q2 financial presentation 2012 dof asadof.no/files/pdf/dof...

TRANSCRIPT

Q2 Financial Presentation 2012

DOF ASA

DOF ASA - Q2 Presentation 2012

Agenda

Summary

Recent highlights

Overview group

Financials

DOF Subsea update

Outlook

DOF ASA – Q2 Presentation 2012

Several new contracts/renewals in DOF Subsea and in DOF Supply. A strong subsea market is expected to continue. The DOF group is limited exposed to a weak spot market in the

North Sea. Several new contracts renewal under discussion. Remaining newbuilding program close to fully financed.

“All time high” Ebitda of NOK 742 million (NOK 495 million) and

NOK 945 million including gain from sale of assets. Pre tax profit of NOK 333 million adjusted for unrealized currency

gain, and derivatives.

Summary

3

DOF ASA – Q2 Presentation 2012

Recent highlights Vessels

DOF Several vessels started on new contracts:

Skandi Falcon on-hire to MacDow in Australia in April Skandi Atlantic on-hire to Apache in Australia in May Skandi Hawk on-hire to DOF Subsea Asia in May Skandi Foula and Skandi Rona onhire on new contracts with Shell in April

DOF Subsea Sold and delivered the new-build Skandi Bergen to new owner in May Signed a high-end OSCV newbuild contract with delivery May 2013

4

DOF ASA – Q2 Presentation 2012

Contracts New contract on Skandi Skansen with Subsea 7 Subsea 7 exercised option – firm period until July 2013 New contract on Skandi Carla with Fugro, firm until summer 2017 New contract on Skandi Caledonia with MOG, firm until Oct 2015 Subsea 7 exercised 1 year option on Skandi Seven New contract on Skandi Atlantic with Apache Energy Limited, Australia,

900 days from May 12 New 3+ 3 yrs contract on Skandi Constructor with Helix Well Ops 1 yr extension on Skandi Salvador with Chevron Brazil 2 yrs extension on Skandi Chieftain with Petrobras Various project contracts in DOF Subsea

Recent highlights

5

DOF ASA – Q2 Presentation 2012

DOF ASA

Norskan Ltda Modern fleet 17 AHTS’s 6 PSV’s 2 CSV’s

DOF Subsea Holding Ship owning company Modern fleet 3 AHTS’s 17 PSV’s 4 CSV

DOF Subsea Modern fleet & Equipment 22 CSV/ROV vessels 52 ROV’s Leading Subsea Contractor

DOF Installer 3 state of the art installation CSV vessels

Company overview

6

DOF ASA – Q2 Presentation 2012

PSV AHTS ROV/OCSV/DSV/ Total fleetNo. of vessels SEISMIC VESSELSDOF ASA 17 3 4 24

NORSKAN OFFSHORE 6 12 2 20

DOF SUBSEA AS 0 0 22 22

DOF INSTALLER ASA 0 0 3 3

AKER DOF DEEPWATER AS 0 5 0 5

Total fleet 23 20 31 74

Contract coverage 12* 97 % 83 % 89 % 93 %Contract coverage 13* 74 % 67 % 73 % 73 %

The fleet market segment

7

*Not including options

DOF ASA – Q2 Presentation 2012

Angola

GEOGRAPHICAL FOCUS AREAS

Perth Rio de Janeiro

Buenos Aires

Singapore

Houston St. Johns

Aberdeen

Austevoll

Cairo

Brunei

Macae

Jakarta

Manila

Moscow Bergen

32

0

25

8

1

GEOGRAPHICAL FOCUS AREAS

Melbourne

Darwin

Global player

8

DOF ASA – Q2 Presentation 2012 9

DOF group has solid cash flow visibility over the next 3-5 years

By 30 June 2012 the total back-log (incl. options) was approx NOK 38.8 bn Firm contract counts for NOK 18,6 bn Options count for NOK 20,1 bn

Note: Includes extension options on long-term contracts.

Backlog development DOF Group

38 789

35 237

29 783

25 004

20 916

17 388

14 365 11 815

7 838 6 873

-

5 000

10 000

15 000

20 000

25 000

30 000

35 000

40 000

45 000

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Backlog DOF Group

DOF ASA – Q2 Presentation 2012

Update on remaining newbuilding program

Vessel Yard Delivery Type Contract Financing

Skandi Iguazu

STX Brazil Aug 12 AHTS, 325 t BP 8 yrs Petrobras Funding Secured from FMM / BNDES

Skandi Nova STX Norway Sept 12 MRV 05 7 yrs ConocoPhillips N Funding secured from Eksportkreditt, DNB & ABN Ambro

Skandi Marøy STX Norway Oct 12 MRV 05 7 yrs ConocoPhillips N Funding secured from Eksportkreditt, DNB & ABN Amro

Skandi Hugen STX Norway Nov 12 MRV 05 ROV 7 yrs ConocoPhillips N Funding secured from Eksportkreditt, GIEK and SPV

Skandi Urca STX Brazil May 13 AHTS 8 yrs Petrobras Funding secured BNDES. In progress to secure 20% GIEK secured funding

Skandi Bergen (DOF Subsea)

STX Norway May 13 CSV Uncommitted In progress with various banks for funding (CIRR secured)

Skandi Angra STX Brazil Aug 13 AHTS 8 yrs Petrobras Funding secured BNDES. In progress to secure 20% GIEK secured funding

Skandi Paraty STX Brazil Feb 14 AHTS Uncommitted Funding secured BNDES. In progress to secure 20% GIEK secured funding

