private equity & venture capital alternative financing option equity - jacob... · private...

TRANSCRIPT

Private Equity & Venture Capital – Alternative Financing

Option

Indian Association of Investment Professionals

Shwetank Patni

July 6, 2013

1

Agenda

I. Understanding Private Equity

I. Types of Equity Funding

II. Why PE Funding

III. PE Funding Process

II. PE Industry – Current Status

I. Industry Trends

II. Current Challenges

III. Recent Developments

III. Annexures

Presentation only for reference purposes. Not to be reproduced anywhere. Please see disclaimer on disclaimer slide

2

Agenda

I. Understanding Private Equity

I. Types of Equity Funding

II. Why PE Funding

III. PE Funding Process

II. PE Industry – Current Status

I. Industry Trends

II. Current Challenges

III. Recent Developments

III. Annexures

Presentation only for reference purposes. Not to be reproduced anywhere. Please see disclaimer on disclaimer slide

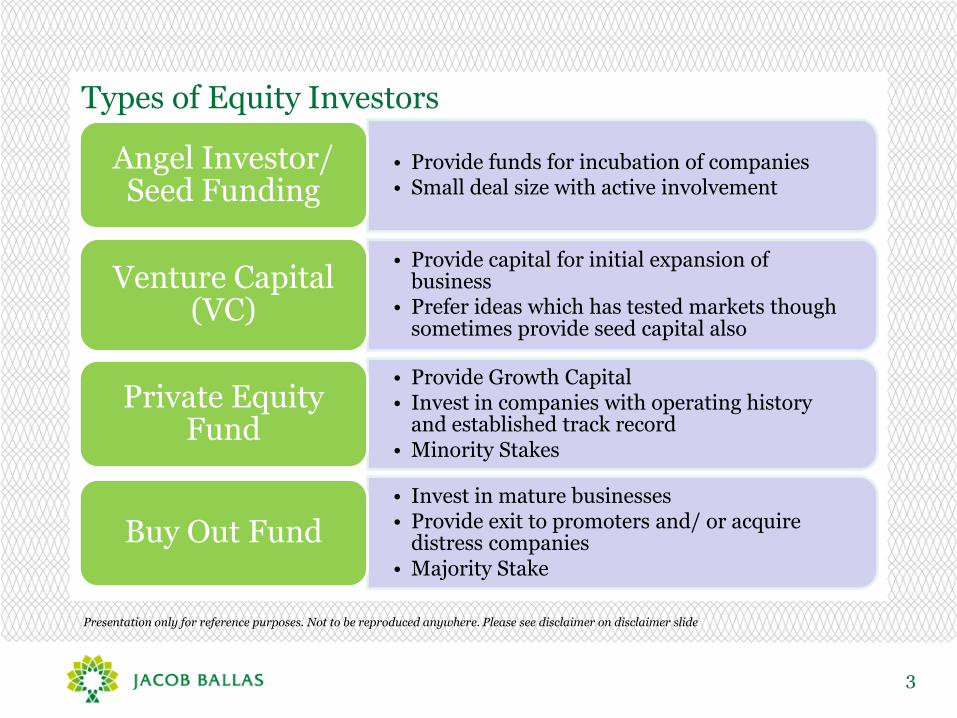

Types of Equity Investors

3

Presentation only for reference purposes. Not to be reproduced anywhere. Please see disclaimer on disclaimer slide

• Provide funds for incubation of companies • Small deal size with active involvement

Angel Investor/ Seed Funding

• Provide capital for initial expansion of business

• Prefer ideas which has tested markets though sometimes provide seed capital also

Venture Capital (VC)

• Provide Growth Capital • Invest in companies with operating history

and established track record • Minority Stakes

Private Equity Fund

• Invest in mature businesses • Provide exit to promoters and/ or acquire

distress companies • Majority Stake

Buy Out Fund

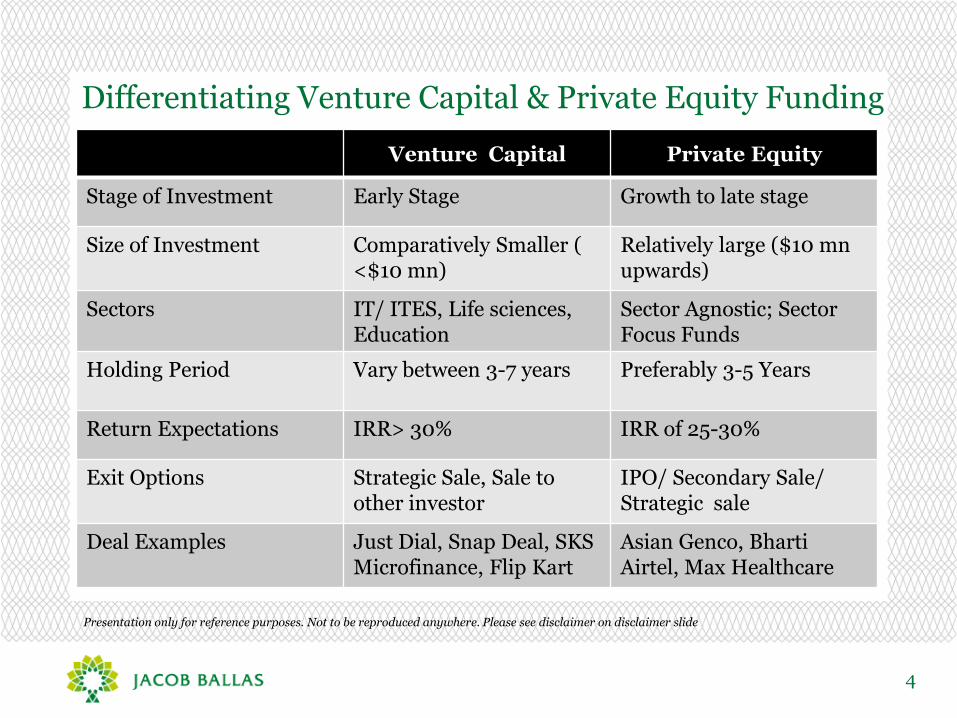

Differentiating Venture Capital & Private Equity Funding

4

Venture Capital Private Equity

Stage of Investment Early Stage Growth to late stage

Size of Investment Comparatively Smaller ( <$10 mn)

Relatively large ($10 mn upwards)

Sectors IT/ ITES, Life sciences, Education

Sector Agnostic; Sector Focus Funds

Holding Period Vary between 3-7 years Preferably 3-5 Years

Return Expectations IRR> 30% IRR of 25-30%

Exit Options Strategic Sale, Sale to other investor

IPO/ Secondary Sale/ Strategic sale

Deal Examples Just Dial, Snap Deal, SKS Microfinance, Flip Kart

Asian Genco, Bharti Airtel, Max Healthcare

Presentation only for reference purposes. Not to be reproduced anywhere. Please see disclaimer on disclaimer slide

5

Presentation only for reference purposes. Not to be reproduced anywhere. Please see disclaimer on disclaimer slide

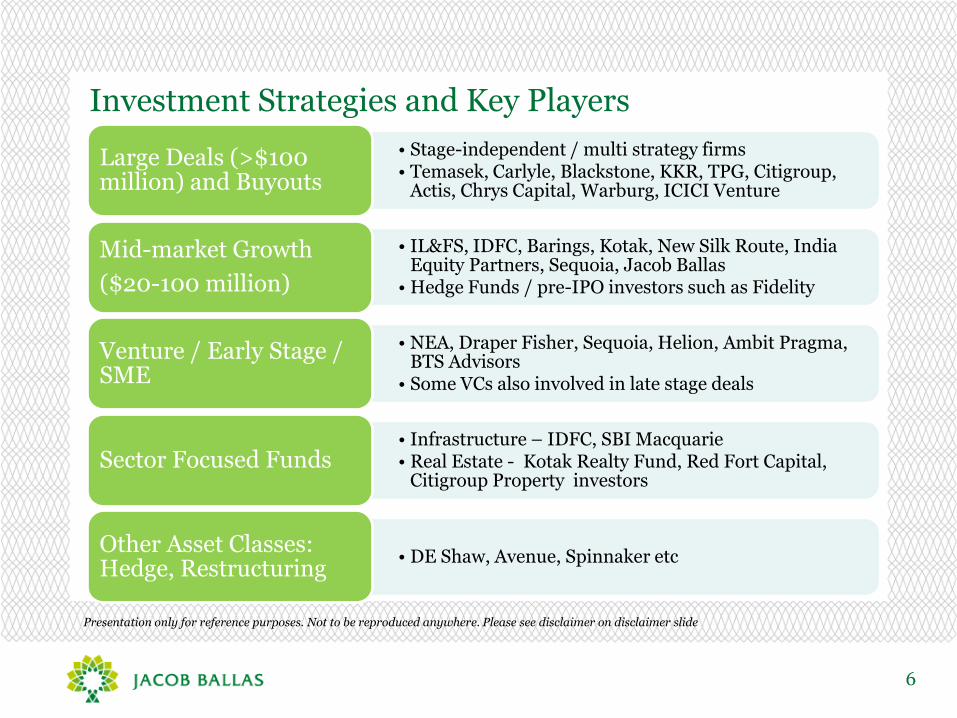

Investment Strategies and Key Players

6

• Stage-independent / multi strategy firms • Temasek, Carlyle, Blackstone, KKR, TPG, Citigroup,

Actis, Chrys Capital, Warburg, ICICI Venture

Large Deals (>$100 million) and Buyouts

• IL&FS, IDFC, Barings, Kotak, New Silk Route, India Equity Partners, Sequoia, Jacob Ballas

