r e s t r i c t e d - army · r e s t r i c t e d r e s t r i c t e d i ... 3-4 significant...

TRANSCRIPT

R E S T R I C T E D

R E S T R I C T E D i

GENERAL HEADQUARTERS ARMED FORCES OF THE PHILIPPINES

OFFICE OF THE CHIEF OF STAFF Camp General Emilio Aguinaldo, Quezon City

25 September 2007

SUBJECT: Promulgation TO: All Concerned

1. The Philippine Army Comptrollership Manual, PAM 6-00, provides the concepts and procedures for the efficient management of Army resources. The manual also provides relevant principles and information on Army Comptrollership.

2. This manual was reviewed by the PA Capability Development

Board and approved by the Commanding General, Philippine Army as official reference on Army Comptrollership.

3. This manual is hereby promulgated for the information and

guidance of all concerned effective this date.

HERMOGENES C ESPERON JR General AFP

R E S T R I C T E D

R E S T R I C T E D ii

R E S T R I C T E D

R E S T R I C T E D iii

COMMANDING GENERAL PHILIPPINE ARMY

Fort Andres Bonifacio, Metro Manila

FOREWORD

The PHILIPPINE ARMY COMPTROLLERSHIP MANUAL (PAM 6-00) is comprehensive reference that contains fundamental concepts and principles for the guidance of our personnel in the effective, efficient and ethical management of resources to accomplish the Army’s mission. The essentials of responsible comptrollership contained in the Manual were tested and validated to ensure effective implementation thereof.

This manual is hereby approved for use by the Philippine Army. I urge all our soldiers to adhere to the provisions of the Manual in

carrying out their respective organizational roles. I likewise encourage all our personnel to contribute to the improvement of this Manual by sending their recommendations to Doctrine Center, TRADOC, PA.

ROMEO P TOLENTINO Lieutenant General, AFP

R E S T R I C T E D

R E S T R I C T E D iv

R E S T R I C T E D

R E S T R I C T E D v

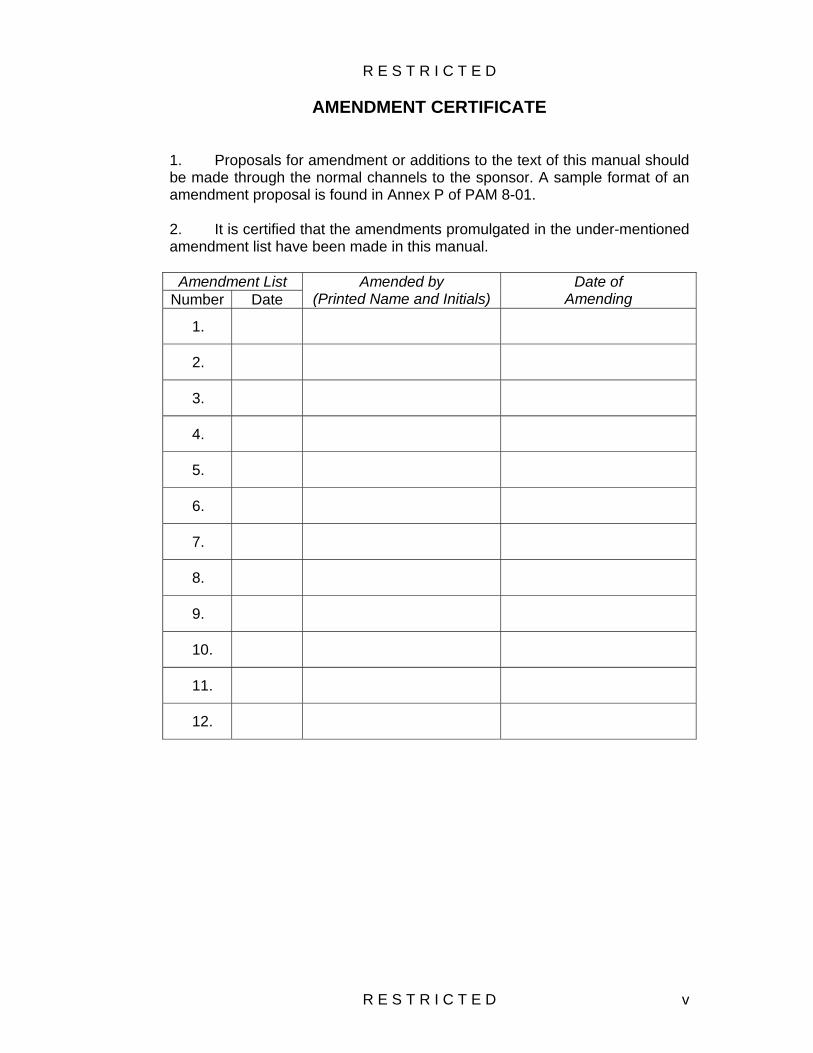

AMENDMENT CERTIFICATE 1. Proposals for amendment or additions to the text of this manual should be made through the normal channels to the sponsor. A sample format of an amendment proposal is found in Annex P of PAM 8-01. 2. It is certified that the amendments promulgated in the under-mentioned amendment list have been made in this manual.

Amendment List Amended by (Printed Name and Initials)

Date of Amending Number Date

1.

2.

3.

4.

5.

6.

7.

8.

9.

10.

11.

12.

R E S T R I C T E D

R E S T R I C T E D vi

R E S T R I C T E D

R E S T R I C T E D vii

PREFACE

The Army Comptrollership family intends to eliminate problem areas and come-up with corrective measures to improve the management of our limited resources. The development and eventual publication of the Army Comptrollership Manual aims to guide Army personnel to be effective, efficient, economical and ethical managers.

Relatedly, it is envisioned that Program Directors and Project Administrators shall serve as agent of change and take an active role in the proper management of comptroller-related services. All units/offices concerned are expected to be more aware in the proper administration and safeguarding of Army resources. Also, they shall be informed on how fund and/or property accountabilities, responsibilities and personal liabilities are incurred.

In effect, the Philippine Army as a trustee of government funds shall not only improve its resource management but also enhance its over-all image as a partner in the country’s socio-economic development through the efficient and effective implementation of its various programs and activities.

R E S T R I C T E D

R E S T R I C T E D viii

R E S T R I C T E D

R E S T R I C T E D ix

CONTENTS

Letter of Promulgation i Foreword iii Amendment Certificate v Preface vii Contents ix

Section Title Page CHAPTER 1 – ARMY COMPTROLLERSHIP

1-1 Introduction 1-1 1-2 Functions 1-2 1-3 Task and Responsibilities 1-2 1-4 The Comptroller Family 1-8 1-5 Program and Budget Advisory Committee (PBAC) 1-8 1-6 Comptrollership Principles and Concepts 1-8 1-7 Evolution of Comptrollership in the Army 1-11

CHAPTER 2- BUDGET AND FISCAL OPERATIONS

2-1 Overview 2-1 2-2 Budgeting Systems and Approaches 2-1 2-3 The Planning, Programming and Budgeting System

(PPBS) 2-2

2-4 Budget Process/Cycle 2-3 2-5 Budget Structure 2-9 2-6 Financial Support Programs 2-12

CHAPTER 3 – ACCOUNTING OPERATIONS

3-1 Overview 3-1 3-2 Accounting Process 3-2 3-3 New Government Accounting System (NGAS) 3-2 3-4 Significant Policies of the New Government

Accounting System (NGAS) 3-4

3-5 Books of Accounts 3-6 3-6 Accounting Registries 3-8 3-7 Statements/Reports Prepared Periodically 3-8 3-8 Flow of Claims 3-10 3-9 Procedures For the Granting and Liquidation of Cash

Advance (COA Cir 90-331 dtd 3 May 90) 3-12

3-10 Role of Accounting in the Procurement System 3-13 3-11 Accounting of Supplies 3-14 3-12 Property Accounting Reports 3-15

R E S T R I C T E D

R E S T R I C T E D x

CHAPTER 4 – MANAGEMENT CONTROL AND ANALYSIS

4-1 Overview 4-1 4-2 Auditing Concept 4-1 4-3 Types of Audit 4-2 4-4 Areas of Appraisal and Audit 4-4 4-5 Internal Auditing 4-5 4-6 Pre-Audit Operations 4-5 4-7 Program Performance Review and Assessment

Procedures (PPRA) 4-6

4-8 Post Audit 4-7 4-9 Determination of Persons Liable for Audit

Disallowances or Charges 4-7

CHAPTER 5 – ACCOUNTABILITY AND

LIQUIDATION

5-1 Overview 5-1 5-2 Persons Primarily and Secondarily Accountable for

Government Property 5-1

5-3 Fund Accountable Personnel 5-1 5-4 Sources of Fund Accountability 5-2 5-5 Acquisition of Accountability/Liability 5-2 5-6 Requirements to Clear/Settle Accountabilities incurred

while on Mission/Schooling 5-3

5-7 Acquisition of Property Accountability 5-4 5-8 Forms used in the Acquisition of Property 5-5 5-9 Clearing of Property Accountability 5-5 5-10 Account Liquidation 5-6 5-11 PA Accountability Board 5-7 5-12 Major Unit Accountability Board (UAB) 5-8 5-13 Transfer of Property Accountability and Responsibility 5-8 5-14 Relief from Fund/Property Accountability 5-12 5-15 Turn-over of Resources 5-15

ANNEXES

A Journal A-1 B Pre Closing Trial Balance B-1

Record of Changes Recommendation for Changes

R E S T R I C T E D

R E S T R I C T E D xi

R E S T R I C T E D

R E S T R I C T E D 1-1

CHAPTER 1 ARMY COMPTROLLERSHIP

Section 1-1 Introduction

Army Comptrollership refers to the command and staff function of managing army fund resources wherein the functions of budgeting and fiscal operations, accounting operations, internal auditing and management analysis are consolidated. Its goal is to achieve a correct translation of army objectives and functional programs into monetary terms. It aims to integrate plans and programs with balance and proportionate allocation of fund resources, account for funds allocated, and analyze the results for cost effectiveness. 1. Brief Historical Background. Prior to World War II, there existed a “Budget Statistics and Legislative Section” of the Headquarters Philippine Army. Its main function was to prepare the budget of the Philippine Army for submission to the Legislature, defend and justify the budget, and control expenditures of the appropriated funds.

In 1945, Budget Division, Army was created as a special division at Headquarters Philippine Army, and placed directly under the Chief of Staff, PA.

Upon the reorganization of the Philippine Army into the Armed Forces of the Philippines pursuant to Section 20, Executive Order No 389 dated 23 December 1950, the Budget Division was transferred by the Secretary of National Defense, Hon. Ruperto Kangleon, to the Office of the Secretary.

Then in 01 July 1957, PA Comptroller Division was again organized at Headquarters, Philippine Army pursuant to General Orders No 562, GHQ, AFP.

In 1970, the AFP Comptroller was redesignated to be one of the Joint Staffs of the AFP until it was finally renamed as the Office of the Deputy Chief of Staff for Comptrollership, J6 in July 1973. Accordingly, Philippine Army Comptroller Division was redesignated as G6 Division, PA.

Under Presidential Decree No 1, as implemented by LOI, GHQ, AFP

dated 8 Aug 1973, the Chief of Staff, AFP issued additional guidelines for the reorganization of the Comptroller Offices with the objective of achieving the integration of comptrollership functions of budgeting, accounting, management evaluation, management information and fund disbursement service in the AFP. Likewise, the Comptroller was to exercise functional supervision over the Finance Centers.

R E S T R I C T E D

R E S T R I C T E D 1-2

Section 1-2 Functions 2. G6 Division and its Functions. The Philippine Army is one of the budgetary agencies of the Armed Forces of the Philippines. The Commanding General, Philippine Army is directly responsible for the management of the financial resources of the Philippine Army. He is assisted by the G6 Division that relieves him of the details of financial management functions in attaining the Command’s objectives.

At the top of G6 Division is the Assistant Chief of Staff for Comptrollership, G6 who is the financial adviser of the Commanding General, Philippine Army. The G6 Division is composed of six (6) Branches which are created to accomplish the different tasks and responsibilities of the office. The function of G6 Division is to provide staff advice and assistance to the Commanding General, Philippine Army and his staff on budgetary and fiscal matters, proper utilization of resources and management.

The G6 or Comptroller Division also maintains internal and external relationship with GHQ and public and private financial agencies. It receives guidance from GHQ on comptrollership matters and likewise gives direction to other G-Staff Program Directors and Major Units Comptroller offices on financial management. It renders periodic reports to GHQ. Guidance and coordination is also maintained with the Department of Budget and Management, the Commission on Audit and other financial agencies. It also exercises functional supervision over the Finance Center.

Section 1-3 Task and Responsibilities

3. Tasks and Responsibilities:

a. Formulates plans and policies relative to budgeting, financial management, accounting systems and services and management control systems.

b. Exercises staff supervision over the determination of budgetary requirements of the Philippine Army.

c. Assists the Commanding General, PA in the presentation of Budget Estimates before administrative and legislative bodies.

d. Supervises financial operations, management control, and accounting systems during the implementation of the budget.

e. Evaluates the accomplishment of the mission through a system

of review, analysis and evaluation of operating programs of the Army.

