production outlook and economic forecast - smmt · production outlook and economic forecast ......

TRANSCRIPT

SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED SMMT, the ‘S’ symbol and the ‘Driving the motor

industry’ brandline are trademarks of SMMT Ltd

Production Outlook and Economic Forecast

Yung Tran, Head of Member Services and Business Improvement, SMMT

Robert Baker, Chief Economist, SMMT

Ian Henry, Director, AutoAnalysis

14 February 2013

SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED PAGE 2

• During presentations (10:30 – 11:00) everyone will be muted so that only

the presenters will be heard.

• The presentation will be followed by a Q&A session. Click on the hand

symbol to show that you have a question.

• If you are experiencing any technical problems please call 0207 344

1611 or 07793 773391

SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED PAGE 3

Robert Baker

Chief Economist

SMMT

SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED SMMT, the ‘S’ symbol and the ‘Driving the motor

industry’ brandline are trademarks of SMMT Ltd

It’s recovery, but not as expected and incomplete:

…UK still searching for a sustainable recovery by 2013

• Growth has slumped, remains weak, is disjointed and slow

• Inflation rate eased, but remains sticky, volatile and untamed

• Financial and restructuring strains constrict confidence

• Car markets stable in total variegated in the mix

SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED SMMT, the ‘S’ symbol and the ‘Driving the motor

industry’ brandline are trademarks of SMMT Ltd

UK macroeconomic agenda for 2013:

- Domestic economic growth may reignite slowly;

- Risks of UK fiscal stance; EZ crisis and FX volatility

• Continued slow growth in consumer spending

• Sticky but lower inflation and resilient employment

• Financial and investment confidence still fickle & unsure

• FLS may be successful in easing credit flow and terms

SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED PAGE 6

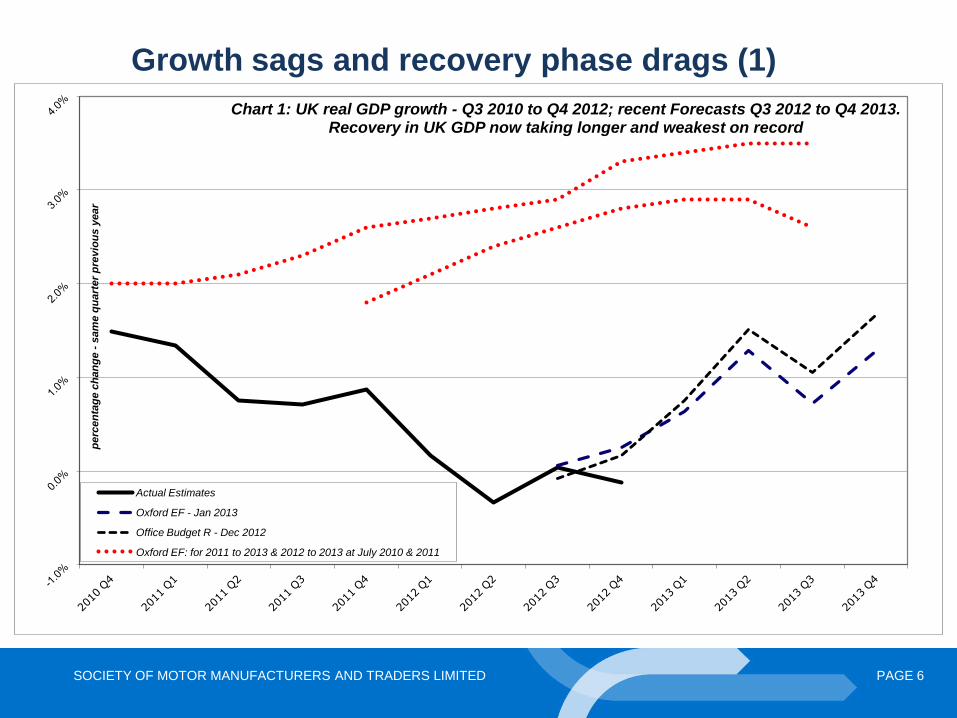

Growth sags and recovery phase drags (1)

pe

rcen

tag

e c

ha

ng

e -

sam

e q

ua

rter

pre

vio

us

year

Chart 1: UK real GDP growth - Q3 2010 to Q4 2012; recent Forecasts Q3 2012 to Q4 2013. Recovery in UK GDP now taking longer and weakest on record

Actual Estimates

Oxford EF - Jan 2013

Office Budget R - Dec 2012

Oxford EF: for 2011 to 2013 & 2012 to 2013 at July 2010 & 2011

SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED PAGE 7

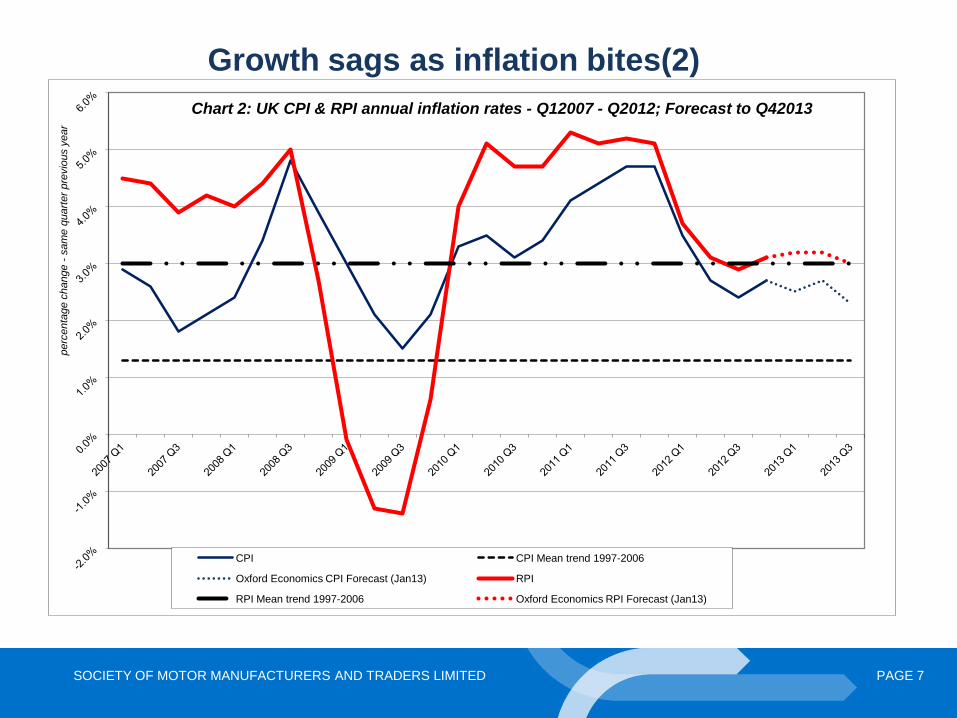

Growth sags as inflation bites(2)

perc

enta

ge c

hange -

sam

e q

uart

er

pre

vio

us y

ear

Chart 2: UK CPI & RPI annual inflation rates - Q12007 - Q2012; Forecast to Q42013

CPI CPI Mean trend 1997-2006

Oxford Economics CPI Forecast (Jan13) RPI

RPI Mean trend 1997-2006 Oxford Economics RPI Forecast (Jan13)

SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED PAGE 8

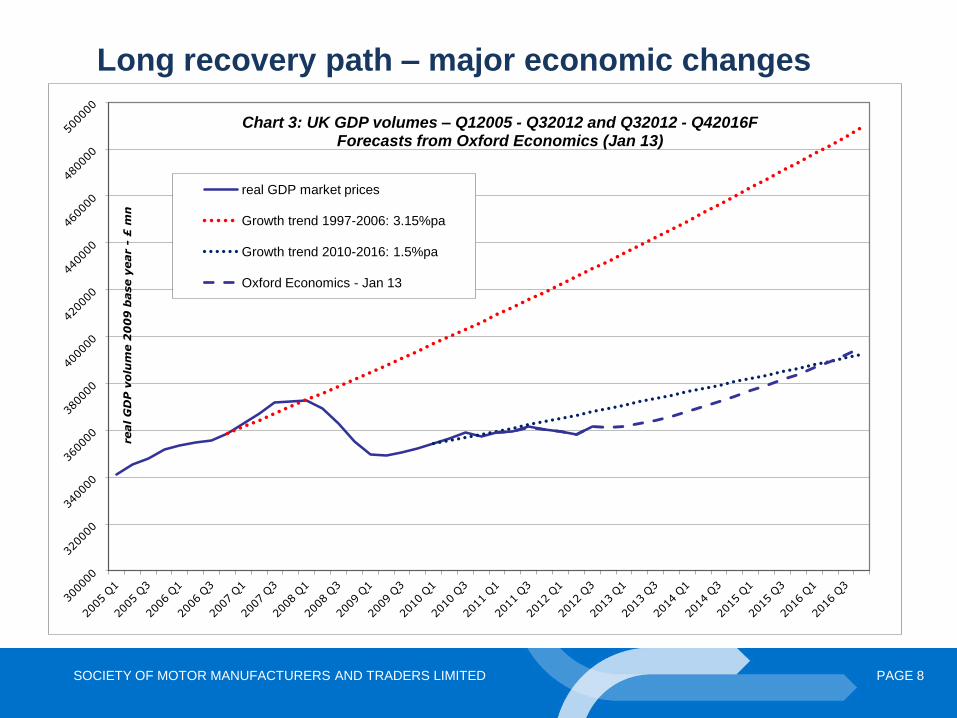

Long recovery path – major economic changes

real G

DP

vo

lum

e 2

00

9 b

ase y

ear -

£ m

n

Chart 3: UK GDP volumes – Q12005 - Q32012 and Q32012 - Q42016F Forecasts from Oxford Economics (Jan 13)

real GDP market prices

Growth trend 1997-2006: 3.15%pa

Growth trend 2010-2016: 1.5%pa

Oxford Economics - Jan 13

SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED PAGE 9

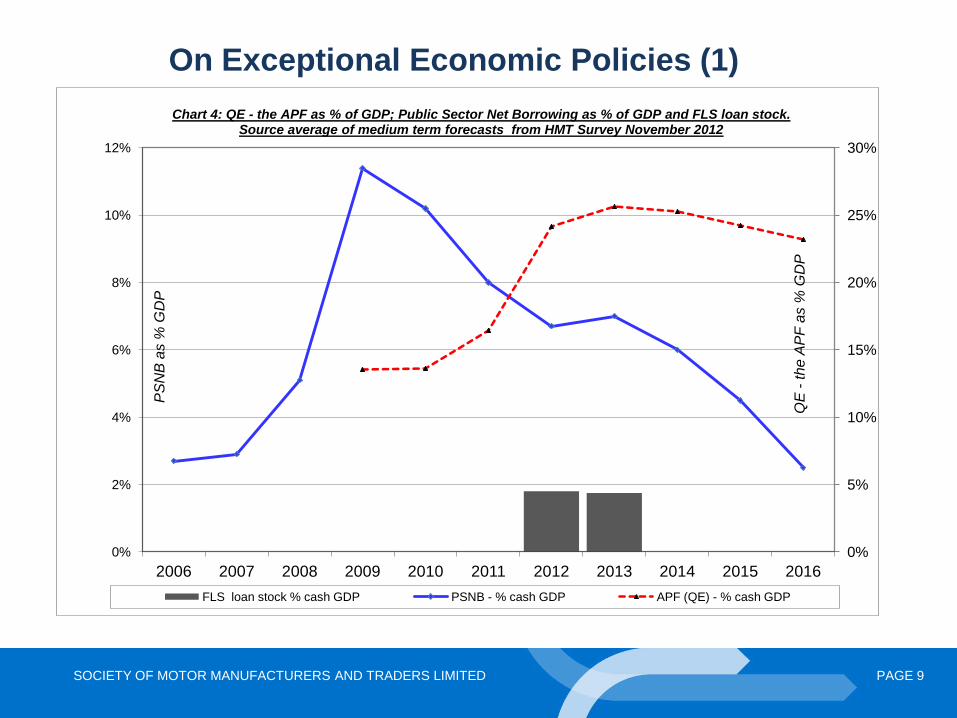

On Exceptional Economic Policies (1)

0%

5%

10%

15%

20%

25%

30%

0%

2%

4%

6%

8%

10%

12%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

QE

- the A

PF

as %

GD

P

PS

NB

as %

GD

P

Chart 4: QE - the APF as % of GDP; Public Sector Net Borrowing as % of GDP and FLS loan stock. Source average of medium term forecasts from HMT Survey November 2012

FLS loan stock % cash GDP PSNB - % cash GDP APF (QE) - % cash GDP

SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED PAGE 10

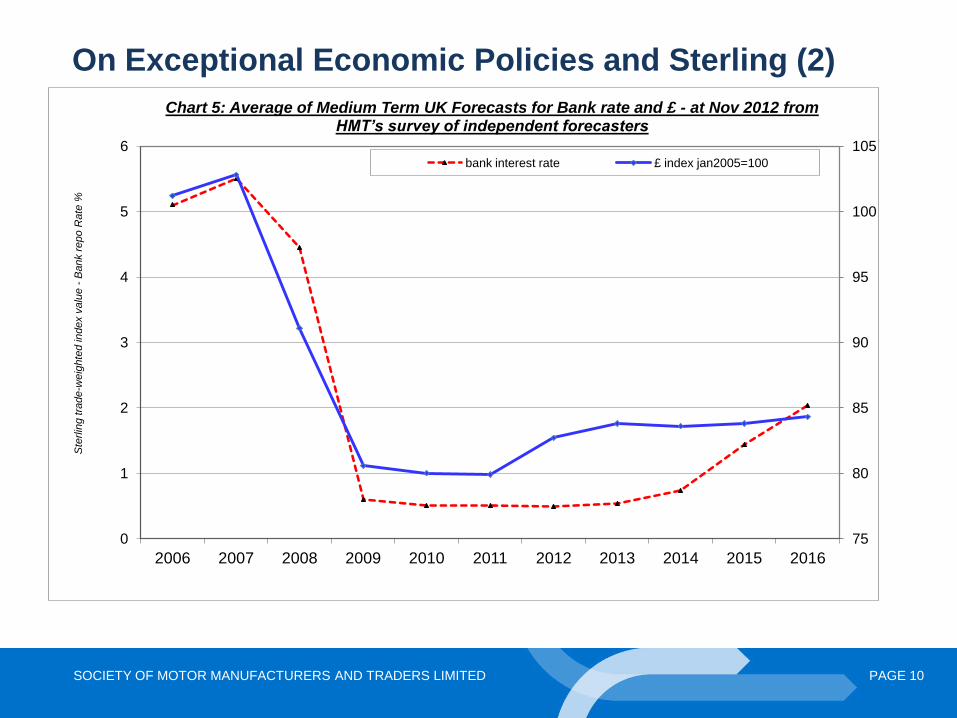

On Exceptional Economic Policies and Sterling (2)

