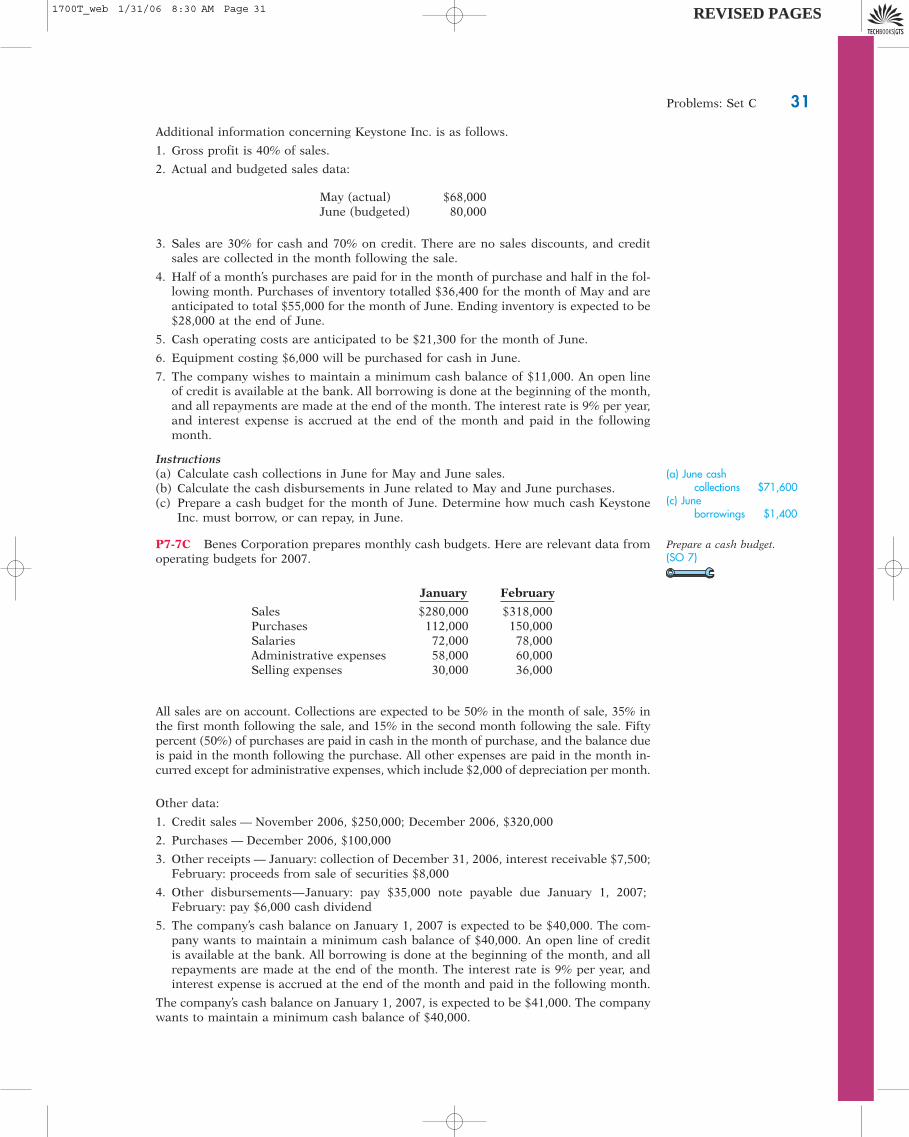

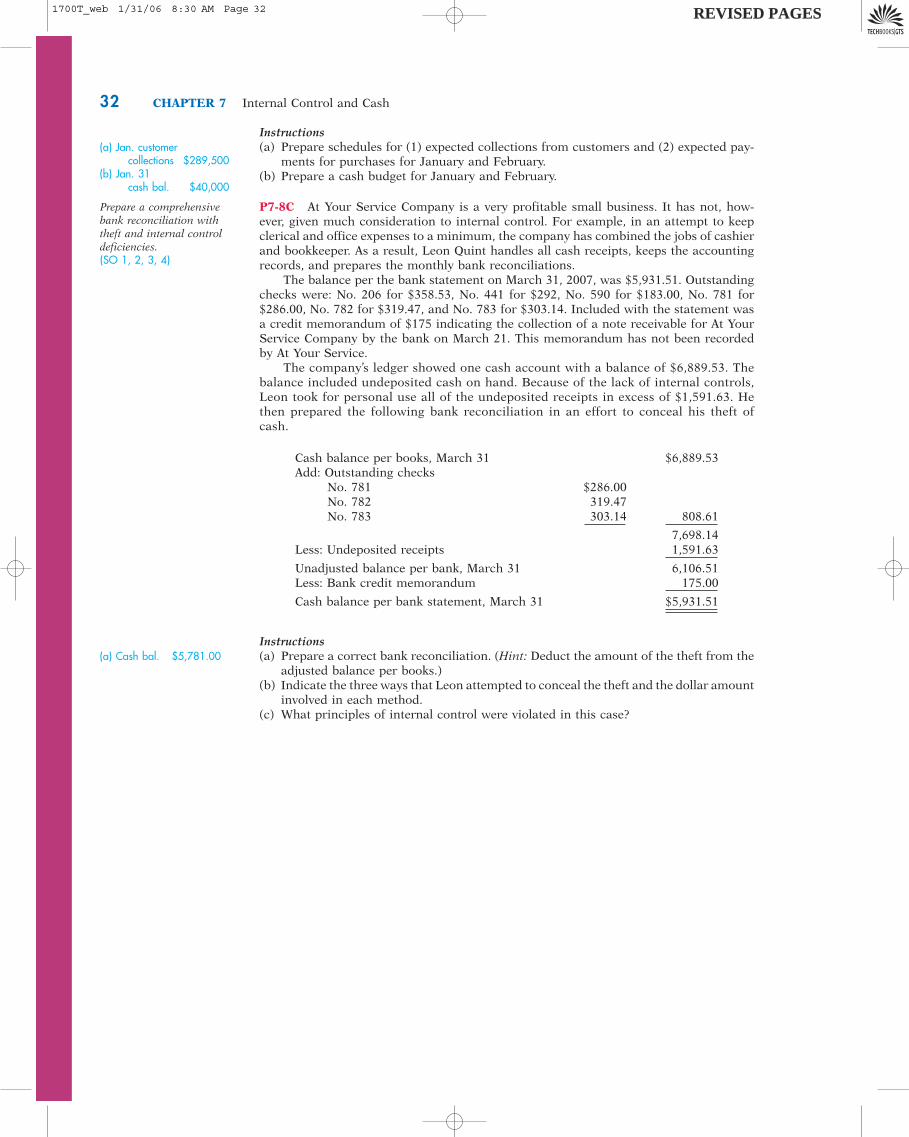

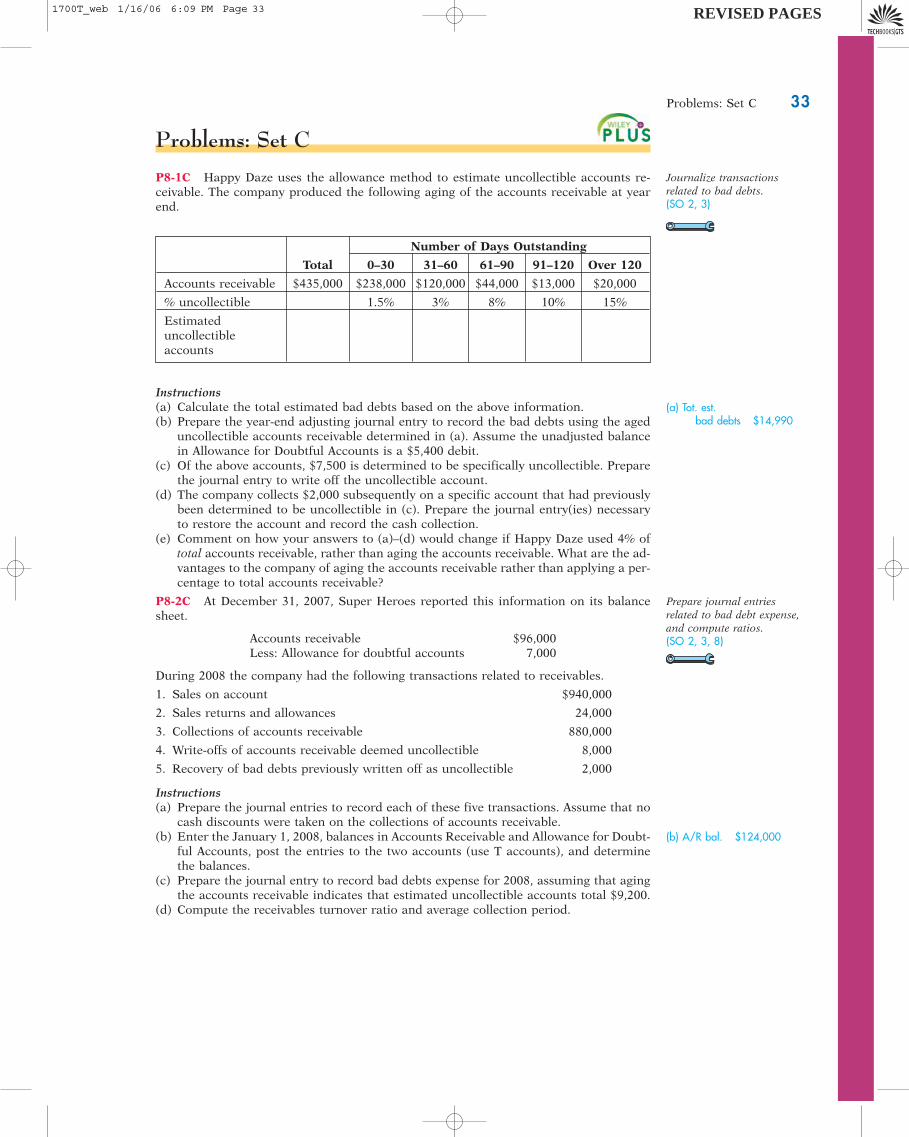

problemset c questions

TRANSCRIPT

Problems: Set C 1

Problems: Set C

P1-1C Presented below are five independent situations.(a) Christy Petersen and Joel Dunn each owned separate plastic molding businesses. They

have decided to combine their businesses. They expect that within the coming yearthey will need significant funds to expand their operations.

(b) Three licensed physical therapists have been working in rehabilitation hospitals forseveral years. They have decided to form a business that will provide therapy in clients’homes. Each has contributed an equal amount of cash and knowledge to the ven-ture. Although there appears to be a great need for their services, they are concernedabout the legal liabilities that their business might confront.

(c) Erik, Geoff, and Janna recently graduated with education degrees. They have beenfriends since childhood. They have decided to start a consulting business focused onassisting “home-schooled” students over the Internet.

(d) Ben Fullerton has been providing routine automotive maintenance and repair serv-ices for several years. He performs his work in customers’ garages out of a cargovan that contains tools, diagnostic equipment, and parts. Customers can continueto work or relax at home while he services their vehicles. His business has been sosuccessful that several regular customers have suggested he expand its operations.Ben is confident that he could find other mechanics to help provide the service butknows the business would require a large investment of capital to outfit the vans.He is also aware that working in customers’ homes could expose him to consider-able liability. Ben has no savings or personal assets. He wants to maintain controlover the business.

(e) Chad Browne, a college student looking for summer employment, opened a flowerstand at a local farmers’ market.

InstructionsIn each case explain what form of organization the business is likely to take—sole pro-prietorship, partnership, or corporation. Give reasons for your choice.

P1-2C Financial decisions often place heavier emphasis on one type of financial statement over the others. Consider each of the following hypothetical situations independently.(a) Nordstroms is considering extending credit to a new customer. The terms of the credit

would require the customer to pay within 30 days of receipt of goods.(b) An investor is considering purchasing common stock of Home Depot Company. The

investor plans to hold the investment for at least 5 years.(c) Wells Fargo is considering extending a loan to a small company. The company would

be required to make interest payments at the end of each year for 5 years, and to re-pay the loan at the end of the fifth year.

(d) The president of American Greetings is trying to determine whether the companyis generating enough cash to increase the amount of dividends paid to investorsin this and future years, and still have enough cash to buy equipment as it isneeded.

InstructionsIn each situation, state whether the decision maker would be most likely to place primaryemphasis on information provided by the income statement, balance sheet, or statementof cash flows. In each case provide a brief justification for your choice. Choose only onefinancial statement in each case.

P1-3C On August 1 Copicat Inc. was started with an initial investment in the company of $10,000 cash. Here are the assets and liabilities of the company atAugust 31, and the revenues and expenses for the month of August, its first month of operations:

Cash $ 3,800 Notes payable $6,000Accounts receivable 1,000 Accounts payable 900Revenue 11,000 Supplies expense 3,000Supplies 1,800 Rent expense 1,600Advertising expense 500 Utilities expense 200Equipment 12,000 Wage expense 3,400

Determine forms of businessorganization.(SO 1)

Identify users and uses offinancial statements.(SO 2, 4, 5)

Prepare an incomestatement, retained earningsstatement, and balance sheet,and discuss results.(SO 4, 5)

1700T_web 1/16/06 6:09 PM Page 1 REVISED PAGES

In August, the company issued no additional stock, but paid dividends of $600.

Instructions(a) Prepare an income statement and a retained earnings statement for the month of

August and a balance sheet at August 31, 2007.(b) Briefly discuss whether the company’s first month of operations was a success.(c) Discuss the company’s decision to distribute a dividend.

P1-4C Presented below is selected financial information for Showalter Corporation forDecember 31, 2007.

Inventory $ 19,000 Cash paid to purchase equipment $ 8,000Cash paid to suppliers 76,000 Equipment 40,000Building 200,000 Revenues 87,000Common stock 40,000 Cash received from customers 93,000Cash dividends paid 4,000 Cash received from issuing

common stock 18,000

Instructions(a) Determine which items should be included in a statement of cash flows and then pre-

pare the statement for Showalter Corporation.(b) Comment on the adequacy of net cash provided by operating activities to fund the

company’s investing activities and dividend payments.

P1-5C Julius Corporation was formed on January 1, 2007. At December 31, 2007, DanJasper, the president and sole stockholder, decided to prepare a balance sheet, which ap-peared as follows.

JULIUS CORPORATIONBalance Sheet

December 31, 2007

Assets Liabilities and Stockholders’ Equity

Cash $20,000 Accounts payable $40,000Accounts receivable 39,000 Notes payable 15,000Motorcycle 17,000 Motorcycle loan 14,000Truck 20,000 Stockholders’ equity 27,000

Dan willingly admits that he is not an accountant by training. He is concerned that hisbalance sheet might not be correct. He has provided you with the following additionalinformation.1. The motorcycle actually belongs to Jasper, not to Julius Corporation. However, because

he thinks he might use it to visit customers occasionally, he decided to list it as an as-set of the company. To be consistent he also listed as a liability of the corporation hispersonal loan that he took out at the bank to buy the motorcycle.

