presentazione standard di powerpoint -...

TRANSCRIPT

21° Convegno della Sezione Componentistica ANIMP, 24

novembre 2015 1

Attachments

SEZIONE COMPONENTISTICA D’IMPIANTO ANIMP

2

Index:

LNG - Liquefaction Regasification Midstream Pipelines

Market trends : Oil & Gas Midstream

SEZIONE COMPONENTISTICA D’IMPIANTO ANIMP

3

Market Trends : LNG - Liquefaction

Outlook

• Global liquefaction capacity MTPA:

• Current: 289

• Expected in 2025 : 450 MTPA

• Huge list of proposed projects but high % of mortality due to:

• LNG demand increase over the next 10 years: less than 100 MTPA

• Risk of over-supply vs announced capacity increase - decrease of

LNG purchasing price in Far East

• Fall in oil & gas prices and overrun on recent megaprojects

• Stringent environment regulations/conflicts with local communities

• Financial weakness of some investors

• 2020 Asia Pacific (in particular Australia), Middle East and North

• Medium term capacity increase: mostly from Australia and US

• New large-scale plants in Canada and East Africa: between

2020-2025

SEZIONE COMPONENTISTICA D’IMPIANTO ANIMP

4

Market Trends : LNG - Liquefaction Overview by geographical area

Asia - Pacific • strongest CAPEX driver during the last few years • Australia:

• Project under construction: 50 MTPA increase by 2018

• High cost escalation – less attractiveness of future projects-no further capacity increase

North America • Largest worldwide Capex driver - expected growth (90

MTPA) between 2014 and 2025 • 5 major onshore liquefaction projects under

construction • More than 40 proposed projects (over 600 MTPA) but

only 15% expected in production by 2025 due to: • Reduced price differentials with oil – companies

announcing spending cuts • Market potentially over supplied • Construction cost/time for greenfield projects • Heavy environment regulations and conflicts with

local communities (Canada) • Significant pipeline infrastructure needed (Canada)

Africa • Significant gas resources in Mozambique/Tanzania • Large scale LNG expected between 2020-2025

(Mozambique) • Risks of executing large-scale projects:

• Undeveloped countries • Lack of infrastructure

Middle East • No more the largest liquefaction capacity area after

2020 • Expected 19% vs 33% of AsiaPacific and 20% of North

America

Russia • Significant gas resources close to Asian markets • LNG export liberalization in 2013 • Sanctions against Russia:

• Difficulties in finding partners/off takers/financing • Potential escalation: risk of sanctions on LNG

technology

• Gas pipelines development: often a better alternative • July 2015 statement: Vladivostok LNG no more a

