presentation to the british society of sugar technologists ... · capital investment plan...

TRANSCRIPT

Presentation to the British Society of Sugar Technologists

17th April 2012.

Simon MitchellS&BE Business Development Director

.

u per z lCountry Paper on Brazil

2

Agenda

Bunge

Why invest in Brazil?

• Overview of Bunge• Who we are, what we do• Entry into sugar

• Scale• Cost of production• Versatility• Growth

Has the CS Brazilgrowth storycome to end?

• Agricultural yields• Cost environment• RoW response• Fuel policy and Exchange rate • Logistics• Growth drivers

3

We Are a Leading Global Agribusiness & Food Company

KEY FACTS

Employees: 37,000

Facilities: 400+

Countries of Operations: 30+

CAPITAL INVESTMENT PLAN

Fertilizer 10%

Food & Ingredients

15%

Agribusiness45%

Sugar & Bioenergy

30%

• A leader in oilseed processing

• A leader in global grain and

oilseed marketing

• Retail fertilizer in Brazil

• Fertilizer operations in

Argentina and the U.S.

• 50% stake in JV with OCP in

Morocco

• Leading producer of consumer

bottled oil brands in South

America, Europe and Asia

• Leading supplier to food service

companies and food processors

in North America

• Leading corn and wheat miller

in the Americas

Fertilizer Agribusiness Food & Ingredients

• 20 MMT sugarcane milling

capacity producing sugar, ethanol

and electricity

• #2 in global trade and distribution

Sugar & Bioenergy

4

What We Do — From Feed to Food to Fuel

Bunge processes soybeans, rapeseed, canola, sunflower seeds, corn, wheat,

sugarcane and other agricultural commodities to make products and ingredients

with numerous applications.

• Feed for animals

• Cooking oils, margarines and

shortenings

• Sugar and ethanol from sugarcane

• Milled corn, wheat and rice for

cereal, snacks, baked goods, beer

and other foods

• Oils used in solvents, inks,

lubricants, hydraulic fluid, foam

and other applications

• Fertilizers that help farmers

produce quality crops

5

A global, integrated, coordinated Chain is essential

Farmer• Soy• Corn• Wheat• Sorghum• Barley• Canola• Rapeseed• Sunseed• Flaxseed• Sugar cane

Product Origination• Storing• Blending• Drying• Financing

Basic Processing• Soybean• Rapeseed• Canola• Sunseed• Specialty

seeds• Raw sugar

Logistics• Rail• Truck• Barge• Ocean

vessel

Sales & Distribution• Raw material• Protein meal• Vegetable oil• Financial

services

Refining, Value Added & Packaging• Edible oils• Margarine• Mayonnaise• Corn, wheat &

rice products• Refined sugar

and ethanol

Risk Management

Value creation shifts along the chain

Agribusiness ChainFood &

Ingredients

6

Bunge’s development in Sugar & Bioenergy

0020052005

q d MAcquired Moema:

� mi 5 mills with 13.7 mmt of apacicapacity

� l Expands Bunge total apaci t mmtcapacity to 20mmt

020102 62 620062006 20072007 0020082008 2 92 920092009

e u r Started sugar trading & s merchandising

p i noperation

� c u Acquired Santa u ll 1s Juliana mill (1st

sasset)

� d v m n Started development f e ro n o mof Pedro Alfonso mill

� is d d a e is d d a e Raised dedicated Raised dedicated u d g a d u d g a d funding to expand funding to expand

o oSugar & BioenergySugar & Bioenergy

� re s Acquired 60% stake in o t r u c n Monte Verde sugarcane

ilmill

� re t e Acquired Tate & Lyle r d sugar trading &

e h i g u smerchandizing business

� d h Announced JV with o h t l n Itochu in Santa Juliana

o A oand Pedro Afonso

111120112011

This raised Bunge’s share of production capacity in Brazil to

~3.6%:

Major Oil companies now own 15% of production

7

Agenda

Bunge

Why invest in Brazil?

• Overview of Bunge• Who we are, what we do• Entry into sugar

• Scale• Cost of production• Versatility• Growth

Has the CS Brazilgrowth storycome to end?

• Agricultural yields• Cost environment• RoW response• Fuel policy and Exchange rate • Logistics• Growth drivers

8

SSUSAUSA

Sao Paulo

Territory: 8.5 million km2

This creates significant logistics challenges!

The distances are vast....

