quarterly activities report and appendix 5b€¦ · and fluorspar mineralisation at surface up to...

TRANSCRIPT

ENABLING LOW CARBON TECHNOLOGIES

Quarterly Activities Report and Appendix 5B December 2017

Developing the Ngualla Project into an – ethically sustainable – long term – high quality supplier of choice to the global high technology rare earth market

DIRECTORSNon-Executive Chairman: Jonathan Murray

Non-Executive Directors: John JetterDarren Townsend

Chief Executive Officer: Rocky Smith

Company Secretary: Graeme Scott

CORPORATE DETAILS

AS AT 31 DEC 2017:

Ordinary Shares on issue: 615.9m

Listed Options PEKOB $0.061 November 2018: 81.2m

52 week range: 3.4c – 13.0c

Market Cap: $32.6m (at 5.3c)

ASX: PEK

Peak Resources Limited Ground Floor, 5 Ord Street, West Perth, Western Australia 6005. PO Box 603, West Perth 6872.

ASX: PEK ACN: 112 546 700

Telephone: +61 8 9200 5360 [email protected] www.peakresources.com.au

* Project economic assessment compared to BFS is summarised in ASX announcement ”Process optimisation study boosts Ngualla’s operating margin” of 28 August 2017. Economic assessment at prevailing prices in ASX announcement “Ngualla Project Update – Process Optimisation enables lower price deck to deliver similar BFS results“ of 12 October 2017.

• Peak continues to actively engage with the Tanzanian government in its efforts to have the Special Mining Licence granted as soon as possible.

• Positive discussions held with officials in Tanzania and support for the project received after new Natural Resources Laws announced.

• Record year for E-mobility in 2017.

• Renounceable 1 for 8 Entitlements Issue Offer and placement of shortfall completed in November 2017 raises A$2.7 million.

• Debt repayment of US$1.5 million made to Appian during the Quarter.

• Rocky Smith appointed as CEO, brings rare earth mines development and operating expertise.

HIGHLIGHTS:

The company was pleased to announce during the Quarter progress made in a number of important areas towards the successful development of its 75% owned Ngualla Rare Earth Project including:

• The Project Optimisation Study enables delivery of similar economic outcomes as the Bankable Feasibility Study (“BFS”)* at a lower price deck:

• Average consolidated annual EBITDA US $150m pa over the 26 year life of the project

• Post Tax NPV8 US$ 612 million and IRR 22%* at the then current rare earth prices

• Total Life of Project Opex intensity US$32.24 / kg NdPr is the breakeven point for a positive cash flow, well below current prices.

For

per

sona

l use

onl

y

2 ENABLING LOW CARBON TECHNOLOGIES

Quarterly Activities Report December 2017

Process Optimisation StudyFollowing the process optimisation study in August and the comprehensive Project Update released in September the Company was pleased to be able to provide a further Project Update during the Quarter (ASX Announcement “Lower price deck delivers similar BFS results for Ngualla” of 12 October 2017) .

The results and assumptions in the Project Update report build on the Bankable Feasibility Study (BFS) completed in April last year by including the improvements gained from the Collector Screening Testwork (ASX Announcement dated 28th August 2017 and titled “Process optimisation study boosts Ngualla’s operating margin”). The update in-cluded the latest rare earth pricing trends at that time, which had seen a 99% increase in NdPr prices in 10 months since November 2016.

HIGHLIGHTS INCLUDE:• Post Tax NPV8 US$ 612 million and IRR 22% at current rare earth price assumptions.

• Total Life of Project Opex intensity US$ 32.24 / kg NdPr is the breakeven point for a positive cash flow, well below current prices.

• Total pre-production CAPEX of US$ 365 million for the Ngualla and Tees Valley refinery combined. This has the potential to be the lowest Capex among its peers for a fully integrated producer.

• Average consolidated annual EBITDA US$ 150* mpa over the 26 year life of the Project.

A financial analysis of the project using the process optimisation improvements combined with a

lower rare earth price assumption delivers project economics at a similar level as the BFS.

The financial evaluation of the Project Update using the price deck of NdPr US$ 77.50/kg, Lanthanum oxide US$ 3.70/kg and Cerium oxide US$ 2.20, shows Ngualla to be a long term and profitable project with substantial upside should prices increase further.

Production Assumptions BFS Project Update

Life of Operation 31 Years 26 Years

Average Annual Production (tonnes) BFS Project Update

Ore Mill Feed 624,000 tpa 711,000 tpa

Processed Mineral Concentrate 28,300 tpa 32,700 tpa

NdPr mixed oxide 2N 2,420 tpa 2,810 tpa

La oxide equivalent (final product: La carbonate) 3,650 tpa 4,230 tpa

Ce oxide equivalent (final product Ce carbonate) 1,660 tpa 1,920 tpa

SEG and Mixed Heavy oxide equivalent (final product mixed carbonate) 280 tpa 330 tpa

Table 1: Comparison of BFS production assumptions to Project Update

* Post ramp-up.

