psg banking review - 2016 - banking... · 2016-12-12 · annual inflation rate was estimated at...

TRANSCRIPT

P a g e | 0

PSG BANKING REVIEW

- 2016

DECEMBER 2016

P a g e | 1

PSG Wealth Management (Namibia) (Pty) Ltd

Table of contents

Introduction ................................................................................................................................................................. 3

Executive Summary ...................................................................................................................................................... 4

PSG - Ranking the Local Banks ....................................................................................................................................... 5

Nature of business ....................................................................................................................................................... 7

Local Banks ............................................................................................................................................................................ 7

SA Banks ................................................................................................................................................................................. 8

Botswana Banks ..................................................................................................................................................................... 9

Zambian Banks ....................................................................................................................................................................... 9

Economic Review and Outlook .................................................................................................................................... 10

Real Economic Growth ........................................................................................................................................................ 10

Namibian Inflation ............................................................................................................................................................... 10

Private Sector Credit Extension (PSCE) ................................................................................................................................ 11

Monetary Policy ................................................................................................................................................................... 11

Local Banks - Financial Results Review ........................................................................................................................ 12

CGP ...................................................................................................................................................................................... 12

FNB ....................................................................................................................................................................................... 12

NED ...................................................................................................................................................................................... 13

SBNH .................................................................................................................................................................................... 13

Balance Sheet ............................................................................................................................................................ 14

Bank Assets .......................................................................................................................................................................... 14

Gross Advances .................................................................................................................................................................... 15

Growth by Loan Category – Local Banks .............................................................................................................................. 16

Mortgage Loans ................................................................................................................................................................... 17

Term Loans and Overdrafts ................................................................................................................................................. 20

Instalment Sales and Leases ................................................................................................................................................ 21

Deposits ..................................................................................................................................................................... 22

Total Revenue ............................................................................................................................................................ 23

Net Interest Income (NI) ...................................................................................................................................................... 23

Non-Interest Revenue (NIR)................................................................................................................................................. 24

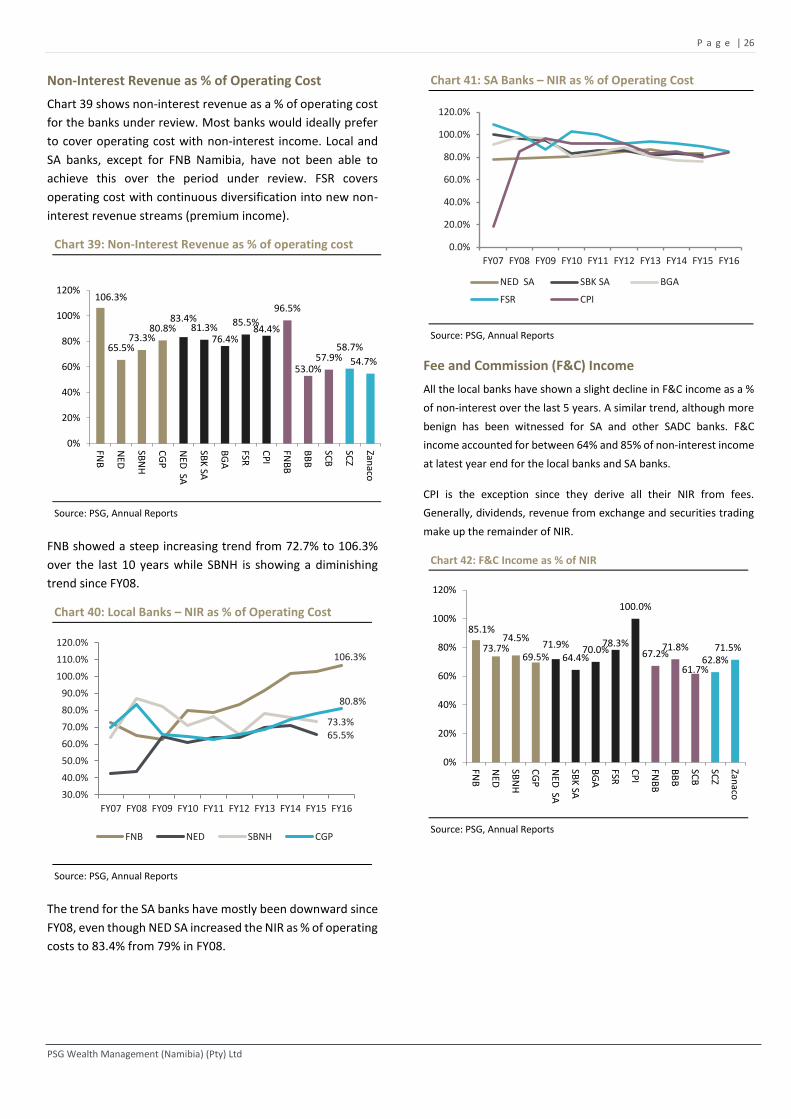

Non-Interest Revenue as % of Operating Cost .................................................................................................................... 26

Fee and Commission (F&C) Income ..................................................................................................................................... 26

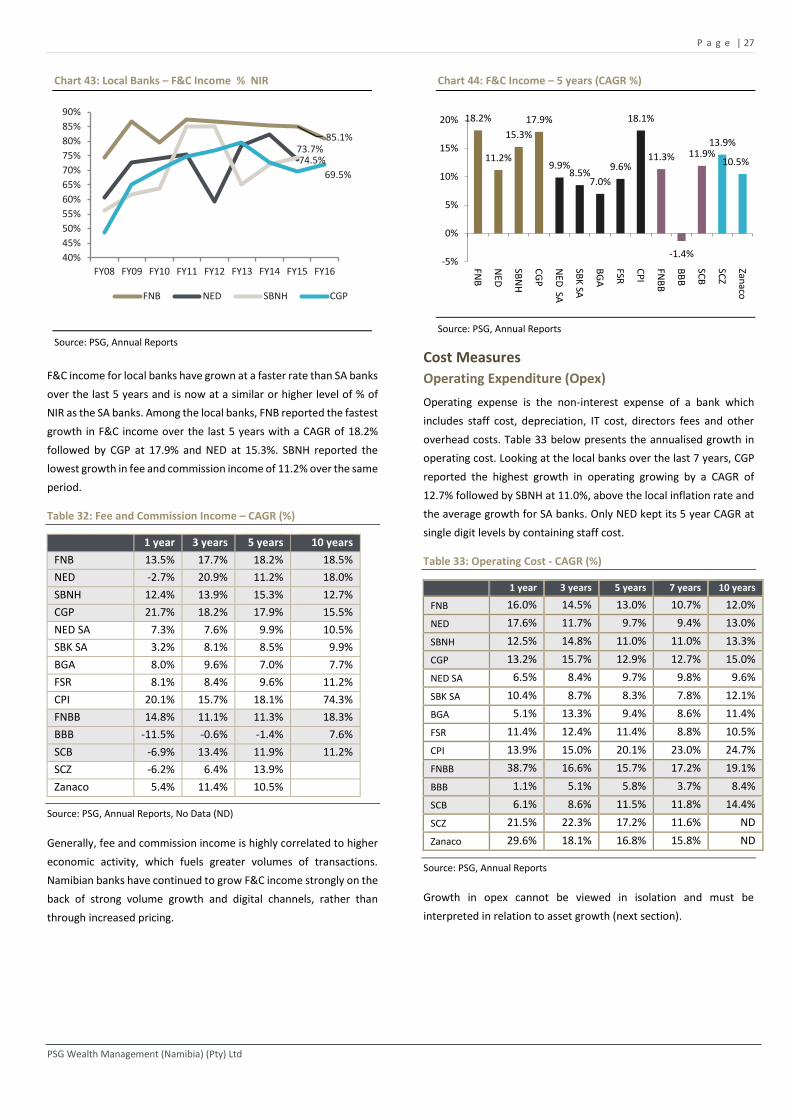

Cost Measures ........................................................................................................................................................... 27

Operating Expenditure (Opex) ............................................................................................................................................. 27

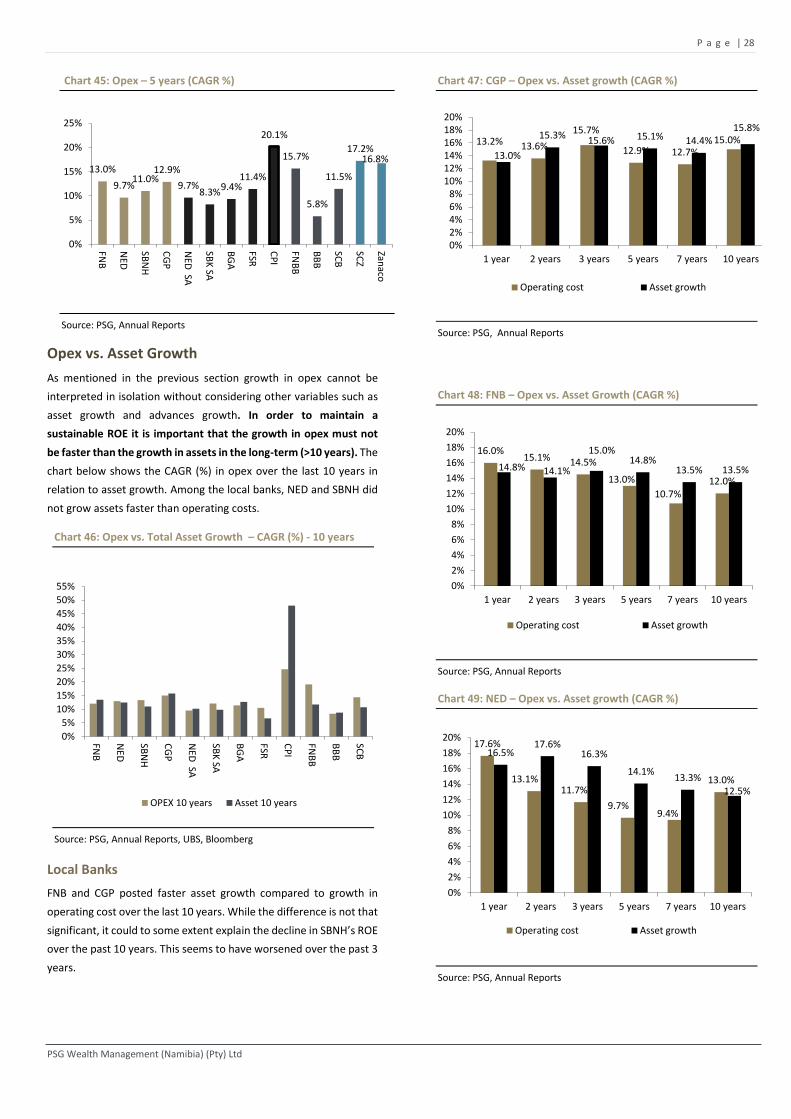

Opex vs. Asset Growth ............................................................................................................................................... 28

Local Banks .......................................................................................................................................................................... 28

SA Banks ............................................................................................................................................................................... 29

Cost-to-Income .......................................................................................................................................................... 31

P a g e | 2

PSG Wealth Management (Namibia) (Pty) Ltd

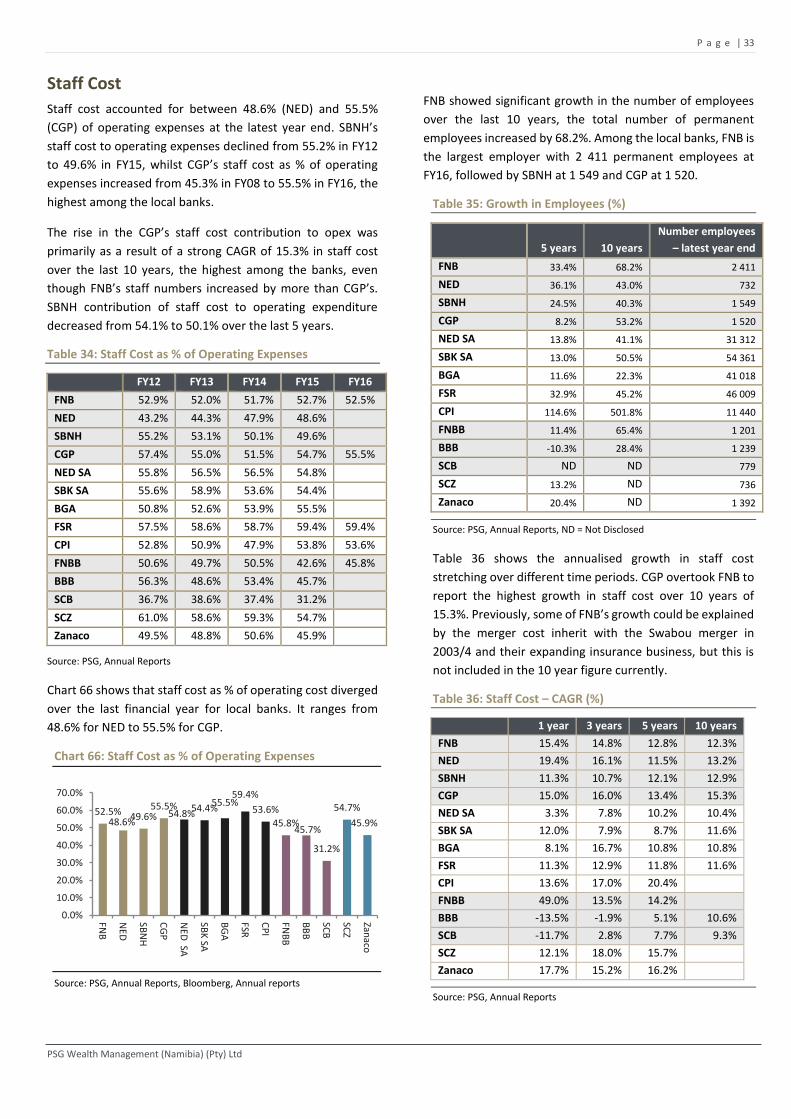

Staff Cost ................................................................................................................................................................... 33

Staff Cost per Employee ...................................................................................................................................................... 34

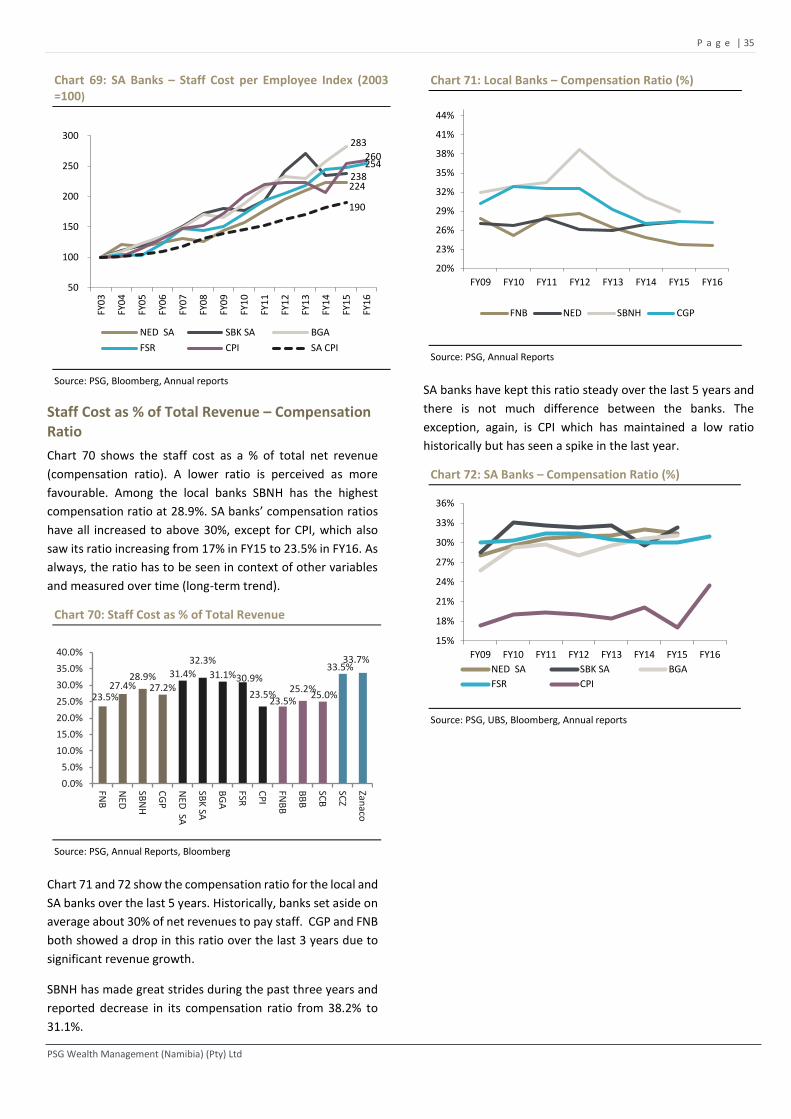

Staff Cost as % of Total Revenue – Compensation Ratio ..................................................................................................... 35

Staff Cost as % of Net Interest Income ................................................................................................................................ 36

Profitability ................................................................................................................................................................ 37