priority

15%

20%

SEZIONE COMPONENTISTICA D’IMPIANTO ANIMP

5

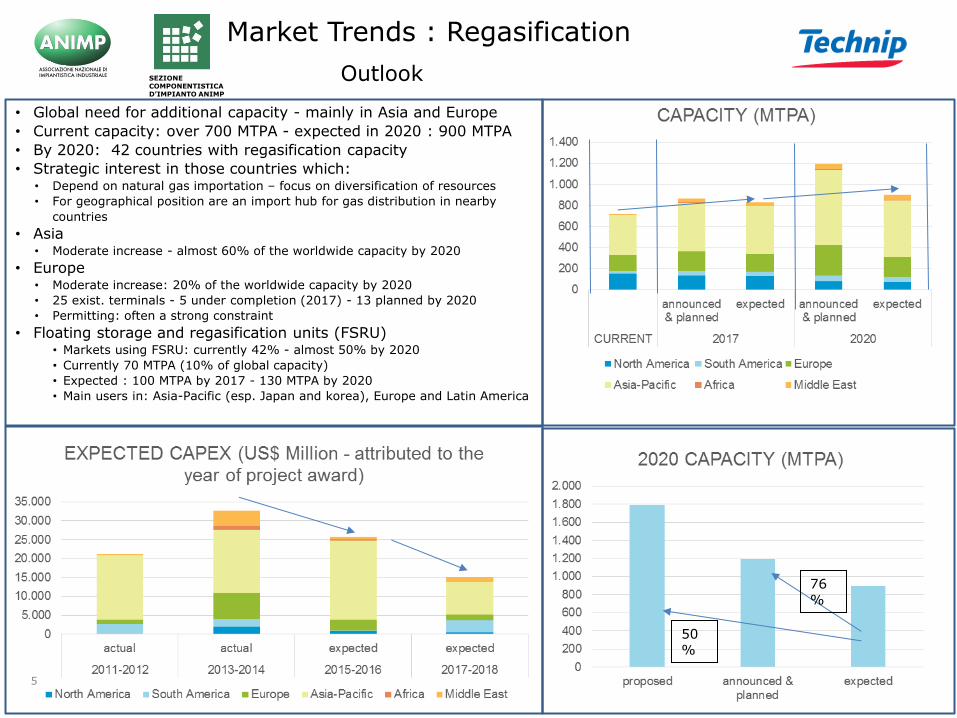

Market Trends : Regasification

Outlook

• Global need for additional capacity - mainly in Asia and Europe

• Current capacity: over 700 MTPA - expected in 2020 : 900 MTPA

• By 2020: 42 countries with regasification capacity

• Strategic interest in those countries which: • Depend on natural gas importation – focus on diversification of resources

• For geographical position are an import hub for gas distribution in nearby

countries

• Asia • Moderate increase - almost 60% of the worldwide capacity by 2020

• Europe • Moderate increase: 20% of the worldwide capacity by 2020

• 25 exist. terminals - 5 under completion (2017) - 13 planned by 2020

• Permitting: often a strong constraint

• Floating storage and regasification units (FSRU) • Markets using FSRU: currently 42% - almost 50% by 2020

• Currently 70 MTPA (10% of global capacity)

• Expected : 100 MTPA by 2017 - 130 MTPA by 2020

• Main users in: Asia-Pacific (esp. Japan and korea), Europe and Latin America

50%

76%

SEZIONE COMPONENTISTICA D’IMPIANTO ANIMP

6

Long terms: 2010-2040:

• global energy demand: expected 35% increase

• natural gas: 65% share of energy mix

• above trend driven by:

– non-OECD countries demand growth and technology advancements (e.g.in liquefied natural gas)

– investment in new infrastructure to support LNG and unconventional gas developments

Short terms: 2015 – 2018:

• limited growth due to:

– significant fall in oil prices

– lower-than-expected economic growth in Asia - unconventional production slowdown in North America

– progress of planned pipeline projects often affected by environmental and geopolitical issues

• onshore pipeline expenditure: US$170b between 2015 - 2018 vs $155b between 2011-2014 - increase limited to 10%

• 115,000 kilometers (km) of new oil and gas pipeline to be built between 2015-2018

• major investors: Gazprom, CNPC, TransCanada, Enbridge and Kinder Morgan

Market Trends : Midstreastream Pipelines

Outlook

SEZIONE COMPONENTISTICA D’IMPIANTO ANIMP

7

Market Trends : Midstreastream Pipelines

Overview by geographical Area

• EMEA: (Europe, Russia & former Soviet Union, except Turkmenistan, Kazakhstan and

Uzbekistan, Middle East and Africa):

• longest Oil and Gas Pipeline additions: 58,981 km of new pipelines (41% of the total

global planned) by 2018

• in Europe:

– new pipeline projects to provide access to natural gas from the Caspian and

Central Asia

– driving factor: diversification of gas sources to avoid over-dependence on Russian

gas supplies

– constraining factor: local communities negative attitude/permitting

• Americas (North America, South and Central America):

• 46,400 Km of new pipelines by 2018 ( 32% of the total global planned)

• In North America:

– driving factor: unconventional production growth

– constraining factor: local communities negative attitude/permitting

• Asia-Pacific:

• 39,321 km of new pipelines by 2018 (27% of the total global planned) - 87%

gas pipelines

• most of these, gas pipelines to be constructed in India, Georgia, China

(15.000km) and Australia.

