promo review romania jan - sept 2012 vs 2011

TRANSCRIPT

Jan-Sept 2012 vs 2011

PROMO

Promo Review of food retailers in 20’top

ReviewJan-Sept 2012 vs

2011

Jan-Sept 2012 vs 2011

RETAILERS SUMMARY

QUANTITATIV KPI Slides

1- LEAFLETS & PROMO OPERATIONS 4-14

60-72

4- PROMO MECHANISMS 50-56

3- PROMO PRESSURE & SHARE OF VOICE

34-49

2- TRADE STRATEGY 15-33

QUALITY KPI 57-59

CONTENT :

Promo Review of food retailers in 20’top

Jan-Sept 2012 vs 2011

VOCABULARY• Promo Pressure: index of promo visibility for a retailer, a category a brand or a format. This

index can be counted by quantity of leaflets or quantity of promotions inside the leaflets.

• Share of Voice: index of promo visibility for a retailer, a category a brand or a format in relative value versus competitors. The Share of Voice index of Hipercom shows the promo activity of the Retailers in the most exhaustive way, taking into consideration the quantity of promotional operations, SKU’s or SNU in Promo, the commercial space (in m2) when the promotion was valid and the number of days of the validity days of that specific promotion.

• Shopper Need Unit ( SNU): One or more SKU from the same family, being on the same promotion (many flavors for juice, many colors for shampoo, many sizes for textile)

• Consumer advantages: All additional trade mechanisms supporting the promo price and mentioned on the promo leaflet.

•Promo price: Price on the leaflet (should be different from the shelf price) •Virtual Price: Promo price – (minus) all consumers advantages •Perimeter of analysis: Romania: CC, Hyper, Super, HDD (Analysis for the Top 20 Retailers of this category)

Jan-Sept 2012 vs 2011

PROMOReview

Promo Review of food retailers in 20’top

1- LEAFLETS & PROMO OPERATIONS

Jan-Sept 2012 vs 2011

Jan-Sept 2012 vs 2011

LEAFLETS & PROMO PRESSURE (traffic leaflets)

NATIONALS OP

REGIONAL OP

Jan-Sept 2012

Jan-Sept 2011

Evolution Pressure

We see that the retailers prefer to investIn regional PO in 2012

*A Promo Operation is a set of leaflets issued by a store network. This set could consist of one leaflet till 25 or more regional variations

367 387 -5% -10%

76 34 124% 112%

* Quantity of leaflets 2012 vs 2011. All traffic leaflets = 100%.

Jan-Sept 2012 vs 2011

LEAFLETS & PROMO PRESSURE (traffic leaflets)

NATIONALS OP

REGIONAL OP

45

24

39

32

( Nationals PO) Jan-

Sept2012(evol) HM SM( Nationals PO) Jan-Sept2012(evol)

+15 (PO)

-2 (PO)41

26

20

18

+1 (PO)

*A Promo Operation is a set of leaflets issued by a store network. This set could consist of one leaflet till 25 or more regional variations

+5 (PO)

367 387 -5% -10%

76 34 124% 112%

Jan-Sept 2012

Jan-Sept 2011

Evolution Pressure

+5 (PO)

* Quantity of leaflets 2012 vs 2011. All traffic leaflets = 100%.

+18(PO)

+5 (PO)

Jan-Sept 2012 vs 2011

LEAFLETS & PROMO PRESSURE (traffic leaflets)

NATIONALS PO

REGIONAL PO

C&C HD34

29

36

39

( Nationals PO) Jan-

Sept2012(evol) ( Nationals PO) Jan-

Sept2012(evol) +23(PO)

*A Promo Operation is a set of leaflets issued by a store network. This set could consist of one leaflet till 25 or more regional variations

367 387 -5% -10%

76 34 124% 112%

Jan-Sept 2012

Jan-Sept 2011

Evolution Pressure

-6 (PO)

+2 (PO)

* Quantity of leaflets 2012 vs 2011. All traffic leaflets = 100%.

-3 (PO)

Jan-Sept 2012 vs 2011

5 TOP TRAFFIC LEAFLET (by PO Share of Voice)

Number of SNU 935 484 404426 416Stores 19 8 824 24Days 31 11 1413 13Benchmark vs

Leader 100% 52% 43%46% 44%

Jan-Sept 2012 vs 2011

NUMBER OF PROMO OPERATIONS (traffic leaflets)

Almost all the retailers increased their quantity of leaflet edition.

45

41

39

39

36

34

32

29

26

24

20

18

+15 po

+5 po

+1 po

+23 po

-6 po

+2 po

+5 po

-3 po

+18 po

-2 po

+5 po

Jan-Sept 2012 vs 2011

81

72

21

20

10

10

4

4

3

3

2

1

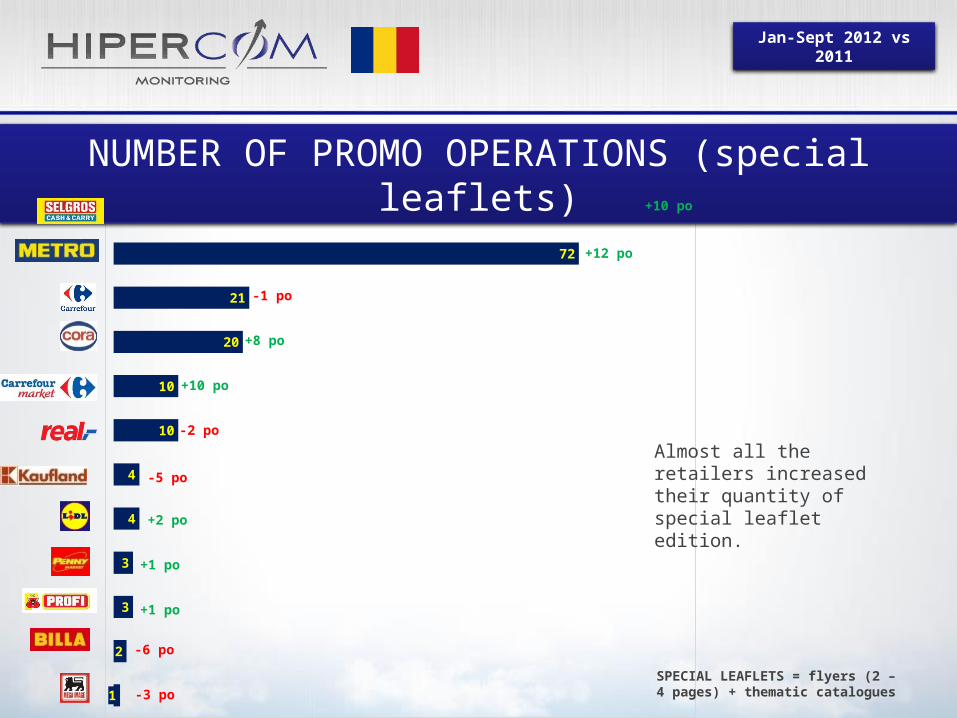

NUMBER OF PROMO OPERATIONS (special leaflets)

Almost all the retailers increased their quantity of special leaflet edition.

+10 po

+12 po

-1 po

+8 po

+10 po

-2 po

-5 po

+2 po

+1 po

+1 po

-6 po

-3 poSPECIAL LEAFLETS = flyers (2 – 4 pages) + thematic catalogues

Jan-Sept 2012 vs 2011

45 pag

31 pag

27 pag

25 pag

18 pag

16 pag

16 pag

13 pag

12 pag

12 pag

10 pag

4 pag

AVERAGE NUMBER OF PAGES/PROMO OP (traffic leaflets)

The number of pages per PO is decreasing or increasing. Only Penny, Cora and Carrefour Market are constant. We can see the most Significant cost cutting in REAL.

2 pag

-6 pag

2 pag

-1 pag

6 pag

2 pag

1 pag

3 pag

1 pag

Jan-Sept 2012 vs 2011

26 pag

22 pag

21 pag

20 pag

18 pag

9 pag

9 pag

7 pag

5 pag

4 pag

4 pag

3 pag

AVERAGE NUMBER OF PAGES/PROMO OP (special leaflets)

The number of pages per PO is decreasing or increasing. Only Cora and Carrefour Market are constant. We can see the mostSignificant cost cutting in PENNY, METRO & REAL.

