preserving the integrity of the financial system ... -...

TRANSCRIPT

AML/CFT Awareness1

Preserving the Integrity of the Financial System:

Prevention of Money Laundering &

Terrorism Financing

Role of Accountants as Effective Gatekeepers

AML/CFT Awareness2

Learning Objectives

Understand role of DNFBPs in prevention of money laundering (ML), terrorism financing

(TF) and proliferation financing (PF)

Awareness on ML/TF risks and application of risk-based approach

Implementation of AML/CFT reporting obligations as effective deterrence

AML/CFT Awareness3

Presentation Outline

Malaysia’s AML/CFT Regime

ML/TF Vulnerabilities & Recent Developments

AML/CFT Requirements

AML/CFT Awareness4

“A process of converting cash

or property derived from criminal activities to give it a legitimate appearance. It is the process of cleaning and disguising the criminal origin

of ‘dirty’ money”

“Process of

financing terrorist

activity either

through legitimate

or illegitimate

sources.”

Critical for a country to have an effective AML/CFT regime…

1. Reduces rewards associated with crime and hence, overall crime rates;

2. Increases government revenue, reduces leakages within the economy;

3. Preserves the integrity and reputation of the market place; and

4. Creates conducive environment for businesses and investors to flourish.

Money Laundering (ML) & Terrorism Financing (TF) defined

AML/CFT Awareness5

All countries are required to comply with the FATF international standards

UN Conventions and Resolutions

Financial Action Task Force (FATF), Headquartered in Paris [Malaysia is a ‘Member’]

All countries are members of a FRSB (except Iran and DPRK)

Principles under the Resolutions have been embedded into the FATF standards

The Vienna Convention

The Palermo Convention Security Council Resolution 1267 and its Successors

Security Council Resolution 1373

International Convention for the Suppression of the Financing of Terrorism

Issues & ensures compliance by jurisdictions to FATF 40 Recommendations (2012) & Methodology (2013)

APG -Malaysia is a ‘Member’ MENAFATF GIABA CFATF MONEYVAL GAFISUD EAG

Principles under the Resolutions have been embedded into the FATF standards

Implementation by FATF-Styled Regional Bodies (FSRBs)

Principles under these Resolutions have been embedded into the FATF standards

AML/CFT Awareness6

Since AMLA was effected in 2001, Malaysia has established a

comprehensive AML/CFT framework for prevention of ML/TF activities

FATF

Standards

• BNM the competent authority for AMLA

• Criminalisation of ML/TF i.e. 362

offences from 44 legislations

• Freezing, seizure & forfeiture of

properties

• Identify & respond to emerging

risks through National Risk

Assessment process

• Adequate investigation &

enforcement powers

• Fully-functional FIU in BNM

• AML/CFT Units set-up in key law

enforcement agencies (LEAs)

• Structured training programs for

financial investigators

• National Coordination

Committee for integrated

approach across 16

Ministries/Agencies

• MoUs and Strategic

Partnerships with Foreign FIUs

& Counterparts

• Strong networks with

International/regional bodies FATF, APG, Egmont Group

Responsibilities of Reporting

Institutions (RIs)

More than 43,000 RIs

Implement effective AML/CFT

compliance programme to detect

and deter ML/TF

Submit CTRs and STRs to

FIED, BNM

AML/CFT Awareness7

Presentation Outline

Malaysia’s AML/CFT Regime

ML/TF Vulnerabilities & Recent Developments

AML/CFT Requirements

AML/CFT Awareness

Reporting institutions (RIs) are the first line of defence

Criminals and

Criminal Activities

Financial Institutions

Law enforcement

Agencies (LEAs)

Non-bank FIs

DNFBPs

• Formation of complex company structures

• Placement of proceeds from unlawful activities

Supervisory authorities

BNM, SC, LFSA

Financial Intelligence Unit

FIED, BNMSubmit Cash Threshold & Suspicious Transaction

Reports

Collect, analyse,

disseminate financial

intelligence

Feedback on effectiveness of financial intelligence

Identify illicit activities and investigate crimes

Monitor & enforceAML/CTF

requirements

AML/CFT PREVENTIVE MEASURES• ML/TF Risk Assessment & Client Risk Profiling• CDD and Enhanced CDD on Clients• Record Keeping • On-going Monitoring of Clients’ Transactions• Promptly Detect & Report Suspicious Transactions

Supervisory authorities

BNM in collab. with licensing bodies & SROs

1

2 3

45

8

AML/CFT Awareness

Example: ML Case involving an Accountant

Timothy Clifford, a methamphetamine manufacturer and dealer in the Waikato region, New