• driving factor: need to secure energy for developing economies with rapidly

growing energy consumption

10%

21°Convegno Annuale Sezione

Componentistica d’Impianto ANIMP

STRATEGIE E PREVISIONI DI MERCATO

PER LA FILIERA DELL’IMPIANTISTICA INDUSTRIALE

“PACKAGES” PER L’IMPIANTISTICA:

UN COMPARTO AD ALTO POTENZIALE

SEZIONE COMPONENTISTICA D’IMPIANTO ANIMP

Grand Hotel Villa Torretta, Sesto

S.G. (Milano)

24 novembre 2015

MARKET TRENDS : PETROCHEMICALS

Dario Pirovano Senior Advisor Business Development

World Polymer Demand

Polyethylene (PE) - Global Demand

Polyethylene (PE) - Additional Production / Capacity

Polypropylene (PP) - Global Demand

Polypropylene (PP) - Additional Production / Capacity

Market Outlook

21° Convegno Sezione Componentistica ANIMP, 24 novembre 2015

21° Convegno Sezione

Componentistica ANIMP, 24

novembre 2015

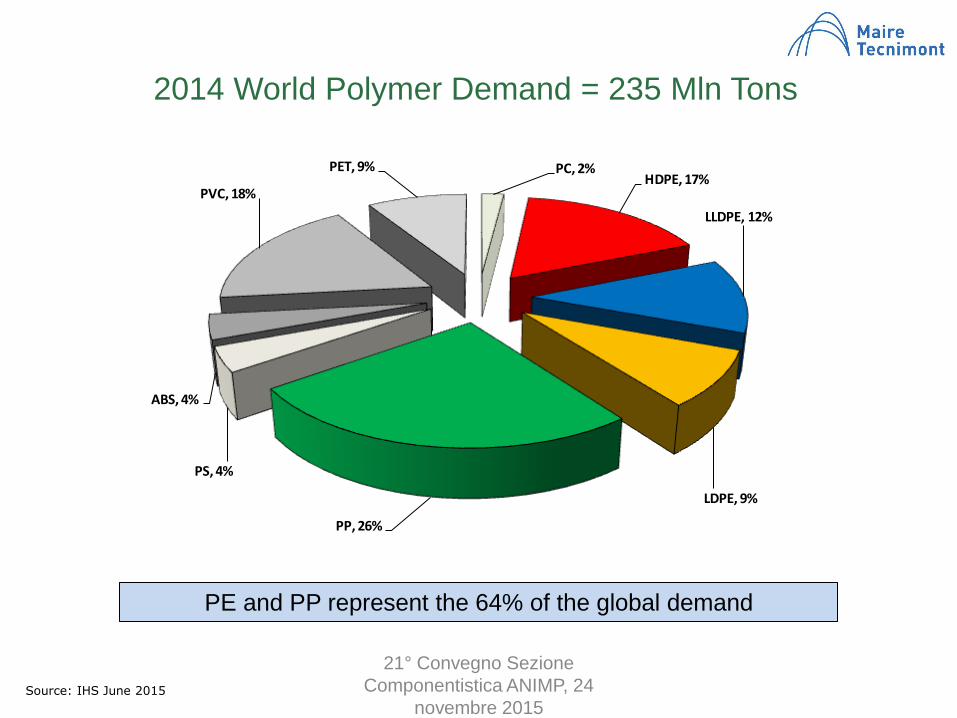

2014 World Polymer Demand = 235 Mln Tons

Source: IHS June 2015

PC, 2%HDPE, 17%

LLDPE, 12%

LDPE, 9%

PP, 26%

PS, 4%

ABS, 4%

PVC, 18%

PET, 9%

PE and PP represent the 64% of the global demand

21° Convegno Sezione

Componentistica ANIMP, 24

novembre 2015

Polyethylene (PE) – Global Demand

SOUTHEAST ASIA, 8%

AFRICA ME, 11%

INDIAN SUBCON, 5%

NAM, 18%

SAM, 6%EUR, 19%

NORTH EAST ASIA, 33%

2014 Global Demand : 84.7 mln tons

SOUTHEAST ASIA, 8%

AFRICA ME, 11%

INDIAN SUBCON, 6%

NAM, 17%

SAM, 6%EUR, 16%

NORTH EAST ASIA, 36%

2019 Global Demand: 105.7 mln tons

