purchase requisition stock requisition specifications standard recipes maximum inventory to keep on...

TRANSCRIPT

Purchase RequisitionStock Requisition

SpecificationsStandard Recipes

Maximum Inventory to Keep on HandVendor Approval

Order Record

KickbacksSteward Sales

Receiving ProceduresStorage

Food Cost AnalysisEmployee Fraud

Direct Control System

Set up an inventory control system.Know how product specifications and

standardized recipes contribute to inventory control systems.

Determine how much inventory an operation should keep on hand.

Explain the ethical and legal consequences of kickbacks and detect their presence.

Manage steward sales.Navigate the vendor approval process.Describe the receiving and storage process.Perform food cost analyses.

Understand the difference between the standard cost of food sold and the actual cost of food sold.

Conduct a physical inventory.Use inventory control procedures to keep

theft, waste, and pilferage at acceptable levels.

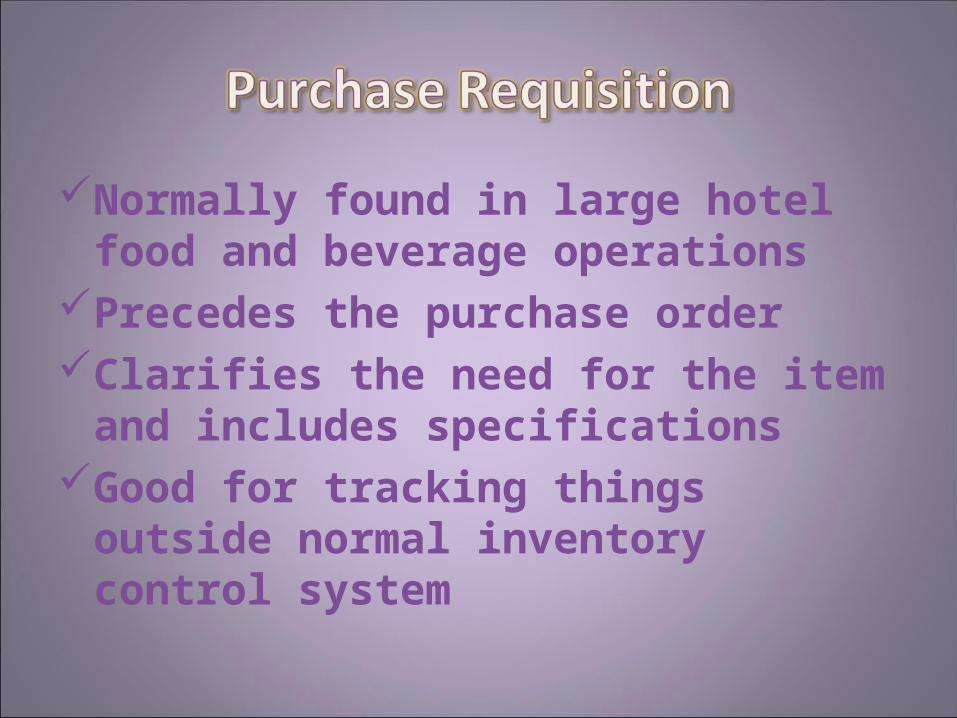

Normally found in large hotel food and beverage operations

Precedes the purchase orderClarifies the need for the item and includes

specificationsGood for tracking things outside normal

inventory control system

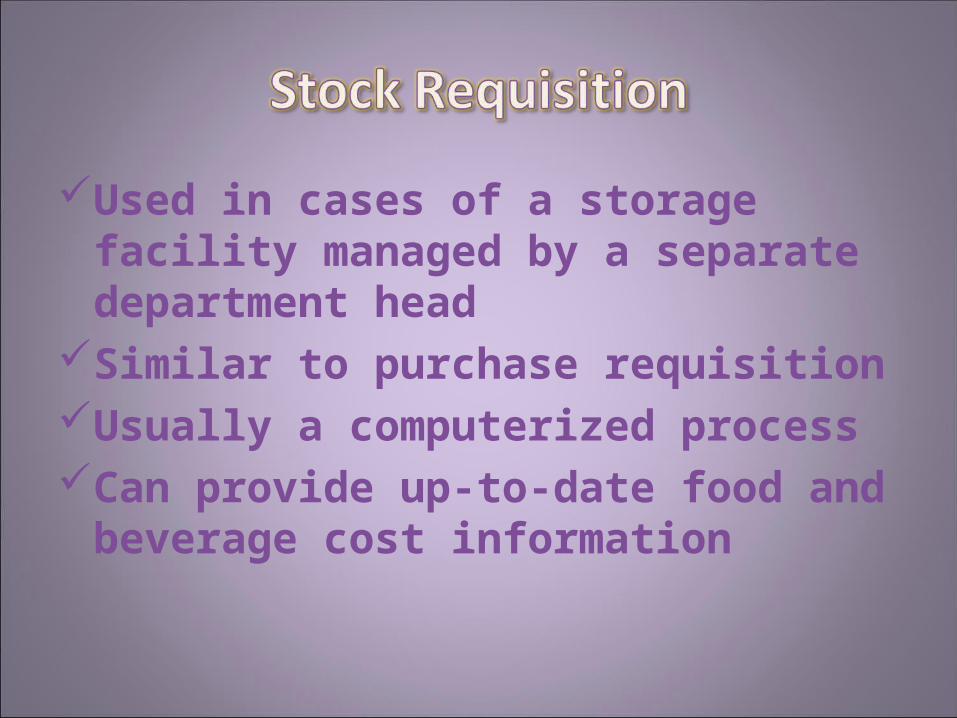

Used in cases of a storage facility managed by a separate department head

Similar to purchase requisitionUsually a computerized processCan provide up-to-date food and beverage

cost information

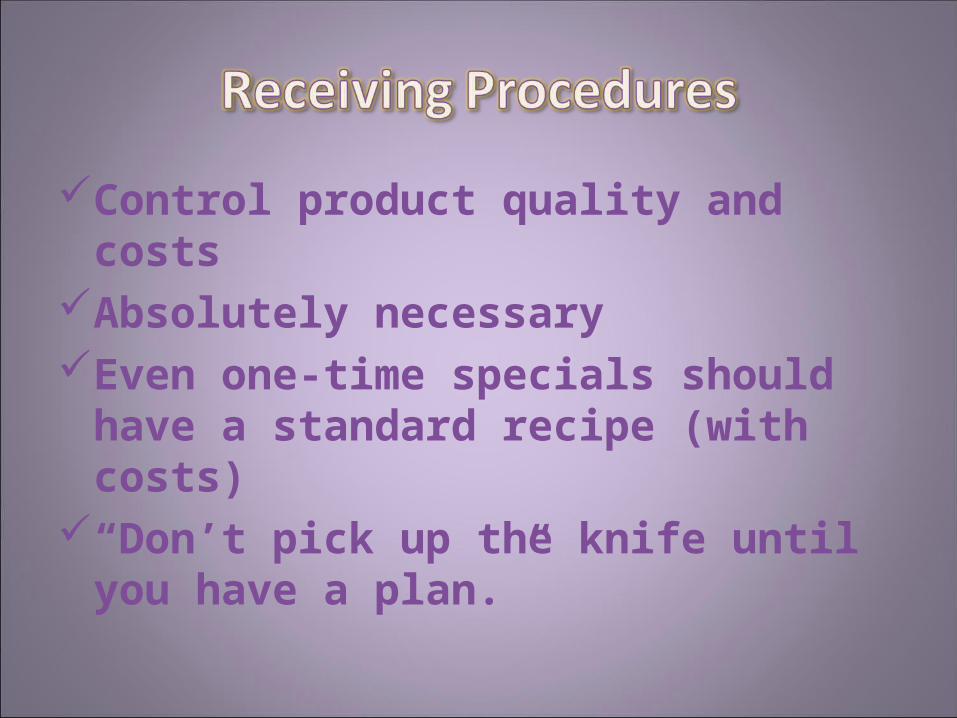

Control product quality and costsConsistency = Predictability = Better

Forecasting

Control product quality and costsAbsolutely necessaryEven one-time specials should have a

standard recipe (with costs)“Don’t pick up the knife until you have a

plan.”