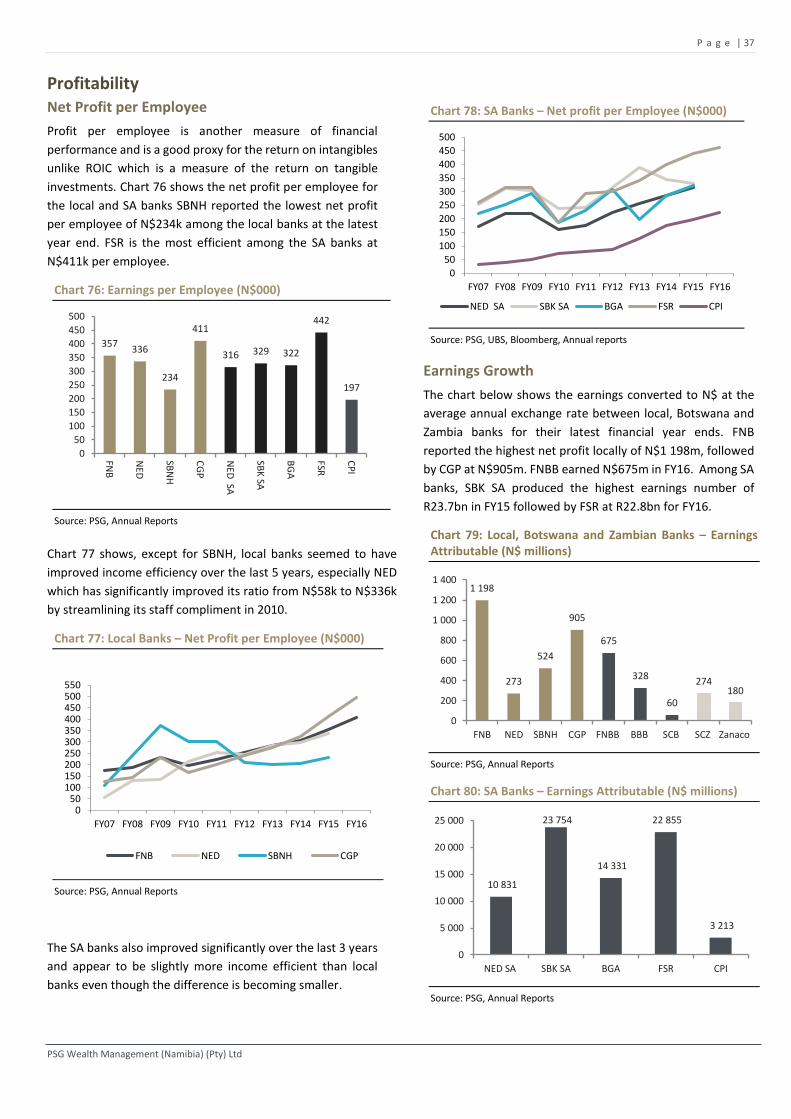

Net Profit per Employee ...................................................................................................................................................... 37

Earnings Growth .................................................................................................................................................................. 37

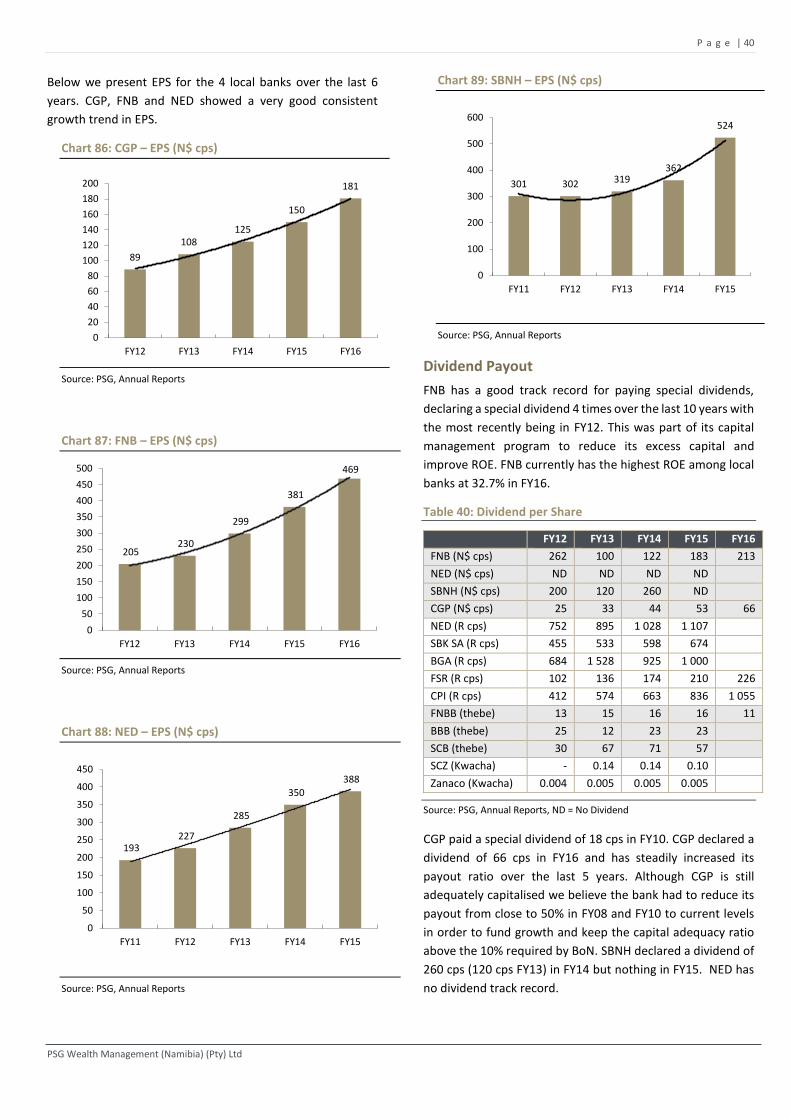

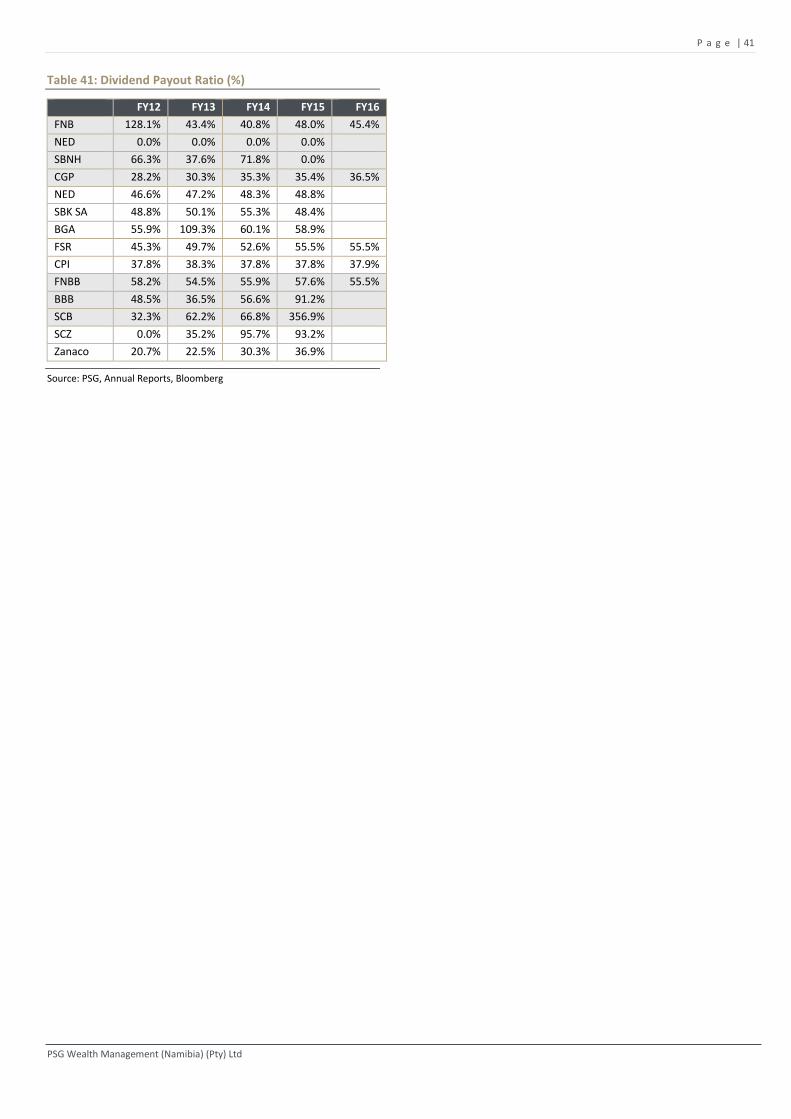

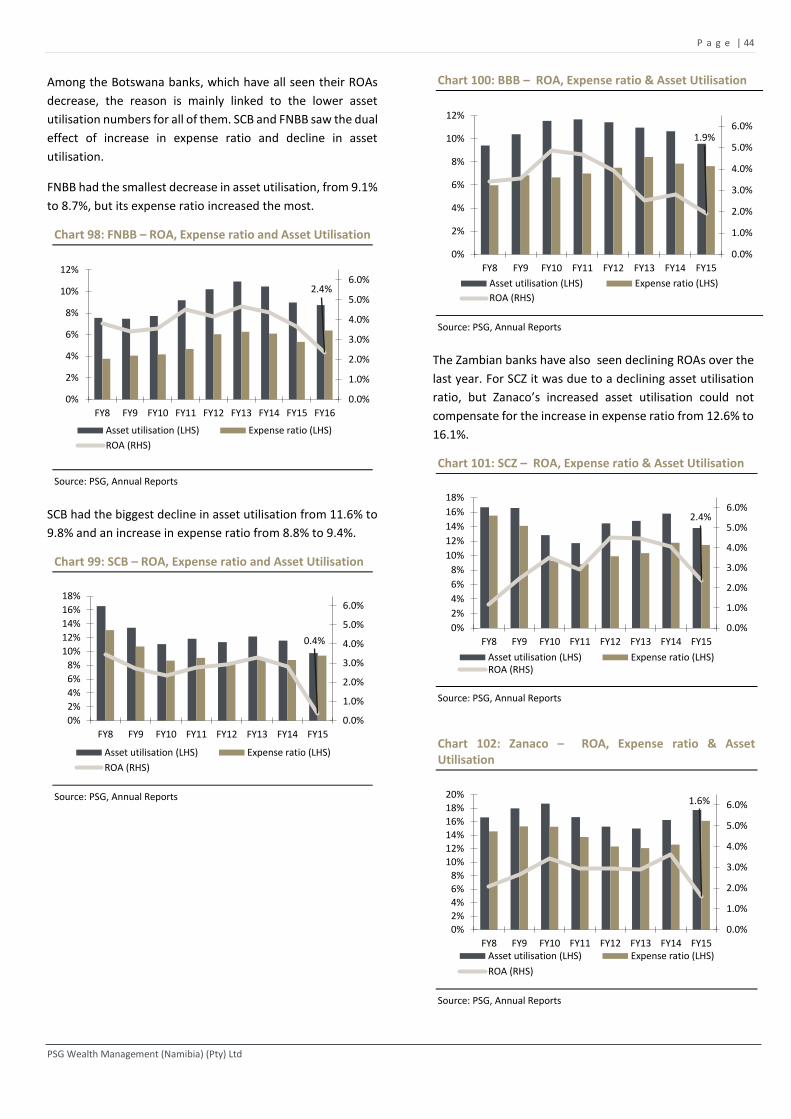

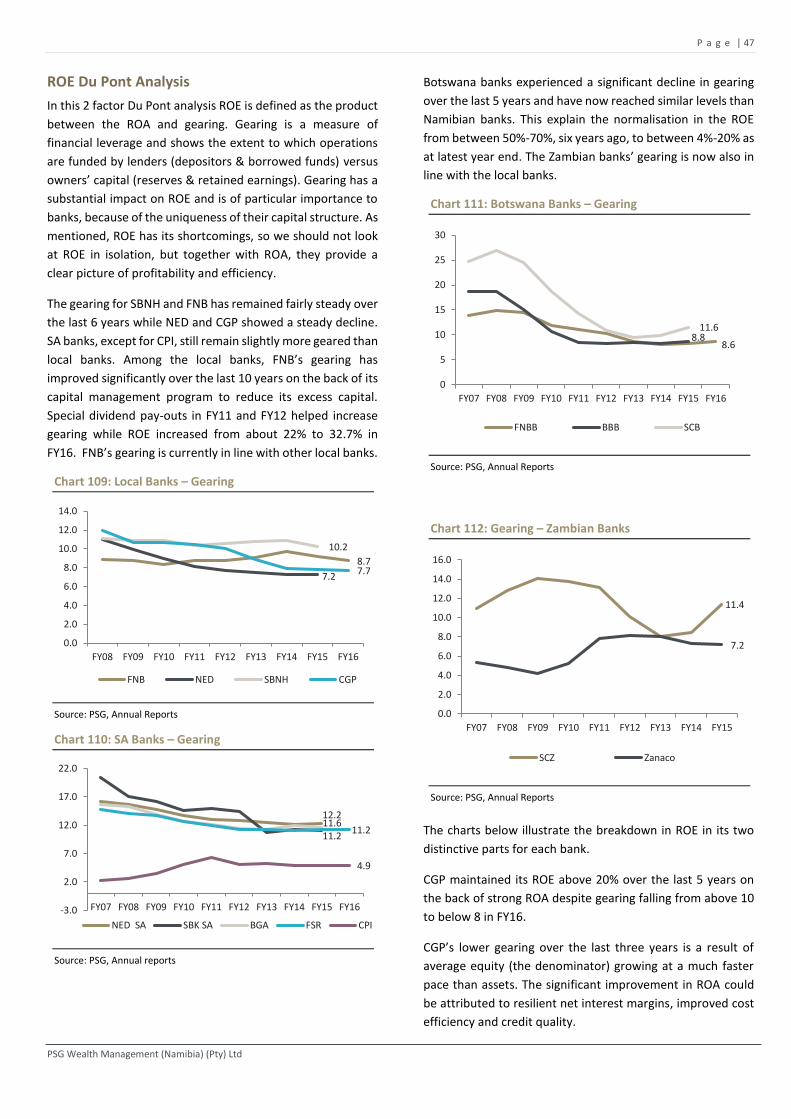

Earnings per Share (EPS) ...................................................................................................................................................... 39

Dividend Payout ................................................................................................................................................................... 40

Return on Average Assets (ROA) ................................................................................................................................. 42

ROA – 2 Factor Du Pont Analysis ......................................................................................................................................... 43

Return on Average Equity (ROE) .................................................................................................................................. 45

ROE Du Pont Analysis ........................................................................................................................................................... 47

Lending Rates ............................................................................................................................................................. 51

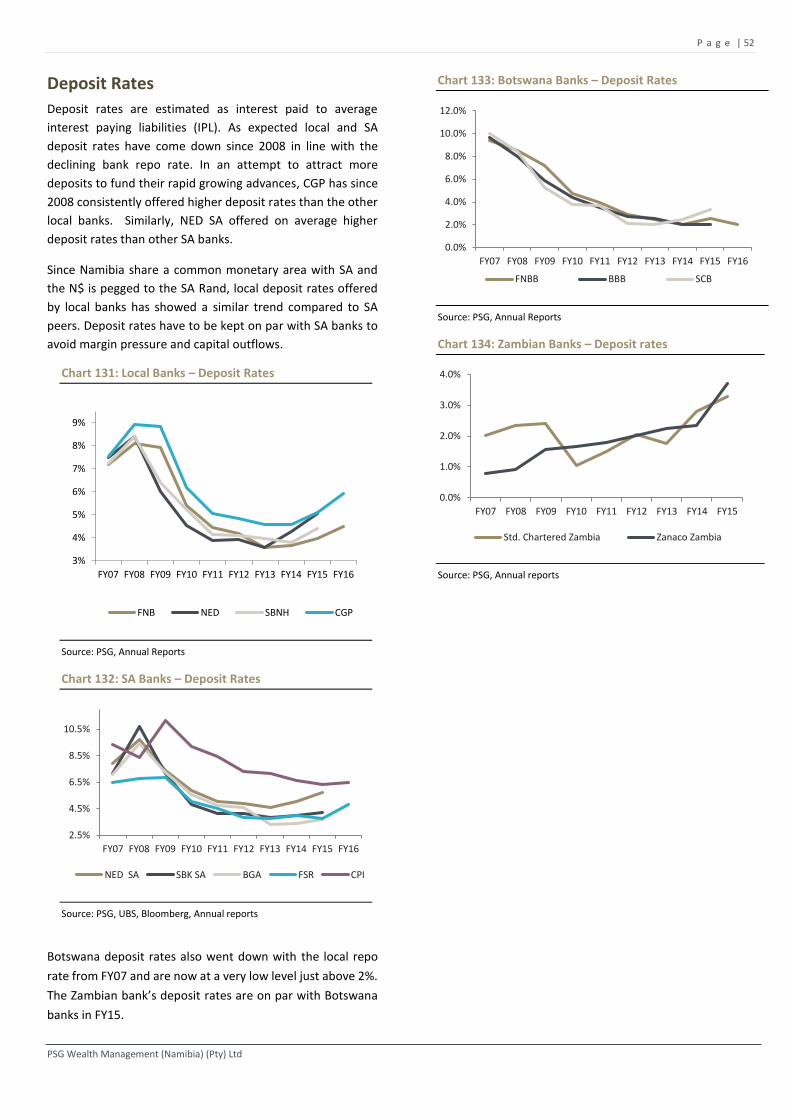

Deposit Rates ............................................................................................................................................................. 52

