profit planning and standard costs & operating performance measures”

TRANSCRIPT

“Case study on profit planning and standard costs & operating

performance measures”

Course: Managerial Accounting

Course code: 302

Submitted to:

Shakila Halim Lecturer Department of Finance University of Dhaka

Submitted by:

Group: Section: A Department of Finance University of Dhaka Date of Submission: 28th June 2015

Group Members:

Serial Name ID

1 Maruf Hossain 19-013

2 Manjurul Ahsan 19-099

3 Md. Abdul Quyum 19-121

4 Md. Ripon Molla 19-123

5 Raqib Hossain 19-157

Letter of Transmittal 28th June 2015 Shakila Halim Lecturer Department of Finance University of Dhaka

Subject: A report on “Case study on profit planning and standard costs &operating performance

measures”

Honorable Madam, This is a great pleasure for us to submit the report on “Case study on profit planning and standard costs

& operating performance measures” as a partial requirement of the BBA program in University of

Dhaka.

Preparation of this report has been a great pleasure & an interesting experience. It enabled us to know about profit planning more broadly than before and also their economic condition. This report helped us tremendously to understand and to know the various term of profit planning and standard costs & operating performance measures. We have undertaken our sincere effort for successful completion of the BBA program. If we have any unintentional errors and omissions that may have entered into this report will be considered with sympathy. Therefore, we beg your kind consideration in this regard, we will be very grateful if you accept our report and oblige there by. Sincerely, On the behalf of members of group

Acknowledgement

We would like to pay our gratitude to all of the related books, articles, journals, authors and related Web Sites that helped us a lot for the completion of this report before, during, and after the working period. At first we would like to acknowledge the Almighty, who helped us every time and was with us and gave us moral support and strength every moment. We are especially grateful to our honorable course instructor Shakila Halim for giving us valuable

suggestions and support to prepare this report. Without her advice and support, it would not be

possible for us to prepare this report.

Executive Summary

The report shows a hypothetical case on profit planning and standard costs & operating

performance measures. Budgeting is an estimate of costs, revenues, and resources over a

specified period, reflecting a reading of future financial conditions and goals. The process of

creating a budget takes management away from its short-term, day-to-day management of

the business and forces it to think longer-term.

The master budget is the aggregation of all lower-level budgets produced by a company's

various functional areas, and also includes budgeted financial statements, cash forecast,

and a financing plan. The master budget is typically presented in either a monthly or

quarterly format or usually covers a company's entire fiscal year. An explanatory text may

be included with the master budget, which explains the company's strategic direction, how

the master budget will assist in accomplishing specific goals, and the management actions

needed to achieve the budget. A properly structured budget should derive the amount of

cash that will be spun off or which will be needed to support operations. This information

is used by the treasurer to plan for the company's funding needs.

The variance calculations that typically accompany a standard costing report are

accumulated in aggregate for a company’s entire production department, and so are unable

to provide information about discrepancies at a lower level, such as the individual work

cell, batch, or unit.

Table of Contents Chapter-1 ...................................................................................................................................................... 7

Introduction .................................................................................................................................................. 7

1.1 Introduction: ........................................................................................................................................... 8

1.2 Origin of the Study: ................................................................................................................................. 8

1.3 Objective of the Study: ........................................................................................................................... 8

1.4 Scope of study: ........................................................................................................................................ 9

1.5 Methodology: .......................................................................................................................................... 9

Chapter 2 ..................................................................................................................................................... 10

Budgeting & its Negative and Positive Aspects .......................................................................................... 10

2.1 What is Budgeting? ............................................................................................................................... 11

2.2 Why do Budgeting? ............................................................................................................................... 11

Planning orientation ................................................................................................................................... 11

Profitability review ...................................................................................................................................... 11

Performance evaluations ............................................................................................................................ 11

Funding planning ......................................................................................................................................... 12

Cash allocation ............................................................................................................................................ 12

