presenting a live minute teleconference with interactive...

TRANSCRIPT

Presenting a live 110‐minute teleconference with interactive Q&A

Sect. 108 and Cancellation of Debt Income:Navigating IRS RulesDeferring Tax Under This Complex Code Section and Under Latest Guidance

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

WEDNESDAY, APRIL 20, 2011

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

Davis Smith Shareholder Kaufman Gilpin McKenzie Thomas Weiss Montgomery AlaDavis Smith, Shareholder, Kaufman Gilpin McKenzie Thomas Weiss, Montgomery, Ala.

Robert Barnett, Member, Capell Barnett Matalon & Schoenfeld, Jericho, N.Y.

Wayne Strasbaugh, Partner, Ballard Spahr, Philadelphia

Annette Ahlers, Partner, Pepper Hamilton, Washington, D.C.

For this program, attendees must listen to the audio over the telephone.

Annette Ahlers, Partner, Pepper Hamilton, Washington, D.C.

Please refer to the instructions emailed to the registrant for the dial-in information.Attendees can still view the presentation slides online. If you have any questions, pleasecontact Customer Service at1-800-926-7926 ext. 10.

Conference Materials

If you have not printed the conference materials for this program, please complete the following steps:

• Click on the + sign next to “Conference Materials” in the middle of the left-hand column on your screen hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a PDF of the slides for today's program.

• Double click on the PDF and a separate page will open. Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

Continuing Education Credits FOR LIVE EVENT ONLY

Attendees must listen to the audio over the telephone. Attendees can still view the presentation slides online but there is no online audio for this program.

Please refer to the instructions emailed to the registrant for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.at 1 800 926 7926 ext. 10.

Tips for Optimal Quality

S d Q litSound Quality

For this program, you must listen via the telephone by dialing 1-866-258-2056and entering your PIN when prompted. There will be no sound over the web connection.co ect o .

If you dialed in and have any difficulties during the call, press *0 for assistance. You may also send us a chat or e-mail [email protected] immediately so we can address the problem.

Viewing QualityTo maximize your screen, press the F11 key on your keyboard. To exit full screen, press the F11 key againpress the F11 key again.

S t 8 d C ll ti f D bt Sect. 108 and Cancellation of Debt Income: Navigating IRS Rules Webinar

April 20, 2011

Wayne Strasbaugh, Ballard Spahr [email protected]

Robert Barnett, Capell Barnett Matalon &

Schoenfeldb tt@ b l

Davis Smith, Kaufman Gilpin McKenzie Thomas Weiss

Annette Ahlers, Pepper Hamilton [email protected]

Today’s Program

Tax Planning For Debt Restructuring: Key Concepts[Robert Barnett]

Principal Transactional Exceptions

Slide 7 – Slide 26

Slide 27 – Slide 39[Wayne Strasbaugh]Acquisitions Or Repurchases[Robert Barnett]Attribute Reductions

Slide 40 – Slide 45

Slide 46 – Slide 56[Annette Ahlers]

Qualified Real Property Business Indebtedness[Robert Barnett]

Exclusions For Bankrupt, Insolvent Corporate Taxpayers Slide 65 – Slide 72

Slide 57 – Slide 64

Exclusions For Bankrupt, Insolvent Corporate Taxpayers[Davis Smith]

TAX PLANNING FOR DEBT Robert Barnett, Capell Barnett Matalon & Schoenfeld

TAX PLANNING FOR DEBT RESTRUCTURING: KEY CONCEPTS

Introduction: Planning ApproachIntroduction: Planning Approach• Get the facts!

• Entity considerations

l l• Some elections are made at entity level

• Loss utilization history

• Review balance sheet and projections

• NOL + PAL credit carryforwards

S l f d b• Solvency of debtor

8

Cancellation Of DebtCancellation Of Debt

• IRC §61(a)(12)– Except as otherwise provided in this subtitle, gross income

means all income from whatever source derived, including (but not limited to) income from discharge of indebtedness.

9

Cancellation Of Debt (Cont.)Cancellation Of Debt (Cont.)

• Generally, the difference between the balance of the indebtedness and the amount of consideration accepted by the lenderp y

• Income is realized at the time the debt is satisfied.

• Solvent taxpayers generally report ordinary income on canceled or reduced debt.

10

McCormick, TC Memo 2009-39McCormick, TC Memo 2009 39

• What is correct amount of CODI?

