probitas private equity survey trends2014

TRANSCRIPT

8/13/2019 Probitas Private Equity Survey Trends2014

http://slidepdf.com/reader/full/probitas-private-equity-survey-trends2014 1/36

Private Equity Inst itutional Investor

Trends for 2014 Survey

8/13/2019 Probitas Private Equity Survey Trends2014

http://slidepdf.com/reader/full/probitas-private-equity-survey-trends2014 2/36

Probitas Partners is a leading independent knowledge, innovation, and solutions provider to privatemarkets clients. We serve both institutional investors who seek to place capital and select leadingfund sponsors who seek to raise capital for private equity, real estate, infrastructure, credit, specialsituations, and hedge funds. These services are offered by a team of employee owners dedicatedto leveraging the rm’s vast knowledge and technical resources to provide the best results for allits clients.

On an ongoing basis, Probitas Partners offers research and investment tools for the alternativeinvestment market as aids to its institutional investor and general partner clients. ProbitasPartners compiles data from various trade and other sources and then vets and enhances thatdata via its team’s broad knowledge of the market.

n. [from Latin probitas: good, proper, honest.] adherenceto the highest principles, ideals and character.

probity¯ ¯˘

8/13/2019 Probitas Private Equity Survey Trends2014

http://slidepdf.com/reader/full/probitas-private-equity-survey-trends2014 3/36

1

© 2013 Probitas Partners Private Equity Institutional Investor Trends for 2014 Survey

C o n t e n t s

The Private Equity Fundraising Environment ...................................2

Private Equity Institutional Investor Survey ......................................3

Overview of Survey Findings ..............................................................3

Profile of Respondents .......................................................................4

Sectors and Geographies of Interest ................................................8

U.S. Middle-Market Funds ................................................................20

Venture Capital .................................................................................21

Niche Private Equity Sectors ............................................................22

Fund Structures and Key Terms .......................................................27

Investor Fears and Concerns ...........................................................30

Our View of the Future .....................................................................33

8/13/2019 Probitas Private Equity Survey Trends2014

http://slidepdf.com/reader/full/probitas-private-equity-survey-trends2014 4/36

Chart I Global Commitments Private Equity Partnerships

U S D

i n b i l l i o n s

600

500

400

300

200

100

0

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 3Q YTD2013

Source: Thomson Reuter

20 27 40 49 6497

148175

301

175

94 99138

306

392

490 477

170

262

168

276

205

2

Private Equity Institutional Investor Trends for 2014 Survey © 2013 Probitas Partners

The Private Equity Fundraising Environment

• Fundraising in 2013 is on pace to exceed 2012’s total as the private equitymarkets return to normalcy in the wake of the Financial Crisis.

• Different trends from 2012 underlie the top line numbers in Chart I.

• Mega buyout funds in the United States and Europe are raising large fundsthat are boosting overall commitments — but most of these funds are targeting

smaller funds than they did at the market peak.

• In Asia, a relative strong point during the Financial Crisis, fundraising hasfallen significantly in 2012 and 2013 — especially for RMB-denominated,China-focused funds that had been growing steadily since 2006.

• The overhang of undrawn commitments that built up from vintage year2006 through 2008 funds is now finally burning off, releasing pressure onlimited partners’ allocations.

• Interest in secondary funds and distressed debt funds is moderating fromlast year.

8/13/2019 Probitas Private Equity Survey Trends2014

http://slidepdf.com/reader/full/probitas-private-equity-survey-trends2014 5/36

3

© 2013 Probitas Partners Private Equity Institutional Investor Trends for 2014 Survey

Private Equity Institutional Investor Survey

Probitas Partners conducted its online survey to measure investor interest,opinions, and perspectives on investing in private equity in October 2013. Thissurvey is administered annually to gauge emerging trends and to compareinvestors’ changing views over a longer period of time. One hundred and thirty-seven responses were received from senior investment executives globally,representing such institutions as public and corporate pension plans, fund-of-funds, family offices, endowments and foundations, and consultants and advisors.

Overview of Survey Findings

The following summarizes the top-line findings from the survey:

• Steady interest in private equity. The rebound from the Financial Crisiscontinues, and investors are likely to commit slightly more to private equity in2014 than 2013. Though the appetite for new managers is increasing, a numberof investors remain focused on triaging current fund manager relationships asthe last group of managers yet to raise since the beginning of the FinancialCrisis comes back to market.

• Continued focus on smaller buyout and growth capital funds. Investorsremain focused on smaller- and middle-market buyout and growth capital fundsin the United States and Europe to diversify portfolios and commit capital tostrategies where managers can prove recurring added value.

• Many investors have already established core relationships in these sectors,so are not looking to add many new ones.

• Interest in emerging markets is declining. Investors are increasinglyconcerned with political risk in the emerging markets and are less convincedthat the inherent high growth story necessarily leads to strong privateequity gains.

• Credit Vehicles (distinct from mezzanine funds) are rising in interest.Credit-oriented strategies and vehicles have come into fashion, especiallysenior debt and opportunistic credit strategies in Europe and North America,as difficulties in the debt markets have continued to create opportunities.

• Energy focused funds remain a significant focus for investors, especially inNorth America. This is true in no small part due to outperformance the sectorhas delivered over the past couple of years compared with the broader privateequity markets.

• Large investors increasingly focused on co-investments. Large investors withthe team and capital resources necessary to develop co-investment programs

are increasingly targeting co-investments in an effort to enhance overall andnet returns; the largest investors are pursuing direct investments as well.

8/13/2019 Probitas Private Equity Survey Trends2014

http://slidepdf.com/reader/full/probitas-private-equity-survey-trends2014 6/36

Chart II Respondents by Institution TypeI represent a:

Source: Probitas Partners’ Private Equity Institutional Investor Trends for 2014 Survey

Public Pension

Corporate Pension/

Private Pension PlanEndowment/Foundation

Fund-of-Funds Manager

Family Ofce

Sovereign Wealth Fund/Government Entity

Insurance Company

Bank

Consultant/Advisor

Other

3%

13%

4%

14%

11%5%

9%

31%

6%4%

4

Private Equity Institutional Investor Trends for 2014 Survey © 2013 Probitas Partners

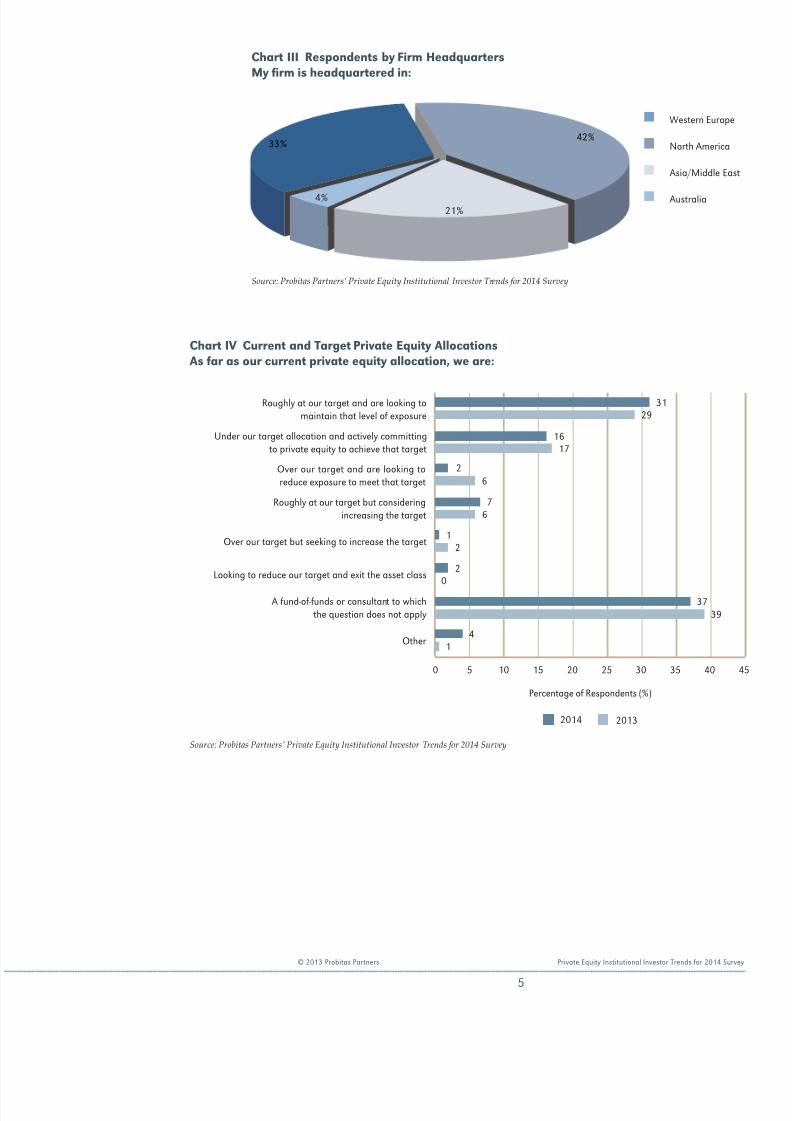

Profile of Respondents

• There were 137 respondents to the survey; most respondents were from pensionplans, funds-of-funds, insurance companies, and family ofces (Chart II).

• Respondents were geographically diverse, with strong participation fromNorth America, Europe, and Asia; within Asia there was a particularly strongresponse from Japan (Chart III).

• As Chart IV details, many investors are near the top of their allocations, thoughinvestors expressed more allocation flexibility this year than they had last year.

• Funds-of-funds are different — allocations are not really relevant as their abilityto invest is driven by their ability to raise fund vehicles or separate accounts.

8/13/2019 Probitas Private Equity Survey Trends2014

http://slidepdf.com/reader/full/probitas-private-equity-survey-trends2014 7/36

Chart III Respondents by Firm HeadquartersMy rm is headquartered in:

Source: Probitas Partners’ Private Equity Institutional Investor Trends for 2014 Survey

Western Europe

North America

Asia/Middle East

Australia21%

4%

33%42%

Chart IV Current and Target Private Equity Allocations As far as our current private equity allocation, we are:

Roughly at our target and are looking tomaintain that level of exposure

Under our target allocation and actively committingto private equity to achieve that target

Over our target and are looking toreduce exposure to meet that target

Roughly at our target but consideringincreasing the target

Over our target but seeking to increase the target

Looking to reduce our target and exit the asset class

A fund-of-funds or consultant to whichthe question does not apply

Other

Percentage of Respondents (%)

Source: Probitas Partners’ Private Equity Institutional Investor Trends for 2014 Survey

0 5 10 15 20 25 30 35 40 45

20132014

31

1617

26

76

1

20

4

3739

12

29

5

© 2013 Probitas Partners Private Equity Institutional Investor Trends for 2014 Survey

8/13/2019 Probitas Private Equity Survey Trends2014

http://slidepdf.com/reader/full/probitas-private-equity-survey-trends2014 8/36

Chart V Drivers of Sector InvestmentOur sector investment focus in 2014 is being driven by:

My institution simply pursues the best funds and managers available in the market

A focus on those private equity sectors I believewill outperform others in this vintage year

Maintaining established relationships with fundmanagers returning to market this year

Targeting funds that will provideaccess to co-investments

My institution’s need to diversifyits private equity portfolio

My need to decrease exposureto private equity

My need to deploy signicant amountsof capital allocated to private equity

The strategies that my clientshave directed us to pursue

Other

Percentage of Respondents (%)

Source: Probitas Partners’ Private Equity Institutional Investor Trends for 2014 Survey

0 10 20 30 40 50

47

12

9

7

3

2

14

5

1

6

Private Equity Institutional Investor Trends for 2014 Survey © 2013 Probitas Partners

• What drives investors to invest? Consistent with Probitas Partners’ past surveys,all other reasons are secondary to “pursuing the best available managers andfunds,” though the focus on best managers has become increasingly importantto investors since the Financial Crisis (Chart V).

• Proven, top quartile managers can be difficult to access, and since funds onlycome to market every three to five years, many investors feel compelled tocommit to these managers when they are available and open.

• Family offices are much more likely to focus on private equity sectors theybelieve will outperform, with 33% of those respondents following that strategy.

• More respondents are looking to increase commitments as 2014 approaches,continuing the allocation rebound after the bottom of the fundraising marketin 2009 (Chart VI).

• Chart VII shows that two-thirds of respondents are focused on their currentgeneral partner relationships, with only 28% strongly focused on developingnew general partner relationships.

• Based on our discussions with investors, many continue the process of triaginggeneral partner relationships that they began following the Financial Crisis.

• Only 3% of respondents targeted separate accounts as their primary means ofinvesting in private equity, the same number as last year.

