propertylink group 2016 09 15 - research-doc.credit-suisse.com

TRANSCRIPT

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, LEGAL ENTITY DISCLOSURE AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

15 September 2016 Asia Pacific/Australia

Equity Research Real Estate Management & Development

Propertylink Group

(PLG.AX / PLG AU) Rating OUTPERFORM Price (15-Sep,A$) .75 Target Price (A$) .92 Target price ESG risk (%) Market cap (A$mn) 452.1 Yr avg. mthly trading (A$mn) 109.0 Projected return: Capital gain (%) 22.7 Dividend yield (net %) 9.3 Total return (%) 32.0 *Stock ratings are relative to the relevant country benchmark.

¹Target price is for 12 months.

[V] = Stock Considered Volatile (see Disclosure Appendix)

Research Analysts

Mikhail Mohl

61 2 8205 4413

Ian Randall

612 8205 4580

Martin Patz

61 2 8205 4018

Specialist sales: Bhupen Master

61 2 8205 4792

INITIATION

8.70% implied cap rate, 5% MT growth

■ 32% Total Return. We initiate coverage on PLG with an Outperform rating

and a $0.92 Target Price. Our SOTP val ascribes no premium to the book

WACR (7.65%) & 12.0x to funds mgt, similarly, our DCF val adopts a sector

high 11.2% geared cost of equity. PLG offers a prospective distribution yield

of 9.1%, which equates to a 420bp spread to the A-REIT average.

■ What's being priced in? At current levels, PLG is trading on an implied cap

rate of 8.70%, reflecting a 7% discount to current book values vs the 6% avg

premium implied for A-REITs. Similarly, running spot bonds through our DCF

valuations suggests PLG is pricing in un-levered terminal growth of -1.8% vs

+1.4% for A-REITs. Notably, this is despite PLG's 5.2%pa MT (FY17-21)

FFO growth trajectory under our base case or 8.0%pa under our bull case.

Our base case assumes a 39% reduction in average AUM growth (in

absolute terms) relative to FY15 & FY16 AUM growth. As such, we believe

execution risks around leasing & FUM growth are being more than priced in.

■ Investment case. PLG is an Australia-focused internally managed property

trust with a fully integrated real estate platform, a $685mn portfolio of 33

predominantly industrial assets (>80% Sydney & Melbourne) with a rapidly

growing funds management platform (~$1bn) backed by 8 global institutional

investors. PLG backs its deep in-house asset management capability to take

advantage of typically B–Grade commercial assets with value add potential.

■ Solid progress since listing. PLG has made a promising start to the 2017

fiscal year. 2.5mths into the year, PLG is running ahead of PDS estimates on

a number of fronts including leasing (90% tenant retention ytd / 11 of 27

deals completed), debt costs, co-investment income and property

management & leasing fees. Post the Denison acquisition (~$176m), PLG is

targeting a further ~$500m of acquisitions in FY17 and is currently bidding

(or in exclusive due-diligence) on ~$280m of potential transactions.

Performance 1M 3M 12M Absolute (%) -7.41 Relative (%) -2.13

Financial and valuation metrics

Year 6/17E 6/18E 6/19E Revenue (A$ mn) - - - EBITDA (A$ mn) 53 58 60 EBIT (A$ mn) 53 58 60 Net Income (Adj.) (A$ mn) 43 47 49 EPS (Adj.) (Ac) 7.21 7.82 8.12 Change from previous EPS (%) EPS growth (%) 8.5 3.9 Consensus EPS (Ac) 7.00 7.00 8.00 P/E (x) 10.4 9.6 9.2 Dividends (Ac) 6.85 7.43 7.69 Dividend yield (%) 9.1 9.9 10.3 Price/Book (x) 0.9 0.9 0.9 Net debt/EBITDA (x) 5.1 4.8 4.7

Source: Company data, Thomson Reuters, Credit Suisse estimates

15 September 2016

Propertylink Group

(PLG.AX / PLG AU) 2

Table of contents

Executive Summary 4

Investment thesis...................................................................................................... 4

PLG overview ........................................................................................................... 4

$0.92 Target Price, Outperform Rating 5

Valuation methodologies .......................................................................................... 7

Peer comparison .................................................................................................... 10

Operational progress since listing 14

Financial Forecasts 15

Strengths and opportunities 20

Key risks 26

Investment portfolio 29

Portfolio metrics and comps ................................................................................... 32

External Funds 34

Business overview .................................................................................................. 34

Historical performance of External funds ............................................................... 36

Management fees ................................................................................................... 36

Co-investments in External funds........................................................................... 37

External fund investors ........................................................................................... 37

Australian Industrial Markets 39

Sydney .................................................................................................................... 39

Melbourne ............................................................................................................... 41

Brisbane ................................................................................................................. 43

Perth ....................................................................................................................... 45

ESG 47

Summary ................................................................................................................ 47

Environment ........................................................................................................... 47

Social ...................................................................................................................... 48

Governance ............................................................................................................ 48

Senior management and board 51

Senior management team ...................................................................................... 51

Board of Directors .................................................................................................. 52

15 September 2016

Propertylink Group

(PLG.AX / PLG AU) 3

Propertylink Group (PLG.AX / PLG AU)

Price (15 Sep 2016): A$0.75; Rating: OUTPERFORM; Target Price: A$0.92; Analyst: Mikhail Mohl

Income Statement 6/17E 6/18E 6/19E

Net Property Income 49 50 51 Residential Development income - - - Construction income - - - Infrastructure development 3 2 1 Operating Expenses (excl. D&A) (11) (12) (12) EBITDA 53 58 60 EBIT 53 58 60 Net interest exp. (9) (10) (10) Other non-operating & non-recurring items (19) (20) (20) Profit before tax 44 48 50 Surplus/deficit on inv property 0 0 0 Income tax (1) (1) (1) Minorities - - - Exceptionals 0 0 0 Net profit (Reported) 43 47 49 Analyst after tax adjustments 0 0 0 Normalised NPAT 43 47 49 Distributable income to unitholders 43 47 49

Balance Sheet 6/17E 6/18E 6/19E

Cash & equivalents 8 10 11 Receivables 0 0 0 Other current assets 4 4 4 Current assets 12 13 15 Property, plant & equip. 92 92 92 Intangibles 5 5 5 Properties under development 0 0 0 Investment properties 614 626 638 Other assets 50 59 67 Total assets 773 795 816 Accounts Payables 0 0 0 Interest bearing debt - Current 0 0 0 Other short-term liabilities 0 0 0 Total current liabilities 0 0 0 Interest bearing debt - Non-Current 280 287 293 Other non-current Liabilities 9 9 9 Total liabilities 288 296 302 Ordinary Equity 485 499 514 Minorities & Others - - - Total liabilities and equity 773 795 816

Cash Flow 6/17E 6/18E 6/19E

EBIT 53 58 60 Net Interest (9) (10) (10) Depr & Amort 0 0 0 Tax Paid (1) (1) (1) Change in Working capital -0 -0 -0 Other cash and non-cash items 1 2 3 Operating cashflow 44 49 52 Capex (17) (1) (1) Capex - expansionary (16) 0 0 Capex - Maintenance (1) (1) (1) Acquisitions & Invest 0 0 0 Asset sale proceeds 9 0 0 Other - - - Investing cashflow (7) (1) (1) Dividends paid (41) (45) (46) Equity raised - - - Net borrowings 7 0 0 Other financing cash in/(outflows) 0 0 0 Financing cashflow (35) (45) (46) Total cashflow 2 3 4 Adjustments 0 0 0 Movement in cash/equivalents 2 3 4

Earnings 6/17E 6/18E 6/19E

Equiv. FPO (period avg) (mn) 603 603 603 EPS (CS underlying) (C) 7.2 7.8 8.1 EPS Growth (%) - 8.5 3.9 Net Income Margin 88.8 93.4 95.2 DPS (C) 6.9 7.4 7.7 AFFO per share (C) 7.1 7.7 7.9 NTA per share (C) 79.7 82.1 84.6 NRI growth - 3.2 1.9

Valuation 6/17E 6/18E 6/19E

EV/EBITDA (x) 13.4 12.4 12.0 P/E (CS) (x) 10.4 9.6 9.2 P/NTA (X) 0.9 0.9 0.9 P/AFFO (X) 10.6 9.8 9.5 Dividend Yield (%) 9.1 9.9 10.3

Returns 6/17E 6/18E 6/19E

Return on Equity (%) 9.0 9.4 9.5 ROIC (avg.) (%) - 7.4 7.5 Asset turnover (X) 0.1 0.1 0.1 Interest Cover 5.7 6.0 6.1

Gearing 6/17E 6/18E 6/19E

Net debt / Investment properties (%) 44.2 44.4 44.2 Debt / EBITDA (X) 5.2 4.9 4.9 Total Liabilities / Total Assets (%) 37.3 37.2 37.0 Dividend Cover - - - Prem/disc NTA (%) (5.9) (8.6) (11.3)

MSCI IVA Rating

Share price performance

On 15-Sep-2016 the S&P ASX 200 Index closed at 5239.9

On 15-Sep-2016 the spot exchange rate was A$1.34/US$1

Source: Company data, Credit Suisse estimates

Global Local Country

Environment Social Governance

0

1

2

3

4

5

6

7

8

G

LC

G

L CG

L

C

15 September 2016

Propertylink Group

(PLG.AX / PLG AU) 4

Executive Summary

Investment thesis

We view Propertylink as a relatively unique real estate investment opportunity in the

context of the A-REIT sector. PLG has an experienced management team (+20yrs

average experience), a fully integrated real estate platform and a sound balance sheet,

which means it is well positioned to deal with its relatively high level of income expiry risk

in the medium term, but also continue to demonstrate its ability to add value. Our analysis

and site visits suggest PLG has had good success in adding value to the majority of

balance sheet and fund acquisitions in recent years on the back of well executed asset

specific leasing and positioning strategies.

In our view, PLG's business model is well positioned to generate above sector average

earnings growth in the medium term. PLG's track record of growing its FUM base

considerably in recent years, whilst still generating very strong returns for its investors

demonstrates this capability. Furthermore, even based on our conservative medium term

FUM growth assumptions, we believe PLG can generate considerably higher quality

investment management fees as the magnitude of transactional fees reduces relative to

the FUM base, but also, we see considerable scope to improve margins overtime given

each dollar of incremental FUM is more than twice as profitable as the existing fee base.

PLG overview

PLG is the only Australia-focused, internally managed industrial & logistics trust and

integrated investment and asset management platform. PLG wholly owns a diversified

portfolio of 33 industrial properties (including Business parks) located across Sydney,

Melbourne, Brisbane and Perth. The portfolio was independently valued at $685m as at 30

June 2016, has an occupancy rate of 95.0%, a weighted average lease expiry (WALE) of

3.6 years (by income and by GLA) and a diversified income profile with approximately 176

tenants and no single tenant contributing more than 5% of lease income.

