rabobank foundation social impact report · pdf filebehaviour is – and why it’s...

TRANSCRIPT

Netherlands P06

Developing countries P14

‘Proud of our cooperative

ventures’Pierre van Hedel Key figures

P03

Statistics

Jacques Diouf AwardReal commitment to smallholder self-reliance p.12

NetherlandsP06

Developing countriesP14

‘Proud of our cooperative

ventures’cooperative

ventures’cooperative

Pierre van Hedel Key figures P03

Statistics

Jacques Diouf AwardReal commitment to smallholder self-reliance p.12

RABOBANK FOUNDATION

SOCIAL IMPACT

REPORT 2017

Netherlands P07 FINANCIAL SELF-RELIANCE

P09 SOCIAL ENTREPRENEURSHIP

Developing countriesP15 AFRICA

P17 LATIN AMERICA

P19 ASIA

Together withP08 GELDFIT

P10 I-DID

P15 MUSONI

P17 CENCOIC

P19 PRADAN

Cooperation with the FAOP13 REAL COMMITMENT TO SMALL-

HOLDER SELF-RELIANCE

This magazine is published by Rabobank in cooperation with

Avance. The data in this publication refer to the 2016 fi nancial year

and are taken from an extensive research report. Those interested

in obtaining a copy of the report can email

Text: Schrijf-Schrijf

Design: Volta_thinks_visual

Copyright: 2017 Rabobank Foundation

People who want to get ahead. Who are fi nancially vulnerable, but working as

hard as they can to become self-suffi cient. It’s those people that we at

Rabobank off er a helping hand.

In the Netherlands, we’re working to help almost 600,000 men, women and

children. And in Africa, Asia and Latin America our eff orts benefi t some fi ve

million smallholders. Which programmes and resources are we deploying to

this end? And what kind of impact are we making? You can read all about it

in this magazine.

We’re not only one of the largest corporate foundations in the Netherlands; at

43 years old we’re also one of the oldest. As managing director I’m often asked

what I’m most proud of. That’s a diffi cult question, because there’s so much to

be proud of. But if I have to name just one thing, it would be: cooperation.

The cooperation within our team, that’s tight-knit and well-informed. And the

cooperation between this team and the professionals who off er us the benefi t

of their expertise. The cooperation between our foundation and partner

organisations. And of course, the cooperation among smallholders who see that

unity is strength, combining forces with one another and with our partners.

I’m also impressed by the fi nancial support we receive. And the trust and

confi dence it refl ects in us. Support that comes from local Rabobanks, from

Rabobank Netherlands and from Rabobank clients such as companies and

wealthy members of the public. And last but not least from Rabobank staff

who donate several euros every month. Without this support, we wouldn’t be

able to do what we do, and we’re very grateful for it. We hope that the results

we have achieved will bolster that commitment. So that we can extend our

work. And so that yet more people will be able to become self-reliant.

Pierre van HedelManaging director, Rabobank Foundation

‘Proud of our cooperative ventures

- internally and externally’

2 Rabobank Foundation content

SUPPORTED 43 Dutch organizations

23 focus countries* incl.Netherlands

288 foreign organizations

PROJECTS DEVELOPING COUNTRIES

TRAINING

4,681 staff and board members trained

208,945 farmers gained 70% were women

PROJECTS NETHERLANDS

109,329VOLUNTEER WORKERS

1,231 PEOPLECOMPLETED EDUCATION AND TRAINING

NUMBER OF PEOPLE GAINING ACCESS TO

SPORT 63,736NUMBER OF CHILDREN OFFERED SUPPORT

Almost 5,5 million people

TOTAL OUTREACH

INVESTED €27,967,240

(including investments by the Rabo Foundation Client Fund and

the Rabo Foundation Employees’ Fund)

Through our project partners

A V E R A G EINCREASE IN FARMER INCOMES13 c

KG

596,907 vulnerable people

Netherlands

4,886,869smallholders

Developing countries

* In 2016 we made exceptions in four extra countries Burkina Faso, Burundi, Mali and Myanmar.

5,608MINIMUMINCOME F A M I L I E S

RABOBANK FOUNDATION

Impact Insights 2017 Each year Rabobank Foundation measures the impact of its activities. We do this together with our project partners, who contribute to our research.

3Rabobank Foundationimpact

See the i-did project on page 10

596,907 VULNERABLE PEOPLE

109,329 VOLUNTEER WORKERS

Foundations Social enterprises

Donations

Loans

€2,739,000

€290,000

Together with: 103 local banks

43

€ 3 million

Rabobank Foundation: what we do

How we workBoosting people’s self-reliance all over the

world. That’s Rabobank Foundation’s most

important objective. To achieve our goal, we

support organizations in the Netherlands and

in 22 developing countries in Africa, Asia and

Latin America. We do so with funds, expertise

and the active deployment of our network.

4 Rabobank Foundation What have we achieved?

How we help people in the NetherlandsIn the Netherlands, we work together with

non-profi t organizations and social enterprises

working for and with vulnerable people.

That way we ensure that people who are

disadvantaged on the labour market fi nd a

suitable job. Or that people regain fi nancial self-

suffi ciency. Just as we do abroad, this is done

through the deployment of funds (donations or

loans), expertise and our network.

Paid and/or meaningful work

Financial health

Social network

Vitality

ULTIMATE OBJECTIVE: CONTRIBUTING TO SELF-RELIANCE THROUGH

Prospects Self-confidence Pride Self-esteem

PEOPLE WHO GAIN SUPPORT THROUGH OUR PROJECTS HAVE MORE

Go to page 16-17

See collaboration with Musoni on page 14-15

5Rabobank FoundationWhat have we achieved?