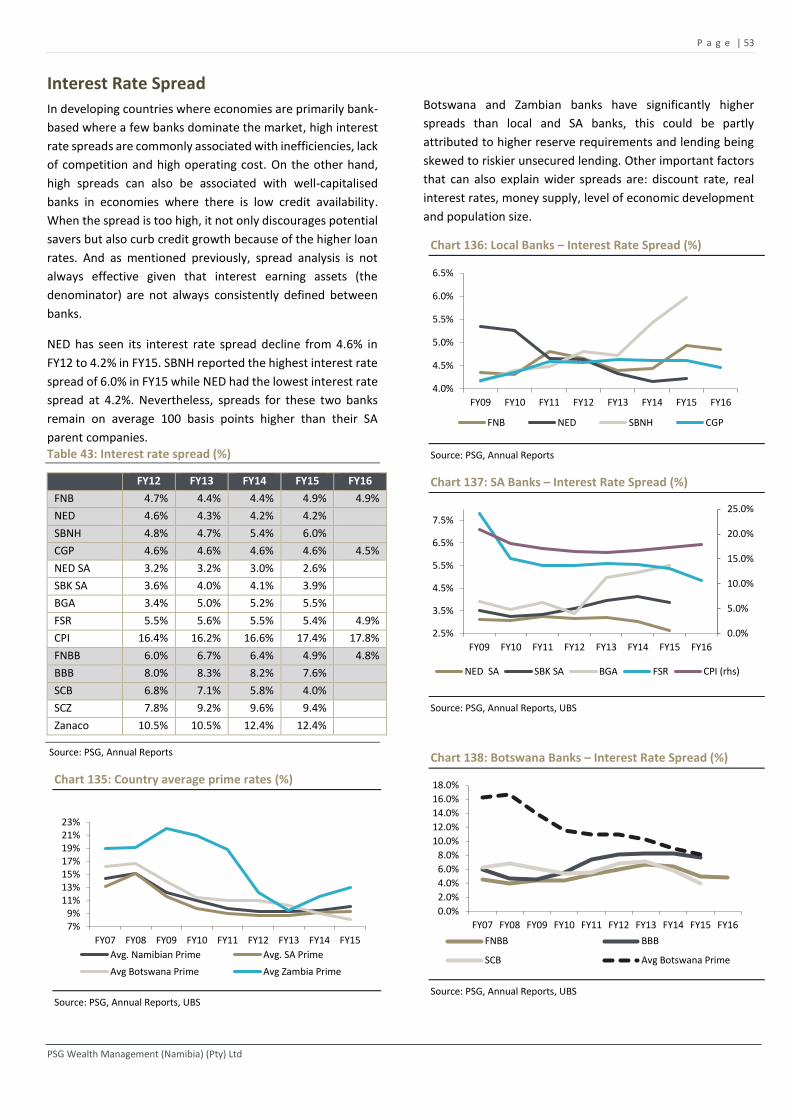

Interest Rate Spread ................................................................................................................................................... 53

Net Interest Margins (NIM) ......................................................................................................................................... 54

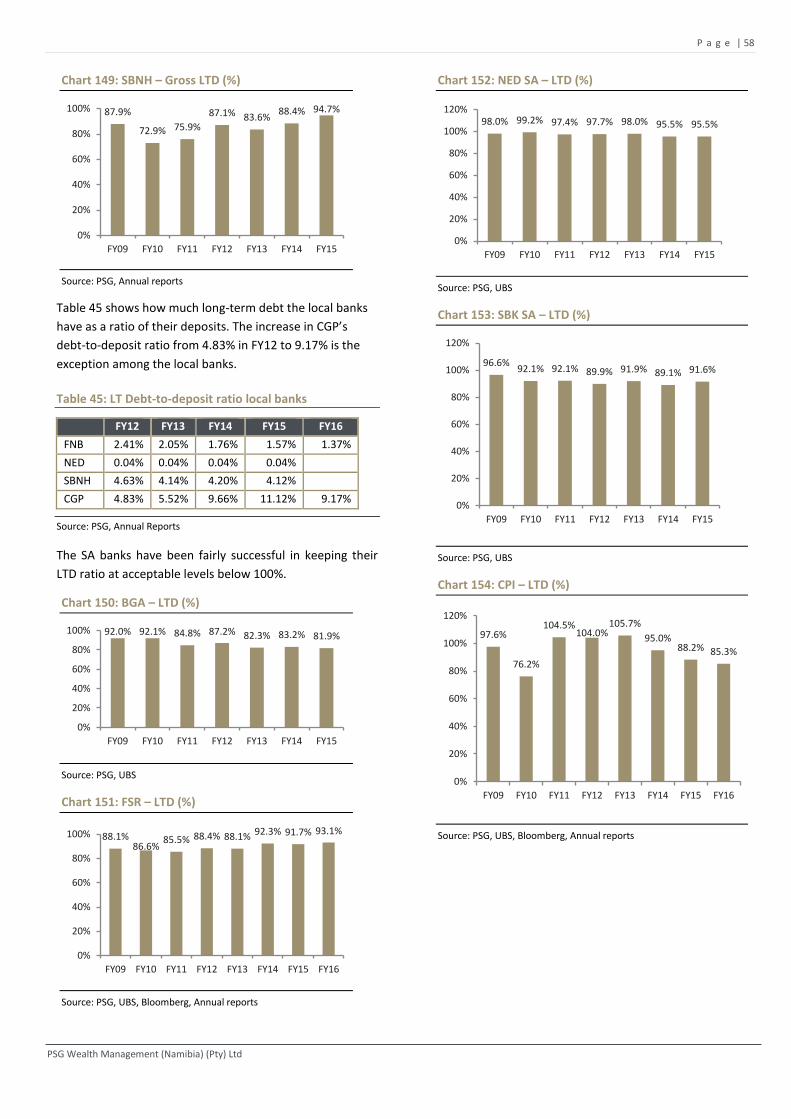

Loan-to-Deposit (LTD) Ratio ................................................................................................................................................ 57

Liquid Assets to Deposit (LADST) ......................................................................................................................................... 60

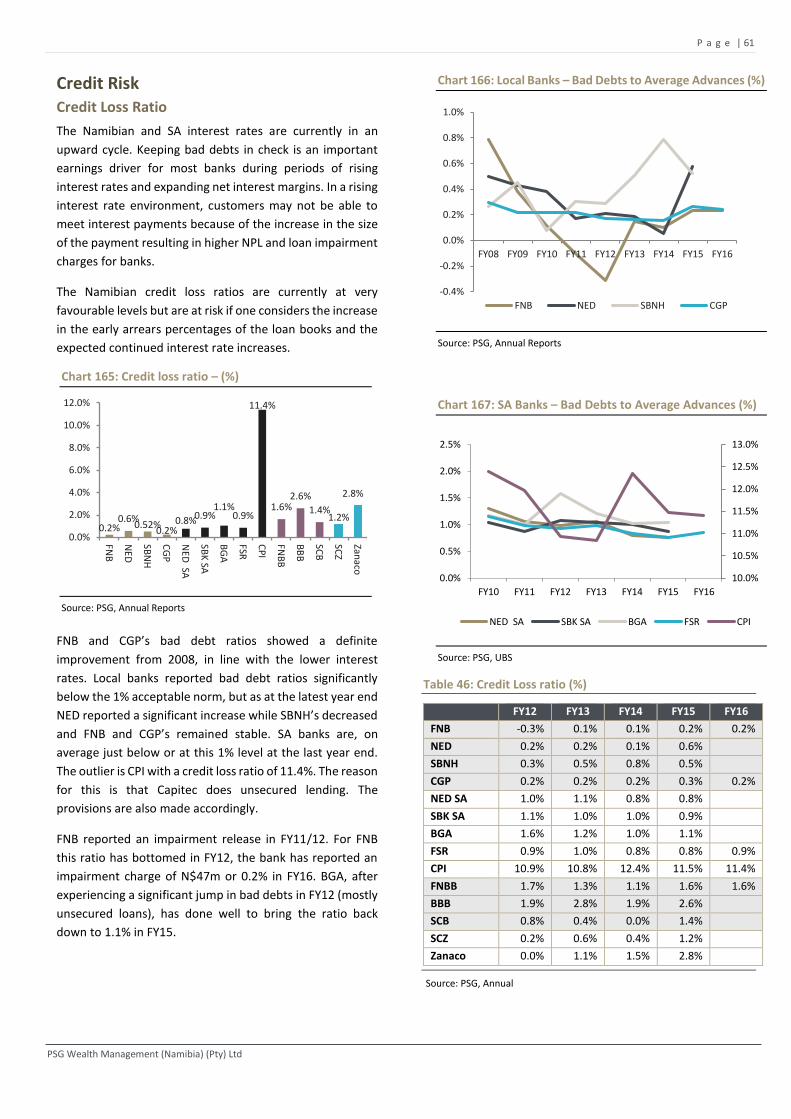

Credit Risk .................................................................................................................................................................. 61

Credit Loss Ratio .................................................................................................................................................................. 61

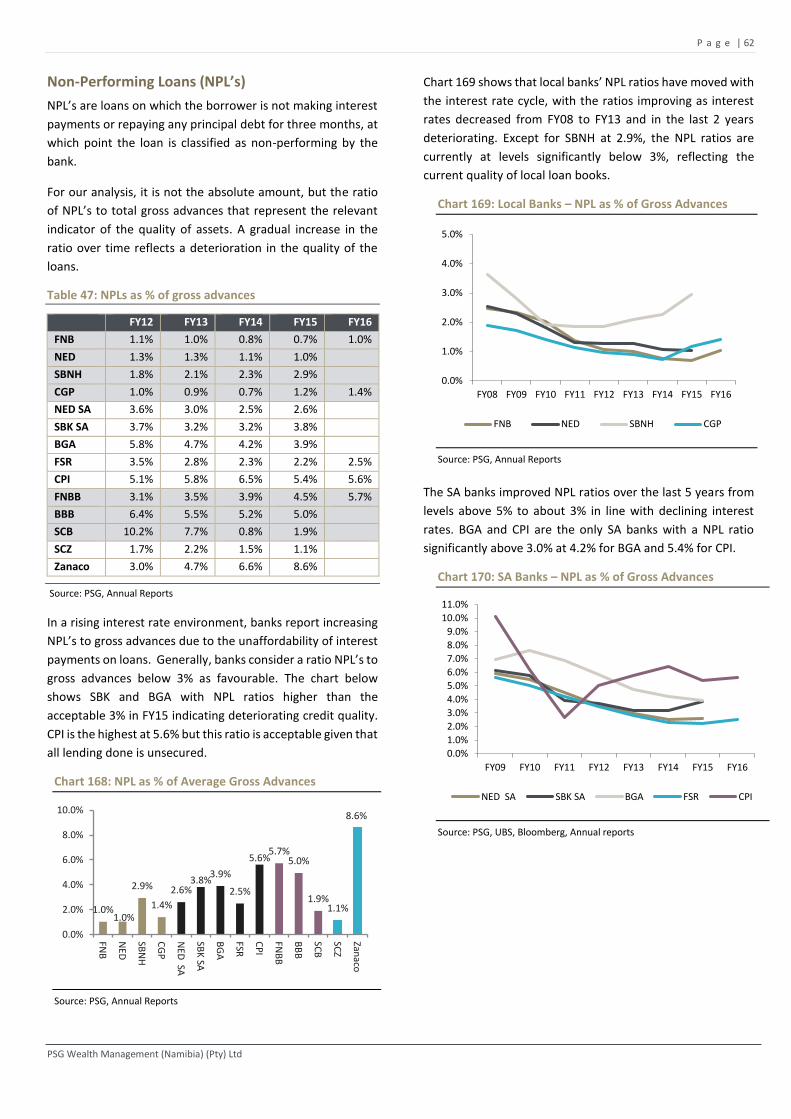

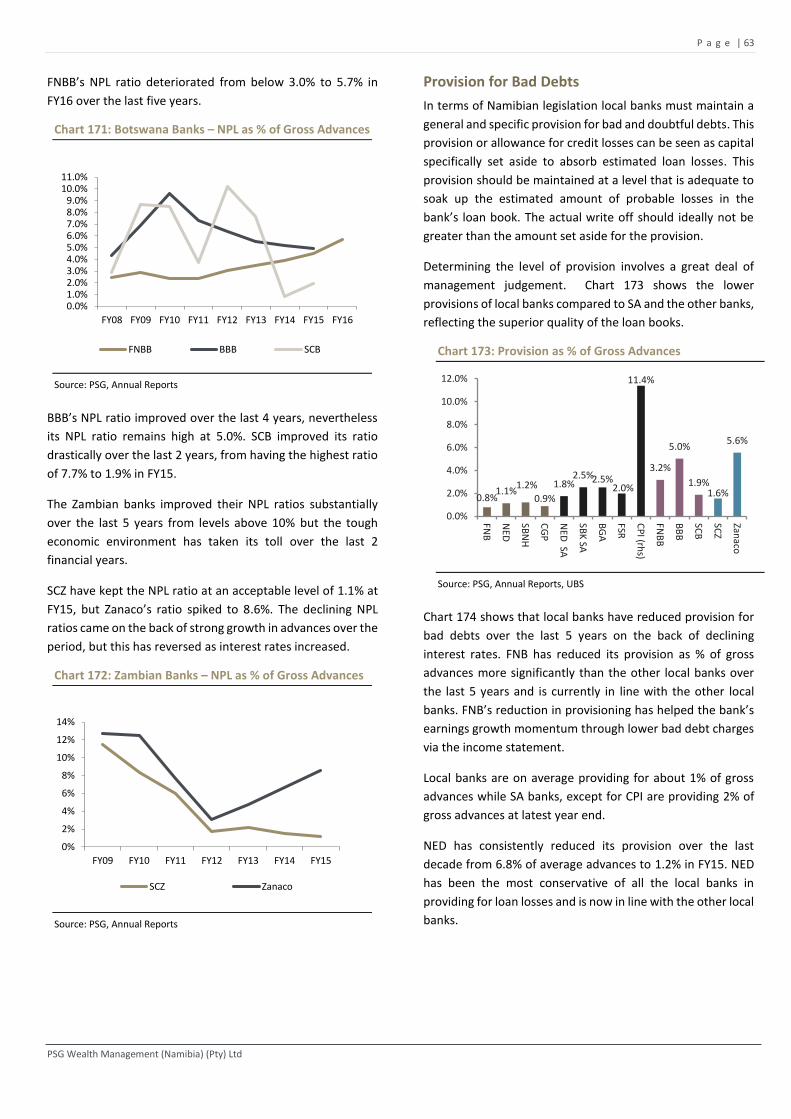

Non-Performing Loans (NPL’s) ............................................................................................................................................. 62

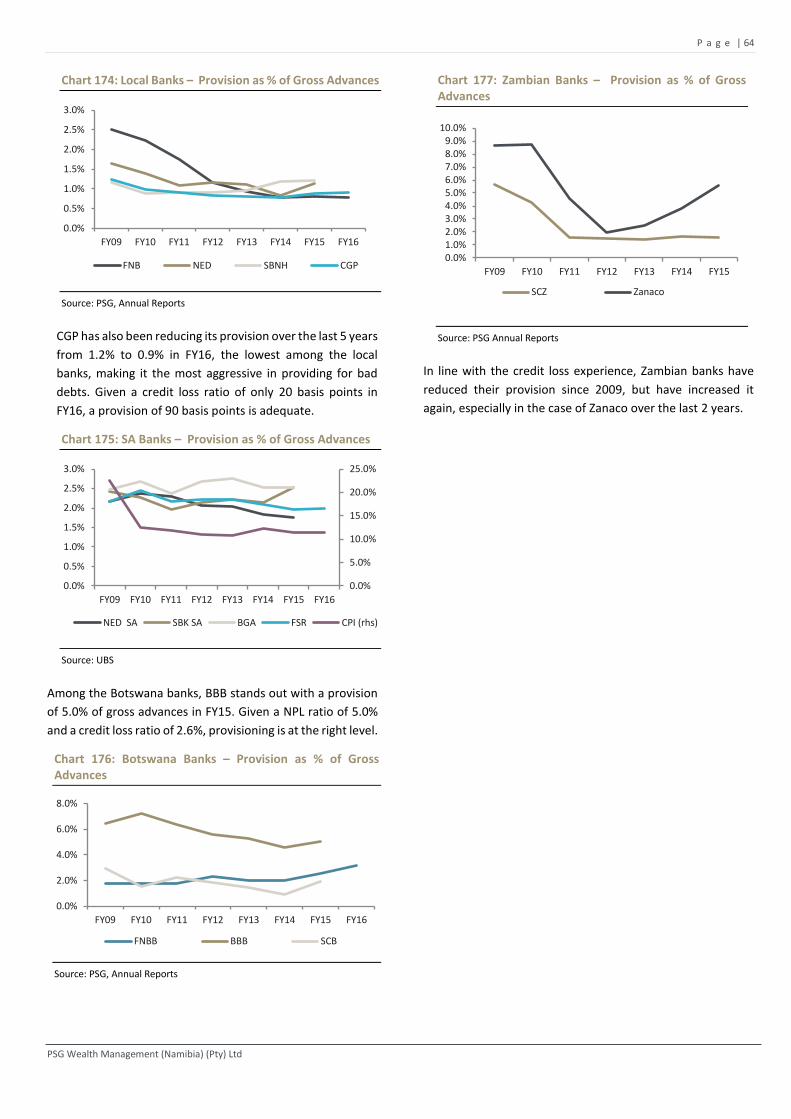

Provision for Bad Debts ....................................................................................................................................................... 63

