progress and issues in ambif discussion prof. shigehito inukai with matthias schmidt adb consultants...

TRANSCRIPT

Progress and Issues in AMBIF Discussion

Prof. Shigehito Inukai

with Matthias SchmidtADB Consultants

13th ABMF Meeting, Tokyo, 25 July 20131

V.2_as at 12 July 2013Not Final (For ABMF-J)

Proposed Agenda① Support for Interim Report from AFMCGM

② Additional Information since Interim Report

③ Addressing Regulatory Concerns

④ Detailing AMBIF Components

⑤ Documentation - Creation of Voluntary ADRB

⑥ Update on Information Platform

⑦ Proposed Phase 3 Activities

⑧ Introduction of ADRB (Voluntary working group for making recommendations on AMBIF Documentation)

⑨ Questions & Answers (in Session 2)

2

① Support for Interim Report from AFMCGM

3

AMBIF Focus is shifting• Basic AMBIF Components agreed in principle• Necessary detailing in progress• Additional information as discussed• Focus on AMBIF Documentation as key

component for implementation based on possible demand expectations

• Focus on possible approaches to AMBIF implementation with regulatory authorities

4

Phase 2 Interim Report – SF1

• Submitted to ABMI on 25 April 2013• Acknowledged by AFMCGM on 2 May

2013, support mentioned for ABMF’s present and future activities

5

② Additional Information relevant for AMBIF since Interim Report

6

Proposed AMBIF Market(s) or Segment(s) for Consideration

Economy Type of Market Candidate MarketProfessional Market as

a result ofParticipation of

Market governed by

SROAccessible to Foreign Institutional Investors

PR China

Issuing & Secondary

Inter-Bank Bond Market (IBBM)

Access/ParticipationInstitutional Investors

PBOC NAFMII via QFII

(Issuing &

Secondary)(Qualified Foreign

Institutional Investor)(Regulation) (QFIIs, B/Ds) (CSRC) (SSE) (YES)

Hong Kong

Issuing HKEx Market PracticeProfessional

InvestorsSFC, HKEx HKEx YES

Issuing & Secondary

OTC Market PracticeProfessional

InvestorsSFC, HKMA - YES

Indonesia MTN Issuing (Private Placement) Market PracticeMarket

Participants- - YES

Japan Issuing Tokyo PRO-BOND Law (FIEA)Specified Investors

FSA, TSE TSE, JSDA YES

KoreaSME + SME

Foreign Issuers Issuances

QIB Market Decree to FSCMAQualified

Institiutional Buyers

KOFIA (FSS) KOFIA Not at the moment

IssuingPrivate PlacementFSCMA defines this

marketMarket Practice

Professional Investors

(KOFIA) (KOFIA) YES

Malaysia

Issuing & Secondary

Excluded Offers Law (CMSA)Sophisticated

InvestorsSC Malaysia - YES

Issuing

Exempt Regime (Listings only)

MembershipInstitutional Investors

Bursa Malaysia - YES

Philippines

Issuing & Secondary

Qualified Investor / Qualified Buyer

MarketParticipation

Qualified Investors /

Qualified BuyersSEC PDEx YES

Singapore

Issuing & Secondary

OTC Market PracticeInstitutional Investors

SGX - YES

Thailand

Issuing & Secondary

Private Placement under AI Regime /

OTCThai SEC Regulation

Accredited Investors (AI, includes II &

HNW))