-3 pag

-6 pag

-7 pag

-2 pag

6 pag

-8 pag

-3 pag

-5 pag

-2 pag

-2 pag

SPECIAL LEAFLETS = flyers (2 – 4 pages) + thematic catalogues

Jan-Sept 2012 vs 2011

Average SNU/page (traffic leaflets)

Number of SNU/page

The most readable is

Selgros

5.9

6.1

6.2

8.1

8.5

9.3

9.4

9.8

9.9

10.6

20.0

20.5

SNU/ page

SNU/ page

SNU/ page

SNU/ page

SNU/ page

SNU/ page

SNU/ page

SNU/ page

SNU/ page

SNU/ page

SNU/ page

SNU/ page

Jan-Sept 2012 vs 2011

Average SNU/page (special leaflets)

Number of SNU/page

The most readable is LIDL

3.8

4.4

5.0

5.5

6.0

6.4

6.8

8.3

10.8

11.4

11.5

14.9

SNU/ page

SNU/ page

SNU/ page

SNU/ page

SNU/ page

SNU/ page

SNU/ page

SNU/ page

SNU/ page

SNU/ page

SNU/ page

SNU/ page

Jan-Sept 2012 vs 2011

2012 vs 2011

PROMOReview

Promo Review of food retailers in 20’top

2 - TRADE STRATEGY

Jan-Sept 2012 vs 2011

Brands

Private Label

Unbranded

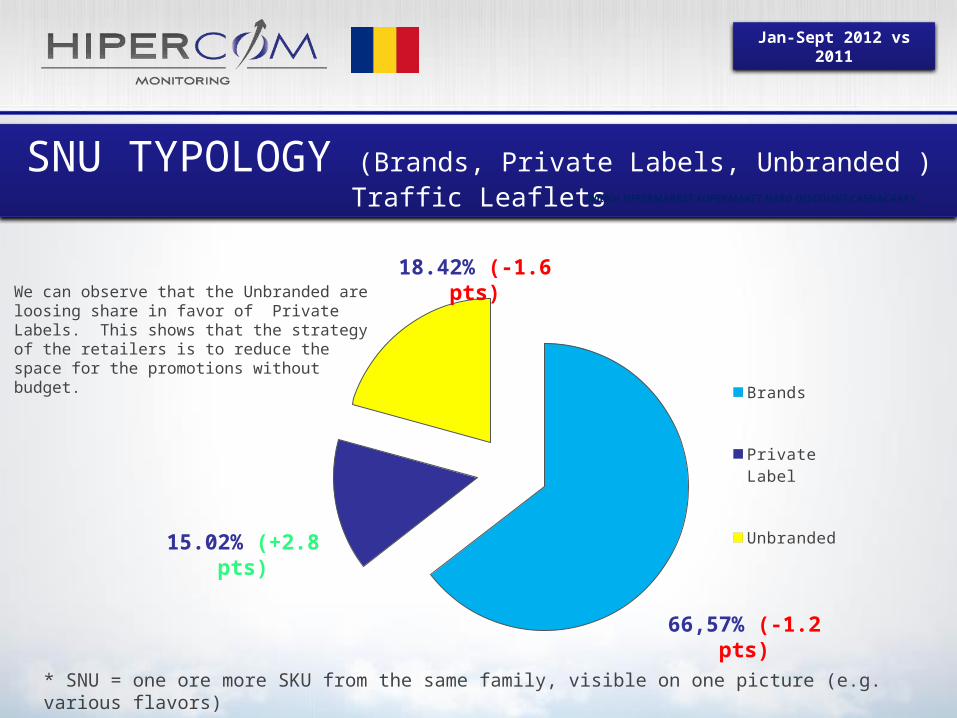

SNU TYPOLOGY (Brands, Private Labels, Unbranded ) Traffic Leaflets

66,57% (-1.2 pts)

15.02% (+2.8 pts)

18.42% (-1.6 pts)

Within HIPERMARKET,SUPERMAKET,HARD DISCOUNT,CASH&CARRY

We can observe that the Unbranded are loosing share in favor of Private Labels. This shows that the strategy of the retailers is to reduce the space for the promotions without budget.

* SNU = one ore more SKU from the same family, visible on one picture (e.g. various flavors)

Jan-Sept 2012 vs 2011

SNU TYPOLOGY (National Brands) Traffic LeafletsNumberSNU/OP

National Brands Private Label UnbrandedEvolution Jan-Sept 2012

vs 2011

* SNU = one ore more SKU from the same family, visible on one picture (e.g. various flavors)

187 ref

355 ref

225 ref

264 ref

148 ref

197 ref

33 ref

57 ref

98 ref

144 ref

235 ref

245 ref

63,85%

(-1,7 pts)

60,60%

(0,9 pts)

54,40%

(1,8 pts)

60,96%

(-0,4 pts)

74,56%

(1,1 pts)

84,66%

(1,3 pts)

67,87%

(19,7 pts)

75,61%

(-0,8 pts)

6,52%(1,6 pts)

67,63%

(4,2 pts)

77,01%

(7,4 pts)

90,95%

(0,5 pts)

-26

38

16

-43

7

82

9

14

34

2

50

16

Jan-Sept 2012 vs 2011

SNU TYPOLOGY (Private Label) Traffic LeafletsNumberSNU/OP

National Brands Private Label UnbrandedEvolution Jan-Sept 2012

vs 2011

* SNU = one ore more SKU from the same family, visible on one picture (e.g. various flavors)

12,30% (0,2 pts)

12,39% (-0,6 pts)

15,08% (-1 pts)

10,94% (0,6 pts)

8,03% (0,8 pts)

14,07% (0,2 pts)

17,29%(-15,5 pts)

6,87% (2,3 pts)

82,69% (-0,2 pts)

14,44% (-0,4 pts)

16,80% (-1,9 pts)

4,34% (-1 pts)

187 ref

355 ref

225 ref

264 ref

148 ref

197 ref

33 ref

57 ref

98 ref

144 ref

235 ref

245 ref

63,85%

(-1,7 pts)

60,60%

(0,9 pts)

54,40%

(1,8 pts)

60,96%

(-0,4 pts)

74,56%

(1,1 pts)

84,66%

(1,3 pts)

67,87%

(19,7 pts)

75,61%

(-0,8 pts)

6,52%(1,6 pts)

67,63%

(4,2 pts)

77,01%

(7,4 pts)

90,95%

(0,5 pts)

-26

38

16

-43

7

82

9

14

34

2

50

16

Jan-Sept 2012 vs 2011

SNU TYPOLOGY (Unbranded) Traffic LeafletsNumberSNU/OP

National Brands Private Label UnbrandedEvolution Jan-Sept 2012

vs 2011

* SNU = one ore more SKU from the same family, visible on one picture (e.g. various flavors)

12,30% (0,2 pts)

12,39% (-0,6 pts)

15,08% (-1 pts)

10,94% (0,6 pts)

8,03% (0,8 pts)

14,07% (0,2 pts)

17,29%(-15,5 pts)

6,87% (2,3 pts)

82,69% (-0,2 pts)

14,44% (-0,4 pts)

16,80% (-1,9 pts)

4,34% (-1 pts)

23,85%(1,5 pts)

27,01%(-0,3 pts)

30,52%(-0,8 pts)

28,10%(-0,2 pts)

17,40%(-1,9 pts)

1,27%(-1,5 pts)

14,84%(-4,1 pts)

17,52%(-1,5 pts)

10,79%(-1,4 pts)

17,93%(-3,8 pts)

6,19%(-5,4 pts)

4,71%(0,4 pts)

187 ref

355 ref

225 ref

264 ref

148 ref

197 ref

33 ref

57 ref

98 ref

144 ref

235 ref

245 ref

63,85%

(-1,7 pts)

60,60%

(0,9 pts)

54,40%

(1,8 pts)

60,96%

(-0,4 pts)

74,56%

(1,1 pts)

84,66%

(1,3 pts)

67,87%

(19,7 pts)

75,61%

(-0,8 pts)

6,52%(1,6 pts)

67,63%

(4,2 pts)

77,01%

(7,4 pts)

90,95%

(0,5 pts)

-26

38

16

-43

7

82

9

14

34

2

50

16

Jan-Sept 2012 vs 2011

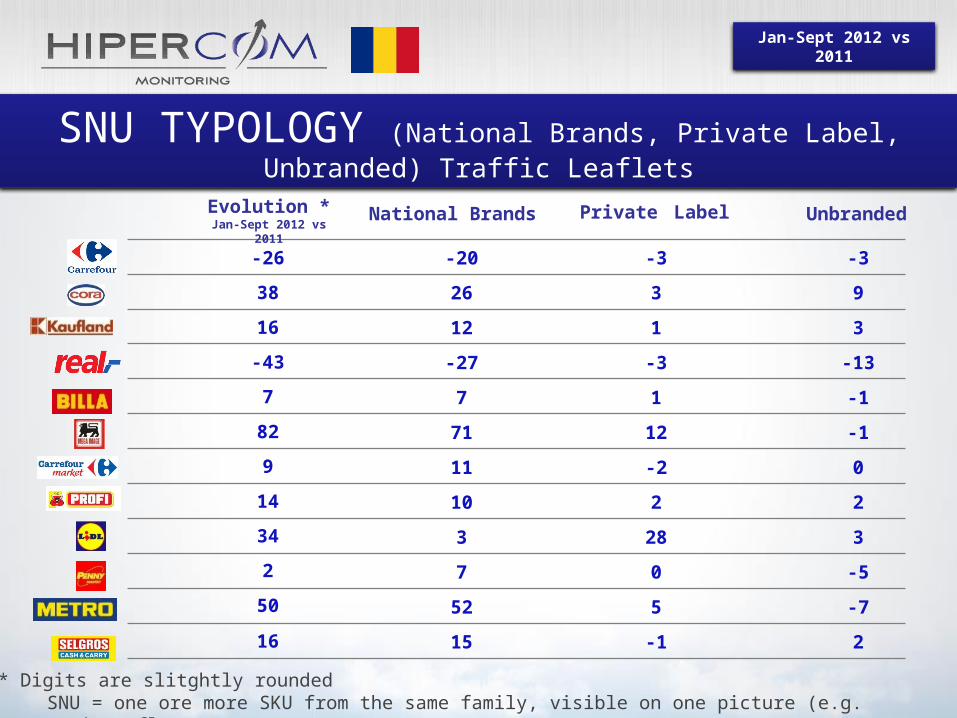

SNU TYPOLOGY (National Brands, Private Label, Unbranded) Traffic Leaflets

National Brands

SNU = one ore more SKU from the same family, visible on one picture (e.g. various flavors)

Private Label UnbrandedEvolution *Jan-Sept 2012 vs

2011

-26

38

16

-43

7

82

9

14

34

2

50

16

* Digits are slitghtly rounded

-20

26

12

-27

7

71

11

10

3

7

52

15

-3

3

1

-3

1

12

-2

2

28

0

5

-1

-3

9

3

-13

-1

-1

0

2

3

-5

-7

2

Jan-Sept 2012 vs 2011

83.2 81.5

71.6

23.0 20.8 17.5 15.6 14.2 13.5 11.3 9.4 7.3

AVERAGE VIRTUAL PRICE & AVERAGE PROMO PRICE (traffic leaflets)

Metro had a severe reduction of the virtual price by 82%, meanwhile Carrefour Market increased the virtual prince by 133%.

