proxy season review 2021 - glasslewis.com

TRANSCRIPT

Proxy Season Review 2021

Key Trends, Season Highlights, Statistics & Notable Meetings

www.glasslewis.com

Canada

Proxy Season Review 2021: Canada 2

Table of Contents About Glass Lewis ........................................................................................................ 4

Executive Summary ...................................................................................................... 5

Key Trends ..................................................................................................................... 7

Board & Governance ................................................................................................................................... 7

Executive Compensation ............................................................................................................................ 8

Season Highlights ......................................................................................................... 9

Governance .................................................................................................................................................. 9

Boards of Directors ..................................................................................................................................................9

Virtual Meetings .......................................................................................................................................................9

Market/Regulatory ...................................................................................................................................................9

Compensation ............................................................................................................................................ 10

All in it Together? .................................................................................................................................................. 10

EBITDAC (Earnings before interest, taxes, depreciation, amortization… …and coronavirus) ..................... 11

Between a Rock and a Hard Place ...................................................................................................................... 11

Executive Pay in the Age of the Meme Stock .................................................................................................... 12

Proxy Statistics ............................................................................................................ 13

Board Composition & Gender Diversity .................................................................................................. 13

Compensation ............................................................................................................................................ 19

Notable Meetings ....................................................................................................... 25

Election of Directors & Say-on-Pay........................................................................................................... 25

ESG & Shareholder Proposals .................................................................................................................. 28

Appendix A ................................................................................................................. 30

Appendix B .................................................................................................................. 35

Connect with Glass Lewis .......................................................................................... 39

Proxy Season Review 2021: Canada 3

Editors & Contributors

Oren Lida Paul McManus

Joanne O’Donnell Robert Richardson

Dimitri Zagoroff

Proxy Season Review 2021: Canada 4

About Glass Lewis Glass Lewis is the world’s choice for governance solutions. We enable institutional investors and publicly listed companies to make sustainable decisions based on research and data. We cover 30,000+ meetings each year, across approximately 100 global markets. Our team has been providing in-depth analysis of companies since 2003, relying solely on publicly available information to inform its policies, research, and voting recommendations.

Our customers include the majority of the world’s largest pension plans, mutual funds, and asset managers, collectively managing over $40 trillion in assets. We have teams located across the United States, Europe, and Asia-Pacific giving us global reach with a local perspective on the important governance issues.

Investors around the world depend on Glass Lewis’ Viewpoint platform to manage their proxy voting, policy implementation, recordkeeping, and reporting. Our industry leading Proxy Paper product provides comprehensive environmental, social, and governance research and voting recommendations weeks ahead of voting deadlines. Public companies can also use our innovative Report Feedback Statement to deliver their opinion on our proxy research directly to the voting decision makers at every investor client in time for voting decisions to be made or changed.

The research team engages extensively with public companies, investors, regulators, and other industry stakeholders to gain relevant context into the realities surrounding companies, sectors, and the market in general. This enables us to provide the most comprehensive and pragmatic insights to our customers.

Join the Conversation Glass Lewis is committed to ongoing engagement with all market participants.

[email protected] | www.glasslewis.com

Proxy Season Review 2021: Canada 5

Executive Summary Dear clients, customers and shareholders, In our 2020 Proxy Season Review we described how the global pandemic had a huge impact on all aspects of life around the world, and proxy voting, for the most part, was no exception. In 2021, the pandemic has roared on, thus far, and has continued to have an impact on proxy voting, particularly through continuing restrictions on in-person gatherings such as shareholder meetings. Canada, already having a regulatory infrastructure for hosting virtual-only meetings in pre-pandemic times, saw an increasing number of issuers come to terms with the virtual-only format. In fact, approximately 89% of companies listed on the S&P/TSX Composite Index chose to hold annual meetings by virtual-only means, up from 76% in 2020. A number of catastrophic weather events in 2021, coupled with the ever-growing threat of climate change, has seen companies continue to face more frequent and detailed proposals regarding climate risk management. It is becoming a necessity for companies to disclose what actions they are taking in order to offset the impact their operations are having on the environment. Say on climate proposals, which offer shareholders an opportunity to voice opinions on companies’ climate plans are becoming more and more prevalent. Apart from the impact of COVID-19 and climate change driven discussions and proposals, Proxy Season 2021 saw a focus on executive compensation, board composition and diversity. While director elections continue to receive a high level of support in Canadian public companies, less leniency was granted in comparison to 2020 when it came to support for companies’ executive compensation programs. With shareholders now able to view 2020 in its totality and with the benefit of hindsight, those who had been expecting boards to have enforced a steep reduction in payouts will be left disappointed. With more Canadian public companies failing their say-on-pay votes than in any other year – most of those at companies that made in-flight award adjustments – it appears that shareholders were willing to voice forceful scepticism at boards’ abilities to rebuff management awards. The representation of women and minorities in the board room and in management leadership positions has continued to slowly increase over the past three years. Interest is being shown not only for diversity in terms of gender or the presence of minorities, but also in terms of the level of diversity of board members’ skillsets. The disclosure of board member skills continues to rise year on year as investor interest in how exactly the company is being run by the individuals in control grows. Investors wish to see a diverse mix of skills in the board room so as to enable the board to have the capabilities of dealing with the wide range of issues which present themselves to public companies. Engagement with public companies is a continued focus for Glass Lewis. This year, over 1,850 global companies used our Issuer Data Report to verify the accuracy of our data, and over 1,000 companies provided their updated list of self-disclosed peers for inclusion in our Glass Lewis peer group methodology. And more companies are taking advantage of our innovative Report Feedback Statement service. Already this year, over 100 companies have included their unedited perspectives alongside the Glass Lewis research.

Proxy Season Review 2021: Canada 6

We now turn our attention to off-season engagement and enhancements to our policies and Proxy Papers. This year, we are targeting engagement on a range of ESG topics, including board diversity, climate, human capital, executive compensation, and responsiveness. We look forward to constructive dialogue about these topics. If you have any comments or feedback regarding this review, please get in touch. Kind Regards,

Rob Richardson Director, Americas (Ex-US) and Shared Services

Proxy Season Review 2021: Canada 7

Key Trends

Board & Governance • 2021 saw shareholders vote on a range of board decisions made in response to the COVID-19 pandemic,

ranging from those made in the heat of the moment to final award decisions taken by boards in early 2021 on the basis of full-year results.

o Shareholders appeared to have broadly given issuers the benefit of the doubt in 2020, with no say-on-pay fails and a rise in support rates. Support levels have dropped substantially in 2021 meetings, with a number of shareholder revolts focused on executive compensation.