• Hedge Funds / pre-IPO investors such as Fidelity

Mid-market Growth

($20-100 million)

• NEA, Draper Fisher, Sequoia, Helion, Ambit Pragma, BTS Advisors

• Some VCs also involved in late stage deals

Venture / Early Stage / SME

• Infrastructure – IDFC, SBI Macquarie • Real Estate - Kotak Realty Fund, Red Fort Capital,

Citigroup Property investors Sector Focused Funds

• DE Shaw, Avenue, Spinnaker etc Other Asset Classes: Hedge, Restructuring

Presentation only for reference purposes. Not to be reproduced anywhere. Please see disclaimer on disclaimer slide

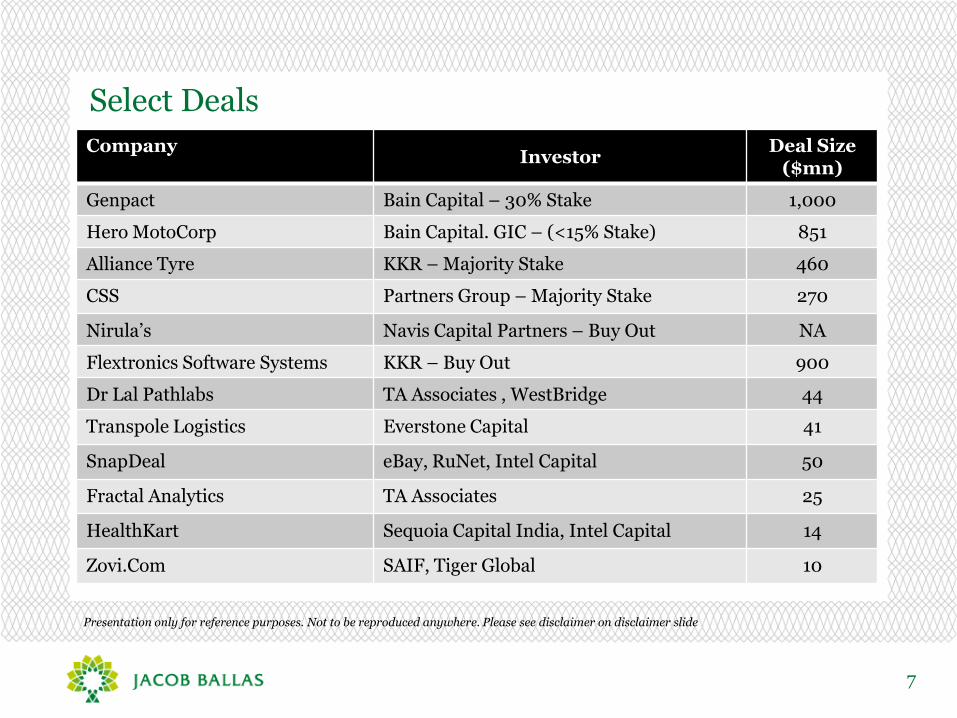

Select Deals

7

Presentation only for reference purposes. Not to be reproduced anywhere. Please see disclaimer on disclaimer slide

Company Investor

Deal Size ($mn)

Genpact Bain Capital – 30% Stake 1,000

Hero MotoCorp Bain Capital. GIC – (<15% Stake) 851

Alliance Tyre KKR – Majority Stake 460

CSS Partners Group – Majority Stake 270

Nirula’s Navis Capital Partners – Buy Out NA

Flextronics Software Systems KKR – Buy Out 900

Dr Lal Pathlabs TA Associates , WestBridge 44

Transpole Logistics Everstone Capital 41

SnapDeal eBay, RuNet, Intel Capital 50

Fractal Analytics TA Associates 25

HealthKart Sequoia Capital India, Intel Capital 14

Zovi.Com SAIF, Tiger Global 10

8

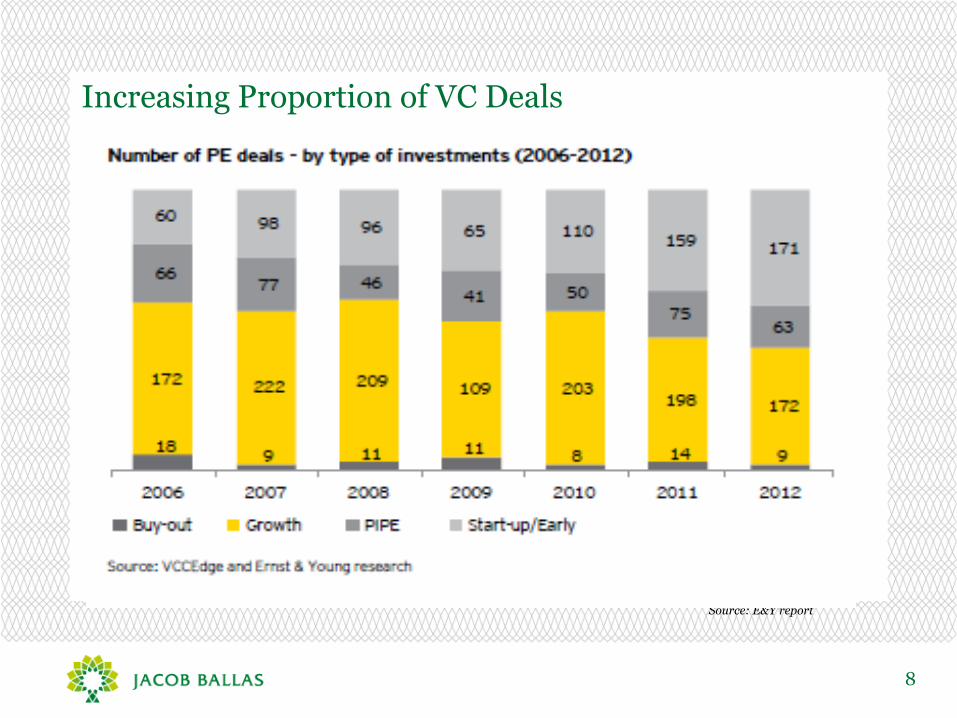

Increasing Proportion of VC Deals

Source: E&Y report

9

Deal Profile Varies Across Geographies

10

Agenda

I. Understanding Private Equity

I. Types of Equity Funding

II. Why PE Funding

III. PE Funding Process

II. PE Industry – Current Status

I. Industry Trends

II. Current Challenges

III. Recent Developments

III. Annexures

Presentation only for reference purposes. Not to be reproduced anywhere. Please see disclaimer on disclaimer slide

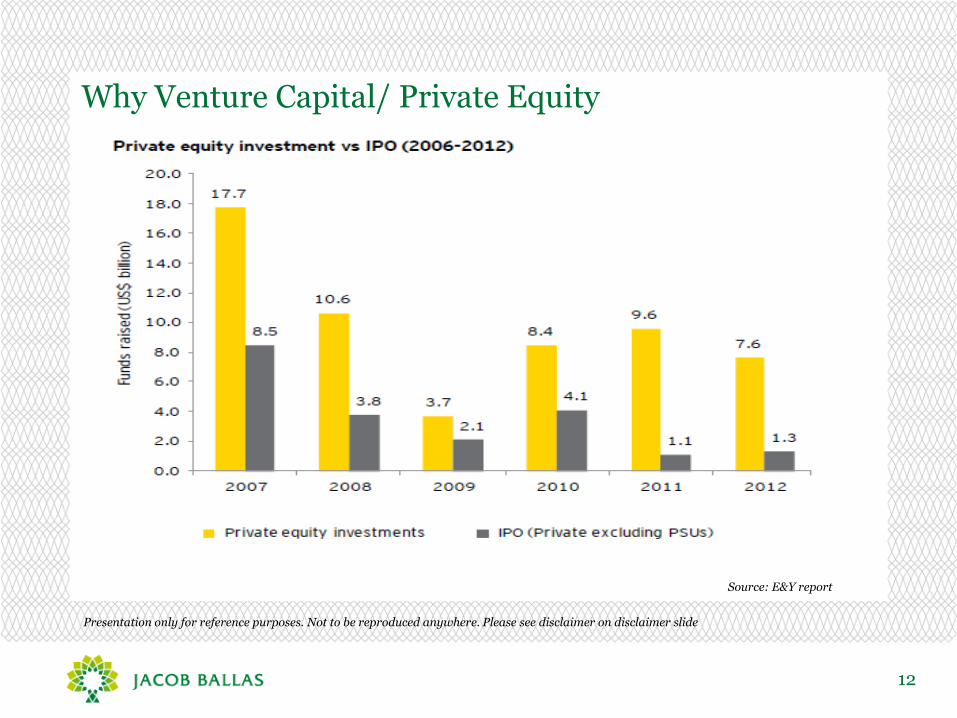

Why Venture Capital/ Private Equity

11

VC/ PE is More Than Just Money

Value Addition Sets a Pricing Benchmark Establishes Credibility

Only Possible Option in Specific Situations

Early stage companies Leveraged and Promoter Funding Not

Available

Better Option than IPO

Low regulatory compliances Possible even in Tough

Market Conditions Faster process at lower cost

Better Option than Debt

No Security required No regular commitments Lesser Covenants

Presentation only for reference purposes. Not to be reproduced anywhere. Please see disclaimer on disclaimer slide

Why Venture Capital/ Private Equity

12

Presentation only for reference purposes. Not to be reproduced anywhere. Please see disclaimer on disclaimer slide