10

DOF ASA - Q2 Presentation 2012

Financials

DOF ASA – Q2 Presentation 2012

Average utilization Subsea fleet (95 %) Good utilization of the project fleet Geoholm partly off-hire due to transit and yard stay before a contract Skandi Singapore partly off-hire due to yard stay in June High activity from Survey and positioning

Average utilization Supply fleet (DOF 98 %, Norskan 91 %) Good performance from the vessels in the North Sea Two vessels has operated in the spot market, good utilization in April/May and

variable in June Higher utilization for the Brazilian CSV fleet compared to previous quarters Three vessels started on new contracts in Q2

Capex & sales in 2nd quarter The new-build, Skandi Bergen, was delivered from the yard in May and sold to a

new owner. The gain from the sale was NOK 203 millions

Finance Refinancing of one loan in Q2 A strong USD has resulted in high unrealized currency losses in Q2

Financial/Operational highlights Q2 2012

12

DOF ASA – Q2 Presentation 2012

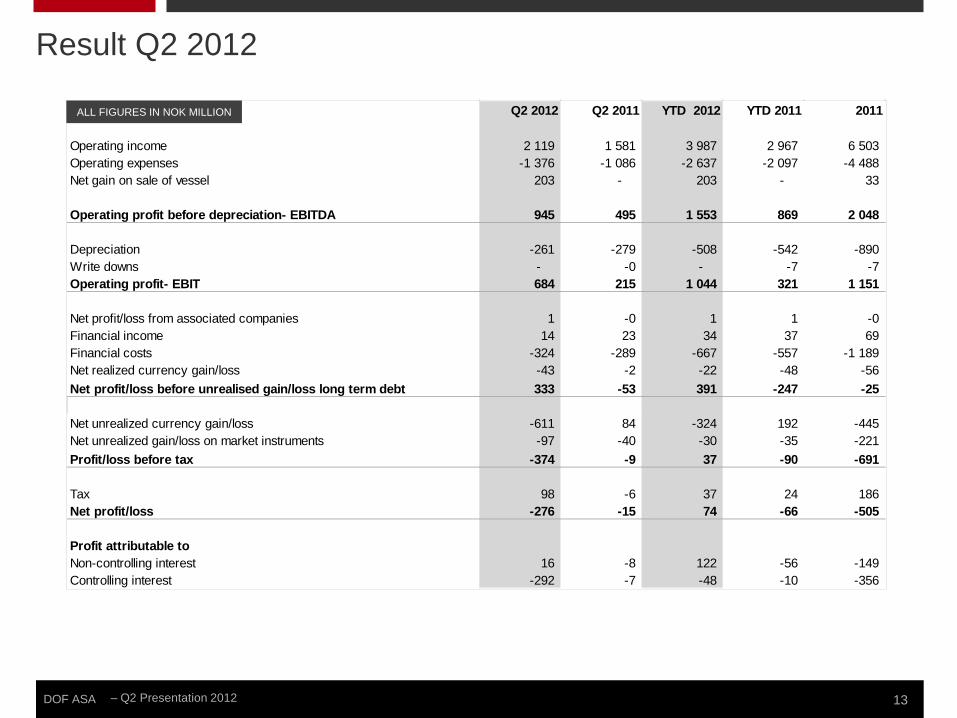

All figures in NOK million Q2 2012 Q2 2011 YTD 2012 YTD 2011 2011

Operating income 2 119 1 581 3 987 2 967 6 503 Operating expenses -1 376 -1 086 -2 637 -2 097 -4 488 Net gain on sale of vessel 203 - 203 - 33

Operating profit before depreciation- EBITDA 945 495 1 553 869 2 048

Depreciation -261 -279 -508 -542 -890 Write downs - -0 - -7 -7 Operating profit- EBIT 684 215 1 044 321 1 151

Net profit/loss from associated companies 1 -0 1 1 -0 Financial income 14 23 34 37 69 Financial costs -324 -289 -667 -557 -1 189 Net realized currency gain/loss -43 -2 -22 -48 -56 Net profit/loss before unrealised gain/loss long term debt 333 -53 391 -247 -25

Net unrealized currency gain/loss -611 84 -324 192 -445 Net unrealized gain/loss on market instruments -97 -40 -30 -35 -221 Profit/loss before tax -374 -9 37 -90 -691

Tax 98 -6 37 24 186 Net profit/loss -276 -15 74 -66 -505

Profit attributable toNon-controlling interest 16 -8 122 -56 -149 Controlling interest -292 -7 -48 -10 -356