Three “Rules” to Choose From:Rule #1: Value of food inventory should

not exceed a week’s food costRule #2: Total inventory should not exceed

1 percent of annual sales revenueRule #3: Food inventory should not exceed

1/3 of the monthly food cost

Example:Total Annual Revenue: $2,000,000 ($500,000

beverage alcohol; $1,500,000 food)Food Costs: 24% or $360,000 ($1,500,000 × .24)

Rule #1Food inventory should not exceed $5,923

(360,000 ÷ 52 = $5,923)

Example:Total Annual Revenue: $2,000,000 ($500,000

beverage alcohol; $1,500,000 food)Food Costs: 24% or $360,000 ($1,500,000 × .24)

Rule #2Food inventory should not exceed $20,000

($2,000,000 × .01)

Example:Total Annual Revenue: $2,000,000 ($500,000

beverage alcohol; $1,500,000 food)Food Costs: 24% or $360,000 ($1,500,000 × .24)

Rule #3Food inventory should not exceed $10,000

($360,000 ÷ 12 months × 1/3)

Most chefs prefer Rule #1Easier to meet food cost percentage goalLess spoilage and wasteNot a lot of temptation for pilferingMay pass up good dealsStockouts may increase

Authors Prefer Rule #3 for FoodCannot accept stockoutsCannot pass up good deals

Use Rule #2 if Responsible for Beverage Inventory and Operating SuppliesGives a little leeway

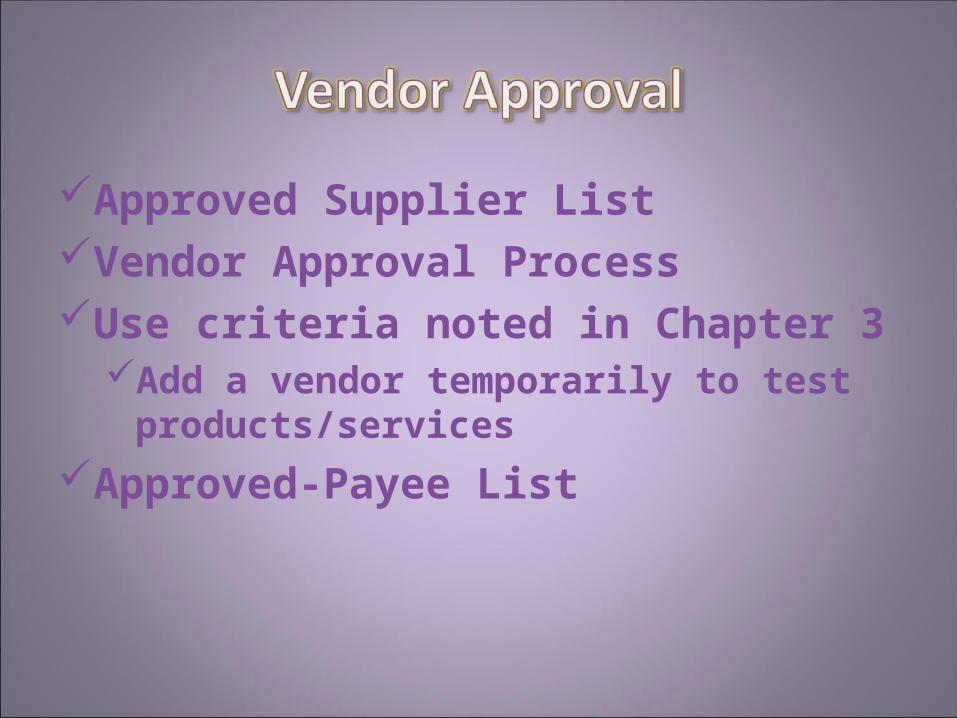

Approved Supplier ListVendor Approval ProcessUse criteria noted in Chapter 3

Add a vendor temporarily to test products/services

Approved-Payee List

Absolutely NecessaryDoesn’t Have to be Formal

Illegal gift by vendor to encourage defrauding of the restaurant

Avoid by Doing All Buying YourselfType of Fraud: Accepting lower-quality

product while paying higher AP price

Allowing employees to purchase items from the restaurant at restaurant prices

Employee perkMost large companies don’t allow thisMay increase stockouts and pilferage

Control product quality and costsAbsolutely necessaryEven one-time specials should have a

standard recipe (with costs)“Don’t pick up the knife until you have a

plan.”