Figure 1: Balance sheet portfolio summary (as at June 2016)

Source: Company data

The investment and asset management business generates fee revenue from the

management of External funds, as well as income from distributions paid in respect of

PLG's fund co-investments. On our estimates, investment management (excluding co-

investment income) represents ~9% of FY17 operating EBIT. As at 30 June 2016, the

investment and asset management business had total AUM of over $1.55bn, of which

approximately $873m is managed through 9 External funds. Subsequent to listing, PLG

launched a 10th fund (Propertylink Enhanced Partnership) to house the ~$176m Denison

portfolio acquisition. In addition, PLG settled on the $135m Charter Hall industrial portfolio

acquisition on behalf of PAIP II. These transactions are consistent with the Group's goal to

grow external FUM by $675m (net) to >$1.5bn in FY17.

Number of properties 33

Independent valuation (A$m) $685.0

Gross lettable area (sqm) 515,403

Occupancy by GLA 95.0%

WALE by income (years) 3.6

WALE by GLA (years) 3.6

Weighted Average Capitalisation Rate 7.92%

Passing net rental income (p.a.) $52,892,279

Fully leased passing net rental income (p.a.) $56,207,488

15 September 2016

Propertylink Group

(PLG.AX / PLG AU) 5

$0.92 Target Price, Outperform Rating We initiative coverage on PLG with an Outperform rating

Our PLG Target Price of $0.92 represents 23% capital upside from current pricing and a

prospective total shareholder return of 32% compared with 3% and 9% (arithmetic

average) respectively on offer from our broader A-REIT coverage universe.

Figure 2: CS Total Shareholder Returns & Ratings Figure 3: Credit Suisse A-REIT ratings composition

Source: Credit Suisse estimates Source: Credit Suisse estimates

Execution risk more than priced in

At PLG's last close of $0.75, PLG is trading on par with its NTA backing, however, this

ignores the contribution from the Group's investment management business, which

contributes 12% of FY18 operating EBIT (post cost allocation). On our estimates, PLG is

trading on an implied cap rate of 8.70% (vs a book WACR of 7.65%) and has the most

undervalued portfolio in the sector (Figure 4). Specifically, we have deducted our valuation

of PLG's investment management business ($82m / 12.0x EBIT multiple) from the current

enterprise value, which implies that the market is ascribing a 6% discount to the book

value of PLG's industrial portfolio compared with a +6% average premium (arithmetic) for

the broader A-REIT sector.

Another valuation exercise we believe provides a good cross-check to our SOTP is to run

spot bonds (risk free rate) through our 5yr DCF valuations in order to estimate the terminal

growth rate that is implied by current share prices. We then compare this on an unlevered

basis and overlay this with the level of capital being retained by each A-REIT over the 5yr

forecast period. Once again, this highlights PLG's considerable relative and absolute value

proposition. Specifically, this analysis suggests that PLG's current share price is implying

unlevered terminal growth of -1.8% vs +1.4% on average for A-REITs (Figure 5).

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

PLG WFD SCG GPT GDI SGP MGR GMG IOF VCX DXS CQR CMW SCP BWP CHC

Neutral UnderperformOutperform

OUTPERFORM25%

NEUTRAL37%

UNDERPERFORM38%

Pricing in a negative terminal growth rate

15 September 2016

Propertylink Group

(PLG.AX / PLG AU) 6

Figure 4: Implied premium (discount) to book value Figure 5: Implied un-levered terminal growth rate

Source: Company data, Credit Suisse estimates Source: Credit Suisse estimates

Below we provide a valuation sensitivity highlighting the valuation upside (downside) vs

the current share price based on tighter (softer) cap rates and higher (lower) EBIT

multiples on investment management EBIT within our SOTP valuation framework (all other

variables/assumptions held constant).

Figure 6: SOTP valuation sensitivity – WACR & Funds Mgmt multiples

Source: Credit Suisse estimates

Figure 7: SOTP valuation upside to current share price

Source: Credit Suisse estimates

Above sector average growth on conservative FUM growth assumptions

Furthermore, we estimate PLG can deliver above sector average (4.2%) FFO ps growth of

5.5% per annum over FY17 to FY20, despite allowing for 39% reduction in FUM growth in

absolute terms relative to the prior two years and PLG's considerably larger FUM base

(/platform). Notably, our estimates assume comparable NOI growth of ~1.9% pa (allowing

for some negative re-leasing spreads detracting from higher embedded fixed increases).

In addition we have not explicitly incorporated any balance sheet acquisitions, which would

be highly accretive given PLG's ~3.2% WACD.

23%

10%9%

8%6% 6%

5%3%

1%

-2% -2%

-4%

-7%-10%

-5%

0%

5%

10%

15%

20%

25%

BW

P

SC

P

CQ

R

DX

S

CM

W

VC

X

IOF

GP

T

SG

P

SC

G

GD

I

MG

R

PLG

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

SC

P

DX

S

CH

C

CM

W

MG

R

CQ

R

VC

X

BW

P

IOF

GP

T

A-R

EIT

WF

D

GM

G

SG

P

SC

G

GD

I

PLG

Implied unlevered term growth (LHS) Sector avg growth (LHS) % of A-FFO retained (RHS)

7.05% 7.25% 7.45% 7.65% 7.85% 8.05% 8.25%

0.0x $0.89 $0.85 $0.81 $0.78 $0.74 $0.71 $0.68

4.0x $0.93 $0.89 $0.86 $0.82 $0.79 $0.76 $0.73

8.0x $0.98 $0.94 $0.90 $0.87 $0.83 $0.80 $0.77

12.0x $1.03 $0.98 $0.95 $0.92 $0.87 $0.84 $0.81

16.0x $1.07 $1.03 $0.99 $0.95 $0.92 $0.88 $0.85

20.0x $1.12 $1.07 $1.03 $1.00 $0.96 $0.93 $0.89

FM MultipleWeighted Avg Cap Rate

7.05% 7.25% 7.45% 7.65% 7.85% 8.05% 8.25%

0.0x 17% 12% 7% 3% -3% -7% -11%

4.0x 22% 17% 13% 8% 4% 0% -4%

8.0x 29% 24% 18% 14% 9% 5% 1%

12.0x 36% 29% 25% 21% 14% 11% 7%

16.0x 41% 36% 30% 25% 21% 16% 12%

20.0x 47% 41% 36% 32% 26% 22% 17%

FM MultipleWeighted Avg Cap Rate

Pricing in cap rate expansion and no value

to Funds Mgmt

6% MT growth despite assuming significantly

slower FUM growth

15 September 2016

Propertylink Group

(PLG.AX / PLG AU) 7

Figure 8: Propertylink AUM growth FY13 to FY20f

Source: Company data, Credit Suisse estimates

Valuation methodologies

We have used two primary valuation techniques in arriving at a valuation of the equity of

PLG: (1) a DCF-based valuation of forecast Adjusted Funds From Operations (A-FFO);

and (2) an NAV-based valuation (SOTP).

DCF-based equity valuation: $0.93

Our DCF valuation discounts five years of forecast Adjusted Funds From Operations (A-

FFO).

Key valuation parameters include:

■ An assumed risk-free rate of 4.0%.

■ Equity risk premium of 5.0%.

■ The adoption of an unlevered Beta of 0.91x.

■ We then adjust the applied Beta to take into account PLG's leverage (debt to equity),

resulting in a cost of equity of 11.2%.

■ We allow for terminal (geared) growth of 3.30%, resulting in a terminal yield of 7.88%.

■ Our A-FFO forecasts assume average External FUM growth via acquisition over FY18-

21 of $263m per annum (vs PLG's forecast $675m of FUM additions in FY17), in

addition to underlying valuation growth for PLG's FUM in line with forecast property

income growth (~2.0% per annum).

39

295

1,068

1,558

2,233

2,6962,859

3,098

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

FY13 FY14 FY15 FY16 FY17pf FY18f FY19f FY20f

43%

21%

6%

8%

656%

262%

46%

15 September 2016

Propertylink Group

(PLG.AX / PLG AU) 8

Figure 9: A-REIT geared cost of equity

Based on a 4% Rf (domestic A-REITs) / 5% ERP & our explicit levered beta assumptions

Source: Credit Suisse estimates

NAV (SOTP) based equity valuation: $0.91

Our SOTP valuation uses FY18F as the base year. With PLG's forecasts assuming a 43%

increase in external FUM over FY17, we believe adopting FY18 as the base valuation year

provides a more "stabilised" picture of PLG's Fund and Asset Management earnings.

Our NAV-based valuation is predicated on the following key valuation parameters:

■ Income from investment properties: Valuation capitalises our estimate of FY18 fully

leased NOI. We apply a WACR of 7.65%, reflecting no additional cap rate tightening to

the current book weighted average cap rate (7.65%). We believe this is conservative

considering the extent to which secondary industrial investment yield compression has

lagged that of prime. This is illustrated in the chart below which is representative of the

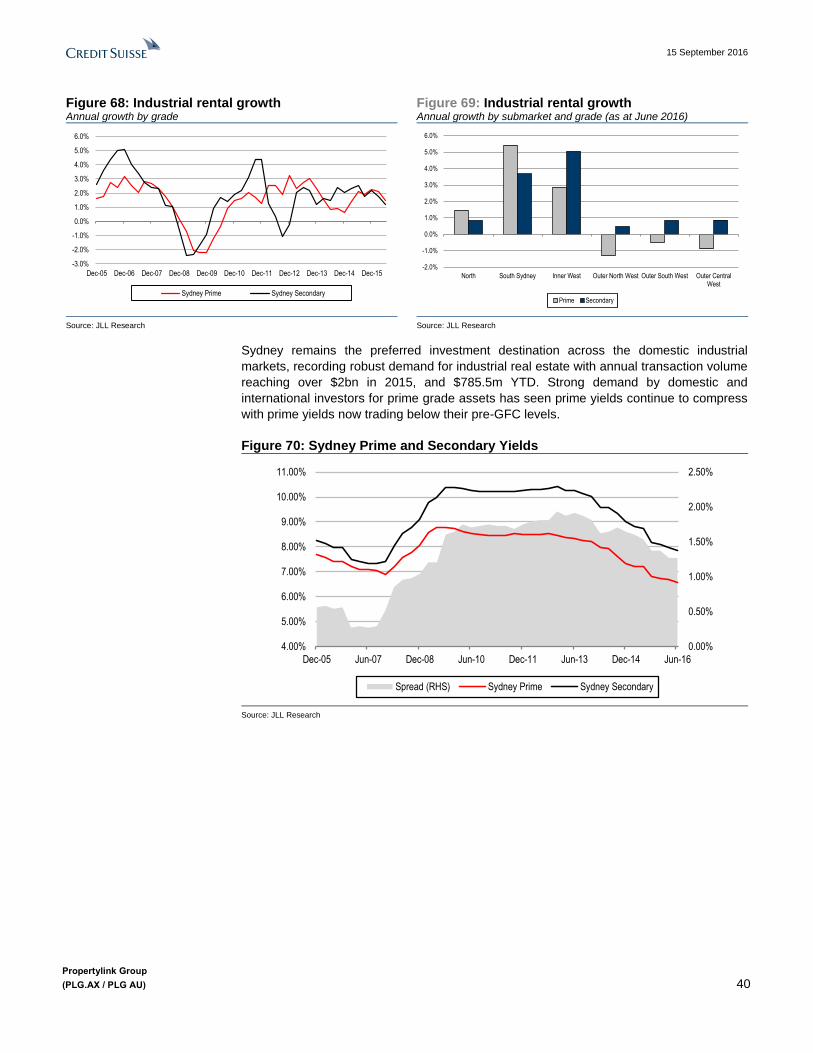

broader Sydney industrial market. We note that as at June 2016, the spread between

prime and secondary industrial yields stood at 127bps compared with only 29bps in

Sep-2007 and an average of 108bps since 2000.

