rbs round up: 02 november 2011

TRANSCRIPT

8/8/2019 RBS Round Up: 02 November 2011

http://slidepdf.com/reader/full/rbs-round-up-02-november-2011 1/9

Equity Structured Products and Warrants

This material has been produced by RBS sales and trading staff and should not be considered independent.

The Round Up

2 November 2010 Issue No. 437

The Round Up is a comprehensive

daily note produced by the RBS

Warrants team providing an overview

of market movements along with

quality ideas for warrant traders and

investors.

Daily Monitor

Global Market Action Scoreboard, commentary

Aussie Market Action SPI Comment, Events & Dividends

Telstra Corp. (TLSKZD) MINI Trading Buy – TLS underperforms global

peers

Santos (STOKZD) MINI Trading Buy – Things can only get better

Origin Energy (ORGKZC) MINI Trading Buy – Cashflow set to surge

Australian Strategy Monthly Market Review - August 2010

8/8/2019 RBS Round Up: 02 November 2011

http://slidepdf.com/reader/full/rbs-round-up-02-november-2011 2/9

Equity Structured Products and Warrants

Overnight Commentary United States Commentary

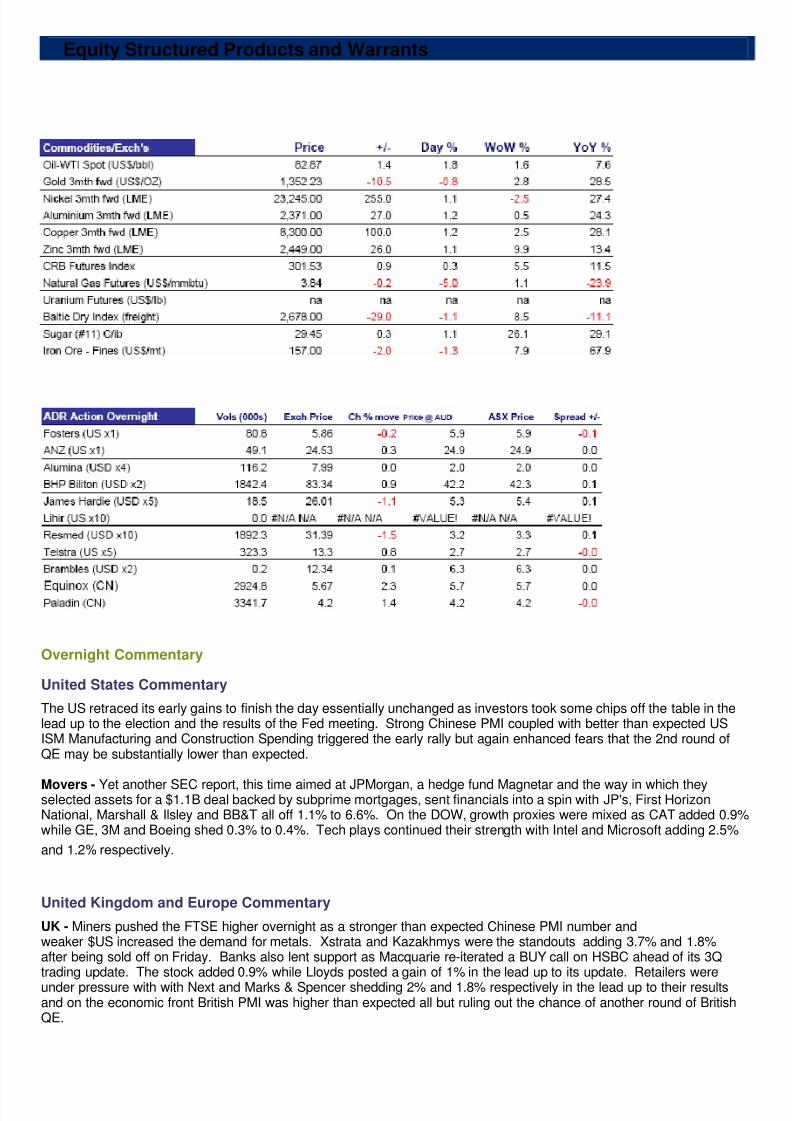

The US retraced its early gains to finish the day essentially unchanged as investors took some chips off the table in thelead up to the election and the results of the Fed meeting. Strong Chinese PMI coupled with better than expected USISM Manufacturing and Construction Spending triggered the early rally but again enhanced fears that the 2nd round ofQE may be substantially lower than expected.

