presentation to the standing committee on finance the international financial market crisis errol...

TRANSCRIPT

Presentation to the Standing Presentation to the Standing Committee on FinanceCommittee on Finance

The International Financial The International Financial Market CrisisMarket Crisis

Presentation to the Standing Presentation to the Standing Committee on FinanceCommittee on Finance

The International Financial The International Financial Market CrisisMarket Crisis

Errol KrugerErrol Kruger

Registrar of BanksRegistrar of Banks

1 September 20101 September 2010

2

OutlineOutlineOutlineOutline

Run-up to the sub-prime market turmoil

What went wrong?What went wrong?

What complicated it?What complicated it?

What did South Africa do? – Key actions takenWhat did South Africa do? – Key actions taken

SA’s response to international supervisory developments SA’s response to international supervisory developments

Anticipated amendments to the bank legislative frameworkAnticipated amendments to the bank legislative framework

ConclusionConclusion

3

What is sub-prime lending?

– Loans granted to lower-end/sub-prime clients who ordinarily would not qualify.

– Higher interest rate charged for higher risk, often with initial low “teaser” rates – resetting after +/- 2 years.

– In extreme cases loans referred to as “Ninja” loans, i.e.:

– No income, jobs or assets.

Where did sub-prime lending occur?

– Predominantly in the United States.

Definition and characteristicsDefinition and characteristicsDefinition and characteristicsDefinition and characteristics

4

– Strong economic growth.– Low interest rates.– High levels of liquidity.– Investors looking for yield.– Buoyant financial markets.– Increasing asset prices.– Relaxing of credit granting standards.

Global economic environment prior Global economic environment prior to sub-prime turmoilto sub-prime turmoil

Global economic environment prior Global economic environment prior to sub-prime turmoilto sub-prime turmoil

5

US Housing marketUS Housing marketUS Housing marketUS Housing market

– Earlier years only fixed rate mortgages (FRMs).

– Introduction of Adjustable Rate Mortgages (ARMs) in 1980s.

– Shift from FRMs to ARMs resulted in rapid growth.

– 2001 – Sub-prime mortgages = 5% of market.

– 2/28 – Lending based on borrower’s ability to pay first 2 years at low “teaser” rates and not the remaining 28 years.

6

OutlineOutlineOutlineOutline

Run-up to the sub-prime market turmoilRun-up to the sub-prime market turmoil

What went wrong?

What complicated it?What complicated it?

What did South Africa do? – Key actions takenWhat did South Africa do? – Key actions taken

SA’s response to international supervisory developments SA’s response to international supervisory developments

Anticipated amendments to the bank legislative frameworkAnticipated amendments to the bank legislative framework

ConclusionConclusion

7

Developments in US during 2006Developments in US during 2006Developments in US during 2006Developments in US during 2006

– Housing market began to cool – housing prices began to decrease.

• Price declines not seen since 1940s.

• Sub-prime lending based on premise that housing prices would continue to increase.

– Sub-prime mortgages with “teaser” rates began to reset.

• Customers unable to meet higher payment obligations.

• Customers unable to refinance loans (negative equity).

– Rapid increase in non-performing sub-prime mortgage loans.

8

OutlineOutlineOutlineOutline

Run-up to the sub-prime market turmoilRun-up to the sub-prime market turmoil

What went wrong?What went wrong?

What complicated it?

What did South Africa do? – Key actions takenWhat did South Africa do? – Key actions taken

SA’s response to international supervisory developments SA’s response to international supervisory developments

Anticipated amendments to the bank legislative frameworkAnticipated amendments to the bank legislative framework

ConclusionConclusion

9

Impact of global economic Impact of global economic environmentenvironment

Impact of global economic Impact of global economic environmentenvironment

– High levels of liquidity and low interest rates resulted in low-yielding investments globally .

– Investors actively searching for better yielding assets.

– High-yielding US sub-prime mortgage market appeared attractive.

– US mortgage market responded to global investor requirements.

• Originate-to-distribute model.

• Asset securitisation, collaterised debt obligations (CDOs).

• Explosion period during 2001-2007.

• Return on securities in good times masked the problem.

• Role of rating agencies.

10

Linkage between sub-prime mortgages, Linkage between sub-prime mortgages, securitisation and CDOssecuritisation and CDOs

Linkage between sub-prime mortgages, Linkage between sub-prime mortgages, securitisation and CDOssecuritisation and CDOs

– Step 1

Origination of sub-prime mortgage loans.

– Step 2

Securitisation of sub-prime mortgages – mortgage-backed securities.

Securities are rated and sold to investors.

“Tranche”/grade Approximate breakdown

AAAAA 87%ABBB Investment grade

≤ BB - 6% Sub-investment grade

First loss - 7% Taken up by originator

11

Linkage between sub-prime mortgages, Linkage between sub-prime mortgages, securitisation and CDOs (cont.)securitisation and CDOs (cont.)

