presented by alpana saksena cit (a) international tax mumbai

TRANSCRIPT

Presented by

Alpana Saksena

CIT (A) International Tax Mumbai

engaged in the equity broking businessIts customers comprise.

Business of the Company

Foreign Institutional Investors

Mutual Funds,

Domestic Financial Institutions

Banks,

PROVIDES Stock Broking services to its AE in Mauritius.

Value of transaction : Rs 1766.94 Crores

Brokerage Earned : Rs 4.22 Crores

Rate of Brokerage : 0.24 %

Nature of International Transaction

TNMMMethod used by taxpayer for computing ALP

Taxpayer short listed 14 independent comparables

Operating Profit Margins of Operating Profit Margins of taxpayertaxpayer

24.8724.87%%

Operating Profit Margins of Operating Profit Margins of 14 Comparable companies14 Comparable companies

8.658.65%%

So, So, taxpayer concludes that transactionsare at arms

length

CUP method rejected because taxpayer stated that

Method used by taxpayer for computing ALP

Volume of business given by the customer

Desire to capture market share

Negotiation power of the customer

Credibility of customer

Marketing efforts involved

Expected future business from the customer

It was stated that reasonable and accurate adjustment cannot be made for

aforesaid factors.

the brokerage rates charged to customers vary on account of various factors such as

the turnover from AE constitutes 42.7% of the total turnover

What triggered investigation?

Main Income was from Clearing House TradesMain Income was from Clearing House Trades

Rate of brokerage earned from third parties ranged between

0.10 % to 0. 50 %.

Rate of brokerage earned from AE 0.24 %.

1. Details of brokerage rate charged for :

CH (Clearing House) trades

3. Average of brokerage rates charged to top 10 clients (in terms of volume) by the taxpayer

What was examined

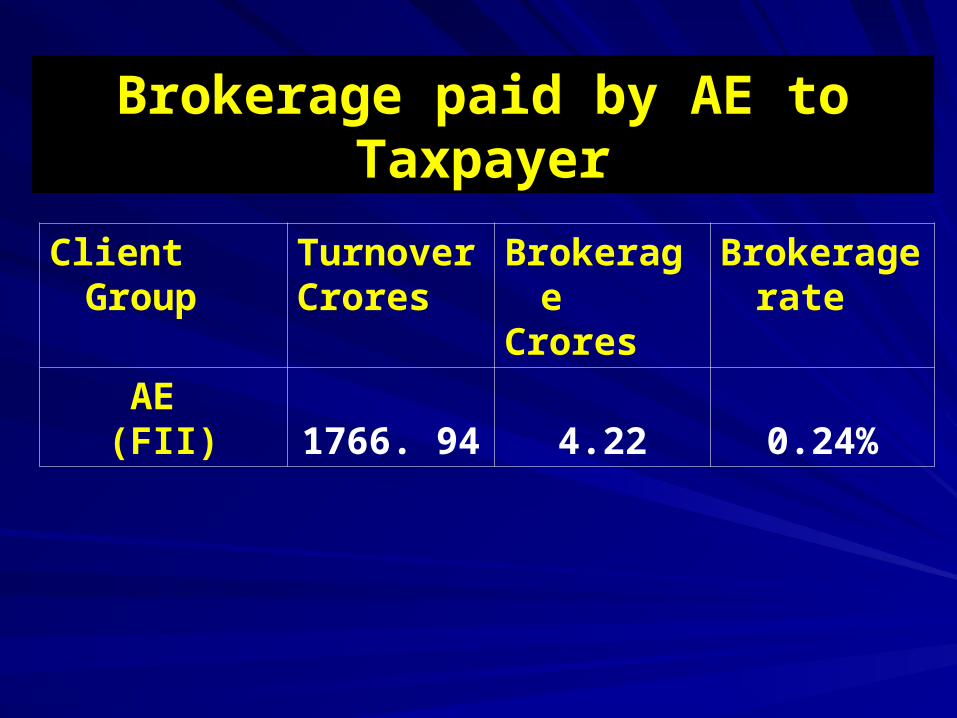

Client Group Turnover Crores

BrokerageCrores

Brokerage rate

AE (FII) 1766. 94 4.22 0.24%

Brokerage paid by AE to Taxpayer

SlNo.

