public sector property forum

TRANSCRIPT

Public Sector Property Forum

Gavin Hulcombe – Southeast Queensland Market Overview

David Hyne – Queensland Market Overview

27 August 2021

The National Perspective

Source: Corelogic Hedonic Home Value Index – August 2021

Brisbane

15.9%

Sydney

18.2%

Canberra

20.5%

Melbourne

10.4% Hobart

21.9%

Perth

10.8%

Darwin

23.4%

Adelaide

15.7%

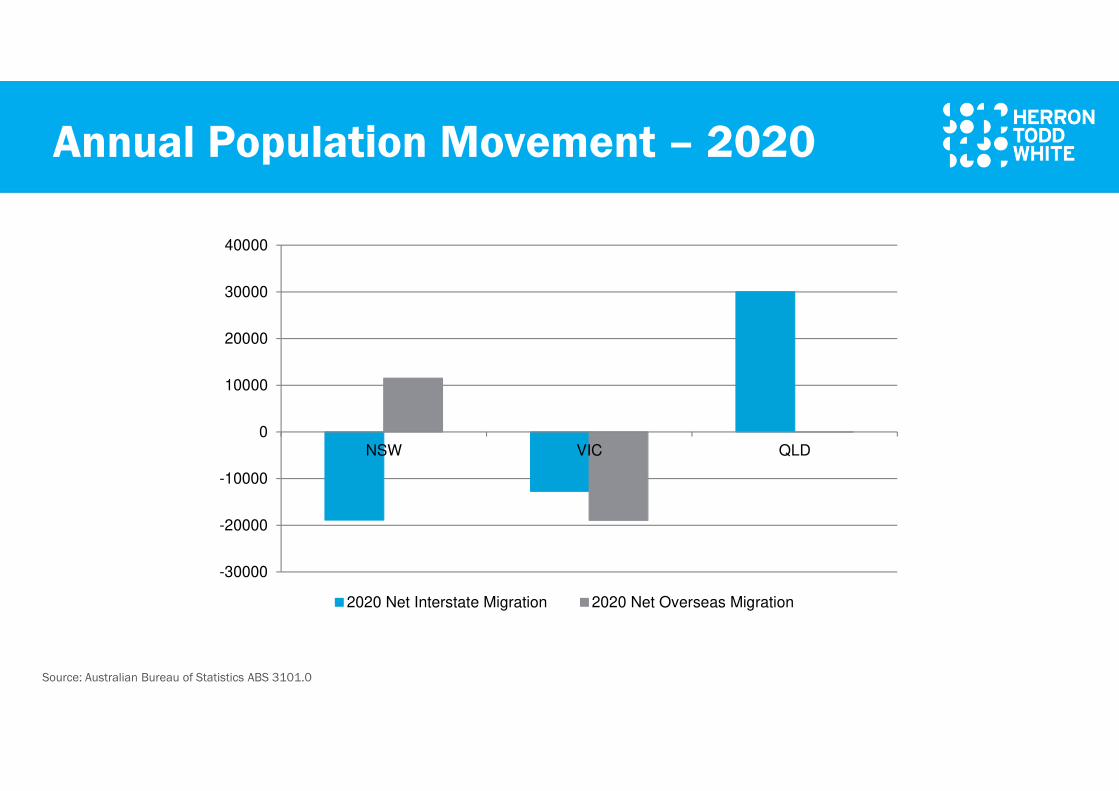

Annual Population Movement – 2020

Source: Australian Bureau of Statistics ABS 3101.0

-30000

-20000

-10000

0

10000

20000

30000

40000

NSW VIC QLD

2020 Net Interstate Migration 2020 Net Overseas Migration