Linkage between sub-prime mortgages, Linkage between sub-prime mortgages, securitisation and CDOs (cont.)securitisation and CDOs (cont.)

– Step 3

Various “tranches” of lower grade mortgage-backed securities are repackaged, assigned ratings and sold off to conduits (structured investment vehicles – SIVs) as CDOs.

• SIVs attracted by high yields.

“Tranche”/grade

AAAAAABBB

12

Linkage between sub-prime mortgages, Linkage between sub-prime mortgages, securitisation and CDOs (cont.)securitisation and CDOs (cont.)

Linkage between sub-prime mortgages, Linkage between sub-prime mortgages, securitisation and CDOs (cont.)securitisation and CDOs (cont.)

– Step 4

Conduit (SIV) owns 5-year CDOs worth R1bn.

Equity R100m

Debt R900m (90 day funding)

Total R1bn (5-year CDOs)

Salient issues:

Long-dated paper funded by 90-day investments – liquidity risk, roll-overs.

13

Impact of defaulting sub-prime loans Impact of defaulting sub-prime loans on structured productson structured products

Impact of defaulting sub-prime loans Impact of defaulting sub-prime loans on structured productson structured products

– Increase in sub-prime loan defaults.

– Market loses confidence in ratings assigned to structured products backed by sub-prime loans.

– Re-financing of CDOs dried up.

• 90-day funding to overnight funding .

– Banks had to take assets/securities back on balance sheet.

– Inter-bank lending dried up and therefore banks obtained liquidity from central banks.

– End-effect is stricter mortgage lending criteria, leading to recession.

14

OutlineOutlineOutlineOutline

Run-up to the sub-prime market turmoilRun-up to the sub-prime market turmoil

What went wrong?What went wrong?

What complicated it?What complicated it?

What did South Africa do? – Key actions taken

SA’s response to international supervisory developments SA’s response to international supervisory developments

Anticipated amendments to the bank legislative frameworkAnticipated amendments to the bank legislative framework

ConclusionConclusion

15

Impact on South AfricaImpact on South AfricaImpact on South AfricaImpact on South Africa

– No direct impact from the first-round effects of the international financial market crisis due to various factors, including the following: • Banking sector not overly exposed to sophisticated, high-risk

securitisation schemes.

• Monetary policy well-implemented.

• Conservative regulatory framework and supervision (early implementation of Basel II and increase in regulatory capital requirement).

• Exchange control.

– However, the secondary effects of the turmoil impacted the South African economy as a whole (e.g. global economic slowdown impacting demand, production, exports, etc.).

– Impact exacerbated by cyclical factors prevalent in the domestic economy (e.g. high interest rates, inflationary pressures, increasing bad debt impairments, etc.).

16

Warning to banks in 2005/6: Stages Warning to banks in 2005/6: Stages of the banking cycleof the banking cycle

Warning to banks in 2005/6: Stages Warning to banks in 2005/6: Stages of the banking cycleof the banking cycle

17

Issues raised with banks in 2007Issues raised with banks in 2007Issues raised with banks in 2007Issues raised with banks in 2007

– Details of direct/indirect exposure to sub-prime market.

– List of securitisation schemes – funding details & recent reviews.

– Review of off-balance sheet activities.

– Details of third-party support to conduits – ALCO, stress testing, etc.

– Participation in geared/leveraged portfolios.

– Foreign funding – reliance thereon, roll-overs, changes in pricing etc.

18

– Banks had no direct exposure to sub-prime mortgage market.

– Traditional cash-backed securitisation schemes.

• Liquidity and capital management purposes.

– Banks acting as third-party liquidity providers – contingent liabilities included in ALCO processes .

– No behavioural change re foreign funding lines.

No alarms raised

Issues raised with banks in 2007 (cont.)Issues raised with banks in 2007 (cont.)Issues raised with banks in 2007 (cont.)Issues raised with banks in 2007 (cont.)

19

Meetings with chief executive officers and Meetings with chief executive officers and chairs of board risk committees (2008)chairs of board risk committees (2008)

Meetings with chief executive officers and Meetings with chief executive officers and chairs of board risk committees (2008)chairs of board risk committees (2008)

– Ongoing, regular communication, including meetings on a monthly basis, with the CEO’s and chairs of board risk committees to monitor developments in the respective banks and the banking sector in general.

– Department requested banks to continuously review positions and report back thereon.

• No adverse reports received.

20

Developments during April to September Developments during April to September 2008 and beyond2008 and beyond

Developments during April to September Developments during April to September 2008 and beyond2008 and beyond

– Review of banks’ securitisation schemes.

