presentation to the public utilities board of manitoba to the public utilities board of manitoba ......

TRANSCRIPT

Presentation to the Public Utilities Board of Manitoba

Manitoba Hydro GRAHearing Start Date: January 5, 2011

2

Presentation Summary

• Corporate Profile• Financial Update• General Rate Application• Rate Comparisons• Energy Conservation Programs• Risk Management• IFRS• Current Water Conditions

3

Corporate Profile at March 31, 2010• $2 billion annual revenue• $12 billion assets• 532 000 electricity customers• 264 000 natural gas customers• Exports to over 30 wholesale customers in USA &

Canada• Electricity rates the lowest in North America• Ranked #1 in Customer Satisfaction by CEA

4

Corporate Profile at March 31, 2010 (cont’d)

• 6 200 employees• A Top 100 Employer in Canada• Leader in Aboriginal employment• Ranked #1 in Safety by CGA• Power Smart Program one of the most aggressive in

North America

5

Financial Update

6

Consolidated Financial ResultsIncome Statement for the Fiscal Year Ended March 31 ($ millions)

2010 2009REVENUEElectric

Manitoba 1,172$ 1,161$ Extraprovincial 427 623

Gas 454 580 2,053 2,364

Cost of gas sold 316 431 1,737$ 1,933$

EXPENSESOperating and administrative 456 442 Finance expense 410 471 Depreciation and amortization 384 368 Water rentals and assessments 121 123 Fuel and power purchased 104 176 Capital and other taxes 99 87

1,574$ 1,667$

NET INCOME 163$ 266$

7

Consolidated Financial ResultsIncome Statement for the Six Months Ended September 30 ($ millions)

2010 2009REVENUEElectric

Manitoba 541$ 532$ Extraprovincial 236 223

Gas 97 123 874 878

Cost of gas sold 53 77 821$ 801$

EXPENSESOperating and administrative 230 222 Finance expense 219 226 Depreciation and amortization 200 193 Water rentals and assessments 56 58 Fuel and power purchased 58 43 Capital and other taxes 48 51

811$ 793$

NET INCOME 10$ 8$

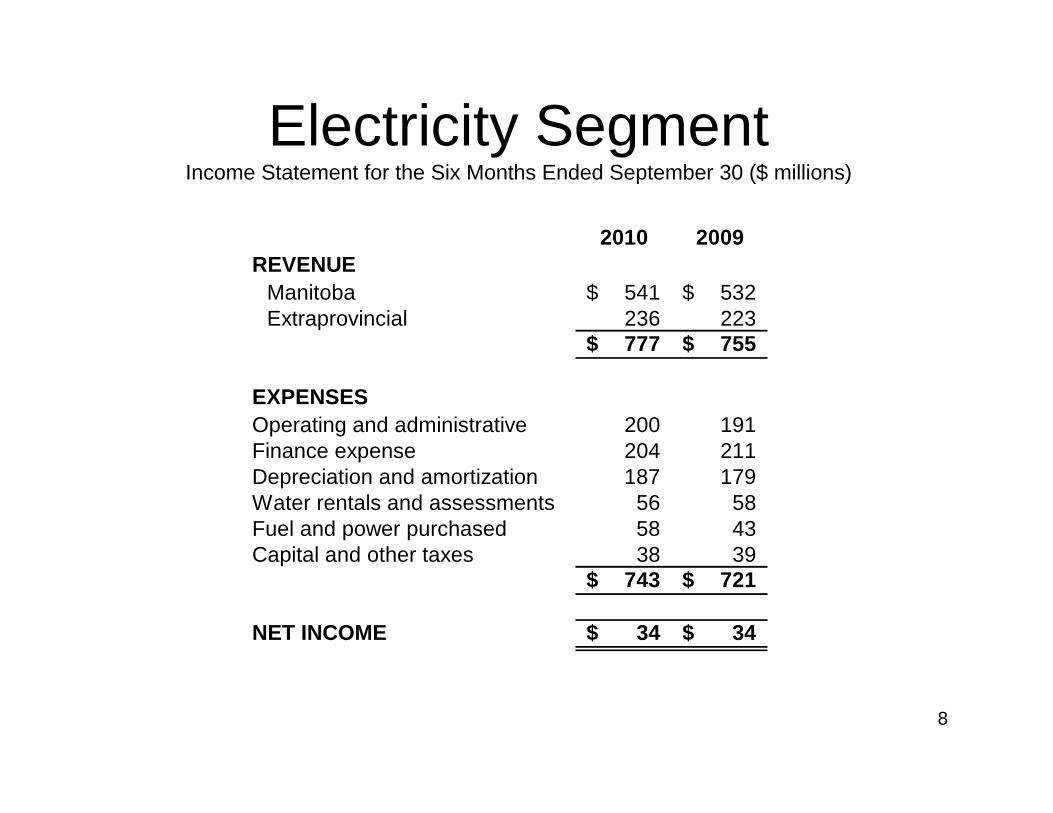

8

Electricity SegmentIncome Statement for the Six Months Ended September 30 ($ millions)

2010 2009REVENUE

Manitoba 541$ 532$ Extraprovincial 236 223

777$ 755$

EXPENSESOperating and administrative 200 191 Finance expense 204 211 Depreciation and amortization 187 179 Water rentals and assessments 56 58 Fuel and power purchased 58 43 Capital and other taxes 38 39

