prospects for oil prices 2011 - chatham house · prospects for oil prices 2011 professor paul...

TRANSCRIPT

Prospects for Oil Prices 2011

Professor Paul StevensSenior Research Fellow (Energy) Chatham HouseProfessor Emeritus, University of DundeeConsulting Professor Stanford University

Chatham House Fossil Fuels Expert Roundtable –Forecasting 2011

London 7th January 2011

2

Presentation outline

• What happened last year?

• Short term prospects for price

• Supply prospects longer term?

• Demand prospects longer term?

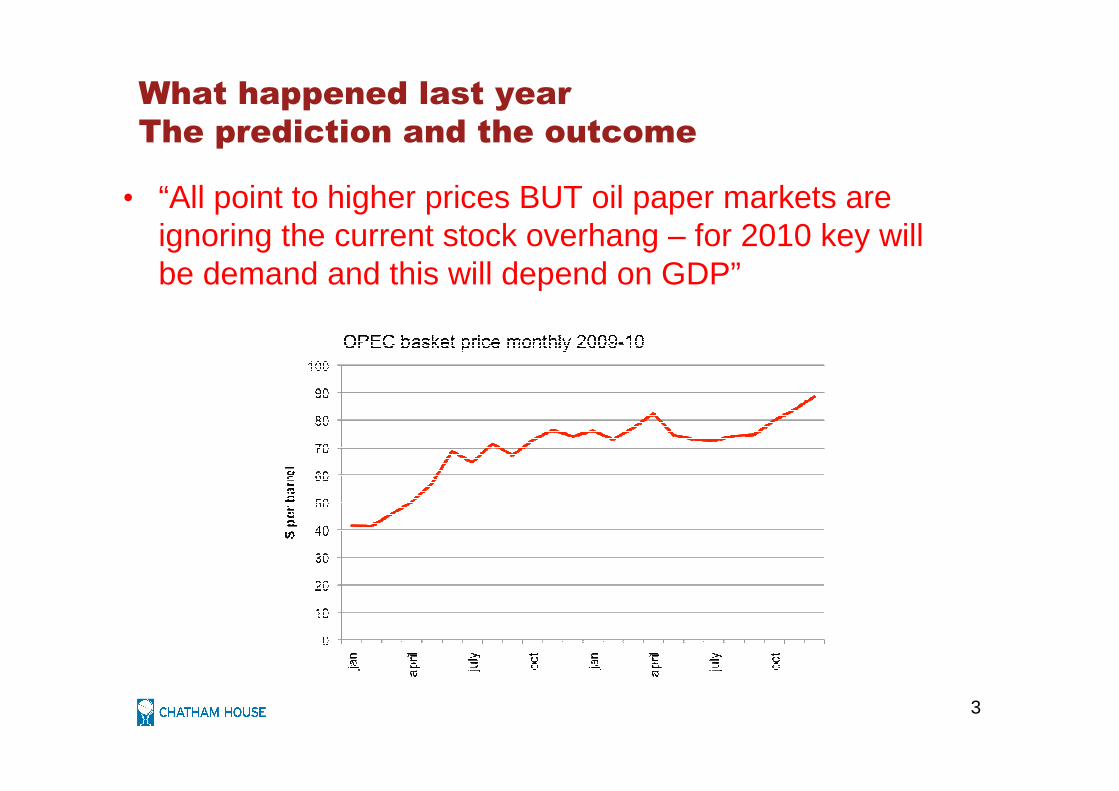

What happened last year

The prediction and the outcome

• “All point to higher prices BUT oil paper markets are ignoring the current stock overhang – for 2010 key will be demand and this will depend on GDP”

