prospects for coal and clean coal technologies in thailand

TRANSCRIPT

Prospects for coal and clean coaltechnologies in Thailand

John Kessels

CCC/165

March 2010

Copyright © IEA Clean Coal Centre

ISBN 978-92-9029-485-6

Abstract

This report examines the prospects for coal and clean coal technologies in Thailand. The report also covers the current energysituation in Thailand and the structure of the electricity sector. The status of existing coal reserves is examined and asks why thefuture coal demand is likely to be met by importing coal. A discussion on the generation capacity in Thailand examines the currentand future prospects for coal-fired power generation. The role of the government in the coal sector is discussed and the powerdevelopment plan being implemented to meet increasing energy demand. Environmental issues related to coal are a major issue inThailand particularly because of earlier problems with SO2 emissions at the Mae Moh power station, although these were solved.In particular, the legacy of the Mae Moh power station SO2 problem and how that was solved with the use of flue gasdesulphurisation. There is also an examination of international organisations such as the ADB, APEC, WB, ASEAN, IEA andUSAID role in clean coal technologies and how this could be improved. The economy is heavily reliant on natural gas with 70%of the power generating sector using gas. The government recognises the need to diversify the energy sector especially with only12 years of proven domestic gas reserves remaining. There is around 2 Gt of coal reserves mostly lignite, high in sulphur andlocated in northern Thailand. It is estimated that currently 1 Gt of those reserves could be used economically. Coal production in2008 was between 18–19 Mt with an additional 17–18 Mt of imports. In the future it is likely that all new coal-fired power stationswill burn imported low sulphur coal with imports projected to rise to 48 Mt by 2021. A challenge facing Thailand is to developand deploy clean coal technologies. This has begun with the first supercritical coal-fired power station being built and due to beoperational by 2011. A key conclusion of this report is that the establishment of a central organisation in the public or privatesector is needed. This could act as a focal point to undertake and promote clean coal technology research, education anddeployment with domestic and international organisations as well as strengthen the sustainable use of coal in Thailand.

Acknowledgements

The author would like to thank experts from power generation companies, government departments, research institutes anduniversities who made time to meet and answer questions about the Thailand energy sector. In particular, the author would like tothank:

Akaraphong Dayananda BanpuChatphol Meesri BanpuNalin Kraikachornkitti BanpuGary Harris BLCP, RayongSuwat Kamolthanat Mitrphol PlcBundhit Energy Research Institute, Chulalongkorn UniversityPinyo Meechumna Energy Research Institute, Chulalongkorn UniversitySurapun Wongopasi Energy Research Institute, Chulalongkorn UniversityBundit Fungtammasan Joint Graduate School of Energy and the EnvironmentBoonrod Sajjakulnukit Department of Alternative Energy Development and EfficiencyPradeep J Tharakan USAID ECO-Asia Clean Development and Climate ProgramOrestes Anastasia USAIDSamerjai Suksumek Energy Policy and Planning OfficeThanwadee Deetae Electricity Generation Authority of ThailandThana Boonyasirikul Electricity Generation Authority of ThailandWichai Anantanasakul Electricity Generation Authority of ThailandVachraras Pasuksuwan World BankChutima Lowattanakarn World BankTassanai Kriatisountorn Norton RosePiroon Wacharamontri Norton RosePhil Napier-Moore Mott MacDonaldNapoleon M Lusica WorleyParsons Group Inc

2 IEA CLEAN COAL CENTRE

ABCSE Australian Business Council for Sustainable EnergyADB Asia Development BankAFOC Asean forum on coalAPEC Asia Pacific Economic CooperationASEAN Association of Southeast Asian nations (formed 1967)ASEM Asia Europe meetingbcm billion m3

BLCP Banpu Limited and China Light and Power CaO calcium oxideCCS carbon capture and storageCCT clean coal technologyCDF community development fundCDM clean development mechanismCEM continuous emissions monitoringCER certified emission reduction (for CDM)CFBC circulating fluidised bed combustion systemCO2 carbon dioxideDEDE Department of Alternative Energy Development and EfficiencyDEDP Department of Energy Development and PromotionDMC developing member countriesDNA designated national authorityECON energy conservation promotion fundEEDA Energy Efficiency Development Association EGAT Electricity Generation Authority of ThailandEGCO Electricity Generating Public CompanyENGO environmental non-governmental organisationsEPPO Energy Policy and Planning OfficeERC Energy Regulatory CommissionERI Energy Research InstituteESI Electricity Supply IndustryESP electrostatic precipitatorFACOS furnace analysing cleaning optimistation systemFBC fluidised bed combustionFGD flue gas desulphurisation (for SO2 removal)Gt gigatonneGEF global environment facilityGDP gross domestic productGW gigawattIAEA International Atomic Energy Agency IEA International Energy AgencyIPP independent power producerIPR intellectual property rightsJGSEE Joint Graduate School of Energy and EnvironmentKMUTT King Mongkut’s University of Technology ThonburiLE life extensionLNG liquefied natural gas MEA Metropolitan Electricity Authority MOE Ministry of EnergyMONRE Ministry of Natural Resources and Environment MSW Municipal solid wasteMtCO2 million tonnes of CO2

MtCO2-e million tonnes of CO2 equivalentMW megawattNEB National Energy Policy BoardsNEPC National Energy Policy Council NOx nitrogen oxidesNPS National Power Supply Company ONRC Ongkharak Nuclear Research Center

3Prospects for coal and clean coal technologies in Thailand

Acronyms and abbreviations

PAD People’s Alliance for DemocracyPC pulverised coalPCD Pollution Control DepartmentPDP power development planPEA Provincial Electricity AuthorityPFBC pulverised fluidised bed combustionPPA Power Purchase AgreementPPP People’s Power PartyPTT Petroleum Authority of Thailand PTTEP Petroleum Authority of Thailand Exploration and Production CompanyPV photovoltaicRATCH Ratchaburi Electricity Generating Holding Company REDP renewable energy development plan RPS renewable portfolio standardsSCR selective catalytic reductionSEC Siam Energy CompanySO2 sulphur dioxideSPP small power producersSSEB Southern States Energy BoardtCO2 tonnes of CO2

tCO2-e tonnes of CO2 equivalentTLFS Thailand load forecast sub-committee TSP total suspended particulateTTM Trans Thailand MalaysiaUNFCCC United Nations Framework Convention on Climate ChangeUSAID United States Agency for International DevelopmentVSPP very small power producersWB World BankWHO World Heath OrganisationWTG wind turbine generators

4

Acronyms and abbreviations

IEA CLEAN COAL CENTRE

Acronyms and abbreviations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

Contents . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 71.1 Key coal facts for Thailand . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 71.2 Political and economic situation in Thailand . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 71.3 Planning for the future . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

2 Energy situation in Thailand. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 102.1 History of electricity sector . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

2.1.1 Deregulation of the electricity sector . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 102.2 Thai energy industry . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

2.2.1 Energy regulatory commission . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 132.3 Thai coal industry . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

2.3.1 Lignite production . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 142.4 Oil. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 142.5 Natural gas . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 142.6 LNG . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 152.7 Renewable energy sources . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

2.7.1 Biomass. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 172.7.2 Solar photovoltaic power programme. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 172.7.3 Geothermal energy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 172.7.4 Wind . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 172.7.5 Energy efficiency . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

2.8 Comments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

3 Meeting the demand for coal . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 203.1 Coal quality . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

3.1.1 Coal geology. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 213.1.2 Further coal exploration . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

3.2 Coal transport and movement . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 223.3 Coal consumption and demand . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 233.4 Coal imports and exports . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 233.5 Non-power coal markets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

3.5.1 Cement . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 233.5.2 Steel and iron . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 243.5.3 Domestic coal use . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

3.6 Comments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

4 Power generation sector . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 254.1 Background of power generation sector . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

4.1.1 Electricity tariffs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 254.2 Power generation capacity in Thailand . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

4.2.1 Electricity requirements and shortages. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 254.2.2 Renovation and modernisation (R&M) and life extension (LE) activities . . . . 28

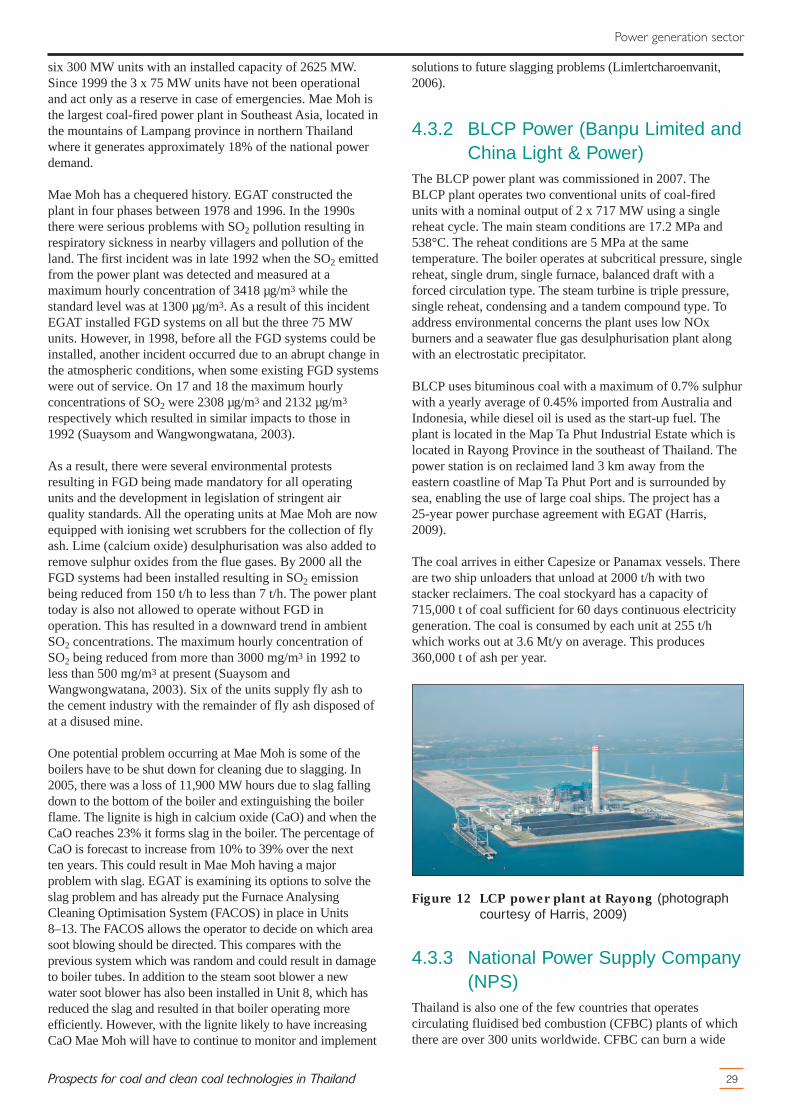

4.3 Coal-fired power stations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 284.3.1 Electricity Generation Authority of Thailand (EGAT). . . . . . . . . . . . . . . . . . . . 284.3.2 BLCP Power (Banpu Limited and China Light & Power). . . . . . . . . . . . . . . . . 294.3.3 National Power Supply Company (NPS) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 294.3.4 Glow Energy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

4.4 Gas-fired power plants . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 304.5 Naphtha and oil-fired power plants . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 314.6 Hydroelectric plants . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 314.7 Wind power . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 314.8 Small power producers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 314.9 Renewable energy plans. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 324.10 Nuclear power . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32

5Prospects for coal and clean coal technologies in Thailand

Contents

4.11 Cross-border power trade . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 324.11.1 Laos. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 324.11.2 Cambodia . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 324.11.3 Myanmar. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 324.11.4 Malaysia . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33

4.12 Comments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33

5 Environmental issues . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 345.1 Environmental control measures adopted . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34

5.1.1 Particulates and other pollutants. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 355.1.2 Utilisation of residues . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 355.1.3 SO2 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 365.1.4 NOx. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36

5.2 Carbon emissions and CCS activities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 365.3 International collaborative activities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37

5.3.1 United States Agency for Development (USAID) . . . . . . . . . . . . . . . . . . . . . . . 375.3.2 Southern States Energy Board (SSEB). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 375.3.3 Asian Development Bank (ADB). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 385.3.4 Asia Pacific Energy Co-operation (APEC) . . . . . . . . . . . . . . . . . . . . . . . . . . . . 385.3.5 ASEAN forum on coal . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 385.3.6 IEA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38

5.4 Comments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39

6 Clean coal activities in Thailand . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 406.1 Clean coal technology deployment in Thailand . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40

6.1.1 Carbon capture and storage (CCS) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 406.1.2 Supercritical PCC power plants . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 416.1.3 Fluidised bed combustion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 416.1.4 Coal gasification and IGCC . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 416.1.5 Coal-to-liquids . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 426.1.6 Underground coal gasification . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 426.1.7 Coal bed methane . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42

6.2 Coal and clean coal related R&D in Thailand. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 426.2.1 Universities and institutes. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42

6.3 Comments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42

7 Conclusions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44

8 References . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47

6

Contents

IEA CLEAN COAL CENTRE

1.1 Key coal facts for Thailand

Total coal production (2008 estimate): 18–19 MtTotal coal demand (2008 estimate): 32–36 MtImports (2008 estimate): 17–18 MtProven reserves (2008 estimate): 2000 Mt

This new report is part of a series examining coal in theASEAN countries. The analysis draws on the publishedliterature about the use of coal in Thailand as well as a seriesof meetings with several of the companies involved in thedevelopment of coal within Thailand. This included meetingswith experts from the Thailand power sector and governmentinstitutions involved in the regulation of the coal sector. Thereport discusses the past, the present and future prospects forthe use of coal and clean coal technologies within the powersector as well as discussing other major coal users, primarilythe cement sector.