743$ 721$

NET INCOME 34$ 34$

9

Key Financial Results

10

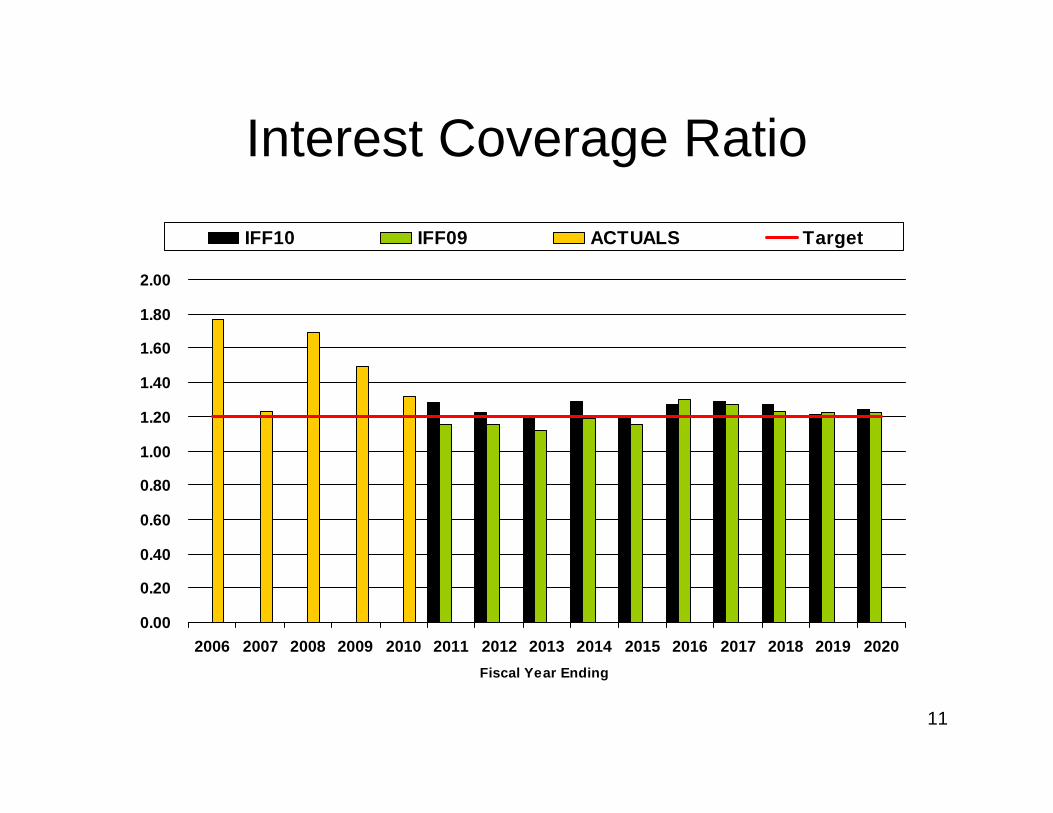

Financial Targets

Interest Coverage: Maintain interest coverage ratio of > 1.20

Capital Coverage:Maintain capital coverage ratio of > 1.20

Debt/Equity:Maintain minimum debt/equity ratio of 75:25

Note: Financial targets may not be maintained during years of major investment in the generation and transmission system.

