public service media nordic ministers of culture have made globalization as one of their top...

TRANSCRIPT

Public Service Media in the Nordic Countries

FACTS & FIGURES

Nordic Public Service Media Map 1/2012

Public Service Media in the Nordic Countries

FACTS & FIGURES

Compiled by

Eva Harrie

NORDICOM

Nordic Public Service Media Map. Volume 1/2012Public Service Media in the Nordic Countries. Facts & Figures

Compiled by: Eva Harrie

Country contributors: Christian Edelvold Berg and Lykke Nordblom (Danish Agency for Culture / Centre for Libraries, Media and Digitalization), Tuomo Sauri (Statistics Finland), Ragnar Karlsson (Statistics Iceland), Nina Bjørnstad and Knut A. Tornes (medianorway), Ulrika Facht (Nordicom-Sweden)

The Nordic Ministers of Culture have made globalization as one of their top priorities, unified in the strategy: “Creativity – the Nordic response to globalization”. The aim is to create a more visible Nordic Region, a more knowledge-based Nordic Region and a more prosperous Nordic Region. This publication is part of “Creativity – the Nordic response to globalization”.

© Nordicom, University of Gothenburg

ISBN 978-91-86523-37-4

Published by:NORDICOMUniversity of GothenburgP O Box 713SE 405 30 GöteborgSwedenwww.nordicom.gu.se

Cover by: Daniel ZachrissonPrinted by: Ale Tryckteam AB, Bohus, Sweden, 2012

Contents

Foreword 7

Introduction 9

Facts & Figures

The Nordic Media Market 13

Financing 31

Television 53

Radio 107

Internet 145

Appendix 157

Country Contributors 165

7

Foreword

In television, there has long been a tendency to seek ‘role models’ among the major channels in big television markets in big countries. In the realm of public service broadcasting, the BBC has long been the paragon par excellence. Today, however, economic reality is such that few public service channels can realistically aspire to emulate ‘the BBC standard’. As a conse-quence, smaller channels in smaller countries are looked to for inspiration, and among these, the public service media in the Nordic countries have attracted considerable and widespread interest – as have our models of social organization over the years.

This, in short, is the background behind Nordicom’s project, A Nordic Public Service Media Map. Nordicom has long been part of the Nordic knowledge society. One of our principal objectives is to ensure the visibility of these five northerly countries, in Europe and further afield. In recent years, we have done quite a lot of work on media in the digital and globalized age: the conditions under which media operate and the changing roles the media play in society, viewed from a Nordic perspective. The project, A Nordic Public Service Media Map, is undertaken as a part of ‘Creative Norden’, one of the globalization strategies of the Nordic Council of Ministers.

It is our hope that the Nordic Public Service Media Map will make a meaningful contri-bution to the work being done on the role media play in democratic societies around the world. At the same time, Nordic media, too, are involved in a learning process, evolving – as always – in response to the changing environments they operate in.

The present publication is the first from this project entitled, Public Service Media in the Nordic Countries. Facts and Figures. There is a wealth of information in the overviews and statistics presented here. The contents form the basis of the next volume – the actual ‘Nor-dic Public Service Media Map’. We also look forward to publishing a number of qualified analyses from Nordic media scholars regarding public service media.

Göteborg in May 2012

Ulla CarlssonDirectorNordicom

9

This publication focuses on public service media in the Nordic region. The five Nordic countries – Denmark, Finland, Iceland, Norway and Sweden – are kindred in many respects, including their media systems and an integrated media market. A long tradition of public service broadcasting is one common trait, including strong support around it, as well as public service mod-els that have developed characterised by the fact that the five countries are small and have relatively small populations.

The Nordic public service broadcasters all have rights granted through legislation and accompanying regula-tions or agreements, with the role of supporting demo-cratic values, national culture and language, and of serving the whole population, through a broad range of programmes, national coverage and availability on several platforms. An important feature they all share is editorial freedom, meaning no interference from the state. Added to this are the many years of cooperation between the Nordic public service organisations con-cerning co-production and programme exchange.

For the media systems, technology shifts throughout the past decades have brought far-reaching changes. In the 1980s communication satellites in combination with liberalisation trends made new means of TV dis-tribution possible – and the Nordic countries, with na-tional public service organisations as single broadcasters, saw a new commercial and regional audiovisual market emerging. Pan-Scandinavian initiatives were launched by private interests, with MTG starting TV3 in Sweden, Denmark and Norway and SBS Broadcasting follow-ing suit with pan-Scandinavian establishment. Today, 20-25 years down the line, both MTG and SBS have important positions in the Nordic television and radio landscape, side by side with other large Nordic media companies such as Bonnier, Egmont and Sanoma, as well as the national public service organisations.

With digitalisation, new technology has again cre-ated new possibilities, challenges and debates. With all media companies meeting in the same arena – the web – competition for audiences and revenues has sharpened. All companies struggle to master the challenges, but the public service actors more so, since development has brought up fundamental questions about their “rai-

son d’être”. In today’s abundance of media output on multiple platforms, what is the role of the public service media? What is public service content? And how should public service operations be organised and financed?

Though mainly Nordic similarities, there have been different paths over the years concerning public service issues, such as type of organisation, ownership struc-tures and how public service rights and obligations can apply to private broadcasters. Also new challenges brought about by the changing landscapes have met different answers. The funding of public service broad-casting is one such issue. The traditional financing system via television licenses – i.e. a fee connected to a household’s or organization’s possession of a TV set – has been, and still is, much discussed. Countries have chosen different solutions. Denmark has introduced a household fee on all equipment that is able to receive programming, while Iceland and Finland are abandon-ing the license fee system altogether. Iceland replaced the license fee payment with an individual media fee (tax) in 2009, and Finland’s parliament has approved a new income-linked tax, replacing the TV license as of 2013. In Sweden, the financing question is the sub-ject of an ongoing government commission on public service.

Another pending issue is the digitalisation of radio. For a few years now terrestrial television has been fully digitalized in all Nordic countries, except Iceland, while radio shows a varied situation. Throughout the region, public service has been locomotive in the digital de-velopment, but otherwise the countries show different strategies concerning choice of technical systems, the rights and obligations of private broadcasters and the future shutdown of the analogue systems. Sofar, only Norway has proposed a closing year, 2017, for its ana-logue net.

The time span of this publication is the past decade in the light of digitalisation trends, with time series starting mostly during year 2000. During this period the Nordic public service broadcasters have lost view-ers and listeners, but more importantly, they still have many users. In order to understand the development of public service media it is necessary to consider the context of the general media landscape – in all its com-

Introduction

Eva Harrie

10

plexity, variety and great offer. Therefore, our aim has been to provide a description of each country’s media landscape today as well as the trends to date, and to offer a coherent overview of the Nordic region.

This publication is the start of our project, Nordic Public Service Media Map, which is part of ‘Creative Norden’ – a globalisation strategy of the Nordic Coun-cil of Ministers, and is intended for an international audience. This first volume concentrates on similarities and differences between the countries when it comes to structure – the public service media’s position on the Nordic media market, their political and financial con-ditions, and the overall output in the form of channels and stations, etc. – and on basic content and audience data. The facts and figures provide a basis for the series’ forthcoming publications, which will look more into the Nordic public service model – if there indeed is such a model – and its role in democracy and citizenship.

Invaluable for the work with this volume has been our longtime experience with the Nordic Media Trends series, with its broad overview of Nordic media devel-opments – and the team of knowledgeable contributors behind it. As in that series, the information and data presented here, were collected and collated in a joint effort by the Danish Agency for Culture (Centre for Libraries, Media and Digitalization), Statistics Fin-land, Statistics Iceland, medianorway and Nordicom-Sweden. Other experts, researchers and people in the industry have also contributed knowledge. We would like to thank all of you who have in any way been in-volved in this publication.

This said, we hope Public Service Media in the Nordic Countries will serve as a great source of information about the Nordic media landscape in general – and the Nordic public service media in particular.