Zealand, used an accountant to receive cash from his drug dealings and convert it into various

purchases of farm land over a number of years

Brief facts of case:

1. Mr Clifford used two of his farm employees to collect and take cash from drug sales to the accountant’s

office;

2. The accountant had 12 accounts held at different banks in which he would deposit the cash. The

accounts were maintained for his accountancy practice, a gift shop he and his wife owned, his personal

accounts and a company account he was nominee director and shareholder of on behalf of Clifford;

3. The accountant went to different branches across the Waikato region and banked the cash into the

various accounts. Among the excuses that he gave about the source of cash were:

o Cash takings from client who owned a bar; and

o Cash takings from a stall he operated at a market.

4. The deposited cash would then be electronically transferred to his accountancy practice to be held on

behalf of Clifford;

5. With his accumulated wealth, Clifford purchased farm land in the name of his family trust. The trustee of

his trust was a corporate trustee company that the accountant was the director and shareholder of. This

trust management enabled Clifford to hide the fact that he owned the farm land. It was estimated that,

over 10 years, Clifford had accumulated $4.8 million from his drug offending.

Investigation Outcome:

• Clifford was sentenced to 12 years prison and his farm land was forfeited by the investigation authority;

• Whilst it was clear the accountant had engaged in money laundering, he was used as a witness against

Clifford in exchange for immunity from prosecution.

Source: APG Typologies Report 2014

AML/CFT Awareness10

Likelihood

POSSIBLE LIKELY VERY LIKELY

Exte

nt

of

Vu

lnera

bil

ity HIGH

MEDIUM

LOW

• Casino

• Gaming Companies

• Jewellers (DPMS)

• Accountants

• Offshore Trust

• Company Secretaries

• Real Estate

• Trust Companies • Lawyers

• Pawn Brokers

• Notaries

LP – onshore /

offshore

NPOs

National ML/TF Risk Assessment 2013 by the National Coordination Committee for ML

Sectoral Risk Assessment for DNFBPs and Other Non-Bank FIs

AML/CFT Awareness11

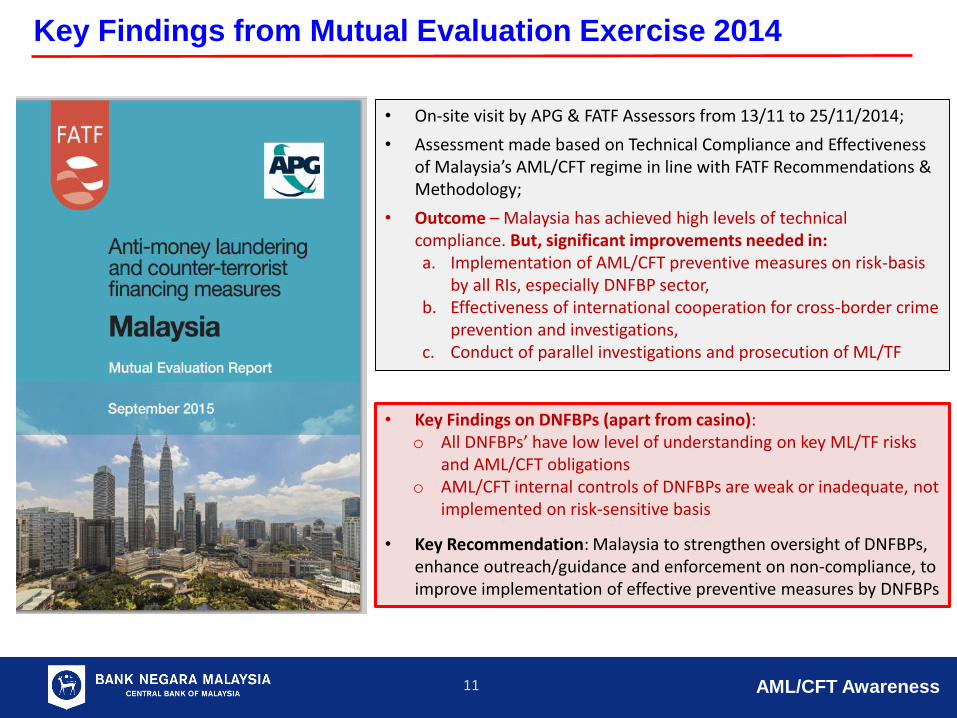

Key Findings from Mutual Evaluation Exercise 2014

• On-site visit by APG & FATF Assessors from 13/11 to 25/11/2014;