ALL FIGURES IN NOK MILLION

Result Q2 2012

13

DOF ASA – Q2 Presentation 2012

ALL FIGURES IN NOK MILLION

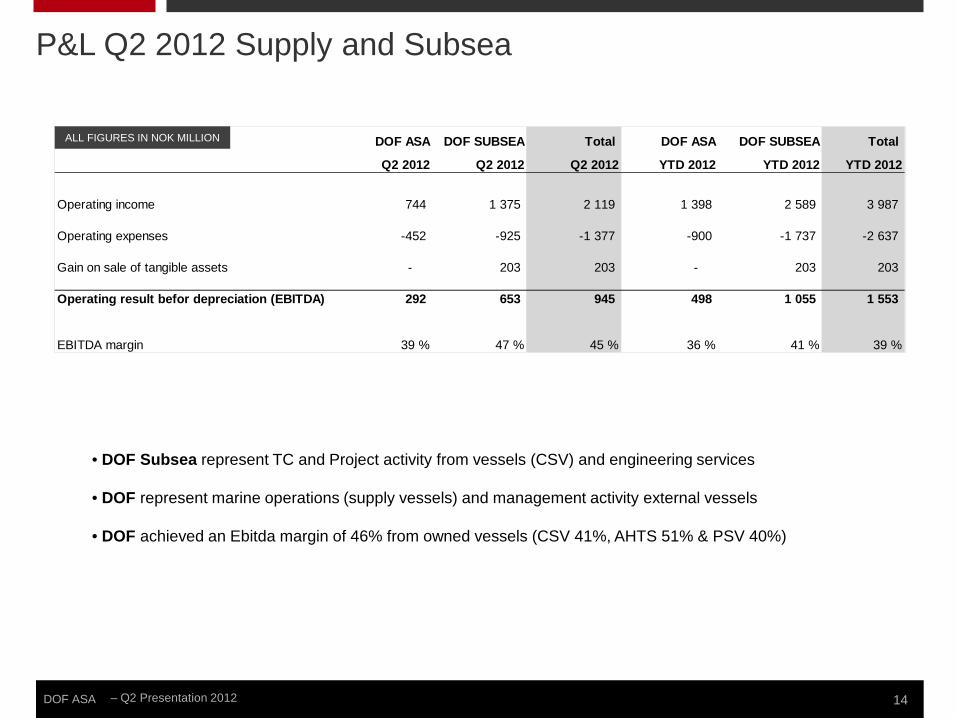

• DOF Subsea represent TC and Project activity from vessels (CSV) and engineering services

• DOF represent marine operations (supply vessels) and management activity external vessels

• DOF achieved an Ebitda margin of 46% from owned vessels (CSV 41%, AHTS 51% & PSV 40%)

14

DOF ASA DOF SUBSEA Total DOF ASA DOF SUBSEA Total

Q2 2012 Q2 2012 Q2 2012 YTD 2012 YTD 2012 YTD 2012

Operating income 744 1 375 2 119 1 398 2 589 3 987

Operating expenses -452 -925 -1 377 -900 -1 737 -2 637

Gain on sale of tangible assets - 203 203 - 203 203

Operating result befor depreciation (EBITDA) 292 653 945 498 1 055 1 553

EBITDA margin 39 % 47 % 45 % 36 % 41 % 39 %

P&L Q2 2012 Supply and Subsea

DOF ASA – Q2 Presentation 2012

ALL FIGURES IN NOK MILLION

EBITDA (MNOK)

Q2 2012 Q2 2011

PSV 92 78

AHTS 155 97

CSV 699 320

Total 945 495

•Installer vessels included in the CSV segment •Three vessels in the CSV segment are owned by DOF

Results – business segments

15

10 %

16 %

74 %

EBITDA Q2 2012

16 %

19 % 65 %

EBITDA Q2 2011

DOF ASA – Q2 Presentation 2012

ALL FIGURES IN NOK MILLION

ALL FIGURES IN NOK MILLION

Financial results Q2 2012

16

Financial items Q2 2012 Q2 2011 YTD 2012 YTD 2011 2011Share of loss profit from associated 1 -0 1 1 -0

Interest reveneue 13 23 35 37 68

Interest costs -300 -257 -625 -506 -1 078

Realized currency gain/loss long debt 0 1 26 -6 -13

Realized currency gain/loss on derivatives -21 2 -31 24 62

Realized operational currency gain/loss (-) -73 -5 -68 -66 -105

Other financial expenses -23 -73 -43 -90 -115

Total financial items -402 -310 -705 -606 -1 180

Unrealized profit/loss on currencies and derivativesUnrealized currency gain/loss -559 84 -272 192 -445

Unrealized gain/loss on derivatives -97 2 -30 4 -218

Total unrealized profit/loss on currencies and derivatives -656 86 -303 196 -663

Total financial items -1 058 -224 -1 008 -410 -1 843

DOF ASA – Q2 Presentation 2012

0 %

5 %

10 %

15 %

20 %

25 %

30 %

35 %

40 %

45 %

50 %

-

500

1 000

1 500

2 000

2 500

Q2 2009 Q3 2009 Q4 2009 Q1 2010 Q2 2010 Q3 2010 Q4 2010 Q1 2011 Q2 2011 Q3 2011 Q4 2011 Q1 2012 Q2 2012 1 083 1 012 1 181 1 129 1 506 1 237 1 574 1 386 1 581 1 674 1 862 1 868 2 119

333 267 315 338 470 433 453 375 495 561 581 607 742 31 % 26 % 27 % 30 % 31 % 35 % 29 % 27 % 31 % 34 % 31 % 32 % 35 %

17 041 17 058 17 827 19 299 20 069 20 904 22 423 23 191 23 832 24 772 26 641 27 418 26 942 4 068 3 845 3 957 3 540 3 545 4 317 4 629 4 163 3 993 4 113 4 187 4 203 4 394

21 109 20 903 21 784 22 839 23 614 25 221 27 052 27 354 27 825 28 885 30 828 31 621 31 336 6 411 6 892 6 809 6 791 6 525 6 645 6 728 6 617 6 618 6 439 6 669 6 906 6 490

11 929 11 630 11 973 12 343 11 539 13 662 16 931 17 036 17 626 18 660 20 012 20 449 20 667 2 769 2 381 3 002 3 705 5 550 4 914 3 393 3 701 3 581 3 785 4 147 4 266 4 179

21 109 20 903 21 784 22 839 23 614 25 221 27 052 27 354 27 825 28 884 30 828 31 621 31 336

Operating revenue EBITDA EBITDA margin

MN

OK

Operating revenue EBITDA EBITDA margin Non-current assets Current assets Total Assets Equity Non-current debt Current debt Total Equity and Debts