8/13/2019 Probitas Private Equity Survey Trends2014

http://slidepdf.com/reader/full/probitas-private-equity-survey-trends2014 9/36

Chart VI Private Equity AllocationsFor 2014, we or the clients we advise are looking to commit across all areas of private equity(in USD):

P e r c e n

t a g e o

f R e s p o n d

e n

t s ( % )

30

25

20

15

10

5

0

<$50 MM $50 MM–$150 MM

$150 MM–$250 MM

$250 MM–$500 MM

$500 MM–$1 B

>$1 B

Source: Probitas Partners’ Private Equity Institutional Investor Trends for 2014 Survey

20132014

19

15

26

22

16

21

1718

13

10 9

14

Chart VII Manager RelationshipsDuring 2014, we would expect our primary focus to be:

Evaluating re-ups with current general partner relationshipswith a limited look at new relationships

Evaluating re-ups with current general partnerrelationships, looking to decrease thenumber of relationships signicantly

Evaluating re-ups with currentgeneral partner relationships

Actively pursuing relationships with new managers

Pursuing separate accounts witha smaller number of managers

Our 2014 commitments have alreadybeen completely allocated

Other

Percentage of Respondents (%)

Source: Probitas Partners’ Private Equity Institutional Investor Trends for 2014 Survey

0 10 20 30 40 50 60

85

55

2828

33

22

20132014

0 3

5454

7

© 2013 Probitas Partners Private Equity Institutional Investor Trends for 2014 Survey

8/13/2019 Probitas Private Equity Survey Trends2014

http://slidepdf.com/reader/full/probitas-private-equity-survey-trends2014 10/36

Chart VIII Private Equity Sectors of InterestDuring 2014, my rm or my clients plan to focus most of our attention on investing in the followingsectors (choose no more than ve):

U.S. Middle-Market Buyouts ($500 million to $2.5 billion)

European Middle-Market Buyouts — Country-Focused

U.S. Small-Market Buyouts (>$500 million)

Growth Capital Funds

Energy Funds

European Middle-Market Buyouts — Pan-European

U.S. Large Buyouts ($2.5 billion to $5 billion)

Credit Strategies

Secondary Funds

Distressed Debt Funds

Asian Country-Focused Funds

Infrastructure Funds

Mezzanine Funds

Pan-Asian FundsU.S. Venture Capital

Restructuring Funds

Fund-of-Funds

Emerging Markets (ex-Asia)

Mega Buyout Funds (>$5 billion or equivalent)

Cleantech/Green-Focused Funds

Mining Funds

European/Israeli Venture Capital

Agriculture Funds

Timber Funds

Other Niche Sectors

Percentage of Respondents (%)

Source: Probitas Partners’ Private Equity Institutional Investor Trends for 2014 Survey

0 10 20 30 40 50 60 70

62

43

41

25

18

15

12

9

9

16

16

19

20

22

23

25

26

30

8

3

3

2

2

2

5

8

Private Equity Institutional Investor Trends for 2014 Survey © 2013 Probitas Partners

Sectors and Geographies of Interest

Chart VIII details the sectors of interest to investors for 2014:

• As has been the case in most of our previous surveys, middle-market buyoutsand growth capital in the United States and Europe dominate interest.

• Interest in Asian country-focused funds declined from 24% last year to 19%this year because of continuing concerns about China.

8/13/2019 Probitas Private Equity Survey Trends2014

http://slidepdf.com/reader/full/probitas-private-equity-survey-trends2014 11/36

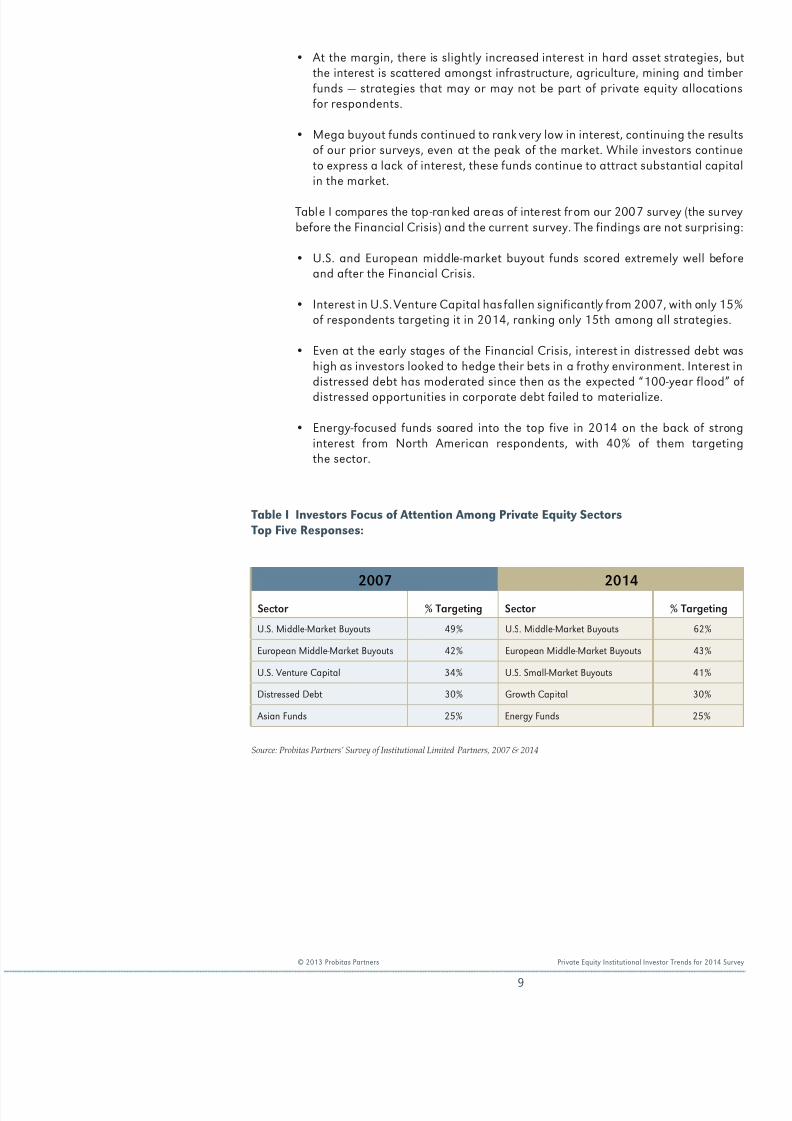

Table I Investors Focus of Attention Among Private Equity Sectors Top Five Responses:

2007 2014

Sector % Targeting Sector % Targeting

U.S. Middle-Market Buyouts 49% U.S. Middle-Market Buyouts 62%

European Middle-Market Buyouts 42% European Middle-Market Buyouts 43%

U.S. Venture Capital 34% U.S. Small-Market Buyouts 41%

Distressed Debt 30% Growth Capital 30%

Asian Funds 25% Energy Funds 25%

Source: Probitas Partners’ Survey of Institutional Limited Partners, 2007 & 2014

9

© 2013 Probitas Partners Private Equity Institutional Investor Trends for 2014 Survey

• At the margin, there is slightly increased interest in hard asset strategies, butthe interest is scattered amongst infrastructure, agriculture, mining and timberfunds — strategies that may or may not be part of private equity allocationsfor respondents.

• Mega buyout funds continued to rank very low in interest, continuing the resultsof our prior surveys, even at the peak of the market. While investors continueto express a lack of interest, these funds continue to attract substantial capitalin the market.

Table I compares the top-ranked areas of interest from our 2007 survey (the surveybefore the Financial Crisis) and the current survey. The findings are not surprising:

• U.S. and European middle-market buyout funds scored extremely well beforeand after the Financial Crisis.

• Interest in U.S. Venture Capital has fallen significantly from 2007, with only 15%of respondents targeting it in 2014, ranking only 15th among all strategies.

• Even at the early stages of the Financial Crisis, interest in distressed debt washigh as investors looked to hedge their bets in a frothy environment. Interest indistressed debt has moderated since then as the expected “100-year flood” ofdistressed opportunities in corporate debt failed to materialize.

• Energy-focused funds soared into the top five in 2014 on the back of stronginterest from North American respondents, with 40% of them targetingthe sector.

8/13/2019 Probitas Private Equity Survey Trends2014

http://slidepdf.com/reader/full/probitas-private-equity-survey-trends2014 12/36

Chart IX Private Equity Sectors of Interest; European Respondents

European Middle-Market Buyouts — Country-Focused

U.S. Middle-Market Buyouts ($500 million to $2.5 billion)

U.S. Small-Market Buyouts (<$500 million)

Growth Capital Funds

European Middle-Market Buyouts — Pan-European

Infrastructure Funds

Credit Strategies

U.S. Large Buyouts ($2.5 billion to $5 billion)

Asian Country-Focused Funds

Restructuring Funds

Distressed Debt Funds

Energy FundsMezzanine Funds

Pan-Asian Funds

Emerging Markets (ex-Asia)

Secondary Funds

Fund-of-Funds

U.S. Venture Capital

Mega Buyout Funds (>$5 billion or equivalent)

Cleantech/Green-Focused Funds

European/Israeli Venture Capital

Mining Funds

Agriculture Funds

Timber Funds

Other Niche Sectors

Percentage of Respondents (%)

Source: Probitas Partners’ Private Equity Institutional Investor Trends for 2014 Survey

0 10 20 30 40 50 60 70 80

78

40

33

22

11

11

7

4

7

11

11

13

16

18

18

24

24

31

60

4

0

2

2

2

2

10

Private Equity Institutional Investor Trends for 2014 Survey © 2013 Probitas Partners

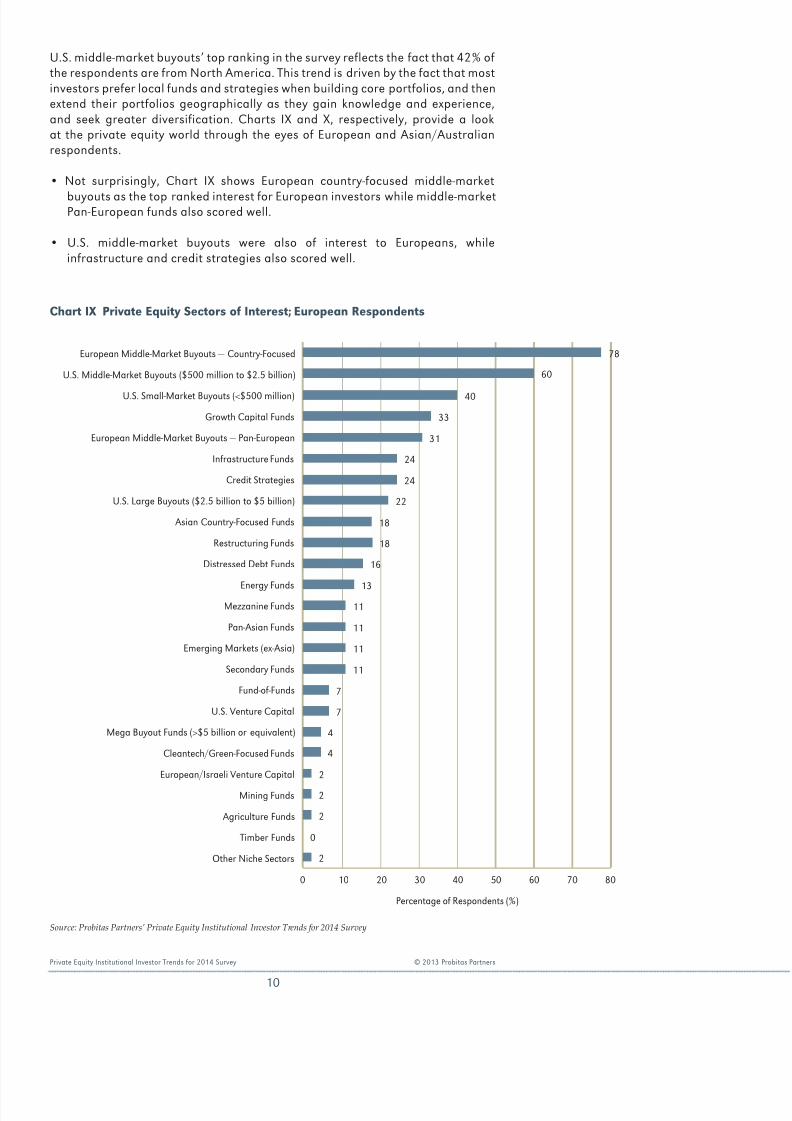

U.S. middle-market buyouts’ top ranking in the survey reflects the fact that 42% ofthe respondents are from North America. This trend is driven by the fact that mostinvestors prefer local funds and strategies when building core portfolios, and thenextend their portfolios geographically as they gain knowledge and experience,and seek greater diversification. Charts IX and X, respectively, provide a lookat the private equity world through the eyes of European and Asian/Australianrespondents.

• Not surprisingly, Chart IX shows European country-focused middle-market

buyouts as the top ranked interest for European investors while middle-marketPan-European funds also scored well.

• U.S. middle-market buyouts were also of interest to Europeans, whileinfrastructure and credit strategies also scored well.