• Assessment made based on Technical Compliance and Effectiveness of Malaysia’s AML/CFT regime in line with FATF Recommendations & Methodology;

• Outcome – Malaysia has achieved high levels of technical compliance. But, significant improvements needed in: a. Implementation of AML/CFT preventive measures on risk-basis

by all RIs, especially DNFBP sector, b. Effectiveness of international cooperation for cross-border crime

prevention and investigations, c. Conduct of parallel investigations and prosecution of ML/TF

• Key Findings on DNFBPs (apart from casino): o All DNFBPs’ have low level of understanding on key ML/TF risks

and AML/CFT obligationso AML/CFT internal controls of DNFBPs are weak or inadequate, not

implemented on risk-sensitive basis

• Key Recommendation: Malaysia to strengthen oversight of DNFBPs, enhance outreach/guidance and enforcement on non-compliance, to improve implementation of effective preventive measures by DNFBPs

AML/CFT Awareness12

Presentation Outline

Malaysia’s AML/CFT Regime

ML/TF Vulnerabilities & Recent Developments

AML/CFT Requirements

AML/CFT Awareness13

Prevailing Laws and Guidelines in Malaysia:

Anti-Money Laundering, Anti-Terrorism Financing

and Proceeds of Unlawful Activities Act 2001 (Act

613) – AMLA

Anti-Money Laundering & Anti-Terrorism

Financing (Reporting Obligations) Order 2007

AML/CFT – Designated Non-Financial Businesses

and Professions (DNFBPs) & Other Non-Financial

Sectors (Sector 5) Guidelines - Revised & reissued

on 1 Nov 2013

Relevant AML/CFT Law, Regulations & Guidelines - Accountants

As specified in First Schedule of AMLA and

Sector 5 Guidelines, AML/CFT reporting

requirements extend to “Activities carried out

by a member as defined in the Accountants Act

1967 [Act 94]”

FATF’s expectations on implementation of

AML/CFT preventive measures by

reporting institutions (RIs):

Immediate Outcome 4 from FATF Methodology

2013

FIs & DNFBPs adequately apply AML/CFT preventive

measures commensurate with their risks, and report

suspicious transactions

• Understand the nature and level of ML/TF risks;

• Develop and apply AML/CFT policies, internal

controls and programmes to adequately mitigate

identified risks;

• Apply appropriate CDD measures to identify and

verify customers and BOs and conduct ongoing

monitoring;

• Adequately detect and report suspicious

transactions; and

• Comply with other AML/CFT requirements.

AML/CFT Awareness14

Key AML/CFT Reporting Obligations from Sector 5 Policy Document

1. Risk Assessment and Client Risk

Profiling

2. CDD, ECDD & Other Requirements

3. AML/CFT Compliance Programme

4. Suspicious Transaction Report

(STR)

5. Combating Financing of

Terrorism

6. Consequences of Non-Compliance

AML/CFT Awareness15

Practical Guide on Key AML/CFT Requirements

No. What’s required Paragraph Reference in

Sector 5 Guidelines

1. Appoint a Compliance officer • 22

• 23

2. Develop and implement internal programme, policies,

procedures and controls to guard against and detect any

offence under AMLA, including

• 22

a. Policies and procedures (P&P) on overall ML/TF risk

assessment, client risk profiling, managing and

mitigating risk identified, periodic update of risk

assessment, and documentation of risk assessment and

findings

• 12

b. P&P on customer due diligence (CDD), enhanced due

diligence (EDD) and on-going due diligence (ODD)

• 13

c. Establish internal criteria (‘red flags’) to detect

suspicious transactions; and establish a reporting

system for assessment and submission of suspicious

transaction reports (STR) in a secure manner

• 23

S19

S20 -21

S22 - 27

S28 - 29

AML/CFT Awareness16

No. What’s required Paragraph Reference in

Sector 5 Guidelines

3. When in ‘doubt’, submit STR • 23

4. Check new and existing client database against the UNSCR

Consolidated List and gazette orders issued by MOHA on

domestic list of sanctioned individuals and entities

• 25

5. Conduct AML/CFT awareness and training programmes

for employees

• 22

6. Put in place adequate management information system (MIS)

to complement CDD process

• 20

7. Keep all CDD information and records for at least 6 years • 21

8. Keeping ML/TF risk assessment up-to-date through

periodic review, and having appropriate mechanisms to

provide risk assessment information to the supervisory

authority, when required

• 12

S30

S31

S32

Practical Guide on Key AML/CFT Requirements (2)