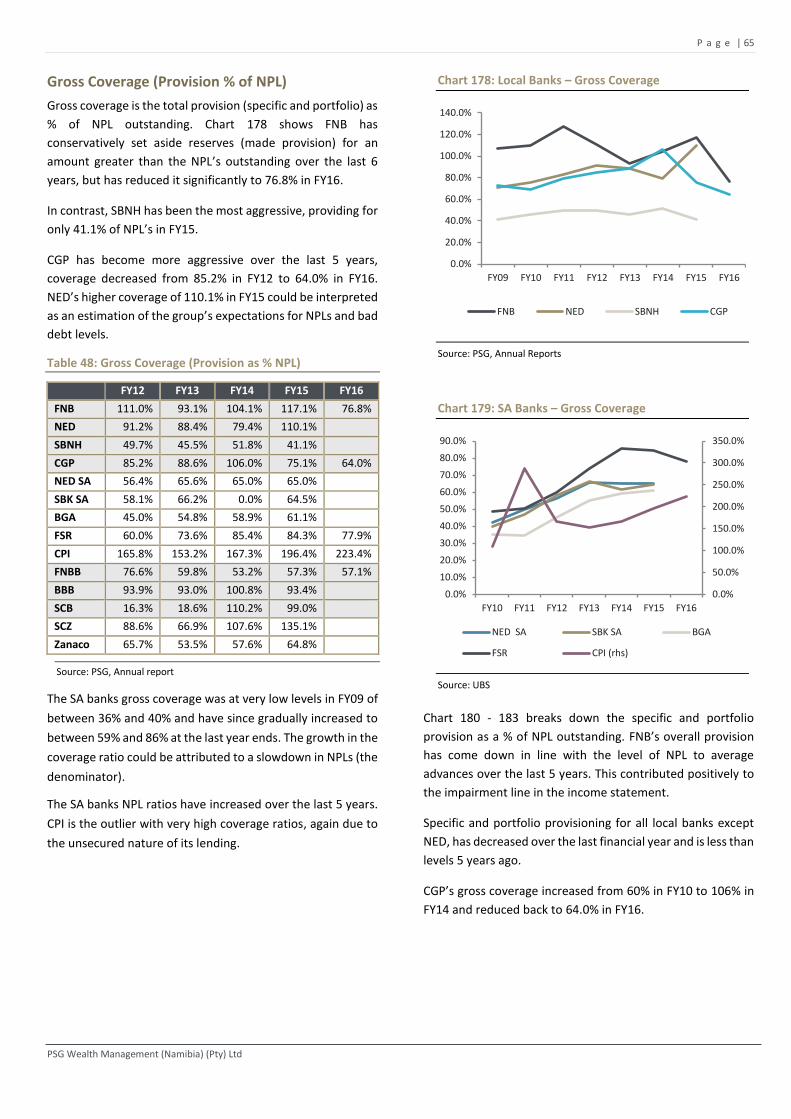

Gross Coverage (Provision % of NPL) ................................................................................................................................... 65

Valuation ................................................................................................................................................................... 67

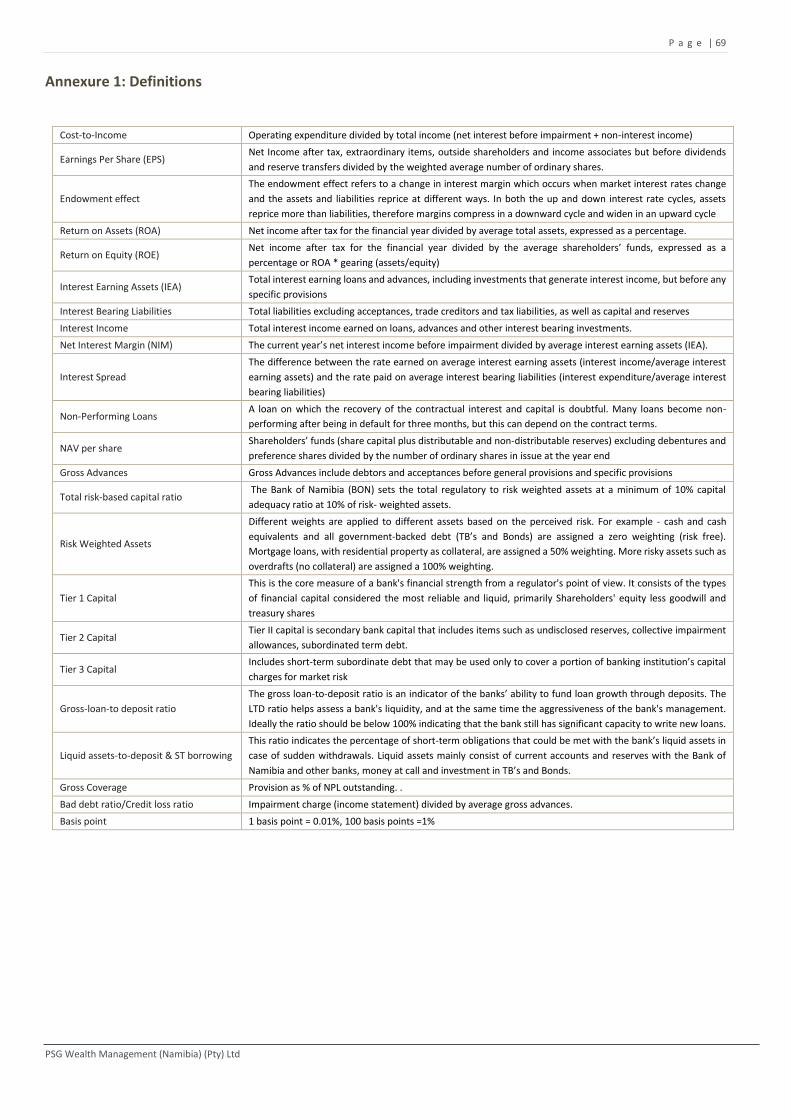

Annexure 1: Definitions .............................................................................................................................................. 69

Annexure 2: Rating and Ratio Definitions .................................................................................................................... 70

Annexure 3: Financial Data ......................................................................................................................................... 71

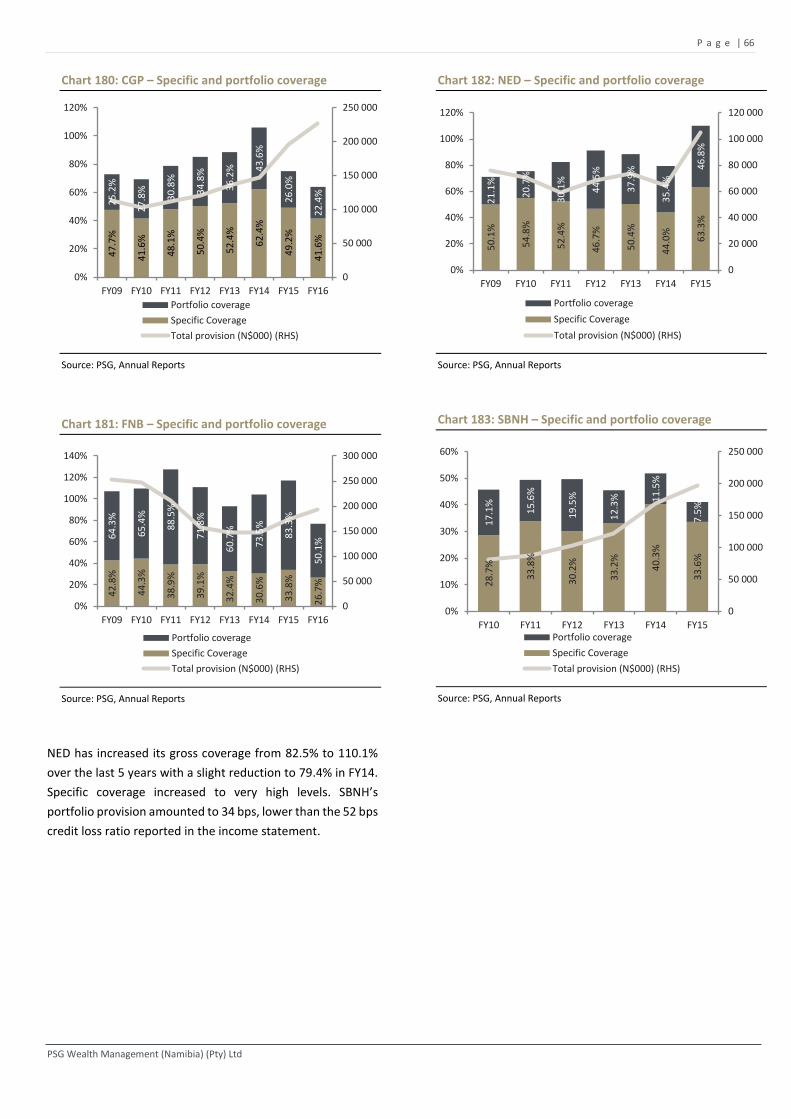

P a g e | 3

PSG Wealth Management (Namibia) (Pty) Ltd

Introduction

The PSG Banking Review provides a detailed time series and

financial ratio analysis between the Namibian and listed South

African, Botswana and Zambian banks. However, the focus will

remain on local banks. The SA banks included in the analysis are

Standard Bank, Nedbank, FirstRand, Capitec and Barclays Group

Africa (previously Absa) while the listed Botswana banks are

Barclays, FNB Botswana and Standard Chartered. The Zambian

banks are Zanaco and Standard Chartered.

Note that the name of Bank Windhoek Holdings changed to

Capricorn Investment Group in 2016. We refer to Capricorn

Investment Group (CGP) throughout this report.

In our 2015 Banking Review, we supplemented the current

analysis by including Capitec. We have also decided to include

the most recently published financial information where it was

available. This means that the report does not refer throughout

to FY15 as in previous versions, but will speak about “as at latest

year-end”. It should be noted that the comparative analysis

amongst the local banks are based on the financial year-end

results with different year-ends (June vs. December). Also note

that Standard Bank Holdings Namibia Ltd (SBNH) data was

consolidated back for comparison purposes from FY07-FY10.

Pre-FY07 remains Standard Bank Limited (the bank) data.

The report starts by studying the dynamics and trends in market

share and Compounded Annualised Growth Rates (CAGR) over

different time periods in terms of total assets, advances,

mortgage loans, term loans, non-interest income and deposits.

Financial ratios include profitability ratios such as Return on

Equity (ROE) and Return on Assets (ROA) broken down by a two

factor Du Pont Analysis. Other ratios include net interest

margins, interest rate spreads, cost efficiency ratios and

liquidity and credit risk ratios. All the formulae and definitions

used in the report are detailed in the annexure.

We conclude the analysis with a fair value estimation of all the

local, Botswana and Zambia banks using the price-to-book

valuation model based on conservative sustainable ROE

assumptions. The fair value estimates allowed us to estimate

the market cap and dividend yield for each of the unlisted banks

for comparison purposes.

Table 1: Year-ends

February June December

Capricorn Investment Group x

FNB Namibia Holdings x

NedNamibia Holdings x

Standard Bank Namibia

Holdings

x

Barclays Group Africa x

FirstRand x

NedBank SA x

Standard Bank SA x

Capitec SA x

Barclays Botswana x

FNB Botswana x

Std. Chartered Botswana x

Std. Chartered Zambia x

Zanaco Zambia x

Source: PSG, Annual Reports

P a g e | 4

PSG Wealth Management (Namibia) (Pty) Ltd

Executive Summary

While profitability remains one of the most important goals of

banks, the efficient provision of financial services through banks

is also critical, especially for a country’s economic growth and

development. A stable and efficient banking system is vital to

provide financial services while having the capability of

absorbing unforeseen shocks through effective risk, credit and

liquidity management. While this study addresses profitability,

more importantly, it enables us to measure the bank’s overall

performance and soundness by identifying their strengths and

weaknesses in terms of other metrics such as liquidity and credit

risk policies. However, it is worthy to note that ratio analysis has

it shortcomings in that it is backward looking, instead of forward

looking.

Economic growth slowed sharply in 2016. The NSA estimates

real GDP growth at -1.2% y-o-y in Q2, down from 3.4% y-o-y in

Q1 2016. The negative growth is mainly attributable to sharp

contractions in real value added recorded by the construction (-

19.9% y-o-y), mining & quarrying (-13.2% y-o-y) and hotels &

restaurants (-15.5% y-o-y) sectors.

Private sector credit extension (PSCE) growth declined in

October, mainly as a result of a decline in demand for credit

from the corporate sector. PSCE growth decreased from 11.1%

y-o-y in September to 10.2% y-o-y in October, therefore,

remaining on a broadly downward trend since March 2015. The

annual inflation rate was estimated at 7.3% y-o-y in October,

higher than the 6.9% y-o-y increase recorded in September and

the highest annual inflation rate since November 2012. The

Namibia prime lending rate increased from 9.75% in January

2015 to 10.75% in December 2016.

In our ranking of the Namibian banks, FNB retains its first place

and all of the other rankings remain the same as well. This is

despite SBNH making up a lot of ground with improvements in

credit risk and cost efficiency. What also emerge from the

analysis is that the two listed banks stand out in terms of ROA.

While the unlisted banks are slightly lagging in terms of this

metric, SBNH have increased ROE significantly over the last

year. In terms of profitability, CGP slid during the last year due

to SBNH and NED outperforming them in 3-year EPS CAGR. NED,

however deteriorated significantly in terms of credit risk due to

worsening credit loss ratios.

Local bank assets made up 69.3% of GDP as at December 2015,

re-iterating the big role it plays it the Namibian economy.

Advances growth remained strong for the local banks at

between 11.6% and 18.3%.

Our finding, based from a range of performance ratios is that

the local banks remain sound in terms of profitability and capital

adequacy with high-quality liquid assets. On the credit risk side,

credit loss ratios remain low. As mentioned last year, we are

concerned about the increasing ratio of the mortgage loan

books that are in early arrears. This is a trend at all the local

banks and it has begun to filter through to impairments.

Although some of the banks experienced margin pressure over

the last 5 years, net interest margins (NIM) have been resilient,

and local banks have benefitted from the rising interest rate

environment. Credit risk did deteriorate slightly, but credit

losses are still well below industry accepted levels. All the local

banks reported double digit annualised compounded growth in

earnings over the last three years, but we could see this taper

as advances growth slows in the challenging economic

environment.

The SA banks experienced mixed results in their EPS growth

numbers over the last year but NPL ratios continue to gradually

improve. Operational expenses growth outpacing asset growth

for most of the SA banks over 5 years creates challenges.

Besides Capitec, SBK SA and BGA are the only banks which grew

assets ahead of opex marginally over 5 years. Credit quality for

the SA banks has remained good. Drawing a comparison

between local banks and SA banks, the analysis reflects the

superior net interest margins, ROE, ROA and credit quality of

local banks for the last year, but the trend is that SA banks’

credit quality is improving, while the Namibian banks are seeing

headwinds.

The two listed Zambian banks have suffered severely over the

last year with earnings declining at double digit rates attributed

to high operating cost and low revenue growth. Cost-to-income

ratios for both banks have increased, but Standard Chartered

Zambia did grow assets ahead of the operating costs. ROE

declined for both banks despite the increase in interest rates in

Zambia. The Zambian banking system is under severe pressure,

and Zanaco specifically have experienced a spike in NPLs. From

the performance metrics broadly, it looks like Standard

Chartered is more resilient in these tough times.

The Botswana banks saw earnings decline by more than 20%

over the last year. Standard Chartered Botswana performed the

worst with earnings declining by 85%. Botswana banks

generally have higher NIM than local and SA banks. These

margins have come under severe pressure with the declining

interest rates in Botswana. Net interest income took a huge hit

for all the Botswana banks. These banks reported NIMs of

between 6.7% and 8.0% in FY13, but this has reduced to 4.0%

to 7.0%.

The outlook for local banks remain positive, although there will

be a period of slower growth and increased credit losses over

the next 18 to 24 months. They remain profitable, well

capitalised with acceptable credit quality.

P a g e | 5

PSG Wealth Management (Namibia) (Pty) Ltd

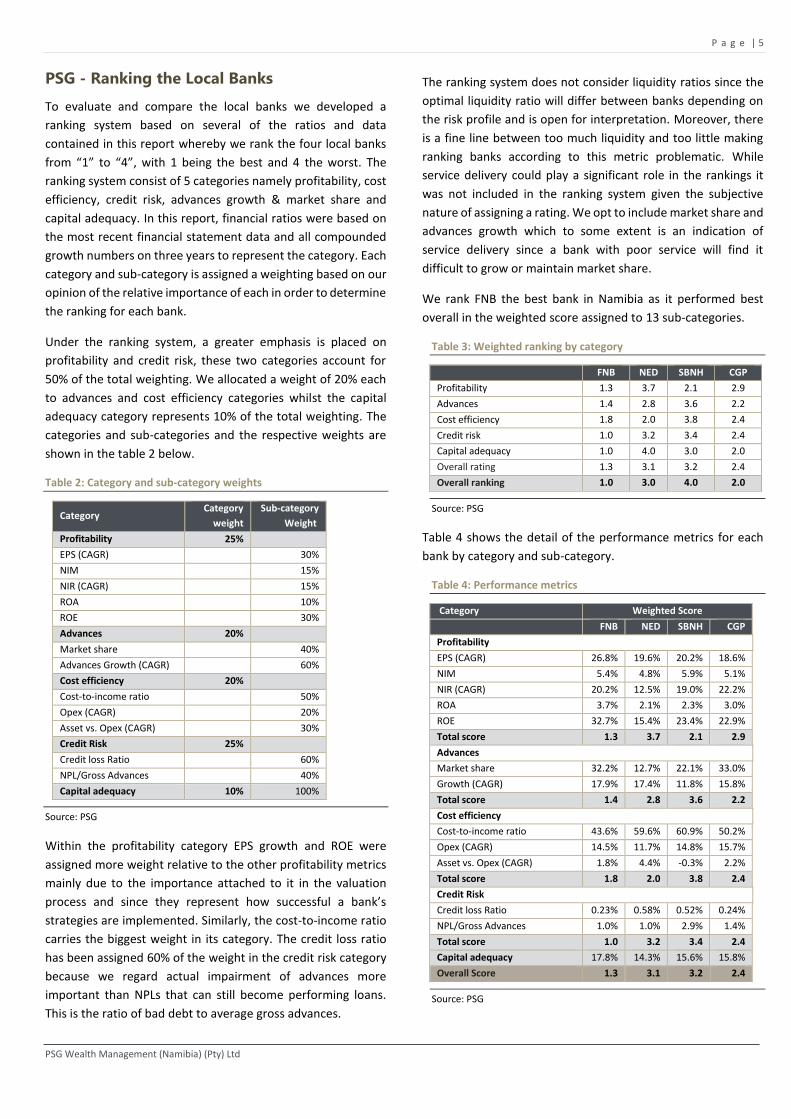

PSG - Ranking the Local Banks

To evaluate and compare the local banks we developed a

ranking system based on several of the ratios and data

contained in this report whereby we rank the four local banks

from “1” to “4”, with 1 being the best and 4 the worst. The

ranking system consist of 5 categories namely profitability, cost

efficiency, credit risk, advances growth & market share and

capital adequacy. In this report, financial ratios were based on

the most recent financial statement data and all compounded

growth numbers on three years to represent the category. Each

category and sub-category is assigned a weighting based on our

opinion of the relative importance of each in order to determine

the ranking for each bank.

