putting fis through cybersecurity drills to prepare … fis through cybersecurity drills to prepare...

TRANSCRIPT

Putting FIs Through Cybersecurity Drills

To Prepare For The Next Big One

The Federal Reserve has announced its 27-member Governance Framework Formation Team

Thirteen Australian banks agree to offer real-time payments in

time for Australia Day

During a crisis

is not the right time

to pass out business cards.

Bill Nelson, CEO of FS-ISAC

NOVEMBER 2017

2

Faster PaymentsTracker™

© 2017 PYMNTS.com all rights reserved

Table of Contents

03

06

09

What’s Inside

Feature Story

News and Trends

The biggest developments across the Faster Payments landscape, including the formation of a new Governance Framework Formation Team, real-time payments progress in new global markets and advancements in blockchain-based solu-tions.

Simulating Cybersecurity Threats To Prepare For The Next Big BreachFrom the recent Equifax breach in the U.S. to ransomware reports in Europe, the reality is that companies must be prepared to address a data breach or a cyberat-tack as it occurs. To that end, organizations like the non-profit Financial Services Information Sharing and Analysis Center (FS-ISAC) are holding training simula-tions to help companies prepare. FS-ISAC CEO Bill Nelson speaks with PYMNTS about how the exercises teach IT professionals to flex “muscle memory” in a crisis — and the lessons that can be applied in the real world.

Notable recent headlines from around the Faster Payments space.

3© 2017 PYMNTS.com all rights reserved

What’s Inside

As faster payments become more readily avail-able, various players — including international governments, banks and companies — have stepped up their efforts to make these payments more accessible and secure.

Here in the U.S., the Federal Reserve recently an-nounced the 27 members of its new Governance Framework Formation Team. The team, established by the Fed’s Faster Payments Task Force, will assist with developing a governance framework for faster payments in the U.S. It will be led by Sean Rodriguez, chair of the Faster Payments Task Force, who over-sees faster payment strategy at the Federal Reserve. Rodriguez noted the new task force will work to ex-amine and improve faster payment capabilities and deliver changes by 2020.

Meanwhile, the U.S. Department of Justice recently announced it will not challenge the real-time pay-ment system (RTP) currently in creation by The Clear-ing House (TCH). TCH members include JPMorgan Chase, Citigroup, Bank of America and Wells Fargo, among others. With the DOJ business review com-pleted, RTP can now come to fruition.

U.S. banks are not the only ones banding together to offer real-time payments. A group of Australian banks recently announced their own plans for real-time pay-ments in the country early next year. The consortium of 13 banks will collaborate on a platform valued at $766.4 million USD ($1 billion AUD) enabling Austra-lian bank customers to send money to one another in real time with identifiers such as phone numbers or email addresses. When the service goes live, it will be the first allowing Australian customers access to real-time payments.

In addition to advancements in expanding real-time payments availability in global markets, some com-panies recently rolled out faster payment solutions

based on blockchain technology. They also released new services to help FIs and other companies ad-dress fraud concerns while engaged in international

“Employing sound business practices and effective risk controls are critical to safeguarding payments. Re-gardless of payment speed, implementing and main-taining measures such as regular risk assessments, layered security and strong access controls and oper-ating procedures will go a long way in managing the risks that cyber threats can impose.

But what’s important to note is that faster payments can actually help mitigate some of those risks. For example, Same Day ACH allows for quicker recovery from errors or fraudulent transactions through faster reversals. It also allows for faster returns, and many faster payment solutions can help minimize credit risk and settlement risk.

Ultimately, the security of payments, including faster payments, starts with sound practices, controls and processes that are put in place early and re-assessed regularly.”

Janet Estep,

CEO of NACHA – The Electronic Payments Association

October was cybersecurity month. What is the most important cybersecurity learning that can

be applied to securing faster payments?

Executive Insight

4© 2017 PYMNTS.com all rights reserved

What’s Inside

commerce. The November Tracker highlights no-table developments made in these fields, including how the global faster payments landscape could change as a result.

Here’s what’s happening around the world of Faster Payments:

Based on recent developments, peer-to-peer (P2P) payments are becoming more available through mo-bile wallet services.