AML/CFT Awareness17

Consequences of Non-Compliance

1. Enforcement action can be taken against a reporting institution and/or on

individual directors, officers and employees for serious non-compliance with

AML/CFT requirements;

2. Penalties upon breach include:

• General Offence (section 86) – Fine not exceeding RM1.0 million e.g. for

failure to conduct CDD and failure to adopt, develop and implement

AML/CFT compliance programme;

• Retention of Records – Fine not exceeding RM3.0 million or

imprisonment for a term not exceeding five (5) years or both

• Opening Account in False Name – Fine not exceeding RM3.0 million or

imprisonment for a term not exceeding five (5) year or both

AML/CFT Awareness

Thank YouPlease visit BNM’s AML/CFT Microsite

for more information.

http://amlcft.bnm.gov.my

18

AML/CFT Awareness19

Roles and Responsibilities of Compliance Officer

WHO

High expectation on role and duty of AML/CFT Compliance Officer

RI’s compliance with AML/CFT requirements

Proper implementation of AML/CFT Procedures

Appropriate AML/CFT procedures and effective implementation

Communication channel between RIs/ staff/ department is secured and kept confidential

AML/CFT Compliance Programme awareness to all staff.

Internally generated STR are evaluated before submission to FIED

Identification of ML/TF risks associated with new products and services

DUTY – to ensure:

For individual RIs who operate within a group (e.g.: partnership):

responsible for own obligation under AMLA;

may appoint particular person (with management responsibilities) within such group to perform the role of compliance officer

1. Individual with management

responsibilities

2. Fit and proper

3. Necessary knowledge and

expertise

Back to S15

AML/CFT Awareness20

Customer risk Geography

Products, services,

transactions/ delivery channels

Other information

1 2 3

• Resident or non-resident

• Company or individual

• Company structure

• PEPs

Business location

Country of origin

Country on sanctions list

Etc.

Cash-based

Non face-to-face

Simple/ complex transactions

Etc.

4

• Suggesting higher risk, if any

RISK ASSESSMENT

RISK PROFILING

RISK CONTROL AND MITIGATION

AML/CFT Awareness21

Risk profile customer based on CDD info collected- Examples of CDD info that can be used as risk profiling factors

i. Customer risk

ii. Geographical risk

iii. Risk associated with Transaction / Delivery Channel

Document Client’s risk

profile

To freeze account if existing client,

to reject if at point of on-boarding a

new client.

Back to S15

AML/CFT Awareness22

Customer Due Diligence (CDD)

1. Three elements:

Identification VerificationOn-Going Due

Diligence

i ii iii

• Identify• Sight ID document

• Make a copy of ID document

• Review and update profile

• Transaction monitoring for consistency with known profile

AML/CFT Awareness23

Meeting AML/CFT Requirements - CDD– In practice, a quick guide

i ii iii

3. When is CDD required (Identification)?

Establishing business relations, where

applicable

If there is suspicion of ML/TF

Doubts on veracity & adequacy of previously

obtained CDD information

2. Info to obtain when conducting CDD

AML/CFT Awareness24

Identify and verify customer

Identify and take reasonable measures to verify beneficial owner (BO)

(a) Name, legal form and proof of existence(b) Powers that regulate and bind customers(c) Address of registered office

(a) Identity of the natural person who ultimately has a controlling ownership interest in a legal person

i. Identification of directors/shareholders with equity interest of 25% or more;ii. Proper authorisation for persons authorised to represent the company (letter of authority/

directors’ resolution); andiii. NRIC / Passport to identify the authorised person(s)

(b) If there is a doubt on the controlling interest - the identity of the natural person exercising control through other means

(c) Where there is no natural person identified- the identity of the natural person who holds the senior management position

Identification & verification of the BOs up to the level of natural persons who have control

Customer Due Diligence (CDD): On Legal Persons

AML/CFT Awareness25

When is Enhanced CDD Required?

Conditions

Requirements

Foreign PEPs

Customers from high risk jurisdictions (black

and grey list)

Domestic PEPs assessed as higher risk

1. Obtain CDD information

3. Inquire on source of wealth

and/or funds

4. Obtain approval from Senior Management

2. Obtain additional

informationClients assessed as

higher risk

Customer Due Diligence (CDD): Enhanced CDD

AML/CFT Awareness26

…are individuals who are or have been entrusted with prominent public

functions by their respective governments or organisations

Heads of State or of government, senior politicians, senior

government, judicial or military officials, senior executives

of state owned corporations, important political party officials

FOREIGN DOMESTICINTERNATIONAL ORGANISATION

Members of senior

management , i.e. directors,

deputy directors and members

of the board or equivalent functions.