Source: IHS June 2015

Area CAGR

SOUTHEAST ASIA 4.5%

AFRICA ME 4.5%

INDIAN SUBCON 8.4%

NAM 3.3%

SAM 4.5%

EUR 1.0%

NORTH EAST ASIA 6.4%

Global Average 4.7%

21° Convegno Sezione

Componentistica ANIMP, 24

novembre 2015

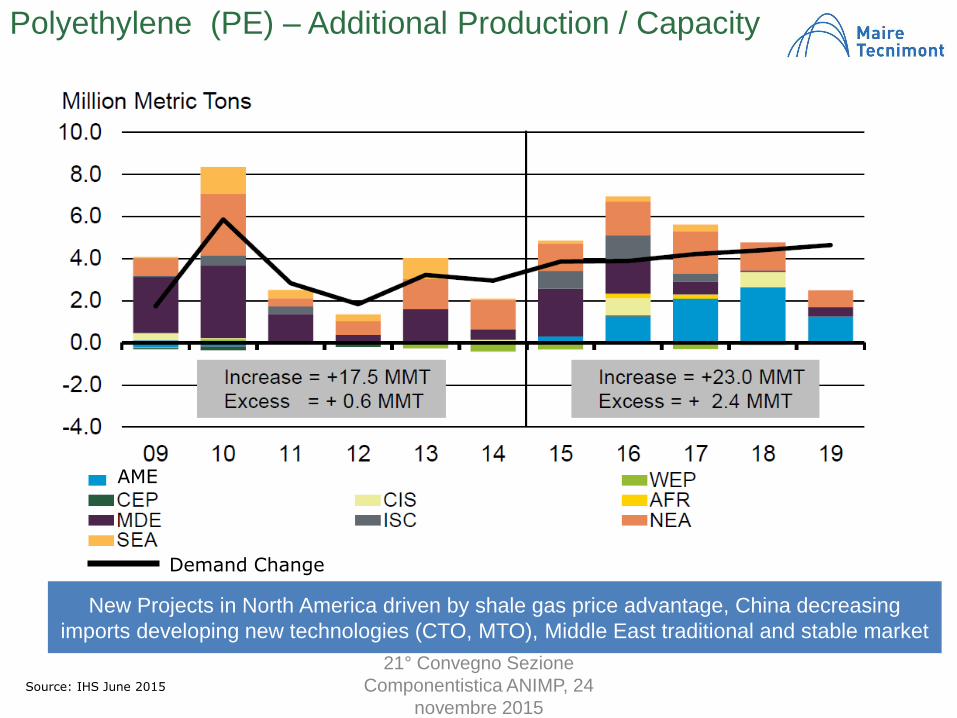

Polyethylene (PE) – Additional Production / Capacity

Source: IHS June 2015

Demand Change

AME

New Projects in North America driven by shale gas price advantage, China decreasing

imports developing new technologies (CTO, MTO), Middle East traditional and stable market

21° Convegno Sezione

Componentistica ANIMP, 24

novembre 2015

Polypropylene (PP) – Global Demand

Source: IHS June 2015

China, 33%

NE Asia, 7%

SE Asia, 8%NAM, 12%

SAM, 5%

EUR, 18%

MDE AFRICA, 10%

INDIAN SUBCON, 7%

China, 37%

NE Asia, 7%

SE Asia, 8%

NAM, 11%

SAM, 4%

EUR, 15%

MDE AFRICA, 10%

INDIAN SUBCON, 8%

2014 Global Demand : 58.8 mln tons 2019 Global Demand: 75.1 mln tons

Area CAGR

China 7.45%

NE Asia 5.02%

SE Asia 5.02%

NAM 3.20%

SAM 0.43%

EUR 1.25%

MDE AFRICA 5.02%

INDIAN SUBCON 7.86%

Global Average 4.40%

21° Convegno Sezione

Componentistica ANIMP, 24

novembre 2015

Polypropylene (PP) - Additional Production / Capacity

Source: IHS June 2015

New Projects mainly in China; CIS to growth in PP market; Middle East facing shortage of

ethane

PP AND PE DEMAND EXPECTED TO GROW 4.4% AND 4.7% PER YEAR RESPECTIVELY, MUCH

HIGHER THAN WORLD GDP GROWTH (3.6% IN 2016)