17

Historical EBITDA excl sales

DOF ASA – Q2 Presentation 2012

Amounts in NOK million 30.06.2012 30.06.2011 31.12.2011

ASSETSIntangible assets 564 482 611Vessel and other tangible assets 24 877 20 626 24 281Newbuildings 1 153 2 334 1 406Financial assets 347 390 343Non-currents assets 26 942 23 832 26 641

Receivables 2 392 2 161 2 147Cash and cash equivalents 2 002 1 831 2 040Current assets 4 393 3 992 4 187

Total assets 31 336 27 825 30 828

EQUITY AND LIABILITIESSubscribted equity 1 452 860 1 452Retained equity 2 332 3 074 2 585Non-controlling equity 2 707 2 684 2 633Equity 6 490 6 618 6 669

Provisions for commitments 522 428 489Other non-current liabilities 20 145 17 198 19 523Non-current liabilities 20 666 17 626 20 013

Debt to credit institutions 1 997 1 902 2 251Other current liabilities 2 182 1 678 1 895Current liabilities 4 179 3 580 4 146

Total equity and liabilities 31 336 27 825 30 828

ALL FIGURES IN NOK MILLION

Balance Q2 2012

18

DOF ASA – Q2 Presentation 2012

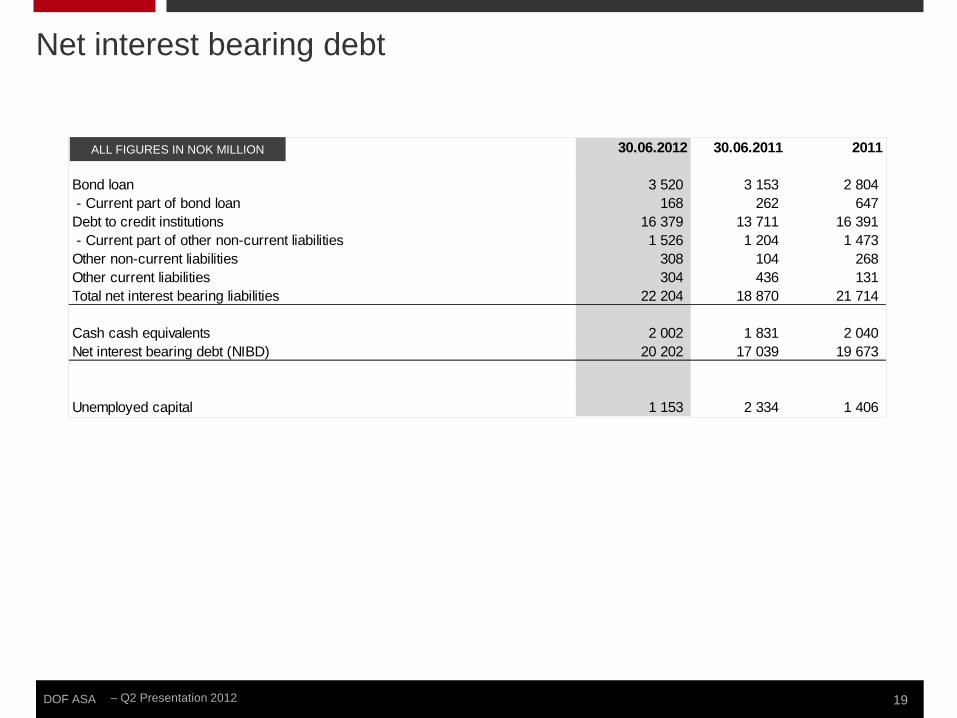

All amounts in NOK million 30.06.2012 30.06.2011 2011

Bond loan 3 520 3 153 2 804 - Current part of bond loan 168 262 647 Debt to credit institutions 16 379 13 711 16 391 - Current part of other non-current liabilities 1 526 1 204 1 473 Other non-current liabilities 308 104 268 Other current liabilities 304 436 131 Total net interest bearing liabilities 22 204 18 870 21 714

Cash cash equivalents 2 002 1 831 2 040 Net interest bearing debt (NIBD) 20 202 17 039 19 673

Unemployed capital 1 153 2 334 1 406

ALL FIGURES IN NOK MILLION

19

Net interest bearing debt

DOF ASA – Q2 Presentation 2012

Key figures Q2 2012

20

Q2 2012 Q2 2011 YTD 2012 YTD 2011 2011FINANCIAL RESULTEBITDA margin ex net gain on sale of vessel 35 % 31 % 34 % 29 % 31 %EBITDA margin 45 % 31 % 39 % 29 % 31 %EBIT margin 32 % 14 % 26 % 11 % 18 %Cashflow per share 1) 5,35 2,49 8,09 3,32 9,03 Profit per share ex. non-controlling interest 2) -2,63 -0,07 -0,43 -0,11 -3,69 Profit per share ex. unrealized loss/gain and taxes 3) 3,00 -0,58 3,52 -2,71 -0,26

BALANCEReturn on net capital 1 % -1 % -8 %Equity ratio 21 % 24 % 22 %Value adjusted equity 40 % 43 % 44 %Capex 1 646 1 957 5 367 Net interest bearing debt (MNOK) 20 202 17 039 19 673 Net interest bearing debt ex. unemployed capital (MNOK) 19 049 14 705 18 268

No of shares 111 051 348 91 037 975 111 051 348 91 037 975 96 464 574 Outstanding number of shares 111 051 348 91 037 975 111 051 348 91 037 975 111 051 348 *) Diluted number of share is the same as number of shares

1) Pre-tax result + depreciation and write downs +/- unrealized gain/loss on currencies +/- net changes in fair value of financial instruments/average no of shares.