2. The truck was purchased for only $18,000, even though Dan knows its “sticker price”was $20,000. He thought it would be best to record it at $20,000.

3. Included in the accounts receivable balance is $8,000 that Dan expects to collect froma customer for a sale that he anticipates will occur in January. Dan included this inthe receivables of Julius Corporation because he has already discussed the potentialsale with the customer.

Instructions(a) Comment on the proper accounting treatment of the three items above.(b) Provide a corrected balance sheet for Julius Corporation. (Hint: To get the balance

sheet to balance, adjust stockholders’ equity.)

2 CHAPTER 1 Introduction to Financial Statements

Determine items included ina statement of cash flows,prepare the statement, andcomment.(SO 4, 5)

(a) Net income $2,300Ret. earnings $1,700Tot. assets $18,600

Comment on properaccounting treatment andprepare a corrected balancesheet.(SO 4, 5)

(a) Net increase $23,000

Tot. assets $69,000

Marginal check figures(in blue) provide a keynumber to let you knowyou’re on the right track.

1700T_web 1/16/06 6:09 PM Page 2 REVISED PAGES

Problems: Set C 3

Problems: Set C

P2-1C The following items are taken from the 2004 balance sheet of Starbucks Corpo-ration. (All dollars are in thousands.)

Intangible assets $ 95,750Common stock 996,078Property and equipment, net 1,551,416Accounts payable 199,346Other assets 85,561Long-term investments 306,926Accounts receivable 140,226Prepaid expenses and other current assets 134,997Short-term investments 353,881Retained earnings 1,478,140Cash and cash equivalents 299,128Long-term debt 3,618Accrued expenses and other current liabilities 425,536Unearned revenue—current 121,377Other long-term liabilities 166,453Inventories 422,663

InstructionsPrepare a classified balance sheet for Starbucks Corporation as of October 3, 2004.

P2-2C These items are taken from the financial statements of Graham Corporation for 2007.

Retained earnings (beginning of year) $26,000Utilities expense 3,000Equipment 38,000Accounts payable 2,400Cash 20,700Salaries payable 1,700Common stock 15,000Dividends 7,000Service revenue 77,000Prepaid insurance 1,950Repair expense 1,800Depreciation expense 5,300Accounts receivable 8,850Insurance expense 3,900Salaries expense 44,000Accumulated depreciation 12,400

InstructionsPrepare an income statement, a retained earnings statement, and a classified balancesheet as of December 31, 2007.

P2-3C You are provided with the following information for Barnette Enterprises, effec-tive as of its September 30, 2007, year-end.

Accounts payable $ 6,300Accounts receivable 2,500Building, net of accumulated depreciation 37,000Cash 2,600Common stock 10,000Cost of goods sold 22,000Current portion of long-term debt 5,000Depreciation expense 2,900Dividends paid during the year 1,800

Prepare a classified balancesheet.(SO 1)

Prepare financial statements.(SO 1, 3)

Tot. current assets $1,350,895Tot. assets $3,390,548

Net income $19,000Tot. assets $57,100

Prepare financial statements.(SO 1, 3)

1700T_web 1/16/06 6:09 PM Page 3 REVISED PAGES

4 CHAPTER 2 A Further Look at Financial Statements

Equipment, net of accumulated depreciation 14,000Income tax expense 2,550Income taxes payable 700Interest expense 3,400Inventories 4,800Land 16,000Long-term debt 31,000Prepaid expenses 1,350Retained earnings, beginning 21,300Revenues 56,800Selling expenses 2,700Short-term investments 3,000Wages expense 15,600Wages payable 1,100

Instructions(a) Prepare an income statement and a retained earnings statement for Barnette

Enterprises for the year ended September 30, 2007.(b) Prepare a classified balance sheet for Barnette Enterprises as of September 30, 2007.

P2-4C Comparative financial statement data for Batman Corporation and Spiderman Cor-poration, two competitors, appear below. All balance sheet data are as of December 31, 2007.

Net income $7,650Tot. current assets $14,250Tot. assets $81,250

Compute ratios; comment onrelative profitability, liquidity,and solvency.(SO 2, 4, 5) Batman Corporation Spiderman Corporation

2007 2007

Net sales $269,000 $504,000Cost of goods sold 130,000 248,000Operating expenses 80,000 132,000Interest expense 12,000 6,000Income tax expense 18,000 44,000

Current assets 146,000 182,000Plant assets (net) 105,000 86,000Current liabilities 44,000 106,000Long-term liabilities 87,000 41,000

Additional information:

Cash from operating activities $36,000 $43,000Capital expenditures $15,000 $28,000Dividends paid $8,000 $10,000Average number of shares

outstanding 30,000 40,000

Instructions(a) Comment on the relative profitability of the companies by computing the net income

and earnings per share for each company for 2007.(b) Comment on the relative liquidity of the companies by computing working capital

and the current ratios for each company for 2007.(c) Comment on the relative solvency of the companies by computing the debt to total

assets ratio and the free cash flow for each company for 2007.

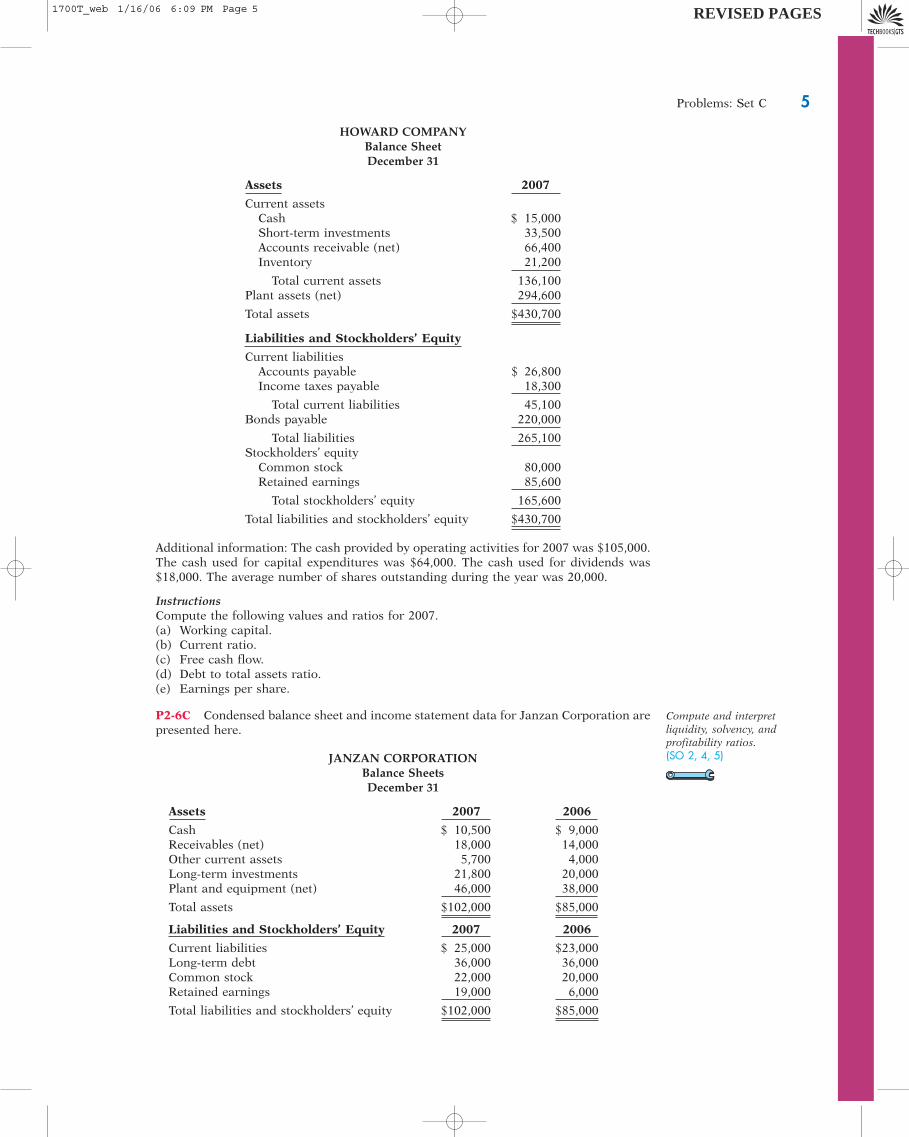

P2-5C Here and on the next page are financial statements of Howard Company.

HOWARD COMPANYIncome Statement

For the Year Ended December 31

2007

Net sales $558,200Cost of goods sold 254,500Selling and administrative expenses 178,000Interest expense 24,000Income tax expense 34,700

Net income $ 67,000

Compute liquidity, solvency,and profitability ratios.(SO 2, 4, 5)

1700T_web 1/31/06 8:30 AM Page 4 REVISED PAGES

Problems: Set C 5

Additional information: The cash provided by operating activities for 2007 was $105,000.The cash used for capital expenditures was $64,000. The cash used for dividends was$18,000. The average number of shares outstanding during the year was 20,000.

InstructionsCompute the following values and ratios for 2007.(a) Working capital.(b) Current ratio.(c) Free cash flow.(d) Debt to total assets ratio.(e) Earnings per share.

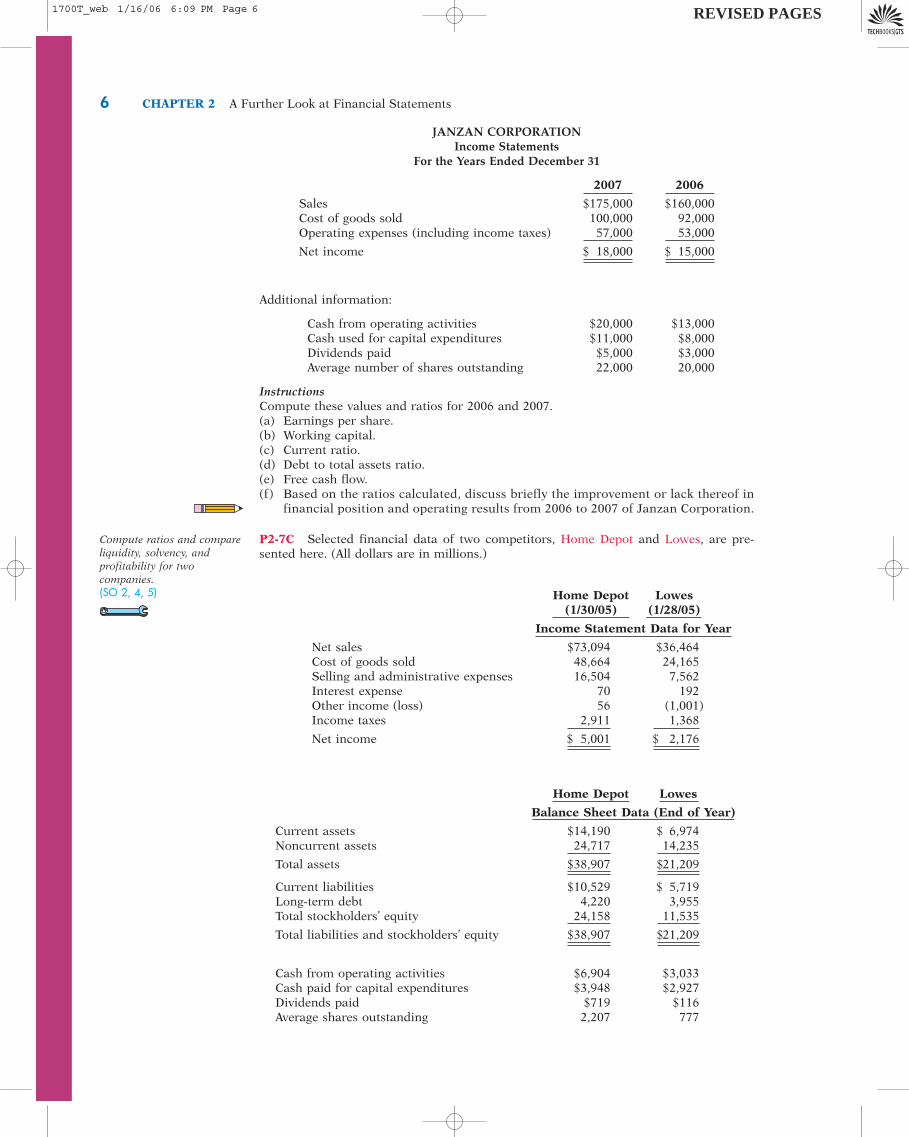

P2-6C Condensed balance sheet and income statement data for Janzan Corporation arepresented here.

HOWARD COMPANYBalance SheetDecember 31

Assets 2007

Current assetsCash $ 15,000Short-term investments 33,500Accounts receivable (net) 66,400Inventory 21,200

Total current assets 136,100Plant assets (net) 294,600

Total assets $430,700

Liabilities and Stockholders’ Equity

Current liabilitiesAccounts payable $ 26,800Income taxes payable 18,300

Total current liabilities 45,100Bonds payable 220,000

Total liabilities 265,100Stockholders’ equity

Common stock 80,000Retained earnings 85,600

Total stockholders’ equity 165,600

Total liabilities and stockholders’ equity $430,700

JANZAN CORPORATIONBalance SheetsDecember 31

Assets 2007 2006

Cash $ 10,500 $ 9,000Receivables (net) 18,000 14,000Other current assets 5,700 4,000Long-term investments 21,800 20,000Plant and equipment (net) 46,000 38,000

Total assets $102,000 $85,000

Compute and interpretliquidity, solvency, andprofitability ratios.(SO 2, 4, 5)

Liabilities and Stockholders’ Equity 2007 2006

Current liabilities $ 25,000 $23,000Long-term debt 36,000 36,000Common stock 22,000 20,000Retained earnings 19,000 6,000

Total liabilities and stockholders’ equity $102,000 $85,000

1700T_web 1/16/06 6:09 PM Page 5 REVISED PAGES

6 CHAPTER 2 A Further Look at Financial Statements

Additional information:

Cash from operating activities $20,000 $13,000Cash used for capital expenditures $11,000 $8,000Dividends paid $5,000 $3,000Average number of shares outstanding 22,000 20,000

InstructionsCompute these values and ratios for 2006 and 2007.(a) Earnings per share.(b) Working capital.(c) Current ratio.(d) Debt to total assets ratio.(e) Free cash flow.(f) Based on the ratios calculated, discuss briefly the improvement or lack thereof in

financial position and operating results from 2006 to 2007 of Janzan Corporation.