IntroductionFocus on the project at-handTrust process to an extremely knowledgeable

employee or do it yourself

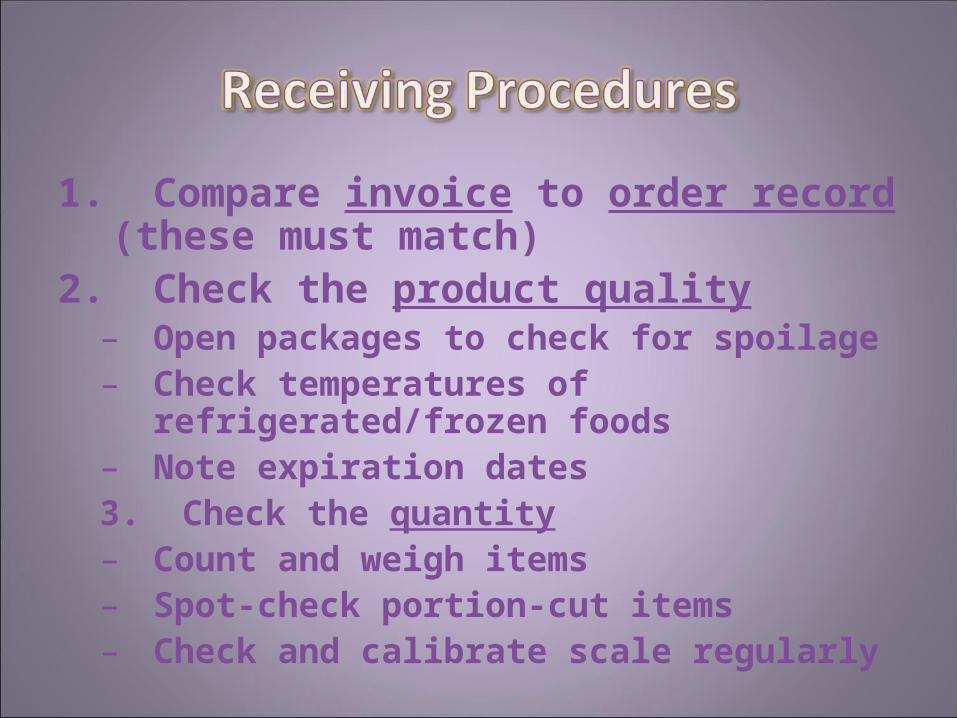

1. Compare invoice to order record (these must match)

2. Check the product quality– Open packages to check for spoilage– Check temperatures of refrigerated/frozen foods– Note expiration dates3. Check the quantity– Count and weigh items– Spot-check portion-cut items– Check and calibrate scale regularly

4. Compare AP prices to quoted prices (spot-check should be okay)

5. Accept shipment/sign invoice6. Rejecting all or part of a shipment

– Ensure proper credit7. Arrange to return unacceptable items

8. Move accepted items into storage– Refrigerated/frozen product most

important– Helps prevent pilferage– Some items may go straight to production9. Complete necessary paperwork

10. If on COD send driver to pick up check 11. If inventory is computerized, update

inventory amounts, AP price changes and bar codes

12. Give driver items for backhaul (returns or recyclables)

13. Follow same procedures with route sales14. Change process to accommodate FedEx,

UPS, etc. orders

1. Limited access is primary defense against theft or pilferage–Lock up expensive items– Other ingredients in open storeroom

2. Use good locking system– Physical locks (Medeco)– Locking system (Marlok)– Alarms (can also warn of refrigeration issues)

3. Use web cam security 4. Rotate stock

– Move older stock to the front of the shelf– Use FIFO method of inventory: first-in, first-out– Purchase a dot system (Daydots)

