proposed amendments made to the budget related …...proposed amendments made to the budget related...

TRANSCRIPT

Proposed amendments made to the budget related policies

Section 17(3)(e) of the MFMA which requires that - when an annual budget is tabled in terms of section 16(2), it must be accompanied by any proposed amendments to the budget-related policies of the municipality; Regulation 15 of schedule A of the Municipal Budget and Reporting regulation requires that the overview of budget-related policies should at least include - - A list of the budget related policies of the municipality including a reference of where the public can locate them; and - The proposed amendments to the budget-related policies taken into account in preparing the annual budget explaining the service delivery

and financial implications for the budget year and at least the two following years.

The public can locate the budget related policies with the proposed amendments on the website of the municipality at the following link: http://www.saldanhabay.co.za/pages/bylaws/by_laws.html

The following policies and proposed amendments are included in this agenda for inputs:

No Policy Reference

1. Supply Chain Management policy The changes to the policy has been summarised in this document (see below). To view the entire policy document, it is available on the website (see link above).

2. Infrastructure procurement and delivery management policy

No changes. The policy is therefore not included in this agenda but is available on the website (see link above).

3. Credit control and debt collection policy The changes to the policy has been summarised in this document (see below). To view the entire policy document, it is available on the website (see link above).

4. Indigent policy The policy and changes to the policy are included in this agenda. The changes are appropriately referenced within the policy document.

5. Property rates policy No changes. The policy is therefore not included in this agenda but is available on the website (see link above).

6. Budget and funds and reserves policy The changes to the policy has been summarised in this document (see below). To view the entire policy document, it is available on the website (see link above).

No Policy Reference

7. Virement policy The changes to the policy has been summarised in this document (see below). To view the entire policy document, it is available on the website (see link above).

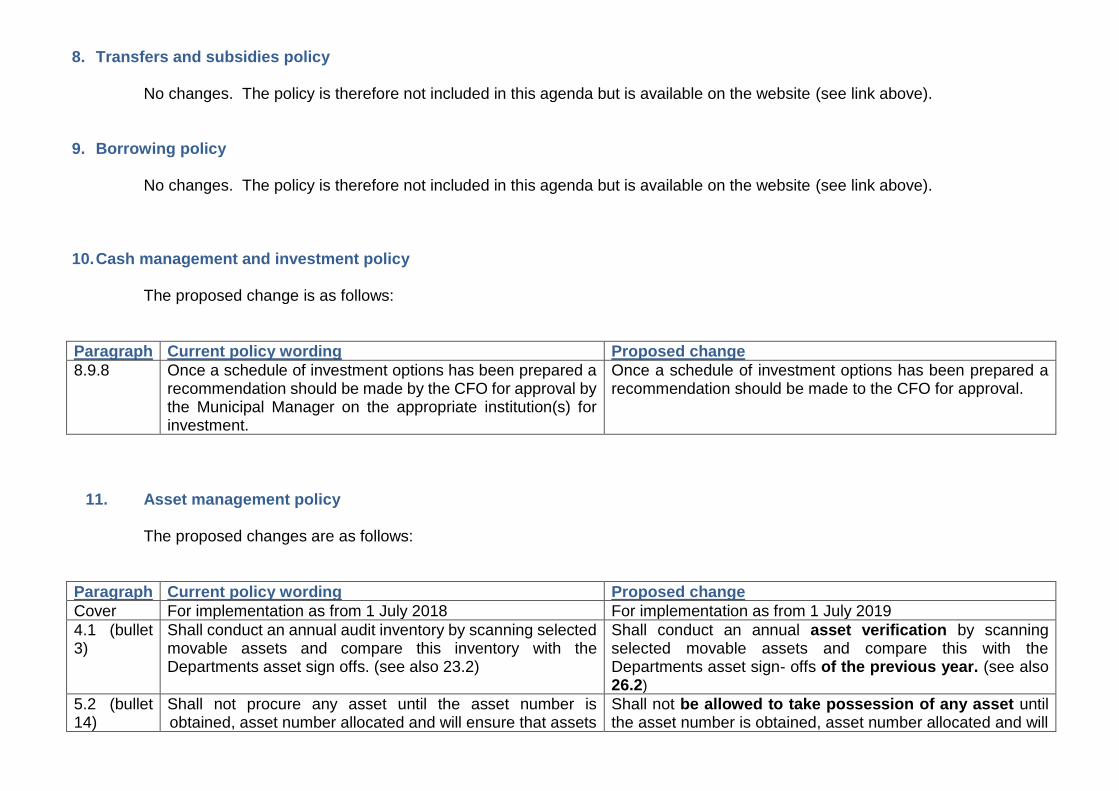

8. Transfers and subsidies policy No changes. The policy is therefore not included in this agenda but is available on the website (see link above).

9. Borrowing policy No changes. The policy is therefore not included in this agenda but is available on the website (see link above).