3

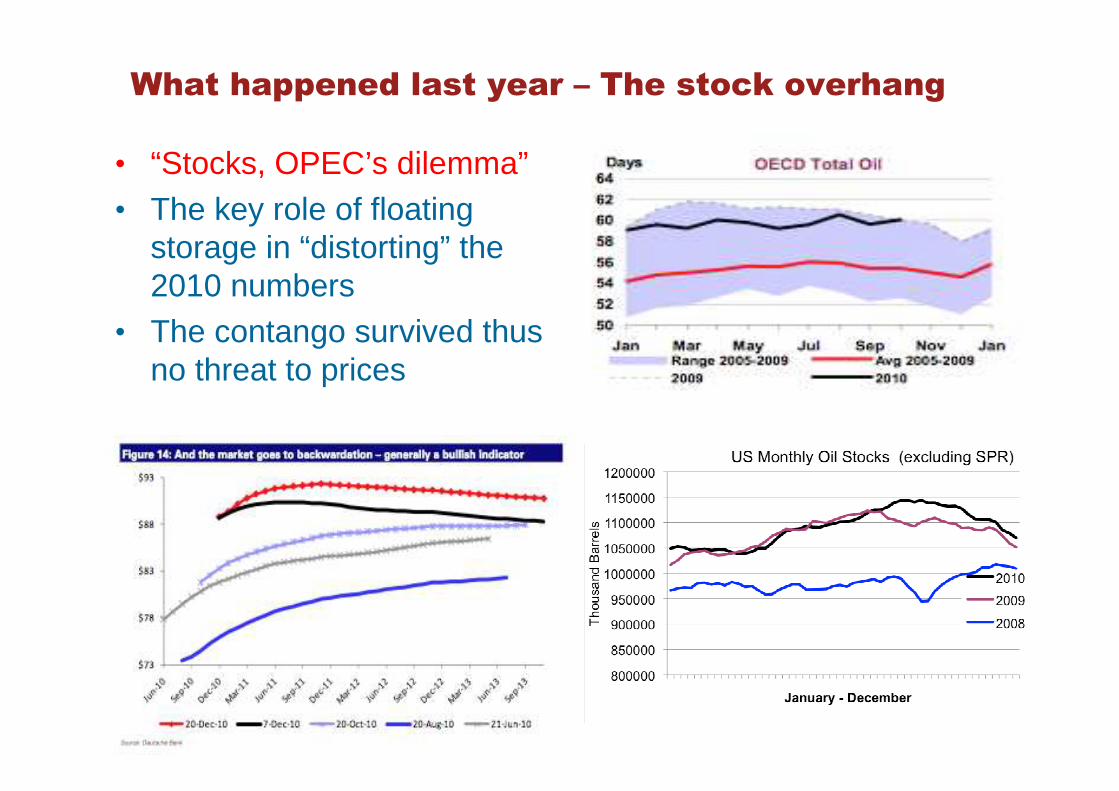

What happened last year – The stock overhang

• “Stocks, OPEC’s dilemma”• The key role of floating

storage in “distorting” the 2010 numbers

• The contango survived thus no threat to prices

4

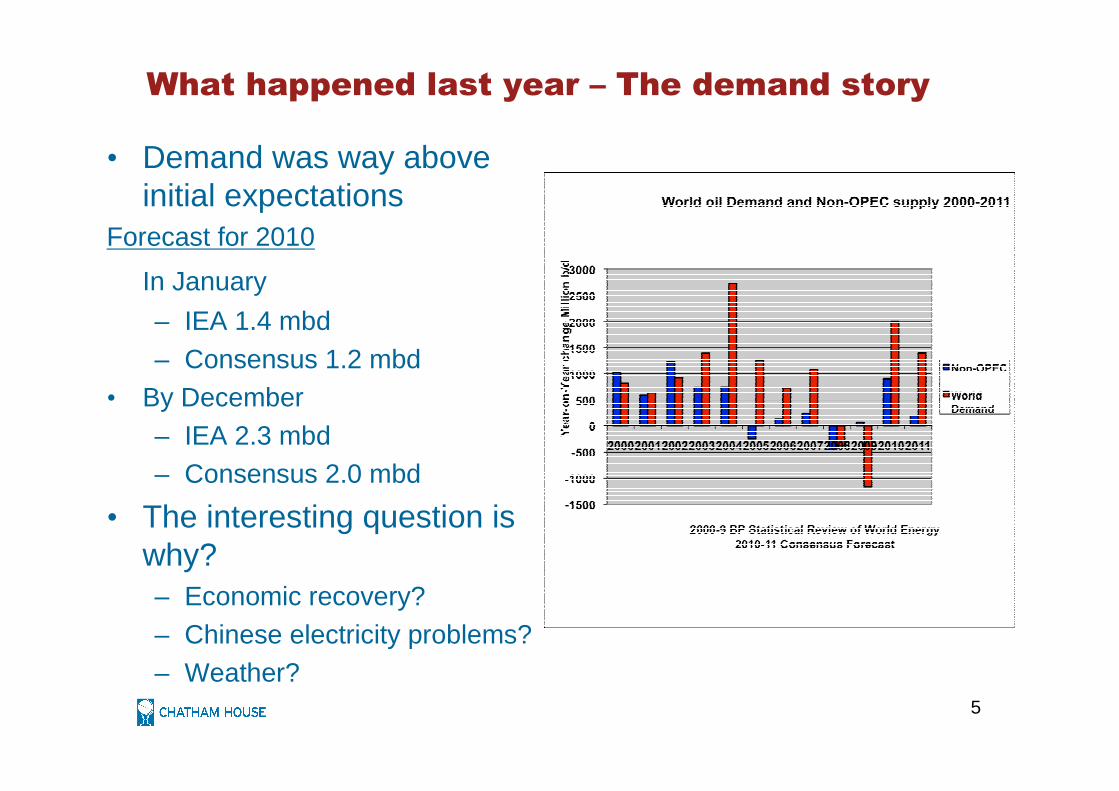

What happened last year – The demand story

• Demand was way above initial expectations

Forecast for 2010

In January

– IEA 1.4 mbd– Consensus 1.2 mbd

• By December– IEA 2.3 mbd– Consensus 2.0 mbd

• The interesting question is why?– Economic recovery?– Chinese electricity problems?– Weather?