For

per

sona

l use

onl

y

3 ENABLING LOW CARBON TECHNOLOGIES

Quarterly Activities Report December 2017

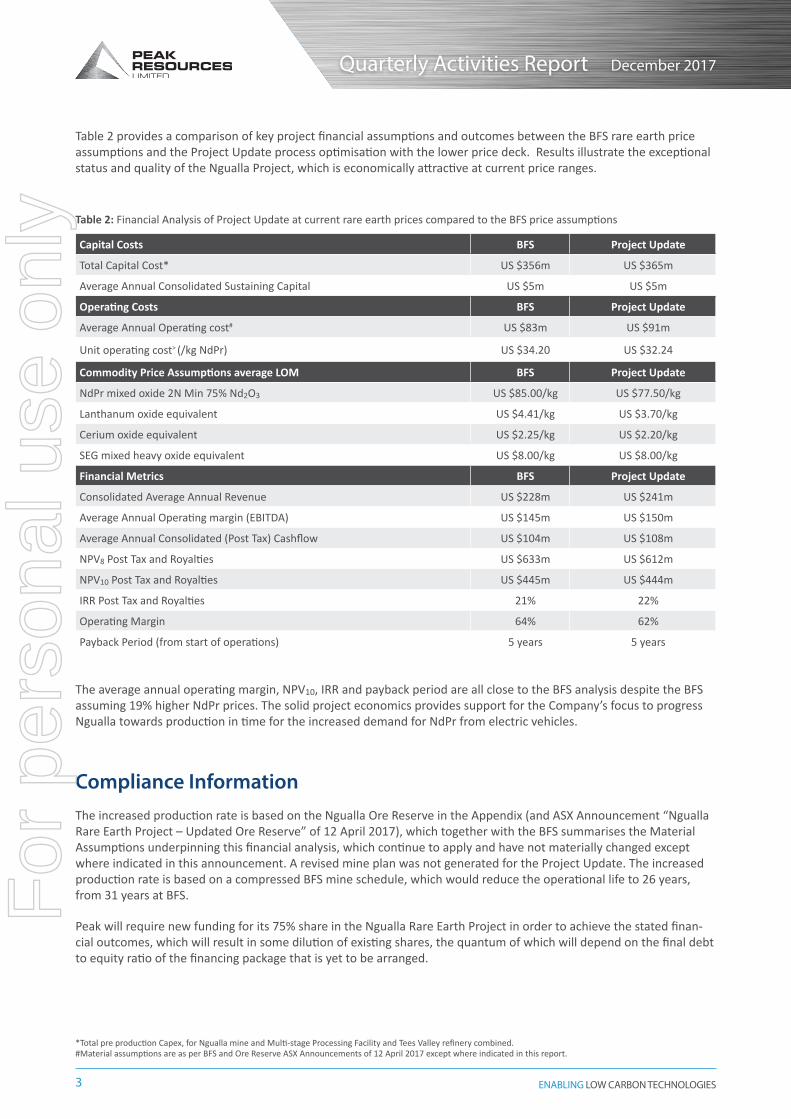

Table 2 provides a comparison of key project financial assumptions and outcomes between the BFS rare earth price assumptions and the Project Update process optimisation with the lower price deck. Results illustrate the exceptional status and quality of the Ngualla Project, which is economically attractive at current price ranges.

Capital Costs BFS Project Update

Total Capital Cost* US $356m US $365m

Average Annual Consolidated Sustaining Capital US $5m US $5m

Operating Costs BFS Project Update

Average Annual Operating cost# US $83m US $91m

Unit operating cost> (/kg NdPr) US $34.20 US $32.24

Commodity Price Assumptions average LOM BFS Project Update

NdPr mixed oxide 2N Min 75% Nd2O3 US $85.00/kg US $77.50/kg

Lanthanum oxide equivalent US $4.41/kg US $3.70/kg

Cerium oxide equivalent US $2.25/kg US $2.20/kg

SEG mixed heavy oxide equivalent US $8.00/kg US $8.00/kg

Financial Metrics BFS Project Update

Consolidated Average Annual Revenue US $228m US $241m

Average Annual Operating margin (EBITDA) US $145m US $150m

Average Annual Consolidated (Post Tax) Cashflow US $104m US $108m

NPV8 Post Tax and Royalties US $633m US $612m

NPV10 Post Tax and Royalties US $445m US $444m

IRR Post Tax and Royalties 21% 22%

Operating Margin 64% 62%

Payback Period (from start of operations) 5 years 5 years

Table 2: Financial Analysis of Project Update at current rare earth prices compared to the BFS price assumptions

*Total pre production Capex, for Ngualla mine and Multi-stage Processing Facility and Tees Valley refinery combined.#Material assumptions are as per BFS and Ore Reserve ASX Announcements of 12 April 2017 except where indicated in this report.

The average annual operating margin, NPV10, IRR and payback period are all close to the BFS analysis despite the BFS assuming 19% higher NdPr prices. The solid project economics provides support for the Company’s focus to progress Ngualla towards production in time for the increased demand for NdPr from electric vehicles.