R E S T R I C T E D

R E S T R I C T E D 1-3

f. Provides financial management information and other professional management services to CG, PA.

g. Exercises functional supervision over the Finance Center, PA. 4. G6 Organization. The G6 Division is organized as follows:

a. Office of the AC of S, G6 b. Office of the Deputy c. Office of the Executive Officer

d. Administrative Branch

e. Budget and Fiscal Operations Branch

f. Modernization Branch g. Management Branch

h. Pre-Audit Branch

i. Accounting Services

5. Duties and Responsibilities

a. Assistant Chief of Staff for Comptrollership, G6, PA:

1) Acts as the principal Staff to the CG, PA on:

(a) Financial strategies and fiscal policies.

(b) Non-tactical operations structures and systems.

(c) Financial resources allocations and controls.

(d) External relations with public and private financial agencies and entities.

2) Acts as Vice Chairman of the Program and Budget Advisory Committee (PBAC).

3) Has functional supervision over the Finance Center, Philippine Army.

b. Deputy:

1) Assists the AC of S, G6 in the performance of his duties.

R E S T R I C T E D

R E S T R I C T E D 1-4

2) Acts on all matters requiring immediate action in the absence of AC of S, G6.

3) Administers the Maintenance Operating Expenses (MOE) of the office.

4) Serves as Vice Chairman of the Program Budget Advisory Committee Working Group (PBAC WG).

c. Executive Officer:

1) Assists the AC of S, G6 in the internal administration of the office by directing, supervising and coordinating the activities of the different branches.

2) Monitors OG6 inter-staff requirements particularly those activities requiring lateral coordination among the branches.

3) Reviews staff actions to ensure that they are adequate and coordinated to produce the intended actions of the AC of S for Comptrollership, G6.

4) Formulates and announces staff policies.

5) Ensures that AC of S for Comptrollership, G6 and the branch chiefs are informed on matters affecting the office.

6) Performs other related functions as directed.

d. Administrative Branch:

1) Responsible for the internal administration and security of the Division.

2) Provides for the supply, motor/vehicular and other operating requirements of the Division.

3) Performs personnel functions for organic personnel including pay and allowance requirements.

4) Receives, routes, dispatches and/or files all communications going in and out of the Division.

5) Provides logistical support to special activities being conducted/hosted by the Division.

R E S T R I C T E D

R E S T R I C T E D 1-5

e. Budget and Fiscal Operations Branch:

1) Prepares the Annual Budget Proposal, Work and Financial Plan and Special Budget in coordination with the different Program Directors.

2) Formulates financial strategies and initiates action to secure funds for PA.

3) Acts as PBAC & PA Comptroller Board Secretariat and assists in the preparation of Quarterly Program of Expenditures for approval of CG, PA.

4) Releases funds in accordance with the approved Program of Expenditures in coordination with the Program Directors.

5) Records and monitors Notices of Cash Allocation (NCA) and releases Notices of Transfer of Allocation (NTA).

6) Prepares fiscal policies and directives and maintains fiscal controls for appropriated/non-appropriated funds.

7) Maintains statistics on budget and fiscal matters.

8) Maintains harmonious relations with other public and private financial agencies.

f. Modernization Branch:

1) Provides technical assistance of G6 in the exercise of his functions as Chairman, Budget and Finance Committee, PA Modernization Board.

2) Prepares and evaluates budgetary estimates/reports concerning the PA Modernization and BCDA Programs.

3) Prepares annual budgetary requirements of the PA Modernization and BCDA Programs in coordination with the Budget and Fiscal Branch, OG6.

4) Formulates and implements strategies to leverage limited

Army resources to maximize benefits that could be derived from the Modernization and BCDA programs.

5) Prepares financial action plans for the implementation of the Modernization and BCDA Programs.

6) Prepares budgetary implications of multi-year contracts to specify yearly cash flow requirements, interest payments and operational requirements of the Modernization Program.

R E S T R I C T E D

R E S T R I C T E D 1-6

7) Develops and trains personnel to be capable of

evaluating, analyzing and reviewing project proposals involving big-ticket projects.

8) Develops systems and procedures within the Army for the management, recording, accounting, disbursement and monitoring of the AFPMATF.

9) Performs other tasks as may be directed in connection with the planning, programming, and implementation of the PA Modernization.

g. Management Branch:

1) Formulates/revises management policies, procedures

and regulations on the effective and efficient utilization of Command resources.

2) Conducts research and prepares staff studies or position papers on comptrollership matters.

3) Performs comprehensive internal audit to provide check and balance in resource utilization.

4) Evaluates, reviews and analyzes audit reports for the purpose of improving and strengthening areas where deficiencies and weaknesses are observed in so far as resource management is concerned.

5) In-charge of Command and Army Comptrollership Program Performance Review and Assessment (PPRA).

6) Maintains records of personnel with money and/or property accountabilities and institutes action for the immediate liquidation of above accountabilities.

7) Prepares periodic reports on the aging, liquidation and current balances of cash advances of active and inactive accountable personnel.

8) Issues clearances or statement of accounts to support bond applications; retirement, death benefits, separation; promotion, reenlistment, and all other legal claims of military and civilian personnel.

9) Performs quasi-judicial function of Philippine Army Accountability Board (PAAB).

10) Provides computer-related services to different branches of the Division.

R E S T R I C T E D

R E S T R I C T E D 1-7

h. Pre-Audit Branch:

1) Determines if the proposed expenditure is for a purpose in compliance with the appropriation law and other laws and regulations.

2) Assures that sufficient funds are available to enable payment of the disbursement voucher.

3) Determines if the proposed expenditure is reasonable and if the unexpended balance of the appropriation to which it would be charged to is sufficient to cover all probable costs.

4) Determines if the transaction is approved by proper authority and duly supported by authentic underlying evidences.

5) Inspects supplies/materials delivered as to quantity and quality as specified in the Purchase Order/Work Order.

6) Conducts pre/post repair inspection of all PA facilities/equipment in coordination with other technical services.

7) Conducts inspection of deliveries of all procured items of the PA.

i. Accounting Services:

1) Renders technical advice to the Command on financial and accounting matters thru the Comptroller.

2) Coordinates all accounting activities of the Philippine Army to insure that policies, rules and regulations in the proper disbursement of funds are strictly observed.

3) Prepares and submits financial statements and accounting reports as required by the Agency, GHQ, AFP, Department of Budget and Management, Bureau of Treasury and the Commission on Audit.

4) Maintains basic accounting records of financial transactions of the Army.

Section 1-4 The Comptroller Family

The Comptroller Family is made up of the G6 Division at HPA and all other Comptroller Offices PA-wide. All major subordinate units particularly the Infantry Divisions and Engineer Brigades have comptroller offices which form part of the G6 family.

R E S T R I C T E D

R E S T R I C T E D 1-8

Subordinate comptroller offices are organized just like the G6 Division. It has a budget and fiscal section; management and pre-audit sections for check and balance. Field Accounting Units servicing field units nationwide remains an integral part of Accounting Services, G6 Division.

In short, the AC of S for Comptrollership, G6 provides the overall control on the Financial Management System. Direction is made thru the Major Subordinate Units’ Comptrollers while control is made thru the Field Accountants.

Section 1-5 Program and Budget Advisory Committee (PBAC)

To ensure coordinated effort of the Program Directors, the Program and Budget Advisory Committee (PBAC) is organized to over-see all the activities of the Command. Each PBAC member provides the Committee with complete information regarding his area of primary responsibility and interest. The functions of the PBAC, are the following:

a. Assists the commanders in coordinating and integrating, and programming and budgeting activities.

b. Recommends policies, objectives and work costs in accordance with the current program and priority guidance.

c. Establishes rational balance between objectives and resources.

d. Reviews and integrates the Operating Program and Budget (OPB).

e. Reviews the results of operations and recommends revision in the Operating Program and Budget to maintain an optimum balance between resources and objectives.

Section 1-6 Comptrollership Principles and Concepts The Comptrollership principles aim to provide a handy and ready reference of the basic knowledge used in managing the Army’s financial resources. These include the following:

a. Program Director - Project Administrator. The Program Director

– Project Administrator Concept establishes the fundamental responsibilities of the planners and the implementers. The members of the general staff shall function as program directors and are responsible to provide staff supervision on the development, execution, review and analysis of the operating program of the Command. These Program Directors are primarily involved in objective

R E S T R I C T E D

R E S T R I C T E D 1-9

setting and planning and not in operational activities. The following are their specific responsibilities:

1) Formulate objectives and policy guidelines.

2) Formulate operating programs and budget estimates.

3) Allocate budget to units.

4) Monitor program implementation. On the other hand, those designated to implement the programs of the Army in order to accomplish specific objectives are the project administrators. Project administration is the decentralized management of the PA financial resources by the Commanders of Major Subordinate Units and Chiefs of Office who are receiving appropriated funds. Designated project administrators are responsible for planning, coordinating, controlling, and supervising the execution of the budget or a portion of the budget that is allocated to their respective unit/office.

Project Administrators of Units shall be responsible for the strict

allocation/distribution of funds in accordance with the updated Operating Program and in the procurement of these requirements. The specific responsibilities of Project Administrators are the following:

1) Ensure that the amount of project/activity does not exceed the authorized amount in the allotment.

2) Facilitate the processing of financial transactions for

immediate funding and payment.

3) Ensure that the mode of procurement and funding are in adherence to existing accounting and auditing rules and regulations.

4) Administer project implementation and cost-effectiveness

of fund utilization.

5) Submit accomplishment/utilization reports to higher headquarters.

b. Comptrollership is a Command responsibility. It is a collective responsibility of all commanders and staff, comptrollers, and all persons charged with fund resource utilization.

c. The objective of comptrollership is to yield the maximum result with the least expenditures within legal bounds. It should satisfy what is needed rather than what is wanted. It should involve the application of the least resources but with optimum results.

R E S T R I C T E D

R E S T R I C T E D 1-10

d. AC of S for Comptrollership, G6 provides the overall control on the PA Financial Management System. Control means making sure that actual results conform to desired results.

e. Direction is made thru the Major Subordinate Units’ Comptrollers. They coordinate the various activities of all their program directors and project administrators and as such provide direction along the way.

f. Control is also made thru the Field Accountants. The actions of the project administrators are guided by the control being exercised by the accountant.

g. Balance between more control by Central Management versus less control but more flexibility by decentralization. The desire of top management for more control should be balanced with the desire of subordinate units/offices for more flexibility through decentralization.

h. Basic System of Planning, Programming and Budgeting System (PPBS). It is performance budgeting system with a planning orientation. It requires that programs, projects and activities are identified in terms of supplies and services to be delivered or rendered.

i. Budget Preparation an “Up - Down - Up” Process. Lower units are involved in the determination of requirement vis-à-vis formulation and accomplishment of functional objectives.

j. Budget Execution is a Program Director-Project Administrator Concept. To delineate staff and line management, staff officers at various headquarters are designated program directors while line officers are designated project administrators.

k. Centralized management for critical items. There are certain

activities that require an integrated approach in planning and execution and therefore cannot be undertaken simultaneously or in part by the subordinate units.

Section 1-7 Evolution of Comptrollership in the Army

The traditional misconception about Comptrollership is for it to be labeled as the treasurer or the money bag.

With the professional development programs implemented over the years, the role of the comptroller has evolved to a higher level of management.

R E S T R I C T E D

R E S T R I C T E D 1-11

The coordinated efforts of the Program Directors or the General Staff have more or less paved the way for an effective, efficient and ethical management of PA resources.

Effectiveness, i.e. doing the right things, efficiency, i.e. doing things the best way possible, and ethical is, being made accountable and responsible for the management of resources.

R E S T R I C T E D

R E S T R I C T E D 1-12

R E S T R I C T E D

R E S T R I C T E D 2-1

CHAPTER 2 BUDGET AND FISCAL OPERATIONS

Section 2-1 Overview The wise and optimal utilization of resources in any military organization is a primary concern of the comptroller. More often than not, the demand for material resources exceeds what is available. Whether the necessary implements to accomplish goals and objectives are sufficient or inadequate, the end-result of resource utilization serves as a measure of the efficiency and effectiveness of management. Among the many activities of resource management, resource allocation is considered the most crucial. If resources are improperly allocated among competing needs, say low priority activities are given high preference over those that will contribute more to the achievement of program objectives, then at the very start, resource management would fall short in deriving the maximum benefits from the resources expended. Hence, there is a need to carefully plan for financing government activities for a fiscal year.

