pwc private equity/venture capital 2014 ... · capital 2014 review and 2015 outlook 5 february 2015...

TRANSCRIPT

www.pwchk.com

PwC Private Equity/Venture Capital 2014 Review and 2015 Outlook

5 February 2015

PwC

Table of contents

Fundraising 3

Investments 8

Exits 17

Key messages 24

2015 outlook & eight mega-trends 27

PwC

Fundraising

3

PwC

Fundraising by PEs remained healthy, with the strongest US$ fundraise since 2008 and a slight uptick in renminbi fundraising.

4

Source: AVCJ and PwC analysis

PE/VC fund raising for China investment* * Excludes PEs investing in China from non-region specific funds

Renminbi Fund Size

Non-renminbi Fund Size

Fund Volume

4.9 6.8

20.3

30.7

20.8

13.3 15.6

50.0

9.7

15.6

17.6

21.6

19.8

28.4

172

165

249

277

123 130

96

0

10

20

30

40

50

60

0

50

100

150

200

250

300

2008 2009 2010 2011 2012 2013 2014

No. US$ billion

PwC

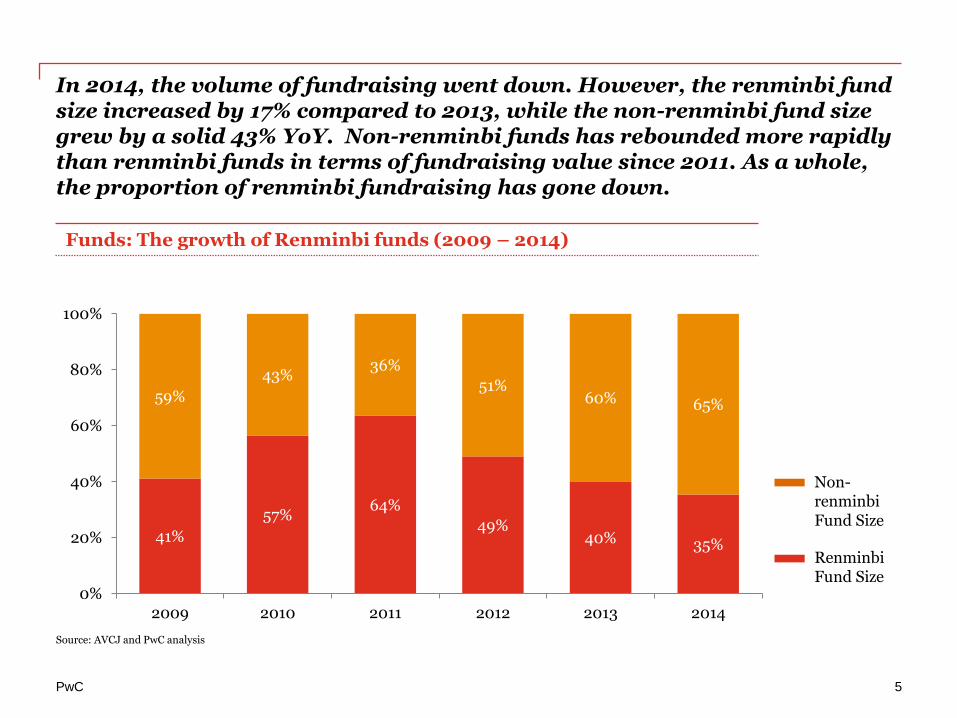

In 2014, the volume of fundraising went down. However, the renminbi fund size increased by 17% compared to 2013, while the non-renminbi fund size grew by a solid 43% YoY. Non-renminbi funds has rebounded more rapidly than renminbi funds in terms of fundraising value since 2011. As a whole, the proportion of renminbi fundraising has gone down.

41%

57% 64%

49% 40% 35%

59%

43% 36%

51% 60% 65%

0%

20%

40%

60%

80%

100%

2009 2010 2011 2012 2013 2014

5

Funds: The growth of Renminbi funds (2009 – 2014)

Source: AVCJ and PwC analysis

Renminbi Fund Size

Non-renminbi Fund Size

PwC

2004 - 2014, Fundraising for the China and Hong Kong markets dominate Asian PE with around US$365 billion raised (not including allocations from non-China specific funds).

