rates are rising, what happens next? - philip stalcup

TRANSCRIPT

Audit | Tax | Advisory | Risk | Performance Audit | Tax | Advisory | Risk | Performance

Introduction to

June 17, 2016

Interest Rate Risk: Rates are Rising, What Happens Next?

NACUSAC 2016 Conference

Presented by:

Justin Van Beek, CPA

Audit | Tax | Advisory | Risk | Performance Audit | Tax | Advisory | Risk | Performance © 2016 Crowe Horwath LLP 2

When Interest Rates Rise

When the interest rates rise, how will that affect the

Credit Union’s:

• Deposit base?

• Investments?

• Loan portfolio?

Audit | Tax | Advisory | Risk | Performance Audit | Tax | Advisory | Risk | Performance © 2016 Crowe Horwath LLP 3

When Interest Rates Rise

• Will revenue growth keep pace with rising deposit

costs?

• Will there be sufficient deposit funding to meet

increasing loan demand, or will potentially depreciated

securities need to be sold for liquidity?

Most importantly, does the credit union need to

change its strategy now to be better prepared for the

future?

Audit | Tax | Advisory | Risk | Performance Audit | Tax | Advisory | Risk | Performance © 2016 Crowe Horwath LLP 4

Deposits

Interest Rate Risk

• In recent years depositors have been presented with

low interest rates, limited alternative investment

opportunities, and general risk aversion due to market

uncertainty.

• This atmosphere has led many individuals and

businesses to hold excess cash in the form of credit

union deposits.

Audit | Tax | Advisory | Risk | Performance Audit | Tax | Advisory | Risk | Performance © 2016 Crowe Horwath LLP 5

Deposits

• The deposit surge was supported by the near-zero

rate environment and the fact that low interest rates

make it inexpensive for depositors to remain liquid.

• Credit unions experienced a shift in deposit

composition in recent years, from time deposits into

non-maturity products such as money market and

savings accounts.

Interest Rate Risk

Audit | Tax | Advisory | Risk | Performance Audit | Tax | Advisory | Risk | Performance © 2016 Crowe Horwath LLP 6

Deposits

Regulators believe that there is a significant level of

uncertainty for:

• The stability of surge non-maturity deposit balances

• The deposit mix on the balance sheet.

• How rates paid on liabilities will change

Interest

Audit | Tax | Advisory | Risk | Performance Audit | Tax | Advisory | Risk | Performance © 2016 Crowe Horwath LLP 7

Deposits

• While increased volumes of NMDs offer low funding

costs and additional liquidity, new challenges loom

as interest rates begin to inch upward from historical

lows.

• How will rising interest rates affect funding profiles?

• Will changing deposit compositions adversely affect

profitability?

• What impact will increasing rates have on interest rate risk

(IRR)?

Interest Rate Risk

Audit | Tax | Advisory | Risk | Performance Audit | Tax | Advisory | Risk | Performance © 2016 Crowe Horwath LLP 8

Deposits

Credit unions commonly use IRR modeling to

help answer these questions

How might IRR modeling be

affected?

Interest Rate

Audit | Tax | Advisory | Risk | Performance Audit | Tax | Advisory | Risk | Performance © 2016 Crowe Horwath LLP 9

Deposits

IRR models rely on assumptions based on deposit

characteristics.

• By researching these characteristics in the context of your credit

union‘s unique deposit base and applying the knowledge gained

directly to modeling assumptions, the reliability of IRR model

outcomes can be enhanced.

• Poorly determined model assumptions have the potential to

produce misleading output and less-than-optimal decisions,

perhaps impeding credit union management from correctly

mitigating risks.

Interest Rate Risk

Audit | Tax | Advisory | Risk | Performance Audit | Tax | Advisory | Risk | Performance © 2016 Crowe Horwath LLP 10

Deposits

Interest Rate Risk

Understanding the characteristics of your credit union's

deposit base is crucial to determining how rate changes

may affect the credit union's profitability, liquidity, and

exposure to interest rate changes.

