procedure manual - cda guwahati · this procedure manual is a departmental publication, ......

TRANSCRIPT

DEFENCE ACCOUNTS DEPARTMENT

PROCEDURE MANUAL

OF THE

OFFICE OF THE CONTROLLER GENERALOF DEFENCE ACCOUNTS

Revised Edition 2007

Issued by the Authority of the CONTROLLER GENERAL OF DEFENCE ACCOUNTS

DEFENCE ACCOUNTS DEPARTMENT

PROCEDURE MANUAL

OF THE

OFFICE OF THE CONTROLLER GENERALOF DEFENCE ACCOUNTS

Revised Edition 2007

Issued by the Authority of the CONTROLLER GENERAL OF DEFENCE ACCOUNTS

PREFACE

This Procedure Manual of the office of the C.G.D.A contains instructions for the conduct and disposal of work dealt with in the various sections. The Manual would also be useful to the PCsDA/CsDA offices to know the procedure being followed.

2. All officers and members of the establishment should make themselves fully conversant with the contents of the Manual. Their particular attention is drawn to the objectives of the CGDA’s office. Departmental activities should be directed towards the achievement of these objectives.

3. The contents of the Manual are not exhaustive accordingly basic and supplementary orders relevant to the subject must also be referred to. Instructions contained in the Manual are supplementary to the rules in the Departmental Codes and Manuals and also to Government regulations. This Procedure Manual is a Departmental Publication, and nothing in this Manual will be held to supersede any rule or order of the Government with which it may be at variance.

4. The AT-Coord Section of the CGDA’s office will be responsible for keeping the Procedure Manual corrected up-to-date.

5. This Manual was last issued in 1979. No further edition was brought out so far although some correction slips have been issued. This is a revised edition.

( JNAN PRAKASH )Controller General of Defence Accounts

New DelhiDated the May, 2007

I

TABLE OF CONTENTS

CHAPTER-I

GENERALPara No. Page No.

Functions of C.G.D.A 1 1Objectives of CGDA’s office 2 1Duties and responsibilities of the CGDA 3 1Organisation of CGDA’s office 4-5 2-3APPENDIX- Distribution of work in Administration Wing 4-6

CHAPTER-II

ADMINISTRATION WINGObjective of Administration Section 6 7Officers of the IDAS Recruitment 7,8 7Promotions 9,10,16,17 7-11Probation pay and conditions of service 11,12 9,10Leave 13 10Right to Information 14 10Conduct Rules 15 10Postings and Transfers 18 11List of IDAS officers 19 11Pension 20 11History of services 21 11Confidential Reports 22,23 11,12Examination of Probationers 24 12Methodex Cards 25 13

Accounts Officers & Sr. Accounts OfficersAppointment 26, 27 13,14Increments 28 14Leave 29 14Methodex Cards 30 14Confidential Reports 31 14,15Deputation 32 15General Roster of Senior Accounts Officers & Accounts Officers 33 15

Subordinate Accounts ServiceAppointment 34 15,16Promotion 35 16Probation 36 16Reservation of Vacancies 37 16Assistant Accounts Officers & Section Officers (A) 38 17Confidential Reports 39 17General Roster of Asstt. Accounts Officers & SOs(A) of SAS 40 17

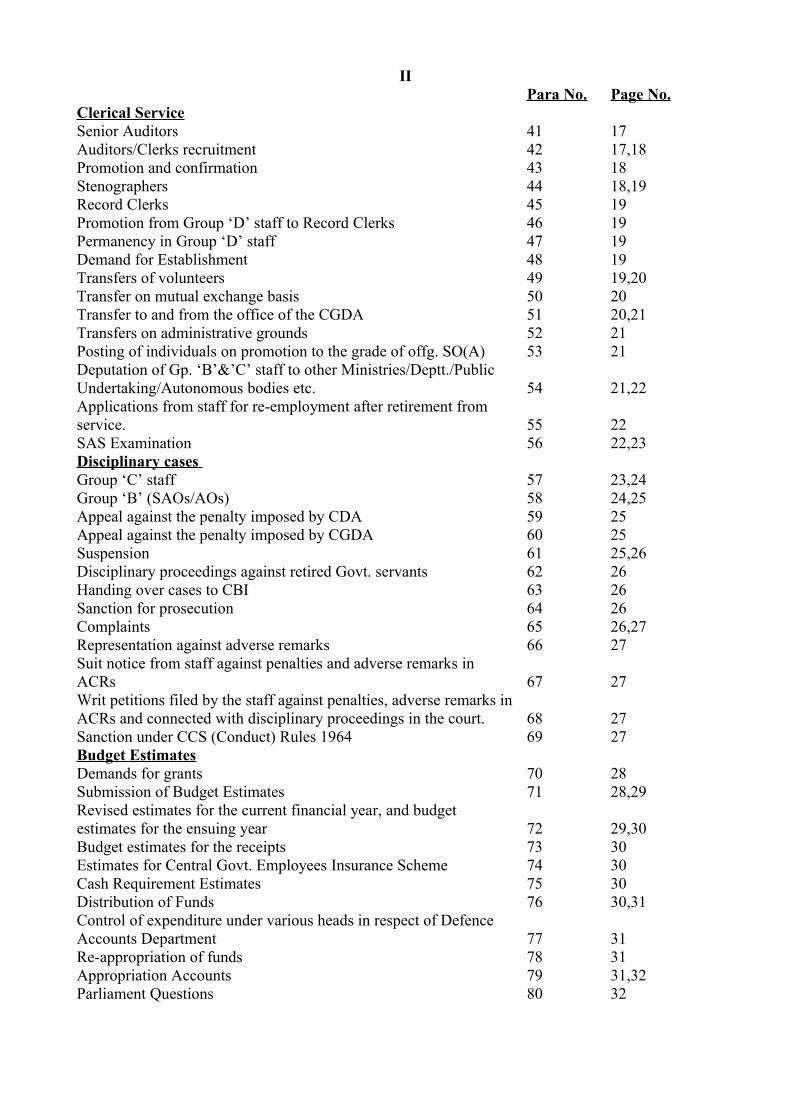

II

Clerical ServicePara No. Page No.

Senior Auditors 41 17Auditors/Clerks recruitment 42 17,18Promotion and confirmation 43 18Stenographers 44 18,19Record Clerks 45 19Promotion from Group ‘D’ staff to Record Clerks 46 19Permanency in Group ‘D’ staff 47 19Demand for Establishment 48 19Transfers of volunteers 49 19,20Transfer on mutual exchange basis 50 20Transfer to and from the office of the CGDA 51 20,21Transfers on administrative grounds 52 21Posting of individuals on promotion to the grade of offg. SO(A) 53 21Deputation of Gp. ‘B’&’C’ staff to other Ministries/Deptt./Public Undertaking/Autonomous bodies etc. 54 21,22Applications from staff for re-employment after retirement from service. 55 22SAS Examination 56 22,23Disciplinary cases Group ‘C’ staff 57 23,24Group ‘B’ (SAOs/AOs) 58 24,25Appeal against the penalty imposed by CDA 59 25Appeal against the penalty imposed by CGDA 60 25Suspension 61 25,26Disciplinary proceedings against retired Govt. servants 62 26Handing over cases to CBI 63 26Sanction for prosecution 64 26Complaints 65 26,27Representation against adverse remarks 66 27Suit notice from staff against penalties and adverse remarks in ACRs 67 27Writ petitions filed by the staff against penalties, adverse remarks in ACRs and connected with disciplinary proceedings in the court. 68 27Sanction under CCS (Conduct) Rules 1964 69 27Budget EstimatesDemands for grants 70 28Submission of Budget Estimates 71 28,29Revised estimates for the current financial year, and budget estimates for the ensuing year 72 29,30Budget estimates for the receipts 73 30Estimates for Central Govt. Employees Insurance Scheme 74 30Cash Requirement Estimates 75 30Distribution of Funds 76 30,31Control of expenditure under various heads in respect of Defence Accounts Department 77 31Re-appropriation of funds 78 31Appropriation Accounts 79 31,32Parliament Questions 80 32

III

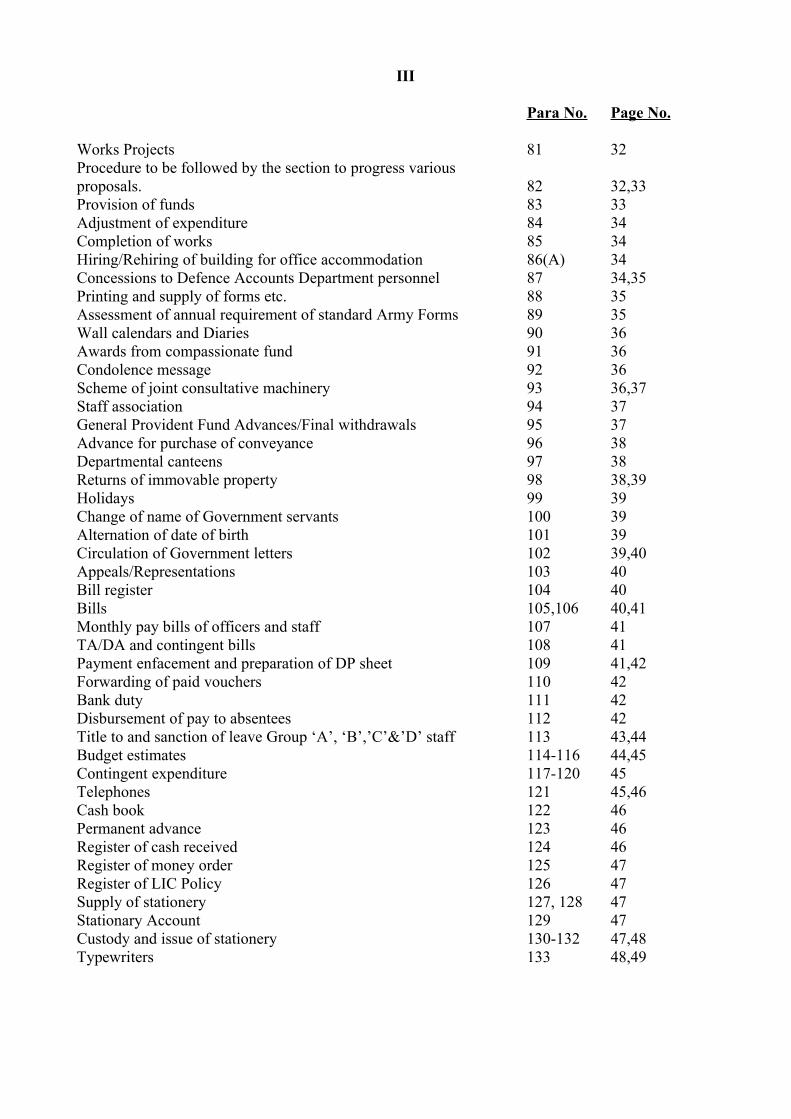

Para No. Page No.

