professor thomson finance 3014

DESCRIPTION

Chapter 2. Financial Statements And Cash Flow Analysis. Professor Thomson Finance 3014. Asset, Liability, Equity. - PowerPoint PPT PresentationTRANSCRIPT

Chapter 2. Financial Statements And

Cash Flow AnalysisProfessor Thomson

Finance 3014

2

Asset, Liability, Equity• Asset – something that has value

(typically can be sold for $). Why does it have value? It produces a benefit such as a cash flow. (Could be money in the bank, a house, car, college education)

• Liability – Something you have to pay for someone to take from you, like a loan (i.e. debt). It has negative value (to you).

• Equity – represents your ownership in something

3

Balance Sheet Identity• Assets = Liabilities + Equity• This statement indicates that assets

are financed either through borrowed money, or through ownership.

• Say your car is worth $10,000 and you have a 7,000 balance on your loan. You have $3000 of equity, or ownership in that car.

• Personal Finance Goal: – Increase your equity

4

Balance SheetCurrent Assets Current Liabilitiescan easily be turned into cash will be paid off within the year

are "liquid" assets

Long Term Debt primarily bonds

often called "financial leverage"

Fixed Assets

Can be tangible (factory)

Can be intangible (goodwill) Owners EquityAre "real" assets

5

GAAP – Generally Accepted Accounting Principles• Used to fairly portray the firm's past

performance• Accountants used an “accrual-based”

approach. Revenue recorded at the point of sales and costs when they are incurred

• Finance professionals focus on the timing and size of the cash flows.

6

Four Key Financial Statements

1.Balance sheet (A=L+E)– snapshot of assets, liabilities, equity

2. Income statement- Shows the flow of revenues and expenses

over a period

3. Statement of retained earnings

4. Statement of cash flows

7

Financial Statements

Financial Managers and analysts use financial statements to conduct:

-Cash Flow Analysis

-Performance (Ratio) Analysis

8

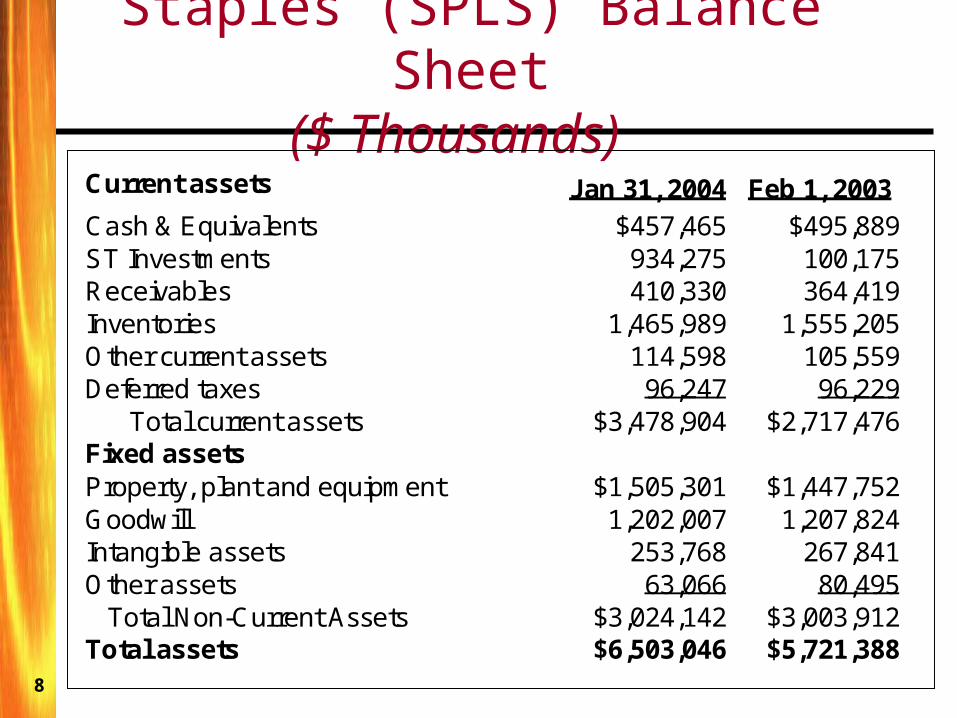

Staples (SPLS) Balance Sheet($ Thousands)