Apple recently launched P2P payments in its most re-cent Apple Watch software updates. With the recent iOS 11 and watchOS 4 updates, Apple Pay users can now make P2P payments through Apple’s Messen-ger service. Users can also ask Siri to send money to contacts using virtual debit and credit card infor-mation.

In addition to Apple’s expanding mobile wallet offer-ing, Google launched a new mobile wallet service of its own in India. The solution, called “Tez,” allows us-ers in the country to pay businesses and send money to contacts.

Several companies in global payments have stepped up their investments in blockchain-based solutions this month, helping businesses send money across borders faster than ever before. Technology compa-ny IBM, for one, launched a new blockchain-based solution for banks aimed at reducing both settlement time and the costs of completing business payments

for businesses and consumers. Meanwhile, payment platform provider SBI Ripple Asia recently partnered with DAYLI Intelligence to bring Ripple’s cross-border blockchain solution to South Korea. The solution will help banks and FIs facilitate cross-border payments between customers in South Korea, Japan and other markets.

As payments become faster and more companies seek to deliver money internationally, some com-panies are turning to machine learning to keep pay-ments safe. Notably, banking and payment solutions provider ACI Worldwide just launched a new fraud protection service called UP Payments Risk Manage-ment. The solution relies on adaptive machine learn-ing and analytics to help banks and their partners quickly detect and respond to fraud threats.

Helping companies flex their crisis ‘muscle memory’

Halloween season may have wrapped up for the year, but data breaches and cyberattacks still present a frightening, year-long reality for many businesses in the financial services industry. To help companies prepare to effectively respond to a cyberthreat, the non-profit Financial Services Information Sharing and Analysis Center (FS-ISAC) has been holding training sessions that simulate an ongoing attack on a company’s operations. FS-ISAC CEO Bill Nelson spoke with PYMNTS about how the exercises teach companies to tap into “muscle memory” so they are better-prepared if, or when, a crisis arises in real life.

5© 2017 PYMNTS.com all rights reserved

FIve Fast FActs

of surveyed financial professionals said real-time payment processing was critical to their organizations.

of corporate treasurers are looking to offer instant cross-border payments.

of corporate treasurers want real-time payments tracking.

81%

50%

42%

100 Members

What’s Inside

are now part of Ripple’s blockchain network, a milestone for the organization.

of U.S. consumers have not heard about The Clearing House real-time payments scheme scheduled to launch later this year.

64%

6© 2017 PYMNTS.com all rights reserved

When October rolls around each year, millions of people in the U.S. and other parts of the world turn out in droves to buy costumes, decorations, pumpkins

and candy for a fun and scary Halloween. But Octo-ber also happens to be a time when financial insti-tutions and businesses prepare for situations much scarier than ghosts and goblins in search of tricks or treats.

Since 2004, October has been observed as National Cyber Security Awareness Month by the Department of Homeland Security (DHS). To mark this annual occasion, DHS holds a campaign to raise awareness of cybersecurity issues and to help companies and financial institutions take steps against the type of threats with consequences significantly more seri-ous than perpetrating a Halloween prank.

Cybersecurity, of course, is top of mind for many businesses and individuals year round, but the events leading up to this year’s DHS campaign were more

extraordinary than usual. In September, the consum-er credit agency Equifax reported that the personal information of roughly 143 million Americans was compromised in a data breach of epic proportions. Meanwhile, the recently released PYMNTS Global Fraud Index, produced in collaboration with Signi-fyd, found that instances of global fraud increased by 5.5 percent from Q2 2016 to Q2 2017. The Index also reported that global fraud can cost merchants in eight different industries $57.8 billion each year and that account takeovers have seen a sharp spike of 45 percent in Q2 2017. The bottom line is that cyber-security threats have costly consequences and are a year-round, round-the-clock concern.