11

Facts & Figures

12

Explanation of Symbols

– Magnitude zero

0 Magnitude less than half of unit employed

.. Data not available

* Category not applicable

13

The largest media companies on the Nordic market

Figure 1 The 25 largest media companies in the Nordic countries 2010 by company revenue 14

Table 2 The 25 largest media companies in the Nordic countries 2010: Company revenue, results and margins 15

Table 3 The 25 largest media companies in the Nordic countries 2010: Company revenue 2000-2010 16

Table 4 The 20 largest Nordic media companies’ total revenue and public service broadcasters’ share 1995-2010 18

Figure 5 The 20 largest Nordic media companies’ and public service broadcasters’ total revenue 1995-2010 18

The largest media companies on the Nordic and respective national markets

Table 6 The 20 largest media companies by media revenue on the Nordic media market 2010 19

Table 7 The ten largest media companies by revenue on the Finnish market 2010 20

Table 8 The six largest media companies by revenue on the Icelandic market 2010 21

Table 9 The ten largest media companies by revenue on the Norwegian market 2010 22

Table 10 The ten largest media companies by revenue on the Swedish market 2010 23

Nordic public service companies

Figure 11 DR (December 2010) 24

Figure 12 TV 2 / Danmark (December 2010) 25

Figure 13 Yleisradio Oy, YLE (Spring 2011) 26

Figure 14 Ríkisútvarpið ohf., RÚV (December 2010) 27

Figure 15 Norsk rikskringkasting AS, NRK (February 2012) 28

Figure 16 The Swedish public service group: SR, SVT and UR (February 2011) 29

The Nordic Media Market

NORDICOM 14 Nordic Public Service Media Map 1/2012

THE NORDIC MEDIA MARKET

1. The 25 largest media companies in the Nordic countries 2010 by company revenue (EUR millions)

0 500 1 000 1 500 2 000 2 500 3 000 3 500

Bonnier

Sanoma

Schibsted Media Group

MTG/Metro 1

Egmont 2

Telenor Broadcast 2,3

SVT/SR/UR 4

Mecom Group 5

NRK

A-pressen 2

Stampen

TDC: YouSee 6

Aller 7

DR

Com Hem

JP/Politikens Hus

Teracom

ProSiebenSat.1 Group 8

YLE

TV 2 Group 2

KF 9

Alma Media

TV 2/Danmark

Otava-Kuvalehdet

TS Group

EUR mill ions

Public service companies shown in colour.

Italics: Companies with domicile outside the Nordic countries. Included due to substantial revenue and activities on the Nordic market (data cover their Nordic opera-tions only).

1 The media holdings of the Stenbeck sphere: Modern Times Group MTG AB and Metro International S.A. The Group’s internet retailing business CDON Group AB was demerged at the end of 2010 and its shares were distributed to MTG’s shareholders. CDON’s revenue of 231 Meuro is not included in MTG’s income statement for 2010, nor in the Stenbeck collected revenue above.

2 On the Norwegian media market there is some cross-ownership: Telenor ASA owns 44% of A-pressen, which in its turn owns 50% of the TV 2 Group. The other 50% of the TV2 Group is owned by Danish Egmont. TV 2 Group’s revenue is included in A-pressen’s and Egmont’s accounts according to share of ownership. (In January 2012 A-pressen sold its share in the TV 2 Group to Egmont, which is now full owner of the group.)

3 Telenor’s broadcasting division. Telenor ASA’s total volume 2010 was 11 826 MEuro.4 Data refer to Förvaltningsstiftelsen, i.e. the owner foundation of Sweden’s three public service programme companies: SR (radio), SVT (television) and UR (educational

programmes, turnover 37 Meuro in 2010). Data exclude transactions within the group. 5 Nordic market only, which represents 47% of Mecom’s total revenue in 2010 (1 415 MEuro).6 TDC’s broadcasting subsidiary YouSee A/S. TDC’s total volume for 2010 was 3 512 MEuro.7 Financial year 1 October 2009 – 30 September 2010.8 Nordic market only, which represents 13% of ProSiebenSat.1’s total revenue in 2010 (3 000 MEuro).9 The media holdings of KF, Kooperativa Förbundet (The Swedish Cooperative Union). KF’s total revenue for 2010 was 3 835 MEuro.

Note: The public service companies in colour, i.e. SR/SVT/UR in Sweden, NRK in Norway, DR in Denmark, YLE in Finland and TV 2/Danmark (only its main channel, TV 2, is public service, but economic data above refer to the whole company).

Sources: Company annual reports and websites

THE NORDIC MEDIA MARKET

NORDICOM 15 Nordic Public Service Media Map 1/2012

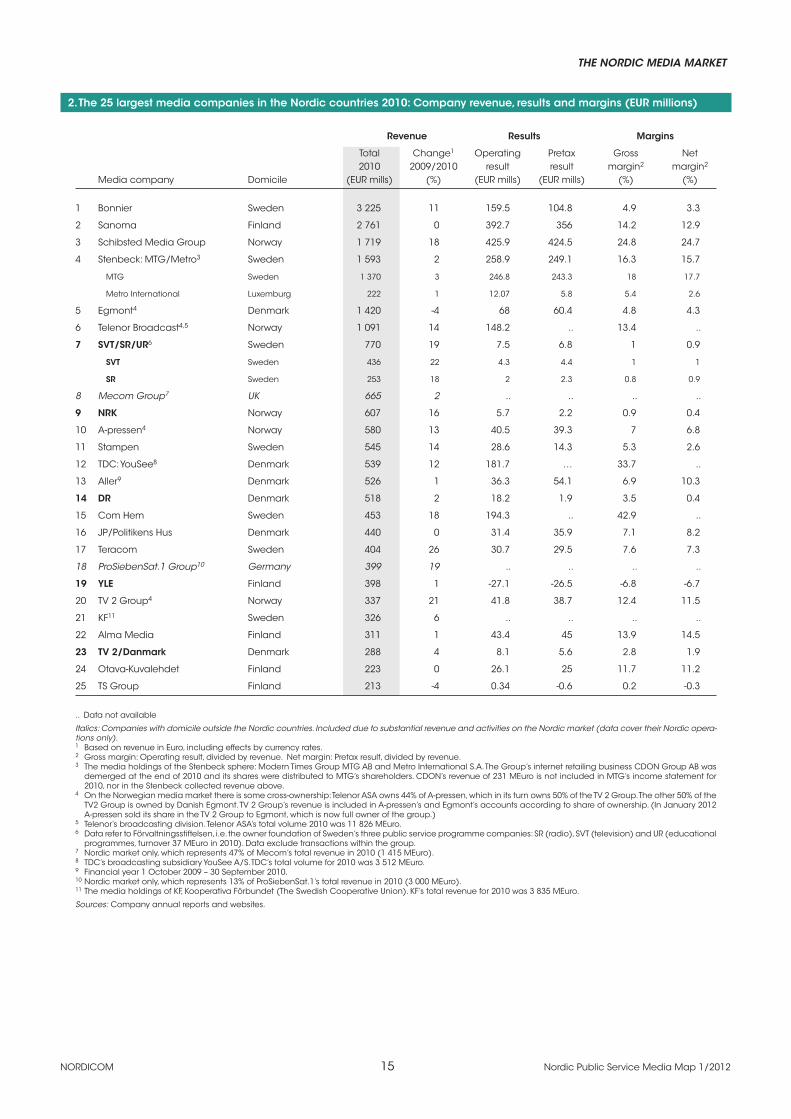

2. The 25 largest media companies in the Nordic countries 2010: Company revenue, results and margins (EUR millions)

Revenue Results Margins

Total Change1 Operating Pretax Gross Net 2010 2009/2010 result result margin2 margin2

Media company Domicile (EUR mills) (%) (EUR mills) (EUR mills) (%) (%)

1 Bonnier Sweden 3 225 11 159.5 104.8 4.9 3.3

2 Sanoma Finland 2 761 0 392.7 356 14.2 12.9

3 Schibsted Media Group Norway 1 719 18 425.9 424.5 24.8 24.7

4 Stenbeck: MTG/Metro3 Sweden 1 593 2 258.9 249.1 16.3 15.7

MTG Sweden 1 370 3 246.8 243.3 18 17.7

Metro International Luxemburg 222 1 12.07 5.8 5.4 2.6

5 Egmont4 Denmark 1 420 -4 68 60.4 4.8 4.3

6 Telenor Broadcast4,5 Norway 1 091 14 148.2 .. 13.4 ..

7 SVT/SR/UR6 Sweden 770 19 7.5 6.8 1 0.9

SVT Sweden 436 22 4.3 4.4 1 1

SR Sweden 253 18 2 2.3 0.8 0.9

8 Mecom Group7 UK 665 2 .. .. .. ..

9 NRK Norway 607 16 5.7 2.2 0.9 0.4

10 A-pressen4 Norway 580 13 40.5 39.3 7 6.8

11 Stampen Sweden 545 14 28.6 14.3 5.3 2.6

12 TDC: YouSee8 Denmark 539 12 181.7 … 33.7 ..

13 Aller9 Denmark 526 1 36.3 54.1 6.9 10.3

14 DR Denmark 518 2 18.2 1.9 3.5 0.4

15 Com Hem Sweden 453 18 194.3 .. 42.9 ..

16 JP/Politikens Hus Denmark 440 0 31.4 35.9 7.1 8.2

17 Teracom Sweden 404 26 30.7 29.5 7.6 7.3

18 ProSiebenSat.1 Group10 Germany 399 19 .. .. .. ..

19 YLE Finland 398 1 -27.1 -26.5 -6.8 -6.7

20 TV 2 Group4 Norway 337 21 41.8 38.7 12.4 11.5

21 KF11 Sweden 326 6 .. .. .. ..

22 Alma Media Finland 311 1 43.4 45 13.9 14.5

23 TV 2/Danmark Denmark 288 4 8.1 5.6 2.8 1.9

24 Otava-Kuvalehdet Finland 223 0 26.1 25 11.7 11.2

25 TS Group Finland 213 -4 0.34 -0.6 0.2 -0.3

.. Data not available

Italics: Companies with domicile outside the Nordic countries. Included due to substantial revenue and activities on the Nordic market (data cover their Nordic opera-tions only).1 Based on revenue in Euro, including effects by currency rates. 2 Gross margin: Operating result, divided by revenue. Net margin: Pretax result, divided by revenue. 3 The media holdings of the Stenbeck sphere: Modern Times Group MTG AB and Metro International S.A. The Group’s internet retailing business CDON Group AB was

demerged at the end of 2010 and its shares were distributed to MTG’s shareholders. CDON’s revenue of 231 MEuro is not included in MTG’s income statement for 2010, nor in the Stenbeck collected revenue above.