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

CM

W

PLG GD

I

CH

C

SC

P

GM

G

CQ

R

SG

P

MG

R

DX

S

IOF

VC

X

GP

T

SC

G

BW

P

WF

D

Rf (trend) Geared premium

Secondary yields spreads to prime

remain considerable

15 September 2016

Propertylink Group

(PLG.AX / PLG AU) 9

Figure 10: Sydney Prime vs Secondary Industrial Yields

Mind the gap

Source: JLL Research, Credit Suisse estimates

■ Income from investment management: Our NAV valuation applies 12.0x to our

FY18F investment management EBIT. In setting our multiple, we have had regard for

the multiples implied by the trading prices of comparable businesses within the A-REIT

sector. Although several A-REITs engage in Funds Management activities, for most

groups, these represent a relatively small component of overall earnings. Hence,

estimating an implied multiple for the Funds Management earnings of these groups

entails a high degree of subjectivity.

In our view, Charter Hall Group (CHC.AX) and Goodman Group (GMG.AX) offer the

"cleanest" comps for PLG's Fund and Asset Management businesses. We estimate

that current market pricing implies FY18F EBIT multiples for these Groups' Investment

Management businesses of 15.8x and 12.5x respectively. In setting our multiple range

for PLG relative to those implied for CHC and GMG, we have taken into account

several factors, including: (1) the absence of performance fees from our earnings

forecasts for PLG (whereas we estimate these will make up 9% and 7% of CHC and

GMG Investment Management revenues respectively in FY18f); (2) PLG's relatively

short track-record in its current form, vs the well-established CHC and GMG

businesses; (3) PLG's far smaller scale in terms of FUM. It could be argued that this

size differential warrants either a discount for PLG (reflecting its less established

nature) or a premium (given greater growth potential and scaleability benefits, given

that PLG believes its current cost base could support far higher levels of FUM).

■ Cornerstone investment in External funds: We value PLG's drawn cornerstone

equity stakes in line with our estimate of their book value in FY18.

■ Corporate expenses & other net assets. From our derived asset-level valuation, we

then deduct forecast RE fees and other expenses (capitalised at 10.0x), net debt and

other assets / (liabilities).

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

4.00%

5.00%

6.00%

7.00%

8.00%

9.00%

10.00%

11.00%

Dec-05 Jun-07 Dec-08 Jun-10 Dec-11 Jun-13 Dec-14 Jun-16

Spread (RHS) Sydney Prime Sydney Secondary

We apply 12x vs 16x implied for CHC

15 September 2016

Propertylink Group

(PLG.AX / PLG AU) 10

Figure 11: PLG.AX – SOTP Val (FY18)

Source: Company data, Credit Suisse estimates

Adopted valuation: $0.92

Our adopted valuation represents the mid-point of our DCF-based and SOTP valuations.

In setting our valuation range, we have also taken into account FFO yield, dividend yield

and price to NTA relativities versus comparable groups. This valuation range reflects:

■ A multiple of 1.22x net tangible assets (NTA).

■ A forecast annualised distributable earnings yield (based on FY17 forecasts) of 7.4%.

■ A forecast annualised distribution yield (again based on FY17 forecasts) of 7.8%.

Figure 12: Valuation summary metrics at variable pricing

Source: IRESS, Company data, Credit Suisse estimates

Peer comparison

As an owner and investment manager of predominantly industrial real estate assets and

funds, PLG has a number of domestic companies that are relevant for valuation purposes.

We have examined eleven comparable A-REITs with reference to a number of valuation

and performance measures.

Investment Properties 56.2 7.65% 735.3

Cornerstones (FY18f avg book value) 54

Management (post notional overhead allocation) 6.5 12.0x 78

Gross Asset Value 867

Corporate costs (50bp MER) -3.7 10.0x -36.8

Net debt (FY18f avg) -274.5

Net other assets -4.8

Net asset value 551.0

Weighted avg securities on issue (FY18; fully diluted) 603

Value per security 0.91$

Propertylink SOTP Val FY18f / trend

income

Cap rate /

multiple

Value

(A$m)

Equity pricing range A$ $0.65 $0.75 $0.85 $0.95 $1.05

Premium / (discount) to last close) -14.5% -1.3% 11.8% 25.0% 38.2%

Premium / (discount) to NTA ps -13.9% -0.7% 12.6% 25.8% 39.1%

Premium / (discount) to CS TP -29.4% -18.6% -7.7% 3.1% 14.0%

FY17 FFO Multiple 9.0x 10.4x 11.8x 13.2x 14.6x

FY18 FFO Multiple 8.3x 9.6x 10.9x 12.1x 13.4x

FY17 DPS Yield 10.5% 9.1% 8.1% 7.2% 6.5%

FY18 DPS Yield 11.4% 9.9% 8.7% 7.8% 7.1%

Weighted average cap rate 7.65% 7.65% 7.65% 7.65% 7.65%

Implied Cap Rate 9.50% 8.72% 8.00% 7.45% 6.95%

15 September 2016

Propertylink Group

(PLG.AX / PLG AU) 11

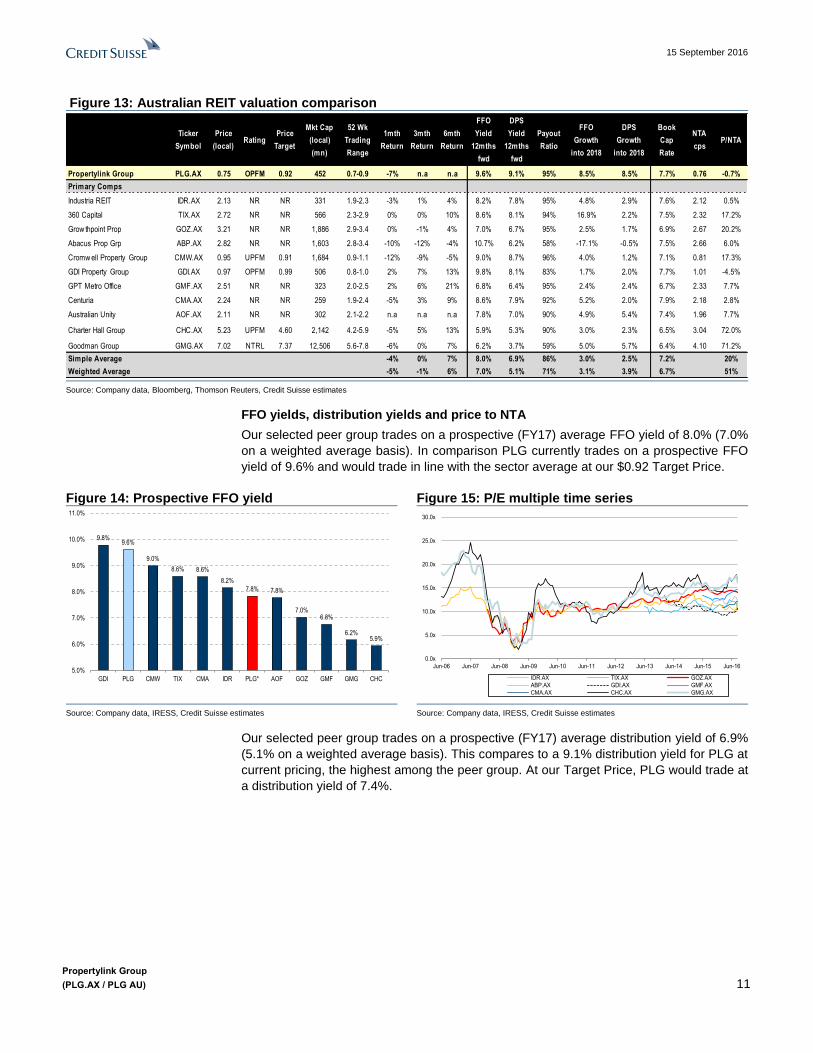

Figure 13: Australian REIT valuation comparison

Source: Company data, Bloomberg, Thomson Reuters, Credit Suisse estimates

FFO yields, distribution yields and price to NTA

Our selected peer group trades on a prospective (FY17) average FFO yield of 8.0% (7.0%

on a weighted average basis). In comparison PLG currently trades on a prospective FFO

yield of 9.6% and would trade in line with the sector average at our $0.92 Target Price.

Figure 14: Prospective FFO yield Figure 15: P/E multiple time series

Source: Company data, IRESS, Credit Suisse estimates Source: Company data, IRESS, Credit Suisse estimates

Our selected peer group trades on a prospective (FY17) average distribution yield of 6.9%

(5.1% on a weighted average basis). This compares to a 9.1% distribution yield for PLG at

current pricing, the highest among the peer group. At our Target Price, PLG would trade at

a distribution yield of 7.4%.