SEC ThaiBMA YES

Viet Nam

Issuing & Secondary

(Private Placement) LawProfessional

InvestorsSSC (VBMA) YES

7

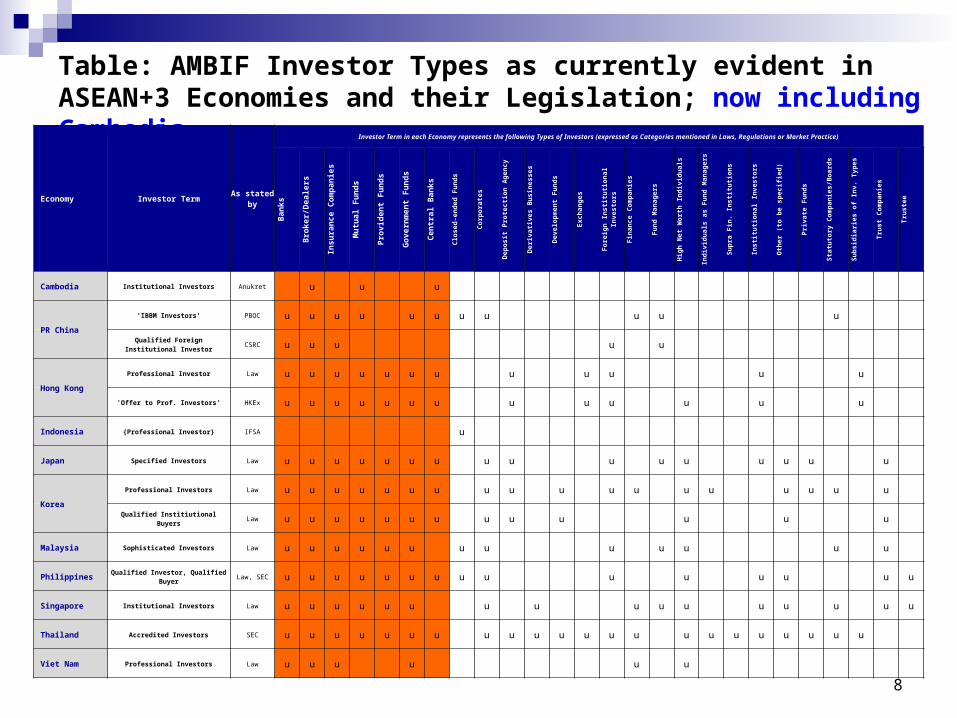

Table: AMBIF Investor Types as currently evident in ASEAN+3 Economies and their Legislation; now including Cambodia

8

Economy Investor TermAs stated

by

Investor Term in each Economy represents the following Types of Investors (expressed as Categories mentioned in Laws, Regulations or Market Practice)

Banks

Broker/

Dealers

Insurance Companies

Mutual

Funds

Provident Fund

s

Governmen

t Fund

s

Central

Banks

Closed-ended Funds

Corporates

Deposit

Protection

Agency

Derivatives

Businesses

Development Funds

Exchanges

Foreign

Institutional

Investors

Finance

Companies

Fund Manag

ers

High Net

Worth Individ

uals

Individuals as Fund

Managers

Supra Fin.

Institutions

Institutional

Investors

Other (to be specifi

ed)Private Funds

Statutory

Companies/Boards

Subsidiaries of Inv. Types

Trust Compa

nies Trustee

Cambodia Institutional Investors Anukret u u u

PR China

'IBBM Investors' PBOC u u u u u u u u u u u

Qualified Foreign Institutional Investor

CSRC u u u u u

Hong Kong

Professional Investor Law u u u u u u u u u u u u

'Offer to Prof. Investors' HKEx u u u u u u u u u u u u u

Indonesia {Professional Investor} IFSA u

Japan Specified Investors Law u u u u u u u u u u u u u u u u

Korea

Professional Investors Law u u u u u u u u u u u u u u u u u u

Qualified Institiutional Buyers Law u u u u u u u u u u u u u

Malaysia Sophisticated Investors Law u u u u u u u u u u u u u

Philippines Qualified Investor, Qualified Buyer Law, SEC u u u u u u u u u u u u u u u

Singapore Institutional Investors Law u u u u u u u u u u u u u u u u

Thailand Accredited Investors SEC u u u u u u u u u u u u u u u u u u u u u u

Viet Nam Professional Investors Law u u u u u u

Issuance Cost: Update

Context: Members’ request to quantify potential AMBIF benefits

Many thanks go to Deutsche Bank, HSBC! Obtained significant amount of information For both international and regional markets Some initial observations on next page

9

Issuance Cost: Initial Observations• Typically: international > domestic markets • Since domestic market issuance not required

to tap typical international services• Further normalisation needed because:

• Markets’ practices, cost components differ• Cost assumptions are solid but may not be

directly comparable to AMBIF features

May need to differentiate between current and AMBIF issuance to determine suitable cost components

10

Accounting/Reporting Standards• Considered a challenge in context of AMBIF,

based on market visit feedback• Thought to be addressed via IFRS (International

Financial Reporting Standards)