Some organizations are taking steps to make sure that the financial services industry is prepared to respond quickly and appropriately to cybersecurity threats whenever they emerge. One such organiza-tion is the Financial Services Information Sharing and Analysis Center (FS-ISAC), a non-profit group established by the financial industry to provide infor-

Feature Story

Putting FIs Through Cybersecurity Drills

To Prepare For The Next Big One

7© 2017 PYMNTS.com all rights reserved

mation on financial security for the broader industry. PYMNTS recently caught up with FS-ISAC CEO Bill Nelson, who reflected on the events that helped cre-ate the organization and spoke about the ways that FS-ISAC helps companies better prepare for the next cyberattack.

A brief history of FS-ISAC

FS-ISAC was launched by different players in the fi-nancial services industry in 1999 in response to a Presidential directive issued the previous year. As Nelson explained, the organization, which operates as a nonprofit, was formed to serve as a resource to enable the financial ser-vices industry to highlight and share information about physical and cybersecurity vulnerabilities.

Nelson joined the organiza-tion in 2006 after previously serving as the executive vice president of NACHA- The Electronic Payments Associ-ation. He told PYMNTS that during his early days at the or-ganization, he saw little infor-mation-sharing about cyber threats between mem-ber organizations taking place. However, a few years after joining the organization, Nelson said he saw an uptick in cyber threat activity in the late 2000s.

Nelson said the organization was alerted by the FBI in 2009 regarding a rise in corporate account take-overs. In an account takeover, a fraudster can take over a corporation’s financial account using phishing, spyware or malware.

“At the time, they were seeing about 80 cases a week,” Nelson said. “It was becoming an epidemic.”

Recognizing the growing threat of account takeovers, Nelson said, FS-ISAC started collaborating with law enforcement and the business and financial commu-nity to develop a strategy to help various organiza-tions secure their online banking environments.

“We hadn’t done that before,” Nelson said. “The whole industry pretty much just said, ‘Hey, don’t click on that link.’ But obviously, that was not good enough.”

To better protect themselves against account take-over attacks, FS-ISAC recommends organizations update their cyber risk assessments, stay informed about potential cybersecurity threats through infor-mation-sharing and follow FS-ISAC’s good “cyber hygiene” suggestions, including locking down an organization’s IT environment using multiple securi-ty layers and evaluating the strength of primary and secondary controls in case one is overridden.

To protect payments from cyberattacks, FS-ISAC also recommends that compa-nies keep their operations that are connected to initi-ating payment transactions at a safe distance from the rest of the company’s net-work. “Do not allow email to go to that computer or other types of web browsing, so malware can’t get on it,” Nel-son said. “It’s very simple.”

Cyberattack fire drills

Nelson explained that providing information and out-lining recommendations between members is one of the ways FS-ISAC works to help its members prepare for cyberattacks. Getting members to practice their responses by running cybersecurity drills is another.

Since 2010, FS-ISAC has also invited members to participate in the organization’s Cyberattack Against Payment Systems (CAPS) exercises. During a CAPS exercise, IT professionals take part in an immersive exercise that simulates an attack on an organiza-tion’s payment operation.

In a recent CAPS exercise, a group of IT profession-als from several different banks and FIs participat-ed in a simulation that took place at IBM Security’s Cyber Range in Cambridge, Mass., that was featured

Do not allow email to go to that computer or other types of web browsing, so malware can’t

get on it, It’s very simple.

Feature Story

8© 2017 PYMNTS.com all rights reserved

on NBC’s Today Show. During the simulation, par-ticipants reacted to different types of hacks, includ-ing leaked CEO emails, compromised financial and health records and infrastructure attacks that left some employees stuck in elevators.

The purpose of the CAPS exercises, said Nelson, is to help IT professionals be better prepared to react to a cyberattack in real time. By practicing a simulated ongoing scenario, senior IT professionals responsi-ble for keeping a company or FI’s data safe get the opportunity to think outside their own job functions and gain a better understanding of how their com-pany or institution should respond in the event of a breach.

“It’s practicing and getting the muscle memory of what happens — if this does happen — to you as a company,” Nelson said. “The exercises are key to making sure people know what to do when it hap-pens.”

The exercises can also encourage IT professionals to understand the roles of different professionals with-in their organization — who controls and manages the various aspects of an organization. These simple introductions among co-workers can go a long way if they are made before a crisis hits, Nelson added.