Customer Due Diligence (CDD): On PEPs

PEPs do not include middle ranking or junior level individuals

AML/CFT Awareness27

Potential Customers Do not open the account or commence business relationship or

perform transaction

Existing Customer Terminate the business relationship

• Also, consider submitting a STR. Remember to document your rationale for submitting or

not submitting the STR

1. If the customer does not want to cooperate or refuses to provide information -What should a RI do?

2. If a RI finds a potential client to be suspicious, but believes that insistence oncompleting the CDD would tip-off the customer – What should a RI do?

• Proceed with the transaction, then immediately submit a STR to FIED, BNM

Failure to Satisfactorily Complete CDD

Back to S15

AML/CFT Awareness

Firm / RIs to establish red-flags or indicators of ML/TF

Transaction Risk:

1. Unusual or unnecessarily complicated business structures or transaction

paths

2. Use of large amount of cash

3. Unusual source of funding

4. Speed of transaction (without reasonable explanation)

5. Unexplained changes in instructions or business entities

6. Transactions where there are doubts about the validity of the documents

submitted

Customer Risk:

1. Transaction inconsistent with the individual’s known occupation or income

2. Unusual involvement of third parties / intermediaries

3. Use of legal entities that hide the identity of ultimate beneficial owner

4. Instruction outside normal geographical area, area of expertise, or client

market

5. Involvement of higher risk clients such as individuals from high risk

jurisdictions, foreign PEPs or domestic PEPs assessed as high risk etc.

6. Formation of shell companies and/or with unclear business purpose

7. Avoiding personal contact without good reason

28

AML/CFT Awareness29

Suspicious Transaction Report: Reporting Mechanism

Internal reporting mechanism:

• RI to have in place policies on

duration taken by Compliance

Officer to review internal STR and

circumstances the timeframe can be

exceeded

TIPPING OFF:

• If RI has formed a suspicion of ML/TF but

believes that performing CDD process would

tip-off the customer, RI is permitted not to

pursue CDD, to proceed with the transaction

and immediately file a STR

Back to S15

Establish clear P&P to guide all staff, which should include:

Guidance on the type of client behavior or transactions that could be considered as

suspicious i.e. internal criteria/red-flags

What to do when doubt arises e.g. types of further scrutiny to conduct, consider

submitting STR if suspicion remains

Who to submit STR to within the firm and where to get STR forms i.e. sample/template

Method for submitting STRs - by staff to CO, by CO to FIED,BNM - to preserve

confidentiality

Timeframe for initial assessment by staff upon formation of doubt before raising STR to

CO, assessment by CO before submitting STR to FIED, BNM

Method for recording of assessment and decision not to submit STR received from staff

and secure filing of these documents for at least 6 years.