AVERAGE PROMO PRICEMetro had a severe reduction of the promo price by 82%, meanwhile Carrefour Market increased the promo prince by 133%.

83.4 81.7

71.8

23.0 21.417.7 15.6 14.3 13.5 11.5 9.7 7.3

AVERAGE VIRTUAL PRICE

-0,5-14,0

3,6

0,4 -95,2 1,1 8,9 0,5 -0,5 -0,3 0,0 -0,2

3,2 -13,5

3,6

0,4 -95,2 1,1 8,9 0,4 -0,5 -0,3 -0,1 -0,2

Jan-Sept 2012 vs 2011

AVERAGE VIRTUAL PRICE & AVERAGE PROMO PRICE (traffic leaflets) (FOOD CATEGORY)

AVERAGE PROMO PRICE

AVERAGE VIRTUAL PRICE

15.6

12.3 11.7 11.5 10.9 10.8 10.68.3 8.1 8.0 8.0 7.2

15.6

12.5 11.9 11.6 11.5 11.1 10.78.7 8.3 8.1 8.0 7.2

8,91,5 1,1 -0,2 -1,1 0,9 0,0

-0,4 0,5 0,5 1,9 0,0

9,0

1,5 1,1 -0,2 -0,9 0,6 -0,5-0,3 0,5 0,5 1,9 0,0

Jan-Sept 2012 vs 2011

METR

O

CARREFO

UR M

ARKET

MEGA

IMAG

E

CARREFO

UR

SELG

ROS

CORA

REAL-H

YPERM

ARKET

PENNY

MAR

KET

PROFI

LIDL

BILLA

KAUFL

AND

11.4 11.1 10.6 9.8 9.7 9.68.6 8.3 8.0 8.0 7.7 7.2

-0,42,0 -0,3 0,8 -0,9 -0,8

0,7 0,5 0,4 -0,4 1,2 -0,1

AVERAGE VIRTUAL PRICE & AVERAGE PROMO PRICE (traffic leaflets) (PRODUSE AMBALATE CU AUTOSERVIRE)

AVERAGE PROMO PRICE

AVERAGE VIRTUAL PRICE

METR

O

CARREFO

UR M

ARKET

MEGA

IMAG

E

CARREFO

UR

SELG

ROS

CORA

REAL-H

YPERM

ARKET

PENNY

MAR

KET

PROFI

BILLA

LIDL

KAUFL

AND

11.7 11.1 10.7 10.0 9.9 9.7 9.0 8.4 8.0 8.0 8.0 7.2

-0,51,9 -0,3 1,2 -0,9 -0,3

0,5 0,5 0,4 1,2 -0,4 -0,1

Jan-Sept 2012 vs 2011

AVERAGE VIRTUAL PRICE & AVERAGE PROMO PRICE (traffic leaflets) (FRUCTE SI LEGUME)

AVERAGE PROMO PRICE

AVERAGE VIRTUAL PRICE

CORA

SELGRO

S

MEG

A IMAG

ELI

DL

CARREFOUR M

A...

METR

O

REAL-H

YPERM

A...

PEN

NY

MARKET

KAUFLA

ND

CARREFOUR

BILLA

PROFI

10.49.2 9.2

8.2 8.06.8

5.0 4.6 4.4 4.4 4.1 3.8

CORA

SELGRO

S

MEG

A IMAG

ELI

DL

CARREFOUR M

A...

METR

O

REAL-H

YPERM

A...

PEN

NY

MARKET

KAUFLA

ND

CARREFOUR

BILLA

PROFI

10.49.2 9.2

8.2 8.06.8

5.0 4.6 4.4 4.4 4.1 3.8

5,9 -1,63,9 -24,3 5,0

-2,30,2 0,5 0,4 -0,3 -0,2 -0,1

5,9-1,6 3,9 -24,3 5,0

-2,3

0,2 0,5 0,4 -0,6 -0,2 -0,1

Jan-Sept 2012 vs 2011

16.814.2 13.3 12.9

11.0 10.4 9.5 9.0 8.97.8 7.2 6.2

9,3 1,0 -2,5 0,7

0,1 7,1 0,7 2,2 0,1 -0,1

-0,1 0,0

AVERAGE VIRTUAL PRICE & AVERAGE PROMO PRICE (traffic leaflets) (CONGELATE)

AVERAGE PROMO PRICE

AVERAGE VIRTUAL PRICE

16.814.4 13.3 13.2

11.1 11.0 9.8 9.5 9.0 7.8 7.3 6.2

9,3 0,9

-2,5 0,6

7,1 -0,1 0,5 2,3 0,5

-0,1 -0,2 0,0

Jan-Sept 2012 vs 2011

AVERAGE VIRTUAL PRICE & AVERAGE PROMO PRICE (traffic leaflets) (FOOD)

AVERAGE PROMO PRICE

AVERAGE VIRTUAL PRICE

16.9

11.59.9 9.7 9.0 7.9 7.4 7.2 6.9 6.7 5.9 5.6

16.9

11.710.0 9.7 9.1

7.9 7.7 7.6 6.9 6.8 6.0 5.6

12,0

1,52,0 -0,1 1,2 0,2

-1,9 -0,8 2,7 0,6 0,6 -0,2

12,1

1,62,0 -0,1 0,9

-0,1 -1,8 -0,8 2,7 0,6 0,6 -0,2

Jan-Sept 2012 vs 2011

AVERAGE VIRTUAL PRICE & AVERAGE PROMO PRICE (traffic leaflets) (DETERGENTI - IGIENA)

AVERAGE PROMO PRICE

AVERAGE VIRTUAL PRICE

REAL-HY-PERMARKET

CARREFOUR CARREFOUR MARKET

PENNY MARKET

SELGROS KAUFLAND METRO CORA BILLA PROFI MEGA IMAGE LIDL

25.622.6 22.0

20.0 18.8 17.9 17.7 16.9 16.0 15.4 13.711.2

REAL-HY-PERMARKET

CARREFOUR CARREFOUR MARKET

PENNY MARKET

SELGROS METRO KAUFLAND CORA BILLA PROFI MEGA IMAGE LIDL

25.823.8 22.0 20.4 19.5 19.3 18.2 17.1 17.0 15.4 13.9

11.3

0,2 3,0 11,61,8 2,8 -1,1 -0,2

1,7 -1,6 -2,3-0,6 1,5

0,0 2,911,6 2,1 3,0 0,0

-0,9 0,7 -1,1 -2,3-0,5 1,6

Jan-Sept 2012 vs 2011

AVERAGE VIRTUAL PRICE & AVERAGE PROMO PRICE (traffic leaflets) (COSMETICE)

AVERAGE PROMO PRICE

AVERAGE VIRTUAL PRICE

24.8

19.014.8 14.5 14.3 14.0 13.0 12.7 12.5 12.2 11.7

9.7

24.8

19.414.9 14.8 14.8 14.5 14.4 13.5 13.3 12.4 12.3

9.7

16,5

3,52,1

-0,71,1 1,8

0,7 0,0 1,5 -0,1 -0,7-0,8

16,5

3,6

2,1 1,4 -0,7 0,5 0,5 1,1 1,4 -0,6 -0,1-0,8

Jan-Sept 2012 vs 2011

AVERAGE VIRTUAL PRICE & AVERAGE PROMO PRICE (traffic leaflets) (PRODUSE VRAC/SERVIRE ASISTATA)

AVERAGE PROMO PRICE

AVERAGE VIRTUAL PRICE

METR

O

CARREFO

UR M

ARKET

MEGA

IMAG

E

SELG

ROS

CARREFO

UR

PENNY

MAR

KET

CORALI

DL

REAL-H

YPERM

ARKET

KAUFL

AND

BILLA

PROFI

24.122.1 22.0

17.714.1 14.0 12.7

9.9 8.6 7.1 6.7 5.6

METR

O

CARREFO

UR M

ARKET

MEGA

IMAG

E

SELG

ROS

CARREFO

UR

PENNY

MAR

KET

CORALI

DL

REAL-H

YPERM

ARKET

KAUFL

AND

BILLA

PROFI

24.122.1 22.0

17.714.1 14.0 12.7

9.9 8.7 7.1 6.7 5.6

-2,514,1 8,6

1,0-0,8 3,1 -3,4

-1,2

-0,1 2,0 0,5 0,3

-2,514,1 8,6

1,0

-

1,0 3,0-4,2 -1,2

-0,1 2,0 0,5 0,3

Jan-Sept 2012 vs 2011

AVERAGE VIRTUAL PRICE & AVERAGE PROMO PRICE (traffic leaflets) (NON FOOD CATEGORY)