11

Interest Coverage Ratio

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

2.00

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020Fiscal Year Ending

IFF10 IFF09 ACTUALS Target

12

Capital Coverage Ratio

0.00

0.50

1.00

1.50

2.00

2.50

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020Fiscal Year Ending

IFF10 IFF09 ACTUALS Target

13

Equity Ratio

0%

5%

10%

15%

20%

25%

30%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020Fiscal Year Ending

IFF10 IFF09 ACTUALS Target

14

Equity Ratio 20 Year Outlook

0%

5%

10%

15%

20%

25%

30%

35%

40%

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

Fiscal Year Ending

15

Capital Coverage

1.10

0.77

0.24

1.30

0.0

0.5

1.0

1.5

2.0

2.5

Equity

0.27

0.08

0.26

0.37

0.00

0.10

0.20

0.30

0.40

0.50

Interest Coverage

1.32

2.17

1.58

1.96

0.0

0.5

1.0

1.5

2.0

2.5

MB Hydro Mar 10

Hydro Quebec Dec 09

BC Hydro Mar 10NB Power Mar 08

Financial Ratios Comparison

16

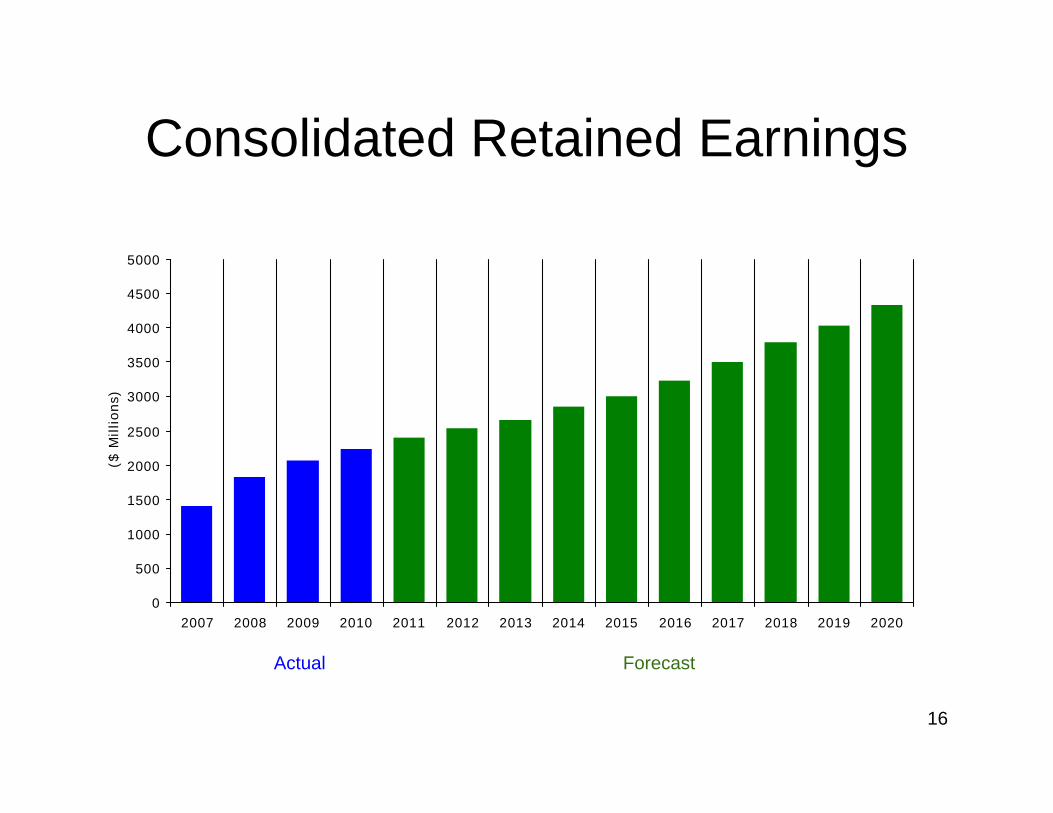

Consolidated Retained Earnings

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

($ M

illions)

Actual Forecast

17

2010/11 Power Resource Plan

• 138 MW St. Joseph wind power 2010/11 to 2011/12• Wuskwatim (200 MW) first power 2011/12• Bipole III 2017/18• 695 MW Keeyask first power 2019/20 • New US interconnection 2019/20• 1 485 MW Conawapa first power 2023/24 • Pointe du Bois spillway replacement 2014/15

18

Operating & Administrative

$0

$100

$200

$300

$400

$500

$600

$700

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020Fiscal Year Ending

Mill

ions

of D

olla

rs

IFF10 IFF09 ACTUALS

19

Operating, Maintenance & Administrative Costs

For the years ending March 31 ($ millions)

CompoundedAverage

2005/06 2006/07 200708 2008/09 2009/10 2010/11 2011/12 Annual Increase

Consolidated OM&A 375$ 386$ 391$ 442$ 456$ 476$ 482$ 4.3%Less:

Centra Gas (53) (54) (56) (60) (61) (63) (64) Subsidiaries (11) (9) (12) (18) (17) (15) (16)

Electric OM&A 311 323 323 364 378 398 402 4.4%

Less Accounting Changes:CICA Changes (10) (13) (13) (13) Reclassifications (3) 2 2 (3) Provision for Acct. Changes (18) (14)

Net Electric OM&A after Accounting Changes 311$ 323$ 323$ 351$ 367$ 369$ 372$ 3.0%

Year over Year % Increase Net of Acctg Changes 4.1% -0.2% 8.9% 4.3% 0.6% 0.9%CPI 2.3% 1.4% 1.2% 1.4% 2.0% 2.0% 1.7%

Actuals Forecast

20

2009/10 OM&AOffice and Building Services

5%

Other 1%

External Services 5%

Materials & Equip Maintenance 6%

Travel and Motor Vehicle 8%

Salaries, Overtime and Benefits 75%

Salaries, Overtime and benefits

Travel and Motor Vehicle

Materials & Equip Maintenance

External Services

Office and Building services

Other

21

Cost Constraint Measures

• Travel restrictions• Hiring freeze• Overtime reductions• Computer life extensions• Fleet reductions• New IT systems