P2-7C Selected financial data of two competitors, Home Depot and Lowes, are pre-sented here. (All dollars are in millions.)

JANZAN CORPORATIONIncome Statements

For the Years Ended December 31

2007 2006

Sales $175,000 $160,000Cost of goods sold 100,000 92,000Operating expenses (including income taxes) 57,000 53,000

Net income $ 18,000 $ 15,000

Home Depot Lowes(1/30/05) (1/28/05)

Income Statement Data for Year

Net sales $73,094 $36,464Cost of goods sold 48,664 24,165Selling and administrative expenses 16,504 7,562Interest expense 70 192Other income (loss) 56 (1,001)Income taxes 2,911 1,368

Net income $ 5,001 $ 2,176

Home Depot Lowes

Balance Sheet Data (End of Year)

Current assets $14,190 $ 6,974Noncurrent assets 24,717 14,235

Total assets $38,907 $21,209

Current liabilities $10,529 $ 5,719Long-term debt 4,220 3,955Total stockholders’ equity 24,158 11,535

Total liabilities and stockholders’ equity $38,907 $21,209

Cash from operating activities $6,904 $3,033Cash paid for capital expenditures $3,948 $2,927Dividends paid $719 $116Average shares outstanding 2,207 777

Compute ratios and compareliquidity, solvency, andprofitability for twocompanies.(SO 2, 4, 5)

1700T_web 1/16/06 6:09 PM Page 6 REVISED PAGES

InstructionsFor each company, compute these values and ratios.(a) Working capital.(b) Current ratio.(c) Debt to total assets ratio.(d) Free cash flow.(e) Earnings per share.(f) Compare the liquidity, solvency, and profitability of the two companies.

P2-8C Meredith Norby recently completed an undergraduate degree in accounting.She has been approached by her older brother and five of his friends to assist them increating an investment club. None have taken any business courses, but all have beenworking for at least five years and feel they are ready to make their money work forthem. Some of the prospective members want to use the fund as part of their retire-ment assets. Others hope to use their portion of the annual earnings to supplementtheir current income.

The group has discussed various types of companies to invest in. Some members pre-fer to choose well-established companies that are traded on national stock exchanges.Others want to “get in on the ground floor” by investing in new businesses that may haveonly a few stockholders. One member has suggested buying into a company started byhis best friend from high school who claims that his business has tripled its earnings dur-ing its first two years of operations.

It has become clear to Meredith that this group of prospective investors has little orno understanding of financial reporting or generally accepted accounting principles(GAAP).

Instructions(a) Explain what is meant by financial reporting and GAAP.(b) Considering the variety of members’ goals and suggestions, indicate the type of fi-

nancial information that should be most useful in addressing investment choices.

Problems: Set C 7

Comment on the objectivesand qualitative characteris-tics of financial reporting.(SO 6, 7)

1700T_web 1/16/06 6:09 PM Page 7 REVISED PAGES

8 CHAPTER 3 The Accounting Information System

Analyze transactions andcompute net income.(SO 1)

(a) Cash $6,600Ret. earnings $600

Problems: Set C

P3-1C On April 1 Test Prep Inc. was established. These transactions were completedduring the month.

1. Stockholders invested $12,000 cash in the company in exchange for common stock.

2. Paid $1,400 cash for April office rent.

3. Purchased office equipment for $4,300 cash.

4. Purchased $500 of advertising in School News, on account.

5. Paid $700 cash for office supplies.

6. Earned $6,000 for services provided: Cash of $1,000 is received from customers, andthe balance of $5,000 is billed to customers on account.

7. Paid $100 cash dividends.

8. Paid School News amount due in transaction (4).

9. Paid employees’ salaries $3,400.

10. Received $4,000 in cash from customers who have previously been billed in trans-action (6).

Instructions(a) Prepare a tabular analysis of the transactions using these column headings: Cash,

Accounts Receivable, Supplies, Office Equipment, Accounts Payable, Common Stock, andRetained Earnings. Include margin explanations for any changes in Retained Earnings.

(b) From an analysis of the column Retained Earnings, compute the net income or netloss for April.

P3-2C Judy Takahashi started her own consulting firm, Takahashi Consulting Inc., onNovember 1, 2007. The following transactions occurred during the month of November.

Nov. 1 Stockholders invested $15,000 cash in the business in exchange forcommon stock.

2 Paid $1,000 for office rent for the month.3 Purchased $750 of supplies on account.5 Paid $400 to advertise in the Small Business Times.9 Received $800 cash for services provided.

12 Paid $100 cash dividend.15 Performed $4,400 of services on account.17 Paid $2,100 for employee salaries.20 Paid for the supplies purchased on account on November 3.23 Received a cash payment of $1,800 for services provided on account on

November 15.26 Borrowed $8,000 from the bank on a note payable.29 Purchased office equipment for $3,500 paying $200 in cash and the

balance on account.30 Paid $220 for utilities.

Instructions(a) Show the effects of the previous transactions on the accounting equation using the

following format. Assume the note payable is to be repaid within the year.

Analyze transactions andprepare financial statements.(SO 1)

GLS

Stockholders’Assets � Liabilities � Equity

Accounts Office Notes Accounts Common RetainedDate Cash �

Receivable� Supplies �

Equipment�

Payable�

Payable�

Stock�

Earnings

(a) Cash $20,830Ret. earnings $1,380

Include margin explanations for any changes in Retained Earnings.(b) Prepare an income statement for the month of November.(c) Prepare a classified balance sheet at November 30, 2007.

P3-3C Din Liu created a corporation providing legal services, Din Liu Inc., on March 1,2007. On March 31 the balance sheet showed: Cash $6,500; Accounts Receivable $2,000;

(b) Net income $1,480

GLS

1700T_web 1/16/06 6:09 PM Page 8 REVISED PAGES

Problems: Set C 9

Supplies $800; Office Equipment $7,000; Accounts Payable $4,700; Common Stock $8,000;and Retained Earnings $3,600. During April the following transactions occurred.

1. Collected $1,300 of accounts receivable due from customers.

2. Paid $3,200 cash for accounts payable due.

3. Earned revenue of $7,100 of which $4,000 is collected in cash and the balance is duein May.

4. Purchased additional office equipment for $1,000, paying $200 in cash and the bal-ance on account.

5. Paid salaries $2,700, rent for April $800, and advertising expenses $280.

6. Declared and paid a cash dividend of $400.

7. Received $3,500 from Metro Bank; the money was borrowed on a 4-month note payable.

8. Incurred utility expenses for the month on account $320.

Instructions(a) Prepare a tabular analysis of the April transactions beginning with March 31 balances.

The column heading should be: Cash � Accounts Receivable � Supplies � OfficeEquipment � Notes Payable � Accounts Payable � Common Stock � Retained Earn-ings. Include margin explanations for any changes in Retained Earnings.

(b) Prepare an income statement for April, a retained earnings statement for April, anda classified balance sheet at April 30.

P3-4C Skating By, Inc. was opened on May 1 by James Bea. These selected events andtransactions occurred during May.

May 1 Stockholders invested $80,000 cash in the business in exchange for com-mon stock of the corporation.

3 Purchased BoardWorld for $60,000 cash. The price consists of land$20,000, building $30,000, and equipment $10,000. (Record this in a sin-gle entry.)

5 Advertised the opening of the skate board park, paying advertisingexpenses of $500 cash.

6 Paid cash $6,000 for a 1-year insurance policy.10 Purchased equipment for $4,600 from T. Hawks Company, payable in

30 days.18 Received $1,500 in cash from customers for fees earned.19 Sold 150 coupon books for $40 each in cash. Each book contains five

coupons that enable the holder to use the park. (Hint: The revenue is notearned until the customers use the coupons.)

25 Declared and paid a $300 cash dividend.30 Paid salaries of $1,280.30 Paid T. Hawks in full for equipment purchased on May 10.31 Received $1,100 of fees in cash from customers for fees earned.

The company uses these accounts: Cash, Prepaid Insurance, Land, Buildings, Equipment,Accounts Payable, Unearned Revenue, Common Stock, Retained Earnings, Dividends,Revenue, Advertising Expense, and Salaries Expense.

InstructionsJournalize the May transactions, including explanations.

P3-5C Castle Architects incorporated as licensed architects on September 1, 2007. Duringthe first month of the operation of the business, these events and transactions occurred:

Sept. 1 Stockholders invested $22,000 cash in exchange for common stock of thecorporation.

1 Hired a secretary-receptionist at a salary of $410 per week, payable monthly.2 Paid office rent for the month $1,500.3 Purchased architectural supplies on account from Taliesin Company $1,150.

10 Completed blueprints on a carport and billed client $1,700 for services.11 Received $800 cash advance from M. Stewart to design a new home.20 Received $4,900 cash for services completed and delivered to R. Husch.30 Paid secretary-receptionist for the month $1,640.30 Paid $600 to Taliesin Company for accounts payable due.

Analyze transactions andprepare an income statement,retained earnings statement,and balance sheet.(SO 1)

(a) Cash $7,720Ret. earnings $6,200

(b) Net income $3,000

Journalize a series oftransactions.(SO 3, 5)

GLS

GLS

Journalize transactions, post,and prepare a trial balance.(SO 3, 5, 6, 7, 8)

GLS

1700T_web 1/16/06 6:09 PM Page 9 REVISED PAGES

10 CHAPTER 3 The Accounting Information System

The company uses these accounts: Cash, Accounts Receivable, Supplies, AccountsPayable, Unearned Revenue, Common Stock, Service Revenue, Salaries Expense, andRent Expense.

Instructions(a) Journalize the transactions, including explanations.(b) Post to the ledger T accounts.(c) Prepare a trial balance on September 30, 2007.

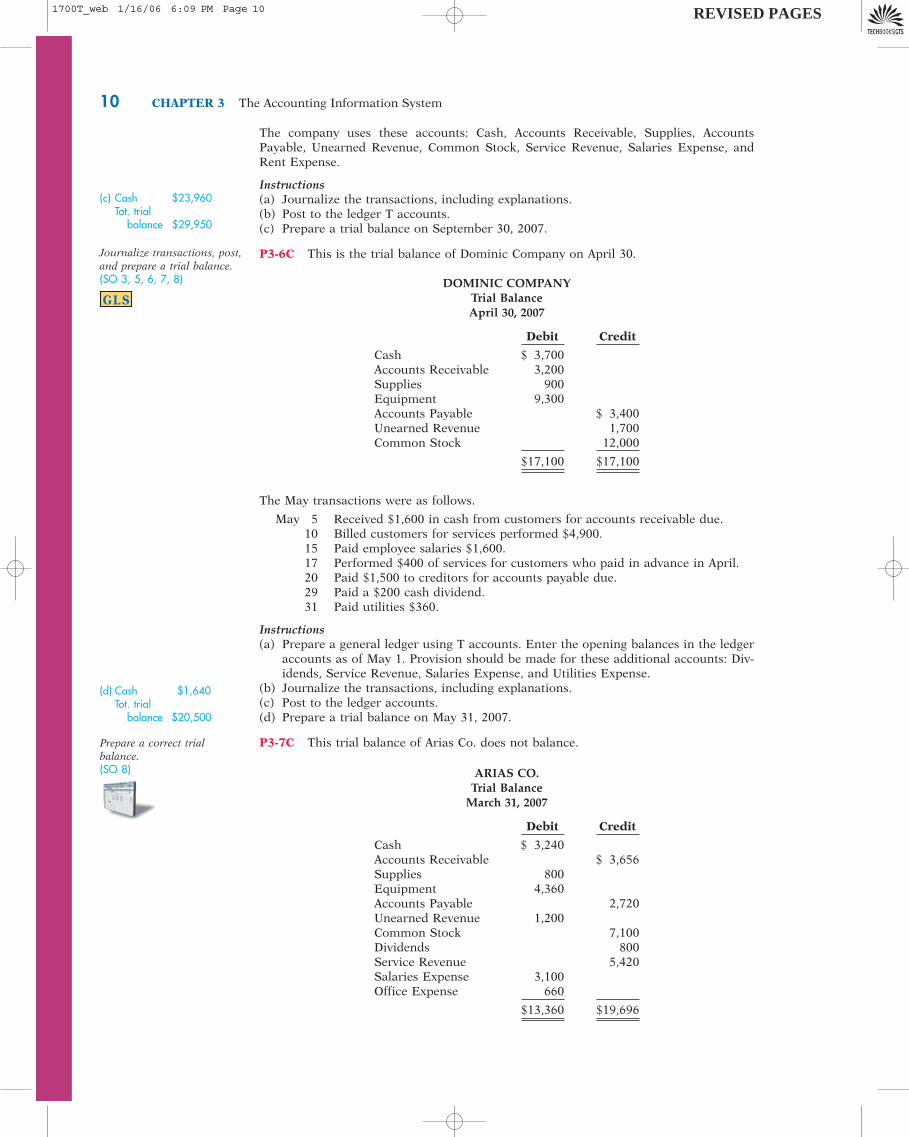

P3-6C This is the trial balance of Dominic Company on April 30.

(c) Cash $23,960Tot. trial

balance $29,950

Journalize transactions, post,and prepare a trial balance.(SO 3, 5, 6, 7, 8) DOMINIC COMPANY

Trial BalanceApril 30, 2007

Debit Credit

Cash $ 3,700Accounts Receivable 3,200Supplies 900Equipment 9,300Accounts Payable $ 3,400Unearned Revenue 1,700Common Stock 12,000

$17,100 $17,100

GLS

The May transactions were as follows.

May 5 Received $1,600 in cash from customers for accounts receivable due.10 Billed customers for services performed $4,900.15 Paid employee salaries $1,600.17 Performed $400 of services for customers who paid in advance in April.20 Paid $1,500 to creditors for accounts payable due.29 Paid a $200 cash dividend.31 Paid utilities $360.

Instructions(a) Prepare a general ledger using T accounts. Enter the opening balances in the ledger

accounts as of May 1. Provision should be made for these additional accounts: Div-idends, Service Revenue, Salaries Expense, and Utilities Expense.

(b) Journalize the transactions, including explanations.(c) Post to the ledger accounts.(d) Prepare a trial balance on May 31, 2007.

P3-7C This trial balance of Arias Co. does not balance.