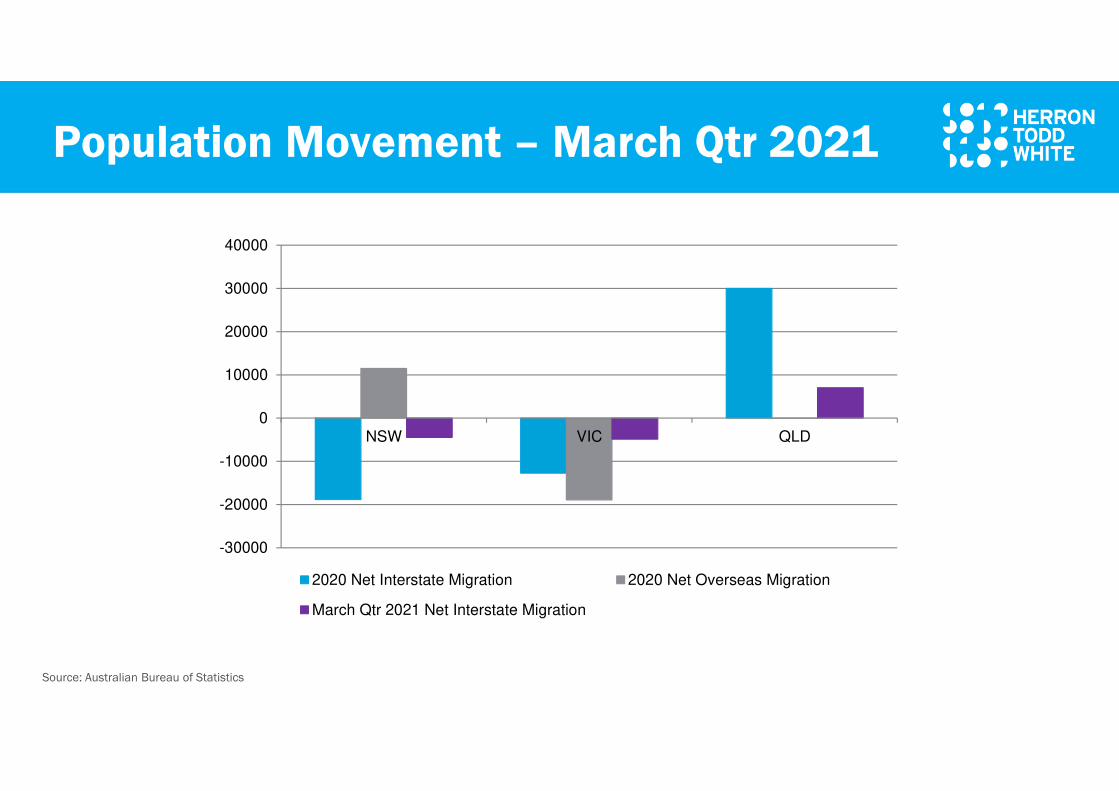

Population Movement – March Qtr 2021

Source: Australian Bureau of Statistics

-30000

-20000

-10000

0

10000

20000

30000

40000

NSW VIC QLD

2020 Net Interstate Migration 2020 Net Overseas Migration

March Qtr 2021 Net Interstate Migration

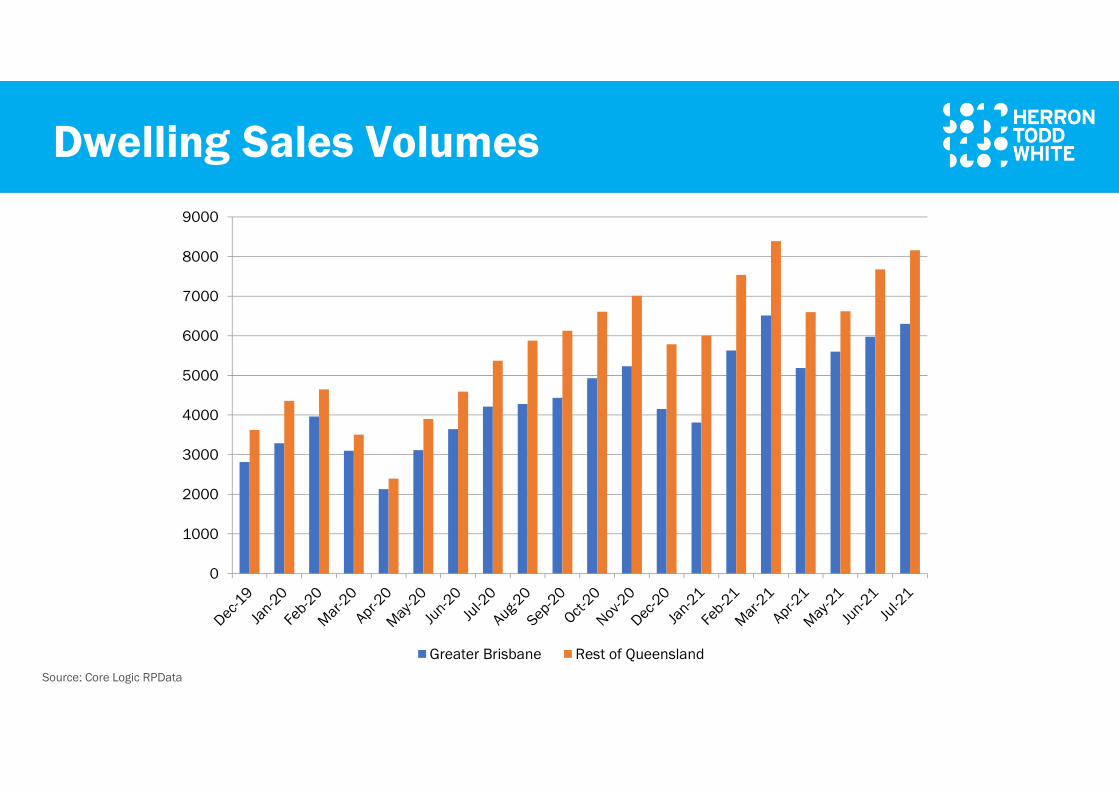

Dwelling Sales Volumes

Source: Core Logic RPData

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

Greater Brisbane Rest of Queensland

Lifestyle

Image Source: Queensland.com.au

Key Olympic Sites

Image Source: Brisbane Development

How strong is the Brisbane market?