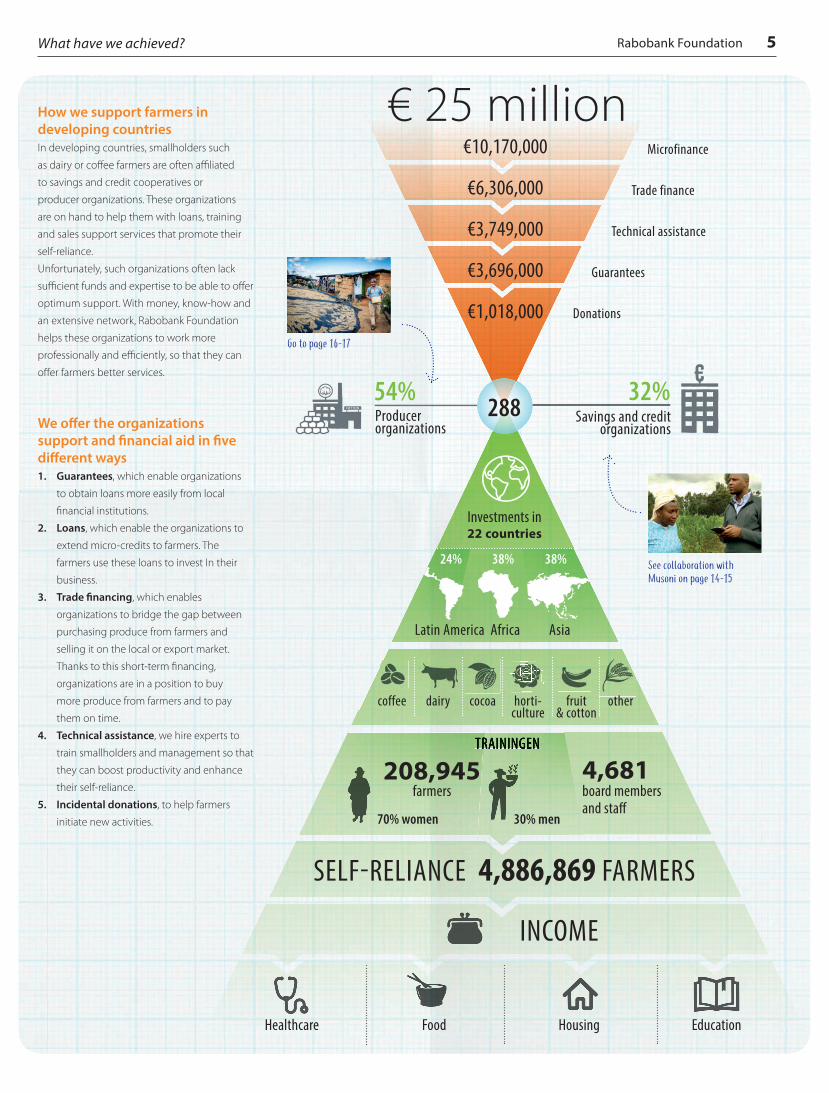

€ 25 million€10,170,000

€6,306,000

€3,749,000

€3,696,000

€1,018,000

INCOME

SELF-RELIANCE 4,886,869 FARMERS

Healthcare Food Housing Education

Producer organizations

Savings and credit organizations

Investments in 22 countries

Microfinance

Trade finance

Technical assistance

Guarantees

Donations

Latin America Africa Asia

54% 32%

24% 38%38%

TRAININGENTRAININGENTRAININGENTRAININGEN

208,945 farmers

4,681 board members and sta�

30% men70% women

288

How we support farmers in developing countriesIn developing countries, smallholders such

as dairy or coff ee farmers are often affi liated

to savings and credit cooperatives or

producer organizations. These organizations

are on hand to help them with loans, training

and sales support services that promote their

self-reliance.

Unfortunately, such organizations often lack

suffi cient funds and expertise to be able to off er

optimum support. With money, know-how and

an extensive network, Rabobank Foundation

helps these organizations to work more

professionally and effi ciently, so that they can

off er farmers better services.

We off er the organizations support and fi nancial aid in fi ve diff erent ways1. Guarantees, which enable organizations

to obtain loans more easily from local

fi nancial institutions.

2. Loans, which enable the organizations to

extend micro-credits to farmers. The

farmers use these loans to invest In their

business.

3. Trade fi nancing, which enables

organizations to bridge the gap between

purchasing produce from farmers and

selling it on the local or export market.

Thanks to this short-term fi nancing,

organizations are in a position to buy

more produce from farmers and to pay

them on time.

4. Technical assistance, we hire experts to

train smallholders and management so that

they can boost productivity and enhance

their self-reliance.

5. Incidental donations, to help farmers

initiate new activities.

coffee dairy cocoa horti-culture

fruit & cotton

other

Financial self-reliance

Roelie van Stempvoort

was one of the founder

members of the Rabobank

Foundation’s programmes in

the Netherlands. She is

programme manager for the

programmes ‘All kids take

part’, ‘Financial self-reliance’

and ‘Sport without limits’

‘We help people to become fi nancially self-reliant’The Netherlands numbers more than 3,4 million people in fi nancial diffi culties. Together with

other organizations, Rabobank Foundation aims to boost Dutch people’s fi nancial self-reliance.

Programme manager Roelie van Stempvoort explains how.

‘All kids take part’The number of children reached by a project5,608

society some €11 billion annually, for example

through absenteeism caused by fi nancial

worries plus the costs incurred by local

authorities for social relief or youth care.’

QA

How does Rabobank Foundation

attempt to prevent � nancial problems?

‘By, for example, supporting programmes that

help people to budget successfully. In the

‘Financial Self-suffi ciency’ programme, we’re

working together with national partners such

as the National Institute for Family Finance

Information Nibud, community organization

Humanitas, debt aid foundation

QA

How big is the problem of debt and

poverty in the Netherlands?

‘There are a large number of problem debts in

the Netherlands. One in fi ve Dutch households

are so far in arrears that they can be termed as

having problem debts.’

QA

How debilitating is it to have � nancial

problems?

‘Financial problems can happen to anyone, and

the impact is huge. People can become socially

isolated and stop using healthcare services.

Children are unable to join in with their peers.

What’s more, fi nancial problems cost Dutch

SchuldHulpMaatje and social inclusion

cooperative Mee.nl.

We support initiatives that contribute towards

building fi nancial awareness as well as

helping to further develop fi nancial awareness

programmes. In this way, we reached out to

some 54,000 people in 2016. We trained

volunteer workers in Thuisadministratie,

which supports people in managing their

household accounts, so enhancing their ability

to respond to requests for help. And we

boosted money awareness among young

people through a series of lesson programmes

on managing money.’

53,658 people helped

31,352 Lessons programme/awarenessDealing with money

17,056 Assistance with home �nances

5,000 Other �nancial self-reliance

SpecificationNumber of people reached:TOGETHER WITH 5 ORGANIZATIONSOUTREACH TO:

53,658P E O P L E

6 Rabobank Foundation

QA

Why is awareness so important in

tackling � nancial problems?

‘People only become fi nancially self-reliant

once they know or learn what healthy money

behaviour is – and why it’s important. It’s also

key they gain an insight into their fi nancial

situation, the possible consequences of being

in debt and what kind of fi nancial products and

services are available. We always support

projects and programmes that help to foster

such awareness.’