5

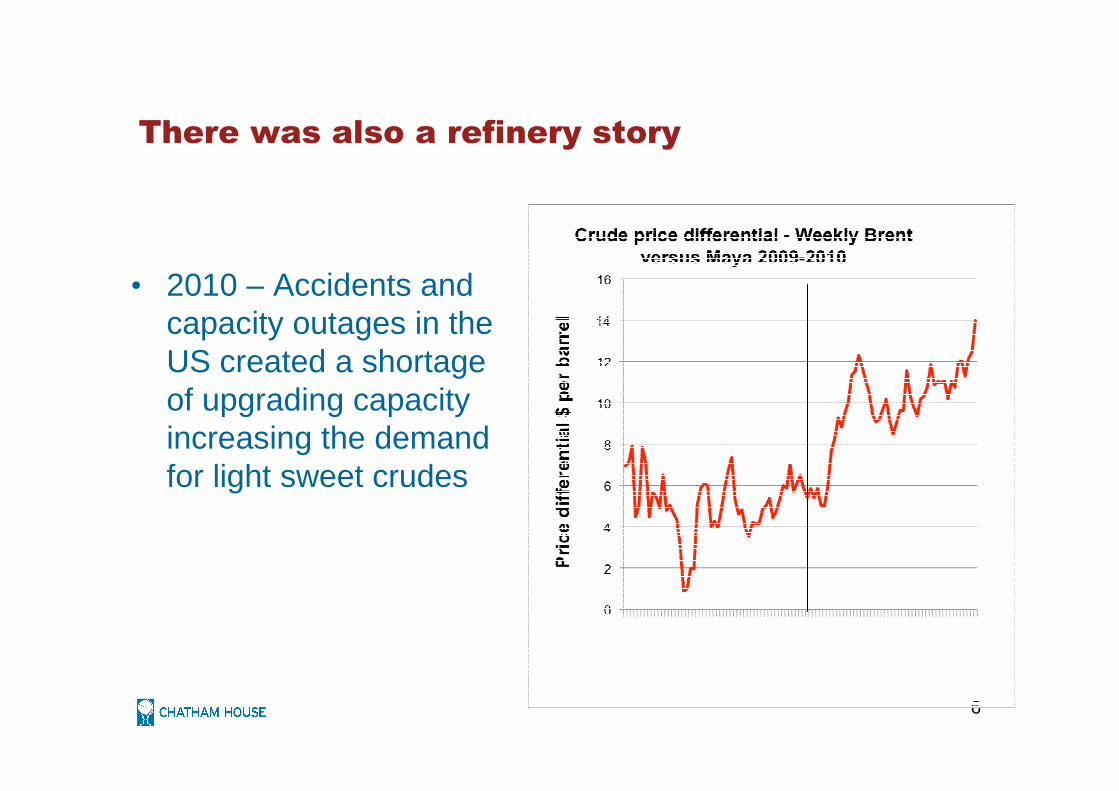

There was also a refinery story

• 2010 – Accidents and capacity outages in the US created a shortage of upgrading capacity increasing the demand for light sweet crudes

6

7

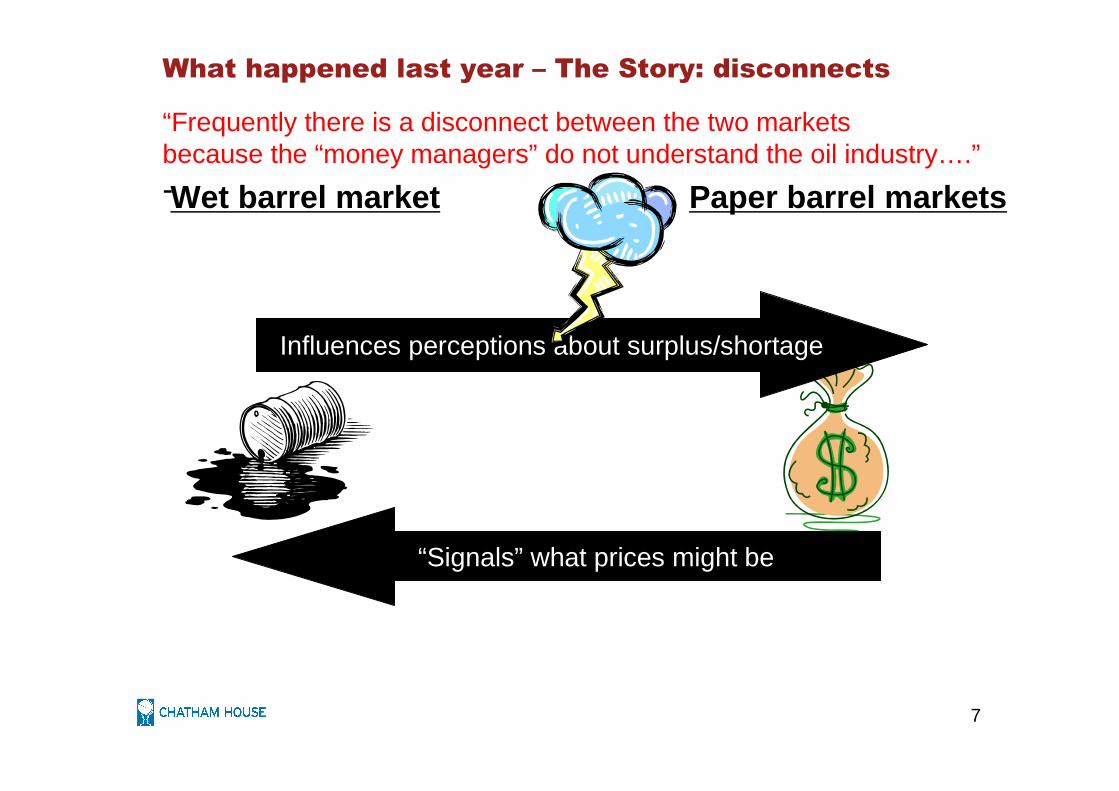

What happened last year – The Story: disconnects

Wet barrel market Paper barrel markets

Influences perceptions about surplus/shortage

“Signals” what prices might be

“Frequently there is a disconnect between the two marketsbecause the “money managers” do not understand the oil industry….”-