• Two directors failed to receive a majority of votes cast, up from one the prior year. Of these, one

director has left the board and the other has committed to reduce their external board commitments, thought to be the main reason behind the high withhold vote.

o Overall shareholder support for director elections was consistent with prior years. Less than 5% of nominees received less than 80% support, and nearly nine out of ten received over 90% support.

• Slowly but surely, women continue to occupy more board and management leadership positions. The

pace is nonetheless slow, with women making up just less than a quarter of TSX board positions in 2021, and only 5% of CEOs.

o There’s a clear difference between large- and mid-cap behaviour and that of smaller-cap companies. In the TSX Composite, just one board (less than 1% of total) is all-male, compared to 22% of non-index companies.

• This is the second year that companies incorporated federally under the Canada Business Corporations

Act (CBCA) have been required to report on the inclusion of “designated groups” on the board and senior management.

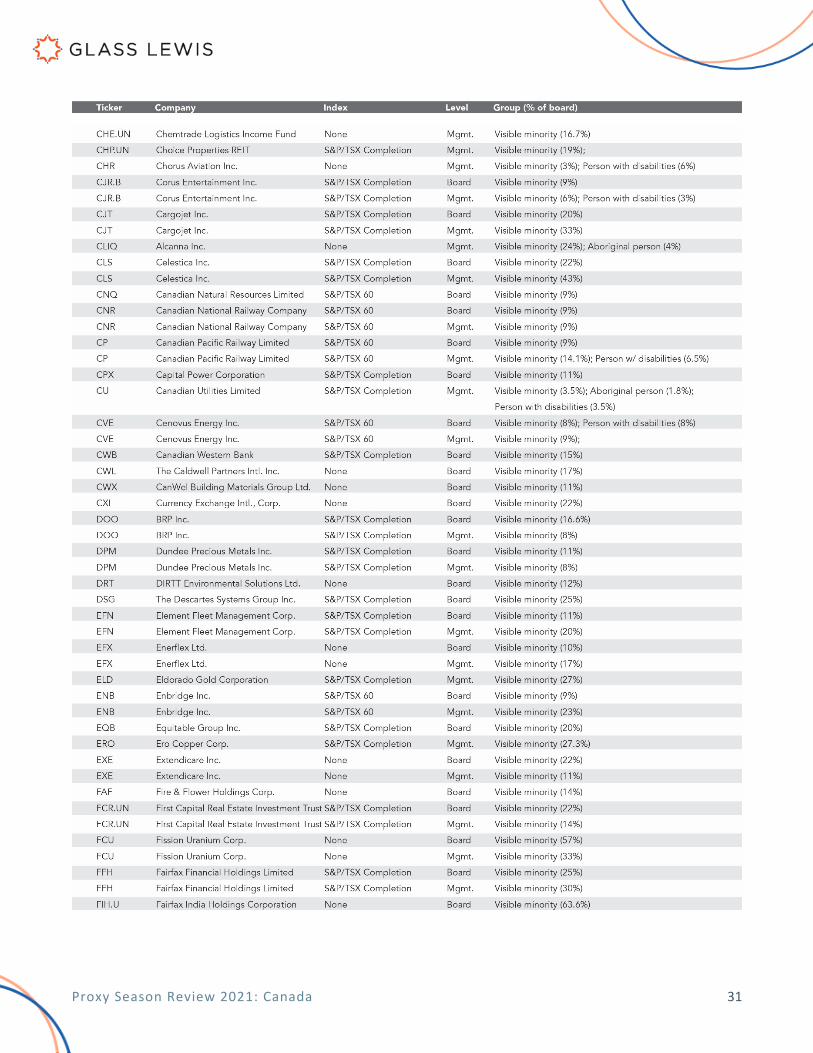

o The term “designated groups” takes its meaning from the federal Employment Equity Act, and includes women, Aboriginal peoples, persons with disabilities and members of visible minorities. For a full company-by-company breakdown of board and management-level diversity, see Appendix A.

• Disclosure of board skills rose in the past year, with just under half of all covered TSX issuers now

including a skills matrix. o One company justified rejecting the resignation of a director who failed to get elected by way of

referencing their importance to the overall skills configuration of the board, illustrating the importance of ensuring that information pertaining to the spread of competencies is not kept in a black box from shareholders.

Proxy Season Review 2021: Canada 8

Executive Compensation • After companies breezed through their compensation votes held during a chaotic 2020 –when zero say-

on-pay fails were recorded -- pay opposition rebounded back to pre-pandemic levels, with a record six issuers failing to receive a majority of votes in favor.

o The lowest result recorded was RioCan’s 24% support, while BlackBerry only narrowly missed joining the fail club due to the substantial voting power of the largest shareholder – who also happens to be chair of the compensation committee.

• The past year saw a notable decrease in the number of S&P/TSX 60 issuers utilizing single trigger change

in control benefits, now down to less than one in ten. o There was also a significant increase in the number of non-index companies utilizing clawback,

up to 88% of total from 68% in 2020.

Proxy Season Review 2021: Canada 9

Season Highlights Governance Boards of Directors

While the composition of boards is slowly changing – becoming more diverse across a number of measures – the practice of electing directors is much the same as in past years. Hardly any directors failed to get elected, and for the 11.5% of nominees who got less than 90% support, the reasons were largely consistent with past years. Specific concerns thrown up by the pandemic were far more likely to be expressed under compensation or shareholder proponent proposals.

Virtual Meetings

As far as actually holding the meeting goes, more issuers got to grips with convening a successful virtual-only event, as local restrictions on gatherings remained in place.

Percentage of Companies that Held Virtual-Only Meetings

Market/Regulatory

The pandemic appears to have put the brakes on efforts by Canadian legislators and regulators to bring about widespread adoption of certain governance cornerstones. The Government of Ontario and the federal government (through the CBCA) both have bills in the pipeline that would, among other things, mandate TSX

Proxy Season Review 2021: Canada 10

issuers to disclose fuller diversity data, hold annual say-on-pay votes, and adopt a true majority standard for election of directors.