QA

What does Rabobank Foundation do

for children growing up in minimum-

income households?

‘That holds true for one in eight children in the

Netherlands. For them we run the ‘All kids take

part’ programme, working together with the

Youth Culture Fund, Youth Sport Fund and the

Leergeld foundation. Thanks to this

programme, more than 5,500 children were

able to take part in school activities or become

members of a sports club or cultural institution

in 2016.’

QA

How do you keep your programmes up

to date?

‘Through ongoing dialogue with our project

partners. For example, last year we organized a

brainstorm session with our partners Nibud,

SchuldHulpMaatje and literacy promotion

foundation Stichting Lezen en Schrijven. We

also invited health insurers Zilveren Kruis and

Achmea as well as telecoms provider T-Mobile

and energy company Nuon. Together we

wanted to explore the issue of how we could

identify money problems at an even earlier

stage and help prevent them.’

QA

What insights did you gain from the

session?

‘Two key insights came to the fore. Stichting

Lezen en Schrijven showed us how many

fi nancial problems stem from poor literacy.

And SchuldHulpMaatje contributed valuable

insights into Dutch neighbourhoods where

the risk of problem debts is greatest. Using

this information we were able to reach out to

people in fi nancial diffi culties. At the end of

the day we came to the conclusion that it was

time for a fresh initiative, and that’s led to the

creation of a new online platform: Geldfi t.nl.’

(See box).

QA

Rabo Foundation as a driving force?

‘Certainly. As a foundation we’re in a

position to give new initiatives a chance and

to foster awareness within the Rabobank

organization. We played a key role in setting up

Geldfi t.nl by facilitating the dialogue and

fi nancing the pilot. That was important, but we

haven’t stopped there. We’re now involved in

helping to devise a way of rolling out the

initiative further nationwide and making it

independent.’

Geldfit – How it works in practice

Financial problems resolvedA family from Zwolle with three children was in fi nancial diffi culties. Matters were made worse when their debt administrator failed to pay their health insurance premiums for six months as a result of which the family looked to be forced to foot the bill for their children’s high care costs themselves.

Via the online platform Geld� t.nl the family came into contact with SchuldHulpMaatje Zwolle. The organization helped them to stabilize their � nancial situation and to change their administrator. What’s more, SchuldHulpMaatje Zwolle had close contacts with health insurer Zilveren Kruis’s escalation team, which allowed all the parties involved to

work together in � nding a solution. The family received restitution for the cost of the children’s medical care and was able to work towards a debt-free future.

How Geldfi t.nl worksThe objective of Geld� t.nl is that people with money worries don’t end up In � nancial di� culties. They � ll out a short questionnaire on the website, and are given a list of tips, tools and voluntary organizations in their area able to help them with their � nancial a� airs. Partners in the initiative comprise national and regional organizations such as SchuldHulpMaatje, Huma-ni tas, Stichting Lezen en Schrijven, Zilveren Kruis, Sallandse Dialoog and Rabobank Foundation.

7Rabobank FoundationNetherlands

Social entrepreneurship

Alongside selling products or services, many companies are keen to

serve society – by supporting the vulnerable in society, for example.

‘The number of social enterprises is growing and they represent a

key player in society,’ says Nynke Struik, programme manager at

Rabobank Foundation.

1,231 Training completed

395 On-the-job training

508 Fixed and temporary employment contractd

131 Sheltered placement

217 Internship

Transition into workEducation completed

Nynke: ‘The state has too few resources to

solve all of society’s problems. That’s why

it’s good that the number of social

enterprises in the Netherlands is growing. They

off er added value for society. After all, social

entrepreneurs off er innovative solutions for

social challenges.’

Focus and expertise‘We help social entrepreneurs to become self-

suffi cient’, Nynke explains. ‘We focus particularly

on companies that off er places within their

organization to people who are disadvantaged

in their eff orts to fi nd work. Examples are men

and women who have been on welfare for a

long time, young people without qualifi cations

and people who are learning impaired, have a

physical impairment or suff er psychological

problems.’

The majority of social enterprises train these

vulnerable people and supervise their transition

into paid work. ‘We feel it’s important that

everyone has the opportunity to work’, says

Nynke. ‘Because having a job means having an

income, access to a social network and

generates self-esteem.’ Among other things,

Rabobank Foundation supports social

enterprises by off ering them expertise. ‘Through

us, they can follow a Rabobank MiniMaster

course or a course in Social Entrepreneurship at

Nyenrode Business University’.

That’s very useful, says the programme manager:

‘Social entrepreneurs who are starting out can

often use extra help in business management.’

Money and respect‘Businesses starting out often have high initial

costs due to the fact that they invest heavily in

training their workforce. That means they can’t

always easily access fi nance,’ says Nynke. In many

cases they can obtain credit from Rabobank

Foundation. ‘We agree targets with them – such

as the number of people that they manage to

transition into paid work via their enterprise.’

For Rabobank Foundation in the Netherlands,

extending credit is new. ‘Up until 2016, we only

gave donations to this type of enterprise,’ says

Nynke. ‘My background is in commercial lending

and I believe that social entrepreneurs, too,

should work towards a profi table business

model and thus should be in a position to pay

interest and redeem the principal. By giving

them a loan, Rabobank Foundation is taking

social entrepreneurs seriously, viewing them as a

real business. That’s a form of respect. What’s

more, when loans are paid off it means we have

more funds to support a greater number of

initiatives as a result of which we can make an

even bigger impact.’

‘Helping entrepreneurs achieve their goals’

Nynke Struik

has been working at Rabobank

Foundation since 2016 as

programme manager social

enterprises. Prior to joining the

foundation, she worked in the

commercial credit sector and has

always been active in fi nancing

enterprises from small to large. Number of people who successfully completed a course of education or went on to find work 2,482

8 Rabobank Foundation

1. What is i-did?Founder Mireille Geijsen: ‘i-did makes a wide

range of design products, from handbags to

laptop sleeves, which are sold throughout the

Netherlands. We make them using recycled

textiles. The goods are produced in part by

vulnerable people who have diffi culties in

gaining a foothold on the labour market. At i-did

they acquire employee skills, grow as people

and rediscover their enthusiasm for work.’