Compliance InformationThe increased production rate is based on the Ngualla Ore Reserve in the Appendix (and ASX Announcement “Ngualla Rare Earth Project – Updated Ore Reserve” of 12 April 2017), which together with the BFS summarises the Material Assumptions underpinning this financial analysis, which continue to apply and have not materially changed except where indicated in this announcement. A revised mine plan was not generated for the Project Update. The increased production rate is based on a compressed BFS mine schedule, which would reduce the operational life to 26 years, from 31 years at BFS.

Peak will require new funding for its 75% share in the Ngualla Rare Earth Project in order to achieve the stated finan-cial outcomes, which will result in some dilution of existing shares, the quantum of which will depend on the final debt to equity ratio of the financing package that is yet to be arranged.

For

per

sona

l use

onl

y

4 ENABLING LOW CARBON TECHNOLOGIES

Quarterly Activities Report December 2017

Figure 1: Annual operational cash flow (EBITDA) over the 26 year life of the Project

Peak CEO meets with Tanzanian OfficialsSince the changes to the mining legislation in Tanzania in July this year (see ASX Announcement dated 31 July 2017 and titled “Tanzanian Legislative Changes”) Peak’s senior executives have spent considerable time in Tanzania continuing to develop the excellent relationship the Company enjoys with the Tanzanian Government and other stakeholders. On his visit in December, Rocky Smith, Peak’s CEO met with senior officials in the new Ministry of Minerals obtaining further clarity on the implementation of the new legislation as well as the timing of Peak’s pending Mining Licence applica-tion (see ASX Announcement dated 6 September 2017 and titled “Peak lodges Special Mining Licence application for Ngualla”).

Rocky Smith, Peak’s CEO commented “We are extremely encouraged by our ongoing interactions with the Tanzanian Government. There is clear recognition by officials of the uncertainty that the announcement of the legislative changes created, and they are working pro-actively to demonstrate that Tanzanian is still an attractive investment destination and open for business.”

“We gained the following key insights from our recent meetings with the Ministry of Mines: There is a desire to kick start the mining industry and restore investor confidence and Special Mining Licence (SML) applications will be given priority by the Mining Commission. The Ministry confirmed that Peak’s SML application is one of only three current applications.”

“The Mining Commission will assess project requirements on their own merits on a case by case basis. Early indica-tions from the Ministry are that they understand that the export of the rare earth concentrate to Teesside is a practical requirement for the viability of the Ngualla project. Member-ship of the new Commission is expected to be announced by the end of the year.”

“These reassurances provide me with confidence that we can look forward to seeing some substantive progress on Ngualla’s final project development permitting in early 2018.”

Additional Peak meetings included; Member of Parliament for Songwe Province which incorporates Ngualla, the Regional and District Commissioners for Songwe, the Chairman of the Geological Survey who was deeply involved with the recent Acacia negotiations, and many other government officials and bureaucrats. Without exception they have all expressed sup-port for Ngualla, acknowledging the substantial benefits that will flow to Tanzania and its people through the development of Ngualla.

Figure 2: Rocky Smith CEO and Lucas Stanfield GM Development meeting with the Deputy Minister for Minerals Hon. Stanslaus Nyongo MP

For

per

sona

l use

onl

y

5 ENABLING LOW CARBON TECHNOLOGIES

Quarterly Activities Report December 2017

Trenching of Fluorspar Mineralisation ContinuesTrenching operations for fluorspar mineralisation as per Figure 1 below was completed in the Quarter. Trenches were completed in the northern area of the fenite alteration rim in October where previous sampling identified rare earth and fluorspar mineralisation at surface up to 53m at 2.37% REO and 66m at 31% fluorspar. Westward extensions to trenches NCS015 to NCS014 were completed in November. Samples have been collected from site and are on route to SGS for preparation prior to export to Perth for analysis.

Figure 2: Fluorspar sampling map.

New Minister of Minerals Encourages Mining InvestmentA new Minister of Minerals, the Honourable Angellah Kairuki, has been appointed. At the swearing in ceremony for new cabinet ministers in Dar es Salaam on Monday, 9 October 2017 the Honourable Minister stated that her top priori-ty is to improve relations with investors with a view to ensuring that the mining sector as a whole contributes to its full capacity to Tanzania’s economic growth.

The Minister also took the opportunity to reassure that the prevailing investment climate in Tanzania is truly inves-tor-friendly and that the Tanzania government remains ready to receive prospective investors with an open mind. (ASX Announcement “New Minister appointment and Regional support for Ngualla” of 16 October 2017).

The appointment of the Minister is a positive move towards the practical implementation of the new mining laws, which will enable the progression of the Company’s SML application. The Company looks forward to working with the Minister to develop the Ngualla Project on a win - win basis for all stakeholders.

For

per

sona

l use

onl

y

6 ENABLING LOW CARBON TECHNOLOGIES

Quarterly Activities Report December 2017

Pricing UpdateAfter an impressive price rally in 2017, mainly caused by the Chinese government crackdown activities on illegal mining and non-compliant environmental operations before its 19th CPC National Congress in October 2017, the NdPr price peaked with a 103% increase compared to January 2017. Following this prices have entered into an expected consol-idation phase. However, it provided a glimpse of the potential rare earth pricing landscape should the Chinese rare earth industry adhere to its own government's directives.