75

80

85

90

95

100

105

0

1

2

3

4

5

6

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Ste

rlin

g tra

de

-weig

hte

d in

dex v

alu

e -

Bank r

epo R

ate

%

Chart 5: Average of Medium Term UK Forecasts for Bank rate and £ - at Nov 2012 from HMT’s survey of independent forecasters

bank interest rate £ index jan2005=100

SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED PAGE 11

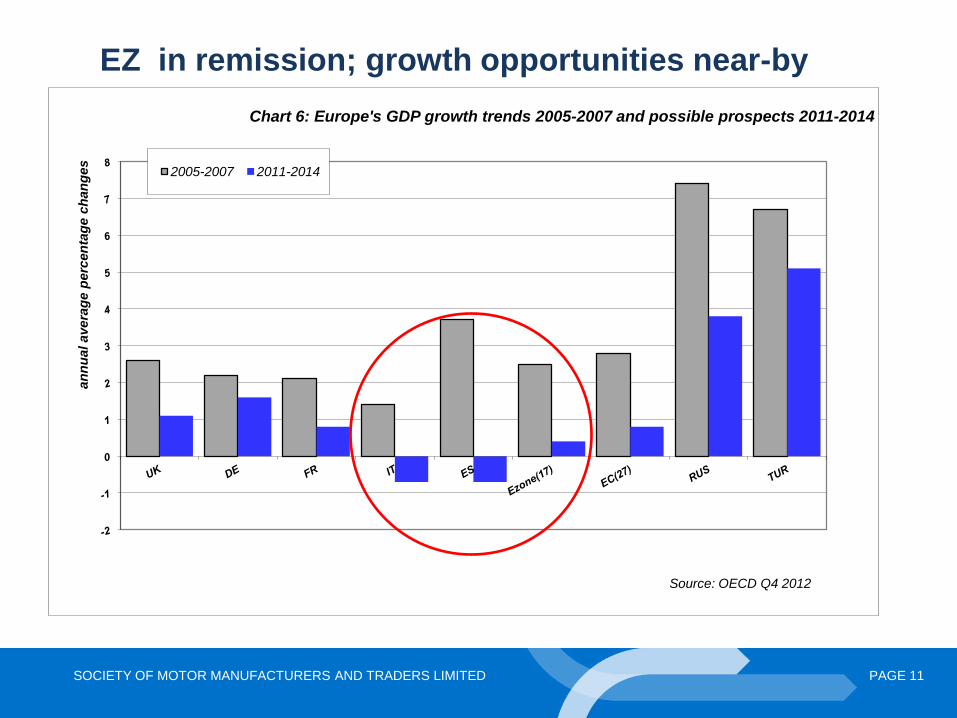

EZ in remission; growth opportunities near-by

an

nu

al avera

ge p

erc

en

tag

e c

han

ges

Chart 6: Europe's GDP growth trends 2005-2007 and possible prospects 2011-2014

2005-2007 2011-2014

Source: OECD Q4 2012

SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED PAGE 12

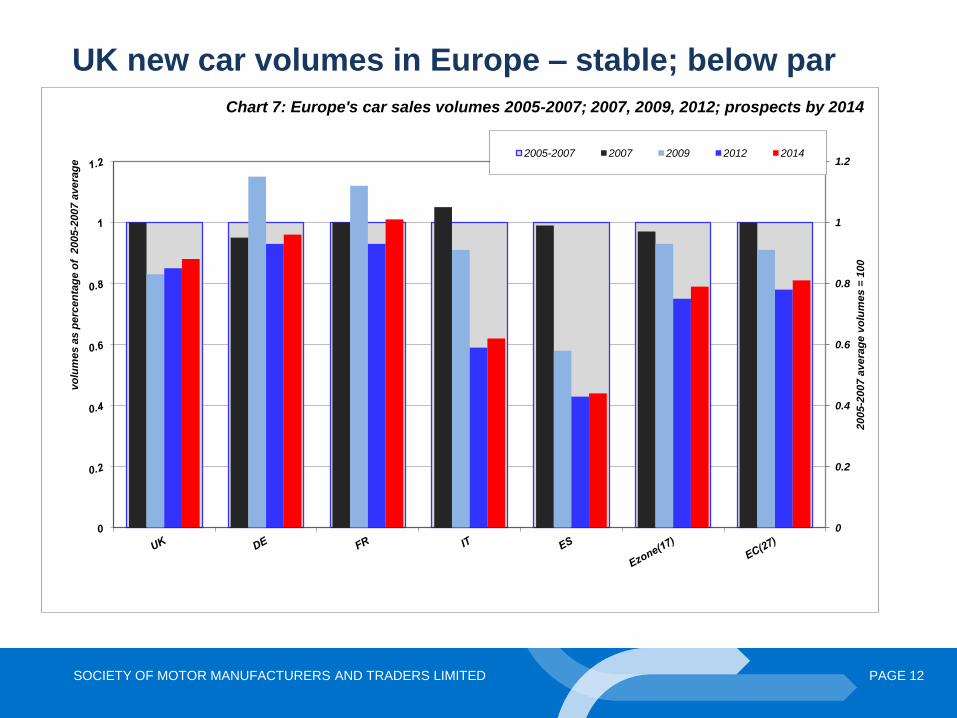

UK new car volumes in Europe – stable; below par

0

0.2

0.4

0.6

0.8

1

1.2

2005-2

007 a

vera

ge

vo

lum

es =

100

vo

lum

es a

s p

erc

en

tag

e o

f 2

005

-2007 a

vera

ge

Chart 7: Europe's car sales volumes 2005-2007; 2007, 2009, 2012; prospects by 2014

2005-2007 2007 2009 2012 2014

SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED PAGE 13

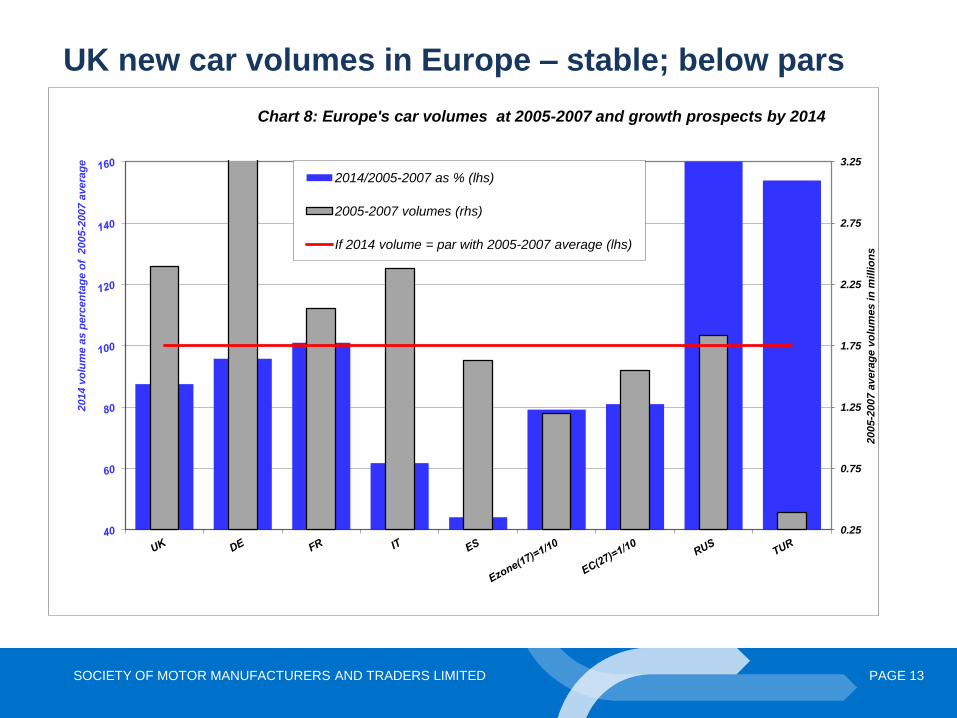

UK new car volumes in Europe – stable; below pars

0.25

0.75

1.25

1.75

2.25

2.75

3.25

2005-2

007 a

vera

ge

vo

lum

es in

millio

ns

2014 v

olu

me a

s p

erc

en

tag

e o

f 2

005

-2007 a

vera

ge

Chart 8: Europe's car volumes at 2005-2007 and growth prospects by 2014

2014/2005-2007 as % (lhs)

2005-2007 volumes (rhs)

If 2014 volume = par with 2005-2007 average (lhs)

SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED PAGE 14

UK’s unique revival in private car demand?