• Initial findings: nothing untoward observed .

– Subsequent to September 2008.

• Continuous monitoring of domestic and international developments and the impact thereof on the banking system.

• Ongoing interaction and close monitoring of South African banks, inter alia:

o Meetings with boards of directors and board sub-committees.

o Prudential meetings with senior management.

o Focussed on-site reviews (credit risk, market risk and operational risk).

o Thematic reviews (liquidity risk, interest rate risk, etc.)

21

BSD’s BSD’s interaction with the board / board interaction with the board / board sub-committeessub-committees

BSD’s BSD’s interaction with the board / board interaction with the board / board sub-committeessub-committees

– The key role and responsibilities of the board is recognised in the regulatory and supervisory framework applied by BSD.

– Focussed interaction with the board of directors and board sub-committees:

• Annual meeting with the board of each bank (presenting BSD’s perspective of the risk profile of the bank and discussion thereof).

• Annual meeting with the audit committee of each bank.

• Flavour of the year topics covered during meetings with the board and board sub-committees (focussing on key risks/issues):

o 1999 – (1) Y2K presentation and (2) Quantitative/qualitative risk assessment i.r.o. FX trading activities.

o 2000 – (1) Functioning of the audit committee and its role vis-à-vis the compliance function and (2) The role of collateral in credit risk management.

22

BSD’s BSD’s interaction with the board / board sub-interaction with the board / board sub-committees (cont.)committees (cont.)

BSD’s BSD’s interaction with the board / board sub-interaction with the board / board sub-committees (cont.)committees (cont.)

• Flavour of the year topics covered (cont.):

o 2001 – (1) Management of risk inherent in derivative activities and (2) The role of the compliance function.

o 2002 – (1) Overview of global co-ordinated group risk management and entrenchment of uniform risk management processes and (2) The effectiveness of operational risk management in the treasury environment and (3) Overview of the process of corporate governance.

o 2003 – (1) Strategy and plans for the implementation of Basel II.

o 2004 – (1) Discussion of the terms of reference , composition, functioning, interaction and key decisions of the audit committee, risk committee and directors’ affairs committee.

o 2005 – (1) Overview of liquidity risk management within the bank/banking group and (2) Overview of credit risk management with specific reference to the mortgage portfolio of the bank.

o 2006 – (1) Overview of business continuity management framework in respect of major business disruptions.

23

BSD’s BSD’s interaction with the board / board sub-interaction with the board / board sub-committees (cont.)committees (cont.)

BSD’s BSD’s interaction with the board / board sub-interaction with the board / board sub-committees (cont.)committees (cont.)

• Flavour of the year topics covered (cont.):

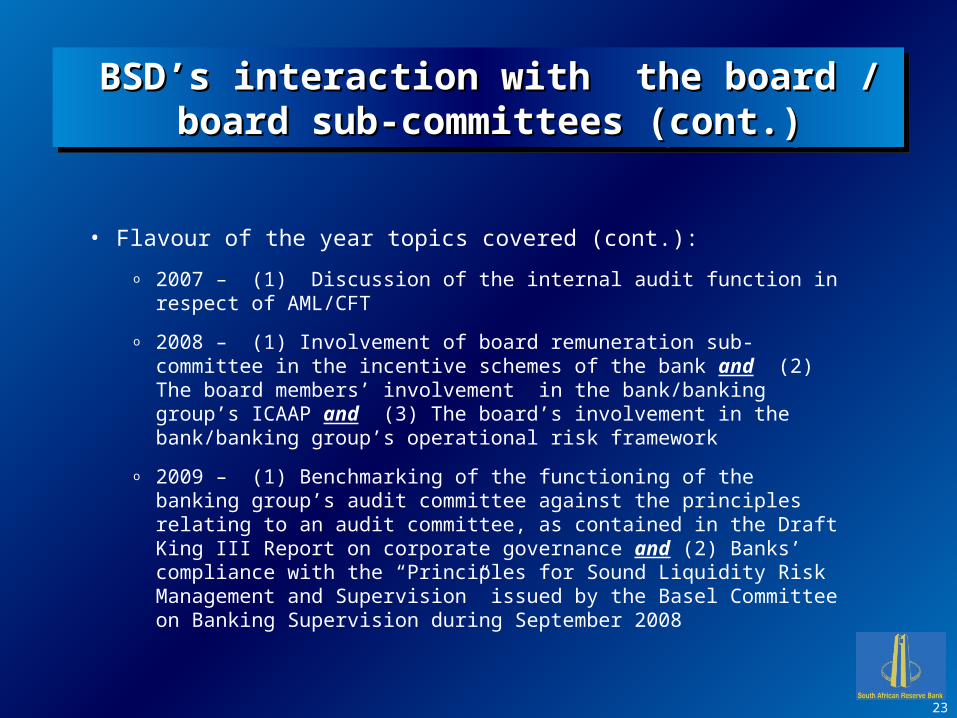

o 2007 – (1) Discussion of the internal audit function in respect of AML/CFT

o 2008 – (1) Involvement of board remuneration sub-committee in the incentive schemes of the bank and (2) The board members’ involvement in the bank/banking group’s ICAAP and (3) The board’s involvement in the bank/banking group’s operational risk framework