Section 2-2 Budgeting Systems and Approaches Budgeting is basically planning and controlling. It is the process of costing programs or the translation of programs into monetary terms. Based on a budget guidance, the evaluated programs are transcribed into the proper budget form and appropriation language. The resulting budget estimate then undergoes through the regular government budgeting process. Thus, in budgeting, there is a need for wise selection of essential activities or programs to be undertaken and for a coordinated plan of financing such activities of programs

The Philippine Army adopts various budgeting system that can be combined from time to time with other approaches as follows:

1. As to nature:

a. Annual Budget – covers a period of one year. It is the basis of an annual appropriation.

b. Supplemental Budget –claims to supplement or adjust a previous budget which is deemed inadequate for its intended purpose. This is the basis for a supplemental appropriation.

c. Special Budget – of special nature and generally submitted in special forms on account of the fact that itemization is not adequately

R E S T R I C T E D

R E S T R I C T E D 2-2

provided in the appropriation act or that amounts are not at all included in the appropriation act. 2. As to basis:

a. Performance budgeting - requires the functions, activities and programs to be identified clearly in terms of desired objectives. Under this concept, objectives are identified, work or service to be accomplished is stressed and measured quantitatively and their total unit costs determined. This is short-term oriented with expenditures linked to planned work activities.

b. Line item budgeting is the listing of all activities that are to be

funded and budgeted. This concept is expenditure-oriented with little emphasis on objectives. 3. As to approach and technique:

a. Zero-Base Budgeting - is an operating, planning and budgeting process which requires each manager to justify his entire budget request in detail and shifts the burden of proof to each manager to justify why he should spend any money.

b. Incremental budgeting - begins with the prior year’s budget as its base and directs decision-making to incremental changes in various section of the budget. This budgeting approach involves evaluation and analysis of only the additional budgetary requirements to an existing budget. Section 2-3 The Planning, Programming and Budgeting System (PPBS)

The main vehicle for resource allocation in the Philippine Army is the Planning, Programming and Budgeting System (PPBS). It is a performance budgeting system with a planning orientation that provides a structure to guide and facilitate coordination on what to do, how best to do it, and with what resources. It requires that programs, projects and activities are identified in terms of supplies and services to be delivered or rendered. Under this concept, supplies and services are ascertained, measured quantitatively, and their unit and total costs are determined. Budget requests and authorizations are therefore stated in these terms to provide the approving authority a readily understandable basis in decision-making. 4. Planning. Is the determination of the basic goals of the organization, the evaluation of alternative courses of action and selection of the programs best calculated to achieve these goals. The main item in the planning is the formulation of the AFP Medium Term Development Plan (AFPMTDP). The AFPMTDP is a five (5) year-plan being reviewed and rolled forward yearly. This activity is undertaken by the Plans family and the AFP Planning Committee under the supervision by the DCS for Plans, J5.

R E S T R I C T E D

R E S T R I C T E D 2-3

a. The first step in planning is the review of the strategic intelligence estimate which is designed to determine the threat environment inside and outside the country.

b. Second is the internalization of the national objectives and policies in relation to the current and emerging threats.

c. Third is the determination of available resources. 5. Programming. Entails the scheduling and execution, as efficiently as possible, of the specific projects required to implement planned programs. It links planning to budget. In programming, ways to address the objectives of the AFP are determined. The functions of the program are to cost out the plans to keep them feasible and realistic and to make planners face the hard choices.

Once the AFP Medium Term Development Plan is approved, programs are developed to carry out AFP plans. A Preliminary Program and Budgeting Guidance (PPBG) is then issued. This is used by Commanders of the Major Services and AFP-Wide Support and Separate Units in the preparation of their Preliminary Operating Program and Budget Estimates for the target fiscal year. The Office Primary Responsibility (OPR) for AFP Programming is DCS for Operations, J3 with the support of the Program Budget Advisory Committee (PBAC) 6. Budgeting. Process of costing programs or the translation of programs into monetary terms. Based on the Preliminary Program and Budget Guidance (PPBG), the evaluated programs are transcribed into the proper budget form and appropriation language. The resulting budget estimate then undergoes the four stages of the regular government budgeting process.

Section 2-4 Budget Process/Cycle

It will be recalled that the mid-range plan or the STROP is ideally approved 1½ years or 18 months before its affectivity. Within this period, programming and budgeting activities of the AFP for the first calendar year covered by the plan take place. Goals, objectives and standards are established, activities are scheduled, and resource requirements are estimated. The resulting budget estimate then undergoes the regular government budget process.

The approval of the STROP signals the start of the budget process. Budget is undertaken using a process that consists of four (4) phases, namely: PHASE I - BUDGET PREPARATION PHASE II - BUDGET AUTHORIZATION

R E S T R I C T E D

R E S T R I C T E D 2-4

PHASE III - BUDGET EXECUTION PHASE IV - BUDGET ACCOUNTABILITY 7. Budget Preparation

a. PDBS, DBM “Budget Call” AND PPBG:

Once the STROP is approved by the Chief of Staff, GHQ issues the Program Development and Budget Summary (PDBS) for the five (5) years covered by the STROP.

The PDBS contains the statements of the AFP’s objectives, programs and policy guidelines. It provides the basis for the formulation of a more detailed program and budget development for the target fiscal year.

At about this time, the Executive Branch of the government thru the Department of Budget and Management issues the “Budget Call” for the target year. This document reminds the different agencies in the government to prepare their respective budget in accordance with approved over-all budget ceiling and parameter. It also contains the projected revenue of the government, the projected inflation rate, allocations of government sectors, priorities of expenditure and the schedules for the development of budget estimates of the different agencies.

Based on the PDBS and the DBM “Budget Call”, GHQ formulates the AFP Preliminary Program and Budget Guidance (PPBG). The primary staff concerned in the preparation of the PPBG is the Deputy Chief of Staff for Operations, J3. This PPBG contains the objectives and activities to be undertaken during the target fiscal year. This document is issued by GHQ to the major service commanders as the latter’s basis for the preparation and submission of their respective Preliminary Operating Program and Budget (POPB).

b. Army Preliminary Operating Program and Budget (POPB). The formulation of the Army Preliminary Operating Program and Budget (POPB) rests on the Program and Budget Advisory Committee (PBAC). The PBAC is chaired by the Chief of Staff, PA and the members of the Army General Staff are designated as members. Specifically, the PBAC functions under the following principles:

1) All major functional programs and interests are represented (G1 for Morale and Welfare and Health Services, G2 for Intelligence, G3 for Operations, G4 for Logistics, G5 for Strategic Planning and International Commitments, G7 for Civil Military Operations, G8 for Education and Training, G10 for Reservists Affairs and G11 for Communications-Electronics and Information System. G6, the Army Comptroller, acts as the financial adviser and vice chairman of PBAC).

2) The actions of the PBAC reflect the total coordinated

effort of command and management.

R E S T R I C T E D

R E S T R I C T E D 2-5

3) The interest of a single member of the PBAC is

subordinated to the interest of the command.

c. Army Major Unit PPBGs and POPBs:Upon receipt of the AFP PPBGs, the Army, thru the PBAC, prepares and publishes a similar PPBG to the Major Unit Commanders. The Philippine Army major subordinate units in turn prepare their respective PPBGs as the bases in the preparation and submission of POPBs of operating units under them. This is to ensure that lower units are involved in the determination of requirement vis-a-vis, formulation and accomplishment of functional objectives. The POPBs are then submitted to the Army Comptroller who consolidates and forwards the POPBs to the PBAC for review and evaluation. The PBAC sees to it that the POPBs are consistent with the Army commander’s guidance as contained in the Army PPBG. This results in the formulation of the Army POPB which is forwarded to GHQ for further review.

8. Budget Authorization. The POPB of the Major Services including that of GHQ are submitted to the Deputy Chief of Staff for Comptrollership, J6, for consolidation. These POPBs are then referred to the members of the joint staff who are also designated program directors at the AFP level. After ensuring that the POPBs of the Major Services comply with the provisions and specific guidelines as contained in the AFP PPBG, GHQ formulates the AFP Budget Proposal and forwards it to DND. DND in turn reviews and consolidates the budgets of the agencies and offices under it and later submits the budget proposals to DBM.

To ensure that all the budget proposals of government agencies are consistent with the “Budget Call,” DBM conducts reviews and budget hearings through its technical staff. The proposals are presented by DBM to the Executive Review Board of the Cabinet for further review. Based on the results of evaluations and hearings, DBM subsequently prepares the proposed National Budget Proposal or the proposed program of expenditure for submission to the President.

From the President, the proposed national budget is indorsed to the Lower House through the Committee on Appropriations, which in turn conducts budget hearings. Later, this budget is passed to the Committee on Finance of the Upper House which also conducts similar hearings. Once Congress has passed the appropriations bill, this is indorsed back to the President for final approval. This bill becomes the General Appropriations Act (GAA), once it is signed by the President. 9. Budget Execution

a. DBM Budget Circular on the Preparation of WFPs. After the approval of the appropriations act, DBM usually publishes a National Budget Circular providing specific guidelines in the implementation of the budget. This circular prescribes the policies and procedures in the preparation and submission of the Work and Financial Plans (WFPs) of government agencies.

R E S T R I C T E D

R E S T R I C T E D 2-6

The WFP is the annual projection of an agency as to how much shall be released to them out of their approved appropriations by quarter and how much is their cash requirements per month. The guidance also includes centrally managed activities and budget reserves, if there are any.

b. Final Operating Programs and Budget Guidance. Based on the DBM guidance, GHQ issues the AFP Final Operating Program and Budget Guidance (FOPB). Similar to the DBM guidance, it includes how much will be withheld out of the appropriations of the major services for agency reserve and centrally managed activities.

To attain flexibility, reserves are imposed to provide support to unprogrammed activities and other exigencies requiring resources.

With the publication of the AFP FOPB Guidance, the major services likewise prepare their FOPBs. For the Philippine Army, the FOPB is also called the Army Operating Program or AOP. The AOP essentially includes the specific objectives of Army units by major functional programs. The preparation of this document is a responsibility of the “threes” supervised by the AC of S for Operations, in close coordination with the “sixes”, the PA Comptrollers. It also includes the budget ceiling of Army operating units, to support the accomplishments of the specific objectives.

c. Operating Program and Budget (OPB). After the publication of the Army FOPB or AOP, major Army units prepare their Operating Programs and Budget (OPBs) for submission to the AC of S for Operation (G3). At the Infantry Division levels, FOPBs are commonly called the Division Operating Program. These OPBs are then consolidated at Army Headquarters by the AC of S for Operations (G3) copy furnished all Program Directors and the AC of S for Comptrollership, G6.

d. Modified Disbursement Scheme (MDS). Budget execution refers to the release of funds based on the WFP for purposes as authorized under the General Appropriations Act and the Program of Expenditures approved by the CSAFP.

The Joint Department of Budget and Management -

Department of Finance Circular Number 1-90 dated 27 February 1990, also known as the Modified Disbursement Scheme, prescribes the policies and procedures to be adopted in the execution of the budget. Based on its approved WFP, the Army’s Whole Networking Appropriation (WNA) is usually released by DBM at the start of the Fiscal Year in the form of a General Allotment Release Order (GARO) and/or Special Allotment Release Order (SARO). The WNA is the actual amount released by DBM out of the Army’s appropriation exclusive of DBM and GHQ reserves and Centrally Managed Items (CMIs). The major components of the DBM Advice include the following details:

1) Appropriation item code or the prescribed budget structure.

R E S T R I C T E D

R E S T R I C T E D 2-7

2) Allotment expense class and object class.

3) Reserves, unprogrammed appropriations and funds of

later release.

4) Releases by quarter.

As a general principle, allotments for succeeding quarters cannot be obligated and liquidated. However, carried-over balances from previous quarters can be obligated and liquidated. Unobligated funds (except continuing appropriations) are usually reverted to the general funds after the end of each fiscal year. Continuing appropriations are those funds released Capital Outlay which can be obligated and liquidated within a two (2) year period.

Based on the approved quarterly Program of Expenditures (POEs), the Army releases the fund allocation of Army operating units thru Advices of Sub-Allotment (ASAs). These ASAs normally pass thru the Accounting Services for journalization. Upon receipt of the ASAs by operating units, obligations and liquidations are done in the field through the services of the Field Accounting Units, Finance Services Units and the designated government servicing bank.

Notices of Cash Allocations (NCAs) are also issued by DBM on monthly basis to ensure that cash is available to pay obligations of Army units. Copies of these notices are furnished to the Bureau of Treasury (BTR) and the government servicing bank (Land Bank of the Philippines - LBP). Upon receipt of the NCA, the Army likewise allocates and transfers appropriate cash allocation to the accounts of the different Finance Service Units (FSUs), Finance Center, Philippine Army. This will ensure that obligations of operating units for a given period are fully supported. 10. Budget Accountability. The last phase of the budget cycle is budget accountability. It refers to the set of policies and procedures adopted by the Philippine Army thru the accounting services to ensure that funds are properly accounted for and are used for its intended purpose. Accountability includes periodic reporting of performance under the approved budget, management control of activities and programs and fiscal and policy formulation as guided by auditing, accounting regulations and management policies, such as:

a. Management Review – an appraisal and analysis of the performance of the unit/office regarding administration of fiscal resources by its project administrators. The management review of period reporting of the unit’s/office’s performance and accomplishments against their budget allocations thru Program Review and Analysis (PRA).

b. Pre-Audit/Fiscal Control – is the examination of a financial transaction before payment is made either through cash, warrants, checks or other instruments. With the withdrawal of pre-audit by COA except for certain

R E S T R I C T E D

R E S T R I C T E D 2-8

transactions mandated by law, the AFP management assumed full responsibility for the propriety of transactions entered into by the AFP. In this regard, Major Service Commanders and other AFP major units Commanders shall strengthen the review procedures of the Comptroller Accounting Finance and Logistics offices. In lieu of the COA pre-audit, the management staff or fiscal control assistants under the AFP Comptrollers shall perform final examination or fiscal control on AFP financial transactions prior to payment. The management staffs of the Major Services and other AFP units shall fall within the purview of PEMRAD, OJ6 with regard technical matters, standardization, and monitoring of fiscal control activities. The management staff and fiscal control assistants shall be selected by the Comptrollers based on their knowledge of auditorial procedures, integrity and mission orientation.

c. Post-Audit – is the examination of a financial transaction after payment and the recording thereof. It involves the tracing of the transaction to the pertinent books of accounts. The scope of the post-audit/work embraces, the three components of comprehensive audit namely: Financial compliance, efficiency, and economy and program results of effectiveness. With the issuance of COA Cir Nr 82-195 dtd 25 October 1982, subject: “Lifting of Pre-Audit on Government Transactions”, COA now focuses on the post-audit. This post audit activity is carried through the Certificate of Settlement and Balances. The Certificate has been devised to appraise the accountable officer and the Head of the Agency concerned of any deficiency found in the audit and settlement of the former’s account and of giving him an opportunity to explain such deficiencies promptly. It enables the COA to determine the disallowances found in the audit of the accounts as well as the official or officials liable thereof.