1.2 Political and economic situationin Thailand

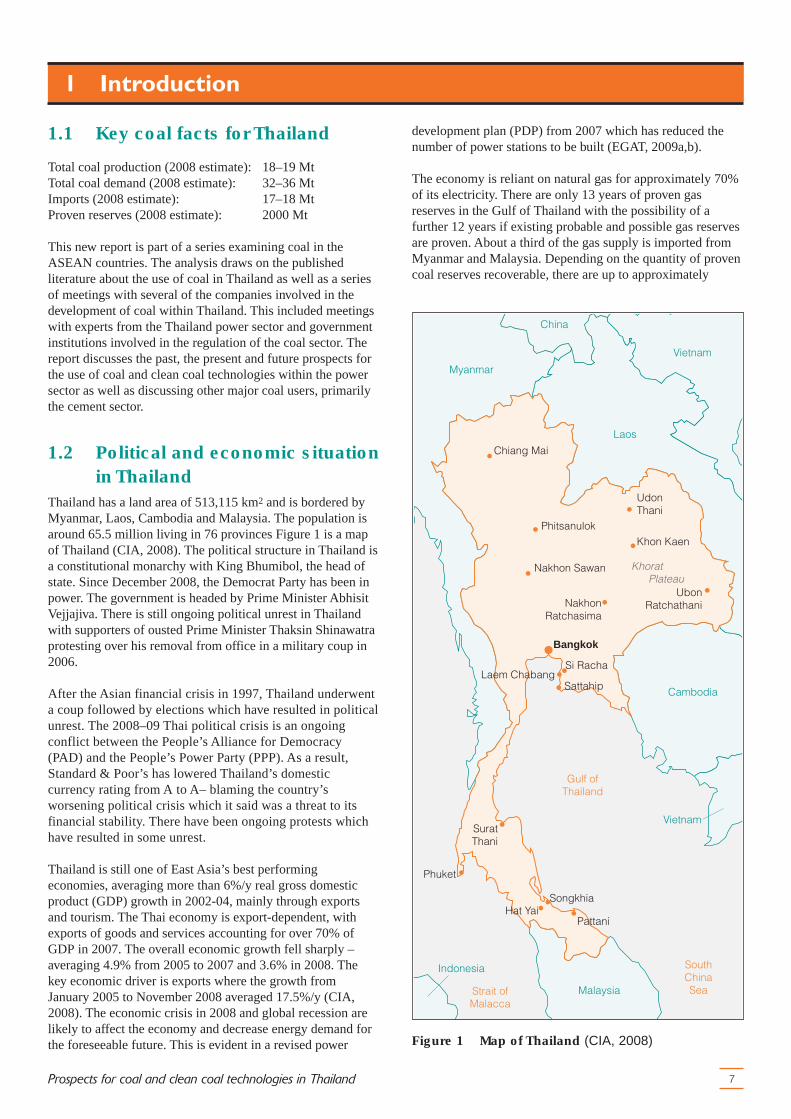

Thailand has a land area of 513,115 km2 and is bordered byMyanmar, Laos, Cambodia and Malaysia. The population isaround 65.5 million living in 76 provinces Figure 1 is a mapof Thailand (CIA, 2008). The political structure in Thailand isa constitutional monarchy with King Bhumibol, the head ofstate. Since December 2008, the Democrat Party has been inpower. The government is headed by Prime Minister AbhisitVejjajiva. There is still ongoing political unrest in Thailandwith supporters of ousted Prime Minister Thaksin Shinawatraprotesting over his removal from office in a military coup in2006.

After the Asian financial crisis in 1997, Thailand underwenta coup followed by elections which have resulted in politicalunrest. The 2008–09 Thai political crisis is an ongoingconflict between the People’s Alliance for Democracy(PAD) and the People’s Power Party (PPP). As a result,Standard & Poor’s has lowered Thailand’s domesticcurrency rating from A to A– blaming the country’sworsening political crisis which it said was a threat to itsfinancial stability. There have been ongoing protests whichhave resulted in some unrest.

Thailand is still one of East Asia’s best performingeconomies, averaging more than 6%/y real gross domesticproduct (GDP) growth in 2002-04, mainly through exportsand tourism. The Thai economy is export-dependent, withexports of goods and services accounting for over 70% ofGDP in 2007. The overall economic growth fell sharply –averaging 4.9% from 2005 to 2007 and 3.6% in 2008. Thekey economic driver is exports where the growth fromJanuary 2005 to November 2008 averaged 17.5%/y (CIA,2008). The economic crisis in 2008 and global recession arelikely to affect the economy and decrease energy demand forthe foreseeable future. This is evident in a revised power

7Prospects for coal and clean coal technologies in Thailand

development plan (PDP) from 2007 which has reduced thenumber of power stations to be built (EGAT, 2009a,b).

The economy is reliant on natural gas for approximately 70%of its electricity. There are only 13 years of proven gasreserves in the Gulf of Thailand with the possibility of afurther 12 years if existing probable and possible gas reservesare proven. About a third of the gas supply is imported fromMyanmar and Malaysia. Depending on the quantity of provencoal reserves recoverable, there are up to approximately

1 Introduction

Myanmar

Cambodia

China

Vietnam

Laos

Vietnam

Indonesia

Malaysia

Chiang Mai

UdonThani

Phitsanulok

Nakhon Sawan

Khon Kaen

UbonRatchathaniNakhon

Ratchasima

Si RachaLaem Chabang

Sattahip

SuratThani

Phuket

SongkhiaHat Yai

Pattani

Gulf ofThailand

SouthChinaSeaStrait of

Malacca

Bangkok

Khorat Plateau

Figure 1 Map of Thailand (CIA, 2008)

75 years of reserves. Due to the heavy reliance on gas anddwindling reserves, the government is examining its optionsfor diversifying the energy supply sector with nuclear power,increasing renewables, energy efficiency and increasing use ofcoal.

In December 2008, the installed generating capacity ofThailand was 29 GW. The Electricity Generation Authority ofThailand (EGAT) power plants make up 15 GW, or 50%, ofthe country’s total generation capacity. The private powersector is made up of independent power producers (IPP),38%, and small power producers (SPP), 10%, under powerpurchase agreements (PPA). Approximately 0.6 GW, or 2%of power was imported from Laos and Malaysia, respectively(EGAT, 2009a,b).

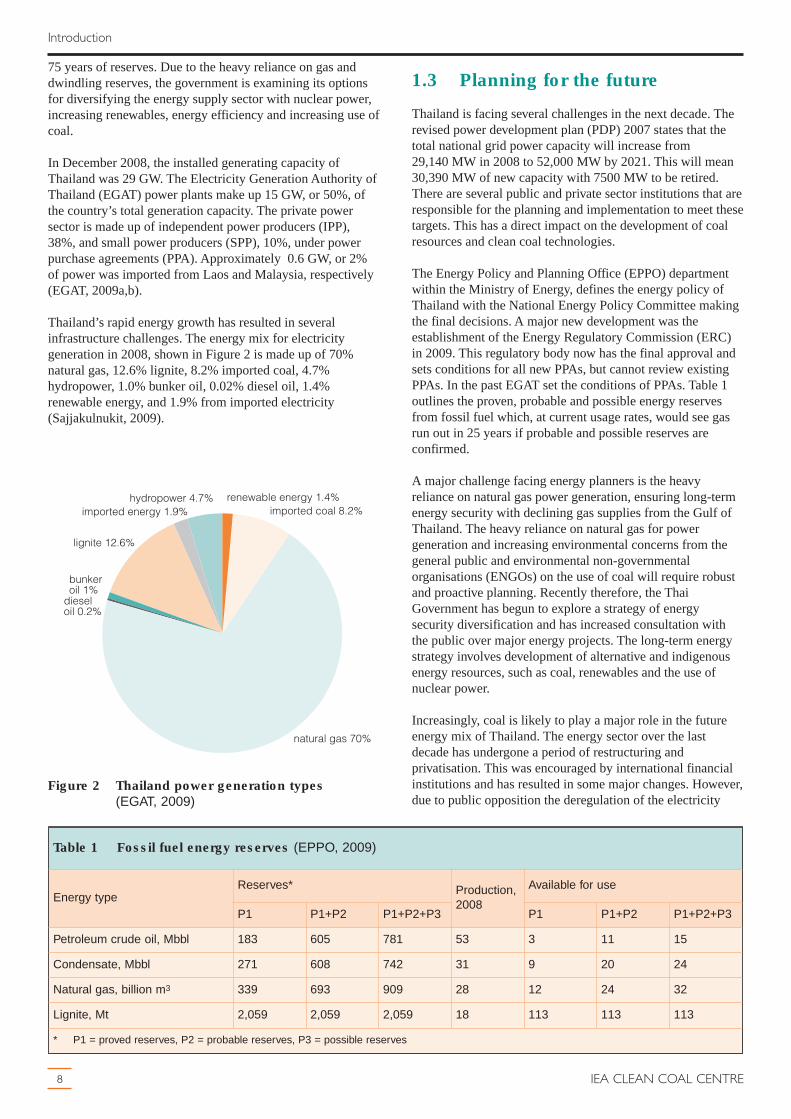

Thailand’s rapid energy growth has resulted in severalinfrastructure challenges. The energy mix for electricitygeneration in 2008, shown in Figure 2 is made up of 70%natural gas, 12.6% lignite, 8.2% imported coal, 4.7%hydropower, 1.0% bunker oil, 0.02% diesel oil, 1.4%renewable energy, and 1.9% from imported electricity(Sajjakulnukit, 2009).

8

Introduction

IEA CLEAN COAL CENTRE

1.3 Planning for the future

Thailand is facing several challenges in the next decade. Therevised power development plan (PDP) 2007 states that thetotal national grid power capacity will increase from29,140 MW in 2008 to 52,000 MW by 2021. This will mean30,390 MW of new capacity with 7500 MW to be retired.There are several public and private sector institutions that areresponsible for the planning and implementation to meet thesetargets. This has a direct impact on the development of coalresources and clean coal technologies.

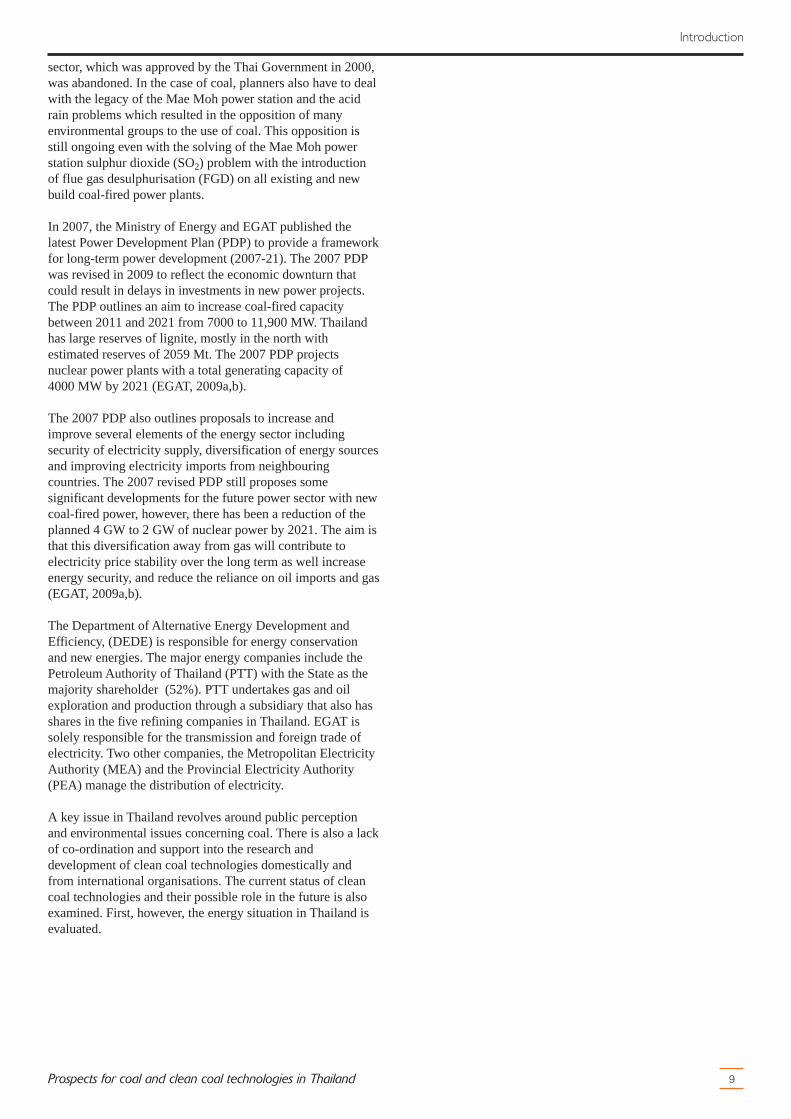

The Energy Policy and Planning Office (EPPO) departmentwithin the Ministry of Energy, defines the energy policy ofThailand with the National Energy Policy Committee makingthe final decisions. A major new development was theestablishment of the Energy Regulatory Commission (ERC)in 2009. This regulatory body now has the final approval andsets conditions for all new PPAs, but cannot review existingPPAs. In the past EGAT set the conditions of PPAs. Table 1outlines the proven, probable and possible energy reservesfrom fossil fuel which, at current usage rates, would see gasrun out in 25 years if probable and possible reserves areconfirmed.