Works Projects 81 32Procedure to be followed by the section to progress various proposals. 82 32,33Provision of funds 83 33Adjustment of expenditure 84 34Completion of works 85 34Hiring/Rehiring of building for office accommodation 86(A) 34Concessions to Defence Accounts Department personnel 87 34,35Printing and supply of forms etc. 88 35Assessment of annual requirement of standard Army Forms 89 35Wall calendars and Diaries 90 36Awards from compassionate fund 91 36Condolence message 92 36Scheme of joint consultative machinery 93 36,37Staff association 94 37General Provident Fund Advances/Final withdrawals 95 37Advance for purchase of conveyance 96 38Departmental canteens 97 38Returns of immovable property 98 38,39Holidays 99 39Change of name of Government servants 100 39Alternation of date of birth 101 39Circulation of Government letters 102 39,40Appeals/Representations 103 40Bill register 104 40Bills 105,106 40,41Monthly pay bills of officers and staff 107 41TA/DA and contingent bills 108 41Payment enfacement and preparation of DP sheet 109 41,42Forwarding of paid vouchers 110 42Bank duty 111 42Disbursement of pay to absentees 112 42Title to and sanction of leave Group ‘A’, ‘B’,’C’&’D’ staff 113 43,44Budget estimates 114-116 44,45Contingent expenditure 117-120 45Telephones 121 45,46Cash book 122 46Permanent advance 123 46Register of cash received 124 46Register of money order 125 47Register of LIC Policy 126 47Supply of stationery 127, 128 47Stationary Account 129 47Custody and issue of stationery 130-132 47,48Typewriters 133 48,49

IVPara No. Page No.

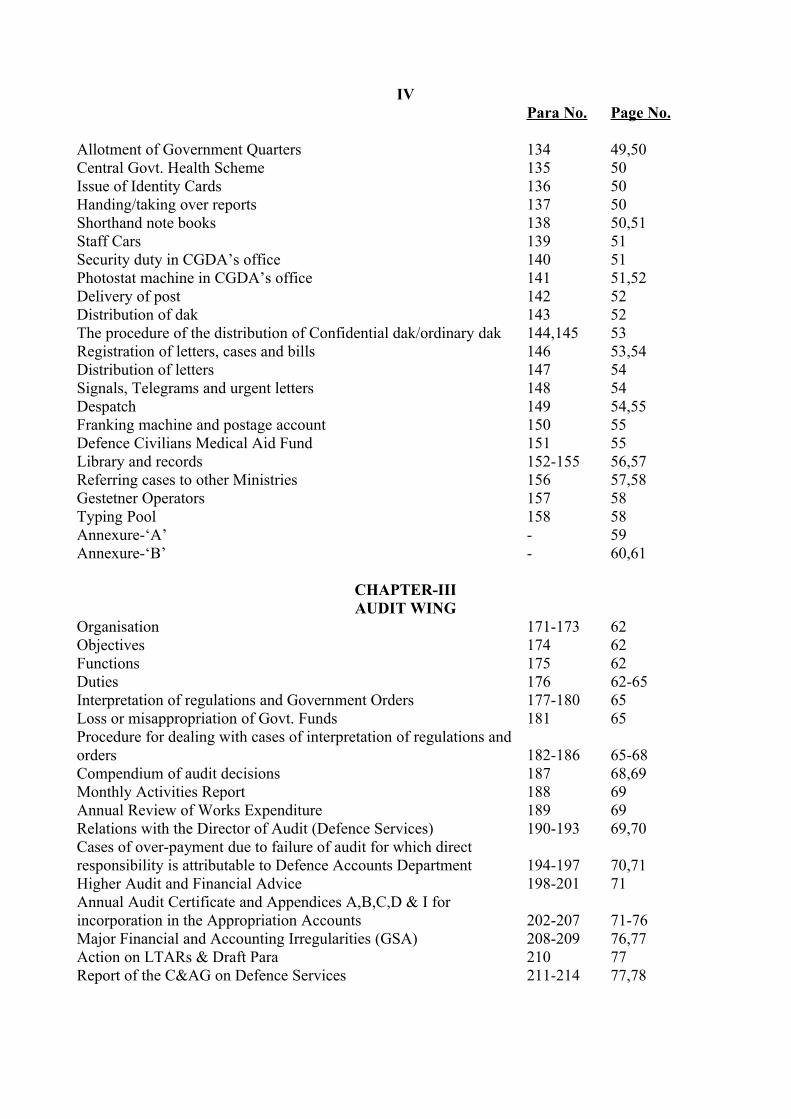

Allotment of Government Quarters 134 49,50Central Govt. Health Scheme 135 50Issue of Identity Cards 136 50Handing/taking over reports 137 50Shorthand note books 138 50,51Staff Cars 139 51Security duty in CGDA’s office 140 51Photostat machine in CGDA’s office 141 51,52Delivery of post 142 52Distribution of dak 143 52The procedure of the distribution of Confidential dak/ordinary dak 144,145 53Registration of letters, cases and bills 146 53,54Distribution of letters 147 54Signals, Telegrams and urgent letters 148 54Despatch 149 54,55Franking machine and postage account 150 55Defence Civilians Medical Aid Fund 151 55Library and records 152-155 56,57Referring cases to other Ministries 156 57,58Gestetner Operators 157 58Typing Pool 158 58Annexure-‘A’ - 59Annexure-‘B’ - 60,61

CHAPTER-IIIAUDIT WING

Organisation 171-173 62Objectives 174 62Functions 175 62Duties 176 62-65Interpretation of regulations and Government Orders 177-180 65Loss or misappropriation of Govt. Funds 181 65Procedure for dealing with cases of interpretation of regulations and orders 182-186 65-68Compendium of audit decisions 187 68,69Monthly Activities Report 188 69Annual Review of Works Expenditure 189 69Relations with the Director of Audit (Defence Services) 190-193 69,70Cases of over-payment due to failure of audit for which direct responsibility is attributable to Defence Accounts Department 194-197 70,71Higher Audit and Financial Advice 198-201 71Annual Audit Certificate and Appendices A,B,C,D & I for incorporation in the Appropriation Accounts 202-207 71-76Major Financial and Accounting Irregularities (GSA) 208-209 76,77Action on LTARs & Draft Para 210 77Report of the C&AG on Defence Services 211-214 77,78

VPara No. Page No.

Annual Accounts of Military Farms 215 78Annual (Commercial) Accounts of CSD 216 79Procedure for communicating audit decisions 217,218 79,80New Pension Scheme 219 80Procedure for submission of cases 220-226 80, 81Performance Audit 227-230 81Complaint Cell 231-233 81, 82Position of CGDA in regard to:

Pay Accounts maintained by AF and Navy 234-236 82,83Pay and Accounts Office, Ministry of DefenceOrdnance Factories under the integrated set-up

Inspection GroupOrganisation and distribution of work 237 83General 238 83Objectives of inspection 239 83Functions 240 83,84Scope of work 241, 242 84Periodicity of inspection 243 84Organizing inspection 244 84Allocation of work 245, 246 84, 85Preparation and disposal of inspection report 247 85Inspection programme 248 85

Organisation and Methods Cell:Objectives 249, 250 86Duties of O&M Cell 251 86Systems and Procedure Section:Objectives 252 87Functions 253 87Detailed Instructions 254-260 87, 88Hindi Cell 261-266 88, 89Miscellaneous 267, 268 90Annexure ‘A’ - 91-94Annexure ‘B’ - 95Annexure ‘C’ - 96Annexure ‘D’ - 97Annexure ‘E’ - 98

CHAPTER-IVACCOUNTS SECTION

Objectives 281 99Functions 282 99, 100Review of monthly Revenue, Debt and Remittance Heads and Service Heads Compilation. 283, 284 100, 101Preparation and rendition of financial statement and accounts 285 101, 102Miscellaneous 286-290 102-105Adjustment of Inter-Departmental Transactions outside the books of RBI. 291, 292 105

VI

CHAPTER-VPRINCIPAL IFA WING

Para No. Page No.

Organisation 301 106Objectives 302 106Duties 303 106-108Monitoring system 304 108, 109

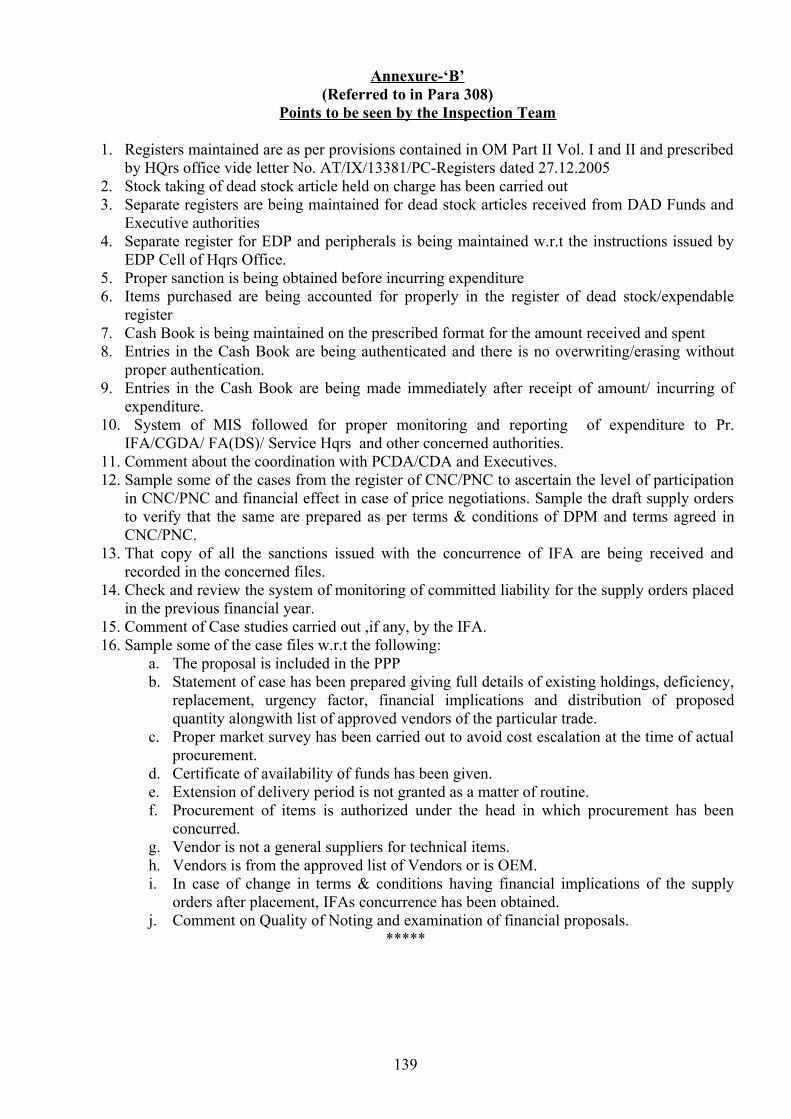

Inspection of IFAs:Introduction 305 109Inspection Programme 306 109Periodicity of inspection 307 109Scope of works 308 109, 110Organizing inspection 309 110Allocation of works 310 110Preparation and disposal of Inspection Report 311 110Annexure-‘A’ - 111, 112Annexure-‘B’ - 113