• A timely (low) point on recovery’s route for many habitual new car buyer types and confidence raised

• Postponed buying meant heightened needs to buy new

• Ability to buy as jobs stable, cash & collateral rich; PPI miss-selling payments windfalls (£9.5bn); housing in doldrums

• Willing to replace from earlier buying vintages

• OEMs ready to respond – dire EZ! £/€ attractive Packaged marketing & asset-backed car finance must have helped too

SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED PAGE 15

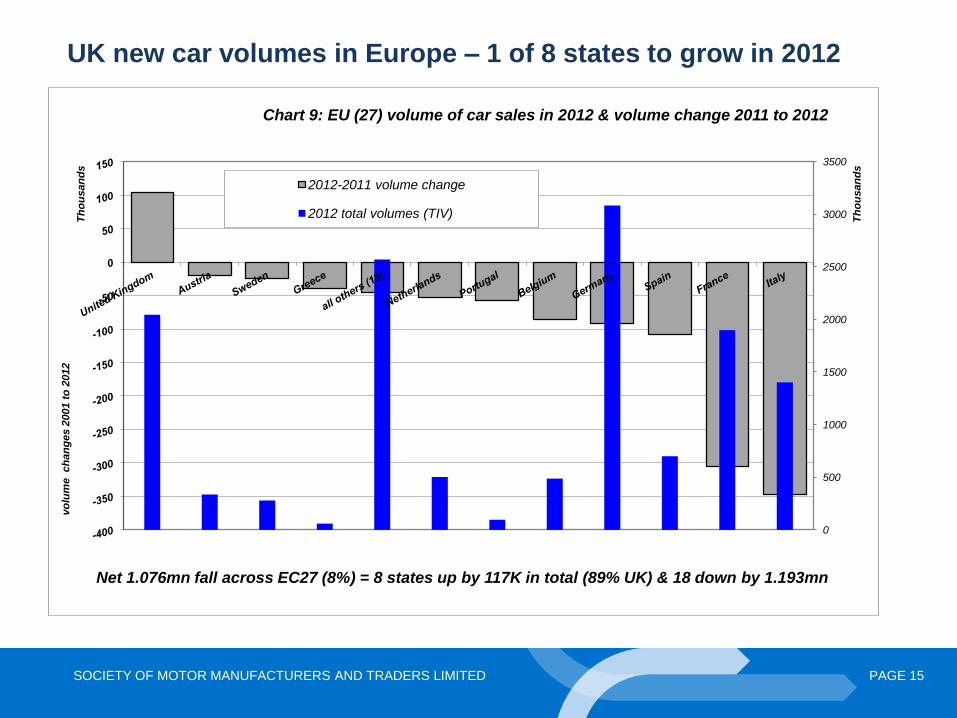

UK new car volumes in Europe – 1 of 8 states to grow in 2012

0

500

1000

1500

2000

2500

3000

3500

Th

ou

san

ds

vo

lum

e ch

an

ges 2

001 t

o 2

012

Th

ou

san

ds

Chart 9: EU (27) volume of car sales in 2012 & volume change 2011 to 2012

2012-2011 volume change

2012 total volumes (TIV)

Net 1.076mn fall across EC27 (8%) = 8 states up by 117K in total (89% UK) & 18 down by 1.193mn

SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED PAGE 16

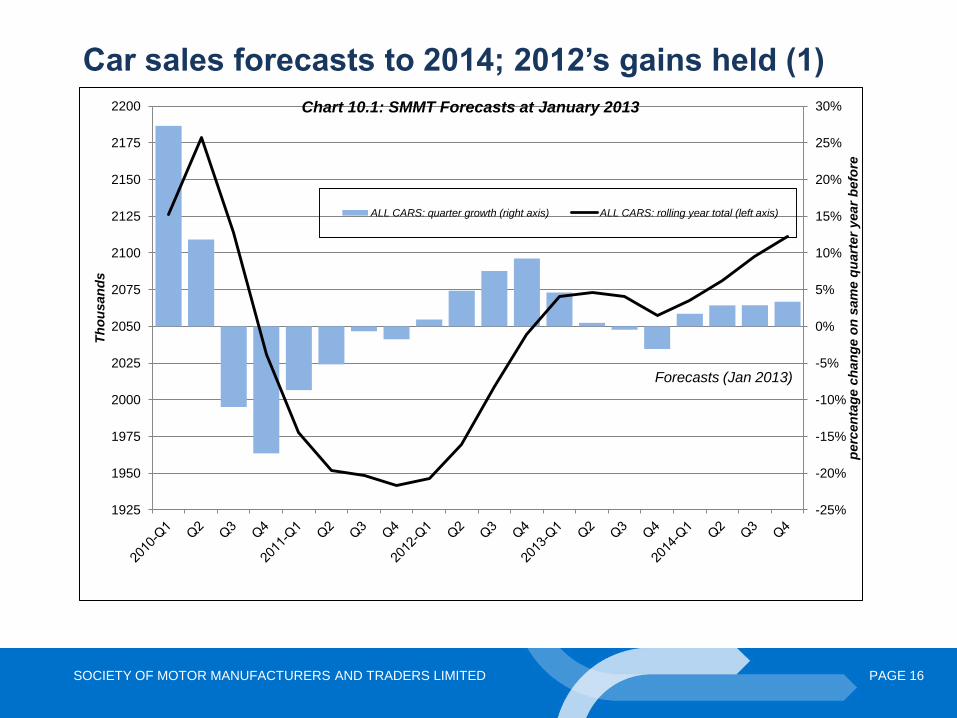

Car sales forecasts to 2014; 2012’s gains held (1)

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

1925

1950

1975

2000

2025

2050

2075

2100

2125

2150

2175

2200

perc

en

tag

e c

han

ge o

n s

am

e q

uart

er

year

befo

re

Th

ou

san

ds

Chart 10.1: SMMT Forecasts at January 2013

ALL CARS: quarter growth (right axis) ALL CARS: rolling year total (left axis)

Forecasts (Jan 2013)

SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED PAGE 17

Private cars forecasts to 2014; 2012’s gains held (2)

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

750

800

850

900

950

1000

1050

1100

1150

perc

en

tag

e c

han

ge o

n s

am

e q

uart

er

year

befo

re

Th

ou

san

ds

Chart 10.2: SMMT forecasts at January 2013

PRIVATE: quarter growth (right axis)

PRIVATE: rolling year total (left axis)

Forecasts (Jan 2013)

SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED PAGE 18

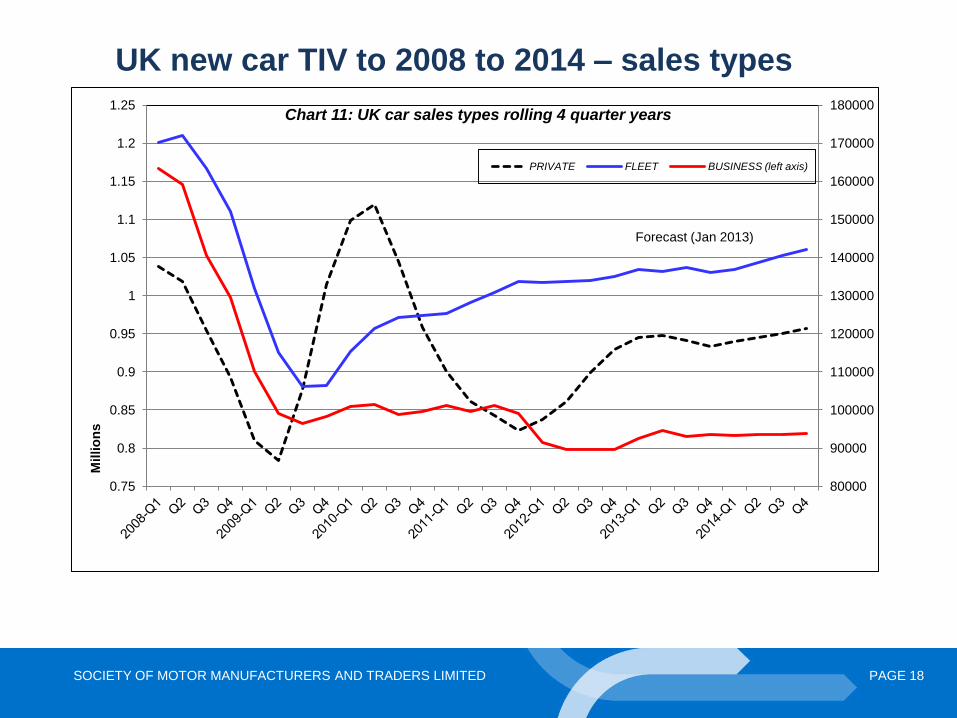

UK new car TIV to 2008 to 2014 – sales types

80000

90000

100000

110000

120000

130000

140000

150000

160000

170000

180000

0.75

0.8

0.85

0.9

0.95

1

1.05

1.1

1.15

1.2

1.25 M

illio

ns

Chart 11: UK car sales types rolling 4 quarter years

PRIVATE FLEET BUSINESS (left axis)

Forecast (Jan 2013)

SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED PAGE 19

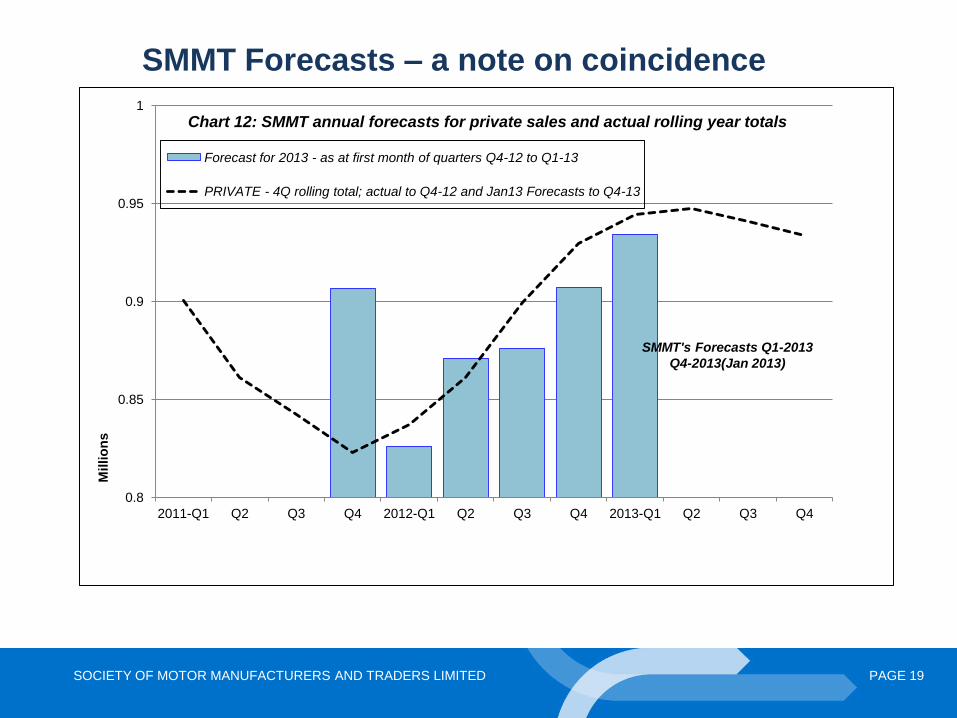

SMMT Forecasts – a note on coincidence

0.8

0.85

0.9

0.95

1

2011-Q1 Q2 Q3 Q4 2012-Q1 Q2 Q3 Q4 2013-Q1 Q2 Q3 Q4

Millio

ns

Chart 12: SMMT annual forecasts for private sales and actual rolling year totals

Forecast for 2013 - as at first month of quarters Q4-12 to Q1-13

PRIVATE - 4Q rolling total; actual to Q4-12 and Jan13 Forecasts to Q4-13

SMMT's Forecasts Q1-2013

Q4-2013(Jan 2013)

SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED PAGE 20

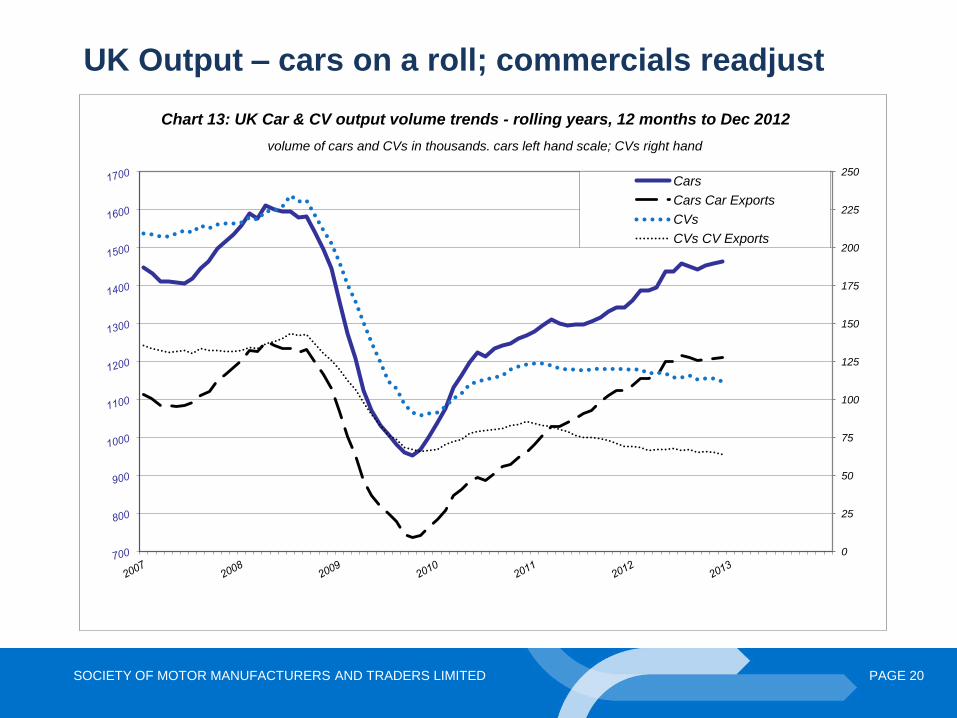

UK Output – cars on a roll; commercials readjust

0

25

50

75

100

125

150

175

200

225

250

Chart 13: UK Car & CV output volume trends - rolling years, 12 months to Dec 2012