START UP IN 2015-2017 OF NEW PLANTS IN USA, CHINA, RUSSIA AND MIDDLE EAST WILL ADD

SIGNIFICANTLY INSTALLED CAPACITY ( SHALE GAS IN USA, COAL AND PDH IN CHINA,

TRADITIONAL FEEDSTOCK IN ME)

NEW INVESTMENTS UNCERTAIN DUE TO :

TEMPORARY OVER CAPACITY TILL 2017

SLOW DOWN OF ECONOMY GROWTH IN CHINA (MAJOR CONSUMER) AND OIL

PRODUCING COUNTRIES (CIS, BRAZIL, MIDDLE EAST) SUFFERING SHORTAGE OF CASH

FOR LOW OIL PRICE

POLITICAL INSTABILITY IN MENA

EFFECT OF SANCTIONS IN RUSSIA AND IRAN

IN THE SHORT/MEDIUM TERMS NEW PROJECTS IN COUNTRIES OF RELATIVELY NEW

PETROCHEMICAL INDUSTRIALIZATION SUCH AS OMAN, MALAYSIA, AZERBAIJAN,

KAZAKHSTAN, AND NEW EMERGING MARKETS IN SOUTH AMERICA AND AFRICA

SOME OPPORTUNITIES OF NEW PROJECTS IN EUROPE AS REPLACEMENT OR

MODERNIZATION OF OLD PLANTS

IN MEDIUM LONG TERM SECOND WAVE OF NEW PETROCHEMICAL PROJECTS IN USA, RUSSIA

AND CHINA

21° Convegno Sezione

Componentistica ANIMP, 24

novembre 2015

MARKET OUTLOOK

21°Convegno Annuale

Sezione Componentistica d’Impianto ANIMP

STRATEGIE E PREVISIONI DI MERCATO

PER LA FILIERA DELL’IMPIANTISTICA INDUSTRIALE

“PACKAGES” PER L’IMPIANTISTICA:

UN COMPARTO AD ALTO POTENZIALE

SEZIONE COMPONENTISTICA D’IMPIANTO ANIMP

Grand Hotel Villa Torretta, Sesto S.G. (Milano)

