qualitas medical group limited - finanznachrichten.de

TRANSCRIPT

QUALITAS MEDICAL GROUP LIMITED

CORPORATE PRESENTATION

July 2009

Contents

Our Business

Our Competitive Edge

Corporate Developments

Growth Strategies

Financial Highlights

Summary

Our Business

4

Who We Are

Established in 1997

A leading primary healthcare services

provider in Malaysia Operates GP clinics with supporting diagnostic

services under Qualitas brand name

Network of 160 clinics across the country

More than 1 million patient visits annually

Established MNC client base

Regional network in India, Cambodia & New Zealand

Scaleable & replicable business model

Listed on SGX Catalist on 1 September 2008

5

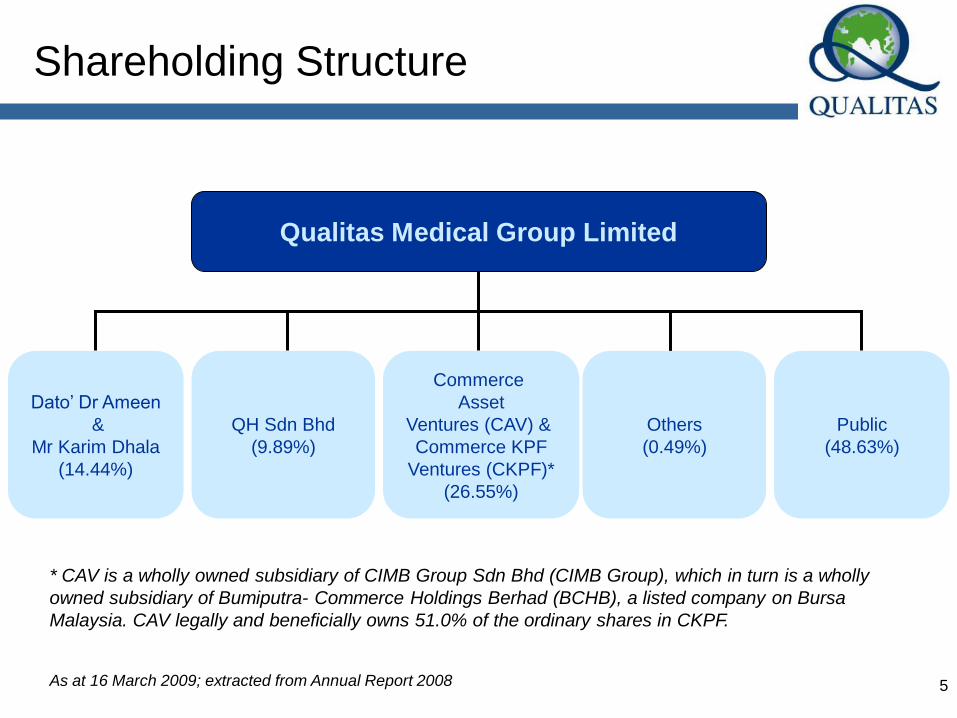

Shareholding Structure

Dato’ Dr Ameen

&

Mr Karim Dhala

(14.44%)

QH Sdn Bhd

(9.89%)

Qualitas Medical Group Limited

Commerce

Asset

Ventures (CAV) &

Commerce KPF

Ventures (CKPF)*

(26.55%)

Public

(48.63%)

Others

(0.49%)

* CAV is a wholly owned subsidiary of CIMB Group Sdn Bhd (CIMB Group), which in turn is a wholly

owned subsidiary of Bumiputra- Commerce Holdings Berhad (BCHB), a listed company on Bursa

Malaysia. CAV legally and beneficially owns 51.0% of the ordinary shares in CKPF.