Audit | Tax | Advisory | Risk | Performance Audit | Tax | Advisory | Risk | Performance © 2016 Crowe Horwath LLP 11

Deposits

Interest Rate Risk

Audit | Tax | Advisory | Risk | Performance Audit | Tax | Advisory | Risk | Performance © 2016 Crowe Horwath LLP 12

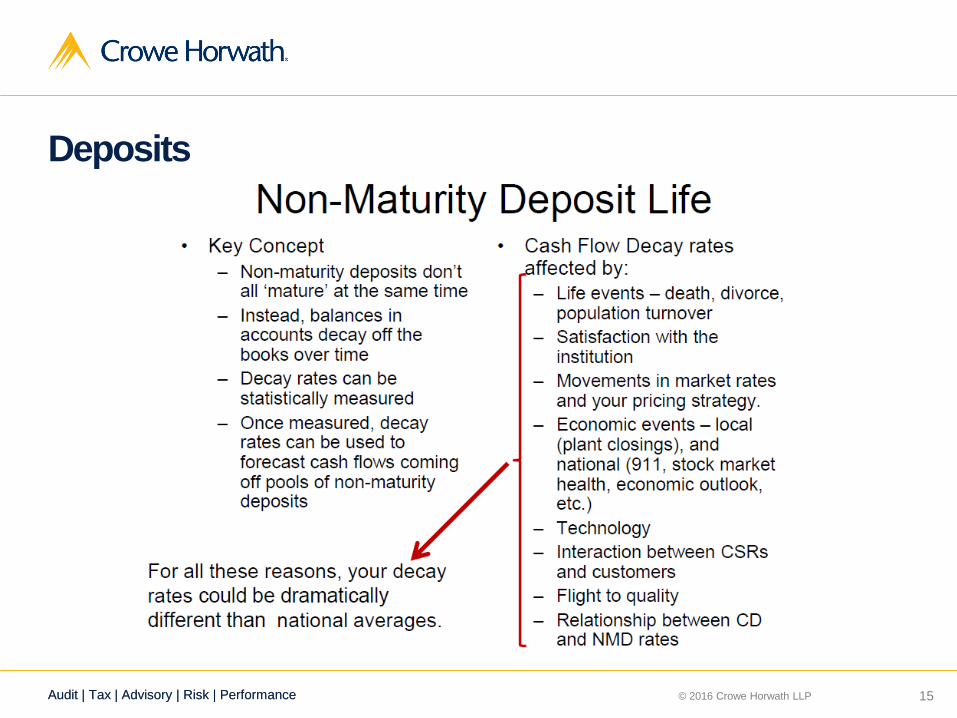

Deposits

Traditionally, NMDs are assumed to be less volatile

than other funding sources.

• Historically interest rates on NMD accounts

respond moderately and slowly in response to

changes in market rates.

• NMD balances are retained for long periods of time

in spite of rate behavior.

Interest Rate Risk

Audit | Tax | Advisory | Risk | Performance Audit | Tax | Advisory | Risk | Performance © 2016 Crowe Horwath LLP 13

Deposits

Given that the low rate environment of the past few years

has been accompanied by deposit growth and shifts in

deposit mix, credit unions should revisit decay rate

assumptions.

The surge in deposit inflows during the post-recession

period may result in decay rates in a rising rate environment

that are more volatile than the stable characteristics

traditionally assumed.

Interest Rate Risk

Audit | Tax | Advisory | Risk | Performance Audit | Tax | Advisory | Risk | Performance © 2016 Crowe Horwath LLP 14