10. Cash management and investment policy The changes to the policy has been summarised in this document (see below). To view the entire policy document, it is available on the website (see link above).

11. Asset management policy The changes to the policy has been summarised in this document (see below). To view the entire policy document, it is available on the website (see link above).

12. Tariff policy The policy and changes to the policy are included in this agenda. The changes are appropriately referenced within the policy document.

13. Insurance management policy The changes to the policy has been summarised in this document (see below). To view the entire policy document, it is available on the website (see link above).

14. Special rating area policy No changes. The policy is therefore not included in this agenda but is available on the website (see link above).

15. Policy on the disposal of unserviceable, obsolete or redundant assets

The policy was reviewed and re-drafted. The entire document is included in the agenda

16. Incentives policy This is a new policy and is included in this agenda.

1. Supply Chain Management policy The changes to the policy has been summarised in this document (see below). To view the entire policy document, it is available on the website (see link above).

Paragraph Current policy wording Proposed change

Preface Preface The National Treasury in 2004 issued the Supply Chain Management Regulation which gave rise to the supply chain management model policy for adoption by municipalities and municipal entities in terms of section 111 of the Municipal Finance Management Act, No 56 of 2003. The model policy prescribes the minimum requirements and principles which municipalities and municipal entities must adhere to for their supply chain management systems. The above mentioned policy was issued principally for the acquisition of goods and services. In October 2015 via NT circular 77, the National Treasury issued a Supply Chain Management Model Policy for Infrastructure Procurement and Delivery Management, in terms of Section 168 of the Municipal Finance Management Act of 2003 (Act 56 of 2003) in reference to SCM Regulation 3(2), this model policy prescribes the standards and gateways system requirements and principles which municipalities and municipal entities must adhere to when procuring infrastructure related services linking to CIDB and ISO standards and ethos, therefore the model policy for infrastructure Delivery and procurement serves as a conduit for the alignment between CIDB Act and supply chain management systems. To this end the Saldanha Bay Municipality adopts a supply chain management policy framework consisting of annexure A and B. Annexure A is the SCM Model Policy for goods and services, which will be used for procurement of goods and services, non- infrastructure related. Annexure B is the Supply Chain Management Model Policy for infrastructure, which will be used for all infrastructure related procurement and services.

The Saldanha Bay Municipality' Supply Chain Management Policy consist out of the following: Annexure A is the SCM Model Policy for goods, services, construction works related procurement depending on the implementation of the Infrastructure Procurement and Delivery Management Policy. Annexure B is the Supply Chain Management Model Policy for infrastructure, which will be used for all infrastructure related procurement and services.

ANNEXURE A: SUPPLY CHAIN MANAGEMENT POLICY FOR GOODS AND SERVICES

SUPPLY CHAIN MANAGEMENT POLICY FOR GOODS, SERVICES AND CONSTRUCTION WORKS

1. Definitions New “Green Procurement” means that environmental criteria are taken into account for goods and services to be purchased in order to ensure that the related environmental impact is minimised.

New “Single source” refers to when competition exist in the market, but from a selected few suppliers due to technical capabilities and abilities to comply with the requirements of the municipality.

New “Sole Supplier” refers to instances where there is no competition and only one service provider exist in the market, with sole distribution rights and/or patent rights or manufacturer.

10. System of demand management 2)

New

2) The demand management system must – f) incorporate green procurement as far as reasonably

possible for all specification of goods, services and construction works; and

g) take requirements set for appointment of consultant in consideration.

11. System of acquisition management 1)

e) that any Treasury guidelines on acquisition management are properly taken into account.

Removed

14. Lists of accredited prospective providers / Central Supplier Database

New 4) A supplier must complete a MBD 4 in terms of the paragraph 12.

5) If a supplier’s tax status is non-compliant, the supplier

will be given the opportunity to rectify his status. The SARS database will also be used to verify the tax status if it is disputed by the supplier and proof will be attached if there is a discrepancy between the CSD and the SARS database.

4) 6)

18. Procedures for procuring goods or services through informal written quotations and formal written price quotations

7) 8)

9) 10)

New 7) include local content and production requirements, if applicable;

8) the request for an exemption letter for a specific quote or

bid by the supplier must be submitted with the exemption letter received from Department Trade and Industry (DTI), if applicable;

21.Bid documentation for competitive bids 1)

b) specifications, criteria for evaluation and adjudication procedure to be followed where applicable, and include where in exceptional circumstances, site meetings/inspections are compulsory;

b) specifications, criteria for evaluation, local content and production requirements and adjudication procedure to be followed where applicable, and include where in exceptional circumstances, site meetings/inspections are compulsory;

c) general conditions in terms of Regulation 13;

Removed

l) a provision for the termination of the contract in the case of non- or under-performance and objections and complaints must be included in the bid documentation. Refer to section 46 of SCM policy.

l) a provision for the termination of the contract in the case of non- or under-performance and objections and complaints must be included in the bid documentation.

iv) Bid documents must stipulate that the responsibility for registration and verification on the Central Supplier Database rests solely with the bidder.