Cars

Cars Car Exports

CVs

CVs CV Exports

volume of cars and CVs in thousands. cars left hand scale; CVs right hand

SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED PAGE 21

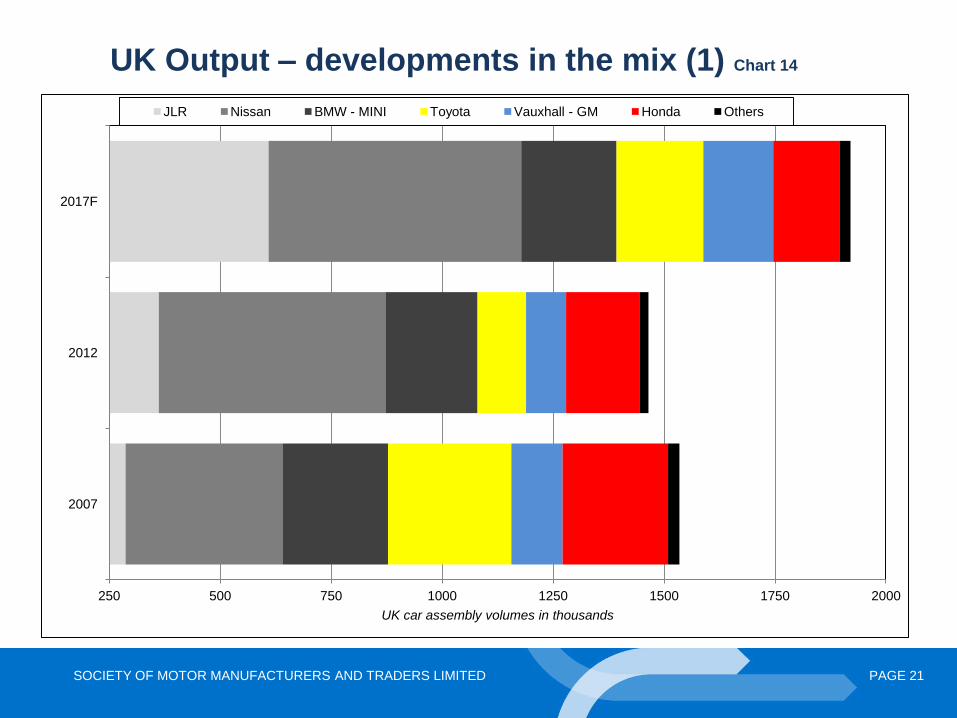

UK Output – developments in the mix (1) Chart 14

250 500 750 1000 1250 1500 1750 2000

2007

2012

2017F

UK car assembly volumes in thousands

JLR Nissan BMW - MINI Toyota Vauxhall - GM Honda Others

SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED PAGE 22

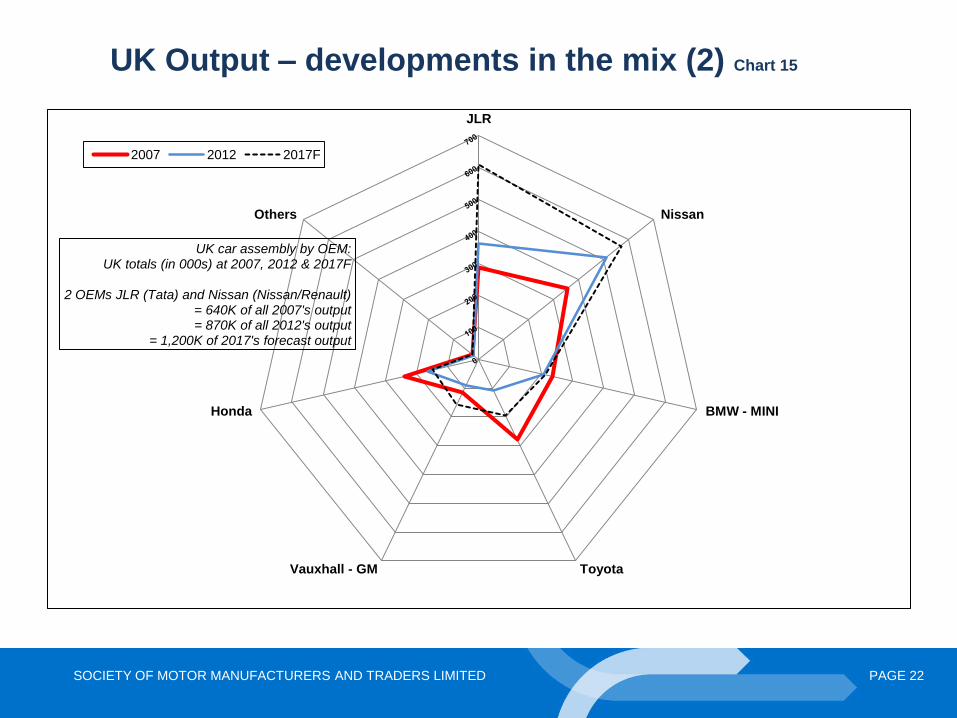

UK Output – developments in the mix (2) Chart 15

JLR

Nissan

BMW - MINI

Toyota Vauxhall - GM

Honda

Others

UK car assembly by OEM: UK totals (in 000s) at 2007, 2012 & 2017F

2 OEMs JLR (Tata) and Nissan (Nissan/Renault)

= 640K of all 2007's output = 870K of all 2012's output

= 1,200K of 2017's forecast output

2007 2012 2017F

SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED PAGE 23

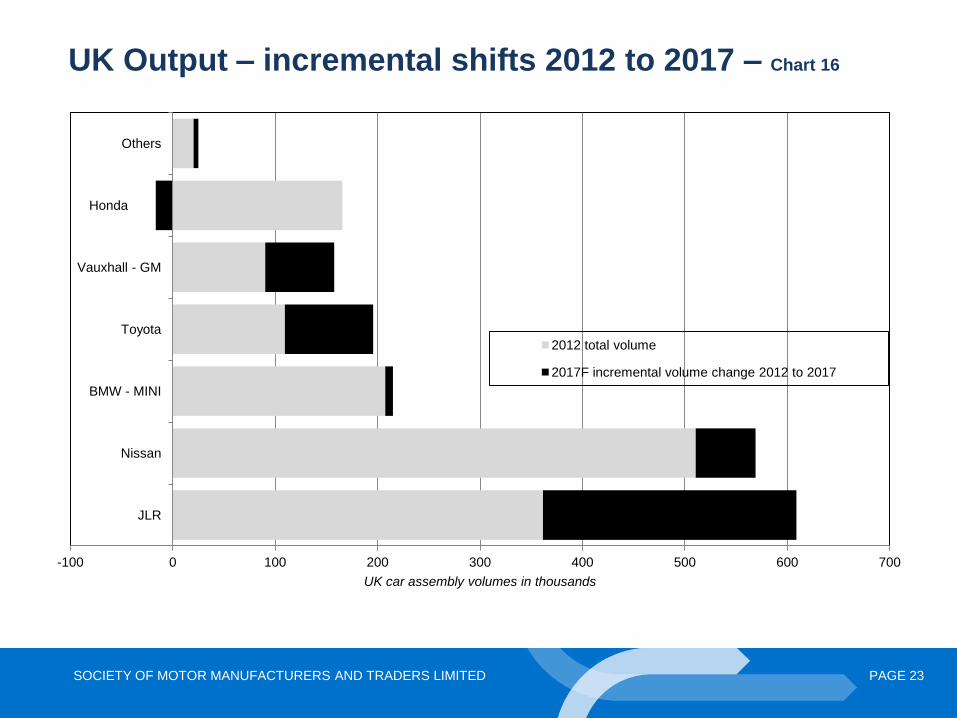

UK Output – incremental shifts 2012 to 2017 – Chart 16

-100 0 100 200 300 400 500 600 700

JLR

Nissan

BMW - MINI

Toyota

Vauxhall - GM

Honda

Others

UK car assembly volumes in thousands

2012 total volume

2017F incremental volume change 2012 to 2017

SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED PAGE 24

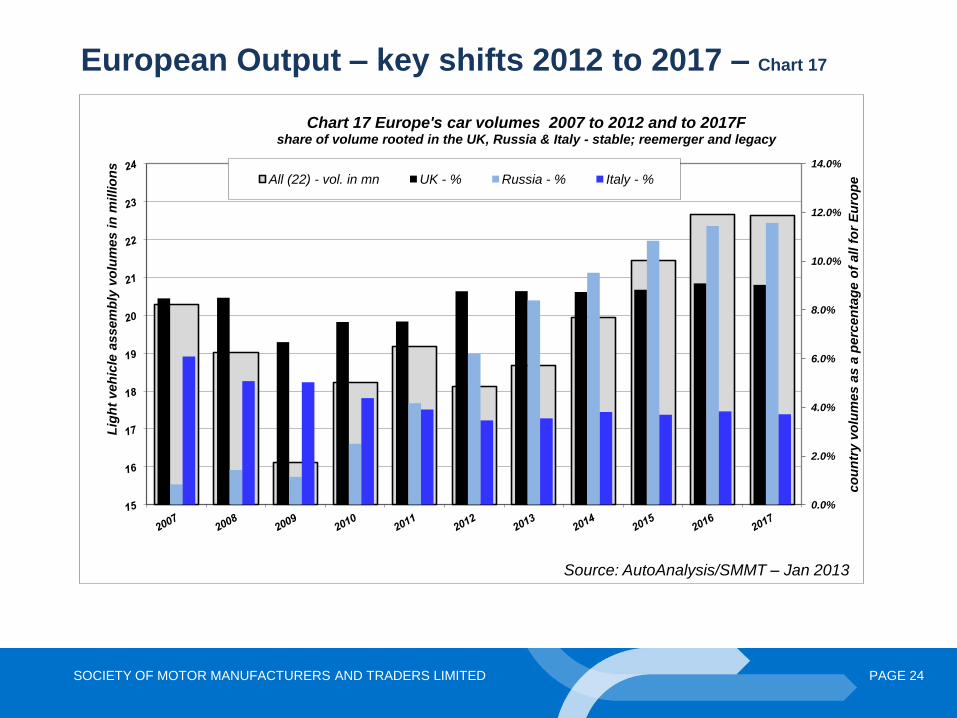

European Output – key shifts 2012 to 2017 – Chart 17

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

co

un

try v

olu

mes a

s a

perc

en

tag

e o

f all f

or

Eu

rop

e

Lig

ht

veh

icle

assem

bly

vo

lum

es i

n m

illio

ns

Chart 17 Europe's car volumes 2007 to 2012 and to 2017F

share of volume rooted in the UK, Russia & Italy - stable; reemerger and legacy

All (22) - vol. in mn UK - % Russia - % Italy - %

Source: AutoAnalysis/SMMT – Jan 2013

SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED PAGE 25

In conclusion, on the UK economy and cars

Recovered; stable; firmer growth later not sooner

• Less restrictive outlook for immediate household spending

• External threats to trade, credit and confidence remain also

domestic concerns on austerity & unique monetary policy

• Domestic growth potential & opportunities yet to be realised

• Car TIV and assembly stable, but big shifts in the mix