2) Net profit excl. non controlling interest/average no of shares

3) Net profit excl.unrealized currency gain/loss on debt and market instruments and taxes/average no of shares

DOF ASA – Q2 Presentation 2012 21

DOF Supply

DOF Subsea

DOFSUB 03 PRO - NOK 500 million - Maturity July 2012 - Net NOK 168 million

DOFSUB 04 - NOK 750 million - Maturity April 2014

- Net NOK 601 million

DOFSUB 05 - NOK 750 million - Maturity April 2016

DOFSUB 06 - NOK 700 million - Maturity Oct 2015 - Net NOK 500 million

DOF 07 - NOK 950 million - Maturity July 2013 - Net NOK 410 million

DOF 08 - NOK 600 million - Maturity Dec 2015

DOF 09 - NOK 700 million - Maturity Feb 2017

Debt maturity profile

168 -

601 500 750

-

645 946 918

718 544

3 543

- -

308

1 362

1 004

- -

500

1 000

1 500

2 000

2 500

3 000

3 500

4 000

2012E 2013E 2014E 2015E 2016E After

Bond Loan Bank Debt Balloons

409,5

600 700

281

624 630 484

333 296

2185

260

1 107

816

306

-

500

1 000

1 500

2 000

2 500

2012 2013 2014 2015 2016 2017 After

Bond Loan Bank debt Balloons

DOF ASA – Q2 Presentation 2012

-

2 000

4 000

6 000

8 000

10 000

12 000

14 000

16 000

18 000

20 000

2006 2007 2008 2009 2010 2011 2012 2013 Value year end 11 112 16 606 18 474 14 025 11 654 6 892 3 090 - Value delivered - 1 550 2 550 4 450 6 238 6 631 4 378 3 090

Valu

e N

ewbu

ilds

(MN

OK

)

DOF and DOF Subsea – Value newbuild fleet

The total Order book from 2006 til 2013 and onwards is NOK 28.5 billion and 44 vessels 23 vessels are Subsea vessels with a value of NOK 18.0 billion 21 vessels are PSVs and AHTSs with a value of NOK 10.5 billion

22

DOF ASA – Q2 Presentation 2012

-

100

200

300

400

500

600

700

800

MNOK

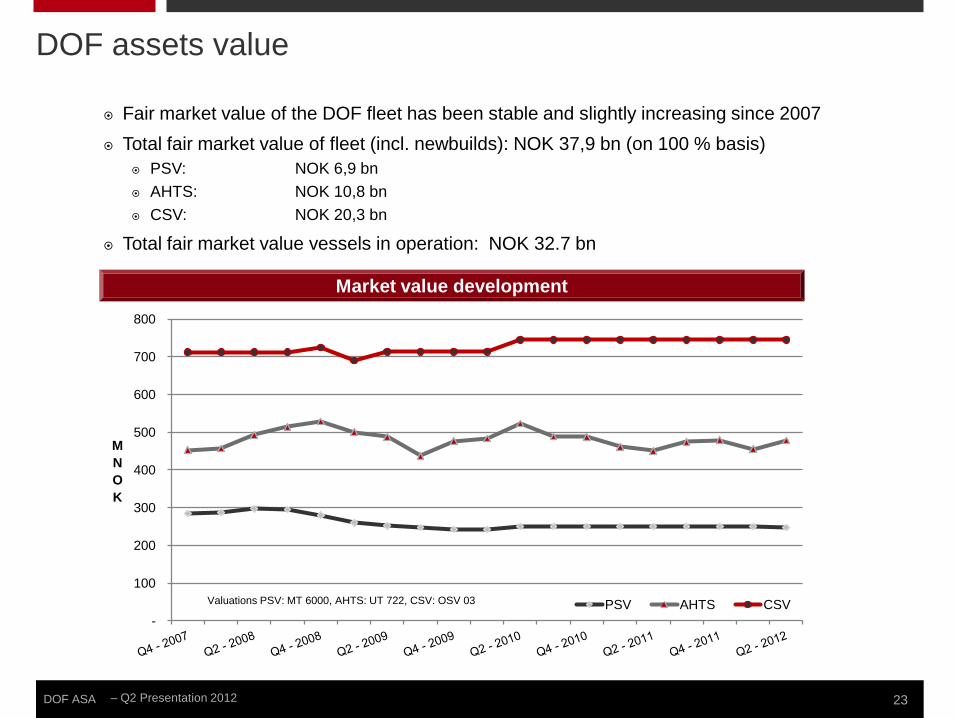

Valuations PSV: MT 6000, AHTS: UT 722, CSV: OSV 03 PSV AHTS CSV

Fair market value of the DOF fleet has been stable and slightly increasing since 2007 Total fair market value of fleet (incl. newbuilds): NOK 37,9 bn (on 100 % basis)

PSV: NOK 6,9 bn AHTS: NOK 10,8 bn CSV: NOK 20,3 bn

Total fair market value vessels in operation: NOK 32.7 bn

DOF assets value

Market value development

23

DOF ASA – Q2 Presentation 2012

0 %

20 %

40 %

60 %

80 %

100 %

120 %

57 % 62 % 62 % 59 % 53 % 46 %

43 % 38 % 38 % 41 % 47 % 54 %

Debt Equity

Gearing forecast – summary Total Fleet Market value

Vessels MNOK 12,946

Newbuilds (a) MNOK 4,522

Total Fleet MNOK 17,470

Note: Vessel values as of 30 June 2012 (a) Newbuilds to be delivered in 2012 & 2013

* The figures reflects amortization and balloon payments on debt drawn as pr 30 June 2012

Combined market value DOF Supply fleet including newbuild is NOK 17.5 billion

New-building program to be completed in 2014

Asset-level gearing on the existing fleet is 57%, decreasing to 46% in 2016

Significant gearing reduction forecasted upon completion of the current newbuild program