Ticker

Symbol

Price

(local)Rating

Price

Target

Mkt Cap

(local)

(mn)

52 Wk

Trading

Range

1mth

Return

3mth

Return

6mth

Return

FFO

Yield

12mths

fwd

DPS

Yield

12mths

fwd

Payout

Ratio

FFO

Growth

into 2018

DPS

Growth

into 2018

Book

Cap

Rate

NTA

cpsP/NTA

Propertylink Group PLG.AX 0.75 OPFM 0.92 452 0.7-0.9 -7% n.a n.a 9.6% 9.1% 95% 8.5% 8.5% 7.7% 0.76 -0.7%

Primary Comps

Industria REIT IDR.AX 2.13 NR NR 331 1.9-2.3 -3% 1% 4% 8.2% 7.8% 95% 4.8% 2.9% 7.6% 2.12 0.5%

360 Capital TIX.AX 2.72 NR NR 566 2.3-2.9 0% 0% 10% 8.6% 8.1% 94% 16.9% 2.2% 7.5% 2.32 17.2%

Grow thpoint Prop GOZ.AX 3.21 NR NR 1,886 2.9-3.4 0% -1% 4% 7.0% 6.7% 95% 2.5% 1.7% 6.9% 2.67 20.2%

Abacus Prop Grp ABP.AX 2.82 NR NR 1,603 2.8-3.4 -10% -12% -4% 10.7% 6.2% 58% -17.1% -0.5% 7.5% 2.66 6.0%

Cromw ell Property Group CMW.AX 0.95 UPFM 0.91 1,684 0.9-1.1 -12% -9% -5% 9.0% 8.7% 96% 4.0% 1.2% 7.1% 0.81 17.3%

GDI Property Group GDI.AX 0.97 OPFM 0.99 506 0.8-1.0 2% 7% 13% 9.8% 8.1% 83% 1.7% 2.0% 7.7% 1.01 -4.5%

GPT Metro Office GMF.AX 2.51 NR NR 323 2.0-2.5 2% 6% 21% 6.8% 6.4% 95% 2.4% 2.4% 6.7% 2.33 7.7%

Centuria CMA.AX 2.24 NR NR 259 1.9-2.4 -5% 3% 9% 8.6% 7.9% 92% 5.2% 2.0% 7.9% 2.18 2.8%

Australian Unity AOF.AX 2.11 NR NR 302 2.1-2.2 n.a n.a n.a 7.8% 7.0% 90% 4.9% 5.4% 7.4% 1.96 7.7%

Charter Hall Group CHC.AX 5.23 UPFM 4.60 2,142 4.2-5.9 -5% 5% 13% 5.9% 5.3% 90% 3.0% 2.3% 6.5% 3.04 72.0%

Goodman Group GMG.AX 7.02 NTRL 7.37 12,506 5.6-7.8 -6% 0% 7% 6.2% 3.7% 59% 5.0% 5.7% 6.4% 4.10 71.2%

Simple Average -4% 0% 7% 8.0% 6.9% 86% 3.0% 2.5% 7.2% 20%

Weighted Average -5% -1% 6% 7.0% 5.1% 71% 3.1% 3.9% 6.7% 51%

9.8%9.6%

9.0%

8.6% 8.6%

8.2%

7.8% 7.8%

7.0%6.8%

6.2%5.9%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

11.0%

GDI PLG CMW TIX CMA IDR PLG* AOF GOZ GMF GMG CHC

0.0x

5.0x

10.0x

15.0x

20.0x

25.0x

30.0x

Jun-06 Jun-07 Jun-08 Jun-09 Jun-10 Jun-11 Jun-12 Jun-13 Jun-14 Jun-15 Jun-16

IDR.AX TIX.AX GOZ.AX

ABP.AX GDI.AX GMF.AX

CMA.AX CHC.AX GMG.AX

15 September 2016

Propertylink Group

(PLG.AX / PLG AU) 12

Figure 16: Prospective dividend yield Figure 17: Distribution yield time-series

Source: Company data, IRESS, Credit Suisse estimates Source: Company data, IRESS, Credit Suisse estimates

Our selected peer group trades on an average price to NTA multiple of 1.20x or 1.53x for

Group's with active income streams such as GMG, CHC and CMW. In comparison PLG

currently trades at a 1% discount to NTA.

Figure 18: Premium (discount) to NTA Figure 19: Price/NTA time-series

Source: Company data, IRESS, Credit Suisse estimates Source: Company data, IRESS, Credit Suisse estimates

9.1%

8.7%

8.1% 8.1% 7.9%7.8%

7.4%

7.0%6.7%

6.4%6.2%

5.3%

3.7%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

PLG CMW GDI TIX CMA IDR PLG* AOF GOZ GMF ABP CHC GMG

*At price target

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

11.0%

12.0%

Feb-10 Aug-10 Feb-11 Aug-11 Feb-12 Aug-12 Feb-13 Aug-13 Feb-14 Aug-14 Feb-15 Aug-15 Feb-16 Aug-16

IDR.AX TIX.AX GOZ.AX ABP.AX GDI.AX

GMF.AX AOF.AX CHC.AX GMG.AX

72.0% 71.2%

21.8% 20.2%17.3% 17.2%

7.7% 7.7% 6.0%2.8%

0.5%

-0.7%-4.5%-10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

CHC GMG PLG* GOZ CMW TIX GMF AOF ABP CMA IDR PLG GDI

*At price target

0.6x

0.8x

1.0x

1.2x

1.4x

1.6x

1.8x

2.0x

2.2x

2.4x

Jul-13 Oct-13 Jan-14 Apr-14 Jul-14 Oct-14 Jan-15 Apr-15 Jul-15 Oct-15 Jan-16 Apr-16 Jul-16

IDR.AX TIX.AX GOZ.AX ABP.AX GDI.AX

GMF.AX CMA.AX CHC.AX GMG.AX

15 September 2016

Propertylink Group

(PLG.AX / PLG AU) 13

Credit Suisse bottom up A-REIT valuation tables

Figure 20: A-REIT Leader Tables

Source: Company data, Credit Suisse estimates

Bottom Up Sector Valuation Preferences

TickerCurrent

Price ($)

Target

Price ($)

Prem. / (Disc)

to Target

Price

Dividend

Yield

TSR

(%)

Earnings

Yield

12mth

fwd PE

FY16-17

EPS

Growth

FY17-19

EPS

Growth

EPS Yield

plus 3yr

growth

Book Cap

Rate

Prem. /

(Disc) to NTARating

LLC.AX 13.26 17.00 -22.9% 5.3% 33.7% 9.8% 10.2x 8.2% 9.4% 19.2% NA n.a OUTPERFORM

PLG.AX 0.76 0.92 -19.7% 9.1% 31.1% 9.5% 10.5x n.a 6.5% 16.0% 7.7% -0.7% OUTPERFORM

WFD.AX 9.56 11.34 -16.0% 3.5% 22.2% 4.9% 20.5x 5.2% 12.5% 17.3% 4.9% 60.4% OUTPERFORM

SCG.AX 4.53 5.27 -14.5% 4.8% 21.3% 5.3% 18.9x 5.3% 5.2% 10.5% 5.6% 31.5% OUTPERFORM

GPT.AX 4.77 5.21 -9.4% 5.1% 14.4% 6.4% 15.7x 2.9% 4.1% 10.5% 5.9% 8.9% NEUTRAL

GDI.AX 0.94 0.99 -7.0% 8.2% 13.8% 9.6% 10.4x -0.7% 5.4% 15.1% 7.5% -7.2% OUTPERFORM

MGR.AX 2.16 2.30 -7.2% 4.8% 11.6% 6.7% 14.9x 11.3% 1.8% 8.5% 6.5% 12.2% NEUTRAL

SGP.AX 4.50 4.73 -6.1% 5.7% 11.0% 6.6% 15.3x 6.0% 6.0% 12.5% 6.5% 17.7% NEUTRAL

GMG.AX 6.93 7.37 -6.7% 3.7% 10.1% 6.2% 16.1x 7.0% 6.6% 12.8% 6.6% 69.0% NEUTRAL

IOF.AX 4.33 4.48 -4.4% 4.6% 8.3% 6.8% 14.8x 2.2% 2.8% 9.5% 6.3% 2.2% NEUTRAL

VCX.AX 3.02 3.08 -3.2% 5.8% 7.8% 6.2% 16.1x -1.7% 4.3% 10.6% 6.1% 16.6% NEUTRAL

DXS.AX 8.68 8.78 -2.2% 5.2% 6.4% 7.3% 13.7x 0.6% -1.0% 6.4% 6.5% 15.3% UNDERPERFORM

CQR.AX 4.08 4.00 0.3% 7.1% 5.3% 7.5% 13.3x 1.1% 3.6% 11.1% 6.9% 7.5% UNDERPERFORM

CMW.AX 0.96 0.91 3.8% 8.7% 3.2% 8.8% 11.3x -9.5% 2.0% 10.9% 7.5% 18.8% UNDERPERFORM

SCP.AX 2.13 2.04 2.8% 5.9% 2.0% 6.6% 15.1x 2.5% 4.7% 11.3% 7.3% 10.7% UNDERPERFORM

BWP.AX 3.06 2.92 3.5% 5.7% 1.1% 5.7% 17.6x 3.3% 3.1% 8.7% 6.8% 19.5% UNDERPERFORM

CHC.AX 5.17 4.60 11.1% 5.4% -5.6% 6.0% 16.7x 2.0% 3.8% 9.8% 6.6% 70.1% UNDERPERFORM

Average -5.8% 5.8% 11.6% 7.1% 14.8x 2.9% 4.8% 11.8% 6.6% 22.0%

Weighted -9.1% 5.0% 14.8% 6.3% 16.3x 4.4% 5.6% 11.9% 5.7% 28.9%

Thursday, 15 Sep, 2016

15 September 2016

Propertylink Group

(PLG.AX / PLG AU) 14

Operational progress since listing PLG has made a promising start to the 2017 fiscal year. Two and a half months into the

year, we note that PLG is running ahead of PDS estimates on a number of fronts including

investment portfolio leasing, debt costs, co-investment income and is well on track in

regards to property management, leasing and acquisition fees.

Denison transaction – 26% targeted FY17 acquisitions in the bag

Most notably, PLG exercised its option to acquire the 13 asset Denison portfolio on August

31 2016 for ~$176m. As expected, PLG acquired 9 of the assets for $142m and

subsequently sold 4 assets to individual buyers at a ~10% premium (~$3m) to PLG's

acquisition price. Notably, PLG acquired the portfolio at a ~10% discount to book values

and reflected a passing yield of 8.9%. In line with the supplementary PDS, PLG have

committed $17.7m of equity (or 25%) to the new PEP fund which includes Goldman Sachs

as the sole investor. Management are confident of growing the PEP fund with further

acquisitions and PLG are likely to maintain a 25% stake in the fund. The large co-

investment stake in PEP (25%) means that PLG has already secured its FY17 PDS

forecast for co-investment income.