4 On the Norwegian media market there is some cross-ownership: Telenor ASA owns 44% of A-pressen, which in its turn owns 50% of the TV 2 Group. The other 50% of the TV2 Group is owned by Danish Egmont. TV 2 Group’s revenue is included in A-pressen’s and Egmont’s accounts according to share of ownership. (In January 2012 A-pressen sold its share in the TV 2 Group to Egmont, which is now full owner of the group.)

5 Telenor’s broadcasting division. Telenor ASA’s total volume 2010 was 11 826 MEuro.6 Data refer to Förvaltningsstiftelsen, i.e. the owner foundation of Sweden’s three public service programme companies: SR (radio), SVT (television) and UR (educational

programmes, turnover 37 MEuro in 2010). Data exclude transactions within the group. 7 Nordic market only, which represents 47% of Mecom’s total revenue in 2010 (1 415 MEuro).8 TDC’s broadcasting subsidiary YouSee A/S. TDC’s total volume for 2010 was 3 512 MEuro.9 Financial year 1 October 2009 – 30 September 2010.10 Nordic market only, which represents 13% of ProSiebenSat.1’s total revenue in 2010 (3 000 MEuro).11 The media holdings of KF, Kooperativa Förbundet (The Swedish Cooperative Union). KF’s total revenue for 2010 was 3 835 MEuro.

Sources: Company annual reports and websites.

NORDICOM 16 Nordic Public Service Media Map 1/2012

THE NORDIC MEDIA MARKET3.

Th

e 2

5 la

rge

st m

ed

ia c

om

pa

nie

s in

th

e N

ord

ic c

ou

ntr

ies

2010

: Co

mp

any

reve

nue

200

0-20

10 (

EUR

mill

ion

s)

Re

ven

ue

(EU

R m

illio

ns)

C

ha

ng

e (

%)1

M

ed

ia c

om

pa

ny

2000

20

01

2002

20

03

2004

20

05

2006

20

07

2008

20

09

2010

20

00-2

010

2009

-201

0

1 Bo

nn

ier

1 97

4 1

840

1 90

7 2

063

2 15

6 2

253

2 23

3 3

211

3 09

2 2

910

3 22

5 63

11

2 Sa

no

ma

1

448

1 73

4 2

358

2 39

6 2

505

2 62

2 2

742

2 92

6 3

030

2 76

8 2

761

91

0

3 Sc

hib

ste

d M

ed

ia G

rou

p

1 02

0 99

0 1

048

1 06

9 1

158

1 22

7 1

447

1 69

7 1

674

1 45

9 1

719

69

18

4 St

en

be

ck:

MTG

/Me

tro2

765

833

836

899

1 01

3 1

178

1 45

2 1

558

2 95

3 1

555

1 59

3 10

8 2z

MTG

64

3 69

2 65

6 69

2 74

5 86

3 1

096

1 22

7 1

371

1 33

4 1

370

114

3

Me

tro

84

98

125

180

243

289

331

331

295

220

222

164

1

5 Eg

mo

nt

1 06

6 1

169

1 23

0 1

126

1 08

8 1

119

1 25

4 1

514

1 58

2 1

478

1 42

0 33

-4

6 Te

len

or B

roa

dc

ast

3 ..

301

448

580

623

689

763

872

851

970

1 09

1 ..

11

7 SV

T/SR

/UR4

693

709

726

740

760

765

762

764

719

648

770

11

19

SVT

424

410

411

420

445

450

443

436

411

358

436

3 22

SR

195

222

234

240

231

235

245

240

228

214

253

30

18

8 M

eco

m G

rou

p5

* *

* *

* *

839

847

805

652

665

* 2

Ork

la M

ed

ia6

867

926

943

922

989

1 08

3 *

* *

* *

* *

9 N

RK

391

402

456

431

441

461

482

500

530

522

607

55

16

10

A-p

ress

en

(N

orw

ay)

27

8 28

6 32

2 30

5 31

9 37

1 42

1 59

1 59

6 51

3 58

0 10

9 13

11

Sta

mp

en

18

7 15

6 16

0 17

8 17

8 19

2 32

6 54

7 53

2 47

8 54

5 19

1 14

12

TDC

: Yo

uSe

e7

147

160

180

205

237

283

329

380

427

483

539

267

12

13

Alle

r8 42

8 44

2 46

9 47

1 48

3 51

1 53

1 54

6 57

7 51

9 52

6 23

1

14

DR

392

392

402

425

442

454

453

481

488

508

518

32

2

15

Co

m H

em

9 81

95

11

7 14

3 17

3 24

1 25

6 38

2 39

8 38

5 45

3 46

2 18

16

JP/P

olit

ike

ns

Hu

s10

* *

* 39

9 41

8 45

1 47

3 49

7 48

1 44

1 44

0 *

0

Polit

ike

n

216

216

215

* *

* *

* *

* *

* *

Jylla

nd

s-Po

ste

n

159

149

140

* *

* *

* *

* *

* *

17

Tera

co

m

183

175

194

206

235

291

325

358

332

321

404

120

26

18

Pro

Sieb

enSa

t.1 G

rou

p11

*

* *

* *

* *

* 49

1 33

5 39

9 *

19

SB

S Br

oa

dc

ast

ing

12

190

183

193

219

241

.. 48

1 *

* *

* *

*

19

YLE13

36

2 38

1 37

5 33

0 35

9 37

5 38

4 38

5 38

1 39

4 39

8 10

1

20

TV 2

Gro

up

(N

orw

ay)

18

6 18

7 20

8 20

2 21

2 24

3 28

7 32

6 33

4 27

9 33

7 81

21

21

KF14

14

8 16

4 21

1 21

7 24

4 28

9 31

7 36

4 35

8 30

9 32

6 12

0 6

22

Alm

a M

ed

ia

484

478

486

461

465

286

302

329

341

308

311

-36

1

23

TV 2

/Da

nm

ark

22

0 21

6 22

3 20

6 21

3 22

8 26

3 29

7 29

0 27

7 28

8 31

4

24

Ota

va-K

uva

leh

de

t 18

5 20

9 21

9 22

0 23

0 23

3 24

6 23

4 23

7 22

3 22

3 21

0

25

TS G

rou

p

247

276

293

279

272

309

339

336

306

222

213

-14

-4

THE NORDIC MEDIA MARKET

NORDICOM 17 Nordic Public Service Media Map 1/2012

* N

ot a

pp

lica

ble

(c

om

pa

ny d

id n

ot e

xist

, or h

ad

no

ac

tiviti

es

on

the

No

rdic

ma

rke

t)

.. D

ata

no

t ava

ilab

le

Italic

s: C

om

pa

nie

s w

ith d

om

icile

ou

tsid

e th

e N

ord

ic c

ou

ntr

ies.

Incl

ud

ed

du

e to

su

bst

an

tial r

eve

nue

an

d a

ctiv

itie

s o

n th

e N

ord

ic m

ark

et (

da

ta c

ove

r th

eir

No

rdic

op

era

tion

s o

nly

).

1 B

ase

d o

n re

ven

ue

in E

uro

, in

clu

din

g e

ffec

ts b

y c

urre

nc

y ra

tes.

2 M

ed

ia h

old

ing

s o

f th

e S

ten

be

ck

sph

ere

: Mo

de

rn Ti

me

s G

rou

p M

TG A

B, M

etro

Inte

rna

tion

al S

.A. p

lus

the

me

dia

ho

ldin

gs

of T

ele

2 A

B (2

000-

2006

). A

ll c

om

pa

nie

s a

re c

on

trolle

d b

y th

e S

ten

be

ck

fam

ily.

