private credit, public debt, and financial crises

TRANSCRIPT

Prepared for FRBSF Seminar: Understanding the Slow Recovery

April 10, 2013

Òscar Jordà Research Advisor

Federal Reserve Bank of San Francisco

Thanks to Early Elias for research assistance, and FRBSF Community Development, Economic Research

for advice. Based on work with Moritz Schularick (U. of Bonn) and Alan M. Taylor (U. of Virginia).

Private Credit, Public Debt, and

Financial Crises

140 years, 17 countries: Lessons

1. The long view and emerging trends

2. Credit and financial crises

3. Public debt and the recovery

4. Implications for policymakers

2

The long view and emerging trends

3

Financial crises return…Why?

4

0

1

2

3

4

5

6

7

8

9

1870 1880 1890 1900 1910 1920 1930 1940 1950 1960 1970 1980 1990 2000 2010

Countries experiencing a crisis in a given yearFinancial Crises

Out of 17

Bretton

Woods

Bretton Woods: what was different?

• Capital controls

• Fixed exchange rates

• Low leverage banking

• Govt. securities a much higher proportion of bank assets (less portfolio risk)

• Primitive finance did not hinder investment: Average growth = 3.8% in 1947-1970, 3.2% in 1971-2007

• BW eventually collapsed 5

Banking sector explodes since Bretton Woods

6

0

50

100

150

200

250

1870 1880 1890 1900 1910 1920 1930 1940 1950 1960 1970 1980 1990 2000 2010

As a percent of GDP, average across 17 countries

Bank Lending, Bank Assets and MoneyPercent

Bank assets

Bank loans

Money

Bretton Woodsends

Age of money ushers the age of credit

7

-200

-150

-100

-50

0

50

100

150

1870 1880 1890 1900 1910 1920 1930 1940 1950 1960 1970 1980 1990 2000 2010

Average across 17 countries

Bank Aggregates Relative to Money Percent

Bank assets

Bank loans

From nuts and bolts to bricks and mortar

8

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

1880 1890 1900 1910 1920 1930 1940 1950 1960 1970 1980 1990 2000 2010

Ratio of US Real Estate Lending to US Total Lending Ratio

Commercial

Household

Total real estate

Total Liabilities then and now

9

0

100

200

300

400

500

6002007 Percent

0

100

200

300

400

500

6001928 Percent

Public debtBank liabilities

Unprecedented reversal of reserves

• Lesson of 1990s emerging markets (EM) crises:

– Crisis more painful w/o foreign reserves

• Since:

– Globalization = expansion of balance sheets

– Private capital flows from DM to EM

– Official capital flows from EM to DM

• Great Reserve Accumulation: $10T officially + $4T in sovereign wealth funds

10

Demographic trends reversing: Savings?

11

45

50

55

60

65

70

75

80

85

1970 1980 1990 2000 2010 2020 2030 2040 2050Source: U.N. Population Statistics; see Pradhan and Taylor (2011)

Working age = ages 20-64; dependents = ages 0-19 and 65+

Dependents as a Percentage of Working AgePercent

World

Less developed

More developed

Recent trends are game changers

• Unprecedented expansion of credit: financial

assets/GDP = 150% in 1975 → 350% in 2008.

Bank loans/GDP doubled.

• The banks’ asset mix: govt. securities 60-70% in

1950; 0% in the 2000s

• Switch to wholesale funding (uninsured) from

deposits (insured): Shadow banking

• Public debt growing globally before the crisis

12

Credit and financial crises

13

Financial crises are different

14

-10

-5

0

5

10

15

0 1 2 3 4 5

Cumulative change from the start of the recession

USA real GDP per capita

Years

Percentage points

Financial

Normal

Financial crises: disinvestment and deflation

15

-70

-60

-50

-40

-30

-20

-10

0

10

20

30

40

0 1 2 3 4 5

Cummulative change from the start of the recession

USA Investment

Years

Percentage points

Financial

Normal

-15

-10

-5

0

5

10

15

20

25

0 1 2 3 4 5

Cumulative change since the start of the recession

USA CPI Prices

Years

Percentage points

Financial

Normal

Private credit predicts financial crises

Predict financial crises with: (1) (2) (3) (4) (5)

Change in private credit - -

Change in public debt - -

Level of credit/GDP - - - -

Level of debt/GDP - - - -

Both interacted - - -

AUC 0.72 0.61 0.71 0.71 0.62

16

• Public debt does not work

• External imbalances (not shown) do no work

• Let’s not kid ourselves, financial crises are difficult to predict

Excess credit trumps debt accumulation

17

-8

-6

-4

-2

0

2

4

6

0 1 2 3 4 5

Normal vs. financial as a function of credit and debt

The Recession and the Recovery

Years

Percent

Normal

Low credit

and low debt

Low credit

and high debt

High credit

and low debt

High credit

and high debt

Public debt and the recovery

18

Public debt growing again…

19

0

20

40

60

80

100

120

140

1870 1890 1910 1930 1950 1970 1990 2010

Total Public Debt to GDP Ratio Percent of GDP

USA

Average (exclud. USA and Japan)