Movers - Yet another SEC report, this time aimed at JPMorgan, a hedge fund Magnetar and the way in which theyselected assets for a $1.1B deal backed by subprime mortgages, sent financials into a spin with JP's, First HorizonNational, Marshall & Ilsley and BB&T all off 1.1% to 6.6%. On the DOW, growth proxies were mixed as CAT added 0.9%while GE, 3M and Boeing shed 0.3% to 0.4%. Tech plays continued their strength with Intel and Microsoft adding 2.5%

and 1.2% respectively.

United Kingdom and Europe Commentary

UK - Miners pushed the FTSE higher overnight as a stronger than expected Chinese PMI number andweaker $US increased the demand for metals. Xstrata and Kazakhmys were the standouts adding 3.7% and 1.8%after being sold off on Friday. Banks also lent support as Macquarie re-iterated a BUY call on HSBC ahead of its 3Qtrading update. The stock added 0.9% while Lloyds posted a gain of 1% in the lead up to its update. Retailers wereunder pressure with with Next and Marks & Spencer shedding 2% and 1.8% respectively in the lead up to their resultsand on the economic front British PMI was higher than expected all but ruling out the chance of another round of BritishQE.

8/8/2019 RBS Round Up: 02 November 2011

http://slidepdf.com/reader/full/rbs-round-up-02-november-2011 3/9

Equity Structured Products and Warrants

Commodities Commentary

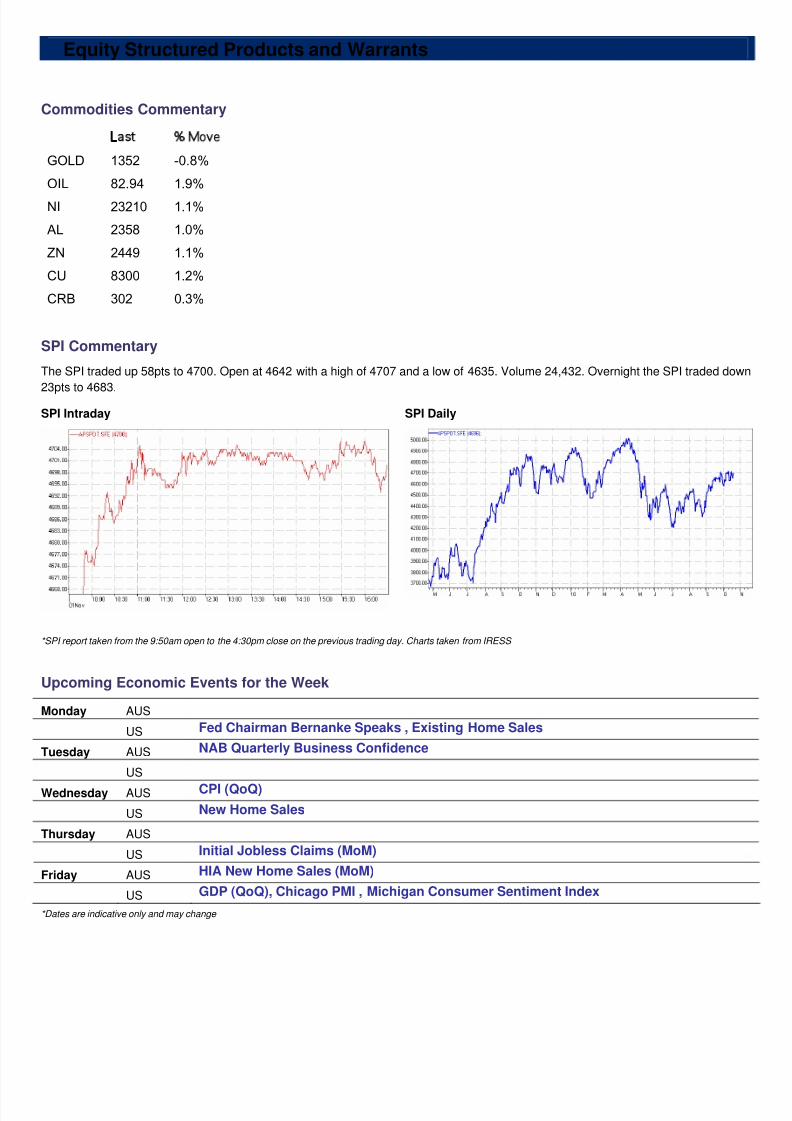

Last % Move

GOLD 1352 -0.8% OIL 82.94 1.9% NI 23210 1.1% AL 2358 1.0% ZN 2449 1.1% CU 8300 1.2% CRB 302 0.3%

SPI Commentary

The SPI traded up 58pts to 4700. Open at 4642 with a high of 4707 and a low of 4635. Volume 24,432. Overnight the SPI traded down

23pts to 4683.

SPI Intraday SPI Daily

*SPI report taken from the 9:50am open to the 4:30pm close on the previous trading day. Charts taken from IRESS

Upcoming Economic Events for the Week

Monday AUS

US Fed Chairman Bernanke Speaks , Existing Home Sales

Tuesday AUS NAB Quarterly Business Confidence

US

Wednesday AUS CPI (QoQ)

US New Home Sales

Thursday AUS

US Initial Jobless Claims (MoM)

Friday AUS HIA New Home Sales (MoM)

US GDP (QoQ), Chicago PMI , Michigan Consumer Sentiment Index

*Dates are indicative only and may change

8/8/2019 RBS Round Up: 02 November 2011

http://slidepdf.com/reader/full/rbs-round-up-02-november-2011 4/9

Equity Structured Products and Warrants

MINI Trading Buy: Telstra Corporation (TLSKZD) - Telstra underperforms global peers