• The McCormick family received a 1099 C from Citi FinancialThe McCormick family received a 1099 C from Citi Financial

• IRC §6201(d): In any court proceeding:T bl di– Taxpayer asserts reasonable dispute

– To income reported on an information return– Taxpayer fully cooperated

THEN …

11

Burden Of Proof Shifts

• To IRS

• Correct CODI was $49.66Correct CODI was $49.66

• IRS could not rely on 1099C

• CCA 201112008: Borrowers received payments in settlement of unfair lending dispute; viewed as equitable reformationg p ; q

• Timing, Gaffney, TC Summary 2010-128

12

Example 1Example 1

• Debtor transfers property in a voluntary foreclosure.

• Of RECOURSE DEBT

RECOURSE DEBT D b f hi h b i ll li bl • RECOURSE DEBT: Debt for which a borrower is personally liable. Whether a debt is recourse or non-recourse may vary from state to state, depending on state law.

13

Example 1 (Cont.)

• 1099C reports

Debt cancelled in Box 2 $465,000$ ,

Box 7: FMV $195,000

• Box 3 should report accrued but unpaid interest.

14

Example 1 (Cont.)Example 1 (Cont.)

• Recourse debt is bifurcated

• Amount of debt cancelled = $465 000Amount of debt cancelled = $465,000

• Fair market value = - $195,000

• CODI: $270,000

OR IS IT?

15

CODICODI

• §108(e)(2)– Should NOT include amounts which would give rise to a tax

deduction if paid

• How was FMV determined?

16

Gain/LossGain/Loss

• Taxpayer’s gain or loss is measured by the difference between the Taxpayer s gain or loss is measured by the difference between the amount realized and the adjusted basis of the property.

17

Example: RentalExample: Rental

• Rental property

• Purchase price = $500 000Purchase price = $500,000

• Adjusted basis = $400,000

• IRC §1231 Loss = $205,000

(400,000 – 195,000)

18

Non-Recourse DebtNon Recourse Debt

• Amount realized = $465,000

• Basis = - $400 000Basis = $400,000

• Capital gain = $65,000

• Non-recourse debt is defined as debt for which a borrower is not personally liable.

19

When Is Debt Discharged?When Is Debt Discharged?

• Debt modification: Any change in terms, collateral, etc.

• Significant modification: Will trigger an exchange of the old debt for a new debt§1001§1001

• Old debt satisfied for issue price of new debt

20

RepurchaseRepurchase

• Debtor buys back its debt.

• Related parties – example: Acquire $1 000 of debt for $500Related parties example: Acquire $1,000 of debt for $500

• COD + OID result

• OID income recognized by related party over term of new debt. Debtor has a corresponding deduction.

• Presumption (six months prior)

21

Exchanges

• Debt for debt: Satisfied old debt with amount of $ equal to the ISSUE • Debt for debt: Satisfied old debt with amount of $ equal to the ISSUE PRICE of new debt

22

Exchanges (Cont.)Exchanges (Cont.)

• CODI = Adjusted issue price of old debt minus issue price of new debt

• OID = Stated redemption price at maturity minus issue price of new debt

• USE AFR INTEREST RATE on new debt, so debt is equivalent

23

Form 982Form 982

• Form 982 is used to reduce tax attributes due to discharge of indebtedness.

• The form must be attached to a timely filed return. yExtensions of time to file may be allowed if the taxpayer acted reasonably and in good faith under Treas. Reg. 301.9100-3.

• IRC §1017 provides rules for basis reduction.

24

25

26

PRINCIPAL TRANSACTIONAL Wayne Strasbaugh, Ballard Spahr LLP

PRINCIPAL TRANSACTIONAL EXCEPTIONS

D b F D b E hDebt‐For‐Debt ExchangesI. Basic terms

A. Issue price

1. Issued for money: Cash paid

2 P bli l d d d b F i k l2. Publicly traded debt: Fair market value

3. Issued for publicly traded property: FMV of property surrendered

4. Other cases: Imputed issue price, or SRPM

B. Stated redemption price at maturity (SRPM)

1 All h h lifi d d i (QSI) 1. All payments other than qualified stated interest (QSI)

C. QSI

1. Interest payable at least annually, at a single fixed rate

28

1. Interest payable at least annually, at a single fixed rate

D bt f D bt E h (C t ) Debt‐for‐Debt Exchanges (Cont.) II. Measurement of income in debt-for-debt exchange (IRC Sect. 108

(e)(10))

A. In determining the amount of discharge of indebtedness, the debtor is treated as having satisfied existing debt for an amount of debt equal to issue price of new debt.