Removed

New iv) Only an alternative bid submitted with the highest rank bid shall be considered during the evaluation of bids.

v) If the alternative bid of the highest rank acceptable bid is considered to have merit, then the alternative bid shall be ranked along with all of the acceptable bids received.

vi) An alternative of the highest ranked acceptable bid that is priced higher than the first ranked bid may be recommended for award, provided that the ranking of the alternative bid is higher than the ranking of the next ranked acceptable bid.

22. Public invitation for competitive bids 1) b)

v) - ix)

vi) - x)

New v) refer to local content and production provision (i.e. Stipulations in terms of local content and production is applicable on this tender. Details are included in the bidding document.)

22. Public invitation for competitive bids 2)a)

New ii) All amendments must be approved by the Bid Specification Committee and Director who has initially approved the bid specifications after considering the reasons for the amendment.

23.Procedure for handling, opening and recording of bids 1)

ix) the responsible official who opened the bid shall forthwith place his/her signature on the bid opening record and shall ensure that the bid opening record, the bid prices and BEE status, where applicable, are made available for public inspection and are published on the Municipality’s official website.

ix) the responsible official who opened the bid shall forthwith place his/her signature on the bid opening record and shall ensure that the bid opening record, the bid prices, the applicable local content percentage, if possible, and BEE status, where applicable, are made available for public inspection and are published on the Municipality’s official website.

35. Appointment of consultants

2) 3) 4) 5)

3) 6) 7) 8)

New 2) Consultants are engaged primarily for the following reasons: a) To provide specialized services for limited periods

without any obligation of permanent employment; b) To benefit from superior knowledge, transfer of skills

and upgrading of a knowledge base while executing an assignment;

c) To provide independent advice on the most suitable approaches, methodologies and solutions of projects.

New 4) Approval to utilize external capacity must be obtained by the director from the municipal manager which include the following: a) A gap analysis by the directorate must be conducted

to ensure that the request for specific capacity is indeed required by the directorate;.

b) The assessment should also take into account whether or not internal capacity and/or other resources required are available to perform the specific project;.

c) The directorate should provide a concise overview of the type of services which are required and why a proposal/motivation (non-financial benefits) for appointment of consultants should be supported;.

d) A cost benefit analysis must be done (taking similar future needs into account);.

e) Indicate if transfer of skills is going to be part of the appointment. Reasons must be provided if skills transfer is not going to be part of the appointment;.

f) The directorate must indicate in their request to appoint a consultant which process is going to be followed;. and

g) All appointments of consultants in the municipality shall be in writing and approved by the Accounting Officer.

New 5) The approved memorandum must be submitted with the specifications to appoint a consultant to the SCM unit for tabling at the Bid Specification Committee meeting.

New 9) Consultants, including construction and infrastructure related services, must only be remunerated at the rates equal to or below those: a) determined in the “Guidelines on fees for audits done

on behalf of the Auditor-General South Africa”, issued by the South African Institute of Chartered Accountants (SAICA);

b) set out in the “Guide on Hourly Fee Rates for Consultants”, by the Department of Public Service and Administration (DPSA);

c) prescribed by the body regulating the profession of the consultant i.e ECSA guidelines; or

d) at a rate determined fair or equitable by the Accounting Officer and agreed upon by both parties.

36. Deviation from, and ratification of minor breaches of, procurement processes 1)

ii) if such goods or services are produced or available from a single provider only;

ii) if such goods or services are produced or available from a sole provider or a single source (as per definition);

50.Contract administration and management

New 1) Line departments are fully responsible for contract administration and management.

1) – 9) 2) – 10) 3)

2. Infrastructure procurement and delivery management policy

No changes. The policy is therefore not included in this agenda but is available on the website (see link above).

3. Credit control and debt collection policy

Paragraph Current policy wording Proposed change

Cover page CUSTOMER CARE AND MANAGEMENT, CREDIT CONTROL AND DEBT COLLECTION POLICY

CREDIT CONTROL AND DEBT COLLECTION POLICY

4. Principles a) The administrative integrity of the municipality must be maintained at all costs. The democratically elected officials are responsible for policy-making, while it is the responsibility of the municipal manager to execute these policies.

a) The administrative integrity of the municipality must be maintained at all costs. The democratically elected councillors are responsible for policy-making, while it is the responsibility of the municipal manager to execute these policies.

6.1 Communication and Feedback

6.1.2 Council’s Customer Care and Management, and Debt Collection Policy, will be available in English, and will be made available by general publication on specific request, and will also be available at Council’s cash collection points and website.

b) This policy will be available in English, and will be made available by general publication on specific request, and will also be available at Council’s cash collection points and website.