Fro

m 2

007

on

th

e m

ed

ia h

old

ing

s o

f Te

le2

AB,

i.e

. ca

ble

TV

op

era

tion

s in

Sw

ed

en

, are

no

t d

iffe

ren

tiate

d in

th

e c

om

pa

ny’s

ac

co

un

ts a

nd

are

th

ere

fore

no

t in

clu

de

d t

he

rea

fter

(rev

en

ue

200

6 w

as

24 M

Euro

). Th

e G

rou

p’s

inte

rne

t re

taili

ng

bu

sin

ess

CD

ON

Gro

up

AB

wa

s d

em

erg

ed

at

the

en

d o

f 201

0 a

nd

its

sha

res

we

re d

istr

ibu

ted

to M

TG’s

sh

are

ho

lde

rs. C

DO

N’s

reve

nu

e o

f 231

MEu

ro is

no

t in

clu

de

d in

MTG

’s in

co

me

sta

tem

en

t fo

r 201

0, n

or i

n th

e c

olle

cte

d S

ten

be

ck

reve

nu

e a

bo

ve.

3 T

ele

no

r’s b

roa

dc

ast

ing

div

isio

n. T

ele

no

r ASA

’s to

tal v

olu

me

for 2

010

wa

s 11

826

MEu

ro.

4 D

ata

refe

r to

Fö

rva

ltnin

gss

tifte

lse

n, i

.e. t

he

ow

ne

r fo

un

da

tion

of S

we

de

n’s

th

ree

pu

blic

se

rvic

e p

rog

ram

me

co

mp

an

ies:

SR

(ra

dio

), SV

T (t

ele

visi

on

) a

nd

UR

(ed

uc

atio

na

l pro

gra

mm

es,

turn

ove

r 37

M

Euro

in 2

010)

. Da

ta e

xclu

de

tra

nsa

ctio

ns

with

in th

e g

rou

p.

5 N

ord

ic m

ark

et o

nly

, wh

ich

rep

rese

nts

47%

of M

ec

om

’s to

tal r

eve

nu

e in

201

0 (1

415

MEu

ro).

The

op

era

tion

s, fo

rme

rly p

art

of t

he

No

rwe

gia

n c

om

pa

ny, O

rkla

Me

dia

, we

re s

old

to th

e B

ritis

h c

om

pa

ny

Me

co

m G

rou

p P

lc in

Fa

ll 20

06. O

pe

ratio

ns

in N

orw

ay

we

re re

na

me

d E

dd

a M

ed

ia A

S; th

e D

an

ish

op

era

tion

s w

ere

inte

gra

ted

into

De

t Be

rlin

gsk

e O

ffic

in (

tod

ay

Berli

ng

ske

Me

dia

). (I

n D

ec

em

be

r 201

1 M

ec

om

an

d A

-pre

sse

n re

ac

he

d a

n a

gre

em

en

t wh

ere

by

A-p

ress

en

will

ac

qu

ire E

dd

a M

ed

ia. T

he

ag

ree

me

nt i

s p

en

din

g a

pp

rova

l by

No

rwe

gia

n c

om

pe

titio

n a

uth

orit

ies.

)6

Ork

la M

ed

ia a

cq

uire

d th

e D

an

ish

new

spa

pe

r co

mp

any

De

t Be

rlin

gsk

e O

ffic

in in

late

200

0, ju

ridic

ally

1 J

an

ua

ry 2

001.

Rev

en

ue

for 2

000

is p

ro fo

rma

an

d in

clu

de

s D

et B

erli

ng

ske

Offi

cin

. In

200

6 O

rkla

M

ed

ia’s

pa

ren

t co

mp

any

, Ork

la A

SA, s

old

Ork

la M

ed

ia to

the

Brit

ish

co

mp

any

Me

co

m G

rou

p P

lc (

see

no

te 5

). 7

Da

ta fo

r TD

C’s

su

bsi

dia

ry Y

ou

See

A/S

(c

ab

le-T

V p

rovi

de

r). Y

ou

See

is th

e n

am

e fr

om

200

7 o

n; p

revi

ou

s n

am

e w

as

TDC

Ka

be

l-TV.

TD

C G

rou

p’s

tota

l vo

lum

e 2

010

wa

s 3

512

MEu

ro.

8 2

000=

1999

/200

0 e

tc.

9 D

ata

for 2

000-

2005

an

d 2

009-

2010

rep

rese

nt C

om

He

m A

B; 2

006-

2008

No

rdic

Ca

ble

Ac

qu

isiti

on

Ho

ldin

g A

B (t

he

the

n o

wn

er o

f Co

m H

em

). 10

Po

litik

en

an

d J

ylla

nd

s-Po

ste

n m

erg

ed

1 J

an

200

3 to

form

JP/

Polit

ike

ns

Hu

s A

/S.

11 P

roSi

eb

en

Sa

t.1 G

rou

p a

cq

uire

d m

ed

ia h

old

ing

s in

the

No

rdic

co

un

trie

s in

200

7 b

y p

urc

ha

sin

g S

BS B

roa

dc

ast

ing

, co

nso

lida

ted

into

Pro

Sie

be

nSa

t.1 a

s o

f 1 J

uly

200

7. D

ata

ab

ove

inc

lud

e th

e N

ord

ic

ma

rke

t on

ly, w

hic

h re

pre

sen

ts 1

3% o

f Pro

Sie

be

nSa

t.1’s

tota

l rev

en

ue

in 2

010

(3 0

00 M

Euro

).

12

No

rdic

Ma

rke

t on

ly, w

hic

h in

200

6 re

pre

sen

ted

48%

of S

BS B

roa

dc

ast

ing

’s to

tal v

olu

me

.13

Da

ta fo

r 200

3 a

nd

the

rea

fter r

ep

rese

nt Y

leis

rad

io O

y; e

arli

er d

ata

rep

rese

nt Y

LE G

rou

p, w

hic

h in

clu

de

d th

e T

V n

etw

ork

op

era

tor D

igita

Oy.

14 T

he

me

dia

ho

ldin

gs

of

KF, K

oo

pe

rativ

a F

örb

un

de

t (t

he

Sw

ed

ish

Co

op

era

tive

Un

ion

). D

ata

200

0-20

05, 2

010:

exc

lud

ing

tra

nsa

ctio

ns

with

in t

he

gro

up

, 200

6-20

09: i

nc

lud

ing

tra

nsa

ctio

ns

with

in t

he

g

rou

p. K

F’s

tota

l rev

en

ue

for 2

010

wa

s 3

835

MEu

ro.

Sou

rce

s: C

om

pa

ny a

nn

ua

l re

po

rts

an

d w

eb

site

s.

NORDICOM 18 Nordic Public Service Media Map 1/2012

THE NORDIC MEDIA MARKET

5. The 20 largest Nordic media companies’ and public service broadcasters’ total revenue 1995-2010 (EUR millions)

1 DR, YLE, NRK and SVT/SR/UR (all of which are also included in top 20 total). Not including TV 2 / Danmark.

Note: Data for 2005 and 2007 include some estimates. TV distribution companies are not included.

Sources: Company annual reports, Nordicom.

0

2 000

4 000

6 000

8 000

10 000

12 000

14 000

16 000

18 000

20 000

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

EUR

mill

ion

s

Top 20 total Public service broadcasters1

4. The 20 largest Nordic media companies’ total revenue and public service broadcasters’ share 1995-2010 (EUR millions)

Revenue (EUR millions)

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Top 20 total 7 583 8 326 8 467 9 125 10 580 11 611 12 013 13 122 13 367 13 995 14 818 15 744 18 046 18 204 16 570 17 623

Public service broadcasters1 1 544 1 656 1 665 1 674 1 752 1 837 1 884 1 958 1 926 2 002 2 056 2 081 2 129 2 118 2 072 2 293

PSBs’ share of all (%) 20 20 20 18 17 16 16 15 14 14 14 13 12 12 13 13

1 DR, YLE, NRK and SVT/SR/UR (all of which are also included in top 20 total). Not including TV 2 / Danmark.

Note: Data for 2005 and 2007 include some estimates. TV distribution companies are not included.

Sources: Company annual reports, Nordicom.