Well positioned in terms of investment management fees for FY17

Similarly, PLG has secured in excess of 3 quarters of its forecast property management,

leasing fees and acquisition fees. Compositionally, the gap is largely made up by

acquisition fees. To date, PLG has secured $1.5m of the $3.5m full year forecast. We note

that PLG anticipate to complete a further ~$500m of acquisitions by year end and are

currently bidding (or in due diligence) on ~$280m of opportunities at present for its PAIP II

and SEDCO Funds. We note that PLG is also on track to dispose of 36-52 National

Boulevard, Campbellfield (Vic), with settlement forecast for late September 2016.

Year-to-date tenant retention running at 90%

We note that PLG has already completed 11 of the 27 leases that are forecast to be

completed over FY17. We understand that 10 of these were renewals with no income

downtime and the single new lease over ~600sqm of office space at the Villawood

property was not included in PDS forecasts for FY17. Below we highlight some more

colour on leasing progress to date on several key assets.

Figure 21: Leasing progress and update on key expiries

Source: Company data, Credit Suisse estimates

Secured interest swaps 32bp below PDS forecasts

PLG secured better than expected terms on interest rate hedging over 50% of its drawn

debt ($128m). PLG locked in 3yr and 5yr swaps at a rate of 1.83%, which was 32bp below

PDS expectations of 2.15%. PLG are now forecasting a WACD of ~3.2% for FY17.

Property State BV $%

Total

Cap

Rate

Occu-

pancy

WALE

(yrs)

GLA

(sqm)CS Comment

Gundah & Beaumont Rd, Mt Kuring-GaiNSW 56.2 8% 7.25% 98% 1.8 34,037

In discussions w ith key tenant Sheldon & Hammond (14% NPI) re a 5yr lease extension over 5,300sqm expiring in

Jan-17

Whitside & Main Rd, Clayton VIC 24.0 4% 8.50% 100% 0.5 28,195

Were previously looking to extend Corning Cable on a ST basis over ~11,000sqn, how ever, there is another tenant

interested in a a longer term deal over the entre 28,000sqm

Melbourne Markets, EppingVIC 92.0 13% 7.50% 100% 5.5 74,968

PLG replaced a distressed tenant w ith a new tenant on a long term (10yr) deal and achieved a 20% higher rent

7 Modal Crescent, Canning ValeWA 16.4 2% 8.00% 100% 0.3 15,251

Cahill Transport expected to renew its lease over 7,090sqm (October 2016 expiry)

44 Mandarin St, Villaw oodNSW 18.0 3% 9.75% 92% 3.0 20,294

Completed an off ice lease over 600sqm to a new tenant - upside to PDS forecasts

17-19 Leadership Way, WangaraWA 7.0 1% 8.25% 100% 0.6 5,415

Existing teant Pentair renew ed over the entire property 5,145sqm (August 2016 expiry). Likely to have exercised its

3 year option

39-41 McDow ell St, WelshpoolWA 8.0 1% 8.00% 100% 0.7 6,925

Confident that existing tenant (Iron Mountain) is likely to renew its lease over the entire property

8 Sylvania Way, LisarowNSW 7.4 1% 10.00% 100% 0.9 9,933

Demand stronger than expected w ith 2 potential leasing options. Non-core asset. Likely to be sold post leasing

success

122 New ton Rd, Wetherill ParkNSW 16.3 2% 7.00% 0% 0.0 9,614

Confident spec development w ill be leased on completion (Feb 2017)

15 September 2016

Propertylink Group

(PLG.AX / PLG AU) 15

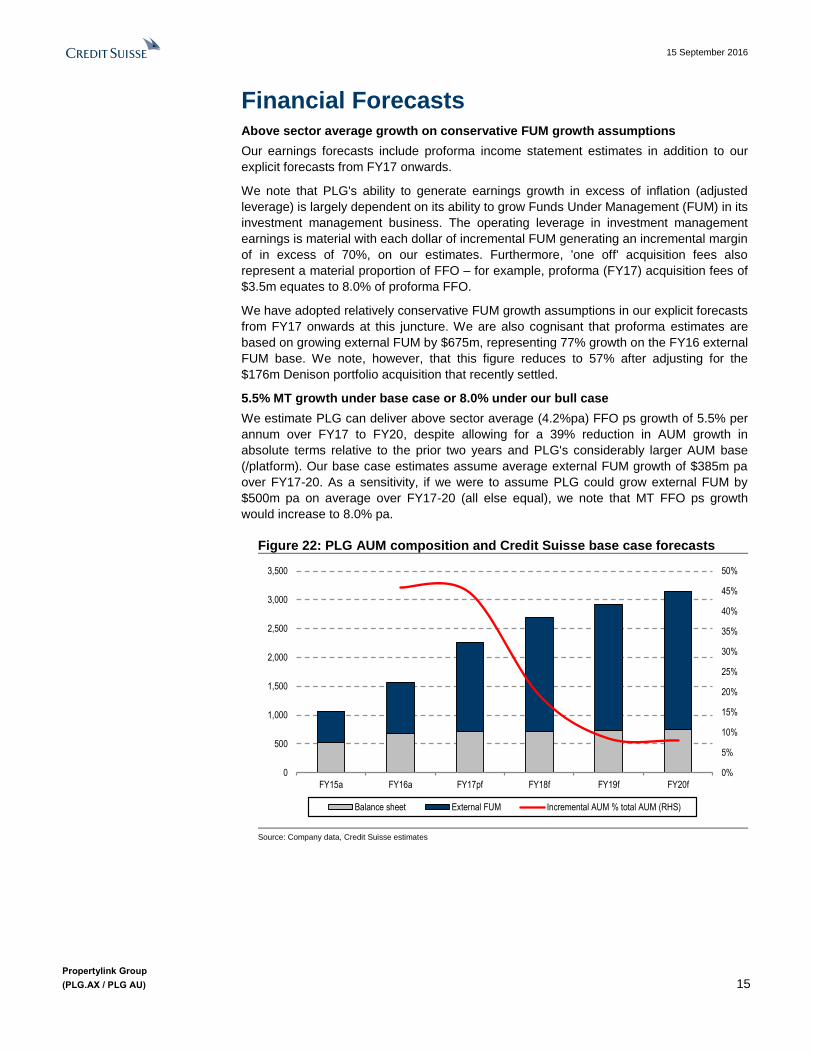

Financial Forecasts Above sector average growth on conservative FUM growth assumptions

Our earnings forecasts include proforma income statement estimates in addition to our

explicit forecasts from FY17 onwards.

We note that PLG's ability to generate earnings growth in excess of inflation (adjusted

leverage) is largely dependent on its ability to grow Funds Under Management (FUM) in its

investment management business. The operating leverage in investment management

earnings is material with each dollar of incremental FUM generating an incremental margin

of in excess of 70%, on our estimates. Furthermore, 'one off' acquisition fees also

represent a material proportion of FFO – for example, proforma (FY17) acquisition fees of

$3.5m equates to 8.0% of proforma FFO.

We have adopted relatively conservative FUM growth assumptions in our explicit forecasts

from FY17 onwards at this juncture. We are also cognisant that proforma estimates are

based on growing external FUM by $675m, representing 77% growth on the FY16 external

FUM base. We note, however, that this figure reduces to 57% after adjusting for the

$176m Denison portfolio acquisition that recently settled.

5.5% MT growth under base case or 8.0% under our bull case

We estimate PLG can deliver above sector average (4.2%pa) FFO ps growth of 5.5% per

annum over FY17 to FY20, despite allowing for a 39% reduction in AUM growth in

absolute terms relative to the prior two years and PLG's considerably larger AUM base

(/platform). Our base case estimates assume average external FUM growth of $385m pa

over FY17-20. As a sensitivity, if we were to assume PLG could grow external FUM by

$500m pa on average over FY17-20 (all else equal), we note that MT FFO ps growth

would increase to 8.0% pa.

Figure 22: PLG AUM composition and Credit Suisse base case forecasts

Source: Company data, Credit Suisse estimates

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0

500

1,000

1,500

2,000

2,500

3,000

3,500

FY15a FY16a FY17pf FY18f FY19f FY20f

Balance sheet External FUM Incremental AUM % total AUM (RHS)

15 September 2016

Propertylink Group

(PLG.AX / PLG AU) 16

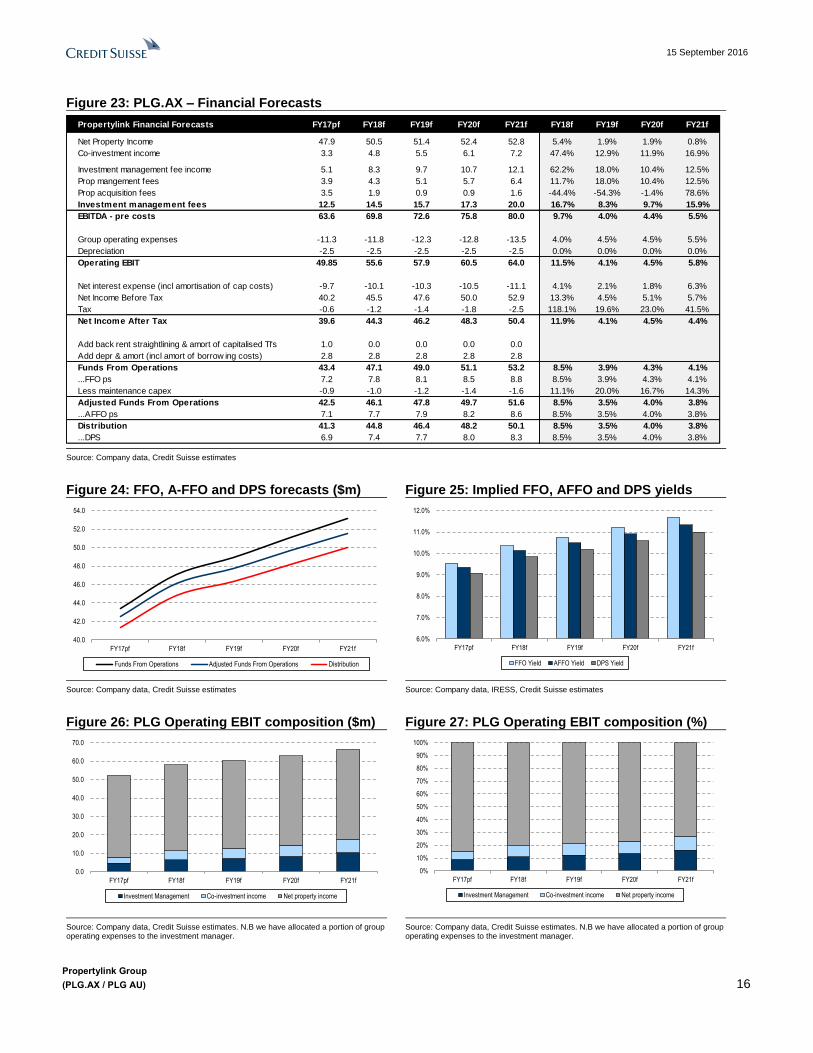

Figure 23: PLG.AX – Financial Forecasts

Source: Company data, Credit Suisse estimates

Figure 24: FFO, A-FFO and DPS forecasts ($m) Figure 25: Implied FFO, AFFO and DPS yields

Source: Company data, Credit Suisse estimates Source: Company data, IRESS, Credit Suisse estimates

Figure 26: PLG Operating EBIT composition ($m) Figure 27: PLG Operating EBIT composition (%)

Source: Company data, Credit Suisse estimates. N.B we have allocated a portion of group operating expenses to the investment manager.