8/13/2019 Probitas Private Equity Survey Trends2014

http://slidepdf.com/reader/full/probitas-private-equity-survey-trends2014 13/36

Chart X Private Equity Sectors of Interest; Asian Respondents

U.S. Middle-Market Buyouts ($500 million to $2.5 billion)

Asian Country-Focused Funds

Pan-Asian Funds

European Middle-Market Buyouts — Pan-European

Infrastructure Funds

Secondary Funds

U.S. Large-Buyouts ($2.5 billion to $5 billion)

Mezzanine Funds

Energy Funds

Growth Capital Funds

U.S. Small-Market Buyouts (<$500 million)

European Middle-Market Buyouts -— Country-Focused

Credit Strategies

Mega Buyout Funds (>$5 billion or equivalent)

Restructuring Funds

Fund-of-Funds

Distressed Debt Funds

Cleantech/Green-Focused Funds

U.S. Venture Capital

Mining Funds

Timber Funds

Emerging Markets (ex-Asia)European/Israeli Venture Capital

Agriculture Funds

Other Niche Sectors

Percentage of Respondents (%)

Source: Probitas Partners’ Private Equity Institutional Investor Trends for 2014 Survey

0 10 20 30 40 50 60

52

35

35

28

21

14

14

7

10

14

14

21

21

24

24

28

28

31

3

3

0

00

0

7

11

© 2013 Probitas Partners Private Equity Institutional Investor Trends for 2014 Survey

• U.S. venture capital was of little interest — though it did outscore Europeanventure capital.

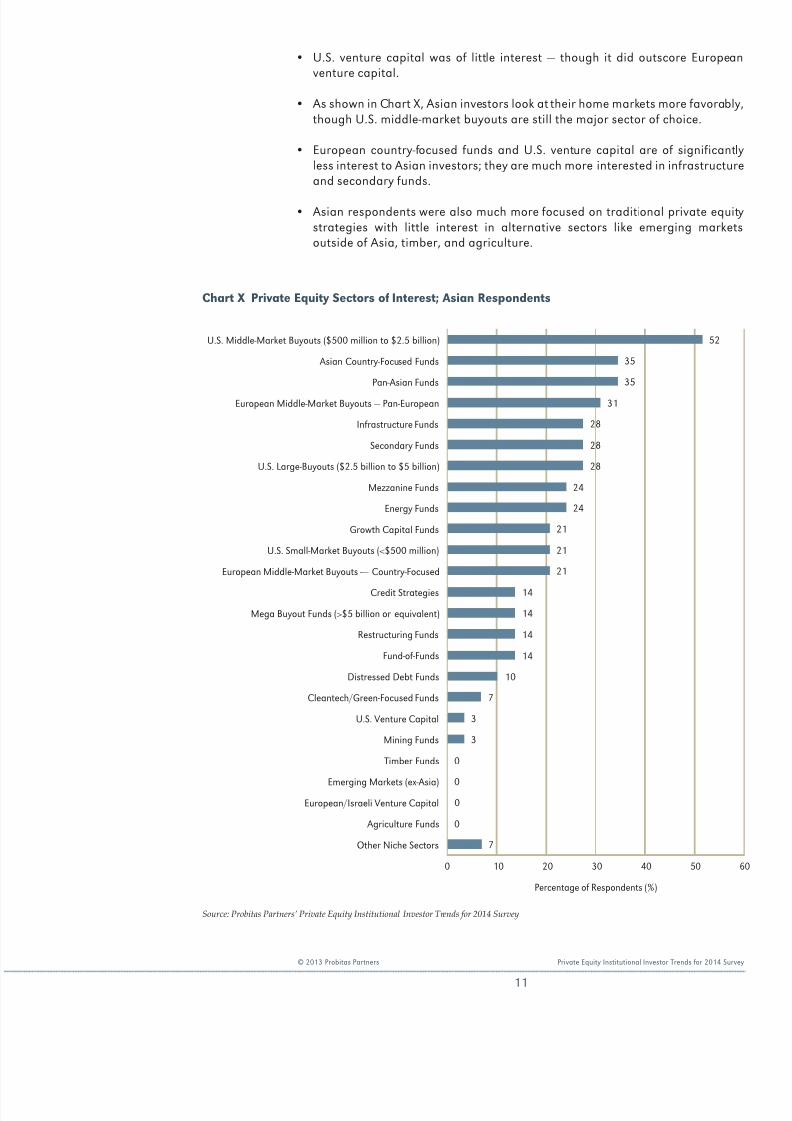

• As shown in Chart X, Asian investors look at their home markets more favorably,though U.S. middle-market buyouts are still the major sector of choice.

• European country-focused funds and U.S. venture capital are of significantlyless interest to Asian investors; they are much more interested in infrastructureand secondary funds.

• Asian respondents were also much more focused on traditional private equitystrategies with little interest in alternative sectors like emerging marketsoutside of Asia, timber, and agriculture.

8/13/2019 Probitas Private Equity Survey Trends2014

http://slidepdf.com/reader/full/probitas-private-equity-survey-trends2014 14/36

Chart XI Private Equity Geographical FocusDuring 2014, I anticipate that the three major geographical focuses for our program will be:

P e r c e n

t a g e o

f R e s p o n d

e n

t s ( % )

100

90

80

70

60

50

40

30

20

10

0

North America

WesternEurope

Asia EmergingMarketsGlobally

Latin America

Central andEastern Europe

Africa MENA Other

Source: Probitas Partners’ Private Equity Institutional Investor Trends for 2014 Survey

2 2

92

49

139

85

51

12

Private Equity Institutional Investor Trends for 2014 Survey © 2013 Probitas Partners

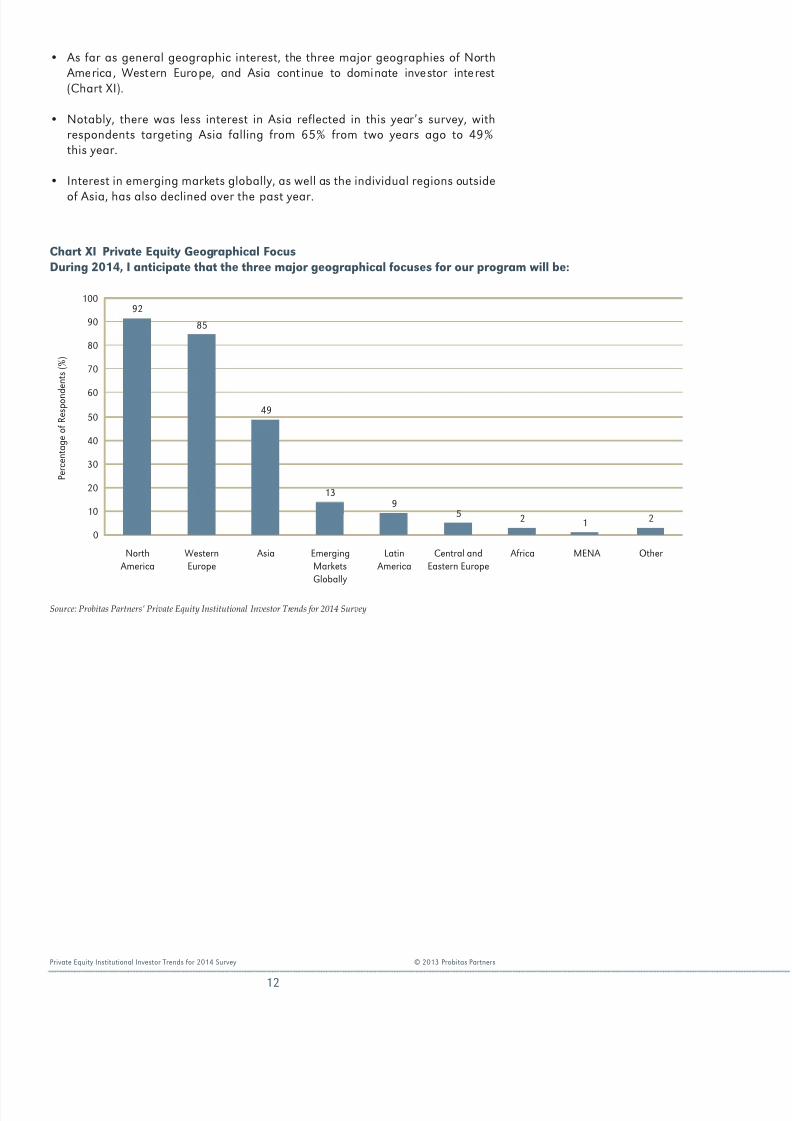

• As far as general geographic interest, the three major geographies of North America, Western Europe, and Asia cont inue to dominate investor interest(Chart XI).

• Notably, there was less interest in Asia reflected in this year’s survey, withrespondents targeting Asia falling from 65% from two years ago to 49%this year.

• Interest in emerging markets globally, as well as the individual regions outside

of Asia, has also declined over the past year.

8/13/2019 Probitas Private Equity Survey Trends2014

http://slidepdf.com/reader/full/probitas-private-equity-survey-trends2014 15/36

20132014

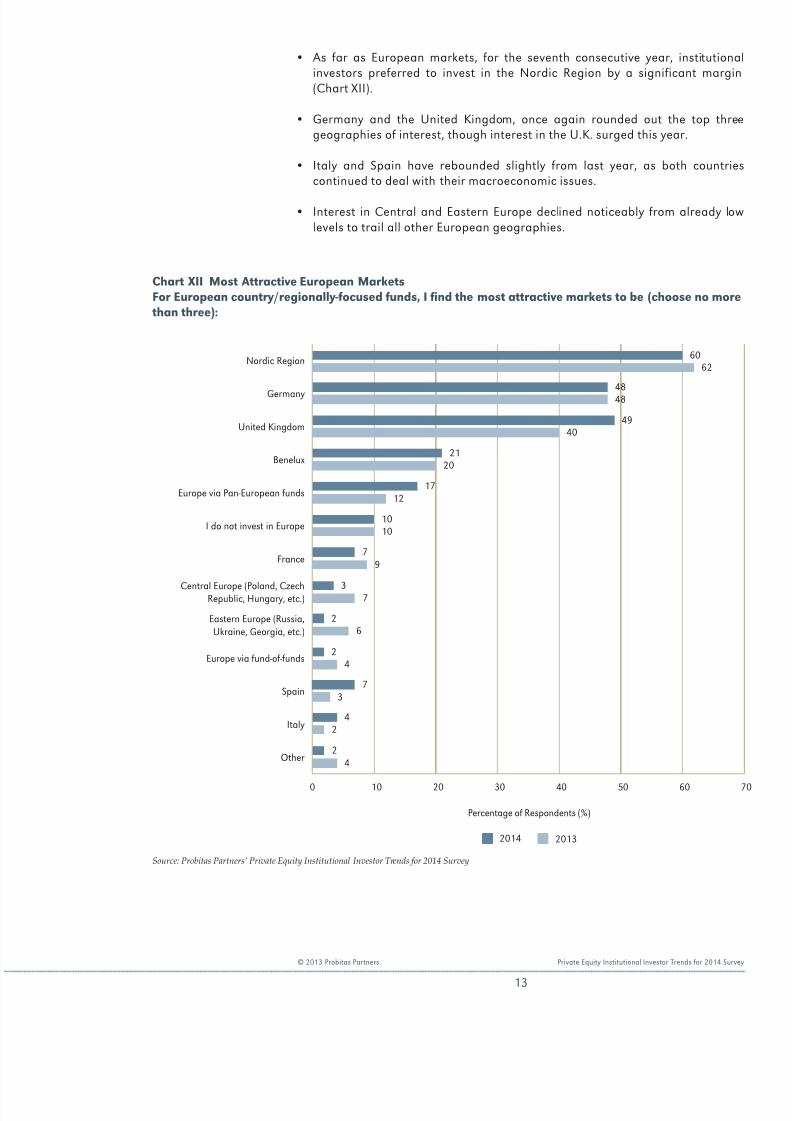

Chart XII Most Attractive European MarketsFor European country/regionally-focused funds, I nd the most attractive markets to be (choose no morethan three):

Nordic Region

Germany

United Kingdom

Benelux

Europe via Pan-European funds

I do not invest in Europe

France

Central Europe (Poland, CzechRepublic, Hungary, etc.)

Eastern Europe (Russia,Ukraine, Georgia, etc.)

Europe via fund-of-funds

Spain

Italy

Other

Percentage of Respondents (%)

Source: Probitas Partners’ Private Equity Institutional Investor Trends for 2014 Survey

0 10 20 30 40 50 60 7

4848

2120

1217

79

1010

3 7

26

42

73

24

4940

6062

24

13

© 2013 Probitas Partners Private Equity Institutional Investor Trends for 2014 Survey

• As far as European markets, for the seventh consecutive year, institutionalinvestors preferred to invest in the Nordic Region by a significant margin(Chart XII).

• Germany and the United Kingdom, once again rounded out the top threegeographies of interest, though interest in the U.K. surged this year.

• Italy and Spain have rebounded slightly from last year, as both countriescontinued to deal with their macroeconomic issues.

• Interest in Central and Eastern Europe declined noticeably from already lowlevels to trail all other European geographies.