THE NORDIC MEDIA MARKET

NORDICOM 19 Nordic Public Service Media Map 1/2012

6. T

he

20

larg

est

me

dia

co

mp

an

ies

by

me

dia

reve

nue

on

th

e N

ord

ic m

ed

ia m

ark

et

2010

(EU

R m

illio

ns)

Me

dia

reve

nu

e

Ch

an

ge

in m

ed

ia

In

the

No

rdic

To

tal c

om

pa

ny

No

rdic

sh

are

of

reve

nu

e in

the

To

tal c

om

pa

ny

Me

dia

sh

are

of

c

ou

ntr

ies

me

dia

reve

nu

e

tota

l me

dia

reve

nu

e

No

rdic

co

un

trie

s re

ven

ue

to

tal c

om

pa

ny

Me

dia

co

mp

any

D

om

icile

(E

UR

mill

ion

s)

(EU

R m

illio

ns)

(%

) 20

09/2

010

(%)

(EU

R m

illio

ns)

re

ven

ue

(%

)

1 Bo

nn

ier

Swe

de

n

2 66

2 3

225

83

13

3 22

5 10

0

2 Sa

no

ma

Fi

nla

nd

1

433

2 76

1 52

0

2 76

1 10

0

3 Sc

hib

ste

d M

ed

ia G

rou

p

No

rwa

y 1

432

1 71

9 83

21

1

719

100

5 Eg

mo

nt1

De

nm

ark

1

169

1 42

0 82

-1

1

420

100

4 St

en

be

ck:

MTG

/Me

tro2

Swe

de

n

1 11

2 1

593

70

9 9

897

16

6 Te

len

or B

roa

dc

ast

1,3

No

rwa

y 1

091

1 09

1 10

0 12

11

826

9

7 SV

T/SR

/UR

(Fö

rva

ltnin

gss

tifte

lse

n)4

Swe

de

n

770

770

100

19

770

100

8 M

ec

om

Gro

up

U

K 66

5 1

415

47

2 1

415

100

9 N

RK

No

rwa

y 60

7 60

7 10

0 16

60

7 10

0

10

Sta

mp

en

Sw

ed

en

54

5 54

5 10

0 14

54

5 10

0

11

TDC

: Yo

uSe

e5

De

nm

ark

53

9 53

9 10

0 12

3

512

15

12

A-p

ress

en

1 N

orw

ay

532

580

92

11

580

100

13

Alle

r6 D

en

ma

rk

526

526

100

1 52

6 10

0

14

DR

De

nm

ark

51

8 51

8 10

0 3

518

100

15

Co

m H

em

Sw

ed

en

45

3 45

3 10

0 18

45

3 10

0

16

JP/P

olit

ike

ns

Hu

s D

en

ma

rk

440

440

100

0 44

0 10

0

17

Tera

co

m

Swe

de

n

404

404

100

27

404

100

18

Pro

Sie

be

nSa

t.1 G

rou

p

Ge

rma

ny

399

3 00

0 13

19

3

000

100

19

YLE

Fin

lan

d

398

398

100

1 39

8 10

0

20

TV 2

Gro

up

1 N

orw

ay

337

337

100

21

337

100

1 O

n t

he

No

rwe

gia

n m

ed

ia m

ark

et

the

re is

so

me

cro

ss o

wn

ers

hip

: Te

len

or A

SA o

wn

s 44

% o

f A-p

ress

en

, wh

ich

in

its tu

rn o

wn

s 50

% o

f th

e T

V 2

Gro

up

. Th

e o

the

r 50%

of t

he

TV

2 G

rou

p is

ow

ne

d b

y D

an

ish

Eg

mo

nt.

TV 2

Gro

up

’s

reve

nu

e is

inc

lud

ed

in

A-p

ress

en

’s a

nd

Eg

mo

nt’s

ac

co

un

ts a

cc

ord

ing

to s

ha

re o

f ow

ne

rsh

ip. (

In J

an

ua

ry 2

012

A-p

ress

en

so

ld it

s sh

are

in th

e T

V 2

Gro

up

to E

gm

on

t, w

hic

h is

no

w fu

ll o

wn

er o

f th

e g

rou

p.)

2 Th

e m

ed

ia h

old

ing

s o

f th

e S

ten

be

ck

sph

ere

: Mo

de

rn T

ime

s G

rou

p M

TG A

B a

nd

Me

tro In

tern

atio

na

l S.A

. Th

e

Gro

up

’s in

tern

et

reta

ilin

g b

usi

ne

ss C

DO

N G

rou

p A

B w

as

de

me

rge

d a

t th

e e

nd

of

2010

an

d it

s sh

are

s w

ere

d

istr

ibu

ted

to M

TG’s

sh

are

ho

lde

rs. C

DO

N’s

reve

nu

e o

f 231

Me

uro

is n

ot i

nc

lud

ed

in M

TG’s

inc

om

e s

tate

me

nt f

or

2010

, no

r in

the

co

llec

ted

Ste

nb

ec

k m

ed

ia re

ven

ue

ab

ove

.

3 T

ele

no

r’s b

roa

dc

ast

ing

div

isio

n. T

ele

no

r ASA

’s to

tal v

olu

me

201

0 w

as

11 8

26 M

Euro

.4

Da

ta re

fer t

o F

örv

altn

ing

sstif

tels

en

, i e

the

ow

ne

r fo

un

da

tion

of S

we

de

n’s

thre

e p

ub

lic s

erv

ice

pro

gra

mm

e c

om

-p

an

ies:

SR

(ra

dio

), S

VT

(te

levi

sio

n)

an

d U

R (e

du

ca

tion

al p

rog

ram

me

s). D

ata

exc

lud

e t

ran

sac

tion

s w

ithin

th

e

gro

up

.5

TD

C’s

bro

ad

ca

stin

g s

ub

sid

iary

Yo

uSe

e A

/S. T

DC

’s to

tal v

olu

me

201

0 w

as

3 51

2 M

Euro

.6

Fin

an

cia

l ye

ar 1

Oc

tob

er 2

009

– 30

Se

pte

mb

er 2

010.

Sou

rce

s: C

om

pa

ny a

nn

ua

l re

po

rts

an

d w

eb

site

s.

NORDICOM 20 Nordic Public Service Media Map 1/2012

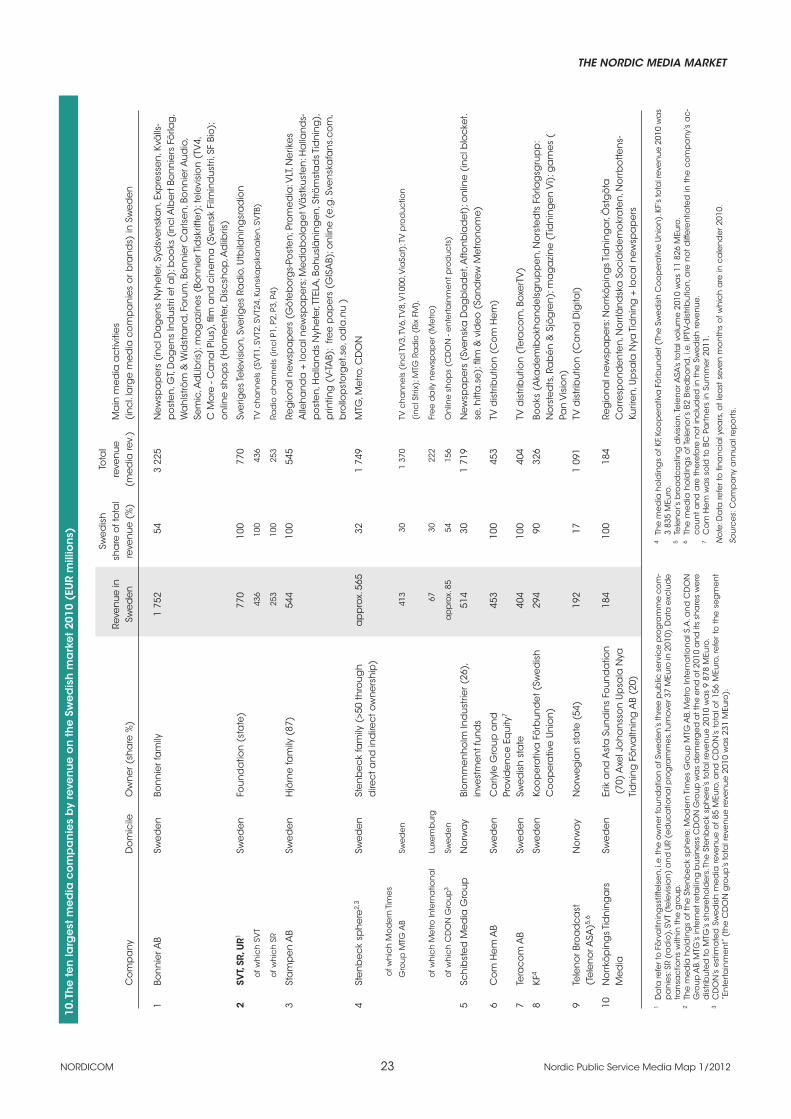

THE NORDIC MEDIA MARKET7.