The NdPr domestic price in China peaked at 525 RMB/kg (US$ 80.07/kg, 14/09/2017 Asian Metal all prices incl. 17% VAT) in the first and second week of September 2017, and dropped then within a few months to a low of 265 RMB/kg (US$ 40.04/kg) on the 11 December 2017.

After hitting the bottom of 265 RMB/kg the prices bounced back, closing the year 2017 at 305 RMB/kg. Since then the price has continued to increase further reaching 335 RMB/kg (US$ 52.36/kg) by the end of January 2018.

Pricing Tables

#Target price which is required to realise similar financial performance as communicated in the BFS incorporating the process improvements of the “Process optimisation study boosts Ngualla’s operating margin” dated 28 August 2017

Figure 3: NdPr Prices China in US$/kg over the past 14 months. Source: Asian Metal (China Domestic)

Figure 4: Recent rare earth price increases in context with long term trends

For

per

sona

l use

onl

y

7 ENABLING LOW CARBON TECHNOLOGIES

Quarterly Activities Report December 2017

We anticipate that prices will stay approximately at this level until after Chinese New Year commencing on 16th of Feb-ruary. Most of the companies will get back to business by the 5th of March. This is when we expect that NdPr prices and volume gain new momentum. Traditionally after Chinese New Year trading activities ramp up and market partic-ipants will look to replenish their inventories, which is anticipated to support further price increase especially for NdPr.

A positive short-term element on the pricing could be the Chinese governmental stockpiling program. The market is waiting for direction from the government in regards to their next round of rare earth strategic stockpiling purchase program. Based on market rumours the purchase has been postponed several times since September 2017 and the next one is expected in the first half year in 2018. If this occurs, it is perceived as a supporting and accelerating ele-ment for further price increases.

The MarketElectric mobility had another record year in 2017. First preliminary sales reports for 2017 were published and show again an outstanding performance. The global plug-in vehicle sales reached 1.2 million registered units, 57 % higher than 2016. These include all global BEV and PHEV passenger cars sales, light trucks in USA/Canada and light commer-cial vehicle in Europe. In 2017, 66 % of sales were pure electric (BEV) and 34 % were plug-in hybrids (PHEV). All-electric vehicles have been winning share, as the BEV-friendly Chinese market continues to win importance.

That this trend will continue is underpinned by the latest announcements that the global automotive industry committed to invest so far US$ 90 billion in electrification, future vehicle platforms and new models. Recent positive announcement on the legislation side from China - as one of the biggest single automotive markets globally - will en-sure that this momentum will continue as already proven by recent announcement for example from Ford, Toyota, Infiniti, and others.