24

DOF Supply – Asset coverage

DOF ASA – Q2 Presentation 2012

Combined market value DOF Subsea’s fleet is NOK 16,5 billion

Asset-level gearing on the existing fleet is 56%, decreasing to 43% in 2014 Provides a significant equity cushion on top of the existing vessel-level

financing Significant gearing reduction forecasted upon completion of the current

newbuild program

Gearing forecast – summary Total Fleet Market value*

Vessels NOK 16,476

Other Equipment (a) NOK 1,378

Total Fleet NOK 17,854

Note: Vessel values as pr 30 June 2012 (a) Includes ROVs, AUV, diving systems, other equipment * Mill. NOK

* The figure reflects amortization and balloon payments on debt drawn as pr 30 June 2012

25

0 %

20 %

40 %

60 %

80 %

100 %

120 %

2012E 2013E 2014E 2015E 2016E

56 % 51 % 43 % 31 % 21 %

44 % 49 % 57 % 69 % 79 %

Fleet Level Gearing Market Value Cushion Debt Equity

DOF Subsea Group AS – Asset coverage

- Q2 Presentation 2012 DOF ASA

Contract Coverage

DOF ASA – Q2 Presentation 2012

FIRM CONTRACTS UNDER CONSTRUCTION OPTIONAL PERIOD

DOF – Contract coverage

27

A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D

Skandi Falcon 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 2 2

Skandi Marstein 1 1 1 1 1 1 1 1 1 1 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2

Skandi Foula 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

Skandi Rona 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

Skandi Buchan 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2

Skandi Sotra 1 1 1 1 1 1 1 2 2Skandi Caledonia 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1Skandi Barra 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2

Skandi Texel 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2

Skandi Mongstad 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 2 2 2 2

Skandi Flora 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2

Skandi Gamma 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 2 2 2 2 2 2 2 2 2

Skandi Waveney 1 1 1 1 1 1 1 1 1 1 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2

Skandi Feistein 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

Skandi Kvitsøy 3 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

Skandi Nova 3 3 3 3 3 3 3 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

Skandi Marøy 3 3 3 3 3 3 3 3 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

Skandi Hugen 3 3 3 3 3 3 3 3 3 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

Skandi Stord 1 1 1 1 1 1 1 1 1

Skandi Admiral 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

Skandi Vega 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2

Skandi Fjord 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2

Skandi Olympia 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 2 2 2 2 2 2 2 2 2 2 2 2

Skandi Hawk 3 3 1 1 1 1 1 1 1 1 1 1 1 1 2 2 2 2 2 2 2 2 2 2 2 2 0 0 0 0 0 0 0

Skandi Commander 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

DOF Supply

PSV

AH

TSC

SV

20162012 2013 2014 2015

DOF ASA – Q2 Presentation 2012

A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D

Skandi Peregrino 1 1 1 1 1 1 1 1 1 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2Skandi Emerald 0

Skandi Saigon

Skandi Pacific 1 1 1 1 1

Skandi Atlantic 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

2012 2013 2014 2015 2016

AH

TS

Aker DOF Deepwater

SPOT

SPOT

SPOT

Aker DOF Deepwater – Contract coverage

28

FIRM CONTRACTS UNDER CONSTRUCTION OPTIONAL PERIOD

DOF ASA – Q2 Presentation 2012

Norskan – Contract coverage

29

FIRM CONTRACTS UNDER CONSTRUCTION OPTIONAL PERIOD

A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D

Skandi Leblon 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2

Skandi Flamengo 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 2 2 2 2 2 2 2 2 2 2 2 2 2

Skandi Yare 1 1 1 1 1 1 1 1

Skandi Stolmen 1 1 1 1 1 1 1 1 1 1 1 1 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2

Skandi Captain 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2

Skandi Copacabana 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2Skandi Botafogo 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2Skandi Rio 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 2 2 2 2

Skandi Fluminense 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 2 2 2 2 2 0 0 0 0 0 0

Skandi Giant 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2

Skandi Møgster 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 2 2 2 2 2 2 2 2 2 2 2 2Skandi Ipanema 1 1 1 1 1 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 0 0 0 0

Skandi Amazonas 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

Skandi Iguacu 3 3 3 3 3 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

Skandi Angra 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

Skandi Urca 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

Skandi Paraty 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

Skandi Chieftain 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

Skandi Hav 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2

2015 20162012 2013 2014

CS

VP

SV

AH

TS

Norskan

DOF ASA – Q2 Presentation 2012 30

FIRM CONTRACTS UNDER CONSTRUCTION OPTIONAL PERIOD * TC from DOF

A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D

1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 2 2 2 2 2 2 2 2 2

Ocean Protector 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2

Skandi Seven 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2Skandi Salvadore 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1Skandi Vitoria 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2

Skandi Aker 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2

Skandi Santos 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2

Skandi Patagonia 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1Skandi Carla 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1Skandi Neptune 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2

Skandi Achiever 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2

Skandi Acergy 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 2 2 2 2

Skandi Arctic 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1Skandi Niteroi 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2

1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1Skandi Skansen 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 2 2 2 1 1 1 2 2 2 1 1 1 2 2 2 2 2 2 2 2 2

Skandi Inspector 1 1 1 1 1 1 1 1 1 1 1 1 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2Skandi Constructor 1 1 1 1 1 1 1 0 0 0 0 0 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 2 2 2 2 2 2 2 2 2

Skandi Singapore 1 1 1 1 1 1 1Skandi Hercules 1 1 1 1 1 1 1 1 1Skandi Skolten 1 1 1 1 1 1 1 1 1 1Skandi Hawk* 1 1 1 1 1 1