2. Why does Rabobank Foundation support i-did?Rabobank Foundation programme manager

Nynke Struik: ‘i-did’s social objective dovetails

with the Foundation’s mission. And we saw

that they urgently required fi nancing. Mireille

had attracted furniture giant Ikea as a new

client, and for this she needed to ramp up

production and train new staff . So we aided

her enterprise with a loan, as part of a

co-fi nancing arrangement with the DOEN

Foundation.’

3. What was the social impact generated by the loan?Mireille Geijsen: ‘We made an agreement with

Rabobank Foundation that through our

company more people would transition into

education or paid work. To achieve this

objective, we take people on for six months of

work and training. We help them gauge where

their talents lie and what steps are required

for progress on the labour market. During

this time, we ready them for participation in

training and education or to apply for a job.

Onward placements are already up from 0 to

25 percent.’

4. And what does the future bring?Nynke: ‘i-did is achieving good results. The

challenge now is for the enterprise to remain

profi table and to grow, so that it can

generate an even greater impact.’ Mireille

Geijsen: ‘We look forward to a bright future.

The cooperation with Rabobank Foundation

is an important support. They’re accessible,

enthusiastic, think along with us, identify

opportunities and act as ambassador. The

Foundation is an unbelievably good partner

to have.’

4 QUESTIONS ABOUT I-DID Social enterprise rekindles people’s will to work

Netherlands 9Rabobank Foundation

Highlights

6 highlights Molly Koyekyemga (UGANDA)ACPCU member

‘Producer organization ACPCU taught me

how to boost the yield and quality of my

coff ee crop. I learned for example that coff ee

benefi ts from being grown alongside other

crops. That’s why I now also grow bananas

and eucalyptus trees. I was also able to get a

loan via the ACPCU which I used to invest in

soil improvement.’

Worldwide, we reached almost 5,5 million people.

Here we share some of their personal stories.

10 Rabobank Foundation

Walter (NETHERLANDS)Participant in ITvitae training programme

‘ITvitae’s Software Development training programme gave

me a fresh start. Due to my autism, I ended up on welfare

support several years ago. Getting off benefi ts is diffi cult but

this course will help me. I’m going to work like crazy for a job

as an ICT professional!’

Bui Thi Hoa (vietnam)Member of VietED

‘My husband and I were able to get a loan from VietED, that we

used in part to buy artifi cial fertilizer. I was also able to follow a

training course at VietED. That course taught me how to use the

right amount of fertilizer to boost production and what the best

time is for sowing to obtain bigger fruit. Our yields have increased

and our income has gone up.’

James Owino (KENYA)CFO, Musoni

‘Musoni could never have become so successful without the

help of the Rabobank Foundation. We are keen to further

strengthen and expand our partnership so that we can

have an even greater social impact on the lives of small-scale

farmers in Kenya.’

11Rabobank FoundationHighlights

Ujang Jalaludin ( INDONESIA)KPGS member

‘During one of the KPGS training courses I learned how to grow

a better type of grass to boost milk yields. Thanks to this grass

and the concentrate feed from the cooperative, my cows now

produce one to two more litres of milk daily.

Vilma Moscoso Ayte (PERU)Member of Qori Wasi

‘It’s imperative for us as producers to have a

communal place for the sale of our produce and

to be able to borrow money. Banks are not willing

to lend to us, or set impossible requirements as

regards collateral. Thanks to Qori Wasi we’re able

to take out small loans on reasonable terms. That

way I was able to obtain a loan to build a shed for

my chickens.’

Sociaal ondernemen

to farmer self-reliance’

FAO

In 2015 Rabobank Foundation decided to take

part in the Improved Productivity and Profi tability

Program of the United Nations’ Food and

Agriculture Organization (FAO). The farmers

taking part in the programme require capital to

invest in their agricultural businesses. Thanks to

fi nancing from the Rabobank Foundation and

training programmes by FAO, the participating

farmers are able to buy good seed and hire

people to sow and to weed. As a result, they are

able to utilize more of their land as well as

boosting the productivity per square metre. One

of the women to benefi t from the scheme is

Beatrice Nthambi Kimilu.

GOAL 1An end to poverty

In 2016 Rabobank Foundation reached almost 4,9 million small-scale farmers in developing countries and 590,000 vulnerable people in the Netherlands.Rabobank Foundation invested almost €28 million in total over 2016, of which €25 million in projects in developing countries and €3 million in projects in the Netherlands.

GOAL 2An end to hunger

In 2016 Rabobank Foundation invested in 155 producer organizations and 91 savings and credit institutions in 22 di� erent countries. As a result, these organizations were able to o� er more services to small farmers. In this way Rabobank Foundation stimulates technological development among farmers, enabling farmers in developing countries to produce more and to produce more e� ciently.

GOAL 3To foster the health and welfare of people of all ages

In 2016 Rabobank Foundation supported seven organizations in the Netherlands that promote sporting activities for people with physical and/or learning disabilities. Together these seven organizations reached over 60,000 people.

GOAL 8Decent jobs and economic growth

In 2016 Rabobank Foundation invested in technical support for farmers in developing countries. More than 208,000 small-scale farmers bene� ted, among others through training courses on agricultural methods.

GOAL 17Partnerships for the objectives

Rabobank Foundation actively seeks partnerships to work together to achieve the sustainable development goals. A good example of this is the partnership with the Food and Agriculture Organization (FAO).

OUR CONTRIBUTION TO SUSTAINABLE DEVELOPMENT GOALS

12 Rabobank Foundation

13Rabobank Foundation

Rabobank Foundation is working together with the world food

organization of the United Nations (FAO) to boost the self-suffi ciency

of farmers in developing countries. The FAO rewarded us for our

contribution with the Jacques Diouf Award 2016-2017.

to farmer self-reliance’ ‘Real commitment

Rabobank Foundation wins Jacques Diouf Award

Once every two years the FAO

presents the Jacques Diouf Award

to organizations that have made an

important contribution to improving food

security. Rabobank Foundation was awarded

the prize for its technical and fi nancial

support to producer organizations. These

organizations don’t qualify for micro-

fi nancing or donations, but fail to obtain

funding from commercial banks. ‘Rabobank

bolsters the self-reliance of small-scale farmers

and boosts global food security,’ according to

the jury.

Our impact Together with the FAO Rabobank Foundation

works on projects that off er smallholders access

to fi nancial services, agro-inputs (such as

pesticides and natural and artifi cial fertilizers),

agricultural technologies and other services. As a

result the farmers are able to produce more

effi ciently and boost their incomes. In this way

we contribute to the Sustainable Development

Goals (SDGs) of the United Nations (UN). The UN

objectives focus on ending extreme poverty, on

health, education, clean drinking water,

sustainable energy, reduction of inequality and

tackling climate change.