Source: Herron Todd White, Core Logic RPData

Suburb Property Type Sale Price Sale DatePrev. Sale

Price

Prev. Sale

Date% Change

Bulimba 29 Coutts Street $2,380,000 March 2021 $1,750,000 August 2020 36%

Moggill 68 Outlook Place $1,100,000 April 2021 $860,000 May 2020 28%

Caboolture 14 Tuckerbox Street $415,000 May 2021 $324,900 June 2020 28%

Cleveland 20 Bowspirit Parade $1,600,000 June 2021 $1,290,000 November 2020 24%

BrisbaneUnit 2504, Abian

140 Alice Street$2,200,000 February 2021 $1,910,000 November 2020 15%

Camp Hill 34 Arrol Street $2,800,000 February 2021 $2,475,000 April 2020 13%

Paddington 10 Wilden Street $1,860,000 June 2021 $1,720,000 February 2021 8%

Source: Herron Todd White

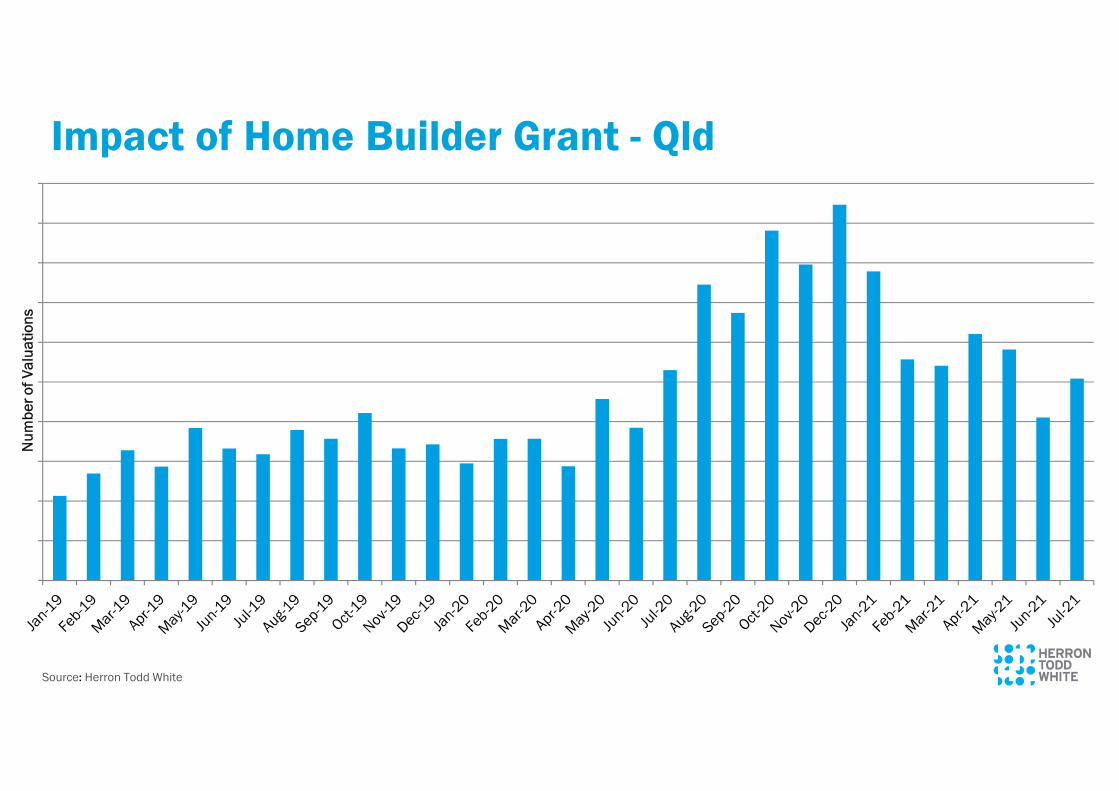

Impact of Home Builder Grant - Qld

Nu

mb

er

of

Va

lua

tio

ns

Source: Core Logic RPData, Herron Todd White Research

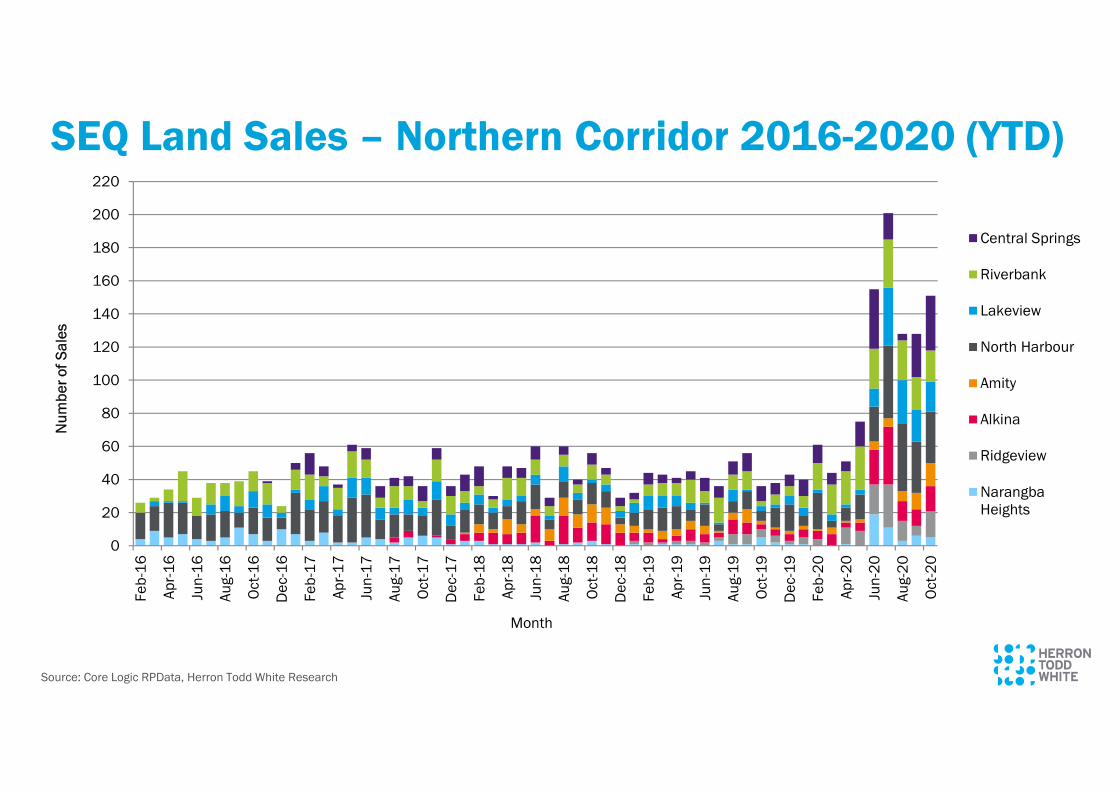

SEQ Land Sales – Northern Corridor 2016-2020 (YTD)