A major challenge facing energy planners is the heavyreliance on natural gas power generation, ensuring long-termenergy security with declining gas supplies from the Gulf ofThailand. The heavy reliance on natural gas for powergeneration and increasing environmental concerns from thegeneral public and environmental non-governmentalorganisations (ENGOs) on the use of coal will require robustand proactive planning. Recently therefore, the ThaiGovernment has begun to explore a strategy of energysecurity diversification and has increased consultation withthe public over major energy projects. The long-term energystrategy involves development of alternative and indigenousenergy resources, such as coal, renewables and the use ofnuclear power.

Increasingly, coal is likely to play a major role in the futureenergy mix of Thailand. The energy sector over the lastdecade has undergone a period of restructuring andprivatisation. This was encouraged by international financialinstitutions and has resulted in some major changes. However,due to public opposition the deregulation of the electricity

renewable energy 1.4%imported coal 8.2%

natural gas 70%

dieseloil 0.2%

bunkeroil 1%

lignite 12.6%

imported energy 1.9%hydropower 4.7%

Figure 2 Thailand power generation types(EGAT, 2009)

Table 1 Fossil fuel energy reserves (EPPO, 2009)

Energy typeReserves* Production,

2008

Available for use

P1 P1+P2 P1+P2+P3 P1 P1+P2 P1+P2+P3

Petroleum crude oil, Mbbl 183 605 781 53 3 11 15

Condensate, Mbbl 271 608 742 31 9 20 24

Natural gas, billion m3 339 693 909 28 12 24 32

Lignite, Mt 2,059 2,059 2,059 18 113 113 113

* P1 = proved reserves, P2 = probable reserves, P3 = possible reserves

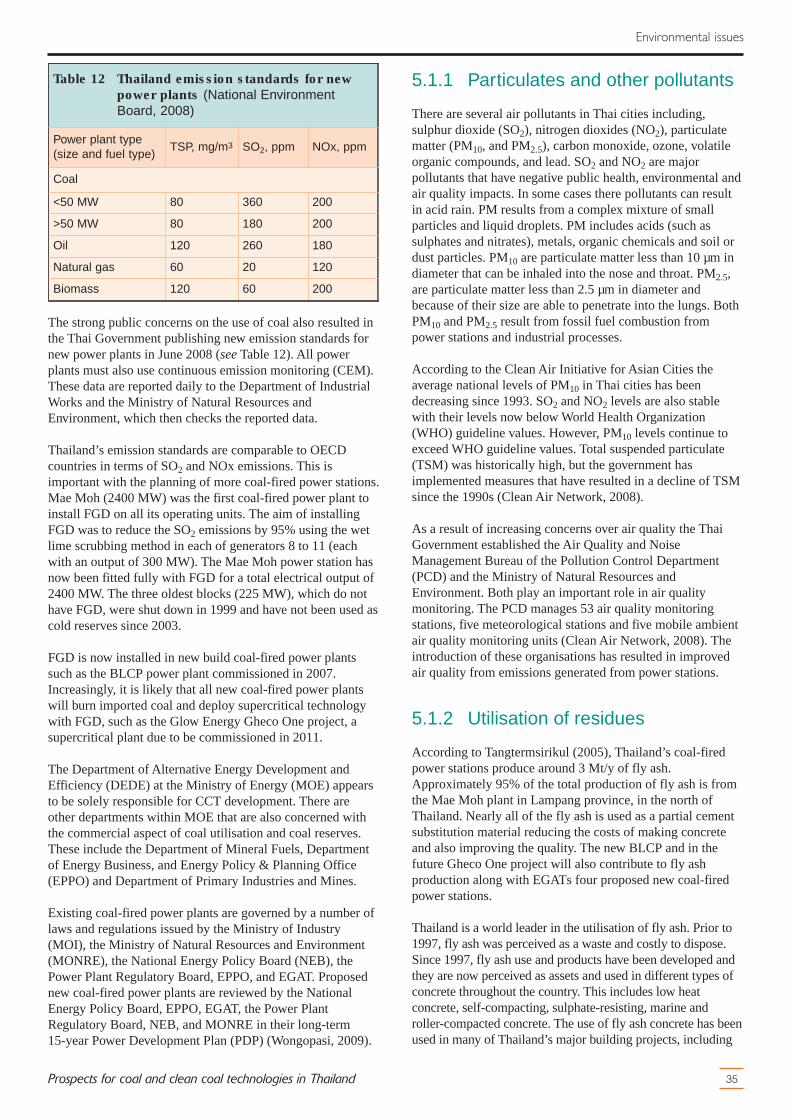

sector, which was approved by the Thai Government in 2000,was abandoned. In the case of coal, planners also have to dealwith the legacy of the Mae Moh power station and the acidrain problems which resulted in the opposition of manyenvironmental groups to the use of coal. This opposition isstill ongoing even with the solving of the Mae Moh powerstation sulphur dioxide (SO2) problem with the introductionof flue gas desulphurisation (FGD) on all existing and newbuild coal-fired power plants.

In 2007, the Ministry of Energy and EGAT published thelatest Power Development Plan (PDP) to provide a frameworkfor long-term power development (2007-21). The 2007 PDPwas revised in 2009 to reflect the economic downturn thatcould result in delays in investments in new power projects.The PDP outlines an aim to increase coal-fired capacitybetween 2011 and 2021 from 7000 to 11,900 MW. Thailandhas large reserves of lignite, mostly in the north withestimated reserves of 2059 Mt. The 2007 PDP projectsnuclear power plants with a total generating capacity of4000 MW by 2021 (EGAT, 2009a,b).

The 2007 PDP also outlines proposals to increase andimprove several elements of the energy sector includingsecurity of electricity supply, diversification of energy sourcesand improving electricity imports from neighbouringcountries. The 2007 revised PDP still proposes somesignificant developments for the future power sector with newcoal-fired power, however, there has been a reduction of theplanned 4 GW to 2 GW of nuclear power by 2021. The aim isthat this diversification away from gas will contribute toelectricity price stability over the long term as well increaseenergy security, and reduce the reliance on oil imports and gas(EGAT, 2009a,b).

The Department of Alternative Energy Development andEfficiency, (DEDE) is responsible for energy conservationand new energies. The major energy companies include thePetroleum Authority of Thailand (PTT) with the State as themajority shareholder (52%). PTT undertakes gas and oilexploration and production through a subsidiary that also hasshares in the five refining companies in Thailand. EGAT issolely responsible for the transmission and foreign trade ofelectricity. Two other companies, the Metropolitan ElectricityAuthority (MEA) and the Provincial Electricity Authority(PEA) manage the distribution of electricity.

A key issue in Thailand revolves around public perceptionand environmental issues concerning coal. There is also a lackof co-ordination and support into the research anddevelopment of clean coal technologies domestically andfrom international organisations. The current status of cleancoal technologies and their possible role in the future is alsoexamined. First, however, the energy situation in Thailand isevaluated.

9

Introduction

Prospects for coal and clean coal technologies in Thailand

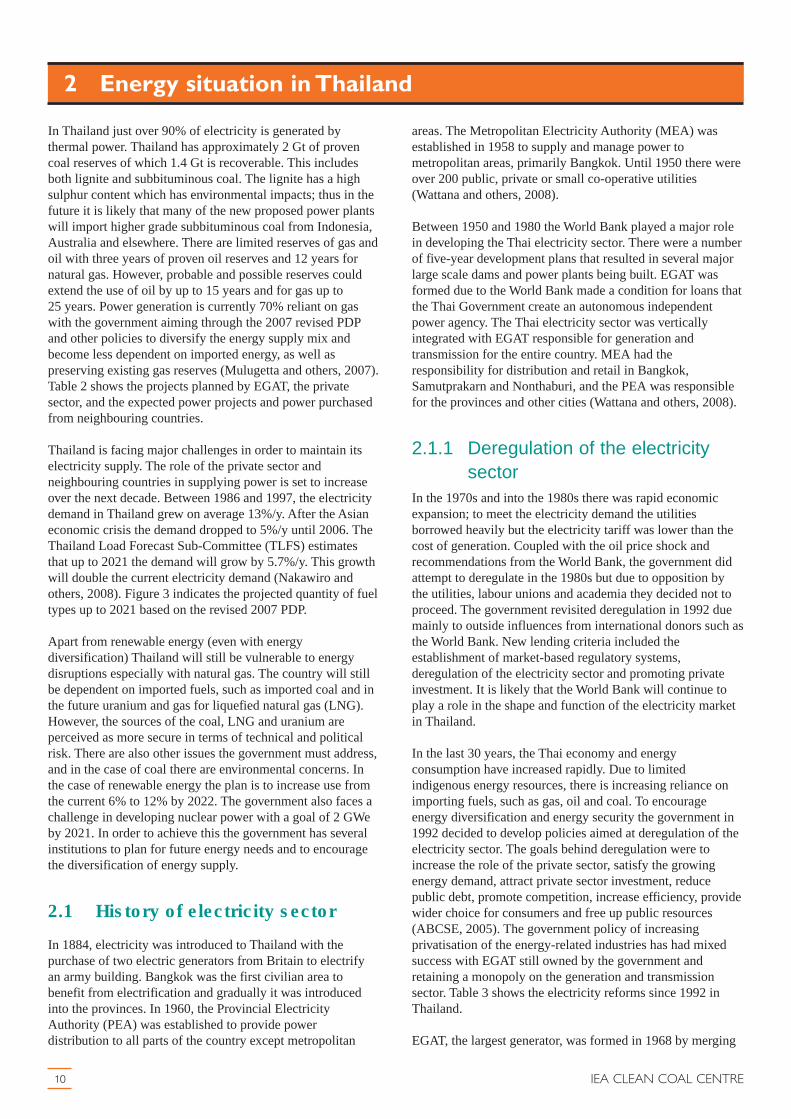

In Thailand just over 90% of electricity is generated bythermal power. Thailand has approximately 2 Gt of provencoal reserves of which 1.4 Gt is recoverable. This includesboth lignite and subbituminous coal. The lignite has a highsulphur content which has environmental impacts; thus in thefuture it is likely that many of the new proposed power plantswill import higher grade subbituminous coal from Indonesia,Australia and elsewhere. There are limited reserves of gas andoil with three years of proven oil reserves and 12 years fornatural gas. However, probable and possible reserves couldextend the use of oil by up to 15 years and for gas up to25 years. Power generation is currently 70% reliant on gaswith the government aiming through the 2007 revised PDPand other policies to diversify the energy supply mix andbecome less dependent on imported energy, as well aspreserving existing gas reserves (Mulugetta and others, 2007).Table 2 shows the projects planned by EGAT, the privatesector, and the expected power projects and power purchasedfrom neighbouring countries.

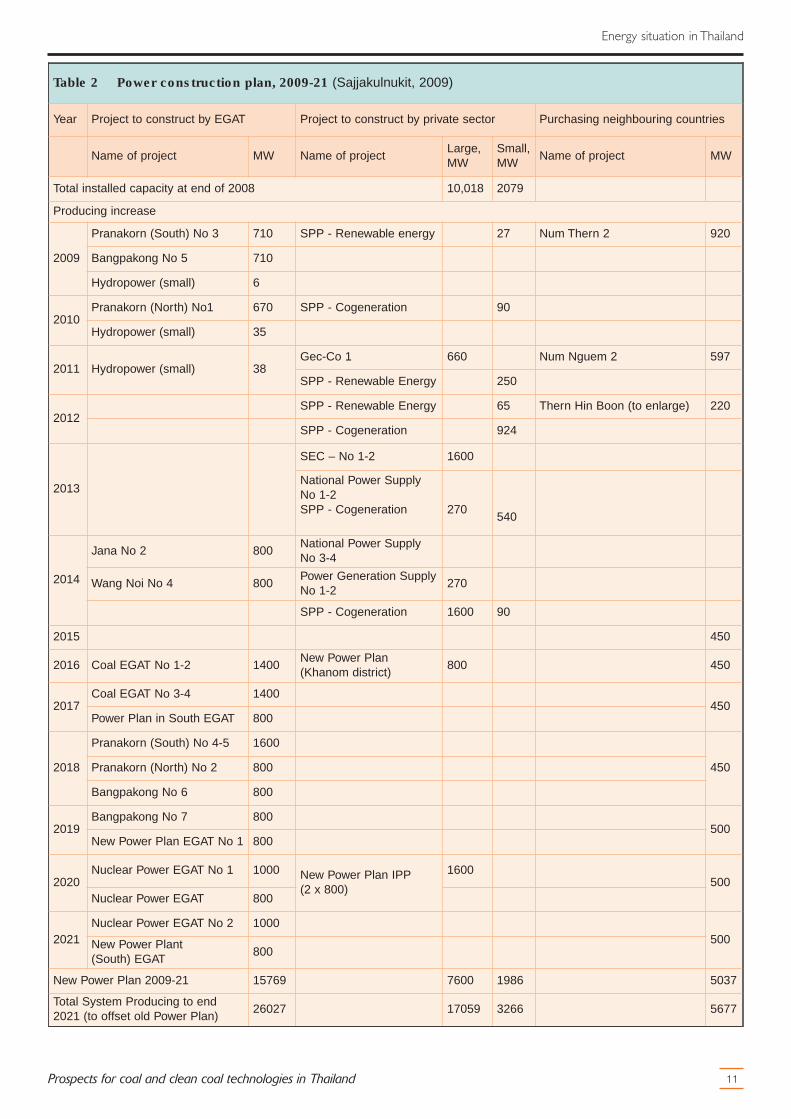

Thailand is facing major challenges in order to maintain itselectricity supply. The role of the private sector andneighbouring countries in supplying power is set to increaseover the next decade. Between 1986 and 1997, the electricitydemand in Thailand grew on average 13%/y. After the Asianeconomic crisis the demand dropped to 5%/y until 2006. TheThailand Load Forecast Sub-Committee (TLFS) estimatesthat up to 2021 the demand will grow by 5.7%/y. This growthwill double the current electricity demand (Nakawiro andothers, 2008). Figure 3 indicates the projected quantity of fueltypes up to 2021 based on the revised 2007 PDP.