Current assets Jan 31, 2004 Feb 1, 2003 Cash & Equivalents $457,465 $495,889 ST Investments 934,275 100,175 Receivables 410,330 364,419 Inventories 1,465,989 1,555,205 Other current assets 114,598 105,559 Deferred taxes 96,247 96,229 Total current assets $3,478,904 $2,717,476 Fixed assets Property, plant and equipment $1,505,301 $1,447,752 Goodwill 1,202,007 1,207,824 Intangible assets 253,768 267,841 Other assets 63,066 80,495 Total Non-Current Assets $3,024,142 $3,003,912 Total assets $6,503,046 $5,721,388

9

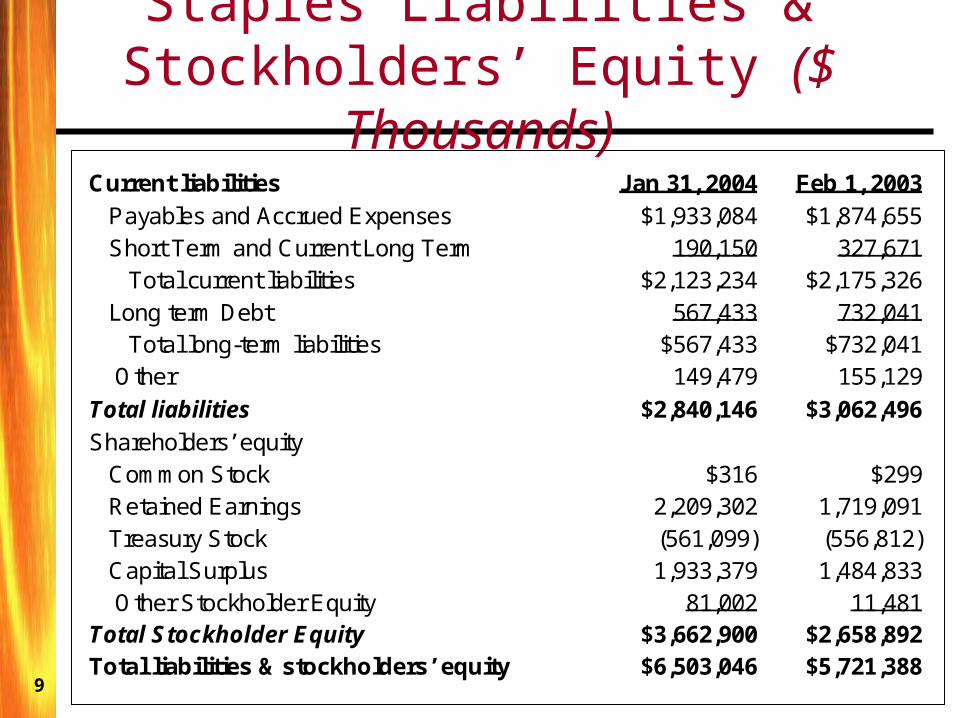

Staples Liabilities & Stockholders’ Equity ($

Thousands) Current liabilities Jan 31, 2004 Feb 1, 2003 Payables and Accrued Expenses $1,933,084 $1,874,655 Short Term and Current Long Term 190,150 327,671 Total current liabilities $2,123,234 $2,175,326 Long term Debt 567,433 732,041 Total long-term liabilities $567,433 $732,041 Other 149,479 155,129 Total liabilities $2,840,146 $3,062,496 Shareholders’ equity Common Stock $316 $299 Retained Earnings 2,209,302 1,719,091 Treasury Stock (561,099) (556,812) Capital Surplus 1,933,379 1,484,833 Other Stockholder Equity 81,002 11,481 Total Stockholder Equity $3,662,900 $2,658,892 Total liabilities & stockholders’ equity $6,503,046 $5,721,388