8

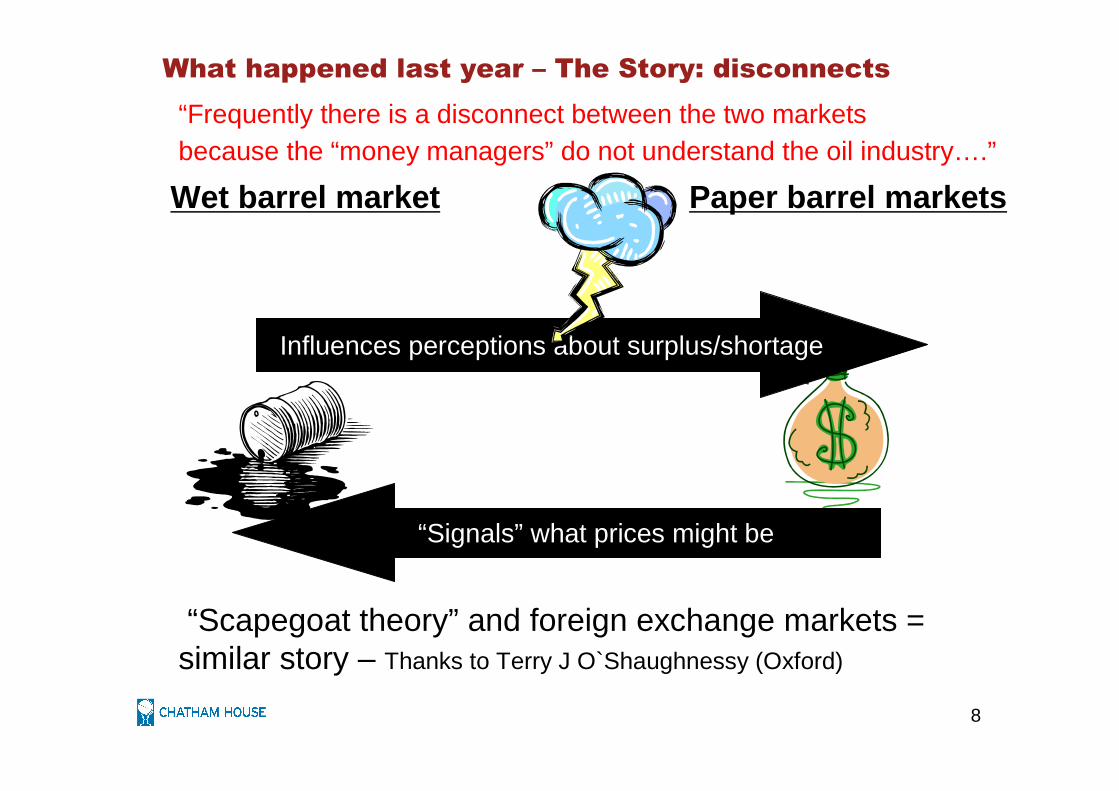

What happened last year – The Story: disconnects

Wet barrel market Paper barrel markets

Influences perceptions about surplus/shortage

“Signals” what prices might be

“Frequently there is a disconnect between the two marketsbecause the “money managers” do not understand the oil industry….”

“Scapegoat theory” and foreign exchange markets = similar story – Thanks to Terry J O`Shaughnessy (Oxford)

What happened last year – The Story: disconnects

• The paper markets seemed to ignore the continued stock overhang.

• Dollar exchange rate weaker dollar = higher oil prices.– April-November correlation between monthly $/Euro rate and

WTI Rsquared= -0.83

• S & P 500 – traditional strength before and after the US Mid-term elections.– Deutsch Bank claims 50 points up increases oil prices by $4.00

• Sentiment is very much towards higher prices in the future

9

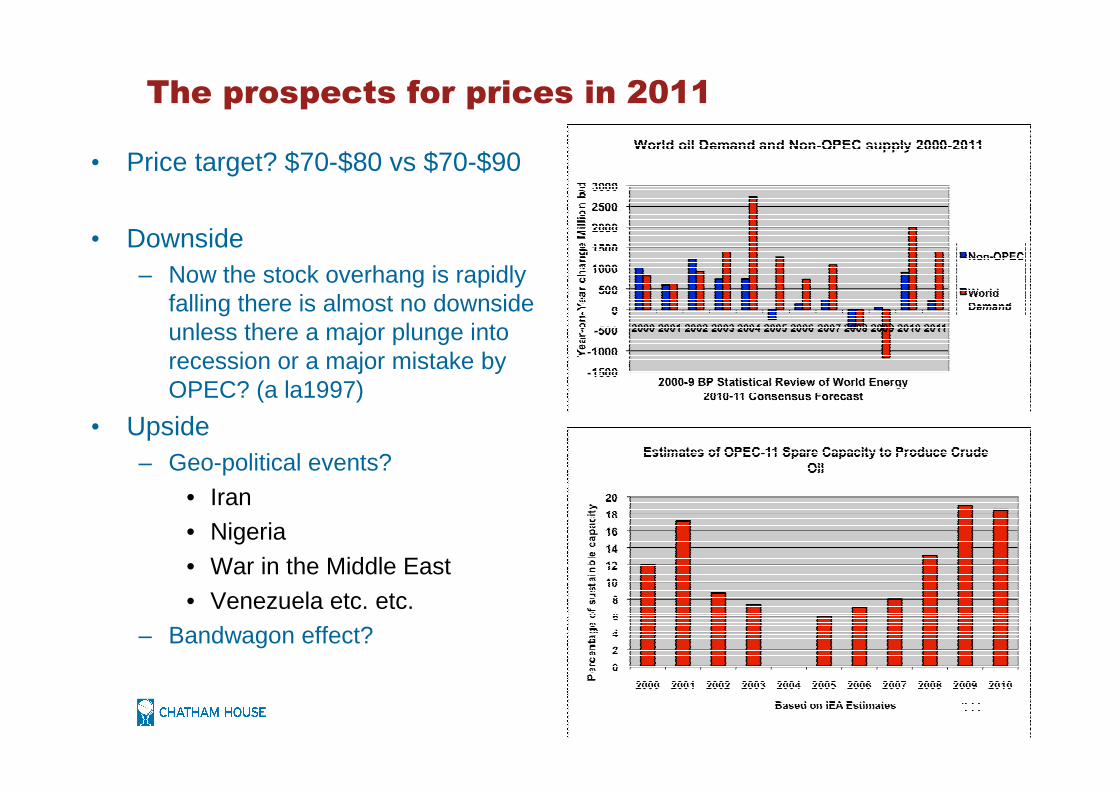

The prospects for prices in 2011

• Price target? $70-$80 vs $70-$90

• Downside– Now the stock overhang is rapidly

falling there is almost no downside unless there a major plunge into recession or a major mistake by OPEC? (a la1997)

• Upside– Geo-political events?