Compensation “Canadian issuers do not tend to face very many shareholder revolts over pay”

This was how we opened our discussion of compensation in our review of proxy season 2020; after the first half of 2021, we might revise our expectations.

The six say-on-pay fails recorded in the first six months of the year is a significant uptick – the most ever in a single Canadian proxy season – bringing the rate of outright shareholder opposition up to typical U.S. proportions (where around 3% of all say-on-pay votes fail annually).

Last year, we speculated that the nascent impact of COVID-19 on business conditions might be leading shareholders to give boards the benefit of the doubt, cautiously supporting ballot items in the interests of freeing them to navigate the unprecedented conditions without the extra headache of appeasing shareholders. Moreover, in 2020, companies were primarily reporting on 2019 compensation, with only a nod towards 2021 plans – usually provisional decisions whose optics played well, such as executives voluntarily giving up salaries and cautious but unrevealing estimates as to how COVID might impact bonus plans. Boards were given a relatively clear runway to plot a course through 2021. It was always likely that when shareholders and the wider public were presented with complete information, there’d be controversy.

A full year later, and with all companies having disclosed not just provisional adjustments but the full picture of how final full-year results fed into final executive payouts, shareholders have been less forgiving. The average support levels for say-on-pay proposals fell back from the high enjoyed in 2020. Yet the overall proportion of say-on-pays that received less than 75% support actually fell too. So it’s not that more companies were being shown a yellow card and that this inevitably led to more reds for the outliers. Rather, it appears that voting shareholders agreed – in significant enough numbers to make an impact – which specific companies were those outliers who deserved to be called out.

All in it Together?

Since disclosure of senior management compensation became mandatory and has gradually grown in scale and complexity, executive pay has been a hot-button and polarising issue. High payouts are often referenced as evidence of steeply widening inequality in society.

It can be easy to score a quick headline out of particularly large sums reported by public companies, especially when the firm or its CEO are (in)famous. A lot of factors can underlie the reported figures, particularly in North America, where the largest grants are in the form of “long-term incentive” (LTI) or equity, reported at “grant-date” valuations and contingent on stock price performance, not typically intended or permitted to be realized for a number of years. With annual grants the norm, past grants may easily fade out of mind even as they continue to vest or be performance-assessed in subsequent years.

North American market participants are slowly coming around to the importance of ‘realized’ payouts, or in other words, the actual take-home pay deriving from salary, bonus and vesting LTI (which will usually have been

Proxy Season Review 2021: Canada 11

awarded 3-4 years back). Nonetheless, it’s easy to be distracted by the headline new grant amounts. If an annual grant of $5m is only worth $1m when it finally vests, that may be a pretty fair reflection of performance.

The onset of the pandemic provided a unique opportunity to test the extent to which final vesting outcomes depart from grant-date levels. While each company’s experience was different and there are some fascinating outliers, the broad-brush picture is that on average, 2020 payouts were largely in line with previous years across all categories of compensation (salary, short- and long-term). Put another way, if you were a Martian looking at the three-year average charts, and you knew a once-in-a-century pandemic had shattered financial assumptions in one of those years across almost all industries, you’d struggle to identify the year.

EBITDAC (Earnings before interest, taxes, depreciation, amortization … and coronavirus)

With the pandemic a known quantity for most companies by the time they set annual grants for the current fiscal year, most did not need to actively intervene in annual bonus plans.

Indeed, given the choice, companies would have been well-advised to set lower targets at the outset of the 2020 performance cycle, which would necessitate less intervention that might come under scrutiny as “in-flight” adjustment or upward discretion. We noted just under half of companies reporting a specific change to compensation plans resulting from COVID. This might understate matters, since it’s impossible to imagine any board could discuss compensation in the last year and a half without acknowledging the pandemic.

We have collated a list of the most noteworthy adjustments relating to COVID as disclosed in the 2021 management information circulars.

Of the 16 Canadian issuers that received less than 75% support for their pay schemes, nine had made significant interventions into their incentive plans to explicitly adjust or account for the pandemic. This indicates that, while pandemic pay was not the only concern for shareholders voting against say-on-pays, boards that played with targets or adjusted payouts, or bypassed the need through supplementary “one-time” grants, were more at risk of drawing shareholder ire.

Between a Rock and a Hard Place

Certain companies, by virtue of their industry, were always going to have a tougher time navigating the pandemic – not just surviving as a business, but dealing with extra-intensive public oversight and comment on their decisions. This was especially true of companies providing healthcare services, airlines, and any business dependent on stable crude oil prices. Any and every compensation decision in such a year was likely to be scrutinized closely not just by investors, but by the workforce and unions, the media and the wider public. And yet, as their boards would doubtless argue, these companies faced just as many talent and retention issues as others, if not more given the stresses unique to their line of work.

Like many public long-term care home operators, Sienna Senior Living, Chartwell Retirement Residences and Extendicare were significantly affected by the virus. Unlike many companies, their job was not just to survive the pandemic, but to play a crucial role in fighting it, by protecting their customers and employees – an especially vulnerable and at-risk constituency – from catastrophe.

Proxy Season Review 2021: Canada 12

Operating retirement homes, many of which were devastated by the uncontrolled spread of the disease, presented unique and sensitive challenges. Elderly and vulnerable patients had to be shielded, and staff who came into regular contact with medical cases and carriers of the disease inevitably suffered higher rates of infection and sickness, exacerbating carer shortages in a role already severely understaffed. At the midway point of 2020, approximately 80% of the country’s COVID-related deaths had taken place in such homes.

In the most extreme cases, the Canadian armed forces needed to be deployed to avert an even greater catastrophe. Statistics circulated evaluating the ‘performance’ of the various care and retirement home operators in terms of mortality rates of customers. The data did not show the for-profit care home operators in a flattering light. By end of 2020, 21 retirement residences and 10 long-term care homes operated by Chartwell had been declared by public health officials to be in a COVID-19 outbreak.