B. If an issue price would otherwise be SRPM, then the issue price is reduced by unstated interest.

C. EXAMPLE: Original note with principal amount of $100, interest of 10% payable annually and term of three years is exchanged for replacement note with principal amount of $130, with no interest payable currently and term of three years. Assume that 10% compounded annually is the applicable federal rate (AFR), and that neither note is publicly traded.

29

D b F D b E h (C )Debt‐For‐Debt Exchanges (Cont.)1. Imputed issue price of replacement note is $100, and there is

no discharge of indebtedness income. Debtor deducts $30 as original issue discount (OID) over the term of the replacement note.

2. If AFR were 11%, imputed issue price of replacement note would be less than $100, and there would be discharge of indebtedness income that would be matched by additional d d ti f d OID th t f th l t deductions of accrued OID over the term of the replacement note.

3. If replacement note were publicly traded and had FMV (i.e. i i ) f l th $100 th th ld b di h issue price) of less than $100, then there would be discharge of indebtedness income regardless of adequacy of AFR. 2011 proposed regulations would significantly broaden definition of “publicly traded ” if adopted in current form

30

publicly traded, if adopted in current form.

D b F D b E h (C )Debt‐For‐Debt Exchanges (Cont.)III. Deemed exchanges of debt instruments (Treas. Regs. Sect. 1.1001-3)

A O t th f C tt S i A C i i 499 U S 554 (1991)A. Outgrowth of Cottage Savings Assn. v. Commissioner, 499 U.S. 554 (1991)B. Focus on modifications: Any alteration is a modification, except that

modifications occurring by operation of the terms of the debt instrument are not alterations.

C Si ifi difi i C. Significant modifications 1. Change in yield of more than de minimis amount (25 basis points)2. Change in timing of payments; safe harbor for extension of the

lesser of five years or 50% of original term3. Substitution of new obligor on recourse instruments4. Substitution of a substantial amount of collateral on non-recourse

instruments5. Certain other changes (e.g. subordination) that change payment g ( g ) g p y

expectations D. Result of deemed exchange is measurement of potential discharge of

indebtedness under IRC Sect. 108 (e)(10)

31

D b F S k E hDebt‐For‐Stock ExchangesI. Measurement of discharge of indebtedness income (Sect. 108 (e)(8))

A. Debt is deemed satisfied to the extent of the fair market value of the stock received.

B. Tiny residue of common law “stock-for-debt” exception from y precognition of discharge of indebtedness income that was whittled away by Bankruptcy Tax Act of 1980 and subsequent statutes. See Capento Sec. Corp. v. Commissioner, 47 B.T.A. 691 (1942), aff'd 140 F.2d 381 (1st Cir. 1944); and Commissioner v. Motor Mart Trust, 156 F.2d 122 (1st Cir. 1946)

C. Sect. 351 does not protect creditor contributor from recognition of gain or loss, unless debt is a “security.” IRC Sect. 351 (d)(2)

D. In case of S corporation, necessary to elect to close books to avoid discharge of indebtedness income to creditor

32

D b f S k E h (C )Debt‐for‐Stock Exchanges (Cont.)E. Different result if simultaneous steps? Formation of new E. Different result if simultaneous steps? Formation of new

corporation by creditor and debtor. Cf. Kniffen v. Commissioner, 39 T.C. 553 (1962); IRC Sect. 357(d)

F EXAMPLE: Debt with principal amount of $100 is exchanged F. EXAMPLE: Debt with principal amount of $100 is exchanged for stock of debtor worth $90, and debt is extinguished. Discharge of indebtedness income of $10 is recognized.

G. EXAMPLE: Debt with principal amount of $100 is contributed to Newco by creditor, and assets subject to debt are contributed by debtor. Debtor potentially recognizes gain under Sect. 357(c) prior to extinguishment of debt by merger of debtor and creditor.

33

Debt‐For‐Partnership Interest Exchanges

I Measurement of discharge of indebtedness income (IRC Sect 108(e)(8))I. Measurement of discharge of indebtedness income (IRC Sect. 108(e)(8))

A. Debt (recourse or non-recourse) is deemed satisfied to the extent of the FMV of a profits or capital interest received. Liquidation value may be used to determine FMV if capital accounts are maintained under IRC Sect. 704(b), valuation by partners and partnership is consistent, and certain other requirements are met.

B. Consequence of enactment of American Jobs Creation Act of 2004 (AJCA): Prior common law was assumed by many to contain a complete debt forPrior common law was assumed by many to contain a complete debt-for-partnership interest exclusion.