Th

e te

n la

rge

st m

ed

ia c

om

pa

nie

s b

y re

venu

e o

n t

he

Fin

nis

h m

ark

et

2010

(EU

R m

illio

ns)

Fi

nn

ish

Re

ven

ue

in

sha

re o

f to

tal

Tota

l M

ain

me

dia

ac

tiviti

es

C

om

pa

ny

Do

mic

ile

Ow

ne

r (sh

are

%)

Fin

lan

d

reve

nu

e (

%)

reve

nu

e

(in

cl.

larg

e m

ed

ia c

om

pa

nie

s o

r bra

nd

s) in

Fin

lan

d

1 Sa

no

ma

Oyj

Fi

nla

nd

Er

kko

fam

ily (

41)

1 41

7 51

2

761

Da

ily n

ewsp

ap

ers

(in

cl.

He

lsin

gin

Sa

no

ma

t, Ilt

a-S

an

om

at)

, we

b-o

nly

new

spa

pe

r (Ta

lou

sssa

no

ma

t.fi),

free

da

ily n

ewsp

ap

er (

Me

tro),

ma

ga

zin

es

(Sa

no

ma

Ma

ga

zin

es)

, le

arn

ing

ma

teria

ls a

nd

so

lutio

ns,

TV c

ha

nn

els

(in

cl.

Ne

lon

en

, Jim

, Liv

), ra

dio

ch

an

ne

ls (

inc

l. Ra

dio

Ro

ck,

Rad

io A

alto

), w

eb

ma

rke

tpla

ce

s

2 YL

E, Y

leis

rad

io O

y Fi

nla

nd

Th

e F

inn

ish

sta

te

398

100

398

TV c

ha

nn

els

(YL

E TV

1, Y

LE T

V2,

YLE

Tee

ma

, YLE

FST

5), r

ad

io c

ha

nn

els

(in

cl. Y

LE R

ad

io1,

YLE

Ra

dio

Su

om

i, YLE

Ra

dio

Ve

ga

)

3 Bo

nn

ier A

B Sw

ed

en

Bo

nn

ier f

am

ily

375

12

3 22

5 TV

ch

an

ne

ls (

inc

l. M

TV3,

Su

b, A

va, C

Mo

re -

Ca

na

l Plu

s), r

ad

io

c

ha

nn

el (

Rad

io N

ova

), b

oo

ks (

Tam

mi,

WSO

Y), m

ag

azi

ne

s (B

on

nie

r

Pub

lica

tion

s), p

ho

no

gra

ms,

vid

eo

4 A

lma

Me

dia

Oyj

Fi

nla

nd

Ilk

ka-Y

hty

mä

(30

) 29

8 96

31

1 D

aily

new

spa

pe

rs (

inc

l. A

am

ule

hti,

Ilta

leh

ti, K

au

pp

ale

hti)

, lo

ca

l

new

spa

pe

rs, c

ust

om

er m

ag

azi

ne

s (A

lma

Me

dia

Le

hd

en

teki

jät)

,

we

b m

ark

etp

lac

es

6 TS

-Yh

tym

ä O

y Fi

nla

nd

Ke

ton

en

fam

ily

190

89

213

Da

ily n

ewsp

ap

ers

(in

cl. T

uru

n S

an

om

at)

, lo

ca

l new

spa

pe

rs, l

oc

al

ra

dio

ch

an

ne

ls, p

rintin

g

5 O

tava

Oy

Fin

lan

d

Ree

np

ää

fam

ily

222

99

223

Boo

ks (

Kust

an

nu

sosa

keyh

tiö O

tava

, Lik

e K

ust

an

nu

s), c

on

sum

er

m

ag

azi

ne

s (O

tava

me

dia

), c

ust

om

er m

ag

azi

ne

s, b

oo

k c

lub

s

(i

nc

l. Su

uri

Suo

ma

lain

en

Kirj

ake

rho

)

8 Ke

skis

uo

ma

lain

en

Oyj

Fi

nla

nd

N

o m

ajo

r ow

ne

r 10

2 10

0 10

2 D

aily

new

spa

pe

rs (

inc

l. Ke

skis

uo

ma

lain

en

, Sa

von

Sa

no

ma

t), l

oc

al

n

ewsp

ap

ers

7 Ed

ita O

y Fi

nla

nd

Th

e F

inn

ish

sta

te

57

52

110

Boo

ks, c

ust

om

er m

ag

azi

ne

s, m

ark

etin

g c

om

mu

nic

atio

ns

serv

ice

s,

p

rintin

g

9 A

-leh

de

t Oy

Fin

lan

d

Lyyt

ikä

ine

n fa

mily

91

10

0 91

C

on

sum

er m

ag

azi

ne

s (A

-leh

de

t, Im

ag

e K

ust

an

nu

s), c

ust

om

er

m

ag

azi

ne

s (M

ark

kin

oin

tivie

stin

tä D

ialo

gi)

10

Poh

jois

-Ka

rjala

n k

irja

pa

ino

Fi

nla

nd

La

akk

on

en

fam

ily

85

100

85

Da

ily n

ewsp

ap

er (

Karja

lain

en

), lo

ca

l new

spa

pe

rs, p

rintin

g

Sou

rce

s: C

om

pa

ny a

nn

ua

l re

po

rts

an

d w

eb

site

s, St

atis

tics

Fin

lan

d.

THE NORDIC MEDIA MARKET

NORDICOM 21 Nordic Public Service Media Map 1/2012

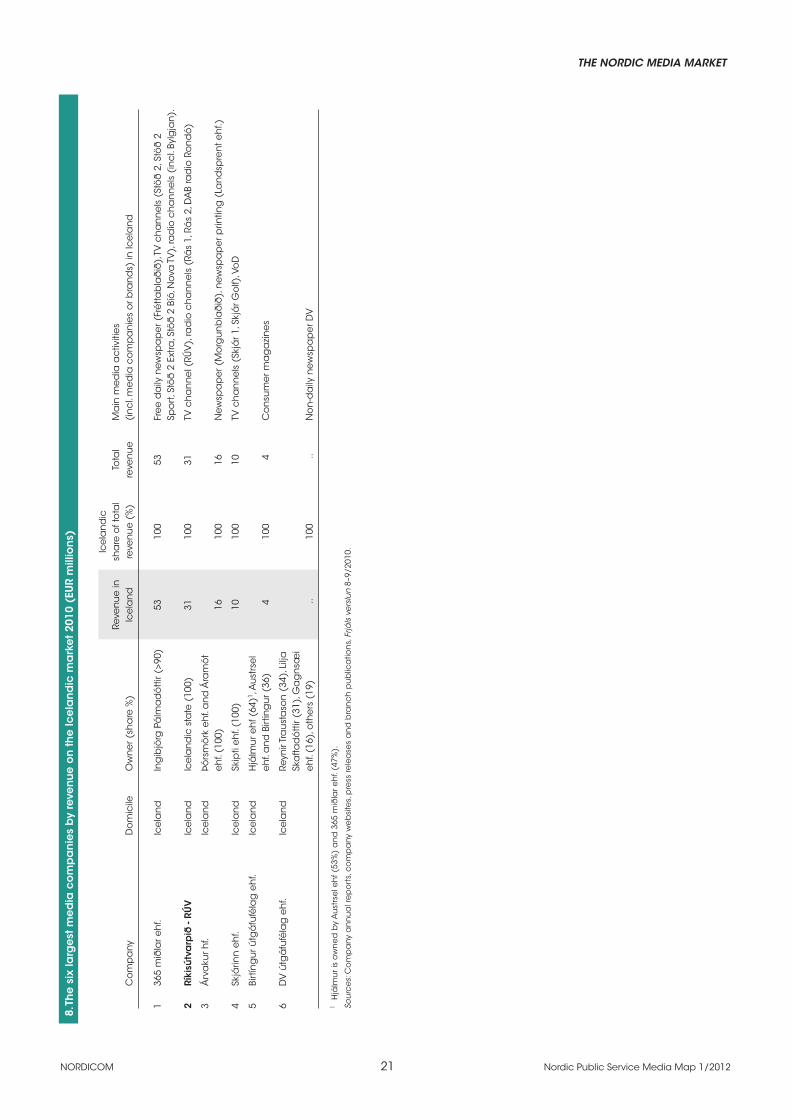

8. T

he

six

larg

est

me

dia

co

mp

an

ies

by

reve

nue

on

th

e Ic

ela

nd

ic m

ark

et

2010

(EU

R m

illio

ns)

Ic

ela

nd

ic

Reve

nu

e in

sh

are

of t

ota

l To

tal

Ma

in m

ed

ia a

ctiv

itie

s

Co

mp

any

D

om

icile

O

wn

er (

sha

re %

) Ic

ela

nd

re

ven

ue

(%

) re

ven

ue

(i

nc

l. m

ed

ia c

om

pa

nie

s o

r bra

nd

s) in

Ice

lan

d

1 36

5 m

iðla

r eh

f. Ic

ela

nd

In

gib

jörg

Pá

lma

dó

ttir

(>90

) 53

10

0 53

Fr

ee

da

ily n

ewsp

ap

er (

Fré

ttab

lað

ið),

TV c

ha

nn

els

(St

öð

2, S

töð

2

Sp

ort

, Stö

ð 2

Ext

ra, S

töð

2 B

íó, N

ova

TV

), ra

dio

ch

an

ne

ls (

inc

l. By

lgja

n).