As at 16 March 2009; extracted from Annual Report 2008

6

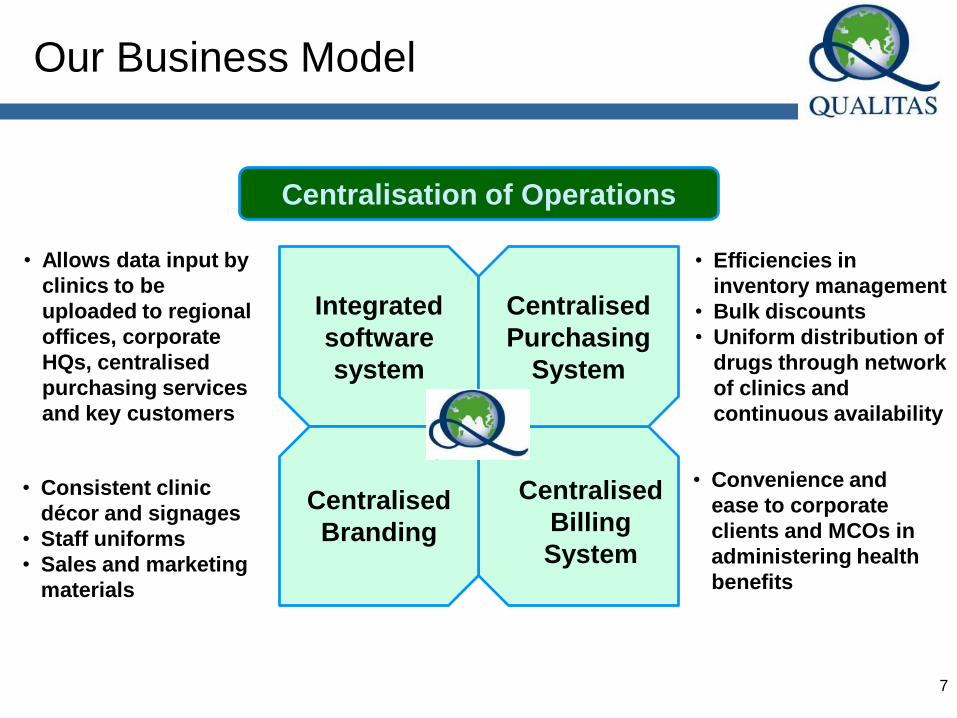

Our Business Model

Doctor-led and doctor-governed

Network of doctor-shareholders

Focus on primary healthcare services

Outpatient services by GPs

One-stop higher-end clinics with a team of GPs

Prolonged care & monitoring of patients with chronic conditions

Health maintenance & general health screening and periodic

vaccinations

Equipped with supporting medical diagnostics services eg ECGs,

ultrasound and X-ray facilities

• Consistent clinic

décor and signages

• Staff uniforms

• Sales and marketing

materials

• Allows data input by

clinics to be

uploaded to regional

offices, corporate

HQs, centralised

purchasing services

and key customers

Our Business Model

Centralisation of Operations

Integrated

software

system

Centralised

Purchasing

System

Centralised

Billing

System

Centralised

Branding

• Efficiencies in

inventory management

• Bulk discounts