• However, research to date indicates that acceptance is slowing and direct applicability of IFRS may be limited

• Instead, markets and listing places appear willing to accept multiple standards

• Phase 2 Report to reflect this11

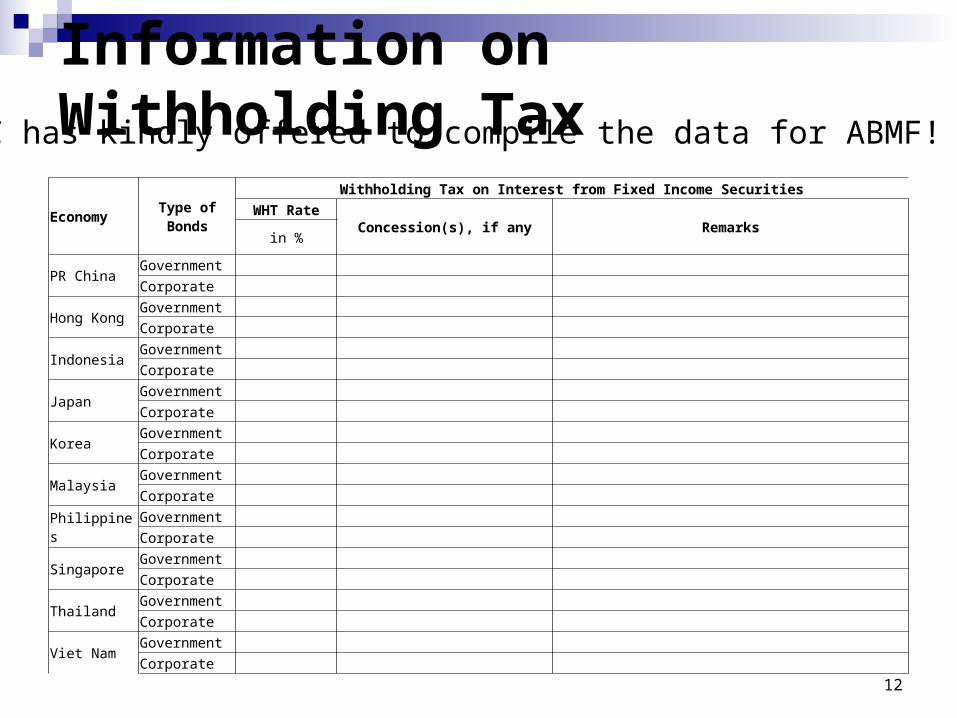

Information on Withholding Tax

12

PWC has kindly offered to compile the data for ABMF!

Economy Type of BondsWithholding Tax on Interest from Fixed Income Securities

WHT RateConcession(s), if any Remarks

in %

PR ChinaGovernment Corporate

Hong KongGovernment Corporate

IndonesiaGovernment Corporate

JapanGovernment Corporate

KoreaGovernment Corporate

MalaysiaGovernment Corporate

PhilippinesGovernment Corporate

SingaporeGovernment Corporate

ThailandGovernment Corporate

Viet NamGovernment Corporate

Information on Withholding Tax

Envisaged withholding tax (WHT) information for members’ information and consideration:

• Headline (official) tax rates• Concessionary rates, as may exist• Details on concessions

13

14

③ Addressing Regulatory Concerns and Feedback

Regulatory Concerns/Feedback

• Regulatory mandate to be confirmed• Suitable regulatory process, taking into

consideration market-specific regulatory processes (many/none), multiple regulators

• Understanding of investor types for AMBIF• Practical issues on regulatory process• Approach to AMBIF Implementation• One possible Adoption of AMBIF