ARIAS CO.Trial Balance

March 31, 2007

Debit Credit

Cash $ 3,240Accounts Receivable $ 3,656Supplies 800Equipment 4,360Accounts Payable 2,720Unearned Revenue 1,200Common Stock 7,100Dividends 800Service Revenue 5,420Salaries Expense 3,100Office Expense 660

$13,360 $19,696

(d) Cash $1,640Tot. trial

balance $20,500

Prepare a correct trialbalance.(SO 8)

1700T_web 1/16/06 6:09 PM Page 10 REVISED PAGES

Problems: Set C 11

Tot. trial balance $16,660

Journalize transactions, post,and prepare a trial balance.(SO 3, 5, 6, 7, 8)

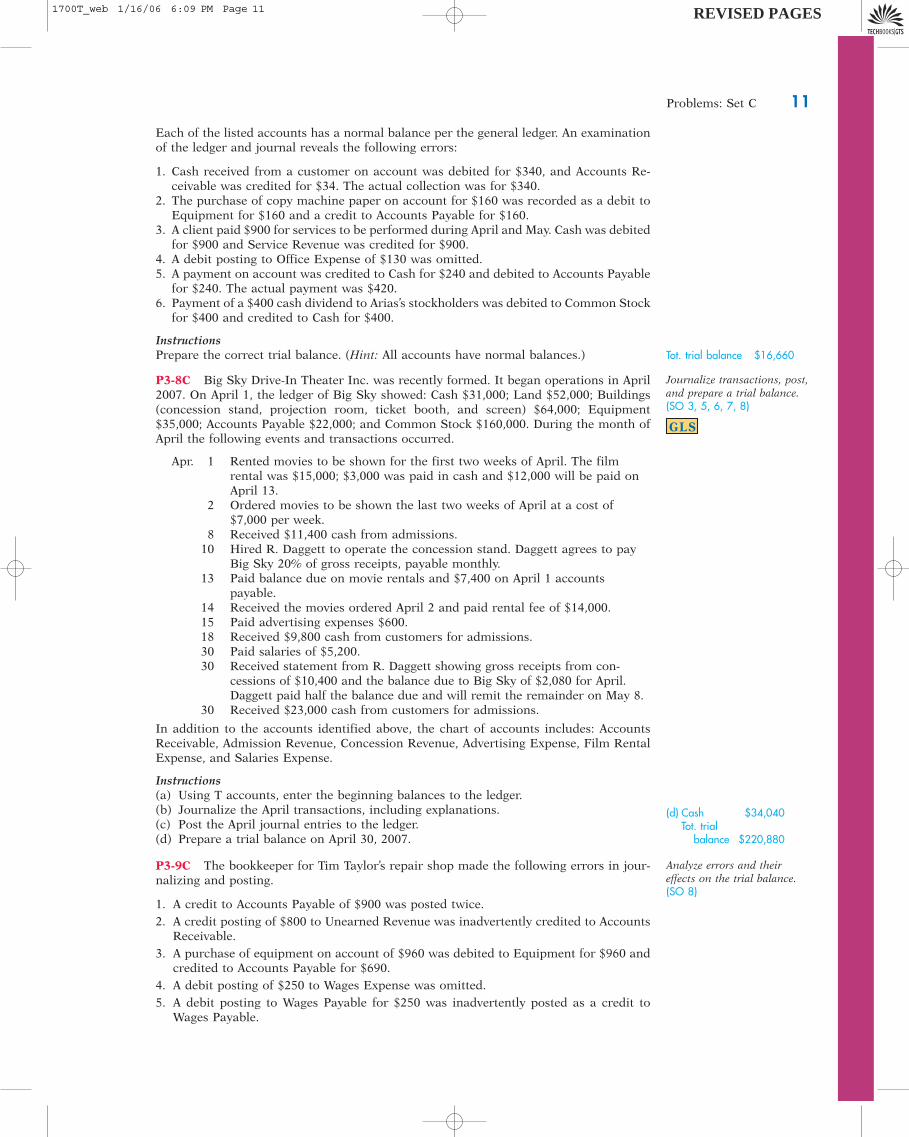

Each of the listed accounts has a normal balance per the general ledger. An examinationof the ledger and journal reveals the following errors:

1. Cash received from a customer on account was debited for $340, and Accounts Re-ceivable was credited for $34. The actual collection was for $340.

2. The purchase of copy machine paper on account for $160 was recorded as a debit toEquipment for $160 and a credit to Accounts Payable for $160.

3. A client paid $900 for services to be performed during April and May. Cash was debitedfor $900 and Service Revenue was credited for $900.

4. A debit posting to Office Expense of $130 was omitted.5. A payment on account was credited to Cash for $240 and debited to Accounts Payable

for $240. The actual payment was $420.6. Payment of a $400 cash dividend to Arias’s stockholders was debited to Common Stock

for $400 and credited to Cash for $400.

InstructionsPrepare the correct trial balance. (Hint: All accounts have normal balances.)

P3-8C Big Sky Drive-In Theater Inc. was recently formed. It began operations in April2007. On April 1, the ledger of Big Sky showed: Cash $31,000; Land $52,000; Buildings(concession stand, projection room, ticket booth, and screen) $64,000; Equipment$35,000; Accounts Payable $22,000; and Common Stock $160,000. During the month ofApril the following events and transactions occurred.

Apr. 1 Rented movies to be shown for the first two weeks of April. The filmrental was $15,000; $3,000 was paid in cash and $12,000 will be paid onApril 13.

2 Ordered movies to be shown the last two weeks of April at a cost of$7,000 per week.

8 Received $11,400 cash from admissions.10 Hired R. Daggett to operate the concession stand. Daggett agrees to pay

Big Sky 20% of gross receipts, payable monthly.13 Paid balance due on movie rentals and $7,400 on April 1 accounts

payable.14 Received the movies ordered April 2 and paid rental fee of $14,000.15 Paid advertising expenses $600.18 Received $9,800 cash from customers for admissions.30 Paid salaries of $5,200.30 Received statement from R. Daggett showing gross receipts from con-

cessions of $10,400 and the balance due to Big Sky of $2,080 for April.Daggett paid half the balance due and will remit the remainder on May 8.

30 Received $23,000 cash from customers for admissions.

In addition to the accounts identified above, the chart of accounts includes: AccountsReceivable, Admission Revenue, Concession Revenue, Advertising Expense, Film RentalExpense, and Salaries Expense.

Instructions(a) Using T accounts, enter the beginning balances to the ledger.(b) Journalize the April transactions, including explanations.(c) Post the April journal entries to the ledger.(d) Prepare a trial balance on April 30, 2007.

P3-9C The bookkeeper for Tim Taylor’s repair shop made the following errors in jour-nalizing and posting.

1. A credit to Accounts Payable of $900 was posted twice.

2. A credit posting of $800 to Unearned Revenue was inadvertently credited to AccountsReceivable.

3. A purchase of equipment on account of $960 was debited to Equipment for $960 andcredited to Accounts Payable for $690.

4. A debit posting of $250 to Wages Expense was omitted.

5. A debit posting to Wages Payable for $250 was inadvertently posted as a credit toWages Payable.

GLS

(d) Cash $34,040Tot. trial

balance $220,880

Analyze errors and theireffects on the trial balance.(SO 8)

1700T_web 1/16/06 6:09 PM Page 11 REVISED PAGES

12 CHAPTER 3 The Accounting Information System

6. A debit posting for $800 of Dividends was inadvertently posted to Wage Expenseinstead.

7. A debit posting to Cash and a credit posting to Service Revenue for $600 were inad-vertently posted twice.

8. A debit to Accounts Receivable of $400 was debited to Accounts Payable.

InstructionsFor each error, indicate (a) whether the trial balance will balance; (b) the amount of thedifference if the trial balance will not balance; and (c) the trial balance column that willhave the larger total. Consider each error separately. Use the following form, in whicherror 1 is given as an example.

(a) (b) (c)Error In Balance Difference Larger Column

1. No $900 Credit

1700T_web 1/16/06 6:09 PM Page 12 REVISED PAGES

Problems: Set C 13

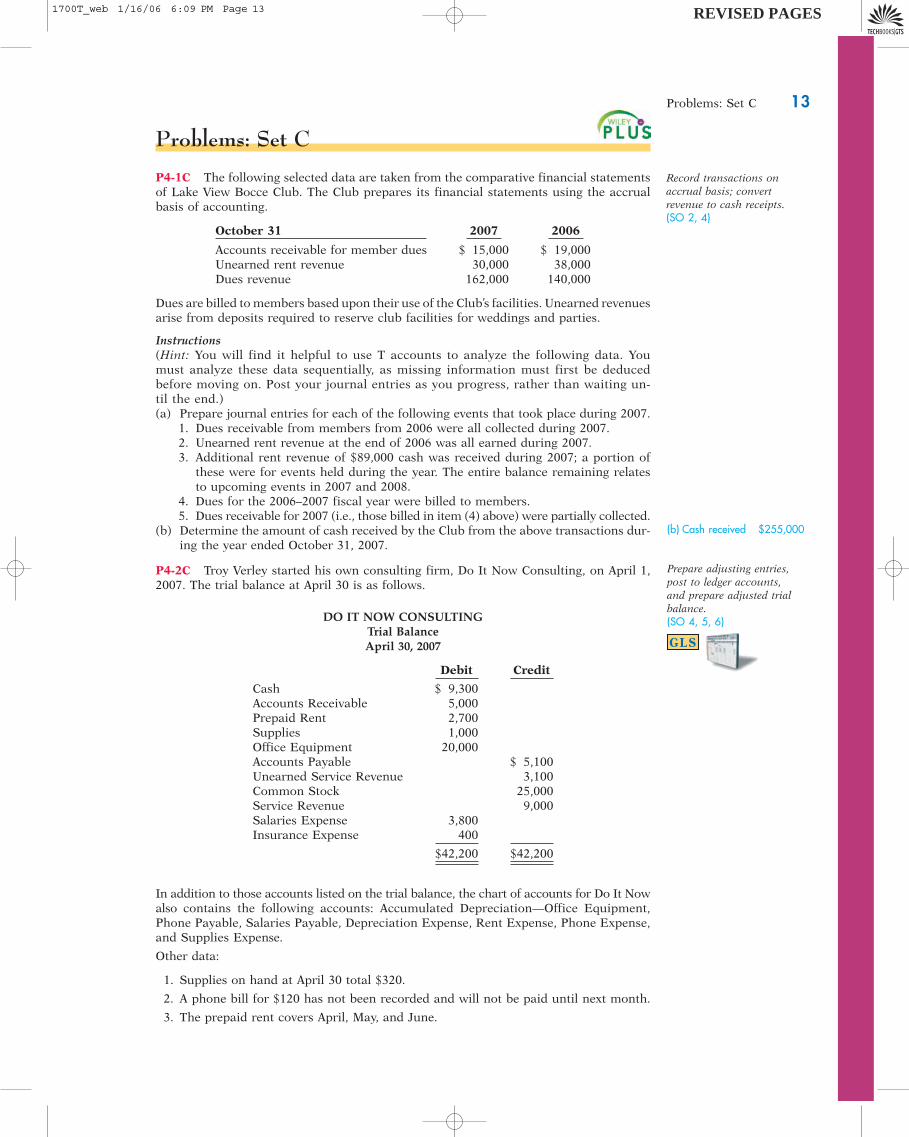

DO IT NOW CONSULTINGTrial BalanceApril 30, 2007

Debit Credit

Cash $ 9,300Accounts Receivable 5,000Prepaid Rent 2,700Supplies 1,000Office Equipment 20,000Accounts Payable $ 5,100Unearned Service Revenue 3,100Common Stock 25,000Service Revenue 9,000Salaries Expense 3,800Insurance Expense 400

$42,200 $42,200

Problems: Set C

P4-1C The following selected data are taken from the comparative financial statementsof Lake View Bocce Club. The Club prepares its financial statements using the accrualbasis of accounting.

October 31 2007 2006

Accounts receivable for member dues $ 15,000 $ 19,000Unearned rent revenue 30,000 38,000Dues revenue 162,000 140,000

Dues are billed to members based upon their use of the Club’s facilities. Unearned revenuesarise from deposits required to reserve club facilities for weddings and parties.

Instructions(Hint: You will find it helpful to use T accounts to analyze the following data. Youmust analyze these data sequentially, as missing information must first be deducedbefore moving on. Post your journal entries as you progress, rather than waiting un-til the end.)(a) Prepare journal entries for each of the following events that took place during 2007.

1. Dues receivable from members from 2006 were all collected during 2007.2. Unearned rent revenue at the end of 2006 was all earned during 2007.3. Additional rent revenue of $89,000 cash was received during 2007; a portion of

these were for events held during the year. The entire balance remaining relatesto upcoming events in 2007 and 2008.

4. Dues for the 2006–2007 fiscal year were billed to members.5. Dues receivable for 2007 (i.e., those billed in item (4) above) were partially collected.

(b) Determine the amount of cash received by the Club from the above transactions dur-ing the year ended October 31, 2007.

P4-2C Troy Verley started his own consulting firm, Do It Now Consulting, on April 1,2007. The trial balance at April 30 is as follows.

Record transactions onaccrual basis; convertrevenue to cash receipts.(SO 2, 4)

Prepare adjusting entries,post to ledger accounts,and prepare adjusted trialbalance.(SO 4, 5, 6)

(b) Cash received $255,000

GLS

In addition to those accounts listed on the trial balance, the chart of accounts for Do It Nowalso contains the following accounts: Accumulated Depreciation—Office Equipment,Phone Payable, Salaries Payable, Depreciation Expense, Rent Expense, Phone Expense,and Supplies Expense.

Other data:

1. Supplies on hand at April 30 total $320.

2. A phone bill for $120 has not been recorded and will not be paid until next month.

3. The prepaid rent covers April, May, and June.

1700T_web 1/16/06 6:09 PM Page 13 REVISED PAGES

14 CHAPTER 4 Accrual Accounting Concepts

4. $2,200 of unearned service revenue has been earned at the end of the month.

5. Salaries of $1,460 are accrued at April 30.

6. The office equipment has a 5-year life with salvage value of $2,000 and is beingdepreciated at $300 per month for 60 months.

7. Invoices representing $2,800 of services performed during the month have not beenrecorded as of April 30.

Instructions(a) Prepare the adjusting entries for the month of April.(b) Post the adjusting entries to the ledger accounts. Enter the totals from the trial bal-

ance as beginning account balances. Use T accounts.(c) Prepare an adjusted trial balance at April 30, 2007.

P4-3C The Welcome Inn opened for business on March 1, 2007. Here is its trial bal-ance before adjustment on March 31.