Figure 5: Monthly Plug-in Vehicle Sales

Figure 6: Plug-in Sales and % Growth

For

per

sona

l use

onl

y

8 ENABLING LOW CARBON TECHNOLOGIES

Quarterly Activities Report December 2017

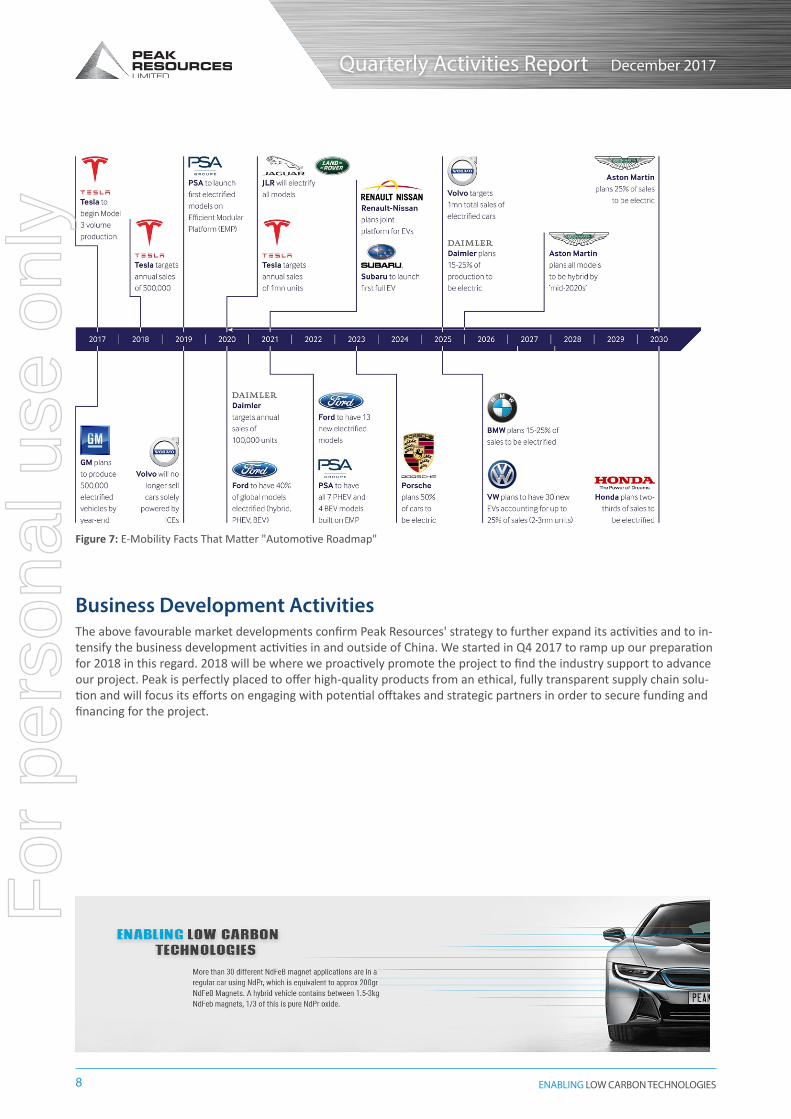

Business Development ActivitiesThe above favourable market developments confirm Peak Resources' strategy to further expand its activities and to in-tensify the business development activities in and outside of China. We started in Q4 2017 to ramp up our preparation for 2018 in this regard. 2018 will be where we proactively promote the project to find the industry support to advance our project. Peak is perfectly placed to offer high-quality products from an ethical, fully transparent supply chain solu-tion and will focus its efforts on engaging with potential offtakes and strategic partners in order to secure funding and financing for the project.

Figure 7: E-Mobility Facts That Matter "Automotive Roadmap"

For

per

sona

l use

onl

y

9 ENABLING LOW CARBON TECHNOLOGIES

Quarterly Activities Report December 2017

Corporate Social Responsibility ProgramsThe Company places great importance on the active and positive relationship it maintains with the communities in which it operates and continues its committment to assisting with their improvement according to the priorities identi-fied by those communities and the District authorities.

Work on the construction of two classrooms and a teacher’s office at Itiziro village located 1km south of Ngwala has been completed for the year. The buildings have had the tin roofs installed along with the ceiling blundering. Work will resume next year when the camp reopens.

Figure 8: Construction of two classrooms and a teacher’s office at the Itiziro Primary School near Ngwala.

CorporateOrganisational Changes

The Company was pleased to advise that Mr. Rocky Smith accepted the role of Chief Executive Officer following his appointment as interim CEO in the September quarter.

Rocky is one of the very few western mining executives who possess an in-depth knowledge of the rare earth industry, including the supply chain, coupled with extensive experience with start-up and operations of complex chemical process facilities including rare earths. Rocky was formerly Managing Director for Molycorp’s Mountain Pass Rare Earth operations. The fact that the Company can attract and retain an executive of Rocky’s calibre is a further validation of the strong fundamentals of the Ngualla Project.

Rocky Smith

Rocky’s current focus is to deliver the near-term objectives of Peak’s strategy to progress the project to development to meet the expected upsurge in demand for the neodymium/praseodymium magnet metals from the Electric Vehicle revolution. Key work streams include:

• Finalisation of permitting and grant of the mining license application for Ngualla through active engagement with the Tanzanian Government and other stakeholders;

• Advancing offtake discussions with potential customers;

• Develop strategic partnerships that will assist our working relationship with the Tanzanian government;

• Advance discussions with potential financers; and

• Progress opportunities identified which may further improve the already robust economics of the Ngualla Project.

For

per

sona

l use

onl

y

10 ENABLING LOW CARBON TECHNOLOGIES

Quarterly Activities Report December 2017

Mr. Lucas Stanfield, Peak’s General Manager of Development took over responsibility for the Company’s activities in Tanzania. Lucas was previously the manager for the Com-pany’s scoping, preliminary feasibility, refinery location selection and bankable feasi-bility studies. During this time he has spent a considerable amount of time in Tanzania representing the Company and has an excellent working relationship with all stakehold-ers in country and is very well placed to further advance the Ngualla Project.

Lucas has been with Peak for over 5 years. His background is as a mining engineer with over 15 years’ experience in mining and project management in Australia, Africa, and the United Kingdom. He graduated with a Bachelor of Engineering (Mining) from the University of New South Wales in 1998.Lucas Stanfield

Board of Directors

Mr Peter Harold ceased as Chairman effective 31 December 2017. Mr Jonathan Murray will fill the role of interim Non-Executive Chairman whist the Company finalises the recruitment process already underway.

In addition, Mr Darren Townsend completed the transition from Managing Director to Non-executive Director on confirmation of Mr Rocky Smith’s appointment as CEO noted above. Mr Dave Hammond also ceased employment, as Technical Director, with the Company in early November 2017 following Mr Lucas Stanfield assuming full responsibility for the Company’s activities in Tanzania.

Annual General Meeting (AGM)

The Company held its AGM on 29 November 2017 with all resolutions put to the meeting passed on a show of hands.

Capital Raising ActivitiesRenounceable Entitlement Offer

In October 2017 the company closed a pro-rata renounceable Entitlement issue of one (1) fully paid ordinary shares in the capital of the Company for every eight (8) shares held and shortly thereafter, in November 2017, closed placement of the shortfall. A total of 68,431,891 new shares were issued at $0.04 per share raised $2,737,276 (before costs). In addition a total of 81,215,888 free attaching options with an exercise price of $0.06, exercisable by 1 November 2018 were issued on a 1 for 2 basis to participants in the Entitlement issue, shortfall placement and September 2017 place-ment (69,215,888 options), and to consultants for services provided in connection with the Company’s capital raising activities (12,000,000 options).