“During a crisis is not the right time to pass out busi-ness cards,” Nelson said wryly.

This year, Nelson said the CAPS program had 2,000 participants, which is the program’s highest single participation to date. Given these numbers, he add-ed, he’s encouraged by the engagement of the finan-cial sector to stay on top of emerging threats, keep fellow organizations in the loop and give them the groundwork necessary to prepare for and respond to the next cyber threat.

“The great thing about the private sector is that we always seem to find solutions to problems,” Nelson said.

Based on recent activity, it’s clear that online thieves and criminals have no intention of slowing down and that there is likely to be another major data breach or cyberattack in the future. But being better prepared can at least potentially make the next cyber incident slightly less daunting. And having a resource devot-ed to helping businesses and FIs stay informed and respond quickly to threats is something many play-ers in the financial sector can be thankful to have available.

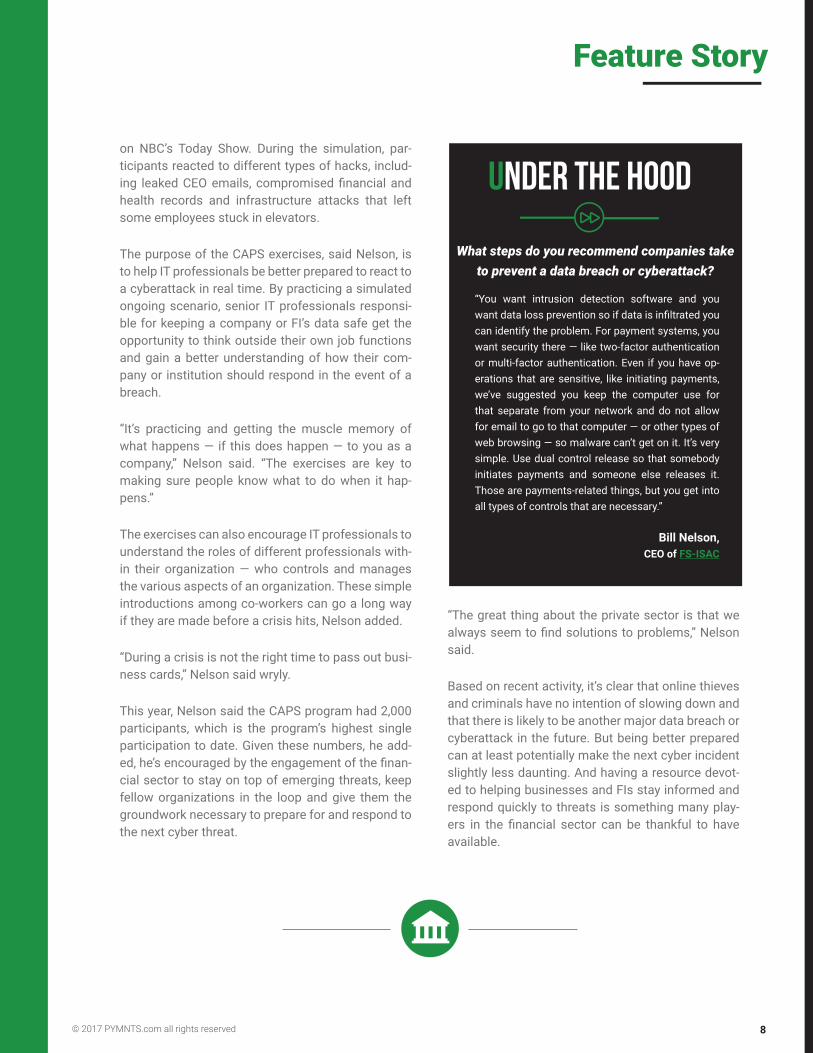

“You want intrusion detection software and you want data loss prevention so if data is infiltrated you can identify the problem. For payment systems, you want security there — like two-factor authentication or multi-factor authentication. Even if you have op-erations that are sensitive, like initiating payments, we’ve suggested you keep the computer use for that separate from your network and do not allow for email to go to that computer — or other types of web browsing — so malware can’t get on it. It’s very simple. Use dual control release so that somebody initiates payments and someone else releases it. Those are payments-related things, but you get into all types of controls that are necessary.”