2 Rí

kisú

tva

rpið

- RÚ

V

Ice

lan

d

Ice

lan

dic

sta

te (

100)

31

10

0 31

TV

ch

an

ne

l (RÚ

V),

rad

io c

ha

nn

els

(Rá

s 1,

Rá

s 2,

DA

B ra

dio

Ro

nd

ó)

3 Á

rva

kur h

f. Ic

ela

nd

Þó

rsm

örk

eh

f. a

nd

Ára

mó

t

eh

f. (1

00)

16

100

16

New

spa

pe

r (M

org

un

bla

ðið

), n

ewsp

ap

er p

rintin

g (

Lan

dsp

ren

t eh

f.)

4 Sk

járin

n e

hf.

Ice

lan

d

Skip

ti e

hf.

(100

) 10

10

0 10

TV

ch

an

ne

ls (

Skjá

r 1, S

kjá

r Go

lf), V

oD

5 Bi

rtín

gu

r útg

áfu

féla

g e

hf.

Ice

lan

d

Hjá

lmu

r eh

f (64

)1 , A

ust

rse

l

eh

f. a

nd

Birt

ing

ur (

36)

4 10

0 4

Co

nsu

me

r ma

ga

zin

es

6 D

V ú

tgá

fufé

lag

eh

f. Ic

ela

nd

Re

ynir

Tra

ust

aso

n (

34),

Lilja

Ska

ftad

ótt

ir (3

1), G

ag

nsæ

i

eh

f. (1

6), o

the

rs (

19)

.. 10

0 ..

No

n-d

aily

new

spa

pe

r DV

1 H

jálm

ur i

s o

wn

ed

by

Au

strs

el e

hf (

53%

) a

nd

365

mið

lar e

hf.

(47%

).

Sou

rce

s: C

om

pa

ny a

nn

ua

l re

po

rts,

co

mp

any

we

bsi

tes,

pre

ss re

lea

ses

an

d b

ran

ch

pu

blic

atio

ns,

Frjá

ls v

ers

lun

8–9

/201

0.

NORDICOM 22 Nordic Public Service Media Map 1/2012

THE NORDIC MEDIA MARKET9.

Th

e te

n la

rge

st m

ed

ia c

om

pa

nie

s b

y re

venu

e o

n t

he

No

rwe

gia

n m

ark

et

2010

(EU

R m

illio

ns)

N

orw

eg

ian

Re

ven

ue

in

sha

re o

f to

tal

Tota

l M

ain

me

dia

ac

tiviti

es

C

om

pa

ny

Do

mic

ile

Ow

ne

r (sh

are

%)

No

rwa

y re

ven

ue

(%

) re

ven

ue

(i

nc

l. m

ed

ia c

om

pa

nie

s o

r bra

nd

s) in

No

rwa

y

1 Sc

hib

ste

d M

ed

ia G

rou

p

No

rwa

y Bl

om

me

nh

olm

Ind

ust

rier

918

53

1 72

0 N

ewsp

ap

ers

(in

cl. V

G, A

ften

po

ste

n, B

erg

en

s Ti

de

nd

e, S

tava

ng

er

(S

tifte

lse

n T

iniu

s) (

26),

Afte

nb

lad

), o

nlin

e c

lass

ifie

ds

(Fin

n.n

o),

bo

oks

/ma

ga

zin

es

Fo

lke

tryg

dfo

nd

et (

8)

(S

ch

ibst

ed

Fo

rlag

).

2 Te

len

or G

rou

p

No

rwa

y N

orw

eg

ian

sta

te (

54),

62

5 57

1

091

TV a

nd

rad

io d

istr

ibu

tion

via

ca

ble

, sa

telli

te a

nd

DTT

(in

cl.

Ca

na

l

(Te

len

or B

roa

dc

ast

)1,2

Fo

lke

tryg

dfo

nd

et (

5)

D

igita

l, N

ork

ring

, Rik

sTV

33%

), TV

ch

an

ne

ls (

TV 2

Ze

bra

45%

, TV

2 S

po

rt

45

%, C

an

al+

/C M

ore

Gro

up

35%

)

3 N

RK A

S N

orw

ay

No

rwe

gia

n s

tate

60

7 10

0 60

7 TV

(in

cl.

NRK

1, N

RK2,

NRK

3), r

ad

io (

inc

l. P1

, P2,

P3)

, TV

dis

trib

utio

n

(R

iksT

V 3

3%)

4 Eg

mo

nt F

ou

nd

atio

n2

De

nm

ark

Se

lf-o

wn

ing

fou

nd

atio

n

585

41

1 42

0 Bo

oks

& m

ag

azi

ne

s (C

ap

pe

len

Da

mm

50%

, Eg

mo

nt H

jem

me

t

Mo

rte

nse

n, E

gm

on

t Se

riefo

rlag

et)

, film

dis

trib

utio

n (

No

rdis

k Fi

lm),

TV (

TV 2

Gru

pp

en

50%

)

5 A

-pre

sse

n A

S2 N

orw

ay

Tele

no

r (44

), LO

an

d c

on

ne

cte

d

532

92

580

49 lo

ca

l new

spa

pe

rs, N

etta

vise

n (

50%

), TV

2 G

rou

p (

50%

)

lab

ou

r un

ion

s (4

5), A

-pre

sse

n (

8),

Th

e F

ree

do

m o

f Exp

ress

ion

Fou

nd

atio

n (

3)

6 TV

2 G

rou

p A

S2 N

orw

ay

A-p

ress

en

(50

), Eg

mo

nt (

50)

338

100

338

TV (

inc

l. TV

2, T

V 2

Blis

s, TV

2 N

yhe

tska

na

len

, TV

2 F

ilmka

na

len

, TV

2

Ze

bra

55%

, TV

2 S

po

rt 5

5%),

TV d

istr

ibu

tion

(Ri

ksTV

33%

)

7 Bo

nn

ier A

B Sw

ed

en

Bo

nn

ier f

am

ily

302

9 3

225

Boo

ks &

ma

ga

zin

es

(Ca

pp

ele

n D

am

m 5

0%, B

on

nie

r Me

dia

), fil

m

d

istr

ibu

tion

(SF

No

rge

), c

ine

ma

s (S

F Ki

no

)

8 M

ec

om

Gro

up

Plc

U

K A

viva

Plc

(19

), Le

ga

l & G

en

era

l 26

1 18

1

415

Edd

a M

ed

ia (

21 lo

ca

l new

spa

pe

rs)

G

rou

p P

lc (

16),

Jup

iter A

sse

t

Ma

na

ge

me

nt L

imite

d (

8)

9 M

od

ern

Tim

es

Gro

up

Sw

ed

en

St

en

be

ck

fam

ily (

>50

thro

ug

h

252

18

1 37

0 TV

(TV

3, V

iasa

t 4, T

V10

00),

rad

io (

P4, P

5), T

V p

rod

uc

tion

MTG

AB

d

irec

t an

d in

dire

ct o

wn

ers

hip

)

(Str

ix Te

levi

sjo

n),

TV d

istr

ibu

tion

(V

iasa

t).

10

Pola

ris M

ed

ia A

SA3

No

rwa

y SE

B En

skild

a (

32),

Roll

Seve

rin

226

100

226

24 re

gio

na

l an

d lo

ca

l new

spa

pe

rs

C

o A

S’b

an

kru

ptc

y e

sta

te (

19),

Mu

st In

vest

(15

%),

Sch

ibst

ed

Me

dia

Gro

up

(7%

)

1 T

ele

no

r’s m

ed

ia re

ven

ue

in N

orw

ay

is m

ed

ian

orw

ay’

s e

stim

ate

. Th

e w

eb

po

rta

l ABC

Sta

rtsi

de

n in

clu

de

d, r

eve

nu

e

in N

orw

ay

2010

am

ou

nts

to 6

42 M

Euro

, an

d Te

len

or B

roa

dc

ast

’s to

tal (

all

co

un

trie

s) to

1 1

09 M

Euro

. Th

e Te

len

or

gro

up

’s to

tal r

eve

nu

e w

as

11 8

45 M

Euro

. 2

On

th

e N

orw

eg

ian

me

dia

ma

rke

t, th

ere

is s

om

e c

ross

ow

ne

rsh

ip: T

ele

no

r ASA

ow

ns

44%

of A

-pre

sse

n, w

hic

h in

its

tu

rn o

wn

s 50

% o

f th

e T

V 2

Gro

up

. Th

e o

the

r 50

% o

f th

e T

V2

Gro

up

is o

wn

ed

by

Da

nis

h E

gm

on

t. TV

2 G

rou

p’s

re

ven

ue

is in

clu

de

d in

A-p

ress

en

’s a

nd

Eg

mo

nt’s

ac

co

un

ts a

cc

ord

ing

to s

ha

re o

f ow

ne

rsh

ip. (

In J

an

ua

ry 2

012

A-p

ress

en

so

ld it

s sh

are

in th

e T

V 2

Gro

up

to E

gm

on

t, w

hic

h is

no

w fu

ll o

wn

er o

f th

e g

rou

p.)

