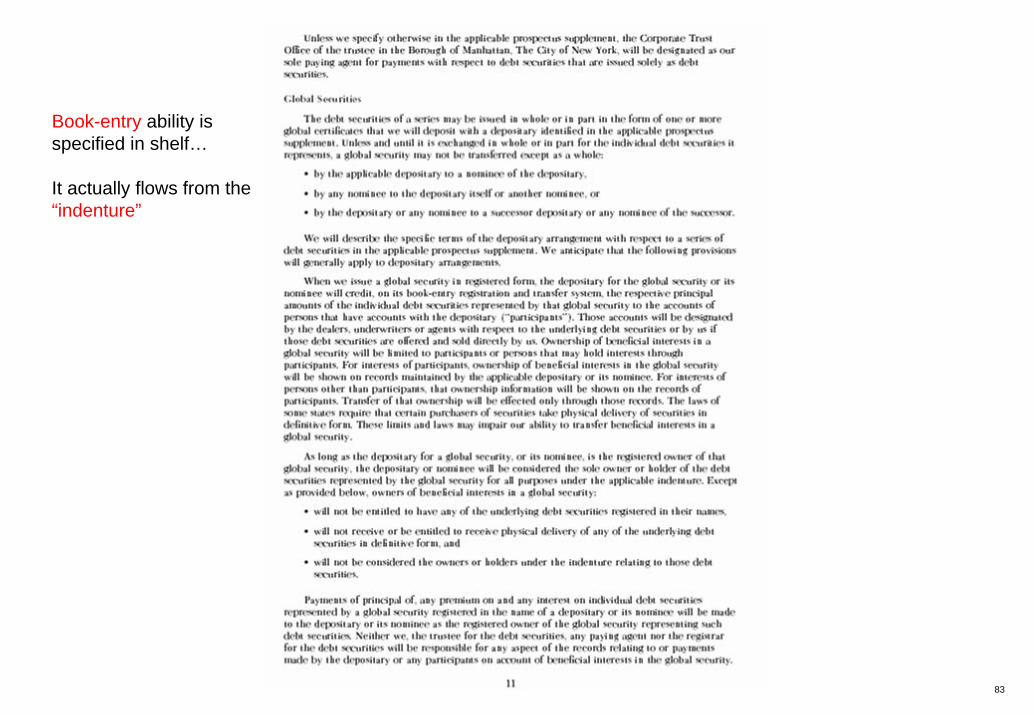

Book-entry ability is specified in shelf…

It actually flows from the“indenture”

84

“Underwriters,” “dealers”and “agents” (‘MTN’s”)

85

NEW ISSUE SYNDICATE“THE DEAL”