365

77 62 51

37 37 25

0

50

100

150

200

250

300

350

400

China/HK Japan India S Korea Singapore Australia Others

US$ billion

6

Source: AVCJ

Total funds raised by fund country, with geographic preference in Asia (2004 - 2014)

PwC

2014, funds raised in China accounted for 9% of the fund raised globally, three percentage points up compared to 2013, almost back to 2012 levels.

318 294

341

390

532

486

17 36 48 42 33 44

0

100

200

300

400

500

600

2009 2010 2011 2012 2013 2014

US$ billion

World

China

7

Funds: PE/VC funds raised in China vs ROW (2009 – 2014)

Source: AVCJ, Preqin and PwC analysis

PwC

Investments

8

PwC

2014 was a banner year for new investments by PEs with record volumes (up 51%) and values (up 101%); participation in SOE reforms and - for the first time at scale - outbound deals involving Chinese GPs and financial buyers underpinned this performance.

9

Private equity deals (2008 – 2014)

Source: ThomsonReuters, ChinaVenture and PwC analysis

369

264

434

529

358 392

593

22.0 22.8

27.0

41.0

34.3 36.4

73.2

0

10

20

30

40

50

60

70

80

0

50

100

150

200

250

300

350

400

450

500

550

2008 2009 2010 2011 2012 2013 2014

No. US$ billion

Announced Deal Value

Announced Deal Volume

PwC

… In 2014, the total VC deal volume shot up by 81% compared to a year ago, reaching a record high since 2008.

10

Venture Capital deals by volume (2008 – 2014)

Source: Thomson Reuters, China Venture, AVCJ, and PwC analysis

694 712

1011 903

473

738

1334

0

200

400

600

800

1000

1200

1400

1600

2008 2009 2010 2011 2012 2013 2014

Deal Volume

PwC

China has been the single largest PE investment destination in Asia since 2008 and accounted for 41% of Asian PE deal values in 2014.

10 11 17 16 16 27 34

26 21 35 3

8

17 16

8 7

17 9 9

14

8

2 3

8

18

11 5

9 9 7 9

10 17

8

5

8

9 6

6

3

2

6

4

8

4 4 8 9

11

3

8

16

23

12 11

8 11 7 7

8

0

20

40

60

80

100

120

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

US$ billion

Others

South Korea

Japan

India

Australia

Hong Kong

Mainland China

11

Source: AVCJ

Deals: Deal values by Asian country (2004 – 2014)

PwC

Although, globally, China has a much smaller share. China deal value increased by 103% in 2014 compared to 2013. Meanwhile, globally, there was only a 10% increase in deal value.

113

236

267 267

302

332

23 27 41 34 36

73

0

50

100

150

200

250

300

350

2009 2010 2011 2012 2013 2014

US $ billion

World

China

12

Source: AVCJ, Preqin and PwC analysis

Deals: Deal values China vs ROW (2009 – 2014)

PwC

PE deals in technology and consumer-related sectors accounted for more than half the total reflecting investment plans intended to align with the strategic direction of the wider economy …

23 34 55 36 49

224

54 98

126 74 73

102

50

89

99

46 85

85

20

47

30

46 33

35

20 24

22 19 49 62

0

100

200

300

400

500

600

700

2009 2010 2011 2012 2013 2014

Others

Retail

Materials

Energy and Power

Real Estate

Media and Entertainment

Financial Services

Healthcare

Industrials

Consumer related

High Technology

No.

13

Source: Thomson Reuters, ChinaVenture and PwC analysis

PE deal volume by industry sector

PwC

… and a similar trend was seen in deal values: in total there were 15 PE deals valued at more than US$1bn in 2014, another record.