Appian Debt Repayment

Subsequent to completion of the Company’s capital raisings and pursuant to the terms of the loan facility provided to the Company by Appian, approximately US$1.5 million was applied towards repayment of the loan. Following repay-ment, the outstanding loan balance at end of the Quarter was approximately US$2.2 million. The loan facility matures in September 2019.

For

per

sona

l use

onl

y

11 ENABLING LOW CARBON TECHNOLOGIES

Quarterly Activities Report December 2017

Corporate Structure and Cash at Hand

The corporate structure as at 31 December 2017 was:

* From 01 January 2017 to 31 December 2017 ** Average from 1 October 2017 to 31 December 2017 # expired unexercised 5 January 2018.^ PAM, 75% PEK ownership, also retained cash at bank of US$9k at the end of the Quarter.

Competent Person's Statements:

The information in this report that relates to exploration results is based on information compiled and/or reviewed by David Hammond, who is a

Member of the Australasian Institute of Mining and Metallurgy. David has sufficient experience which is relevant to the style of mineralisation and

type of deposit under consideration and the activity which he is undertaking to qualify as a Competent Person in terms of the Australasian Code for

Reporting of Exploration Results, Mineral Resources and Ore Reserves (the JORC Code, 2012 edition). David Hammond consents to the inclusion in

the report of the matters based on his information in the form and contest in which it appears.

The information in this report that relates to infrastructure, project execution and cost estimating is based on information compiled and / or

reviewed by Lucas Stanfield who is a Member of the Australasian Institute of Mining and Metallurgy. Lucas Stanfield is the General Manager -

Development for Peak Resources Limited and is a Mining Engineer with sufficient experience relevant to the activity which he is undertaking to be

recognised as competent to compile and report such information. Lucas Stanfield consents to the inclusion in the report of the matters based on his

information in the form and context in which it appears.

ASX: PEK

Ordinary Shares on Issue: 615.9 million

Cash at hand: $2.8 million^ (Peak Resources Limited only)

Appian Debt (due September 2019): US$2.2 million

52 week range: 3.4c – 13.0c*

Market Cap: $32.6m (at 5.3c)

Rocky Smith, Chief Executive Officer

PEKOB Listed $0.06 1 November 2018Options on Issue: 81.2 million

Unlisted Performance Rights: 8 million#

Unlisted Options outstanding: 20.6 million#

(exercise prices A$0.15 to A$0.55)

Liquidity: 1.220 million shares per trading day(average over 3 months**)

For

per

sona

l use

onl

y

12 ENABLING LOW CARBON TECHNOLOGIES

Quarterly Activities Report December 2017

Summary of Mining Tenements and Areas of InterestAs at 31 December 2017

Project Tenement End of September 2017 Quarter

End of December 2017 Quarter

Status Arrangement/Comment

Mikuwo PL 9157/2013 75% 75% GrantedHeld by 100% Tanzanian associate company PR NG Minerals Ltd

Mlingi PL10897/2016 75% 75% GrantedHeld by 100% Tanzanian associate company PR NG Minerals Ltd

Ngualla SML/00601/2017 75% 75% PendingHeld by 100% Tanzanian associate company PR NG Minerals Ltd

For

per

sona

l use

onl

y

13 ENABLING LOW CARBON TECHNOLOGIES

Quarterly Activities Report December 2017

Appendix 5BMining exploration entity and oil and gas exploration entity quarterly report

+ See chapter 19 for defined terms1 September 2016 Page 1

+Rule 5.5

Appendix 5B

Mining exploration entity and oil and gas exploration entity quarterly report

Introduced 01/07/96 Origin Appendix 8 Amended 01/07/97, 01/07/98, 30/09/01, 01/06/10, 17/12/10, 01/05/13, 01/09/16

Name of entity

PEAK RESOURCES LIMITED

ABN Quarter ended (“current quarter”)

72112546700 DECEMBER 2017

Consolidated statement of cash flows Current quarter $A’000

Year to date(6 months)

$A’000

1. Cash flows from operating activities- -1.1 Receipts from customers

1.2 Payments for

- -(a) exploration & evaluation

(b) development (602) (1,229)

(c) production - -

(d) staff costs (net of development allocations)

(158) (432)

(e) administration and corporate costs (443) (555)

(f) development costs recovered 152 291

(g) administration costs recovered 11 32

1.3 Dividends received (see note 3) - -

1.4 Interest received 6 8

1.5 Interest and other costs of finance paid (141) (291)

1.6 Income taxes paid - -

1.7 Research and development refunds 562 562

1.8 Other (provide details if material) - -

1.9 Net cash from / (used in) operating activities

(613) (1,614)

2. Cash flows from investing activities

(1) (2)

2.1 Payments to acquire:

(a) property, plant and equipment

(b) tenements (see item 10) - -

For

per

sona

l use

onl

y

14 ENABLING LOW CARBON TECHNOLOGIES

Quarterly Activities Report December 2017

Appendix 5BMining exploration entity and oil and gas exploration entity quarterly report