8/13/2019 Probitas Private Equity Survey Trends2014

http://slidepdf.com/reader/full/probitas-private-equity-survey-trends2014 16/36

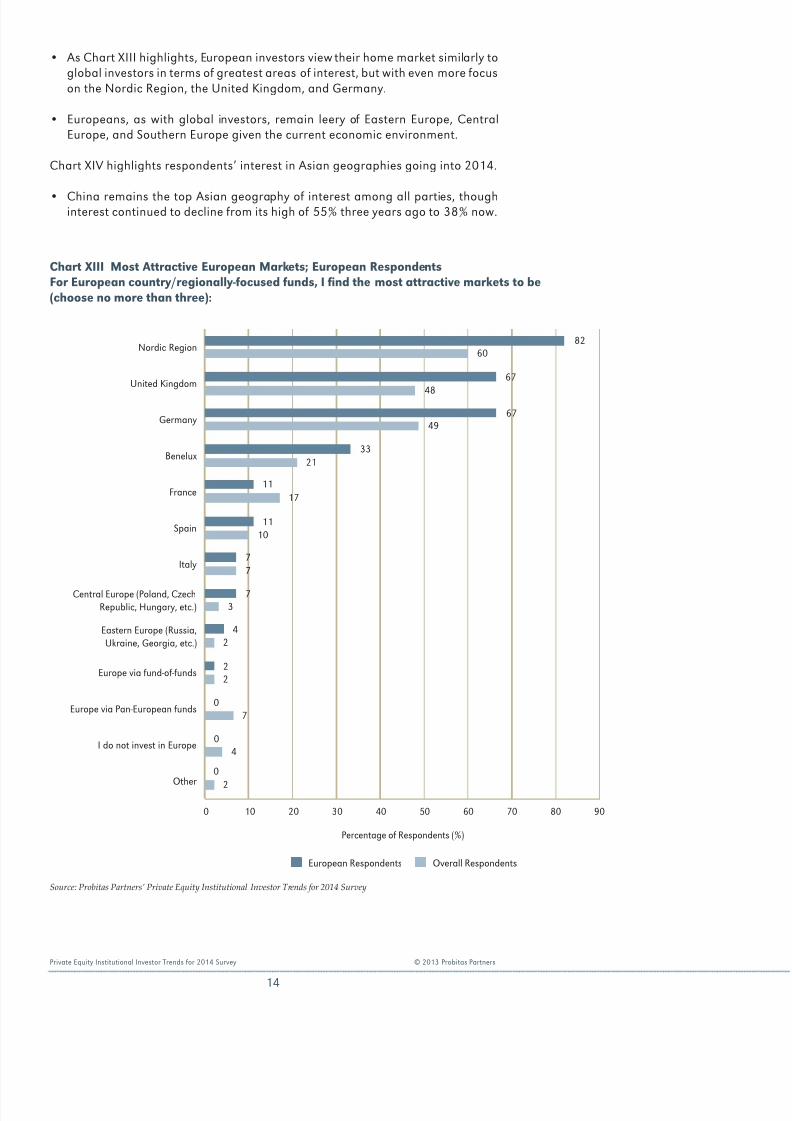

Chart XIII Most Attractive European Markets; European RespondentsFor European country/regionally-focused funds, I nd the most attractive markets to be(choose no more than three):

Nordic Region

United Kingdom

Germany

Benelux

France

Spain

Italy

Central Europe (Poland, CzechRepublic, Hungary, etc.)

Eastern Europe (Russia,Ukraine, Georgia, etc.)

Europe via fund-of-funds

Europe via Pan-European funds

I do not invest in Europe

Other

Percentage of Respondents (%)

Source: Probitas Partners’ Private Equity Institutional Investor Trends for 2014 Survey

0 10 20 30 40 50 60 70 80 90

Overall RespondentsEuropean Respondents

8260

0

2

22

73

04

3321

6749

67

48

07

1117

1110

77

42

14

Private Equity Institutional Investor Trends for 2014 Survey © 2013 Probitas Partners

• As Chart XIII highlights, European investors view their home market similarly toglobal investors in terms of greatest areas of interest, but with even more focuson the Nordic Region, the United Kingdom, and Germany.

• Europeans, as with global investors, remain leery of Eastern Europe, CentralEurope, and Southern Europe given the current economic environment.

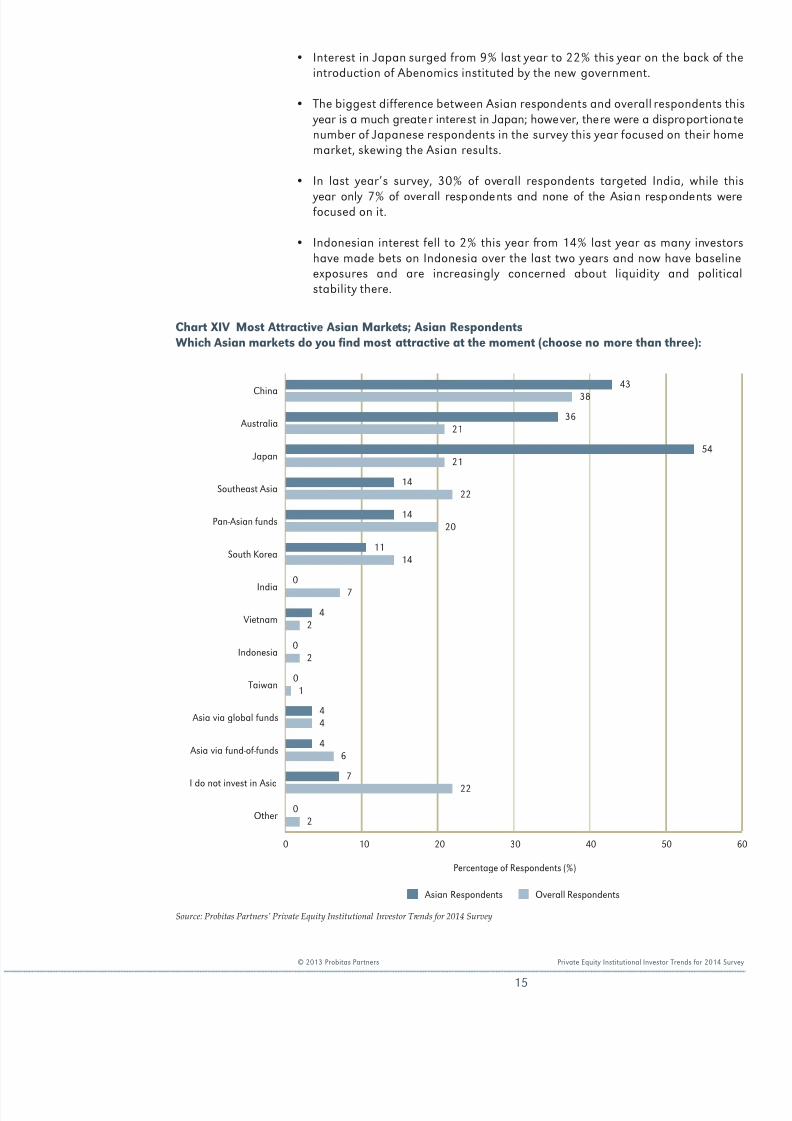

Chart XIV highlights respondents’ interest in Asian geographies going into 2014.

• China remains the top Asian geography of interest among all parties, thoughinterest continued to decline from its high of 55% three years ago to 38% now.

8/13/2019 Probitas Private Equity Survey Trends2014

http://slidepdf.com/reader/full/probitas-private-equity-survey-trends2014 17/36

Chart XIV Most Attractive Asian Markets; Asian RespondentsWhich Asian markets do you nd most attractive at the moment (choose no more than three):

China

Australia

Japan

Southeast Asia

Pan-Asian funds

South Korea

India

Vietnam

Indonesia

Taiwan

Asia via global funds

Asia via fund-of-funds

I do not invest in Asia

Other

Percentage of Respondents (%)

Source: Probitas Partners’ Private Equity Institutional Investor Trends for 2014 Survey

0 10 20 30 40 50 60

3621

1422

1420

07

1114

42

02

44

6

5421

4338

7

0

01

4

22

2

Overall Respondents Asian Respondents

15

© 2013 Probitas Partners Private Equity Institutional Investor Trends for 2014 Survey

• Interest in Japan surged from 9% last year to 22% this year on the back of theintroduction of Abenomics instituted by the new government.

• The biggest difference between Asian respondents and overall respondents this year is a much greater interest in Japan; however, there were a disproportionatenumber of Japanese respondents in the survey this year focused on their homemarket, skewing the Asian results.

• In last year’s survey, 30% of overall respondents targeted India, while this

year only 7% of overall respondents and none of the Asian respondents werefocused on it.

• Indonesian interest fell to 2% this year from 14% last year as many investorshave made bets on Indonesia over the last two years and now have baselineexposures and are increasingly concerned about liquidity and politicalstability there.

8/13/2019 Probitas Private Equity Survey Trends2014

http://slidepdf.com/reader/full/probitas-private-equity-survey-trends2014 18/36

Table II Which Geographies in Asia Are of the Most Interest in Private Equity? Top four responses:

2007 2014

Country/Region % Targeting Country/Region % Targeting

China 28% China 38%

India 28% Southeast Asia 22%

Japan 25% Australia 22%

I do not invest in Asia 25% Japan 22%

Source: Probitas Partners’ Survey of Institutional Limited Partners, 2007 & 2014

16

Private Equity Institutional Investor Trends for 2014 Survey © 2013 Probitas Partners

Table II highlights how investor interests within the Asian market have changedsince the Financial Crisis started.

• In 2007, China, India, and Japan enjoyed nearly equal investor interest. Sincethen, interest in India has fallen precipitously as investors grew increasinglyconcerned over a lack of exits.

• Appetite for Japan has gone through a cycle of steady decline through 2013,then rebounding strongly this year on the back of the economic policies of the

new Japanese government.

• Interest in Southeast Asian funds has increased only over the last three years,driven in part by investor’s desire to diversify away from China exposure, while

Australia benefits in this year’s survey from a large number of Austral ianrespondents targeting their home market.

• The biggest change in emerging market interest over the last year, detailed inChart XV, is the increased number not investing in emerging markets — nearlydouble last year, rising from 18% to 32%.

• China and Brazil continue to lead investors’ interest in emerging markets,though interest in both has declined noticeably over the last year.

• Interest in India continued its decline the last few years as investorscomplain about the lack of exits from previous Indian funds they backed,while interest in Turkey plummeted as political turmoil negatively affectedinvestor’s perceptions.

• The other BRIC country — Russia — continued to trail significantly in the survey,as it has for a number of years. Limited partners tell us that they are concernedabout investors’ rights under Russian law.

8/13/2019 Probitas Private Equity Survey Trends2014

http://slidepdf.com/reader/full/probitas-private-equity-survey-trends2014 19/36

Chart XV Most Attractive Emerging MarketsWhich emerging markets do you nd most attractive (choose no more than four):

China

Brazil

Turkey

Southeast Asia

Indonesia

I do not invest in emerging markets

Pan-Latin America

India

South Korea

Central Europe (Poland, Czech Republic, Hungary, etc.)

Colombia

Mexico

Pan-Asia

Russia

Peru

Eastern Europe (Russia, Ukraine, Georgia, etc.)

Chile

MENA

I only invest in global emerging market funds

Vietnam

Sub-Saharan Africa

Other

Emerging market via funds-of-funds

Percentage of Respondents (%)

Source: Probitas Partners’ Private Equity Institutional Investor Trends for 2014 Survey

0 5 10 15 20 25 30 35 40

20132014

33

18

20

18

23

9

10

10

6

54

8

6

2

3

2

13

33

5

20

11

32

1817

12

610

7

98

118

24

4

0

2

3

6

3

3

3

5

38

20

7

17

© 2013 Probitas Partners Private Equity Institutional Investor Trends for 2014 Survey

8/13/2019 Probitas Private Equity Survey Trends2014

http://slidepdf.com/reader/full/probitas-private-equity-survey-trends2014 20/36

Chart XVI Interest in Emerging Market Private Equity My interest in emerging market private equity is driven by (check all that apply):

Strong long-term economic growthin a number of these countries

Desire to diversify my private equity portfolio by geographyto achieve benets of lack of correlation

I am less interested in emerging markets i n general than inexposure to a few specic countries with large opportunities

Lower forecast returns in the established markets of private

equity make this sector relatively more attractive As an institutional investor from an emerging market,

I am looking to support my home markets

Other

Percentage of Respondents (%)

Source: Probitas Partners’ Private Equity Institutional Investor Trends for 2014 Survey

0 10 20 30 40 50 60

55

36

20

18

3

10

18

Private Equity Institutional Investor Trends for 2014 Survey © 2013 Probitas Partners

• The driving factor that attracted investor’s interest in emerging markets wasthe prospect of strong long-term economic growth that was likely to positivelyimpact returns. However, the number of respondents who felt compelled toinvest in emerging markets on that theory dropped from 77% two years agoto 55% (Chart XVI).