CHAPTER-VI

TRAININGObjective 331 114In house training 332 114Regional Training Centres 333 114Regional Advisory Committees 334 114Centres of Excellence 335 115National Institute of Defence Finance Management, Pune 336 115Training Division, Brar Square, Delhi 337 115, 116

CHAPTER-VII

CGDA-EDP SECTION

CGDA-EDP Section 351 117Functions of EDP Section 252 117Responsibilities of EDP Centre 353 117, 118

9

CHAPTER IGENERAL

Functions of the C.G.D.A

1. The Controller General of Defence Accounts is the head of the Defence Accounts Department. He functions on behalf of the Secretary Defence (Finance)/ Financial Adviser (Defence Services), as the Chief Authority in all matters affecting financial advice, internal audit and the accounting in respect of expenditure pertaining to the Defence Services. Under the scheme of Departmentalization of accounts in the Ministry of Defence, the Defence Secretary will be the Chief Accounting Authority for all transactions of the Ministry of Defence and this responsibility is discharged by him through and with the assistance of Secretary Defence (Finance)/ Financial Adviser (Defence Services), who will function for and on behalf of the Chief Accounting Authority. The payments and accounting functions in respect of the Ministry of Defence are entrusted to the Controller General of Defence Accounts who will function as the Principal Accounting Officer.

Objectives of C.G.D.A’s office

2. The objectives of the office of the C.G.D.A are to ensure that

(i) the activities of the Defence Accounts Department are organized to meet the accounting, internal audit and financial advice needs of the Defence Services consistent with the policy of the Government.

(ii) adequate and up-to-date procedures obtain for efficient discharge of the functions of the Department in the field of Accounts, Internal Audit and Financial Advice.

(iii) proper planning is made in respect of personnel and facilities required for the efficient functioning of the Department in tune with modern management concepts.

Duties & Responsibilities of C.G.D.A.

3. The C.G.D.A is responsible for the administration and efficient working of the Defence Accounts Department. All Principal Controllers/Controllers in the Department function under his over-all guidance and direction and are directly responsible to him. He may on his own motion or on a reference being made to him by the Government of India or the Services Headquarters, review any audit decision of any audit officer of the Defence Accounts Department and take a final decision in the matter.

The Controller General of Defence Accounts is in-charge of the Headquarters Office of the Defence Accounts Department. He issues necessary instructions to Principal Controllers/Controllers of Defence Accounts, Principal Controller/Controllers of Accounts (Factories), Principal IFA/IFAs in matters relating to maintenance and internal audit of accounts, accounts and audit procedure, classification of receipts and charges, etc. either on his own responsibility, or after taking orders of the Government of India, if necessary. He gives audit rulings, in consultation with the Ministry of Defence (Finance), where necessary on doubtful points arising from internal audit and referred to him by the Principal Controllers/Controllers of Defence Accounts/Principal Controller/Controller of Accounts (Fys), Principal IFA/IFA. These audit rulings refer to the internal audit exercised by the Defence Accounts Department and not to statutory audit exercised by the D.G.A.D.S on behalf of the Comptroller and Auditor General.

10

He assists the Government of India with advice on all questions of audit and accounts procedure relating to Defence expenditure, which may be referred to him.

He maintains up-to-date and relevant information relating to personnel management assesses the requirements of officers and establishment for the whole department and posts them to the various offices according to their requirements. He also sends at his discretion officers and staff on deputation to the Ministries, other Government Departments and Public Sector Undertakings. He coordinates and pursues with the Government the projects of office and residential accommodation required by the Department at various stations. He coordinates the funds requirements of various Controllers Organizations, prepares budget estimates for the Department, makes budgetary allocation of funds to the Principal Controllers/Controllers and watches their utilization.

The Controller General of Defence Accounts prepares an annual Statement of Central Transactions (SCT) of Defence Services Receipts and charges each year and sends it to the Controller General of Accounts, Ministry of Finance, and Department of Expenditure, New Delhi on the date prescribed by them. The statement of Central Transactions is prepared from the material available in the Consolidated Compilation of Revenue, Debt and Remittances Heads for March Supplementary (including correction thereto if any).

A copy of the Statement of Central Transaction will also be forwarded by the Controller General of Defence Accounts to the Ministry of Defence (Finance), the Principal controllers/Controllers of Defence Accounts and all command officers of DGADS.

He prepares certain subsidiary statements in connection with the Appropriation Accounts as prescribed in Defence Audit Code and submits them to the Financial Adviser, Defence Services/Secretary (Defence Finance). He also renders annually to the Financial Adviser, Defence Services/Secretary (Defence Finance) an Audit Certificate on the accounts of the Defence Services.

He prepares the portion of the combined Finance and Revenue Accounts pertaining to the Defence Services and submits it to the Controller General of Accounts and Director General of Audit, Defence Services for incorporation in the combined Finance and Revenue accounts of the Central and State Government in India. He is the Principal Accounting Officer for the Civil Estimates of the Ministry of Defence. He prepares the Appropriation Accounts of the above Estimates and sends the same to the Financial Adviser, Defence Services/Secretary (Defence Finance) and the Defence Secretary for onward transmission to the Controller General of Accounts and Director General of Audit, Defence Services.

He also prepares the statement of central transactions in respect of Civil Estimates and forwards it to the Controller General of Accounts.

Organisation of C.G.D.A’s Office

4. (i) The office of the C.G.D.A comprises Administration, Audit, Accounts & Budget, Training, Pr. IFA and EDP wings. Each wing is sub-

11

divided into functional groups as shown in Appendix-I to this Para, Appendix-I to Para-176.

(ii) There are two Additional Controllers General of Defence Accounts under him, who are in charge of Audit wing. There are two Principal Controllers of Defence Accounts who are in charge of HRD and IFA Wings. There is a Joint Controller General of Defence Accounts in charge of Administration and other Joint Controllers General of Defence Accounts in charge of various Audit/Accounts/Training/Pr. IFA/EDP Wings. These officers are assisted by the Senior Deputy Controllers General/Deputy Controllers General of Defence Accounts, Assistant Controllers General of Defence Accounts, Senior Accounts Officers and Accounts Officers for the various groups under their charge.

5 (i) The General Section which was hitherto looking after the internal administration of C.G.D.A’s office now forms part of Administration Section on reorganization of the Section.

(ii) The C.G.D.A's office is organized broadly on the pattern of a Controller’s Office. The procedure laid down in the different Office Manuals is also applicable to the various functions in C.G.D.A's office wherever such provisions are relevant.

12

APPENDIX-I (See Para-4)

DISTRIBUTION OF WORK IN ADMINISTRATION WING

Group Broad description of functions

AN-I (IDAS) All matters concerning IDAS officers and other Gp-A posts. viz Recruitment, Promotions, Confirmation, transfers, Representation/appealsConfidential reports

AN-II (A.O) Work relating to the DPC for promotion to A.O’s Grade, SAO’s grade, Hindi Officer’s grade, Sr. PS grade. Promotion, Transfer, confidential reports, of SAO/AO/Sr.PS except discipline.

AN-III (Coord) Opening-closing of DAD offices. Creation of new posts of SAOs/AOs/Sr.PSMonitoring/clearance of arrears/weekly progress report.Review of reports and returns pertaining to administrative matters.Diarising and distribution of classified dak. Preparation of DP Sheets in respect of payments in CGDA’s office.Legal Cell work of CGDA’s office, Processing of applications received under RTI Act.

AN-IV (Establishment)

General Administration including postings, transfers, ACRs, and discipline in CGDA’s office.Budget Estimates-CGDA office.Pay bills of officers and staff.GP Fund advance, House building advance and other advances—officers and staff.Screening of staff after 50/55 years of age.Receipt, diarizing and distribution of dak, telegrams, Govt. letters etc.Despatch of dak, telegrams etc. and maintenance of stamp account.Pension task including cash payment in lieu of unutilized Earned Leave on the date of retirement; Maintenance of service book and leave Accounts.Arranging Security passes for the staffPeriodical destruction of old records.Maintenance of Library, keeping all the books of Regulations etc. corrected up to date.Issue of no objection certificate for passport.

AN-V (Cash) Cash transactions, disbursement of pay and allowances of staffEmployment of Causal Labour.Security measures.Payment of contingent and other charges. Receipt and distribution of cheques for contingent & other chargesAccommodation for office and staff. Maintenance and control of staff cars.Provision and maintenance of Dead stock-Articles, Medical bills.Housekeeping in CGDA’s office.

AN-VI Accounts Section of CGDA’s officeJCM and Staff Associations

13

AN-VII Budget estimates of DAD and budgetary control, Allocation of funds under locally controlled heads and P-Loans and Advances.Parliament questions.Orders on House Building Advance.Sanction of permanent advance to sub-offices.Regularisation of losses in DAD, Condemnation Board Proceedings.Awards, Fees and Honorarium.GPF advance/withdrawal of PCsDA/CsDA.DAD Employees Co-operative Societies.Allocation of funds of CSD.Representation relating to discrepancy in GP Fund.Advances for House Building and Conveyance by PCsDA/CsDA.Orders regarding medical reimbursement claims.CGHS Scheme.Family planning allowancesDefence Civilian Medical Aid Fund

AN-VIII Demand for establishment.Fixation of strength in the Controllers’ organization.Framing of Recruitment Rules for Group C & D Services and amendments thereof.Conversion of Ty. Posts of Group C & D to permanent posts.Verification of character and antecedents.Compassionate appointments.D Section work of CGDA’s office

AN-IX Deputation Group C Staff and AAOs/Permanent absorption of Group C staff in outside organizations. Inter-command transfer of AAOs/SOs (A).Promotion to the grade of Supervisor (A/Cs)Provisioning of SAS Pt.II passed candidates

AN-X Inter-Command transfer of Group C & D staff except SOs (A).Transfer of Group C staff to and from CGDA’s office.Transfer policy and connected matters.

AN/XI Promotion, ACP, Probation and Confirmation in respect of AAOs, PS (Gp.B) and Group C and D Grade; and de-reservation of vacancies of AAOs, SOs (A), Senior Auditors grade and Auditors grade.Screening of staff after 50/55 years. Termination of service under Rule 5 of CCS (TS) Rules.

AN/XII Formulation of plans, budget allocation and monitoring of progress in the field of construction of permanent office/residential accommodation for DAD.

AN-XIII All matters relating to discipline / vigilance cases of Group B, C and D staff.Complaints against DAD staff.Rendition of Reports and Returns on disciplinary cases to higher authorities.Representation against adverse remarks in CRs up to AAOs level and general orders regarding CRs.Cases of defalcation/fraud.