5. Maintain proper temperature, ventilation, humidity

6. Clean and sanitize storage area7. Arrange inventory conveniently on shelves

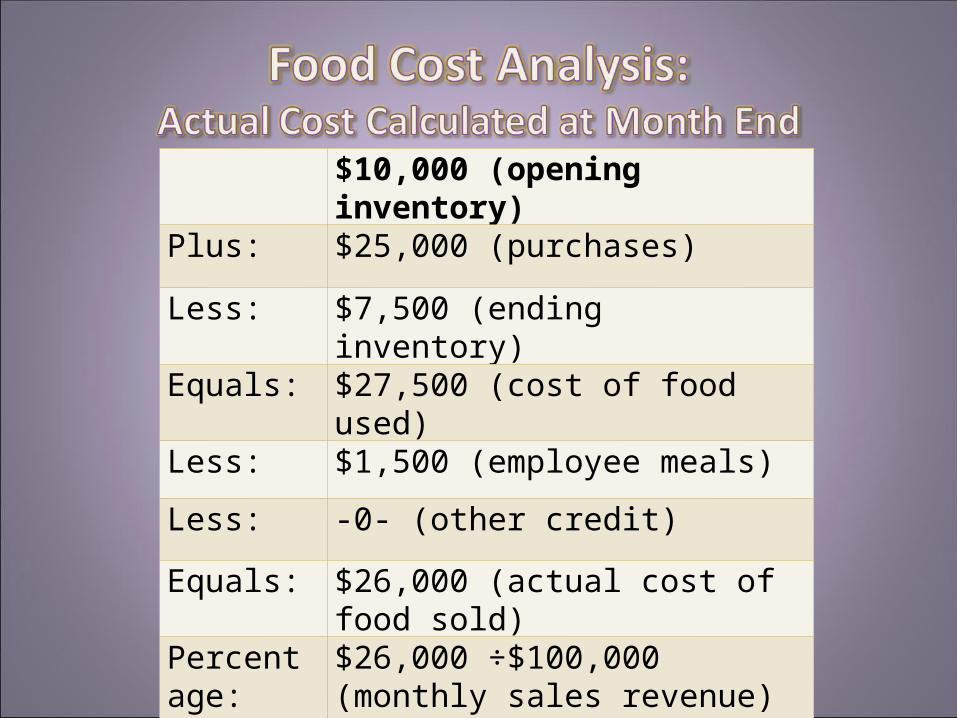

Opening (beginning) food inventory on first day of the month

Plus: Food purchases during the month

Less: Closing (ending) food inventory on last day of the month

Equals: Actual cost of food used during the month

Less: Cost of employee meals during the month (you can make an estimate)

Less: Other credit (such as manager’s personal use) during the month

Equals: Actual cost of food sold during the month

$10,000 (opening inventory)

Plus: $25,000 (purchases)

Less: $7,500 (ending inventory)

Equals: $27,500 (cost of food used)

Less: $1,500 (employee meals)

Less: -0- (other credit)

Equals: $26,000 (actual cost of food sold)

Percentage:

$26,000 ÷$100,000 (monthly sales revenue) = 0.26 or 26%

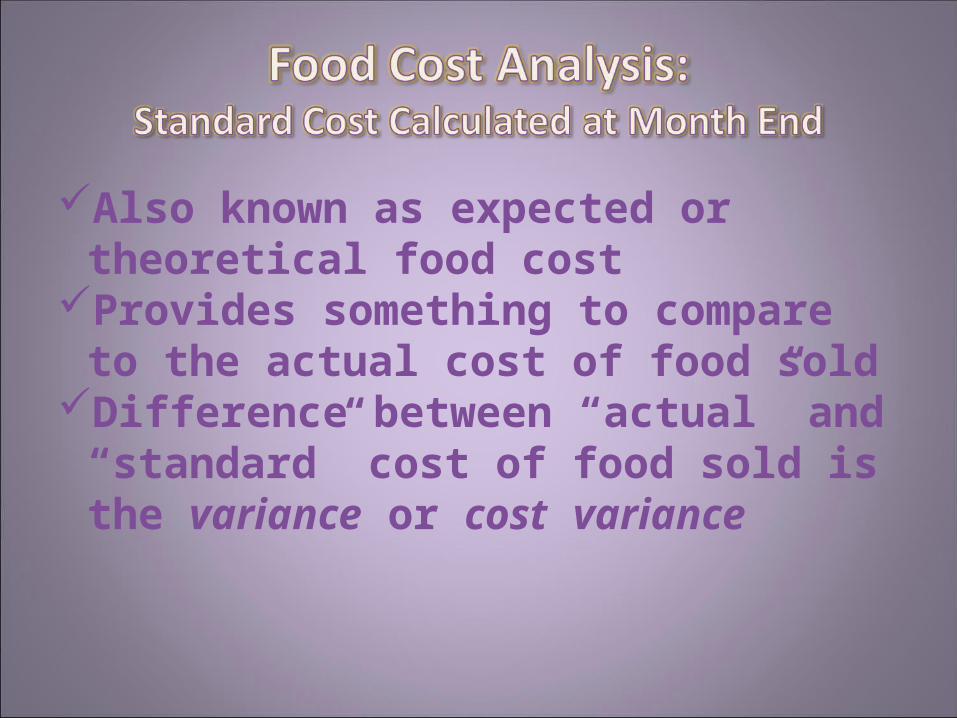

Also known as expected or theoretical food cost

Provides something to compare to the actual cost of food sold

Difference between “actual” and “standard” cost of food sold is the variance or cost variance