Over in airlines, meanwhile, Air Canada needed a government bailout, the terms of which will severely limit the executive pay they can offer in the forthcoming years. Perhaps tempted to leave management a souvenir of the good times, they made a series of one-off grants designed to effectively nullify the salary and bonus plan cuts made in the previous year. Politicians and labor groups immediately weighed in and most of the most senior officers walked back their grants.

Executive Pay in the Age of the Meme Stock

One new phenomenon that investors in public markets have had to get used to over the past year is the concept of ‘meme’ stocks: the sudden retail-driven share price explosions in January 2021 affecting certain publicly traded brands with a household but nostalgic feel to them, most famously GameStop, but also AMC, Nokia and others. While it was mostly U.S. stocks that got swept up in this trend, Canada’s BlackBerry, which dual-trades on the TSX and NYSE, also became a target for the retail investors who shared tips and coordinated stock purchases on social media platforms such as Reddit.

The result for the targets was extremely volatile trading patterns wholly unrelated to any business updates or events disclosed by the companies themselves. And for the executives of some of those companies, this volatility had a lucrative impact on their compensation. In particular, the trading yielded several substantial payouts from incentive plans based around “rolling” share price hurdles.

Glass Lewis typically warns shareholders about “rolling” share price hurdles that can be achieved over a matter of days at any point during a multi-year window, as these have the potential to enable windfalls for brief spikes in share performance, as well as effectively offering an ongoing performance “retesting” mechanism to management. These windows are generally based around 30-day average weighted share price – but in some cases they can be set to 10 days, or even shorter depending on how they are structured – see our discussion of BlackBerry’s 2021 AGM in the “Contentious Meetings” section for further discussion.

It would be difficult to conceive of a better illustration of the risk that factors wildly outside the influence of managers can enable excessive and undue windfalls when such narrow performance targets and measurement windows are selected for a metric subject to extreme short-term volatility.

Far from incentivizing longer service from a valued executive, dubious windfalls such as these may end up undermining the retentive value – the stock has hit some of heights it was supposed to, but not for long, and not for the ‘right’ reasons.

Proxy Season Review 2021: Canada 13

Proxy Statistics

Board Composition & Gender Diversity

Key Findings

• In the 2nd year of wider diversity disclosure, more companies have added minorities to boards and management of TSX issuers.

• The proportion of women on boards and in senior leadership positions has increased in each of the past three years. Still, women are a tiny portion of CEOs, chairs, and lead directors.

• Recommendations against nominees on the basis of lack of gender diversity rose to 14% of all negative recommendations.

What Proportion of the Board are Women?

The only S&P/TSX Composite index member to have zero women on the board was Village Farms International (VFF).

Proxy Season Review 2021: Canada 14

Board Gender (Im)Balance

There is a slow trend towards gender parity on boards, while an ever-smaller proportion of overall TSX companies have all-male boards – most of these non-index constituents. Women make up just over 1/3 of new appointees.

Women in Board Leadership Positions

Proxy Season Review 2021: Canada 15

Women continue to occupy growing proportions of board and management leadership positions. In this area too, there’s a clear difference between large- and mid-cap behaviour and that of smaller-cap companies.

Women in Senior Management Positions

Proxy Season Review 2021: Canada 16

Board-Level Additional Diversity

Management-Level Additional Diversity

Proxy Season Review 2021: Canada 17

E&S Oversight in 2021

Beginning 2022, Glass Lewis will be recommending against S&P/TSX 60 companies that do not provide clear disclosure concerning the board-level oversight afforded to environmental and/or social issues.

Proxy Season Review 2021: Canada 18

Main Drivers of Glass Lewis Recommendations Against Directors

Proxy Season Review 2021: Canada 19

Compensation

Key Findings • Opposition to say-on-pay proposals rebounded after a forgiving 2020, with a record six say-on-pay failures. • No equity compensation plans failed to receive majority support, despite a couple of close shaves. • Concerning decisions made in response to COVID-19 were the primary driver for almost 30% of Glass Lewis’

against recommendations.

Say-on-Pay (SOP) Overview

2019 2020 2021

Canadian SOPs Covered 203 200 214 Failed 2 0 6

Total Below 75% Support 18 8 16 % Below 75% Support 8.7% 4.0% 7.5%

Average Shareholder Support 90.3% 93.1% 91.3% Glass Lewis Against Rate 11.8% 11.5% 12.1%

Equity Plan Overview

2019 2020 2021

Average Shareholder Support 85.6% 90.1% 87.5% Glass Lewis Against Rate 18.1% 16.9% 21.0%

Number of Failed Proposals 3 (1.6%)

0 0

Number with 25%-50% Opposition 28 (15.8%)

18 (8.7%)

28 (13.7%)

COVID-19 Breakdown

• Nearly half of Canadian companies amended executive compensation due to COVID (46%) o Of these, only around 10% effected an overall pay reduction. 90% of the revisions resulted in an overall

higher pay outcome, usually through upward adjustment of bonus targets or use of “one-time” replacement awards.

o More total companies increased STI outcomes (30% of total) than LTI outcomes (9%) • Companies that amended either STI or LTI outcomes got 91% support on average, but • The roughly 6% of companies that amended both STI and LTI outcomes averaged just 75% support

Proxy Season Review 2021: Canada 20

COVID Pay Adjustments + Low Shareholder Support

While all of the companies above made COVID-related adjustments and saw low shareholder support on their Say-on-Pay, the two aren’t necessarily connected. In particular, COVID-related adjustments at Chemtrade and Blackberry were relatively minor, and opposition likely reflected other factors.

Components Adjusted

Primary Action Adjustments made Final payouts in relation to stated targets

Vote Result

RioCan STI & LTI Upward discretion & exclusion of pandemic perf. period

STI: Metric eliminated and maximum opportunity reduced LTI: PSU cycle split into unadjusted pre-pandemic and pandemic with reduced hurdles

STI: below original target, at maximum revised opportunity LTI 2020 vesting cycle: below original target

24.1%

Chemtrade STI No disclosed in-flight adjustments Delayed setting targets until May 2020

STI: Above target LTI: 0%

40.1%

Gildan Activewear

STI, LTI & One-time

Upward discretion/revised targets down

STI: Replaced perf. Targets with discretionary quantitative and qualitative targets One-time: Substantial equity grants to NEOs

STI: At target LTI: 0%

40.9%

BlackBerry Limited

STI & LTI Upward discretion/revised targets down

STI: Enhanced discretionary authority. LTI: Adjusted 2021 PSU targets of other NEOs.