o 2009 – (1) Benchmarking of the functioning of the banking group’s audit committee against the principles relating to an audit committee, as contained in the Draft King III Report on corporate governance and (2) Banks’ compliance with the “Principles for Sound Liquidity Risk Management and Supervision” issued by the Basel Committee on Banking Supervision during September 2008

24

BSD’s BSD’s interaction with the board / board sub-interaction with the board / board sub-committees (cont.)committees (cont.)

BSD’s BSD’s interaction with the board / board sub-interaction with the board / board sub-committees (cont.)committees (cont.)

• Flavour of the year topics covered (cont.):

o 2010 – (1) A comprehensive presentation by the external and internal auditors and audit committee of banks on the key external and internal audit findings in respect of the latest financial year-end as brought to the attention of the audit committees; and

o 2010 – (2) A discussion of the key concerns regarding banks’ control environment as identified by the external and internal auditors; and

o 2010 – (3) A presentation by the chair persons of banks’ risk and capital management committees regarding the functioning of the said committees during the past year, including methodologies and practices followed to ensure compliance with regulatory requirements pertaining to such committees; and

o 2010 – (4) Consolidated supervision - A detailed discussion oin respect of the management and board oversight of the risks posed, and the controls instigated to mitigate the risks posed, by diversified banking groups.

25

OutlineOutlineOutlineOutline

Run-up to the sub-prime market turmoilRun-up to the sub-prime market turmoil

What went wrong?What went wrong?

What complicated it?What complicated it?

What did South Africa do? – Key actions takenWhat did South Africa do? – Key actions taken

SA’s response to international supervisory developments

Anticipated amendments to the bank legislative frameworkAnticipated amendments to the bank legislative framework

ConclusionConclusion

26

– International regulatory/supervisory standard-setting bodies (e.g.: the Financial Stability Board & the Basel Committee on Banking Supervision - BCBS), continued their respective processes of developing/issuing guidance and standards to strengthen the resilience of the financial sector in general and the banking sector in particular.

– The main thrust of regulatory/supervisory issues during the period 2008 to 2010 are those flowing from initiatives being undertaken by the BCBS in response to the global crisis.

– Key initiatives include the following:

• Strengthening banks’ capital base:o Raise the quality, consistency and transparency of the Tier 1 capital base

of banks/banking groups.o Introduce a framework for countercyclical capital buffers.o Assess the need for a capital surcharge to mitigate the risk of systemic

banks.

International regulatory developmentsInternational regulatory developments

27

– Key initiatives include the following (cont.):

• Strengthening the Basel II framework in the area of securitisation and trading book positions.

• Leverage ratio: introduce a leverage ratio as a supplementary measure to the Basel II risk-based framework.

• Liquidity: introduce a minimum global standard for funding liquidity, which includes a stressed liquidity coverage ratio requirement.

• Systemic risk: Recommendations to reduce the systemic risk associated with resolution of cross border banks.

• Provisioning: promote forward-looking provisions based on expected losses.

• Align compensation practices with long-term performance and prudent risk-taking.

International regulatory developments (cont.)

International regulatory developments (cont.)