Bottleneck analysis ..................................................................................................................................... 12

2.3 Limitations & Disadvantages of Budgeting: .......................................................................................... 12

Time required. ............................................................................................................................................. 12

Gaming the system. .................................................................................................................................... 12

Blame for outcomes .................................................................................................................................... 13

Expense allocations .................................................................................................................................... 13

Spend it or lose it ........................................................................................................................................ 13

Only considers financial outcomes ............................................................................................................. 13

Strategic rigidity .......................................................................................................................................... 13

2.4 What is Master Budget? ....................................................................................................................... 14

2.5 Components of Master Budget: ............................................................................................................ 14

2.7 Standard Cost & Operating Performance Measures: ........................................................................... 15

What is Standard Costing? .......................................................................................................................... 15

Why do Standard Costing? .......................................................................................................................... 15

Budgeting. ................................................................................................................................................... 15

Inventory costing ........................................................................................................................................ 15

Overhead application .................................................................................................................................. 16

Price formulation ........................................................................................................................................ 16

Limitation of standard costing: ................................................................................................................... 16

Cost-plus contracts ..................................................................................................................................... 16

Drives inappropriate activities .................................................................................................................... 16

Fast-paced environment ............................................................................................................................. 17

Slow feedback ............................................................................................................................................. 17

Unit-level information ................................................................................................................................. 17

Chapter 3 ..................................................................................................................................................... 18

Hypothetical Case of Budgeting .................................................................................................................. 18

Schedule 1: .................................................................................................................................................. 19

Schedule 2: .................................................................................................................................................. 21

Schedule 3: .................................................................................................................................................. 22

Schedule 4: .................................................................................................................................................. 23

Schedule 5: .................................................................................................................................................. 24

Schedule 6: .................................................................................................................................................. 25

Schedule 7: .................................................................................................................................................. 26

Schedule 8: .................................................................................................................................................. 27

Schedule 9: .................................................................................................................................................. 28

Schedule 10: ................................................................................................................................................ 29

Chapter 4 ..................................................................................................................................................... 30

Comparison between actual and standard operation ................................................................................ 30

Direct Material Variance ............................................................................................................................. 31

Direct Labor Variance .................................................................................................................................. 31

Variable Overhead Variance ....................................................................................................................... 32

Conclusion: .................................................................................................................................................. 33

Chapter-1

Introduction

1.1 Introduction: A budget is a quantitative expression of a plan for a defined period of time. It may include

planned sales volumes and revenues, resource quantities, costs and expenses, assets,

liabilities and cash flows. It expresses strategic plans of business units, organizations,

activities or events in measurable terms. Budget should be logical and have basement for

historical data. In a budget, we need to consider future possibilities as well as the future

threat that can affect company’s operation.

1.2 Origin of the Study: This paper is prepared for Ms. Shakila Halim Course instructor of “Managerial Accounting”,

Department of Finance, and Faculty of Business Studies at University of Dhaka as a partial

requirement of the course. Our course instructor has assigned us to make a report on “Case

Study on Budgeting & Standard Cost and Operating Performance Measures”. This report is

prepared during the first Semester, Third Year and would be submitted in the same

semester. The standard procedure for the long, formal report is followed here as part of the

instruction of the course instructor.

1.3 Objective of the Study: The main objectives of this report are stated below:

To review the concept of budgeting

To know the practical implication of budgeting

To overview the steps of budgeting

To develop future forecasting skill

To review the concept of standard cost and operating performance measures.

To outline the importance of standard cost and operating performance measures.

To review the method of real-life variance

To apply the knowledge in practical problem

1.4 Scope of study: This report will give a clear idea about “Case study on profit planning and standard costs &

operating performance measures”

What is profit Budgeting?

What are the ways of budget planning?

What are the steps of budget planning?

What is the importance of Budget Planning?

How does budget planning use in practical world?

What is standard cost and operating performance measures?