Improved income Together with the FAO the Rabobank

Foundation aims to make a diff erence for

thousands of farmers in developing countries.

Examples of the impact we had include the

realization of trade fi nancing for 1,500 farmers

in Kenya and training 400 farmers in Ethiopia. In

Tanzania 500 farmers gained access to a new

trading system, as a result of which they now

enjoy an improved income. And 2,000 young

farmers in Uganda gained fi nancing.

Weakest link Annamaria Pastore, responsible at FAO for

cooperative partnerships with the private

sector, says that the cooperation with the

Rabobank Foundation is one of the most

successful to date. ‘The Rabobank Foundation’s

work is very concrete and hands on – the

organization works primarily at a local level.

In addition, the Foundation is always prepared

to look for innovative solutions and to tailor its

approach. Their commitment to supporting

farm businesses that are not easily fi nanced is

commendable. Rabobank Foundation is

really committed to the self-suffi ciency of

these farmers, who represent the weakest link

in the chain.’

‘The Rabobank Foundation’s work is very concrete and hands on, and they are always prepared to look for innovative solutions’

ANNAMARIA PASTORE FAO

via a mobile phone’‘Access to money

Through Rabobank Foundation’s aid to 91 savings and credit organizations and micro-fi nancing

institutions, small-scale farmers from Africa and elsewhere gain access to fi nancial services

more easily. That facilitates their ability to borrow and invest in their businesses. ‘One of the

organizations making this possible is Musoni. And what’s more, they do it in a very

innovative way,’ says Madelon Pfeiff er, programme manager at Rabobank Foundation.

In Kenya, many smallholders have few savings

and live in remote areas. That makes access to

fi nance even more diffi cult. In 2009 Musoni

came up with an interesting concept for issuing

credit to this target group in particular. Via a

mobile phone. That way it’s easier to borrow,

because no cash or paperwork is required. In

addition Musoni visits the farmer with a tablet

to make the credit application so that the

farmer needn’t go to the bank which is often

situated many miles away. In this way Musoni

launched a new method of fi nancing for small-

scale farmers onto the market.

Very fi rst fi nancial backer‘We believe in Musoni’s innovative solution.

That’s why we decided in 2009 to become

their very fi rst fi nancial backer,’ says Pfeiff er.

‘The support was key to Musoni’s growth in

Kenya. Because fi nancing via a mobile phone

didn’t yet exist in practice, the organization

found it diffi cult to attract funds from other

parties. Rabobank Foundation took part

because we believe that good innovation

can benefi t farmers and their families. A key

condition for our loan to Musoni was that they

would off er farmers equitable interest rates.’

This is an example of how Rabobank

Foundation also focuses on innovative projects.

Innovation is crucial, because it can off er

solutions to small farmers, such as easier access

to loans, improved insight into the terms of a

loan and the ability to gain credit faster. ‘But

innovation costs both time and money,’ says

Rabobank Foundation Rabobank Foundation works together with Musoni* in Kenya

Pfeiff er. ‘This new way of gaining credit was also

new for the farmers. Many farmers weren’t used

to mobile money and initially thought that they

needn’t pay it back. So Musoni off ered

workshops to create the awareness that it

wasn’t possible to borrow without repayments.

Musoni also found it helped to send sms

messages to remind farmers they needed to

make repayments. In addition farmers can

check the status of their loan via their mobile.’

Families benefi t‘Farmers not only benefi t fi nancially from a loan

from Musoni. It also has positive results socially.

As soon as the farmer’s business improves, he’s

able to pay his children’s school fees, for

example. Other farmers see that and want the

same. In this way, savings and credit

organizations or micro-fi nancing institutions

that do their work well garner more and more

members, who increasingly become more

prosperous. That leads to more savings being

managed for them by the organization, that can

in turn support more farmers and, in the longer

term, stand on its own two feet.’

Madelon Pfeiff er

has been working at

Rabobank Foundation

since 2015 as programme

manager Africa.

How does Musoni work?Each member fi rst registers with mobile money platform M-PESA, which is extremely popular in Kenya. Musoni has linked its systems to M-PESA. After registration, members are able to apply for a loan from Musoni, either individu-ally or as a group. Loan offi cers help them with their applications; monitoring their investment plans, explaining how ‘mobile money’ works and checking the required documents and/or digital documents. Once everything is in order, Musoni furnishes the credit.

*Musoni: an abbreviation of ‘mobile usoni’, which is Swahili for ‘mobile future’.