(c) Rent revenue $12,300Tot. trial

balance $147,005

Prepare adjusting entries,adjusted trial balance, andfinancial statements.(SO 4, 5, 6, 7)

(b) Service rev. $14,000(c) Tot. trial balance $46,880

GLS

(d) Net income $4,295

Prepare adjusting entries andfinancial statements; identifyaccounts to be closed.(SO 4, 5, 6, 7)

GLS

WELCOME INNTrial Balance

March 31, 2007

Debit Credit

Cash $ 2,700Prepaid Insurance 2,400Supplies 3,300Land 25,000Lodge 85,000Furniture 22,400Accounts Payable $ 9,200Unearned Rent Revenue 2,800Mortgage Payable 50,000Common Stock 72,000Rent Revenue 11,000Salaries Expense 3,000Utilities Expense 800Advertising Expense 400

$145,000 $145,000

Other data:

1. Insurance expires at the rate of $400 per month.

2. An inventory of supplies shows $1,900 of unused supplies on March 31.

3. Annual depreciation is $4,440 on the lodge and $3,600 on furniture.

4. The mortgage interest rate is 9%. (The mortgage was taken out on March 1.)

5. Unearned rent of $1,300 has been earned.

6. Salaries of $960 are accrued and unpaid at March 31.

Instructions(a) Journalize the adjusting entries on March 31.(b) Prepare a ledger using T accounts. Enter the trial balance amounts and post the

adjusting entries.(c) Prepare an adjusted trial balance on March 31.(d) Prepare an income statement and a retained earnings statement for the month of

March and a classified balance sheet at March 31.(e) Identify which accounts should be closed on March 31.

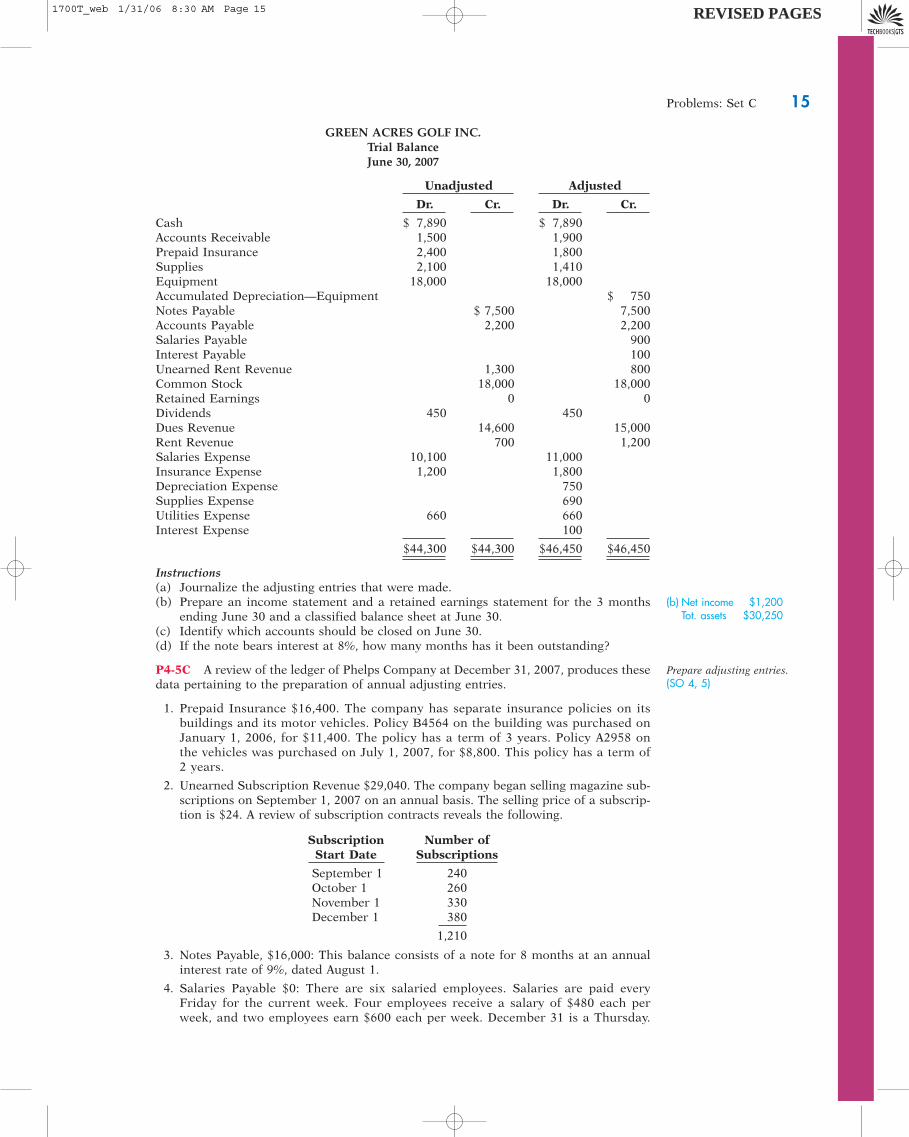

P4-4C Green Acres Golf Inc. was organized on April 1, 2007. Quarterly financial state-ments are prepared. The trial balance and adjusted trial balance on June 30 are shownon the next page.

1700T_web 1/31/06 2:10 PM Page 14 REVISED PAGES

Problems: Set C 15

GREEN ACRES GOLF INC.Trial BalanceJune 30, 2007

Unadjusted Adjusted

Dr. Cr. Dr. Cr.

Cash $ 7,890 $ 7,890Accounts Receivable 1,500 1,900Prepaid Insurance 2,400 1,800Supplies 2,100 1,410Equipment 18,000 18,000Accumulated Depreciation—Equipment $ 750Notes Payable $ 7,500 7,500Accounts Payable 2,200 2,200Salaries Payable 900Interest Payable 100Unearned Rent Revenue 1,300 800Common Stock 18,000 18,000Retained Earnings 0 0Dividends 450 450Dues Revenue 14,600 15,000Rent Revenue 700 1,200Salaries Expense 10,100 11,000Insurance Expense 1,200 1,800Depreciation Expense 750Supplies Expense 690Utilities Expense 660 660Interest Expense 100

$44,300 $44,300 $46,450 $46,450

Instructions(a) Journalize the adjusting entries that were made.(b) Prepare an income statement and a retained earnings statement for the 3 months

ending June 30 and a classified balance sheet at June 30.(c) Identify which accounts should be closed on June 30.(d) If the note bears interest at 8%, how many months has it been outstanding?

P4-5C A review of the ledger of Phelps Company at December 31, 2007, produces thesedata pertaining to the preparation of annual adjusting entries.

1. Prepaid Insurance $16,400. The company has separate insurance policies on itsbuildings and its motor vehicles. Policy B4564 on the building was purchased onJanuary 1, 2006, for $11,400. The policy has a term of 3 years. Policy A2958 onthe vehicles was purchased on July 1, 2007, for $8,800. This policy has a term of2 years.

2. Unearned Subscription Revenue $29,040. The company began selling magazine sub-scriptions on September 1, 2007 on an annual basis. The selling price of a subscrip-tion is $24. A review of subscription contracts reveals the following.

Subscription Number ofStart Date Subscriptions

September 1 240October 1 260November 1 330December 1 380

1,210

3. Notes Payable, $16,000: This balance consists of a note for 8 months at an annualinterest rate of 9%, dated August 1.

4. Salaries Payable $0: There are six salaried employees. Salaries are paid everyFriday for the current week. Four employees receive a salary of $480 each perweek, and two employees earn $600 each per week. December 31 is a Thursday.

(b) Net income $1,200Tot. assets $30,250

Prepare adjusting entries.(SO 4, 5)

1700T_web 1/31/06 8:30 AM Page 15 REVISED PAGES

16 CHAPTER 4 Accrual Accounting Concepts

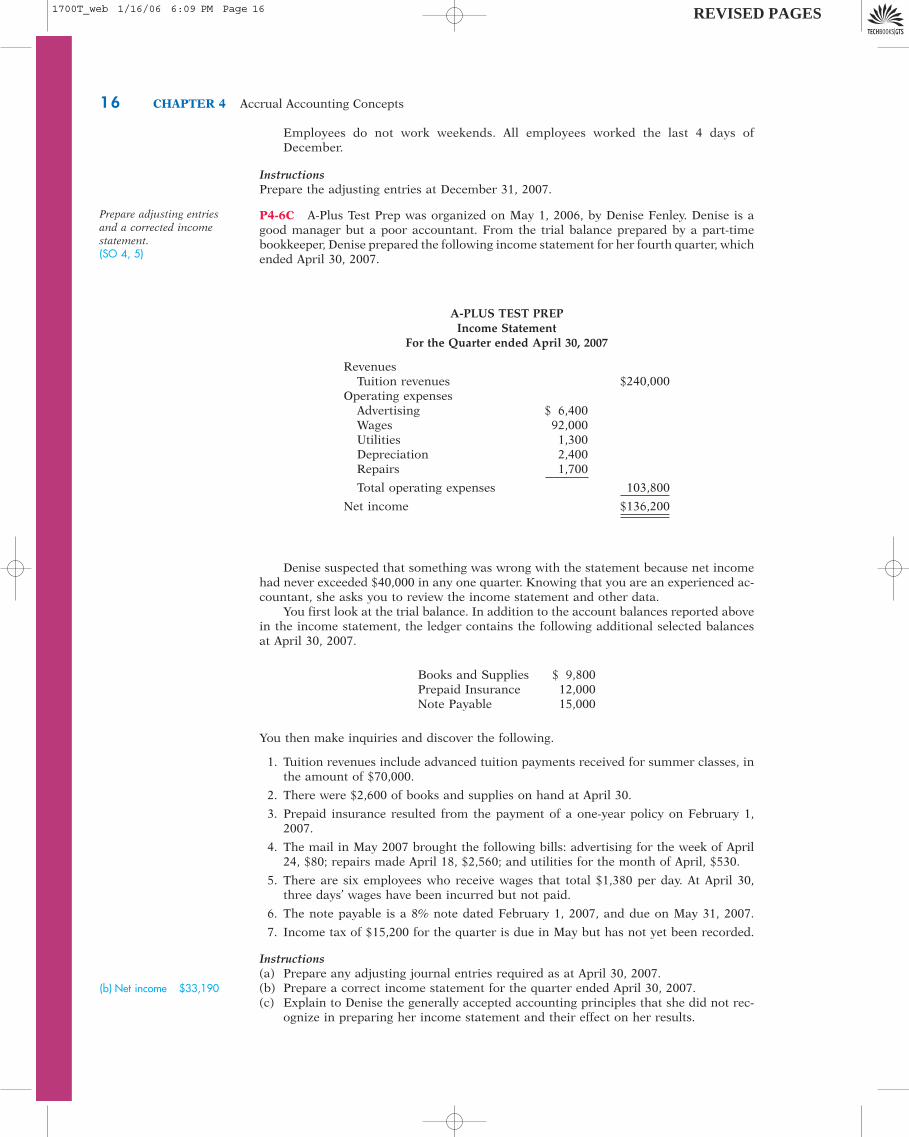

A-PLUS TEST PREPIncome Statement

For the Quarter ended April 30, 2007

RevenuesTuition revenues $240,000

Operating expensesAdvertising $ 6,400Wages 92,000Utilities 1,300Depreciation 2,400Repairs 1,700

Total operating expenses 103,800

Net income $136,200

Denise suspected that something was wrong with the statement because net incomehad never exceeded $40,000 in any one quarter. Knowing that you are an experienced ac-countant, she asks you to review the income statement and other data.

You first look at the trial balance. In addition to the account balances reported abovein the income statement, the ledger contains the following additional selected balancesat April 30, 2007.

Books and Supplies $ 9,800Prepaid Insurance 12,000Note Payable 15,000

You then make inquiries and discover the following.

1. Tuition revenues include advanced tuition payments received for summer classes, inthe amount of $70,000.

2. There were $2,600 of books and supplies on hand at April 30.

3. Prepaid insurance resulted from the payment of a one-year policy on February 1,2007.

4. The mail in May 2007 brought the following bills: advertising for the week of April24, $80; repairs made April 18, $2,560; and utilities for the month of April, $530.

5. There are six employees who receive wages that total $1,380 per day. At April 30,three days’ wages have been incurred but not paid.

6. The note payable is a 8% note dated February 1, 2007, and due on May 31, 2007.

7. Income tax of $15,200 for the quarter is due in May but has not yet been recorded.

Instructions(a) Prepare any adjusting journal entries required as at April 30, 2007.(b) Prepare a correct income statement for the quarter ended April 30, 2007.(c) Explain to Denise the generally accepted accounting principles that she did not rec-

ognize in preparing her income statement and their effect on her results.

Employees do not work weekends. All employees worked the last 4 days ofDecember.

InstructionsPrepare the adjusting entries at December 31, 2007.

P4-6C A-Plus Test Prep was organized on May 1, 2006, by Denise Fenley. Denise is agood manager but a poor accountant. From the trial balance prepared by a part-timebookkeeper, Denise prepared the following income statement for her fourth quarter, whichended April 30, 2007.

Prepare adjusting entries and a corrected incomestatement.(SO 4, 5)

(b) Net income $33,190

1700T_web 1/16/06 6:09 PM Page 16 REVISED PAGES

Problems: Set C 17

P4-7C On August 1, 2007, the following were the account balances of Bob and NormRepair Services.

Debits Credits

Cash $ 6,040 Accumulated Depreciation $ 600Accounts Receivable 2,910 Accounts Payable 2,300Supplies 1,030 Unearned Service Revenue 1,260Store Equipment 10,000 Salaries Payable 1,420

Common Stock 10,000Retained Earnings 4,400

$19,980 $19,980

During August the following summary transactions were completed.

Aug. 5 Received $1,200 cash from customers in payment of account.10 Paid $3,120 for salaries due employees, of which $1,700 is for August and

$1,420 is for July salaries payable.12 Received $2,800 cash for services performed in August.15 Purchased store equipment on account $2,000.17 Purchased supplies on account $860.20 Paid creditors $2,500 of accounts payable due.22 Paid August rent $380.25 Paid salaries $2,900.27 Performed services on account and billed customers for services provided

$3,130.29 Received $780 from customers for services to be provided in the future.

Adjustment data:

1. Supplies on hand are valued at $960.

2. Accrued salaries payable are $1,540.

3. Depreciation for the month is $320.

4. Unearned service revenue of $800 is earned.

Instructions(a) Enter the August 1 balances in the ledger accounts. (Use T accounts.)(b) Journalize the August transactions.(c) Post to the ledger accounts. Use Service Revenue, Depreciation Expense, Supplies

Expense, Salaries Expense, and Rent Expense.(d) Prepare a trial balance at August 31.(e) Journalize and post adjusting entries.(f) Prepare an adjusted trial balance.(g) Prepare an income statement and a retained earnings statement for August and a

classified balance sheet at August 31.

P4-8C Laura Young opened Magic Carpet Cleaners Inc. on January 1, 2007. DuringJanuary the following transactions were completed.