10

Staples Income Statement ($ Thousands)

Jan 31, 2004

Feb 01, 2003 Total Revenue $13,181,222 $11,596,075 Cost of Revenue (9,559,123) (8,652,593) Gross Profit $3,622,099 $2,943,482 Operating/Selling 2,282,092 1,795,428 General/Admin. Exp. (includes DEPN) 524,094 451,501 Non Recurring 9,639 8,746 Other 7,986 2,135 Operating income $798,288 $682,672 Earnings Before Interest and Taxes $798,288 $682,672 Interest Expense 20,176 20,609 Income Tax Expense 287,901 215,963 Net Income from Continuing Operations

$490,211 $446,100

Net income $490,211 $446,100

11

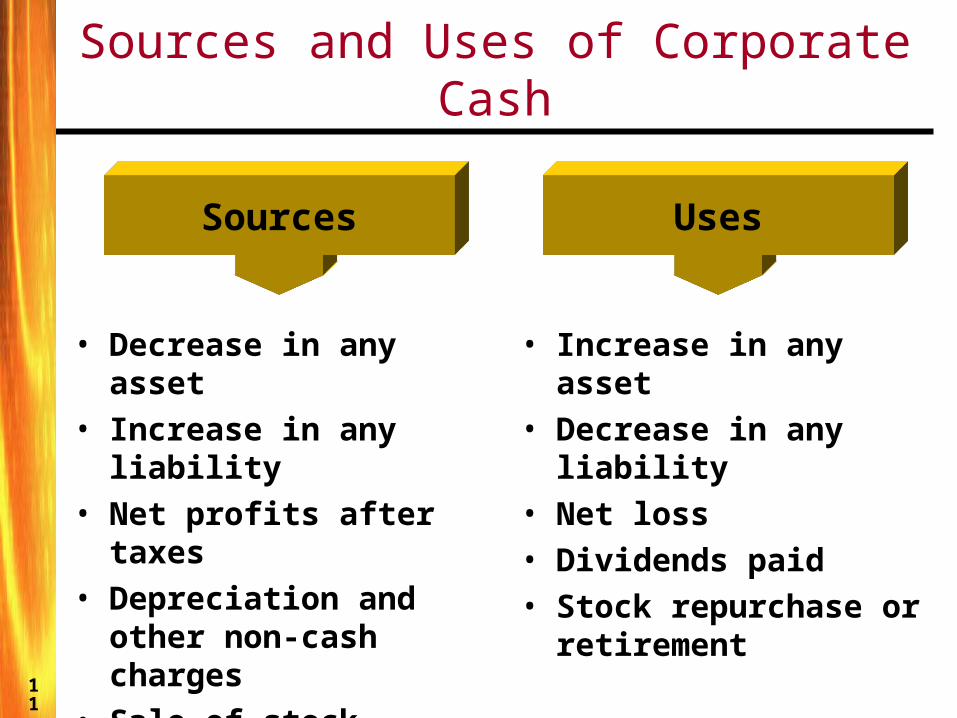

Sources and Uses of Corporate Cash

Sources

• Decrease in any asset

• Increase in any liability

• Net profits after taxes

• Depreciation and other non-cash charges

• Sale of stock

Uses

• Increase in any asset• Decrease in any