24 novembre 2015

Total Global Refining capacity is currently around 96 MMbpd

By end of decade, additional 5 – 6 MMbpd of new capacity

will begin operations, reaching around 102 MMbpd

This means over $550 B in Capex

IEA forecast are that oil demand will increase from 93

MMpbd in 2014 to around 99 MMbdp in 2020

Refining industry is growing, but toward overcapacity

21° Convegno Sezione Componentistica ANIMP, 24 novembre 2015

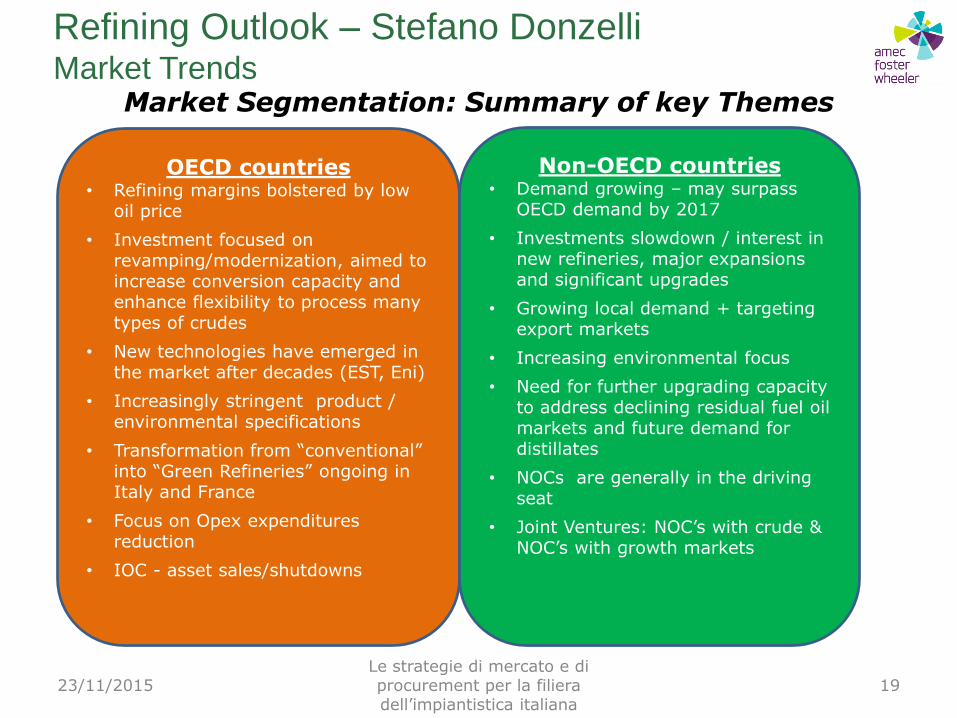

Refining Outlook – Stefano Donzelli Market Trends

23/11/2015 Le strategie di mercato e di procurement per la filiera dell’impiantistica italiana

18

Political stability and objectives still

drive investment plans

• Majority of this new capacity will go in non-OECD

nations, mostly in Asia followed by Middle-East;

• NOC’s will control many investments:

• Long term Client’s relationships

• Local presence and content

• Difficult business environment

• Political influence on project development

• Preference for LSTK contracts

• A huge amount of investment is still required as

clean fuels legislation sweeps across the globe.

Refining Outlook – Stefano Donzelli Market Trends

23/11/2015 Le strategie di mercato e di procurement per la filiera dell’impiantistica italiana

19

Market Segmentation: Summary of key Themes

OECD countries • Refining margins bolstered by low

oil price

• Investment focused on revamping/modernization, aimed to increase conversion capacity and enhance flexibility to process many types of crudes

• New technologies have emerged in the market after decades (EST, Eni)

• Increasingly stringent product / environmental specifications

• Transformation from “conventional” into “Green Refineries” ongoing in Italy and France

• Focus on Opex expenditures reduction

• IOC - asset sales/shutdowns

Non-OECD countries • Demand growing – may surpass

OECD demand by 2017

• Investments slowdown / interest in new refineries, major expansions and significant upgrades

• Growing local demand + targeting export markets

• Increasing environmental focus

• Need for further upgrading capacity to address declining residual fuel oil markets and future demand for distillates

• NOCs are generally in the driving seat

• Joint Ventures: NOC’s with crude & NOC’s with growth markets

Refining Outlook – Stefano Donzelli Market Trends

Residue Upgrading: Profitable Refining with Focused High Conversion

Residue upgrading

& conversion

Significant political pressure to address environmental issues

Declining markets for high sulfur fuel oil

Light / heavy crude spread

Increased demand for distillates and ‘clean fuels’

New crudes sources and extra heavy crude upgraders

Catalytic Non-catalytic Delayed Coking Flexicoking Visbreaking Solvent deasphalting

Residue FCC Residue Hydrocracking

20

23/11/2015 Le strategie di mercato e di procurement per la filiera dell’impiantistica italiana

Refining Outlook – Stefano Donzelli Market Trends

23/11/2015 Le strategie di mercato e di procurement per la filiera dell’impiantistica italiana

21

Gasoline

0 ppm 15-30 ppm 30-80 ppm

200-600 ppm Up to 2500 ppm

100-150 ppm

Source: IFQC

0 ppm 10 or 15 ppm 50 ppm 350 ppm

>2000 ppm 2000 ppm

500 ppm

Source: IFQC

Diesel

• All export refineries are built to the latest clean fuels specifications

• Existing domestic refineries react to domestic legislation

Environmental regulations will impact investment plans

Refining Outlook – Stefano Donzelli Market Trends

23/11/2015 Le strategie di mercato e di procurement per la filiera dell’impiantistica italiana

22

1. Availability of Cheap Gas

2. Marine Fuel Oil Specifications - A Major Challenge for Refiners?

• Still a key market for lower quality/higher sulphur refinery residual fuel oil

• Planned legislation for ships’ SOx emissions will require more stringent constraints

• This will imply investments to treat the «bottom of the barrel»

• Cheap gas will influence not only the level of investment, but also the optimal configuration for refineries

• Will boost investments in petrochemical sector

A couple of wildcards

Refining Outlook – Stefano Donzelli Market Trends

grazie per la cortese attenzione

21° Convegno Sezione Componentistica ANIMP

24 novembre 2015