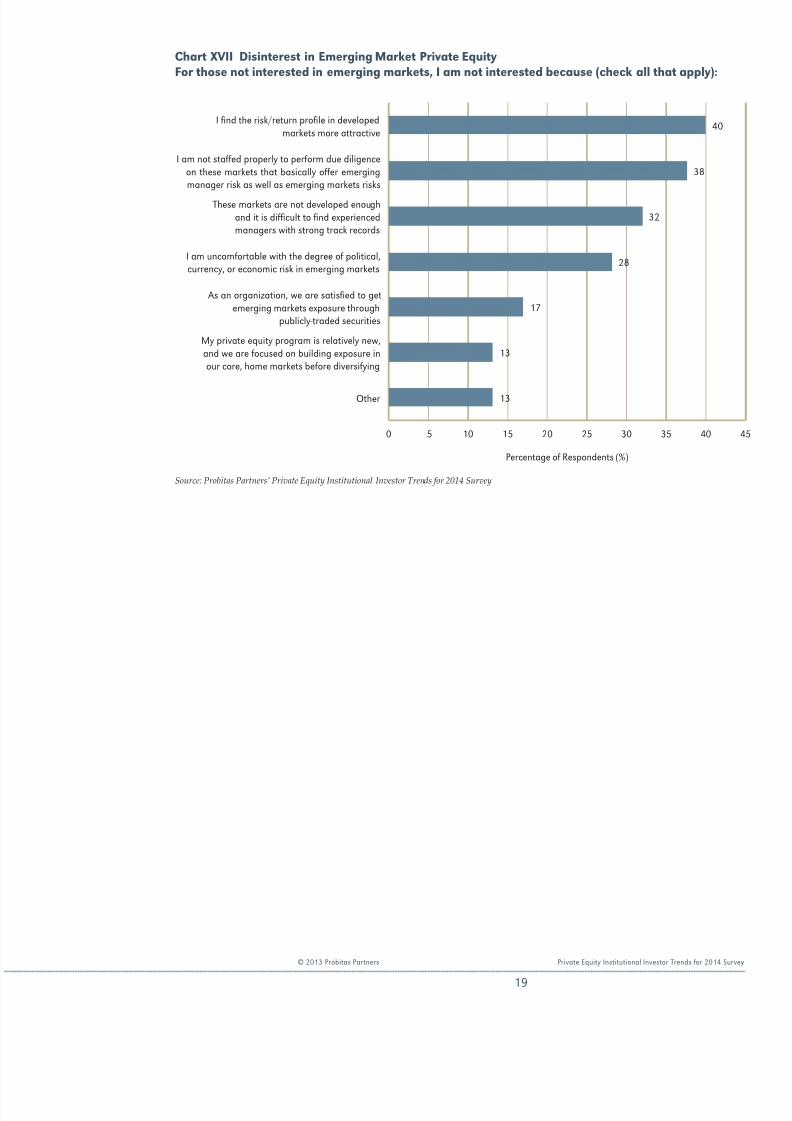

• For investors who are not interested in emerging markets (Chart XVII), thereasons are much more diverse and not dominated by a single reason.

8/13/2019 Probitas Private Equity Survey Trends2014

http://slidepdf.com/reader/full/probitas-private-equity-survey-trends2014 21/36

Chart XVII Disinterest in Emerging Market Private Equity For those not interested in emerging markets, I am not interested because (check all that apply):

I nd the risk/return prole in developedmarkets more attractive

I am not staffed properly to perform due diligenceon these markets that basically offer emergingmanager risk as well as emerging markets risks

These markets are not developed enoughand it is difcult to nd experiencedmanagers with strong track records

I am uncomfortable with the degree of political,currency, or economic risk in emerging markets

As an organization, we are satised to getemerging markets exposure through

publicly-traded securities

My private equity program is relatively new,and we are focused on building exposure inour core, home markets before diversifying

Other

Percentage of Respondents (%)

Source: Probitas Partners’ Private Equity Institutional Investor Trends for 2014 Survey

0 5 10 15 20 25 30 35 40 45

40

38

32

28

17

13

13

19

© 2013 Probitas Partners Private Equity Institutional Investor Trends for 2014 Survey

8/13/2019 Probitas Private Equity Survey Trends2014

http://slidepdf.com/reader/full/probitas-private-equity-survey-trends2014 22/36

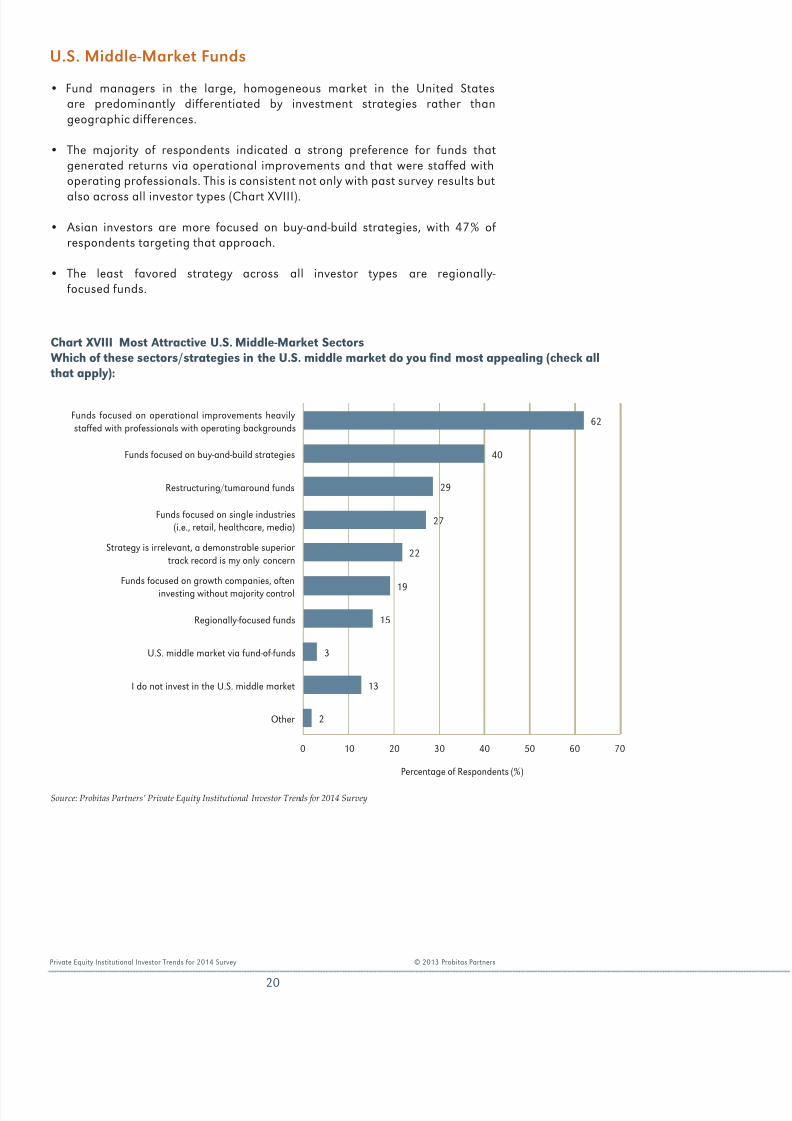

Chart XVIII Most Attractive U.S. Middle-Market SectorsWhich of these sectors/strategies in the U.S. middle market do you nd most appealing (check allthat apply):

Funds focused on operational improvements heavilystaffed with professionals with operating backgrounds

Funds focused on buy-and-build strategies

Restructuring/turnaround funds

Funds focused on single industries(i.e., retail, healthcare, media)

Strategy is irrelevant, a demonstrable superiortrack record is my only concern

Funds focused on growth companies, ofteninvesting without majority control

Regionally-focused funds

U.S. middle market via fund-of-funds

I do not invest in the U.S. middle market

Other

Percentage of Respondents (%)

Source: Probitas Partners’ Private Equity Institutional Investor Trends for 2014 Survey

0 10 20 30 40 50 60 70

62

40

19

2

29

27

22

13

3

15

20

Private Equity Institutional Investor Trends for 2014 Survey © 2013 Probitas Partners

U.S. Middle-Market Funds

• Fund managers in the large, homogeneous market in the United Statesare predominantly differentiated by investment strategies rather thangeographic differences.

• The majority of respondents indicated a strong preference for funds thatgenerated returns via operational improvements and that were staffed withoperating professionals. This is consistent not only with past survey results but

also across all investor types (Chart XVIII).

• Asian investors are more focused on buy-and-build strategies, with 47% ofrespondents targeting that approach.

• The least favored strategy across all investor types are regionally-focused funds.

8/13/2019 Probitas Private Equity Survey Trends2014

http://slidepdf.com/reader/full/probitas-private-equity-survey-trends2014 23/36

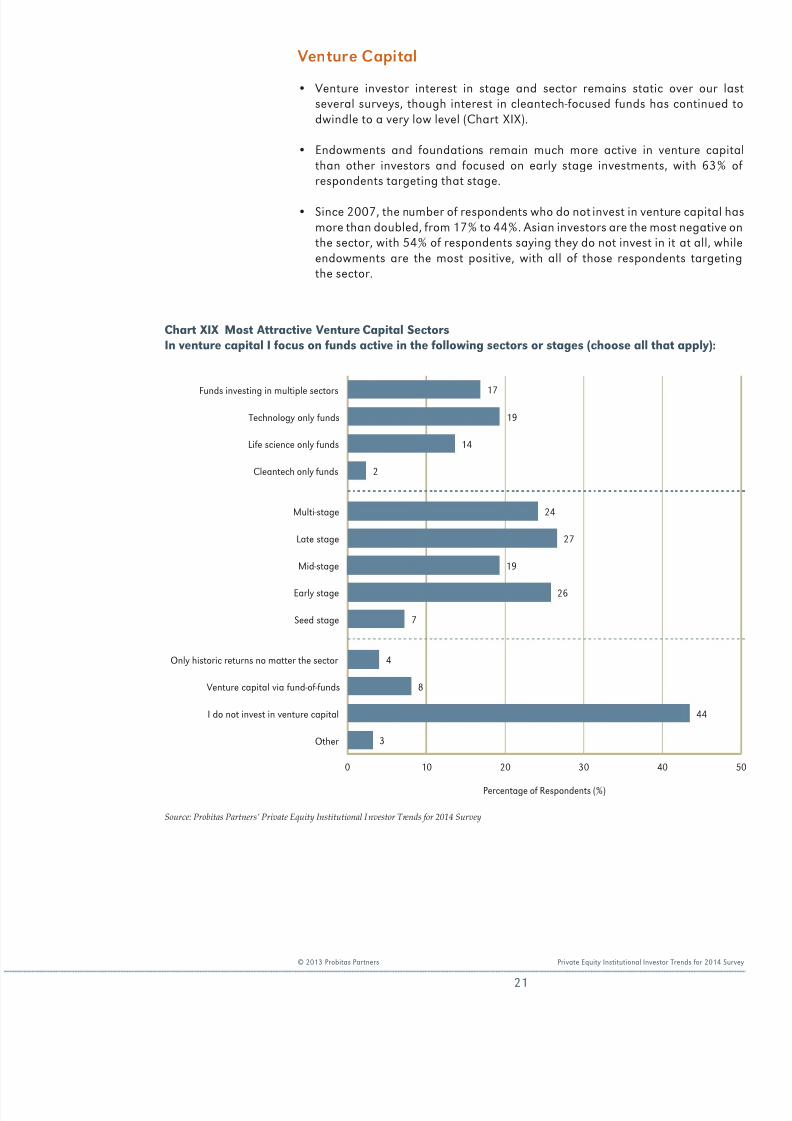

Chart XIX Most Attractive Venture Capital SectorsIn venture capital I focus on funds active in the following sectors or stages (choose all that apply):

Funds investing in multiple sectors

Technology only funds

Life science only funds

Cleantech only funds

Multi-stage

Late stage

Mid-stage

Early stage

Seed stage

Only historic returns no matter the sector

Venture capital via fund-of-funds

I do not invest in venture capital

Other

Percentage of Respondents (%)

Source: Probitas Partners’ Private Equity Institutional Investor Trends for 2014 Survey

0 10 20 30 40 50

24

27

2

3

7

26

4

14

44

17

19

8

19

21

© 2013 Probitas Partners Private Equity Institutional Investor Trends for 2014 Survey

Venture Capital

• Venture investor interest in stage and sector remains static over our lastseveral surveys, though interest in cleantech-focused funds has continued todwindle to a very low level (Chart XIX).

• Endowments and foundations remain much more active in venture capitalthan other investors and focused on early stage investments, with 63% ofrespondents targeting that stage.

• Since 2007, the number of respondents who do not invest in venture capital hasmore than doubled, from 17% to 44%. Asian investors are the most negative onthe sector, with 54% of respondents saying they do not invest in it at all, whileendowments are the most positive, with all of those respondents targetingthe sector.

8/13/2019 Probitas Private Equity Survey Trends2014

http://slidepdf.com/reader/full/probitas-private-equity-survey-trends2014 24/36

Chart XX Distressed InvestmentsWithin the distressed debt/restructuring sector, I am most interested in (choose no more than two):

Restructuring/turnaround funds (focusedon equity, not debt)

Distressed debt for control funds(loan-to-own)

Opportunistic credit (mispriced debt, smallloan portfolios, etc.)