STI: Guaranteed bonus for CEO; below target for other NEOs LTI: 3/5 Extension PSU tranches vested (see Contentious Meetings); below target for other NEOs

58.8%

NuVista Energy Ltd.

STI Upward discretion/revised targets down

Inappropriate metrics removed STI & LTI: Below target 66.7%

Chartwell Retirement Residences

STI Upward discretion & exclusion of pandemic perf. period

STI: split 2020 perf. Period and reduced targets for period after March 15; scored 100% on customer service and reputation management.

STI & LTI: Below target 69.5%

Air Canada STI, LTI & One-time

Upward discretion & exclusion of pandemic perf. period

STI: replaced by discretionary plan. LTI: 2020 performance year cancelled for past cycles and award size reduced proportionately One-time: SARs issued but then cancelled for NEOs

Replacement STI: 60% of original target for CEO LTI: Below target

71.3%

Cineplex Inc. STI, LTI & One-time

One-time/ Replacement awards

Buyout of underwater options STI: 0% LTI: Below target

72.5%

Proxy Season Review 2021: Canada 21

Main Drivers of Glass Lewis SOP Against Recommendations

Glass Lewis Pay for Performance Grade Distribution

Proxy Season Review 2021: Canada 22

Total CEO Compensation in S&P/TSX 60

The impact of COVID-19 on final pay outcomes for Canada’s highest earners, as suggested from realized pay averages, was limited.

That said, the higher rate of companies in the 25%+ shareholder opposition range, including the six say-on-pay fails, indicates that shareholders were focusing their ire on the companies with the least convincing explanations for pandemic pay decisions.

S&P/TSX Composite Average Total Granted vs. Realised Compensation

Proxy Season Review 2021: Canada 23

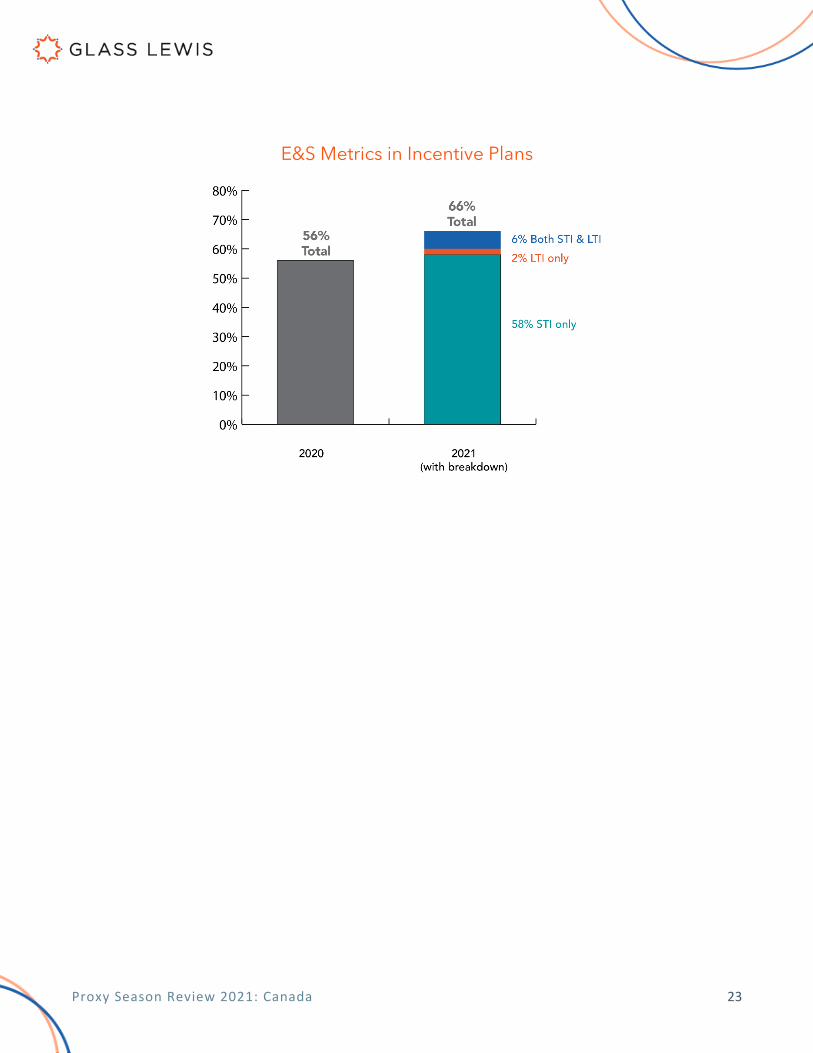

E&S Metrics in Incentive Plans

Proxy Season Review 2021: Canada 24

Full List of Say-on-Pay Proposals with Notable Shareholder Opposition

Ticker Company Sector Index Support GL Rec Reason if Against

Prior Year Result

REI.UN

RioCan Real Estate Investment Trust Real Estate S&P/TSX Completion 24% Against

Poorly justified adjustments relating to COVID-19 79%

CIX CI Financial Corp. Financials S&P/TSX Completion 38% Against

Insufficient response to shareholder dissent 73%

CHE.UN

Chemtrade Logistics Income Fund Materials No index 40% For 82%

GIL

Gildan Activewear Inc.