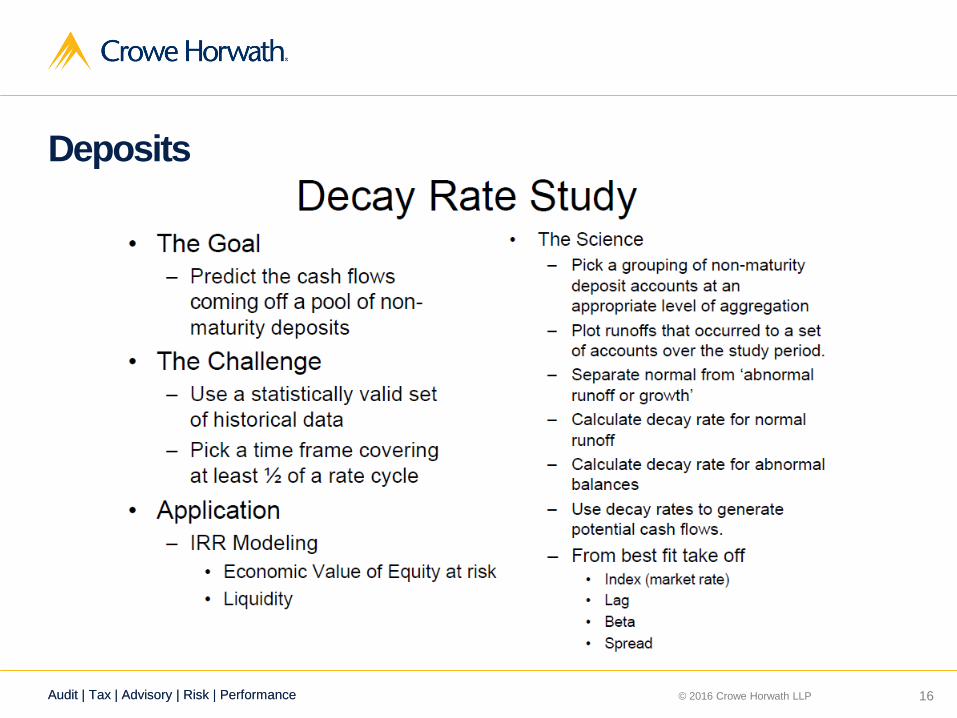

Deposits

hhh

Interest Rate Risk

Audit | Tax | Advisory | Risk | Performance Audit | Tax | Advisory | Risk | Performance © 2016 Crowe Horwath LLP 15

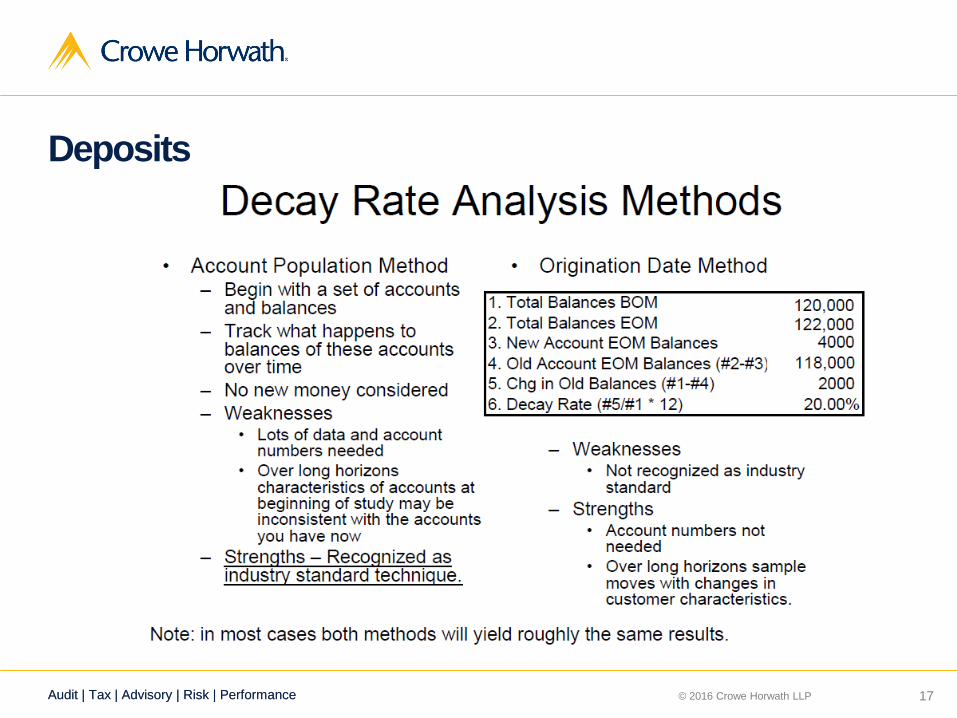

Deposits

Interest Rate

Audit | Tax | Advisory | Risk | Performance Audit | Tax | Advisory | Risk | Performance © 2016 Crowe Horwath LLP 16

Deposits

Interest Rate

Audit | Tax | Advisory | Risk | Performance Audit | Tax | Advisory | Risk | Performance © 2016 Crowe Horwath LLP 17

Deposits

Interest Rate

Audit | Tax | Advisory | Risk | Performance Audit | Tax | Advisory | Risk | Performance © 2016 Crowe Horwath LLP 18