0

20

40

60

80

100

120

140

160

180

200

220

Fe

b-1

6

Ap

r-1

6

Jun

-16

Au

g-1

6

Oct-

16

De

c-1

6

Fe

b-1

7

Ap

r-1

7

Jun

-17

Au

g-1

7

Oct-

17

De

c-1

7

Fe

b-1

8

Ap

r-1

8

Jun

-18

Au

g-1

8

Oct-

18

De

c-1

8

Fe

b-1

9

Ap

r-1

9

Jun

-19

Au

g-1

9

Oct-

19

De

c-1

9

Fe

b-2

0

Ap

r-2

0

Jun

-20

Au

g-2

0

Oct-

20

Nu

mb

er

of

Sa

les

Month

Central Springs

Riverbank

Lakeview

North Harbour

Amity

Alkina

Ridgeview

NarangbaHeights

Rental Vacancy Rates – Brisbane

Source: SQM Research, Herron Todd White

0

2

4

6

8

10

12

14

Pe

rce

nta

ge

Oct-18 Oct-20 Jul-21

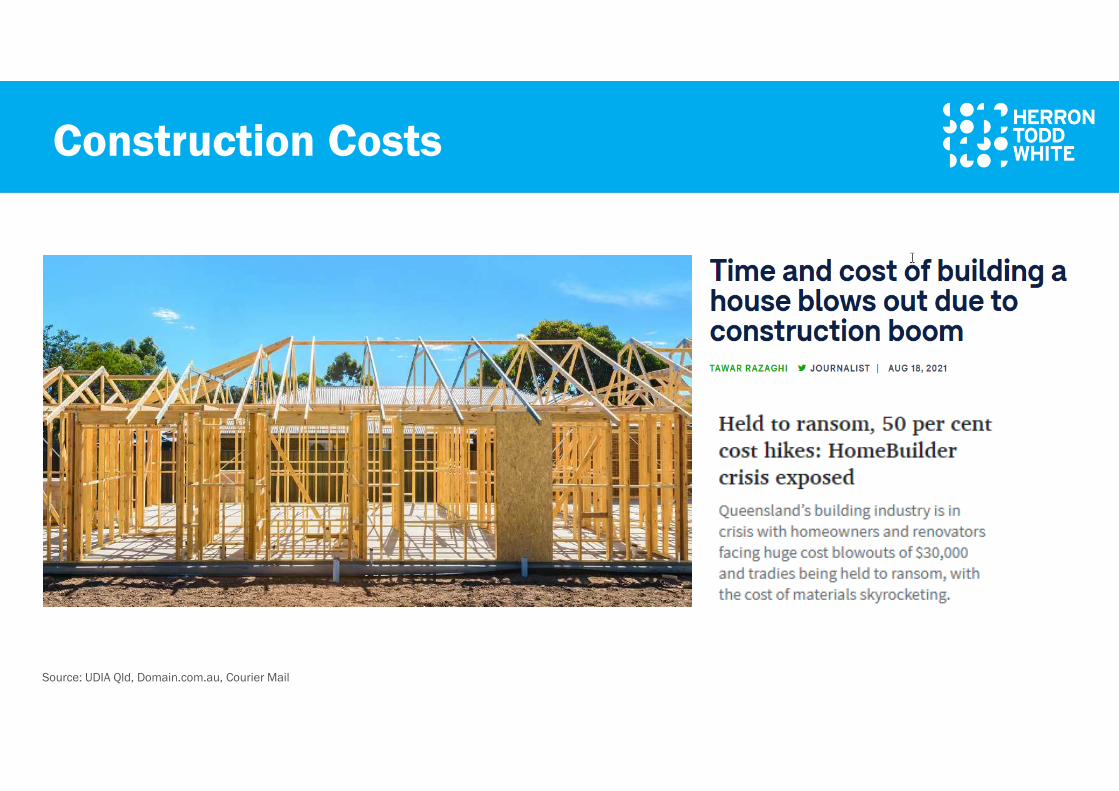

Construction Costs

Source: UDIA Qld, Domain.com.au, Courier Mail

Penthouse – Soul, Surfers Paradise 5 McMillan Ct, Southport 2 Heron Ave, Mermaid Beach

1,070 m² GFA

Sold May 2021

$15,250,000

3,442 m² Block

Sold March 2021

$23,750,000

2,112 m² Block

Sold February 2021

$25,000,000

875 676 476

Gold Coast – Prestige Sales

Source: Core Logic RPData

2 Belmore Terrace, Sunshine Beach Webb Road, Sunshine Beach Unit 11 ‘La Mer’ Hastings St, Noosa

1,258 m² Block

Sold Mar 2021

$21,000,000

2,015 m² block

Reportedly sold July 2021

$34,000,000

183 m²

Sold Nov 2020: $9,800,000

$53,488/m²

265 34 123

Sunshine Coast – Prestige Sales

Source: Core Logic RPData

What are the risks?

• The broader economy

• Migration

• Interest rates

• Affordability

• Availability of funds

Key Office Takeaways

• Very few institutional transactions…capital markets at a

standstill with uncertainty

• Leasing predominantly smaller fitted out spaces…Very few major

new leasing deals have been done