Source: Company data, Credit Suisse estimates. N.B we have allocated a portion of group operating expenses to the investment manager.

Propertylink Financial Forecasts FY17pf FY18f FY19f FY20f FY21f FY18f FY19f FY20f FY21f

Net Property Income 47.9 50.5 51.4 52.4 52.8 5.4% 1.9% 1.9% 0.8%

Co-investment income 3.3 4.8 5.5 6.1 7.2 47.4% 12.9% 11.9% 16.9%

Investment management fee income 5.1 8.3 9.7 10.7 12.1 62.2% 18.0% 10.4% 12.5%

Prop mangement fees 3.9 4.3 5.1 5.7 6.4 11.7% 18.0% 10.4% 12.5%

Prop acquisition fees 3.5 1.9 0.9 0.9 1.6 -44.4% -54.3% -1.4% 78.6%

Investment management fees 12.5 14.5 15.7 17.3 20.0 16.7% 8.3% 9.7% 15.9%

EBITDA - pre costs 63.6 69.8 72.6 75.8 80.0 9.7% 4.0% 4.4% 5.5%

Group operating expenses -11.3 -11.8 -12.3 -12.8 -13.5 4.0% 4.5% 4.5% 5.5%

Depreciation -2.5 -2.5 -2.5 -2.5 -2.5 0.0% 0.0% 0.0% 0.0%

Operating EBIT 49.85 55.6 57.9 60.5 64.0 11.5% 4.1% 4.5% 5.8%

Net interest expense (incl amortisation of cap costs) -9.7 -10.1 -10.3 -10.5 -11.1 4.1% 2.1% 1.8% 6.3%

Net Income Before Tax 40.2 45.5 47.6 50.0 52.9 13.3% 4.5% 5.1% 5.7%

Tax -0.6 -1.2 -1.4 -1.8 -2.5 118.1% 19.6% 23.0% 41.5%

Net Income After Tax 39.6 44.3 46.2 48.3 50.4 11.9% 4.1% 4.5% 4.4%

Add back rent straightlining & amort of capitalised TI's 1.0 0.0 0.0 0.0 0.0

Add depr & amort (incl amort of borrow ing costs) 2.8 2.8 2.8 2.8 2.8

Funds From Operations 43.4 47.1 49.0 51.1 53.2 8.5% 3.9% 4.3% 4.1%

...FFO ps 7.2 7.8 8.1 8.5 8.8 8.5% 3.9% 4.3% 4.1%

Less maintenance capex -0.9 -1.0 -1.2 -1.4 -1.6 11.1% 20.0% 16.7% 14.3%

Adjusted Funds From Operations 42.5 46.1 47.8 49.7 51.6 8.5% 3.5% 4.0% 3.8%

...AFFO ps 7.1 7.7 7.9 8.2 8.6 8.5% 3.5% 4.0% 3.8%

Distribution 41.3 44.8 46.4 48.2 50.1 8.5% 3.5% 4.0% 3.8%

...DPS 6.9 7.4 7.7 8.0 8.3 8.5% 3.5% 4.0% 3.8%

40.0

42.0

44.0

46.0

48.0

50.0

52.0

54.0

FY17pf FY18f FY19f FY20f FY21f

Funds From Operations Adjusted Funds From Operations Distribution

6.0%

7.0%

8.0%

9.0%

10.0%

11.0%

12.0%

FY17pf FY18f FY19f FY20f FY21f

FFO Yield AFFO Yield DPS Yield

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

FY17pf FY18f FY19f FY20f FY21f

Investment Management Co-investment income Net property income

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY17pf FY18f FY19f FY20f FY21f

Investment Management Co-investment income Net property income

15 September 2016

Propertylink Group

(PLG.AX / PLG AU) 17

Below, we provide some additional colour on key income and expense items:

Net property income

Our estimates assume comparable NOI growth of ~1.9% pa (implicitly incorporating

negative re-leasing spreads partly offsetting the positive impact of higher embedded fixed

increases) and relatively stable occupancy and tenant retention levels (~95% and ~65%,

respectively). We believe this is appropriate given PLG has c.47% of income expiring over

the next 3 years. In addition, we have not explicitly incorporated any balance sheet

acquisitions, which would be highly accretive given PLG's 3.2% WACD.

Figure 28: A-REIT avg occupancy & comp NOIg Figure 29: A-REIT Industrial Comp NOI growth

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates. N.B DXS on effective basis.

Co-investment income

PLG's co-investment income consists of its equity accounted share of income from co-

investment stakes in its External Funds. PLG typically targets co-investment stakes of 5-

10%. Notably, given the relatively high leverage (~55%) in PLG's external funds, the co-

investment stakes generate a high yield (>10%).

Our forecasts assume PLG's co-investment stakes grow in-line with our discrete external

FUM growth assumptions (in addition to organic asset growth) – i.e. we have assumed a

constant PLG co-investment stake (~10%) for acquisitions from FY17 onwards. We

assume PLG's $23.9m drawn co-investment stake as at June 2016 increases to $49.9m

by June 2017 (consistent with PDS forecasts for an additional $26m to co-invest in the

$750m of targeted acquisitions).

Specifically, PLG has already committed $17.7m (25% equity stake) towards the recently

established PEP fund following the settlement of the Denison portfolio ($142m). The

remaining $8.3m of co-investments which form the $26m of additional forecast co-

investments over FY17 are expected to be invested in PAIP II, POP III and SEDCO.

Investment management

PLG generates both recurring and 'one-off' transactional and performance fees from its

External Funds platform (detailed below).

Notably, acquisition fees represent 28% of FY17 proforma investment management EBIT,

however, given our assumption for a more moderate rate of FUM growth over FY-18-21,

this reduces to 8% on average. As such, the underlying quality of investment management

earnings should improve overtime. We note that our forecasts do not explicitly assume any

performance fees including the $9.5m of performance fees that would be crystalised if the

asset in the POP II (320 Pitt St) Fund was sold down at its current valuation.

94.4%

-1.3%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

92.5%

93.5%

94.5%

95.5%

96.5%

97.5%

98.5%

Dec-08 Dec-09 Dec-10 Dec-11 Dec-12 Dec-13 Dec-14 Dec-15

A-REIT average occupancy A-REIT average comparable NOI growth

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

Dec-12 Jun-13 Dec-13 Jun-14

Dec-14 Jun-15 Dec-15 Jun-16

GPT DXSGPT MGR

15 September 2016

Propertylink Group

(PLG.AX / PLG AU) 18

Figure 30: PLG—External fund fee schedule

Source: Company data

We forecast investment management fees (comprising funds management, acquisition

and property management and leasing) increase from $12.5m in FY17 (proforma) to

$20.1m by FY21 (12.6% CAGR). We note however that this does not take into account the

scalability benefits as unallocated group costs increase below the rate of FUM growth.

After separately allocating trust expenses (based on a 50bp MER), our analysis suggests

that net investment management EBIT increases by 23%pa over FY17 to FY21.

This is illustrated below, Figure 31 highlights that net investment management fees (after

allowing for our estimate of the costs required to achieve those fees) as a percentage of

External FUM are forecast to moderately improve despite the fact that acquisition fees

reduce by 69% on average ($1.3m) over FY18-21 relative to FY17 ($3.5m)

Figure 31: Investment Management Fees as % External FUM

Net IM fees should steadily increase despite lower transactional fees in our est.

Source: Credit Suisse estimates

Type Description Typical Range

Acquisition feesPayable when Propertylink acquires property on behalf of the External Fund. A one-off

fee paid on settlement of an asset acquisition.0.45% - 0.50% of GAV p.a.

Base feesAn ongoing base management fee. Typically paid on a quarterly basis in arrears in

March, June, September and December.0.45% - 0.50% of GAV p.a.

Performance fees

A performance fee payable to Propertylink, and based on the level of return Propertylink

has generated for the investors in the External Funds. Typically paid on the return of

capital to External Funds Investors post an asset sale (or sales).

20.0% - 40.0% of fund

outperformance above hurdles

of 10.0% - 15.0%

Property management feesA fee payable for the day to day management of the properties in the External Fund. Paid

monthly in arrears.

2.0% - 2.5% of gross income

p.a.

Leasing fees

Payable when Propertylink signs a new tenant to the property or renews a lease, and

may be based on the length of the tenancy. Paid on the successful execution of a new

lease.

Market standard rates

Project management feesPayable where Propertylink oversees projects undertaken on properties (including

developments and improvements). Paid as invoices are paid in relation to a project.Market standard rates

0.00%

0.20%

0.40%

0.60%

0.80%

1.00%

1.20%

FY17pf FY18f FY19f FY20f FY21f

Gross IM fees % External FUM Net IM fees % External FUM

15 September 2016

Propertylink Group

(PLG.AX / PLG AU) 19

Interest expense

PLG has initially drawn $256.6m (35% balance sheet gearing) from its $300m syndicated

bank debt facility, which comprises two tranches of $150m over both three and five year

durations and in aggregate giving the group a weighted average debt maturity of four

years. Notably, the margin on the 3yr facility of 135bp compares to 160bp for the 5yr

facility, however these rates increase to 150bp and 160bp, respectively in the event that

PLG's balance sheet LVR exceeds 40%.

We note that PLG's policy is to hedge its interest rate exposure to between 50% and

100% of drawn borrowing. We understand that post-IPO, PLG has hedged 50% of its

drawn debt at more favorable rates than those assumed in PDS forecasts.

PLG guided to a WACD of 3.52% for FY17, which we have assumed will be relatively

static in the MT (with upside potential) based on our economists view that the interest rate

easing cycle may still have some way to go. We allow for interest costs to tick up to 4.25%

by FY20, which is broadly consistent with what we have assumed for other A-REITs with

standard hedging profiles.