Consumer Discretionary S&P/TSX 60 41% Against Excessive grants 96%

VET Vermilion Energy Inc. Energy S&P/TSX Completion 42% For 65%

PD

Precision Drilling Corporation Energy No index 42% Against

Insufficient response to shareholder dissent 78%

BB BlackBerry Limited

Information Technology S&P/TSX Completion 59% Against

Concerning pay practices 94%

BNS The Bank of Nova Scotia Financials S&P/TSX 60 61% For 94%

NVA NuVista Energy Ltd. Energy No index 67% For 99%

CSH.UN

Chartwell Retirement Residences Health Care S&P/TSX Completion 69% Against

Poorly justified adjustments relating to COVID-19 82%

AC Air Canada Industrials S&P/TSX Completion 71% For 95%

OBE Obsidian Energy Ltd. Energy No index 72% Against

Concerning pay practices 51%

ENGH

Enghouse Systems Limited

Information Technology S&P/TSX Completion 72% Against

Insufficient response to shareholder dissent 76%

CGX Cineplex Inc. Communication Services No index 72% Against

Buyout of underwater options 97%

APS

Aptose Biosciences Inc. Health Care No index 75% Against Excessive grants N/A

KL

Kirkland Lake Gold Ltd. Materials S&P/TSX 60 75% For 92%

Proxy Season Review 2021: Canada 25

Notable Meetings

Election of Directors & Say-on-Pay

BlackBerry Ltd. (BB) June 23, 2021

• Election of V. Prem Watsa 17% opposition o Excluding shares affiliated w/ Watsa 22% opposition*

• Say-on-Pay 41% opposition o Excluding shares affiliated w/ Watsa 52% opposition*

*Assumes that ~47 million shares held by Fairfax group companies were voted in favor of these proposals

While the meme stock phenomenon may have been a fleeting curiosity for most market participants – a bemusing spike in nominal equity valuations and heightened news interest – it had a very real, very lucrative, effect on CEO John Chen’s compensation at BlackBerry.

Under the specific hurdles of Mr. Chen’s retention agreement signed in 2018, the CEO could unlock huge tranches of PSUs if BB stock hit ascending share price targets of $16 through $20 over any 10-day average measurement period – a tantalisingly realistic possibility if you’re the CEO of a company whose shares are periodically being pumped by an investor crowd solely for the sake of a rising stock price in itself.

A new disclosure in the company’s annual report for fiscal 2021 further clarified that these price hurdles could be achieved upon a volume-weighted 10-day average, something not previously disclosed.

This meant that over any ten-day period, even if the simple average closing price is comfortably below $16, the -volume-weighted average could exceed that hurdle if there was an especially high volume of trading activity made on the days in which the shares closed highest.

In the end, for BlackBerry’s John Chen, three days is all it took. The trading volume in the three days beginning January 25 was so high (averaging 326 million trades a day for a stock that averaged over the trailing six months just 10 million a day) that even though the shares only closed above $16 on those first three days - peaking at $25.10 on January 27 – the volume-weighted average for the period was $18.24, clearing not one, not two, but three of the five performance hurdles that were seen as very ambitious at the time the board made the retention award.

In a footnote to an unassuming table, the company disclosed that three out of Mr. Chen’s five retention PSU tranches were earned in fiscal 2021, unlocking 3 million PSUs for time-vesting, worth around $42 million at June prices. It is fair to say that the board at the time could not have foreseen the shares vesting in such conditions back in 2018.

Proxy Season Review 2021: Canada 26

Chartwell Retirement Residences (CSH.UN) May 20, 2021

• Election of Huw Thomas: 15% opposition • Election of Michael Harris: 13% • Say-on-Pay: 31%

Sienna Senior Living (SIA), June 2, 2021

• Say-on-Pay: 15% opposition

Extendicare Inc. (EXE)- May 27, 2021

• Say-on-Pay: 1.5% opposition

As discussed in the Highlights section, Canada’s already depleted long-term care operators faced greater challenges, and greater public scrutiny, than most.

The boards of Chartwell and Sienna were unable to resist the temptation to make concessions to management. In light of the issues affecting retirement home operators and the potentially devastating impacts from the pandemic that were faced by staff and customers alike, the decisions of the boards to make adjustments to in-flight plans – excluding the worst of the pandemic – in order to enable higher annual bonus payouts was met with criticism. Extendicare’s board, perhaps crucially, did not use employ upward discretion, while there was less public outrage focused on them specifically. Chartwell, the largest of the three, got the sternest criticism.

Facing a Vote No campaign against former Ontario governor Michael Harris, if the Chartwell board’s intention was to deflect further criticism, they did not help themselves by awarding maximum bonuses for a quality assessment component based on customer satisfaction, reputation and media profile.

RioCan Real Estate Investment Trust (REI.UN), May 26, 2021

• Say-on-Pay: 76% opposition

At 24%, the percentage of votes in favor is the second lowest recorded in the past decade, in front only of Barrick’s lowly 15% recorded at their 2013 AGM. This result caps a low point for RioCan after years of steadily declining results in the face of pay-for-performance concerns and aggregate NEO pay consistently well above the peer median. The board acknowledged the unsatisfactory outcome and has committed to disclosing to unitholders, within six months of the meeting, a summary of feedback received and any intended changes to the executive compensation programs.

GFL Environmental (GFL) May 19, 2021

• Say-on-Pay: 10% opposition*

*The company has a multi-class share structure, and does not break down votes by class nor by affiliation. Excluding the votes of significant or affiliated shareholders and multiple voting shares (10 votes per share), approximately 34% of unaffiliated shareholders opposed the proposal.

Proxy Season Review 2021: Canada 27

GFL went public in 2020 and this was the first AGM since its debut. While newly floated issuers typically get a grace period, the combination of concerns identified at board-level and on compensation led to a recommendation against one director and the inaugural pay plan, which included total pay of C$37 million for the CEO. A significant portion of that total was a C$26.6 million stock option grant; in addition to excessive quantum, we identified significant board discretion over variable payouts, no performance based long-term incentives and single trigger change in control benefits as further pay concerns. The cost of the CEO’s fixed salary, cash bonus and perquisites were notably high considering the company’s stage of development and peer practices.

Meanwhile, at board level, our assessment found independence to be far below that advertised by the company in its classification. GFL was also targeted by an activist short seller early on in its life as a public company.

While the results of the company’s initial pay vote primarily reflect the convoluted capital and ownership landscape, they may also indicate some early disquiet among minority shareholders hoping for the long-term success – and not just fleeting gains – of this ostensibly green stock play.

Air Canada (AC) June 29, 2021

• Say-on-Pay: 29% opposition

Air Canada negotiated a government bailout, the terms of which will severely limit the executive pay they can offer in the forthcoming years. Perhaps tempted to leave management a souvenir of the good times, they made a series of one-off grants designed to effectively nullify the salary and bonus plan cuts made in the previous year. Politicians and labor groups immediately weighed in and most of the most senior officers walked back their grants. This was not enough to assuage around 30% of the voting shareholder public.