Distressed debt: active/non-control funds

Distressed debt trading funds

Distressed debt hedge funds

I do not invest in this sector

Other

Percentage of Respondents (%)

Source: Probitas Partners’ Private Equity Institutional Investor Trends for 2014 Survey

0 10 20 30 40 50 60

26

21

18

3

50

55

3

1

22

Private Equity Institutional Investor Trends for 2014 Survey © 2013 Probitas Partners

Niche Private Equity Sectors

• There are several distinct distressed strategies, but many fund managerspursue a combination of these approaches within the same fund.

• Most respondents prefer strategies with a value-added focus that generateshigher multiples of return. In all our previous surveys, restructuring/turnaroundfunds and distressed debt for control funds have switched back and forth forthe lead in the sector (Chart XX).

• Opportunistic credit funds (that usually have a strong focus on assets otherthan corporate debt) are another area of focus for investors. While someinvestors have expanded their distressed debt category to include more creditstrategies, others still consider it a straight credit or fixed income product, andtherefore not in their alternatives allocation.

8/13/2019 Probitas Private Equity Survey Trends2014

http://slidepdf.com/reader/full/probitas-private-equity-survey-trends2014 25/36

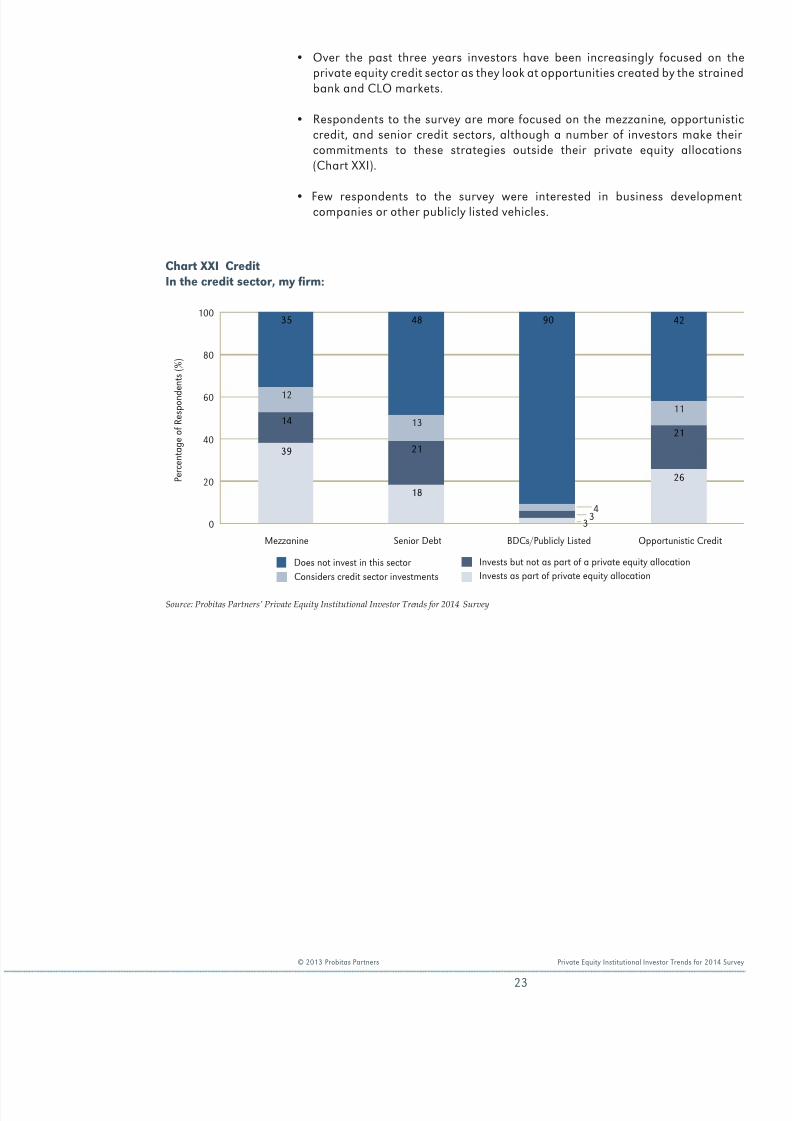

Chart XXI CreditIn the credit sector, my rm:

P e r c e n

t a g e o

f R e s p o n d e n

t s ( % )

100

80

60

40

20

0

Mezzanine Senior Debt BDCs/Publicly Listed Opportunistic Credit

Source: Probitas Partners’ Private Equity Institutional Investor Trends for 2014 Survey

Considers credit sector investmentsDoes not invest in this sector Invests but not as part of a private equity allocation

Invests as part of private equity allocation

35

12

14

39

48

13

21

18

90

26

21

11

42

334

23

© 2013 Probitas Partners Private Equity Institutional Investor Trends for 2014 Survey

• Over the past three years investors have been increasingly focused on theprivate equity credit sector as they look at opportunities created by the strainedbank and CLO markets.

• Respondents to the survey are more focused on the mezzanine, opportunisticcredit, and senior credit sectors, although a number of investors make theircommitments to these strategies outside their private equity allocations(Chart XXI).

• Few respondents to the survey were interested in business developmentcompanies or other publicly listed vehicles.

8/13/2019 Probitas Private Equity Survey Trends2014

http://slidepdf.com/reader/full/probitas-private-equity-survey-trends2014 26/36

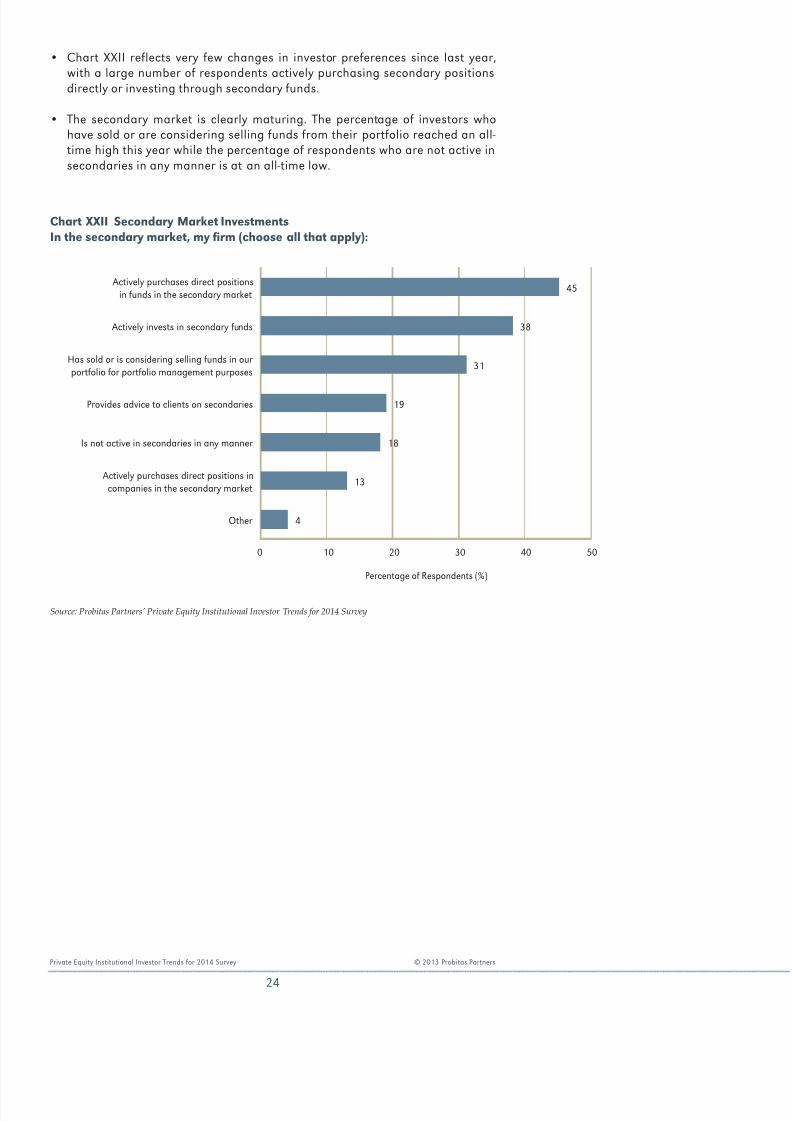

Chart XXII Secondary Market InvestmentsIn the secondary market, my rm (choose all that apply):

Actively purchases direct positionsin funds in the secondary market

Actively invests in secondary funds

Has sold or is considering selling funds in ourportfolio for portfolio management purposes

Provides advice to clients on secondaries

Is not active in secondaries in any manner

Actively purchases direct positions incompanies in the secondary market

Other

Percentage of Respondents (%)

Source: Probitas Partners’ Private Equity Institutional Investor Trends for 2014 Survey

0 10 20 30 40 50

45

38

31

19

18

13

4

24

Private Equity Institutional Investor Trends for 2014 Survey © 2013 Probitas Partners

• Chart XXII reflects very few changes in investor preferences since last year,with a large number of respondents actively purchasing secondary positionsdirectly or investing through secondary funds.

• The secondary market is clearly maturing. The percentage of investors whohave sold or are considering selling funds from their portfolio reached an all-time high this year while the percentage of respondents who are not active insecondaries in any manner is at an all-time low.

8/13/2019 Probitas Private Equity Survey Trends2014

http://slidepdf.com/reader/full/probitas-private-equity-survey-trends2014 27/36

Chart XXIII Directs and Co-InvestmentsRegarding directs and co-investments, my rm (choose all that apply):

Has an active internal co-investment program

Only opportunistically pursues co-investments

Does not invest in co-investmentsnor directly invests in companies

Provides advice to clients on co-investment

or direct investments

Invests directly in companies

Requires or prefers a co-investment as ameans of diligencing a new fund manager

Has an outsourced co-investment program

Other

Percentage of Respondents (%)

Source: Probitas Partners’ Private Equity Institutional Investor Trends for 2014 Survey

Note: “Large Investors” denotes those survey respondents who plan to commit $500 million or more to private equity in 2014

0 10 20 30 40 50 60

Large Investors All Respondents

30

3019

3426

35

1211

1226

47

20

14

25

© 2013 Probitas Partners Private Equity Institutional Investor Trends for 2014 Survey

• As Chart XXIII details, the majority of institutional investors do not pursue co-investments or direct investments, or only do so opportunistically because ofstaff or capital limitations.

• However, the largest investors are much more likely to have an active co-investment program; 59% of these large respondents have an active internalco-investment program, while another 7% have outsourced programs and 11%invest directly in companies.

8/13/2019 Probitas Private Equity Survey Trends2014

http://slidepdf.com/reader/full/probitas-private-equity-survey-trends2014 28/36

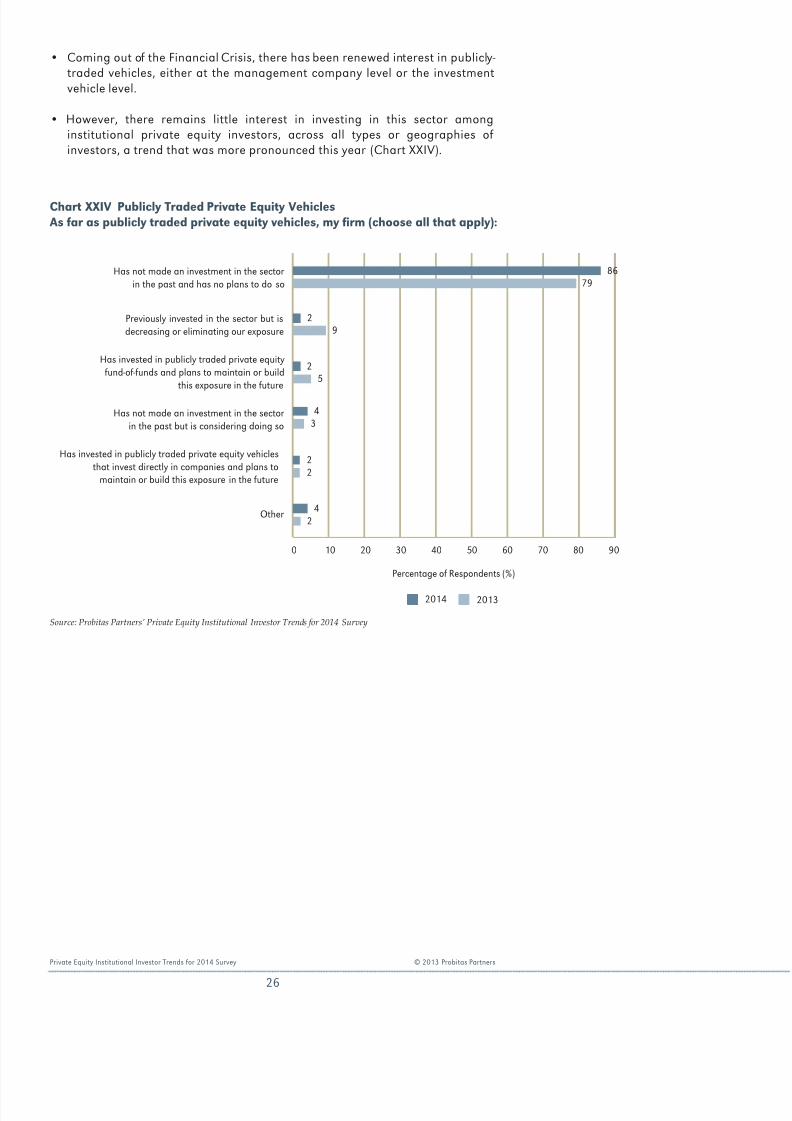

Chart XXIV Publicly Traded Private Equity Vehicles As far as publicly traded private equity vehicles, my rm (choose all that apply):

Has not made an investment in the sectorin the past and has no plans to do so

Previously invested in the sector but isdecreasing or eliminating our exposure

Has invested in publicly traded private equityfund-of-funds and plans to maintain or build

this exposure in the future

Has not made an investment in the sectorin the past but is considering doing so

Has invested in publicly traded private equity vehiclesthat invest directly in companies and plans to

maintain or build this exposure in the future

Other

Percentage of Respondents (%)

Source: Probitas Partners’ Private Equity Institutional Investor Trends for 2014 Survey

0 10 20 30 40 50 60 70 80 90

2013 2014

43

25

79

29

22

2

86

4

26

Private Equity Institutional Investor Trends for 2014 Survey © 2013 Probitas Partners

• Coming out of the Financial Crisis, there has been renewed interest in publicly-traded vehicles, either at the management company level or the investmentvehicle level.