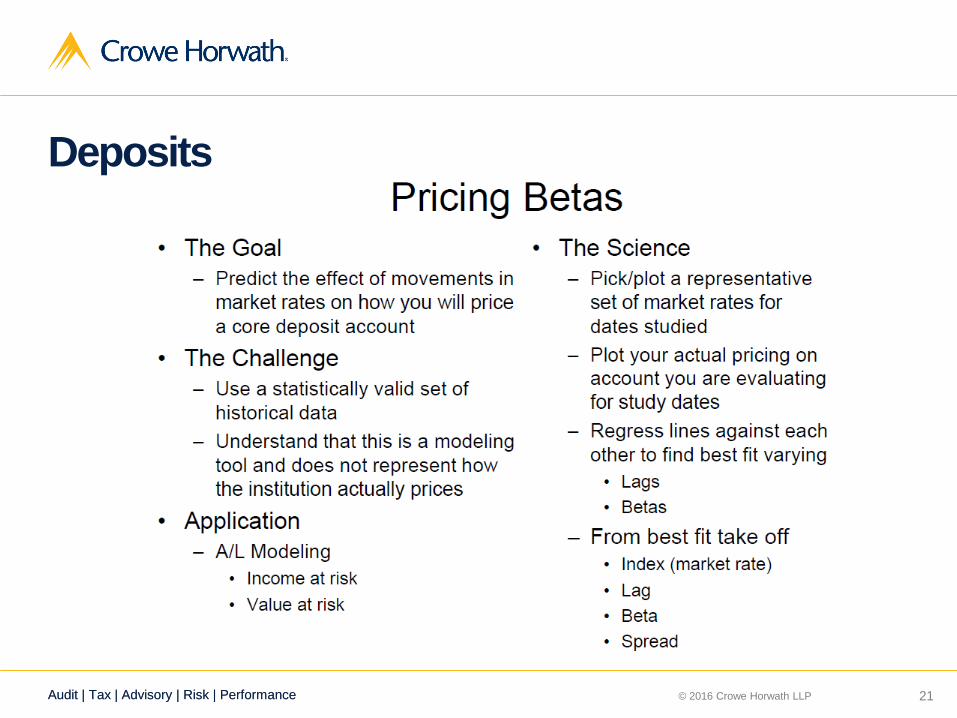

Deposits

Pricing Betas – the extent to which a change in market

rates is passed along to deposit customers

• Income at risk analysis

• EVE analysis

Interest Rate Risk

Audit | Tax | Advisory | Risk | Performance Audit | Tax | Advisory | Risk | Performance © 2016 Crowe Horwath LLP 19

Deposits

Pricing Beta Assumption Example:

•IRR Model assumption is that when market rates

increase 100 basis points (1%) the beta for the

change in MMDAs is 30 basis points (30% *100

basis points)

If current MMDA rate is .40% and market interest rates

increase 2% then MMDA rates are expected to be:

.40% + (30% * 200 basis points) = .40% + .60% = 1.00%

Interest Rate

Audit | Tax | Advisory | Risk | Performance Audit | Tax | Advisory | Risk | Performance © 2016 Crowe Horwath LLP 20

Deposits

Pricing Betas can be:

• Estimated by Management

• Derived statistically from historical data

Regulators prefer the latter

Interest Rate Risk | Risks | IRR Risk Management Process | IRR Modeling Process

Audit | Tax | Advisory | Risk | Performance Audit | Tax | Advisory | Risk | Performance © 2016 Crowe Horwath LLP 21

Deposits

Interest Rate

Audit | Tax | Advisory | Risk | Performance Audit | Tax | Advisory | Risk | Performance © 2016 Crowe Horwath LLP 22

Deposits

Time Deposit early redemption rates

Historically, few depositors have redeemed time

deposits prior to maturity.

Would this behavior change if market interest rates for

CDs increase 2%? - or 3%? - or 4%?

Interest Rate

Audit | Tax | Advisory | Risk | Performance Audit | Tax | Advisory | Risk | Performance © 2016 Crowe Horwath LLP 23

Deposits

Time Deposit early redemption rates

A significant change in market interest rates may result

in scenarios where paying the early redemption

prepayment penalty or more than offset by the

increased interest income.

Interest Rate

Audit | Tax | Advisory | Risk | Performance Audit | Tax | Advisory | Risk | Performance