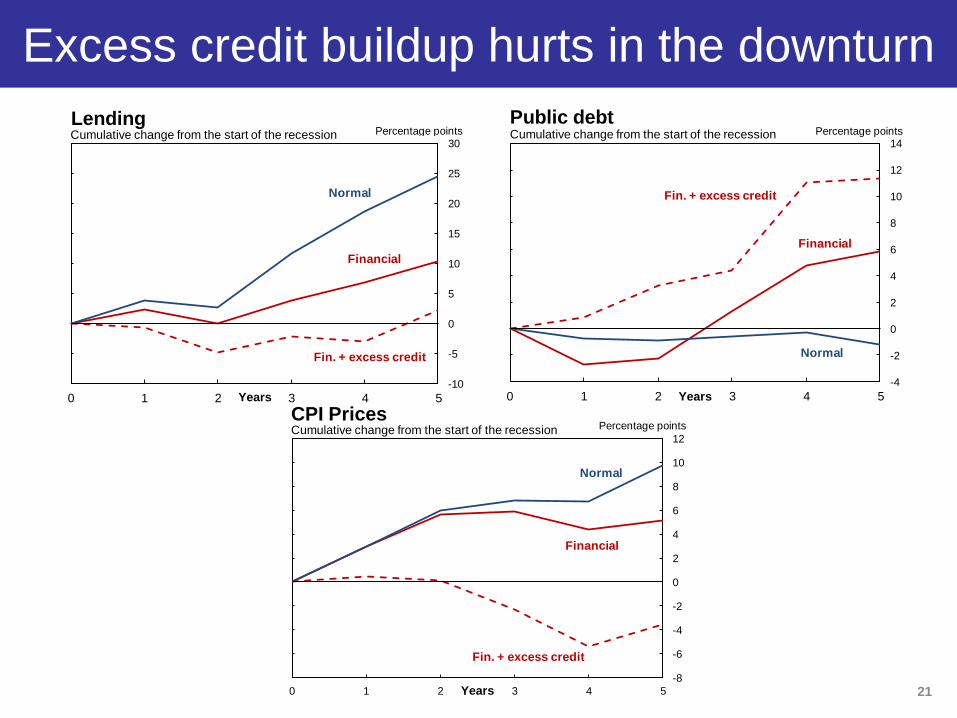

Excess credit buildup hurts in the downturn

20

-10

-8

-6

-4

-2

0

2

4

6

0 1 2 3 4 5

Cumulative change from the start of the recessionReal GDP per capita

Years

Percentage points

Financial

Fin. + excess credit

Normal

Norm. + excess credit

Excess credit buildup hurts in the downturn

21 -8

-6

-4

-2

0

2

4

6

8

10

12

0 1 2 3 4 5

Cumulative change from the start of the recessionCPI Prices

Years

Percentage points

Financial

Fin. + excess credit

Normal

-10

-5

0

5

10

15

20

25

30

0 1 2 3 4 5

Cumulative change from the start of the recessionLending

Years

Percentage points

Financial

Fin. + excess credit

Normal

-4

-2

0

2

4

6

8

10

12

14

0 1 2 3 4 5

Cumulative change from the start of the recession

Public debt

Years

Percentage points

Financial

Fin. + excess credit

Normal

The level of debt matters in the downturn

22

-12

-10

-8

-6

-4

-2

0

2

4

6

0 1 2 3 4 5

Cumulative change from the start of the recessionReal GDP per capita

Years

Percentage points

Normal

FinancialDebt/GDP = 50

FinancialDebt/GDP = 100

-25

-20

-15

-10

-5

0

5

10

15

0 1 2 3 4 5

Cumulative change from the start of the recessionCPI Prices

Years

Percentage points

Normal

FinancialDebt/GDP = 50

FinancialDebt/GDP = 100

-10

-5

0

5

10

15

20

25

30

0 1 2 3 4 5

Cumulative change from the start of the recession

Lending

Years

Percentage points

Normal

FinancialDebt/GDP = 50

FinancialDebt/GDP = 100

-20

-15

-10

-5

0

5

10

0 1 2 3 4 5

Cumulative change from the start of the recessionPublic Debt

Years

Percentage points

Normal

FinancialDebt/GDP = 50

FinancialDebt/GDP = 100

US vs UK recovery (± shadow banking)

23

-10

-5

0

5

10

15

0 1 2 3 4 5

Cumulative change since the start of the 2007 recession

UK real GDP per capita

Years

Percentage points

Actual

Predicted

Normal

-10

-5

0

5

10

15

0 1 2 3 4

Cumulative change since the start of the 2007 recession

USA real GDP per capita

Years

Percentage points

Actual

Predicted

Normal

Implications for policymakers

24

Maybe this time is different

• Monitor credit and leverage. New age of

credit:

– Excess credit makes recessions worse,

recoveries slower

– Turns some into financial crises

• Excess public debt:

– Not the same as credit

– But high levels complicate recoveries from

financial crises

• New EM and demographic trends

25

Further reading

26

Useful References

• Jordà, Òscar. 2012. Credit: A Starring Role in the Downturn. FRBSF Economic Letter, 2012-12.

• Jordà, Òscar, Moritz Schularick and Alan M. Taylor. 2011. Financial Crises, Credit Booms, and External Imbalances: 140 Years of Lessons. IMF Economic Review, 59.

• Jordà, Òscar, Moritz Schularick and Alan M. Taylor. 2012. When Credit Bites Back: Leverage, Business Cycles, and Crises. FRBSF working paper.

• Reinhart, Carmen M. and Kenneth Rogoff. 2009. This Time Is Different: Eight Centuries of Financial Folly. Princeton University Press.

• Schularick, Moritz and Alan M. Taylor. 2012. Credit Booms Gone Bust: Monetary Policy, Leverage Cycles, and Financial Crises, 1870-2008. American Economic Review, 102(2).

• Taylor, Alan M. 2012. The Great Leveraging. NBER working paper 18290 27