Figure 32: PLG vs peer weighted average debt cost Figure 33: PLG vs peer look through gearing

Source: Company data Source: Company data

Figure 34: PLG vs peer weighted avg debt maturity Figure 35: PLG vs peer % debt hedged

Source: Company data Source: Company data

Distributions

PLG's distribution policy is to payout 80% to 100% of distributable earnings. PDS

forecasts for FY17 reflect a 95% payout ratio on this basis. Our explicit forecasts from

FY18-21 assume an average payout ratio of 94% of distributable income or 97.1% of

Adjusted Funds From Operations (A-FFO).

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

ABP GMF CHC GDI GOZ IDR CMA TIX AOF Propertylink

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

TIX GOZ Propertylink GDI CMA IDR ABP AOF GMF CHC

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

AOF GOZ Propertylink CHC CMA GMF ABP IDR GDI TIX

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

TIX CHC AOF GOZ IDR GMF CMA ABP GDI Propertylink

15 September 2016

Propertylink Group

(PLG.AX / PLG AU) 20

Strengths and opportunities Australia focused and internally managed platform

We note that PLG is the only Australia-focused, internally managed industrial & logistics

trust and integrated investment and asset management platform

Stable income and structured rental growth & Portfolio diversification

PLG provides investors exposure to institutional grade industrial, logistics and commercial

office real estate assets which are well diversified by geography, tenants and leasing

profile. We see the portfolio's 81% exposure (by revenue) to Sydney and Melbourne and

the portfolio's diversified tenant base (with no single tenant contributing more than 5% of

total lease income) as attractive. We also note that approximately 90% of leases (by

income) are subject to annual fixed or CPI-linked rent reviews. Furthermore, PLG has a

strong history of retaining existing tenants. We note the retention rate for all expiring

leases for the 12 months ending 30 June 2016 was 83.9%.

Figure 36: Portfolio geographic diversification Figure 37: Portfolio asset diversification

Note: As at 30 June 2016. Source: Company data Note: As at 30 June 2016. Source: Company data

Access to an experienced and stable management team with over 20 years average

experience and majority independent board. Highly experienced management team

and majority independent board

PLG's senior management team has over 20 years average experience and has worked

together since 2009. Furthermore, we note that PLG has a well-established governance

structure due to its 15 years as an unlisted public company. The board has over 30 years

average corporate and industry experience and in excess of five years average tenure in

relation to PLG.

Established and rapidly growing investment and asset management platform,

backed by leading global investors

Since 30 June 2013, the business has successfully grown AUM from $39m to over

$1.55bn as at 30 June 2016. Management forecasts AUM growth of $675m in FY17,

which is generally consistent with the quantum of AUM growth achieved over the past two

years. In August, PLG launched a 10th fund (Propertylink Enhanced Partnership) to house

the $142m Denison portfolio acquisition.

Sydney46%

Melbourne34%

Brisbane15%

Perth5%

Unit Estate21%

Business Park17%

Logistics31%

Industrial29%

Development2%

15 September 2016

Propertylink Group

(PLG.AX / PLG AU) 21

Figure 38: PLG historical and forecast growth in total AUM

A$m unless otherwise stated

Source: Company data

PLG intends to establish new external funds as additional capital is made available by its

new and existing investors. It is currently in the process of raising further capital for two of

the External funds:

■ PAIP II: The second PLG Australian Industrial Partnership vehicle has a target AUM of

$700m to $900m. As noted above, PAIP II has a mandate to pursue core-plus and

value-add industrial and logistics investment opportunities across Australia’s capital

cities. As at 30 June 2016, PAIP II had $127.0m of equity commitments and $166.8m

of assets.

■ POP III: A multi-asset fund targeting core-plus and value-add office assets. As at 30

June 2016, the fund had $44.5m of equity commitments and had successfully acquired

$91.1m of assets.

According to Colliers International, PLG was the second largest acquirer of Industrial

assets (by value) over 2014/15. The company was second to Frasers Centrepoint but

came in ahead of Charter Hall, Mapletree Logistics Trust and Mirvac Group.

We note that the balance sheet portfolio was originally the PLG Australian Industrial

Partnership (PAIP), which was the Group's flagship External fund. The cornerstone

investors of this fund were Goldman Sachs and Grosvenor. Notably, the Fund achieved

rapid growth through acquisitions from early 2014 to mid-2015.

On our estimates, almost 70% of the portfolio (PAIP) was acquired by way of portfolio

acquisitions as illustrated below. Breaking these transactions down by their book value (as

at 30 June 2016), we can see that the majority of the portfolio was acquired from Equity

Commonwealth (19%), Abacus (18%), Valad (18%), AMP (13%) and Dexus (11%). We

note that many of these transactions included additional assets that form part of PLG's

External funds.

39

295

1,068

1,558

2,233

$0

$500

$1,000

$1,500

$2,000

$2,500

FY13 FY14 FY15 FY16F FY17F

43%

656%

262%

46%

15 September 2016

Propertylink Group

(PLG.AX / PLG AU) 22

Figure 39: Book value of balance sheet portfolio acquisitions

As at 30 June 2016

Source: Company data

PLG's existing investors within its External funds include significant global institutional

investors from North America, Europe, Middle East, Asia and Australia. These include

Goldman Sachs, Grosvenor Group, The Norinchukin Bank, Townsend Group, Fosun,

Sedco and Al Salam Bank. We note these investors have considerable AUM and some

are actively looking to increase their exposure to Australian commercial real estate. Given

five of these major investors have only invested in Australia with PLG to date, we believe

PLG is well positioned to grow AUM from both existing and new funds with its existing

investor base.

Operational leverage in funds management

PLG typically earns 70-75bp in recurring fees (investment management and property

management) on external AUM and one-off acquisition fees, which are typically 50bp of

the fair value of the assets acquired. In our view, the funds management business has

considerable operating leverage with operating margins expected to grow as AUM grows.

PLG has now reached a scale where significant increases in AUM will only require a

relatively small increase in direct headcount.

Opportunity to earn performance fees

We note that since the establishment of POP I, POP II, PALT and PAIP, PLG has

delivered a weighted average equity (levered) IRR of 28.5% across these External funds.

To date, PLG has earned a performance fee of $26.2m from the divestment of the PAIP

fund. While this fee is not attributable to new investors, any future performance fees will

however be available for distribution to PLG Security holders. Whilst performance fees are

not included in the pro forma forecasts we note that a performance fee of $9.5m would be

payable to PLG if the properties in the External funds were sold at their current valuation

on 30 June 2016. However, we note that the final amount of performance fees is ultimately

dependent on the sale proceeds realised for the properties when actually sold.

Further value potential through active asset management

PLG has a fully integrated investment and asset management business platform which

provides it with the ability to actively manage assets to deliver superior risk-adjusted

returns. As such, PLG sees its relatively low weighted average lease expiry (WALE) as an

AMP13%

Valad8%

Abacus18%

Equity Commonwealth

19%

Dexus11%

Other31%

15 September 2016

Propertylink Group

(PLG.AX / PLG AU) 23

opportunity to re-set leases on better terms for certain properties and extend the WALE,

which should result in valuation uplift (all else equal).

15 Talavera Rd, Macquarie Park is one case study. This property was acquired from

AMP in June 2015 for ~$34m. Since acquiring the asset, PLG has re-leased 75% of the

leases, increasing the WALE from 2.4 years to 4.4 years and is currently refurbishing the

building. The property has since been re-valued at $62m as at 30 June 2016. Similarly, we

also note that the ten assets acquired from Abacus and its managed (ADIF II) fund in June

2014 for $106.7m have since been re-valued at $124.8m reflecting leasing success such

as the new ten-year lease at 144-168 National Boulevard, Campbellfield with the existing

tenant and new leases (albeit short-term) over 100% of the property at 4 Brunker Rd,

Chullora.

122 Newton Rd, Wetherill Park is another value-add opportunity. The property was

acquired from Metcash in May 2015 and is entirely vacant. PLG will speculatively develop

a new 8,914 sqm warehouse at the rear of the property and refurbish the existing

warehouse (9,614 sqm). PLG has allowed for $9.6m in capital expenditure in FY17 with

work scheduled to commence in August 2016 and practical completion expected in

February 2017. PLG will target rents of $115-120/sqm for the new warehouse and

$105/sqm for the existing property. Given the tight prevailing occupier conditions in this

established industrial market, we expected lease enquiry levels should ramp up as

building works near completion.

144-156 McCredie Rd, Smithfield is another property where leasing success could

deliver solid valuation upside given the current book value of $19.7m equates to a

relatively modest $997/sqm of GLA. We note the property was acquired as part of a

portfolio transaction with Valad in October 2014. This existing tenant (Trust Company) will

formally vacate the c.20,000 sqm property in January 2017. The property is a classic

secondary industrial warehouse located in a well-established industrial market that attracts

national and international manufacturing and logistics space users. The property is

suitable for a variety of users given its 7 to 10m clearance and a flexible configuration that

provides future subdivision opportunities. PLG will undertake a comprehensive

refurbishment program at expiry in order to minimise downtime and enhance the

marketability of the asset to prospective tenants.

In the table below, we also highlight a number of other balance sheet properties where

PLG will look to add value through active asset management.

15 September 2016

Propertylink Group

(PLG.AX / PLG AU) 24

Figure 40: Key opportunities to add value through active management

Source: Company data

We also note two assets within the single-asset External funds POP I and POP II, which

have considerable potential upside through repositioning and may ultimately result in

performance fees for the Group:

■ 73 Miller St, North Sydney (POP I). PLG acquired the property in January 2015 for

$116.5m from an Investa managed wholesale fund. The acquisition was acquired

through POP I which is backed by cornerstone investor Fosun. The book value of the

property is $130m as at 30 June 2016 and PLG has a $5.8m co-investment in the fund.

Notably, PLG is awaiting the outcome of the current planning review under way in

North Sydney. However, based on its preliminary due diligence, it may be feasible to

demolish the existing 13-storey building in order to build a taller more efficient (c.20-

storey) commercial building. The property is fully leased and the major tenant is

Government Property NSW which has a June 2019 expiry. As such, any potential re-

development would not take place until late 2019.

■ 320 Pitt St, Sydney (POP II). PLG acquired the property in June 2015 for $200m

(8.26% cap rate) from Equity Commonwealth Trust as part of a broader transaction

($303.3m) which included eight industrial assets. This specific asset was acquired

through POP II, which is backed by cornerstone investors Goldman Sachs and

Grosvenor Group. The longer term strategy is to reposition this secondary property

through refurbishment. We note that PLG investigated the feasibility of residential

conversion but found this would be challenging given the building has no basement car

parking.