• Uniform distribution of

drugs through network

of clinics and

continuous availability

• Convenience and

ease to corporate

clients and MCOs in

administering health

benefits

7

8

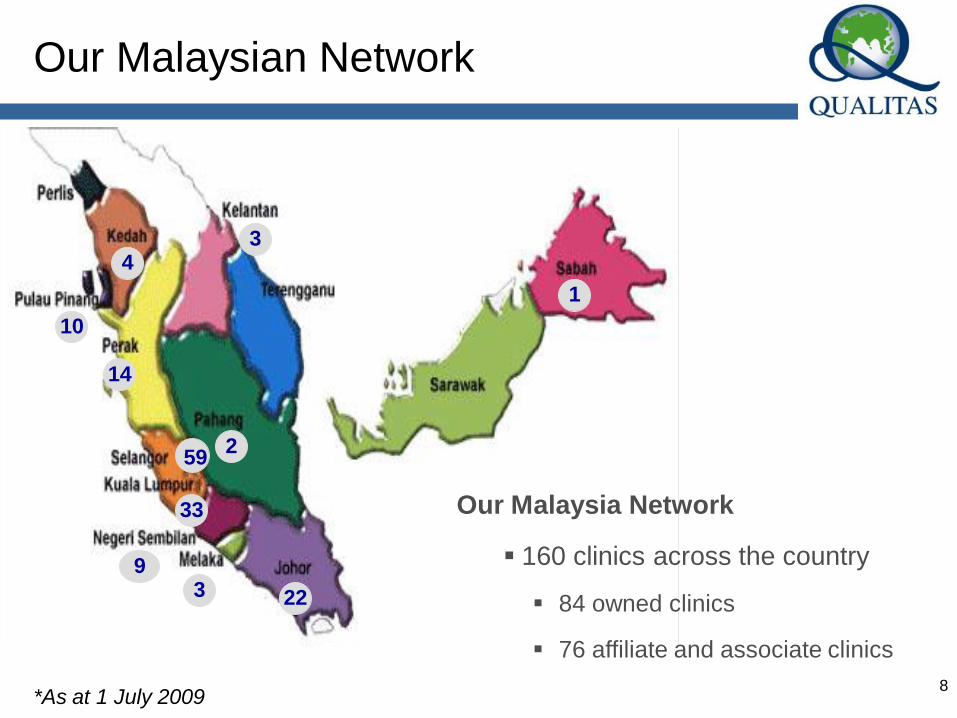

Our Malaysian Network

*As at 1 July 2009

Our Malaysia Network

160 clinics across the country

84 owned clinics

76 affiliate and associate clinics

4

10

3

14

59

33

93 22

2

1

9

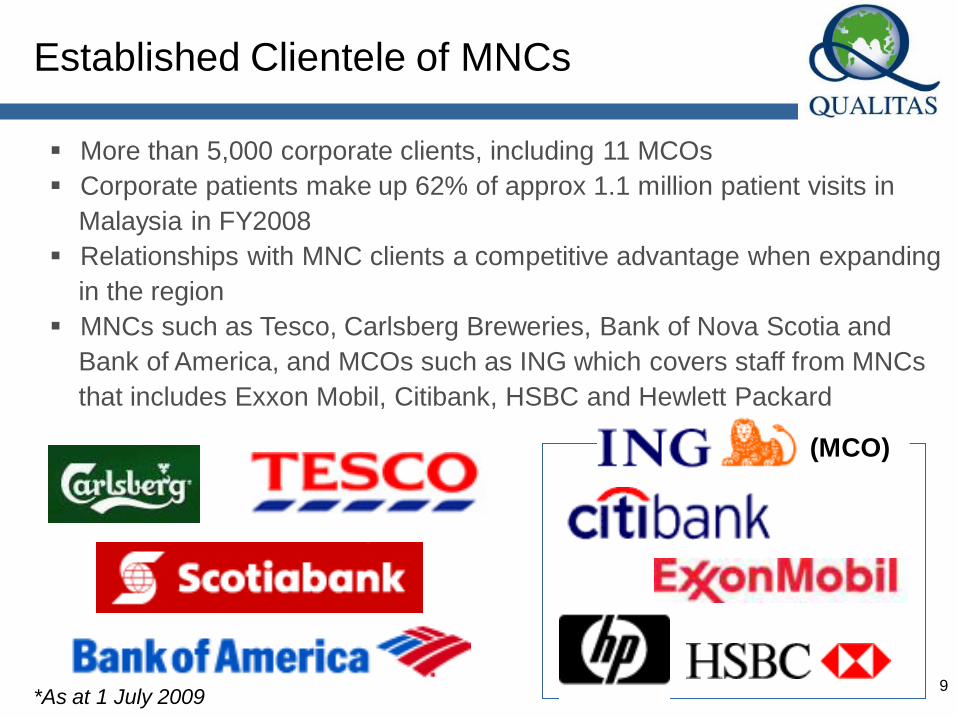

Established Clientele of MNCs

More than 5,000 corporate clients, including 11 MCOs

Corporate patients make up 62% of approx 1.1 million patient visits in

Malaysia in FY2008

Relationships with MNC clients a competitive advantage when expanding

in the region

MNCs such as Tesco, Carlsberg Breweries, Bank of Nova Scotia and

Bank of America, and MCOs such as ING which covers staff from MNCs

that includes Exxon Mobil, Citibank, HSBC and Hewlett Packard

(MCO)

*As at 1 July 2009

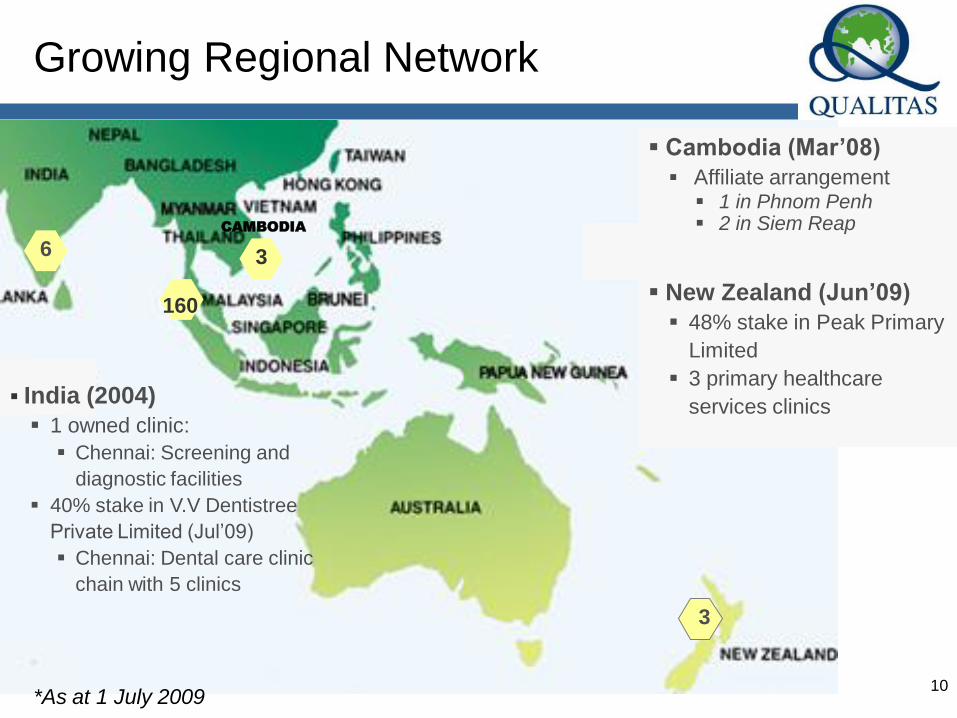

India (2004)