Bill Nelson, CEO of FS-ISAC

What steps do you recommend companies take to prevent a data breach or cyberattack?

UNDER THE HOOD

Feature Story

9© 2017 PYMNTS.com all rights reserved

News & TrendsWhat’s Trending

Government faster payment actionsFed announces Governance Framework Forma-tion Team members

In October, the Federal Reserve’s Faster Payments Task Force announced the 27 members of is Gover-nance Framework Formation Team, a group tasked with developing and establishing a governance framework for faster payments in the U.S.. With this new team in place, the Fed is following through on one of the recommendations outlined in an earlier re-port from its Faster Payments Task Force.

The team will be chaired by Sean Rodriguez, faster payments strategy leader at the Federal Reserve and chair of the Faster Payments Task Force. In a state-ment, Rodriguez said the task force will work to de-velop and improve faster payments capabilities in the U.S. by 2020.

DOJ greenlights TCH/Bank real-time payment network

In other regulatory news, the U.S. Department of Jus-tice recently announced it will not challenge the re-al-time payment system (RTP) currently in creation by The Clearing House (TCH). TCH members include JPMorgan Chase, Citigroup, Bank of America and Wells Fargo, among others. With the DOJ business review completed, RTP can now come to fruition.

“We are pleased that the Department of Justice has concluded that our forthcoming real-time payments system will promote competition in payment ser-vices,” said Sean Oblack, a spokesman for TCH, in an email to American Banker. “Their determination is

well-timed as we prepare to launch the system later this year.”

Is Mastercard filing a blockchain patent?

Another government agency has been asked to help a financial services firm address points of friction in business-to-business (B2B) payments. A patent application from Mastercard for a payment solution which can integrate blockchain into its payment in-frastructure — and establish a “uniform settlement system” — was recently published by the U.S. Patent and Trademark Office (USPTO).

In its application, Mastercard indicated the system could include a blockchain-based ledger of transac-tions. The blockchain-based ledger will be capable of automatically monitoring all changes made to the ledger, the firm said, establishing a verifiable record of data and preventing cybercriminals from forging or altering records in the system.

Mobile wallet movesP2P payments now on Apple Watch

Apple Watch users have a new tool enabling them to quickly send and receive money with a tap on the wrist. With the recent release of its watchOS 4 and iOS 11 software updates, Apple’s Apple Pay users can now make P2P payments to contacts through Apple’s Messenger system.

Alternatively, users can also ask Siri, Apple’s virtu-al assistant, to pay a contact using a virtual debit or credit card already loaded into the users’ digital

10© 2017 PYMNTS.com all rights reserved

wallet. When users get paid, they will receive funds immediately through the new Apple Pay Cash card which will live in the Apple Wallet.

The company has been making a concerted effort to encourage Apple Pay adoption. Some of its moves can be seen in China, where mobile wallet adop-tion has been stronger than in the U.S. market. In fact, in September, Chinese rideshare service Didi announced it would offer Apple Pay as a payment option in its Didi Premier, Didi Express and Didi Luxe personal mobility services.

Google launches new digital payment tool ‘Tez’

In India, Google has rolled out its own mobile wal-let service that uses a different method to share data. The service, known as “Tez,” will allow users in the country to pay local businesses and send money to friends and family using the country’s gov-ernment-backed Unified Payments Interface (UPI) service, currently being used by 55 local banks. Tez, which is Hindi for “fast,” works through an app on both iOS and Android devices. The service also has an audio QR function allowing users to transfer money by transmitting data embedded in ultrasonic frequencies instead of exchanging bank account or phone numbers.

Tez will be competing with other mobile wallets al-ready launched in India, including WhatsApp, Uber and Truecaller. The news comes almost a year after the Indian government announced plans to demone-tize and remove larger bank notes from circulation.

First Tech Credit Union signs onto Zelle

A federal credit union recently announced it is offer-ing a new payment service for its members. The FI, First Tech Federal Credit Union, has enabled Zelle through its mobile app, making First Tech one of the first credit unions to offer the P2P service. Zelle al-lows the FI’s members to send funds to one another in a matter of minutes.