14

Source: Thomson Reuters, ChinaVenture and PwC analysis

PE deal value by industry sector

0.3 0.8 0.6 0.9 0.5 0.0

15.7

1.0 0.5 1.2 1.5 3.3 6.3

13.6

3.2 3.1 7.9 9.4 3.5

4.3

10.4

3.0

1.2 2.0

3.9

9.8

7.1 6.3

3.0

4.4

9.6

0.4 11.5

3.0

7.8

12.3 2.6

4.0

2.4 1.0 1.1

3.5 0.9

1.7

2.6

0

10

20

30

40

50

60

70

80

2008 2009 2010 2011 2012 2013 2014

US$ billion

Others

Energy and Power

Healthcare

Telecommunications

Raw Materials

Media and Entertainment

Financial Services

Industrials

Real Estate

Consumer related

High Technology

Retail

PwC

Outbound investment by local PEs almost doubled in volume terms …

15

Source: Thomson Reuters, ChinaVenture and PwC analysis

No.

China mainland PE backed outbound deal volume by PE category

4 10 9

27 26 25

49

0

10

20

30

40

50

60

2008 2009 2010 2011 2012 2013 2014

PwC

… and outbound deal values also reached a record high; PEs typically look for overseas businesses which have a strong China-angle in their growth strategies.

16

Source: Thomson Reuters, ChinaVenture and PwC analysis

China mainland PE backed outbound deal value by PE category

1.7

3.7

1.4

8.2

10.3

1.1

14.3

0

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

2008 2009 2010 2011 2012 2013 2014

US$ billion

PwC

Exits

17

PwC

The second half of 2014 saw a performance equal to the first half. However, if we see it as a whole, the cross-board IPOs backed by PE funds made a strong comeback in 2014. Noticeably, overseas IPOs took the majority of the proportion.

64

34

6

29

59 55

52

62

80

56

55 56

4

4

4 7

3 4

0

20

40

60

80

100

120

140

1H2012 2H2012 1H2013 2H2013 1H2014 2H2014

18

No.

Source: AVCJ and PwC analysis

PE/VC backed deal exit volume by type (2012 – 2014 half yearly)

M&A - trade

IPO

M&A - PE

PwC

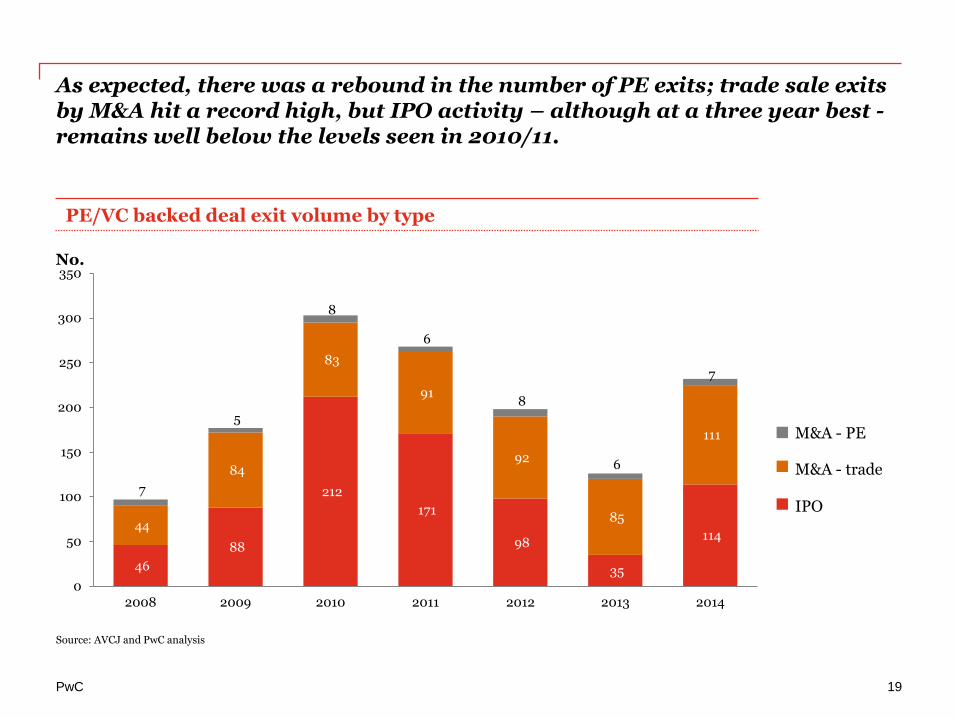

As expected, there was a rebound in the number of PE exits; trade sale exits by M&A hit a record high, but IPO activity – although at a three year best - remains well below the levels seen in 2010/11.

19

No.