1 owned clinic:

Chennai: Screening and

diagnostic facilities

40% stake in V.V Dentistree

Private Limited (Jul’09)

Chennai: Dental care clinic

chain with 5 clinics

10

Growing Regional Network

6 3

160

Cambodia (Mar’08)

Affiliate arrangement 1 in Phnom Penh 2 in Siem Reap

New Zealand (Jun’09)

48% stake in Peak Primary

Limited

3 primary healthcare

services clinics

3

CAMBODIA

*As at 1 July 2009

Competitive Strengths

12

One of the Largest Networks of

Private Clinics in Malaysia

Believed to be one of the largest and most comprehensive

geographical coverage in Malaysia

Represents a critical mass of doctors

Several of whom with requisite seniority and experience to take on

quality and supervisory roles on in-house committees and as

medical directors

Attractive to clients and potential partners

Corporate employers and MNCs seeking to provide primary

healthcare benefits to employees in Malaysia

Individual patients seeking quality healthcare

Small private clinics seeking to join or become affiliated or

associated with a larger group

Distributors and suppliers of pharmaceutical and medical supplies

13

Economies of Scale

Centralised Purchasing System

Enjoys bulk discounts

Minimises inventory levels and obsolescence

Centralised Marketing with Consolidated Billings

Greater clout to negotiate and contract as a single party with

corporate employers and MNCs

Convenient for corporate clients and MCOs to administer

healthcare benefits to employees and clients

14

Scaleable Business Model

Customised IT infrastructure to manage network of clinics in

Malaysia

Ability to remotely and actively monitor operations of clinics in different

areas

Access to patient charges, registration records, database and medicines

dispensed

Comprehensive system of management of clinics

Scaleable and replicable in other parts of region

IT system will form backbone of regional expansion plans

Management able to monitor operations closely

15

Capacity to Provide Wide Range of

Primary Healthcare Services

Capacity to acquire necessary equipment and provide wide

range of primary healthcare services, such as ECGs &

scanning facilities

Due to comparatively large proportion of corporate patient load

Larger one-stop high-end clinics possess supporting

diagnostic tests equipment

Allows us to cater to diagnostic needs in addition to usual GP

services

Owned clinics located at premises of large corporate

employers

Eg Bank Negara Malaysia, F&N, Carlsberg Brewery, RJ

Reynolds Tobacco, Tractors Malaysia & Sanyo

Enjoys captive market

16

Reputable Qualitas Brand Name

Qualitas brand gaining recognition amongst corporate employers,

MNCs and local communities in Malaysia

Centralised branding strategy maximised by large number of clinics in

network

Co-branding with existing practice names of acquired clinics

Affiliate clinics licensed to use Qualitas brand

Patient-centric philosophy

Doctors to focus on clinical functions

Management & other professionals take on non-clinical functions

17

Experienced & Proven Management Team

Doctor-led and doctor-governed

Interests of doctor-employee shareholders aligned with shareholders

Management team of dedicated and qualified professionals

Proven track records in healthcare industry

Founder, Chairman & Managing Director Dato’ Dr Ameen

responsible for growing business

His experience spans both public and private sectors for last 32 years

Supported by Executive Director Mr Karim Dhala

Oversees Group’s finance, accounting and general administrative and

IT functions, and assists Dato Dr Ameen in setting out strategies and

policies for Group’s operations and development

Team of Executive Officers and various in-house professional

committees

Ability to identify new market opportunities, implement strategic

plans and exercise prudent financial management

Corporate

Developments

19

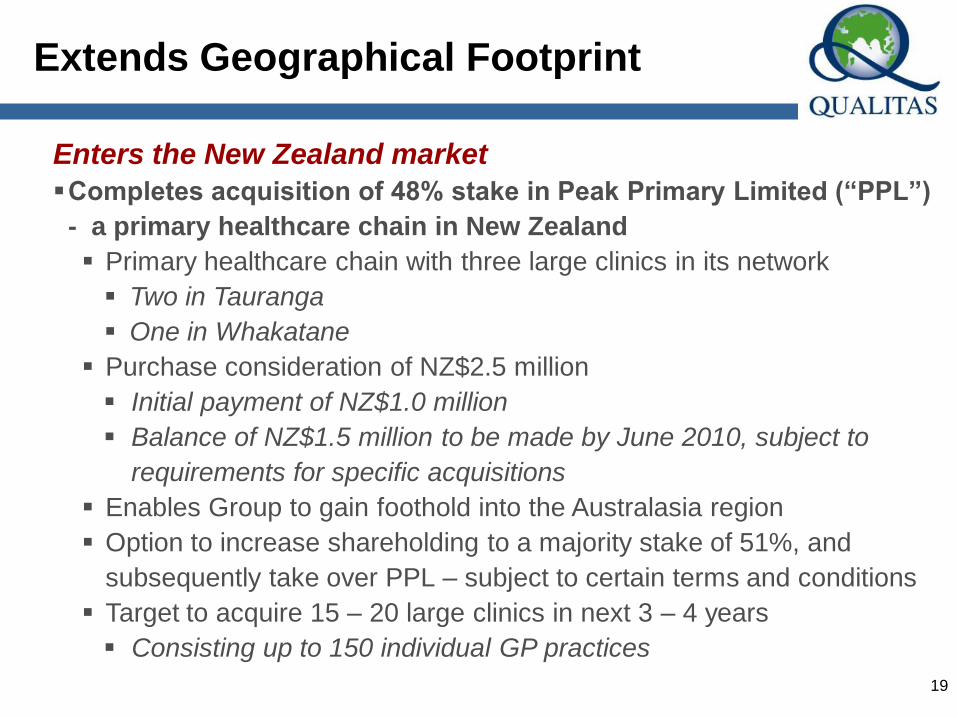

Extends Geographical Footprint

Enters the New Zealand market

Completes acquisition of 48% stake in Peak Primary Limited (“PPL”)