AVERAGE PROMO PRICE

AVERAGE VIRTUAL PRICE

METR

O

CARREFO

UR

CORA

REAL-H

YPERM

ARKET

SELG

ROS

PENNY

MAR

KETLI

DL

KAUFL

AND

BILLA

CARREFO

UR M

ARKET

MEGA

IMAG

E

PROFI

266.8232.3

186.8149.8

70.647.2 34.2 29.9 25.3 9.4 8.5 8.1

-248,015,6

5,4-0,4

-7,4 7,1-0,4 -2,2 7,1 1,0 1,0 -2,5

METR

O

CARREFO

UR

CORA

REAL-H

YPERM

ARKET

SELG

ROS

PENNY

MAR

KETLI

DL

KAUFL

AND

BILLA

CARREFO

UR M

ARKET

MEGA

IMAG

E

PROFI

266.8232.4

187.0150.0

70.647.4 34.2 29.9 25.4 9.4 8.5 8.1

-249,2-16,5

-2,9-0,4

-7,5 7,2-0,4 -2,2 7,1 1,0 -1,1 -2,5

Jan-Sept 2012 vs 2011

AVERAGE VIRTUAL PRICE & AVERAGE PROMO PRICE (traffic leaflets) (ELECTRO-FOTO-CINEMA-SUNET)

AVERAGE PROMO PRICE

AVERAGE VIRTUAL PRICE

METR

O

CORA

CARREFO

UR

REAL-H

YPERM

ARKET

SELG

ROS

PENNY

MAR

KETLI

DL

KAUFL

AND

BILLA

CARREFO

UR M

ARKET

MEGA

IMAG

E

PROFI

778.3

610.2 607.3480.3

178.4 137.773.3 68.1 51.3 11.0 4.0

METR

O

CORA

CARREFO

UR

REAL-H

YPERM

ARKET

SELG

ROS

PENNY

MAR

KETLI

DL

KAUFL

AND

BILLA

CARREFO

UR M

ARKET

MEGA

IMAG

E

PROFI

778.3

611.0 607.4480.4

178.4 137.873.3 68.1 51.3 11.0 4.0

-301,853,6 62,8

-41,3

-90,3 0,4 -25,2 5,34,7 0,0 4,0 -55,0

-304,6

27,6 61,4-41,3

-90,3 0,2

-

25,25,3 4,7 0,0 4,0 -55,0

Jan-Sept 2012 vs 2011

AVERAGE VIRTUAL PRICE & AVERAGE PROMO PRICE (traffic leaflets) (BAZAR)

AVERAGE PROMO PRICE

AVERAGE VIRTUAL PRICE

CARREFOUR CORA REAL-HYPERMARKET METRO LIDL SELGROS PENNY MARKET KAUFLAND BILLA MEGA IMAGE PROFI CARREFOUR MARKET

93.8

76.2 72.0

37.5 35.8 30.5 28.9 27.9 23.38.4 8.1 7.9

CARREFOUR CORA REAL-HYPERMARKET METRO LIDL SELGROS PENNY MARKET KAUFLAND BILLA MEGA IMAGE PROFI CARREFOUR MARKET

93.9

76.2 72.1

37.6 35.8 30.5 29.1 27.9 23.48.4 8.1 7.9

1,5

6,7 21,3

-62,2 3,2 2,3 4,7 -2,4 8,5

0,0 -1,6 0,3

0,53,9

21,2

-62,33,2 2,3 4,8 -2,4 8,5

0,0 -1,6 0,3

Jan-Sept 2012 vs 2011

AVERAGE VIRTUAL PRICE & AVERAGE PROMO PRICE (traffic leaflets) (TEXTILE)

AVERAGE PROMO PRICE

AVERAGE VIRTUAL PRICE

METR

O

CORA

CARREFO

UR

REAL-H

YPERM

ARKET

PENNY

MAR

KETLI

DL

SELG

ROS

KAUFL

AND

BILLA

MEGA

IMAG

E

PROFI

45.2 42.437.9

32.2 31.526.6

21.9 21.015.2

11.9

METR

O

CORA

CARREFO

UR

REAL-H

YPERM

ARKET

PENNY

MAR

KETLI

DL

SELG

ROS

KAUFL

AND

BILLA

MEGA

IMAG

E

PROFI

45.2 42.438.0

32.6 31.826.6

21.9 21.015.2 11.9

7,85,7

-9,6-3,4 3,4

-3,40,5 -0,8

1,9-6,0

-10,8

7,84,2 -9,8

-3,4 3,6-3,4

0,0 -0,81,6 -6,0

-10,8

Jan-Sept 2012 vs 2011

PROMOReview

Promo Review of food retailers in 20’top

3 – PROMO PRESSURE & SHARE OF VOICE

Jan-Sept 2012 vs 2011

Jan-Sept 2012 vs 2011

PROMO PRESSURE GROWTH* (SNU)Traffic Leaflets

PROMO PRESSURE

FOOD

NON - FOOD

+1.2 %

-4.0 %

HIPERMARKET

SUPERMARKET

CASH&CARRY

HARD DISCOUNT

+1.41%

-5.94%

The Promo Pressure has a positive trend in the Jan-Sept v/s Y-1. We have seen previously that the number of Promo Operation was growing. Taking a look at how retailers behaved in 2012, we see that Hypermarkets and Hard Discounters have a positive trend respect the other formats.

*The Promo Pressure growth is calculated in SNU . A growth < 0 means a mix of less SNU promoted

Growth v/s Y-1

+9.2 %

-6.23%

+10.17%

Jan-Sept 2012 vs 2011

PROMO PRESSURE GROWTH* (SNU) vs AVERAGE NUMBER OF PAGES/PROMO OP

The detailed promo pressure growth by player shows the correlation between number of pages downsize and promo pressure reduction.

*The Promo Pressure growth is calculated in SNU . A growth < 0 means a mix of less SNU promoted

Average number of pages/OP

BILLA

CARREFOUR

CARREFOUR MARKET

CORA

KAUFLAND

LIDL

MEGA IMAGE

METRO

PENNY MARKET

PROFI

REAL-HYPERMARKET

SELGROS

9.24%

20.45%

-5.35%

1.39%

-1.25%

-2.21%

21.31%

-6.55%

-11.28%SELGROS

REAL-HYPERMARKET

METRO

CARREFOUR

LIDL

PENNY MARKET

BILLA

KAUFLAND

PROFI

MEGA IMAGE

CORA

CARREFOUR MARKET

45 pag

31 pag

27 pag

25 pag

18 pag

16 pag

16 pag

13 pag

12 pag

12 pag

10 pag

4 pag

2 pag

-6 pag

2 pag

-1 pag

6 pag

0 pag

2 pag

1 pag

3 pag

1 pag

0 pag

0 pag

Jan-Sept 2012 vs 2011

PROMO PRESSURE GROWTH* (SNU)

*The Promo Pressure growth is calculated in SNU . A growth < 0 means a mix of less SNU promoted

FOOD CATEGORY

PRODUSE AMBALATE CU AUTOSERVIRE

FRUCTE SI LEGUME

CONGELATE

FOOD

DETERGENTI - IGIENA

COSMETICE

PRODUSE VRAC/SERVIRE ASISTATA

NON FOOD CATEGORY

ELECTRO-FOTO-CINEMA-SUNET

BAZAR

TEXTILE

6.50%

-17.53%

35.13%

-29.90%

31.61%

4.55%

-15.64%

14.57%

-11.43%

-27.12%

-9.76%

10.68%

Jan-Sept 2012 vs 2011

PROMO PRESSURE GROWTH* (SNU)

*The Promo Pressure growth is calculated in SNU . A growth < 0 means a mix of less SNU promoted

FOOD CATEGORY

PRODUSE AMBALATE CU AUTOSERVIRE

FRUCTE SI LEGUME

CONGELATE

FOOD

DETERGENTI - IGIENA

COSMETICE

PRODUSE VRAC/SERVIRE ASISTATA

NON FOOD CATEGORY

ELECTRO-FOTO-CINEMA-SUNET

BAZAR

TEXTILE

-0.86%

15.22%

-54.47%

-10.16%

-8.47%

-2.09%

-5.34%

12.10%

1.25%

-7.53%

-2.69%

14.87%

Jan-Sept 2012 vs 2011

PROMO PRESSURE GROWTH* (SNU)

*The Promo Pressure growth is calculated in SNU . A growth < 0 means a mix of less SNU promoted

FOOD CATEGORY

PRODUSE AMBALATE CU AUTOSERVIRE

FRUCTE SI LEGUME

CONGELATE

FOOD

DETERGENTI - IGIENA

COSMETICE

PRODUSE VRAC/SERVIRE ASISTATA

NON FOOD CATEGORY

ELECTRO-FOTO-CINEMA-SUNET

BAZAR

TEXTILE

1.62%

-9.76%

2.48%

-2.23%

11.65%

11.63%

3.41%

-10.40%

-4.71%

-30.17%

5.48%

-16.03%

Jan-Sept 2012 vs 2011

PROMO PRESSURE GROWTH* (SNU)

*The Promo Pressure growth is calculated in SNU . A growth < 0 means a mix of less SNU promoted