14 Rabobank Foundation Financing

REACHED 1,410,421SMALL FARMERS IN AFRICA

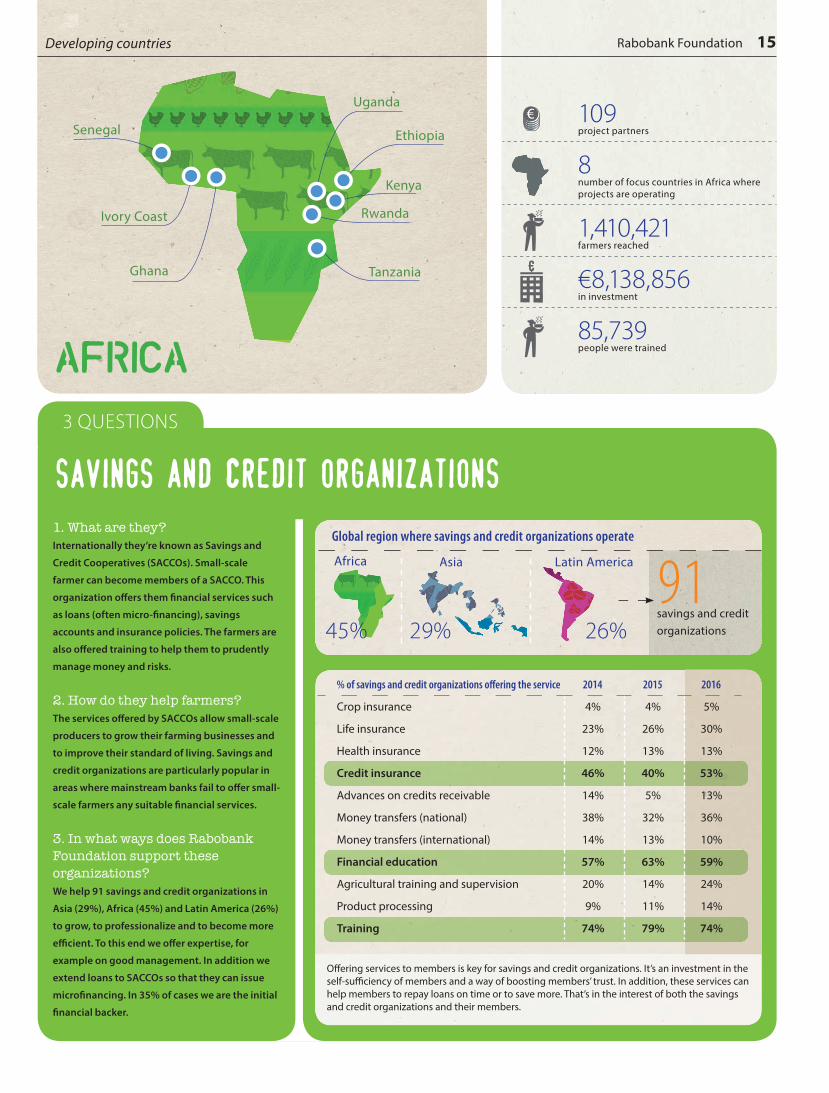

1. What are they?Internationally they’re known as Savings and

Credit Cooperatives (SACCOs). Small-scale

farmer can become members of a SACCO. This

organization off ers them fi nancial services such

as loans (often micro-fi nancing), savings

accounts and insurance policies. The farmers are

also off ered training to help them to prudently

manage money and risks.

2. How do they help farmers? The services off ered by SACCOs allow small-scale

producers to grow their farming businesses and

to improve their standard of living. Savings and

credit organizations are particularly popular in

areas where mainstream banks fail to off er small-

scale farmers any suitable fi nancial services.

3. In what ways does Rabobank Foundation support these organizations? We help 91 savings and credit organizations in

Asia (29%), Africa (45%) and Latin America (26%)

to grow, to professionalize and to become more

effi cient. To this end we off er expertise, for

example on good management. In addition we

extend loans to SACCOs so that they can issue

microfi nancing. In 35% of cases we are the initial

fi nancial backer.

SAVINGS AND CREDIT ORGANIZATIONS

3 QUESTIONS

Uganda

Rwanda

Tanzania

Senegal

Ivory Coast

Ghana

109project partners

8number of focus countries in Africa where projects are operating

1,410,421farmers reached

€8,138,856in investment

85,739people were trained

AfriCa

% of savings and credit organizations off ering the service 2014 2015 2016

Crop insurance 4% 4% 5%

Life insurance 23% 26% 30%

Health insurance 12% 13% 13%

Credit insurance 46% 40% 53%

Advances on credits receivable 14% 5% 13%

Money transfers (national) 38% 32% 36%

Money transfers (international) 14% 13% 10%

Financial education 57% 63% 59%

Agricultural training and supervision 20% 14% 24%

Product processing 9% 11% 14%

Training 74% 79% 74%

O� ering services to members is key for savings and credit organizations. It’s an investment in the self-su� ciency of members and a way of boosting members’ trust. In addition, these services can help members to repay loans on time or to save more. That’s in the interest of both the savings and credit organizations and their members.

Ethiopia

Kenya

15Rabobank FoundationDeveloping countries

45%

Global region where savings and credit organizations operate

91savings and credit organizations

Latin America Africa Asia

29% 26%45%

Global region where savings and credit organizations operate

91savings and credit organizations

Latin America Africa Asia

29% 26%

Knowledge

a better future’‘Better coffee =

Rabobank Foundation supports 155 producer organizations. Of these

44% are coffee cooperatives, mostly from Latin America. Our expertise

can be of immense value in helping cooperatives expand, as in the case

of CENCOIC in Colombia. A chance encounter during a coffee trade fair in

Seattle marked the start of a partnership.

‘A a small coffee farmer in Colombia you

come up against a range of obstacles,’

says Isabel van Bemmelen, programme

manager at Rabobank Foundation. ‘Take the

Cauca region, for example, an area that for many

years has been ravaged by rebel movement

FARC. Many farmers there have been driven off

their land. Nor are banks willing to lend to the

indigenous population. The CENCOIC

organization offers solutions, and we help them.’

‘Our support for producer organizations is

growing. In Latin America, we’re mainly involved

with cooperatives for small-scale indigenous

coffee farmers. Like the Central Cooperativa

Indigena de la Cauca – CENCOIC for short.

During the Specialty Coffee Expo in Seattle in

2013 the manager of CENCOIC told me that his

cooperative lacked access to financing. His

account had such urgency that just a week later I

was on my way to the Colombian region to pay

them a visit. That’s when our partnership began.’

Better coffee‘Our aid to CENCOIC included financing for a

coffee laboratory. In this lab the cooperative

tests the quality of the coffee. That’s imperative

in order to distinguish between the different

qualities of coffee and subsequently to identify

the best markets for the different coffee grades:

export or local. That’s because exporters pay

more than buyers on the local market, and also

more than the Colombian government, which

buys up all the unsold coffee at a standard rate,

regardless of its quality.

‘CENCOIC helps all its members to produce

good quality coffee; preferably organic because

that’s better for the environment and often

more attractive for export. An increasing

number of farmers are managing to attain the

required level of quality, but not all. Coffee that

CENCOIC is unable to sell on the export market,

in part because of this poor quality, it sells

locally and to the FNC.

‘Together CENCOIC and Rabobank Foundation

conducted research into the type of financial

support most suited to this differentiation in

sales markets. It transpired that loans in local

currency were the best for sales on the local

market, while trade financing in US dollars was

best for export. We adhere to these insights in

furnishing credit. As a result CENCOIC is able to

find buyers for its coffee, even though the

demand for fair trade coffee has since declined.’

Better future‘CENCOIC’s approach has attracted an

increasing number of farmers from the region.

They are keen to become members of a

cooperative that will always buy their coffee –

even if that’s partly at local market prices or

below. The price is higher and above local

market rates when the coffee is of good quality.

‘Thanks in part to our support, CENCOIC has

grown from 2000 members in 2013 to three

thousand now. The different types of loans

enable the cooperative to sell differing qualities

of coffee on the most appropriate market. This

strengthens the cooperative’s bargaining power.

By offering technical support to farmers around

agronomics, the cooperative also promotes the

production of better quality coffee. That

ultimately results in a better coffee price for

CENCOIC’s members, so helping them to

achieve self-sufficiency sooner.’