+ See chapter 19 for defined terms1 September 2016 Page 2

Consolidated statement of cash flows Current quarter $A’000

Year to date(6 months)

$A’000(c) investments in associate companies (1,708) (1,708)

(d) other non-current assets - -

2.2 Proceeds from the disposal of:

3 3(a) property, plant and equipment

(b) tenements (see item 10) - -

(c) investments - -

(d) other non-current assets - -

2.3 Cash flows from loans to / from other entities – associate companies

1,273 891

2.4 Dividends received (see note 3) - -

2.5 Other (provide details if material)

2.6 Net cash from / (used in) investing activities

(433) (816)

3. Cash flows from financing activities2,737 5,5373.1 Proceeds from issues of shares

3.2 Proceeds from issue of convertible notes - -

3.3 Proceeds from exercise of share options - -

3.4 Transaction costs related to issues of shares, convertible notes or options

(380) (385)

3.5 Proceeds from borrowings – Appian loan 127 262

3.6 Repayment of borrowings (1,943) (1,943)

3.7 Transaction costs related to loans and borrowings

(356) (356)

3.8 Dividends paid - -

3.9 Other – Restricted cash for debt repayment 376 -

3.10 Net cash from / (used in) financing activities

561 3,115

4. Net increase / (decrease) in cash and cash equivalents for the period

3,287 2,1174.1 Cash and cash equivalents at beginning of

period

4.2 Net cash from / (used in) operating activities (item 1.9 above)

(613) (1,614)

4.3 Net cash from / (used in) investing activities (item 2.6 above)

(433) (816)

4.4 Net cash from / (used in) financing activities (item 3.10 above)

561 3,115

For

per

sona

l use

onl

y

15 ENABLING LOW CARBON TECHNOLOGIES

Quarterly Activities Report December 2017

Appendix 5BMining exploration entity and oil and gas exploration entity quarterly report

+ See chapter 19 for defined terms1 September 2016 Page 3

Consolidated statement of cash flows Current quarter $A’000

Year to date(6 months)

$A’0004.5 Effect of movement in exchange rates on

cash held- -

4.6 Cash and cash equivalents at end of period

2,802 2,802

5. Reconciliation of cash and cash equivalentsat the end of the quarter (as shown in the consolidated statement of cash flows) to the related items in the accounts

Current quarter$A’000

Previous quarter$A’000

5.1 Bank balances 757 3,242

5.2 Call deposits 2,045 45

5.3 Bank overdrafts - -

5.4 Other (provide details) - -

5.5 Cash and cash equivalents at end of quarter (should equal item 4.6 above)

2,802 # 3,287#

#figure excludes cash at end of the Quarter retained by Peak’s majority (75%) owned associate company Peak African Minerals (PAM). PAM had cash at bank at the end of Quarter of US$9k(previous quarter US$10k).

6. Payments to directors of the entity and their associates Current quarter$A'000

6.1 Aggregate amount of payments to these parties included in item 1.2 312

6.2 Aggregate amount of cash flow from loans to these parties included in item 2.3

-

6.3 Include below any explanation necessary to understand the transactions included in items 6.1 and 6.2

6.1 includes salaries (including annual leave and long service leave entitlements paid out on cessation of employment), directors fees paid to Directors and payments to Steinepreis Paganin Lawyers & Consultants, an entity related to Non-executive Director Jonathan Murray.

7. Payments to related entities of the entity and their associates

Current quarter$A'000

7.1 Aggregate amount of payments to these parties included in item 1.2 -

7.2 Aggregate amount of cash flow from loans to these parties included in item 2.3

-

7.3 Include below any explanation necessary to understand the transactions included in items 7.1 and 7.2

For

per

sona

l use

onl

y

16 ENABLING LOW CARBON TECHNOLOGIES

Quarterly Activities Report December 2017

Appendix 5BMining exploration entity and oil and gas exploration entity quarterly report