• Sub-Lease accommodation on the rise

• Incentives increasing

• Yields generally stagnant

• Owner occupiers a bright spot. Strong demand for good strata

space and sub $5 million freestanding buildings.

• The retail market is undergoing significant upheaval but not

even across the sector

• COVID relief has essentially ended

• Rents in CBD have fallen

• Rents in suburban convenience complexes stable

• Investors are highly scrutinizing lease covenants and income

security.

• Still good demand for well leased assets but limited stock

• Two tiered market?

Key Retail Takeaways

Key Industrial Takeaways

• Prime industrial not badly COVID affected

• Prime Industrial yields have tightened by up to 100bp

• Industrial rental rates are remaining stable

• Very strong investment demand…strongest sector

• Shortage of good investment stock

• Shortage of well priced land, especially larger parcels. Prices

increasing

The Road Ahead

• Strong growth future across

SEQ as Infrastructure and

Olympic projects ramp up

• Increasing migration

• Affordable gap relative to

Sydney and Melbourne.

Queensland Regions and Rural

Image Sources: Wikipedia, Queensland Times, Herron Todd White

Mining Tourism Agriculture

Disclaimer

The information contained in this report is provided in good faith and

has been derived from sources believed to be reliable and accurate.

However, the report is not intended to be comprehensive or render

advice and neither Herron Todd White nor any persons involved in the

preparation of this report accepts any form of liability for its contents.

This report has copyright and cannot be reproduced without written

permission of Herron Todd White.