Source: AVCJ and PwC analysis

PE/VC backed deal exit volume by type

M&A - trade

IPO

M&A - PE

46

88

212

171

98

35

114 44

84

83

91

92

85

111

7

5

8

6

8

6

7

0

50

100

150

200

250

300

350

2008 2009 2010 2011 2012 2013 2014

PwC

The resurgence of Chinese IPOs was due to the CSRC lifting the listing freeze. However, the world’s biggest IPO, a Chinese company, listed on NYSE rather than one of the Chinese exchanges.

20 25

12 8 9 18

14

7

2

3 5

18

14

6

4

25

0

10

20

30

40

50

60

70

2009 2010 2011 2012 2013 2014

US$ billion Including this Chinese company’s US$21.8 bn IPO exit in NYSE

20 20

Exits: China PE/VC backed IPO exits — amounts raised by bourse (2009 – 2014)

Source: AVCJ

NYSE/NASDAQ

Shenzhen

Other

Shanghai A

Hong Kong

PwC

A-share listings, although rebounding, nevertheless remain somewhat challenging and overseas listings in Hong Kong and New York are important exit routes.

21

Exits: China PE/VC backed IPO exits — number of exits by bourse (2009 – 2014)

Source: AVCJ

NYSE/NASDAQ

Shenzhen

Other

Shanghai A

Hong Kong 21

48

118 106

70

-

45 12

27

39

26

11

29

38

2

-

11

18

11

-

17

4

7

30

11

2

6

13

0

50

100

150

200

250

2008 2009 2010 2011 2012 2013 2014

PwC

In 2014 China bounced back to join level with the US in terms of volume of PE /VC backed IPOs after a fall in 2013.

13

66 50 49

81

115

88

214

172

98

35

114

0

50

100

150

200

250

2009 2010 2011 2012 2013 2014

No.

US

China

22

Exits: PE/VC backed IPO exits China vs US (2009 – 2014)

Source: AVCJ ,Thomson Reuters and NVCA

PwC

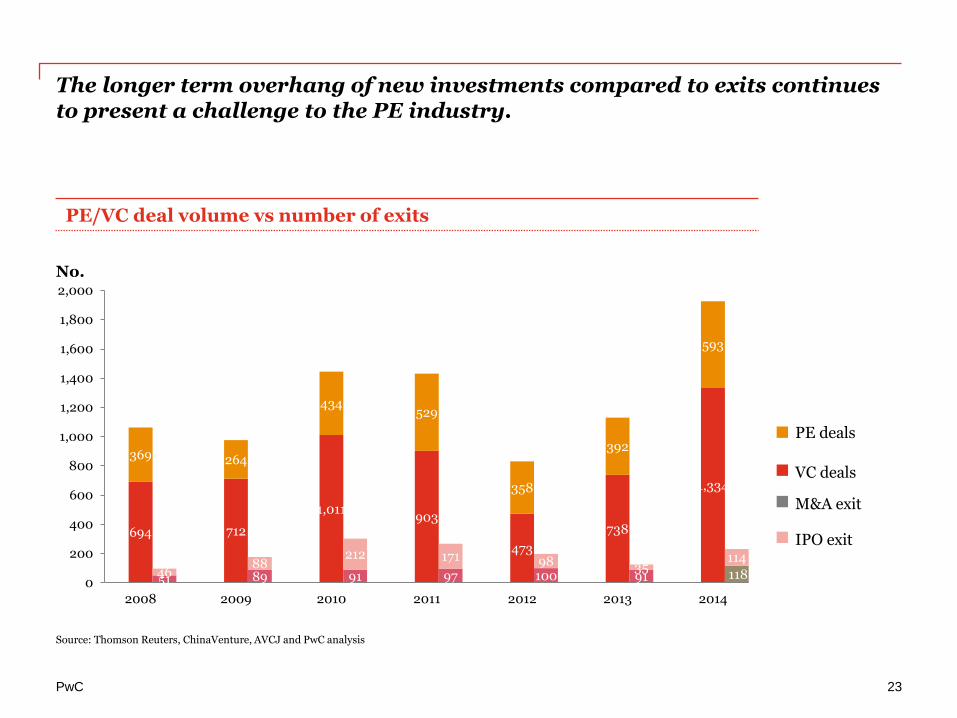

The longer term overhang of new investments compared to exits continues to present a challenge to the PE industry.