AN/XIV Orders/ cases regarding Pay & Allowances to DAD Staff.Orders/ cases regarding increment, Leave, Medical –Reimbursement

14

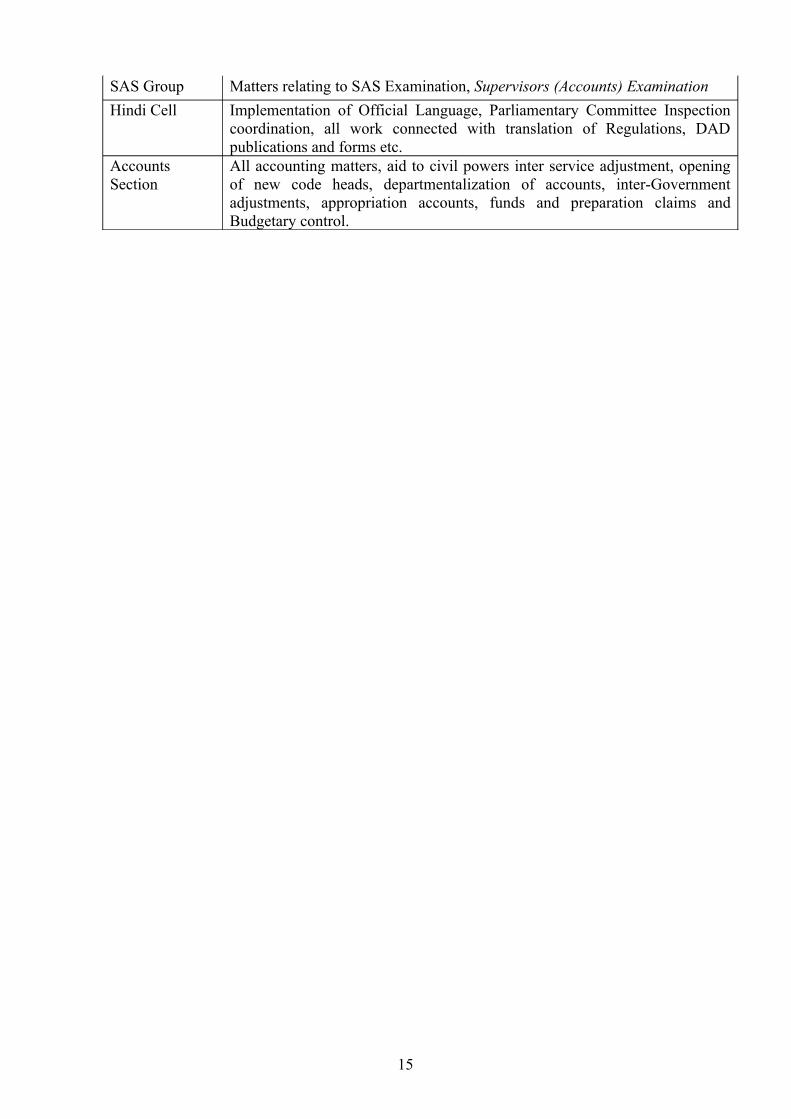

SAS Group Matters relating to SAS Examination, Supervisors (Accounts) ExaminationHindi Cell Implementation of Official Language, Parliamentary Committee Inspection

coordination, all work connected with translation of Regulations, DAD publications and forms etc.

Accounts Section

All accounting matters, aid to civil powers inter service adjustment, opening of new code heads, departmentalization of accounts, inter-Government adjustments, appropriation accounts, funds and preparation claims and Budgetary control.

15

CHAPTER – II

ADMINISTRATION WING

Detailed Instructions

Objective of Administrative Section

6. The Objective of Administration Section is to ensure proper planning and execution of policies regarding personnel administration and allied matters. Officers of the Indian Defence Accounts Service-Recruitment .

7. The relevant provisions in O.M. Part I regarding recruitment appointment, pay, leave etc., of I.D.A.S. Officers may be referred to in this connection. Further detailed instructions are furnished below. The Recruitment Rules in respect of Indian Defence Accounts Service are at Annexure ‘D’ of Chapter II of Office Manual Part-I. Vacancies in the Indian Defence Accounts Service are filled by the following methods:

(i) 65 % of the total posts in the service shall be filled by direct recruitment through the competitive examination held in India by the Union Public Service Commission.

(ii) 35 % by promotion, of officers of Subordinate service. 8. The vacancies available for direct recruitment are reported to the Financial Adviser, Ministry of Defence (Finance)/ Secretary (Defence Finance) for communication to the Union Public Service Commission, as and when called for by the Commission. While computing annual vacancies in IDAS cadre, the ‘drop outs’ of one year will be carried forward to the next year. The Commission then notifies the number of vacancies available for competition at the examination held annually for recruitment to the I.D.A.S. On receipt of the results of the examination, selection of probationers for the Indian Defence Accounts Service is made by the Department of Personnel and Training, Ministry of Personnel, Pension and Pensioners Grievances.

Promotions

9. To various grades in the Indian Defence Accounts Service are made on the recommendation of Departmental promotion Committees. The composition of the Departmental Promotion Committees will be as under: -

(A) Promotion of Senior Accounts Officer to the regular cadre of Indian Defence Accounts Service:

(i) Chairman/Member U.P.S.C. ……Chairman(ii) Controller General of Defence Accounts. .….. Member(iii) Addl. Financial Adviser/Dy. Financial Adviser, MOD (Finance Division) ….. Member(iv) Principal Controller of Defence Accounts PIFA//Principal Controller of Accounts (Fys)/Joint Controller General of Defence Accounts/

16

Controller of Finance and Accounts (Fys)/Integrated Fin. Adviser ….. Member

(B) (a) Promotion of from Junior Time Scale to Senior Time scale: (i) Controller General of Defence Accounts/Additional Controller General of Defence Accounts ….. Chairman(ii) Principal CDA/PCA (Fys)/Pr. IFA ….. Member(ii) Controller of Defence Accounts/Integrated Financial Adviser ….. Member (iv) Addl. Financial Adviser, MOD(Finance) ….. Member(v) Director/Deputy Financial Adviser, MOD (Finance Division) ….. Member

(b) Confirmation in Junior Time Scale:

(i) Controller General of Defence Accounts/Additional Controller General of Defence Accounts ….. Chairman(ii) Addl. Financial Adviser/Dy.Financial Adviser MOD (Finance Division) .. Member (iii) Pr. CDA / PCA (Fys)/ Joint Controller General of Defence Accounts/ Controller of Defence Accounts / Controller of Finance and Accounts (Fys) /Integrated Fin. Adviser. . …. Member

(C) Promotion from Senior Scale of the I.D.A.S to Junior Administrative Grade:

(i) Chairman/Member U.P.S.C. …. Chairman(ii) Secretary(Defence Finance)/Financial Adviser (Defence Services) …… Member(iii) Controller General of Defence Accounts. …… Member(iv) Additional Financial Adviser, MOD(Finance Division) ……. Member (v) Pr. CDA / PCA (Fys)/Controller of Defence Accounts/Controller of Finance & Accounts (Factories)/Integrated Financial Adviser …… Member

(D) Promotion to the Non-Functional Selection Grade of the Junior Administrative Grade:

(i) Secretary (Defence Finance)/ Financial Adviser (Defence Services)….. Chairman (ii) Controller General of Defence Accounts ….. Member(iii) Additional Financial Adviser, MOD(Finance) ….. Member (iv) Joint Secretary(AN), Ministry of Home Affairs as nominee of Establishment Officer, Department of Personnel & Training ….. Member

(E) Promotion to the Senior Administrative Grade:

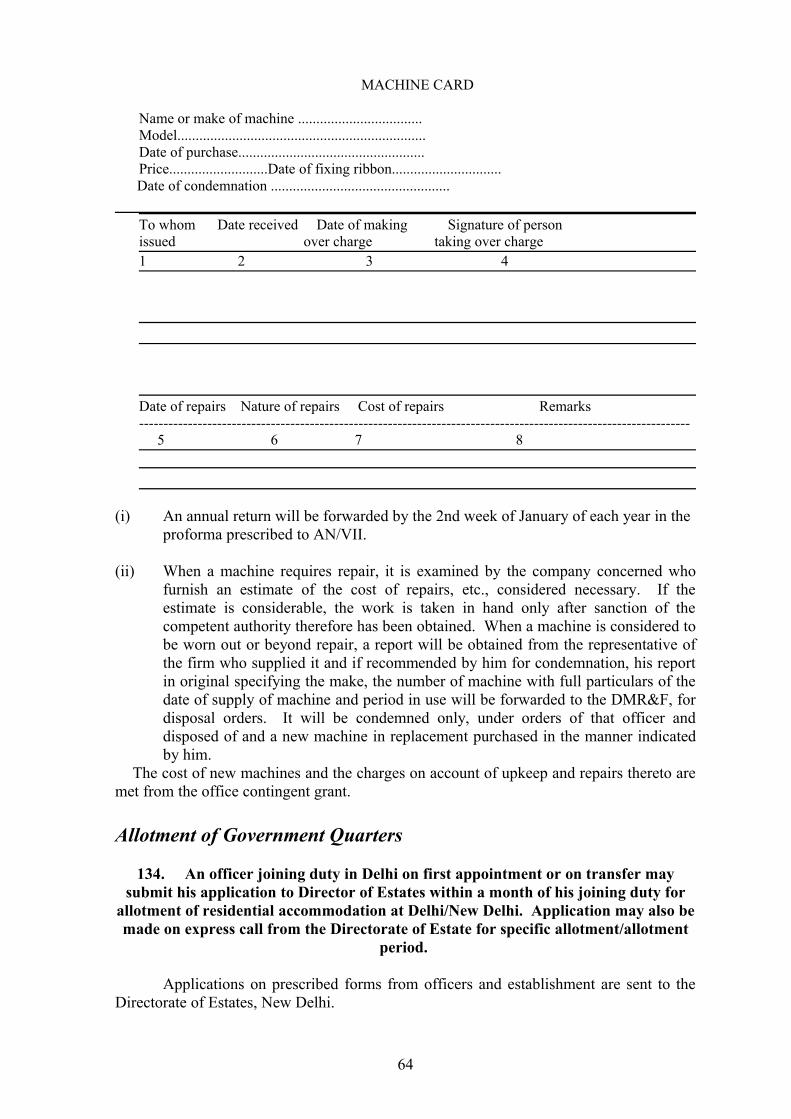

(i) Chairman/Member U.P.S.C. ..….Chairman(ii) Secretary(Defence Finance)/Financial Adviser(Defence Services) …… Member(iii) Controller General of Defence Accounts .….. Member

(F) Promotion to the grade of Principal Controller of Defence Accounts and equivalent posts:

(i) Chairman/Member U.P.S.C. …….Chairman(ii) Secretary(Defence Finance)/Financial Adviser(Defence Services) …… Member(iii) Controller General of Defence Accounts ….. Member