15

16

Possible AMBIF Regulatory Processes

Using Typical Modalities of Standardizing Regulations

Degree of standardization Strong

Fea

sibi

lity

Diff

icul

t

Harmonization

Mutual Agreement

Acceptance of Equivalence

Mutual Recognition

Substituted Compliance

Target Area

16

Understanding AMBIF Investors

Will be addressed in next Chapter

17

Practical Considerations

Please refer to Information Platform

18

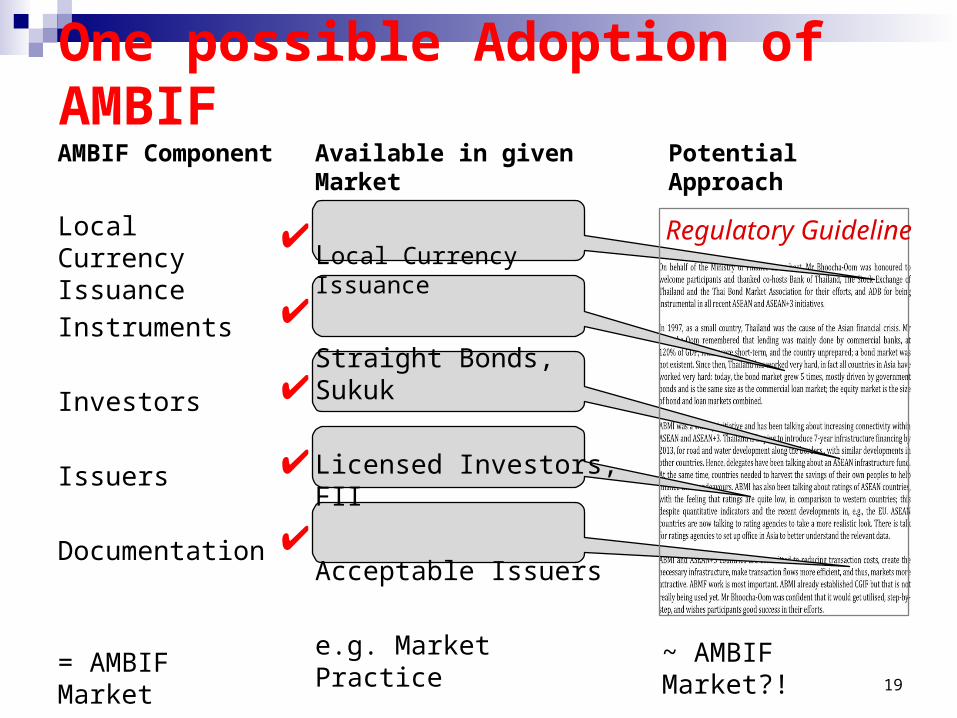

One possible Adoption of AMBIFAMBIF Component

Local Currency Issuance

Instruments

Investors

Issuers

Documentation

= AMBIF Market

19

Available in given Market

Local Currency Issuance

Straight Bonds, Sukuk

Licensed Investors, FII

Acceptable Issuers

e.g. Market Practice

Prerequisites in place?

Potential Approach

Regulatory Guideline

~ AMBIF Market?!