6.1.5 The press will be encouraged to give prominence to Council’s Customer Care and Credit Control Debt Collection issues, and will be invited to Council meetings where these are discussed.

e) The media will be encouraged to give prominence to Council’s Credit Control and Debt Collection issues and will be invited to Council meetings where these are discussed.

Paragraph Current policy wording Proposed change

6.2 Service application and agreements

6.2.5 Within a specified period (in the agreement) of change of ownership, meters will be read and an account posted.

e) Within a specified period (in the agreement) of change of ownership, meters will be read and an account posted, or send by email.

6.11 Incentives for prompt payment

New c) Incentive measures may be implemented as per Council resolution.

New d) Where a customer is prepared to pay off the capital amount on an outstanding account, older than 3 years, in one payment, then the municipality will write off 33% of interest charged. For any other payment incentive arrangement, the CFO must approve it.

7.4 Collection Process

New e) Annual accounts

i) Should annual accounts remain unsettled after 30 September of the applicable year, notice will be given to the owner/customer that the amount owed must be settled within fourteen (14) days, failure of which legal proceedings will be instituted.

7.4.5 The legal process will be conducted in term of the approved internal Standard Operating Procedure

f) Legal Process i) The municipality will, when a debtor is 30 days in

arrears, commence a collection process against that debtor, which process could involve final demands, summonses, court trails, judgments, garnishee orders and/or sales in execution of property.

ii) A physical residential address or work address is required for summonsing. The Magistrate’s Court will issue the summons and a case number will be assigned. The sheriff of the court will serve the debtor with the summons. The debtor will be granted 10 (ten) days to defend his/her case if he/she is not in agreement with the claim stipulated in the summons, or to settle the total account, or to arrange for the necessary repayment terms.

Paragraph Current policy wording Proposed change

iii) When the summons and summons record are received back from the sheriff of the court, the municipality will process the sheriff’s fee and add it to the debtor’s account. The sheriff’s account must be paid on a monthly basis by the municipality, but the cost is recovered from the debtor.

iv) If the sheriff of the court was unable to serve the debtor with a summons, a notice of non-issuing will be sent, and the cost will be added to the debtor’s account. The account will then be moved to the tracing cycle. The tracking fee will also be added to the debtors account but will be first paid by the municipality.

v) If the debtor is traced, the new address is captured on the financial system and the summons is once again sent to the Court for approval (corrected by hand on original summons). The summons is now sent to the sheriff of the court to serve the debtor.

vi) If no defence is noted and no payment is received after summonsing, a sentence application will be submitted to the Magistrate court.

vii) All documents (original summons, notices of summons from the sheriff and sentencing documents) are sent to the Magistrate’s Court, where the sentence will be granted.

viii) After the sentencing process by the Magistrate’s Court, the Court sends the documents back to the municipality. The information is then captured on the financial system.

ix) If no further action is received from the debtor, a “Notice of Sentence” letter is mailed to the debtor. This letter informs the debtor that he is sentenced and that he/she should pay the outstanding amount within 10 days after the issuing date of the letter, or his/her moveable assets will be confiscated.

x) Sentencing of a debtor entails the following:

Paragraph Current policy wording Proposed change

• The name of the debtor will be published in the “official gazette” used by all credit managers and businesses providing credit;

• The sentence is valid for 5 years; • The moveable assets of the debtor can be sold to

the value of total amount in arrears; • The immoveable assets of the debtor can be sold to

the value of total amount in arrears. xi) At any stage while the debt is outstanding, all

reasonable steps shall be taken to ensure that the ultimate sanction of a sale-in execution is avoided or taken as a last resort. Saldanha Bay Municipality, however, has total commitment to a sale-in execution should the debtor fail to make use of the alternatives provided by the municipality from time to time. As part of the recovery process the Municipal Manager may determine a reserve price equal to the municipal property value. The remaining outstanding debt in excess of the net proceeds of the auction will be written off.

7.5 Rates Clearance

On the sale of any property in the municipal jurisdiction, Council will withhold the transfer until all rates and service charges related to the property are paid by withholding a rates clearance certificate in accordance with Section 118 of the Systems Act (including recent court cases) and with further consideration of Section 102 of the Local Government Municipal Systems Act, No 32 of 2000. This must also be read with paragraph 6.15.

a) On the sale of any property in the municipal jurisdiction, Council will withhold the transfer until all rates and service charges related to the property are paid by withholding a rates clearance certificate in accordance with Section 118 of the Systems Act (including recent court cases) and with further consideration of Section 102 of the Local Government Municipal Systems Act, No 32 of 2000. This must also be read with paragraph 6.15.

b) Council will accept a guarantee from the transfer attorney that all outstanding debt will be paid on date of registration of such property.

c) The municipality will issue such clearance certificate on receipt of an application on the prescribed form from the conveyancer.