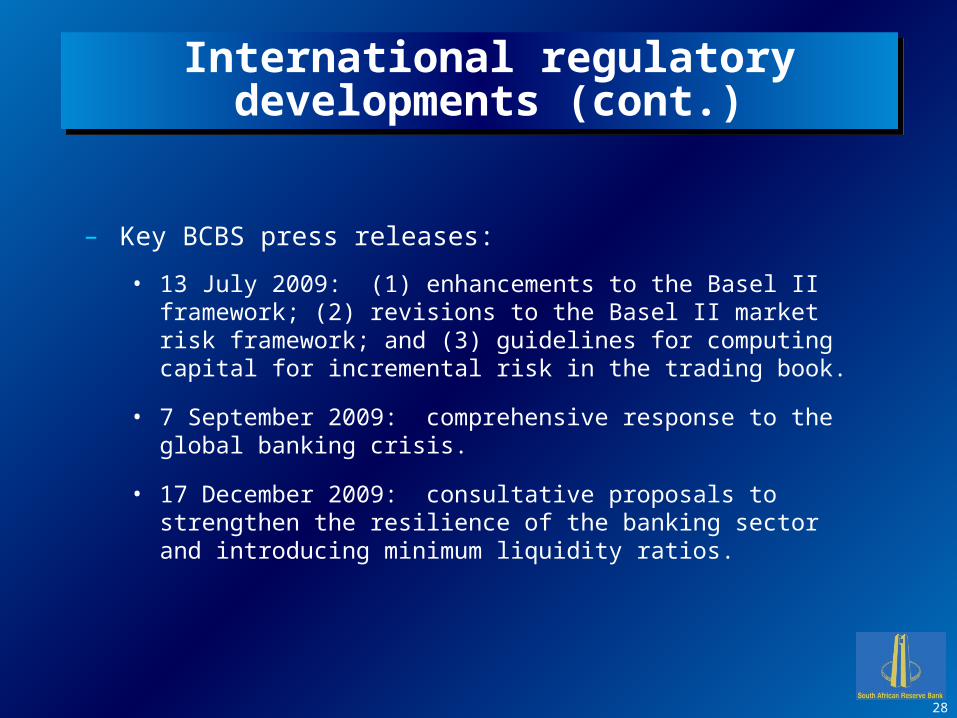

– Key BCBS press releases:

• 13 July 2009: (1) enhancements to the Basel II framework; (2) revisions to the Basel II market risk framework; and (3) guidelines for computing capital for incremental risk in the trading book.

• 7 September 2009: comprehensive response to the global banking crisis.

• 17 December 2009: consultative proposals to strengthen the resilience of the banking sector and introducing minimum liquidity ratios.

28

International regulatory developments (cont.)

International regulatory developments (cont.)

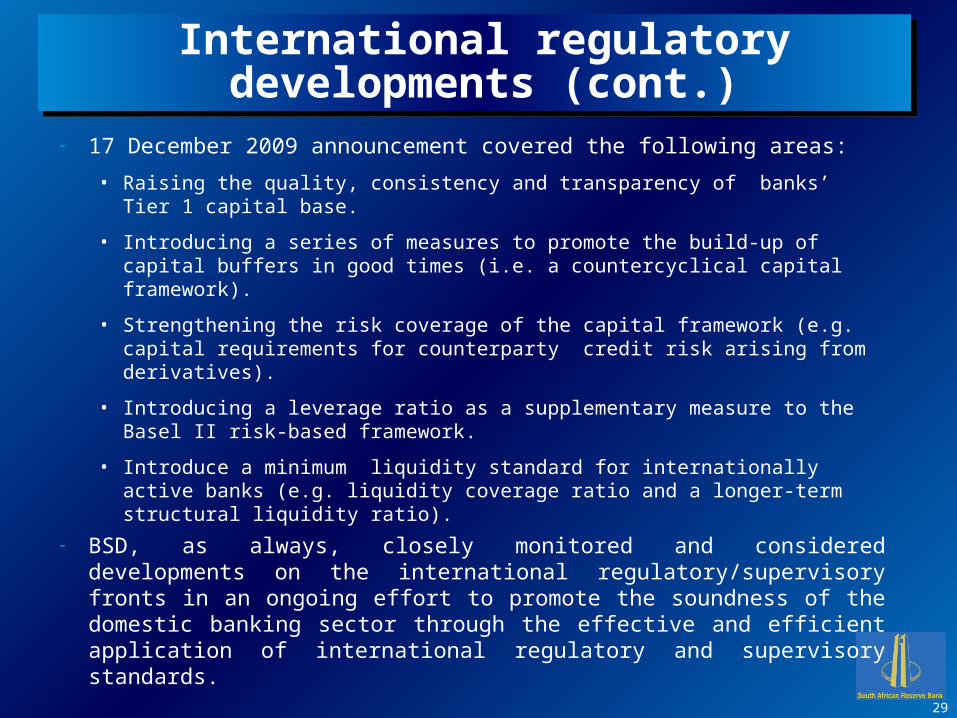

– 17 December 2009 announcement covered the following areas:

• Raising the quality, consistency and transparency of banks’ Tier 1 capital base.

• Introducing a series of measures to promote the build-up of capital buffers in good times (i.e. a countercyclical capital framework).

• Strengthening the risk coverage of the capital framework (e.g. capital requirements for counterparty credit risk arising from derivatives).

• Introducing a leverage ratio as a supplementary measure to the Basel II risk-based framework.

• Introduce a minimum liquidity standard for internationally active banks (e.g. liquidity coverage ratio and a longer-term structural liquidity ratio).

– BSD, as always, closely monitored and considered developments on the international regulatory/supervisory fronts in an ongoing effort to promote the soundness of the domestic banking sector through the effective and efficient application of international regulatory and supervisory standards.

29

International regulatory developments (cont.)

International regulatory developments (cont.)