3 P

ola

ris M

ed

ia is

th

e re

sult

of a

fusi

on

of r

eg

ion

al m

ed

ia h

ou

ses

in 2

008,

with

Sc

hib

ste

d a

s la

rge

st o

wn

er.

In

2009

Sc

hib

ste

d d

ep

osi

ted

mo

st o

f its

sh

are

s in

Po

laris

at

SEB

Ensk

ilda

. Th

e r

ea

son

wa

s th

at

Sch

ibst

ed

wa

s o

rde

red

by

the

Me

dia

Au

tho

rity

to s

ell

do

wn

in P

ola

ris in

co

nn

ec

tion

with

th

e e

sta

blis

hm

en

t o

f new

spa

pe

r g

rou

p M

ed

ia N

org

e. T

he

sh

are

s d

ep

osi

ted

at

SEB

Ensk

ilda

wa

s so

ld in

201

1 to

th

ree

Sw

ed

ish

ne

wsp

ap

er

gro

up

s a

nd

an

inve

stm

en

t co

mp

any

.

Sou

rce

s: C

om

pa

ny a

nn

ua

l re

po

rts,

me

dia

no

rwa

y.

THE NORDIC MEDIA MARKET

NORDICOM 23 Nordic Public Service Media Map 1/2012

10. T

he

ten

larg

est

me

dia

co

mp

an

ies

by

reve

nue

on

th

e S

we

dis

h m

ark

et

2010

(EU

R m

illio

ns)

Sw

ed

ish

To

tal

Reve

nu

e in

sh

are

of t

ota

l re

ven

ue

M

ain

me

dia

ac

tiviti

es

C

om

pa

ny

Do

mic

ile

Ow

ne

r (sh

are

%)

Swe

de

n

reve

nu

e (

%)

(me

dia

rev.

) (i

nc

l. la

rge

me

dia

co

mp

an

ies

or b

ran

ds)

in S

we

de

n

1 Bo

nn

ier A

B Sw

ed

en

Bo

nn

ier f

am

ily

1 75

2 54

3

225

New

spa

pe

rs (

inc

l Da

ge

ns

Nyh

ete

r, Sy

dsv

en

ska

n, E

xpre

sse

n, K

välls

-

po

ste

n, G

T, D

ag

en

s In

du

stri

et a

l); b

oo

ks (

inc

l Alb

ert

Bo

nn

iers

Fö

rlag

,

Wa

hls

tröm

& W

idst

ran

d, F

oru

m, B

on

nie

r Ca

rlse

n, B

on

nie

r Au

dio

,

Sem

ic, A

dLi

bris

); m

ag

azi

ne

s (B

on

nie

r Tid

skrif

ter)

; te

levi

sio

n (

TV4,

C M

ore

- C

an

al P

lus)

, film

an

d c

ine

ma

(Sv

en

sk F

ilmin

du

stri,

SF

Bio

);

o

nlin

e s

ho

ps

(Ho

me

en

ter,

Dis

csh

op

, Ad

libris

)

2 SV

T, SR

, UR1

Swe

de

n

Fou

nd

atio

n (

sta

te)

770

100

770

Sve

rige

s Te

levi

sio

n, S

verig

es

Rad

io, U

tbild

nin

gsr

ad

ion

of w

hic

h S

VT

436

100

436

TV c

ha

nn

els

(SV

T1, S

VT2

, SV

T24,

Ku

nsk

ap

ska

na

len

, SV

TB)

of w

hic

h S

R

25

3 10

0 25

3 Ra

dio

ch

an

ne

ls (

inc

l P1,

P2,

P3,

P4)

3 St

am

pe

n A

B Sw

ed

en

H

jörn

e fa

mily

(87

) 54

4 10

0 54

5 Re

gio

na

l new

spa

pe

rs (

Gö

teb

org

s-Po

ste

n; P

rom

ed

ia: V

LT, N

erik

es

Alle

ha

nd

a +

loc

al n

ewsp

ap

ers

; Me

dia

bo

lag

et V

äst

kust

en

: Ha

llan

ds-

po

ste

n, H

alla

nd

s N

yhe

ter, T

TELA

, Bo

hu

slä

nin

ge

n, S

tröm

sta

ds

Tid

nin

g),

prin

ting

(V-

TAB)

; fre

e p

ap

ers

(G

ISA

B); o

nlin

e (

e.g

. Sve

nsk

afa

ns.

co

m,

b

rollo

pst

org

et.s

e, o

dla

.nu

)

4 St

en

be

ck

sph

ere

2,3

Swe

de

n

Ste

nb

ec

k fa

mily

(>5

0 th

rou

gh

a

pp

rox.

565

32

1

749

MTG

, Me

tro, C

DO

N

d

irec

t an

d in

dire

ct o

wn

ers

hip

)

of w

hic

h M

od

ern

Tim

es

Gro

up

MTG

AB

Swe

de

n

41

3 30

1

370

TV c

ha

nn

els

(in

cl T

V3,

TV

6, T

V8,

V10

00, V

iaSa

t); T

V p

rod

uc

tion

(i

nc

l Str

ix);

MTG

Ra

dio

(Ri

x FM

),

of w

hic

h M

etro

Inte

rna

tion

al

Luxe

mb

urg

67

30

222

Fre

e d

aily

new

spa

pe

r (M

etro

)

of w

hic

h C

DO

N G

rou

p3

Swe

de

n

a

pp

rox.

85

54

156

On

line

sh

op

s (C

DO

N -

en

tert

ain

me

nt p

rod

uc

ts)

5 Sc

hib

ste

d M

ed

ia G

rou

p

No

rwa

y Bl

om

me

nh

olm

Ind

ust

rier (

26),

51

4 30

1

719

New

spa

pe

rs (

Sve

nsk

a D

ag

bla

de

t, A

fton

bla

de

t); o

nlin

e (

inc

l blo

cke

t.

inve

stm

en

t fu

nd

s

se, h

itta

.se

); fi

lm &

vid

eo

(Sa

nd

rew

Me

tron

om

e)

6 C

om

He

m A

B Sw

ed

en

C

arly

le G

rou

p a

nd

45

3 10

0 45

3 TV

dis

trib

utio

n (

Co

m H

em

)

Pro

vid

en

ce

Eq

uity

7

7 Te

rac

om

AB

Swe

de

n

Swe

dis

h s

tate

40

4 10

0 40

4 TV

dis

trib

utio

n (

Tera

co

m, B

oxe

rTV

)

8 KF

4 Sw

ed

en

Ko

op

era

tiva

Fö

rbu

nd

et (

Swe

dis

h

294

90

326

Boo

ks (

Aka

de

mib

okh

an

de

lsg

rup

pe

n, N

ors

ted

ts F

örla

gsg

rup

p:

C

oo

pe

rativ

e U

nio

n)

N

ors

ted

ts, R

ab

én

& S

jög

ren

); m

ag

azi

ne

(Ti

dn

ing

en

Vi)

; ga

me

s (

Pa

n V

isio

n)

9 Te

len

or B

roa

dc

ast

N

orw

ay

No

rwe

gia

n s

tate

(54

) 19

2 17

1

091

TV d

istr

ibu

tion

(C

an

al D

igita

l)

(T

ele

no

r ASA

)5,6

10

No

rrkö

pin

gs

Tid

nin

ga

rs

Swe

de

n

Erik

an

d A

sta

Su

nd

ins

Fou

nd

atio

n

184

100

184

Reg

ion

al n

ewsp

ap

ers

: No

rrkö

pin

gs

Tid

nin

ga

r, Ö

stg

öta

Me

dia

(70

) A

xel J

oh

an

sso

n U

psa

la N

ya

C

orre

spo

nd

en

ten

, No

rrlä

nd

ska

So

cia

lde

mo

kra

ten

, No

rrb

otte

ns-

Tid

nin

g F

örv

altn

ing

AB

(20)

Kurir

en

, Up

sala

Nya

Tid

nin

g +

loc

al n

ewsp

ap

ers

1 D

ata

refe

r to

Fö

rva

ltnin

gss

tifte

lse

n, i

.e. t

he

ow

ne

r fo

un

da

tion

of S

we

de

n’s

thre

e p

ub

lic s

erv

ice

pro

gra

mm

e c

om