22

Manitoba Hydro Workforce Demographics

Equity Demographics at November 30, 2000

Male ND, 68.8%

Aboriginal, 7.4%

Women, 20.8%

Disability, 2.9%

Vis Minority, 3.1%

Equity Demographics at November 30, 2010

Male ND, 57.3%

Aboriginal, 15.4%

Women, 24.4%

Disability, 4.8%

Vis. Minority, 5.6%

23

General Rate Application

24

General Rate Application

a) 2.8% increase effective April 1, 2010

b) 2.9% increase effective April 1, 2011

c) Final approval of SEP ex parte Orders

d) Final approval of CRP ex parte Order

e) Final approval of Billing Demand Concessions

25

Residential Rates

Interim Approved

April 1, 2010Proposed

April 1, 2011

Basic Charge 6.85$ 6.85$

Energy Charge:First 900 kWh 6.38 ¢ 6.52 ¢Balance kWh 6.57 ¢ 6.84 ¢

26

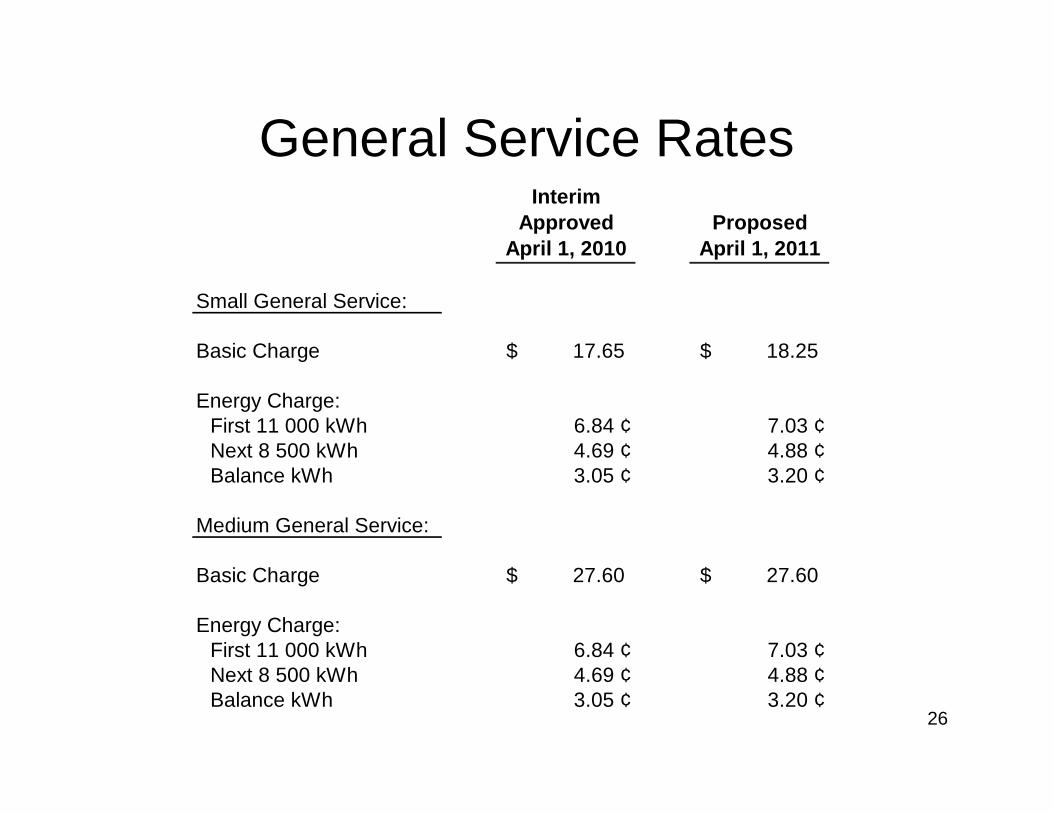

General Service RatesInterim

Approved April 1, 2010

Proposed April 1, 2011

Small General Service:

Basic Charge 17.65$ 18.25$

Energy Charge:First 11 000 kWh 6.84 ¢ 7.03 ¢Next 8 500 kWh 4.69 ¢ 4.88 ¢Balance kWh 3.05 ¢ 3.20 ¢

Medium General Service:

Basic Charge 27.60$ 27.60$

Energy Charge:First 11 000 kWh 6.84 ¢ 7.03 ¢Next 8 500 kWh 4.69 ¢ 4.88 ¢Balance kWh 3.05 ¢ 3.20 ¢