• Iran• Nigeria

• War in the Middle East

• Venezuela etc. etc.– Bandwagon effect?

10

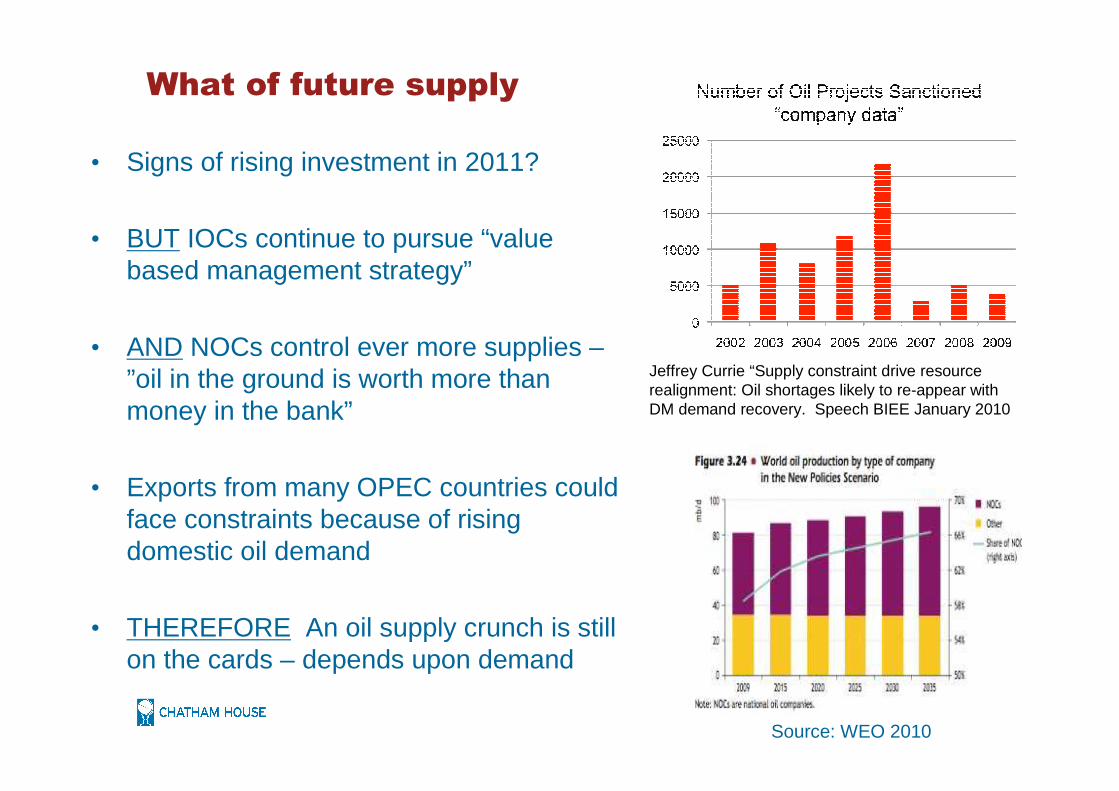

What of future supply

11

• Signs of rising investment in 2011?

• BUT IOCs continue to pursue “value based management strategy”

• AND NOCs control ever more supplies –”oil in the ground is worth more than money in the bank”

• Exports from many OPEC countries could face constraints because of rising domestic oil demand

• THEREFORE An oil supply crunch is still on the cards – depends upon demand

Jeffrey Currie “Supply constraint drive resource realignment: Oil shortages likely to re-appear with DM demand recovery. Speech BIEE January 2010

Source: WEO 2010

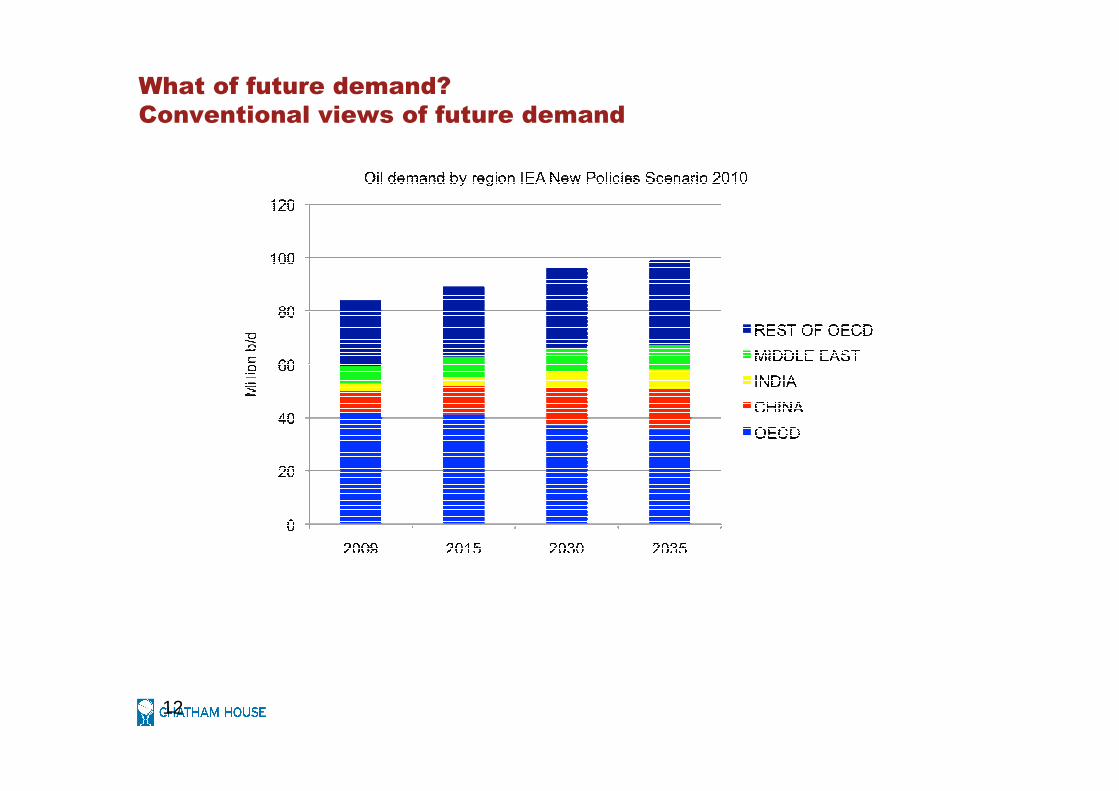

What of future demand?