liability• Net loss• Dividends paid• Stock repurchase or

retirement

12

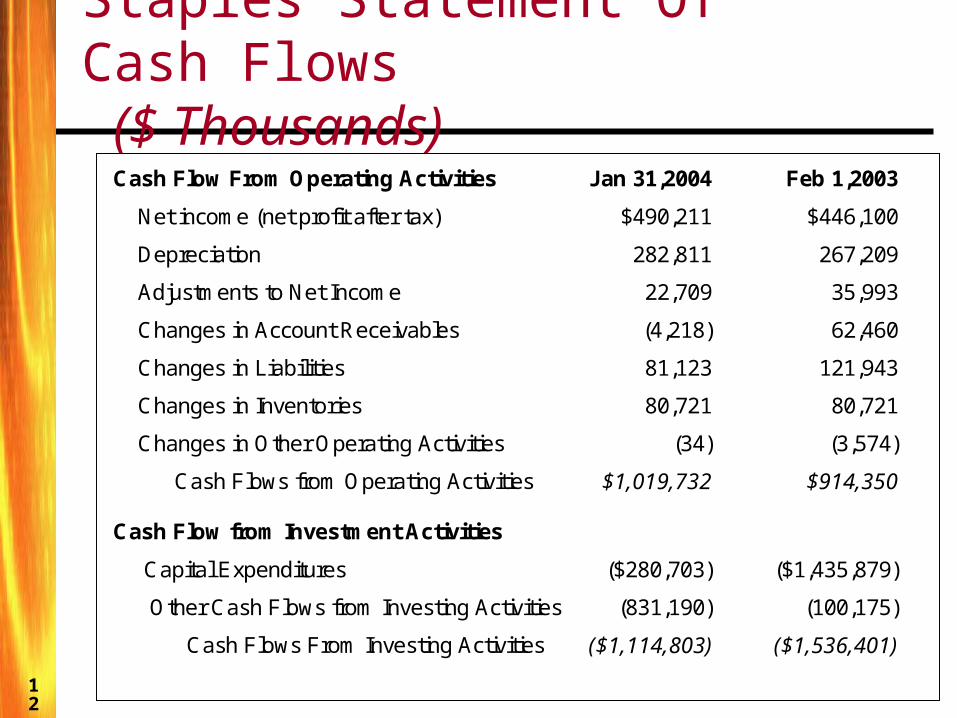

Staples Statement Of Cash Flows ($ Thousands)

Cash Flow From Operating Activities

Jan 31,2004

Feb 1,2003 Net income (net profit after tax) $490,211 $446,100

Depreciation 282,811 267,209

Adjustments to Net Income 22,709 35,993

Changes in Account Receivables (4,218) 62,460

Changes in Liabilities 81,123 121,943

Changes in Inventories 80,721 80,721

Changes in Other Operating Activities (34) (3,574)

Cash Flows from Operating Activities $1,019,732 $914,350

Cash Flow from Investment Activities

Capital Expenditures ($280,703) ($1,435,879)

Other Cash Flows from Investing Activities (831,190) (100,175)

Cash Flows From Investing Activities ($1,114,803) ($1,536,401)

13

Staples Statement Of Cash Flows ($Thousands)