Source: E&Y report

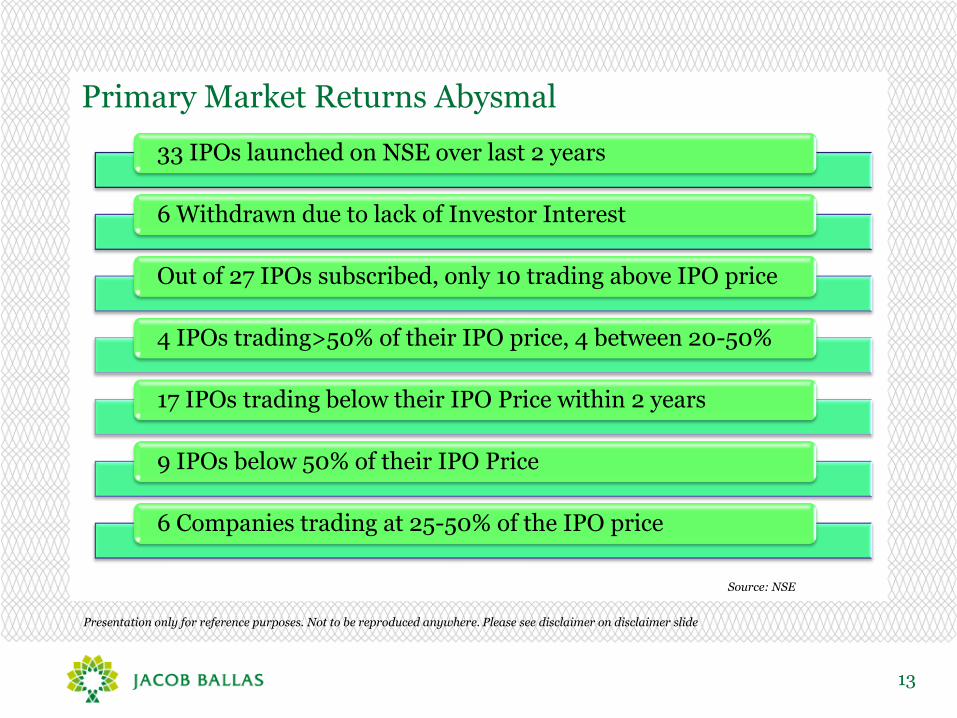

Primary Market Returns Abysmal

13

Presentation only for reference purposes. Not to be reproduced anywhere. Please see disclaimer on disclaimer slide

Source: NSE

33 IPOs launched on NSE over last 2 years

6 Withdrawn due to lack of Investor Interest

Out of 27 IPOs subscribed, only 10 trading above IPO price

4 IPOs trading>50% of their IPO price, 4 between 20-50%

17 IPOs trading below their IPO Price within 2 years

9 IPOs below 50% of their IPO Price

6 Companies trading at 25-50% of the IPO price

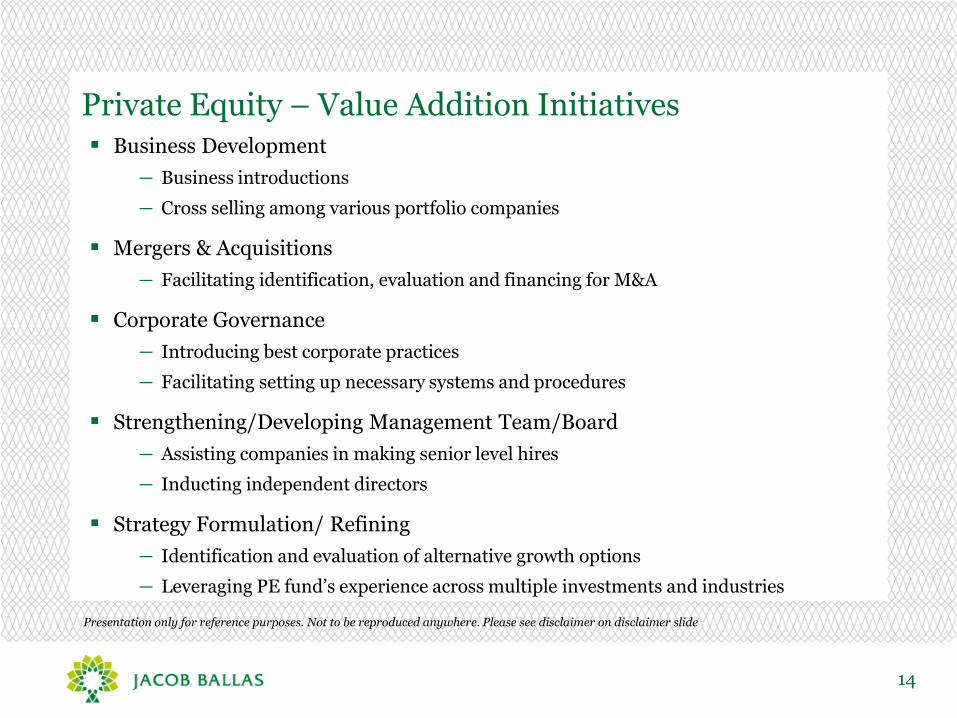

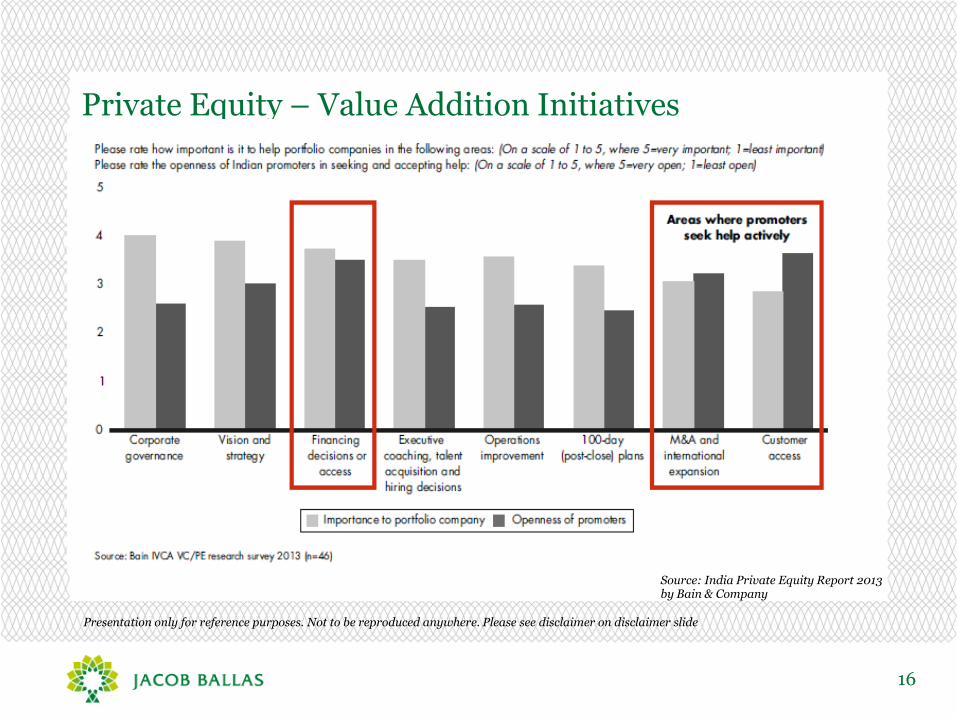

Private Equity – Value Addition Initiatives

14

Business Development

― Business introductions

― Cross selling among various portfolio companies

Mergers & Acquisitions

― Facilitating identification, evaluation and financing for M&A

Corporate Governance

― Introducing best corporate practices

― Facilitating setting up necessary systems and procedures

Strengthening/Developing Management Team/Board

― Assisting companies in making senior level hires

― Inducting independent directors

Strategy Formulation/ Refining

― Identification and evaluation of alternative growth options

― Leveraging PE fund’s experience across multiple investments and industries

Presentation only for reference purposes. Not to be reproduced anywhere. Please see disclaimer on disclaimer slide

Private Equity – Value Addition Initiatives

15

Operations & Systems Improvement

― Improvement in MIS

― Cost optimization

Fund Raising

― Identification and evaluation of alternative fund raising options

― Working with the company to provide necessary inputs to a potential investor

IPO/ Listing Preparation

― Selection of bankers, lawyers and other intermediaries

― Support in preparation and review of offer documents

― Support in pre-IPO transaction, if any

Presentation only for reference purposes. Not to be reproduced anywhere. Please see disclaimer on disclaimer slide

Private Equity – Value Addition Initiatives

16

Presentation only for reference purposes. Not to be reproduced anywhere. Please see disclaimer on disclaimer slide

Source: India Private Equity Report 2013 by Bain & Company

Blackstone – Intelenet*

17

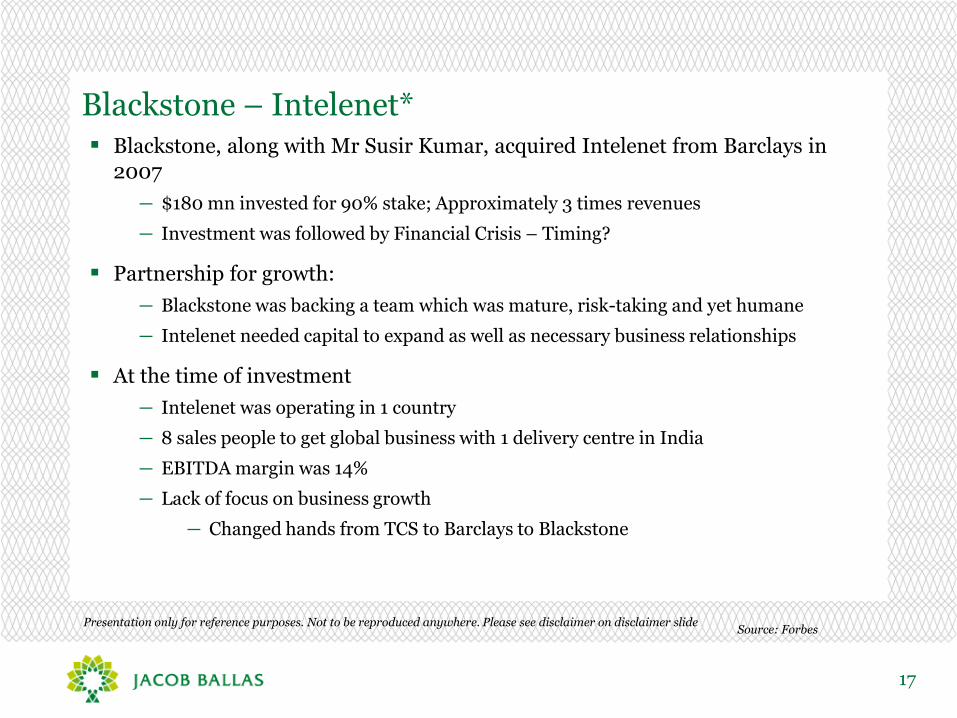

Blackstone, along with Mr Susir Kumar, acquired Intelenet from Barclays in 2007

― $180 mn invested for 90% stake; Approximately 3 times revenues

― Investment was followed by Financial Crisis – Timing?