Under the ranking system, a greater emphasis is placed on

profitability and credit risk, these two categories account for

50% of the total weighting. We allocated a weight of 20% each

to advances and cost efficiency categories whilst the capital

adequacy category represents 10% of the total weighting. The

categories and sub-categories and the respective weights are

shown in the table 2 below.

Table 2: Category and sub-category weights

Category Category

weight

Sub-category

Weight

Profitability 25%

EPS (CAGR) 30%

NIM 15%

NIR (CAGR) 15%

ROA 10%

ROE 30%

Advances 20%

Market share 40%

Advances Growth (CAGR) 60%

Cost efficiency 20%

Cost-to-income ratio 50%

Opex (CAGR) 20%

Asset vs. Opex (CAGR) 30%

Credit Risk 25%

Credit loss Ratio 60%

NPL/Gross Advances 40%

Capital adequacy 10% 100%

Source: PSG

Within the profitability category EPS growth and ROE were

assigned more weight relative to the other profitability metrics

mainly due to the importance attached to it in the valuation

process and since they represent how successful a bank’s

strategies are implemented. Similarly, the cost-to-income ratio

carries the biggest weight in its category. The credit loss ratio

has been assigned 60% of the weight in the credit risk category

because we regard actual impairment of advances more

important than NPLs that can still become performing loans.

This is the ratio of bad debt to average gross advances.

The ranking system does not consider liquidity ratios since the

optimal liquidity ratio will differ between banks depending on

the risk profile and is open for interpretation. Moreover, there

is a fine line between too much liquidity and too little making

ranking banks according to this metric problematic. While

service delivery could play a significant role in the rankings it

was not included in the ranking system given the subjective

nature of assigning a rating. We opt to include market share and

advances growth which to some extent is an indication of

service delivery since a bank with poor service will find it

difficult to grow or maintain market share.

We rank FNB the best bank in Namibia as it performed best

overall in the weighted score assigned to 13 sub-categories.

Table 3: Weighted ranking by category

FNB NED SBNH CGP

Profitability 1.3 3.7 2.1 2.9

Advances 1.4 2.8 3.6 2.2

Cost efficiency 1.8 2.0 3.8 2.4

Credit risk 1.0 3.2 3.4 2.4

Capital adequacy 1.0 4.0 3.0 2.0

Overall rating 1.3 3.1 3.2 2.4

Overall ranking 1.0 3.0 4.0 2.0

Source: PSG

Table 4 shows the detail of the performance metrics for each

bank by category and sub-category.

Table 4: Performance metrics

Category Weighted Score

FNB NED SBNH CGP

Profitability

EPS (CAGR) 26.8% 19.6% 20.2% 18.6%

NIM 5.4% 4.8% 5.9% 5.1%

NIR (CAGR) 20.2% 12.5% 19.0% 22.2%

ROA 3.7% 2.1% 2.3% 3.0%

ROE 32.7% 15.4% 23.4% 22.9%

Total score 1.3 3.7 2.1 2.9

Advances

Market share 32.2% 12.7% 22.1% 33.0%

Growth (CAGR) 17.9% 17.4% 11.8% 15.8%

Total score 1.4 2.8 3.6 2.2

Cost efficiency

Cost-to-income ratio 43.6% 59.6% 60.9% 50.2%

Opex (CAGR) 14.5% 11.7% 14.8% 15.7%

Asset vs. Opex (CAGR) 1.8% 4.4% -0.3% 2.2%

Total score 1.8 2.0 3.8 2.4

Credit Risk

Credit loss Ratio 0.23% 0.58% 0.52% 0.24%

NPL/Gross Advances 1.0% 1.0% 2.9% 1.4%

Total score 1.0 3.2 3.4 2.4

Capital adequacy 17.8% 14.3% 15.6% 15.8%

Overall Score 1.3 3.1 3.2 2.4

Source: PSG

P a g e | 6

PSG Wealth Management (Namibia) (Pty) Ltd

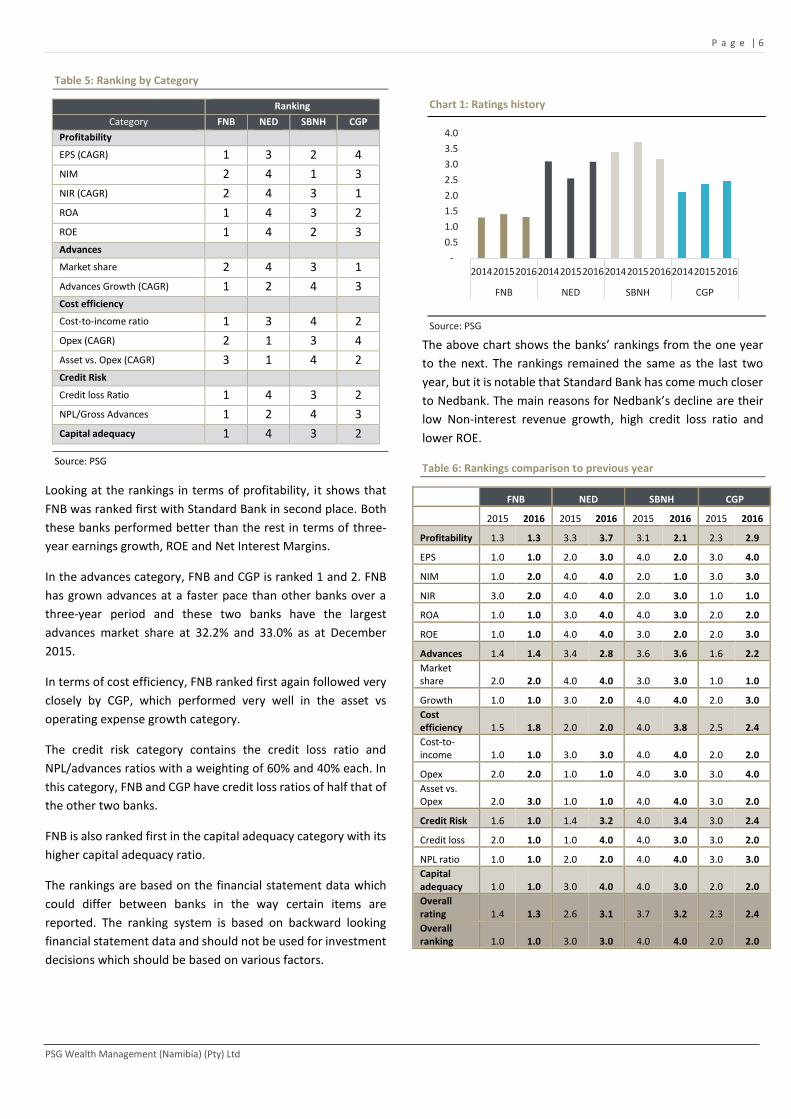

Table 5: Ranking by Category

Ranking

Category FNB NED SBNH CGP

Profitability

EPS (CAGR) 1 3 2 4

NIM 2 4 1 3

NIR (CAGR) 2 4 3 1

ROA 1 4 3 2

ROE 1 4 2 3

Advances

Market share 2 4 3 1

Advances Growth (CAGR) 1 2 4 3

Cost efficiency

Cost-to-income ratio 1 3 4 2

Opex (CAGR) 2 1 3 4

Asset vs. Opex (CAGR) 3 1 4 2

Credit Risk

Credit loss Ratio 1 4 3 2

NPL/Gross Advances 1 2 4 3

Capital adequacy 1 4 3 2

Source: PSG

Looking at the rankings in terms of profitability, it shows that

FNB was ranked first with Standard Bank in second place. Both

these banks performed better than the rest in terms of three-

year earnings growth, ROE and Net Interest Margins.

In the advances category, FNB and CGP is ranked 1 and 2. FNB

has grown advances at a faster pace than other banks over a

three-year period and these two banks have the largest

advances market share at 32.2% and 33.0% as at December

2015.

In terms of cost efficiency, FNB ranked first again followed very

closely by CGP, which performed very well in the asset vs

operating expense growth category.

The credit risk category contains the credit loss ratio and

NPL/advances ratios with a weighting of 60% and 40% each. In

this category, FNB and CGP have credit loss ratios of half that of

the other two banks.

FNB is also ranked first in the capital adequacy category with its

higher capital adequacy ratio.

The rankings are based on the financial statement data which

could differ between banks in the way certain items are

reported. The ranking system is based on backward looking

financial statement data and should not be used for investment

decisions which should be based on various factors.

Chart 1: Ratings history

Source: PSG

The above chart shows the banks’ rankings from the one year

to the next. The rankings remained the same as the last two

year, but it is notable that Standard Bank has come much closer

to Nedbank. The main reasons for Nedbank’s decline are their

low Non-interest revenue growth, high credit loss ratio and

lower ROE.

Table 6: Rankings comparison to previous year

FNB NED SBNH CGP

2015 2016 2015 2016 2015 2016 2015 2016

Profitability 1.3 1.3 3.3 3.7 3.1 2.1 2.3 2.9

EPS 1.0 1.0 2.0 3.0 4.0 2.0 3.0 4.0

NIM 1.0 2.0 4.0 4.0 2.0 1.0 3.0 3.0

NIR 3.0 2.0 4.0 4.0 2.0 3.0 1.0 1.0

ROA 1.0 1.0 3.0 4.0 4.0 3.0 2.0 2.0

ROE 1.0 1.0 4.0 4.0 3.0 2.0 2.0 3.0

Advances 1.4 1.4 3.4 2.8 3.6 3.6 1.6 2.2

Market share 2.0 2.0 4.0 4.0 3.0 3.0 1.0 1.0

Growth 1.0 1.0 3.0 2.0 4.0 4.0 2.0 3.0

Cost efficiency 1.5 1.8 2.0 2.0 4.0 3.8 2.5 2.4

Cost-to-income 1.0 1.0 3.0 3.0 4.0 4.0 2.0 2.0

Opex 2.0 2.0 1.0 1.0 4.0 3.0 3.0 4.0

Asset vs. Opex 2.0 3.0 1.0 1.0 4.0 4.0 3.0 2.0

Credit Risk 1.6 1.0 1.4 3.2 4.0 3.4 3.0 2.4

Credit loss 2.0 1.0 1.0 4.0 4.0 3.0 3.0 2.0

NPL ratio 1.0 1.0 2.0 2.0 4.0 4.0 3.0 3.0

Capital adequacy 1.0 1.0 3.0 4.0 4.0 3.0 2.0 2.0

Overall rating 1.4 1.3 2.6 3.1 3.7 3.2 2.3 2.4

Overall ranking 1.0 1.0 3.0 3.0 4.0 4.0 2.0 2.0

-

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

201420152016201420152016201420152016201420152016

FNB NED SBNH CGP

P a g e | 7

PSG Wealth Management (Namibia) (Pty) Ltd

Nature of business

Local Banks

Capricorn Group Holdings (CGP)

CGP is an investment holding company with a 100%

shareholding in Bank Windhoek Ltd, Namib Bou (Pty) Limited,

Capricorn Unit Trust Management Company Limited (CUTM)

and Capricorn Asset Management (Pty) Ltd (CAM). Bank

Windhoek Ltd is one of the largest commercial banks in

Namibia. CGP also has strategic interests in Santam Namibia

(28%) and Sanlam Namibia (29.5%). Capricorn Investment

Holdings (CIH) has a 56.81% shareholding in CGP. The group

offers a complete range of retail, business, corporate and

investment banking, insurance and wealth management. CGP

announced in December 2016 that they will acquire 65% of the

issued share capital of Capricorn Investment Holdings

(Botswana) Limited, which owns 100% of the share capital of

Bank Gaborone, and 97.9% of Cavmont Capital Holdings Zambia

Plc, which owns 100% of the share capital of Cavmont Bank.

FNB Namibia Holdings (FNB)

FNB Namibia Holdings has a 100% shareholding in First National Bank

of Namibia Limited. South African group, FirstRand EMA Holdings is

the majority shareholder of FNB, with a 58.4% shareholding. GIPF holds

14.8% with the remainder of the shareholding held by the general

public. Five percent of FirstRand’s has been allocated to a black

empowerment group, with 1% allocated to black employees and 4% to

a BEE Consortium. The BEE consortium consists of two groups, namely

Sovereign Capital and Chappa’Ai Investments. FNB also have a 51%

holding in OUTsurance Insurance Company Namibia (Pty) Limited. The

group also has a 100% holding in RMB Namibia (Pty) Ltd and FNB

Namibia Unit Trusts Limited. FNB recently concluded a transaction to

purchase 100% of the shares in Pointbreak.

NedNamibia Holdings (NED)

Nedbank Group Limited is the South African controlling shareholder

(100%) of NedNamibia Holdings Limited. NedNamiba Holdings Ltd has

a 100% interest in Nedbank Namibia Limited and also in the following

subsidiaries: NedProperties (Pty) Limited, NedCapital Namibia (Pty)

Limited, NedPlan Insurance Brokers Namibia (Pty) Limited and

Coversure Limited. Nedbank Namibia Ltd holds a 100% shareholding in

CBN Nominees (Pty) Limited, 25% in Namclear (Pty) Limited, 80% in

Nedloans (Pty) Limited, 50% in Ten Kaiser Wilhelm Strasse (Pty) Limited

and 50% in Walvis Bay Land Syndicate (Pty) Limited.

Standard Bank Namibia Holdings Limited (SBNH)

The Standard Bank Group Limited, registered and listed in South

Africa and dual listed on the NSX, transferred its ownership to

Standard Bank Holdings Limited effective 01 January 2011.

Standard Bank Holdings Limited acts as an investment holding

company with 100% shareholding in Standard Insurance

Brokers (Namibia) (Proprietary) Limited, (a short term insurance

broker), Stanfin (Namibia) (Proprietary) Limited, (a long term

insurance broker) and Standard Bank Namibia Limited.

P a g e | 8

PSG Wealth Management (Namibia) (Pty) Ltd

SA Banks

Barclays Group Africa (BGA) Barclays Group Africa, one of the big four banks in South Africa,

was established in 1999. Barclays acquired a controlling stake in

2006, and raised its shareholding further to 62.3% in July 2013.

BGA offers a complete range of retail, business, corporate and

investment banking, plus insurance and wealth management.

FirstRand (FSR)

FirstRand was created in 1998 through the merger of the

financial services interests of Anglo American and RMB

Holdings. Subsidiaries include FNB (retail & corporate),

WesBank (asset finance & unsecured lending), RMB (corporate

& investment banking).

NedBank SA (NED SA)

Nedbank, a subsidiary of Old Mutual, has been listed on the JSE

since 1969. It focuses on southern Africa, offering corporate

banking, business banking, investment banking, retail banking,

wealth management and bancassurance. Having made a big

loss in 2003, it was recapitalised through a rights issue. Nedbank

generates most of its earnings from corporate and investment

banking, but is also rebuilding its retail franchise, which has

been lagging the other big banks.

Standard Bank SA (SBK SA)

Standard Bank was listed on the JSE in 1970. The group offers

corporate & investment banking and retail banking. It has a

controlling stake in Liberty Holdings, a listed insurer. SBK is

operating in 17 African countries. Having embarked on

expansion into emerging markets before the global financial

crisis, it is now refocusing its strategy on Africa.

Capitec (CPI)

Capitec Bank Holdings Limited has been listed on the JSE since

2002. The Company's subsidiaries conduct retail banking. The

Company owns 100% of its principal subsidiary, Capitec Bank

Limited (Capitec Bank). Capitec Bank is a retail bank, which

focuses on banking services and provides savings, transacting

and unsecured lending products to individuals. Capitec does not

at this stage provide any services to businesses Home loan

origination is provided but it is outsourced to SA Home Loans

P a g e | 9

PSG Wealth Management (Namibia) (Pty) Ltd

Botswana Banks

Barclays Bank Botswana (BBB) The Bank is controlled by Barclays Africa Group Limited which

owns 67.82% of the ordinary shares, which is a subsidiary of

Barclays PLC (incorporated in the United Kingdom). The

remaining 32.18% of the shares are widely held. The bank

employs 1 247 people and has 43 branches and 115 ATMs

throughout the country. Their consumer business serves

customers across a network of 43 branches, which is the largest

branch network in Botswana, and 115 ATMs.

First National Bank of Botswana (FNBB)

FNBB was registered in 1991, as a wholly owned subsidiary of

First National Bank Holdings (Botswana). The Bank became a

listed entity on the Botswana Stock Exchange in 1993. The

Company’s stated capital consists of 2 563 700 000 ordinary

shares, of which First National Bank Holdings (Botswana)

Limited holds 1 780 590 000 shares (69.45%), and the balance is

traded on the Botswana Stock Exchange (BSE).

Standard Chartered Botswana (SCB)

SCB first opened for business in 1897, making it the country's

oldest bank. The Bank was locally incorporated in 1975 with a

full board. The bank operates with 19 branches and 25% of its

shares are listed on the Botswana Stock Exchange.

Zambian Banks

Standard Chartered Bank of Zambia (SCZ)

The bank was established in 1906 and has a total of 25 branches

spread across the country, 47 automated teller machines

(ATMs) and 719 employees. The Bank, which is a registered

commercial bank under the Zambian Banking and Financial

Services Act 1994, is owned 90% by Standard Chartered

Holdings (Africa) BV, a company incorporated in the

Netherlands, which in turn is wholly owned by Standard

Chartered Plc, a company incorporated in the England and

Wales.

Zambia National Commercial Bank Plc (Zanaco)

Zanaco was established in 1969. The bank remains majority-

owned by Zambians. In 2007, the Government of Zambia sold a

49% stake in the bank to Rabo Financial Institutions

Development (RFID) a subsidiary of Rabobank of the

Netherlands. Following the Banks Initial public offer in 2008

RFID sold 3.41% stake to Lizara Investments Limited (a nominee

of the Zambia National Farmers Union (ZNFU). Current

shareholding 25% GRZ, 45.59% RFID, 3.41% ZNFU and 25.6%

free float.