Isabel van Bemmelen

worked as programme

manager Latin America

until November 2017,

when she became a

director at Progresso.

16 Rabobank Foundation

3 QUESTIONS

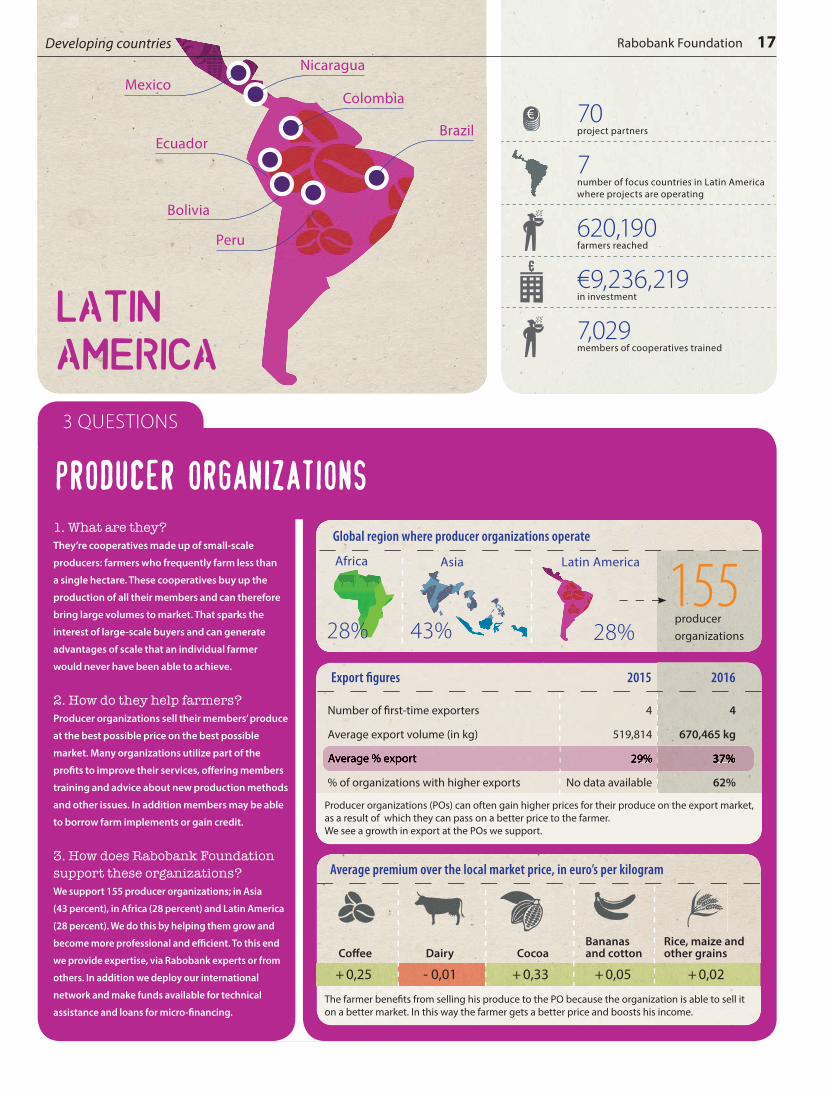

1. What are they?They’re cooperatives made up of small-scale

producers: farmers who frequently farm less than

a single hectare. These cooperatives buy up the

production of all their members and can therefore

bring large volumes to market. That sparks the

interest of large-scale buyers and can generate

advantages of scale that an individual farmer

would never have been able to achieve.

2. How do they help farmers?Producer organizations sell their members’ produce

at the best possible price on the best possible

market. Many organizations utilize part of the

profi ts to improve their services, off ering members

training and advice about new production methods

and other issues. In addition members may be able

to borrow farm implements or gain credit.

3. How does Rabobank Foundation support these organizations?We support 155 producer organizations; in Asia

(43 percent), in Africa (28 percent) and Latin America

(28 percent). We do this by helping them grow and

become more professional and effi cient. To this end

we provide expertise, via Rabobank experts or from

others. In addition we deploy our international

network and make funds available for technical

assistance and loans for micro-fi nancing.

PRODUCER ORGANIZATIONS

Brazil

Peru

Bolivia

Ecuador

Colombia

NicaraguaMexico

LATIN

AMERICA

Export figures 2015 2016

Number of � rst-time exporters 4 4

Average export volume (in kg) 519,814 670,465 kg

Average % export 29% 37%

% of organizations with higher exports No data available 62%

Average % export 29% 37%

Producer organizations (POs) can often gain higher prices for their produce on the export market, as a result of which they can pass on a better price to the farmer.We see a growth in export at the POs we support.

Coffee Dairy CocoaBananas and cotton

Rice, maize and other grains

+ 0,25 - 0,01 + 0,33 + 0,05 + 0,02

Average premium over the local market price, in euro’s per kilogram

The farmer bene� ts from selling his produce to the PO because the organization is able to sell it on a better market. In this way the farmer gets a better price and boosts his income.

70project partners

7number of focus countries in Latin America where projects are operating

620,190farmers reached

€9,236,219in investment

7,029members of cooperatives trained

17Rabobank FoundationDeveloping countries

28%

Global region where producer organizations operate

155producer organizations

Latin AmericaAfrica Asia

43% 28%

in less than 10 years’ ‘Financially self-suffi cient

How do you help organizations really get ahead? Together with Indian

NGO Pradan, Rabobank Foundation set up a cooperative: Madhya

Pradesh Women Poultry Producers Company. Thanks to the partnership,

in 2018 the cooperative can stand on its own two feet fi nancially.

Rishabh Sood explains how. Rishabh, an Indian,

is a local staff member for Rabobank Foundation.

QA

Why did Rabobank Foundation team up

with Pradan in 2009?

‘Pradan is a non-governmental organization

(NGO) in India. Together with them we set up a

cooperative model, to which thousands of

small poultry farmers are affi liated. Around

10,000 women are organized in over twenty

poultry cooperatives that together generated

more than €45 million turnover in 2016.

Rabobank Foundation decided to partner

Pradan in 2009 when farmers appeared to lose

interest in the poultry sector. The poultry

farmers needed to invest in their businesses,

but were unable to obtain loans.’

QA

In what ways do you work together with

Pradan?