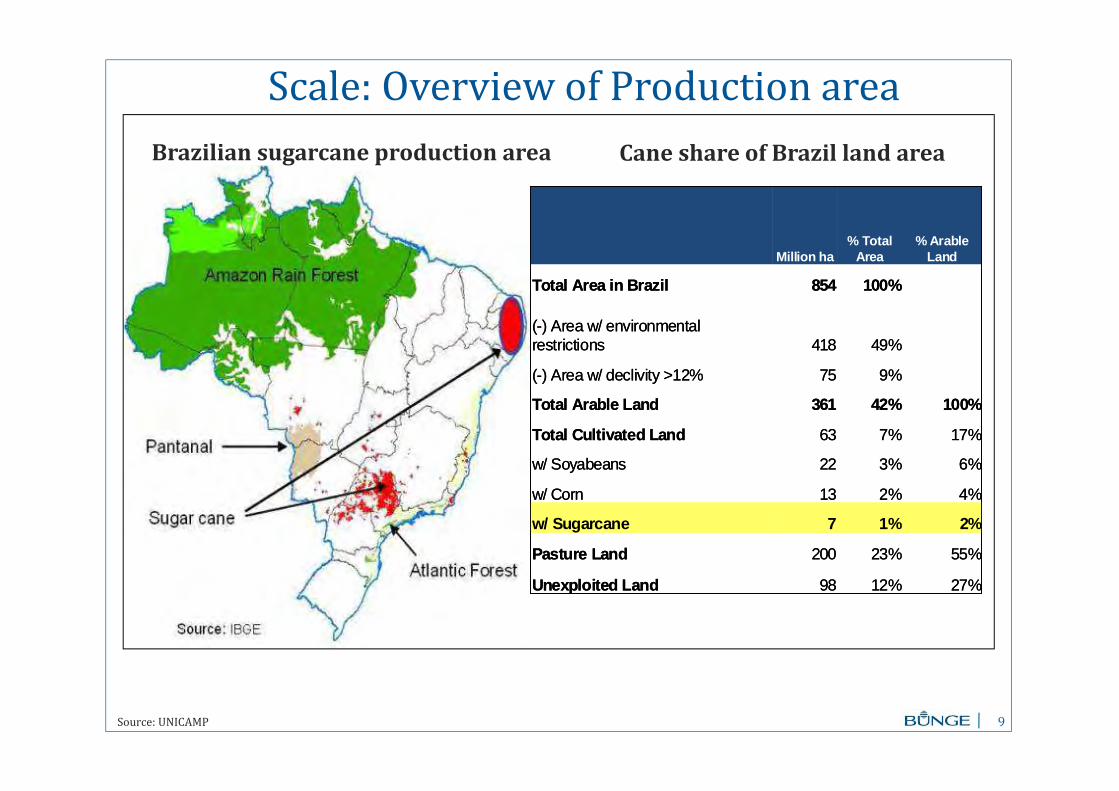

Scale: Just to put into context how big Brazil is!

9Source: UNICAMP

Scale: Overview of Production area

Million ha % Total

Area % Arable

Land

Total Area in Brazil 854 100%

(-) Area w/ environmental restrictions 418 49%

(-) Area w/ declivity >12% 75 9%

Total Arable Land 361 42% 100%

Total Cultivated Land 63 7% 17%

w/ Soyabeans 22 3% 6%

w/ Corn 13 2% 4%

w/ Sugarcane 7 1% 2%

Pasture Land 200 23% 55%

Unexploited Land 98 12% 27%

Million ha % Total

Area % Arable

Land

Total Area in Brazil 854 100%

(-) Area w/ environmental restrictions 418 49%

(-) Area w/ declivity >12% 75 9%

Total Arable Land 361 42% 100%

Total Cultivated Land 63 7% 17%

w/ Soyabeans 22 3% 6%

w/ Corn 13 2% 4%

w/ Sugarcane 7 1% 2%

Pasture Land 200 23% 55%

Unexploited Land 98 12% 27%

Brazilian sugarcane production area Cane share of Brazil land area

10

Scale: Brazil has experienced huge growth in cane production

200

250

300

350

400

450

500

550

600

99-00 01-02 03-04 05-06 07-08 09-10 11-12

CS Sugarcane Crush (MMT)

NEARLY 300% GROWTH IN 10 YEARS

?

11

Moema Ownership%

MTBA

DF

TO

MS

PR

MG

RibeirãoPreto RJ

ES

Paranaguá

Santos

Vitória

Scale: Large players benefit from flexible and efficient clusters

Moema (SP)

Frutal (MG)

Ouroeste (SP)

Guariroba (SP)

Itapagipe (MG)

MonteVerde (MS)*

SantaJuliana (MG)*

PedroAfonso (TO)*

OriginalBungeMills

AdditionalMills fromMoema Group

* Bunge has a 80% stake at Pedro Afonso and Santa Juliana and 60% stake at Monteverde.