Section 2-5 Budget Structure 11. By Expense Class: 801-830 - Personal Services 831-950 - Maintenance and Other Operating Expenses 951-957 - Financial Expenses 12. By Function/Program/Activity (Subject to a yearly change as indicated in the Appropriations Act): A.1.a - Command and Management Activities A.1.b - Morale and Welfare Activities A.2.a - Medical Services A.2.b - Dental Services A.3.a - Intelligence Services A.4.a - Operations A.5.a - Logistics A.6.a - Civil Relations Activities A.7.a - Education and Training Services

R E S T R I C T E D

R E S T R I C T E D 2-9

A.8.a - Strategic Planning and International Commitments 13. By Object Classification:

a. Personal Services:

801 - Salaries and Wages – Regular Pay 802 - Salaries and Wages – Part Time Pay 803 - Salaries and Wages – Casual/Contractual 804 - Personnel Economic Relief Allowance (PERA) 805 - Additional Compensation (ADCOM) 806 - Representation Allowance (RA) 807 - Transportation Allowance (TA) 808 - Clothing Allowance 809 - Honoraria 810 - Hazard Pay 811 - Overtime and Night Pay 812 - Holiday Pay 813 - Christmas Bonus 814 - Cash Gift 815 - Productivity Incentive Benefits 816 - Other Bonuses And Allowances 817 - Life and Retirement Insurance Contributions 818 - PAG-IBIG Contributions 819 - PHILHEALTH Contributions 820 - ECC Contributions 821 - Pensions and Retirement Benefits 822 - Terminal Leave Benefits 823 - Other Personal Benefits

b. Maintenance and other Operating Expenses:

831 - Traveling Expenses – Local 832 - Traveling Expenses – Foreign 833 - Training and Seminar Expenses 834 - Water 835 - Electricity 836 - Cooking Gas 837 - Telephone/Internet 838 - Postage and Deliveries 839 - Subscription Expense 840 - Advertising Expense 841 - Rent Expense 842 - Insurance Expense 843 - Fidelity Bond Premium 848 - Accountable Forms with Face Value 849 - Office Supplies Expense 850 - Medical, Dental & Laboratory Supplies Expense 851 - Spare Parts Expense 852 - Gasoline, Oil and Lubricants Expense

R E S T R I C T E D

R E S T R I C T E D 2-10

854 - Printing and Binding Expenses 855 - Auditing Service 856 - Consultancy Services 857 - General Services 858 - Security Services 859 - Taxes, Duties and Fees 864 - Buildings Maintenance 865 - School Buildings Maintenance 866 - Market and Slaughterhouse Maintenance 867 - Hospitals and Health Center Maintenance 868 - Other Structures Maintenance 869 - Heavy Equipment Maintenance 870 - Machinery and Equipment Maintenance 871 - Firefighting Equipment and Accessories

Maintenance 872 - Construction Equipment Maintenance 873 - Industrial Machineries Maintenance 874 - Technical and Scientific Equipment Maintenance 875 - IT Hardware and Software Maintenance 876 - Telegraph, Telephone, Cable, TV and Radio

Equipment Maintenance 877 - Artesian Wells, Reservoir, Pumping Stations,

Etc. Maintenance 878 - Motor Vehicles Maintenance 879 - Watercrafts Maintenance 880 - Trains Maintenance 881 - Aircrafts Maintenance 882 - Office Equipment Maintenance 883 - Other Equipment Maintenance 884 - Furniture and Fixtures Maintenance 885 - Ordnance Maintenance 887 - Other Repairs and Maintenance 888 - Awards and Indemnities 889 - Rewards and Other Claims 890 - Grants and Donations 891 - Representation Expenses 892 - Extraordinary and Miscellaneous Expense 893 - Confidential and Intelligence Expenses 894 - Bad Debts Expense 895 - Loss on Sale of Assets 896 - Subsidy to Local Government 897 - Subsidy to Government Corporations 898 - Subsidy to Regional Office 899 - Subsidy to Operating Units 900 - Subsidy to Other Funds 901 - Subsidy to Special Funds 902 - Tax Credit Subsidy 903 - Depreciation-Leasehold Improvement 904 - Depreciation-Buildings 905 - Depreciation-School Buildings

R E S T R I C T E D

R E S T R I C T E D 2-11

906 - Depreciation-Market and slaughterhouse 907 - Depreciation-Hospitals and Health Centers 908 - Depreciation-Other Structures 909 - Depreciation-Heavy Equipment 910 - Depreciation-Machinery and Equipment 911 - Depreciation-Firefighting Equip. & Accessories 912 - Depreciation-Construction Equipment 913 - Depreciation-Industrial Machineries 914 - Depreciation-Technical and Scientific Equipment 915 - Depreciation-IT Equipment 916 - Depreciation-Telegraph, Telephone, Cable, TV

and Radio 917 - Depreciation-Artesian Wells, Reservoirs and

Pumping Stations 918 - Depreciation-Motor Vehicles 919 - Depreciation-Watercrafts 920 - Depreciation-Trains 921 - Depreciation-Aircrafts 922 - Depreciation-Office Equipment 923 - Depreciation-Other Equipment 924 - Depreciation-Furniture and Fixtures 925 - Depreciation- Ordnance 927 - Depreciation-Other Fixed Assets 928 - Obsolescence-IT Software 939 - Other Expenses

c. Financial Expenses:

951 - Bank Charges 952 - Interest Expense 953 - Commitment Charges 954 - Other Financial Charges 955 - Foreign Exchange (FOREX) Loss 956 - Debt Services Subsidy to GOCCs 957 - Loss on Guaranty

Section 2-6 Financial Support Programs The Philippine Army provides financial support to its subordinate units. Sources of financial support for these units are as follows: 14. Current Operating Expenditures – Appropriation for the purchase of goods and services for current consumption or for benefits expected to terminate within the fiscal year. Current Operating Expenditures are classified into:

R E S T R I C T E D

R E S T R I C T E D 2-12

a. Personal Services (PS)

The Pay and Allowances or Personal Services is another source for which the Finance Center and its Finance Service Units act as the Project Administrators.

b. Maintenance and Other Operating Expenses (MOOE):

1) The Regular Maintenance Operating System (MOE)

Allocation is the principal source of support which is the subject of periodic POE. This is provided its operating units for their quarterly maintenance and operating expenses by the Philippine Army. These regular allocations or ceilings may vary depending on the area of a unit. As an example, units confronting priority enemy fronts have higher allocations compared to those operating in less threatened areas. These supports are over and above the releases provided by HPA for specific projects.

2) HPA Centrally Managed Funds are usually received in kind. These are common supplies or services for general support items such as POL, tires and batteries, which are centrally procured for economy and better distribution to the field units. Units also receive funds for PA wide services such as repair of vehicles and facilities.

3) Internal Security Operation (ISO) Funds. In translating the operational intent of the AFP Campaign Plan, funds for the sustainment of this internal security operation thru the Operation Enhancement Fund (OEF) are allocated to units addressing priority fronts. It is intended to provide the commanders flexibility to prioritize fund support to their tactical units so that they can better influence the result of operations.

4) Specific Fund Release. Units may request for HPA funds to support specific activities. 15. Capital Outlay. Appropriations for the purchase of goods and services, the benefits of which extend beyond the fiscal year and which add to the assets of government, including investments in the capital of government-owned or controlled corporations and their subsidiaries. 16. Trust Fund. Officially granted to any agency of the government or to a public officer or trustee, agent or administrator for the fulfillment of a specific obligation. These funds shall be available and be spent only for specific purposes for which the trust was created.

a. AFP Modernization Trust Fund – the financial support for the Modernization Program will be provided by the operation of the AFP Modernization Trust Fund, which shall be used solely for the said Program, exclusive of salaries and allowances and will be funded out of the following:

R E S T R I C T E D

R E S T R I C T E D 2-13

1) Appropriations for the AFP Modernization Program.

2) Proceeds from the sale, lease or joint development military reservations not covered by BCDA.

3) Shares from the proceeds of the sale military camps under BCDA.

4) Proceeds from the sale of the products of government arsenal.

5) Proceeds from the disposal of excess and/or uneconomically repairable equipment and other movable assets of the AFP and the government arsenal.

6) Funds from the budgetary surplus.

7) Other revenues as authorized by law and those that are to be identified under JR 28.

8) All interest income of the trust fund

b. Trust Receipts

1) Trust Receipts – are authorized collection of funds from non-income sources by a government office or agency acting as a trustee, administrator or guarantor for the fulfillment of an obligation.

2) Trust Liabilities – are receipt out of remittance to agency. This particular account in used to record the liability for collections received or amount withheld in trust for the account of National Government Agencies for specific purpose. 17. Inter-Agency Transferred Funds .Inter-agency transferred funds are the cash or money transferred or sub-allotted by another agency of the government to the Philippine Army for the implementation of a specific government project.

a. General Guidelines:

1) The Source Agency shall enter into an agreement with a PA unit for the undertaking by the latter of the project of the former.

2) The Agreement shall provide for the requirements for project implementation and reporting.

3) The cash/money transferred shall be taken up as Cash, Inter-agency Transferred Funds (8-70-684) by the source agency (SA) and as a trust liability (8-84-100) by the Philippine Army. For this purpose, a special

R E S T R I C T E D

R E S T R I C T E D 2-14

budget to be submitted to and approved by the Department of Budget and Management (DBM) is not required.

4) The fund to be transferred or sub-allotted to the PA unit shall be (a) in an amount sufficient for three months operation subject to replenishment upon submission of the reports of disbursements by the PA, or (b) the total project cost, as may be determined by the Heads of the two agencies in either case.

5) The check shall be issued in the name of the PA unit for deposit to its trust account in its authorized government depository bank. The concerned PA unit shall issue its official receipt in acknowledgment.

6) A separate subsidiary record for each account shall be maintained by the PA unit whether or not a separate bank account is opened.

7) Within ten (10) days after the end of each month/end of the agreed period for the project, the PA unit shall submit the Report of Checks Issued (RCI) and the Report of Disbursement (RD) to report the utilization of the funds. Only actual project expenses shall be reported. The reports shall be approved by the head of the PA.

8) The Source Agency (SA) shall draw a journal voucher to take up the reports. The amount to take up the liquidation per the RCI shall be net of the cash advances granted by the PA to its accountable officers in accordance with Commission on Audit Circular Nr 90-331 dated May 3, 1990.

9) The PA auditor shall audit the disbursements out of the trust accounts in accordance with existing COA regulations.

10) The PA shall return to the SA any unused balance upon completion of the project.

R E S T R I C T E D

R E S T R I C T E D 3-1

CHAPTER 3 ACCOUNTING OPERATIONS

Section 3-1 Overview

Accounting operations encompass the processes of analyzing, recording, classifying, summarizing and communicating all transactions involving the receipt and disposition of funds and property and interpreting the results thereof. 1. It gives substance to the concept of public accountability of officers and employees with regard to:

a. Safeguarding resources against loss or wastage,

b. Adherence to the requirements of law and administrative policies and regulations,

c. Economy and efficiency in operations, and

d. Delivering the desired results of programs and activities. 2. The general purposes of accounting are:

a. To establish accountability over receipts, property and expenditures, and

b. To generate information that permits continuous review of government program and the efficiency with which they are implemented. 3. Generally Accepted Government Accounting Principles

a. The accounts of an agency shall be kept in such detail as necessary to meet the needs of the agency and at the same time be adequate to furnish the information needed by fiscal or control agencies of the government (Sec 111, PD 1445).

b. The highest standards of honesty, objectivity and consistency shall be observed in the keeping of accounts to safeguard against inaccurate or misleading information (Sec 111, PD 1445).

c. The government accounting shall be on a double entry basis with a general ledger in which all financial transactions are recorded. Subsidiary records shall be kept when necessary (PD 114, PD 1445).

d. The chart of accounts for government agencies shall be so prescribed by the Commission on Audit and shall be so designed as to:

R E S T R I C T E D

R E S T R I C T E D 3-2

1) Permit agency heads to review their activities according to selected areas of responsibility;

2) Allow for a clearer definition of obligation accounting leading to a more precise budgetary control;

3) Provide for a wider range of analytical information designed for use in management audit or legislative review;

4) Furnish information regarding the production of income and the investment in capital items which is of value in fiscal and economic planning.

5) Enable tighter accounting control to be exercised over agencies financial relationship with the Treasury.

6) Permit a more simplified preparation of Trial Balances and a simpler and more orderly process of national consolidation; and,

7) Facilitate the application of automatic accounting procedures for more effective protection against error and irregularity and yielding economies in operation (Sec 113, PD 1445).

e. To permit effective budgetary control and to establish uniformity in financial reports, accounts shall be classified in balanced fund groups. The group for each fund shall include all accounts necessary to set forth its operations and condition. All financial statements shall follow this classification (Sec 116, PD 1445).

f. A common terminology and classification shall be used consistently throughout the budget, the accounts and financial reports (Sec 115, PD 1445).

g. The general accounting system shall include budgetary control accounts for revenues, expenditures and debt, as provided for by PD 1177 (Sec 117, PD 1445).

h. Estimated revenues which remain unrealized at the close of the fiscal year shall not be booked or credited to unappropriated surplus or any account (Sec 108, PD 1445).

i. All lawful expenditures and obligations incurred during the year shall be taken up in the accounts of that year (Sec 119, PD 1445).