What is the importance of it?

What is the application in real case of standard cost and operating performance?

1.5 Methodology: Each and every information used here is hypothetical.

Assumptions are done after study on this sector.

Logical flow of information is maintained over calculations and assumptions.

Steps are taken from Course Book ( Managerial Accounting, Garrison-Noreen-

Brewer)

Chapter 2

Budgeting & its Negative and Positive

Aspects

2.1 What is Budgeting? Budgeting is an estimate of costs, revenues, and resources over a specified period,

reflecting a reading of future financial conditions and goals.

One of the most important administrative tools, a budget serves also as a (1) plan of action

for achieving quantified objectives, (2) standard for measuring performance, and (3) device

for coping with foreseeable adverse situations.

2.2 Why do Budgeting?

Planning orientation The process of creating a budget takes management away from its short-term, day-to-day

management of the business and forces it to think longer-term. This is the chief goal of

budgeting, even if management does not succeed in meeting its goals as outlined in the

budget - at least it is thinking about the company's competitive and financial position and

how to improve it.

Profitability review It is easy to lose sight of where a company is making most of its money, during the

scramble of day-to-day management. A properly structured budget points out what aspects

of the business produce money and which ones use it, which forces management to

consider whether it should drop some parts of the business, or expand in others.

Assumptions review. The budgeting process forces management to think about why the

company is in business, as well as its key assumptions about its business environment. A

periodic re-evaluation of these issues may result in altered assumptions, which may in turn

alter the way in which managements decides to operate the business.

Performance evaluations You can work with employees to set up their goals for a budgeting period, and possibly also

tie bonuses or other incentives to how they perform. You can then create budget versus

actual reports to give employees feedback regarding how they are progressing toward

their goals. This approach is most common with financial goals, though operational goals

(such as reducing the product rework rate) can also be added to the budget for

performance appraisal purposes. This system of evaluation is called responsibility

accounting.

Funding planning A properly structured budget should derive the amount of cash that will be spun off or

which will be needed to support operations. This information is used by the treasurer to

plan for the company's funding needs.

Cash allocation There is only a limited amount of cash available to invest in fixed assets and working

capital, and the budgeting process forces management to decide which assets are most

worth investing in.

Bottleneck analysis Nearly every company has a bottleneck somewhere, and the budgeting process can be

used to concentrate on what can be done to either expand the capacity of that bottleneck or

to shift work around it.

2.3 Limitations & Disadvantages of Budgeting:

Time required. It can be very time-consuming to create a budget, especially in a poorly-organized

environment where many iterations of the budget may be required. The time involved is

lower if there is a well-designed budgeting procedure in place, employees are accustomed

to the process, and the company uses budgeting software. The time requirement can be

unusually large if there is a participative budgeting process in place, since such a system

involves an unusually large number of employees.

Gaming the system. An experienced manager may attempt to introduce budgetary slack, which involves

deliberately reducing revenue estimates and increasing expense estimates, so that he can

easily achieve favorable variances against the budget. This can be a serious problem, and

requires considerable oversight to spot and eliminate.

Blame for outcomes If a department does not achieve its budgeted results, the department manager may blame

any other departments that provide services to it for not having adequately supported his

department.

Expense allocations The budget may prescribe that certain amounts of overhead costs be allocated to various

departments, and the managers of those departments may take issue with the allocation

methods used.

Spend it or lose it If a department is allowed a certain amount of expenditures and it does not appear that the

department will spend all of the funds during the budget period, the department manager

may authorize excessive expenditures at the last minute, on the grounds that his budget

will be reduced in the next period unless he spends all of the amounts authorized in the

current budget.

Only considers financial outcomes Budgets are primarily concerned with the allocation of cash to specific activities, and the

expected outcome of business transactions - they do not deal with more subjective issues,

such as the quality of products or services provided to customers. These other issues can

be stated as part of the budget, but this is not typically done.