C. Recognized discharge of indebtedness income allocated to partners immediately before the discharge exchange y g g

D. Presumably allocated first as chargeback of minimum gain, if non-recourse debt; need to allocate in way consistent with deemed distributions under IRC Sect. 752 but yet satisfy IRC Sect. 704(b) “ b t ti l i ff t”

34

“substantial economic effect”

Debt‐For‐Partnership Interest Exchanges (Cont.)

E. EXAMPLE: Debt of $100 is exchanged for 10% profits and capital $ g p pinterest worth $90. Discharge of indebtedness income of $10 is allocated in accordance with partnership percentage interests prior to the issuance of the new interest. Deemed distribution of $10 under IRC Sect. 752

F. Proposed regulations (Prop. Regs. Sec. 1.108-8) issued in 2008 indicate that creditor will recognize no gain or loss on exchange by reason of Sect. 72l. Loss of partial bad debt deduction was criticized by many commentators. Two-step transactions raise “old-and-cold” issues.

G. Proposed regulations indicate equity received for accrued interest or original issue discount (OID) is taxable, even if accrued prior to contributor partner’s ownership. Also, one would ll d f d d O

35

allocate equity received first to accrued interest and OID.

Contribution Of Debt By Existing Shareholder

I. Measurement of discharge of indebtedness income (IRC Sect. g (108(e)(6))A. Shareholder is treated as having satisfied the debt in

amount equal to its basis for the debt.1. If shareholder is the original lender, then basis should

be equal to amount of debt, and no discharge of indebtedness income would be created.

2. If shareholder acquired debt at a discount after issuance or has accrued interest as a cash basis taxpayer, then discharge of indebtedness income would be recognizedwould be recognized.

3. In case of an S corporation, basis reductions to debt for S corporation losses are not taken into account. IRC Sect 108(d)(7)©

36

IRC Sect. 108(d)(7)©

Contribution Of Debt By Existing Shareholder (Cont.)

4. Technically, an exception appears to be available without 4. Technically, an exception appears to be available without regard to corporate solvency. But, if contribution does not make corporation solvent, it may not be a capital contribution and therefore may not be within this exception. Compare Mayo 16 TCM 49 (1957); Giblin 227 F 2d 682 (5thCompare Mayo, 16 TCM 49 (1957); Giblin, 227 F.2d 682 (5Cir. 1955) with Lidgerwood, 229 F.2d 241 (2d Cir. 1956)

a. Creditor receives bad debt deduction if IRC Sect. 108(e)(6) inapplicable

B. How to distinguish from stock-for-debt exception?

1. May simply be a matter of form. See LTR 200537026; LTR 9050031; LTR 9018005. But cf. TAM 9822005

2. “Meaningless gesture” cases suggest that Sect. 351 may apply, in which case issuance of stock to shareholder will be imputed and stock-for-debt exception will govern. See Rev. Rul 64-155

37

Rul. 64-155

Contribution Of Debt By Existing Shareholder (Cont.)

C. Where not “meaningless gesture,” shareholder arguably has C. Where not meaningless gesture, shareholder arguably has made gift to other shareholders

D. Application to partnerships?

1. It appears that there is no analog for contribution of debt to 1. It appears that there is no analog for contribution of debt to a partnership by an existing partner.

2. Proportionate contributions of partnership debt may result in discharge of indebtedness income, if no corresponding i i it lincrease in equity value.

3. EXAMPLE: Partnership holds property with FMV of $70 subject to non-recourse debt of $100 held proportionately by partners Partners contribute debt increasing partnership partners. Partners contribute debt increasing partnership equity value (representing value of interests received) by $70. Apparently, $30 of discharge of indebtedness income is recognized.

38

Partial Debt Exchanges: Which Exception?

I. EXAMPLE: Debt of $100 held by a sole shareholder with basis of $100. Sh h ld ib $50 f d b i I iShareholder contributes $50 of debt to corporation. Is transaction:A. Exchange of debt for stock in a “meaningless gesture” transaction

governed by IRC Sect. 108(e)(8), with possible discharge of indebtedness income depending on the value of shares of stock indebtedness income depending on the value of shares of stock constructively received?

B. Capital contribution of debt of $50 under IRC Sect. 108(e)(6), with no discharge of indebtedness income because there was no formal gexchange of remainder of debt?

C. Exchange of $100 debt for debt of $50 under IRC Sect. 108(e)(10) and the deemed exchange rule of Treas. Regs. Sect. 1001-3?

D. A combination of alternative C with either of alternatives A or B?E. Does codification of the economic substance doctrine have any

effect on the answer to these questions?