✔

✔

✔

✔

✔

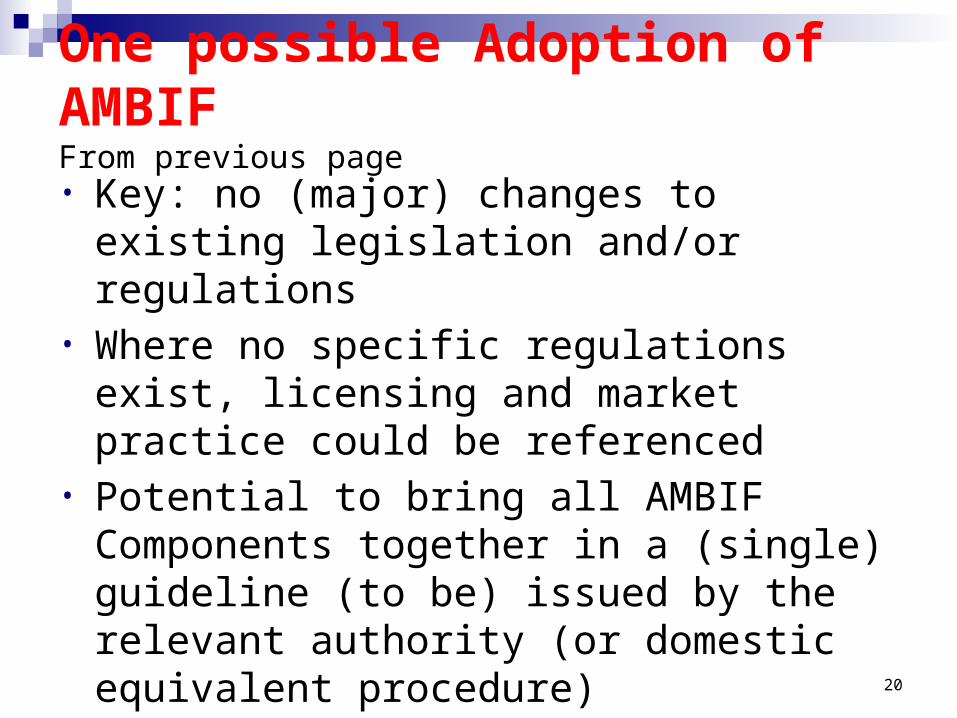

One possible Adoption of AMBIFFrom previous page

• Key: no (major) changes to existing legislation and/or regulations

• Where no specific regulations exist, licensing and market practice could be referenced

• Potential to bring all AMBIF Components together in a (single) guideline (to be) issued by the relevant authority (or domestic equivalent procedure)

• Related guideline may be issued by authority

20

21

④ Detailing AMBIF Components

AMBIF Instruments in Local Currency

• No strong opinions recorded on proposed instruments or local currency issuance, but would like to confirm with members:

Straight bonds and Sukuk? Intention not to prevent issuance in foreign

currencies• Being other ASEAN+3 local currencies• Being e.g. USD or EUR

22

AMBIF Investors: Clarification• Proposed AMBIF Investor type:

Investment Advisory Businesses

• Investor type meant to represent member economies varying definitions of professional• Asset managers• Fund managers• Investment advisors• Investment managers• Mutual Funds / Unit Trusts

Not intended to unify, but to be inclusive23

AMBIF Investors - FII

• Interim Report: no intended limitations or restrictions for Foreign Institutional Investors (FII), other than those in place

• FII may be seen as representing potentially significant demand for each domestic AMBIF bond issuance

• FII = investors from other ASEAN+3 markets as well

24

AMBIF Issuers

• No objection or feedback on AMBIF Issuers so far, but further detailing desired• Who may be interested to issue?• What may be their considerations?

• Other relevant information

Intention to provide more detailed info by 14th ABMF

25

26

⑤ Documentation – Creation of Voluntary ADRB

Update on AMBIF Documents

• Creation of Voluntary “Asian Common Professional Bond Market Practices and Documentation Recommendation Board” (ADRB or AMBIF-PDRB) by market practitioners

• Types of docs at present• Basic objectives

27

Expression of General Interest between Markets- Sample / To be checked with Market Sources

28

Issuers’ Home Market

PR China Hong Kong

Indonesia Japan Korea Malaysia Philippines

Singapore

Thailand Viet Nam

Issuing Market

PR China ○ ○ ○Hong Kong ○ ○ ○Indonesia ○ ○Japan ○ ○Korea ○ ○ ○Malaysia ○ ○Philippines ○Singapore ○ ○Thailand ○ ○Viet Nam ○

Above matrix is just an image.

29

⑥ Update on proposed Information Platform

(Based on Dr. Hyun’s Idea)