P a g e | 10

PSG Wealth Management (Namibia) (Pty) Ltd

Economic Review and Outlook

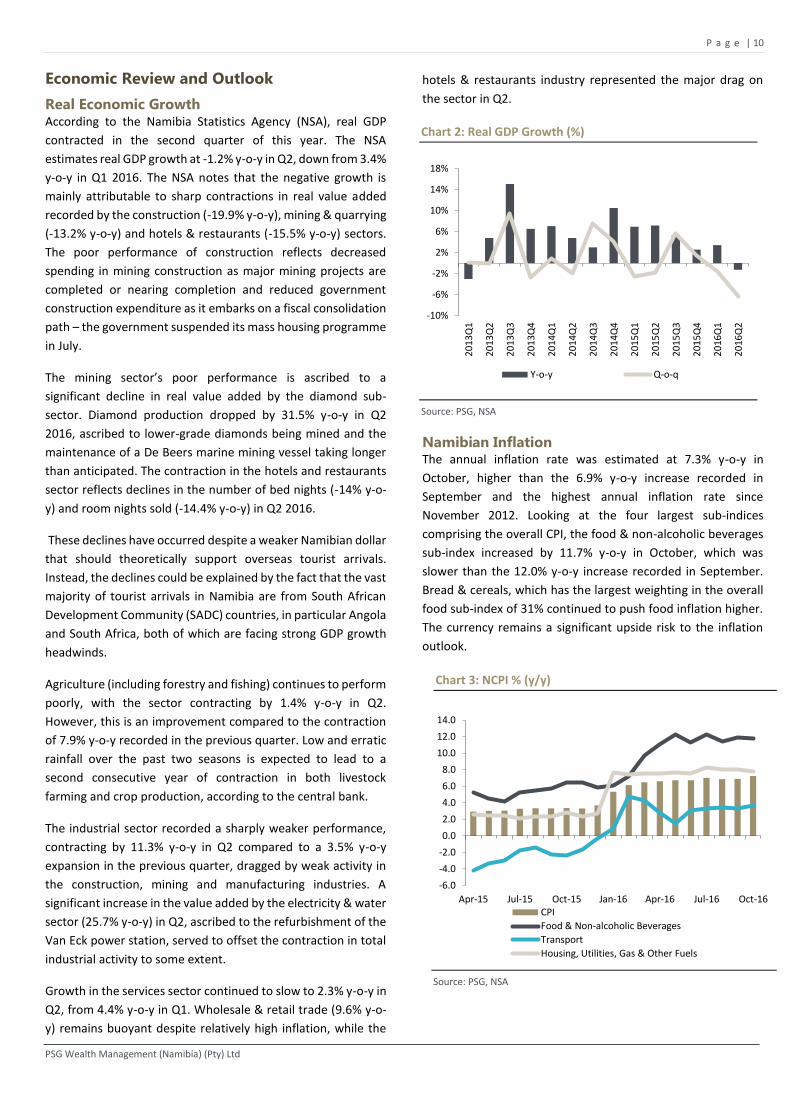

Real Economic Growth According to the Namibia Statistics Agency (NSA), real GDP

contracted in the second quarter of this year. The NSA

estimates real GDP growth at -1.2% y-o-y in Q2, down from 3.4%

y-o-y in Q1 2016. The NSA notes that the negative growth is

mainly attributable to sharp contractions in real value added

recorded by the construction (-19.9% y-o-y), mining & quarrying

(-13.2% y-o-y) and hotels & restaurants (-15.5% y-o-y) sectors.

The poor performance of construction reflects decreased

spending in mining construction as major mining projects are

completed or nearing completion and reduced government

construction expenditure as it embarks on a fiscal consolidation

path – the government suspended its mass housing programme

in July.

The mining sector’s poor performance is ascribed to a

significant decline in real value added by the diamond sub-

sector. Diamond production dropped by 31.5% y-o-y in Q2

2016, ascribed to lower-grade diamonds being mined and the

maintenance of a De Beers marine mining vessel taking longer

than anticipated. The contraction in the hotels and restaurants

sector reflects declines in the number of bed nights (-14% y-o-

y) and room nights sold (-14.4% y-o-y) in Q2 2016.

These declines have occurred despite a weaker Namibian dollar

that should theoretically support overseas tourist arrivals.

Instead, the declines could be explained by the fact that the vast

majority of tourist arrivals in Namibia are from South African

Development Community (SADC) countries, in particular Angola

and South Africa, both of which are facing strong GDP growth

headwinds.

Agriculture (including forestry and fishing) continues to perform

poorly, with the sector contracting by 1.4% y-o-y in Q2.

However, this is an improvement compared to the contraction

of 7.9% y-o-y recorded in the previous quarter. Low and erratic

rainfall over the past two seasons is expected to lead to a

second consecutive year of contraction in both livestock

farming and crop production, according to the central bank.

The industrial sector recorded a sharply weaker performance,

contracting by 11.3% y-o-y in Q2 compared to a 3.5% y-o-y

expansion in the previous quarter, dragged by weak activity in

the construction, mining and manufacturing industries. A

significant increase in the value added by the electricity & water

sector (25.7% y-o-y) in Q2, ascribed to the refurbishment of the

Van Eck power station, served to offset the contraction in total

industrial activity to some extent.

Growth in the services sector continued to slow to 2.3% y-o-y in

Q2, from 4.4% y-o-y in Q1. Wholesale & retail trade (9.6% y-o-

y) remains buoyant despite relatively high inflation, while the

hotels & restaurants industry represented the major drag on

the sector in Q2.

Namibian Inflation The annual inflation rate was estimated at 7.3% y-o-y in

October, higher than the 6.9% y-o-y increase recorded in

September and the highest annual inflation rate since

November 2012. Looking at the four largest sub-indices

comprising the overall CPI, the food & non-alcoholic beverages

sub-index increased by 11.7% y-o-y in October, which was

slower than the 12.0% y-o-y increase recorded in September.

Bread & cereals, which has the largest weighting in the overall

food sub-index of 31% continued to push food inflation higher.

The currency remains a significant upside risk to the inflation

outlook.

Chart 2: Real GDP Growth (%)

Source: PSG, NSA

Chart 3: NCPI % (y/y)

Source: PSG, NSA

-10%

-6%

-2%

2%

6%

10%

14%

18%

20

13Q

1

20

13Q

2

20

13Q

3

20

13Q

4

20

14Q

1

20

14Q

2

20

14Q

3

20

14Q

4

20

15Q

1

20

15Q

2

20

15Q

3

20

15Q

4

20

16Q

1

20

16Q

2

Y-o-y Q-o-q

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

Apr-15 Jul-15 Oct-15 Jan-16 Apr-16 Jul-16 Oct-16CPI

Food & Non-alcoholic Beverages

Transport

Housing, Utilities, Gas & Other Fuels

P a g e | 11

PSG Wealth Management (Namibia) (Pty) Ltd

Private Sector Credit Extension (PSCE)

Private sector credit extension (PSCE) growth declined in

October, mainly as a result of a decline in demand for credit

from the corporate sector, according to the Bank of Namibia’s

(BoN, the central bank) recently released Money and Banking

Statistics report. PSCE growth decreased from 11.1% y-o-y in

September to 10.2% y-o-y in October, therefore, remaining on

a broadly downward trend since March 2015.

Growth in credit extended to businesses dropped by 90.2 bps

to 10.2% y-o-y in October, while credit growth to households

remained unchanged at 9.7% y-o-y. The growth in mortgage

credit, which accounts for more than 50% of total PSCE, slowed

to 9.4% y-o-y in October, compared to 10.1% y-o-y in the

preceding month.

Elsewhere in the report, the central bank said that the stock of

international reserves dropped to N$25.1bn at the end of

October, from N$26.5bn in the prior month. “The decrease

emanated mainly from net government payments and net

foreign currency purchases by commercial banks during the

reviewed period,” the BoN said.

Chart 4: PSCE (% y/y)

Source: BoN

Monetary Policy

The Monetary Policy Committee (MPC) of the Bank of Namibia

(BoN, the central bank) decided to keep the repo rate

unchanged following its most recent meeting. The policy rate

therefore remains stable at 7%. According to the MPC, a repo

rate at this level “is appropriate to support growth and maintain

the one-to-one link of the Namibian dollar to the South African

rand”. The central bank states that since the previous MPC

meeting in October 2016, monetary policy stances in both key

advanced economies and emerging market economies have

remained accommodative.

No doubt the South African Reserve Bank’s (SARB) decision to

keep its policy rate unchanged in November contributed to the

decision to hold Namibian rates steady. Furthermore, the BoN’s

decision was supported by the downward trend in private

sector credit extension (PSCE) growth and a sharp drop in

overall economic growth during the first 10 months of 2016.

PSCE growth slowed to an average of 11.8% y-o-y over the first

10 months of 2016, compared to 15.5% y-o-y for the same

period in 2015.

According to the central bank, weaker economic growth is

ascribed to declines in the production of diamonds and zinc as

well as slower growth in the construction, agriculture and

transport sectors. However, wholesale & retail trade as well as

communications continue to perform well. The BoN still

projects real GDP growth of 2.5% in 2016, sharply lower than

the 5.3% recorded in 2015.

Chart 5: Namibian vs. South African Interest Rates

Source: PSG

Nevertheless, the outlook for monetary policy remains very

uncertain and the exchange rate continues to be a significant

upside risk to the inflation outlook. In recent months, the

inflation rate kept close to 7% y-o-y and we still expect price

pressures to remain elevated in 2017.

A source of depreciatory pressure on the rand is the substantial

risk that South Africa will lose its investment-grade status

during the course of 2017. Despite the recent decisions by credit

rating agencies not to downgrade South Africa’s foreign

currency credit rating, both S&P Global Ratings and Fitch

Ratings now have the country on “BBB-” with a negative

outlook.

Looking ahead, our baseline expectation is for the BoN to raise

the repo rate by 25 bps during 2017. This is on the back of our

projected 50 bps hike in the US federal funds rate next year,

which will put pressure on the Namibian dollar, as well as our

expectation of elevated food and administrated prices well into

2017.

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

Oct

-15

No

v-15

Dec

-15

Jan

-16

Feb

-16

Mar

-16

Ap

r-16

May

-16

Jun

-16

Jul-

16

Au

g-16

Sep

-16

Oct

-16

%ch

g, y

-o-y

PSCE Corporates Households

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

Jan

-14

Mar

-14

May

-14

Jul-

14

Sep

-14

No

v-1

4

Jan

-15

Mar

-15

May

-15

Jul-

15

Sep

-15

No

v-1

5

Jan

-16

Mar

-16

May

-16

Jul-

16

Sep

-16

No

v-1

6

Nam Prime SA Prime

Nam repo SA Repo rate

Nam Real Interest

P a g e | 12

PSG Wealth Management (Namibia) (Pty) Ltd

Local Banks - Financial Results Review

At time of writing this report, the two local listed banks, FNB and CGP have

already published annual results for the year ended June 2016.

CGP

After reporting strong interim results, advances growth slowed

in the second half of FY16. Headline earnings increased by

20.5% from 151 cps in FY15 to 182cps in FY16. The net interest

margin (IEA) after impairment charges remained resilient at

4.9% on the back of 15.1% growth in net interest income despite

lower advances growth of 12.6%.

In FY16 there was an increase of 65 bps in interest income on

average IEA and an increase of 82 bps in the interest expense

on average interest paying assets.

After peaking at 62.9% in 2010, the cost-to-income ratio has

consistently come down and has improved to 50.2% in the 2016

financial year. This has been because of increased income but

also a substantial curbing of operating cost growth in the last

two years.

The loan to deposit ratio increased further to 111%. This ratio

remaining above 100% shows the bank is not only relying on

deposits to fund loan growth but also on borrowed funds.

ROE increased further over the last year from 22.4% to 22.9%.

While gearing has continued to come down over the three-year

period, it was offset by strong improvement in asset utilisation

from 2.8% in FY15 to 3.0% in FY16 keeping ROE above 22%.

Despite this, the liquid assets to deposits and short term

borrowing figure improved further to 19.5% from 18.3% in

FY15. CGP is well capitalised with a total capital adequacy ratio

of 15.8%.

The group declared a total dividend of 66 cps up 10.6% from last

year (53cps).

Table 7: CGP - Key Financial Data at Year-end

FY14 FY15 FY16

Growth net interest income 15.6% 19.9% 15.1%

Growth non-interest income 29.9% 19.4% 17.5%

ROA 2.6% 2.6% 2.8%

ROE 21.9% 22.4% 22.9%

Interest margin (Avg. IEA) 4.8% 4.8% 4.9%

Cost- to-income 53.6% 51.6% 50.2%

Gross advances growth (%) 14.7% 16.7% 12.6%

NPL/Avg. Advances 0.7% 0.7% 1.4%

Credit loss Ratio (%) 0.15% 0.26% 0.24%

Compensation ratio (%) 28.3% 27.5% 27.9%

DPS (cps) 44 53 66

Capital Adequacy (%) 15.8% 15.8% 15.8%

Growth operating Cost (%) 19.9% 13.9% 13.2%

Source: PSG, Annual Reports

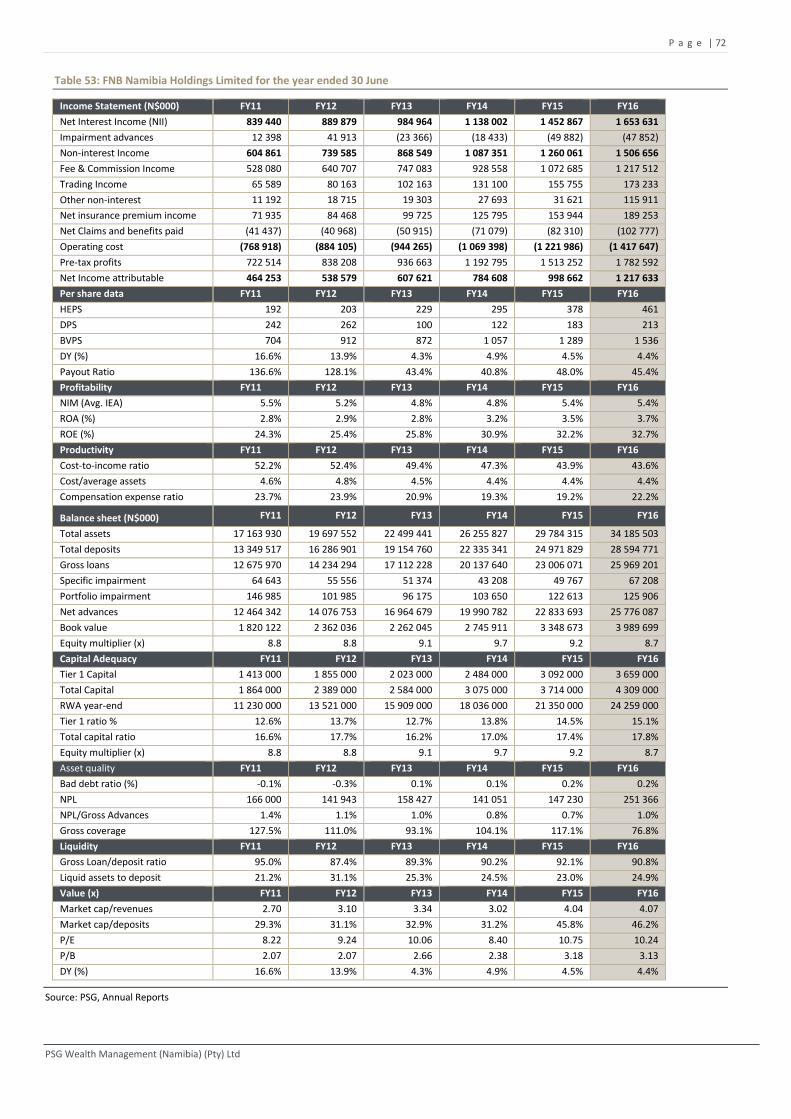

FNB

FNB reported an excellent set of financial results for the 12

months ended 30 June 2016. The group increased headline

earnings by 22.0% for the year. Non-interest income growth at

19.6% was higher than our forecasted 14.9%, but net interest

income was lower which meant that Profit before tax growth of

17.8% is in line with our expectations.

FY16 has been more challenging, there was an increase of 40

bps in interest income on average IEA and an increase of 48 bps

in the interest expense on average interest paying assets.

Non-performing loans were also higher at 0.97% but is

influenced by a large commercial transaction write-off which is

expected to be recovered.

The size of the growth in digital channels is significant and the

continued strong growth in non-interest income despite the

removal of cash deposit fees for individuals and SMEs. Also, the

strong growth in deposits bodes very well for the future funding

requirements of the bank.

Credit losses, however, have remained at very low levels of

below 1% and even during the current economic slowdown it

has not increased in FY16. We are seeing that NPLs are

increasing as expected from 0.7% to 1.0%.

The group declared a total dividend of 213 cps up 16.4% from

last year (183cps). ROE improved further from 32.2% in FY15 to

32.7% in FY16 driven by a significant increase in ROA from 3.5%

to 3.7%.

Table 8: FNB - Key Financial Data at Year-end

FY14 FY15 FY16

Growth net interest income 15.5% 27.7% 13.8%

Growth non-interest income 25.2% 15.9% 19.6%

ROA 3.2% 3.5% 3.7%

ROE 30.9% 32.2% 32.7%

Interest margin (Avg. IEA) 4.8% 5.4% 5.4%

Cost- to-income 47.3% 43.9% 43.6%

Gross advances growth (%) 17.8% 14.2% 12.9%

NPL/Avg. Advances 0.8% 0.7% 1.0%

Credit loss Ratio (%) 0.10% 0.23% 0.23%

Compensation ratio (%) 19.3% 19.2% 22.2%

DPS (cps) 122 183 213

Capital Adequacy (%) 17.0% 17.4% 17.8%

Growth operating Cost (%) 13.3% 14.3% 16.0%

Source: PSG, Annual Reports

P a g e | 13

PSG Wealth Management (Namibia) (Pty) Ltd

NED

NED reported an average set of financial results for the 12

months ending 30 December 2015. EPS increased by 10.8%. Net

interest income growth accelerated strongly to 31.2% but

interest expenditure growth was even higher at 40.0%.