Cash Flow From Financing Activities Jan 31, 2004 Feb 1, 2003

Sale (Purchase) of Stock $385,506 $78,421

Net Borrowings (350,235) 635,662

Net Cash Provided by Financing Activities $35,271 $714,038

Effect of exchange rate changes on cash 21,376 9,033

Net (decrease) increase in cash ($38,424) $101,065

Cash and Cash Equivalents, End of Period $457,465 $495,889

14

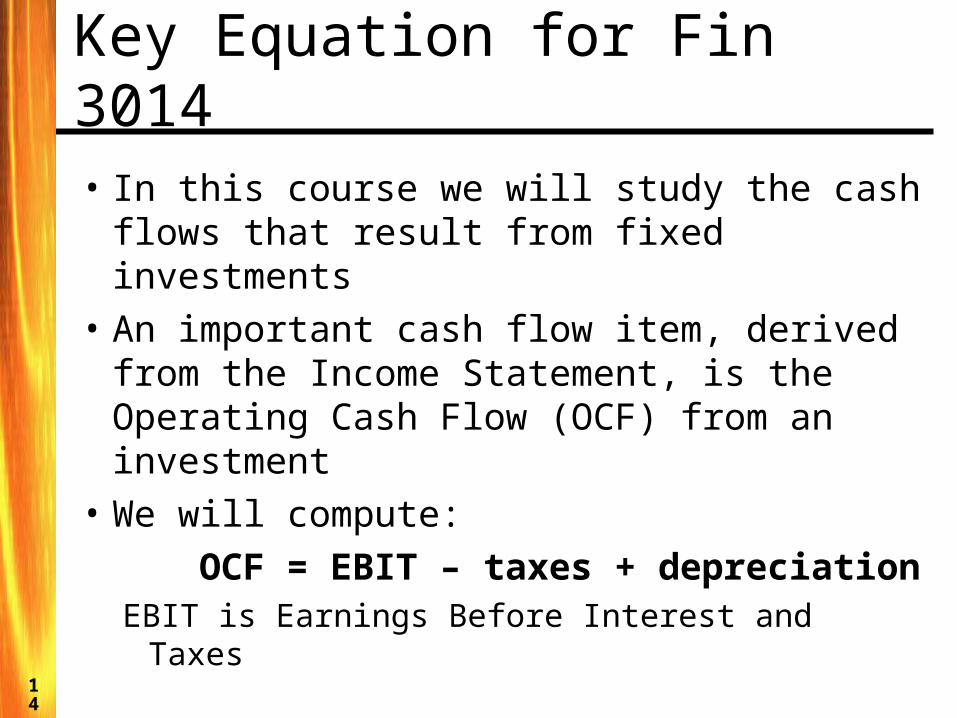

Key Equation for Fin 3014• In this course we will study the cash

flows that result from fixed investments• An important cash flow item, derived

from the Income Statement, is the Operating Cash Flow (OCF) from an investment

• We will compute: OCF = EBIT – taxes +

depreciationEBIT is Earnings Before Interest and Taxes

15

• Current ratio • Quick ratio• Inventory turnover ratio• Average collection period• Debt-to-equity ratio• Times interest earned ratio• Gross margin• EPS• P/E ratio• Market-to-book ratio

Types Of Financial Ratios

Activity Ratios

Debt Ratios

Profitability Ratios

Market Ratios

Liquidity Ratios

16

Financial Ratios: Trends and Benchmarking

Benchmarking: comparison of a company’s ratio values to industry competitors’ ratios

Firms’ financial ratios compared at the same point in time

Trend analysis - performance evaluation over time

Developing trends can be seen using multi-year comparisons.

17

Liquidity Ratios (short term obligations) note:NWC = CA - CL

seitilibailcurrent assetscurrent = ratioCurrent

seitilibailcurrent inventoryassets-current = ratioQuick

Staples (2004)

64.1 = ratioCurrent 95.0 = ratioQuick

Office Depot (2004)

57.1 = ratioCurrent 98.0 = ratioQuick

18

Activity Ratios

inventorysold goods ofcost = turnoverInventory

assets fixednet sales = overasset turn Fixed

52.6 = turnoverInventory 36.4 = overasset turn Fixed

Staples (2004)

Office Depot (2004)

35.6 = turnoverInventory 81.4 = overasset turn Fixed

19

Activity Ratios (Continued)

daypersalesAveragereceivableAccounts = periodcollectionAverage

365salesAnnual

= daypersalesAverage

assets totalsales = overasset turn Total

99.936,112,36$ = daypersalesAveragedays 36.11 = periodcollectionAverage

03.2 = overasset turn Total Staples (2004)

Office Depot (2004)