- a primary healthcare chain in New Zealand

Primary healthcare chain with three large clinics in its network

Two in Tauranga

One in Whakatane

Purchase consideration of NZ$2.5 million

Initial payment of NZ$1.0 million

Balance of NZ$1.5 million to be made by June 2010, subject to

requirements for specific acquisitions

Enables Group to gain foothold into the Australasia region

Option to increase shareholding to a majority stake of 51%, and

subsequently take over PPL – subject to certain terms and conditions

Target to acquire 15 – 20 large clinics in next 3 – 4 years

Consisting up to 150 individual GP practices

20

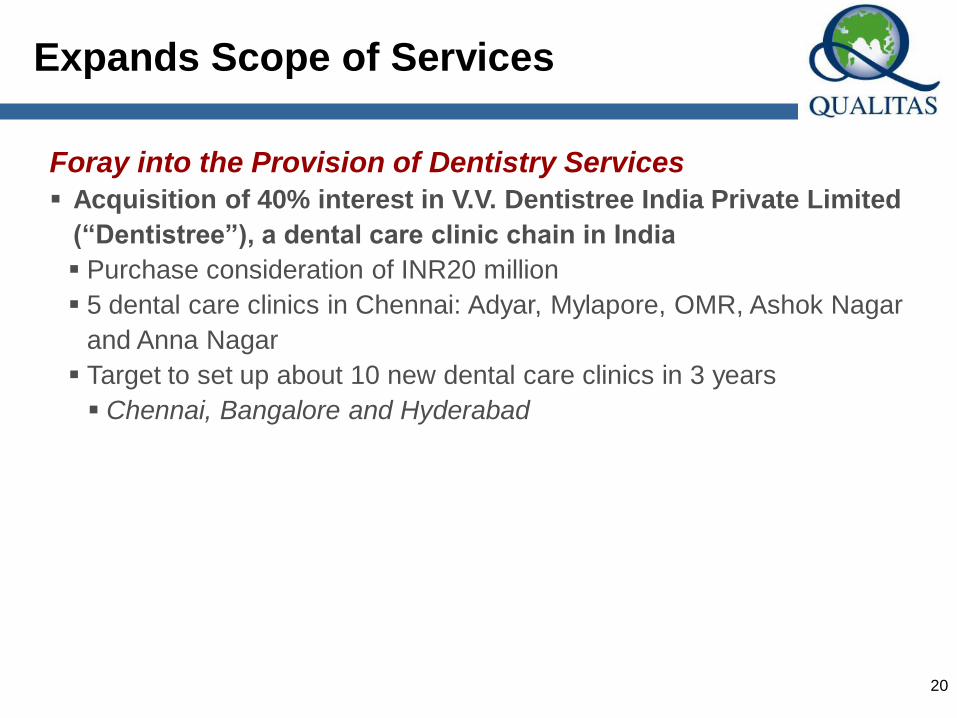

Expands Scope of Services

Foray into the Provision of Dentistry Services

Acquisition of 40% interest in V.V. Dentistree India Private Limited

(“Dentistree”), a dental care clinic chain in India