1 1 1 0 11 1 1 1 1 1 1 2 2 2 20 1 1 1 1 1 1 1

NB 776 3 3 3 3 3 3 3 3 3 3 3 3 2 2 2 2 2 2 2 2 2 2 2 2 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

2012 2013 2014 2015 2016

Geograph

Geobay

CS

V

Geoholm

Geosea

DOF Subsea

Geosund

DOF Subsea – Contract coverage (vessels)

DOF ASA - Q2 Presentation 2012

DOF Subsea

DOF ASA – Q2 Presentation 2012

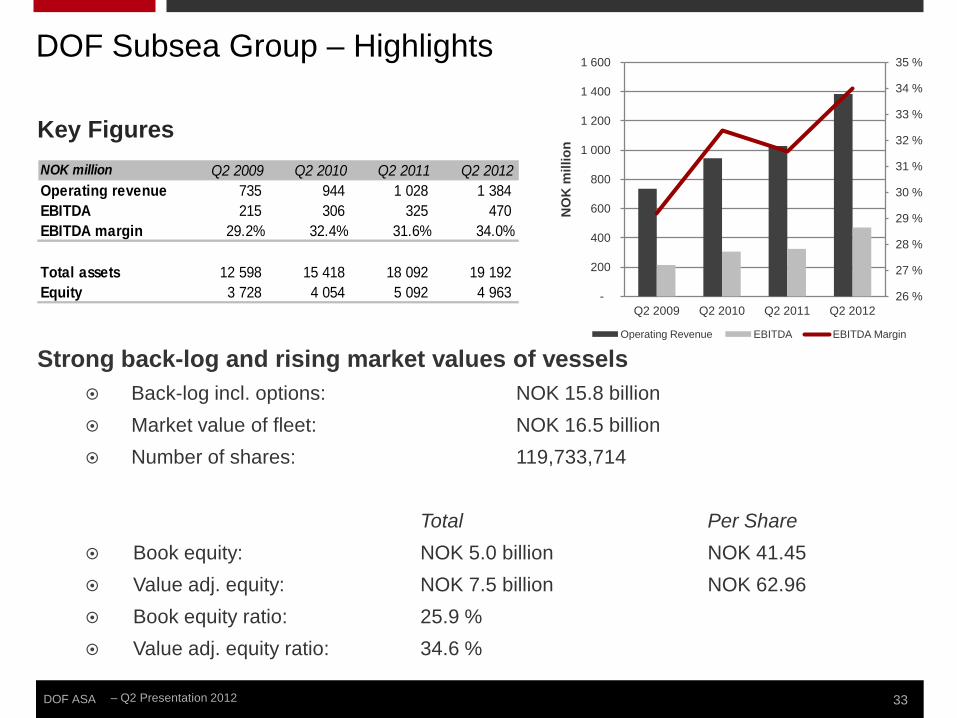

Fleet One of the largest subsea vessel owners in the world Operates a fleet of 25 vessels with a total market value of NOK16.5

billion Operates 52 ROVs, including 5 newbuilds

Global organization

Head office in Bergen Regional offices in Australia, Singapore, Norway, UK, Angola, US,

Canada and Brazil

Total of 2,332 employees Subsea employees: 1,332 Of which offshore engineers and project staff: 900 Marine crew: 1,000

32

Norway Brazil Canada US UK Asia Pacific Angola

233 316 36 62 313 354 18 * As pr 30th June 2012

DOF Subsea Group – Highlights

DOF ASA – Q2 Presentation 2012 33

Strong back-log and rising market values of vessels Back-log incl. options: NOK 15.8 billion Market value of fleet: NOK 16.5 billion Number of shares: 119,733,714

Total Per Share

Book equity: NOK 5.0 billion NOK 41.45 Value adj. equity: NOK 7.5 billion NOK 62.96 Book equity ratio: 25.9 % Value adj. equity ratio: 34.6 %

Key Figures

26 %

27 %

28 %

29 %

30 %

31 %

32 %

33 %

34 %

35 %

-

200

400

600

800

1 000

1 200

1 400

1 600

Q2 2009 Q2 2010 Q2 2011 Q2 2012

NO

K m

illio

n

Operating Revenue EBITDA EBITDA Margin

NOK million Q2 2009 Q2 2010 Q2 2011 Q2 2012Operating revenue 735 944 1 028 1 384 EBITDA 215 306 325 470 EBITDA margin 29.2% 32.4% 31.6% 34.0%

Total assets 12 598 15 418 18 092 19 192 Equity 3 728 4 054 5 092 4 963

DOF Subsea Group – Highlights

DOF ASA – Q2 Presentation 2012

GEOGRAPHICAL FOCUS AREAS

Rio de Janeiro (316)

Buenos Aires

Singapore (91)

Houston (62) St. Johns (36)

Aberdeen (313)

Bergen (233)

Cairo

Brunei

Macae Jakarta (3)

Manila

Angola (18)

St. Petersburg

Perth (255)

34

(5)