• Economy adjusting to major restructuring, rebalancing and

reorientation agenda – unsure and unsteady growth likely

SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED PAGE 26

Ian Henry

Director

AutoAnalysis

SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED PAGE 27

Production Outlook – 2012 key facts

– Provisional 2012 European production inc. Russia = 18.1mn, >1mn down on 2011:

– W/out Russia = 17mn, down >1.4mn

– Production collapse prevented by modest growth in Czech Rep., Hungary, Romania & UK – and boost in Slovakia from VW Up!

– Big 2012 losers = Spain (c460k), Italy (c120k), France (c340k) and even Germany (c540k)

– Larger than expected fall in Germany due to wholesale decline at Ford & Opel and model cycle effects at Mercedes & especially Audi (A4/A6/Q5) and switch to new Golf

SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED PAGE 28

Production Outlook – recovery highlights

– Germany will recover: by 2017 should be back at 2007 peak

– France, Italy & Spain = long-term losers, in 2017:

– France should be c30%/900k down on 2007

– Italy down one-third/400k and Spain c20%/600k on 2007

– Eastwards shift continues 2012-2017:

– Czech +c20%; Hungary + c140%

– Romania +c40%; Slovakia +c10% or quite possibly more

– UK production still growing, by as much as c25% 2012-2017 if Mini, JLR and Nissan fulfil expectations, reaching c2mn upa:

– Mini parts production boosted by Mini production in Netherlands

SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED PAGE 29

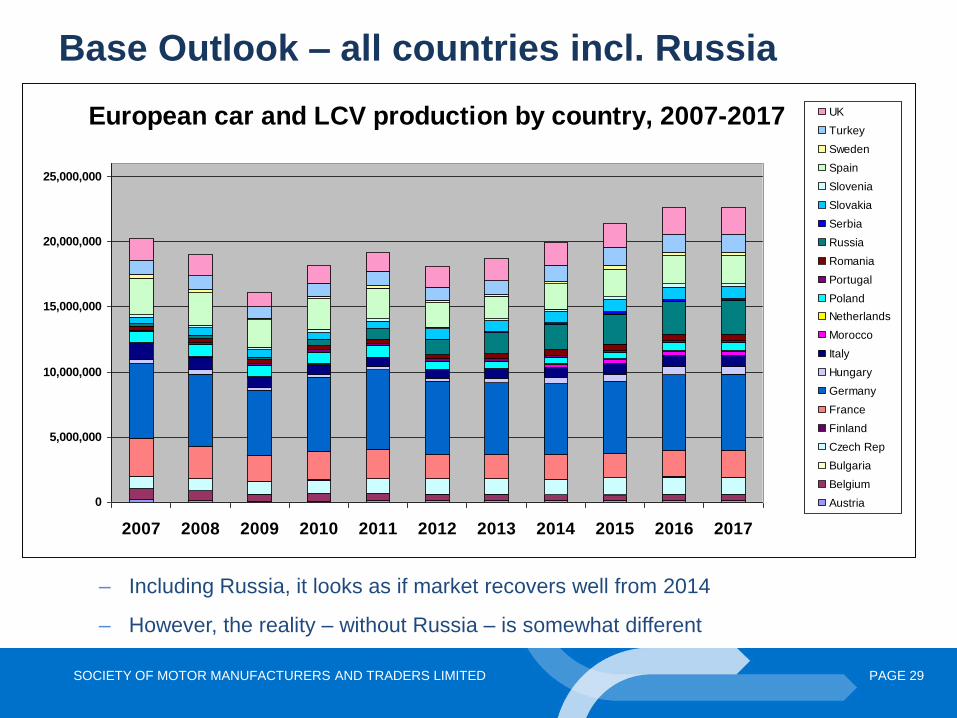

Base Outlook – all countries incl. Russia

– Including Russia, it looks as if market recovers well from 2014

– However, the reality – without Russia – is somewhat different

European car and LCV production by country, 2007-2017

0

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

UK

Turkey

Sweden

Spain

Slovenia

Slovakia

Serbia

Russia

Romania

Portugal

Poland

Netherlands

Morocco

Italy

Hungary

Germany

France

Finland

Czech Rep

Bulgaria

Belgium

Austria

SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED PAGE 30

Without Russia, the picture is less attractive

– Without Russia, and being optimistic, Europe takes until 2016 to recover to 2007 volumes