Paragraph Current policy wording Proposed change

d) All payments will be allocated to the registered seller’s municipal accounts and all refunds will be made to such seller. No interest shall be paid in respect of these payments.

e) The municipality will hold the current owner liable for debt and collect all outstanding monies before the rates clearance certificate is issued. The debt may not be carried forward to the new owner.

7.6 Prescription of debt

New Debt prescribes when payment is not demanded, legal action is not taken or not any communication is taking place with a debtor. This is on condition that the municipality can provide reasonable evidence that during the prescription period (three years for services, i.e. water and electricity consumption and 30 years for property rates and availability of services) an attempt was made to contact the debtor. Prescription will not apply if: i) The debt is acknowledged; ii) Legal action was taken; iii) The debtor is residing outside South Africa; iv) The debt is within the prescription period as mentioned

above.

10. Department of Finance: Structures

Council shall regularly receive a report from the Chief Financial Officer, if necessary after consultation with suitable consultants, on the manpower and systems requirements of Finance which requirements take into account Council’s agreed targets of customer care and management, and debt collection, and, after considering this report, Council will within reason vote such resources as are necessary to ensure that Finance

Council shall regularly receive a report from the Chief Financial Officer, if necessary after consultation with suitable consultants, on the manpower and systems requirements of Finance which requirements take into account Council’s agreed targets of credit control and debt collection, and, after considering this report, Council will within reason vote such resources as are necessary to ensure that Finance has the staffing and structures to meet Council’s targets in this regard or to outsource the service.

Paragraph Current policy wording Proposed change

has the staffing and structures to meet Council’s targets in this regard or to outsource the service.

4. Indigent policy See policy document with the tracked changes elsewhere in this agenda.

5. Property rates policy

No changes. The policy is therefore not included in this agenda but is available on the website (see link above). 6. Budget and funds and reserves policy

The proposed changes are as follows:

Paragraph Current policy wording Proposed change

2.4 New definition “Capital Project” means capital project as per mSCOA project segment

2.5 New definition Capital Project section 19 of the MFMA and MBRR 13 (2) (c)” means a capital project with the total costs of R 50 million and above. The cost should include all capital costs until the project is operational.

2.21 New definition Senior manager refers to the officials directly reporting to the Municipal Manager.

2.23 New definition “Surplus” for the four major services, electricity, water, waste management, and waste water management is calculated by using the total revenue (gross revenue less development charges, less capital grants) minus total expenditure, plus gains or losses. The percentage surplus/ or deficit is calculated by dividing the surplus or deficit through the total expenditure.

Paragraph Current policy wording Proposed change

2.13 New definition 2.13. “Fixed operating expenditure” means total operating expenditure excluding (Depreciation, Amortisation, and Provision for Bad Debts, Impairment and Loss on Disposal of Assets)

3.8 3.8 The following funds, reserves, liabilities and provisions must be cash-backed at all times: A Cash and cash equivalents B Investments C Cash-backed reserves and provisions 1 Unspent conditional grants 2 Housing development fund 3 Unspent loans 4 Loan repayments due 5 Provision for environmental rehabilitation 6 Employee benefit obligation 7 Self-insurance funds 8 Consumer deposits 9 Capital replacement reserve that includes: Funding source for capital projects Development charges New municipal building reserve Property sales proceeds D Working capital (A+B-C=D)

3.8. The following funds, reserves, liabilities and provisions must be cash-backed always: 3.8.1. Unspent conditional grants; 3.8.2. Housing development fund; 3.8.3. Unspent loans; 3.8.4. Loan repayments due; 3.8.5. Provision for environmental rehabilitation; 3.8.6. Employee benefit obligation; 3.8.7. Consumer deposits; 3.8.8. Capital replacement reserve; and 3.8.9. Working capital (to be equal to budgeted fixed operating expenditure divided by 12.).

3.26.1 Electricity service – surplus of 10% of total electricity revenue. The tariffs will be calculated to be cost reflective and the rendering of the service may result in a surplus of not more than 10% of total revenue for the service;

Electricity service (excludes streetlighting)– surplus of maximum of 15% of total electricity operating expenditure. The tariffs will be calculated to be cost reflective and the rendering of the service may result in a surplus of not more than 15% of total operating expenditure for the service;

3.26.2 Water service – maximum surplus of 10% of total water revenue. The tariffs will be calculated to be cost reflective and the rendering of the service may result in a surplus of not more than 10% of total revenue for the service;

Water service – maximum surplus of 25% of total water operating expenditure. The tariffs will be calculated to be cost reflective and the rendering of the service should result in a surplus of not more than 25% of total operating expenditure for the service;

Paragraph Current policy wording Proposed change

3.26.3 Refuse removal service – at least a break even situation. The ideal is that the refuse removal service will break even as it is an economical service. The tariffs must be calculated in such a way that the rendering of the service will result in a breakeven point or generate a very small surplus.