• However, there remains little interest in investing in this sector amonginstitutional private equity investors, across all types or geographies ofinvestors, a trend that was more pronounced this year (Chart XXIV).

8/13/2019 Probitas Private Equity Survey Trends2014

http://slidepdf.com/reader/full/probitas-private-equity-survey-trends2014 29/36

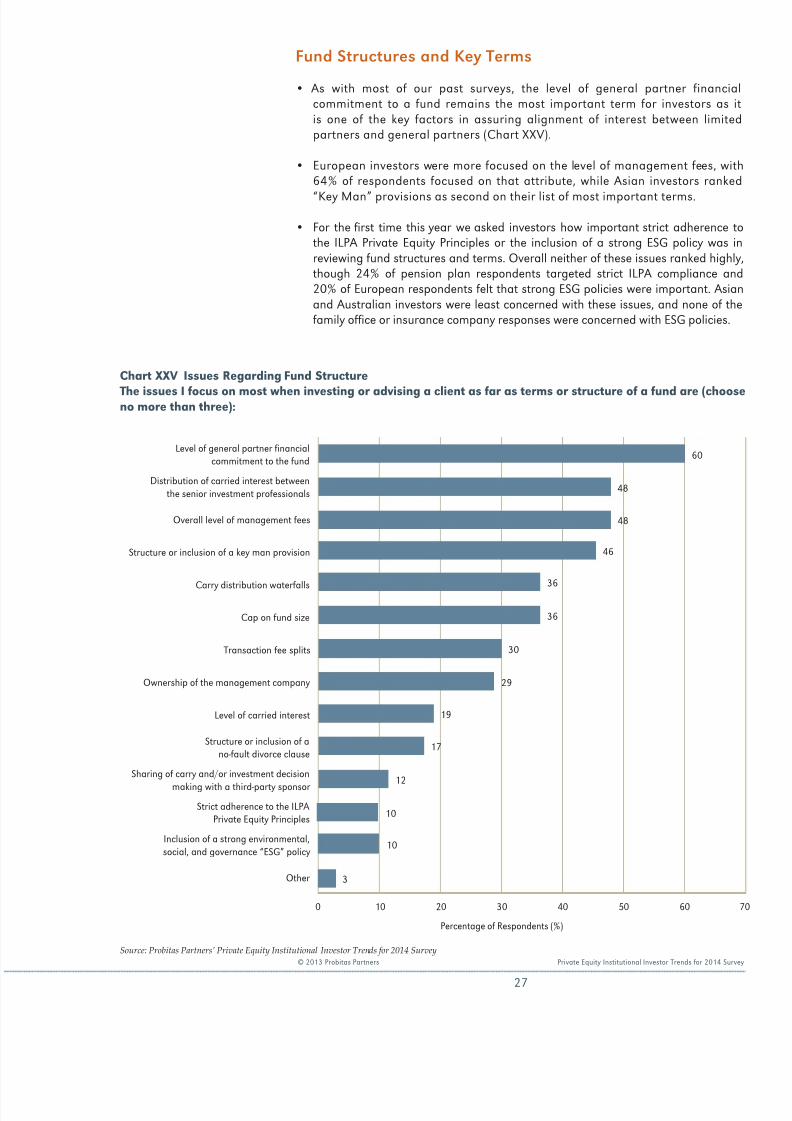

Chart XXV Issues Regarding Fund Structure

The issues I focus on most when investing or advising a client as far as terms or structure of a fund are (chooseno more than three):

Level of general partner nancialcommitment to the fund

Distribution of carried interest betweenthe senior investment professionals

Overall level of management fees

Structure or inclusion of a key man provision

Carry distribution waterfalls

Cap on fund size

Transaction fee splits

Ownership of the management company

Level of carried interest

Structure or inclusion of ano-fault divorce clause

Sharing of carry and/or investment decision

making with a third-party sponsor Strict adherence to the ILPA

Private Equity Principles

Inclusion of a strong environmental,social, and governance “ESG” policy

Other

Percentage of Respondents (%)

Source: Probitas Partners’ Private Equity Institutional Investor Trends for 2014 Survey

0 10 20 30 40 50 60 70

17

19

29

30

36

36

46

48

48

12

10

60

3

10

27

© 2013 Probitas Partners Private Equity Institutional Investor Trends for 2014 Survey

Fund Structures and Key Terms

• As with most of our past surveys, the level of general partner financialcommitment to a fund remains the most important term for investors as itis one of the key factors in assuring alignment of interest between limitedpartners and general partners (Chart XXV).

• European investors were more focused on the level of management fees, with64% of respondents focused on that attribute, while Asian investors ranked

“Key Man” provisions as second on their list of most important terms.

• For the rst time this year we asked investors how important strict adherence tothe ILPA Private Equity Principles or the inclusion of a strong ESG policy was inreviewing fund structures and terms. Overall neither of these issues ranked highly,though 24% of pension plan respondents targeted strict ILPA compliance and20% of European respondents felt that strong ESG policies were important. Asianand Australian investors were least concerned with these issues, and none of thefamily ofce or insurance company responses were concerned with ESG policies.

8/13/2019 Probitas Private Equity Survey Trends2014

http://slidepdf.com/reader/full/probitas-private-equity-survey-trends2014 30/36

28

Private Equity Institutional Investor Trends for 2014 Survey © 2013 Probitas Partners

• In past surveys we asked investors in more detail about the ILPA Private EquityPrinciples and found that though few investors insisted on strict compliance tothe Principles, a majority of investors of all types used them as a starting point forterms negotiations.

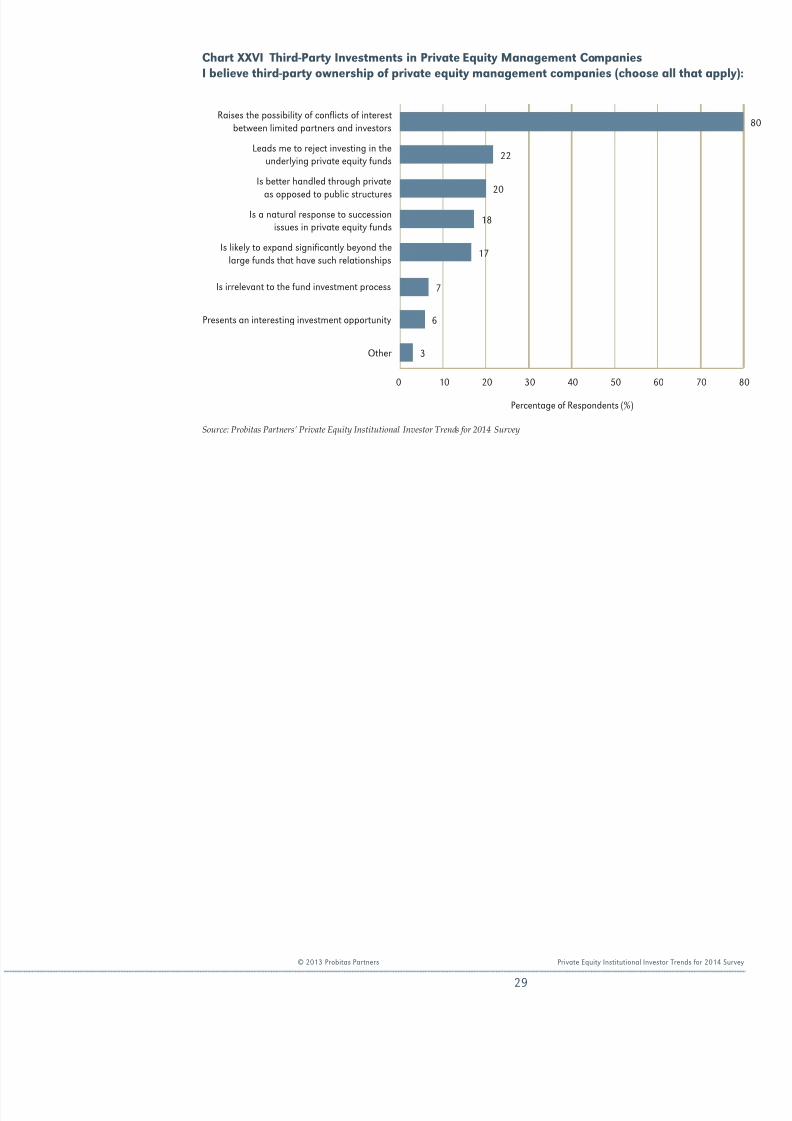

• After a pause during the Financial Crisis, there has been a resurgence in third-party investment in private equity management companies.

• Similar to our previous surveys, limited partners’ strongest reaction is that

these investments create possible conflicts of interest between investors whoacquire positions in general partner management companies and limitedpartners in the funds (Chart XXVI).

• Though many investors feel these structures create potential conflicts ofinterest, only 22% stated that this would lead them to reject investing inthe underlying funds, down from 41% last year. Geographically, there is adistinct difference, with only 5% of Asian investors saying they would reject afund because of third-party investment in the general partner, while 31% ofEuropean respondents said that they would reject such a fund.

• Only 6% of respondents felt that investing in a private equity managementcompany represented an attractive opportunity.

8/13/2019 Probitas Private Equity Survey Trends2014

http://slidepdf.com/reader/full/probitas-private-equity-survey-trends2014 31/36

Chart XXVI Third-Party Investments in Private Equity Management CompaniesI believe third-party ownership of private equity management companies (choose all that apply):

Raises the possibility of conicts of interestbetween limited partners and investors

Leads me to reject investing in theunderlying private equity funds

Is better handled through private

as opposed to public structuresIs a natural response to succession

issues in private equity funds

Is likely to expand signicantly beyond thelarge funds that have such relationships

Is irrelevant to the fund investment process

Presents an interesting investment opportunity

Other

Percentage of Respondents (%)

Source: Probitas Partners’ Private Equity Institutional Investor Trends for 2014 Survey

6

7

17

20

22

3

0 10 20 30 40 50 60 70 80

18

29

© 2013 Probitas Partners Private Equity Institutional Investor Trends for 2014 Survey

8/13/2019 Probitas Private Equity Survey Trends2014

http://slidepdf.com/reader/full/probitas-private-equity-survey-trends2014 32/36

30

Private Equity Institutional Investor Trends for 2014 Survey © 2013 Probitas Partners