Precision Drilling (PD) June 29, 2021

• Say-on-Pay: 58% opposition

The traditional energy sector, and by association the companies that provide drilling services for oil and natural gas extraction, were racked by the twin crises in early 2020 of the global pandemic and a sharp fall in crude prices. Nonetheless, total compensation at Precision and many of its peers did not drop as precipitously as either their share price or revenue. While the company cited steep competition for global talent, shareholders may have been perturbed by pay standards in the industry as a whole – among Precision’s peers, four had filed for bankruptcy just in 2020. Investors may have been left questioning if it was really performance they were paying for.

Proxy Season Review 2021: Canada 28

ESG & Shareholder Proposals

Imperial Oil Limited (IMO) May 4, 2021

Given the threat of climate change, companies have faced increasingly more frequent and nuanced proposals regarding climate-risk management in recent years. At its 2021 AGM, Imperial Oil Limited received a shareholder proposal requesting that it adopt a corporate-wide ambition to achieve net-zero carbon emissions at or before 2050. If adopted, the proposal would have pertained to Scope 1 and 2 emissions.

Proponents acknowledged Imperial Oil’s goal to achieve a 10% decrease in GHG emissions intensity by 2023 but remained concerned that it had not committed to longer-term targets in line with the Paris Agreement, particularly in light of net-zero by 2050 targets adopted by peer companies. The proponents also pointed to net-zero by 2050 targets held by 28 countries, including Canada, which had also committed to reducing GHG emissions by 30% by 2030.

The board opposed the proposal, stating that until the company could successfully identify clear, achievable steps to net-zero, such a commitment would be premature. Instead, Imperial Oil stated that its preference was to set a series of concrete targets with specific action plans. It stated its support for the goals of the Paris Agreement and maintained that Imperial Oil was developing pathways to reduce GHG emissions intensity in support of a net-zero future. It also stated that it was supporting customers in reducing their emissions and asserted the potential viability of CCS technology.

We found Imperial Oil’s climate-related disclosure to be deficient in some respects in comparison to peers; for example, the company did not appear to have received external assurance for its GHG emissions disclosure and did not provide a comprehensive index of TCFD disclosures, though it did state that its disclosure was guided by TCFD recommendations. Imperial Oil also had not set a long-term GHG emissions reduction target. Additionally, given the board’s response that it was developing pathways to reduce its GHG emissions intensity in support of a net-zero future, we felt that shareholder support for the proposal would serve to further encourage Imperial Oil in the development of these pathways and its preference to set concrete targets. As such, we recommended support for this proposal.

The proposal failed to pass with majority approval as only 14% of shareholders voted in favor.

Canadian Pacific Railway Limited (CP) April 21, 2021

Canadian National Railway (CNR) April 27, 2021

The 2021 proxy season saw a number of Say on Climate proposals offering shareholders the opportunity to vote annually on companies’ climate plans. Canadian Pacific Railway received a shareholder proposal at its 2021 AGM requesting that it annually present shareholders with a climate action plan disclosing GHG emission levels consistent with TCFD recommendations and its strategy for future emissions reductions, as well as progress year-over-year. Meanwhile, Canadian National Railway’s board presented a similar proposal for shareholder approval, upon which the plans of both companies would be subject to an annual non-binding advisory vote.

Proxy Season Review 2021: Canada 29

Proponents of the Canadian Pacific Railway shareholder proposal stated that the requested plan was an important means of assuring shareholders that management takes seriously the physical and transition risks associated with climate change. Canadian Pacific Railway’s board recommended in favor of the proposal, stating its commitment to transparency regarding GHG reduction targets and its climate strategy, and maintaining that its strategy is aligned with TCFD recommendations and overseen by the board. Meanwhile, Canadian National Railway’s board stated that its climate action plan describes the extent of board oversight, GHG emission levels consistent with TCFD recommendations, and its reduction strategy. It also stated that if the proposal did not receive majority shareholder support, it would engage with shareholders to solicit their specific concerns regarding the company’s climate action plan and review said plan accordingly.

Upon review, we noted some concerns regarding the companies’ disclosures. Canadian Pacific Railway lacked emissions reduction targets and comprehensive TCFD reporting; and Canadian National Railway lacked Scope 3 emissions reduction targets and did not appear to maintain a net-zero ambition. Ultimately, we recommended against both proposals due to concerns regarding the terms of the proposals themselves. Though we were supportive of both companies developing and presenting to shareholders a climate action plan consistent with TCFD recommendations, we were concerned with the prospect of the companies seeking non-binding shareholder approval of those climate action plans. Ultimately, we were concerned that this mechanism would allow boards to delegate oversight responsibilities for the setting of corporate strategy to shareholders by allowing them to effectively approve this strategy through an up/down vote. Further, companies might view providing a vote on their climate strategies as a substitute for robust shareholder engagement. We also expressed concern that, though non-binding in nature, the legal structure and implications of casting a vote on Say on Climate resolutions are unknown and untested. Therefore, our overall opposition to the proposals stemmed entirely from their mechanics, and we maintained that this opposition should not be interpreted by the companies as reason not to provide the requested reporting to shareholders.

Largely due to management support, both proposals received majority shareholder support, with the shareholder proposal at Canadian Pacific Railway receiving 85% support and the management proposal at Canadian National Railway receiving 92% support.