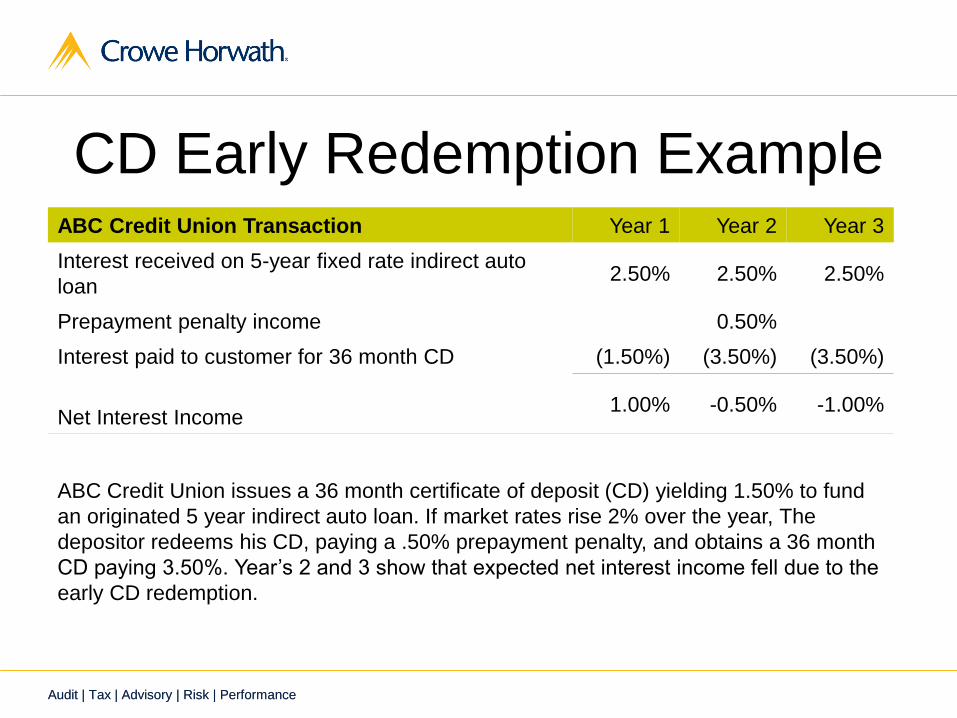

CD Early Redemption Example

ABC Credit Union Transaction Year 1 Year 2 Year 3

Interest received on 5-year fixed rate indirect auto

loan 2.50% 2.50% 2.50%

Prepayment penalty income 0.50%

Interest paid to customer for 36 month CD (1.50%) (3.50%) (3.50%)

Net Interest Income 1.00% -0.50% -1.00%

ABC Credit Union issues a 36 month certificate of deposit (CD) yielding 1.50% to fund

an originated 5 year indirect auto loan. If market rates rise 2% over the year, The

depositor redeems his CD, paying a .50% prepayment penalty, and obtains a 36 month

CD paying 3.50%. Year’s 2 and 3 show that expected net interest income fell due to the

early CD redemption.

Audit | Tax | Advisory | Risk | Performance Audit | Tax | Advisory | Risk | Performance © 2016 Crowe Horwath LLP 25

Deposits

Given the uncertainty in a rising rate environment of :

• The stability of surge deposits

• Potential changes in the deposit mix where surge

inflows may be present

• Deposit pricing volatility

Regulators expect credit unions to model

alternative deposit assumptions to understand the

range of potential outcomes

Interest Rate

Audit | Tax | Advisory | Risk | Performance Audit | Tax | Advisory | Risk | Performance © 2016 Crowe Horwath LLP 26

Deposits

KEY RISKS:

Inaccurate model assumptions surrounding deposits

decay rate and price volatility behaviors can produce

unreliable model output that may result in poor

decision-making.

IRR exposure to increased CD redemption rates in a

rapid rising interest rate environment may be

underestimated in the IRR model.

Interest Rate Risk

Audit | Tax | Advisory | Risk | Performance Audit | Tax | Advisory | Risk | Performance © 2016 Crowe Horwath LLP 27

Deposits

What can we do?

• IRR model assumptions should be reviewed to

determine if these CD redemption rates are

assumed to increase in rising rate scenarios.

• CD prepayment penalties should be reviewed to

assess whether there is sufficient protection from

early redemptions arbitrage.

Interest Rate

Audit | Tax | Advisory | Risk | Performance Audit | Tax | Advisory | Risk | Performance © 2016 Crowe Horwath LLP 28

Deposits

What can we do?

Perform “Key Assumption” sensitivity testing for:

• Deposit Beta Assumptions

• Deposit Decay Rate Assumptions

• CD Early Redemption Assumptions (If there is a

concentration of CDs maturing in >12 months)

Interest Rate

Audit | Tax | Advisory | Risk | Performance Audit | Tax | Advisory | Risk | Performance © 2016 Crowe Horwath LLP 29

Deposits

What is key assumption sensitivity testing?

Sensitivity testing takes one key assumption, such as

deposit betas, and changes the value to be larger or

smaller than its current value. The model scenarios

(+ 400 basis point rate shocks) are then run again to

see what impact changing one key assumption has on

the overall IRR model NII and EVE results.

Interest Rate

Audit | Tax | Advisory | Risk | Performance Audit | Tax | Advisory | Risk | Performance © 2016 Crowe Horwath LLP 30

Deposits

What is key assumption sensitivity testing?