Apart from renewable energy (even with energydiversification) Thailand will still be vulnerable to energydisruptions especially with natural gas. The country will stillbe dependent on imported fuels, such as imported coal and inthe future uranium and gas for liquefied natural gas (LNG).However, the sources of the coal, LNG and uranium areperceived as more secure in terms of technical and politicalrisk. There are also other issues the government must address,and in the case of coal there are environmental concerns. Inthe case of renewable energy the plan is to increase use fromthe current 6% to 12% by 2022. The government also faces achallenge in developing nuclear power with a goal of 2 GWeby 2021. In order to achieve this the government has severalinstitutions to plan for future energy needs and to encouragethe diversification of energy supply.

2.1 History of electricity sector

In 1884, electricity was introduced to Thailand with thepurchase of two electric generators from Britain to electrifyan army building. Bangkok was the first civilian area tobenefit from electrification and gradually it was introducedinto the provinces. In 1960, the Provincial ElectricityAuthority (PEA) was established to provide powerdistribution to all parts of the country except metropolitan

10 IEA CLEAN COAL CENTRE

areas. The Metropolitan Electricity Authority (MEA) wasestablished in 1958 to supply and manage power tometropolitan areas, primarily Bangkok. Until 1950 there wereover 200 public, private or small co-operative utilities(Wattana and others, 2008).

Between 1950 and 1980 the World Bank played a major rolein developing the Thai electricity sector. There were a numberof five-year development plans that resulted in several majorlarge scale dams and power plants being built. EGAT wasformed due to the World Bank made a condition for loans thatthe Thai Government create an autonomous independentpower agency. The Thai electricity sector was verticallyintegrated with EGAT responsible for generation andtransmission for the entire country. MEA had theresponsibility for distribution and retail in Bangkok,Samutprakarn and Nonthaburi, and the PEA was responsiblefor the provinces and other cities (Wattana and others, 2008).

2.1.1 Deregulation of the electricitysector

In the 1970s and into the 1980s there was rapid economicexpansion; to meet the electricity demand the utilitiesborrowed heavily but the electricity tariff was lower than thecost of generation. Coupled with the oil price shock andrecommendations from the World Bank, the government didattempt to deregulate in the 1980s but due to opposition bythe utilities, labour unions and academia they decided not toproceed. The government revisited deregulation in 1992 duemainly to outside influences from international donors such asthe World Bank. New lending criteria included theestablishment of market-based regulatory systems,deregulation of the electricity sector and promoting privateinvestment. It is likely that the World Bank will continue toplay a role in the shape and function of the electricity marketin Thailand.

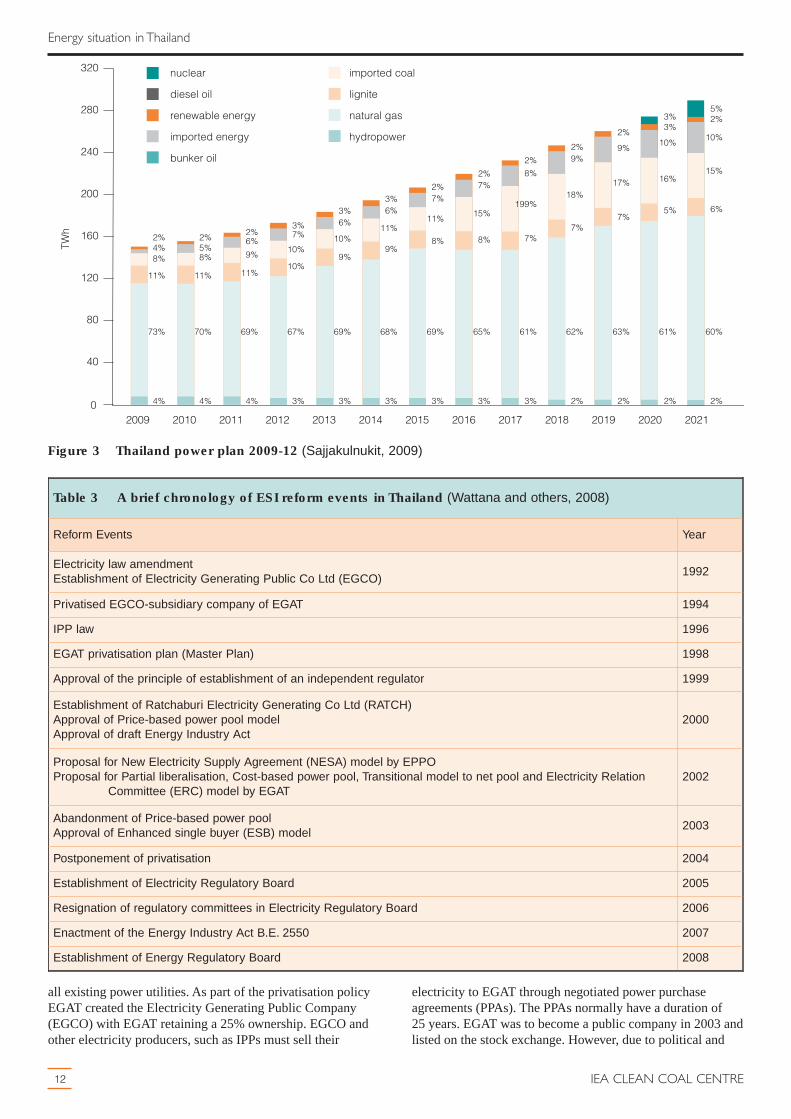

In the last 30 years, the Thai economy and energyconsumption have increased rapidly. Due to limitedindigenous energy resources, there is increasing reliance onimporting fuels, such as gas, oil and coal. To encourageenergy diversification and energy security the government in1992 decided to develop policies aimed at deregulation of theelectricity sector. The goals behind deregulation were toincrease the role of the private sector, satisfy the growingenergy demand, attract private sector investment, reducepublic debt, promote competition, increase efficiency, providewider choice for consumers and free up public resources(ABCSE, 2005). The government policy of increasingprivatisation of the energy-related industries has had mixedsuccess with EGAT still owned by the government andretaining a monopoly on the generation and transmissionsector. Table 3 shows the electricity reforms since 1992 inThailand.

EGAT, the largest generator, was formed in 1968 by merging

2 Energy situation in Thailand

11

Energy situation in Thailand

Prospects for coal and clean coal technologies in Thailand

Table 2 Power construction plan, 2009-21 (Sajjakulnukit, 2009)

Year Project to construct by EGAT Project to construct by private sector Purchasing neighbouring countries

Name of project MW Name of projectLarge,MW

Small,MW

Name of project MW

Total installed capacity at end of 2008 10,018 2079

Producing increase

2009

Pranakorn (South) No 3 710 SPP - Renewable energy 27 Num Thern 2 920

Bangpakong No 5 710

Hydropower (small) 6

2010Pranakorn (North) No1 670 SPP - Cogeneration 90

Hydropower (small) 35

2011 Hydropower (small) 38Gec-Co 1 660 Num Nguem 2 597

SPP - Renewable Energy 250

2012SPP - Renewable Energy 65 Thern Hin Boon (to enlarge) 220

SPP - Cogeneration 924

2013

SEC – No 1-2 1600

National Power SupplyNo 1-2SPP - Cogeneration 270

540

2014

Jana No 2 800National Power SupplyNo 3-4

Wang Noi No 4 800Power Generation SupplyNo 1-2

270

SPP - Cogeneration 1600 90

2015 450

2016 Coal EGAT No 1-2 1400New Power Plan(Khanom district)

800 450

2017Coal EGAT No 3-4 1400

450Power Plan in South EGAT 800

2018

Pranakorn (South) No 4-5 1600

450Pranakorn (North) No 2 800

Bangpakong No 6 800

2019Bangpakong No 7 800

500New Power Plan EGAT No 1 800

2020Nuclear Power EGAT No 1 1000 New Power Plan IPP

(2 x 800)

1600500

Nuclear Power EGAT 800

2021Nuclear Power EGAT No 2 1000

500New Power Plant(South) EGAT

800

New Power Plan 2009-21 15769 7600 1986 5037

Total System Producing to end2021 (to offset old Power Plan)

26027 17059 3266 5677

all existing power utilities. As part of the privatisation policyEGAT created the Electricity Generating Public Company(EGCO) with EGAT retaining a 25% ownership. EGCO andother electricity producers, such as IPPs must sell their

12

Energy situation in Thailand

IEA CLEAN COAL CENTRE

electricity to EGAT through negotiated power purchaseagreements (PPAs). The PPAs normally have a duration of25 years. EGAT was to become a public company in 2003 andlisted on the stock exchange. However, due to political and

Figure 3 Thailand power plan 2009-12 (Sajjakulnukit, 2009)

02009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

320

280

240

200

160

120

80

40

nuclear

diesel oil

renewable energy

imported energy

bunker oil

TWh

imported coal

lignite

natural gas

hydropower

5%2%

10%

15%

6%

60%

2%

3%3%

10%

16%

5%

61%

2%

2%

9%

17%

7%

63%

2%

2%9%

18%

7%

62%

2%

2%

8%

199%

7%

61%

3%

2%7%

15%

8%

65%

3%

2%7%

11%

8%

69%

3%

3%6%

11%

9%

68%

3%

3%6%

10%

9%

69%

3%

3%7%

10%

10%

67%

3%

2%6%

9%

11%

69%

4%

2%5%8%

11%

70%

4%

2%4%8%

11%

73%

4%

Table 3 A brief chronology of ESI reform events in Thailand (Wattana and others, 2008)

Reform Events Year

Electricity law amendmentEstablishment of Electricity Generating Public Co Ltd (EGCO)

1992

Privatised EGCO-subsidiary company of EGAT 1994

IPP law 1996

EGAT privatisation plan (Master Plan) 1998

Approval of the principle of establishment of an independent regulator 1999

Establishment of Ratchaburi Electricity Generating Co Ltd (RATCH)Approval of Price-based power pool modelApproval of draft Energy Industry Act

2000

Proposal for New Electricity Supply Agreement (NESA) model by EPPOProposal for Partial liberalisation, Cost-based power pool, Transitional model to net pool and Electricity Relation

Committee (ERC) model by EGAT2002

Abandonment of Price-based power poolApproval of Enhanced single buyer (ESB) model

2003

Postponement of privatisation 2004

Establishment of Electricity Regulatory Board 2005

Resignation of regulatory committees in Electricity Regulatory Board 2006

Enactment of the Energy Industry Act B.E. 2550 2007

Establishment of Energy Regulatory Board 2008

public opposition the privatisation plans were cancelled by theSupreme Administrative Court in 2006 (Chirarattananon andNirukkanaporn, 2006).

A major obstacle to investment in Thailand is the low fixedelectricity tariff set by EGAT. The price of electricity ismainly driven by the public sector with EGAT purchasingelectricity from IPPs, SPPs and then selling on the electricityto some direct customers and the remainder to MEA and PEAfor distribution to end-users.

EGAT promotes and subsidises several programmes forenergy efficiency and renewable energy technologies.However, the structure of the electricity tariff for IPPsoperating large fossil fuel power stations is low, which candiscourage the use of clean coal technologies such assupercritical pulverised coal combustion and carbon captureand storage, due to their additional costs. However, there aresome companies willing to build coal-fired power stationswith Gheco One currently building the first supercriticalcoal-fired power station in Rayong.

Many companies are investigating the option of buildingpower stations in neighbouring countries and transmitting theelectricity back to Thailand. One obstacle is the low fixedtariff with some banks reluctant to fund supercritical coalplants, preferring instead to fund subcritical as it is seen to bemore reliable. The fixed tariff electricity price does make iteconomically risky to build more expensive supercriticalpower plants unless there is some form of additional subsidyor a company is willing to take the risk in meeting theperformance guarantees required by banks.

Banpu generates power as an IPP and entered into a 50:50joint venture with CLP Power to build a 1400 MW subcriticalcoal-fired power station at Rayong. The power station wascompleted in 2007 and has a 25-year PPA with EGAT. Thetotal cost of the project has been estimated at US$1.3 billion,and US$1.1 billion has been received in debt financing from aconsortium of financing institutions. The plant uses importedcoal from Indonesia and Australia.

The strict air quality regulations and standards also result ingas being the preferred choice for power rather than coal. Thisreliance on gas is contrary to government policy to diversifyenergy sources. Without increasing coal-fired generation ornuclear it is likely in the future that blackouts could occur ifthere is any major ongoing disruption of gas supplies fromMyanmar, the Gulf of Thailand or Malaysia.