Partnership for growth:

― Blackstone was backing a team which was mature, risk-taking and yet humane

― Intelenet needed capital to expand as well as necessary business relationships

At the time of investment

― Intelenet was operating in 1 country

― 8 sales people to get global business with 1 delivery centre in India

― EBITDA margin was 14%

― Lack of focus on business growth

― Changed hands from TCS to Barclays to Blackstone

Presentation only for reference purposes. Not to be reproduced anywhere. Please see disclaimer on disclaimer slide Source: Forbes

Blackstone – Intelenet*

18

Initiatives Takes

― Strengthening top management team

― ESOPs to employees to align interest

― Introduction to global investee companies of Blackstone

― Expand sales team; Significant investment in improving sales network

― Cost rationalisation

At the time of Exit

― Intelenet was operating in 7 countries

― 25 percent of Intelenet’s revenues come from Blackstone’s portfolio companies

― Sales team expanded to 41 people

― EBITDA margin was 20%

Blackstone exited Intelenet in 2011 – Sale to Serco @ 3.0x Invested Capital

Wealth creation for employees through ESOPs

Presentation only for reference purposes. Not to be reproduced anywhere. Please see disclaimer on disclaimer slide Source: Forbes

19

Agenda

I. Understanding Private Equity

I. Types of Equity Funding

II. Why PE Funding

III.PE Funding Process

II. PE Industry – Current Status

I. Industry Trends

II. Current Challenges

III. Recent Developments

III. Annexures

Presentation only for reference purposes. Not to be reproduced anywhere. Please see disclaimer on disclaimer slide

Investment Lifecycle

20

Preparing the Company for Investment

Investment Process

Monitoring

Exit

Presentation only for reference purposes. Not to be reproduced anywhere. Please see disclaimer on disclaimer slide

21

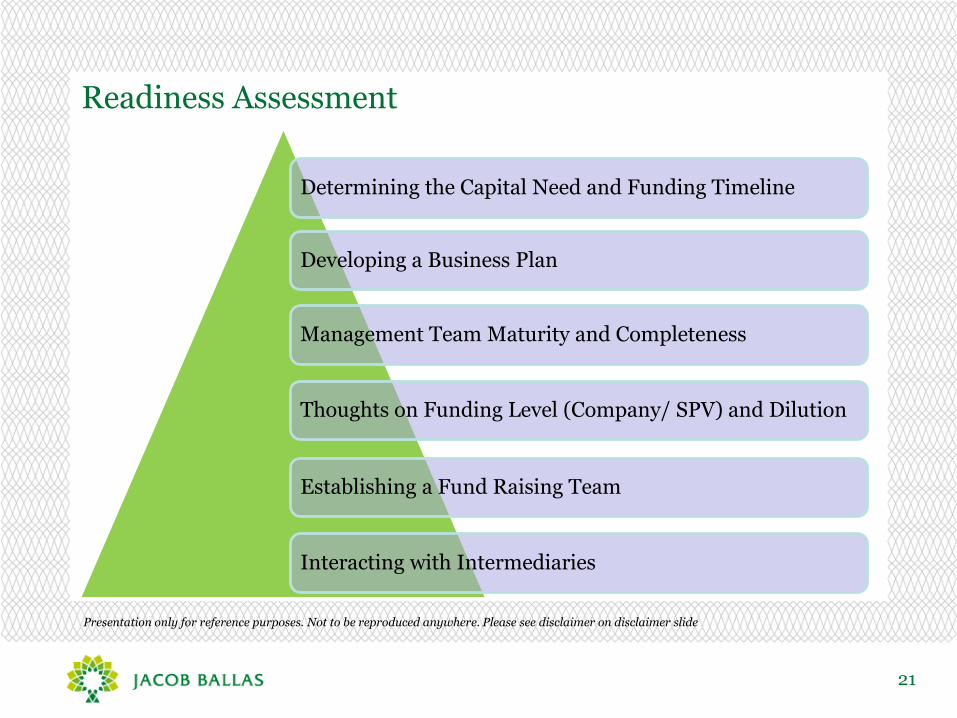

Readiness Assessment

Determining the Capital Need and Funding Timeline

Developing a Business Plan

Management Team Maturity and Completeness

Thoughts on Funding Level (Company/ SPV) and Dilution

Establishing a Fund Raising Team

Interacting with Intermediaries

Presentation only for reference purposes. Not to be reproduced anywhere. Please see disclaimer on disclaimer slide

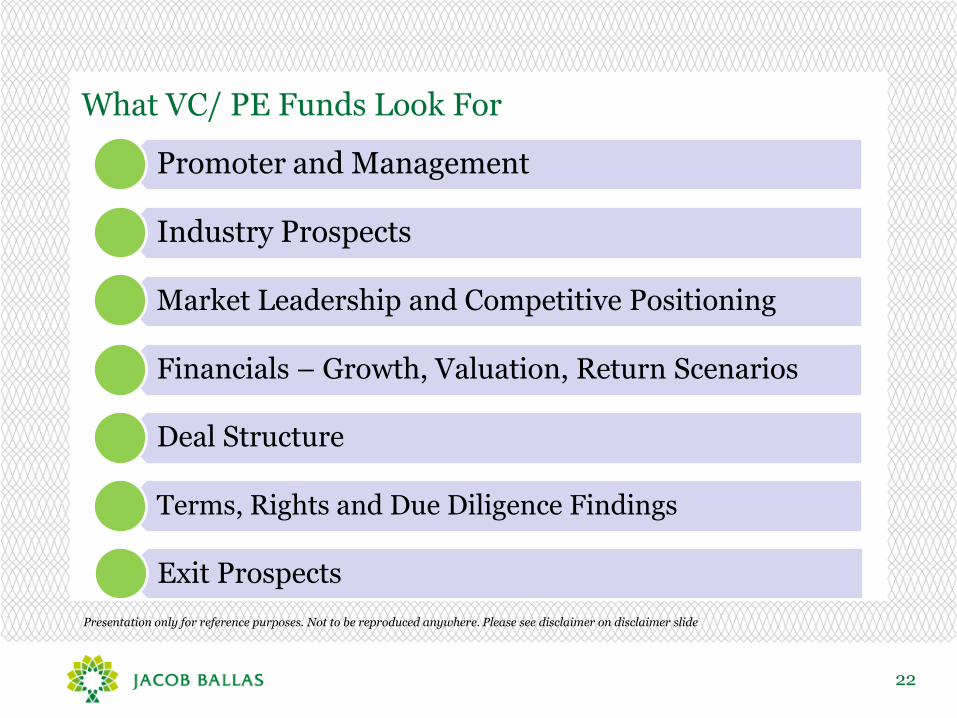

What VC/ PE Funds Look For

22

Presentation only for reference purposes. Not to be reproduced anywhere. Please see disclaimer on disclaimer slide

Promoter and Management

Industry Prospects

Market Leadership and Competitive Positioning

Financials – Growth, Valuation, Return Scenarios

Deal Structure

Terms, Rights and Due Diligence Findings

Exit Prospects

23

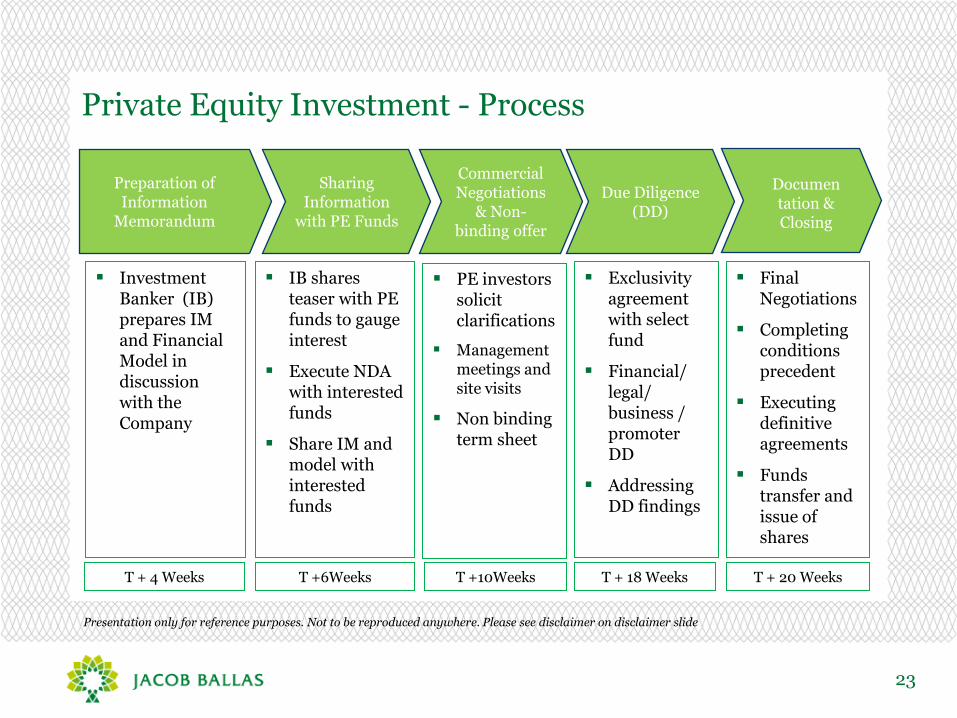

Private Equity Investment - Process

Preparation of Information

Memorandum

Sharing Information

with PE Funds

Due Diligence (DD)