17

(G) Promotion to the grade of Additional Controller General of Defence Accounts (i) Chairman/Member U.P.S.C. …….Chairman(ii) Secretary(Defence Finance)/Financial Adviser(Defence Services) …… Member(iii) Controller General of Defence Accounts ….. Member

(H) Promotion to C.G.D.A. (i) Chairman/Member U.P.S.C. …….Chairman(ii) Secretary, Ministry of Defence ……. Member(iii) Secretary (Defence Finance)/Financial Adviser (Defence Services) ……. Member Procedure for processing proposals for promotion and confirmation of officers

10. The I.D.A.S probationers (Direct Recruits) will become due for confirmation in the Junior Time Scale on satisfactory completion of two years probation and after passing both the parts of Department Examination. As and when the IDAS probationers (Direct Recruits) complete two years service, orders of C.G.D.A will be obtained for constitution of DPC consisting of members indicated in para 9 above. The recommendations of the DPC will be submitted to the Ministry of Defence (Finance) for their approval. After the approval of the Ministry of Defence (Finance) is received, Gazette Notification confirming Probationers found fit for such confirmation will be issued. Senior Accounts officers promoted to the regular cadre of the Indian Defence Accounts Service will be on probation for a period of two years. On satisfactory completion of probation period, their cases for clearance of probation will be considered by a DPC composed of members indicated in para 9 (for confirmation). The recommendations of the DPC will be sent to the Ministry of Defence (Finance) for their approval and on receipt of approval, the same will be notified in Gazette notification. IDAS Officers who have completed four years service in the Junior Time Scale will be eligible for consideration for promotion to Senior Time Scale. Proposal for DPC for promotion will be initiated as per extant orders of DOP&T to consider their cases for promotion to Senior Time Scale. The proceedings of the DPC will be sent to the Secretary (Defence Finance)/FA (DS) for obtaining the approval of the Raksha Mantri. On acceptance of the recommendations of the D.P.C., the officers recommended will be appointed to Senior Time Scale and designated where necessary.

In the case of other promotions, i.e. Senior Accounts Officers grade to the regular IDAS, promotions from Senior Time Scale to Junior Administrative Grade, Junior Administrative Grade to the Senior Administrative Grade, from the Senior Administrative grade to the Higher Administrative grade and for promotion to the grade of Addl. Controller General of Defence Accounts and equivalent posts proposals will be sent to the Union Public Service Commission in the prescribed proforma for convening the DPC and for fixation of date for DPC meeting. As and when DPC proceedings are received from the UPSC, they will be submitted to Ministry of Defence (Finance)) for obtaining the approval of the Raksha Mantri to DPC proceedings. In the case of promotions to the Senior Administrative Grade and above, promotions will be made after obtaining the approval of the Appointments Committee of the Cabinet.

Probation

18

11. Rules for the training and departmental examination of officers appointed direct as a probationer in the Indian Defence Accounts Service are laid down in Annexure ‘B’ to Chapter II of Office Manual Part I. When a probationer has completed his training he is posted to one of the offices of the department for regular duties.

Pay and conditions of service

12. The conditions of service and rates of pay, etc. of officers of the IDAS are contained in Chapters II and III of Office Manual Part I.

Leave 13. Principal Controllers of Defence Accounts/Controllers of Defence Accounts and equivalent ranks have been delegated powers to grant leave to the Indian Defence Accounts Service Officers of the rank of Additional CDA and below except where replacements are required. However, where the total period of leave (including extension) exceeds four months, leave will be sanctioned by Principal Controllers/Controllers, even where replacement is not required, with the prior concurrence of the C.G.D.A. Grant of all kinds of leave to Officers in the Higher Administrative Grade and Senior Administrative Grade and above in the office of the C.G.D.A and also Principal Controllers/Controllers, where no officiating arrangements are to be made will be made by the C.G.D.A. However, in those offices where CsDA report to PCsDA, the leave sanctioning authority would be the Principal Controllers. As far as IDAS officers and staff employed in CGDA’s office is concerned, leave will be sanctioned as per the delegation of powers made by CGDA indicated at Annexure-‘A’ to Chapter-II.

Right to Information

14. In accordance with the provisions of Section 4 (xvi) of the Right to Information Act, 2005 notified by the Government of India, Senior Deputy CGDA (Admin) has been appointed as the Public Information Officer and the Joint CGDA (Admin) as the Appellate Authority for the HQrs Office of the CGDA. Similarly, Public Information Officers and Appellate authorities have also been appointed in the field offices of the Department. Applications received under RTI Act are processed by AN-III section and put up to the CPIO/ Appellate Authority for orders.

Conduct Rules

15. Officers of the Indian Defence Accounts Service are governed by the Central Civil Services (Classification Control and Appeal) Rules, 1965, Central Civil Services (Conduct) Rules 1964 and the Fundamental Rules for purposes of appointment discipline, suspension, dismissal, removal or compulsory retirement from service.

Promotions

16. Promotions to various grades in the Indian Defence Accounts Services are made on the recommendations of the Departmental Promotion Committees. Promotions of Senior Accounts Officers to the Indian Defence Accounts Service require the approval of the

19

Government of India in each case. Promotion of officers of the IDAS either in an officiating or permanent capacity to the appointment of Controller General of Defence Accounts, or Additional Controller General of Defence Accounts and equivalent, or Principal Controller of Defence Accounts and equivalent or Controllers of Defence Accounts and equivalent require the approval of the Raksha Mantri and the Appointments Committee of the Cabinet.

20

17. While submitting proposals of promotion of officers of the department of Government of Government, the question whether promotion of any officer of the department will necessitate the promotion of any of the officers serving outside the regular line such as the Deputy Financial Advisers, etc., under the ‘Next Below Rule’ should be carefully examined and this point prominently submitted for orders of the Secretary (Defence Finance)/Financial Adviser, Ministry of Defence (Finance).

Postings & Transfers

18. Controller General of Defence Accounts has powers to order transfer of Indian Defence Accounts Service officers upto the rank of Additional CDA/Jt. CsDA within the Department. Transfers and postings of officers of the Senior Administrative Grade / Higher Administrative Grade will, however, be made with the approval of the Raksha Mantri. Controller General of Defence Accounts is also empowered to transfer IDAS officers except those of the Senior Administrative Grade/Higher Administrative Grade on deputation to other departments or on foreign service and to select IDAS officers of all ranks for training in India except in cases where the specific orders of the Raksha Mantri are required.

List of officers of the Indian Defence Accounts Service

19. A list of the officers of the Indian Defence Accounts Services called Pink List is prepared periodically. A copy of this list will be furnished to all IDAS officers. Sufficient spare copies will also be kept for the use of UPSC or to meet other requirements. Correction of the lists is made from the information available in the office of CGDA. The office copy of the list should always be kept corrected up-to-date.

Pensions

20. The pension of the officers of the Indian Defence Accounts Service are governed by the rules contained in Central Civil services (Pension) Rules 1972 as amended from time to time.

History of services

21. History of services of the IDAS officers are centrally maintained by the Principal Controller of Defence Accounts (Pensions), Allahabad.

Confidential Reports

22. As soon as an officer is relieved from an organization, his MTCR (for relief before 31st March) or the ACR will be initiated by the concerned organization. The same will be finalized immediately and forwarded to the CGDA. For ACRs, the time frame prescribed will be followed. While completing the column ‘integrity’ in the Annual Confidential Report, the instructions contained in Ministry of Home Affairs O.M. 51/4/64-Estt (A). date 21.6.65 should be kept in mind. Integrity of the officer concerned will be certified. In case it is not possible to do so, the column pertaining to integrity should be recorded and sent together with the character roll to the next Superior officer, who should ensure that the follow-up action is taken with due expedition. If as a result of the follow-up action, an officer is exonerated, his integrity should be certified and an entry made in the character roll. If suspicions regarding his integrity are confirmed, this fact can also be recorded and

21

duly communicated to the officer concerned. The Confidential Report should contain an overall assessment of the officer’s personality, his good qualities and short-comings and should in particular, touch the following points: viz., quality of mind (originality and comprehension); Knowledge of work; power of expression (on paper and in discussion); power of acquiring general information; attention to detail, industry and conscientiousness; judgment; speed of disposal; willingness to accept responsibility and take decisions; relations with subordinates and colleagues; Public relations. Confidential Report and Assessment Reports of all IDAS officers will be written by the officers under whom they are serving and will be reviewed and accepted as per orders prevalent.

After the Confidential reports are accepted by the concerned authorities they will be recorded in the CR dossier of the officer concerned and page numbered and indexed. Whenever a CR dossier or copies thereof are sent to Union Public service Commission, Ministry of Defence (Finance) and other Ministries/Departments and organizations in connection with promotions, confirmations and deputation etc., an entry will be made in the register opened for the purpose on the proforma indicated below and return watched:

Register for watching the return of CR dossiers sent to other Department/Ministries/U.P.S.C-----------------------------------------------------------------------------------------------------------------------------------Sl Name of the Mini- No.and No. and Initials Officer stry/ date of date of Mi of Deptt. Letter nistry/Deptt Auditor/ to which under letter under SO(A) sent which which CR dossier CR was returned

dossier forwarded --------------------------------------------------------------------------------------------- ------------------------- 1 2 3 4 5 6

--------------------------------------------------------------------------------------------- -----------------------------------

Custody of Confidential reports

23 The Confidential Reports dossiers of officers of the Senior Administrative Grade and above will be held in the personal custody of the Controller General of Defence Accounts. The Confidential Report dossiers of officers of the Junior Administrative Grade (including Selection Grade of the Junior Administrative Grade) will be held in the personal custody of Joint Controller General of Defence Accounts (Administration). Confidential report of all other IDAS officer will be kept in the personal custody of Deputy Controller General of Defence Accounts (AN)

Examination of Probationers

24. Departmental examination of the probationers in the Department is held in two parts, Part I and Part II of the examination unless they have passed in Part I. A test in Hindi also forms a part of the Departmental examination which the probationers are required to take along with Part I of the examination. But those who fail in Hindi test alone may be allowed to take it again along with the Part II of the examination. The

22

subjects for the different papers in Parts I and II of the examination are indicated in Annexure ‘C’ to Chapter II of Office Manual Part I. Question Papers for the examination are set by the officers selected for the purpose by the Controller General of Defence Accounts. The officers selected for setting the question papers will send the question papers to the Controller General of Defence Accounts, who in turn will send them to the Controller of Defence Accounts (Training) or to the Controller of Defence Accounts to whose office the probationers are attached, for holding the examination on the dates fixed therefore. The names of the examiners will be simultaneously notified to the Controller of Defence Accounts (Training) or to the Controller of Defence Accounts to whose office the probationers are attached, to enable him to forward the answer books of the probationers to the examiners direct. The examiners will forward the answer book to the Controller General of Defence Accounts with a statement showing the marks allotted to each probationer and a report on the degree of efficiency or otherwise attained by him/her on the subject and his/her general aptitude for the discharge of duties of the Department. The Controller General of Defence Accounts will then decide whether or not a probationer has passed the examination. After a probationer has been declared as having passed the departmental examination, he/she will be kept on probation during which he/she will be tried on the regular duties of the department.