Conventional views of future demand

12

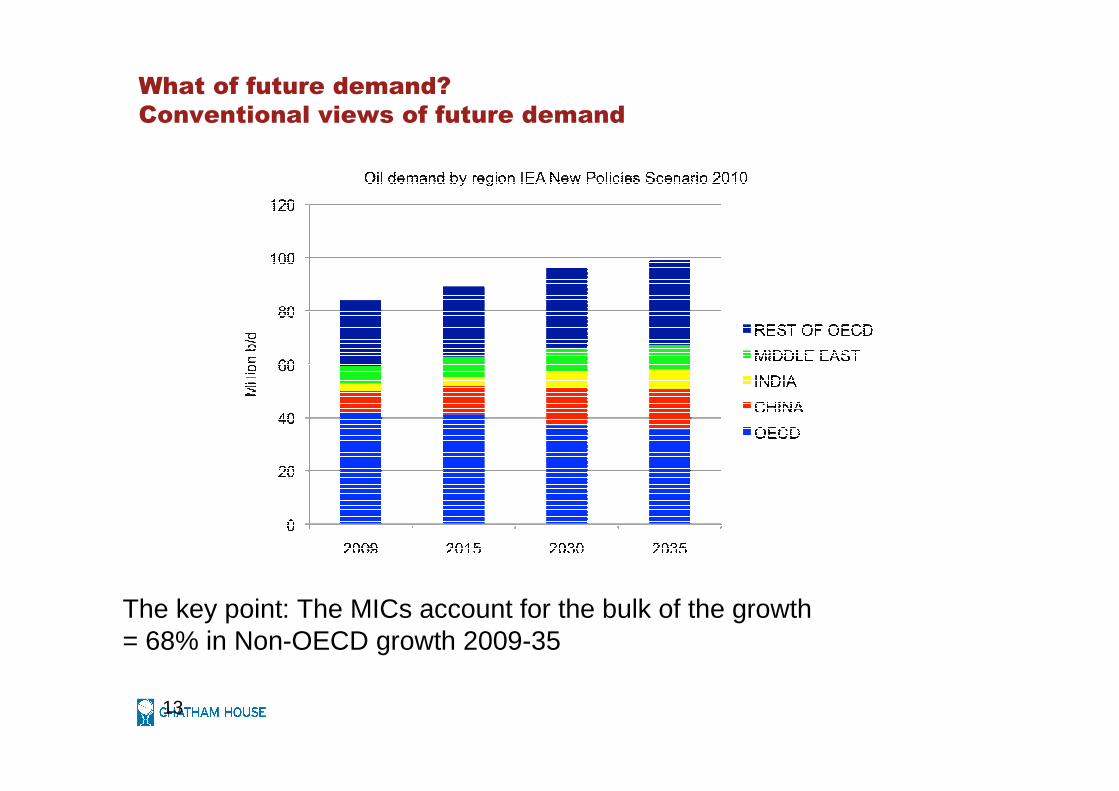

What of future demand?

Conventional views of future demand

13

The key point: The MICs account for the bulk of the growth = 68% in Non-OECD growth 2009-35