Documentation & Closing

Commercial Negotiations

& Non-binding offer

Investment Banker (IB) prepares IM and Financial Model in discussion with the Company

IB shares teaser with PE funds to gauge interest

Execute NDA with interested funds

Share IM and model with interested funds

PE investors solicit clarifications

Management meetings and site visits

Non binding term sheet

Exclusivity agreement with select fund

Financial/ legal/ business / promoter DD

Addressing DD findings

Final Negotiations

Completing conditions precedent

Executing definitive agreements

Funds transfer and issue of shares

T + 4 Weeks

T +6Weeks

T + 18 Weeks

T + 20 Weeks

T +10Weeks

Presentation only for reference purposes. Not to be reproduced anywhere. Please see disclaimer on disclaimer slide

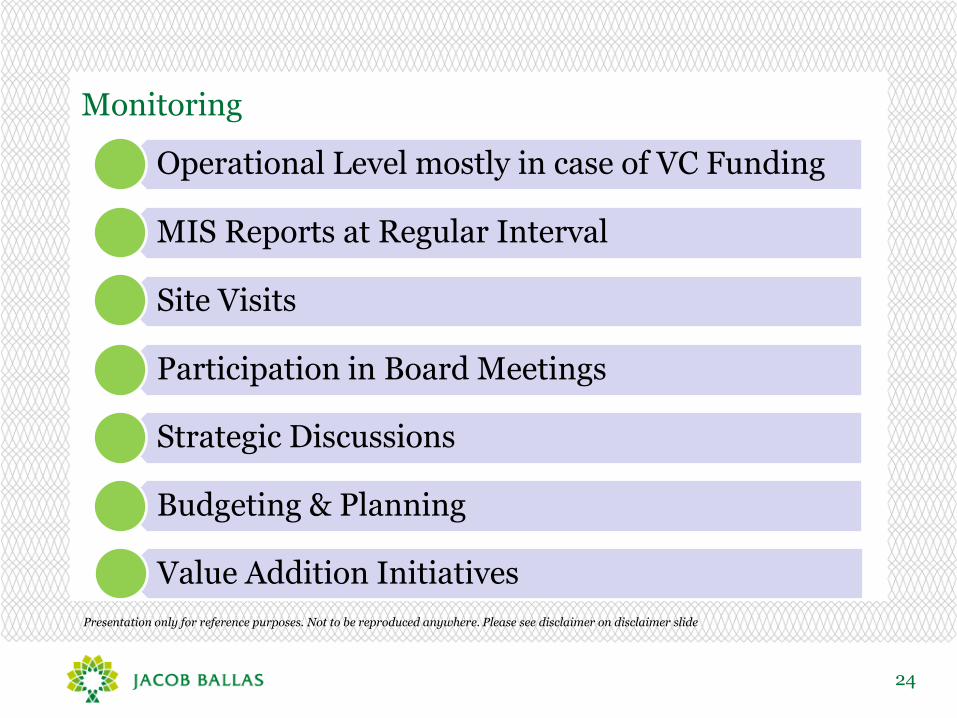

Monitoring

24

Operational Level mostly in case of VC Funding

MIS Reports at Regular Interval

Site Visits

Participation in Board Meetings

Strategic Discussions

Budgeting & Planning

Value Addition Initiatives

Presentation only for reference purposes. Not to be reproduced anywhere. Please see disclaimer on disclaimer slide

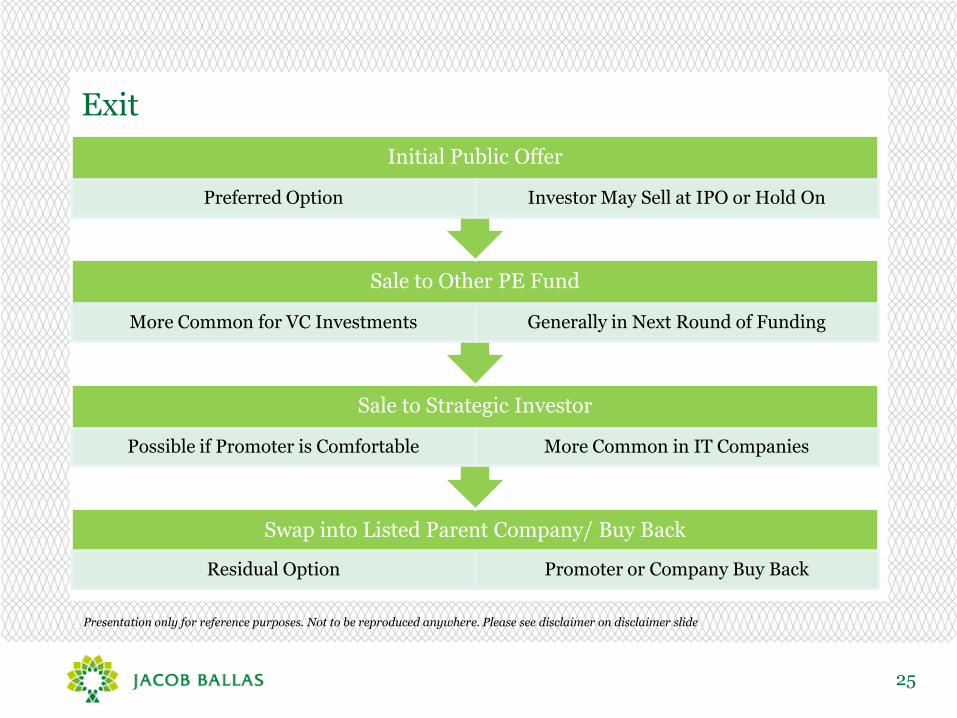

Exit

25

Swap into Listed Parent Company/ Buy Back

Residual Option Promoter or Company Buy Back

Sale to Strategic Investor

Possible if Promoter is Comfortable More Common in IT Companies

Sale to Other PE Fund

More Common for VC Investments Generally in Next Round of Funding

Initial Public Offer

Preferred Option Investor May Sell at IPO or Hold On

Presentation only for reference purposes. Not to be reproduced anywhere. Please see disclaimer on disclaimer slide

26

Agenda

I. Understanding Private Equity

I. Types of Equity Funding

II. Why PE Funding

III. PE Funding Process

II. PE Industry – Current Status

I. Industry Trends

II. Current Challenges

III. Recent Developments

III. Annexures

Presentation only for reference purposes. Not to be reproduced anywhere. Please see disclaimer on disclaimer slide

27

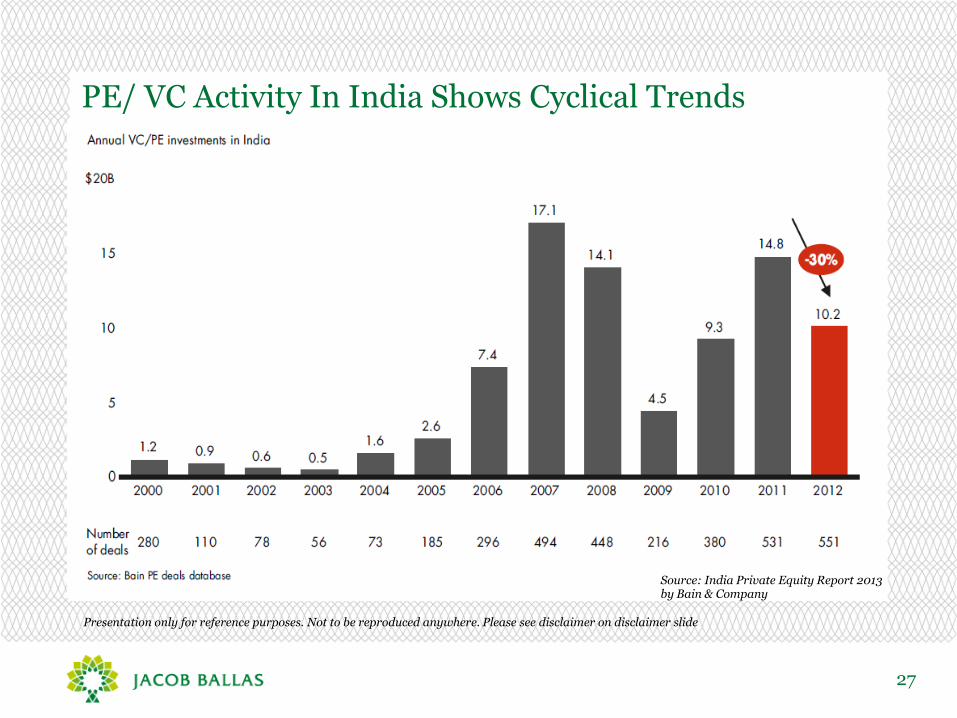

PE/ VC Activity In India Shows Cyclical Trends

Presentation only for reference purposes. Not to be reproduced anywhere. Please see disclaimer on disclaimer slide