39

ACQUISITIONS OR Robert Barnett, Capell Barnett Matalon & Schoenfeld

QREPURCHASES

Acquisition By DebtorAcquisition By Debtor

• Will give rise to CODI if purchased at a discount

41

Acquisition Of Indebtedness By l d bPerson Related To Debtor

• IRC §108(e)(4) and Reg. §1.108-2 provide that:– The acquisition of outstanding indebtedness by a person related to The acquisition of outstanding indebtedness by a person related to

the debtor from a person who is not related to the debtor is treated as an acquisition by the debtor, and results in the realization by the debtor of CODI income under IRC §61.

– Such income may still be excludible from gross income to the extent provided in §108(a).

42

Who Is Considered A Related Party?

• For purposes of §108, persons are considered related if they are related within the meaning of §267(b) as modified by §108(e)(4)(B) or §707(b)(1).

• §267(b) provides, in relevant part, that related party includes:– Members of a family– An individual and a corporation more than 50% in value of the An individual and a corporation more than 50% in value of the

outstanding stock of which is owned, directly or indirectly, by or for such individual

– Two corporations which are members of the same controlled groupTwo corporations which are members of the same controlled group

• Presumption: Six months prior

43

FamilyFamily

• Notwithstanding §267(b), §108(e)(4) limits members of a family to the individual’s spouse, children, grandchildren, parents, and any p , , g , p , yspouse of the individual’s children or grandchildren.

• For example: The father-in-law of the individual would NOT be For example: The father in law of the individual would NOT be considered a related party under the terms of the statute and regulations.

44

PurchasePurchase

• Example: Related party acquires $1,000 debt for $500

• COD + OID result

• OID income recognized by related party over term of new debt; debtor has corresponding deduction

• Presumption: Six months prior

45

ATTRIBUTE REDUCTIONSAnnette Ahlers, Pepper Hamilton

General Rules• Sect. 108(b)(1): The amount of COD excluded from gross income

under Sect. 108(a)(1) requires the reduction of attributes of the taxpayer.p y

• Sect. 108(b)(2): In general, attributes shall be reduced in the following order:

1. Net operating losses (NOLs); first any loss from the current year, then NOL carryovers from prior yearsthen NOL carryovers from prior years

2. General business credits, including any carryovers3. Minimum tax credit available under Sect. 53(b) “as of the

beginning of the taxable year of the discharge”g g y g4. Capital loss carryovers; current year first, then any carryover5. Basis reduction of the property of the taxpayer6. Passive activity loss and credit carryovers; any loss under Sect.

469(b) f th t bl f di h469(b) from the taxable year of discharge7. Foreign tax credit carryovers to or from the taxable year of the

discharge, for purposes of determining the credit allowable under Sect. 27

47

Amount Of ReductionAmount Of Reduction

• Under 108(b)(3): The exclusions are dollar-for-dollar the amount excluded by 108(a).y ( )

• For reduction of credits and passive activity losses, the reductions shall be 33 1/3 cents for each dollar excluded by 108(a)shall be 33 1/3 cents for each dollar excluded by 108(a).

48

Ordering RulesOrdering Rules

108(b)(4) R d i d f d i i f f bl• 108(b)(4): Reductions made after determination of tax for taxable year of discharge

– First, reduce tax losses of the year of discharge.– Second reduce carryovers from prior years in the order fromSecond, reduce carryovers from prior years, in the order from

which such carryovers arose (oldest NOLs reduced first). – Third, credit reductions shall be made in the order from which

such carryovers are taken into account.F ffili t d fili lid t d t tt ib t– For affiliated groups filing a consolidated return, attribute reduction is done on a consolidated basis, not on a separate company basis.

See CCA 201033031 (April 26, 2010) and Treas. Reg. Section 1.1502-28T

49

Available ElectionsAvailable Elections

• Sect. 108(b)(5): The taxpayer may elect to apply any portion of the ib d i fi d h b i f d i blattribute reduction first to reduce the tax basis of depreciable

property.

Li it ti S h d ti t d th t dj t d• Limitation: Such reduction cannot exceed the aggregate adjusted bases of the depreciable property held by the taxpayer as of the beginning of the taxable year following the year of the discharge.

• If this election is made, other attributes are not reduced.

• An election must be made on the taxpayer’s return for the taxable• An election must be made on the taxpayer s return for the taxable year in which the discharge occurs, or upon permission of the secretary.