.9333,859,084$ = daypersalesAveragedays 86.37 = periodcollectionAverage

01.2 = overasset turn Total

20

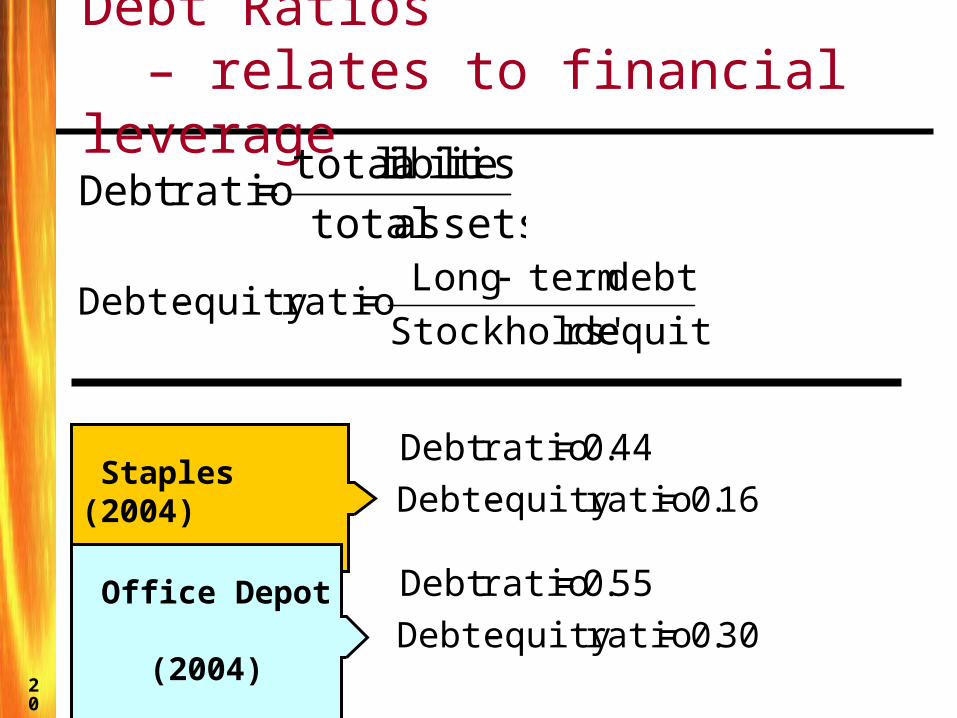

Debt Ratios – relates to financial leverage

equityrs'StockholdedebttermLong = ratioequity Debt-

assets totalseitilibail total

= ratioDebt

44.0 = ratioDebt 16.0 = ratioequity Debt-

Staples (2004)

Office Depot (2004)