SP

12

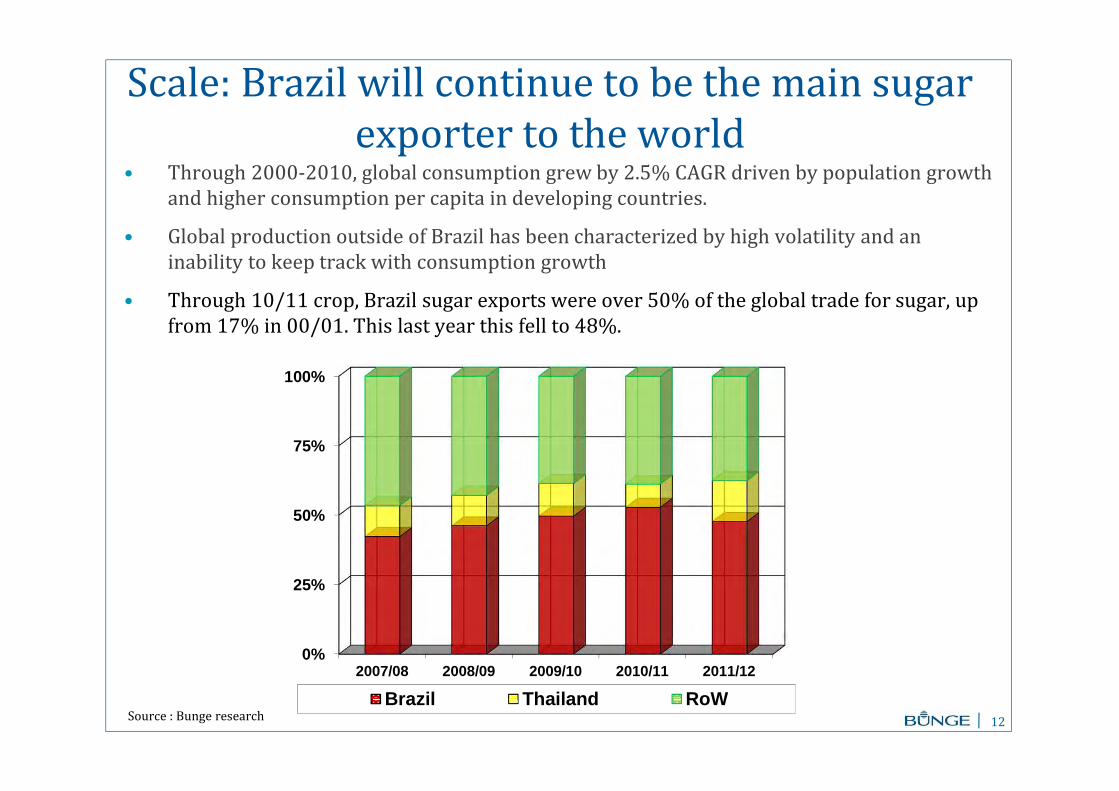

Scale: Brazil will continue to be the main sugar exporter to the world

• Through 2000-2010, global consumption grew by 2.5% CAGR driven by population growth and higher consumption per capita in developing countries.

• Global production outside of Brazil has been characterized by high volatility and an inability to keep track with consumption growth

• Through 10/11 crop, Brazil sugar exports were over 50% of the global trade for sugar, up from 17% in 00/01. This last year this fell to 48%.

0%

25%

50%

75%

100%

2007/08 2008/09 2009/10 2010/11 2011/12

Brazil Thailand RoWSource : Bunge research

13

Cost of production: Brazil still the world leader, but losing its cost advantage

CS Brazil’s cost advantage vs. Top 4 RoW exporters

(Ex-Mill - US$ / mt)

Source : LMC International

Has encouraged a supply side response from RoW, but which other country has the land, agronomics and cost

structure to materially increase supply ?