Strategic rigidity When a company creates an annual budget, the senior management team may decide that

the focus of the organization for the next year will be entirely on meeting the targets

outlined in the budget. This can be a problem if the market shifts in a different direction

sometime during the budget year. In this case, the company should shift along with the

market, rather than adhering to the budget.

2.4 What is Master Budget?

The master budget is the aggregation of all lower-level budgets produced by a company's

various functional areas, and also includes budgeted financial statements, cash forecast,

and a financing plan. The master budget is typically presented in either a monthly or

quarterly format or usually covers a company's entire fiscal year. An explanatory text may

be included with the master budget, which explains the company's strategic direction, how

the master budget will assist in accomplishing specific goals, and the management actions

needed to achieve the budget. There may also be a discussion of the headcount changes

that are required to achieve the budget. A master budget is the central planning tool that a

management team uses to direct the activities of a corporation, as well as to judge the

performance of its various responsibility centers. It is customary for the senior

management team to review a number of iterations of the master budget and incorporate

modifications until it arrives at a budget that allocates funds to achieve the desired results.

Hopefully, a company uses participative budgeting to arrive at this final budget, but it may

also be imposed on the organization by senior management, with little input from other

employees.

2.5 Components of Master Budget: Master budget has two major sections which are the operational budget and the financial

budget. They have following components:

1. Operational Budget

Sales Budget

Production Budget

Direct Material Purchases Budget

Direct Labor Budget

Overhead Budget

Selling and Administrative Expenses Budget

Cost of Goods Manufactured Budget

2. Financial Budget

Schedule of Expected Cash Receipts from Customers

Schedule of Expected Cash Payments to Suppliers

Cash Budget

Budgeted Income Statement

Budgeted Balance Sheet

2.7 Standard Cost & Operating Performance Measures:

What is Standard Costing? Standard costing is an important subtopic of cost accounting. Standard costs are usually

associated with a manufacturing company's costs of direct material, direct labor, and

manufacturing overhead. Standard costing is the practice of substituting an expected cost

for an actual cost in the accounting records, and then periodically recording variances

showing the difference between the expected and actual costs.

Why do Standard Costing? Though most companies do not use standard costing in its original application of

calculating the cost of ending inventory, it is still useful for a number of other applications.

In most cases, users are probably not even aware that they are using standard costing, only

that they are using an approximation of actual costs. Here are some potential uses:

Budgeting. A budget is always composed of standard costs, since it would be impossible to include in

it the exact actual cost of an item on the day the budget is finalized. Also, since a key

application of the budget is to compare it to actual results in subsequent periods, the

standards used within it continue to appear in financial reports through the budget period.

Inventory costing It is extremely easy to print a report showing the period-end inventory balances (if you are

using a perpetual inventory system), multiply it by the standard cost of each item, and

instantly generate an ending inventory valuation. The result does not exactly match the

actual cost of inventory, but it is close. However, it may be necessary to update standard

costs frequently, if actual costs are continually changing. It is easiest to update costs for the

highest-dollar components of inventory on a frequent basis, and leave lower-value items

for occasional cost reviews.

Overhead application If it takes too long to aggregate actual costs into cost pools for allocation to inventory, then

you may use a standard overhead application rate instead, and adjust this rate every few

months to keep it close to actual costs.

Price formulation If a company deals with custom products, then it uses standard costs to compile the

projected cost of a customer’s requirements, after which it adds on a margin. This may be

quite a complex system, where the sales department uses a database of component costs

that change depending upon the unit quantity that the customer wants to order. This

system may also account for changes in the company’s production costs at different volume

levels, since this may call for the use of longer production runs that are less expensive.

Limitation of standard costing: Despite the advantages just noted for some applications of standard costing, there are

substantially more situations where it is not a viable costing system. Here are some

problem areas:

Cost-plus contracts If you have a contract with a customer under which the customer pays you for your costs

incurred, plus a profit (known as a cost-plus contract), then you must use actual costs, as

per the terms of the contract. Standard costing is not allowed.