Telstra's share price has significantly underperformed its global peers in recent weeks. It is now trading at alarger than usual discount to its international peer group on both a PE multiple and dividend yield basis. BuyTLSKZD MINI and play up to RBS Research Target Price of $3.06.

Source: IRESS

Telstra share price underperforms peers Our recent marketing trip to Asia highlighted to us that Telstra is starting to come back onto the radar screen for globaltelecoms investors following its recent underperformance relative to global peers. Telstra's share price has fallen 8% overthe last 2 months vs the FTSE World Telecom Index which is up 11% over the same period (eg Vodafone up 10% and BTup 9%).

Telstra PE multiple of 10.0x is below MSCI world Telecom index on 12.1x The PE multiple for the MSCI world Telecom services index has tracked up to 12.1x in recent weeks and is close to its 5-yr average of 12.7x (based on IBES 12m forward earnings estimates). Telstra, on the other hand, trades on a PE of 10.2x(below its 5yr average of 12.6x) and at a 15% discount to the MSCI index. Telstra's dividend yield of 10.6% is well abovethe MSCI Telecoms index on 5.6%, with the gap having increased in the last couple of months (although there are some

risk factors specific to Telstra that explain the size of this differential).

Limited visibility over key rerating catalysts Whilst Telstra's trading multiples look increasingly attractive vs global peers, there is still limited visibility over the keycatalysts for a rerating, including: 1) clearer evidence that the strategy to cut prices and increase spend is deliveringsustained customer growth and revenue growth; and 2) Parliamentary and regulatory approval of the NBN which isrequired to deliver greater certainty around payments to Telstra to decommission its copper network.

Risk reward equation seems to be improving. Hold maintained We believe that value may be starting to emerge in Telstra at current levels, particularly when compared to global peers.Consensus earnings forecasts have been reduced to a level where they are starting to look relatively conservative andthe balance of risk/reward may be starting to shift to the upside. However, we expect the market to want clearer evidenceof success with the turnaround strategy and more certainty over NBN before rerating the stock. RBS Research retain a

Hold rating and A$3.06 price target (10% discount to A$3.40 DCF valuation).