Purchase consideration of INR20 million

5 dental care clinics in Chennai: Adyar, Mylapore, OMR, Ashok Nagar

and Anna Nagar

Target to set up about 10 new dental care clinics in 3 years

Chennai, Bangalore and Hyderabad

Growth Strategies

22

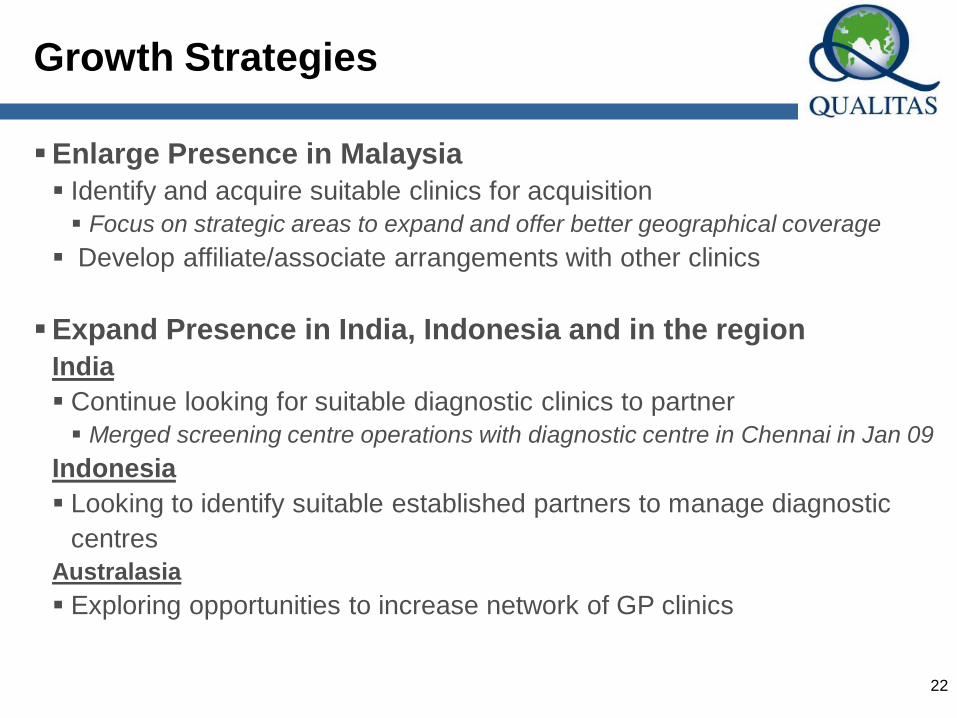

Growth Strategies

Enlarge Presence in Malaysia

Identify and acquire suitable clinics for acquisition

Focus on strategic areas to expand and offer better geographical coverage

Develop affiliate/associate arrangements with other clinics

Expand Presence in India, Indonesia and in the region

India

Continue looking for suitable diagnostic clinics to partner

Merged screening centre operations with diagnostic centre in Chennai in Jan 09

Indonesia

Looking to identify suitable established partners to manage diagnostic

centres

Australasia

Exploring opportunities to increase network of GP clinics