Another approach to sensitivity testing is to reallocate

a portion of NMD balances into CDs. By measuring

traditional deposit mix balances, a credit union can be

informed of possible outcomes should funds revert

back to a more traditional NMD/CD deposit mix that

prevailed before 2008.

Interest Rate

Audit | Tax | Advisory | Risk | Performance Audit | Tax | Advisory | Risk | Performance © 2016 Crowe Horwath LLP 31

Investments

Many credit inions increased their aggregate

investment portfolios since the 2008 crisis, primarily

because of strong deposit inflows, slowed loan growth,

and continued pressure on net interest margins (NIM).

Much of the increase in investment portfolios has been

concentrated in in residential Mortgage Backed

Securities (MBS).

Interest Rate

Audit | Tax | Advisory | Risk | Performance Audit | Tax | Advisory | Risk | Performance © 2016 Crowe Horwath LLP 32

Investments

Significant concentrations in MBS could make some

credit unions more vulnerable to IRR because of the

potential for duration extension in a rising rate

environment.

What is duration extension?

Interest Rate

Audit | Tax | Advisory | Risk | Performance Audit | Tax | Advisory | Risk | Performance © 2016 Crowe Horwath LLP 33

Investments

Duration extension is the extension of the

average life of MBS investments in a rising

rate environment. Prepayment cash flow is

reduced, thereby reducing the funds

available to invest at higher yields.

Why MBS Securities?

Why does this happen?

Interest Rate

Audit | Tax | Advisory | Risk | Performance Audit | Tax | Advisory | Risk | Performance © 2016 Crowe Horwath LLP 34

Investments

Why MBS Securities?

Mortgage backed securities are collateralized by pools

of residential home mortgages. Each month the credit

union receives principal prepayments from mortgages

in the collateral pools when some borrower repay the

principal on their mortgages. MBS securities share

many of the same risk characteristics as your credit

union’s home mortgage loan portfolio.

Interest Rate

Audit | Tax | Advisory | Risk | Performance Audit | Tax | Advisory | Risk | Performance © 2016 Crowe Horwath LLP 35

Investments

Why does duration extend?

Home mortgage borrowers in MBS investment

collateral pools act in their personal best interest.

When market rates for home mortgages increase in a

rising rate environment borrowers in place greater and

greater value on their below market rate home loan,

reducing the rate of early loan payoffs.

Interest Rate

Audit | Tax | Advisory | Risk | Performance Audit | Tax | Advisory | Risk | Performance © 2016 Crowe Horwath LLP 36

Investments

What does this mean to the Credit Union in a rising

rate environment?

• Decreases the institution’s liquidity

• Increases Net Interest Income and EVE volatility

• Adversely affects NIM

• Increases the amount of unrealized losses reported in the

balance sheet

Interest rate risk for MBS investments increases in a rising rate

environment as less cash flow from MBS is received on a monthly

basis and extending the length of time that the credit union will

hold an investment paying below market interest rates.

Interest Rate

Audit | Tax | Advisory | Risk | Performance Audit | Tax | Advisory | Risk | Performance © 2016 Crowe Horwath LLP 37

Investments

KEY RISK:

IRR exposure to reduced MBS prepayment rates in a

rapid rising interest rate environment may be

underestimated in the IRR model.

Interest Rate

Audit | Tax | Advisory | Risk | Performance Audit | Tax | Advisory | Risk | Performance © 2016 Crowe Horwath LLP 38

Investments

What can we do?

• If MBS investments are a significant concentration

in the investment portfolio, the IRR model’s MBS

prepayment assumptions should sensitivity tested.

Sensitivity testing should takes the IRR model’s MBS

prepayment rate assumptions and change the values

to be larger or smaller than current values. Model

scenarios (+ 400 basis point rate shocks) should be

reviewed to see what impact the change has on the

overall IRR model NII and EVE results.

Interest Rate

Audit | Tax | Advisory | Risk | Performance Audit | Tax | Advisory | Risk | Performance © 2016 Crowe Horwath LLP 39

Loans

• In attempting to improve their NIM, many credit

unions have increasingly focused on residential

home mortgage loans. As a result, these institutions’

earnings, equity capital, and liquidity could be

adversely affected by a sustained and substantial

increase in interest rates.

Interest Rate

Audit | Tax | Advisory | Risk | Performance Audit | Tax | Advisory | Risk | Performance © 2016 Crowe Horwath LLP 40

Loans

• Similar to MBS, extension risk may be significant for

institutions with a concentration of fixed rate

residential mortgage loans in the loan portfolio.