Security ExPrc Stop Loss CP ConvFac Delta Description

TLSKZC 2.4588 2.57 Long 1 1 Long MINI

TLSKZD 2.1131 2.32 Long 1 1 Long MINI

8/8/2019 RBS Round Up: 02 November 2011

http://slidepdf.com/reader/full/rbs-round-up-02-november-2011 5/9

Equity Structured Products and Warrants

MINI Trading Buy: Santos (STO.AX): $29.5Bn CSG Projects get the go ahead

STO has delivered a 3Q result that was largely in line with our expectations. The delays to

Kipper were a mild disappointment, but the Santos story remains firmly about GLNG in thenear term. With the environmental approval now received a deal with Kogas is just around thecorner.

Source: IRESS Production of 12.9mmboe in line with our 12.8mmboe forecast No major variances, although condensates production (especially Bonaparte) was a little bit ahead. Sales revenue ofA$535m was also a touch ahead of our A$522m forecast, with a slightly higher realised crude price (A$83/bbl vs RBSA$80/bbl) and average gas price. The only change to guidance metrics was a lowering of capex by A$300m to A$2bn,largely on the back of GLNG FID delays.

Kipper delays drive a small downgrade in FY11F... Another six-month delay in Kipper (technical design issues) has knocked about 1mmboe off our FY11 production forecast

(see Table 1) and trimmed NPAT slightly. Our FY10 forecasts have increased slightly (+5%) after factoring in today'squarterly. We are now looking for 50mbbls (guidance 49-52). The net change to our valuation has been a 5c fall toA$15.75 ps.

Buy maintained, we think STO is great value and has some positive potential catalystsRightly or wrongly, the market's sole focus right now is STO's GLNG project and sentiment has been hit hard since someelements of the Total deal surprised the market (stock off 12% since then). Looking forward, we believe things can onlyget better from here. Post Federal environmental approvals, a pre FID deal with Kogas is still a possibility and we thinkthe final capex number should give the market some comfort (RBS A$20bn). An equity raising could be on the horizon,but the recent upsizing of the hybrid has reduced equity needs further. We have pencilled in A$1.5bn, but the finalnumber will depend on what S&P's magic box spits out. At current levels, STO is our top pick in the energy sector. RBS MINIs over STO

Security ExPrc Stop Loss CP ConvFac Delta Description

STOKZD 942.82 10.30 Long 1 1 MINI Long

8/8/2019 RBS Round Up: 02 November 2011

http://slidepdf.com/reader/full/rbs-round-up-02-november-2011 6/9

Equity Structured Products and Warrants

MINI Trading Buy: Origin Energy (ORGKZC) – Cashflow set to surge ORG's FY10 earnings fell a little short of our forecasts, but, importantly, FY11 is on track to be a bigyear on the earnings front. With cashflows set to surge over the coming years, on our estimates, we

think the market is underestimating ORG's financial flexibility and optionality. Buy maintained.Buy maintained with RBS Target Price of $18.25

Source: IRESS

Underlying NPAT of A$585m was behind our A$611m forecast EBITDA of A$1,304m (incl associates) was the main variance to RBS Research numbers (A$1,321m forecast) but D&A(variance of A$9m) and minorities (variance of A$9m) also impacted. Operationally, the generation and E&P contributionswere lower than we expected with retail offsetting. Management has suggested it would have hit its 15% growth target ifnot for the overseas exploration write-downs, although RBS Research had these in the numbers already. OPCF ofA$789m was a little below RBS Research’s expectations (A$840m), but the 25c dividend was in line.

ORG has guided for 15% NPAT growth in FY11 FY11 guidance has been set at +35% EBITDAF growth and +15% NPAT growth in FY11. Importantly, the guidance nowincludes a reasonably aggressive A$170m exploration programme and RBS Research have pushed up forecasts for

exploration write-offs to about A$65m (from A$40m). This has been the sole driver of RBS Research’s earningsdowngrade. Importantly, the valuation impact is negligible.