According to a news release, First Tech has more than 110,000 members working in the tech sector of Silicon Valley. “We are a credit union serving em-ployees in the tech sector, so, naturally, our members have high expectations when it comes to their mobile banking experiences,” said Greg Mitchell, First Tech Federal Credit Union’s CEO, in a statement. The news follows a report by Zelle in early September that more than 50,000 consumers were enrolling in the service daily. Zelle also reported more than 100 million re-al-time P2P payments, valued at $33.6 billion, were made in the first half of 2017.

News & Trends

11© 2017 PYMNTS.com all rights reserved

News & Trends

First Tech has a history of early investment in emerg-ing payment tech. The credit union began offering its members mobile banking services in 2000 and be-came one of the first to offer its mobile app on the three major smartphone platforms (iOS, Android and Windows).

Real-time paymentsPayment Data Systems offers Same Day ACH debits

In other P2P news, integrated electronic payment solutions provider Payment Data Systems an-nounced it now offers businesses and consumers Same Day ACH debits. With the service in place, the company will enable business and consumer clients to send and receive payments on the same banking day using the ACH Network.

The availability of Same Day ACH debits enables businesses and billers to offer customers the option to pay bills on the same day a payment is authorized, thus avoiding potential late fees or other types of fi-nancial penalties. Businesses can also use the ser-vice to make same-day payroll payments to employ-ees, and process payments faster for internet-based and point-of-sale (POS) payment transactions and invoice payments.

ACI rolls out UP for financial institutions

A new solution from ACI Worldwide could offer banks greater flexibility in routing real-time payments. The electronic banking and payment platform solutions provider recently launched UP Real-Time Payments Solution, a solution enabling FIs to manage their Real Time Gross Settlement (RTGS), SWIFT messaging and real-time payment needs through a single of-fering. The solution combines ACI’s Money Transfer system with UP Immediate Payments to offer users connectivity to immediate payment schemes and global RTGS services.

A news release noted banks can use the service to decide how to route real-time payments, removing the complexity FIs sometimes face in operating sep-

arate systems for low and high-value payment op-tions. The release also explained banks can optimize their transaction costs and orchestrate payment type, channel, currency or network into a single or multi-bank setup.

In addition, ACI launched a new fraud protection ser-vice, dubbed UP Payments Risk Management solu-tion, that uses adaptive machine learning and analyt-ics to tap into shared intelligence. This helps banks, intermediaries and telecom companies quickly react to emerging fraud threats.

FIS, Citi partner on corporate real-time payments

Other new developments could offer corporate trea-suries greater cash flow capabilities. In one such de-velopment, financial services technology company FIS recently announced a partnership with Citi Trea-sury and Trade Solutions to offer real-time payments and cash management solutions for corporate trea-sury customers. Under the agreement, FIS will con-nect its Trax corporate payments service to the Citi Treasury and Trade Solutions using CitiConnect ap-plication programming interfaces (APIs).

The integration, according to a news release, will offer FIS access to Citi’s treasury management services, including payment initiation, transaction status and balance inquiry capabilities. The release noted the collaboration will help corporate customers better prepare for the demands required by open banking and cross-border payments, and also improve cash management by offering greater financial visibility.

Australian banks plan to offer real-time pay-ments for Australia Day

South of the equator, a recent partnership means some Australian bank customers will get their first taste of real-time payments early next year. A group of 13 banks in the country have formed a collabo-ration to enable customers to make real-time pay-ments beginning on Jan. 26, the Australia Day na-tional holiday. The banks agreed to work together on a platform worth $766.4 million USD ($1 billion AUD) to be run by a new company called New Payments Platform Australia (NPP Australia). The service will

12© 2017 PYMNTS.com all rights reserved

enable customers to set their own personal identi-fiers for individual Australian banks, such as email addresses or phone numbers, instead of more com-plicated alternatives such as bank codes or account numbers.