Client Group TurnoverIn crores

BrokerageIn Lacs

Brokerage rate

1 J Co (FII) 336 117 0.35

2 K Co 302 74 0.25

3 B Co 143 30 0.21

4 G Co (FII) 141 70 0.50

5 H Co (FII) 139 39 0.28

6 U Co 133 20 0.15

7 M Co (FII) 124 50 0.41

8 A Co 117 34 0.29

9 X Co (FII) 86 43 0.50

Average Brokerage Charged 0.27%

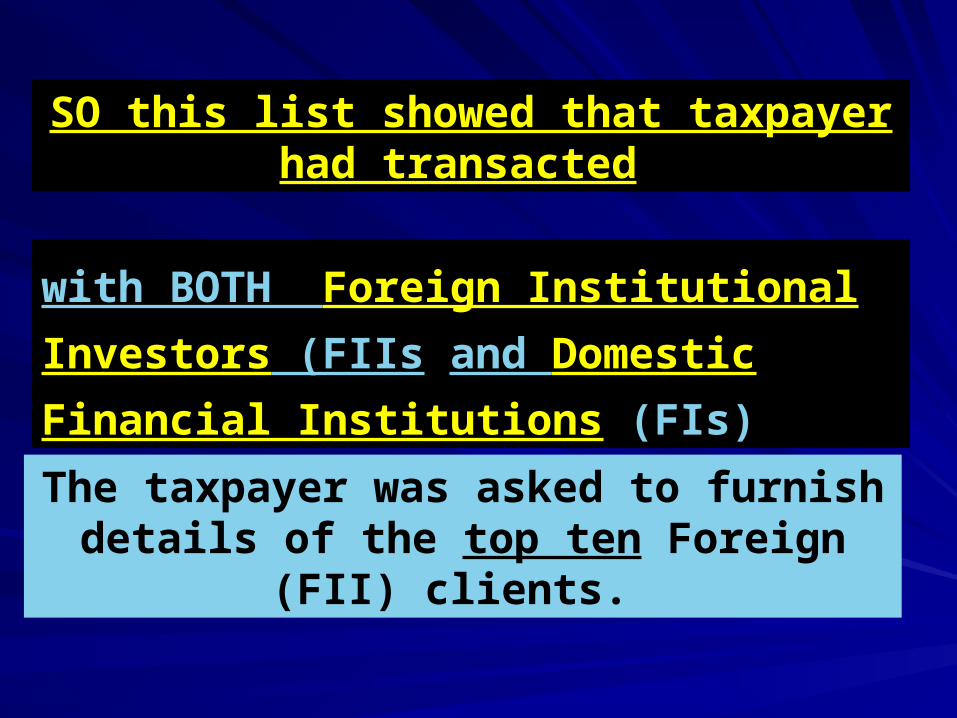

SO this list showed that taxpayer had transacted

with BOTH Foreign Institutional Investors

(FIIs and Domestic Financial Institutions (FIs)

The taxpayer was asked to furnish details of the top ten Foreign (FII) clients.