FOOD CATEGORY

PRODUSE AMBALATE CU AUTOSERVIRE

FRUCTE SI LEGUME

CONGELATE

FOOD

DETERGENTI - IGIENA

COSMETICE

PRODUSE VRAC/SERVIRE ASISTATA

NON FOOD CATEGORY

ELECTRO-FOTO-CINEMA-SUNET

BAZAR

TEXTILE

-3.55%

-9.77%

1.02%

-7.05%

-7.50%

8.09%

11.98%

-1.46%

5.02%

5.61%

1.42%

9.56%

Jan-Sept 2012 vs 2011

PROMO PRESSURE GROWTH* (SNU)

*The Promo Pressure growth is calculated in SNU . A growth < 0 means a mix of less SNU promoted

FOOD CATEGORY

PRODUSE AMBALATE CU AUTOSERVIRE

FRUCTE SI LEGUME

CONGELATE

FOOD

DETERGENTI - IGIENA

COSMETICE

PRODUSE VRAC/SERVIRE ASISTATA

NON FOOD CATEGORY

ELECTRO-FOTO-CINEMA-SUNET

BAZAR

TEXTILE

1.45%

-7.39%

10.63%

22.71%

-3.28%

37.92%

2.14%

7.98%

-18.25%

-26.43%

-19.00%

1.12%

Jan-Sept 2012 vs 2011

PROMO PRESSURE GROWTH* (SNU)

*The Promo Pressure growth is calculated in SNU . A growth < 0 means a mix of less SNU promoted

FOOD CATEGORY

PRODUSE AMBALATE CU AUTOSERVIRE

FRUCTE SI LEGUME

CONGELATE

FOOD

DETERGENTI - IGIENA

COSMETICE

PRODUSE VRAC/SERVIRE ASISTATA

NON FOOD CATEGORY

ELECTRO-FOTO-CINEMA-SUNET

BAZAR

TEXTILE

4.05%

13.51%

20.29%

144.61%

-5.57%

-29.41%

11.32%

25.88%

-17.54%

0.72%

-21.16%

-16.66%

Jan-Sept 2012 vs 2011

PROMO PRESSURE GROWTH* (SNU)

*The Promo Pressure growth is calculated in SNU . A growth < 0 means a mix of less SNU promoted

FOOD CATEGORY

PRODUSE AMBALATE CU AUTOSERVIRE

FRUCTE SI LEGUME

CONGELATE

FOOD

DETERGENTI - IGIENA

COSMETICE

PRODUSE VRAC/SERVIRE ASISTATA

NON FOOD CATEGORY

ELECTRO-FOTO-CINEMA-SUNET

BAZAR

TEXTILE

0.02%

25.23%

-31.54%

-10.02%

7.28%

-14.71%

-26.46%

-3.65%

-0.53%

0.00%

7.64%

-68.66%

Jan-Sept 2012 vs 2011

PROMO PRESSURE GROWTH* (SNU)

*The Promo Pressure growth is calculated in SNU . A growth < 0 means a mix of less SNU promoted

FOOD CATEGORY

PRODUSE AMBALATE CU AUTOSERVIRE

FRUCTE SI LEGUME

CONGELATE

FOOD

DETERGENTI - IGIENA

COSMETICE

PRODUSE VRAC/SERVIRE ASISTATA

NON FOOD CATEGORY

ELECTRO-FOTO-CINEMA-SUNET

BAZAR

TEXTILE

1.86%

-10.57%

17.32%

-20.27%

-1.87%

-51.59%

-16.47%

71.45%

-88.61%

-77.22%

-92.41%

0.00%

Jan-Sept 2012 vs 2011

PROMO PRESSURE GROWTH* (SNU)

*The Promo Pressure growth is calculated in SNU . A growth < 0 means a mix of less SNU promoted

FOOD CATEGORY

PRODUSE AMBALATE CU AUTOSERVIRE

FRUCTE SI LEGUME

CONGELATE

FOOD

DETERGENTI - IGIENA

COSMETICE

PRODUSE VRAC/SERVIRE ASISTATA

NON FOOD CATEGORY

ELECTRO-FOTO-CINEMA-SUNET

BAZAR

TEXTILE

1.95%

-11.46%

346.30%

21.92%

6.88%

-34.64%

2.29%

111.40%

-1.38%

21.72%

-5.27%

1.54%

Jan-Sept 2012 vs 2011

PROMO PRESSURE GROWTH* (SNU)

*The Promo Pressure growth is calculated in SNU . A growth < 0 means a mix of less SNU promoted

FOOD CATEGORY

PRODUSE AMBALATE CU AUTOSERVIRE

FRUCTE SI LEGUME

CONGELATE

FOOD

DETERGENTI - IGIENA

COSMETICE

PRODUSE VRAC/SERVIRE ASISTATA

NON FOOD CATEGORY

ELECTRO-FOTO-CINEMA-SUNET

BAZAR

TEXTILE

0.98%

-18.94%

9.59%

75.79%

1.24%

23.63%

-10.08%

15.64%

-12.55%

6.46%

Jan-Sept 2012 vs 2011

PROMO PRESSURE GROWTH* (SNU)

*The Promo Pressure growth is calculated in SNU . A growth < 0 means a mix of less SNU promoted

FOOD CATEGORY

PRODUSE AMBALATE CU AUTOSERVIRE

FRUCTE SI LEGUME

CONGELATE

FOOD

DETERGENTI - IGIENA

COSMETICE

PRODUSE VRAC/SERVIRE ASISTATA

NON FOOD CATEGORY

ELECTRO-FOTO-CINEMA-SUNET

BAZAR

TEXTILE

21.52%

-4.24%

46.73%

-1.09%

25.28%

38.60%

43.13%

8.98%

-81.67%

-86.67%

-78.14%

-72.52%

Jan-Sept 2012 vs 2011

PROMO PRESSURE GROWTH* (SNU)

*The Promo Pressure growth is calculated in SNU . A growth < 0 means a mix of less SNU promoted

FOOD CATEGORY

PRODUSE AMBALATE CU AUTOSERVIRE

FRUCTE SI LEGUME

CONGELATE

FOOD

DETERGENTI - IGIENA

COSMETICE

PRODUSE VRAC/SERVIRE ASISTATA

NON FOOD CATEGORY

ELECTRO-FOTO-CINEMA-SUNET

BAZAR

TEXTILE

-1.29%

12.48%

19.85%

-6.93%

0.59%

0.71%

-10.35%

-32.52%

13.74%

49.60%

8.68%

-5.86%

Jan-Sept 2012 vs 2011

SHARE OF VOICE (SNU) Traffic Leaflets

*where Others represents the retailers outside selection with the same chain format as selected.

Others* 10.5%

100% = Total Retailers Jan-Sept 2012

The most important player is Kaufland.

-6.8 pts

11.2%

10.8%

10.7%

10.7%

10.2%

9.0%

7.7%

7.2%

5.0%

4.5%

1.3%

1.1%

0,2 pts

-0,6 pts

-0,8 pts

1,8 pts

-0,1 pts

-1,1 pts

0,7 pts

-0,2 pts

2,6 pts

3,3 pts

0,2 pts

0,8 pts

Jan-Sept 2012 vs 2011

PROMOReview

Promo Review of food retailers in 20’top

4 – PROMO MECHANISMS

Jan-Sept 2012 vs 2011

Jan-Sept 2012 vs 2011

PROMO MECHANISMS(SNU) Traffic LeafletsProducts with consumer benefits by retailer format

Regarding the consumer benefits an important increasing was in CASH AND CARYY with 7 pts in 2012 vs 2011.

CASH AND CARRY HARD DISCOUNT HIPERMARKET SUPERMARKET

34.9%

39.5%

52.4%

48.7%

42.0%44.8%

53.2% 54.2%

2011

2012

Jan-Sept 2012 vs 2011

PROMO MECHANISMS(SNU) Traffic LeafletsProducts with consumer benefits per retailer

HIPERMARKET SUPERMARKET

Analyzing the consumer benefits by retailer, we have a clear picture of the evolution of these. In Hypermarkets Real increased with 6.2 pts, while in Supermarkets Billa is leading, although it has registered a decreased of 9.1pts.

14.66%

34.63%33.19%

17.52%15.79%

28.26%

32.23%

23.72%

2011

2012

88.48%

0.19%3.16%

8.17%

79.33%

0.53%

10.80%9.33%

2011

2012

Jan-Sept 2012 vs 2011

PROMO MECHANISMS(SNU) Traffic LeafletsProducts with consumer benefits per retailer

HARD DISCOUNTCASH&CARRY

In Cash&Carry METRO registered a positive evolution of +8.3 pts vs. previous year.