50

Attribute Reduction PlanningAttribute Reduction Planning

• Consideration of election to reduce bases of property ahead of NOLs or other tax attributes– May benefit taxpayer in short term, because NOLs would be

available to offset income in post-COD years, and tax basis of certain assets would not benefit taxpayer in same way (longer p y y ( glife depreciation or amortization)

– Only works if COD does not exceed tax bases of these assets, and if other rules (such as sections 382, 384 or 269) do not ( , )otherwise limit the use of the NOLs or other tax attributes

51

Sect. 1017 Ordering RulesSect. 1017 Ordering Rules

• Applies to the reduction of property held by the taxpayer

• Reduction is taken into account with respect to “property held on the first day of the taxable year” following the year of the COD event

• Basis of property is not reduced below zero

52

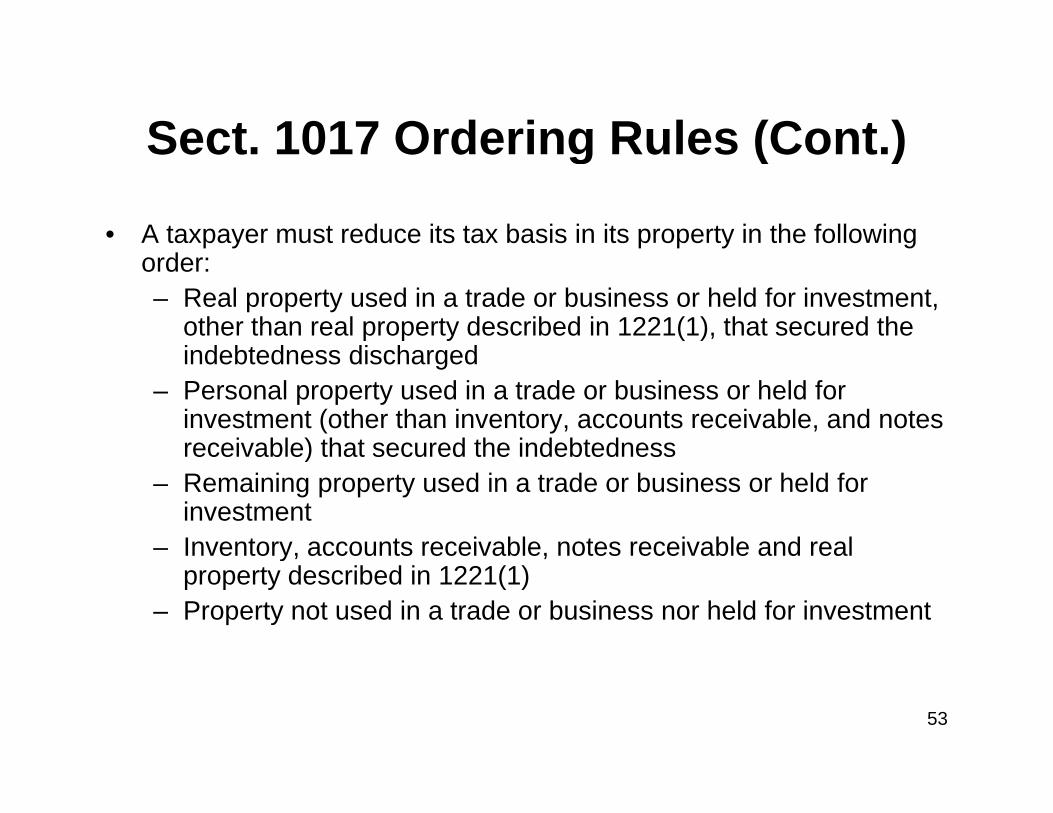

Sect. 1017 Ordering Rules (Cont.)Sect. 1017 Ordering Rules (Cont.)

• A taxpayer must reduce its tax basis in its property in the following dorder:

– Real property used in a trade or business or held for investment, other than real property described in 1221(1), that secured the indebtedness dischargedindebtedness discharged

– Personal property used in a trade or business or held for investment (other than inventory, accounts receivable, and notes receivable) that secured the indebtedness)

– Remaining property used in a trade or business or held for investment

– Inventory, accounts receivable, notes receivable and real yproperty described in 1221(1)

– Property not used in a trade or business nor held for investment

53

Attribute Reduction In Bankruptcy( )(Special Liability Floor Rule)

• Treas. Reg. Sect. 1.1017-1(b)(3): If COD income arises from a discharge while the taxpayer is in a Title 11 bankruptcy or while the taxpayer is insolvent:

Th b i d ti d S t 108(b)(2)(E) h ll t d– The basis reduction under Sect. 108(b)(2)(E) shall not exceed the excess of the aggregate adjusted bases of the property and the amount of money held by the taxpayer, over