• MECHANICS

• STRATEGY

• TIMING

• HEDGING

86

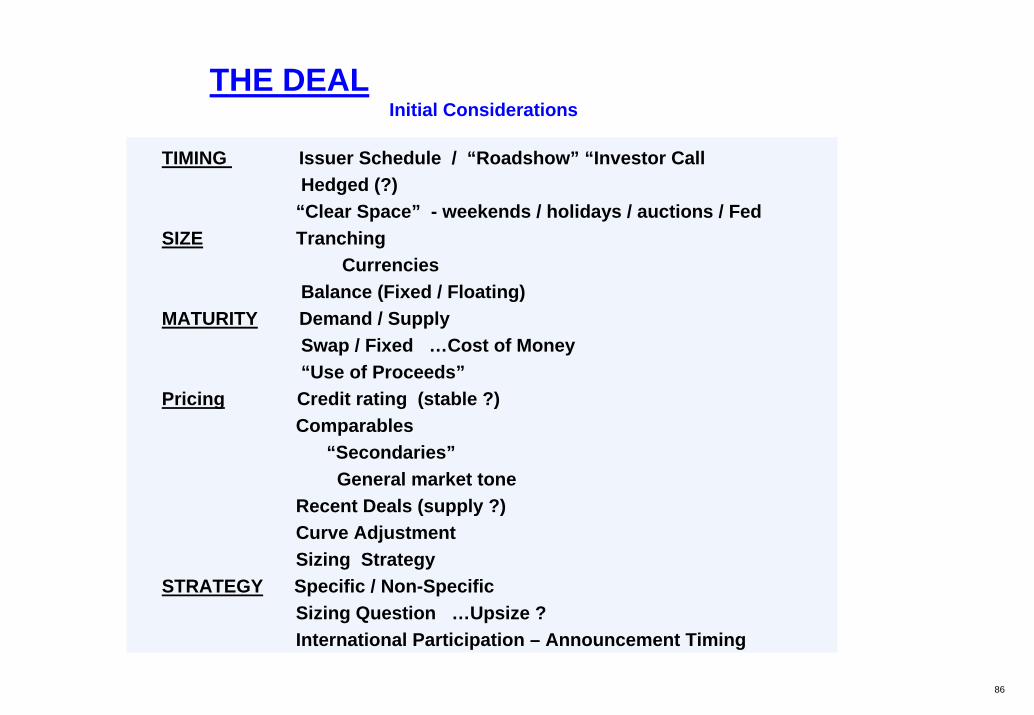

THE DEALInitial Considerations

TIMING Issuer Schedule / “Roadshow” “Investor CallHedged (?)

“Clear Space” - weekends / holidays / auctions / FedSIZE Tranching

CurrenciesBalance (Fixed / Floating)

MATURITY Demand / SupplySwap / Fixed …Cost of Money“Use of Proceeds”

Pricing Credit rating (stable ?)Comparables

“Secondaries”General market tone

Recent Deals (supply ?)Curve AdjustmentSizing Strategy

STRATEGY Specific / Non-SpecificSizing Question …Upsize ?International Participation – Announcement Timing