Section 3-2 Accounting Process

Government accounting like any other accounting is concerned with financial transactions and their result. The common transactions in the

R E S T R I C T E D

R E S T R I C T E D 3-3

government includes: cash receipts and disbursements, purchase of goods and services, tax levies, collections of taxes, licenses, permits, fees and fines, sales of goods and services, and the transfer and borrowing of funds. 4. The different phases of government accounting:

a. Journalization – Transactions are analyzed to determine the accounts involved. They are recorded in the journal or books of original entry by debits and credits to the proper accounts.

b. Posting – The entries in the books of original entry are transferred to the ledger or books of final entry. Summaries of increases and decreases of each account are posted in the corresponding ledger sheet.

c. Preparation of Financial Statements –Statements that show receipt and expenditures, obligations incurred, obligations liquidated, allotments, appropriations, fixed asset, invested surplus, fixed liabilities, and investments and analysis of surplus are prepared periodically.

d. Analysis of the Financial Reports – Financial reports are examined to determine their accuracy as well as the efficiency and effectiveness of agency operations.

Section 3-3 New Government Accounting System (NGAS)

The New Government Accounting System is a simplified set of accounting concepts, guidelines and procedures designed to ensure correctness, completeness and timeliness in the recording of government financial transactions and production of financial reports. This system was conceptualized and designed with the following objectives:

a. Simplify government accounting b. Confirm to international accounting standards; and c. Generate periodic and relevant financial reports for better

monitoring performance.

Section 3-4 Significant Policies of the New Government Accounting System (NGAS)

5. A modified accrual basis of accounting shall be used. Under this method, all expenses shall be recognized when incurred and are recorded and reported in the financial statements in the period to which it relates. Income shall be on accrual basis except for transactions where accrual basis is impractical or when other methods are required by law.

R E S T R I C T E D

R E S T R I C T E D 3-4

6. This system adopts the one fund concept. Separate fund accounting shall be done only when specifically required by law or by a donor agency or when otherwise necessitated by circumstances subject to prior approval of the Commission on Audit. 7. All national agencies shall maintain two sets of books, namely:

a. Regular Agency (RA) Books. These shall be used to record the receipt of Notice of Cash Allocation (NCA) and other income/receipts for which the agencies are authorized to use and to deposit to an h authorized government depository bank, disbursements, and other related transactions. These shall consist of journals and ledgers. The Journals are: Cash Receipts Journal (CRJ); Cash Disbursement Journal (CDJ); Check Disbursements Journal (CDJ); and General Journal (GJ). The General Ledger (GL) shall be supported with Subsidiary Ledgers (SL) for Cash, Receivables, Inventories, Investments, Property, Plant and Equipment, Construction in Progress, Liabilities, and Income.

b. National Government (NG) Books. These shall be used to record income, which the agencies are not authorized to use, and are required to be remitted to the National Treasury (NT). These shall consist of: Cash Journal (CJ), General Journal (GJ), General Ledger, and Subsidiary Ledger (SL).

c. Chart of Accounts and Account Codes. The agency uses a new Chart of Accounts with a three-digit account numbering system as prescribed by COA effective year 2002.

d. The following accounting reports shall be prepared: (1) Trial Balance, (2) Balance Sheet, (3) Statement of Income and Expenses, (4) Statement of Cash Flow, and (5) Statement of Government Equity. Except for the Trial Balance, these accounting reports shall be supported by necessary Notes to Financial Statements and Supplementary Reports.

e. The two-money column Trial Balance showing the account balances shall be used.

f. The receipts of allotments from the Department of Budget and Management (DBM) and the incurrence of obligations by the agency shall be recorded in separate registries.

g. Financial expenses such as bank charges, interest expenses, commitment charges, and other related expenses shall be separately classified from Maintenance and Other Operating Expenses (MOOE).

h. The receipt of Notice of Cash Allocation (NCA) shall be taken up in the books as a debit to account “Cash – National Treasury, Modified Disbursement System (MDS)” and credit to account “Subsidy Income from National Government (SING).

R E S T R I C T E D

R E S T R I C T E D 3-5

i. Supplies and materials purchased for inventory purposes shall

be recorded using the perpetual inventory system. Regular purchases shall be coursed thru the inventory account and issuances thereof shall be recorded as they take place except those purchased out of Petty Cash Fund which shall be charged directly to the appropriate expense accounts. The Petty Cash Fund shall not be used to purchase regular inventory/items for stock.

j. Cost of ending inventory of supplies and materials shall be computed using the moving average method.

k. The straight-line method of depreciation shall be used. Depreciation shall start on the second month after purchase of the property, plant and equipment, and a residual value equivalent to ten percent (10%) of the purchase cost shall be set.

l. Assets declared by proper authorities as obsolete and unserviceable, including assets of the agency no longer used, shall be reclassified to “Other Assets” account from the corresponding inventory and property, plant and equipment accounts.

m. An Allowance for Doubtful Accounts shall be set up for estimated uncollectible from “Accounts Receivables” and “Notes Receivables”.

n. Contingent accounts shall no longer be used. Cash shortages and disallowed payments which become final and executory shall be recorded under receivables accounts such as “Due from Officers and Employees” or “Receivables-Disallowances/Charges” as the case may be.

o. Liability shall be recognized at the time goods and services are accepted or rendered and supplier/creditor bills are received.

p. Interest income and/or expense shall be accrued and recognized in the books of accounts whenever practical and appropriate.

q. All borrowings and loans incurred shall be recorded direct to the appropriate liability accounts.

r. Acquisition/disposition of assets shall be debited/credited direct to the appropriate asset accounts. If an error is committed, an adjusting entry shall be prepared to correct the original entry. This stops the use of corollary and negative journal entries.

s. The Petty Cash Fund shall be maintained under the imprest system. As such, all replenishments shall be directly charged to the expense account and at all times, the Petty Cash Fund must be equal to the total cash on hand and the unreplenished expenses.

R E S T R I C T E D

R E S T R I C T E D 3-6

t. Correction in any of the accounts or transaction shall be made by means of an adjusting entry using the Journal Entry Voucher to reverse/correct the original entry.

Section 3-5 Books of Accounts

8. Regular Agency Books

a. Books of Original Entry. Financial transactions are recorded in chronological order in the General and Special Journals which shall serve as the books of original entry. Each entry shall be supported with Journal Entry Voucher (JEV).

1) General Journal (GJ) – shall be used to record all transactions which cannot be recorded in the four special journals.

2) Special Journals – Designed to record transactions which are repetitive in nature. Special columns are provided to facilitate summation and posting in the General Ledger. These are:

(a) Cash Receipts Journal (CRJ) – used to record all collections and deposits reported during the month for the RA book. The source of entries is the JEV which shall be prepared using the Report of Collections and Deposits (RCD) submitted by the Cashier/Collecting Officers to the Accounting Unit or the official receipt acknowledging collections.

(b) Cash Journal (CJ) – used to record all collections and deposits reported during the month for the NG books. The source of entries is the JEV which shall be prepared using the RCD submitted by the Cashier/Collecting Officer to the Accounting Unit or the official receipt acknowledging collections.

(c) Check Disbursements Journal (CDJ) – used to record check payments made by the Cashier or Disbursing Officer. Recording to this journal shall be based on the JEV supported with paid Disbursement Vouchers (DVs) and duplicate copies of checks listed in the Report of Checks Issued (RCI) submitted by the Cashier/Disbursing Officers.

(d) Cash Disbursements Journal (CDJ) – used to record all payments made in cash by the Regular/Special Disbursing Officers out of their cash advances. Recording to this journal shall be based on the JEV supported with Report of Disbursements (RD) where all payments are listed including payroll as the case maybe.

b. Books of Final Entry. These are the records for classifying and summarizing the effects of the transactions on individual accounts. Each entry shall be taken up from the Books of Original Entry.

R E S T R I C T E D

R E S T R I C T E D 3-7

1) General Ledger (GL) – a book of final entry containing accounts arranged in the same sequence as in the chart of accounts. Totals of columns in the special journals and the individual entries in the GJ are directly posted in this book. At the end of each month, the accounts are footed and at the end of each year, these are totaled, ruled and closed and the balance extracted to serve as the opening balance of the new fiscal year. Likewise, the account balances (i.e. difference between Debits and Credits) shall appear in the trial balance.

2) Subsidiary Ledgers (SL) - contains the details or breakdown of the balances of the controlling account appearing in the GL. Postings to the SL generally come from source documents. Examples of GL accounts which have SL are: Cash- Collecting Officers; Cash-Disbursing Officers; Cash in Bank-Local Currency; Current Account; Accounts Receivable; Notes Receivable; Property, Plant and Equipment; Supplies; and Investment. 9. National Government Books – A separate set of books to record cash receipts/collections which are required to be remitted to the Bureau of Treasury and other related transactions, such as Cash Journal (Receipts and Remittances), General Journal, and General ledger.

Section 3-6 Accounting Registries 10. Registry of Allotments and Obligations (RAO) – These are used to record allotments from DBM and the obligations charged against such allotments by the Budget Unit/Authorized Official of the agency. The balance is extracted every time an entry is made to prevent incurrence of obligations in excess of allotment received. These registries are:

a. Registry of Allotments and Obligations-Capital Outlay (RAOCO) – used to record allotments received and obligations incurred for capital outlay.

b. Registry of Allotments and Obligations-Maintenance and Other Operating Expenses (RAOMO) – used to record allotments received and obligations incurred for expenses classified under Maintenance and Other Operating Expenses.

c. Registry of Allotments and Obligations-Personal Services (RAOPS) – used to record allotments received and obligations incurred for expenses classified under Personal Services.

d. Registry of Allotments and Obligations-Financial Expenses (RAOFE) – used to record allotment received and obligations incurred for financial expenses, so as to distinguish them from the regular maintenance and other operating expenses.

R E S T R I C T E D

R E S T R I C T E D 3-8

11. Registry of Allotments and Notice of Cash Allocations (RANCA) – shall be maintained by the agency to monitor the allotment and NCA received, and utilized, and the balance as of a given date.