30

SA’s responseSA’s response

Capital:

– Prescribed minimum primary capital adequacy ratio of 7% (internationally currently 4%).

– Predominant form of banking sector primary capital is common shares and retained (formally appropriated) reserves.

– SA did not allow hybrid instruments to the same extent as its international counterparts.

• Strict qualifying criteria apply.

• May not exceed 25% of total Tier 1 capital.

– Discussions with CEO’s of 6 largest SA banks early in 2009 – focussed effort by banks to further improve capital levels and quality:

• Banking sector primary capital adequacy ratio as at June 2010 was 11,2% (June 2009: 10,7%).

• Banking sector total capital adequacy ratio as at June 2010 was 14,3% (June 2009 : 13,7%).

31

Capital (cont.):

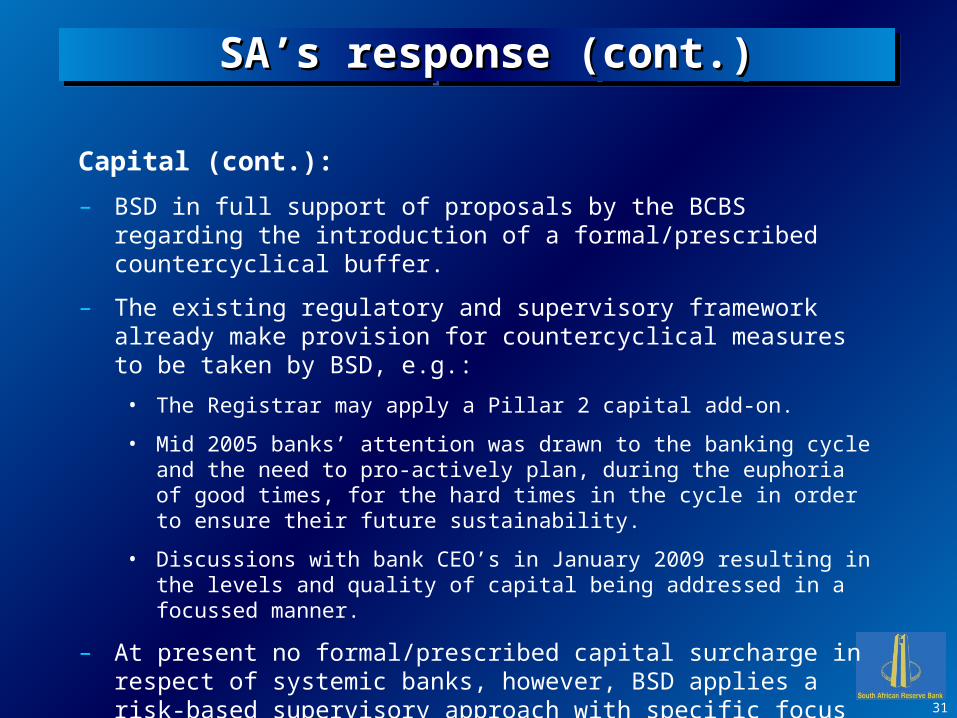

– BSD in full support of proposals by the BCBS regarding the introduction of a formal/prescribed countercyclical buffer.

– The existing regulatory and supervisory framework already make provision for countercyclical measures to be taken by BSD, e.g.:

• The Registrar may apply a Pillar 2 capital add-on.

• Mid 2005 banks’ attention was drawn to the banking cycle and the need to pro-actively plan, during the euphoria of good times, for the hard times in the cycle in order to ensure their future sustainability.

• Discussions with bank CEO’s in January 2009 resulting in the levels and quality of capital being addressed in a focussed manner.

– At present no formal/prescribed capital surcharge in respect of systemic banks, however, BSD applies a risk-based supervisory approach with specific focus on systemically relevant banks.

SA’s response (cont.)SA’s response (cont.)SA’s response (cont.)SA’s response (cont.)

32

Strengthening the Basel II framework:

– BSD in full support of the guidelines by the BCBS regarding the strengthening of the Basel II framework in the areas of securitisation and trading book positions.

– Amendments to regulatory and supervisory framework that are required to give effect to the enhancements to the Basel II framework are being considered.

SA’s response (cont.)SA’s response (cont.)SA’s response (cont.)SA’s response (cont.)

33

Leverage ratio (multiple):

– Monitoring of banks’ leverage ratio introduced as part of the revised supervisory review and evaluation process subsequent to the implementation of Basel II.

– South African banking sector leveraged between 15 and 20 times (as at June 2010: 15,4 times).

– In comparison, many large global banking institutions are leveraged in excess of 30 times, and as high as 60 times.

SA’s response (cont.)SA’s response (cont.)SA’s response (cont.)SA’s response (cont.)

Leverage multiple formula:

Total liabilities and equity divided by total equity attributable to shareholders.