Need to know the following:Number of each menu item sold (from POS

system)Standard recipe cost of each item

Multiple these two figures and then add all together for total standard cost of food sold

Dividing the total standard cost by the total sales revenue gives standard cost of food sold percentage

Calculate the difference between the actual and standard cost percentages to determine the variance

If the variance is too high, the cause(s) must be found and eliminate

Often standard costs are estimates at best

A legal pad will do the trickFive columns

Typical items (fish, meat, etc.)How many at start of shiftHow many issued during shiftHow many left at end of shiftHow many used during shift

Separate sheet for each shift

Roast for pork cutlets – 25 lbs with loss of 5.5 pounds

AP price for pork roasts – $4.50 per poundStandard Portion – 9 ounces

Opening inventory – 115 pounds (AP)Issued during period – 235 pounds (AP)

Ending inventory – 110 pounds (AP)Sold – 300 cutlet entrees at price of $15.95

115 lb. + 235 lb. – 110 lb. = 240 lb. actual usage300 sold × 9 ounces = 2,700 ounces (EP)

or 169 lb. (EP)Calculate yield percentage: (25 lb. – 5.5 lb) ÷ 25

lb. = 0.78 or 78%169 ÷ .78 = 217 lb.

Should have used 217 lb. (AP) for 300 cutletsVariance = 240 lb. (AP) – 217 lb. (AP) =

23 lb. Usage Variance

23 lb. (AP) × $4.50 per lb. = $103.50 Cost Variance

23 lb. (AP) × .78 = 18 lb. (EP)18 lb. × 16 ounces per lb. = 288 ounces

288 ounces ÷ 9 = 32 portions32 portions × $15.95 =

$510.40 Sales Revenue Variance

Chicken breast for fajitas AP price for chicken breasts – $3.19 per pound

1 pound (AP) yields 3 servingsOpening Inventory – 75 pounds (AP)

Purchased during period – 90 pounds (AP)Ending inventory – 25 pounds (AP)

Sold – 350 orders of chicken fajitas for $8.95

75 lb. + 90 lb. – 25 lb. = 140 actual usage(1 lb. ÷ 3 servings) = (X lb. ÷ 3 servings) × 350X lb. = (1 lb. ÷ 3 servings) × 350 servings = 117

140 lb. – 117 lb. = 23 lb. Usage Variance

23 lb. × $3.19 per pound =$73.37 Cost Variance

23 lb. × 3 servings × $8.95 =$617.55 Sales Revenue Variance

Coffee ServiceAP price for coffee – $3.25 per pound

1 pound (AP) yields 58 cupsOpening Inventory – 50 pounds (AP)

Purchased during period – 75 pounds (AP)Ending inventory – 42 pounds (AP)

2,585 guests expected to drink 1 ½ cups each

50 lb. + 75 lb. – 42 lb. = 84 lb. actual usage2,585 customers × 1.5 cups each = 3,878 cups

3,878 cups ÷ 58 cups per pound = 67 lb. (AP) expected use − 83 lb. actual use =

16 lb. Usage Variance16 lb. × $3.25 per pound =

$52 Cost Variance (approximately)

Bar OperationAP price for Seagram’s Gin – $14.50 per liter

Drink size – 1.5 oz.Opening Inventory – 5 liters (AP)Ending inventory – 2.5 liters (AP)

75 drinks @ $6 per drink

2.5 liters = actual usage2.5 × 33.8 oz. = 84.5 oz. actual usage

75 × 1.5 oz. = 112.5 ounces expected usage112.5 − 84.5 =

28 Ounces or 8/10 Liter Usage Variance14.50 × .80 =

$11.50 Cost Variance (approximately)Note: Actual is LESS than Expected

Consider outsourcing to inventory-taking serviceCount everythingCalculate actual cost of beverage usedCalculate actual cost of beverage soldSuggest order sizeCalculate sales revenue you should have

collected

The answer variesIf it varies too much:

Your calculations may be wrongYou received a shipment of off-spec

productsThere is extra production wastePortion sizes are too small (or too big)Someone is ripping you off

Labor Cost ControlLabor needs fluctuate with the number of

guests to a certain point – if a line cook can produce 40 meals, adding another 10 doesn’t add the need for another cook; if the number of meals drop to 30, you will still need the cook (it’s hard to hire ¾ of a cook no matter how hard you try)

You are the direct control systemWalk around Be visibleDon’t sit in your chair (if you have a chair)