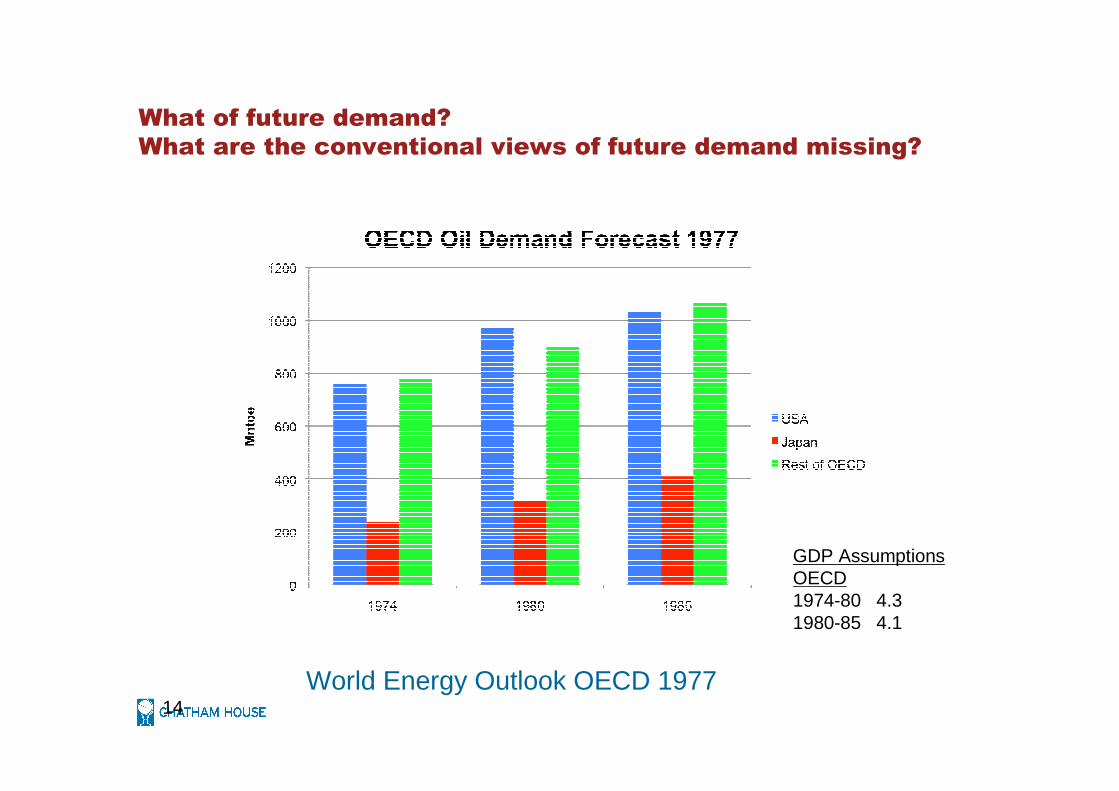

What of future demand?

What are the conventional views of future demand missing?

14World Energy Outlook OECD 1977

GDP Assumptions OECD1974-80 4.31980-85 4.1

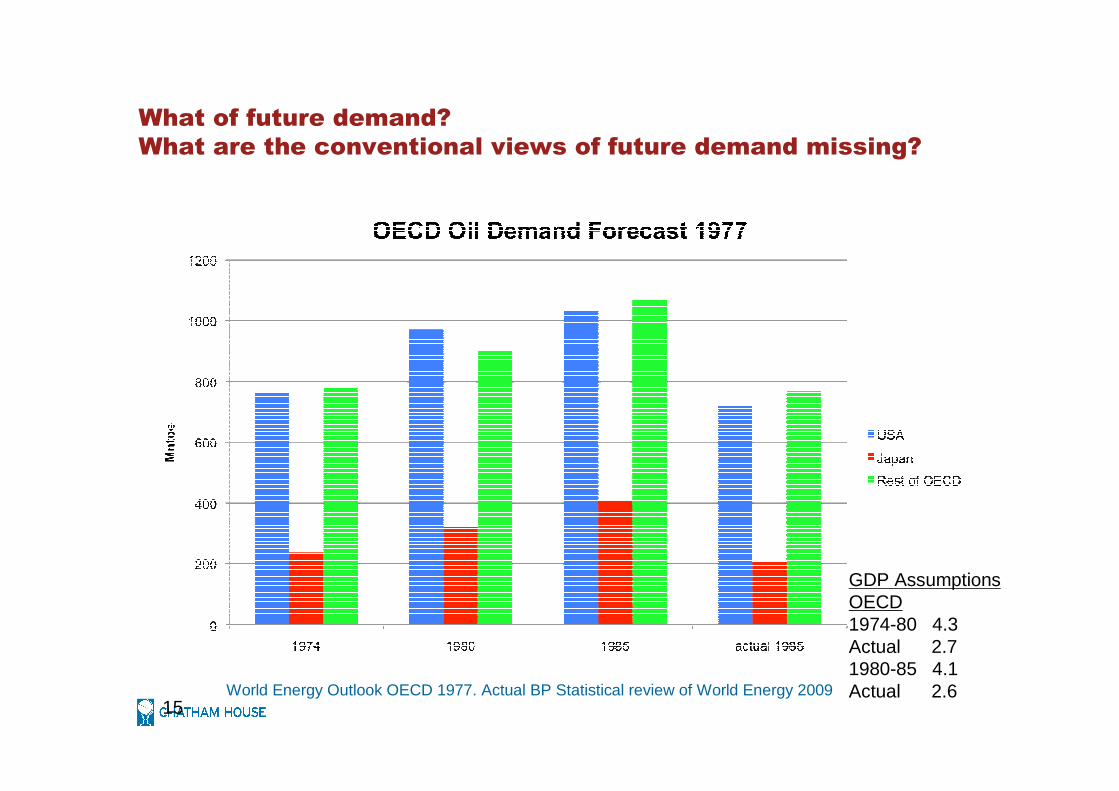

What of future demand?

What are the conventional views of future demand missing?

15World Energy Outlook OECD 1977. Actual BP Statistical review of World Energy 2009

GDP Assumptions OECD1974-80 4.3Actual 2.71980-85 4.1Actual 2.6

What of future demand?

