property taxation – time for reform? jeremy edge edge planning & development plrg 2011...

TRANSCRIPT

Property Taxation – Time for Reform?Jeremy Edge

Edge Planning & DevelopmentPLRG 2011 Programme

LSBUThursday 3rd February

Background

• RICS Research Project – Property Taxation• Purpose - Engage with Treasury to introduce

simplification• Lack of knowledge regarding the magnitude of

tax raised through property• Lack of understanding of the effects of reliefs

and exeptions

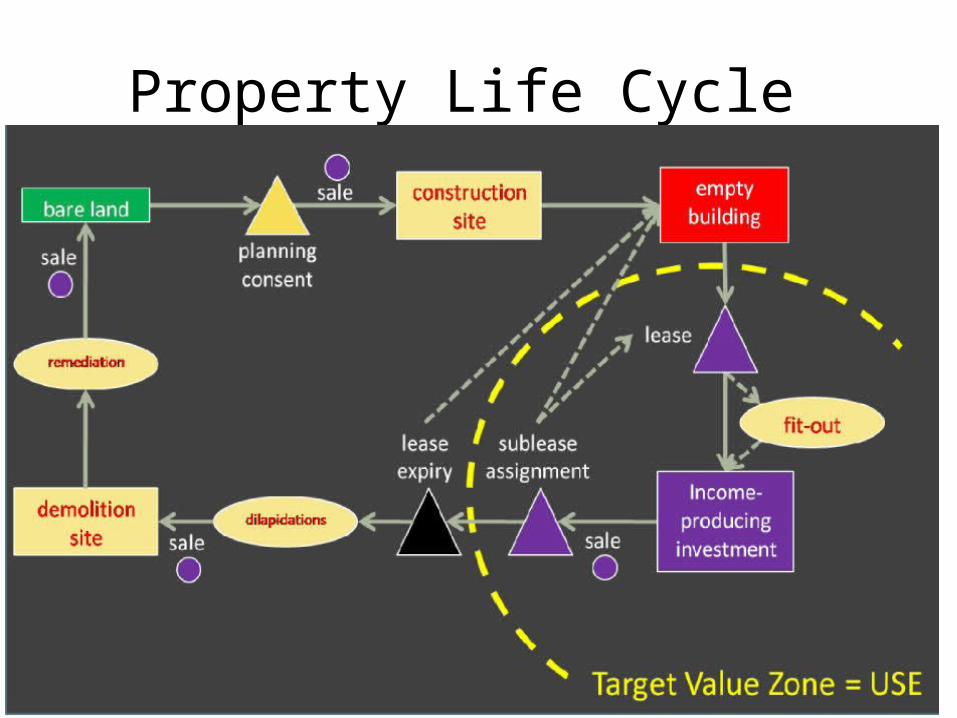

The Property Cycle – A Taxation Opportunity

LAND Planning Application Consent Construction EMPTY

BUILDING

Dilapildations Fit Out Lease or Sale

OCCUPIED BUILDING

Lease TerminationDemolition

Remediation

Property Life Cycle

Commercial Property Taxation Opportunities

Residential Property – Life Cycle

LAND Planning

Construction EMPTY PROPERTY

Social landlords

Owner Occupier

Buy to let

occupylease

lease

Residential Property Taxation

LAND Planning

Construction EMPTY PROPERTY

Social landlords

Owner Occupier

Buy to let

occupylease

lease

VAT on feesPAYE & NI on salaries

S106 costsS278 costs

CIL

VATPAYE & NI

Corporation TaxTransport TaxesInsurance Tax

Supply Chain

SDLTCGT

VAT on fees

Council Tax

SDLTCGT

VAT on fees Council Tax

VATPAYE & NI

CorporationTax

Council Tax

Council Tax

Occupational tax – regardless of ownershipA variety of exemptions exist, such as those detailed below:• The property is empty• Only one adult lives there• The occupier is disabled• The occupier is a student• Low income families can also qualify for council tax benefit

Council Tax Bands

Band Value Ratio Ratio as % Average

A up to £40,000 6/9 67% £845

B £40,001 to £52,000 7/9 78% £986

C £52,001 to £68,000 8/9 89% £1,127

D £68,001 to £88,000 9/9 100% £1,268

E £88,001 to £120,000 11/9 122% £1,550

F £120,001 to £160,000 13/9 144% £1,832

G £160,001 to £320,000 15/9 167% £2,113

H £320,001 and above 18/9 200% £2,536

Council Tax – Geographic Value Distortion

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

North East North West

Yorkshire and The Humber

West Midlands

East Midlands

East of England

South West

South East London Wales Scotland

Band A Band B Band C Band D Band E Band F Band G Band H Band I

Stamp Duty Land Tax

RESIDENTIALValue up to: Rate

£125,000 0%£250,000 1%£500,000 3%

Top rate (£500,000 +) 4%NON-RESIDENTIALValue up to: annual rent Rate

£150,000 < £1,000 0%£150,000 £1,000 + 1%£250,000 n/a 1%£500,000 n/a 3%

Top rate (£500,000 +) n/a 4%Notes(1) First time buyers exempt from SDLT up to £250,000(2) For disadvantaged areas lowest threshold is £150,000(3) SDLT also payable on some new leases, dependent upon rents

Stamp Duty Thresholds

0%

1%

2%

3%

4%

5%

0 100,000 200,000 300,000 400,000 500,000 600,000 700,000

Stam

p du

ty ra

te (%

)

Value of property (£)

SDLT residential rate

SDLT non-resi rate

Developer Contributions • Nationalisation of Development Value• Betterment Levy• Development Land Tax• S106 agreements – need for transparency• Tariffs• Planning Gain Supplement • Community Infrastructure Levy –

• Planning Act 2008• CIL Regulations April 2010

• Charging Schedules• Scaled back s106 arrangements

Viability Assessment

• S106 contributions - subject to viability testing• Affordable Housing provision• Cross Rail Levy and hypothecation• Modelling to assess the planning gain tax

Conclusions

• Property taxation needs an overhaul• Equity and efficiency issues need to be addressed• Vested interests are likely to resist change and seek

new exemptions and reliefs• Do we need to try other approaches?