Drives inappropriate activities A number of the variances reported under a standard costing system will drive

management to take incorrect actions to create favorable variances. For example, they may

buy raw materials in larger quantities in order to improve the purchase price variance,

even though this increases the investment in inventory. Similarly, management may

schedule longer production runs in order to improve the labor efficiency variance, even

though it is better to produce in smaller quantities and accept less labor efficiency in

exchange.

Fast-paced environment A standard costing system assumes that costs do not change much in the near term, so that

you can rely on standards for a number of months or even a year, before updating the costs.

However, in an environment where product lives are short or continuous improvement is

driving down costs, a standard cost may become out-of-date within a month or two.

Slow feedback A complex system of variance calculations are an integral part of a standard costing system,

which the accounting staff completes at the end of each reporting period. If the production

department is focused on immediate feedback of problems for instant correction, the

reporting of these variances is much too late to be useful.

Unit-level information The variance calculations that typically accompany a standard costing report are

accumulated in aggregate for a company’s entire production department, and so are unable

to provide information about discrepancies at a lower level, such as the individual work

cell, batch, or unit.

Chapter 3

Hypothetical Case of Budgeting

Fortuna Perfume Ltd.

31st July, 2016

Schedule 1:

Assumptions for Sales Budget

Budgeted Sales 500000 Unit

Quarter 1 100000 Unit

Quarter 2 200000 Unit

Quarter 3 100000 Unit

Quarter 4 100000 Unit

Selling Price 200 Taka

Percentage of sales on account 50%

Percentage of sales on Cash 50%

Account Receivable 500000 Taka

Fortuna Perfume Ltd.

31st July, 2016

Sales Budget

Quarter Total

1 2 3 4

Budgeted Sales Unit

100,000

200,000

100,000

100,000

500,000

Sales Price 180 180 180 180 180

Total Sales ( TK. )