0

20

40

60

80

2003/04 2004/05 2005/06 2006/07 2007/08 2008/09 2009/10 2010/11 2011/12

14

There is significant versatility for the uses of Sugar cane

Cane Mill Ethanol

Sugar

Co-Gen

Ethanol

Molasses

Power

Juice

Cellulosic Ethanol

(Potential for new technology to mature

in the future)

Fermentation to Food and Feed products

e.g. amino acids (Lysine, Threonine, MSG), Organic Acids (Citric Acid, Lactic Acid), Vitamins (Vitamin C)…

Processing to Industrial Chemicals

Ethanol based ethylene and thermoplastics Fermentation to other chemicals

Fermentation to Biofuels and Hydrocarbons

e.g. Diesel and lubricants; short-term oleochemicals or edible products, new fermentation technologies and catalysts being developed

A

C

B

Vinasses + Ashes

(Fertilizer used in house)

15

Versatility: Brazil can respond to sugar/ethanol S&D and pricing

38%

40%

42%

44%

46%

48%

50%

52%

2001-02 2003-04 2005-06 2007-08 2009-10 2011-12

CS crush ATR mix to sugar(% to sugar)

Brazil can relatively easily switch from sugar to ethanolSource : Bunge

16

Growth: Global sugar S&D will remain tight

Assumes: - Normal weather patterns

- CS Brazil capacity to grow by ~10mmt by 2020- RoW will grow by ~25mmt by 2020- S&D kept in balance by CS Brazil

140

150

160

170

180

190

200

210

2000/01 2002/03 2004/05 2006/07 2008/09 2010/11 2012/13 2014/15 2016/17 2018/19

World Production Consumption MMT

World production CS Brazil Expansion Production Consumption

17

Growth: Brazil ethanol demand (led by fuel ethanol) will outstrip supply

0

10

20

30

40

50

60

2005 2007 2009 2011 2013 2015

Total ethanol production Total potential ethanol demand

Ethanol production in million m3

Source : Bunge estimates

18

Agenda

Bunge

Why invest in Brazil?

• Overview of Bunge• Who we are, what we do• Entry into sugar

• Scale• Cost of production• Versatility• Growth

Has the CS Brazilgrowth storycome to end?

• Agricultural yields• Cost environment• RoW response• Fuel policy and Exchange rate • Logistics• Growth drivers

19

Brazil Agricultural yields under pressure

Financially stretched mills have under-invested in the field, hence the recent increase in average age of the cane

TRS (kg/mt) Yield (mt/ha) evolution

65.00

70.00

75.00

80.00

85.00

90.00

2005/20062007/20082009/2010 2011/12

Yield (mt/ha)

125.00

130.00

135.00

140.00

145.00

150.00

2000/01 2003/04 2006/07 2009/10

TRS (kg/mt) in CS Brazil

Source Bunge

20

Trends increasing production costs• High financial costs: Many mills paying the price for over expansion (2006 – 2009)

• New social law requires mills to concede social benefits for the traditional workers from the NO/NE and minimum wages increasing faster than inflation

• Green cane protocol requires mills to stop cane burning by 2014 pushing mills into aggressive mechanisation schedules with;

– Loss of sugar content volume and ATR

– Shortage of trained labour

– High capital outlay

– Long lead time to efficient returns from mechanization

• Over last 5 years UNICA suggest field production costs have increased by 38.5%, mainly in land leasing (+57.12%), but also manpower (+47.12%) and mechanisation (+28.17%)

But leading millers have invested significantly in agriculture to address this underperformance

Source : Bunge Research

21

Brazil’s Cost Environment has recently been difficult

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

7-J

an

-08

7-M

ar-

08

7-M

ay

-08

7-J

ul-

08

7-S

ep

-08

7-N

ov

-08

7-J

an

-09

7-M

ar-

09

7-M

ay

-09

7-J

ul-

09

7-S

ep

-09

7-N

ov

-09

7-J

an

-10

7-M

ar-

10

7-M

ay

-10

7-J

ul-

10

7-S

ep

-10

7-N

ov

-10

7-J

an

-11

7-M

ar-

11

7-M

ay

-11

7-J

ul-

11

Global Rebar Price Trend by Aug 1, 2011Rebar N.America FOB Midwest mill $/t

Rebar Europe Delivered $/t

Rebar East Aisa Import CFR $/T

Rebar Shanghai Inc VAT $/T

Shanghai rebar FOB

Inflation(US$ c/lb)

Steel(US$c/lb)

Very hostile to manufacturing in Brazil

0

2

4

6

8

10

12

14

16

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

%

Year

Inflation

Infla…

Construction Index

Cost of borrowing

Steel prices expanding (SBB)

Inflation to rise 6% compound through to 2016 (IMF)

Domestic cost of borrowing 12%. 6% in real terms (Tradingeconomics.com)

Construction costs outstripping inflation

CAGR = 8.2%

Sources: IMF, SBB, Tradingeconomics.com, Bunge Research

22

The RoW is catching up

Africa constrained by high political risk, water issues, high transport costs from the interior and high capital costs.