SlNo

FII TurnoverCrores

BrokerageIn lacs

Brokerage %

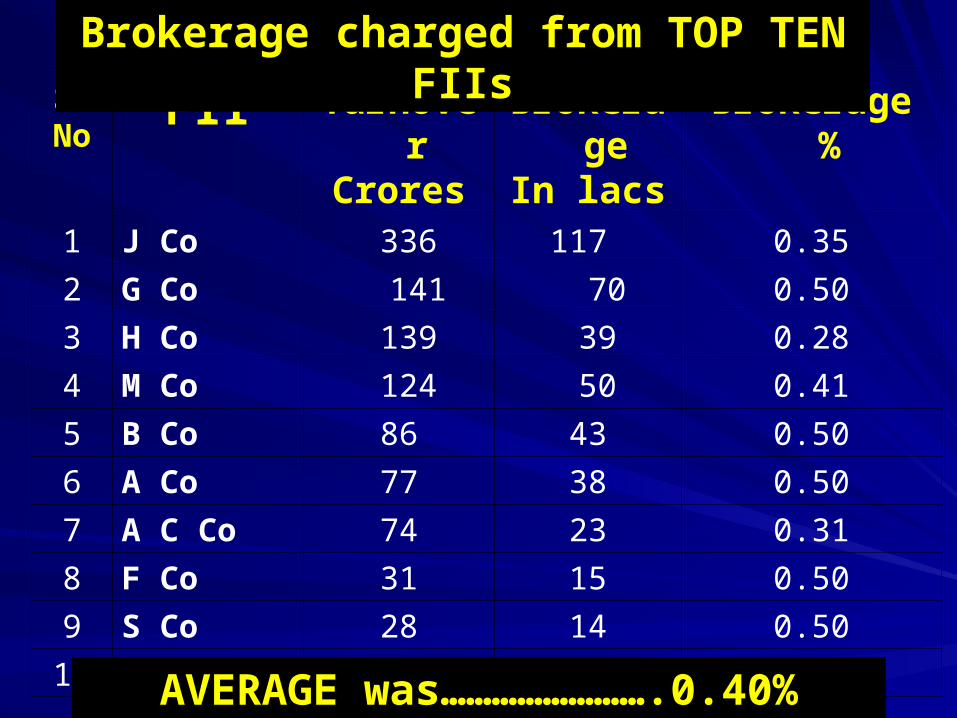

1 J Co 336 117 0.35

2 G Co 141 70 0.50

3 H Co 139 39 0.28

4 M Co 124 50 0.41

5 B Co 86 43 0.50

6 A Co 77 38 0.50

7 A C Co 74 23 0.31

8 F Co 31 15 0.50

9 S Co 28 14 0.50

10 D Co 25 43 0.17

Brokerage charged from TOP TEN FIIs

AVERAGE was…………………….0.40%

Thus it was seen that there was a wide difference between average brokerage rates of

0.40% charged from (FIIs)

0 .24% charged from AE who was also an FII

Client Range of brokerage charged

Foreign Institutional Investors (FIIs)

0.40%

AE 0.24%

Pattern of Brokerage was………

Thus much lower rates charged from AE……and

There was

an Internal CUP available

Reason for variation in brokerage rate charged to third party FII customers

Reason for not using CUP to benchmark the brokerage income

If the AE had committed giving volume to the taxpayer …..then

To produce the Agreement entered with AE, if any for volume of business

The questions asked

CUP can not be used

Brokerage rate charged to different customers vary on account of various factors.

Taxpayer’s defence

Since, reasonable and accurate adjustments cannot be made for several factors

brokerage rate charged to third party customers can not be used as CUP

Even if CUP is to be used

1. Volume adjustment should be done

2. no marketing and selling expenses incurred for procuring business from its AE

Hence, Marketing and selling cost should be adjusted in the brokerage rate of third parties

Taxpayer’s Defence

whereas taxpayer to incur these expenses for procuring business from third parties

To arrive at ALP

CUP is the appropriate method to benchmark the brokerage rate charged to AE

Brokerage rate charged by the assessee to third parties can be considered as CUP

In this case the average brokerage rates, in case of foreign clients (FIIs) was considered as Arm’s Length Rates and the same are 0.40%

Department’s contention

Department’s contention

Volume adjustment can be made

No history of volumes seen

No agreement of any sort with the AE existed

that the AE had committed to give volume business to the assessee

if the taxpayer can prove

Marketing and selling efforts are involved in respect of business obtained from Non AEs

Thus, adjustments for marketing functions had to be worked out.