18,000,000

36,000,000

18,000,000

18,000,000

90,000,000

Expected Cash Collection

Quarter Total

1 2 3 4

Beginning Account Receivable

8,000,000

8,000,000

1st Quarter 9,000,000

9,000,000

18,000,000

2nd Quarter 18,000,000

18,000,000

36,000,000

3rd Quarter 9,000,000

9,000,000

18,000,000

4th Quarter 9,000,000

9,000,000

Total Cash Collection 17000000 27,000,000

27,000,000

18,000,000

89,000,000

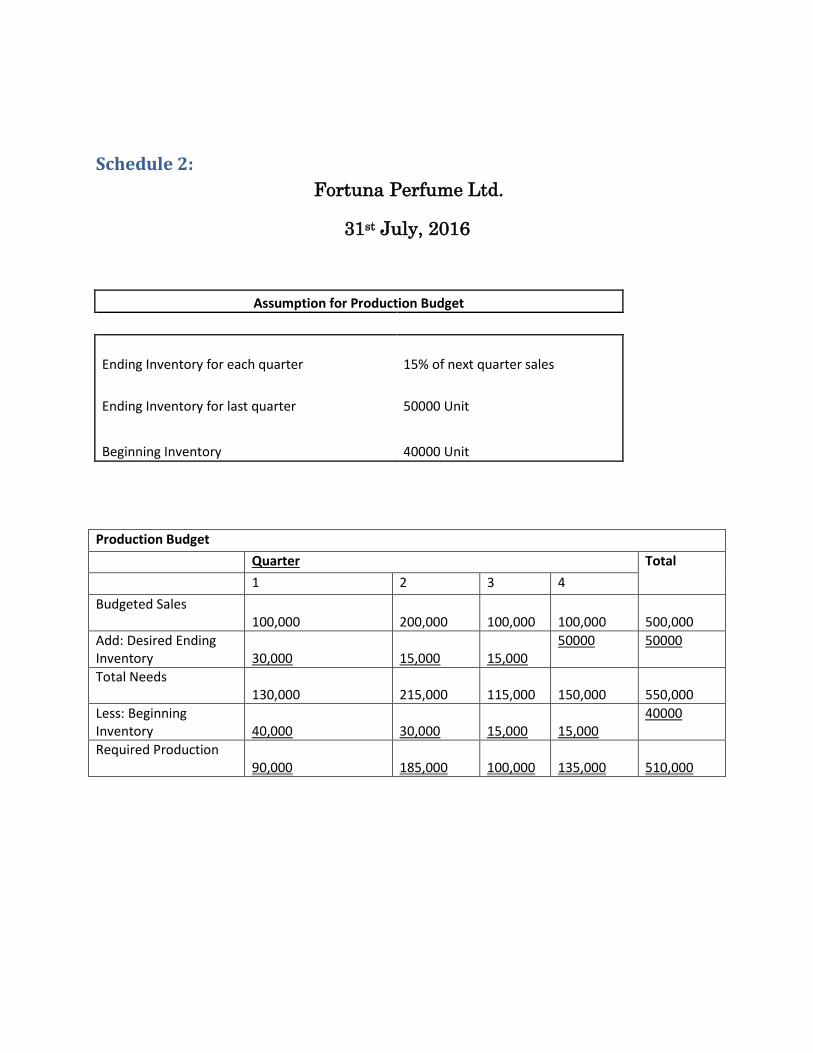

Schedule 2:

Fortuna Perfume Ltd.

31st July, 2016

Assumption for Production Budget

Ending Inventory for each quarter 15% of next quarter sales

Ending Inventory for last quarter 50000 Unit

Beginning Inventory 40000 Unit

Production Budget

Quarter Total

1 2 3 4

Budgeted Sales 100,000

200,000

100,000

100,000

500,000

Add: Desired Ending Inventory

30,000

15,000

15,000

50000 50000

Total Needs 130,000

215,000

115,000

150,000

550,000

Less: Beginning Inventory

40,000

30,000

15,000

15,000

40000

Required Production 90,000

185,000

100,000

135,000

510,000

Schedule 3:

Fortuna Perfume Ltd.

31st July, 2016

Assumption for Direct Material Budget

DM Needed Per Unit 10

Ending Inventory for each quarter 20% of Following Quarter

Beginning Inventory for each quarter 10% of Previous Quarter

Ending Inventory 500000

Beginning Inventory 400000

Percentage of buy on Cash 40%

Percentage of buy on Account 60%

Per Unit Price 6 TK.

A/C Payable 700000

Direct Material Budget

Quarter Total

1 2 3 4

Required Production 90,000

185,000

100,000

135,000

510,000

DM Needed Per Unit 10 10 10 10 10

Production Needs 900,000

1,850,000

1,000,000

1,350,000

5,100,000

Add: Ending Inventory 370,000

200,000

270,000

500000 500000

Total Needs 1,270,000

2,050,000

1,270,000

1,850,000

5,600,000

Less: Beginning Inventory

400000 370,000

200,000

270,000

400000

Raw Material to be Produced

870,000

1,680,000

1,070,000

1,580,000

5,200,000

Cost of RM per unit 6 6 6 6 6

Cost for RM 5,220,000

10,080,000

6,420,000

9,480,000

31,200,000

Expected Cash Payment

Quarter Total

1 2 3 4

Beginning Account Payable

700,000

700,000

1st Quarter 2,088,000

3,132,000

5,220,000

2nd Quarter 4,032,000

6,048,000

10,080,000

3rd Quarter 2,568,000

5,688,000

8,256,000

4th Quarter 3,792,000

3,792,000

Total Cash Collection 2788000 7,164,000

8,616,000

9,480,000

28,048,000

Schedule 4:

Fortuna Perfume Ltd.