Balance Sheet Properties State BV $/sqmOccu-

pancy

Cap

Rate

GLA

(sqm)

WALE

(yrs)CS Comment

7 Gundah & 22 Beaumont Rd, Mt Kuring-Gai NSW 56.2 1,604 98.0% 7.25% 35,037 1.8Acquired from local private developer. Well presented and modern multi-unit estate. Looking to renew Sheldon &

Hammond (14.1% NPI) on a longer term lease. Market rents around $125/sqm. Incentives relatively low at ~10%

10-12 Pike St, Rydelmere NSW 21.9 1,094 100.0% 8.50% 20,022 2.0

Older syle secondary grade industrial facility located in a precinct that has been identif ied for higher & better use.

100% leased to WACO Kw ikform until June 2018. Strategy is to renew as much as as possible and generate cash

f low , w hilst continuing to explore future development potential w ith neighbouring landlords (i.e. GMG, DXS, AMP)

150-156 McCredie Rd, Smithfield NSW 19.7 997 100.0% 8.50% 19,765 0.6Secondary grade property - looking for new tenant w ith the near term expected departure of the incumbent tenant

(Trust Company).

122 New ton Rd, Wetherill Park NSW 16.3 1,695 0.0% 7.00% 9,614 0.0Previously occupied by Mitre 10. Propertylink is planning to refurbish the existing building and speculatively develop

the rear building and w ill target rents of $115-120/sqm for the new build

4 Brunker Rd, Chullora NSW 11.0 1,711 100.0% 7.25% 6,428 2.7 Was 25% vacant w hen acquired. Now 100% leased

1 Orielton Rd, Smeaton Grange NSW 8.2 1,066 30.6% 7.50% 7,689 1.2 This is a secondary grade Unit Estate and is just under 70% vacant.

8 Sylvania Way, Lisarow NSW 7.4 745 100.0% 10.00% 9,933 0.9 Non-core asset. Likely to be sold to ow ner occupier at some point dow n the track

71-93 Whitside & 74-78 Main Rd, Clayton VIC 24.0 851 100.0% 8.50% 28,195 0.53 buildings on 6.6ha of land w ith future subdivision potential. Entirely leased to Corning Cable w ho supply cable to

NBNco. Likely to contract to 11ksqm on a S-T extentsion. PLG noted that another tenant may lease the entire facility

18-24 Ricketts Rd, Mount Waverley VIC 16.9 1,895 100.0% 7.75% 8,916 2.4B-grade Business Park. Multi-tenanted property. Office Rents $185-225/sqm & Industrial $75/sqm. Strategy to

extend WALE through renew als

1-5 Lake Dr, Dingley VIC 16.4 941 100.0% 7.50% 17,430 2.0Built late 80's. Leased to Unicharm w ho manufacture nappies. Tenant may look to contract from 18ksqm to 10ksqm.

Tenant may relocate to new smaller facility. Propertylink could strata the property. Property is currently over-rented

82 Taryn Dr, Epping VIC 12.3 1,161 100.0% 7.00% 10,590 1.8Leased to Stanley Black & Decker w ho have a brief in the market and are looking to re-locate to the South East

region - expect to vacate

25 Strezlecki Ave, Sunshine West VIC 10.7 1,022 100.0% 7.50% 10,467 3.5Strategy is to entend the current lease w ith Bitzer and also in discussions w ith the tenant about the potential to

develop another facility on the residual land of the site

36-52 National Blvd, Campbellf ield* VIC 9.3 795 0.0% 7.50% 11,705 0.0 100% vacant and currently in DD w ith local investor. Currently expected to settle in September 2016

571 Mount Derrimut Rd, Derrimut VIC 7.7 921 0.0% 7.25% 8,357 0.0 Completely vacant since Nov-15. Previously occupied by GAM steel. Highly competitive market

7 Modal Crescent, Canning Vale WA 16.4 1,075 100.0% 8.00% 15,251 0.3 Strategy is to renew the Cahill Transport lease, w hich is set to expire in October 2016 (7,090sqm)

17-19 Leadership Way, Wangara WA 7.0 1,293 100.0% 8.25% 5,415 0.6 Pentair Flow Control has exercised its right to extend the least by 3 years over the entire facility

39-41 McDow ell St, Welshpool WA 8.0 1,155 100.0% 8.00% 6,925 0.7100% leased to Iron Mountain (lease expiry on Feb-17). Tenant (Recall) delayed renew al negotiations after being

acquired by Iron Mountain. Management expect to renew this lease

15 September 2016

Propertylink Group

(PLG.AX / PLG AU) 25

However, given the current strength of the Sydney B-Grade office market, which is

expected to improve further as c.60,000 sqm of commercial space is withdrawn to

accommodate new metro stations (displacing incumbent tenants), we expect the longer

term strategy will be a major refurbishment. PLG is likely to undertake a rolling

refurbishment of the building including lobby upgrades, new lifts and end of trip

facilities. This will enable the property to attract higher rents than the current passing

rent of c.$600/sqm (market closer to $700/sqm). The timing will largely depend on

Telstra who is the major tenant with a lease expiry in 2020.

15 September 2016

Propertylink Group

(PLG.AX / PLG AU) 26

Key risks Retention of key personnel

PLG's senior management team is a critical part of the company's business and growth

strategy. If PLG was to lose any of its senior management members or was unable to

employ adequate replacement personnel, its operations could be adversely affected. In

particular, we see the greatest "key man" risk in the External funds business, which, like

any Funds Management business, is underpinned by relationships with the existing

management team. In the event of a material change in personnel, it is not unreasonable

to assume that the potential growth of the External funds business and the existing Assets

Under Management (AUM) could be negatively impacted.

Ability to secure additional capital and fund assets at attractive pricing

In our view, PLG's ability to grow Fund and Asset Management earnings is dependent on

sourcing additional capital from investors and acquiring further assets for third party funds

at attractive prices. Importantly, further growth in FUM is implicit in our adopted valuation

range for PLG.

FUM growth key to generating above sector average FFO ps growth

We note that PLG's ability to generate earnings growth in excess of inflation (adjusted

leverage) is largely dependent on its ability to grow Funds Under Management (FUM) in its

investment management business. The operating leverage in investment management

earnings is material with each dollar of incremental FUM generating an incremental margin

of in excess of 70%, on our estimates. Furthermore, 'one off' acquisition fees also

represent a material proportion of FFO – for example, proforma (FY17) acquisition fees of

$3.5m equates to 8.0% of proforma FFO or 28% of Fund and Asset Management

revenues. We are also cognisant that proforma estimates are based on growing external

FUM by $675m, representing 77% growth on the FY16 external FUM base. We note,

however, that this figure reduces to 57% after adjusting for the $176m Denison portfolio

acquisition that recently settled.

Figure 41: PLG growth drivers: FY17-21 CAGR

Source: Credit Suisse estimates

Cyclicality of real estate values

PLG's Fund Management fees are tied to the market value of its Funds Under

Management. Hence, material shifts in industrial market valuations (upward or downward)

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

Net PropertyIncome

Net interestexpense

Groupoperatingexpenses

AdjustedFunds FromOperations

Distribution Funds FromOperations

Investmentmanagement

fees

Co-investmentincome

15 September 2016

Propertylink Group

(PLG.AX / PLG AU) 27

will impact (positively or negatively) upon PLG's Fund Management fees and overall level

of profitability.

Re-leasing and vacancy risk given PLG's relatively short WALE

PLG's assets are generally secondary grade in nature and could be subject to higher

downtime and capital expenditure (incentives and maintenance capex) when leases

expire, which in turn could have a negative impact on rental income.

We note that PLG's portfolio has relatively high lease expiry risk relative to peers with

~44% of leases expiring by CY18. Similarly, PLG's portfolio WALE of 3.6 years is the

second lowest in the sector after ABP and is below the A-REIT average of 5.6 years. We

note however, that PLG's tenant retention rate for all expiring leases for the 12 months

ending 30 June 2016 was 83.9% and the retention rate for the Portfolio on a standalone

basis was 63.2%, which fares well relative to peers.

Figure 42: PLG Portfolio Lease Expiry Profile Figure 43: A-REIT Industrial Portfolio WALE

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

We believe that in certain instances, some smaller secondary grade industrial assets will

be more difficult to lease-up, particularly those exposed to more challenging markets. For

example, we see potential downside risks to existing vacancies and near-term expiries for

properties located in West Melbourne, Campbellfield and Perth.

Specifically, the existing vacancy at 571 Mount Derrimut Rd, Derrimut (8,357 sqm) is

located in the highly competitive Melbourne West market where there is over 350,000 sqm

of vacant stock according to Knight Frank. To date, the property has received only limited

enquiry. The property has been vacant since November 2015 and is forecast to be re-

leased by the end of the calendar year.

PLG's second largest Melbourne asset at 71-93 Whitside Rd, Clayton in the South East

of Melbourne is entirely leased to Corning Cable over 28,195 sqm which is also PLG's

largest single tenant exposure (c.5% income). Notably, PLG expects the tenant will

downsize by around 17,700 sqm and may only extend their lease for a relatively short

duration (c.2 years) at this juncture. More recently however, we understand that PLG is in

discussions with a prospective tenant which may look to occupy the entire facility on a

longer term lease. We note the property comprises three freestanding warehouses and

offers good heavy vehicle access, facilitated by multiple entry points along two street

frontages. We note that the potential risks are party mitigated by the stronger occupier

market conditions in the South East Melbourne market with existing vacant stock tracking

at historic average levels.

Similarly, we see potential risk at 82 Taryn Drive, Epping (VIC), located in the

oversupplied Melbourne North market, which has the highest overall vacancy (430,000

sqm) of all the Melbourne industrial markets, according to Knight Frank. The property has

a WALE of 1.8 years and the major tenant Stanley Black and Decker has notified PLG of

its intention to vacate in May 2018. Despite the challenging market backdrop, we note that

the property is relatively modern (built in 2008) and offers a high clearance distribution

12.6%16.3% 15.3%

9.0%

46.8%

0%

10%

20%

30%

40%

50%

60%

70%

CY16 CY17 CY18 CY19 CY20+ 0.1

1.1

2.1

3.1

4.1

5.1

6.1

7.1

8.1

9.1

GPT MGR GOZ IDR TIX DXS Propertylink ABP

15 September 2016

Propertylink Group

(PLG.AX / PLG AU) 28

warehouse with direct access to the Hume Freeway. The site is suitable for a range of

users and is located in the established suburb of Epping and is in close proximity to the

new Melbourne Markets.

Figure 44: PLG - major vacancies Figure 45: PLG - upcoming lease expiries

Source: Company data Source: Company data

Development risk

There are typically higher risks associated with development activities than holding

developed assets. The risks faced by PLG in relation to existing or future development

projects include construction delays (which may result in a loss of rent), and development

costs may be materially greater than expected.

Following completion of development works, PLG may also be exposed to residual

defects, which although are mitigated by certain contractual protections and obligations or