27

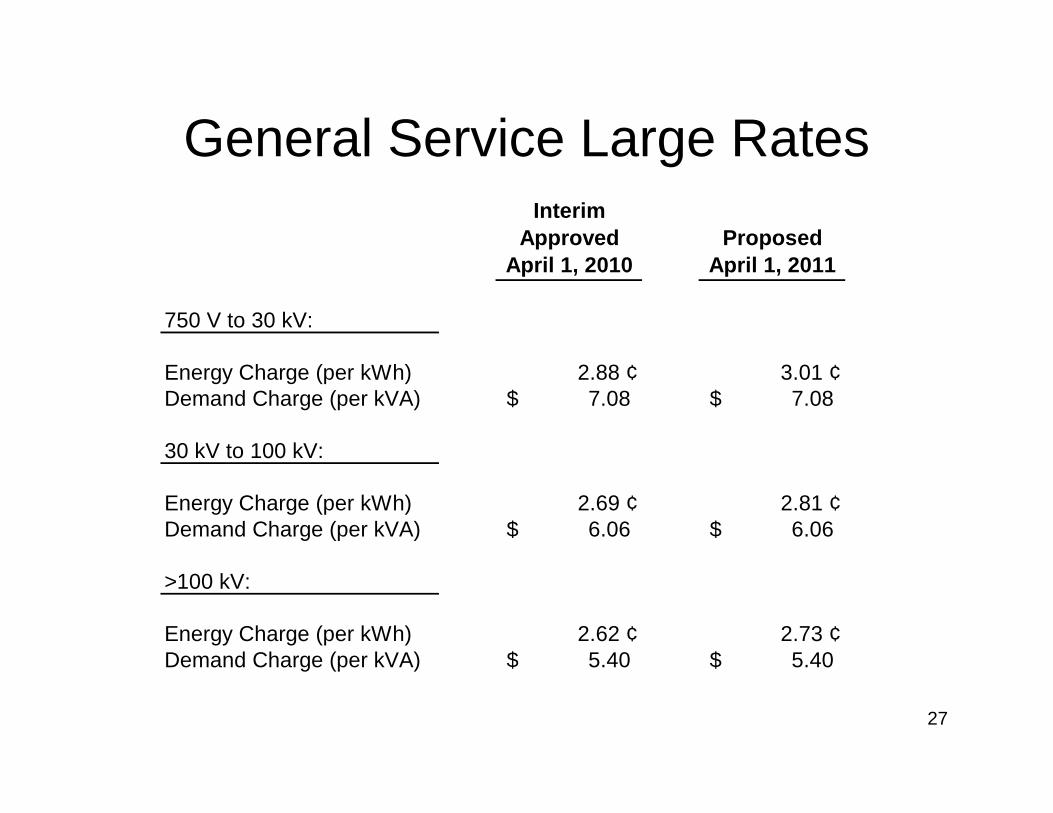

General Service Large RatesInterim

Approved April 1, 2010

Proposed April 1, 2011

750 V to 30 kV:

Energy Charge (per kWh) 2.88 ¢ 3.01 ¢Demand Charge (per kVA) 7.08$ 7.08$

30 kV to 100 kV:

Energy Charge (per kWh) 2.69 ¢ 2.81 ¢Demand Charge (per kVA) 6.06$ 6.06$

>100 kV:

Energy Charge (per kWh) 2.62 ¢ 2.73 ¢Demand Charge (per kVA) 5.40$ 5.40$

28

Rate Comparisons

29

5.445.72

6.306.51

6.67 6.68 6.72

7.297.41 7.43

4.55.05.56.06.57.07.58.0

Manito

ba

British

Colu

mbia

Wyo

ming

Quebec

Kentuck

y

Wash

ington

Idaho

Utah

North Dak

ota

West

VirginiaC

ents

/ kW

.h (C

anad

ian)

Average Retail Price of ElectricityTen Lowest Cost Provinces/ States in North America

Source: US Dept of Energy (May 2010) & Edison Electric Survey (January 2010)(Exchange rate = 1.0279)

30

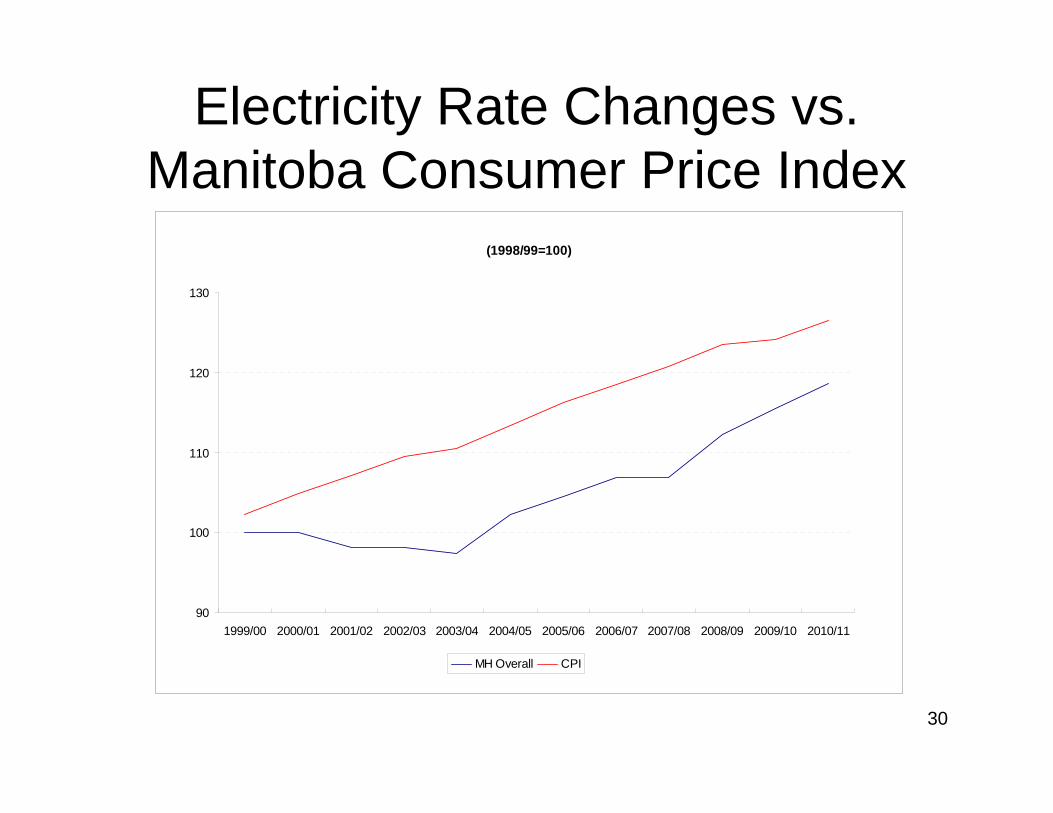

Electricity Rate Changes vs. Manitoba Consumer Price Index

(1998/99=100)

90

100

110

120

130

1999/00 2000/01 2001/02 2002/03 2003/04 2004/05 2005/06 2006/07 2007/08 2008/09 2009/10 2010/11