23

Source: Thomson Reuters, ChinaVenture, AVCJ and PwC analysis

No.

PE/VC deal volume vs number of exits

VC deals

PE deals

M&A exit

IPO exit 694 712

1,011 903

473

738

1,334

369 264

434 529

358

392

593

51 89 91 97 100 91 118 46 88

212 171 98 35 114

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2008 2009 2010 2011 2012 2013 2014

PwC

Key messages

24

PwC

Key messages

25

Fundraising

• Fundraising by PEs remained healthy, with the strongest US$ fundraise since 2008 and a slight uptick in renminbi fundraising.

• 2004 - 2014, Fundraising for the China and Hong Kong markets dominate Asian PE with around US$365 billion raised (not including allocations from non-China specific funds).

Investments

• 2014 was a banner year for new investments by PEs with record volumes (up 51%) and values (up 101%); participation in SOE reforms and - for the first time at scale - outbound deals involving Chinese GPs underpinned this performance.

• In 2014, the total VC deal volume shot up by 81% compared to a year ago, reaching a record high since 2008.

• Although, globally, China has a much smaller share. China deal value increased by 103% in 2014 compared to 2013. Meanwhile, globally, there was only a 10% increase in deal value.

• PE deals in technology and consumer-related sectors accounted for more than half the total reflecting investment plans intended to align with the strategic direction of the wider economy; a similar trend was seen in deal values: in total there were 15 PE deals valued at more than US$1bn in 2014, another record.

PwC

Key messages

26

Exits

• As expected, there was a rebound in the number of PE exits; trade sale exits by M&A hit a record high, but IPO activity – although at a three year best - remains well below the levels seen in 2010/11.

• In 2014 China bounced back to join level with the US in terms of volume of PE or VC backed IPOs after a fall in 2013.

• The longer term overhang of new investments compared to exits continues to present a challenge to the PE industry.

PwC

2015 outlook & eight mega-trends

27

PwC

The scale of PE activity in China will remain robust in 2015. There are exceptionally strong tailwinds for the PE industry in China over the medium term (1 of 2)

The eight mega-trends

• Demand for capital in China’s private sector: PE has emerged as a key provider of capital to the liquidity starved private sector in China with real policy support as well as new regulations. The state-owned sector may also start to come into play as part of the ongoing SOE reforms.

• Consolidation: But there will be winners and losers in the sector - high quality, professional PEs will thrive.

• Flight to quality: Within China, the days where PEs could throw money at deals and expect a “rising tide to float all boats” have gone; careful and professional diligence is vitally important.

• Outbound, and emergence of China’s home grown global PEs: Yuan denominated PE fund raising is here to stay and the big players in China will emerge to compete with their global peers; we are already seeing a step-up in outbound M&A involving some of the pre-eminent Chinese PEs and the outbound trend is happening much faster than many people predicted or even realise

28

PwC

The scale of PE activity in China will remain robust in 2015. There are exceptionally strong tailwinds for the PE industry in China over the medium term (2 of 2)

• The buy-out trend: there are an increasing number of buy-out opportunities and more PEs are looking to do control transactions.

• Quantum leap in exit activity: The industry as a whole is moving into an “exit phase”; the backlog of exits represents a real challenge for the sector; it is more than IPO markets can absorb, and trade and secondary sales by M&A will become more frequent.

• Importance of A-shares: The A-share market has been and will continue to be an important exit route for PE.

• The “wall of money”: Unlike in developed markets, Yuan denominated PE fundraising has hitherto been dominated by retail investors; this is changing as institutions in China including securities and insurance companies are granted permission to invest in PE; the resulting theoretical “wall of money” which could become available for PE investment over the medium term is measured in hundreds of billions of renminbi.

29

Thank you

© 2015 PricewaterhouseCoopers. All rights reserved. "PricewaterhouseCoopers" refers to the Hong Kong firm of PricewaterhouseCoopers or, as the context requires, the network of member firms of PricewaterhouseCoopers International Limited, each of which is a separate and independent legal entity.