3.29. Refuse removal service – at least a break-even position. The ideal is that the refuse removal service will break even as it is an economical service. The tariffs must be calculated in such a way that the rendering of the service will result in a breakeven point or generate a surplus of not more than 10%

3.26.4 Sewerage service – at least a break even situation. The ideal is that the sewerage service will break even as it is an economical service. The tariffs must be calculated in such a way that the rendering of the service will result that the service breaks even or generate a very small surplus.

3.30. Sewerage service – at least a break-even position. The ideal is that the sewerage service will break even as it is an economical service. The tariffs must be calculated in such a way that the rendering of the service will result that the service breaks even or generate a surplus of not more than 10%

3.27 The following tariffs increases will be adjusted on a yearly basis per financial year and will be determine based on the principles as expressed above: a) Property rates b) Sewerage charges c) Refuse removal fees d) Water sales e) All other sundry tariffs

3.32. The following tariffs increases will be adjusted on a yearly basis per financial year and will be determine based on the principles as expressed above: 3.32.1. Property rates; 3.32.2. Electricity charges 3.32.3. Sewerage charges; 3.32.4. Refuse removal fees; 3.32.5. Water sales; and 3.32.6. All other sundry tariffs.

New long term debt will only be incurred if the financial ratios, norms and credit rating of the municipality is positive and the indicators are of such nature that it will not put undue pressure on the tariffs and affordability levels of the community. Proper financial viability and sustainability studies must be performed to determine and prove that it is financially viable for the municipality to take up any long term debt for consideration by council. These studies and analysis must be submitted to council in a report format as record that all relevant factors have been considered. These will be

7.2. New long-term debt will only be incurred if the financial ratios, norms and credit rating of the municipality is positive and the indicators are of such nature that it will not put undue pressure on the tariffs and affordability levels of the community. External loans should not exceed 25% of own revenue (total revenue less total grants)

Paragraph Current policy wording Proposed change

submitted through the Long term financial plan. External loans should not exceed 25% of own revenue (total revenue less total grants)

New New paragraph 11.4.2.1 11.4.2.1 To ensure compliance with section 19 of the

MFMA as well as Regulation 13 of the MBRR,

council will consider and approve an individual

capital project with the estimated total cost at

the time of approval of the budget that exceeds

R 50 million, only if included in a separate

resolution and annexure fully completed and

signed off by the relevant director, and included

in the budget documents in the annual and

adjustments budget which annexure must

include the following:

11.4.2.2 The project description;

11.4.2.3 Total estimated capital cost of the project;

11.4.2.4 The total estimated cost of the project per

financial year until the project is operational;

11.4.2.5 The date Environmental impact studies had

started or will start;

11.4.2.6 The date Environmental impact studies will be

finalised;

11.4.2.7 The estimated starting and completion date of

the project;

11.4.2.8 The planned date when the project will be

operational;

11.4.2.9 The future estimated operational costs of the

project for a period of 3 years after the project

is operational that includes estimated additional

employment costs; estimated interest in the

case of funding or partial funding from an

external loan, depreciation charges, estimated

maintenance costs and any other operational

Paragraph Current policy wording Proposed change

expenditure, as well as possible savings

envisaged that will be realised with the

implementation of the project;

11.4.2.10 The sources of funding of the project. Funding

must be available (secured) and may not be

committed for any other purposes;

11.4.2.11 The implications of the operational costs on

municipal property rates and other tariffs, if

relevant. The operational expenditure for a full

financial year will be translated as a

percentage increase in property rates or

service charge whichever is relevant to the

specific project after taking into account the

direct revenue the project will generate or

whether it will be absorbed by tariffs;

11.4.2.12 The future estimated revenue the project will

generate covering a period of 3 financial years

after the project is operational;

11.4.2.13 Whether section 33 of the MFMA is applicable

and that it has been complied with or to be

complied with and the extent to which it will be

applicable – (The relevant Director

responsible for implementation of the project

must indicate this information on the

prescribed form.

11.4.2.14 The Municipal manager and Directors (Senior

managers) must advise the budget office and

Budget steering committee during the budget

process should the total cost of any project be

estimated to be more than R 50 million.

11.12. The AFS, Assets and Reporting department shall determine the depreciation expenses to be charged to each vote, calculate the interest and

11.12. The AFS, Assets and Reporting department shall determine the depreciation expenses to be charged to each vote, calculate the interest and redemption on borrowings on

Paragraph Current policy wording Proposed change

redemption on borrowings on existing and all new planned external loans and operating and finance leases, the apportionment of interest payable to the appropriate cost centres, the estimates of withdrawals from (claims) and contributions to (premiums) the self-insurance reserve, and the contributions to the provisions for bad debts, accrued leave entitlements and obsolescence and slow moving of Inventory for the annual and adjustments budgets and provide these to the budget office in accordance with the budget process plan and time table.

existing and all new planned external loans and operating and finance leases, the apportionment of interest payable to the appropriate cost centres, the estimates of withdrawals from (claims) and contributions to (premiums) the self-insurance reserve, and the contributions to the provisions for bad debts, accrued leave entitlements and obsolescence and slow moving of Inventory for the annual and adjustments budgets and provide these to the budget office in accordance with the budget process plan and time table.