55.0 = ratioDebt 30.0 = ratioequity Debt-

21

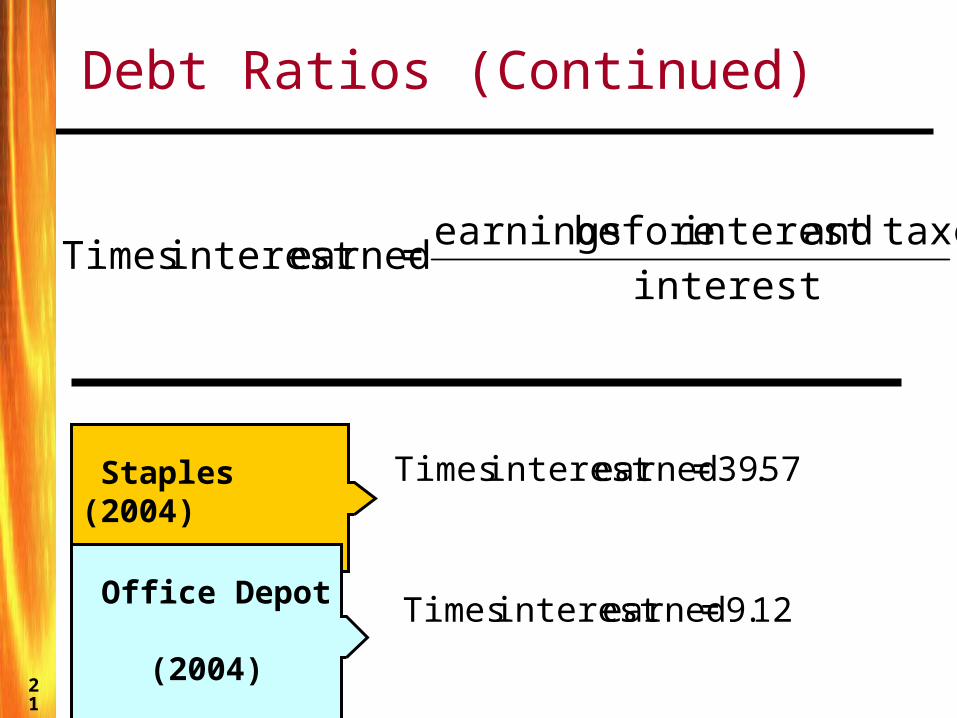

Debt Ratios (Continued)

interest taxesandinterest before earnings = earnedinterest Times

57.39 = earnedinterest Times Staples (2004)

Office Depot (2004) 12.9 = earnedinterest Times

22

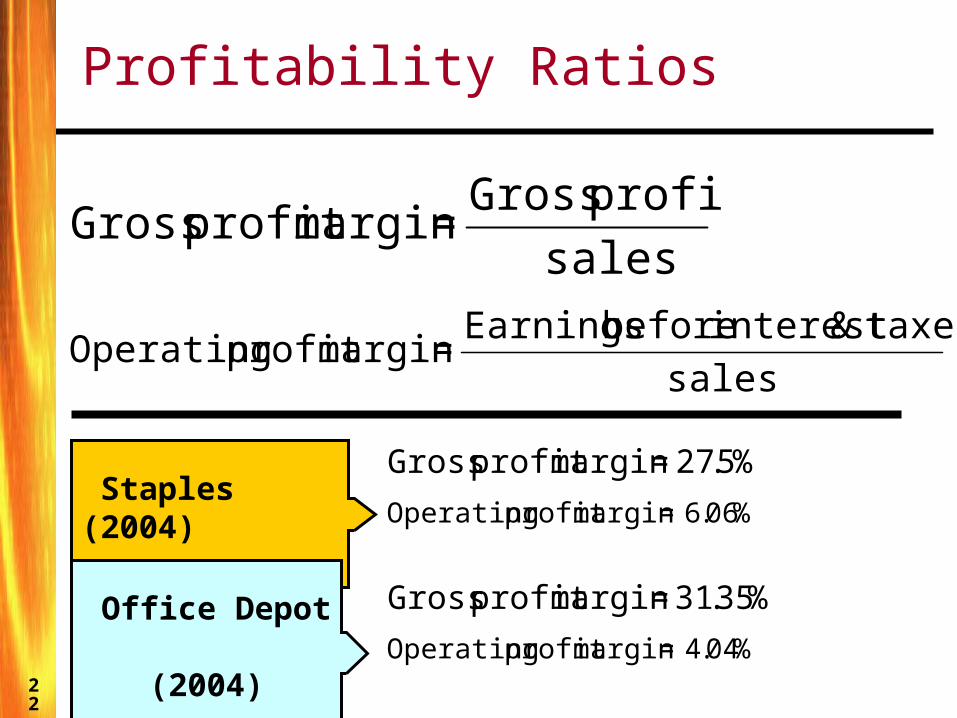

Profitability Ratios

salestaxes&interestbeforeEarnings = marginprofit Operating

sales

profitsGross = marginprofit Gross

%5.27 = marginprofit Gross%06.6 = marginprofit Operating

Staples (2004)

Office Depot (2004)

%35.31 = marginprofit Gross%04.4 = marginprofit Operating

23

Profitability Ratios (Continued)

salesincomeNet = marginprofit Net

goutstandinstock common of shares ofnumber incomeNet = shareper Earnings

%72.3 = marginprofit Net 98.0$ = shareper Earnings

Staples (2004)

Office Depot (2004)

%24.2 = marginprofit Net 89.0$ = shareper Earnings

24

Net profit margin (2004 data)• Consider two highly profitable

companies:• Wal-Mart: NPM = 3.3%• Microsoft: NPM = 14.3%

• Which is the best company to invest in?