• Changes in IRR exposure from rising interest rates

primarily correlates to a reduction in loan

prepayments speeds.

Loan prepayment speed = The rate that loans are

repaid prior to the contractual maturity date.

Interest Rate

Audit | Tax | Advisory | Risk | Performance Audit | Tax | Advisory | Risk | Performance © 2016 Crowe Horwath LLP 41

Loans

What does this mean to the Credit Union in a rising

rate environment?

• Decreases in loan prepayment speeds decrease the

institution’s liquidity

• Decreases in loan prepayment speeds increases Net Interest

Income and EVE volatility

• Decreases in loan prepayment speeds adversely affects NIM

Interest rate risk for long-term fixed rate loans increases in a

rising rate environment as less pre-payment cash flow from the

loan portfolio is received on a monthly basis and extending the

length of time that the credit union will hold a loan paying below

market interest rates.

Interest Rate

Audit | Tax | Advisory | Risk | Performance Audit | Tax | Advisory | Risk | Performance © 2016 Crowe Horwath LLP 42

Loans

What is Basis Risk?

• “Basis risk’’ is the imperfect correlation in the

change in loan rates compared to a designated

index rate (for example, the one-year Treasury Bill

rate).

The accuracy of IRR model projections for loan yields

and NII is subject to Basis Risk.

Interest Rate

Audit | Tax | Advisory | Risk | Performance Audit | Tax | Advisory | Risk | Performance © 2016 Crowe Horwath LLP 43

Loans

Why is Basis Risk Important?

The IRR model projections calculates loan yields in

+100 bp, +200 bp, + 300 bp and +400 bp rising rate

shock scenarios as an index + a spread rate (for

example, indirect new auto loan rates are based on

the one-year Treasury Bill index +1.50%).

The model assumes that there is a 100% correlation in

changes in the one-year Treasury Bill index and new

indirect auto loan rates.

Interest Rate

Audit | Tax | Advisory | Risk | Performance Audit | Tax | Advisory | Risk | Performance © 2016 Crowe Horwath LLP 44

Loans

Why is Basis Risk Important?

When the correlation of changes in a loan product’s

interest rate does not correlate 100% to changes in the

designated index for that product in the IRR model the

forecasted loan portfolio yield and NII projection are

adversely affected.

Interest Rate

Audit | Tax | Advisory | Risk | Performance Audit | Tax | Advisory | Risk | Performance © 2016 Crowe Horwath LLP 45

Loans

KEY RISKS:

• IRR exposure to reduced loan prepayment rates in

a rapid rising interest rate environment may be

underestimated in the IRR model.

• Changes in loan product rates may not correlate

well with changes in assigned index rates

Interest Rate

Audit | Tax | Advisory | Risk | Performance Audit | Tax | Advisory | Risk | Performance © 2016 Crowe Horwath LLP 46

Loans

What can we do?

• If long-term, fixed rate loans are a significant

concentration in the loan portfolio, the IRR model’s loan

prepayment assumptions should sensitivity tested.

Sensitivity testing should takes the IRR model’s loan

prepayment rate assumptions and change the values to be

larger or smaller than current values. Model scenarios (+

400 basis point rate shocks) should be reviewed to see

what impact the change has on the overall IRR model NII

and EVE results.

Interest Rate

Audit | Tax | Advisory | Risk | Performance Audit | Tax | Advisory | Risk | Performance © 2016 Crowe Horwath LLP 47

Loans

What can we do?

Sensitivity testing should takes the IRR model’s spread to

index assumptions and change the values to be larger or

smaller than current values. Model scenarios (+ 400 basis

point rate shocks) should be reviewed to see what impact

the change has on the overall IRR model NII and EVE

results.

Interest Rate

Audit | Tax | Advisory | Risk | Performance Audit | Tax | Advisory | Risk | Performance © 2016 Crowe Horwath LLP 48

Any Other Risks?

What About Yield-Curve Risk?

Yield-curve risk occurs when there are nonparallel

shifts in the yield curve.

For example, mortgage assets tend to be priced off 10-

year U.S. Treasury rates. Suppose 10-year

Treasury rates change significantly, while all other

Treasury rates remain unchanged.

What happens?

Audit | Tax | Advisory | Risk | Performance Audit | Tax | Advisory | Risk | Performance © 2016 Crowe Horwath LLP 49

Any Other Risks?

What About Yield-Curve Risk?