Payment network newsIcon achieves compliance of EBA Clearing’s RT1 platform

Financial service consulting firm Icon Solutions re-cently announced it had successfully completed EBA Clearing’s testing procedures for SCT Inst payments. The successful completion of the tests means Icon is compliant with the requirements of the RT1 in-frastructure solution of EBA Clearing and the EPC Scheme Rulebook and, in turn, that Icon’s instant payment framework (IPF) is ready to connect with RT1 system participants. The RT1 instant payment system goes live this month.

Icon previously completed connectivity testing be-tween IPF and another connectivity option called SIAnet, offering users access to EBA Clearing’s SCT Inst platform. In a statement, Icon Solutions head of payments Tom Hay said that with IPF compliance with the RT1 platform, the framework will give “banks a plug-and-play option to connect to EBA Clearing’s

pan-European Instant Payments infrastructure.”

SWIFTNet Instant offers RT1 System access

RT1 users will also be able to access the EBA Clear-ing pan-European Instant Payments infrastructure using financial messaging service SWIFT starting next year. SWIFT recently announced that RT1 users will be able to access the platform using SWIFTNet Instant as of November 2018. Using SWIFT, RT1 cus-tomers will be able to access features such as mes-saging, file transfers and a browse solution.

Instant payments by SWIFT will work from anywhere in the world to enable customers to access multi-ple instant payment clearing and settlement mech-anisms. A SWIFT news release noted the company has already agreed to offer connectivity to EBA Clear-ing’s RT1 system for the Single Euro Payments Area (SEPA) as well as the Eurosystem’s Target Instant Payment Settlement (TIPS) platform.

Global payment newsIBM launches new blockchain solution for global payments

To help FIs more efficiently make cross-border pay-ments, technology provider IBM announced a new

News & Trends

13© 2017 PYMNTS.com all rights reserved

blockchain banking solution that reduces settlement time and cuts the costs of completing global pay-ments for businesses and consumers. The new solu-tion is powered by IBM Blockchain — in partnership with Stellar.org and KlickEx Group — and will help FIs clear and settle payment transactions over a single network in near real time.

A news release noted the solution is already process-ing live transactions in 12 currency corridors in the Pacific Islands, Australia, New Zealand and the U.K. The same release noted international payments can occur in multiple currencies and require multiple in-termediaries, which could prolong the completion of the transaction over several days or weeks.

The World Bank noted initiatives to modernize pay-ments and provide expanded financial access could improve the flow of currency and commerce, helping to achieve the goal of extending financial services to 1 billion people worldwide by 2020.

Ripple comes to South Korea

Blockchain-based solution SBI Ripple Asia recently signed a partnership with DAYLI Intelligence, a divi-sion of DAYLI Financial Group, to offer Ripple’s block-chain solution for cross-border payments in South Korea. According to a news release announcing the partnership, DAYLI Intelligence will offer blockchain solutions and artificial intelligence (AI)-based tech-nology infrastructure, enabling FIs to work with SBI Ripple Asia to facilitate cross-border payments be-tween customers in Japan, South Korea and other global markets.

“South Korea is one of the most active markets worldwide when it comes to blockchain innovation and trading of digital assets,” said Takashi Okita, SBI Ripple Asia CEO, in a statement. “With trade flows into and out of the country totaling $960 billion every year, we also see a high and growing demand for Rip-ple’s frictionless payments solution in the country.”

Starling announces plans for business banking solution

A U.K. challenger bank is also preparing to enable customers to send funds globally, as recent reports indicate that Starling Bank intends to launch a busi-ness banking service early next year. The news fol-lows Starling’s move to offer an app-only current (checking) account service for customers.

Starling Bank founder and CEO Anne Boden said cor-porate banking and business lending has been “high-ly concentrated with a few big players for too long.” In a recent interview, Boden offered few details of what the B2B service would offer, but said it would take users five minutes or less to get started. Reports indicate the Starling corporate account solution will offer a free business account with linked invoicing and accounting solutions, and will support real-time international payments.