Methodex Cards

25 Service details of all serving IDAS officers giving details regarding their date of birth, date of Appointment, dates of promotion to various grades/various assignments held and training courses undergone, GPF Account No., Permanent Address etc., will be maintained in Methodex Cards and it will be ensured that the up-to-date details are recorded in the cards. The relevant Methodex Cards should be put up along with any proposal relating to IDAS officers. With the advent of EDP, the cards will be prepared in O.A. system.

Accounts Officers and Senior Accounts Officers

Appointment

26. The total number of posts of Accounts Officers and Senior Accounts Officers in the Department, both in Group ‘B’’ are distributed in the ratio of 20:80. Appointment/promotion to the posts of Accounts Officers and Senior Accounts Officers are made as described below:

(i) Accounts Officers

The number of vacancies of Accounts Officers due to arise during the next financial year is computed and based on this data and other relevant factors, Assistant Accounts Officers who have completed four years’ regular service in that grade on the crucial date are considered for promotion by a Departmental Promotion Committee consisting of (a) CGDA/Senior most Additional CGDA; (b) Additional CGDA; (c) Joint CGDA (Admin); (d) Two Controllers of Defence Accounts. The vacancies are filled by ‘selection’ method. The select lists drawn up by the Departmental Promotion Committee, after approval by the CGDA is followed for making promotion of Assistant Accounts Officers to the grade of Accounts Officer as and when vacancies occur, provided the work and conduct of the selected Assistant Accounts Officer have remained satisfactory.

23

Copies of office orders notifying such promotions made by Pr. CsDA/ CsDA as ordered by the CGDA should be sent to him for notification of the appointment in the Gazette of India.

(ii) Senior Accounts Officers

These posts are filled by appointment of Accounts Officers of the Department, failing which by transfer on deputation. Accounts Officers who have completed three years’ regular service in the Department on the crucial date are considered for appointment to the Senior Accounts Officer’s grade by a Departmental Promotion Committee consisting of: (a) CGDA/Senior most Additional CGDA; (b) Additional CGDA; (c) Joint CGDA(Admin); (d) Two Controllers of Defence Accounts The promotions are made by ‘non-selection’ method.

27 All casualties except posting transfer and leave relating to Gazetted Officer are notified in the Gazette of India by the C.G.D.A.

Increments

28. An increment shall ordinarily be drawn as a matter of course unless it is withheld by the authority competent to withhold such increment in accordance with the relevant provisions of CCS (CC&A) Rules.

Leave

29. Leave of Accounts Officers will be dealt with by the Controllers, after admissibility of leave has been certified by the Audit Officer concerned. Controllers will issue a consolidated Part II Office Order on the first of each month showing the names of Accounts Officers who were granted leave during the previous months and other necessary details. These Part II Office Orders will contain a certificate regarding continuation of officiating appointment during the period of leave and copies thereof will be endorsed to the Audit Officer concerned amongst others.

Methodex Cards

30. Service Cards (Methodex Cards) are maintained in respect of all Accounts Officers. These Cards show important details, i.e. date of birth, date of joining the department, date of passing SAS, date of Promotion to AO’s grade, date of promotion to the SAO’s grade, qualifications, stations where served earlier etc., details of deputation are also shown. The Service Cards are maintained up-to-date with reference to the various casualties intimated by the Controllers. These Cards will be put up along with any case relating to the officer.

Confidential Reports

31. Principal CDA/CDA is the accepting authority for the confidential reports of all Accounts Officers and Senior Accounts Officers. Principal Controllers/Controllers are required to forward all the Confidential Reports of all Accounts Officers and Senior Accounts Officers serving in their organization including those held on the proforma

24

strength so as to reach the CGDA’s office by 30th April of each year. Principal Controllers/Controllers are required to communicate adverse remarks, if any, contained in the Confidential Reports to the Accounts Officers and Senior Accounts Officers. Representations against the adverse remarks along with the comments are submitted to the office of the CGDA for the competent authority to consider representations against the adverse remarks contained in the confidential reports. In respect of the Accounts Officers and Senior Accounts Officers serving in the office of the CGDA will be written by the officers under whom they are serving and accepted and reviewed as per extant orders.

Deputation

32. In order to deal with the requests of the borrowing Departments for the services of Senior Accounts Officers and Accounts Officers of Defence Accounts Department for appointment on deputation, the Controllers are requested to furnish the names of all volunteers so that a panel is prepared of all available eligible Senior Accounts Officers / Accounts Officers for sponsoring suitable names on deputation to the borrowing Department. Where, however, there are specific requirement from borrowing organizations, not adequately covered by the panel, action will be taken to call for suitable volunteers from the Controllers. On receipt of the selection of the names of the Senior Accounts Officers / Accounts Officers from the borrowing department, orders will issued to the Controllers, for relief of the officer concerned. A separate list is maintained to watch the period of deputation and to take suitable action either to deal with the request for extension of period of deputation or to take the action for the reversion of the officer by the due dates.

Note: - With a view to avoid delay in obtaining and sponsoring suitable names for deputation, a print out will be obtained from the computerized data showing the personal details of all the officers who fulfill all the requirements. These particulars will be utilized to select suitable persons expeditiously. General Roster of Senior Accounts Officers and Accounts Officers

33. A Roster of Senior Accounts Officers and Accounts Officers of the Defence Accounts Department is prepared once in three years showing the position as on 31st December of the concerned year. Cyclostyled/Printed copies of the Roster are distributed to the various Controllers who are asked to check the particulars given therein in respect of the Senior Accounts Officers and Accounts Officers serving under them and intimate corrections if any. Corrections where necessary, are carried out in the Roster and the working copy of the Roster should be kept corrected up-to-date. The Roster number will remain unchanged during the period of 3 years.

Subordinate Accounts Service

Appointment

34. The normal method of appointment to the Subordinate Accounts Service will be by promotion of those who have passed the Subordinate Accounts Service examination and who have been adjudged fit by the Local Promotion Committee held in the Pr. Controllers Office/Controllers Officer/C.G.D.A’s office. Immediately after publication of results of Pt. II of the subordinate Accounts Service examination, the Controllers will furnish, in the form prescribed for the purpose, the information necessary for fixing the seniority in

25

respect of those who have passed the examination. Seniority of SOs (A) will be fixed according to the dates of their passing the subordinate Accounts service examination. The relative seniority in the Roster of SOs (A) as between individuals passing in the same examination will be determined with reference to date of confirmation in the Auditor’s Grade or if their dates are the same, with reference to their dates of appointment in the clerical cadre and if their dates happen to be the same again with reference to their dates of birth, the older in age being treated as senior.

In the interest of service, the C.G.D.A. may make direct appointments to the subordinate Accounts Services of Persons with higher educational qualifications. The conditions relating to such appointments are governed by orders issued by the Government and C.G.D.A from time to time Paras 94-96 of OM Part I, 1979 edition refer in this connection.

As promotions to SOs (A) Grade are centrally controlled in CGDAs office with reference to the vacancies arising from time to time, a Register called ‘Vacancy Register’ will be maintained separately. Based on the information furnished by the Pr. CsDA/CsDA through their monthly reports the vacancy register will be completed and the total available vacancies will be worked out. Necessary orders in regard to the promotion/confirmation will be issued after they have been approved by the Controller General of Defence Accounts.

Promotion

35. Immediately after the publication of the results of SAS Part II examination, the Pr. Controllers / controllers will furnish in the prescribed form the information necessary for fixing the seniority in respect of clerical staff of their organization, who have passed the examination. Pr. Controllers / Controllers would indicate specifically the recommendations of the Local Promotion Committee regarding the suitability in respect of each individual for promotion to the officiating grade of Section Officer. On receipt of the statements in this office they will be scrutinized. The names of the individuals will be arranged in order of relative seniority and the orders of the CGDA in regard to their promotion to the officiating grade of SOs (A) will be obtained and indicated to the Pr. Controllers / Controllers concerned for notification.

Probation

36. According to the existing procedure officiating Section Officers (Accounts) will remain on probation for a period of two years. They will be considered for retention in that grade after the successful completion of probationary period. For this purpose the Local Promotion Committee will adjudicate each case to determine the fitness or otherwise retention in the promoted grade, based on the Assessment Reports of the individuals. Cases of extension of probation beyond four years will be referred to the Controller General of Defence Accounts office for orders.

Reservation of Vacancies

37. Vacancies to the extent prescribed by the Government will be reserved for the SC/ST communities. For this purpose, a separate Roster called 200 Point Roster will be maintained in which the vacancies will be worked out. In the event of non-availability of

26

candidates belonging to the reserved communities the sanction of the Department of Personnel and Training will be obtained to get the vacancies de-reserved.

27

Assistant Accounts Officers and Section Officers (A)

38. 80% of the authorized strength of the Section Officer (Accounts) are placed in the higher grade/pay scale of Assistant Accounts Officers (Group “B” Gazetted) and the remaining 20% in the lower grade/scale of Section Officers (Accounts) (Group “C” Non-gazetted). Section Officers (Accounts) with three years service in the grade on the crucial date are considered for promotion to the grade of Assistant Accounts Officers. 90% of posts of Section Officer (Accounts) are filled by promotion of those who pass the SAS Part II examination. The remaining 10% of posts are named as Supervisor (Accounts) are filled by promotion of those who qualify the Supervisor (Accounts) examination as per extant recruitment rules.

Confidential Reports

39. Confidential reports of Assistant Accounts Officers up to a specified Roster number will be called for by the CGDA and will be furnished by the Pr. Controllers/Controllers by the stipulated date.

General Roster of Assistant Accounts Officers and SOs (A) of subordinate Accounts Service

40. Roster of Assistant Accounts Officers and SOs (A) of the Subordinate Accounts Service of the Defence Accounts Department is prepared once in a five years and kept corrected upto and inclusive of 31st December. Cyclostyled/printed copies of the Roster are distributed to the various controllers who are asked to check the particulars given therein in respect of the Assistant Accounts Officers and SOs (A) serving under them and intimate any corrections that may be found necessary. On receipt of reply corrections wherever necessary are carried out in the Roster and it is seen that no item thereof has been left unchecked. The working copy of the Roster should be kept corrected upto date. For example, the Roster prepared in December 2003 will be valid upto 2008 and the Roster numbers will remain unchanged during this period.

Clerical Service

Senior Auditors

41. 80% of the total authorized strength of the Auditors are placed in the higher grade/pay 1scale of Senior Auditors and the remaining 20% in the lower grade/pay scale of Auditors. Auditors with three years service in that grade and who have successfully completed probation wherever prescribed will be eligible for consideration for appointment to the grade of Senior Auditor by the DPC. The appointment will be on seniority basis subject to the rejection of the unfit.