51.97%

48.03%

60.29%

39.71%

2011

2012

6.53%

93.47%

18.48%

81.52%

2011

2012

Jan-Sept 2012 vs 2011

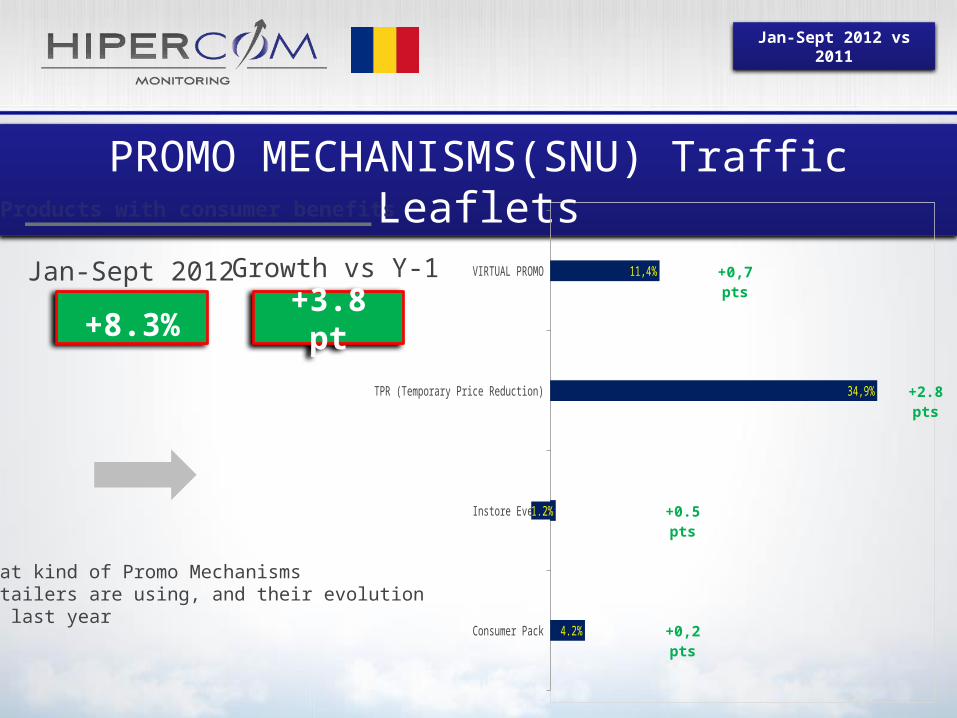

PROMO MECHANISMS(SNU) Traffic Leaflets

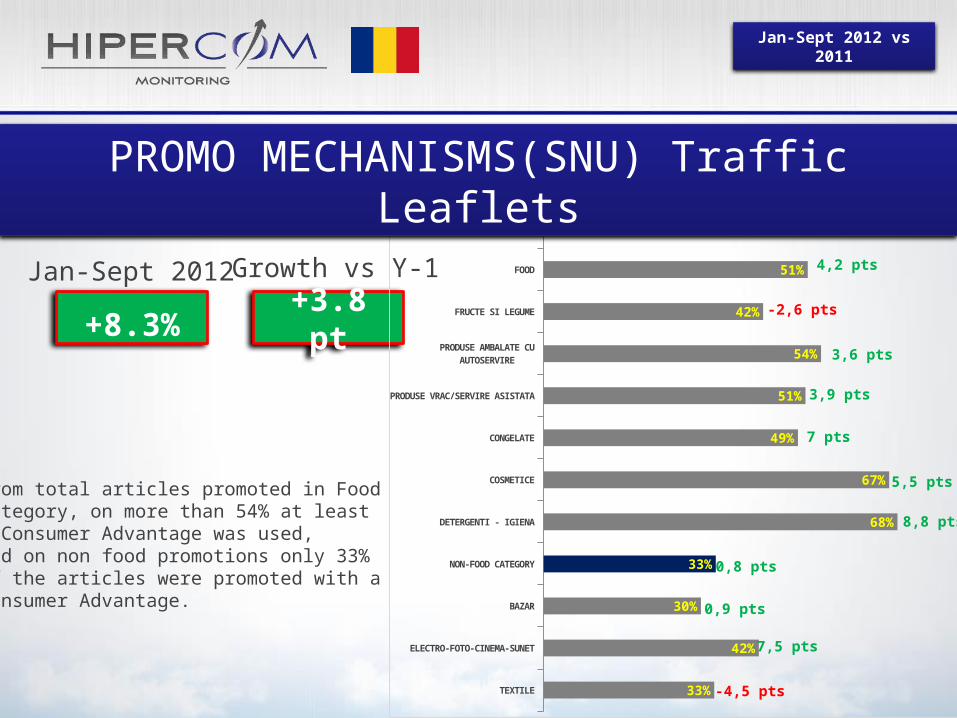

+8.3%+3.8

pt

Products with consumer benefits

Jan-Sept 2012 Growth vs Y-1

What kind of Promo MechanismsRetailers are using, and their evolutionVs last year

Consumer Pack

Instore Event

TPR (Temporary Price Reduction)

VIRTUAL PROMO

4.2%

1.2%

34,9%

11,4% +0,7 pts

+2.8 pts

+0.5 pts

+0,2 pts

Jan-Sept 2012 vs 2011

Products with consumer benefits

+8.3%+3.8

pt

Jan-Sept 2012 Growth vs Y-11 + 1 gratis 0,4%

(-0,3 pts)

2 + 1 gratis 1,2%(-0,4 pts)

Other VL 8,4%(1.7 pts)

X% From the 2nd product (Identical or not) 1,5%

(-0,3 pts)

BUYBACK 0,0% (0 pts)

LOTTERY/GAMES 1.2%(0,5 pts)

GIFTS ON PACK 4.2%(0,2 pts)

GRATUITES 3.1%(-2.0 pts)

CROSSED PRICE 2,6%(-0,2 pts)

CUPON 0,0%(-0,1 pts)

LOYALTY POINTS 3.2%(-1,2 pts)

MONEYTICKET 3.0%(0,5 pts)

PRICE DISCOUNT 25.5%(3.6 pts)

SPECIAL PRICE 0,6%(0,3 pts)

Consumer Pack

Instore Event

TPR (Temporary Price Reduction)

VIRTUAL PROMO

4.2%

1.2%

34.9%

11,4% +0,7 pts

+2.8 pts

+0.5 pts

+0,2 pts

PROMO MECHANISMS(SNU) Traffic Leaflets

Jan-Sept 2012 vs 2011

From total articles promoted in Food category, on more than 54% at least 1 Consumer Advantage was used, And on non food promotions only 33% of the articles were promoted with a Consumer Advantage.

+8.3%+3.8

pt

Products with consumer benefits

Jan-Sept 2012 Growth vs Y-1

FOOD CATEGORY

FOOD

FRUCTE SI LEGUME

PRODUSE AMBALATE CU AUTOSERVIRE

PRODUSE VRAC/SERVIRE ASISTATA

CONGELATE

COSMETICE

DETERGENTI - IGIENA

NON-FOOD CATEGORY

BAZAR

ELECTRO-FOTO-CINEMA-SUNET

TEXTILE

54%

51%

42%

54%

51%

49%

67%

68%

33%

30%

42%

33%

4,4 pts

4,2 pts

-2,6 pts

3,6 pts

3,9 pts

7 pts

5,5 pts

8,8 pts

0,8 pts

0,9 pts

7,5 pts

-4,5 pts

PROMO MECHANISMS(SNU) Traffic Leaflets

Jan-Sept 2012 vs 2011

PROMOReview

Promo Review of food retailers in 20’top

3 – QUALITY KPI

Jan-Sept 2012 vs 2011

Jan-Sept 2012 vs 2011

COMPLEXITY INDICATOR

We can easily see that BILLA is using at least 1 Consumer Advantage on 81% of the promoted articles, while Carrefour Market is using Consumer Advantages only on 3.86 % of the promoted articles.

BILLA

KAUFLAND

CORA

PROFI

REAL-HYPERMARKET

METRO

PENNY MARKET

SELGROS

CARREFOUR

MEGA IMAGE

LIDL

CARREFOUR MARKET

81.22%

66.63%

60.34%

55.95%

51.10%

47.83%

47.23%

35.52%

34.11%

17.02%

17.00%

3.86%

-3,15%

-0,88%

-7,58%

5,31%

16,87%

11,77%

6,21%

1,77%

-2,90%

8,14%

-1,08%

-0,76%

Jan-Sept 2012 vs 2011

0 mechanisms 1 mechanisms 2 mechanisms 3 mechanisms

50.40%47.49%

2.06%0.04%

COMPLEXITY INDICATOR

Number of Promo mechanisms / item

(HM,HDD, SM & CC, on Food &Non Food)

The most complex or less complex(classified by the number of products with 2 or more mechanisms)

The indicator of complexity is to indicate the level of complexity of the offers of the retailers. As a retailer will have several mechanisms on a promoted item, it will be poorly ranked.