31st July, 2016

Assumption for Direct Labor

Direct Labor per Unit 2

Cost per Unit 15

Direct Labor Budget

Quarter Total

1 2 3 4

Required Production

90,000

185,000

100,000

135,000

510,000

DL per Unit 2 2 2 2 2

Total Direct Labor

180,000

370,000

200,000

270,000

1,020,000

DL per Unit Cost 15 15 15 15 15

Total Cost 2,700,000

5,550,000

3,000,000

4,050,000

15,300,000

Schedule 5:

Fortuna Perfume Ltd.

31st July, 2016

Manufacturing Overhead Assumptions

Variable Manufacturing Overhead Rate 10

Fixed Manufacturing Overhead 1,000,000

Depreciation 500,000

Manufacturing Overhead Budget

Quarter Total

1 2 3 4

Budgeted Direct Labor 180,000

370,000

200,000

270,000

1,020,000

Variable Manufacturing Overhead Rate

10 10 10 10 10

Variable Manufacturing Overhead

1,800,000

3,700,000

2,000,000

2,700,000

10,200,000

Fixed Manufacturing Overhead

1000000 1000000 1000000 1000000 4000000

Total Manufacturing Overhead

2,800,000

4,700,000

3,000,000

3,700,000

14,200,000

Less: Depreciation 500,000

500000 500000 500000 2000000

Cash Disbursement for MO 2,300,000

4,200,000

2,500,000

3,200,000

12,200,000

Total Manufacturing Overhead 14,200,000

Budgeted Direct Labor Hour 1,020,000

Predetermined Overhead Rate 13.92

Schedule 6:

Fortuna Perfume Ltd.

31st July, 2016

Ending Finished Good Inventory Budget

Quantity Cost Total

Production Per Unit: 10 6 60

Direct Material 2 15 30

Direct Labor 2 13.92 27.84

Manufacturing Overhead

117.84

Unit Product Cost

Finished Goods Inventory:

Ending Finished Goods 3000

Per Unit Cost 117.84

Ending Finished Goods in TK.

353,529

Schedule 7:

Fortuna Perfume Ltd.

31st July, 2016

Assumption for Selling & Administrative Budget

Variable selling and administrative cost 10

Advertising 200000

Executive Salaries 500000

Insurance 100000

Property Tax 40000

Depreciation 60000

Selling & Administrative Budget

Quarter Total

1 2 3 4

Budgeted Sales Unit 100,000

200,000

100,000

100,000

500,000

Variable selling and administrative cost

10 10 10 10 10

Variable selling and administrative cost

1,000,000

2,000,000

1,000,000

1,000,000

5,000,000

Fixed Selling & Administrative Expense:

Advertising 200000 200000 200000 200000 800000

Executive Salaries 500000 500000 500000 500000 2000000

Insurance 100000 100000 100000 100000 400000

Property Tax 40000 40000 40000 40000 160000

Depreciation 60000 60000 60000 60000 240000

Total Fixed Selling & Administrative Expense

900000 900000 900000 900000 3600000

Total Selling & Administrative Expense

1,900,000

2,900,000

1,900,000

1,900,000

8,600,000

Less: Depriciation 60000 60000 60000 60000 240000

Cash Disbursement for selling & administrative Expense

1,840,000

2,840,000

1,840,000

1,840,000

8,360,000

Schedule 8: Fortuna Perfume Ltd.