Proxy Season Review 2021: Canada 30

Appendix A Designated Groups Under CBCA Regulation

Proxy Season Review 2021: Canada 31

Proxy Season Review 2021: Canada 32

Proxy Season Review 2021: Canada 33

Proxy Season Review 2021: Canada 34

Proxy Season Review 2021: Canada 35

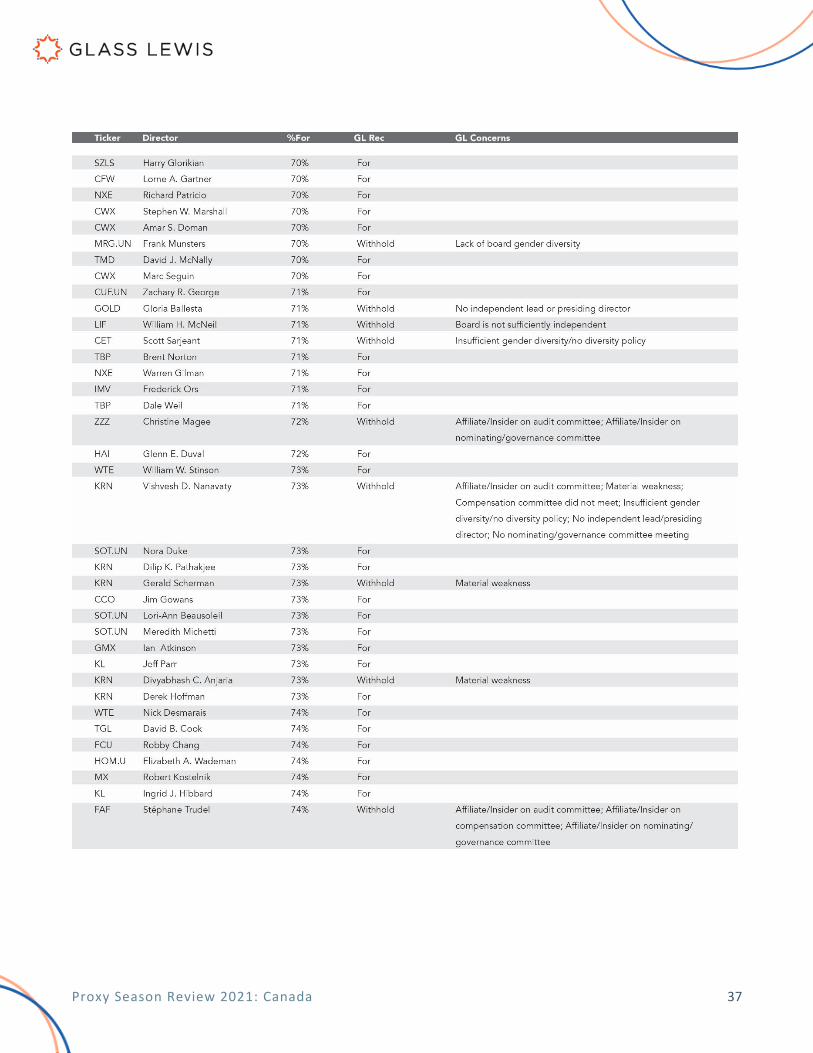

Appendix B Directors with 25% or More Opposition

Proxy Season Review 2021: Canada 36

Proxy Season Review 2021: Canada 37

Proxy Season Review 2021: Canada 38

Proxy Season Review 2021: Canada 39

Connect with Glass Lewis Corporate Website | www.glasslewis.com Email | [email protected]

Social | @glasslewis Glass, Lewis & Co.

Global Locations

North America

United States Headquarters 255 California Street Suite 1100 San Francisco, CA 94111 +1 415 678 4110 +1 888 800 7001

44 Wall Street Suite 503 New York, NY 10005 +1 646 606 2345

2323 Grand Boulevard Suite 1125 Kansas City, MO 64108 +1 816 945 4525

Asia Pacific

Australia CGI Glass Lewis Suite 5.03, Level 5 255 George Street Sydney NSW 2000 +61 2 9299 9266

Japan Shinjuku Mitsui Building 11th floor 2-1-1, Nishi-Shinjuku, Shinjuku-ku, Tokyo 163-0411, Japan

Europe Ireland 15 Henry Street Limerick V94 V9T4 +353 61 292 800

United Kingdom 80 Coleman Street Suite 4.02 London EC2R 5BJ +44 20 7653 8800

Germany IVOX Glass Lewis Kaiserallee 23a 76133 Karlsruhe +49 721 35 49 622

Proxy Season Review 2021: Canada 40

DISCLAIMER

© 2021 Glass, Lewis & Co., and/or its affiliates. All Rights Reserved. This report is intended to provide a general overview of some of the issues that were up for shareholder vote during this past proxy season. It is not intended to be exhaustive and does not address all issues that were up for shareholder vote. Glass Lewis provides its clients with research, data, and analysis of proxy voting issues, and makes recommendations as to how institutional shareholders should vote their proxies, without commenting on the investment merits of the securities issued by the subject companies. Therefore, none of Glass Lewis’ proxy vote recommendations should be construed as a recommendation to invest in, purchase, or sell any securities or other property. Moreover, Glass Lewis’ proxy vote recommendations are solely statements of opinion, and not statements of fact, on matters that are, by their nature, judgmental. Glass Lewis research, analyses, and recommendations are made as of a certain point in time and may be revised based on additional information or for any other reason at any time. The information contained in this report is based on publicly available information. While Glass Lewis exercises reasonable care to ensure that all information included in this report is accurate and is obtained from sources believed to be reliable, no representations or warranties express or implied, are made as to the accuracy or completeness of any information included herein. Such information may differ from public disclosures made by the subject company. In addition, third-party content attributed to another source, including, but not limited to, content provided by a vendor or partner with whom Glass Lewis has a business relationship, as well as any Report Feedback Statement, are the statements of those parties and shall not be attributed to Glass Lewis. Neither Glass Lewis nor any of its affiliates or third-party content providers shall be liable for any losses or damages arising from or in connection with the information contained herein or the use or inability to use any such information. Glass Lewis expects its subscribers to possess sufficient experience and knowledge to make their own decisions entirely independent of any information contained in its reports. Subscribers are ultimately and solely responsible for making their own voting decisions. Glass Lewis’ reports are intended to serve as a complementary source of information and analysis for subscribers in making their own voting decisions and therefore should not be relied on by subscribers as the sole determinant in making voting decisions. All information contained in this document is protected by law, including but not limited to, copyright law, and none of such information may be copied or otherwise reproduced, repackaged, further transmitted, transferred, disseminated, redistributed or resold, or stored for subsequent use for any such purpose, in whole or in part, in any form or manner or by any means whatsoever, by any person without Glass Lewis’ express prior written consent. This document should be read and understood in the context of other information Glass Lewis makes available concerning, among other things, its research philosophy, approach, methodologies, sources of information, and conflict management, avoidance and disclosure policies and procedures, which information is incorporated herein by reference. Glass Lewis recommends all clients and any other consumer of this document carefully and periodically evaluate such information, which is available at: http://www.glasslewis.com.