Source: India Private Equity Report 2013 by Bain & Company

28

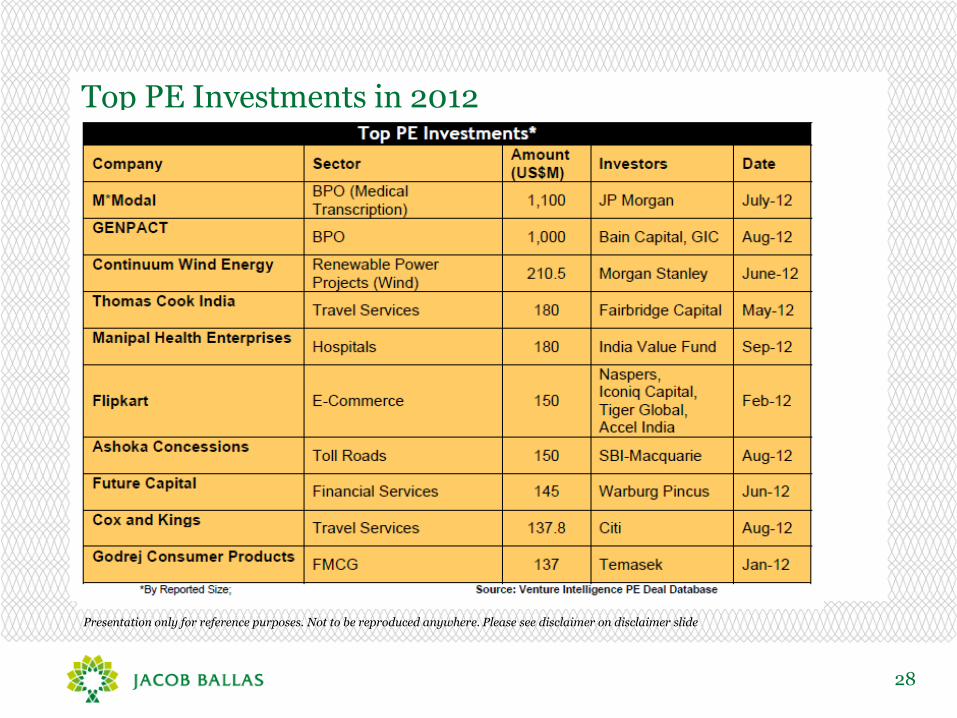

Top PE Investments in 2012

Presentation only for reference purposes. Not to be reproduced anywhere. Please see disclaimer on disclaimer slide

29

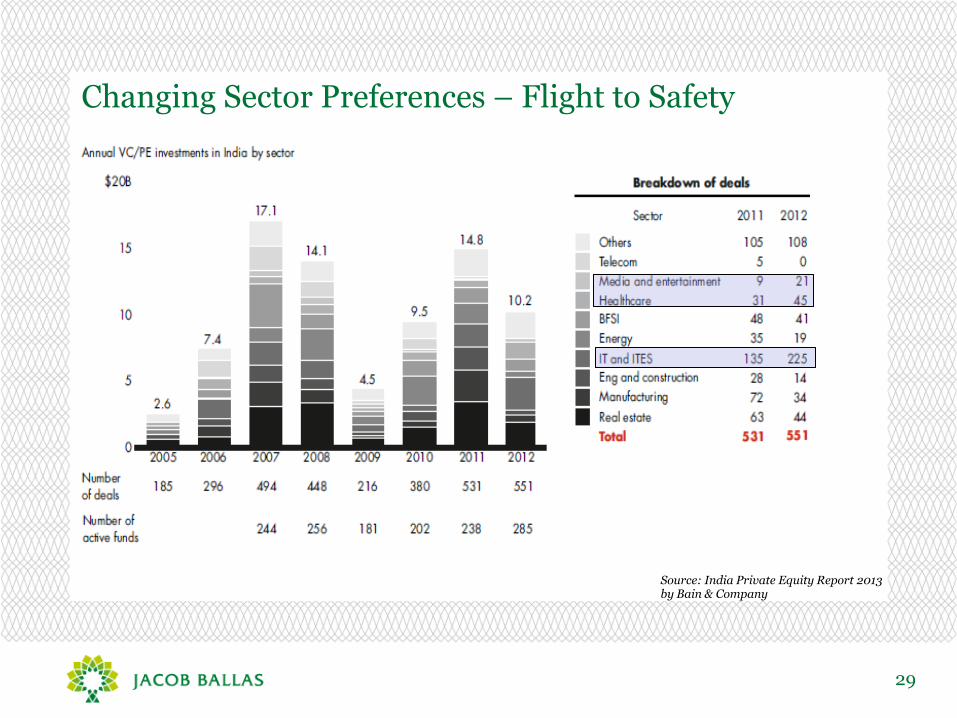

Changing Sector Preferences – Flight to Safety

Source: India Private Equity Report 2013 by Bain & Company

30

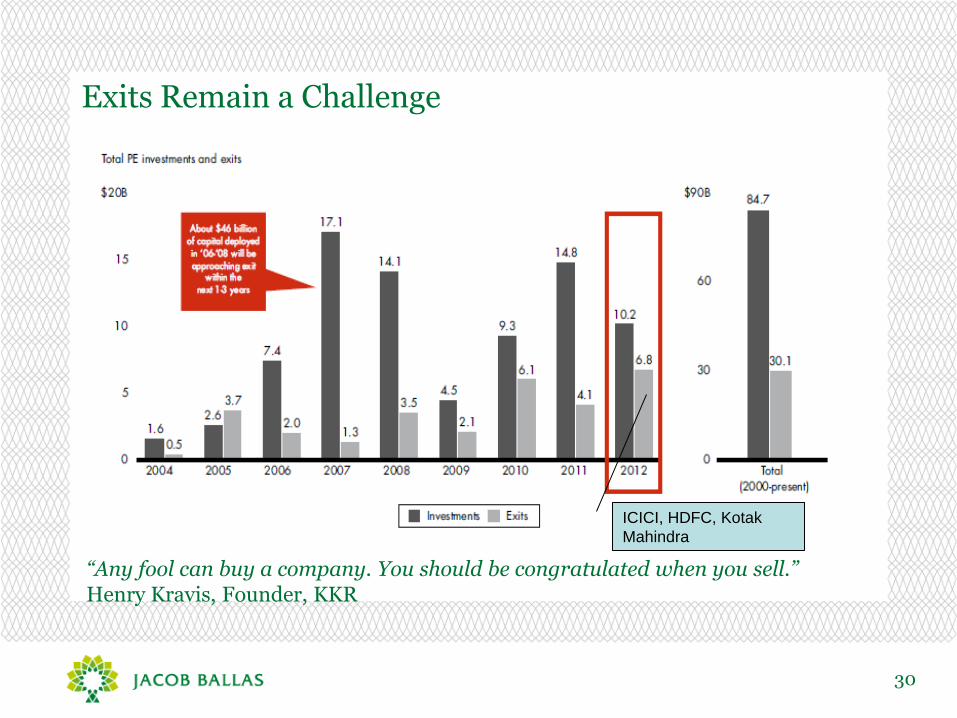

Exits Remain a Challenge

“Any fool can buy a company. You should be congratulated when you sell.” Henry Kravis, Founder, KKR

ICICI, HDFC, Kotak

Mahindra

31

Agenda

I. Understanding Private Equity

I. Types of Equity Funding

II. Why PE Funding

III. PE Funding Process

II. PE Industry – Current Status

I. Industry Trends

II. Current Challenges

III. Recent Developments

III. Annexures

Presentation only for reference purposes. Not to be reproduced anywhere. Please see disclaimer on disclaimer slide

32

So What Happened to India & Private Equity?

India: from Breakout Nation to Blackout Nation

India has moved from Boundless Optimism to Bottomless Pessimism*

Concerns on governance and economic policies

Economic Data not comforting

Private Equity returns have plunged since 2006

Fund-raising has hit a wall

India received only $3.5 billion of the $320 billion funding raised globally in 2012; $6.9 billion committed in 2011

Players such as 3i, Starwood Capital etc are exit India; Actis cuts its fund size by 2/3rd

Negative sentiment swirling around

Take a Pause

Data Source: Economic times, Bain PE Report

Presentation only for reference purposes. Not to be reproduced anywhere. Please see disclaimer on disclaimer slide