+ See chapter 19 for defined terms1 September 2016 Page 4

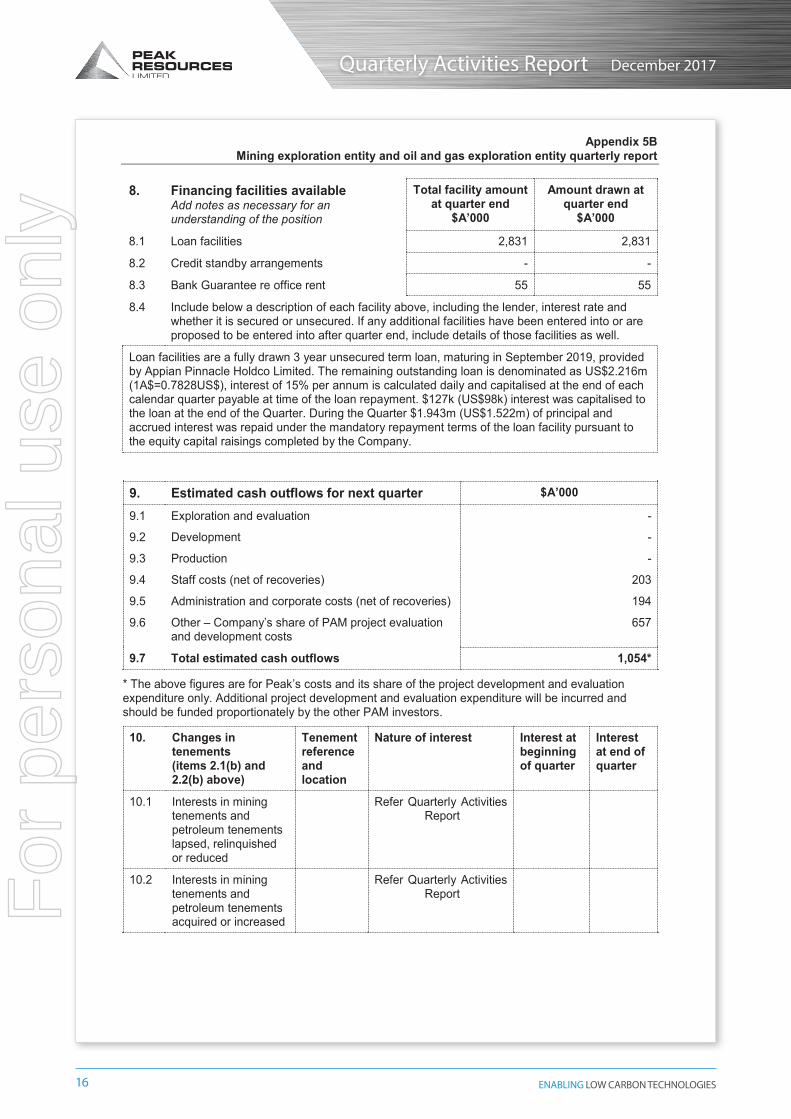

8. Financing facilities availableAdd notes as necessary for an understanding of the position

Total facility amount at quarter end

$A’000

Amount drawn at quarter end

$A’000

8.1 Loan facilities 2,831 2,831

8.2 Credit standby arrangements - -

8.3 Bank Guarantee re office rent 55 55

8.4 Include below a description of each facility above, including the lender, interest rate and whether it is secured or unsecured. If any additional facilities have been entered into or are proposed to be entered into after quarter end, include details of those facilities as well.

Loan facilities are a fully drawn 3 year unsecured term loan, maturing in September 2019, provided by Appian Pinnacle Holdco Limited. The remaining outstanding loan is denominated as US$2.216m(1A$=0.7828US$), interest of 15% per annum is calculated daily and capitalised at the end of each calendar quarter payable at time of the loan repayment. $127k (US$98k) interest was capitalised to the loan at the end of the Quarter. During the Quarter $1.943m (US$1.522m) of principal and accrued interest was repaid under the mandatory repayment terms of the loan facility pursuant to the equity capital raisings completed by the Company.

9. Estimated cash outflows for next quarter $A’000

9.1 Exploration and evaluation -

9.2 Development -

9.3 Production -

9.4 Staff costs (net of recoveries) 203

9.5 Administration and corporate costs (net of recoveries) 194

9.6 Other – Company’s share of PAM project evaluation and development costs

657

9.7 Total estimated cash outflows 1,054*

* The above figures are for Peak’s costs and its share of the project development and evaluation expenditure only. Additional project development and evaluation expenditure will be incurred and should be funded proportionately by the other PAM investors.

10. Changes in tenements(items 2.1(b) and 2.2(b) above)

Tenement reference and location

Nature of interest Interest at beginning of quarter

Interest at end of quarter

10.1 Interests in mining tenements and petroleum tenements lapsed, relinquished or reduced

Refer Quarterly Activities Report

10.2 Interests in mining tenements and petroleum tenements acquired or increased

Refer Quarterly Activities ReportF

or p

erso

nal u

se o

nly

17 ENABLING LOW CARBON TECHNOLOGIES

Quarterly Activities Report December 2017

Appendix 5BMining exploration entity and oil and gas exploration entity quarterly report

+ See chapter 19 for defined terms1 September 2016 Page 5

Compliance statement

1 This statement has been prepared in accordance with accounting standards and policies which comply with Listing Rule 19.11A.

2 This statement gives a true and fair view of the matters disclosed.

Sign here: ......Graeme Scott.......................... Date: ...29 January 2018...............Company secretary

Print name: ....Graeme Scott............................

Notes1. The quarterly report provides a basis for informing the market how the entity’s activities have been

financed for the past quarter and the effect on its cash position. An entity that wishes to disclose additional information is encouraged to do so, in a note or notes included in or attached to this report.

2. If this quarterly report has been prepared in accordance with Australian Accounting Standards, the definitions in, and provisions of, AASB 6: Exploration for and Evaluation of Mineral Resources and AASB 107: Statement of Cash Flows apply to this report. If this quarterly report has been prepared in accordance with other accounting standards agreed by ASX pursuant to Listing Rule 19.11A, the corresponding equivalent standards apply to this report.

3. Dividends received may be classified either as cash flows from operating activities or cash flows from investing activities, depending on the accounting policy of the entity.

For

per

sona

l use

onl

y