– The aggregate of the liabilities of the taxpayer immediately afterThe aggregate of the liabilities of the taxpayer immediately after the discharge

Can create a “black hole” COD in which COD exceeds amountCan create a black hole COD in which COD exceeds amount of attributes or basis that can be reduced; thus, no COD income and no attribute required for such amounts

54

Qualified Real Property Business I d bt dIndebtedness

• Taxpayer is not a C corporation• Sect. 108(a)(1): Excluded COD reduces the basis of the depreciable

real property of the taxpayer • Apply Sect. 1017 in making the required reductions• Limited

– Excluded amount cannot exceed the excess of the outstanding principal amount of indebtedness, over the FMV of the real property that is “qualified real property business property ”property that is qualified real property business property.

– Overall exclusion cannot exceed the aggregate adjusted bases of the depreciable real property held by the taxpayer immediately before the discharge.before the discharge.

– Cannot include real property acquired in contemplation of such discharge

55

Qualified Principal Residence I d bt dIndebtedness

• Basis reduction– 108(h): Amount excluded from gross income under 108(a)(1)(E)

shall be applied to reduce the basis of the principal residence of the taxpayer.

• Cannot be reduced below zero• Up to $2 million in principal amount• Discharge cannot relate to the provision of servicesDischarge cannot relate to the provision of services

performed for the lender.• Principal residence is defined in Sect. 121.

56

QUALIFIED REAL PROPERTY Robert Barnett, Capell Barnett Matalon & Schoenfeld

QBUSINESS INDEBTEDNESS

QRPBI: Qualified Real Property Business I d b dIndebtedness

• Taxpayers other than C corporations can exclude from gross income discharge of qualified real property business indebtedness.

• Amount excluded must reduce the taxpayers’ basis in real property.

• Amount cannot exceed the basis of real property held by the taxpayer• Amount cannot exceed the basis of real property held by the taxpayer.

• Anti-stuffing provision disallows purchase in contemplation of such di hdischarge.

58

ElectionElection

• Elective exclusion: USE FORM 982

• Qualified real property business indebtedness: Debt incurred to acquire, construct, or substantially renovate real propertyq , , y p p y

• Used in a trade or business, and

• Secured by such real property

• Note that the insolvency and bankruptcy exceptions come first.

59

Limitations And RecaptureLimitations And Recapture

• The exclusion cannot exceed:– The amount by which the principal amount of the debt exceeds the

fair market value of the property securing the debt, orp p y g ,– The aggregate adjusted bases of the taxpayer’s depreciable real

property

• The basis reduction is treated as ordinary income RECAPTURE upon sale of the property, based upon the IRC §1250 depreciation rules using the straight line method of depreciationthe straight line method of depreciation.

60

PartnershipPartnership

• PARTNERSHIP discharge and whether the debt was incurred in connection with a real property trade or business is made by reference p p y yto the business of the partnership

• The ELECTION to exclude or discharge real property business The ELECTION to exclude or discharge real property business indebtedness is made at the partner level on a partner-by-partner basis.

61

IRC §1017IRC §1017

• IRC §1017 provides that the partner’s interest in the partnership is treated as depreciable real property, to the extent of the partner’s proportionate interest in the partnership’s depreciable real property.

• A partner’s election to treat the partnership interest as depreciable real property will result in both the partner’s basis in the partnership and p p y p p pthe partnership’s basis in the depreciable real property allocable to such partner as reduced.

• Generally, the partnership may grant or withhold consent, unless the taxpayer owns more than 50% partnership interest.

62

S CorporationS Corporation

• Election made at corporate level + attribute reduction

• No adjustment to shareholder stock

A d f l• Acts as a deferral

63

Principal ResidencePrincipal Residence

• Temporary exclusion before Jan. 1, 2013

• QUALIFIED principal residence indebtednessQUALIFIED principal residence indebtedness

• Not a second home

• Later §121 exclusion may protect basis reduction

• Insolvency exclusion may be preferable

64

EXCLUSIONS FOR BANKRUPT, Davis Smith, Kaufman Gilpin McKenzie Thomas Weiss

,INSOLVENT CORPORATE TAXPAYERSTAXPAYERS

Exclusion For Bankrupt Corporate ( )( )( )Taxpayers: Sect. 108(a)(1)(A)

• COD income excluded if occurs in a “Title 11” case– Refers to a petition for bankruptcy filed under Title 11 of the

United States Code, but only if:• The taxpayer is under the jurisdiction of the court in such case andcase, and

• The discharge of the debt is either– Granted by court order, orP t t l d b th t– Pursuant to a plan approved by the court

• Debt does not have to be listed debt as long as discharged by court

• Entire amount of COD income excluded• Entire amount of COD income excluded• If more than one exclusion applies under Sect. 108(a)(1), then

bankruptcy exclusion has priority.