0.0%

0.2%

0.2%

0.3%

0.7%

1.6%

2.4%

2.8%

3.2%

3.3%

3.9%

7.1%

Jan-Sept 2012 vs 2011

Jan-Sept 2012 vs 2011

PROMOReview

Promo Review of food retailers in 20’top

RETAILERS SUMMARY

Jan-Sept 2012 vs 2011

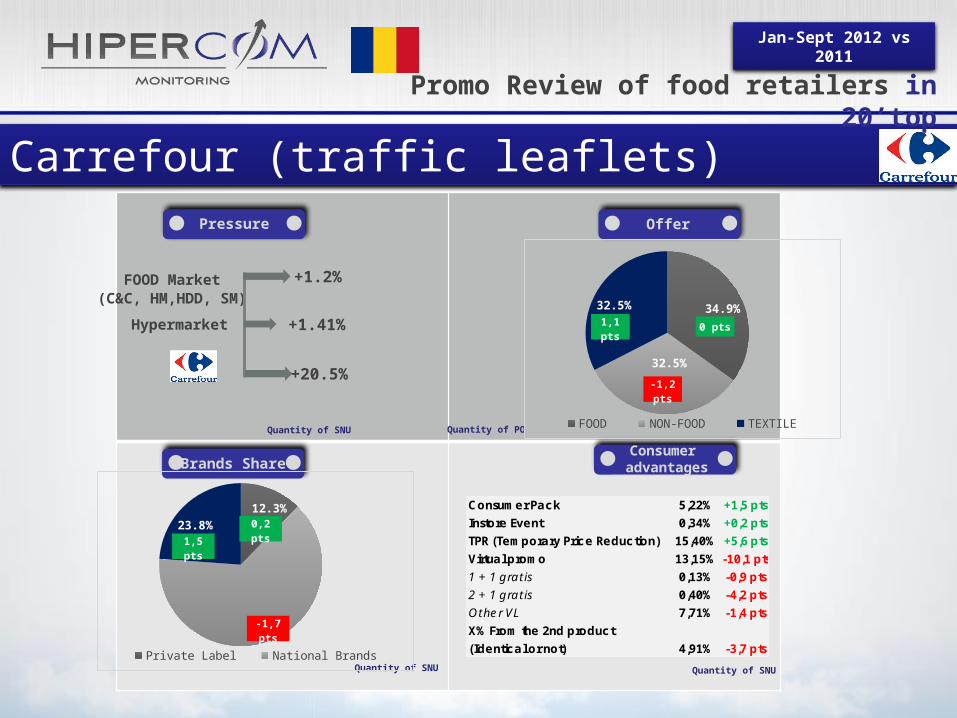

Carrefour (traffic leaflets)Pressure Offer

Consumer advantagesBrands Share

FOOD Market(C&C, HM,HDD, SM)

Hypermarket

Quantity of SNU

Quantity of PO

+1.41%

Quantity of SNU

+20.5%

+1.2%

Quantity of SNU

Promo Review of food retailers in 20’top

12.3%

63.9%

23.8%

Private Label National Brands Unbranded

0,2 pts

-1,7 pts

1,5 pts

34.9%

32.5%

32.5%

FOOD NON-FOOD TEXTILE

Consumer Pack 5,22% +1,5 pts

Instore Event 0,34% +0,2 pts

TPR (Temporary Price Reduction) 15,40% +5,6 pts

Virtual promo 13,15% -10,1 pts

1 + 1 gratis 0,13% -0,9 pts

2 + 1 gratis 0,40% -4,2 pts

Other VL 7,71% -1,4 pts

X% From the 2nd product

(Identical or not) 4,91% -3,7 pts

0 pts

-1,2 pts

1,1 pts

Jan-Sept 2012 vs 2011

Cora (traffic leaflets)Pressure Offer

Brands Share

FOOD Market(C&C, HM,HDD, SM)

Hypermarket

Quantity of SNU

Quantity of PO

+1.41%

Quantity of SNU

-5.4%

+1.2%

Quantity of SNU

Consumer advantages

Promo Review of food retailers in 20’top

12.4%

60.6%

27.0%

Private Label National Brands Unbranded

-0,6 pts

0,9 pts

-0,3 pts

33.3%

33.3%

33.3%

FOOD NON-FOOD TEXTILE

Consumer Pack 1,47% -1,1 pts

Instore Event 0,05% -0,9 pts

TPR (Temporary Price Reduction) 56,60% -5,3 pts

Virtual promo 2,22% -0,3 pts

1 + 1 gratis 0,04% -0,1 pts

2 + 1 gratis 0,08% -0,4 pts

Other VL 0,73% +0,2 pts

X% From the 2nd product

(Identical or not) 1,37% 0 pts

0 pts 0 pts

0 pts

Jan-Sept 2012 vs 2011

Real (traffic leaflets)Pressure Offer

Brands Share

FOOD Market(C&C, HM,HDD, SM)

Hypermarket

Quantity of SNU

Quantity of PO

+1.41%

Quantity of SNU

-6.6%

+1.2%

Quantity of SNU

Consumer advantages

Promo Review of food retailers in 20’top

10.9%

61.0%

28.1%

Private Label National Brands Unbranded

0,6 pts

-0,4 pts

-0,2 pts

33.7%

33.7%

32.6%

FOOD NON-FOOD TEXTILE

Consumer Pack 5,71% +0,4 pts

Instore Event 1,07% +0,2 pts

TPR (Temporary Price Reduction) 38,47% +17,2 pts

Virtual promo 5,85% -0,8 pts

1 + 1 gratis 2,55% 0 pts

2 + 1 gratis 2,36% -0,8 pts

Other VL 0,73% -0,1 pts

X% From the 2nd product

(Identical or not) 0,21% +0 pts

-0,9 pts

-0,9 pts

1,9 pts

Jan-Sept 2012 vs 2011

Kaufland (traffic leaflets)Pressure Offer

Offer/Brands

FOOD Market(C&C, HM,HDD, SM)

Hypermarket

Quantity of SNU

Quantity of PO

+1.41%

Quantity of SNU

+1.4%

+1.2%

Quantity of SNU

Consumer advantages

Promo Review of food retailers in 20’top

15.1%

54.4%

30.5%

Private Label National Brands Unbranded

-1 pts

1,8 pts

-0,8 pts

34.5%

34.5%

31.0%

FOOD NON-FOOD TEXTILE

Consumer Pack 2,07% +1 pts

Instore Event 0,15% 0 pts

TPR (Temporary Price Reduction) 62,83% -3 pts

Virtual promo 1,58% +1,2 pts

1 + 1 gratis 0,19% 0 pts

2 + 1 gratis 0,09% +0 pts

Other VL 1,16% +1,1 pts

X% From the 2nd product

(Identical or not) 0,14% +0,1 pts

0,6 pts

0,6 pts

-1,2 pts

Jan-Sept 2012 vs 2011

Billa (traffic leaflets)Pressure Offer

Brands Share

FOOD Market(C&C, HM,HDD, SM)

Supermarket

Quantity of SNU

Quantity of POQuantity of SNU

-5.94%

+9.2%

+1.2%

Quantity of SNU

Consumer advantages

Promo Review of food retailers in 20’top

8.0%

74.6%

17.4%

Private Label National Brands Unbranded

0,8 pts

1,1 pts

-1,9 pts

40.6%

40.6%

18.8%

FOOD NON-FOOD TEXTILE

0.1 pts

Consumer Pack 2,91% +0,8 pts

Instore Event 0,33% -0,1 pts

TPR (Temporary Price Reduction) 61,37% -5,9 pts

Virtual promo 16,61% +2 pts

1 + 1 gratis 0,17% -1,1 pts

2 + 1 gratis 4,56% +1,7 pts

Other VL 11,29% +2 pts

X% From the 2nd product

(Identical or not) 0,60% -0,6 pts

0.1 pts

-0,3 pts

Jan-Sept 2012 vs 2011

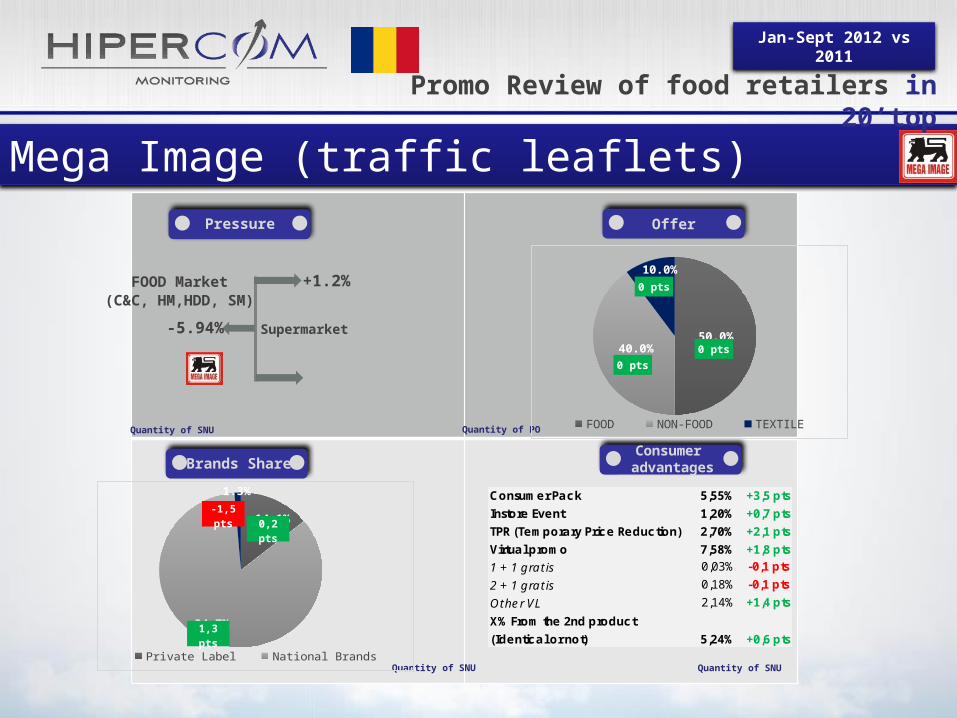

Mega Image (traffic leaflets)Pressure Offer

Brands Share

+3,5pts

Quantity of SNU

Quantity of POQuantity of SNU

Supermarket-5.94%

+1.2%FOOD Market(C&C, HM,HDD, SM)