87

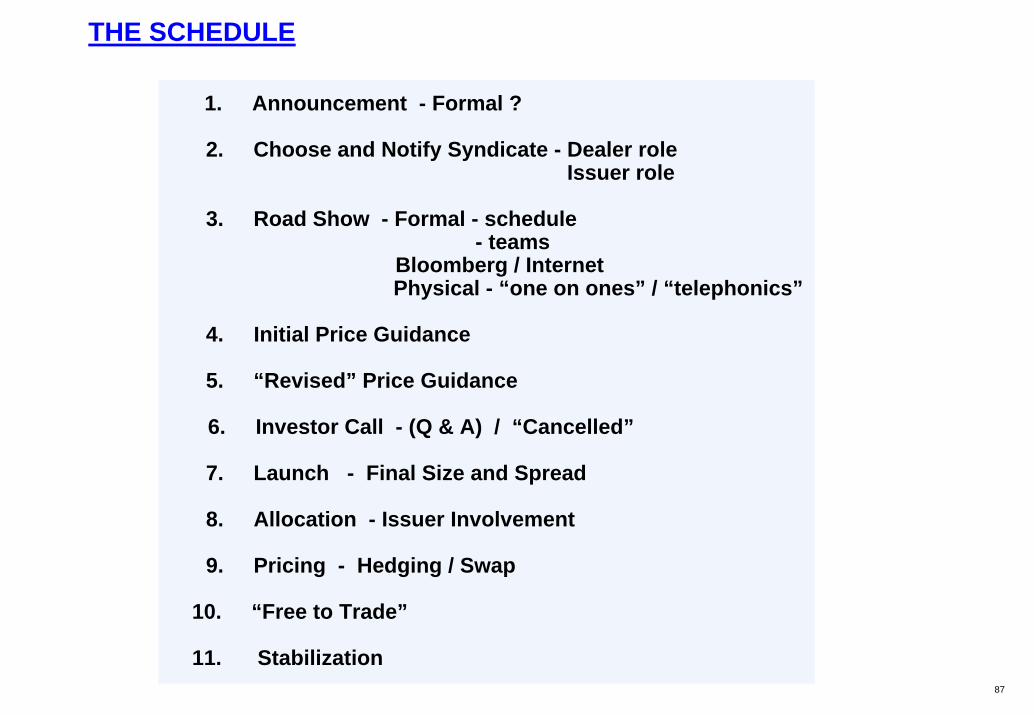

THE SCHEDULE

1. Announcement - Formal ?

2. Choose and Notify Syndicate - Dealer role Issuer role

3. Road Show - Formal - schedule - teams

Bloomberg / InternetPhysical - “one on ones” / “telephonics”

4. Initial Price Guidance

5. “Revised” Price Guidance

6. Investor Call - (Q & A) / “Cancelled”

7. Launch - Final Size and Spread

8. Allocation - Issuer Involvement

9. Pricing - Hedging / Swap

10. “Free to Trade”

11. Stabilization

88

89

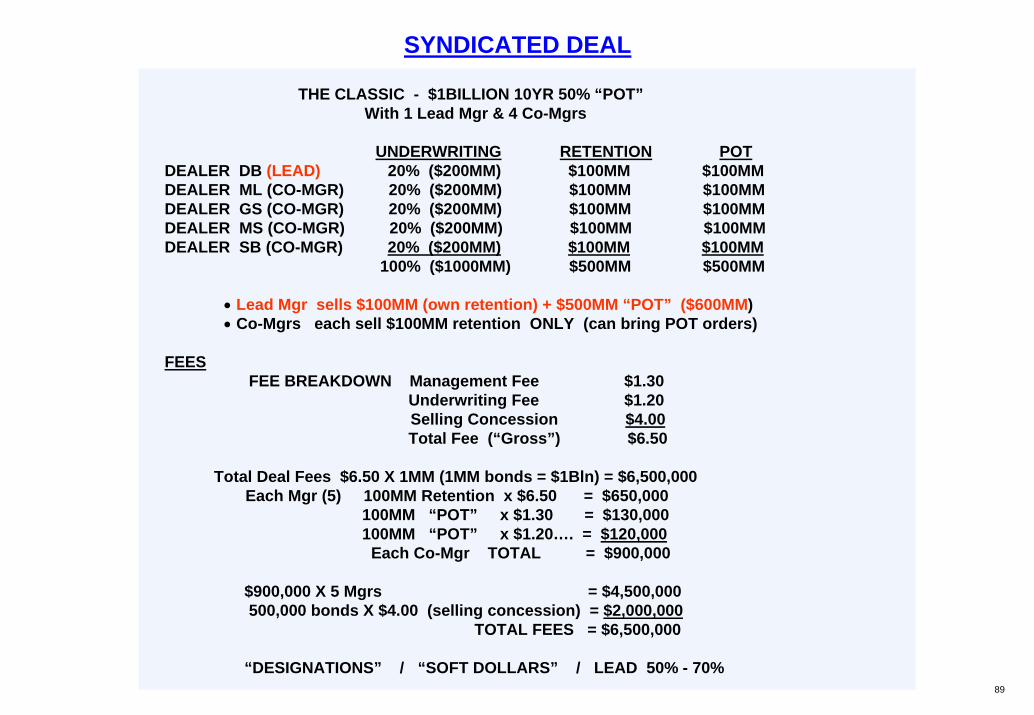

SYNDICATED DEAL

THE CLASSIC - $1BILLION 10YR 50% “POT”With 1 Lead Mgr & 4 Co-Mgrs

UNDERWRITING RETENTION POTDEALER DB (LEAD) 20% ($200MM) $100MM $100MMDEALER ML (CO-MGR) 20% ($200MM) $100MM $100MMDEALER GS (CO-MGR) 20% ($200MM) $100MM $100MMDEALER MS (CO-MGR) 20% ($200MM) $100MM $100MMDEALER SB (CO-MGR) 20% ($200MM) $100MM $100MM