APLNG - is consolidation lurking? Today ORG appeared the most open to collaborating with another project proponent since the Conoco deal was struckalmost two years ago and we continue to believe that any news on that front would be well received by the market. Likeall investors, we would like to see an off-take arrangement done before we get too excited about the project, but, in ourview, an investor is not paying a dime for any LNG upside.

Buy maintained, ORG's balance sheet about to go to work ORG's major capex programme is taking a breather and the company will have very substantial cashflow over the comingyears. Throw in an under-geared balance sheet and we believe the market is under-estimating the opportunities ahead.The NSW energy sell-down and APLNG are the obvious candidates, but we wouldn't be surprised to see some accretive

acquisition from left field that could create shareholder value.BUY ORGKZC for 1-for-1 upside towards RBS Target Price of $18.25

RBS MINIs over ORG Security ExPrc Stop Loss CP ConvFac Delta Description

ORGKZC 1116.75 12.20 Call 1 1 MINI Long

8/8/2019 RBS Round Up: 02 November 2011

http://slidepdf.com/reader/full/rbs-round-up-02-november-2011 7/9

Equity Structured Products and Warrants

RBS Round Up Corner: Monthly Market Review - September 2010

September was a good month for equities with the S&P/ASX 200 up over 4%. The ongoing

surge in the AUD was a key feature, particularly during the past two weeks. With expectationsof a sustained period of currency strength, there was increased focus at month-end on theearnings implications of an AUD at parity.

Australia's performance vs the worldIn local currency, the All Ordinaries (+4.5%) underperformed the US S&P 500 (+8.8%), the World MSCI ex AustraliaIndex (+9.0%) and the regional MSCI ex Japan Index (+11.6%).

The best- and worst-performing sectorsThe best performers for the month were Industrials (+6.7%), Materials (+6.3%) and Utilities (+5.9%). The worstperformers were elecommunication Services (-4.4%), Property (-1.1%) and Health Care (+0.7%).

The top-five and bottom-five performing S&P/ASX 200 stocksThe top-five performers from the S&P/ASX 200 (price) Index for the month were Sundance Resources (+72.4%), LynasCorporation (+39.3%), Carnarvon Petroleum (+29.9%), Virgin Blue (+26.1%) and Ausenco (+25.7%). The bottom-fiveperformers were PaperlinX (-20.7%), TPG Telecom (-13.1%), iSoft Group (-10.7%), Carsales.com (-10.6%) and Santos (-9.8%).

Consensus earnings revisionsThe top-five upgrades were Intoll Group (+26.8%), Spark Infrastructure (+13.9%), Map Group (+11.6%), Duet (+4.3%)and Commonwealth Property Office Fund (+2.4%). The topfive downgrades were Macquarie Group (-16.3%), Paladin

Energy (-15.0%), Aquarius Platinum (-9.0%), Ten Network Holdings (-8.6%) and AWE (-5.5%).

8/8/2019 RBS Round Up: 02 November 2011

http://slidepdf.com/reader/full/rbs-round-up-02-november-2011 8/9

Equity Structured Products and Warrants

Strong balance sheets to drive investment and acquisitionsOver the past couple of years, we have consistently highlighted the strength of corporate Australia’s balance sheet.Reporting season again supported this, as evident in the charts below.

We forecast net debt will decline in absolute terms over the next few years. However, as shown in the chart below, M&Aactivity has been quite muted in Australia over the past 12 months.

But this conservative approach has created some unique expansion opportunitiesDue to the capital raising/preservation policies, corporate Australia is now well placed to expand over the next 6-18months. We believe corporate thinking might go along the following lines: Despite some setbacks, the worst of the global financial crisis looks to have passed. The Asian economies (Australia inparticular) look to be strong. We don’t expect a double-dip in the US, although growth may be slow.