2.2 Thai energy industry

Thailand has limited indigenous fuel resources. Thegovernment has followed a path of deregulation as it is seenas a policy that would encourage the more efficient andeconomic use of existing resources. This has resulted in thecreation of several energy companies with many in partial orentire government ownership. The structure of the Thaienergy industry is largely driven by government-ownedcompanies with ownership in private companies. Six keyenergy companies in Thailand with government interest are:

13

Energy situation in Thailand

Prospects for coal and clean coal technologies in Thailand

� Electricity Generating Authority of Thailand (EGAT);� Metropolitan Electricity Authority (MEA);� Provincial Electricity Authority (PEA);� Petroleum Authority of Thailand (PTT Public Co Ltd);� PTT Exploration and Production Co Ltd (PTTEP);� Bangchak Petroleum Public Co Ltd (Bangchak).

The government also has shares in the following companies:� Thai Oil Co: PTT holds 49%;� Electricity Generating Public Co Ltd (EGCO): EGAT

holds 25.8%;� Fuel Pipeline Transportation Co Ltd (FPT): PTT,

Bangchak, Thai Airways International Public Co Ltd andAirports Authority of Thailand hold 44%;

� Thai Petroleum Pipeline Co Ltd (THAPPLINE): PTTholds 30.6%;

� Thai LNG Power Co Ltd (TLPC): PTT holds 40%;� Esso (Thailand) Public Co: The Ministry of Finance

holds 12.5%;� Rayong Refinery Co (RRC): PTT holds 36%;� Bangkok Aviation Fuel Services Co Ltd (BAFS): PTT,

Thai Airways and Airports Authority of Thailand hold49%.

There are also several private companies operating in theenergy sector using or planning to use coal and they includeBLCP Power, National Power Supply and Glow Energy.

2.2.1 Energy regulatory commission

In 2007 the Thai Government enacted an Energy Act whichestablished an Energy Regulatory Commission (ERC). This isan independent agency with seven members responsible forregulating and monitoring power and gas sectors to ensure thereliability and security of power and gas supplies. TheCommission is responsible for reviewing a national powerdevelopment plan and submitting recommendations to theCabinet. The ERC also regulates and approves gastransportation and electricity tariffs including the automatictariff adjustment mechanism. Other functions of the ERC areto issue licences; regulate the energy sector in a fair andtransparent manner; ensure the delivery of quality and reliableenergy services; and protect the rights and interests of energyconsumers, local communities and general public(Wongopasi, 2009). The ERC is still in a transitional stageand it is too early to report on any major changes as to howthis organisation will impact on the power sector(Dayananda, 2009).

2.3 Thai coal industry

The coal mining industry in Thailand is dominated by two keyplayers with the majority of domestic coal mined by theEGAT lignite mine at Amphoe Mae Moh in Lampang. Thismine produces around 16 Mt/y. Banpu is the next largest coalproducer and distributor in Thailand. The company has acombined production capacity of 3.3 Mt/y producing lignitecoals, which are suitable for use as a base load fuel fordomestic cement producers as well as general industries.Production facilities are located in Lamphun, Lampang, and

Payao Provinces in the north of Thailand. Banpu miningoperations in Thailand have been closed since the end of 2008upon depletion of their coal reserves. Additionally, there iscoal production from several small mines in the north withcombined production capacity of 2 Mt/y. However, thesemines have very small reserves and a short mine life (Banpu,2009).

Thailand has a subbituminous and lignite coal reserve ofaround 2000 Mt. The measured or proven reserve is 2059 Mt.There are different views on how long the reserve will lastwith BP estimating a reserve to production ratio of up to75 years (BP, 2009). However, the Ministry of Energyestimates 113 years (EPPO, 2009). The coal deposits intertiary basins are mostly located in northern Thailand withsmaller deposits in central, southern and northeastern regions.The lignite has a high sulphur content.

2.3.1 Lignite production

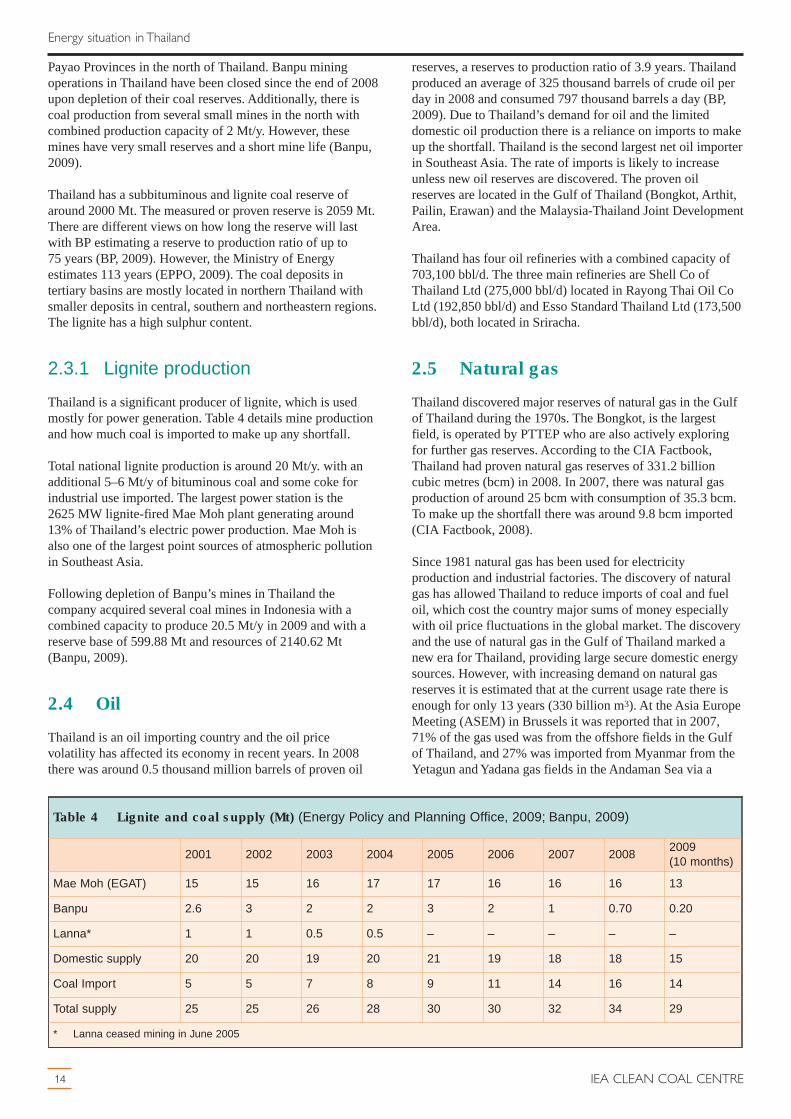

Thailand is a significant producer of lignite, which is usedmostly for power generation. Table 4 details mine productionand how much coal is imported to make up any shortfall.

Total national lignite production is around 20 Mt/y. with anadditional 5–6 Mt/y of bituminous coal and some coke forindustrial use imported. The largest power station is the2625 MW lignite-fired Mae Moh plant generating around13% of Thailand’s electric power production. Mae Moh isalso one of the largest point sources of atmospheric pollutionin Southeast Asia.

Following depletion of Banpu’s mines in Thailand thecompany acquired several coal mines in Indonesia with acombined capacity to produce 20.5 Mt/y in 2009 and with areserve base of 599.88 Mt and resources of 2140.62 Mt(Banpu, 2009).

2.4 Oil

Thailand is an oil importing country and the oil pricevolatility has affected its economy in recent years. In 2008there was around 0.5 thousand million barrels of proven oil

14

Energy situation in Thailand

IEA CLEAN COAL CENTRE

reserves, a reserves to production ratio of 3.9 years. Thailandproduced an average of 325 thousand barrels of crude oil perday in 2008 and consumed 797 thousand barrels a day (BP,2009). Due to Thailand’s demand for oil and the limiteddomestic oil production there is a reliance on imports to makeup the shortfall. Thailand is the second largest net oil importerin Southeast Asia. The rate of imports is likely to increaseunless new oil reserves are discovered. The proven oilreserves are located in the Gulf of Thailand (Bongkot, Arthit,Pailin, Erawan) and the Malaysia-Thailand Joint DevelopmentArea.

Thailand has four oil refineries with a combined capacity of703,100 bbl/d. The three main refineries are Shell Co ofThailand Ltd (275,000 bbl/d) located in Rayong Thai Oil CoLtd (192,850 bbl/d) and Esso Standard Thailand Ltd (173,500bbl/d), both located in Sriracha.

2.5 Natural gas

Thailand discovered major reserves of natural gas in the Gulfof Thailand during the 1970s. The Bongkot, is the largestfield, is operated by PTTEP who are also actively exploringfor further gas reserves. According to the CIA Factbook,Thailand had proven natural gas reserves of 331.2 billioncubic metres (bcm) in 2008. In 2007, there was natural gasproduction of around 25 bcm with consumption of 35.3 bcm.To make up the shortfall there was around 9.8 bcm imported(CIA Factbook, 2008).

Since 1981 natural gas has been used for electricityproduction and industrial factories. The discovery of naturalgas has allowed Thailand to reduce imports of coal and fueloil, which cost the country major sums of money especiallywith oil price fluctuations in the global market. The discoveryand the use of natural gas in the Gulf of Thailand marked anew era for Thailand, providing large secure domestic energysources. However, with increasing demand on natural gasreserves it is estimated that at the current usage rate there isenough for only 13 years (330 billion m3). At the Asia EuropeMeeting (ASEM) in Brussels it was reported that in 2007,71% of the gas used was from the offshore fields in the Gulfof Thailand, and 27% was imported from Myanmar from theYetagun and Yadana gas fields in the Andaman Sea via a

Table 4 Lignite and coal supply (Mt) (Energy Policy and Planning Office, 2009; Banpu, 2009)

2001 2002 2003 2004 2005 2006 2007 20082009(10 months)

Mae Moh (EGAT) 15 15 16 17 17 16 16 16 13

Banpu 2.6 3 2 2 3 2 1 0.70 0.20

Lanna* 1 1 0.5 0.5 – – – – –

Domestic supply 20 20 19 20 21 19 18 18 15

Coal Import 5 5 7 8 9 11 14 16 14

Total supply 25 25 26 28 30 30 32 34 29

* Lanna ceased mining in June 2005

670 km pipeline. Thailand also produces 2% of gas fromonshore fields (ASEM, 2009).

To address the issue of depleting gas supplies, in 1999 theThai Government signed a contract for Myanmar to supplygas for 30 years from its offshore Yadana gas field. In 2004,gas also began to be supplied from Malaysia to SouthernThailand. Figure 4 shows the current gas network inThailand.

2.6 LNG

Thailand is currently building a liquefied natural gas (LNG)regasification facility at Map Ta Phut (220 km southeast ofBangkok). The project is being developed by PTT LNGCompany Ltd (PTTLNG), a subsidiary of PTT Thai NationalPetro Chemical Company. The facility is being constructednear to the Map Ta Phut industrial complex where a numberof industries are setting up plants that may require natural gasfeedstock. Thailand also announced in May 2009 that thegovernment is to invest in the construction of a LNGreceiving terminal with an initial capacity of 5 Mt/y. The

15

Energy situation in Thailand

Prospects for coal and clean coal technologies in Thailand

terminal is expected to be completed by 2011. There is anagreement in place with Qatargas to purchase 1 Mt/y of LNGfrom 2011(Harris, 2009).

2.7 Renewable energy sources

According to the Asian Development Bank (ADB), Thailanddeveloped an Alternative Energy Development Plan thatfocuses on heat and power generation from renewable energysources, including biofuels (ADB, 2009a). The plan aims toincrease the share of renewable energy from the current 6–8%by 2011; this includes a target for biomass of 2800 MW by2011. Table 5 lists the targets for renewable and alternativefuels. The plan includes the current nine ethanol plants whichhave a production capacity of 1.25 million litres per day. Thisnumber is set to increase rapidly with the governmentapproving the construction of an additional 45 ethanol plants(20 sugar mills and 25 cassava mills) with a total capacity of12 million litres per day.

According to some bioenergy experts the target of 2800 MWfrom biomass in Thailand is very challenging and possibly not

Songkhia

Gulf ofThailand

Bangkok

Yadana

Yetagun

Nam Phong

Tha Luang

Wang Noi

Kaeng Khoi

Bang PakangRatchaburi

south power plant

RayongLaem ChabangIndustrial estate

Thap Sakae

Offshore compressor

Benchamas

Tantawan

Platong

Erawan riser platformErawan central platformERP 2

Pailin

Bongkot

JDA

Surat Thani

Khanom

Krabi

Sadao

natural gas demand location

natural gas fields

existing pipeline

parallel pipeline (existing pipeline)

Yadana pipeline (existing pipeline)

master plan - future pipeline

trans-Thailand-Malaysia pipeline

Figure 4 Natural gas pipeline network (Cogen, 2002)

achievable under current conditions. Even with favourableconditions a maximum of only 1000 MW maybe achievable.This is due to the price of oil being under 100 US$/bbl as wellas other factors. According to the Managing Director of aThailand Bioenergy Company which operates two biomasspower plants at Dan Chang and Phu Khieo a target of500 MW is more accurate and achievable. The reasons behindthe lower target are resource constraints, transport costs,loading and unloading costs as well as a low electricity tariffprice. He suggests that even if the price of oil was to riseabove 100 US$/bbl, resource constraints such as land to plantcrops and transport costs, would limit output to 1000 MW(Kamolthanat, 2009).

The plan or roadmap outlines several initiatives to accomplishthe 8% target by 2011. This includes research anddevelopment, renewable portfolio standards (RPS) and feed-intariff laws. The renewable energy sources will includebiomass, municipal solid wastes, hydro, wind, biogas andphotovoltaic (Kamolthanat, 2009).