34

Stressed liquidity coverage ratio:

– Liquidity risk management formed the basis of the BSD’s discussions with the boards of directors of banks during 2009.

– Thematic reviews covering liquidity risk management have been performed at various banks.

– Liquidity simulation exercise already performed certain of the large banks – remainder of the large banks to be focussed on during 2010.

– Should BSD be concerned about liquidity risk management or the level of liquidity risk exposure of a particular bank a Pillar 2(b) add-on may be applied.

– NOTE: Proposals by the BCBS relating to an international framework for liquidity risk standards expected to have a potential material impact on SA owing to structural peculiarities of the SA financial system (e.g. low retail savings, short-term nature of funding, etc.).

SA’s response (cont.)SA’s response (cont.)SA’s response (cont.)SA’s response (cont.)

35

Systemic risk – cross-border banks:

– BSD has regular interaction with regulators/supervisors in key financial jurisdictions.

– MOU’s in place with regulators in key financial jurisdictions.

– SA is represented on the BCBS (and certain sub-committees, working groups), the Financial Stability Board and the G-20.

SA’s response (cont.)SA’s response (cont.)SA’s response (cont.)SA’s response (cont.)

36

Promote forward-looking provisions based on expected losses :

–Provisioning in terms of Basel II already forward-looking.

–This measure is mainly related to IFRS provisioning, of which SAICA forms part of the international forum.

SA’s response (cont.)SA’s response (cont.)SA’s response (cont.)SA’s response (cont.)

37

Compensation practices:

– Compensation practices of banks thoroughly reviewed and discussed with board remuneration committees of banks during 2008 based on a format similar to what is now being proposed by international standard-setters.

– SA banks requested to complete a self-assessment based on the compensation guidance issued by the Financial Stability Board and findings of the assessment will be followed up with banks on a business-as-usual basis.

SA’s response (cont.)SA’s response (cont.)SA’s response (cont.)SA’s response (cont.)

38

OutlineOutlineOutlineOutline

Run-up to the sub-prime market turmoilRun-up to the sub-prime market turmoil

What went wrong?What went wrong?

What complicated it?What complicated it?

What did South Africa do? – Key actions takenWhat did South Africa do? – Key actions taken

SA’s response to international supervisory developments SA’s response to international supervisory developments

Anticipated amendments to the bank legislative framework

ConclusionConclusion

39

Anticipated legislative framework Anticipated legislative framework amendments (cont.)amendments (cont.)

Anticipated legislative framework Anticipated legislative framework amendments (cont.)amendments (cont.)

– Key issues emerging from G-20 working groups, BCBS, Financial Stability Board, FSAP assessments of SA, thus far, should not require material amendments to the Banks Act, 1990.

– However, various amendments to the Regulations relating to Banks will be required.

– Key areas of focus w.r.t. future amendments to the Regulations include the following:

– Macroprudential framework:

• Procyclicality and countercyclical buffers.

• Mitigation of risks related to systemically important banks.

• Strengthening of the cross border bank resolution framework.

– Capital framework:

• Risk coverage of the Basel II framework:

o Banks’ trading books, off-balance-sheet exposures, securitisation, re-securitisation.

• Definition of capital.

• Leverage ratio.

– Funding liquidity framework:

• Global funding liquidity standard.

• Home/host cooperation.

4040

Anticipated legislative framework Anticipated legislative framework amendments (cont.)amendments (cont.)

Anticipated legislative framework Anticipated legislative framework amendments (cont.)amendments (cont.)

– Basel II capital framework enhancements:

• Pillar 1: minimum capital requirement:

o Trading book rules (market risk and guidelines for incremental risk):

– Higher capital requirements to capture the credit risk of complex trading activities.

– Include a stressed VaR requirement.

o Strengthening the treatment for certain securitisations:

– Higher risk weights for resecuritisation exposures (so-called CDOs of ABS).

o Raising the credit conversion factor for short-term liquidity facilities.

4141

Anticipated legislative framework Anticipated legislative framework amendments (cont.)amendments (cont.)

Anticipated legislative framework Anticipated legislative framework amendments (cont.)amendments (cont.)

– Basel II capital framework enhancements (cont.)

• Supplemental guidance under Pillar 2 (the supervisory review process - SREP)

o Addresses the flaws in risk management practices revealed by the crisis.

o It raises the standards for:

– Firm-wide governance and risk management.

– Capturing the risk of off-balance sheet exposures and securitisation activities.

– Managing risk concentrations.

– Providing incentives for banks to better manage risk and returns over the long term.

• Includes enhancements to Pillar 3 (market discipline):o Strengthens disclosure requirements for securitisations, off-balance

sheet exposures and trading activities.