Jan. 1 Issued 12,000 shares of common stock for $18,000 cash.1 Purchased used truck for $12,000, paying $4,000 cash and the balance on

account.3 Purchased cleaning supplies for $940 on account.5 Paid $7,200 cash on 1-year insurance policy effective January 1.

12 Billed customers $4,100 for cleaning services.18 Paid $600 cash on amount owed on truck and $300 on amount owed on

cleaning supplies.20 Paid $2,600 cash for employee salaries.21 Collected $2,300 cash from customers billed on January 12.25 Billed customers $2,850 for cleaning services.31 Paid $450 for gas and oil used in the truck during month.31 Declared and paid $600 cash dividend.

The chart of accounts for Magic Carpet Cleaners contains the following accounts: Cash,Accounts Receivable, Cleaning Supplies, Prepaid Insurance, Equipment, Accumulated

GLS

Journalize transactions andfollow through accountingcycle to preparation offinancial statements.(SO 4, 5, 6)

Complete all steps inaccounting cycle.(SO 4, 5, 6, 7, 8)

(f) Cash $1,920Tot. trial balance $27,490

(g) Net loss $1,040

GLS

1700T_web 1/16/06 6:09 PM Page 17 REVISED PAGES

18 CHAPTER 4 Accrual Accounting Concepts

Depreciation—Equipment, Accounts Payable, Salaries Payable, Common Stock, RetainedEarnings, Dividends, Income Summary, Service Revenue, Gas & Oil Expense, CleaningSupplies Expense, Depreciation Expense, Insurance Expense, Salaries Expense.

Instructions(a) Journalize the January transactions.(b) Post to the ledger accounts. (Use T accounts.)(c) Prepare a trial balance at January 31.(d) Journalize the following adjustments.

(1) Services provided but unbilled and uncollected at January 31 were $2,340.(2) Depreciation on the truck for the month was $320.(3) One-twelfth of the insurance expired.(4) An inventory count shows $210 of cleaning supplies on hand at January 31.(5) Accrued but unpaid employee salaries were $760.

(e) Post adjusting entries to the T accounts.(f ) Prepare an adjusted trial balance.(g) Prepare the income statement and a retained earnings statement for January and a

classified balance sheet at January 31.(h) Journalize and post closing entries and complete the closing process.(i) Prepare a post-closing trial balance at January 31.

(f) Cash $4,550(g) Tot. assets $30,030

1700T_web 1/16/06 6:09 PM Page 18 REVISED PAGES

Problems: Set C 19

Problems: Set C

P5-1C Franklin Craft Store completed the following merchandising transactions in themonth of October. At the beginning of October, Franklin’s ledger showed Cash of $8,000and Common Stock of $8,000.

Oct. 1 Purchased merchandise on account from Michael’s Wholesale Supply for$4,800, terms 1/10, n/30.

2 Sold merchandise on account for $3,900, terms 2/10, n/30. The cost ofthe merchandise sold was $2,400.

5 Received credit from Michael’s Wholesale Supply for merchandisereturned $600.

9 Received collections in full, less discounts, from customers billed onsales of $3,900 on October 2.

10 Paid Michael’s Wholesale Supply in full, less discount.11 Purchased supplies on account for $750.12 Purchased merchandise for cash $2,100.15 Received $200 refund for return of poor-quality merchandise from

supplier on cash purchase.17 Purchased merchandise on account from Handiwork Distributors for

$2,500, terms 2/10, n/30.19 Paid freight on October 17 purchase $310.24 Sold merchandise for cash $6,900. The cost of the merchandise sold

was $4,510.25 Purchased merchandise on account from Hobbytown Inc. for $1,000,

terms 3/10, n/30.27 Paid Handiwork Distributors in full, less discount.29 Made refunds to cash customers for returned merchandise $190. The

returned merchandise had cost $134.31 Sold merchandise on account for $1,460, terms 1/10, n/30. The cost of

the merchandise sold was $950.

Franklin Craft’s chart of accounts includes Cash, Accounts Receivable, MerchandiseInventory, Supplies, Accounts Payable, Common Stock, Sales, Sales Returns and Allowances,Sales Discounts, and Cost of Goods Sold.

Instructions(a) Journalize the transactions using a perpetual inventory system.(b) Post the transactions to T accounts. Be sure to enter the beginning cash and com-

mon stock balances.(c) Prepare an income statement through gross profit for the month of October 2007.(d) Calculate the profit margin ratio and the gross profit rate. (Assume operating expenses

were $2,100.)

P5-2C Crowning Glory Warehouse distributes commercial hair care products in one-gallon bottles to hair salons and extends credit terms of 3/10, n/30 to all of its customers.During the month of April the following merchandising transactions occurred.

Apr. 1 Purchased 190 bottles on account for $6 each (including freight) fromHealthy Hair, terms 2/10, n/30.

3 Sold 40 bottles on account to the Curl Up and Dye salon for $10 each.6 Received $90 credit for 15 bottles returned to Healthy Hair.9 Paid Healthy Hair in full.

12 Received payment in full from the Curl Up and Dye salon.13 Sold 25 bottles on account to Hairport Salon for $10 each.20 Purchased 200 bottles on account for $6 each from Golden Tresses,

terms 1/15, n/30.24 Received payment in full from Hairport Salon.26 Paid Golden Tresses in full.28 Sold 160 bottles on account to Cheaper Cuts salons for $10 each.30 Granted Cheaper Cuts $120 credit for 12 bottles returned costing $72.

(c) Gross profit $4,266

Journalize purchase andsale transactions under aperpetual inventory system.(SO 2, 3)

Journalize, post, preparepartial income statement,and calculate ratios.(SO 2, 3, 4, 6)

GLS

1700T_web 1/17/06 9:17 PM Page 19

20 CHAPTER 5 Merchandising Operations and the Multiple-Step Income Statement

InstructionsJournalize the transactions for the month of April for Crowning Glory Warehouse, usinga perpetual inventory system. Assume the cost of each bottle sold was $6.

P5-3C At the beginning of the current season on November 1, the ledger of LakesideIce House showed Cash $3,300; Merchandise Inventory $4,700; and Common Stock$8,000. The following transactions were completed during November 2007.

Nov. 5 Purchased hockey sticks and pucks on account from Gillmore Co. $1,600,terms 2/10, n/60.

7 Paid freight on Gillmore purchase $90.9 Received credit from Gillmore Co. for merchandise returned $350.

10 Sold merchandise on account for $1,100, terms n/30. The merchandisesold had a cost of $760.

12 Purchased gloves, socks, and other accessories on account from OrrSportswear $945, terms 1/10, n/30.

14 Paid Gillmore Co. in full.17 Received credit from Orr Sportswear for merchandise returned $45.20 Made sales on account for $1,330, terms n/30. The cost of the merchan-

dise sold was $950.21 Paid Orr Sportswear in full.27 Granted an allowance to customers for clothing that did not fit properly

$110.30 Received payments on account for $1,900.

The chart of accounts for the ice house includes Cash, Accounts Receivable, Merchan-dise Inventory, Accounts Payable, Common Stock, Sales, Sales Returns and Allowances,and Cost of Goods Sold.

Instructions(a) Journalize the November transactions using a perpetual inventory system.(b) Using T accounts, enter the beginning balances in the ledger accounts and post the

November transactions.(c) Prepare a trial balance on November 30, 2007.(d) Prepare an income statement through gross profit.

P5-4C Tobin’s China and Collectibles is located in midtown Centralia. During the pastseveral years, net income has been declining because suburban shopping centers havebeen attracting business away from city areas. At the end of the company’s fiscal year onSeptember 30, 2007, these accounts appeared in its adjusted trial balance.

Accounts Payable $ 22,800Accounts Receivable 19,530Accumulated Depreciation—Building 120,000Accumulated Depreciation—Store Equipment 21,000Advertising Expense 6,000Building 200,000Cash 7,800Common Stock 28,000Cost of Goods Sold 520,000Delivery Expense 5,800Depreciation Expense—Building 8,000Depreciation Expense—Store Equipment 4,200Dividends 15,000Gain on Sale of Investment 2,300Insurance Expense 10,300Interest Expense 5,600Merchandise Inventory 31,400Notes Payable 52,000Prepaid Insurance 2,570Property Tax Expense 7,600Property Taxes Payable 7,600Retained Earnings 18,100Salaries Expense 194,700

(c) Tot. trialbalance $10,430

(d) Gross profit $610

Prepare financial statementsand calculate profitabilityratios.(SO 4, 6)

Journalize, post, and preparetrial balance and partialincome statement.(SO 2, 3, 4)

GLS

1700T_web 1/16/06 6:09 PM Page 20 REVISED PAGES

Problems: Set C 21

Sales 886,000Sales Commissions Expense 18,000Sales Commissions Payable 2,200Sales Returns and Allowances 26,000Store Equipment 64,000Utilities Expense 13,500

Additional data: Notes payable are due in 2013.

Instructions(a) Prepare a multiple-step income statement; a retained earnings statement, and a clas-

sified balance sheet.(b) Calculate the profit margin ratio and the gross profit rate.(c) The vice-president of marketing and the director of human resources have devel-

oped a proposal whereby the company would compensate the sales force on astrictly commission basis using 30% of net sales. Given the increased incentive,they expect net sales to increase by 25%. As a result, they estimate that gross profitwill increase by $85,000 and operating expenses by $109,800. Compute the ex-pected new net income. (Hint: You do not need to prepare an income statement).Then compute the revised profit margin ratio and gross profit rate. Comment onthe effect that this plan would have on net income and on the ratios, and evaluatethe merit of this proposal.

P5-5C An inexperienced accountant prepared this condensed income statement forXiong Company, a retail firm that has been in business for a number of years.

Prepare a correct multiple-step income statement.(SO 4)

Net income $145,000

Journalize, post, and prepareadjusted trial balance andfinancial statements.(SO 4)

XIONG COMPANYIncome Statement

For the Year Ended December 31, 2007

RevenuesNet sales $952,000Other revenues 17,000

969,000Cost of goods sold 548,000

Gross profit 421,000Operating expenses

Selling expenses 161,000Administrative expenses 104,000

265,000

Net earnings $156,000

As an experienced, knowledgeable accountant, you review the statement and determinethe following facts.1. Net sales consist of sales $972,000, less delivery expense on merchandise sold $20,000.2. Other revenues consist of sales discounts $12,000 and interest revenue $5,000.3. Selling expenses consist of salespersons’ salaries $88,000; depreciation on store equip-

ment $4,000; sales returns and allowances $46,000; advertising $12,000; and sales com-missions $11,000.

4. Administrative expenses consist of office salaries $54,000; dividends $14,000; utilities$13,000; interest expense $3,000; and rent expense $20,000, which includes prepay-ments totaling $2,000 for the first month of 2008. The utilities represent utilities paid.At December 31, utility expense of $3,000 has been incurred but not paid.

InstructionsPrepare a correct detailed multiple-step income statement.

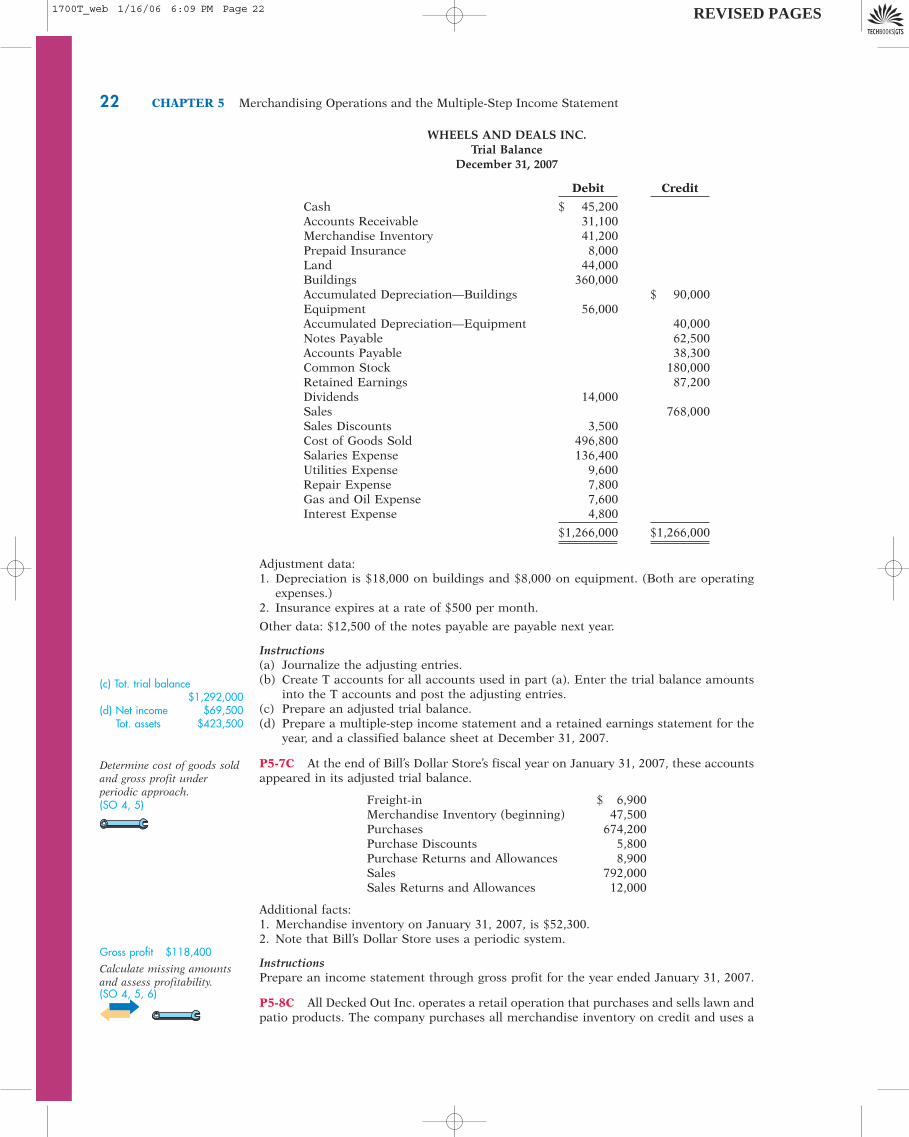

P5-6C The trial balance of Wheels and Deals Inc. contained the accounts shown on thefollowing page as of December 31, the end of the company’s fiscal year.

(a) Net income $68,600Tot. assets $184,300

1700T_web 1/31/06 8:30 AM Page 21 REVISED PAGES

22 CHAPTER 5 Merchandising Operations and the Multiple-Step Income Statement

Adjustment data:1. Depreciation is $18,000 on buildings and $8,000 on equipment. (Both are operating

expenses.)2. Insurance expires at a rate of $500 per month.