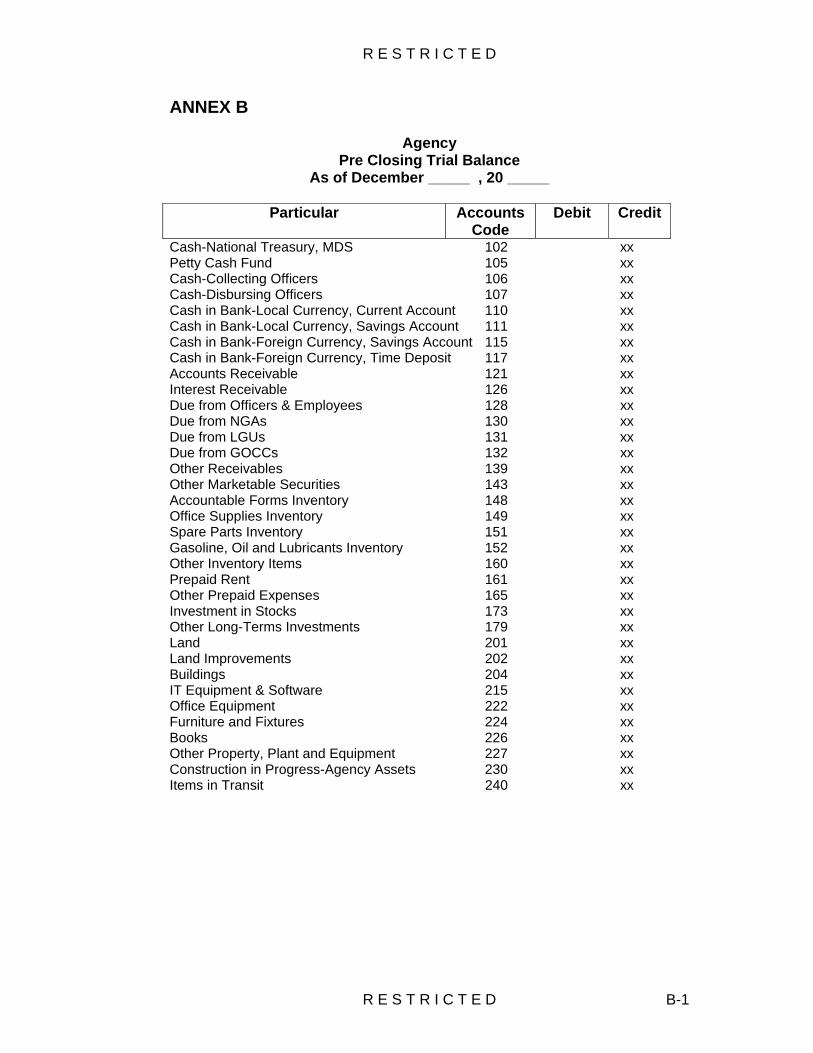

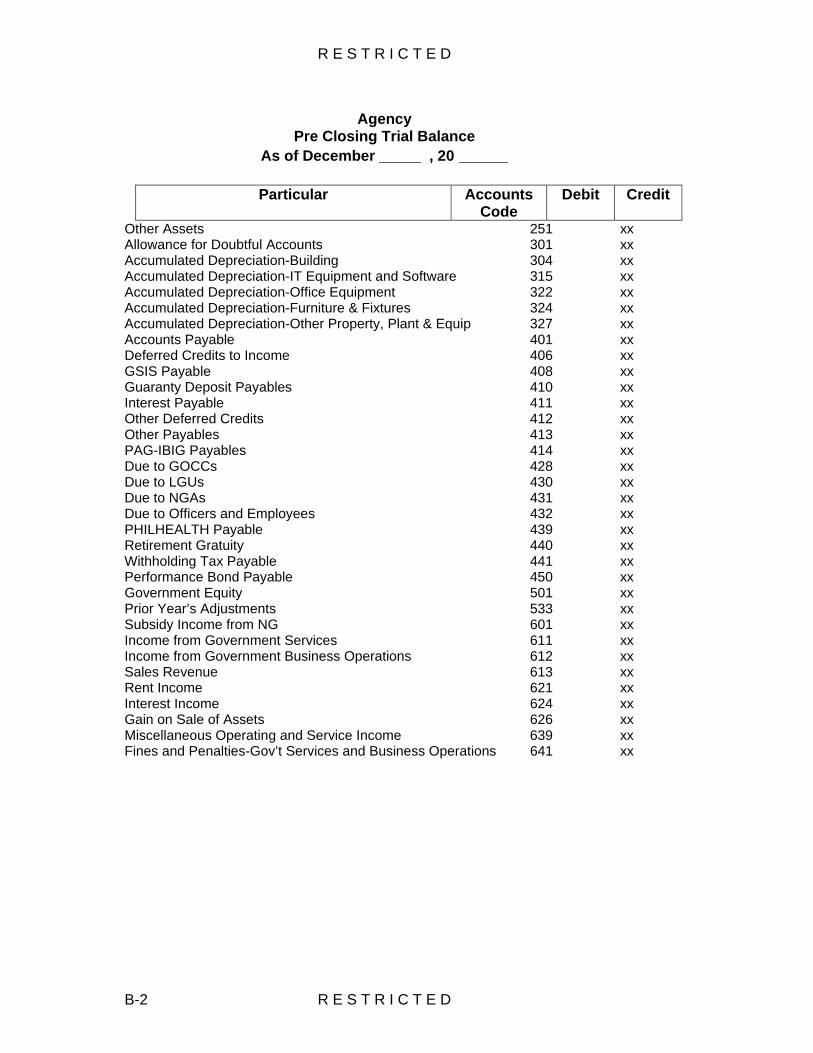

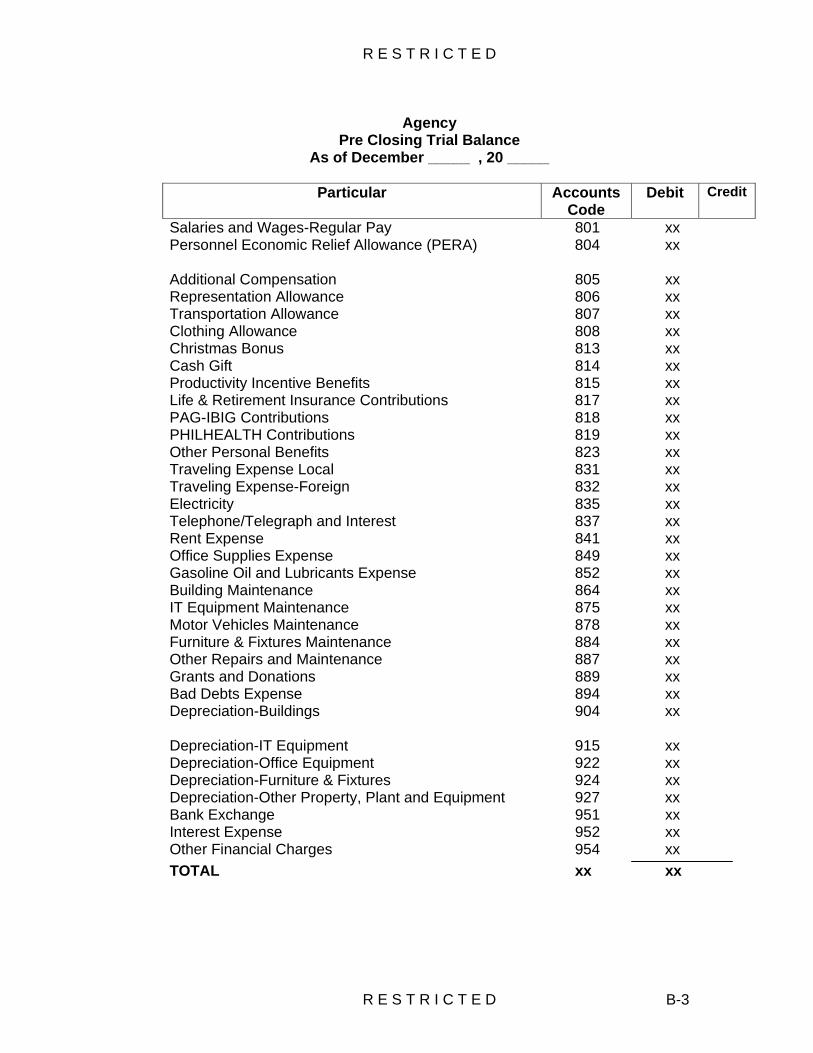

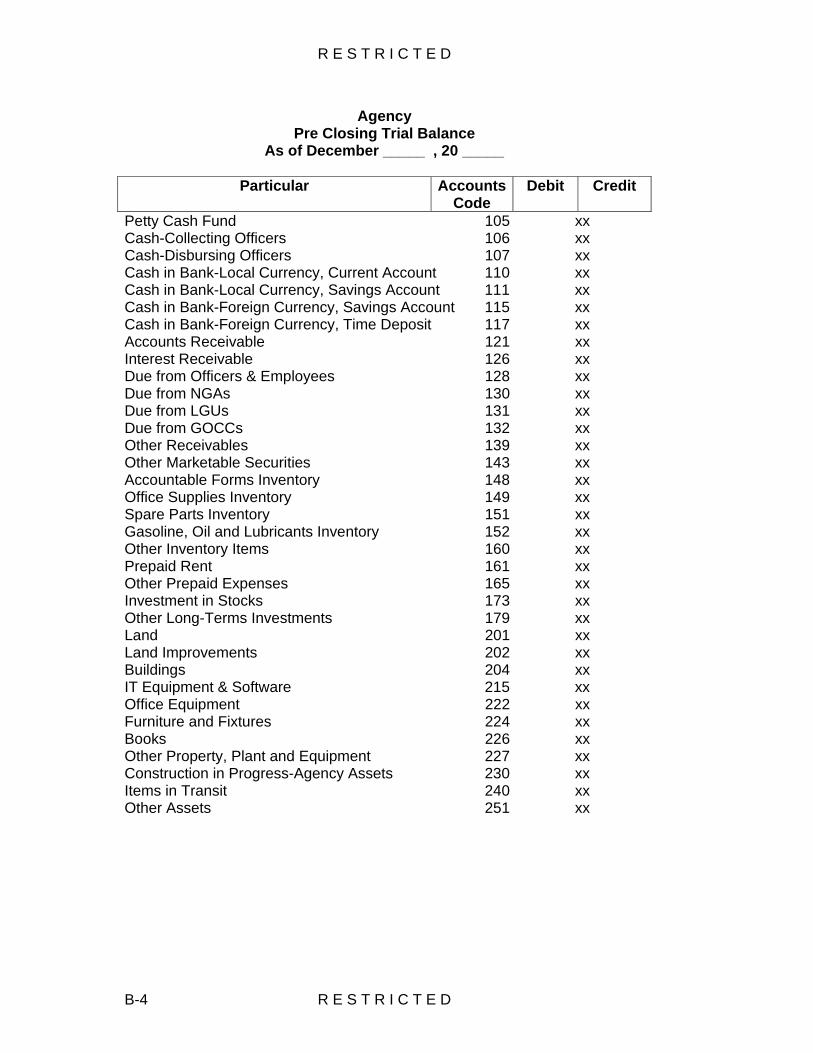

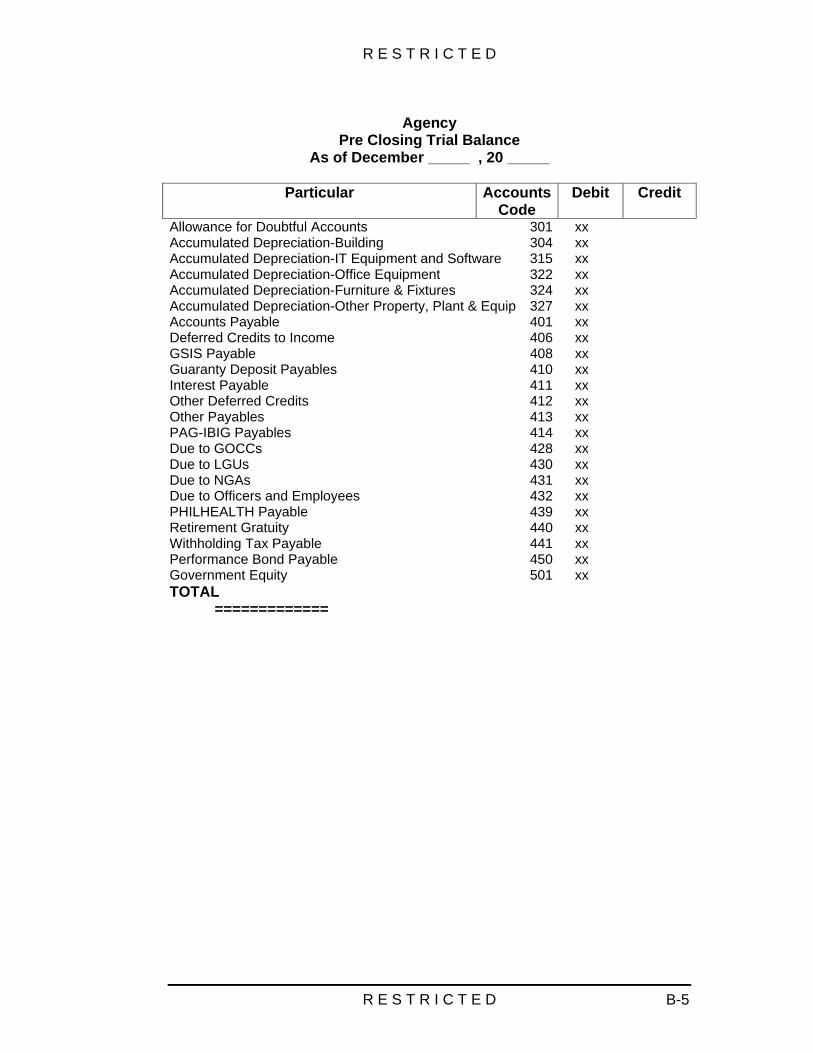

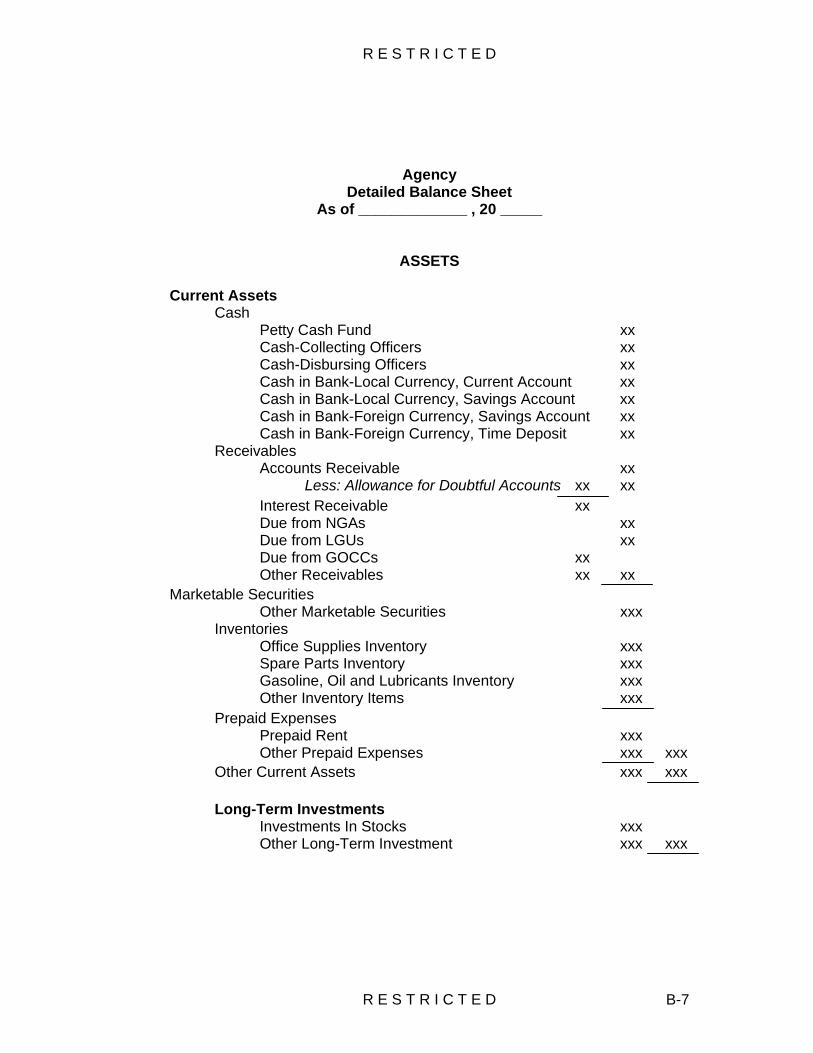

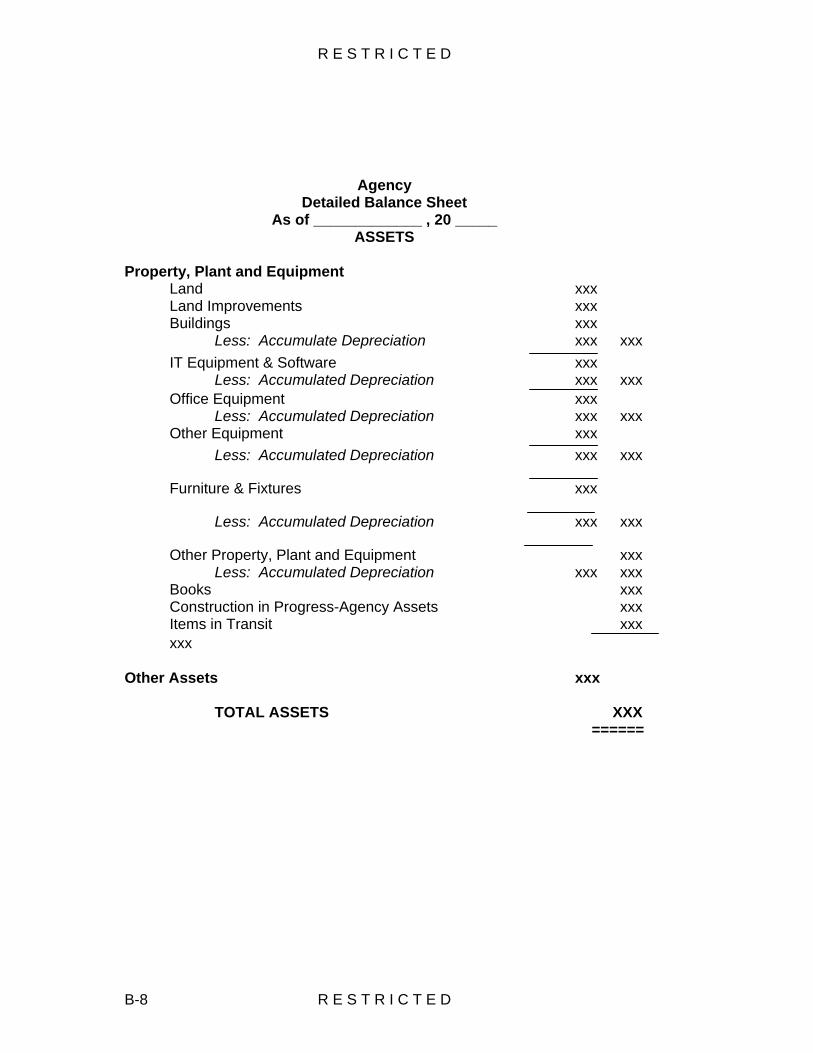

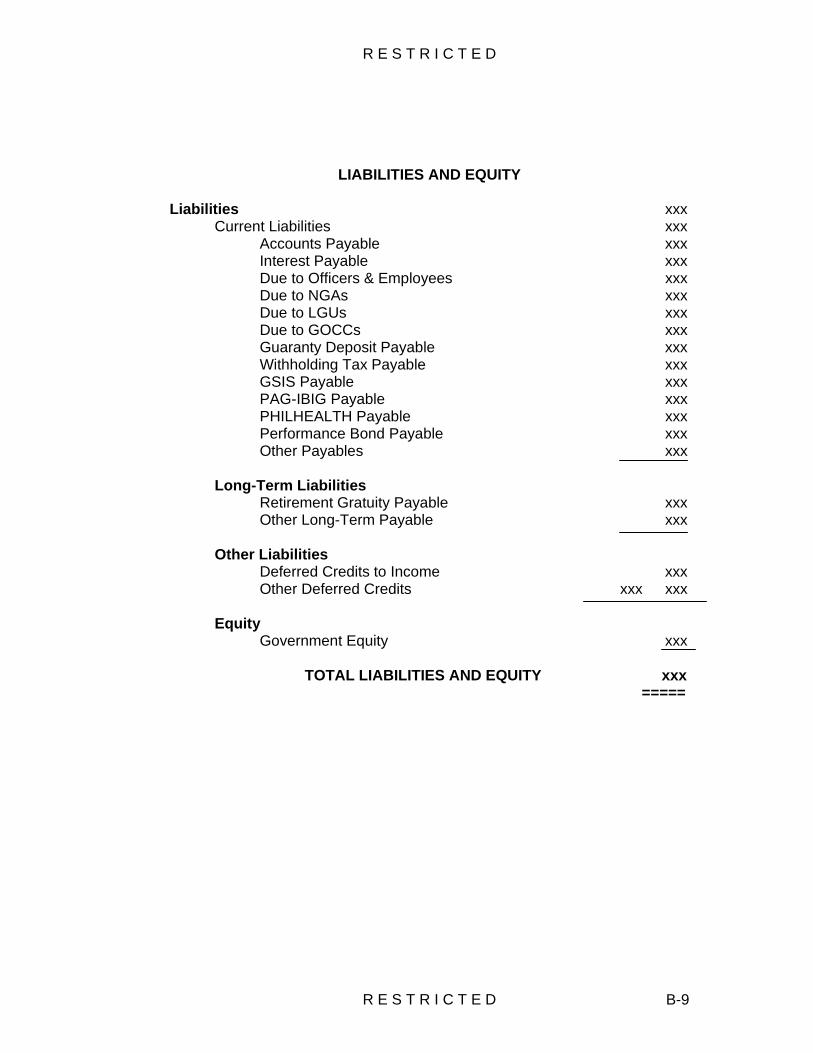

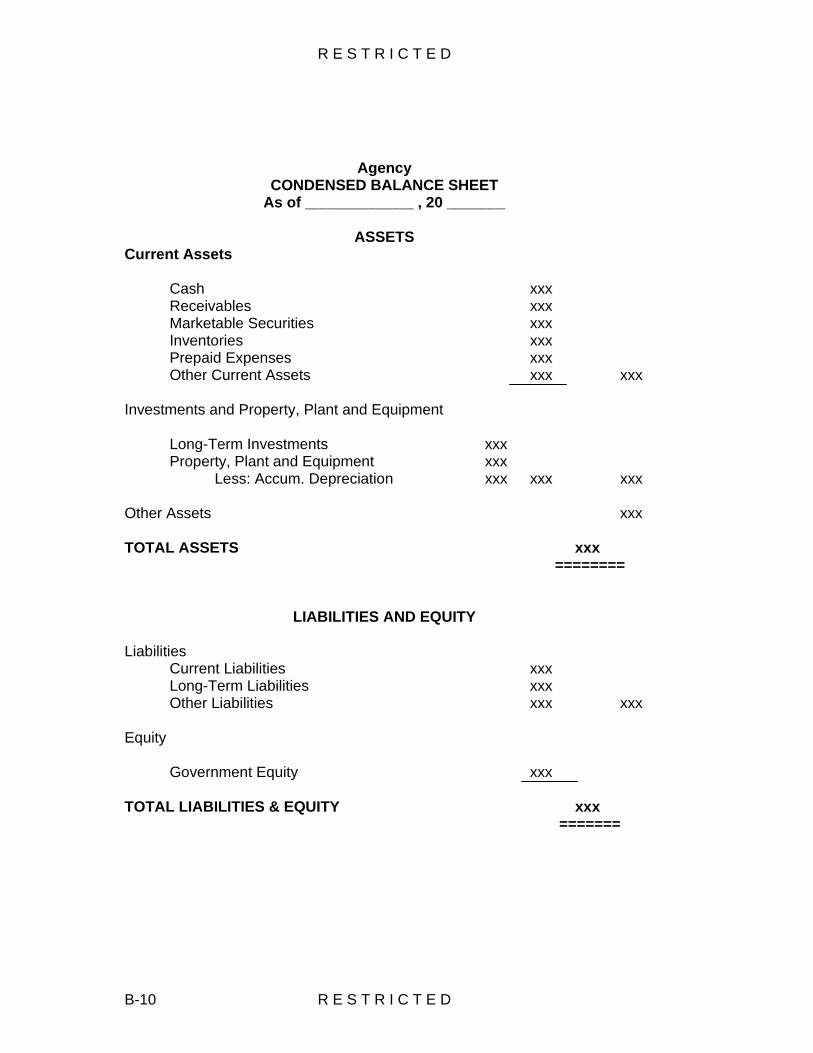

Section 3-7 Statements/Reports Prepared Periodically 12. Trial Balance (TB) – shows the equality of debit and credit balances of all general ledger accounts as of a certain period, which can be monthly, quarterly or annually. At the end of the fiscal year, two trial balances shall be prepared: the pre-closing and the post closing trial balances using the same format. The PA Trial Balance is a consolidation of the Trial Balances of Main Accounting Service and its l5 Field Accounting Units. It is prepared and submitted on a monthly basis. 13. The Pre-Closing Trial Balance (TB) is prepared after posting the adjusting journal entries in the general ledger. It shows the adjusted balances of all accounts before closing. 