31st July, 2016

Cash Budget

For the Year Ended December31,

Quarter Total

1 2 3 4

Cash & bank balance beginning

1,500,000

8,372,000

15,118,000

25,662,000

1,500,000

Add receipts:

Collections from customers 17,000,000

27,000,000

27,000,000

18,000,000

89,000,000

Total cash available 18,500,000

35,372,000

42,118,000

43,662,000

90,500,000

Less disbursements

Direct materials 2,788,000

7,164,000

8,616,000

9,480,000

28,048,000

Direct labor 2,700,000

5,550,000

3,000,000

4,050,000

15,300,000

Manufacturing overhead 2,800,000

4,700,000

3,000,000

3,700,000

14,200,000

Selling and administrative 1,840,000

2,840,000

1,840,000

1,840,000

8,360,000

Equipment purchase 10,000,000

10,000,000

Total disbursments 20,128,000

20,254,000

16,456,000

19,070,000

75,908,000

Excess(deficiency) of cash (1,628,000)

15,118,000

25,662,000

24,592,000

14,592,000

Borrowings(at the begaining of the quarter)

10,000,000

10,000,000

Repayments (10,000,000)

(10,000,000)

Interest (1,200,000)

(1,200,000)

Total financing 10,000,000

-12000000

Cash balance,ending 8,372,000

15,118,000

25,662,000

13,392,000

13,392,000

Schedule 9:

Fortuna Perfume Ltd.

31st July, 2016

Income Statement

For the Year Ended December 31,

BDT

Sales 90,000,000

Cost of goods sold 65,902,200

Gross margin 24,097,800

Selling and administrative expense 8,360,000

Net operating income 15,737,800

Interest expense 1,200,000

Net income 14,537,800

Schedule 10:

Fortuna Perfume Ltd.

Balance Sheet

31st July, 2016

Balance Sheet

As on December 31,2016

BDT

Current Assets:

Cash & bank balance 13,392,000

Accounts receivable 9,000,000

Raw materials inventory 3,000,000

Finished goods inventory 353,529

Total current assets

25,745,529

Plant & equipment

Land 5,000,000

Buildings and equipment 40,000,000

45,000,000

Accumulated depreciation 2,240,000

Plant & equipment net

42,760,000

Total assets 68,505,529

Liabilities& owners’ equity

Current liabilities:

Accounts payable

5,688,000

Long-term loan

10,000,000

Stockholders’ equity

Common stock 7,000,000

Retained earnings 12,491,660

Total stockholder equity

19,491,660

Total liabilities & stockholder equity 35,179,660

Chapter 4

Comparison between actual and standard

operation

Direct Material Variance

Direct Labor Variance

Actual Material Unit 31,250,000

Actual Price 6.05

Standard Material 31,200,000

Standard Price 6

AQ*AP 189,062,500

AQ*SP 187,500,000

SQ*SP 187,200,000

Price Varience 1,562,500

Quantity Varience 300,000

Total Varience 1,862,500

Direct Material Varience

Actual Hour 15,295,000

Actual Price 14.75

Standard Hour 15,300,000

Stardard Price 15

AH*AP 225,601,250

AH*SP 229,425,000

SH*SP 229,500,000

Price Varience (3,823,750)

Quantity Varience (75,000)

Total Varience (3,898,750)

Direct Labor Varience

Variable Overhead Variance

Actual Hour 14205000

Actual Price 9.75

Standard Hour 14,200,000

Stardard Price 10

AH*AP 138,498,750

AH*SP 142,050,000

SH*SP 142,000,000

Price Varience (3,551,250)

Quantity Varience 50,000

Total Varience (3,501,250)

Varience of Manufacturing Overhead

Conclusion:

A budget is a quantitative expression of a plan for a defined period of time. It includes

planned sales volumes and revenues, resource quantities, costs and expenses, assets,

liabilities and cash flows. It expresses strategic plans of business units, organizations,

activities or events in measurable terms. It should be properly managed or the

organizational goals cannot be gained. . Planning is accomplished through the preparation of a

number of budgets, which, when brought through, from an integrated business plan known as

master budget. The master budget is an essential management tool that communicates

management’s plan throughout the organization, allocates resources, and coordinates activities.

Budget should be logical and have basement for historical data. In a budget, we need to

consider future possibilities as well as the future threat that can affect company’s

operation. This will help mangers to accomplish their decisions.