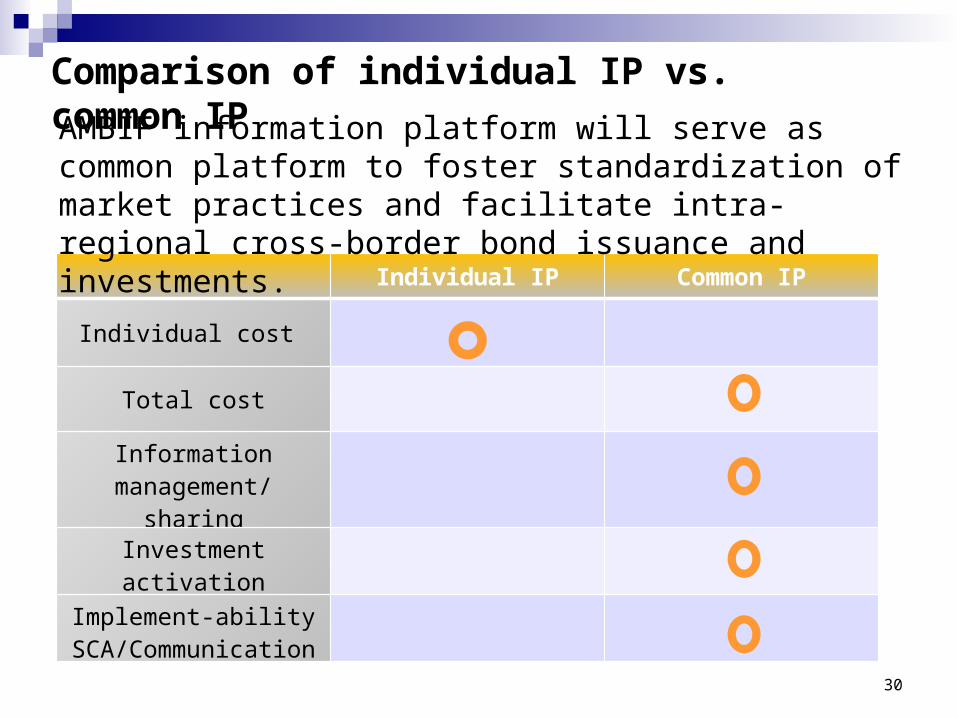

Comparison of individual IP vs. common IP

Individual IP Common IP

Individual cost

Total cost

Information manage-ment/

sharing

Investment activation

Implement-abilitySCA/Communication

AMBIF information platform will serve as common platform to foster standardization of market practices and facilitate intra-regional cross-border bond issuance and investments.

30

Function of Common AMBIF Information Platform

:

:

:

• Common Infrastructure for AMBIF Market:

common infrastructure for ASEAN+3 members in AMBIF Market

• Information Sharing System for AMBIF Bond:

collect and distribute information of ASEAN+3 AMBIF Bond

• Supportive System for Substituted Compliance Approach:

facilitate communication and mutual understanding among ASEAN+3 regulators

• Management System for AMBIF Market:

manage all relevant information of regulatory process and qualification of market participants

31

Next Step for Discussion• The Establishment of AMBIF Information Platform Board

working together with ADRB as may be required• Study process flow of bond issuance in countries with

existing IP (Malaysia, Indonesia, Thailand, Japan, Korea etc)

• Standardize process flow and issuance documents submitted to regulators to implement AMBIF

32

Remainder of Phase 2

13th ABMFTOKYO Meeting

14th ABMF JEJU Meeting

Phase 2 Report Publication

25/26 July 6/7 Nov Dec 2013

Draft Phase 2 Report; AMBIF Conclusions

16-19 Oct

SIBOSDubai

33

Participation by ADB Secretariat

Editing, formatting final Phase 2 Report

&Gathering

of Information for Phase 1 Updates

34

⑦ Proposed Phase 3 Activities

Phase 3 - Proposed Activities

• Phase 1 Market Guides Report Updates• AMBIF Implementation• Pilot Issue• BCLMV Knowledge Support

35

Phase 3 – Market Guide Update

• Envisaged for Q1, 2014

• Members are kindly requested to review and provide updates, necessary revisions by end December 2013

• Use of SWIFT request form, process• Publication target: April 2014, since

second anniversary of original report + to be in time for next AFMCGM in May 2014

36

Phase 3 – AMBIF Implementation

• Key: decision by regulatory bodies or delegated authorities on AMBIF Markets

• Compilation of agreed AMBIF Components, Substituted Compliance Approach and proposed processes, for use and reference in above decisions

• Roll out by/in individual markets• ABMF to create awareness in markets

37

Phase 3 – Proposed Pilot Issue

• Key: AMBIF in place• Opportunity to work through existing and

future issues or challenges with pilot participants

• May induce fine tuning of AMBIF

38

Phase 3 – BCLMV Knowledge Support

• Expected follow-up to Phase 2 support• Dependent on markets’ specific requests• Support creation/update of Cambodia and

other Economies’ market guides

39

40

⑧ Introduction of ADRB (Voluntary working group for making recommendations on AMBIF Documentation)

By Mr. Suzuki of Barclays and Mr. Yanase of NO&T

Prof. Shigehito Inukai

Faculty of Law - Waseda University

1-6-1 Nishiwaseda, Shinjuku-ku

Tokyo 169-8050

Office +81 3 3202 2472

Mobile +81 80 3360 7551

41

Matthias Schmidt

ADB Consultant

Office +61 3 95571314

Mobile +61 423 708910

42

⑨ Questions & Answers

(Session 2)