Verbatim from Economic Times

33

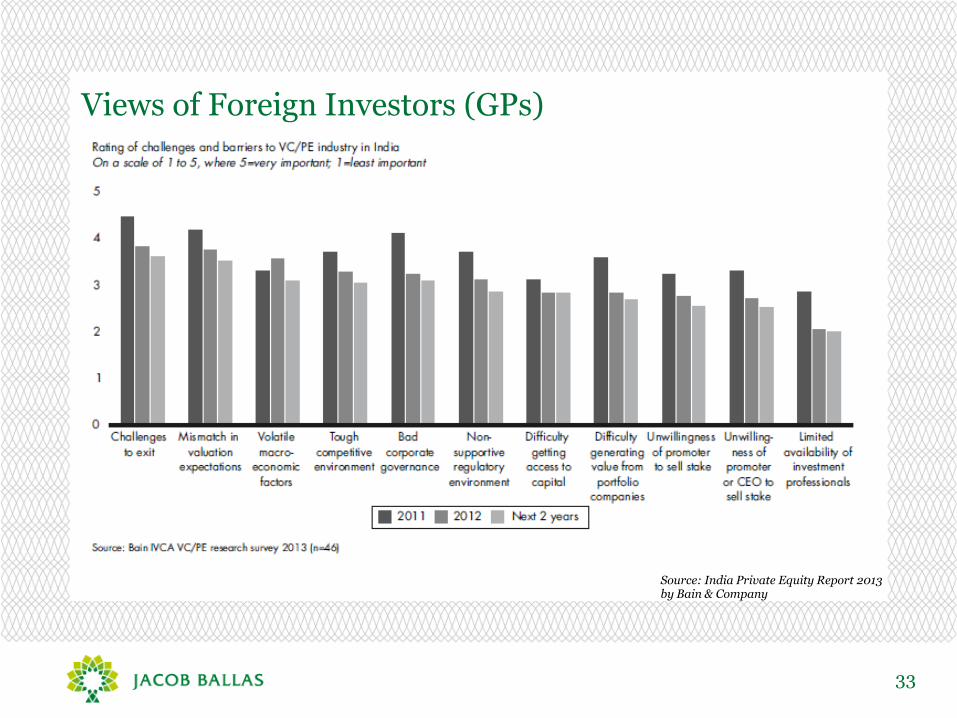

Views of Foreign Investors (GPs)

Source: India Private Equity Report 2013 by Bain & Company

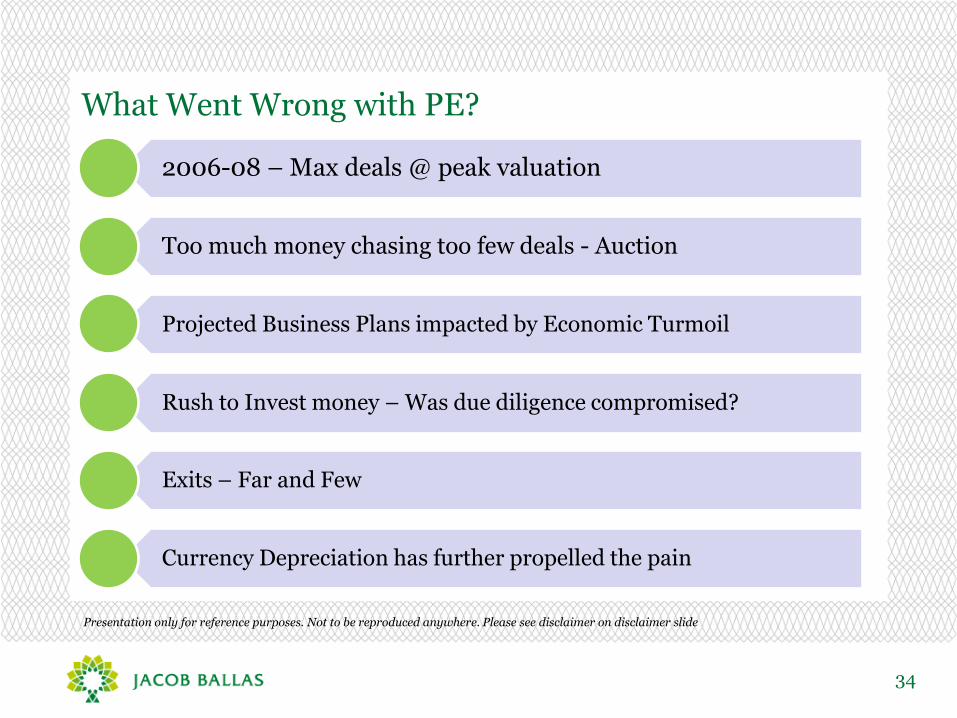

What Went Wrong with PE?

34

2006-08 – Max deals @ peak valuation

Too much money chasing too few deals - Auction

Projected Business Plans impacted by Economic Turmoil

Rush to Invest money – Was due diligence compromised?

Exits – Far and Few

Currency Depreciation has further propelled the pain

Presentation only for reference purposes. Not to be reproduced anywhere. Please see disclaimer on disclaimer slide

35

Source: www.andertoons.com

PE Investment

Timing Issue!!!

36

Source: www.glasbergen.com

Corporate Governance!!!

37

Is the Gloom Greatly Exaggerated?

Positives overshadowed by Negatives

38

India still one of the fastest growing economies

Young Population with median age of 25 years

Increasing VC deals indicate comfort in Indian Entrepreneurs

VC deals in future culminate into PE deals

Valuations are down and investment opportunities exist

Just Dial, Dr Lal Pathlabs, Kotak Bank, Shriram Transport Finance, Paras healthcare etc – Multi-baggers still exist

Presentation only for reference purposes. Not to be reproduced anywhere. Please see disclaimer on disclaimer slide

Every Industry goes through a cycle; so is PE

Industry expected to witness consolidation

LPs to prefer Funds with track record and operating history; GPs need to differentiate

Funds with wider mandate in terms of deal size, stage of investment etc expected to have better prospects

Focus to shift from investment rush to profitable exits

39

Agenda

I. Understanding Private Equity

I. Types of Equity Funding

II. Why PE Funding

III. PE Funding Process

II. PE Industry – Current Status

I. Industry Trends

II. Current Challenges

III.Recent Developments

III. Annexures

Presentation only for reference purposes. Not to be reproduced anywhere. Please see disclaimer on disclaimer slide

Mezzanine Funding

40

Presentation only for reference purposes. Not to be reproduced anywhere. Please see disclaimer on disclaimer slide

Debt Instrument with Potential Equity Upside

― Instruments like Convertible Debentures, Preference Shares, Warrants, Options etc

― Provides regular returns to investor with equity conversion providing upside

― Can be secured by pledge of shares, promoter guarantee , corporate guarantee, escrow of cash flows etc

Addresses 2 key concerns impacting PE Industry today

― Valuation – Debt instrument so no equity valuation required

― Exit – Redeemable, so no exit risks

― Can be structured to match the timing of cash flows

Benefits promoters as

― No equity dilution

― Funding availability in specific situations like foreign acquisitions, promoter funding , restructuring/refinance , buyback, PE exit etc. wherein debt funding from traditional sources may not be easily available

― However, high cost debt and so strong cash flows are required to service it

― Key Players – Indo Star (Everstone, Goldman Sach, Ashmore), KKR, ICICI Ventures, Blackstone, Prop desks of MNC banks such as Stan C, BOAML, CS

Online Funding Platforms

41

Venturesutra and India Venture Board are Pioneers

Purpose – To Connect Entrepreneurs to Investors

Primarily Focused on VC Funds

Entrepreneurs Located in Tier II and Tier III Cities Benefits

― Limited Access to VC Funds

Entrepreneurs Post Business Plan Accessible to Funds

Access to Intermediaries, Legal Counsels etc

Presentation only for reference purposes. Not to be reproduced anywhere. Please see disclaimer on disclaimer slide

42

Annexure

Presentation only for reference purposes. Not to be reproduced anywhere. Please see disclaimer on disclaimer slide

Data in annexure are as on a particular data. Some numbers would have changed, especially pertaining to

market price of listed shares. Annexure is just to highlight specific instances for information purposes only.

43

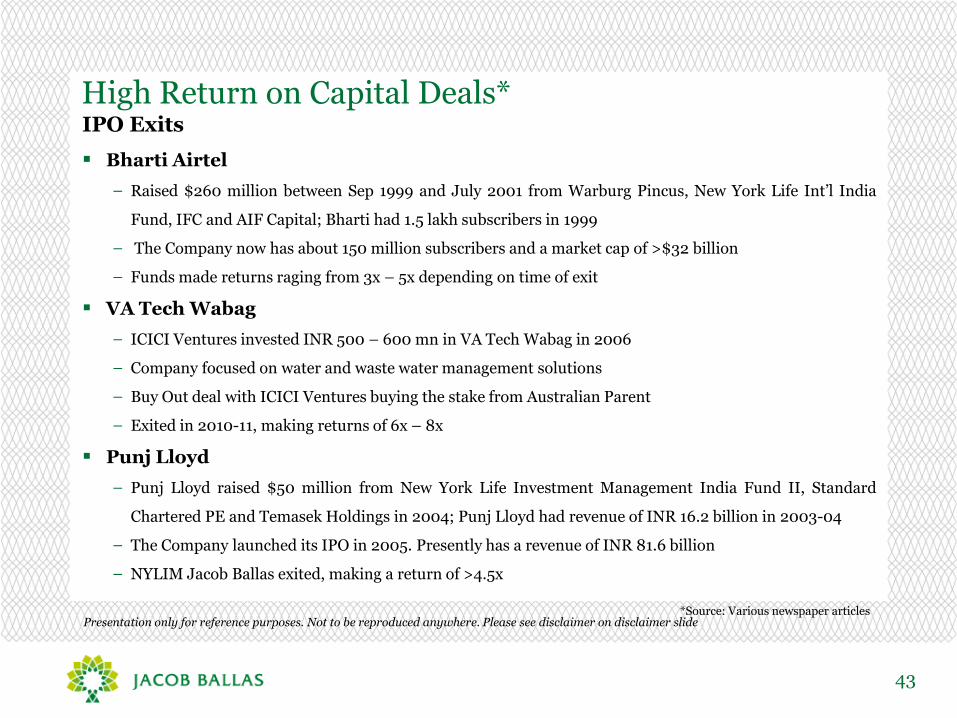

IPO Exits

Bharti Airtel

− Raised $260 million between Sep 1999 and July 2001 from Warburg Pincus, New York Life Int’l India