AML/CFT Awareness30

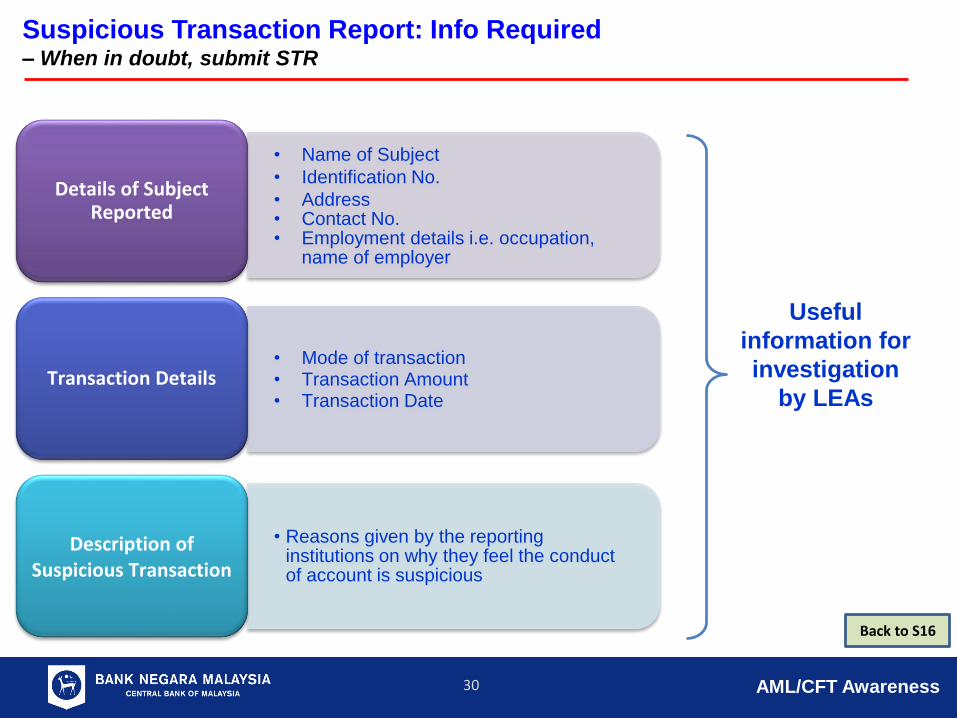

Suspicious Transaction Report: Info Required – When in doubt, submit STR

Useful

information for

investigation

by LEAs

• Name of Subject

• Identification No.

• Address• Contact No.• Employment details i.e. occupation,

name of employer

Details of Subject Reported

• Mode of transaction• Transaction Amount• Transaction Date

Transaction Details

• Reasons given by the reporting institutions on why they feel the conduct of account is suspicious

Description of Suspicious Transaction

Back to S16

AML/CFT Awareness31

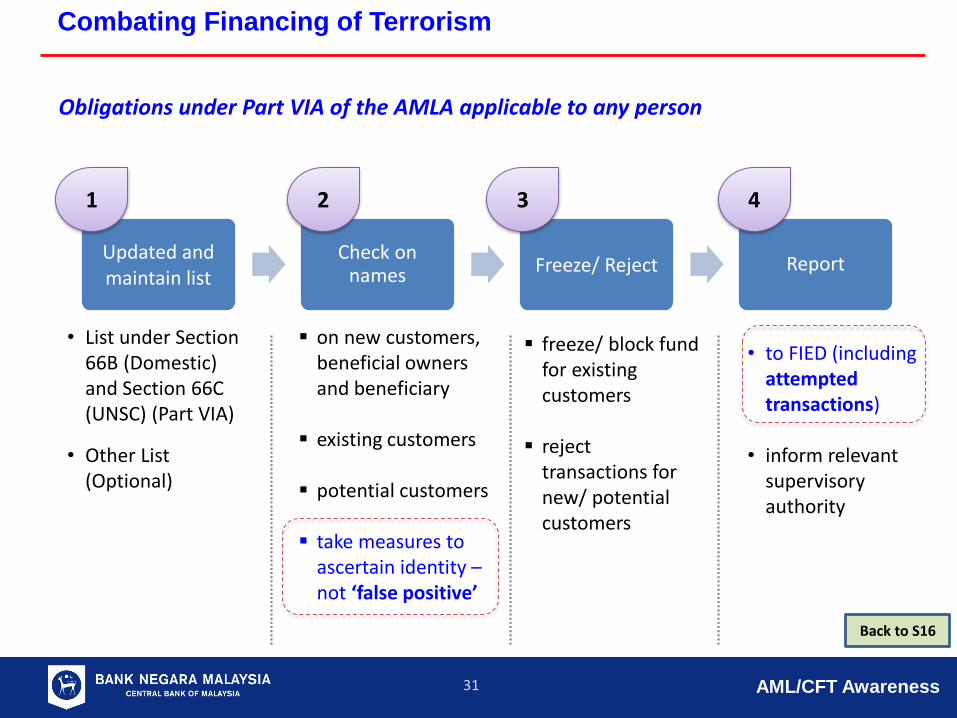

Combating Financing of Terrorism

Updated and maintain list

Check on names Freeze/ Reject Report

1 2 3

• List under Section 66B (Domestic) and Section 66C (UNSC) (Part VIA)

• Other List (Optional)

on new customers, beneficial owners and beneficiary

existing customers

potential customers

take measures to ascertain identity –not ‘false positive’

freeze/ block fund for existing customers

reject transactions for new/ potential customers

4

• to FIED (including attempted transactions)

• inform relevant supervisory authority

Obligations under Part VIA of the AMLA applicable to any person

Back to S16

AML/CFT Awareness32

AML/CFT Training

• Tailored to staff level & nature of works;

• Frequency – correlate with level of risk

Record-keeping

• All records relating to transactions, CDD etcmust be properly maintained, for at least 6 years from the point of termination of the business relationship with the client

Management Information System

• Not necessarily automated

• To commensurate with nature, scale and complexity of operations

Other Requirements

Back to S16