‘Indian legislation prohibits Rabobank

Foundation from extending direct loans, but

we are able to stand as guarantor. Because

Rabobank Foundation assumes part of the risk,

local fi nancial institutions are more inclined to

lend to farmer cooperatives and in this way,

they are able to build up a track record with a

local fi nancial institution. However, to realize

this a strong local network is required, that also

closely monitors loan repayments. In addition,

we advise the cooperative on how it can

develop further, we share our expertise on the

agricultural sector and we bring Pradan into

contact with Dutch poultry experts.’

QA

What have the cooperatives achieved

over the last eight years?

‘A lot. With the initial loans of €1500 per farmer,

the farmers built poultry sheds and the

cooperative improved its operational and

fi nancial systems. The farmers also shared their

know-how with other farmers via the National

Smallholder Poultry Development Trust, which

we helped set up. In addition, Dutch poultry

experts on an exchange instructed the farmers

on various aspects of housing poultry, feed,

drinking water systems and vaccinations. The

latest long-term loan has been used by the

farmers to set up a modern feed concentrate

facility, aimed at boosting their production.’

QA

How out of the ordinary is this project

for Rabobank Foundation?

‘Pradan’s type of cooperative model is unique

and so it’s diff erent from the normal cooperatives

we work with. With our cooperative roots, we felt

it would be interesting to help evolve this model.

But our quest to fi nd a way of off ering fi nancing

products to our Indian partners was also interest-

ing. We’re now using the outcome of that search

– the guarantee – extensively throughout India.’

QA

What have your learned from the

partnership with Pradan?

‘That a cooperative should maintain suffi cient

reserves to be able to cope with extreme price

fl uctuations. Only then can you off er farmers

stable prices as a cooperative. If prices fl uctuate

too much, farmers can suff er major problems.

At Pradan we also remarked how important it is

that the affi liated poultry businesses act as one.

A cooperative is like a family, because you have

the same objectives. And you’re dependent on

one another because you’re investing together.’

QA

What does the future hold?

‘It’s looking good! Our aim was to render

the Madhya Pradesh Women Poultry Producers

Company self-suffi cient. We expect this to be

achieved in 2018. That would mean that the

cooperative has become fi nancially independent

in less than ten years. And that the partnership

can justifi ably be labelled a success.’

Rabobank Foundation works together with Pradan in India

Rishabh Sood

is manager of rural and

development banking. He

lives and works in India,

where he has been

Rabobank Foundation local

staff member since 2012.

18 Rabobank Foundation Co-operation

Rabobank Foundation

Rabobank Foundation in IndiaOur know-how and our networks. That’s what

gives Rabobank Foundation added value in

developing countries. We know all about

cooperatives, banking and the agricultural

sector. We deploy this know-how and

expertise to off er opportunities to

smallholders in developing countries. The way

we do this in India diff ers somewhat from in

other countries because by law we cannot

extend direct credit to farmers. However, we

do act as guarantor for loans to groups of

farmers. Over the last four years Rabobank

Foundation issued fi fty guarantees worldwide,

of which most in India. We’re proud of being

the fi rst foundation to launch a guarantee

product for farmers. Our way of working

makes us unique in India. We have gained the

trust of fi nancial institutions because of our

eff ective due diligence and because we

shoulder part of the risk should things go

wrong. And that’s not all. We are closely

involved with the local fi nancial institutions

and the cooperatives we work with. That can

only be achieved because we have our own

presence in India. Rishabh Saood works locally

in India together with two other colleagues.

Azie

‘It’s almost literally a matter of life and death that the partners in the network learn to seek one another out and support one another’

RISHABH SOOD / PROGRAMME MANAGER

Rabobank Foundation

% organizations where board members and members of sta� have received training

Training for management and members of sta�

Average number of board members who received training

2015

30 39

109project partners

7number of focus countries in Asia where projects are active

2,856,258farmers reached

€8,137,857in investment

116,177members of cooperatives trained

ASIA

26 41

2016

2015 38% 2016 28%

Philippines

LaosIndia

Vietnam

Indonesia

CambodiaSri Lanka

Professional organizationsThe support o� ered by Rabobank Foundation can help organizations professionalize so that they gain more con� dence from their members and can expand further. Training management and board members is an important � rst step in professionalizing an organization.

19Developing countries

We can ’t say i t better :

‘The chances of finding paid work are enhanced, so that refugees no longer have to rely on welfare benefits: 30 people already have jobs.’

VLUCHTELINGENWERK NEDERLAND

‘Because youngsters in secondary vocational education are aware of their income and outgoings when they turn 18, they have fewer problem debts and as a result they don’t experience the consequences arising from financial difficulties.’

CODENAME FUTURE, NETHERLANDS

‘The biggest transformation is that farmers gain entrepreneurial vision. Our organization is increasingly being valued as a key element in improving their production conditions and marketing.’

CAFE COLIMA, MEXICO

‘The organization has succeeded in professionalizing its management and in increasing access to markets. The organization is now Utz certified.’

MRERE KIRWA, TANZANIA

‘Rabobank Foundation helped us to fund more micro-credit applicants. And showed us how regulation and advantages work with external commercial parties. And all this at attractive interest rates, enabling us to reduce the organization’s costs.’

ANNAPURNA, INDIA

‘Thanks to the financing we were able to expand the acreage for the cultivation of organic coffee.’

ASOCIACIÓN DE SERVICIOS FINANCIEROS CAFETALEROS, BOLIVIA

‘Thanks to the support from Rabobank Foundation, our organization is able to meet its members’ need for credit. This support has also enhanced the confidence of our members in our organization. We’ve been able to grow and to boost our self-sufficiency.’

CLECAM EJOHEZA, RWANDA

‘Prior to Rabobank Foundation’s support we were unable to run a shop where farmer members could obtain inputs and artificial fertilizer. Our results have improved and we no longer experience difficulties in procuring inputs and artificial fertilizer.’

KOPERASI SERBA USAHA BRITANI SEJAHTERA, INDONESIA

‘The customary procedure of selling the coffee before it’s been dried is changing. Farmers now supply more processed coffee, which fetches a good price. What’s more, farmers are now using coffee’s waste products to fertilize their land. And that’s all thanks to the fact that we’ve become suppliers of Fairtrade coffee.’

BUZAAYA, UGANDA

‘Sportspeople with learning difficulties are socially more assertive and self-confident and as a result have become more self-reliant. Care (and security deposits) have declined. For example, the sportspeople are now using public transport rather than specialized local taxi services.’

BEST BUDDIES FOUNDATION, NETHERLANDS