The value and cash flows from mortgage loans and

mortgage-related securities will change significantly,

but other assets and liabilities will not experience

similar changes. Thus, credit unions with significant

mortgage asset holdings would be exposed to greater

yield curve risk than those with mortgage assets

comprising a lower percentage of assets.

Audit | Tax | Advisory | Risk | Performance Audit | Tax | Advisory | Risk | Performance © 2016 Crowe Horwath LLP 50

Any Other Risks?

What About Yield-Curve Risk?

KEY RISK:

• IRR model scenarios to not model changes in the

shape of the yield curve and fail to accurately

forecast NII and EVE

Audit | Tax | Advisory | Risk | Performance Audit | Tax | Advisory | Risk | Performance © 2016 Crowe Horwath LLP 51

Any Other Risks?

What can we do?

Interest rate shocks consisting only of parallel shifts

in the yield curve may not be sufficient to adequately

assess the credit union’s IRR exposure. To capture

yield-curve risk the IRR model scenarios should

include changes in the slope and the shape of the

yield curve (flattening yield curve and steepening yield

curve).

Interest Rate

Audit | Tax | Advisory | Risk | Performance Audit | Tax | Advisory | Risk | Performance © 2016 Crowe Horwath LLP 52

Sound IRR Management Practices

Board of Directors

• Board responsibilities might include the following:

• Review and approval of the interest rate risk policy and limits, e.g.

NII and EVE;

• Monitor the financial institutions performance and risk profile;

• Proper level of expertise to understand the issues and risks the

financial institution is facing; and

• Periodically evaluate policies, procedures, limits, etc. and

recommend adjustments as necessary.

Audit | Tax | Advisory | Risk | Performance Audit | Tax | Advisory | Risk | Performance © 2016 Crowe Horwath LLP 53

Sound IRR Management Practices

Senior Management

Senior management responsibilities might include the following:

• Implement policies and procedures related to interest rate risk

which might include the following:

• Lines of authority, e.g. approval of assumptions used in the

model;

• Establishment of risk limits, e.g. NII and EVE;

• Appropriate systems for measuring and monitoring interest rate

risk, e.g. use of a third-party to prepare quarterly reports or the

use of in-house systems such as Sendaro or ProfitStar; and

• All around effective internal controls.

Audit | Tax | Advisory | Risk | Performance Audit | Tax | Advisory | Risk | Performance © 2016 Crowe Horwath LLP 54

Sound IRR Management Practices

Policies and Procedures

Adequate policies and procedures should be established which include the

following:

• Delineate lines of responsibility and accountability over IRR management

decisions,

• Clearly define authorized instruments and permissible hedging and

position taking strategies,

• Identify the frequency and method for measuring and monitoring IRR, and

• Specify quantitative limits that define the acceptable level of risk for the

institution.

• Define the specific procedures and approvals necessary for exceptions to

policies, limits, and authorizations.

Audit | Tax | Advisory | Risk | Performance Audit | Tax | Advisory | Risk | Performance © 2016 Crowe Horwath LLP 55

Sound IRR Management Practices

Systems

• Adequate systems for risk management and reporting should be able to

address several aspects of risk management. They might include the

following:

• Measure all the financial institution’s risks (including off-balance

sheet risk);

• Measure risk associated with all products or instruments offered by

the financial institution (including optionality); and

• Stress testing or back testing results, e.g. actual performance

versus prior projections.

Audit | Tax | Advisory | Risk | Performance Audit | Tax | Advisory | Risk | Performance © 2016 Crowe Horwath LLP 56

Sound IRR Management Practices

Reporting

A credit union’s Asset Liability Committee should receive reports on the credit

union’s IRR profile at least quarterly. IRR reports should provide the following

information:

• Evaluate the level of and trends in the credit union’s aggregate IRR

exposure;

• Demonstrate and verify compliance with all policies and limits;

• Past forecasts or risk estimates should be compared with actual results

as one tool to identify any potential shortcomings in modeling techniques

(i.e. Evaluate the sensitivity and reasonableness of key assumptions).

• Determine whether the credit union holds sufficient net worth for the level

of risk being taken.

Audit | Tax | Advisory | Risk | Performance Audit | Tax | Advisory | Risk | Performance © 2016 Crowe Horwath LLP 57

Lessons Learned

Implement an IRR Strategy.

Implement meaningful IRR limits.

Identify, control, and monitor asset concentrations.

Implement dynamic, forward-looking IRR measurement tools.

Ensure accurate cash flow reporting.

Understand the potential use of borrowings and structured

advances.

Maintain internal control and audit processes.