The balance sheet is strong as a result of the conservative capital policies adopted. Debt markets are freeing up, making funding increasingly available on improving terms. Asset values are generally still well off their highs and/or a number of key growth projects (eg, PNG LNG) areapproaching investment phase. Private equity is also likely to be looking to divest assets acquired in the last cycle.

8/8/2019 RBS Round Up: 02 November 2011

http://slidepdf.com/reader/full/rbs-round-up-02-november-2011 9/9

Equity Structured Products and Warrants

For further information please do not hesitate to contact us on the details below

Equities Structured Products & Warrants

Toll free 1800 450 005 www.rbs.com.au/warrants

Trading Products Team

Ben Smoker 02 8259 2085 [email protected]

Ryan Corrigan 02 8259 2425 [email protected]

Investment Products Team

Elizabeth Tian 02 8259 2017 [email protected]

Tania Smyth 02 8259 2023 [email protected]

Robert Deutsch 02 8259 2065 [email protected]

Mark Tisdell 02 8259 6951 [email protected]

Disclaimer

The information contained in this report has been prepared by RBS Equities (Australia) Limited (“RBS Equities”) (ABN 84 002 768 701) (AFS Licence No 240530) and hasbeen taken from sources believed to be reliable. RBS Equities does not make representations that the information is accurate or complete and it should not be relied on assuch. Any opinions, forecasts and estimates contained in this report are the views of RBS Equities at the date of issue and are subject to change without notice. RBSEquities and its affiliated companies may make markets in the securities discussed. RBS Equities, its affiliated companies and their employees from time to time may holdshares, options, rights and warrants on any issue contained in this report and may, as principal or agent, sell such securities. RBS Equities may have acted as manager orco-manager of a public offering of any such securities in the past three years. RBS Equities’ affiliates may provide, or have provided banking services or corporate finance tothe companies referred to in this report. The knowledge of affiliates concerning such services may not be reflected in this report. This report does not constitute an offer orinvitation to purchase any securities and should not be relied upon in connection with any contract or commitment. RBS Equities, in preparing this report, has not taken intoaccount an individual client’s investment objectives, financial situation or particular needs. Before a client makes an investment decision, a client should consider whether anyadvice contained in this report is appropriate in light of their particular investment needs, objectives and financial circumstances. It is unreasonable to rely on anyrecommendation without first having consulted with your advisor for a personal securities recommendation. The information contained in this report is general advice only.RBS Equities, its officers, directors, employees and agents accept no liability for any loss or damage arising out of the use of all or any part of the information contained in thisreport. This Information is not intended for distribution to, or use by any person or entity in any jurisdiction or country where such distribution or use would be contrary to local

law or regulation. If you are located outside Australia and use this Information, you are responsible for compliance with applicable local laws and regulation. This report maynot be taken or distributed, directly or indirectly into the United States, or to any U.S. person (as defined in Regulation S under the U.S. Securities Act of 1993, as amended).

The warrants contained in this report are issued by RBS Group (Australia) Pty Limited (“RBS”) (ABN 78 000 862 797, AFS Licence No. 247013). The Product DisclosureStatements relating to these warrants are available upon request from RBS Equities or on our website www.rbs.com.au/warrants

RBS Group (Australia) Pty Limited is not an Authorised Deposit-Taking Institution and these products do not form deposits or other liabilities of The Royal Bank of ScotlandN.V. or The Royal Bank of Scotland plc. The Royal Bank of Scotland plc does not guarantee the obligations of RBS Group (Australia) Pty Limited.

© Copyright 2009. RBS Equities. A Participant of the ASX Group.

Explanation of Warrant Tables

Security – refers to the code ascribed to the warrant, ExDate – refers to the date on which the warrant expires or is reset, ExPrc – refers to the exercise price, or second

instalment payment, CP – tells you whether the warrant is a call or a put, ConvFac – the conversion factor of the warrant which tells you how many warrants you need to

exercise in order to take possession of 1 share, Delta – tells you how much the warrant will move for a 1c move in the underlying security, Description – Tells you the typeof warrant.

All charts taken from IRESS unless indicated otherwise