MH Overall CPI

31

24.0%

23.3%

23.7%

12.2%

25.4%

13.5%

CumulativeIncreases

4.9%

8.7%

6.9%

5.3%

1.5%

0.0%

2006

4.2%

3.8%

5.9%

1.9%

2.1%

2.2%

2007

0%

0%

3.0%

2.9%

2.8%

5.0%

2008

8.5%

9.3%

3.0%

1.2%

9.7%

2.9%

2009

4.5%

0%

3.0%

0.4%

7.3%

2.8%

2010

SaskPower

Nova Scotia Power

New Brunswick Power

Hydro Quebec

BC Hydro

Manitoba Hydro

155%

186%

174%

113%

119%

100%

Current Rates Index

Utility Rate Changes

32

Energy Conservation

Programs

33

Power Smart

• Manitoba Hydro recognizes that energy conservation is one of the most cost effective and environmentally friendly alternatives for meeting demand

• The Canadian Energy Efficiency Alliance (CEEA) recently provided Manitoba with an “A+” rating for its efforts to achieve Energy Efficiency– 4th consecutive report card that Manitoba has either led or

been tied for first place in the national rating

34

Power Smart – Future Action

• The 2010 Power Smart Plan involves a 15 year $572 million investment which targets an additional:– 2,133 GW.h of Conserved Electricity– 106 million cubic metres of Conserved Natural Gas

• Including savings to date, by 2024/25 over $950 million invested to achieve an aggregate:– 3,408 GW.h of Conserved Electricity– 149 million cubic metres of conserved natural gas

35

Affordable Energy Program• 3 Components:

– Demand Side Management (Lower Income Energy Efficiency Program)

– Bill Management (Equal Payment Plan, Flexible Arrears Payment plans, etc.)

– Emergency Financial Assistance (Neighbours Helping Neighbours)

• Significant Focus on Lower Income Energy Efficiency Program

36

Lower Income Energy Efficiency Program

• Launched December 2007

• Over 2600 Initial In-home reviews completed:– Approximately 1700 retrofitted with insulation and other

measures– Approximately 1100 high efficient furnaces installed

• Participation Lower Than Expected, however awareness is increasing and Manitoba Hydro continues to:– Work with partners and stakeholders to increase

participation– Aggressively promote the program

37

Risk Management

38

Immediate and Emerging Risks

• Economic Downturn• Major Capital Expansion Plan• Export Power Contracts• Whistleblower• Shale Gas• Regulatory Burden• Generation Development Sequence