11.13. The budget office shall further determine the recommended contribution to the capital replacement reserve and any special contributions to the self-insurance reserve to comply with this policy.

11.13. The budget office shall further determine the recommended contribution to the capital replacement reserve and any special contributions to the self-insurance reserve to comply with this policy.

7. Virement policy

The proposed changes are as follows:

Paragraph Current policy wording Proposed change

2.5. New “Capital Project section 19 of the MFMA and MBRR 13 (2) (c)” means a capital project with the total costs of R 50 million and above. The cost should include all capital costs until the project is operational.

4.15. New - paragraph When a saving is identified, the applying director must in writing demonstrate through calculations and projections that there is in fact a saving for the full financial year.

5.14. Due to the m SCOA implementation and possible challenges with classification and interpretation of certain classifications of expenses and revenue, virements to amend budgets to be

Moved to paragraph 4.13 Due to the mSCOA classification challenges, any virements within a vote to amend the budget to more accurately match the mSCOA classification framework is permitted. These

Paragraph Current policy wording Proposed change

more in line with m SCOA classification will be permitted, subject that any virements must be within a vote.

virements may be authorised by the Senior Manager: Financial Management and Chief Financial Officer in terms of the section 8 of this policy.

5.12 Entertainment budgets may not be increased through virements without approval of the CFO and Accounting Officer.

Entertainment and catering budgets may not be increased through virements without approval of the CFO and Accounting Officer.

5.14 New - paragraph 5.14 No virement may be made to increase any vehicle (transport related) related budget from a non-vehicle (transport) related budgeted project for purchasing of a vehicle without the approval of council, except in the case of insurance claims.

5.15 New - paragraph 5.15 Office furniture and office equipment, machinery & equipment related budgets may not be increased through a virement without the approval of the council, except for insurance claims.

5.16 New - paragraph 5.16 No virement is allowed to utilise the following as sources resulting in a cash outflow.

5.16.1 Bulk Purchases; 5.16.2 Departmental charges 5.16.3 Internal billing

6.3. New - paragraph In compliance with section 19 of the MFMA and MBRR 13, no capital project exceeding R 50 million may be included in the budget through a virement. A report must be submitted to council where the total cost of the project is provided. Such report must include the total project cost covering all financial years until the project is operational, and the future operational cost and revenue on the project, including municipal tax and tariff implications. The section 19 form prescribed by the Budget Office must be completed and signed by the Director.

8. Transfers and subsidies policy

No changes. The policy is therefore not included in this agenda but is available on the website (see link above).

9. Borrowing policy

No changes. The policy is therefore not included in this agenda but is available on the website (see link above).

10. Cash management and investment policy The proposed change is as follows:

Paragraph Current policy wording Proposed change

8.9.8 Once a schedule of investment options has been prepared a recommendation should be made by the CFO for approval by the Municipal Manager on the appropriate institution(s) for investment.

Once a schedule of investment options has been prepared a recommendation should be made to the CFO for approval.

11. Asset management policy

The proposed changes are as follows:

Paragraph Current policy wording Proposed change

Cover For implementation as from 1 July 2018 For implementation as from 1 July 2019

4.1 (bullet 3)

Shall conduct an annual audit inventory by scanning selected movable assets and compare this inventory with the Departments asset sign offs. (see also 23.2)

Shall conduct an annual asset verification by scanning selected movable assets and compare this with the Departments asset sign- offs of the previous year. (see also 26.2)

5.2 (bullet 14)

Shall not procure any asset until the asset number is obtained, asset number allocated and will ensure that assets

Shall not be allowed to take possession of any asset until the asset number is obtained, asset number allocated and will

Paragraph Current policy wording Proposed change

are bar-coded by the Asset Control Section and insured by the Finance Department.

ensure that assets are bar-coded by the Asset Control Section and insured by the Finance Department.

18.1 New paragraph In the case of the free disposal of computer equipment, the provincial department of education must first be approached to indicate within 30 days whether any of the local schools are interested in the equipment. The municipality’s ICT department will indicate to the Asset Section which ICT equipment are not needed to provide the minimum level of basic municipal services and is available to be donated to schools that qualify for the donation in terms of Section 14(2)(b)(iii) of the MFMA.

26.2 26.2 Physical inventory of all movable assets The Asset Control Section will conduct a physical inventory of movable assets annually. They will require the cooperation of departmental personnel in accomplishing the physical inventory task and will attempt to minimise the time demanded of them.