25

Profitability Ratios - what if you have no liabilities?

assets TotalincomeNet = assets on totalReturn

equity rs'StockholdeincomeNet = equitycommon on Return

%54.7 = assets on totalReturn

%4.13 = equitycommon on Return Staples (2004)

Office Depot (2004)

%50.4 = assets on totalReturn

%89.9 = equitycommon on Return

26

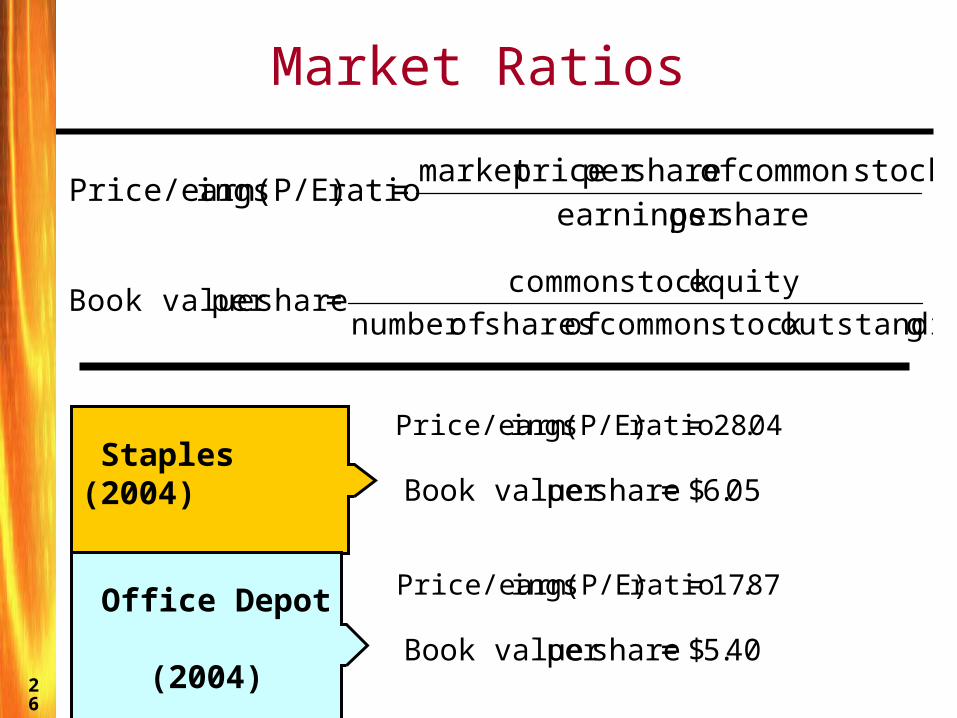

Market Ratios

shareper earningsstockcommon of shareper pricemarket = ratio (P/E) ingsPrice/earn

goutstandinstock common of shares ofnumber equitystock common = shareper Book value

04.28 = ratio (P/E) ingsPrice/earn

05.6$ = shareper Book value Staples (2004)

Office Depot (2004)

87.17 = ratio (P/E) ingsPrice/earn

40.5$ = shareper Book value

27

Market Ratios

stockcommonofsharepervalueBook

stockcommonofsharepervalueMarketratio (M/B)k Market/boo

55.4 ratio (M/B)k Market/boo Staples (2004)

Office Depot (2004) 94.2 ratio (M/B)k Market/boo

28

Corporate Taxes

Significant cash outflow

Ordinary income tax

• Progressive tax rate schedule• Average tax rate: tax divided by

the pretax income• More relevant: marginal tax rate

Capital gains tax

• Under existing tax laws, use ordinary income tax rates for capital gain taxes

Financial Statements and Financial Ratios

Balance Statement Income Statement

Liquidity Ratios Activity Ratios

Debt Ratios Profitability Ratios

Market Ratios