23

Growth Strategies

Increase marketing efforts towards corporate clients and

patients

Provide more value-added services in the form of health talks, health

awareness campaigns, and privilege cards for targeted groups of

patients

Increase operational efficiency and reduce expenses

Continue to monitor operating cost, which is subject to inflationary

pressure

Endeavour to pass on increase in drug prices, medical supplies and

investigations to patients

Financial Highlights

25

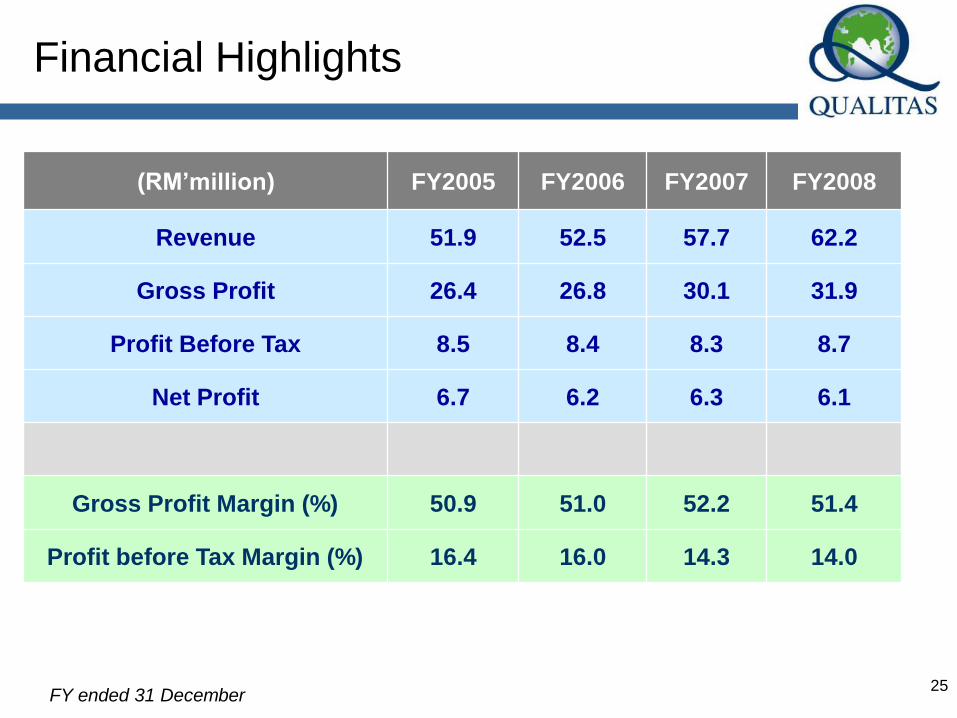

Financial Highlights

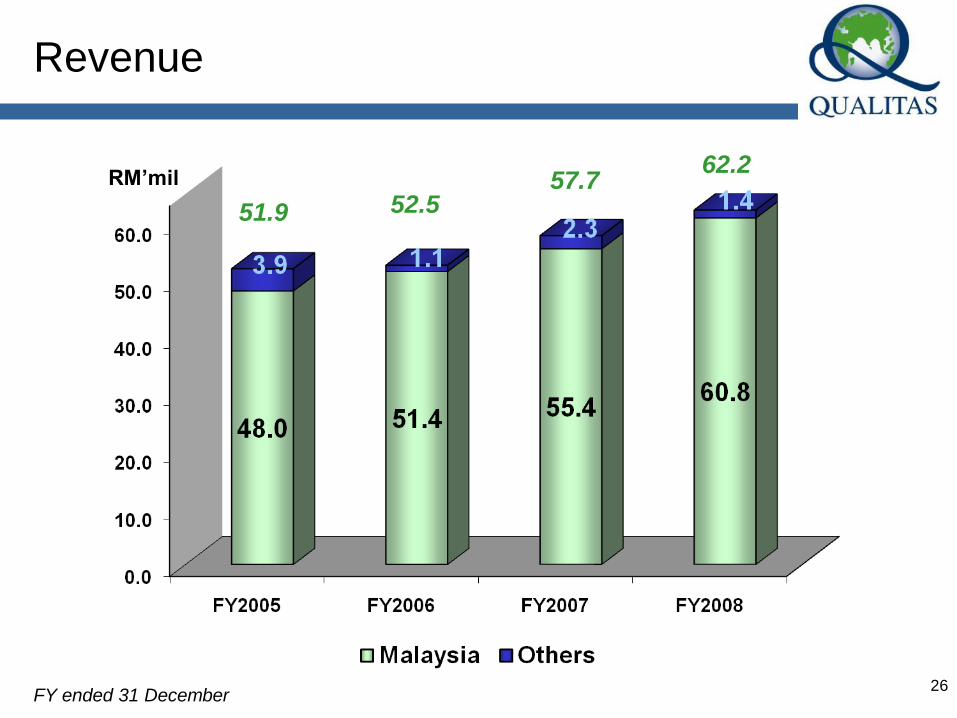

(RM’million) FY2005 FY2006 FY2007 FY2008

Revenue 51.9 52.5 57.7 62.2

Gross Profit 26.4 26.8 30.1 31.9

Profit Before Tax 8.5 8.4 8.3 8.7

Net Profit 6.7 6.2 6.3 6.1

Gross Profit Margin (%) 50.9 51.0 52.2 51.4

Profit before Tax Margin (%) 16.4 16.0 14.3 14.0