14. The Post-Closing Trial Balance (TB) is prepared after recording the closing entries in the General Journal and posting to the General Ledger. It contains a listing of all general ledger accounts that remain open after the closing process is completed.

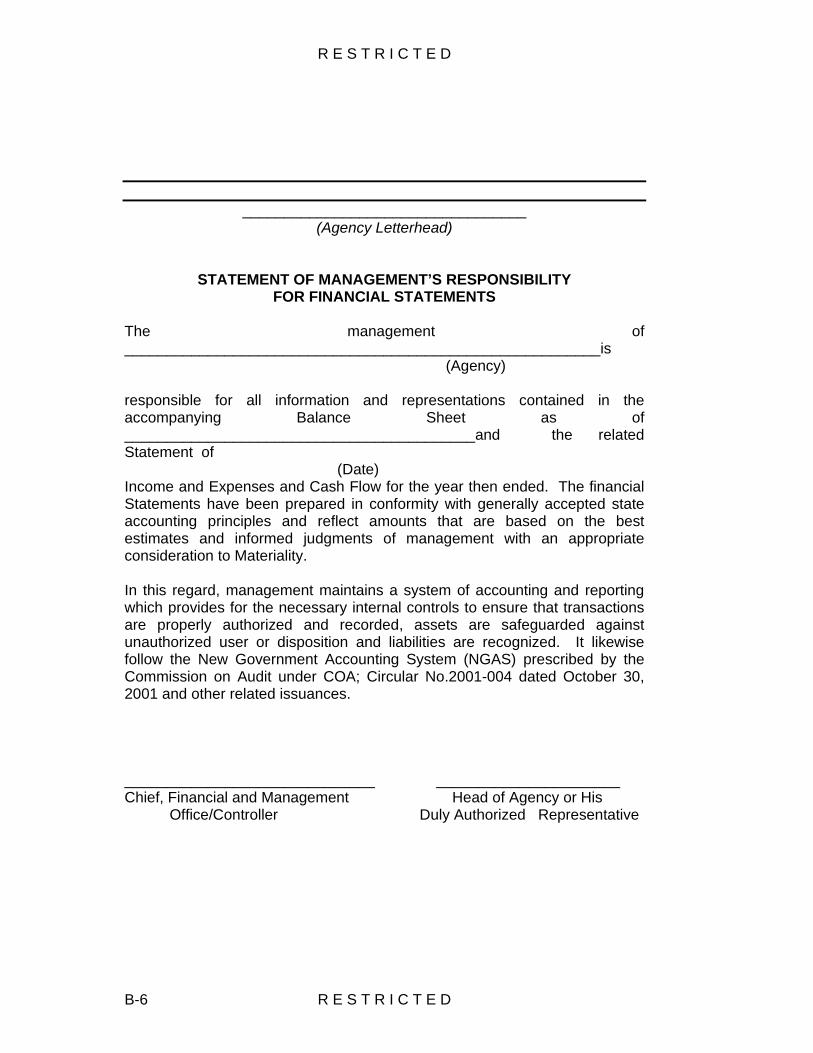

The Statement of Management Responsibility for Financial Statements serves as the cover letter in the transmission of the agencies’ financial statements to the Commission on Audit, Department of Budget and Management, other oversight agencies and other parties. The statement shall be signed by the Chief Accountant, PA and CG, PA or his authorized representative. 15. Balance Sheet. This is a formal statement which shows the financial position/condition of the agency as of a certain date. It includes information on the three elements of financial position which are assets, liabilities and government equity. It is prepared from information taken directly from the Post-Closing Trial Balance at year-end. The Balance Sheet is supported with the following schedules/statements:

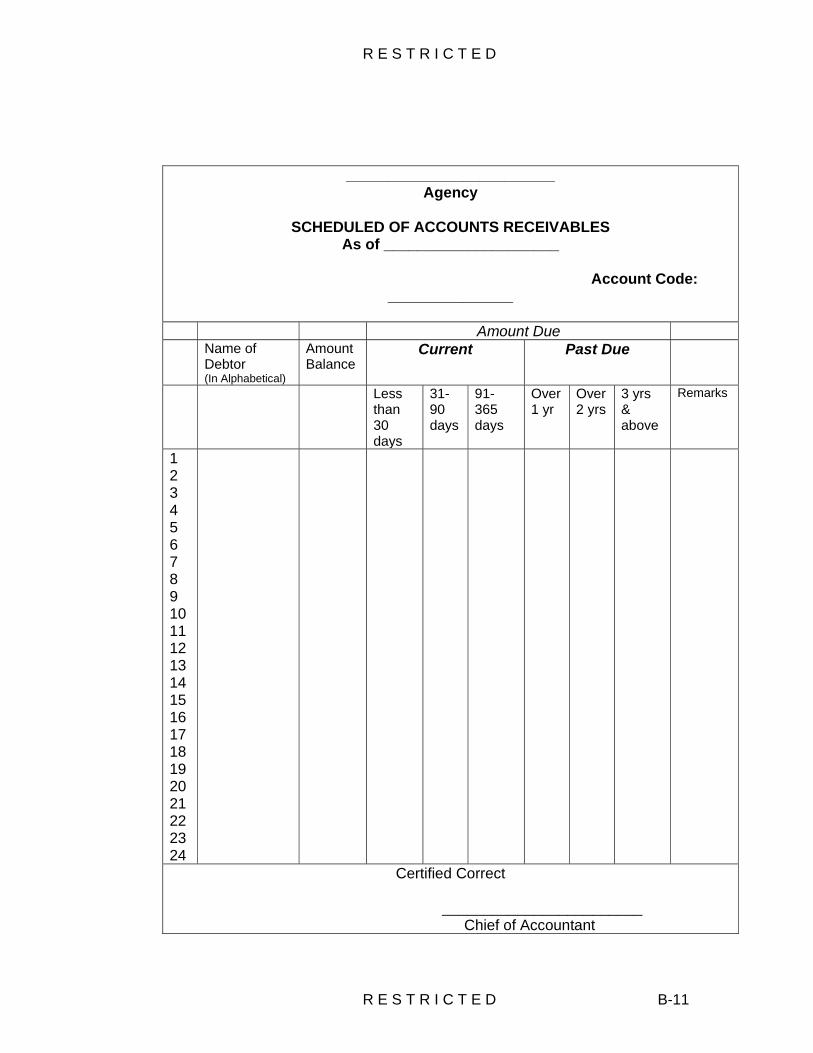

a. Schedules of Accounts Receivables (SAR)

b. Schedules of Accounts Payables (SAP)

c. Statement of Allotments, Obligations and Balances (SAOB)

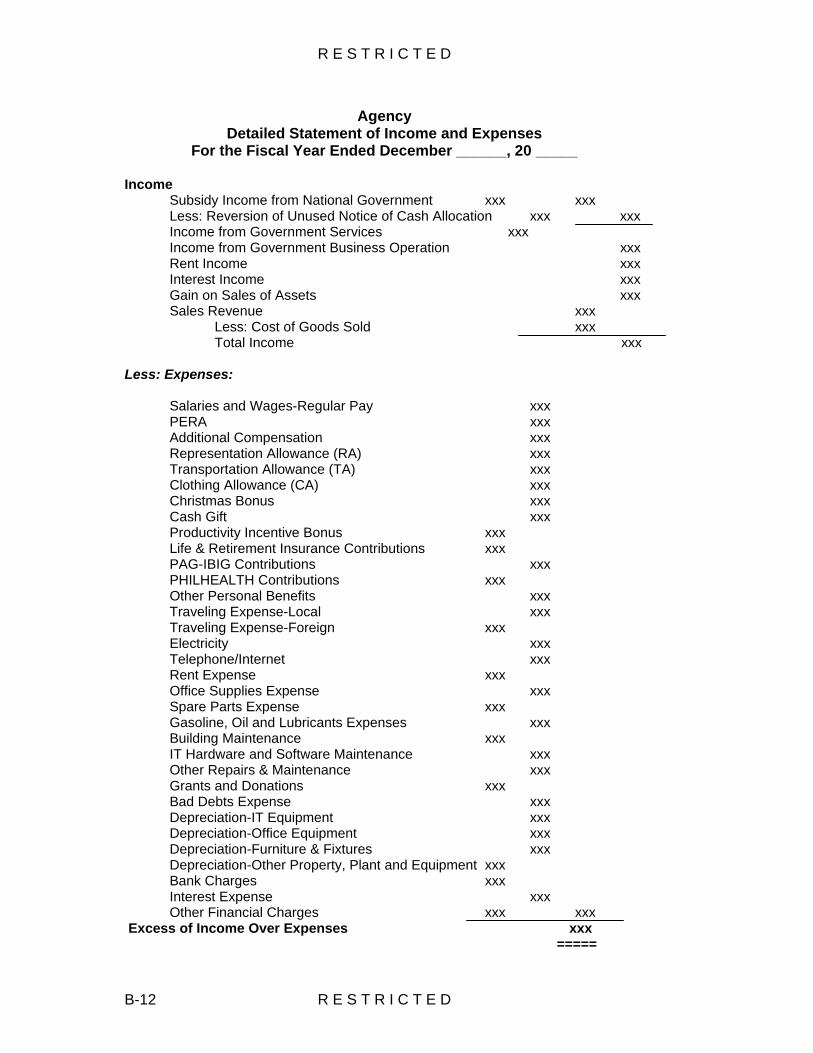

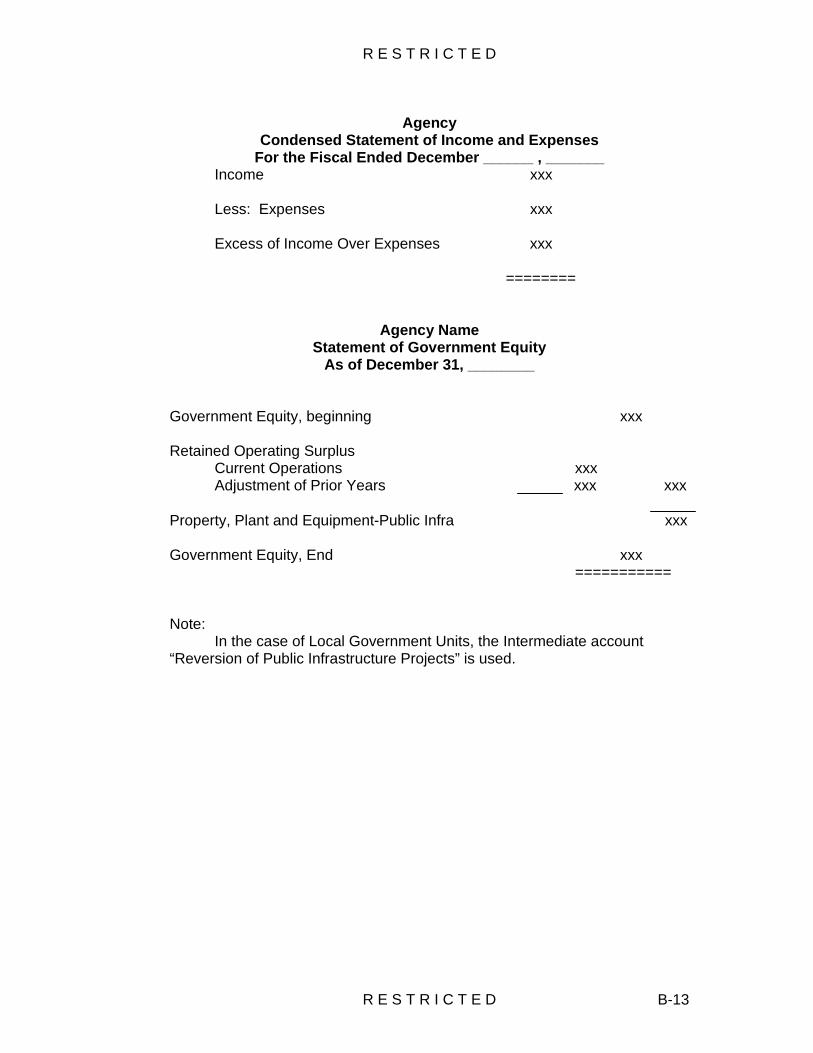

d. Other schedules as may be required 16. Statement of Income and Expenses. This shows the results of operation/performance of the agency at the end of a particular period. It is prepared from information taken direct from the Pre-Closing Trial Balance.

R E S T R I C T E D

R E S T R I C T E D 3-9

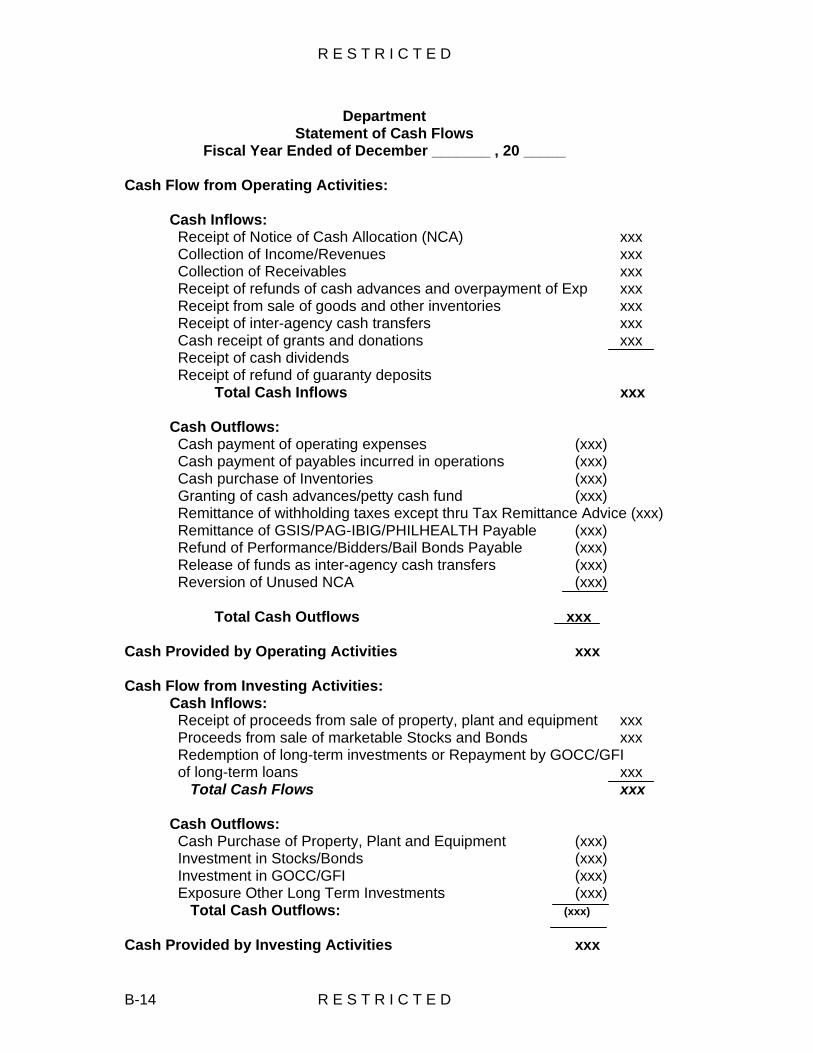

17. Statement of Government Equity. This shows the financial transactions which resulted to the change in Government Equity account at the end of the year. 18. Statement of Cash Flow. This is a statement summarizing all the cash activities of an agency. These include the operating, investing and financing activities of the entity and provide information on the cash receipts and cash payments during the period. 19. Status of Appropriations, Allotments, Obligations, Liquidations, and Balances. This shows a detailed statement of releases, obligations, liquidations, and balances as to expense and object classification. It is prepared quarterly. 20. Statement of Monthly Charges to Accounts Payable. This shows the monthly liquidation to Accounts Payable and is submitted to DBM and COA. 21. Summary List of Checks Issued (SLCI). This report shows the amount of MDS check disbursements for a given period, is prepared monthly and is submitted to DBM as its basis in issuing the NCA. 22. Report of Income. This shows the monthly collection of income deposited with the Bureau of Treasury. It is prepared annually and is submitted to DBM and COA.

23. Status of Cash Advance. This report shows the list of Fund Accountable Officers indicating therein the amount of unliquidated cash advances. It is prepared quarterly for submission to COA and DBM.

24. Bank Reconciliation Statement. This report is prepared monthly for each current account for submission to COA.

Section 3-8 Flow of Claims

25. Flow of Commercial Claims for Current Year

a. Unit Project Administrator. Prepares contract and supporting documents depending on Mode of Procurement.

b. Comptroller. Prepares ALOBS, submits contract and ALOBS to

accounting.

c. Accounting Services/FAU. Assigns ALOBS number, certifies availability of funds and returns contract to unit.

R E S T R I C T E D

R E S T R I C T E D 3-10

d. Procuring Unit. Serves contract to supplier, receives and inspects objects of contract, notifies COA and Pre-Audit for the inspection, prepares DV & supporting documents and submits DV to Acctg Services/FAU.

e. Head of Unit/Agency. Approval of contract and approval of DV.

f. Acctg Services/FAU. Checks and certifies propriety and completeness of DV and supporting documents.

g. Pre-Audit. Performs pre-audit functions, conducts inspection of deliveries upon notification and issues Pre-Audit Inspection Report.

h. FCPA/FSU. Issues check to claimant 26. Flow of disbursement voucher for prior year claims prior years with funding:

a. Pre-Audit. Pre-Audit Claims and approve amount of payment. b. Accounting Services. Prepare listing of DV for certification,

verification by COA.