But the Department accepted

The taxpayer’s contention …..that

For Marketing Function:

Considering the proviso of Rule 10B(1)(a)(ii) of the Act

Taxpayer was asked to furnish details of marketing functions performed along with the

expense incurred for it

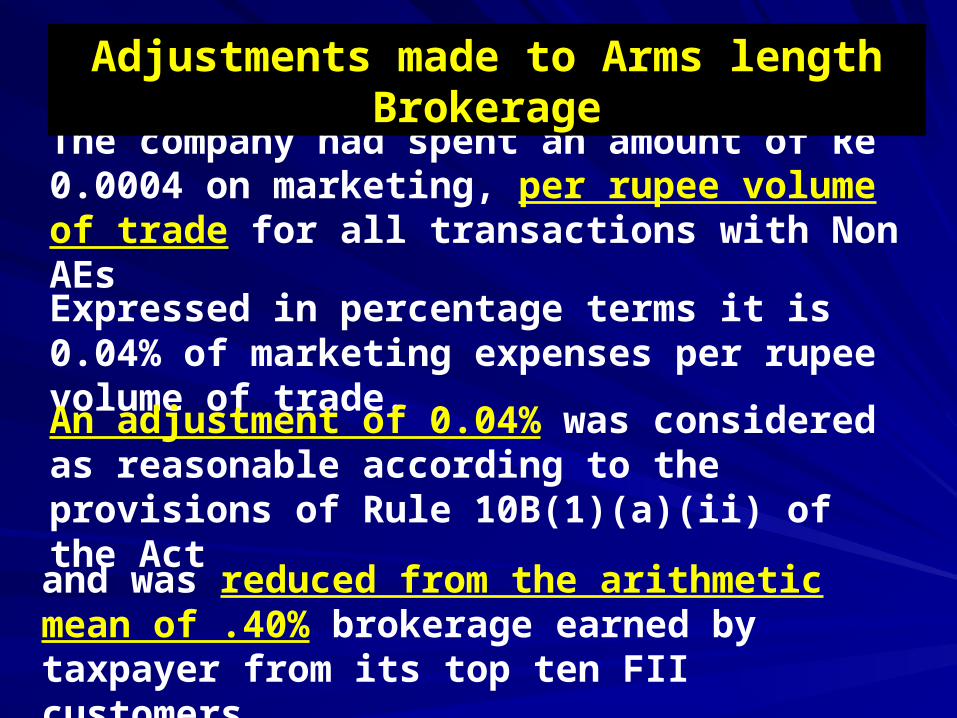

Adjustments made to Arms length Brokerage

Which requires adjustments to be made while calculating ALP

The company had spent an amount of Re 0.0004 on marketing, per rupee volume of trade for all transactions with Non AEs

Expressed in percentage terms it is 0.04% of marketing expenses per rupee volume of trade.

An adjustment of 0.04% was considered as reasonable according to the provisions of Rule 10B(1)(a)(ii) of the Act

and was reduced from the arithmetic mean of .40% brokerage earned by taxpayer from its top ten FII customers.

Adjustments made to Arms length Brokerage

Brokerage rate of 0.40% charged by the assessee to third party FII customers is considered as CUP,

Adjustments were made for marketing and selling expenses.

Arms length brokerage was arrived at

Calculation of Arms length Brokerage

Arithmetic mean of the brokerage earned Arithmetic mean of the brokerage earned by taxpayer from its top ten FII by taxpayer from its top ten FII customers. customers.

0.40%0.40%

Less % of marketing costs incurred for Less % of marketing costs incurred for Non AEs as discussed aboveNon AEs as discussed above

0.04 % 0.04 %

Arms length Brokerage rateArms length Brokerage rate 0.36%0.36%

Calculation of Arms length Brokerage

Was applied to the taxpayer’s Clearing House transactions of Rs 1766.94 crores /- with its AE

Thus the Arms length Brokerage rate of 0.36%

Addition of Rs 2.13 Crores was made

Calculation of Arms length Brokerage

THANK YOU