News & Trends

14© 2017 PYMNTS.com all rights reserved

Disclaimer

The Faster Payments Tracker™ may be updated periodically. While reasonable efforts are made to keep the content accurate and up-to-date, PYMNTS.COM: MAKES NO REPRESENTATIONS OR WARRANTIES OF ANY KIND, EXPRESS OR IMPLIED, REGARDING THE CORRECTNESS, ACCURACY, COMPLETENESS, ADEQUACY, OR RELIABILITY OF OR THE USE OF OR RESULTS THAT MAY BE GENERATED FROM THE USE OF THE INFORMATION OR THAT THE CONTENT WILL SATISFY YOUR REQUIREMENTS OR EXPECTATIONS. THE CONTENT IS PROVIDED “AS IS” AND ON AN “AS AVAILABLE” BASIS. YOU EXPRESSLY AGREE THAT YOUR USE OF THE CONTENT IS AT YOUR SOLE RISK. PYMNTS.COM SHALL HAVE NO LIABILITY FOR ANY INTERRUPTIONS IN THE CONTENT THAT IS PROVIDED AND DISCLAIMS ALL WARRANTIES WITH REGARD TO THE CONTENT, INCLUDING THE IMPLIED WARRANTIES OF MERCHANTABILITY AND FITNESS FOR A PARTICULAR PURPOSE, AND NON-INFRINGEMENT AND TITLE. SOME JURISDICTIONS DO NOT ALLOW THE EXCLUSION OF CERTAIN WARRANTIES, AND, IN SUCH CASES, THE STATED EXCLUSIONS DO NOT APPLY. PYMNTS.COM RESERVES THE RIGHT AND SHOULD NOT BE LIABLE SHOULD IT EXERCISE ITS RIGHT TO MODIFY, INTERRUPT, OR DISCONTINUE THE AVAILABILITY OF THE CONTENT OR ANY COMPONENT OF IT WITH OR WITHOUT NOTICE.

PYMNTS.COM SHALL NOT BE LIABLE FOR ANY DAMAGES WHATSOEVER, AND, IN PARTICULAR, SHALL NOT BE LIABLE FOR ANY SPECIAL, INDIRECT, CONSEQUENTIAL, OR INCIDENTAL DAMAGES, OR DAMAGES FOR LOST PROFITS, LOSS OF REVENUE, OR LOSS OF USE, ARISING OUT OF OR RELATED TO THE CONTENT, WHETHER SUCH DAMAGES ARISE IN CONTRACT, NEGLIGENCE, TORT, UNDER STATUTE, IN EQUITY, AT LAW, OR OTHERWISE, EVEN IF PYMNTS.COM HAS BEEN ADVISED OF THE POSSIBILITY OF SUCH DAMAGES.

SOME JURISDICTIONS DO NOT ALLOW FOR THE LIMITATION OR EXCLUSION OF LIABILITY FOR INCIDENTAL OR CONSEQUENTIAL DAMAGES, AND IN SUCH CASES SOME OF THE ABOVE LIMITATIONS DO NOT APPLY. THE ABOVE DISCLAIMERS AND LIMITATIONS ARE PROVIDED BY PYMNTS.COM AND ITS PARENTS, AFFILIATED AND RELATED COMPANIES, CONTRACTORS, AND SPONSORS, AND EACH OF ITS RESPECTIVE DIRECTORS, OFFICERS, MEMBERS, EMPLOYEES, AGENTS, CONTENT COMPONENT PROVIDERS, LICENSORS, AND ADVISERS.

Components of the content original to and the compilation produced by PYMNTS.COM is the property of PYMNTS.COM and cannot be reproduced without its prior written permission.

You agree to indemnify and hold harmless, PYMNTS.COM, its parents, affiliated and related companies, contractors and sponsors, and each of its respective directors, officers, members, employees, agents, content component providers, licensors, and advisers, from and against any and all claims, actions, demands, liabilities, costs, and expenses, including, without limitation, reasonable attorneys’ fees, resulting from your breach of any provision of this Agreement, your access to or use of the content provided to you, the PYMNTS.COM services, or any third party’s rights, including, but not limited to, copyright, patent, other proprietary rights, and defamation law. You agree to cooperate fully with PYMNTS.COM in developing and asserting any available defenses in connection with a claim subject to indemnification by you under this Agreement.

Disclaimer