India constrained by water issues

Asia Pacific concentrates 60% of the worlds population and struggles for available land

Russia/ Ukraine possible regime change and investment plus increasing beet yields

EU expanding post regime reform and increasing beet yields

35’ North

35’ South

23

Ethanol growth driver for capacity has disappeared

In 2011, Brazil imported 1.7bln litres of ethanol

Brazil Production of ethanol (hydrous and anhydrous)

Source: Unica

0

5,000

10,000

15,000

20,000

25,000

30,000

2005/2006 2006/2007 2007/2008 2008/2009 2009/2010 2010/2011

Anhydrous ethanol Hydrous ethanol

24

Brazilian Fuel Policy results in an upper cap on domestic gasoline prices

At current pricing and FX, Petrobras is losing moneyEthanol prices historically have been capped at 70% of gasoline

prices

25

Motor vehicle Fleet Projections Brazil

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

45.00

50.00

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

FFV cars Gasoline cars Alcohol cars

Can the fuel policy be maintained?

• Petrobras is absorbing losses on fuel imports

• Exports of ethanol have dramatically declined

• Potential demand for hydrous not being satisfied

– 2008 – 80% satisfied

– 2011 – 40% satisfied

(1) Massive growth in flexfuel demand from rapidly expanding economy and credit availability

(2) Brazil gasoline consumption now exceeds gasoline production capacity and increased volumes now rely on gasoline imports*

(3) Ethanol production declined at the expense of sugar

(4) Brazil currently starting to rely on US imports of ethanol

Source : Bunge analysis – considering UNICA/ANP forecasts

* Will reverse [2018-2020] when Pre-Salt oil fields are developed and new refineries come on stream

26

Brazilian Inflation and Exchange Rates

Brazilian inflation and exchange rate (Bloomberg – YoY % change, Real/US$)

Strong Real +

• Curb on inflation

Weak Real -

• Competitiveness for the industry1.5

2

2.5

3

3.5

0%

4%

8%

12%

16%Inflation %

US$/R$

27

Logistics: Santos remains the leading corridor for the mills in the CS State

Centre South

Santos Paranagua

Crop 09/10 19 4.8

Crop 15/16 24 - 26.5 6 - 6.5

Crop 20/21 26.5 - 31 6.5 – 8

It needs on-going investment to prevent logistics congestion and overload!

MMT

70% of sugar through Santos and 18% through Paranagua.> $500m planned investments to improve the Santos line-up

28

US legislation requires Brazil ethanol

Sugar ethanol is one of two commercial available Advanced Biofuels under the Federal RFS 2

California's Low Carbon Fuel Standard (LCFS) will mandate sugar ethanol use to lower carbon intensity

Evolution of US Renewable Fuels Standards 2 Mandates in Bln Gal

EU / Japan / China are deficit markets which continue to rely on Brazil

These markets in the medium term willing to pay a premium over domestic consumers

EU has legislative targets which require up to 6.2bn litres of imports (Brazil included)

Growing demand for Brazilian Ethanol exports

0

5

10

15

20

25

30

35

40

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

Bln

Gal

lon

s Conventional Biofuels (corn ethanol mainly

Cellulosic Biofuels (no real substitute)

Other advanced (Brazil ethanol mainly)

Renewable Diesel (limited upside)

Source : Unica; RFS legislation

With high oil prices, global demand for fuel ethanol is expected to grow significantly!

29

Brazil Sugar Production and Exports

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

2000

/0120

01/02

2002

/0320

03/04

2004

/0520

05/06

2006

/0720

07/08

2008

/0920

09/10

2010

/1120

11/12

2012

/1320

13/14

2014

/1520

15/16

2016

/1720

17/18

2018

/1920

19/20

Sugar production (m mt) Exports (potential) Exports w hites (kmt) Exports raw s (kmt)

Brazil: Sugar Production and exports 2020Sugar crystallisation will not rise in proportion with cane production, but capacity will expand to keep the S&D in broad balance

Export expansion Consolidation

Source : Bunge forecasts

30

Growing demand for new Cane Products

0

10

20

30

40

50

60

70

80

2010/11 2012/13 2014/15 2016/17 2018/19

New Products

Cane crush (m mt)

Date

Mt million

e.g.

Amtris

Mitsui / DOW

Solazyme

Various

green plastic

packaging

initiatives

31