Fund, IFC and AIF Capital; Bharti had 1.5 lakh subscribers in 1999

− The Company now has about 150 million subscribers and a market cap of >$32 billion

− Funds made returns raging from 3x – 5x depending on time of exit

VA Tech Wabag

− ICICI Ventures invested INR 500 – 600 mn in VA Tech Wabag in 2006

− Company focused on water and waste water management solutions

− Buy Out deal with ICICI Ventures buying the stake from Australian Parent

− Exited in 2010-11, making returns of 6x – 8x

Punj Lloyd

− Punj Lloyd raised $50 million from New York Life Investment Management India Fund II, Standard

Chartered PE and Temasek Holdings in 2004; Punj Lloyd had revenue of INR 16.2 billion in 2003-04

− The Company launched its IPO in 2005. Presently has a revenue of INR 81.6 billion

− NYLIM Jacob Ballas exited, making a return of >4.5x

High Return on Capital Deals*

*Source: Various newspaper articles Presentation only for reference purposes. Not to be reproduced anywhere. Please see disclaimer on disclaimer slide

44

IPO Exits

Pipavav Defence

− Pipavav Shipyard raised about $60 million from New York Life Investment Management India

Fund II, Indus Capital and Trinity Capital in early 2007, followed by approximately $150.0 million from

other investors to set up the largest shipbuilding yard in India

− The Company launched its IPO in Sep 2009 and now has a market cap of >$ 1.3 billion

− At Market Price of around INR 75, at 3.0x NYLIM Investment price

Jubilant Foodworks

− JP Morgan and India Private Equity Fund invested in Jubilant Foodworks over a period of 1999-2003

− Total investment approximately INR 500 million

− Exited at IPO in 2010, returns >4x

Shriram Transport

− Chrys Capital invested approximately INR 1,000 – 1,200 million in Shriram Transport in 2004-

05

− Exited in tranches, making a complete exit by 2009

− Returns > 10x

*Source: Various newspaper articles

High Return on Capital Deals*

Presentation only for reference purposes. Not to be reproduced anywhere. Please see disclaimer on disclaimer slide

45

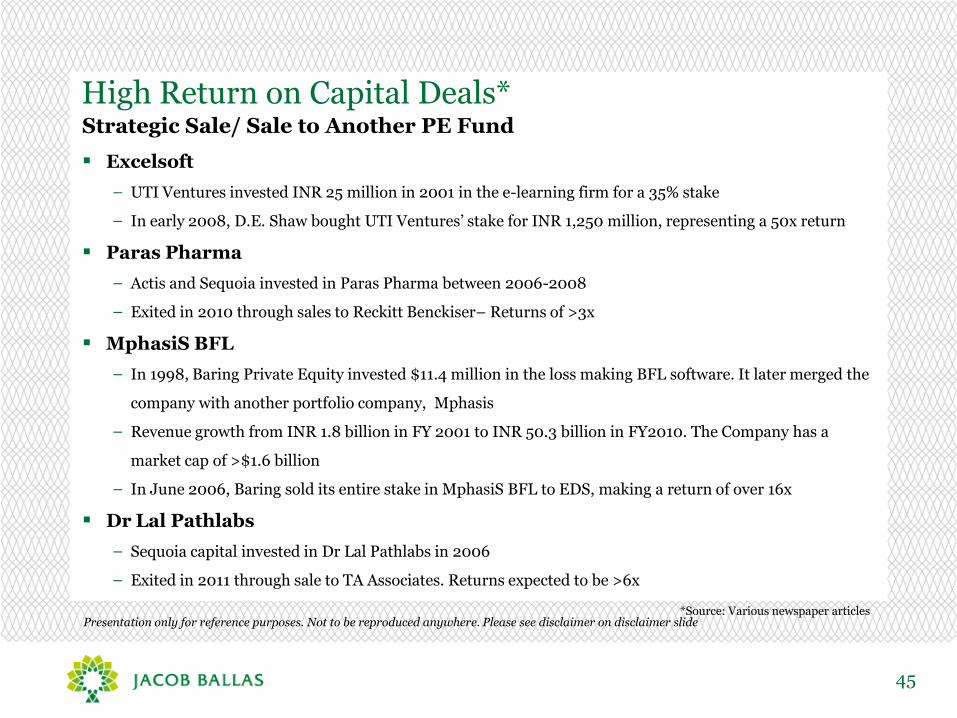

Strategic Sale/ Sale to Another PE Fund

Excelsoft

− UTI Ventures invested INR 25 million in 2001 in the e-learning firm for a 35% stake

− In early 2008, D.E. Shaw bought UTI Ventures’ stake for INR 1,250 million, representing a 50x return

Paras Pharma

− Actis and Sequoia invested in Paras Pharma between 2006-2008

− Exited in 2010 through sales to Reckitt Benckiser– Returns of >3x

MphasiS BFL

− In 1998, Baring Private Equity invested $11.4 million in the loss making BFL software. It later merged the

company with another portfolio company, Mphasis

− Revenue growth from INR 1.8 billion in FY 2001 to INR 50.3 billion in FY2010. The Company has a

market cap of >$1.6 billion

− In June 2006, Baring sold its entire stake in MphasiS BFL to EDS, making a return of over 16x

Dr Lal Pathlabs

− Sequoia capital invested in Dr Lal Pathlabs in 2006

− Exited in 2011 through sale to TA Associates. Returns expected to be >6x

High Return on Capital Deals*

*Source: Various newspaper articles Presentation only for reference purposes. Not to be reproduced anywhere. Please see disclaimer on disclaimer slide

46

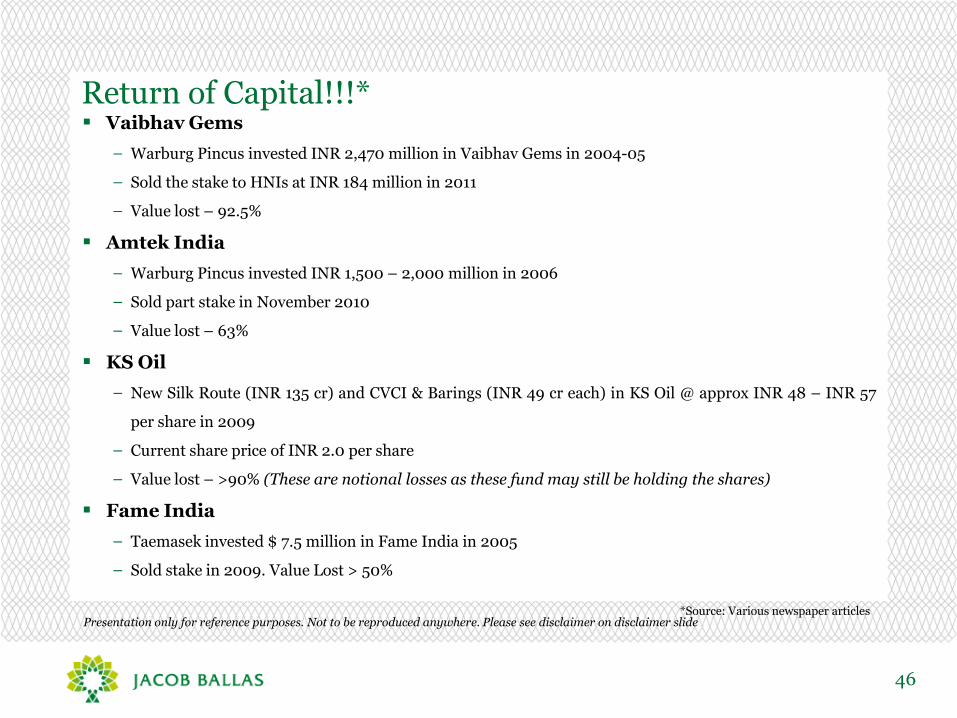

Vaibhav Gems

− Warburg Pincus invested INR 2,470 million in Vaibhav Gems in 2004-05

− Sold the stake to HNIs at INR 184 million in 2011

− Value lost – 92.5%

Amtek India

− Warburg Pincus invested INR 1,500 – 2,000 million in 2006

− Sold part stake in November 2010

− Value lost – 63%

KS Oil

− New Silk Route (INR 135 cr) and CVCI & Barings (INR 49 cr each) in KS Oil @ approx INR 48 – INR 57

per share in 2009

− Current share price of INR 2.0 per share

− Value lost – >90% (These are notional losses as these fund may still be holding the shares)

Fame India

− Taemasek invested $ 7.5 million in Fame India in 2005

− Sold stake in 2009. Value Lost > 50%

Return of Capital!!!*

*Source: Various newspaper articles Presentation only for reference purposes. Not to be reproduced anywhere. Please see disclaimer on disclaimer slide

47

Venture Intelligence

VC Circle

“The Fourth Wheel” – Report on PE from Grant Thornton

Economic Times and other News Articles

Deal Curry

Bain & Company report on PE Industry in India, 2012

EY report on PE industry

References

Presentation only for reference purposes. Not to be reproduced anywhere. Please see disclaimer on disclaimer slide

49

Disclaimer

The presentation represents the personal views of the author and not his organization. No claim is made for its accuracy or otherwise and users should do their own research in arriving at investment decisions. The data has been sourced from various public sources and may not be completely accurate. The data is used more for representation purposes and should not be reproduced anywhere with reference to this presentation. The data mentioned should not be used to judge/ comment on the performance of any fund. Data has been picked up randomly for specific cases and does not reflect an opinion on any fund. The presentation should not be used or reproduced without the consent of the author.