In 2000, hydro-power plants had a total installed capacity ofabout 2936 MWe. There are estimates that Thailand has ahydro-power potential of about 10,000 MWe with feasibilitystudies completed on several hydropower projects for thegeneration up to 1500 MWe. Several of the projects areunlikely to proceed due to potential environmental andpolitical impacts with deforestation and resettlement ofpeople from the lands required for reservoirs.

There is also large hydropower potential on Thailand’sborders with two major rivers, the Mekong and Salween.However, deforestation and resettlement of people wouldagain be issues needed to be resolved before any dams couldproceed. A report by the Mekong River Commissionpublished in 2003 estimated that of the total potential of30,000 MW for feasible hydropower projects in the lowerMekong Basin, approximately 13,000 MW are on the

16

Energy situation in Thailand

IEA CLEAN COAL CENTRE

Mekong’s mainstream, with a further 13,000 MW possible onthe tributaries in Laos in locations possible to send powerback to Thailand (Mekong River Commission, 2003).Figure 5 identifies several of the planned dams in Cambodiaand Laos that could be developed in the future to generatepower for Thailand.

Table 5 Targets for renewable energy and alternative fuels in Thailand (ADB, 2009a)

Power Generation Process Heat Alternative Fuels

MW Ktoe Ktoe million litres/day Ktoe

Targets in 2011 3276 1047 4035 5.4 1606

Solar 45 4 5 n/a n/a

Wind 115 13 n/a n/a n/a

Hydropower 156 17 n/a n/a n/a

Biomass 2800 941 3660 n/a n/a

Municipal solid waste 100 45 n/a n/a n/a

Biogas 60 27 370 n/a

Ethanol n/a n/a n/a 2.4 653

Biodiesel n/a n/a n/a 3.0 953

Existing in 2006 1621 530 2424 0.5

n/a – not available

Googgjoqiao

ManwanXiaowan

Dachaoshan

NuozhaduJinghong Gananba

Mansong

Pak Beng Luang Prabang

Sayabouly

Pak Lay

Sanakham

Sangthong Pakcham

Ban KoumLat Sua

Don SahongStung Treng

Sambon

Vietnam

Thailand

China

Cambodia

dam - operational

dam - under construction

dam - planned

Figure 5 Mekong River potential hydropowerdevelopments (Mekong River commission,2003)

2.7.1 Biomass

The potential for biomass in Thailand has been estimated tobe 3000 MW (Guillermo and others, 2003). The four majoragricultural industries that use biomass as fuel forcogeneration in Thailand are the sugar, rice, palm oil, andwood industries. About 60 Mt/y of wood and agriculturalresidues from bagasse, palm oil residues and rice husks areproduced (Amatayakul and Greacon, 2002). 20 Mt of biomassis used primarily for heat and power requirements by industrywith just over a million tonnes used by rural households.Cogeneration capacity in the agricultural industries totals700 MWe (Srisovanna, 2004).

Thailand has a large biomass energy potential. However, it islimited as previously discussed by the price of oil being under100 US$/bbl, land and resource limitations, low tariffs andhigh transport and handling costs. According to Kamolthanat(2009), a company can produce 10 MWe/y with1600 hectares, however only if the land is available andwithin close proximity to the plant.

There is also the controversial issue of palm oil plantationsand deforestation. The palm oil industry in Thailand began in1968, over 50 years after Indonesia and Malaysia. Since 1975the palm oil industry has grown rapidly in Thailand to0.29 million hectares in 2004 mostly in the southernprovinces of Krabi, Chumphon, Trang, Surat Thani and Satun.The oil yield per hectare in Thailand is 20% lower whencompared to Malaysia, the biggest producer and exporter inthe world of palm oil. This is due to several factors includingthe lower average oil yield of Thai palm fruit as well asdifferent weather and soil conditions (Chavalparit, 2006).

Biomass energy is used in the household sector and insmall-scale industries. The role of biomass is limited in powerdevelopment, but opportunities exist for improving its share inthe electricity sector. There are several circulating fluidisedbed boilers (CFB) burning domestic and imported coals andcofiring with biomass. The Thai Government over the last fewyears has been laying the groundwork to develop morefavourable policy mechanisms to promote not only biomass,but also other renewable energy. These policies and powerpurchase programmes include the energy conservationpromotion fund (ECON) which was established in 1995 tosupport renewable energy and energy conservation projects.The fund gets its revenue from a tax on domestically soldpetroleum.

Another programme is the small power producers (SPP)programme which provides PPAs for clean energytechnologies and power generation with EGAT. This began in1992 and has added over 4000 MW of generating capacity tothe grid and also includes fossil-fuel based cogenerationsystems. The goals of the SPP programme are:� promote the use of indigenous by-product energy sources

and renewable energy for electricity generation;� reduce the cost of government investment in electricity

generation and distribution;� promote more efficient use of primary energy;� encourage participation by the SPP in electricity

generation (Amatayakul and Greacen, 2002).

17

Energy situation in Thailand

Prospects for coal and clean coal technologies in Thailand

There are still a number of policy, technical, financial,institutional and information barriers to overcome before therecan be a greater uptake of biomass as an energy source. One ofthe goals of the Thai Government is to replace 20% of fuelconsumption with biofuels and natural gas by 2012 (ADB,2009). This is a challenging goal and is highly unlikely to bemet even with ongoing government and private sector support.

2.7.2 Solar photovoltaic powerprogramme

Thailand’s location is favourable for solar power. Accordingto Amatayakul and Greacen (2002), a solar map produced bythe Department of Energy Development and Promotion(DEDP) in 1999 indicated most areas of Thailand received themaximum energy from sunlight in April and May, rangingfrom 20 to 24 MJ m2/d.

In Thailand, approximately 80% of photovoltaic (PV)modules installed are funded by the public sector or withoverseas assistance. There are several PV companies inThailand that together manufacture PV modules of around25 MW/y. The PV modules are mainly used fortelecommunications, water pumps, battery charging stations,village electrification, education, health care, navigation andaudio visual aids as well as some domestic lighting.

2.7.3 Geothermal energy

There are several sites in northern Thailand that couldgenerate geothermal energy. However, none of the sites couldgenerate geothermal energy at a commercial scale.

2.7.4 Wind

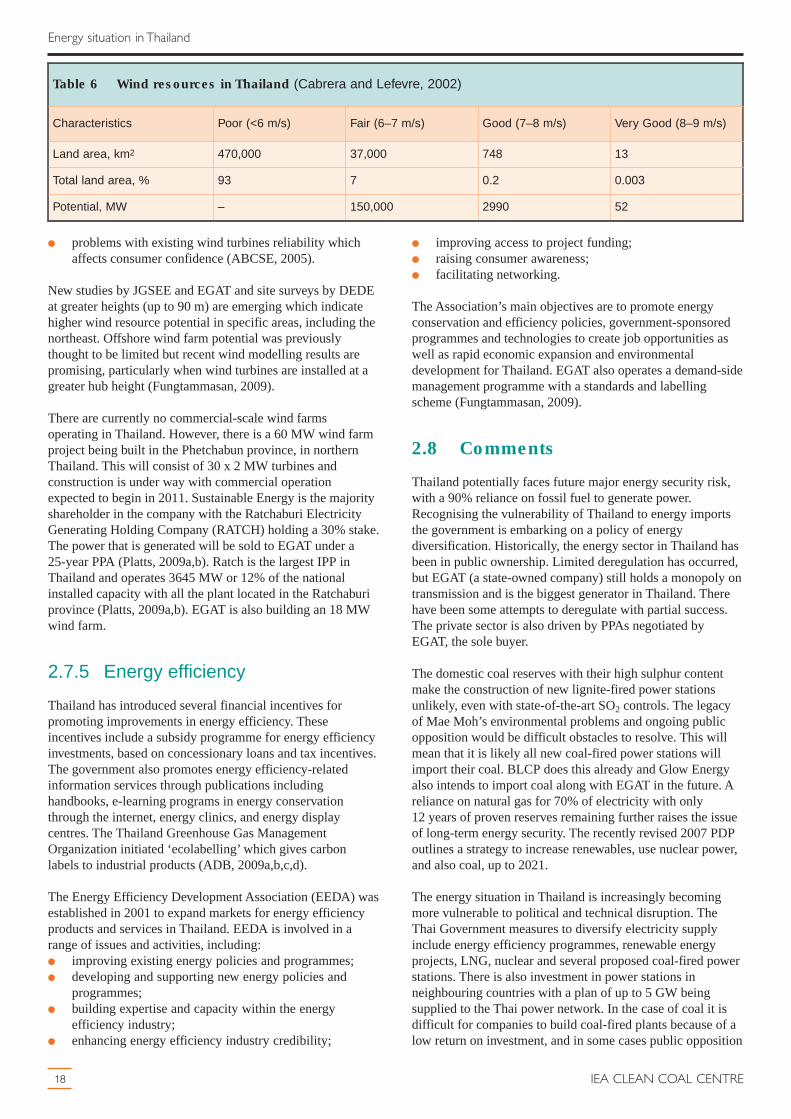

There is some potential for wind energy in Thailand. Thecentral and western regions of Thailand have the bestpotential. There have been several studies assessing thepotential of wind energy in Thailand, beginning in 1975 withdata collected by the Thai Meteorological Department. Laterin 1981 a database for average wind velocity in Thailand at10 m height was developed by EGAT and King Mongkut’sUniversity of Technology Thonburi (KMUTT). In 2001, theDepartment of Alternative Energy Development andEfficiency (DEDE) using the IDRISI program developed awind map of wind frequency, velocity and power at 10, 30and 50 m heights (Major and others, 2008). The World Bankalso carried out a study. One problem that has arisen is theinconsistency of the results making it difficult for wind farmdevelopers to make informed decisions on where, or if, tobuild. Table 6 illustrates the land resource according to windspeed.

There are several constraints to the development of windenergy in Thailand. These include:� no grid connection in rural areas;� lack of finance;� need for accurate wind data to identify wind sites;� no manufacturing or distribution capacity;

� problems with existing wind turbines reliability whichaffects consumer confidence (ABCSE, 2005).

New studies by JGSEE and EGAT and site surveys by DEDEat greater heights (up to 90 m) are emerging which indicatehigher wind resource potential in specific areas, including thenortheast. Offshore wind farm potential was previouslythought to be limited but recent wind modelling results arepromising, particularly when wind turbines are installed at agreater hub height (Fungtammasan, 2009).

There are currently no commercial-scale wind farmsoperating in Thailand. However, there is a 60 MW wind farmproject being built in the Phetchabun province, in northernThailand. This will consist of 30 x 2 MW turbines andconstruction is under way with commercial operationexpected to begin in 2011. Sustainable Energy is the majorityshareholder in the company with the Ratchaburi ElectricityGenerating Holding Company (RATCH) holding a 30% stake.The power that is generated will be sold to EGAT under a25-year PPA (Platts, 2009a,b). Ratch is the largest IPP inThailand and operates 3645 MW or 12% of the nationalinstalled capacity with all the plant located in the Ratchaburiprovince (Platts, 2009a,b). EGAT is also building an 18 MWwind farm.

2.7.5 Energy efficiency

Thailand has introduced several financial incentives forpromoting improvements in energy efficiency. Theseincentives include a subsidy programme for energy efficiencyinvestments, based on concessionary loans and tax incentives.The government also promotes energy efficiency-relatedinformation services through publications includinghandbooks, e-learning programs in energy conservationthrough the internet, energy clinics, and energy displaycentres. The Thailand Greenhouse Gas ManagementOrganization initiated ‘ecolabelling’ which gives carbonlabels to industrial products (ADB, 2009a,b,c,d).

The Energy Efficiency Development Association (EEDA) wasestablished in 2001 to expand markets for energy efficiencyproducts and services in Thailand. EEDA is involved in arange of issues and activities, including:� improving existing energy policies and programmes; � developing and supporting new energy policies and

programmes; � building expertise and capacity within the energy

efficiency industry; � enhancing energy efficiency industry credibility;

18

Energy situation in Thailand

IEA CLEAN COAL CENTRE

� improving access to project funding; � raising consumer awareness;� facilitating networking.

The Association’s main objectives are to promote energyconservation and efficiency policies, government-sponsoredprogrammes and technologies to create job opportunities aswell as rapid economic expansion and environmentaldevelopment for Thailand. EGAT also operates a demand-sidemanagement programme with a standards and labellingscheme (Fungtammasan, 2009).

2.8 Comments

Thailand potentially faces future major energy security risk,with a 90% reliance on fossil fuel to generate power.Recognising the vulnerability of Thailand to energy importsthe government is embarking on a policy of energydiversification. Historically, the energy sector in Thailand hasbeen in public ownership. Limited deregulation has occurred,but EGAT (a state-owned company) still holds a monopoly ontransmission and is the biggest generator in Thailand. Therehave been some attempts to deregulate with partial success.The private sector is also driven by PPAs negotiated byEGAT, the sole buyer.

The domestic coal reserves with their high sulphur contentmake the construction of new lignite-fired power stationsunlikely, even with state-of-the-art SO2 controls. The legacyof Mae Moh’s environmental problems and ongoing publicopposition would be difficult obstacles to resolve. This willmean that it is likely all new coal-fired power stations willimport their coal. BLCP does this already and Glow Energyalso intends to import coal along with EGAT in the future. Areliance on natural gas for 70% of electricity with only12 years of proven reserves remaining further raises the issueof long-term energy security. The recently revised 2007 PDPoutlines a strategy to increase renewables, use nuclear power,and also coal, up to 2021.