26.2 Physical verification of all movable assets The Asset Control Section will conduct a physical verification of movable assets annually. They will require the cooperation of departmental personnel in accomplishing the physical verification task and will attempt to minimise the time demanded of them.

12. Tariff policy The policy and changes to the policy are included in this agenda. The changes are appropriately referenced within the policy document. 13. Insurance management policy

The proposed changes are as follows:

Paragraph Current policy wording Proposed change

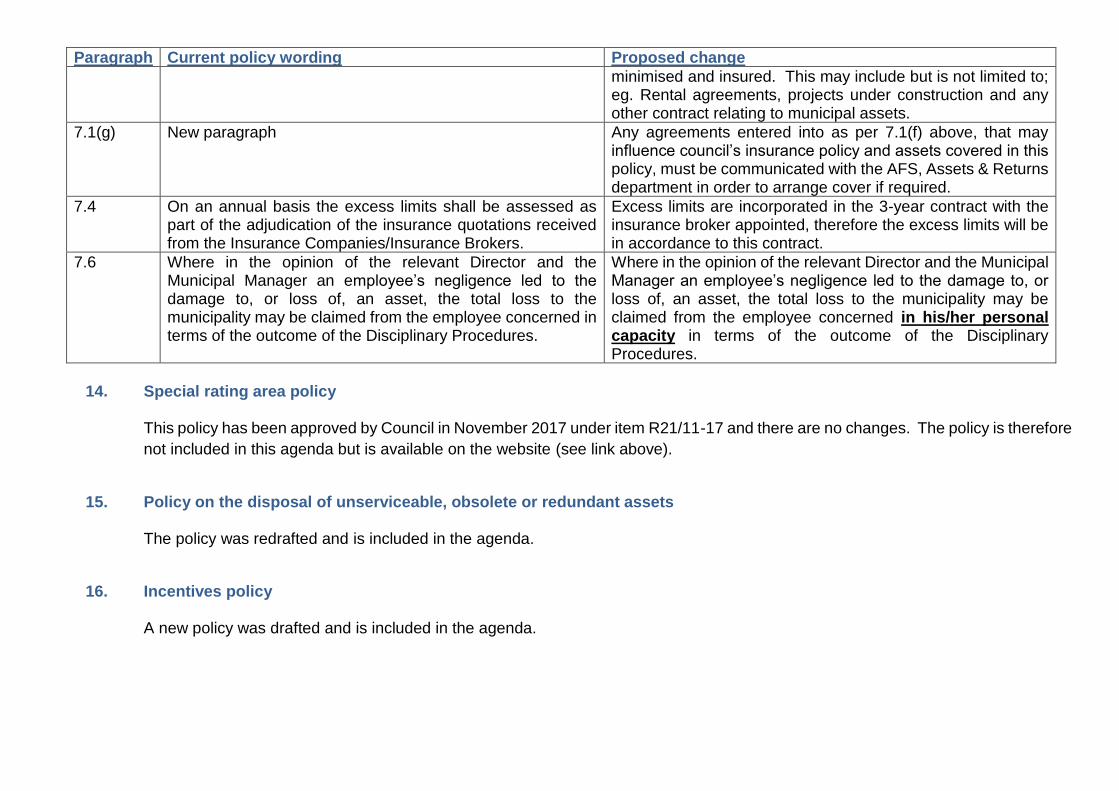

7.1(f) New paragraph All contracts between council and a 3rd party should be monitored to ensure loss or damage to municipal property are

Paragraph Current policy wording Proposed change

minimised and insured. This may include but is not limited to; eg. Rental agreements, projects under construction and any other contract relating to municipal assets.

7.1(g) New paragraph Any agreements entered into as per 7.1(f) above, that may influence council’s insurance policy and assets covered in this policy, must be communicated with the AFS, Assets & Returns department in order to arrange cover if required.

7.4 On an annual basis the excess limits shall be assessed as part of the adjudication of the insurance quotations received from the Insurance Companies/Insurance Brokers.

Excess limits are incorporated in the 3-year contract with the insurance broker appointed, therefore the excess limits will be in accordance to this contract.

7.6 Where in the opinion of the relevant Director and the Municipal Manager an employee’s negligence led to the damage to, or loss of, an asset, the total loss to the municipality may be claimed from the employee concerned in terms of the outcome of the Disciplinary Procedures.

Where in the opinion of the relevant Director and the Municipal Manager an employee’s negligence led to the damage to, or loss of, an asset, the total loss to the municipality may be claimed from the employee concerned in his/her personal capacity in terms of the outcome of the Disciplinary Procedures.

14. Special rating area policy

This policy has been approved by Council in November 2017 under item R21/11-17 and there are no changes. The policy is therefore

not included in this agenda but is available on the website (see link above).

15. Policy on the disposal of unserviceable, obsolete or redundant assets

The policy was redrafted and is included in the agenda.

16. Incentives policy

A new policy was drafted and is included in the agenda.