Other data: $12,500 of the notes payable are payable next year.

Instructions(a) Journalize the adjusting entries.(b) Create T accounts for all accounts used in part (a). Enter the trial balance amounts

into the T accounts and post the adjusting entries.(c) Prepare an adjusted trial balance.(d) Prepare a multiple-step income statement and a retained earnings statement for the

year, and a classified balance sheet at December 31, 2007.

P5-7C At the end of Bill’s Dollar Store’s fiscal year on January 31, 2007, these accountsappeared in its adjusted trial balance.

Freight-in $ 6,900Merchandise Inventory (beginning) 47,500Purchases 674,200Purchase Discounts 5,800Purchase Returns and Allowances 8,900Sales 792,000Sales Returns and Allowances 12,000

Additional facts:1. Merchandise inventory on January 31, 2007, is $52,300.2. Note that Bill’s Dollar Store uses a periodic system.

InstructionsPrepare an income statement through gross profit for the year ended January 31, 2007.

P5-8C All Decked Out Inc. operates a retail operation that purchases and sells lawn andpatio products. The company purchases all merchandise inventory on credit and uses a

WHEELS AND DEALS INC.Trial Balance

December 31, 2007

Debit Credit

Cash $ 45,200Accounts Receivable 31,100Merchandise Inventory 41,200Prepaid Insurance 8,000Land 44,000Buildings 360,000Accumulated Depreciation—Buildings $ 90,000Equipment 56,000Accumulated Depreciation—Equipment 40,000Notes Payable 62,500Accounts Payable 38,300Common Stock 180,000Retained Earnings 87,200Dividends 14,000Sales 768,000Sales Discounts 3,500Cost of Goods Sold 496,800Salaries Expense 136,400Utilities Expense 9,600Repair Expense 7,800Gas and Oil Expense 7,600Interest Expense 4,800

$1,266,000 $1,266,000

(c) Tot. trial balance$1,292,000

(d) Net income $69,500Tot. assets $423,500

Determine cost of goods soldand gross profit underperiodic approach.(SO 4, 5)

Gross profit $118,400Calculate missing amountsand assess profitability.(SO 4, 5, 6)

1700T_web 1/16/06 6:09 PM Page 22 REVISED PAGES

Problems: Set C 23

perpetual inventory system. The accounts payable account is used for recording inven-tory purchases only; all other current liabilities are accrued in separate accounts. You areprovided with the following selected information for the fiscal years 2005 through 2008,inclusive.

Instructions(a) Calculate cost of goods sold for each of the 2006, 2007, and 2008 fiscal years.(b) Calculate the gross profit for each of the 2006, 2007, and 2008 fiscal years.(c) Calculate the ending balance of accounts payable for each of the 2006, 2007, and

2008 fiscal years. The ending balance of accounts payable for 2005 was $19,000.(d) The vice-presidents of sales, marketing, production, and finance are discussing the

company’s results with the CEO. They note that sales declined over the 3-year fiscalperiod, 2006-2008. Does that mean that profitability necessarily also declined?Explain, computing the gross profit rate for each fiscal year to help support youranswer.

*P5-9C At the beginning of the current season on November 1, the ledger of LakesideIce House showed Cash $3,300, Merchandise Inventory $4,700, and Common Stock$8,000. These transactions occured during November 2007.

Nov. 5 Purchased hockey sticks and pucks on account from Gillmore Co. $1,600,terms 2/10, n/60.

7 Paid freight on Gillmore Co. purchases $90.9 Received credit from Gillmore Co. for merchandise returned $350.

10 Sold merchandise on account for $1,100, terms n/30.12 Purchased gloves, socks, and other accessories on account from Orr

Sportswear $945, terms 1/10, n/30.14 Paid Gillmore Co. in full.17 Received credit from Orr Sportswear for merchandise returned $45.20 Made sales on account for $1,330, terms n/30.21 Paid Orr Sportswear in full.27 Granted credit to customers for clothing that did not fit properly $110.30 Received payments on account for $1,900.

The chart of accounts for the ice house includes Cash, Accounts Receivable, Merchan-dise Inventory, Accounts Payable, Common Stock, Sales, Sales Returns and Allowances,Purchases, Purchase Returns and Allowances, Purchase Discounts, and Freight-in.

Instructions(a) Journalize the November transactions using a periodic inventory system.(b) Using T accounts, enter the beginning balances in the ledger accounts and post the

November transactions.(c) Prepare a trial balance on November 30, 2007.(d) Prepare an income statement through Gross Profit, assuming merchandise inventory

on hand at November 30 is $5,196.

Journalize, post, and preparetrial balance and partialincome statement usingperiodic approach.(SO 5, 7)

(c) Tot. trialbalance $10,859Gross profit $610

GLS

2005 2006 2007 2008

Inventory (ending) $18,420 $ 14,300 $ 15,400 $ 12,680Sales 292,000 295,000 284,000Purchases of merchandise

inventory on account 174,000 178,100 162,000Cash payments to suppliers 171,000 183,000 167,000

(a) 2007 cost of goods sold $177,000

2007 Ending acct. payable $17,100

1700T_web 1/16/06 6:09 PM Page 23 REVISED PAGES

24 CHAPTER 6 Reporting and Analyzing Inventory

Problems: Set CP6-1C Farrell Company is trying to determine the value of its ending inventory as ofMarch 31, 2007, the company’s year-end. The following transactions occurred, and the ac-countant asked your help in determining whether they should be recorded or not.(a) On March 30, Farrell shipped to a customer goods costing $800. The goods were

shipped FOB destination, and the receiving report indicates that the customer re-ceived the goods on April 1.

(b) On March 28, Supplier Inc. shipped goods to Farrell FOB shipping point. The invoiceprice was $400 plus $20 for freight. The receiving report indicates that the goodswere received by Farrell on April 2.

(c) Farrell had $750 of consigned goods from Joyce Inc.(d) Farrell had $380 of inventory at Zwingle Variety, on consignment from Farrell.(e) On March 29, Farrell ordered goods costing $640. The goods were shipped FOB des-

tination on March 31. Farrell received the goods on April 3.(f ) A customer returned goods to Farrell on March 31. Upon inspection, the goods were

found to be undamaged and were accepted as returned goods. These goods originallycost $400 and Farrell sold them for $640.

InstructionsFor each of the above transactions, specify whether the item in question should be includedin ending inventory, and if so, at what amount. For each item that is not included in endinginventory, indicate who owns it and what account, if any, it should have been recorded in.

P6-2C Timeless Distribution markets classic children’s books. At the beginning of June,Timeless had in beginning inventory 1,200 books with a unit cost of $3. During June,Timeless made the following purchases of books.

Determine cost of goods soldand ending inventory usingFIFO, LIFO, and averagecost, with analysis.(SO 2, 3)

Determine items andamounts to be recorded ininventory.(SO 1)

Cost of goods sold:FIFO $47,100LIFO $56,500Average $51,578

June 3 3,000 @ $4 June 29 4,000 @ $6June 18 7,800 @ $5

During June, 10,500 books were sold. Timeless uses a periodic inventory system.

Instructions(a) Determine the cost of goods available for sale.(b) Determine (1) the ending inventory and (2) the cost of goods sold under each of the

assumed cost flow methods (FIFO, LIFO, and average cost). Prove the accuracy ofthe cost of goods sold under the FIFO and LIFO methods. (Note: For average cost,round cost per unit to three decimal places.)

(c) Which cost flow method results in (1) the highest inventory amount for the balancesheet and (2) the highest cost of goods sold for the income statement?

P6-3C Byron Company Inc. had a beginning inventory of 200 units of Product ERV ata cost of $6 per unit. During the year, purchases were:

Jan. 24 800 units at $7 Aug. 19 600 units at $ 9Apr. 12 400 units at $8 Nov. 30 300 units at $10

Byron Company uses a periodic inventory system. Sales totalled 1,900 units.

Instructions(a) Determine the cost of goods available for sale.(b) Determine the ending inventory and the cost of goods sold under each of the assumed

cost flow methods (FIFO, LIFO, and average cost). Prove the accuracy of the cost ofgoods sold under the FIFO and LIFO methods.

(c) Which cost flow method results in the lowest inventory amount for the balance sheet?The lowest cost of goods sold for the income statement?

Cost of goods sold:FIFO $14,500LIFO $15,800Average $15,200

Determine cost of goods soldand ending inventory usingFIFO, LIFO, and averagecost in a periodic inventorysystem, and assess financialstatement effect.(SO 2, 3)

1700T_web 1/16/06 6:09 PM Page 24 REVISED PAGES

Problems: Set C 25

Inventory, January 1 (4,000 units) $ 16,000Cost of 105,000 units purchased 470,500Selling price of 100,000 units sold 870,000Operating expenses 185,000

Units purchased consisted of 35,000 units at $4.20 on March 20; 65,000 units at $4.60 onJuly 24, and 5,000 units at $4.90 on December 12. Income taxes are 30%.

Instructions(a) Prepare comparative condensed income statements for 2007 under FIFO and LIFO.

(Show computations of ending inventory.)(b) Answer the following questions for management in the form of a business letter.

(1) Which inventory cost flow method produces the most meaningful inventoryamount for the balance sheet? Why?

(2) Which inventory cost flow method produces the most meaningful net income? Why?(3) Which inventory cost flow method is most likely to approximate the actual phys-

ical flow of the goods? Why?(4) How much more cash will be available under LIFO than under FIFO? Why?(5) How much of the gross profit under FIFO is illusionary in comparison with the

gross profit under LIFO?

P6-5C You have the following information for Alsteen Inc. for the month ended May31, 2007. Alsteen uses a periodic method for inventory.

Unit Cost orDate Description Units Selling Price

May 1 Beginning inventory 40 $20May 6 Purchase 110 23May 7 Sale 90 32May 15 Purchase 70 24May 18 Sale 40 37May 24 Purchase 60 26May 30 Sale 80 38

Instructions(a) Calculate (i) ending inventory, (ii) cost of goods sold, (iii) gross profit, and (iv) gross

profit rate under each of the following methods.(1) LIFO.(2) FIFO.(3) Average cost. (Round cost per unit to three decimal places.)

(b) Compare results for the three cost flow assumptions.

P6-6C You have the following information for Tempus Watches. Tempus uses theperiodic method of accounting for its inventory transactions. Tempus carries only onebrand of hand-crafted jeweled watches—all are identical. Each batch of watches pur-chased is carefully coded and marked with its purchase cost.

July 1 Beginning inventory 220 watches at a cost of $400 per watch.July 2 Purchased 200 watches at a cost of $450 each.July 5 Sold 180 watches for $680 each.July 14 Purchased 350 watches at a cost of $480 each.July 28 Sold 480 watches for $720 each.

Instructions(a) Assume that Tempus uses the specific identification cost flow method.

(1) Demonstrate how Tempus could maximize its gross profit for the month by specif-ically selecting which watches to sell on July 5 and July 28.

(2) Demonstrate how Tempus could minimize its gross profit for the month byselecting which watches to sell on July 5 and July 28.

Compute ending inventory,prepare income statements,and answer questions usingFIFO and LIFO.(SO 2, 3)

Gross profit:FIFO $426,400LIFO $420,500

Calculate ending inventory,cost of goods sold, grossprofit, and gross profit rateunder periodic method;compare results.(SO 2, 3)

Gross profit:LIFO $2,320FIFO $2,630Average $2,472

P6-4C The management of Jorgensen Inc. asks your help in determining the compar-ative effects of the FIFO and LIFO inventory cost flow methods. For 2007 the account-ing records show these data.

Compare specificidentification, FIFO, andLIFO under periodic method;use cost flow assumption toinfluence earnings.(SO 2, 3)

Gross profit:Maximum $174,800Minimum $166,000

1700T_web 1/31/06 8:30 AM Page 25 REVISED PAGES

26 CHAPTER 6 Reporting and Analyzing Inventory

(b) Assume that Tempus uses the FIFO cost flow assumption. Calculate cost of goodssold. How much gross profit would Tempus report under this cost flow assumption?

(c) Assume that Tempus uses the LIFO cost flow assumption. Calculate cost of goodssold. How much gross profit would the company report under this cost flowassumption?

(d) Which cost flow method should Tempus Watches select? Explain.

P6-7C This information is available for the Automotive Sector of Ford Motor Companyfor 2004. Ford uses the LIFO inventory method.

(in millions) 2004

Beginning inventory $ 9,151Ending inventory 10,766LIFO reserve 1,001Current assets 44,703Current liabilities 55,027Cost of goods sold 135,856Sales 147,134

Instructions(a) Calculate the inventory turnover ratio and days in inventory.(b) Calculate the current ratio based on inventory as reported using LIFO.(c) Calculate the current ratio after adjusting for the LIFO reserve.(d) Comment on any difference between parts (b) and (c).

*P6-8C Brong Inc. is a retailer operating in Centralia. Brong uses the perpetual inven-tory method. All sales returns from customers result in the goods being returned to in-ventory. (Assume that the inventory is not damaged.) Assume that there are no credittransactions; all amounts are settled in cash. You are provided with the following infor-mation for Brong Inc. for the month of January 2007.

Unit Cost orDate Description Quantity Selling Price

Dec. 31 Ending inventory 140 $14Jan. 2 Purchase 120 15Jan. 6 Sale 150 30Jan. 9 Sale return 20 30Jan. 9 Purchase 85 17Jan. 10 Purchase return 15 17Jan. 10 Sale 70 35Jan. 23 Purchase 100 19Jan. 30 Sale 110 40

Compute inventory turnoverratio and days in inventory;compute current ratio basedon LIFO and after adjustingfor LIFO reserve.(SO 5, 6)

Instructions(a) For each of the following cost flow assumptions, calculate (i) cost of goods sold,

(ii) ending inventory, and (iii) gross profit.(1) LIFO. (Assume sales returns had a cost of $14 and purchase returns had a cost

of $17.)(2) FIFO. (Assume sales returns had costs of $14 for 10 units and $15 for 10 units,

and purchase returns had a cost of $17.)(3) Moving-average. (Round cost per unit to three decimal places.)

(b) Compare results for the three cost flow assumptions.