The energy situation in Thailand is increasingly becomingmore vulnerable to political and technical disruption. TheThai Government measures to diversify electricity supplyinclude energy efficiency programmes, renewable energyprojects, LNG, nuclear and several proposed coal-fired powerstations. There is also investment in power stations inneighbouring countries with a plan of up to 5 GW beingsupplied to the Thai power network. In the case of coal it isdifficult for companies to build coal-fired plants because of alow return on investment, and in some cases public opposition

Table 6 Wind resources in Thailand (Cabrera and Lefevre, 2002)

Characteristics Poor (<6 m/s) Fair (6–7 m/s) Good (7–8 m/s) Very Good (8–9 m/s)

Land area, km2 470,000 37,000 748 13

Total land area, % 93 7 0.2 0.003

Potential, MW – 150,000 2990 52

to the siting of a plant near their community. A recent tenderto IPPs resulted in several coal-fired power plants beingapproved, including a 700 MW supercritical one. However,whether they all proceed is debatable.

There is no single silver bullet energy supply technology thatwill solve the future energy demand in Thailand; it willrequire a portfolio of different energy supply technologies.Biomass is projected to supply 3 GW but could be limited dueto it being seasonal, the cost of loading, unloading andtransport. Wind has limited potential with few viable sites forcommercial operation. The construction of the LNG plant inRayong and proposed 2 GW of nuclear power will allcontribute to the energy mix.

19

Energy situation in Thailand

Prospects for coal and clean coal technologies in Thailand

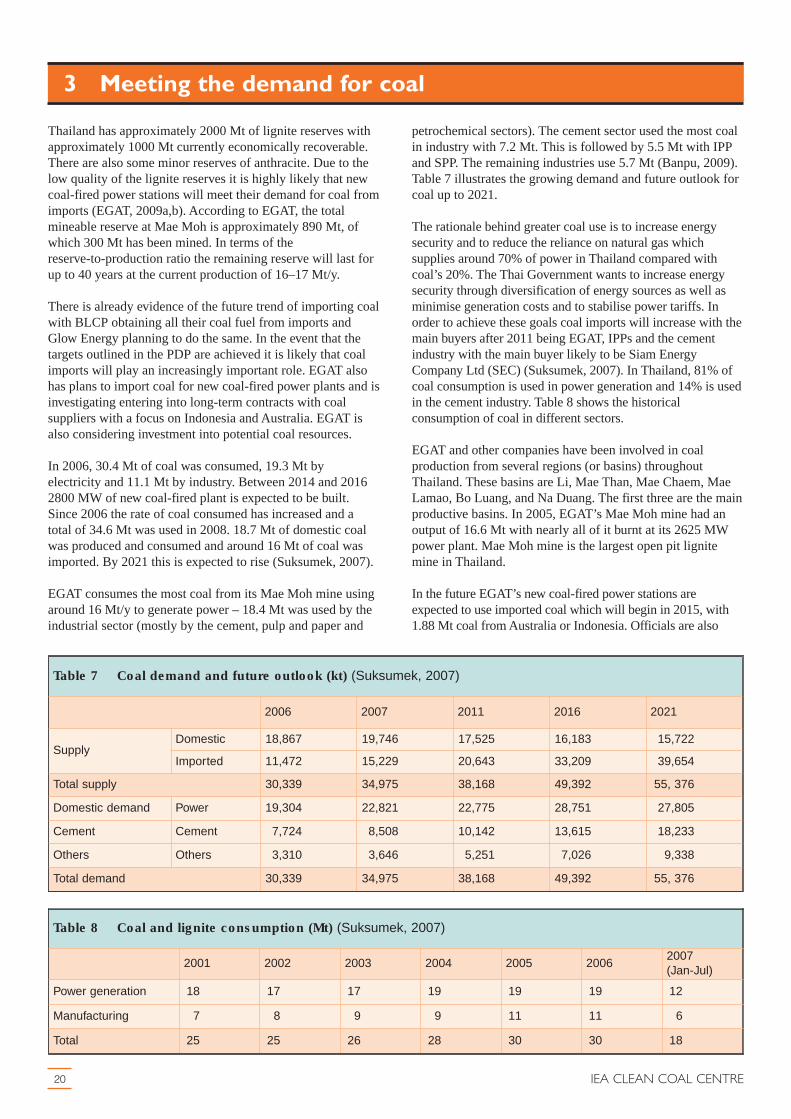

Thailand has approximately 2000 Mt of lignite reserves withapproximately 1000 Mt currently economically recoverable.There are also some minor reserves of anthracite. Due to thelow quality of the lignite reserves it is highly likely that newcoal-fired power stations will meet their demand for coal fromimports (EGAT, 2009a,b). According to EGAT, the totalmineable reserve at Mae Moh is approximately 890 Mt, ofwhich 300 Mt has been mined. In terms of thereserve-to-production ratio the remaining reserve will last forup to 40 years at the current production of 16–17 Mt/y.

There is already evidence of the future trend of importing coalwith BLCP obtaining all their coal fuel from imports andGlow Energy planning to do the same. In the event that thetargets outlined in the PDP are achieved it is likely that coalimports will play an increasingly important role. EGAT alsohas plans to import coal for new coal-fired power plants and isinvestigating entering into long-term contracts with coalsuppliers with a focus on Indonesia and Australia. EGAT isalso considering investment into potential coal resources.

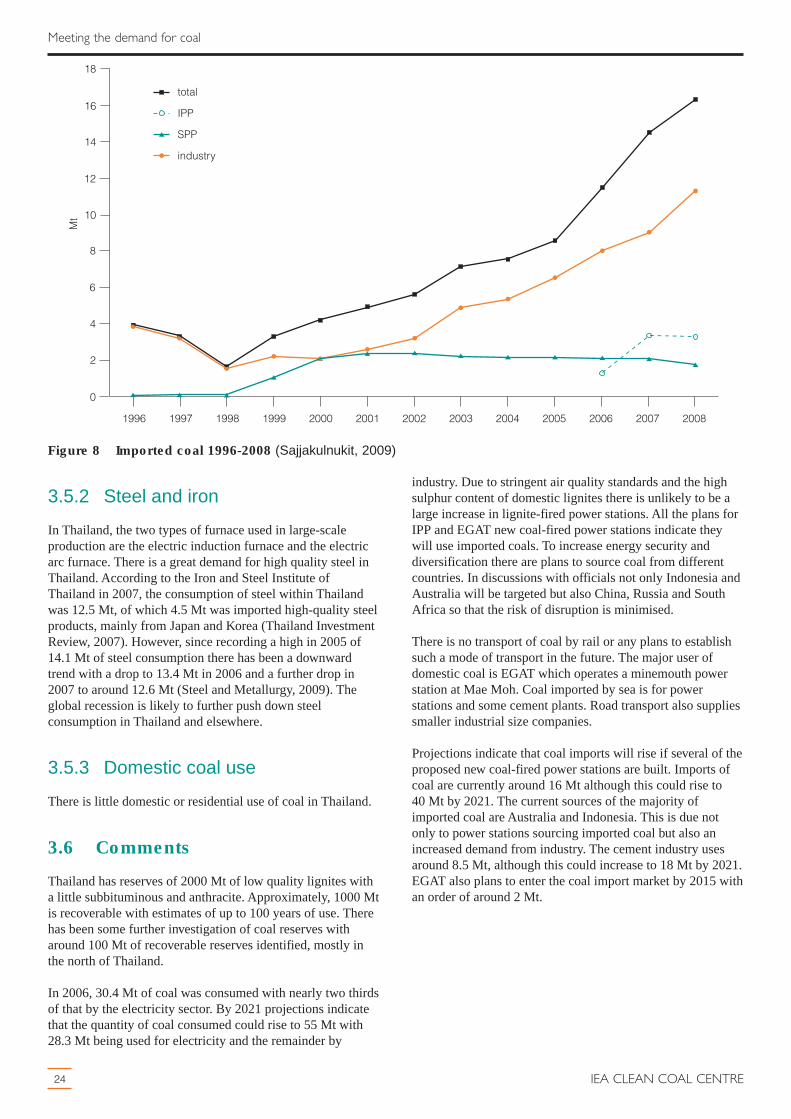

In 2006, 30.4 Mt of coal was consumed, 19.3 Mt byelectricity and 11.1 Mt by industry. Between 2014 and 20162800 MW of new coal-fired plant is expected to be built.Since 2006 the rate of coal consumed has increased and atotal of 34.6 Mt was used in 2008. 18.7 Mt of domestic coalwas produced and consumed and around 16 Mt of coal wasimported. By 2021 this is expected to rise (Suksumek, 2007).

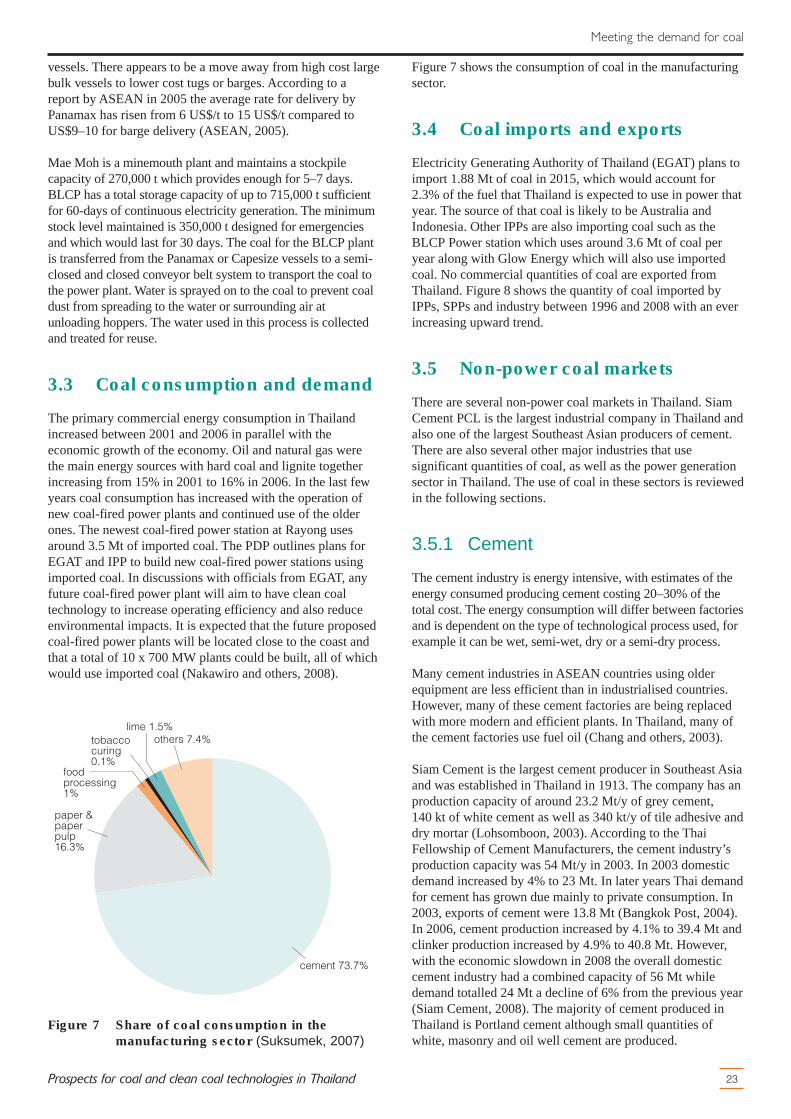

EGAT consumes the most coal from its Mae Moh mine usingaround 16 Mt/y to generate power – 18.4 Mt was used by theindustrial sector (mostly by the cement, pulp and paper and

20 IEA CLEAN COAL CENTRE

petrochemical sectors). The cement sector used the most coalin industry with 7.2 Mt. This is followed by 5.5 Mt with IPPand SPP. The remaining industries use 5.7 Mt (Banpu, 2009).Table 7 illustrates the growing demand and future outlook forcoal up to 2021.

The rationale behind greater coal use is to increase energysecurity and to reduce the reliance on natural gas whichsupplies around 70% of power in Thailand compared withcoal’s 20%. The Thai Government wants to increase energysecurity through diversification of energy sources as well asminimise generation costs and to stabilise power tariffs. Inorder to achieve these goals coal imports will increase with themain buyers after 2011 being EGAT, IPPs and the cementindustry with the main buyer likely to be Siam EnergyCompany Ltd (SEC) (Suksumek, 2007). In Thailand, 81% ofcoal consumption is used in power generation and 14% is usedin the cement industry. Table 8 shows the historicalconsumption of coal in different sectors.

EGAT and other companies have been involved in coalproduction from several regions (or basins) throughoutThailand. These basins are Li, Mae Than, Mae Chaem, MaeLamao, Bo Luang, and Na Duang. The first three are the mainproductive basins. In 2005, EGAT’s Mae Moh mine had anoutput of 16.6 Mt with nearly all of it burnt at its 2625 MWpower plant. Mae Moh mine is the largest open pit lignitemine in Thailand.