Investor Fears and Concerns

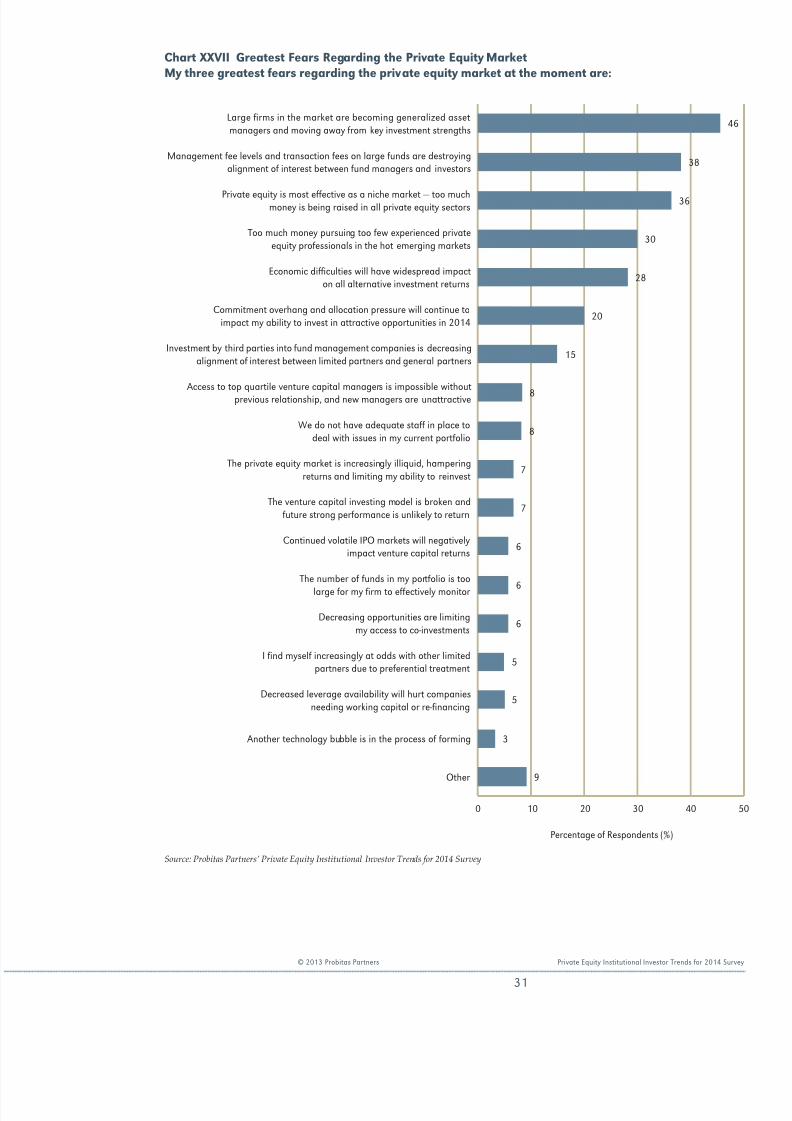

• The greatest fear of most private equity investors was that large funds arebecoming generalized asset managers and are moving away from their keyinvestment strengths. Last year, this was only the third most noted issue with33% of respondents mentioning it (Chart XXVII). European investors felt evenmore strongly about this issue, with 64% mentioning it.

• The biggest difference geographically was in Asia, where the greatest concern

(mentioned by 40% of respondents) was that too much money was chasingtoo few experienced private equity professionals in what are becoming over-heated emerging markets.

• Fears that economic difficulties would impact alternative investment returnsfell significantly from the first-ranked issue last year (mentioned by 48% ofrespondents) to only fifth place this year.

• We also encouraged respondents to state their own greatest fears or concernsnot included in our pre-set list. Answers included the following:

• Fund managers do not have enough “skin in the game” and as a consequencewe are starting to see again practices seen prior to the Financial Crisis interms of leverage level, especially in the United States.

• The opportunity is good, but the investment structures are poor.

• Lack of adequate exit opportunities (IPOs, strategic buyers) to absorbthe number of companies that will need to be exited over the nexttwo to four years.

• Credit bubble fed by aggressive searches of yield will cause another privateequity crisis in a few years’ time.

• Poor liquidity and distributions.

• Generational transition at firms when heir apparents likely have modestattributable track records largely from the last ten years.

• Too much secondary capital to be invested and the rapid increase in co- investment activity.

• Large limited partners are not being active enough with their general partners.

• Are the right funds getting funded, are the right limited partners gettingaccess, are the right entrepreneurs getting funded?

8/13/2019 Probitas Private Equity Survey Trends2014

http://slidepdf.com/reader/full/probitas-private-equity-survey-trends2014 33/36

Chart XXVII Greatest Fears Regarding the Private Equity MarketMy three greatest fears regarding the private equity market at the moment are:

Large rms in the market are becoming generalized assetmanagers and moving away from key investment strengths

Management fee levels and transaction fees on large funds are destroyingalignment of interest between fund managers and investors

Private equity is most effective as a niche market — too muchmoney is being raised in all private equity sectors

Too much money pursuing too few experienced privateequity professionals in the hot emerging markets

Economic difculties will have widespread impacton all alternative investment returns

Commitment overhang and allocation pressure will continue toimpact my ability to invest in attractive opportunities in 2014

Investment by third parties into fund management companies is decreasingalignment of interest between limited partners and general partners

Access to top quartile venture capital managers is impossible withoutprevious relationship, and new managers are unattractive

We do not have adequate staff in place todeal with issues in my current portfolio

The private equity market is increasingly illiquid, hamperingreturns and limiting my ability to reinvest

The venture capital investing model is broken andfuture strong performance is unlikely to return

Continued volatile IPO markets will negativelyimpact venture capital returns

The number of funds in my portfolio is toolarge for my rm to effectively monitor

Decreasing opportunities are limitingmy access to co-investments

I nd myself increasingly at odds with other limitedpartners due to preferential treatment

Decreased leverage availability will hurt companiesneeding working capital or re-nancing

Another technology bubble is in the process of forming

Other

Percentage of Respondents (%)

Source: Probitas Partners’ Private Equity Institutional Investor Trends for 2014 Survey

46

38

36

20

7

6

7

8

8

15

28

30

6

6

3

5

5

9

0 10 20 30 40 50

31

© 2013 Probitas Partners Private Equity Institutional Investor Trends for 2014 Survey

8/13/2019 Probitas Private Equity Survey Trends2014

http://slidepdf.com/reader/full/probitas-private-equity-survey-trends2014 34/36

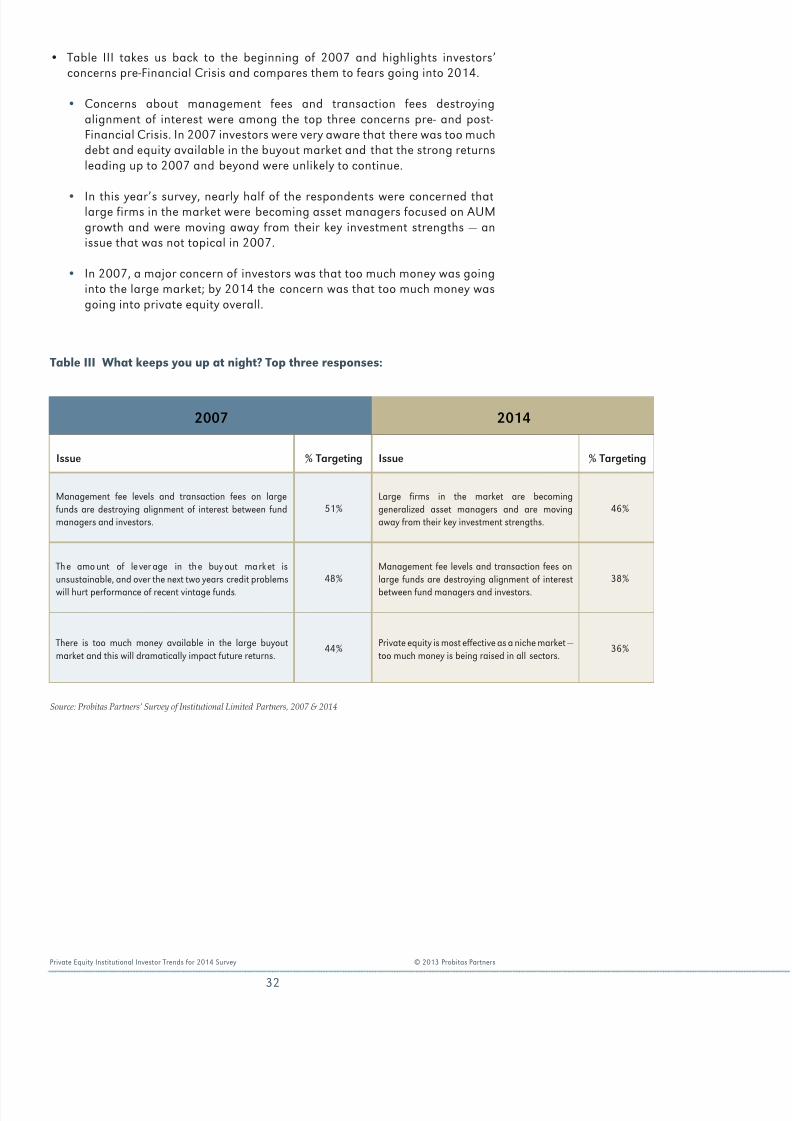

Table III What keeps you up at night? Top three responses:

2007 2014

Issue % Targeting Issue % Targeting

Management fee levels and transaction fees on largefunds are destroying alignment of interest between fundmanagers and investors.

51%Large rms in the market are becominggeneralized asset managers and are movingaway from their key investment strengths.

46%

The amo unt of lever age in the buy out market isunsustainable, and over the next two years credit problemswill hurt performance of recent vintage funds.

48%Management fee levels and transaction fees onlarge funds are destroying alignment of interestbetween fund managers and investors.

38%

There is too much money available in the large buyoutmarket and this will dramatically impact future returns.

44% Private equity is most effective as a niche market —too much money is being raised in all sectors.

36%

Source: Probitas Partners’ Survey of Institutional Limited Partners, 2007 & 2014

32

Private Equity Institutional Investor Trends for 2014 Survey © 2013 Probitas Partners

• Table III takes us back to the beginning of 2007 and highlights investors’concerns pre-Financial Crisis and compares them to fears going into 2014.

• Concerns about management fees and transaction fees destroyingalignment of interest were among the top three concerns pre- and post-Financial Crisis. In 2007 investors were very aware that there was too muchdebt and equity available in the buyout market and that the strong returnsleading up to 2007 and beyond were unlikely to continue.

• In this year’s survey, nearly half of the respondents were concerned thatlarge firms in the market were becoming asset managers focused on AUMgrowth and were moving away from their key investment strengths — anissue that was not topical in 2007.

• In 2007, a major concern of investors was that too much money was goinginto the large market; by 2014 the concern was that too much money wasgoing into private equity overall.

8/13/2019 Probitas Private Equity Survey Trends2014

http://slidepdf.com/reader/full/probitas-private-equity-survey-trends2014 35/36

33

© 2013 Probitas Partners Private Equity Institutional Investor Trends for 2014 Survey

Our View of the Future

Several key trends for 2014 emerge from the survey and our ongoing conversationswith investors:

• Fundraising globally will hit a new post-Financial Crisis high this yearwith continuing strength in 2014. Weakness in Asia and emerging marketfundraising are being made up by strong interest in North America andEurope, while significant realizations and continued strong public markets

valuations are giving limited partners more room to deploy capital. However,the staff of many limited partners is being stressed by a wave of re-ups thatis affecting their bandwidth to review new relationships.

• The new performance metric — cash — driving increased exits. Manyinvestors have added a key metric of performance to IRR and multiple ofcapital: distributions on paid in capital (“DPI”), or actual cash returned.

This new metr ic is forcing greater realizat ions before many fund managersare able to secure new fund commitments. In North America and Europe,increased distributions are leading many investors to recycle cash receivedinto new commitments to funds with solid DPI performance.

• Investors are becoming more cautious regarding emerging markets. A number of key emerging markets have been plagued by limited liquiditywhile others have suffered from political turmoil. Though investors believethat the long-term economic growth potential of emerging markets is high,they are less certain of the shorter-term prospects for private equity returnsin specific markets, especially compared with what appear to be competitivereturns in developed markets with less risk.

• Interest in venture capital will remain weak — but that is not necessarilybad. A large number of investors have given up on venture capital entirely,with 43% of respondents to this year’s survey saying they do not investin venture capital, the highest mark ever. However, a number of limitedpartners still targeting the sector believe that the lack of price inflationfor venture company investments that should result from less competitionshould increase future venture capital returns.

• Increased interest in hard asset plays. A number of sophisticated investorsworried about economic uncertainty and future asset shortages, as wellas those seeking to match long-term liabilities, are increasingly turning tohard asset sectors such as energy, agriculture, mining, and timber. Severalpension funds have created separate inflation-linked allocations outside oftheir private equity, real estate and debt allocations, though many investorswith these allocations express frustration because there are few productsavailable with experienced management teams and deep track records.

• The past as future — “middle-market, operationally-focused funds.” In all

of our past surveys and conversations with investors, there has always beena pronounced preference for middle-market buyout funds with operationalfocus. We do not expect that to change prospectively. What does continueto vary on the topic, however, is the definition of what “middle market” is,or what defines an “operational focus.” Given increased interested in thespace, we expect to see broader definitions emerge.

8/13/2019 Probitas Private Equity Survey Trends2014

http://slidepdf.com/reader/full/probitas-private-equity-survey-trends2014 36/36

Probitas Funds Group, LLC Probitas Funds Group, LLC PFG-UK Ltd. Probitas Hong Kong Limited

425 California Street 1120 Ave. of the Americas 4th Floor Egyptian House Nexxus BuildingSuite 2300 Suite 1802 170-173 Piccadilly Level 15San Francisco, CA 94104 New York, NY 10036 London, W1J 9EJ 41 Connaught RoadUSA USA UK Central, Hong Kong

Private Equity Inst itutional Investor

Trends for 2014 Survey