66

Exclusion For Insolvent Corporate ( )( )( )Taxpayers: Sect. 108(a)(1)(B)

• Two primary differences between bankruptcy exclusion and insolvency exclusion– Bankruptcy exclusion excludes all COD income, while certain limitations apply to the amount of COD incomecertain limitations apply to the amount of COD income that may be excluded by insolvent taxpayers.

– Qualification for bankruptcy exclusion is objective, while qualification for insolvency exclusion is subjectivequalification for insolvency exclusion is subjective.

• Limitation of insolvency exclusion– Definition of “insolvent” – Sect. 108(d)(3)

• Excess of liabilities over fair market value of assets• Determined immediately before the discharge

67

Calculation Of InsolvencyCalculation Of Insolvency

• “Fair market value” is based on valuing corporation as a going concernconcern– Not liquidation value– Off‐balance sheet assets, such as goodwill and going concern

value, are included in the calculation.,– Should obtain an appraisal, since IRS may challenge

• Contingent liabilities are included only if the liabilities are more likely than not to result in a payment by the debtor.– All‐or‐nothing test– Guarantees are not included, unless preponderance of evidence

shows guarantor will be called upon to pay.– Taxpayer has burden of proof.

• Unclear whether tax liabilities arising from workout should be included in calculation

68

Calculation of Insolvency (Cont.)Calculation of Insolvency (Cont.)• Contested liability doctrine

– If dispute is over the amount of the liability, then no COD income should arise from a settlementa settlement.

– If dispute is over the enforceability of the liability, then COD income would result from a settlement.

• Non‐recourse debt: Two 2 optionsp

– Full amount of non‐recourse debt included in calculation, or

– Include the full amount of the debt only if the non‐recourse debt is being discharged; otherwise, include non‐recourse debt only to extent of the fair market l f h ll lvalue of the collateral

• This is Service’s position – see Rev. Rul. 92‐53

• Bonds and other corporate‐issued obligations are valued at adjusted issue price.

• “Immediately before”: Do not take into consideration the reduction in liabilities as a• “Immediately before”: Do not take into consideration the reduction in liabilities as a result of the discharge

• Insolvency exclusion has priority over exclusions for qualified real property business indebtedness and qualified farm indebtedness.

69

Application To Consolidated GroupsApplication To Consolidated Groups

• Consolidated groups

– Eligibility for exclusions is determined on a separate‐company basis

– Which member of the group is the debtor for tax purposes?Which member of the group is the debtor, for tax purposes?

• For example, if one member is a guarantor and other members and parent are thinly capitalized, is the guarantor the debtor for tax purposes?the debtor for tax purposes?

– Inter‐company debt

• Sect. 108(a) does not apply to COD income generated by pp y g ysettlement of inter‐company debt.

• COD income should be offset by bad debt deduction available to other members of the groupavailable to other members of the group.

70

Application To Flow‐Through EntitiesApplication To Flow Through Entities

• S corporations: Qualification for exclusions under Sect. 108 are determined at the entity level.

• Partnerships (including LLCs): Qualification for exclusions under Sect. 108 are determined at the partner level.

– Partner cannot piggyback partnership bankruptcy filing to qualify for a bankruptcy exclusion.

• Disregarded entities (QSubs and SMLLCs)g (Q )

– Does a disregarded entity qualify for the bankruptcy or insolvency exclusions?

– Recently released proposed regulations provide that the owner notRecently released proposed regulations provide that the owner, not the disregarded entity, must qualify.

71

Planning ConsiderationsPlanning Considerations

• Bankruptcy generally provides more certainty for the tax consequences.

– Objective criteria for qualification

– Exclude full amount of COD income

– Drawback is that bankruptcy may be more costly than a workoutDrawback is that bankruptcy may be more costly than a workout

• Pre‐packaged bankruptcy may be an attractive option.

– Combines certainty of tax consequences with cost efficiency of workoutworkout

• Timing is everything in the application of insolvency exclusion.

– Insolvency is determined immediately before the discharge.

– Contribution of new capital to the corporation could affect the insolvency calculation.

– If possible, a cash injection into debtor should be simultaneous with the debt discharge.

72