In the future EGAT’s new coal-fired power stations areexpected to use imported coal which will begin in 2015, with1.88 Mt coal from Australia or Indonesia. Officials are also

3 Meeting the demand for coal

Table 7 Coal demand and future outlook (kt) (Suksumek, 2007)

2006 2007 2011 2016 2021

Supply Domestic 18,867 19,746 17,525 16,183 15,722

Imported 11,472 15,229 20,643 33,209 39,654

Total supply 30,339 34,975 38,168 49,392 55, 376

Domestic demand Power 19,304 22,821 22,775 28,751 27,805

Cement Cement 7,724 8,508 10,142 13,615 18,233

Others Others 3,310 3,646 5,251 7,026 9,338

Total demand 30,339 34,975 38,168 49,392 55, 376

Table 8 Coal and lignite consumption (Mt) (Suksumek, 2007)

2001 2002 2003 2004 2005 20062007(Jan-Jul)

Power generation 18 17 17 19 19 19 12

Manufacturing 7 8 9 9 11 11 6

Total 25 25 26 28 30 30 18

21

Meeting the demand for coal

Prospects for coal and clean coal technologies in Thailand

Burma

China

Vietnam

Laos

Vietnam

Indonesia

Malaysia

Chiang Mai

Nakhon Ratchasima

Suphan Buri

Surat Thani

Songkhia

Gulf ofThailand

SouthChinaSea

Strait ofMalacca

Bangkok

Khorat Plateau

Tak

Prachub Khirikhan

Nakhon Si Thammarat

Yala

Chiang Muan

Mae TeepMae Moh

Mae ThanLi

Bo Luang

Mae Chaern

Mae Tuen

Mae Lamao

Na DuangNa Klang

Nong ya Plong

Krabi

Kantang active coal mine

suspended coal mine

Figure 6 Current active and suspended coalmines (Sajjakulnukit, 2009)

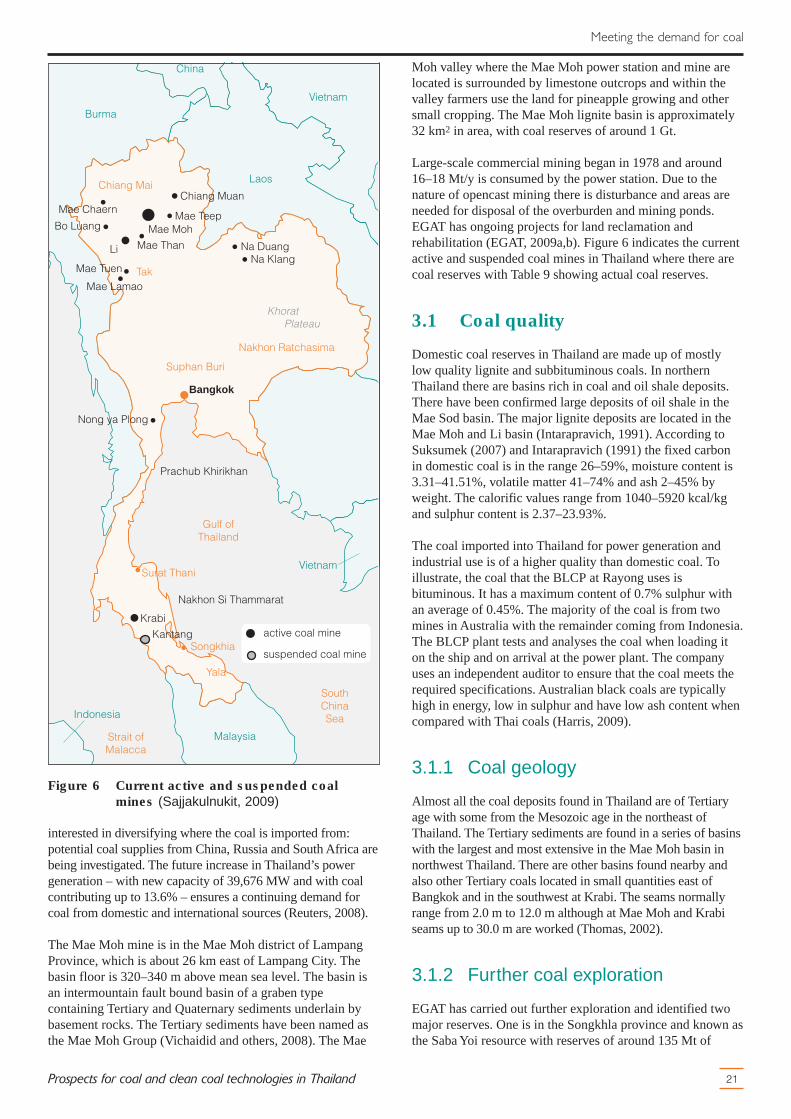

Moh valley where the Mae Moh power station and mine arelocated is surrounded by limestone outcrops and within thevalley farmers use the land for pineapple growing and othersmall cropping. The Mae Moh lignite basin is approximately32 km2 in area, with coal reserves of around 1 Gt.

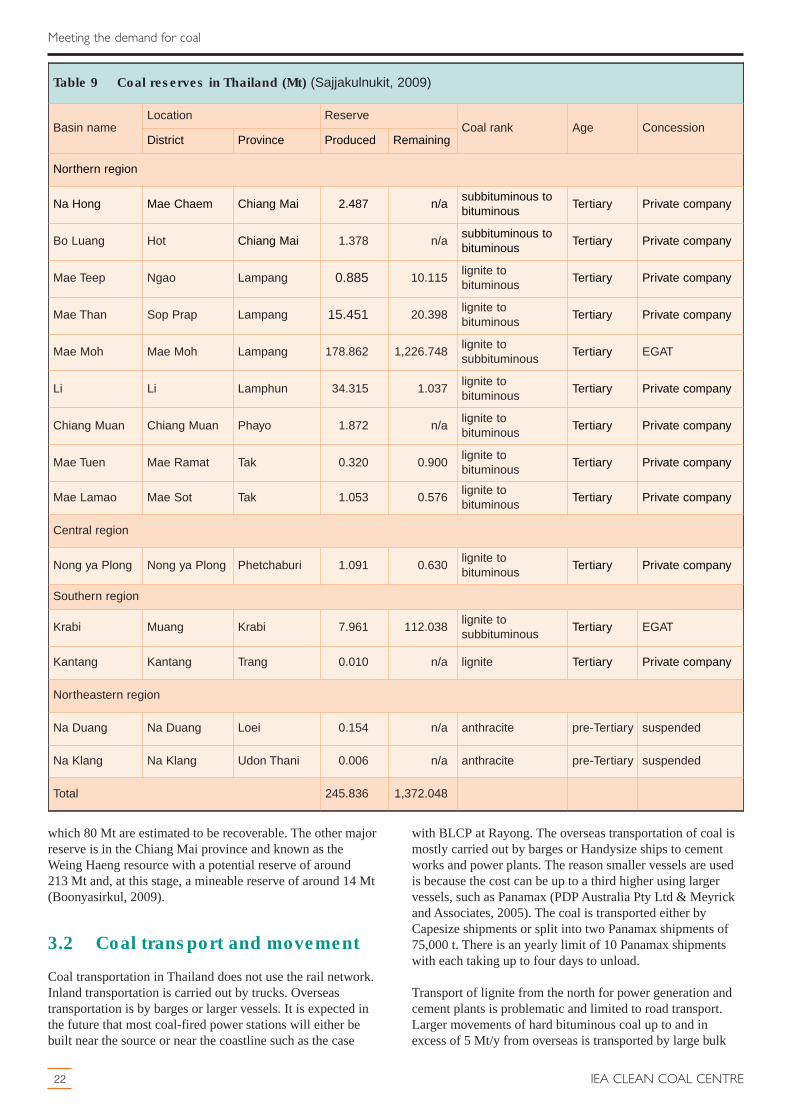

Large-scale commercial mining began in 1978 and around16–18 Mt/y is consumed by the power station. Due to thenature of opencast mining there is disturbance and areas areneeded for disposal of the overburden and mining ponds.EGAT has ongoing projects for land reclamation andrehabilitation (EGAT, 2009a,b). Figure 6 indicates the currentactive and suspended coal mines in Thailand where there arecoal reserves with Table 9 showing actual coal reserves.

3.1 Coal quality

Domestic coal reserves in Thailand are made up of mostlylow quality lignite and subbituminous coals. In northernThailand there are basins rich in coal and oil shale deposits.There have been confirmed large deposits of oil shale in theMae Sod basin. The major lignite deposits are located in theMae Moh and Li basin (Intarapravich, 1991). According toSuksumek (2007) and Intarapravich (1991) the fixed carbonin domestic coal is in the range 26–59%, moisture content is3.31–41.51%, volatile matter 41–74% and ash 2–45% byweight. The calorific values range from 1040–5920 kcal/kgand sulphur content is 2.37–23.93%.

The coal imported into Thailand for power generation andindustrial use is of a higher quality than domestic coal. Toillustrate, the coal that the BLCP at Rayong uses isbituminous. It has a maximum content of 0.7% sulphur withan average of 0.45%. The majority of the coal is from twomines in Australia with the remainder coming from Indonesia.The BLCP plant tests and analyses the coal when loading iton the ship and on arrival at the power plant. The companyuses an independent auditor to ensure that the coal meets therequired specifications. Australian black coals are typicallyhigh in energy, low in sulphur and have low ash content whencompared with Thai coals (Harris, 2009).

3.1.1 Coal geology

Almost all the coal deposits found in Thailand are of Tertiaryage with some from the Mesozoic age in the northeast ofThailand. The Tertiary sediments are found in a series of basinswith the largest and most extensive in the Mae Moh basin innorthwest Thailand. There are other basins found nearby andalso other Tertiary coals located in small quantities east ofBangkok and in the southwest at Krabi. The seams normallyrange from 2.0 m to 12.0 m although at Mae Moh and Krabiseams up to 30.0 m are worked (Thomas, 2002).

3.1.2 Further coal exploration

EGAT has carried out further exploration and identified twomajor reserves. One is in the Songkhla province and known asthe Saba Yoi resource with reserves of around 135 Mt of

interested in diversifying where the coal is imported from:potential coal supplies from China, Russia and South Africa arebeing investigated. The future increase in Thailand’s powergeneration – with new capacity of 39,676 MW and with coalcontributing up to 13.6% – ensures a continuing demand forcoal from domestic and international sources (Reuters, 2008).

The Mae Moh mine is in the Mae Moh district of LampangProvince, which is about 26 km east of Lampang City. Thebasin floor is 320–340 m above mean sea level. The basin isan intermountain fault bound basin of a graben typecontaining Tertiary and Quaternary sediments underlain bybasement rocks. The Tertiary sediments have been named asthe Mae Moh Group (Vichaidid and others, 2008). The Mae

which 80 Mt are estimated to be recoverable. The other majorreserve is in the Chiang Mai province and known as theWeing Haeng resource with a potential reserve of around213 Mt and, at this stage, a mineable reserve of around 14 Mt(Boonyasirkul, 2009).

3.2 Coal transport and movement

Coal transportation in Thailand does not use the rail network.Inland transportation is carried out by trucks. Overseastransportation is by barges or larger vessels. It is expected inthe future that most coal-fired power stations will either bebuilt near the source or near the coastline such as the case

22

Meeting the demand for coal

IEA CLEAN COAL CENTRE

with BLCP at Rayong. The overseas transportation of coal ismostly carried out by barges or Handysize ships to cementworks and power plants. The reason smaller vessels are usedis because the cost can be up to a third higher using largervessels, such as Panamax (PDP Australia Pty Ltd & Meyrickand Associates, 2005). The coal is transported either byCapesize shipments or split into two Panamax shipments of75,000 t. There is an yearly limit of 10 Panamax shipmentswith each taking up to four days to unload.

Transport of lignite from the north for power generation andcement plants is problematic and limited to road transport.Larger movements of hard bituminous coal up to and inexcess of 5 Mt/y from overseas is transported by large bulk

Table 9 Coal reserves in Thailand (Mt) (Sajjakulnukit, 2009)

Basin nameLocation Reserve

Coal rank Age ConcessionDistrict Province Produced Remaining

Northern region

Na Hong Mae Chaem Chiang Mai 2.487 n/asubbituminous tobituminous

Tertiary Private company

Bo Luang Hot Chiang Mai 1.378 n/asubbituminous tobituminous

Tertiary Private company

Mae Teep Ngao Lampang 0.885 10.115lignite tobituminous

Tertiary Private company

Mae Than Sop Prap Lampang 15.451 20.398lignite tobituminous

Tertiary Private company

Mae Moh Mae Moh Lampang 178.862 1,226.748lignite tosubbituminous

Tertiary EGAT

Li Li Lamphun 34.315 1.037lignite tobituminous

Tertiary Private company

Chiang Muan Chiang Muan Phayo 1.872 n/alignite tobituminous

Tertiary Private company

Mae Tuen Mae Ramat Tak 0.320 0.900lignite tobituminous

Tertiary Private company

Mae Lamao Mae Sot Tak 1.053 0.576lignite tobituminous

Tertiary Private company

Central region

Nong ya Plong Nong ya Plong Phetchaburi 1.091 0.630lignite tobituminous

Tertiary Private company

Southern region

Krabi Muang Krabi 7.961 112.038lignite tosubbituminous

Tertiary EGAT

Kantang Kantang Trang 0.010 n/a lignite Tertiary Private company

Northeastern region

Na Duang Na Duang Loei 0.154 n/a anthracite pre-Tertiary suspended

Na Klang Na Klang Udon Thani 0.006 n/a anthracite pre-Tertiary suspended

Total 245.836 1,372.048

vessels. There appears to be a move away from high cost largebulk vessels to lower cost tugs or barges. According to areport by ASEAN in 2005 the average rate for delivery byPanamax has risen from 6 US$/t to 15 US$/t compared toUS$9–10 for barge delivery (ASEAN, 2005).