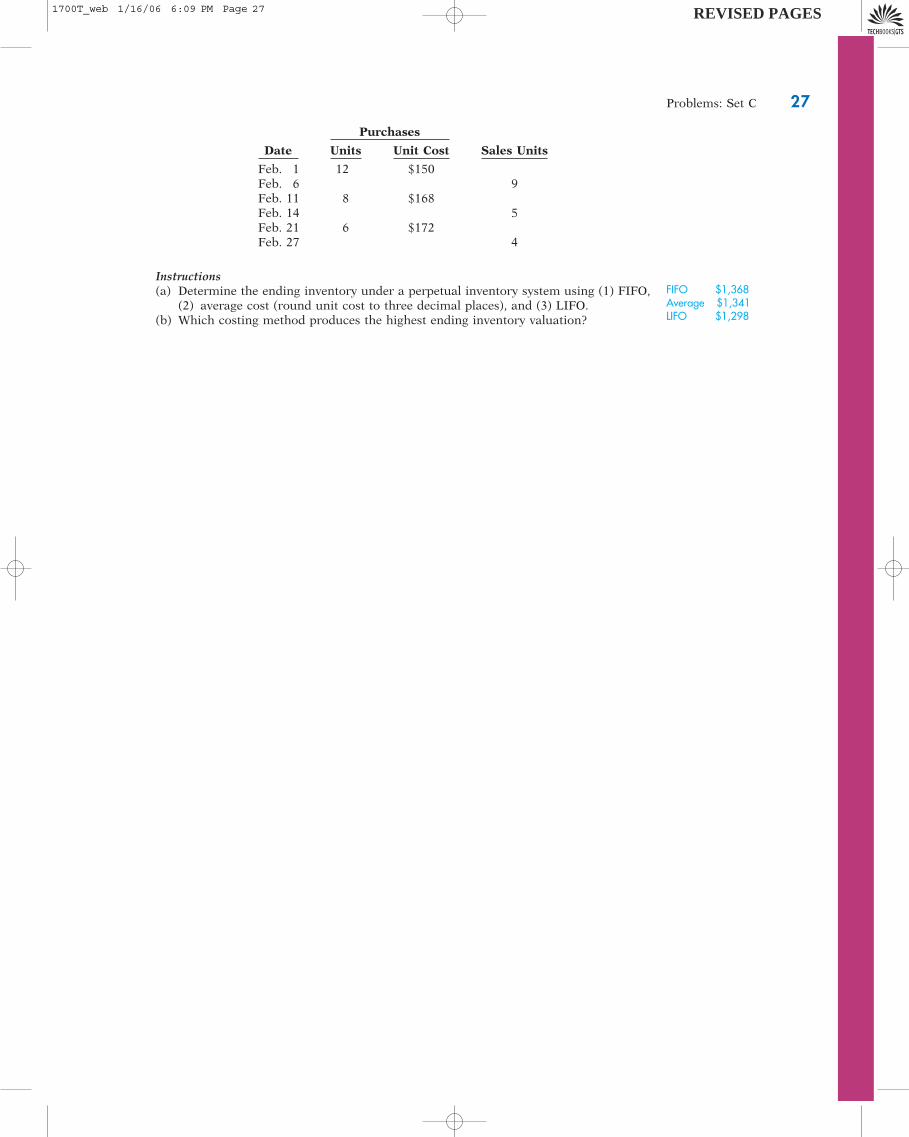

*P6-9C Just Rugs began operations on February 1. It uses a perpetual inventory system.During February the company had the following purchases and sales.

Calculate cost of goods sold,ending inventory, and grossprofit for LIFO, FIFO, andaverage cost under theperpetual system; compareresults.(SO 3, 7)

Determine ending inventoryunder a perpetual inventorysystem.(SO 3, 7)

Gross profit:LIFO $5,580FIFO $6,140Average $5,932

1700T_web 1/16/06 6:09 PM Page 26 REVISED PAGES

Problems: Set C 27

Purchases

Date Units Unit Cost Sales Units

Feb. 1 12 $150Feb. 6 9Feb. 11 8 $168Feb. 14 5Feb. 21 6 $172Feb. 27 4

Instructions(a) Determine the ending inventory under a perpetual inventory system using (1) FIFO,

(2) average cost (round unit cost to three decimal places), and (3) LIFO.(b) Which costing method produces the highest ending inventory valuation?

FIFO $1,368Average $1,341LIFO $1,298

1700T_web 1/16/06 6:09 PM Page 27 REVISED PAGES

28 CHAPTER 7 Internal Control and Cash

Problems: Set C

P7-1C State University’s Accounting Club decided to sell coupon books as a fund-raisingactivity. The books allow users to enjoy restaurants, entertainment, and services such asoil changes, at substantial discounts. The club bought 100 books for $16 each, and mem-bers will sell them for $20. About 20 members attended the last club meeting, and mosttook one or two books to sell. Since the club had already paid for the books and didn’thave other immediate cash needs, members do not have to pay for the books until theysell them.

Extra books are stored on a book shelf in the club’s on-campus office. The office isin a great location with plenty of student traffic. It is shared with the Marketing andInformation Systems clubs. Each club has four sets of keys that are used by its officersand members.

As students sell books, they bring the cash or checks to the club’s office. Studentswith unusual class schedules who arrive when the office is locked can put payments underthe door. Payments are stored in a desk drawer until the treasurer has time to make abank deposit. Students can pick up more books to sell as needed.

Instructions(a) Indicate the weaknesses in internal accounting control in the club’s fund-raising plan.(b) Indicate improvements in internal control procedures for the club’s fund-raising plan.

P7-2C Sam Hill has worked for Dr. Lee Hogan for several years. Sam demonstrates aloyalty that is rare among employees. He is always willing to “cover” for other employeesand hasn’t taken a vacation in three years.

One of Sam’s primary duties at the dental office is to open the mail, list checks re-ceived, and prepare the bank deposit form.

He also collects cash from patients at the cashier window as patients leave. At times,it is so hectic that Sam doesn’t bother to give patients a receipt for the cash paid on theiraccounts. He assures them he will see to it that they receive the proper credit. He is sowell known by most patients that no one has ever complained.

When traffic is slow in the office, Sam offers to help another employee, Mary, postthe payments to patients’ accounts receivable. Dr. Hogan installed a computerized ac-counting program that requires a user ID and password to log in, but Sam and Maryhave found that it is more efficient to just leave the computer on and the receivables fileopen all the time, and minimize the file when it is not in use.

InstructionsIdentify the principles of internal control that may be violated in this situation.

P7-3C On March 31, 2007, Dezelle Company had a cash balance per books of $5,274.20.The statement from Riverside Bank on that date showed a balance of $5,941.40. Acomparison of the bank statement with the cash account revealed the following facts.

1. The bank service charge for March was $28.

2. The bank collected a note receivable of $2,000 for Dezelle Company on March 15, plus$115 of interest. The bank made a $20 charge for the collection. Dezelle has not accruedany interest on the note.

3. The March 31 receipts of $1,681.60 were not included in the bank deposits for March.These receipts were deposited by the company in a night deposit vault on March 31.

4. Company check No. 1245 issued to B. Solveson, a creditor, for $672 that cleared the bankin March was incorrectly entered in the cash payments journal on March 8 for $627.

5. Checks outstanding on March 31 totaled $1,360.00.

6. On March 31 the bank statement showed an NSF charge of $1,033.20 for a checkreceived by the company from Z. Fowler, a customer, on account.

Instructions(a) Prepare the bank reconciliation as of March 31.(b) Prepare the necessary adjusting entries at March 31.

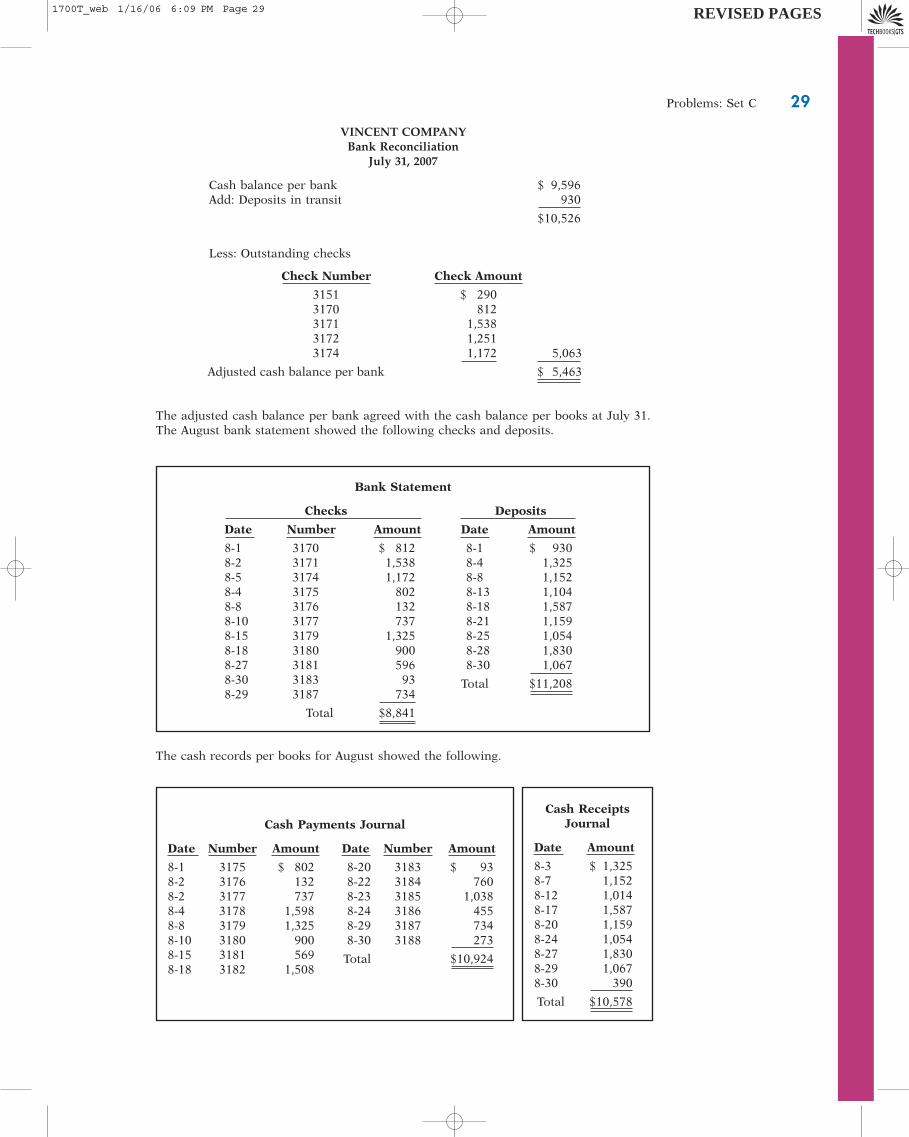

P7-4C The bank portion of the bank reconciliation for Vincent Company at July 31,2007, is shown on the next page.

Identify internal controlweaknesses for cash receipts.(SO 1, 2)

Identify internal controlweaknesses in cash receiptsand cash disbursements.(SO 1, 2, 3)

Prepare a bank reconciliationand adjusting entries.(SO 4)

(a) Cash bal. $6,263Prepare a bank reconciliationand adjusting entries fromdetailed data.(SO 4)

1700T_web 1/31/06 8:30 AM Page 28 REVISED PAGES

Problems: Set C 29

VINCENT COMPANYBank Reconciliation

July 31, 2007

Cash balance per bank $ 9,596Add: Deposits in transit 930

$10,526

The adjusted cash balance per bank agreed with the cash balance per books at July 31.The August bank statement showed the following checks and deposits.

Less: Outstanding checks

Check Number Check Amount

3151 $ 2903170 8123171 1,5383172 1,2513174 1,172 5,063

Adjusted cash balance per bank $ 5,463

Bank Statement

Checks Deposits

Date Number Amount Date Amount

8-1 3170 $ 812 8-1 $ 9308-2 3171 1,538 8-4 1,3258-5 3174 1,172 8-8 1,1528-4 3175 802 8-13 1,1048-8 3176 132 8-18 1,5878-10 3177 737 8-21 1,1598-15 3179 1,325 8-25 1,0548-18 3180 900 8-28 1,8308-27 3181 596 8-30 1,0678-30 3183 93 Total $11,2088-29 3187 734

Total $8,841

Cash Payments Journal

Date Number Amount Date Number Amount

8-1 3175 $ 802 8-20 3183 $ 938-2 3176 132 8-22 3184 7608-2 3177 737 8-23 3185 1,0388-4 3178 1,598 8-24 3186 4558-8 3179 1,325 8-29 3187 7348-10 3180 900 8-30 3188 2738-15 3181 569 Total $10,9248-18 3182 1,508

Cash Receipts Journal

Date Amount

8-3 $ 1,3258-7 1,1528-12 1,0148-17 1,5878-20 1,1598-24 1,0548-27 1,8308-29 1,0678-30 390

Total $10,578

The cash records per books for August showed the following.

1700T_web 1/16/06 6:09 PM Page 29 REVISED PAGES

30 CHAPTER 7 Internal Control and Cash

Cash $ 11,000Accounts receivable 47,600Inventory 21,000Property, plant, and equipment, net of depreciation 70,400Accounts payable 18,200Common stock 110,000Retained earnings 21,800

The bank statement contained two bank memoranda:

1. A credit of $1,670 for the collection of a $1,600 note for Vincent Company plus interestof $80 and less a collection fee of $10. Vincent Company has not accrued any intereston the note.

2. A debit for the printing of additional company checks $70.

At August 31, the cash balance per books was $5,117, and the cash balance per bankstatement was $13,563. The bank did not make any errors, but Vincent Company madetwo errors.

Instructions(a) Using the four steps in the reconciliation procedure described on page 330 of the text-

book, prepare a bank reconciliation at August 31, 2007.(b) Prepare the adjusting entries based on the reconciliation. (Note: The correction of

any errors pertaining to recording checks should be made to Accounts Payable. Thecorrection of any errors relating to recording cash receipts should be made toAccounts Receivable.)

P7-5C Bug Off Company provides insect extermination services. On October 31, 2007,the company’s cash account per its general ledger showed a balance of $4,732.

The bank statement from Newton Bank on that date showed the following balance.

NEWTON BANK

Checks and Debits Deposits and Credits Daily Balance

XXX XXX 10-31 4,070

A comparison of the details on the bank statement with the details in the cash accountrevealed the following facts.

1. The statement included a debit memo of $50 for the printing of additional companychecks.

2. Cash sales of $342 on October 6 were deposited in the bank. The cash receipts jour-nal entry and the deposit slip were incorrectly made for $372. The bank credited BugOff Company for the correct amount.

3. Outstanding checks at October 31 totaled $1,250, and deposits in transit were $2,390.

4. On October 13, the company issued check No. 4263 for $196 to H. Simpson, on account.The check, which cleared the bank in May, was incorrectly journalized and posted byBug Off Company for $169.

5. A $900 note receivable was collected by the bank for Bug Off Company on October 31plus $50 interest. The bank charged a collection fee of $15. No interest has been accruedon the note.

6. Included with the cancelled checks was a check issued by Big Oaf Company for $120that was incorrectly charged to Bug Off Company by the bank.