FY ended 31 December

26

Revenue

FY ended 31 December

RM’mil

51.9 52.557.7

62.2

27

Gross Profit

FY ended 31 December

RM’mil

28

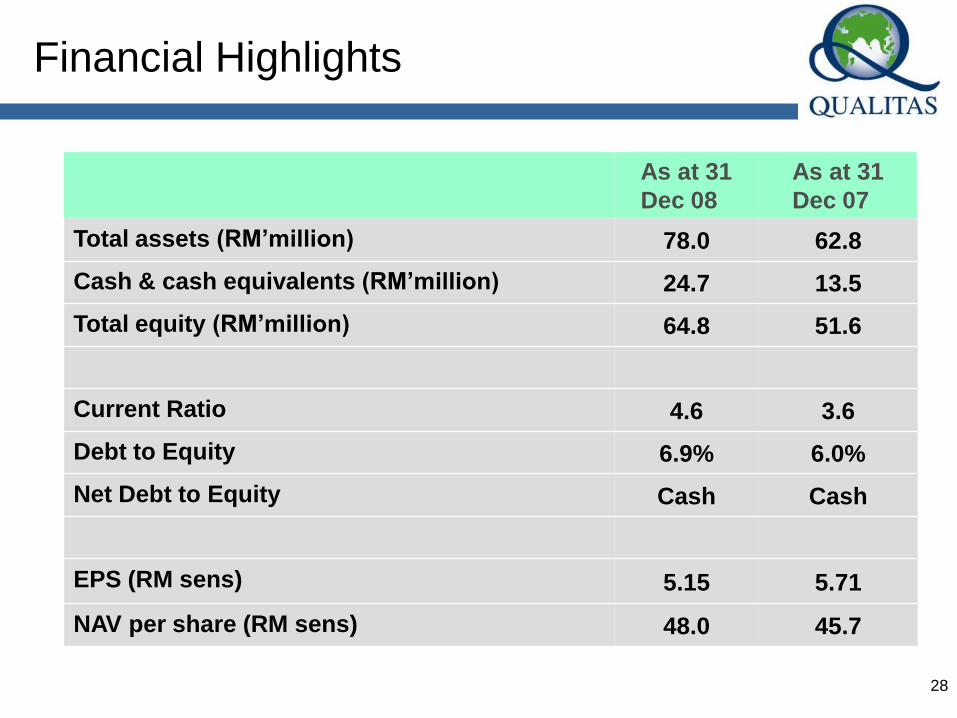

Financial Highlights

As at 31

Dec 08

As at 31

Dec 07

Total assets (RM’million) 78.0 62.8

Cash & cash equivalents (RM’million) 24.7 13.5

Total equity (RM’million) 64.8 51.6

Current Ratio 4.6 3.6

Debt to Equity 6.9% 6.0%

Net Debt to Equity Cash Cash

EPS (RM sens) 5.15 5.71

NAV per share (RM sens) 48.0 45.7

Summary

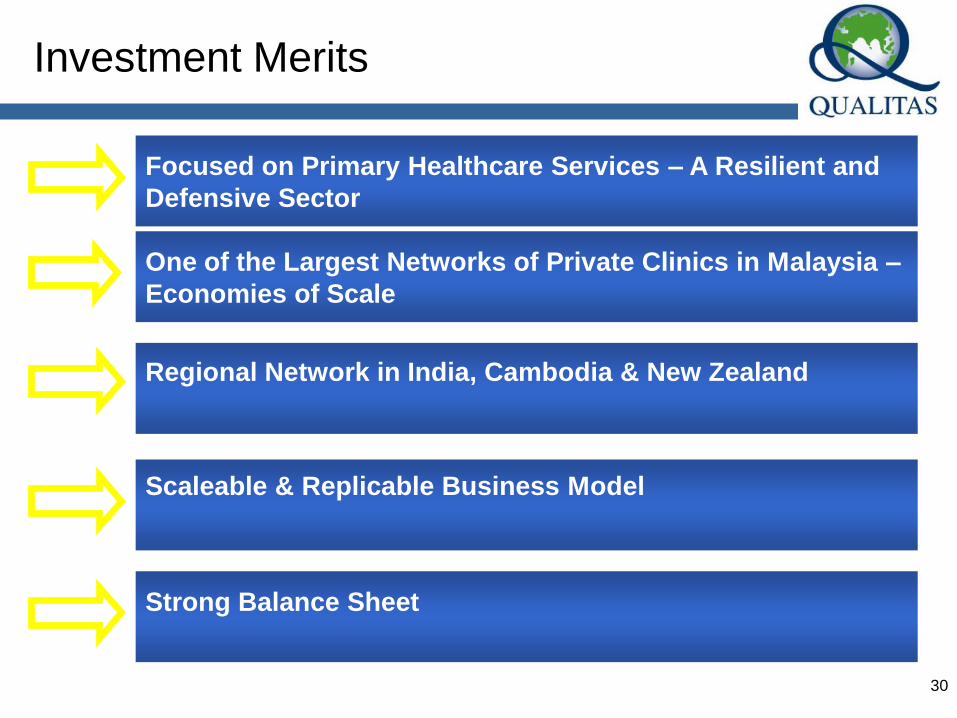

Investment Merits

Scaleable & Replicable Business Model

Strong Balance Sheet

Regional Network in India, Cambodia & New Zealand

One of the Largest Networks of Private Clinics in Malaysia –

Economies of Scale

30

Focused on Primary Healthcare Services – A Resilient and

Defensive Sector

Discussion