100% ($1000MM) $500MM $500MM

• Lead Mgr sells $100MM (own retention) + $500MM “POT” ($600MM)• Co-Mgrs each sell $100MM retention ONLY (can bring POT orders)

FEESFEE BREAKDOWN Management Fee $1.30

Underwriting Fee $1.20Selling Concession $4.00Total Fee (“Gross”) $6.50

Total Deal Fees $6.50 X 1MM (1MM bonds = $1Bln) = $6,500,000Each Mgr (5) 100MM Retention x $6.50 = $650,000

100MM “POT” x $1.30 = $130,000100MM “POT” x $1.20…. = $120,000

Each Co-Mgr TOTAL = $900,000

$900,000 X 5 Mgrs = $4,500,000500,000 bonds X $4.00 (selling concession) = $2,000,000

TOTAL FEES = $6,500,000

“DESIGNATIONS” / “SOFT DOLLARS” / LEAD 50% - 70%

90

THE GLOBAL- THE NEW SYNDICATE

“100% POT” / “FIXED ECONOMICS / JOINT LEADS

ECONOMICS

Joint-Leads (2-4) (Book Runners) 80% – 90%Co-Leads (3-5) (Senior) 5% – 15%Co- Managers (5-10) (Junior) 1% – 5%

FEES

”GLOBAL” $4.50 x $1bln = $4,500,000

LEADS /BOOKS

Joint-Leads / Joint Books = “League Tables”Other “Leads” %/$ smaller / No League Table

No Retention Smaller FeesNo Allocation Bigger DealsNo Designation More ParticipatioNo “Soft Dollars” Less WorkLess Client Contact Less League Table Same “Underwriting Risk” Less “Deal Risk”

91

NEW ISSUE SYNDICATE PRICINGPre-Pricing Preparation

1. Book Reconciliation2. “Dates” - settlement date (T+3) (T+5)

- maturity date – no weekends / holidays3. “Billing and Delivery”

4. Allocation – “No Cry Babies!!”

5. Hedging and Hedge Ratios – the “Drop”

6. “Pricing Call” Roles Set7. Set Coupons - Price @ discount

- “long or short first”

PRICING -New DCX

To Settle1. Establish benchmark “bid side” dollar price ALWAYS

“bid side” yield

2. Execute hedges

3. Add “pricing spread” ( + )

4. Use new issue yield to calculate new issue price

5. Cut-up hedge; set opening stabilization strategy: set opening bid6. Send “pot” lists

7. “Free to trade”8. Cover “short” / stabilize

92

“SECONDARIES”

93

“SETTING THE TREASURIES”

“RISK”

94

PRICING THE NEW NOTE

“RISK”

95

THE “DROP”

96

DCX issues $ 1 Billion 5.70% 3 /13 / 2014Final Deal Spread…………………….. +170 bpsUST Benchmark (10 YR Note)……… 4.25 11 / 15 / 20013Benchmark Dollar Price ……………... 101-25+Benchmark Yield ……………………… 4.025%New DCX Note Yield………………….. 5.725% (4.025 + 170bps)Dollar Price on New DCX Note……… 99.803 (“5.70’s at 5.725 Yld”)New DCX Note Maturity………………. March 15, 2014First DCX Coupon Date………………. September 15, 2004 (“long first”)

DCX “”HEDGING”Benchmark “RISK” Factor……………. 8.089New DCX “RISK” Factor……………... 7.57HEDGE RATIO………………………... .9358 (.936)

THE “DROP”Normal Benchmark Settlement……… February 12 “REGULAR” (NEXT DAY)Normal DCX Note Settlement……….. February 16 “CORPORATE” (T +3)

Holiday !! Now February 17Benchmark financing adj.(“repo cost”) .75 bpsCost of Settlement Difference for Sellers of UST vs New DCX…….. “THE DROP” = 1.5 32nd’s (.6 bp) REPO COST !!)