There was a strong increase in net interest margins (IEA) to 4.8%

from 4.6% and high advances growth of 18.3%. This came at a

cost, however with bad debt charges soaring to N$53 million

from N$4.3 million. NPL as % of gross advances reduced further

to 1.0%.

The gains made in cost efficiency in FY14 was reversed in FY15,

with the cost-to-income ratio returning to 59.6% from 56.6%

The group has not paid a dividend since 2005. ROE declined

from 16.5% in FY14 to 15.4% in FY15, and still remains below

the other local banks.

Table 9: NED - Key Financial Data at Year-end

FY13 FY14 FY15

Growth net interest income 7.2% 24.3% 31.2%

Growth non-interest income 18.9% 10.5% 8.4%

ROA 2.1% 2.3% 2.1%

ROE 16.1% 16.5% 15.4%

Interest margin (Avg. IEA) 4.7% 4.6% 4.8%

Cost- to-income 59.9% 56.6% 59.6%

Gross advances growth (%) 14.4% 19.5% 18.3%

NPL/Avg. Advances 1.3% 1.1% 1.0%

Credit loss Ratio (%) 0.1% 0.0% 0.4%

Compensation ratio (%) 26.0% 27.0% 27.4%

DPS (cps) ND ND ND

Capital Adequacy (%) 14.3% 14.3% 14.3%

Growth operating Cost (%) 8.9% 8.7% 17.6%

Source: PSG, Annual Reports, ND = No Dividend

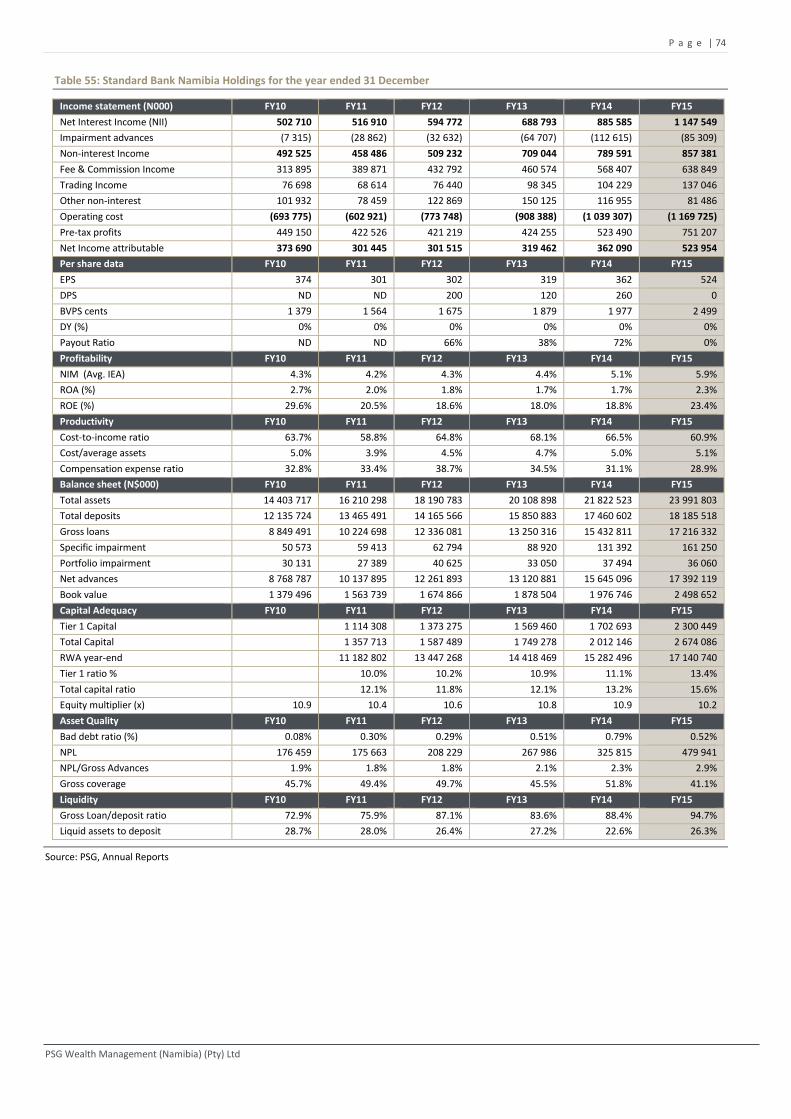

SBNH

SBNH reported results as at 31 December 2015 which were

significantly better than expected with earnings growth at

44.7%, amid continued declining advances growth.

Significant improvement in ROA from 1.7% to 2.3% driving ROE

up to 23.4% from a previous 18.8%. Deposit growth was very

low at 4.2%

The credit loss ratio amounted to 0.44% of total advances, a

significant improvement from the 0.65% for FY14. Net interest

income rose by 29.6% while non-interest revenue grew by 8.6%.

Operating cost was 12.5% higher than the previous year,

resulting in the cost-to-income (after impairment) ratio

declining from 66.5% in FY14 to 60.9% in FY15, the highest

among local banks. SBNH reported a NPL/Advances ratio of

2.9%, the same as in FY14.

The NPL ratio remains the highest among local banks,

nevertheless still favourable below the 3% acceptable level. Net

advances grew by 11.6% in FY15, below the average PSCE

growth rate. ROE increased from 18.8% in FY14 to 23.4% in

FY15. The group declared a total dividend of 260 cps in FY14,

but did not declare any dividends in FY15.

Table 10: SBNH - Key Financial Data at Year-end

FY13 FY14 FY15

Growth net interest income 15.8% 28.6% 29.6%

Growth non-interest income 39.2% 11.4% 8.6%

ROA 1.7% 1.7% 2.6%

ROE 18.0% 18.8% 23.4%

Interest margin (Avg. IEA) 4.4% 5.1% 5.9%

Cost- to-income 68.1% 66.5% 60.9%

Gross advances growth (%) 7.4% 16.5% 11.6%

NPL/Avg. Advances 2.9% 2.9% 2.9%

Credit loss Ratio (%) 0.5% 0.7% 0.4%

Compensation ratio (%) 34.5% 31.1% 26.0%

DPS (cps) 120 260 -

Capital Adequacy (%) 12.1% 13.2% 15.6%

Growth operating Cost (%) 17.4% 14.4% 12.5%

Source: PSG, Annual Reports, ND = No Dividend

On balance, local banks remain profitable while the overall

credit quality remains intact. The NPL/Average advances ratio

remains significantly below the accepted 3% for all the local

banks. All the banks, except for NED improved their cost-to-

income ratios, partly attributable to rising interest rates. The

pressure the economy is under will influence the housing

market which could push up credit losses and NPLs in the next

year.

P a g e | 14

PSG Wealth Management (Namibia) (Pty) Ltd

Balance Sheet

This section measures assets and gross advances as at 31

December to compare all the banks at the exact same point

in time. Interim results from CGP and FNB are used.

Bank Assets

The banking system plays an important role in the economic

development of any country. The importance of the banking

sector in the Namibian economy, in particular for the

contribution to economic growth cannot be underestimated.

Total bank assets between the four local banks as a % of

nominal GDP increased from 60.3% in 2008 to 69.3% in 2015

indicating the importance of the banking sector in Namibia.

Chart 6: Total Local Bank Assets as % of Current GDP

Source: PSG, NSA

Total assets between the four local banks amounted to

N$101.6 billion measured at 31 December 2015, up from

N$88 billion the previous year. FNB and CGP remain the two

largest banks in Namibia with total assets amounting to

N$32.5 and N$31.3bn, respectively, followed by SBNH with

N$23.9bn and NED at N$13.8bn.

Chart 7: Local Banks - Total Assets (N$billion)

Source: PSG, Annual Reports

Table 11 shows the asset market share at December 2015.

FNB remains the market leader with 32.0% of total assets,

followed closely by CGP at 30.8%. NED, the smallest in terms

of assets, increased its market share from 11.9% to 13.6%

over the 5-year period. SBNH has lost significant market share

from ten years ago from 36% to 23.6% in FY15, and is now the

third biggest bank in terms of assets at December 2015.

Table 11: Total Assets at 31 December (N$000)

N$000 2012 2013 2014 2015

FNB 20 226 000 24 793 727 28 101 816 32 479 750

NED 8 786 263 9 999 919 11 871 305 13 828 598

SBNH 18 190 783 20 108 898 21 822 523 23 991 803

CGP 20 167 542 22 761 093 26 323 929 31 346 136

Total 67 370 588 77 663 637 88 119 573 101 646 287

Source: PSG, Annual Reports

Table 12: Total Assets Market Share (%)

2011 2012 2013 2014 2015

FNB 32.5% 30.0% 31.9% 31.9% 32.0%

NED 11.9% 13.0% 12.9% 13.5% 13.6%

SBNH 25.6% 27.0% 25.9% 24.8% 23.6%

CGP 29.9% 29.9% 29.3% 29.9% 30.8%

Source: PSG, Annual Reports

Table 13 shows the Compounded Annualised Growth Rate

(CAGR) in assets over different time periods. All the banks

grew their assets at double digit growth over the last 5 years.

Table 13: Total Assets Market Share (%)

1 year 3 years 5 years

FNB 15.6% 17.1% 13.5%

NED 16.5% 16.3% 14.1%

SBNH 9.9% 9.7% 10.7%

CGP 19.1% 15.8% 14.4%

Source: PSG, Annual Reports

63.5%

60.3%

66.2%67.6%

69.0%

62.8%63.3%63.2%

69.3%

54.0%56.0%58.0%60.0%62.0%64.0%66.0%68.0%70.0%72.0%

2007 2008 2009 2010 2011 2012 2013 2014 2015

20.6

7.5

16.218.9

32.5

13.8

24.0

31.3

-

5

10

15

20

25

30

35

FNB NED SBNH CGP

N$

Bn

2011 2012 2013 2014 2015

Chart 8: Local Banks - Total Assets Market Share (%)

Source: PSG, Annual Reports

32.5%

11.9%

25.6%

29.9%32.0%

13.6%

23.6%

30.8%

0%

5%

10%

15%

20%

25%

30%

35%

FNB NED SBNH CGP

2011 2012 2013 2014 2015

P a g e | 15

PSG Wealth Management (Namibia) (Pty) Ltd

CGP has grown its assets fastest over the last year and over 5

years. FNB is the frontrunner over 3 years. SBNH has lagged in

assets growth over all periods.

Gross Advances

Total loans and advances continued to grow in 2015, at an

average rate of 15.0%, slower than the 16.9% rate in 2014.

Advances grew from N$67.8bn to N$77.9bn.

Table 14: Total Gross Advances at 31 December (N$000)

2012 2013 2014 2015

FNB 15 303 999 18 988 162 21 803 113 25 096 180

NED 6 124 565 7 008 385 8 374 544 9 907 360

SBNH 12 336 081 13 250 316 15 432 811 17 216 332

CGP 16 578 549 18 796 458 22 217 161 25 757 009

Total 50 343 194 58 043 321 67 827 629 77 976 881

Source: PSG, Annual Reports

Among the local banks, CGP have taken the lead in market

share with 33.0% of total advances or N$25.7bn, followed

closely by FNB with N$25.0 or 32.2%. SBNH and NED are

positioned at 3rd and 4th with N$17.2bn and N$9.9bn,

respectively.

Chart 9 shows CGP has retained its market share over the last

5 years at around 33.0%.

In contrast, SBNH lost some market share over the five year

period. SBNH’s market share shrunk from 23.4% to 22.1%.

NED’s market share is the same as it was 5 years ago at 12.7%.

FNB and CGP have retained their market share over 30% over

the last 5 years trading places 1 and 2 over the last few years.

All the local banks reported double digit advances growth in

2015. NED recorded by far the fastest growth of 18.3% for the

year ended December 2015, followed by FNB (15.1%) and

SBNH at 11.6%.

Table 15: CAGR for gross advances at 31 December 2015

CAGR (%) 1 year 3 years 5 years 7 years

FNB 15.1% 17.9% 15.3% 13.9%

NED 18.3% 17.4% 13.5% 12.5%

SBNH 11.6% 11.8% 14.2% 10.6%

CGP 15.9% 15.8% 15.7% 14.5%

Total 15.0% 15.7% 15.0% 13.1%

Source: PSG, Annual Reports

Chart 9: Total Gross Advances Market Share (%)

Source: PSG, Annual Reports

31.0%

12.7%

23.4%

32.9%32.2%

12.7%

22.1%

33.0%

0%

5%

10%

15%

20%

25%

30%

35%

FNB NED SBNH CGP

2011 2012 2013 2014 2015

P a g e | 16

PSG Wealth Management (Namibia) (Pty) Ltd

The data shown from here onwards, refers to the latest

financial year ends of the different banks. There is a timing

difference of 6 months or less.

Chart 10 shows the CAGR in gross advances for all the banks

over a 5 year period. Among the local banks CGP and FNB

posted the fastest annualised growth in gross advances over

the last 5 years, growing at a CAGR of 15.4%. SBNH and NED

are not far behind in terms of advances growth, growing by

14.2% and 13.5%. The slower growth explains the drop or

stagnation in market share for these two banks.

Chart 10: Gross Advances – 5 years (% CAGR)

Source: PSG, Annual Reports, UBS

Advances growth for the SA banks has varied significantly. SBK

and CPI grew at double digit rates of 14.7% and 16.7%

respectively while the other banks grew advances at less than

10%. The fastest advances growth reported among the SA

banks over the last 3, 5 and 7 years, besides CPI, was FSR. SBK

SA and BGA have grown at an annualised rate of 5.0% and

4.7% over the last 5 years.

Table 16: CAGR (%) for gross advances as at financial year end

1 year 3 years 5 years 7 years

FNB 12.9% 14.9% 15.4% 13.4%

NED 18.3% 17.4% 13.5% 12.5%

SBNH 11.6% 11.8% 14.2% 10.6%

CGP 12.6% 14.7% 15.4% 15.7%

NED SA 7.8% 7.7% 6.7% 6.2%

SBK SA 14.7% 4.7% 5.5% 2.5%

BGA 7.3% 9.0% 6.0% 3.8%

FSR 9.3% 12.2% 12.9% 10.5%

CPI 16.7% 18.0% 34.2% 43.7%

FNBB 12.6% 12.0% 15.2% 17.8%

BBB 20.6% 15.5% 11.3% 9.6%

SCB -10.5% 12.9% 15.6% 12.6%

SCZ 12.6% 16.6% 24.5% 19.0%

Zanaco 11.6% 10.6% 14.3% 18.7%

Source: PSG, Annual Reports, UBS

Growth by Loan Category – Local Banks

Advances growth has slowed significantly since January

2016. SBNH and NED numbers only reflect what happened

up to 31 December 2015.

CGP has grown all its loan categories at double digits, with

mortgage loans significantly faster at 17.2%, over the last 5

years. Over the last year, however, term loans and overdrafts

showed the highest growth as mortgage loan growth slowed.

Table 17: CGP - CAGR (%) as at as at 30 June 2016

Loan category 1 year 3 years 5 years 10 years

Mortgage loans 13.2% 16.4% 17.2% 18.7%

Term loans and overdrafts 17.4% 14.7% 14.9% 12.6%

Installment sales and leases 12.2% 13.1% 12.5% 14.2%

Source: PSG, Annual Reports

Out of all the loan categories, FNB has grown term loans and

overdrafts the fastest over the last 5 years, at a CAGR of

24.4%.

Table 18: FNB - CAGR (%) as at 30 June 2016

Loan category 1 year 3 years 5 years 10 years

Mortgage loans 10.5% 11.9% 12.5% 10.8%

Term loans and overdrafts 18.6% 22.0% 24.4% 16.7%

Installment sales and leases 6.4% 10.6% 13.2% 9.8%

Source: PSG, Annual Reports

NED showed significant growth in the instalment sales and

leases category and mortgage loans over the last year at the

expense of term loans and overdrafts. Over the last 5 years,

instalment sales grew in excess of 20% per year.

Table 19: NED - CAGR (%) as at 31 December 2015

Loan category 1 year 3 years 5 years 10 years

Mortgage loans 32.4% 18.2% 15.7% 16.5%

Term loans and over drafts -10.3% 4.9% 4.5% 2.1%

Installment sales and leases 33.8% 35.7% 22.5% 13.6%

Source: PSG, Annual Reports

SBNH expanded all categories in double digits over the last 5

years. Mortgage loan growth, however slowed sharply to

6.8% last year. Over 5 years, term loans grew fastest at 19.7%

Table 20: SBNH - CAGR (%) as at 31 December 2015

Loan category 1 year 3 years 5 years 10 years

Mortgage loans 6.8% 9.0% 10.5% 12.0%

Term loans and over drafts 18.0% 13.7% 19.7% 10.6%

Installment sales and leases 10.9% 15.0% 15.5% 10.8%

Source: PSG, Annual Reports

15.4%

13.5%14.2% 15.4%

6.7%5.5% 6.0%

12.9%

34.2%

15.2%11.3%

15.6%

24.5%

14.3%

0%

5%

10%

15%

20%

25%

30%

35%

40%

FNB

NED

SBN

H

CG

P

NED

SA

SBK

SA

BG

A

FSR

CP

I

FNB

B

BB

B

SCB

SCZ

Zanaco

P a g e | 17

PSG Wealth Management (Namibia) (Pty) Ltd

Mortgage Loans

As mentioned, mortgage loans has gained in significance over

the last decade and remain a major earnings driver for local

commercial banks. As we have done last year, we include a

section on the early arrears of the mortgage loan books. The

total mortgage loans consisting of commercial and residential

loans between the four commercial banks amounted to about

N$36.9bn and account on average for about 46.2% of total

average gross advances at the latest year-ends.