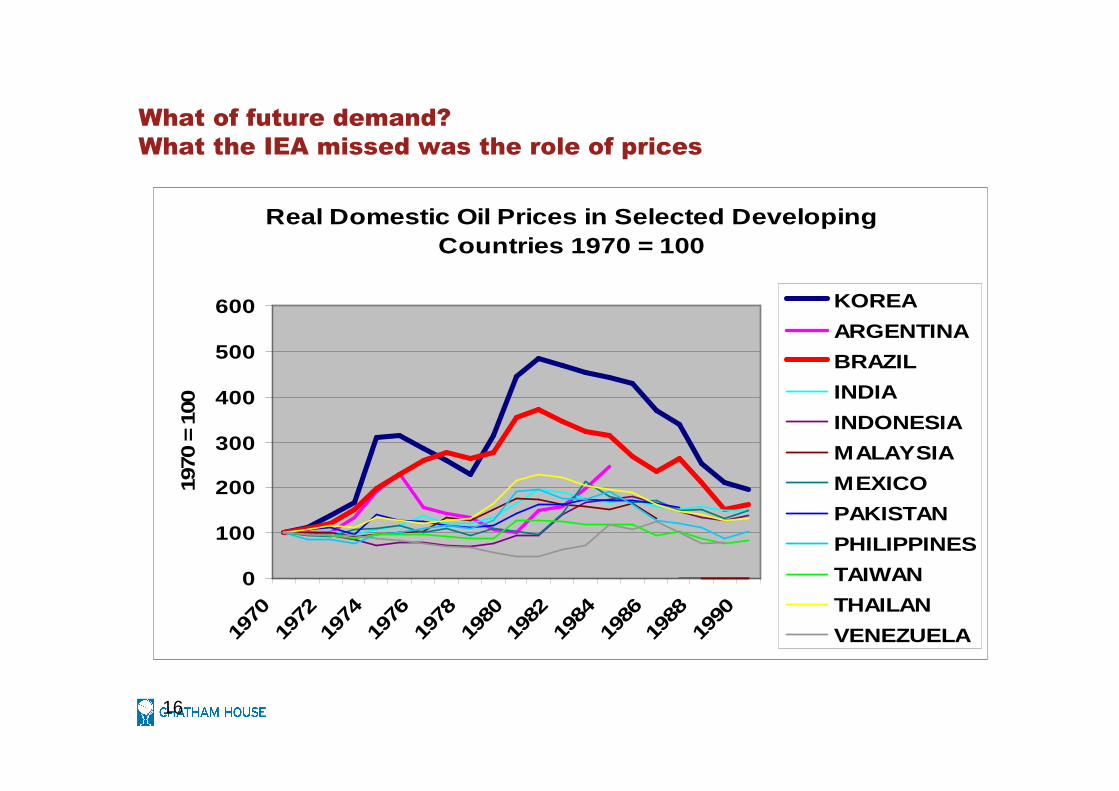

What the IEA missed was the role of prices

16

Real Domestic Oil Prices in Selected Developing Countries 1970 = 100

0

100

200

300

400

500

600

1970

19

72

1974

19

76

1978

19

80

1982

19

84

1986

19

88

1990

1970

= 1

00

KOREA

ARGENTINA

BRAZIL

INDIA

INDONESIA

MALAYSIA

MEXICO

PAKISTAN

PHILIPPINES

TAIWAN

THAILAN

VENEZUELA

What of future demand?

The effect of prices

17

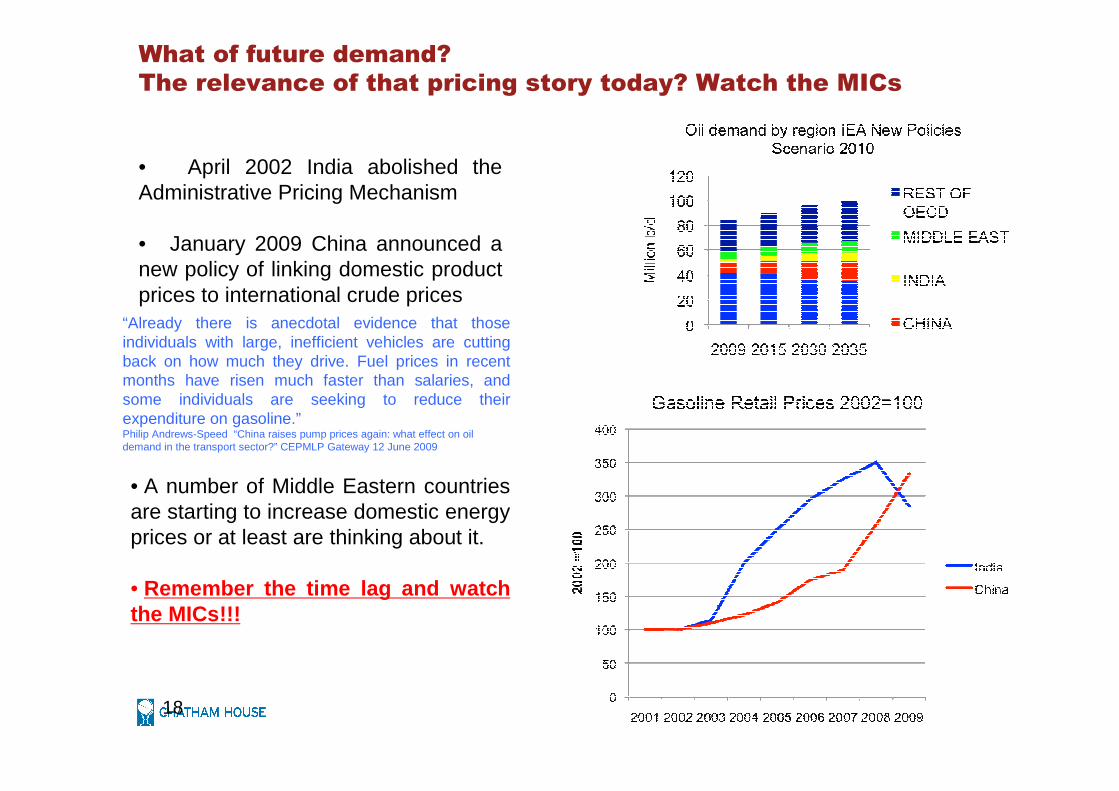

What of future demand?

The relevance of that pricing story today? Watch the MICs

18

• April 2002 India abolished the Administrative Pricing Mechanism

• January 2009 China announced a new policy of linking domestic product prices to international crude prices

“Already there is anecdotal evidence that those individuals with large, inefficient vehicles are cutting back on how much they drive. Fuel prices in recent months have risen much faster than salaries, and some individuals are seeking to reduce their expenditure on gasoline.”Philip Andrews-Speed “China raises pump prices again: what effect on oil demand in the transport sector?” CEPMLP Gateway 12 June 2009

• A number of Middle Eastern countries are starting to increase domestic energy prices or at least are thinking about it.

• Remember the time lag and watch the MICs!!!

THANK YOU FOR YOUR ATTENTION