– Scenarios 1-3 assume fall of 1-5% in major markets above and beyond the falls inherent in our Base Outlook

European Production Excl Russia - Base Outlook & 3 alternative

scenarios

15,000,000

16,000,000

17,000,000

18,000,000

19,000,000

20,000,000

21,000,000

22,000,000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Years

Un

its Base w/o Russia

Scen 1 w/o Russia

Scen 2 w/o Russia

Scen 3 w/o Russia

SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED PAGE 31

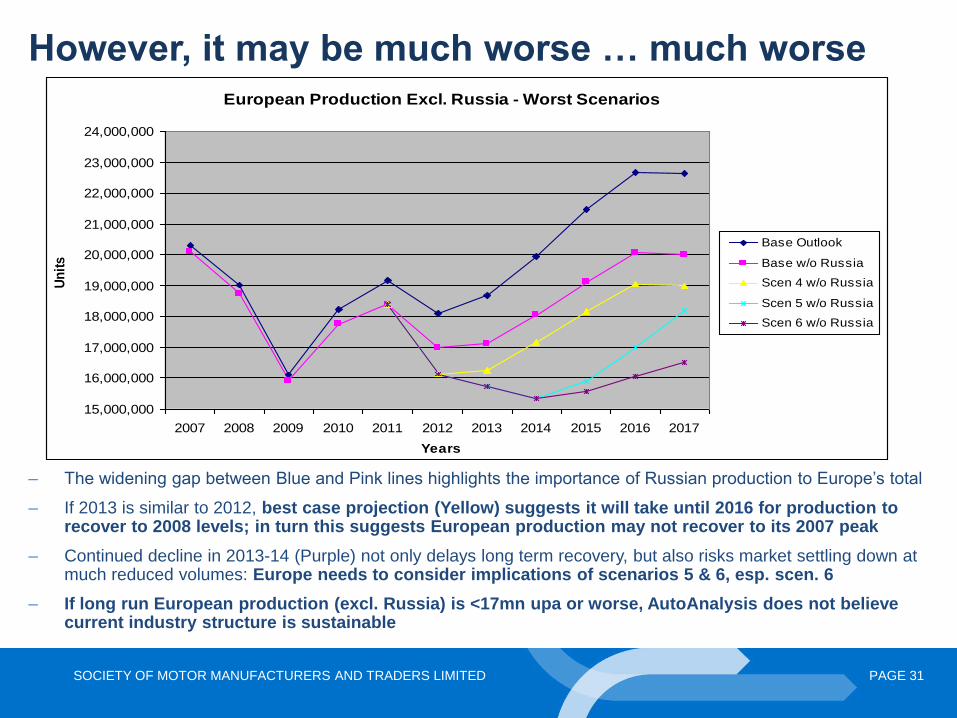

However, it may be much worse … much worse

– The widening gap between Blue and Pink lines highlights the importance of Russian production to Europe’s total

– If 2013 is similar to 2012, best case projection (Yellow) suggests it will take until 2016 for production to recover to 2008 levels; in turn this suggests European production may not recover to its 2007 peak

– Continued decline in 2013-14 (Purple) not only delays long term recovery, but also risks market settling down at much reduced volumes: Europe needs to consider implications of scenarios 5 & 6, esp. scen. 6

– If long run European production (excl. Russia) is <17mn upa or worse, AutoAnalysis does not believe current industry structure is sustainable

European Production Excl. Russia - Worst Scenarios

15,000,000

16,000,000

17,000,000

18,000,000

19,000,000

20,000,000

21,000,000

22,000,000

23,000,000

24,000,000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Years

Un

its

Base Outlook

Base w/o Russia

Scen 4 w/o Russia

Scen 5 w/o Russia

Scen 6 w/o Russia

SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED PAGE 32

Falling sales leading to falling production volumes

and structural change at the volume VMs …

– European car & LCV markets fell in 2012: EU27 at 17-year low

– January 2013 sales shows no sign of improvement, except UK which continued to rise:

– SAAR @ lowest rate since 1987 …

– 01/13 y-o-y falls:

– W Eur: -9.5%; Germany: -8.6%

– France: -15%; Italy: -12.6%; Spain: -9%

– Volume VMs’ European production falling significantly

– Traditional brands facing long-run, structural decline as value brands and premium marques continue to grow:

– New order for VMs in Europe beginning to emerge …

– VMs attempting new strategies: Fiat wants to move core brand upmarket, possibly adding value brand

– Nissan and VW also considering value brands

SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED PAGE 33

Structural change under way at the volume VMs …

– Restructuring began in earnest in 2012:

– Ford, GM & PSA closing plants; GM and PSA bringing forward closure of Bochum and Aulnay

– GM & PSA established a defensive alliance, but benefits not yet apparent …

– Fiat reorganising model allocation between Italian factories, slimming down, but not closing plants:

– Investing €1bn at Melfi for new Fiat and Jeep small SUVs, to be made at 1600/day on a 3-shift basis

– Cutting at least 1,500 jobs in Poland, with 2013 production likely to be ½ that in 2009

– Renault following Fiat approach, for now:

– Claims that union deals (c7,500 job cuts) will lead to additional 180k upa in France, including 80k from “partners”

– Nissan however has confirmed expansion in Barcelona not France

– Highly likely that Fiat & Renault will have to cut capacity

SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED PAGE 34

Although things have changed, are recent actions enough?

• VMs no longer just talking about restructuring – they have had to act: – GM and Ford each lost >€1bn in Europe in 2012; similar or greater losses

expected in 2013

– PSA, Renault and Fiat also loss-making in Europe … PSA reportedly losing €7mn/day – unions expressed fears over potential bankruptcy

• Will closures announced so far be enough? – Can Fiat and Renault avoid closing factories for much longer?

– Will Ford, GM and PSA close more plants?

• Despite strength of German & UK premium brands, Hyundai-Kia and Nissan, we doubt whether non-EU exports can sustain European production in perpetuity, especially at the volume brands:

– VW group, Fiat, PSA, BMW and Mercedes all growing plants outside Europe, esp. in NAFTA, Brazil & China

– VW also cutting Passat production in Germany, but adding shifts to cope with demand for Golf and Tiguan; and adding Golf production in Mexico

SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED PAGE 35

In conclusion …

• Production recovery unlikely before 2014, quite possibly 2015:

– Production revival will be shallower and slower than in 2009 …

• Increasingly likely that long run production volumes will be far below 2007-2008 peaks

• Further re-structuring and capacity cutbacks seem inevitable: – Realistic chance of a major European name disappearing by the

end of the decade, if not before – Rising strength of Koreans & Nissan and enduring appeal of

German/UK premium brands should not be underestimated – More value brands likely to appear

• Not a question of if/when European VMs will restructure further: – Key issue remains: how much more change will be required? – National governments unlikely to be able to save national brands

PAGE 36 SOCIETY OF MOTOR MANUFACTURERS AND TRADERS LIMITED

Questions and Answers

Please click on the hand symbol to raise your hand if you have a question.

Please ensure that you are connected to the audio to ask a question.

Email: [email protected] with your questions after this session.

Slides emailed to participants after this session

Alternatively, you can type your question.