39

High Consequence Risks

Infrastructure > $2 Billion

Drought > $2 Billion

Loss of Export Market > 30% of Revenue

Interest rates Approximately $430 million for a 1% change over 10 years

Foreign exchange Approximately $125 million for a $.10 US change over 10 years

40

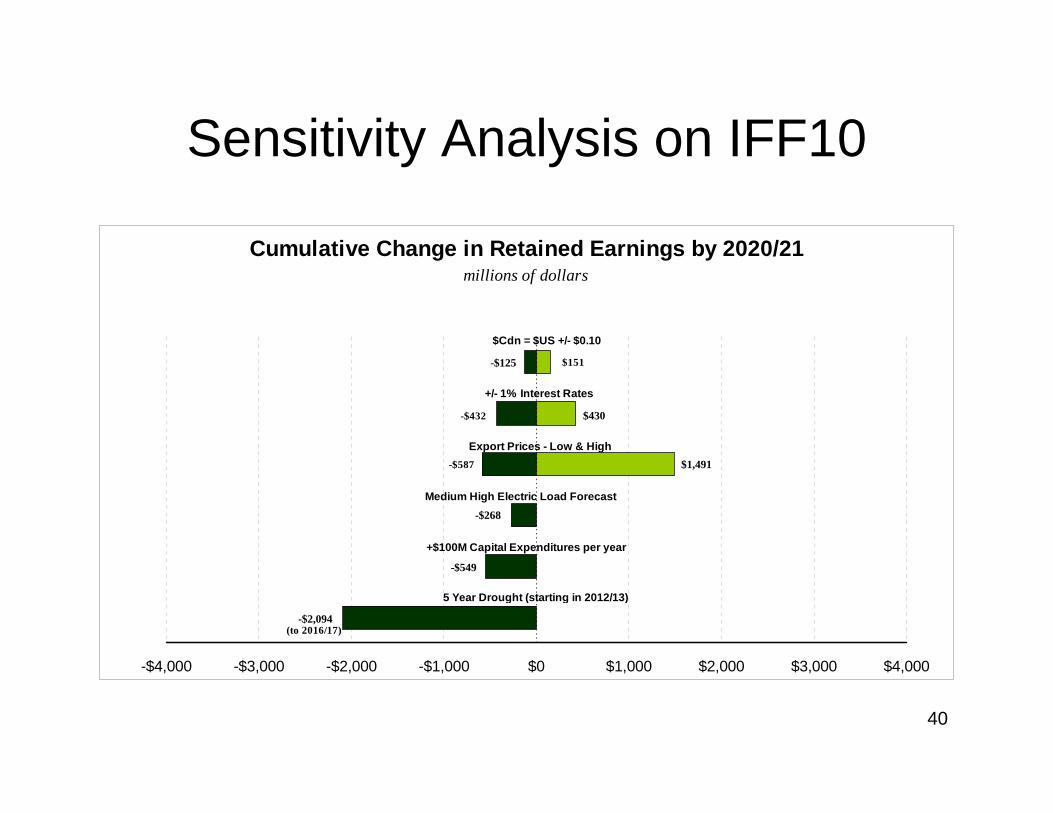

Sensitivity Analysis on IFF10

Cumulative Change in Retained Earnings by 2020/21millions of dollars

-$2,094

-$549

-$268

-$587 $1,491

-$432 $430

-$125 $151

-$4,000 -$3,000 -$2,000 -$1,000 $0 $1,000 $2,000 $3,000 $4,000

$Cdn = $US +/- $0.10

+/- 1% Interest Rates

Export Prices - Low & High

5 Year Drought (starting in 2012/13)

Medium High Electric Load Forecast

+$100M Capital Expenditures per year

(to 2016/17)

41

External Risk Reviews

• ICF• KPMG• PUB Independent Consultants

42

ICF Report Conclusions

• MH should be in the power export business based on the benefits provided to the ratepayers and the Province.

• Manitoba Hydro has developed sophisticated structures and capabilities to manage exports and hydro variability; these structures continue to develop and improve.

• MH has the lowest domestic electricity rates in Canada and North America in part because of exports. Export prices greatly exceed MH’s embedded generation costs, and the revenues are used to decrease domestic rates and/or to provide the financial wherewithal to withstand droughts without rate shocks.

43

ICF Report Conclusions (cont’d)

• Proposed new long-term contracts are expected to provide several types of benefits including lower MH rates than would otherwise be the case without the contracts.

• United States utilities are undertaking new transmission construction to facilitate MH exports. This export driven addition in new transmission can be used to support imports in the case of a drought worse than the worst-on-record.

• Hydroelectric development, combined with long-term firm contracts, is preferred for Manitoba as it avoids the risks involved in developing fossil power plants.

44

ICF Report Conclusions (cont’d)

• MH has a reasonable and adequate risk mitigation plan. Even in the event of a five-year drought, MH has plans to achieve an equity cushion sufficient to accommodate the reduced cash flow due to drought without having to raise rates.

• It is appropriate for MH to enter into long-term firm commitments for 20-30 years in the future in the manner in which MH is proposing.

• The prices proposed for long-term firm contracts appear reasonable and adequate, and MH pricing processes appear adequate.

45

ICF Report Conclusions (cont’d)

• The models used by MH (hydrological forecasting models) are similar to models used by other hydro-electric dependent companies.

• ICF considers MH’s quantification of risk exposure to drought to be reasonable.

• ICF concludes that MH’s risk mitigation strategy related to an extended drought is adequate, and helps meet a key goal of avoiding rate shocks.

46

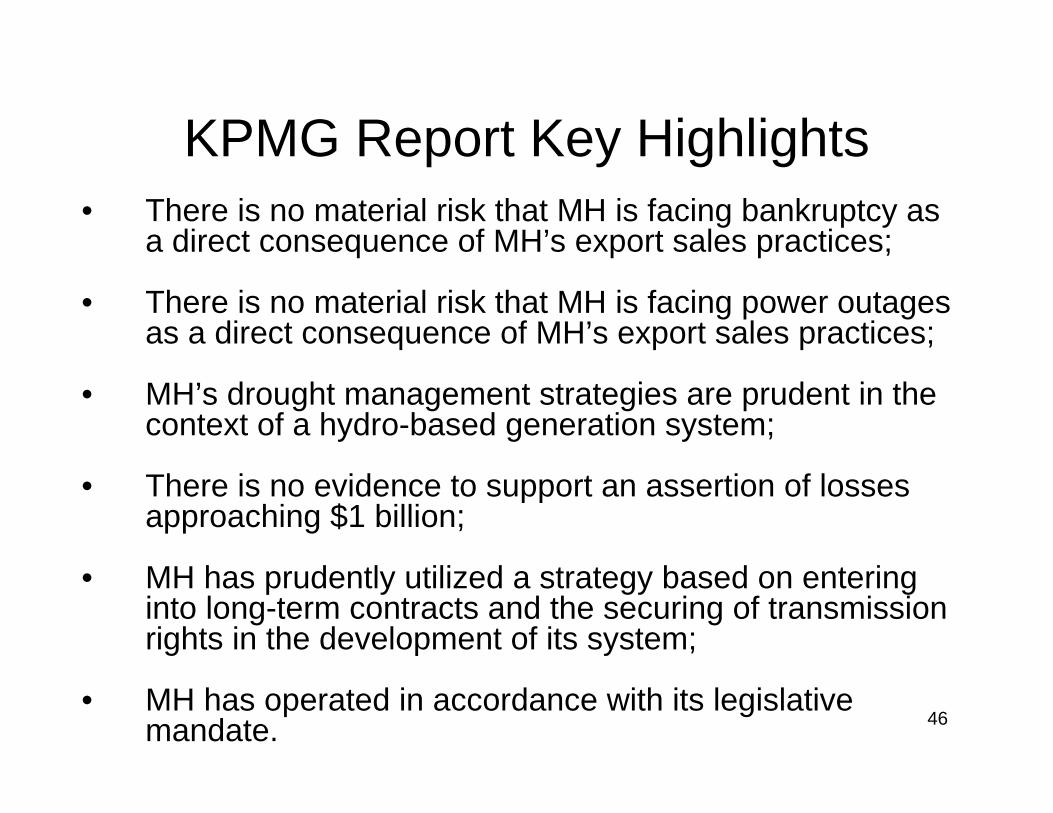

KPMG Report Key Highlights• There is no material risk that MH is facing bankruptcy as

a direct consequence of MH’s export sales practices;