4242

Anticipated legislative framework Anticipated legislative framework amendments (cont.)amendments (cont.)

Anticipated legislative framework Anticipated legislative framework amendments (cont.)amendments (cont.)

– Proposed amendments to the Regulations relating to Proposed amendments to the Regulations relating to Banks –Banks –Draft 1Draft 1:: essentially incorporated the amended essentially incorporated the amended Basel II requirements published by the BCBS on 13 July Basel II requirements published by the BCBS on 13 July 2009 namely:2009 namely:

• Enhancements to the Basel II framework.Enhancements to the Basel II framework.

• Revisions to the Basel II market risk framework.Revisions to the Basel II market risk framework.

• Guidelines for computing capital for incremental risk in the Guidelines for computing capital for incremental risk in the trading book.trading book.

43

Anticipated legislative framework Anticipated legislative framework amendments (cont.)amendments (cont.)

Anticipated legislative framework Anticipated legislative framework amendments (cont.)amendments (cont.)

– Proposed amendments to the Regulations relating to Proposed amendments to the Regulations relating to Banks – Banks – Draft 2Draft 2: the proposed amendments relate mainly : the proposed amendments relate mainly to:to:

• Comments received in respect of draft 1.Comments received in respect of draft 1.

• Financial returns.Financial returns.

• Credit risk returns.Credit risk returns.

• Securitisation and resecuritisation returns.Securitisation and resecuritisation returns.

• Leverage multiple or ratio.Leverage multiple or ratio.

• Corporate governance.Corporate governance.

44

Anticipated legislative framework Anticipated legislative framework amendments (cont.)amendments (cont.)

Anticipated legislative framework Anticipated legislative framework amendments (cont.)amendments (cont.)

– Future drafts to be issued:Future drafts to be issued:

• Comments received in respect of draft 2, etc.Comments received in respect of draft 2, etc.

• Market riskMarket risk

• Consolidated supervisionConsolidated supervision

o Off-shore operationsOff-shore operations

o Related party exposuresRelated party exposures

• Economic returnsEconomic returns

o New returns – IMF studies and questionnaires New returns – IMF studies and questionnaires

• Further pronouncements of the Basel CommitteeFurther pronouncements of the Basel Committee

• IMF/World Bank ROSC ReportIMF/World Bank ROSC Report

• Various policy related mattersVarious policy related matters

45

Anticipated legislative framework Anticipated legislative framework amendments (cont.)amendments (cont.)

Anticipated legislative framework Anticipated legislative framework amendments (cont.)amendments (cont.)

46

OutlineOutlineOutlineOutline

Run-up to the sub-prime market turmoilRun-up to the sub-prime market turmoil

What went wrong?What went wrong?

What complicated it?What complicated it?

What did South Africa do? – Key actions takenWhat did South Africa do? – Key actions taken

SA’s response to international supervisory developments SA’s response to international supervisory developments

Anticipated amendments to the bank legislative frameworkAnticipated amendments to the bank legislative framework

Conclusion

ConclusionConclusionConclusionConclusion

– The BSD proposes to implement one comprehensive set of The BSD proposes to implement one comprehensive set of proposed amended Regulations, on 1 January 2012, that will proposed amended Regulations, on 1 January 2012, that will incorporate:incorporate:• the package released by the Basel Committee on 13 July 2009, the package released by the Basel Committee on 13 July 2009,

as amended;as amended;

• all comments received from banks and other interested persons all comments received from banks and other interested persons on the draft documents released for comment;on the draft documents released for comment;

• further finalised documents or pronouncements of the Basel further finalised documents or pronouncements of the Basel Committee; andCommittee; and

• further or improved requirements, corrections and refinements:further or improved requirements, corrections and refinements:o BSD policy process.BSD policy process.o IMF/ World Bank ROSC Report.IMF/ World Bank ROSC Report.o Other SARB Departments.Other SARB Departments.

47

– Certain work streams of the G20; FSB; BCBS and the IASB, Certain work streams of the G20; FSB; BCBS and the IASB, impacting the regulatory framework, are set to continue impacting the regulatory framework, are set to continue during 2011 and 2012.during 2011 and 2012.• Further proposals, where necessary and relevant for SA, will be Further proposals, where necessary and relevant for SA, will be

incorporated during the next round of amendments to the incorporated during the next round of amendments to the Regulations.Regulations.

• Expected implementation date of next round of amendments: Expected implementation date of next round of amendments: earliestearliest 1 January 2013. 1 January 2013.

– Note: internationally agreed precondition:Note: internationally agreed precondition:• Further proposals not to impede the recovery of the real Further proposals not to impede the recovery of the real

economy.economy.

48

Conclusion (cont.)Conclusion (cont.)Conclusion (cont.)Conclusion (cont.)

49

Thank you Thank you