Chart 11: Total Mortgage Loans at Year-end (N$ billion)

Source: PSG, Annual Reports

Table 21: Mortgage loans - CAGR (%)

1 year 3 years 5 years 10 years

FNB 10.5% 11.9% 12.5% 10.8%

NED 32.4% 18.2% 15.7% 16.5%

SBNH 6.8% 9.0% 10.5% 12.0%

CGP 13.2% 16.4% 17.2% 18.7%

Source: PSG, Annual Reports

Table 22: Mortgage Loans (N$000)

FY13 FY14 FY15 FY16

FNB 8 442 123 9 667 352 10 694 799 11 815 279

NED 3 065 491 3 476 328 4 601 266

SBNH 6 042 297 6 616 835 7 063 798

CGP 8 499 995 9 919 583 11 850 416 13 412 655

Source: PSG, Annual Reports

CGP’s mortgage loan book amounted to N$13.4bn at June

2016 followed by FNB with N$11.8bn. Residential loans

account for about 56% of CGP’s mortgage loan book and

28.4% of total advances at FY16.

CGP has grown its mortgage loans at the fastest annualised

rate of 18.7% over the last 10 years. SBNH reported the

slowest CAGR growth of 12.0% over the last 10 years.

Chart 12: CAGR (%) – 5 years

Source: PSG, Annual Reports

Chart 12 shows CGP superior growth in mortgage loans over

the last 5 years growing by a CAGR of 17.8%. Although NED

has the smallest mortgage loan book amongst the local banks,

it has grown its book at the 2nd fastest pace over the last 5

years at a CAGR of 15.7% while SBNH reported the slowest

growth of 10.5% over the same period.

Chart 13: CAGR (%) – 3 years

Source: PSG, Annual Reports

Chart 14: CAGR (%) – 1 year

Source: PSG, Annual Reports

4.6

7.1

11.8

13.7

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

FNB NED SBNH CGP

N$

bn

FY11 FY12 FY13 FY14 FY15 FY16

12.5%

15.7%

10.5%

17.8%

0%

5%

10%

15%

20%

FNB NED SBNH CGP

11.9%

18.2%

9.0%

17.4%

0%

5%

10%

15%

20%

FNB NED SBNH CGP

10.5%

32.4%

6.8%

15.9%

0%

5%

10%

15%

20%

25%

30%

35%

FNB NED SBNH CGP

P a g e | 18

PSG Wealth Management (Namibia) (Pty) Ltd

NED’s fast growth in mortgages over the last year of 32.4%,

also boosted them to record the fastest growth (18.2%) over

the last 3 years.

Mortgage loans accounted for 45.5% of FNB’s total gross

advances in FY16 while mortgage loans accounted for 46.4%

and 41.0% of total advances for NED and SBNH, respectively.

CGP and NED have increased the share that mortgages make

up of their total advances book, while FNB and SBNH have

decreased their exposure to mortgages.

Chart 15: Mortgage Loans as % of Total Gross Advances

Source: PSG, Annual Reports

Chart 16 shows how mortgage loans continue to account for

a larger part of total loans over the last 10 years. Mortgage

loans as percentage of advances have gradually increased

from between 20% - 40% of total advances a decade ago to

between 40% and 55% at latest year end. Over the last 3

years, though one can see how SBNH and FNB have tapered

their exposure to home loans as % of their total advances.

Interestingly, even though CGP increased its mortgage loan

book as % of total gross advances from 36.5% in FY06 to 51.2%

in FY15. NED’s mortgage loans as a percentage of its total

gross advances increased at a faster pace over the last 10

years from 21% to 46.4% in FY15.

Chart 16: Mortgage Loans as % of total gross advances

Source: PSG, Annual Reports

Mortgage book age analysis

An analysis of the credit quality of the mortgage loan books,

have yielded thought-provoking results. Even though

impairment figures in the mortgage home loan books have

increased slightly since 2011, there is evidence of pressure on

the consumer in the ratio of the books which are 1 or 2

instalments behind.

For FNB, the ratio of the book in good standing has declined

from 98.1% in FY11 to 92.7% in FY16. The ratio of the

mortgage loan book which has missed one or two installments

has increased every year, from 0.7% in FY11 to 6.0% in FY15.

Chart 17: Age analysis of FNB mortgage loans

Source: PSG, Annual Reports

The situation looks markedly different for CGP. Information is

only available since its listing in 2012, but the overall % of the

loan book in good standing has remained above 98.0% since

then.

The model that CGP applies where each branch manager is

responsible for managing his/her own book could be the

reason for their superior early arrear numbers. Despite this,

there is also a trend of the % of early arrears, which are not

accounted for in non-performing loans, increasing every year.

51.7%

45.6%47.6% 46.2%46.4%

41.0%45.5%

51.2%

0%

10%

20%

30%

40%

50%

60%

FNB NED SBNH CGP

FY11 FY12 FY13 FY14 FY15 FY16

20%

30%

40%

50%

60%

FY0

3

FY0

4

FY0

5

FY0

6

FY0

7

FY0

8

FY0

9

FY1

0

FY1

1

FY1

2

FY1

3

FY1

4

FY1

5

FY1

6

FNB NED SBNH CGP

98.1% 97.2% 96.9%95.5%

94.0%92.7%

0.7%1.5% 2.0%

3.5%5.0%

6.0%

1.2% 1.3% 1.1% 1.0% 1.0% 1.3%

80.0%

82.0%

84.0%

86.0%

88.0%

90.0%

92.0%

94.0%

96.0%

98.0%

100.0%

2011 2012 2013 2014 2015 2016

Good standing Early arrears Impaired

P a g e | 19

PSG Wealth Management (Namibia) (Pty) Ltd

Chart 18: Age analysis of CGP mortgage loans

Source: PSG, Annual Reports

NED improved their loans in good standing from 93.1% of

the portfolio in FY11 to 96.0% in FY14, but this deteriorated

significantly in FY15 to 89.4%. This can be as a result of their

very aggressive mortgage advances growth of 32.4%.

Chart 19: Age analysis of NED mortgage loans

Source: PSG, Annual Reports

SBHN has a much lower ratio for loans in good standing than

the other Namibian banks. This could be due to timing

differences in their system. We do, still see the trend of an

increase over the last few years in early arrears even though

FY14 showed some improvement where 86.3% of their home

loans were in good standing. The impairments figure did

increase significantly in FY15 to 2.5% to 3.6%

Chart 20: Age analysis of SBNH mortgage loans

Source: PSG, Annual Reports

This prevailing trend of the early arrears number increasing

for the past 4 years is an indication of the continued pressure

on the Namibian consumer. It is likely that these mortgage

loan arrears do not relate to primary residences, but more to

investment properties where tenants might be struggling to

make rent payments. We are starting to see these early

arrears feeding through to larger impairment and credit loss

numbers, which are discussed in the Credit Risk section.

98.64% 98.60% 98.62% 98.16%

0.61% 0.80% 0.73% 0.97%0.75% 0.60% 0.65% 0.87%

80.0%

82.0%

84.0%

86.0%

88.0%

90.0%

92.0%

94.0%

96.0%

98.0%

100.0%

FY13 FY14 FY15 FY16

Good standing Early arrears Impaired

92.6%94.2% 95.0% 96.1%

94.5% 94.5%

89.4%

1.5%

1.4%2.1%

1.2%2.8% 3.2%

8.5%

5.8%4.4%

2.9% 2.7% 2.7% 2.3% 2.1%

80.0%

82.0%

84.0%

86.0%

88.0%

90.0%

92.0%

94.0%

96.0%

98.0%

100.0%

2009 2010 2011 2012 2013 2014 2015

Good standing Early arrears Impaired

89.0%86.5%

84.2%86.3% 85.6%

8.7%11.1%

13.5%11.2%

10.8%

2.3% 2.4% 2.3% 2.5% 3.6%

80.0%

82.0%

84.0%

86.0%

88.0%

90.0%

92.0%

94.0%

96.0%

98.0%

100.0%

2011 2012 2013 2014 2015

Good standing Early arrears Impaired

P a g e | 20

PSG Wealth Management (Namibia) (Pty) Ltd

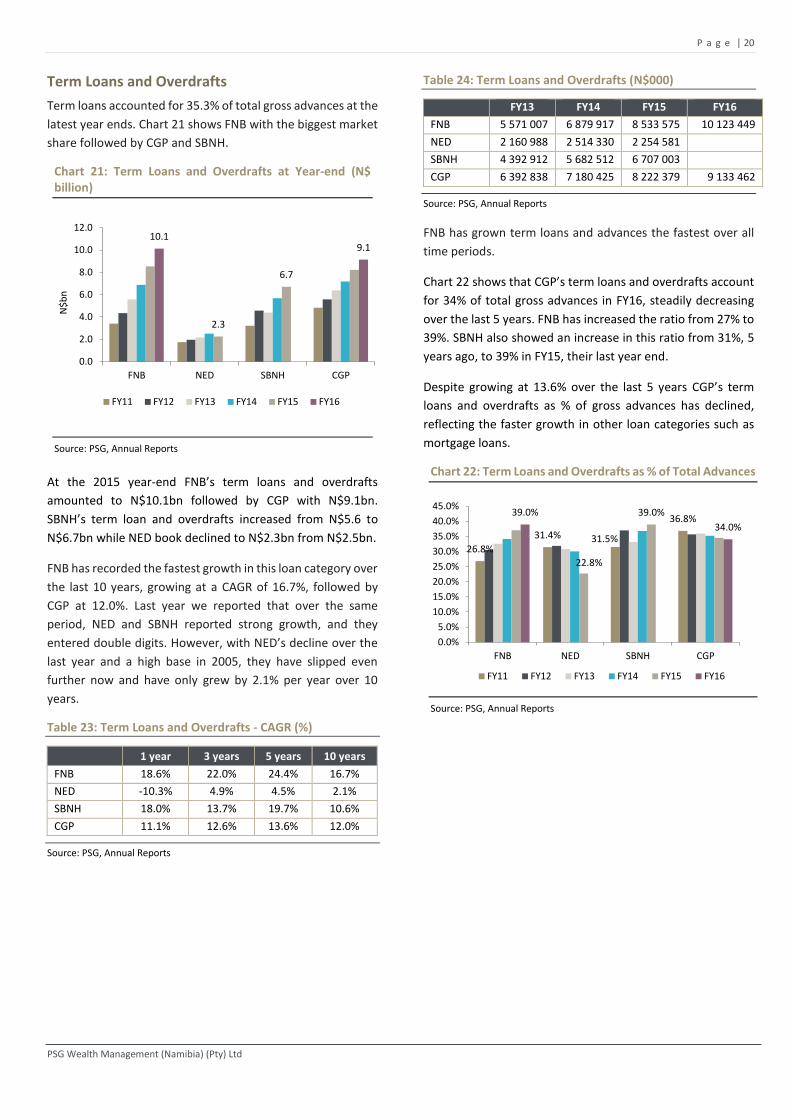

Term Loans and Overdrafts

Term loans accounted for 35.3% of total gross advances at the

latest year ends. Chart 21 shows FNB with the biggest market

share followed by CGP and SBNH.

Chart 21: Term Loans and Overdrafts at Year-end (N$ billion)

Source: PSG, Annual Reports

At the 2015 year-end FNB’s term loans and overdrafts

amounted to N$10.1bn followed by CGP with N$9.1bn.

SBNH’s term loan and overdrafts increased from N$5.6 to

N$6.7bn while NED book declined to N$2.3bn from N$2.5bn.

FNB has recorded the fastest growth in this loan category over

the last 10 years, growing at a CAGR of 16.7%, followed by

CGP at 12.0%. Last year we reported that over the same

period, NED and SBNH reported strong growth, and they

entered double digits. However, with NED’s decline over the

last year and a high base in 2005, they have slipped even

further now and have only grew by 2.1% per year over 10

years.

Table 23: Term Loans and Overdrafts - CAGR (%)

1 year 3 years 5 years 10 years

FNB 18.6% 22.0% 24.4% 16.7%

NED -10.3% 4.9% 4.5% 2.1%

SBNH 18.0% 13.7% 19.7% 10.6%

CGP 11.1% 12.6% 13.6% 12.0%

Source: PSG, Annual Reports

Table 24: Term Loans and Overdrafts (N$000)

FY13 FY14 FY15 FY16

FNB 5 571 007 6 879 917 8 533 575 10 123 449

NED 2 160 988 2 514 330 2 254 581 SBNH 4 392 912 5 682 512 6 707 003 CGP 6 392 838 7 180 425 8 222 379 9 133 462

Source: PSG, Annual Reports

FNB has grown term loans and advances the fastest over all

time periods.

Chart 22 shows that CGP’s term loans and overdrafts account

for 34% of total gross advances in FY16, steadily decreasing

over the last 5 years. FNB has increased the ratio from 27% to

39%. SBNH also showed an increase in this ratio from 31%, 5

years ago, to 39% in FY15, their last year end.

Despite growing at 13.6% over the last 5 years CGP’s term

loans and overdrafts as % of gross advances has declined,

reflecting the faster growth in other loan categories such as

mortgage loans.

Chart 22: Term Loans and Overdrafts as % of Total Advances

Source: PSG, Annual Reports

2.3

6.7

10.19.1

0.0

2.0

4.0

6.0

8.0

10.0

12.0

FNB NED SBNH CGP

N$

bn

FY11 FY12 FY13 FY14 FY15 FY16

26.8%

31.4% 31.5%

36.8%

22.8%

39.0%39.0%

34.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

FNB NED SBNH CGP

FY11 FY12 FY13 FY14 FY15 FY16

P a g e | 21

PSG Wealth Management (Namibia) (Pty) Ltd

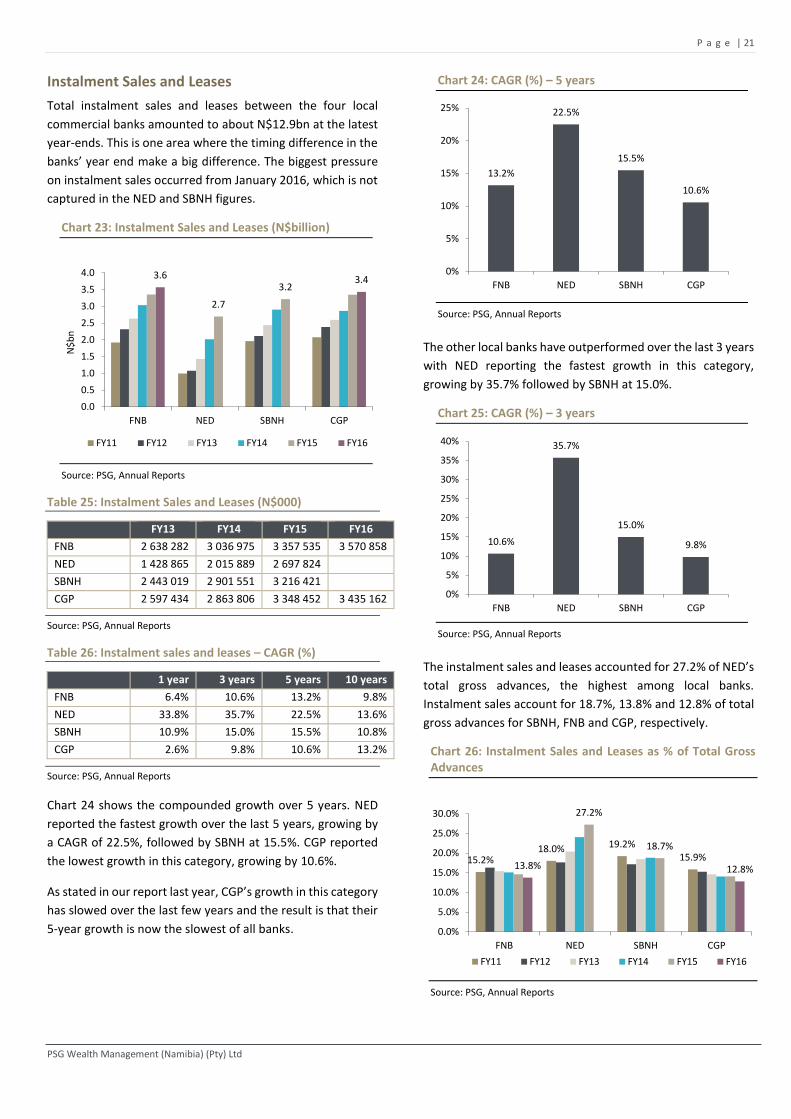

Instalment Sales and Leases

Total instalment sales and leases between the four local

commercial banks amounted to about N$12.9bn at the latest

year-ends. This is one area where the timing difference in the

banks’ year end make a big difference. The biggest pressure

on instalment sales occurred from January 2016, which is not

captured in the NED and SBNH figures.

Chart 23: Instalment Sales and Leases (N$billion)

Source: PSG, Annual Reports

Table 25: Instalment Sales and Leases (N$000)

FY13 FY14 FY15 FY16

FNB 2 638 282 3 036 975 3 357 535 3 570 858

NED 1 428 865 2 015 889 2 697 824

SBNH 2 443 019 2 901 551 3 216 421

CGP 2 597 434 2 863 806 3 348 452 3 435 162

Source: PSG, Annual Reports

Table 26: Instalment sales and leases – CAGR (%)

1 year 3 years 5 years 10 years

FNB 6.4% 10.6% 13.2% 9.8%

NED 33.8% 35.7% 22.5% 13.6%

SBNH 10.9% 15.0% 15.5% 10.8%

CGP 2.6% 9.8% 10.6% 13.2%