Auditor and Clerks

Recruitment

42. The work of direct recruitment of Auditors/Clerks to the Defence Accounts Department has been entrusted to the Staff Selection Commission New Delhi. Pr. Controllers / Controllers have been empowered to intimate the vacancies on account of

28

Direct Recruitment periodically to the Staff Selection Commission. The Staff Selection Commission will furnish to the Pr. Controllers/Controllers the details of selected persons on the basis of the examination held. Appointment letters will be issued by the Pr. Controllers / Controllers.

Promotion & Confirmation

43. The promotion from clerks to auditor’s grade is dealt with by Pr. Controllers/Controllers/CGDA. At present 50% of the vacancies in the Auditor’s grade will be filled from the grade of clerks according to seniority-cum-fitness. Clerks /DEOs who have passed Part I of SAS examination are promoted out-of-turn to the grade of auditors All promotions to the officiating grade and confirmation thereof in the above posts will be made on the recommendation of the Local Promotion Committee convened in the Pr. Controllers/Controllers offices and accepted by the Pr. Controller/Controllers. Pr. Controllers/Controllers will be periodically directed to consider the name of those individuals who come within the zone of Promotion/Confirmation. The Committee shall consist of CDA/Addl.CDA and two other senior officers of the office, and presided over by the CDA/Addl.CDA. Keeping in view the criteria prescribed by the CGDA for recommending the names the Pr. Controller/Controller will endorse on the recommendations of the LPC and forward the same to this office. In cases of individuals whose names are not adjudicated fit for promotion/confirmation, full details giving reasons will be furnished by the Controllers.

Promotion in Group‘C’ i.e. to the post of Record Clerk, Clerk, Auditor, Senior Auditor, Supervisor ( Accounts) , Section Officer ( Accounts) Sr. Hindi Translator, DEO ‘B’ ‘C’ ‘D’, Stenographer –Gd-I, II and in Group ‘B’ i.e. to the post of PS, Sr. PS, Hindi Officer, AAO are made by the office of the C.G.D.A on the recommendations of the Local Promotion Committee (LPC) convened in the Pr. Controllers/Controllers office and by AN Section in the office of the CGDA in respect of staff serving in this office. After approval, Pr. Controllers/Controllers are informed of the names of persons approved for promotion and the date from which promotion is effective. They are responsible to issue Pt.II office orders, in this regard after ensuring that no disciplinary case is pending against him and nothing adverse has since come to notice. The Pr. Controller/Controllers will furnish a certificate to the CGDA’s office confirming that Pt.II O.Os have been published in respect of the persons whose confirmation/ promotion have been approved by the CGDA.

A register of vacancies in which vacancies occurring in each grade by normal wastages ie discharge, dismissal, death, retirement is maintained in the office of CGDA. The relevant data to complete the register are collected from CGDA’s office by the Controllers. All the vacancies are pooled and promotion and confirmation thereto are proposed periodically depending on the available vacancies

Stenographers

44. There are the six grades of stenographers as indicated below:

(i) Stenographer – Grade III (Group “C” non-gazetted) (ii) Stenographer – Grade II (Group “C” non-gazetted)

29

(iii) Stenographer – Grade I (Group “C” non-gazetted) (iv) Personal Secretary (Group “B” gazetted) (v) Senior Personal Secretary (Group “B” Gazetted)(vi) Principal Personal Secretary (Group “A” Gazetted)

Posts of stenographers are filled up by direct recruitment/promotion in accordance with the extant Recruitment Rules.

Record Clerks

45. Records Clerk who have rendered service of not less than three years in the grade and have passed the prescribed departmental test and adjudicated fit are promoted to the clerks grade against 10% of the vacancies in order of their seniority. 10% of the remaining posts are filled by recruitment from the educationally qualified group ‘D’ employees subject to the following conditions:

(i) Selection will be made through a departmental examination confined to Group ‘D’ employees who fulfill the requirement of minimum educational qualification.(ii) Maximum age limit for admission to this examination will be 45 years (50 years for Scheduled Castes/Scheduled Tribes candidates).

Promotion from Group ‘D’ staff to Record Clerks

46. Educationally qualified Peon and Daftries who have rendered a minimum of five years service and have qualified in a departmental examination to judge their suitability for the post of Record Clerks are considered for promotion to these posts in order of seniority according to vacancies as and when available. Permanency in Group ‘D’ Staff

47. Permanency in the grade of Peons Farashes, Chowkidars, Sweepers, Water Carriers and Mali etc. will be done by the Pr. Controller/ controllers concerned and by AN Section in respect of the staff working in the CGDA’s office.

Demand for Establishment

48. The clerical and supervisory establishment required for Pr. Controller’s/Controller’s offices is determined with reference to the demands submitted by them on the basis of the volume of work in their offices and sub-offices. On receipt in the office of the CGDA, these demand are checked with reference to the prescribed scale and the quantum of work shown therein and necessary sanctions for establishment are accorded taking into account the total ceiling strength sanctioned by the Government for the Department as a whole Requirement of staff over and above the ceiling strength of the Department is submitted to the Ministry of Defence (Finance) for sanction.

Transfers of Volunteers

49. Applications for transfer from Group ‘C’ and ‘D’ staff outside the command are considered in the office of the CGDA on the recommendation of the Pr. Controllers/Controllers concerned and those for transfer to station within the Pr. Controllers/Controllers own jurisdiction are dealt with by the respective Pr.

30

Controller/Controllers. The names of applicants for transfer are forwarded by the Pr. Controllers/ Controllers through Volunteers Lists submitted in the month of Oct/ Nov. every year. On the basis of lists received from the controllers, AN- IX and AN-X sections prepare station wise and grade-wise consolidated lists of volunteers. The names of volunteers for transfers are arranged as per stay away seniority in the consolidated lists, which contain the full service particulars of the individuals including the grounds on which the individuals have sought for transfer. These lists contain the particulars of the applicants who applied for transfer to the stations of their choice during the last one-year. These lists are updated and submitted to the DCGDA (AN)/Sr. DCGDA (AN) as and when required. Each case will be considered on its merits and with due regard to the length of service of the individual at the present duty station/outside his home state.

In all cases of transfer TA or joining time will be admissible only in case the applicant has completed three year stay on the present station save in exceptional deserving cases/ tenure cases. In case where no TA/Joining time is granted for the move, the period of transit from the previous office to the new office of posting should be covered by the grant of earned leave or any other leave (except Casual or compensatory leave) at the credit of the individual.

Transfer on Mutual Exchange Basis

50. In the case of requests for inter-Command transfers on mutual exchange basis, the applications are received along with the recommendations of both the Pr. CsDA/CsDA concerned and the consent Note of the individual who is willing to be transferred in place of the individual who seeks transfer. The Pr. CsDA/CDA concerned will initially examine the request keeping in view the following guidelines issued in this regard by the office of the CGDA.

(a) An individual should have a minimum period of stay say 2 years at the present station;

(b) The inter-change is between staff of equal status;(c) Transfer between staff

(i) in the same station or (ii) two nearby stations or (iii) very popular stations are not accepted.

(d) The transfer does not involve move from one vulnerable post to another; say, from one AAO GE’s office to another AAO GE’s office.

On receipt of such requests in the office of the CGDA the cases will be examined on the basis of the recommendations of the Pr.CsDA/CsDA concerned as well as the guidelines indicated above.

Transfers to and from the office of the CGDA

51. Transfer of AAOs and Group ‘C’ staff between the CGDA’s office and other offices of the Department and vice versa are effected under the orders of the C.G.D.A. Pr. Controllers/Controllers of Defence Accounts are periodically asked to sponsor suitable names of AAOs/SOs(A)/ SAs/Auditors/Clerks with particulars of service and experience.

31

A panel Register of AAOs/SOs(A)/SAs/Auditors/Clerks who fulfill the criteria for posting to CGDA’s office and are recommended as fit for posting to CGDA’s office is maintained separately for AAOs/SOs(A)/SAs/Auditors/Clerks. Selection of AAOs/SOs(A)/SAs/ Auditors/Clerks is made from among the individuals included in the panel Selection of stenographers is made from among the suitable names recommended by the Pr. CsDA/CsDA as and when called for.

The tenure of staff in CGDA’s office is 5 years. The individuals who complete the prescribed period of 5 years of their service in the office of the CGDA as on 30th April each year are gradually transferred to other offices of the Department and are replaced by the selected individuals from other offices as indicated above. Individuals who have not completed 5 years may also be transferred out of CGDA’s office.

Transfers on administrative grounds

52. Transfer of staff from one Command to another on administrative ground will also be effected by the C.G.D.A’s office. Posting of Individuals on promotion to the grade of officiating SOs(A)

53. The service particulars of the clerical staff declared successful in the SAS Part II Examination together with the vacancy position of SOs (A) are called for from the Pr. CsDA / CsDA immediately after the results are announced. On receipt of the requisite information from the Pr. CsDA/CsDA necessary statistics regarding the availability of vacancies etc., are prepared. Based on the vacancy position, the persons adjudicated fit are posted to various offices of the Pr. Controllers/Controllers organization in conformity with policy formulated in this regard. Deputation of Group ‘B’ & ‘C’ staff to other Ministries/Departments/Public undertaking/Autonomous Bodies etc.

54. (i) Requisitions for sponsoring suitable names of Group ‘B’ & ‘C’ staff for deputation are received in the CGDA’s office from various Ministries/Departments/Public undertaking/Autonomous Bodies etc. In the case of Assistant Accounts Officers and Section Officer (Accounts) a Deputation Panel Register is maintained for the purpose and Principal Controllers/Controllers of Defence Accounts are periodically asked to sponsor names of suitable AAOs/SOs (A) from among the volunteers for deputation to various Ministries/Departments etc. for sponsoring them for deputation as and when requisitions are received from the borrowing Departments. On receipt of the lists of volunteers from all PCsDA/CsDA these names together with their service particulars, experience etc. are entered according to their Roster Seniority, in the Panel Register. On receipt of the requisitions from the borrowing Departments suitable names of AAOs/SOs(A) are selected from the panel and forwarded to the borrowing Departments along with the copies of their ACRs for the last three years and other particulars as called for. (ii) If, however, no suitable names are available in the panel, PCsDA/CsDA will be requested to sponsor suitable names as per the particular requirement of the borrowing Department. On receipt of such names, suitable names will be selected there from and forwarded to the borrowing Department as indicated above.