Quantity of SNU

Consumer advantages

Promo Review of food retailers in 20’top

14.1%

84.7%

1.3%

Private Label National Brands Unbranded

0,2 pts

1,3 pts

-1,5 pts

50.0%40.0%

10.0%

FOOD NON-FOOD TEXTILE

Consumer Pack 5,55% +3,5 pts

Instore Event 1,20% +0,7 pts

TPR (Temporary Price Reduction) 2,70% +2,1 pts

Virtual promo 7,58% +1,8 pts

1 + 1 gratis 0,03% -0,1 pts

2 + 1 gratis 0,18% -0,1 pts

Other VL 2,14% +1,4 pts

X% From the 2nd product

(Identical or not) 5,24% +0,6 pts

0 pts

0 pts

0 pts

Jan-Sept 2012 vs 2011

Carrefour Market(traffic leaflets)Pressure Offer

Brands Share

Quantity of SNU

Quantity of POQuantity of SNU

Supermarket-5.94%

+1.2%FOOD Market(C&C, HM,HDD, SM)

Quantity of SNU

Consumer advantages

Promo Review of food retailers in 20’top

17.3%

67.9%

14.8%

Private Label National Brands Unbranded

-15,5 pts

19,7 pts

-4,1 pts

92.9%

7.1%

FOOD NON-FOOD TEXTILE

Consumer Pack 1,17% -1,4 pts

Instore Event 0,00% +0 pts

TPR (Temporary Price Reduction) 0,47% -1,6 pts

Virtual promo 2,22% +2,2 pts

1 + 1 gratis 0,12% +0,1 pts

2 + 1 gratis 0,00% +0 pts

Other VL 1,29% +1,3 pts

X% From the 2nd product

(Identical or not) 0,82% +0,8 pts

12,9 pts

-12,9 pts

0 pts

Jan-Sept 2012 vs 2011

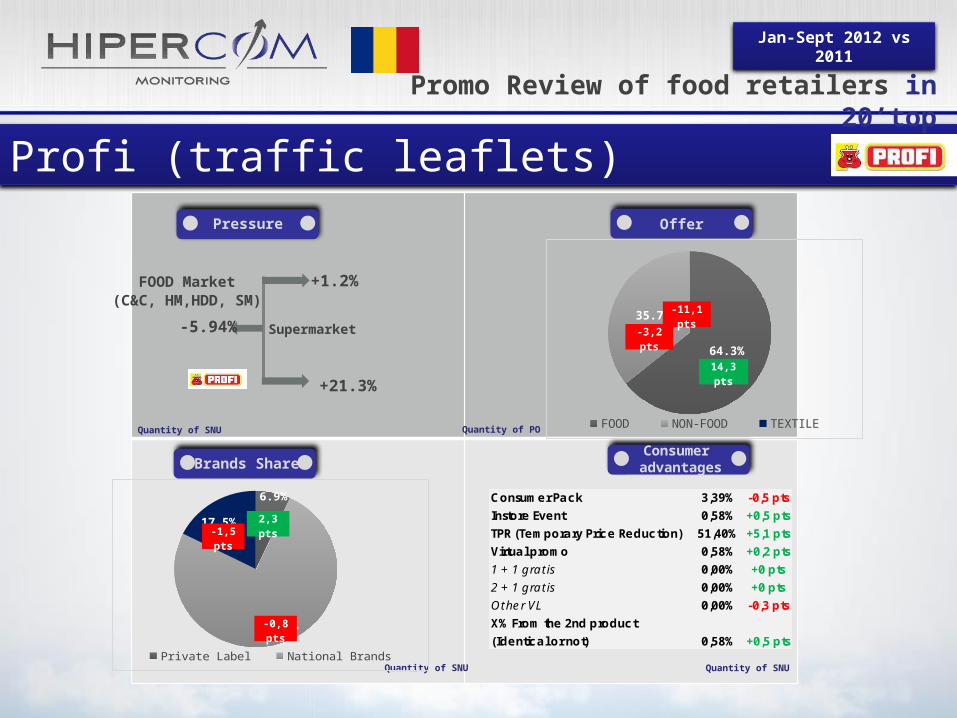

Profi (traffic leaflets)Pressure Offer

Brands Share

-2,8pt

Quantity of SNU

Quantity of POQuantity of SNU

Supermarket-5.94%

+21.3%

+1.2%FOOD Market(C&C, HM,HDD, SM)

Quantity of SNU

Consumer advantages

Promo Review of food retailers in 20’top

6.9%

75.6%

17.5%

Private Label National Brands Unbranded

2,3 pts

-0,8 pts

-1,5 pts

64.3%

35.7%

FOOD NON-FOOD TEXTILE

Consumer Pack 3,39% -0,5 pts

Instore Event 0,58% +0,5 pts

TPR (Temporary Price Reduction) 51,40% +5,1 pts

Virtual promo 0,58% +0,2 pts

1 + 1 gratis 0,00% +0 pts

2 + 1 gratis 0,00% +0 pts

Other VL 0,00% -0,3 pts

X% From the 2nd product

(Identical or not) 0,58% +0,5 pts

14,3 pts

-3,2 pts

-11,1 pts

Jan-Sept 2012 vs 2011

Penny (traffic leaflets)Pressure Offer

Brands Share

Hard Discount

Quantity of SNU

Quantity of POQuantity of SNU

-2.2%

-+10.17%

+1.2%FOOD Market(C&C, HM,HDD, SM)

Quantity of SNU

Consumer advantages

Promo Review of food retailers in 20’top

14.4%

67.6%

17.9%

Private Label National Brands Unbranded

-0,4 pts

4,2 pts

-3,8 pts

37.8%

31.7%

30.5%

FOOD NON-FOOD TEXTILE

Consumer Pack 3,59% +0,7 pts

Instore Event 0,55% +0,5 pts

TPR (Temporary Price Reduction) 39,20% +4,1 pts

Virtual promo 3,89% +0,9 pts

1 + 1 gratis 0,16% 0 pts

2 + 1 gratis 0,23% -0,3 pts

Other VL 1,69% +0,5 pts

X% From the 2nd product

(Identical or not) 1,81% +0,6 pts

0,7 pts

-6,9 pts

6,2 pts

Jan-Sept 2012 vs 2011

Lidl (traffic leaflets)Pressure Offer

Offer/Brands

FOOD Market(C&C, HM,HDD, SM)

Hard Discount

Quantity of SNU

Quantity of POQuantity of SNU

+10.17%

+1.2%

Quantity of SNU

Consumer advantages

Promo Review of food retailers in 20’top

82.7%

6.5%

10.8%

Private Label National Brands Unbranded

-0,2 pts

1,6 pts

-1,4 pts

33.3%

33.3%

33.3%

FOOD NON-FOOD TEXTILE

Consumer Pack 0,14% -0,1 pts

Instore Event 0,00% +0 pts

TPR (Temporary Price Reduction) 16,61% -1,2 pts

Virtual promo 0,25% +0,3 pts

1 + 1 gratis 0,06% +0,1 pts

2 + 1 gratis 0,03% +0 pts

Other VL 0,06% +0,1 pts

X% From the 2nd product

(Identical or not) 0,11% +0,1 pts

0 pts 0 pts

0 pts

Jan-Sept 2012 vs 2011

Metro (traffic leaflets)Pressure Offer

Offer/Brands

FOOD Market(C&C, HM,HDD, SM)

Cash&Carry

Quantity of SNU

Quantity of POQuantity of SNU

-6.23%

-1.2%

+1.2%

Quantity of SNU

Consumer advantages

Promo Review of food retailers in 20’top

16.8%

77.0%

6.2%

Private Label National Brands Unbranded

-1,9 pts

7,4 pts

-5,4 pts

48.6%47.1%

4.3%

FOOD NON-FOOD TEXTILE

Consumer Pack 3,91% +0,6 pts

Instore Event 0,99% +0,8 pts

TPR (Temporary Price Reduction) 2,11% -2,9 pts

Virtual promo 40,81% +13,3 pts

1 + 1 gratis 0,41% -0,1 pts

2 + 1 gratis 2,84% +0,4 pts

Other VL 36,72% +15,2 pts

X% From the 2nd product

(Identical or not) 0,84% -2,1 pts

-2,1 pts2,8

pts

-0,8 pts

Jan-Sept 2012 vs 2011

Selgros (traffic leaflets)Pressure Offer

Share ofBrands

FOOD Market(C&C, HM,HDD, SM)

Cash&Carry

Quantity of SNU

Quantity of POQuantity of SNU

-11.3%

+1.2%

Quantity of SNU

Consumer advantages

Promo Review of food retailers in 20’top

-6.23%

4.3%

90.9%

4.7%

Private Label National Brands Unbranded

-1 pts

0,5 pts

0,4 pts

54.7%30.2%

15.1%

FOOD NON-FOOD TEXTILE

Consumer Pack 5,51% 0 pts

Instore Event 0,86% +0,1 pts

TPR (Temporary Price Reduction) 2,27% +0,8 pts

Virtual promo 26,88% +0,9 pts

1 + 1 gratis 0,24% -0,2 pts

2 + 1 gratis 1,90% +0,2 pts

Other VL 24,57% +0,8 pts

X% From the 2nd product

(Identical or not) 0,17% +0 pts

1,4 pts

-4,8 pts

3,4 pts

Jan-Sept 2012 vs 2011

Thank you for your attention

Florentina VasileProject Manager [email protected]+40 (0) 743 216 282

I remain at your disposal for further information or a life demo

Follow us on social networks for more Markets Intelligence