Global player – DOF Subsea

DOF ASA – Q2 Presentation 2012 35

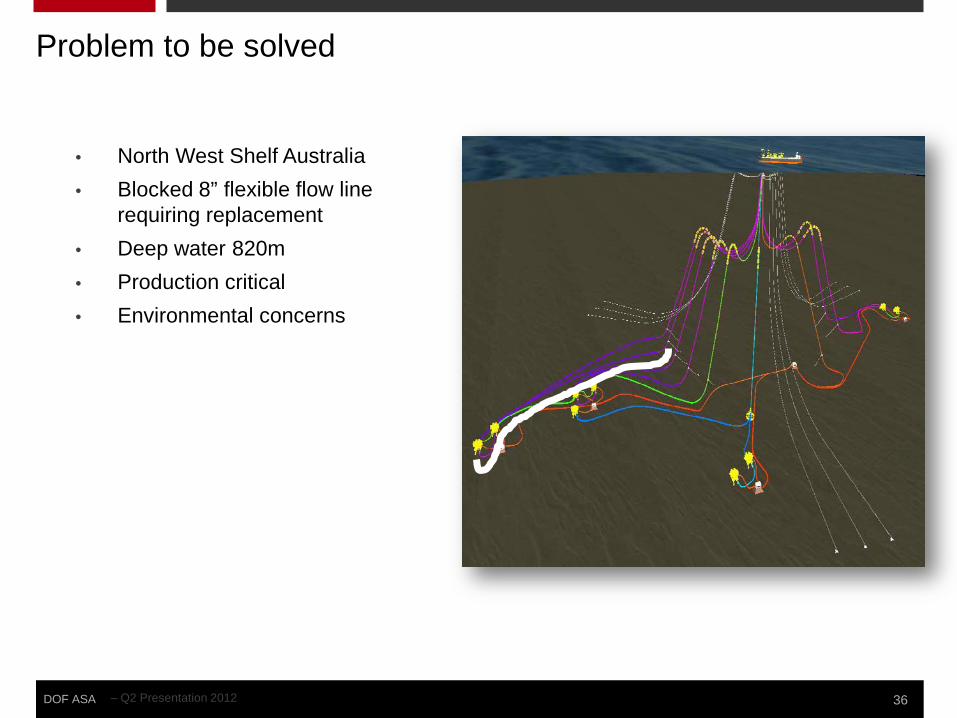

BHP Billiton Stybarrow H4, Remediation Project

DOF ASA – Q2 Presentation 2012

• North West Shelf Australia • Blocked 8” flexible flow line

requiring replacement • Deep water 820m • Production critical • Environmental concerns

36

Problem to be solved

DOF ASA – Q2 Presentation 2012

• Project Management and Engineering • Design and build a Horizontal Lay

System • Transport and installation of 8” flexible • Disconnect existing 8’ flexible • Install new flow line and jumpers • Testing and commissioning • Permanently abandon existing flow line

37

Scope of work

DOF ASA – Q2 Presentation 2012 38

Period Description 8th July 2011 Commenced pre engineering

6th September 2011 Contract award

10th November 2011 Offshore mobilisation

28th December 2011 Project complete and demobilised

Schedule

DOF ASA – Q2 Presentation 2012 39

Marine Spread – Skandi Hercules

DOF ASA - Q2 Presentation 2012

Outlook

DOF ASA – Q2 Presentation 2012 41

Substantial subsea growth announced

Supply side

Newbuilding program within all subsectors limited

Old fleet

Financing constraints

Demand side

Surface to subsea activity increasing

Subsea CAPEX to double by 2014

Increased tendering for equipment

Backlog

“We expect a strong market in all regions”

DOF ASA – Q2 Presentation 2012 42

PSV and AHTS

Demand side

High oil price

Increased E & P spending

Increased deepwater spending

Increased infrastructure spending

Strongest growth in Brazil, West Africa and Asia Pacific

Increased focus on newer, larger and more advanced vessels

Supply side

AHTS (larger than 15,000 BHP)

Newbuilding program is limited

Financing constraints

DOF ASA – Q2 Presentation 2012 43

PSV and AHTS

Supply side

PSV (larger than 3,000 dwt)

Large newbuilding program

Financing constraints, but to a lower degree due to lower CAPEX.

We expect the AHTS market to turn in the favour of owners, with good rates and high utilisation in the spot market and higher rates on term charters.

We are uncertain about the future balance in the PSV market.

DOF ASA – Q2 Presentation 2012

“We expect Q3 to be in line with Q2 or better.” ”We repeat our 2012 guidance”

44

Short term outlook

Thank you

Presented by Mons Aase - CEO Hilde Drønen - CFO

DOF ASA – Q2 Presentation 2012

DISCLAIMER

This presentation by DOF ASA designed to provide a high level overview of aspects of the operations of the DOF ASA Group. The material set out in the presentation is current as at 23 Aug, 2012. This presentation contains forward-looking statements relating to operations of the DOF ASA Group that are based on management’s own current expectations, estimates and projections about matters relevant to DOF ASA‘s future financial performance. Words such as “likely”, “aims”, “looking forward”, “potential”, “anticipates”, “expects”, “predicts”, “plans”, “targets”, “believes” and “estimates” and similar expressions are intended to identify forward-looking statements. References in the presentation to assumptions, estimates and outcomes and forward-looking statements about assumptions, estimates and outcomes, which are based on internal business data and external sources, are uncertain given the nature of the industry, business risks, and other factors. Also, they may be affected by internal and external factors that may have a material effect on future business performance and results. No assurance or guarantee is, or should be taken to be, given in relation to the future business performance or results of the DOF ASA Group or the likelihood that the assumptions, estimates or outcomes will be achieved. While management has taken every effort to ensure the accuracy of the material in the presentation, the presentation is provided for information only. DOF ASA , its officers and management exclude and disclaim any liability in respect of anything done in reliance on the presentation. All forward-looking statements made in this presentation are based on information presently available to management and DOF ASA assumes no obligation to update any forward looking- statements. Nothing in this presentation constitutes investment advice and this presentation shall not constitute an offer to sell or the solicitation of any offer to buy any securities or otherwise engage in any investment activity. You should make your own enquiries and take your own advice (including financial and legal advice) before making an investment in the company's shares or in making a decision to hold or sell your shares.

46