32

(iii) In the case of deputation of SAs, Auditors and Clerks, as and when requisitions are received from Borrowing Departments, PCsDA/CsDA will be asked to sponsor suitable names of individuals for deputation as per the requirement of the borrowing Departments. On receipt of such names, suitable names will be selected therefrom and forwarded to the borrowing Departments as indicated at para (i) above. (iv) On receipt of intimation from the borrowing Department regarding selection of individuals for deputation necessary orders in this regard will be issued by the CGDA to the PCsDA/CsDA concerned. In order to ensure that the staff sent on deputation to various Departments etc. are reverted to DAD on due dates, a separate deputation Register indicating the date of their relief in the parent Department, initial period of deputation, extensions granted etc. is also mentioned. On receipt of intimation regarding reversion of staff from deputation, necessary orders of their posting on reversion to DAD are issued by the CGDA’s office taking into account the availability of vacancies etc.

Applications from staff for re-employment after retirement from service

55. Applications received from members of staff seeking re-employment after their retirement on Superannuation etc., are noted in a Register maintained for\the purpose, for sponsoring the names if and when requisitions for such services are received in the office of the CGDA. Application specifically addressed to other Department/Organization etc. seeking re-employment is forwarded to such addressees along with the service particulars of the individual, for consideration.

SAS Examination

56. The frequency of holding Subordinate Accounts Services Examination - Part I and II is decided by the CGDA on need basis. The examination is held in selected centres as per date and programme approved by the CGDA. The rules for the conduct of the examination will also be decided by the CGDA. The subjects and the rules for the conduct of the examinations are laid down in Annexure ‘C’ to Chapter II of OM Part I. (Refer Para 102) and as per new syllabus notified vide Govt. of India, Ministry of Defence (Finance Division) No. F.26(1)/C/2007 dated 8.3.2007.

The criteria and guidelines as decided by the C.G.D.A. for admission of a candidate for the examination will be intimated to the Pr. Controllers/Controllers. On the basis of the criteria and guidelines, a Board of Officer consisting of CDA/Addl. CDA (President), one IDAS officer and one Accounts Officer will scrutinize the candidature of each individual applying for admission to the examination. After necessary screening the names of the candidates (recommended as well as not recommended) will be forwarded to the CGDA in a simple proforma prescribed for the purpose. On receipt of the names of the candidates for admission to the examination, each candidate will be assigned a Roll number. The list of approved candidates showing the Roll number assigned and the Centre, in which he will take the examination etc., will be circulated to all Pr. Controllers/Controllers and the Centres where examination is held for information of the candidates. In respect of names not recommended, the acceptance or rejection of their candidature will be separately communicated to the Pr. Controllers/Controllers concerned.

33

The CGDA will approve the names of Head Examiners for setting Question papers. Each examiner is then informed that he has been selected to set a particular paper and that the paper together with the model answer should be sent to the Joint CGDA (AN) by name. The papers when received are examined by a Committee nominated by the CGDA with a view to see that the questions are strictly in order and in accordance with the prescribed syllabus. They are kept by the Asstt. CGDA (AN)/ Dy. CGDA (AN)/ Sr. Dy CGDA (AN) in his personal custody and arrangement for the printing and distribution are also made by him.

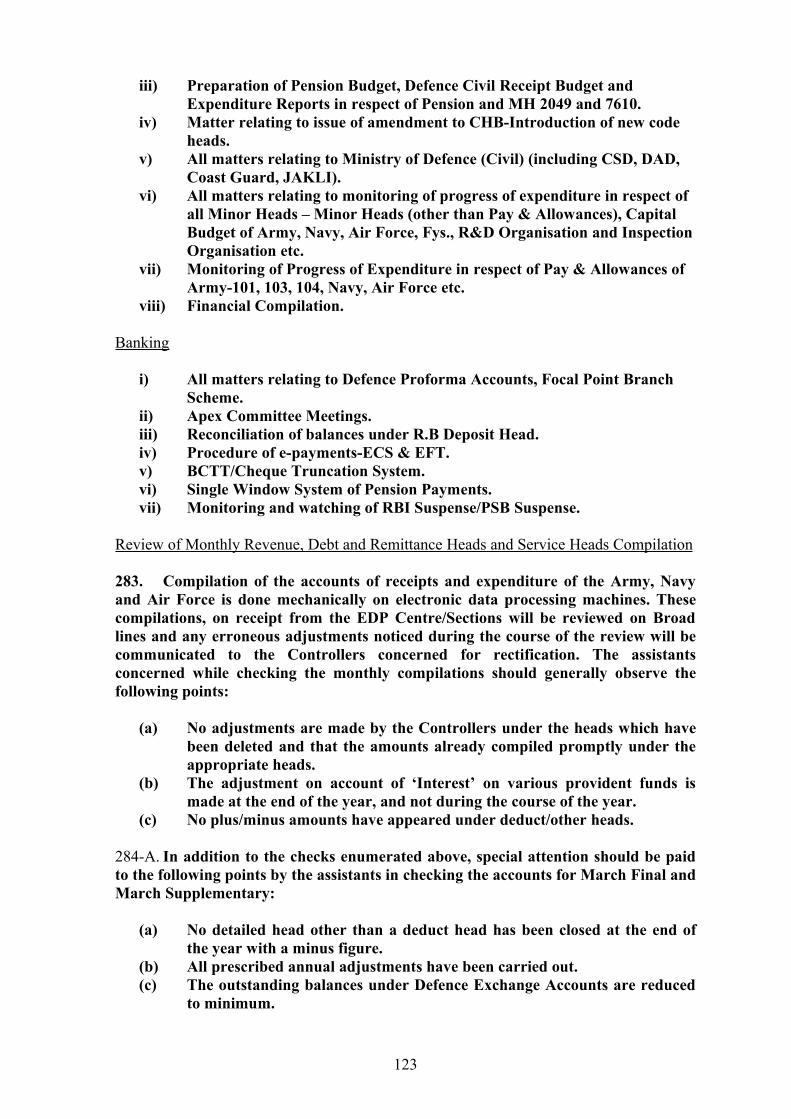

After the examination the answer books are received in CGDA office and evaluation work is done centrally. Each Head examiner is assisted by the Sub- Examiner (s) nominated by the CGDA.

On receipt of the evaluated answer books from the examiners the marks obtained by each candidate in each Subject are entered in a register opened for the purpose. The result is kept strictly confidential, all papers being kept under lock and key until the consolidated result has been approved by the CGDA. After the result is approved by the CGDA, the same will be circulated to all the Pr. Controllers/Controllers of Defence Accounts and the Centre where the examination is conducted to the information of the candidates. The detailed marks secured by the candidates will also be similarly circulated for the information of candidates. The answer papers will be destroyed one year after the last date of the examination. The examiners/ sub- examiner concerned should submit the bills (in triplicate) for the honorarium due to them (less income tax and surcharge) to the CGDA. The bills will be scrutinized in this office with reference to the number of papers valued by the examiners and passed for payment.

Disciplinary Cases Group-‘C’ Staff

57. Controller General of Defence Accounts is the Appointing Authority in respect of Group ‘C’ staff appointed prior to 25.3.67 (except Record Clerks in whose case Pr. Controller/Controllers of Defence Accounts are the Appointing Authorities). He is also competent authority to impose any of the major penalties as enumerated in Rule 11 of the CCS (CC&A) Rules 1965 on the above category of individuals.

Pr. Controller of Defence Accounts/Controllers of Defence Accounts (being disciplinary authorities) are competent to initiate and process the disciplinary cases as for a major penalty upto the stage of inquiry on behalf of CGDA and after receipt of inquiry report if they consider that the case warrant imposition one of the major penalties on the individual, the case will be referred to CGDA’s office with all relevant papers including inquiry officer’s report together with the recommendation of the Pr. CDA/C.D.A for obtaining order of C.G.D.A.

Before the case is submitted to CGDA, it will be examined with a view to see that the disciplinary case has been processed exactly in accordance with the procedure laid down in Rule 14 of the CCS (CC&A) Rules, 1965 and the inquiry report rendered by the Inquiring Authority is in order. After the case has been examined a Note containing a brief history of the case and findings of the Inquiry Officer’s report on each articles of charge framed against the individual will be put up to CGDA for his orders.

34

If CGDA is inclined to accept the findings of the Inquiry Officer’s report, he will record it so on the Note and in case he does not agree with the findings of the Inquiry Officer’s report, he will record his own findings on each Articles of Charge. The Inquiry report along with disagreement note, if any, will be served on the charged official for his representation and final orders will be passed after considering the same. A draft punishment order is put up for approval of CGDA. After approval by him the order is forwarded to the office of the Pr. Controller of Defence Accounts/Controller of Defence Accounts concerned together with a copy of the Inquiry Officer’s report, if any, under a forwarding memo (Confidential and registered) signed by ACGDA (AN)/ Dy. CGDA (AN)/ Sr. Dy. CGDA (AN) for being served on the individual.

Group ‘B’ (Senior Accounts Officers and Accounts Officer)

58. CGDA is also the Appointing Authority in respect of Accounts Officers appointed to that grade on or after 18.6.66 and is competent to impose any of the penalties (minor or major) as specified in Rule 11 of the CCS (CC&A) Rules, 1965 on them.

For initiating disciplinary action against Accounts Officer the proposal is forwarded to this office by Pr. Controller of Defence Accounts/Controllers of Defence Accounts. The proposal is examined and CGDA’s orders taken whether disciplinary proceedings as for a major or minor penalty are to be initiated against the Sr. Accounts Officer/Accounts officer. The Pr. CDA/CDA is then advised to propose draft Articles of charge and statement of Imputations of misconduct or misbehavior and list of witnesses and documents for major penalty or statement of Imputation of Misconduct/misbehavior for minor penalty as the case may be. If the case involves the doubtful integrity of the officer or negligence in the performance of duty resulting in substantial loss to the Government, the case is referred to the Central Vigilance Commission for advice (known as 1st stage advice) before initiating disciplinary action against the officer, if Group- A officer is also involved in the case.

On receipt of the draft Articles of charge together with memorandum from the Pr. CDA/CDA in the case of major penalty or statement of imputations of misconduct/misbehavior together with memo in the case of minor penalty, the same is scrutinized and submitted to CGDA for his approval. After his approval, the fair copy thereof duly signed by him is forwarded to the Pr. CDA/CDA for being served on the Accounts officer with the instruction that the reply from the officer should be obtained within 10 days of receipt of charge sheet and forward to this office with Pr. CDA’s / CDA’s remarks/recommendations. If the officer in his written statement of Defence has pleaded not guilty to the charge/charges or has pleaded guilty to some of the charges unequivocally the case is submitted to CGDA to order for holding an inquiry to enquire into the charges which are not admitted by the officer if the case has been initiated as for a major penalty.

Note: - If the case has been initiated as for a minor penalty holding of inquiry is not mandatory. But on consideration of reply, if any, submitted by the officer, it is proposed to withhold increments of pay with cumulative effect for any period or if the penalty of withholding of increments is likely to effect adversely the amount of pension payable to the officer, an oral inquiry will invariably be held.

While submitting the case to CGDA names of the inquiry officer as also of the Presenting officer are proposed to be approved by CGDA

35

The Inquiry Officer is appointed from IDAS officers either from the same