• There is no material risk that MH is facing power outages as a direct consequence of MH’s export sales practices;

• MH’s drought management strategies are prudent in the context of a hydro-based generation system;

• There is no evidence to support an assertion of losses approaching $1 billion;

• MH has prudently utilized a strategy based on entering into long-term contracts and the securing of transmission rights in the development of its system;

• MH has operated in accordance with its legislative mandate.

47

IFRS

48

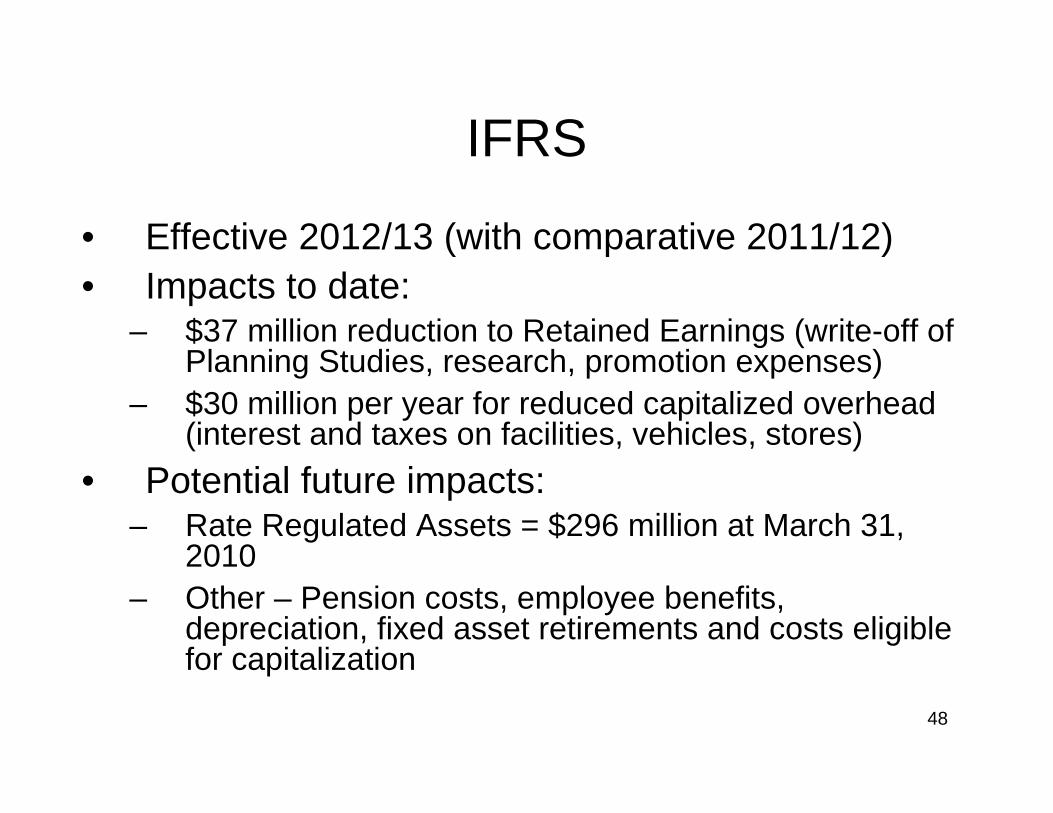

IFRS

• Effective 2012/13 (with comparative 2011/12)• Impacts to date:

– $37 million reduction to Retained Earnings (write-off of Planning Studies, research, promotion expenses)

– $30 million per year for reduced capitalized overhead (interest and taxes on facilities, vehicles, stores)

• Potential future impacts:– Rate Regulated Assets = $296 million at March 31,

2010– Other – Pension costs, employee benefits,

depreciation, fixed asset retirements and costs eligible for capitalization

49

Current Water Conditions

50

Historical Water Supply

0%

20%

40%

60%

80%

100%

120%

140%

160%

1920

1930

1940

1950

1960

1970

1980

1990

2000

2010

Fiscal Year Beginning

% o

f Ave

rage

2010/11

51

Daily Inflows

52

Total Energy in Reservoir StorageTotal Energy in Reservoir Storage

0

2

4

6

8

10

12

14

16

18

20

22

24

26

28

30

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan

Month

Ener

gy (T

Wh)

1977-2008 2009 Average 2010

18.81 TWh - Actual12.51 TWh - Average6.31 TWh - Above Average

53

Total Hydraulic Generation

Total Hydraulic Generation

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

1992/9

3199

3/9419

94/95

1995/96

1996

/97199

7/98

1998

/99199

9/00

2000

/01200

1/02

2002

/03200

3/04

2004

/0520

05/06

2006/07

2007/0

8200

8/0920

09/10

2010/11

Fiscal Year

Gen

erat

ion

(100

0's

GW

h)

Actual Forecast