future challenges for big pharma

DESCRIPTION

Future Challenges for Big Pharma - - Dr. Aurup 1-11-12TRANSCRIPT

Future Challenges for

Big Pharma

Peter Aurup, MDVP & Head - Global

Clinical Trial Operations

January 11, 2012

2

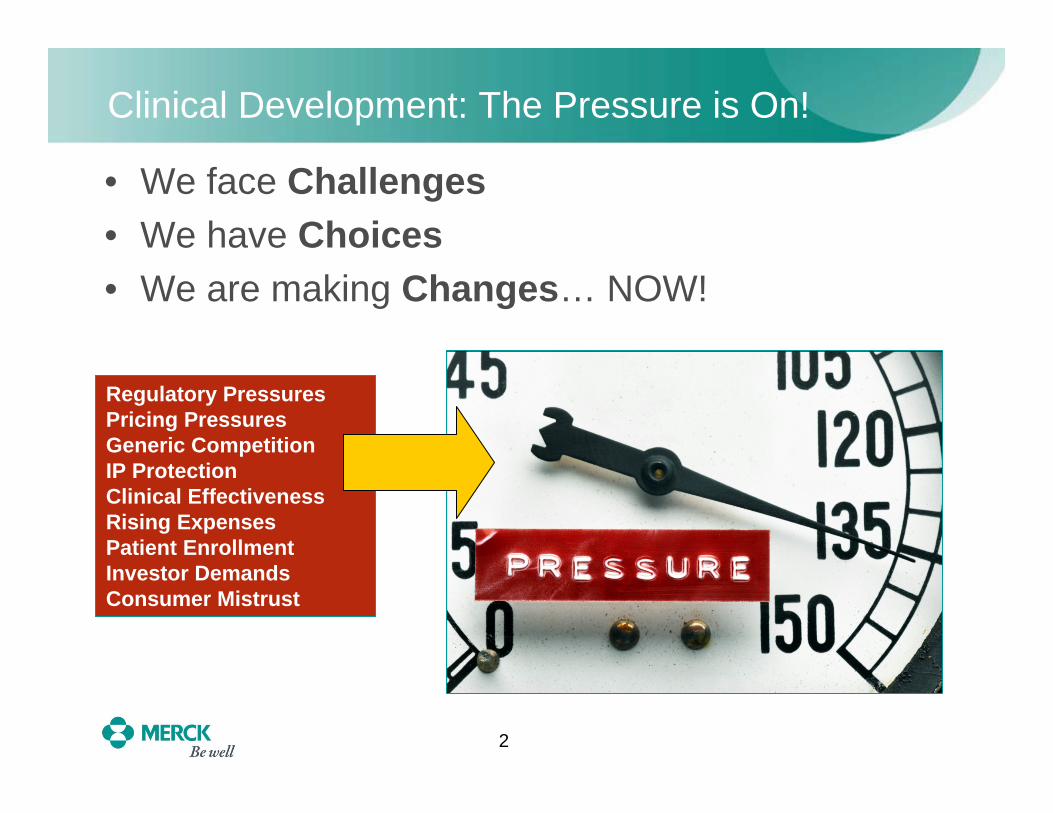

Clinical Development: The Pressure is On!

• We face Challenges• We have Choices• We are making Changes… NOW!

Regulatory PressuresPricing Pressures Generic CompetitionIP ProtectionClinical EffectivenessRising ExpensesPatient EnrollmentInvestor DemandsConsumer Mistrust

CHALLENGES

4

Challenges: The New Industry Reality

1. Development of new medicines and vaccines has become more costly and complex

2. Return on Investment (ROI) is in many cases negative for the pharmaceutical R&D industry

3. The regulatory landscape is transforming

4. The bar for new drug approval and/or reimbursement is constantlybeing raised

5. Investor and consumer pressures are mounting

6. Patents are expiring at a record rate

7. Global reach is now an imperative

8. Changing disease states and aging populations call for an emphasis on new or different therapy groups – Innovation is key!

5

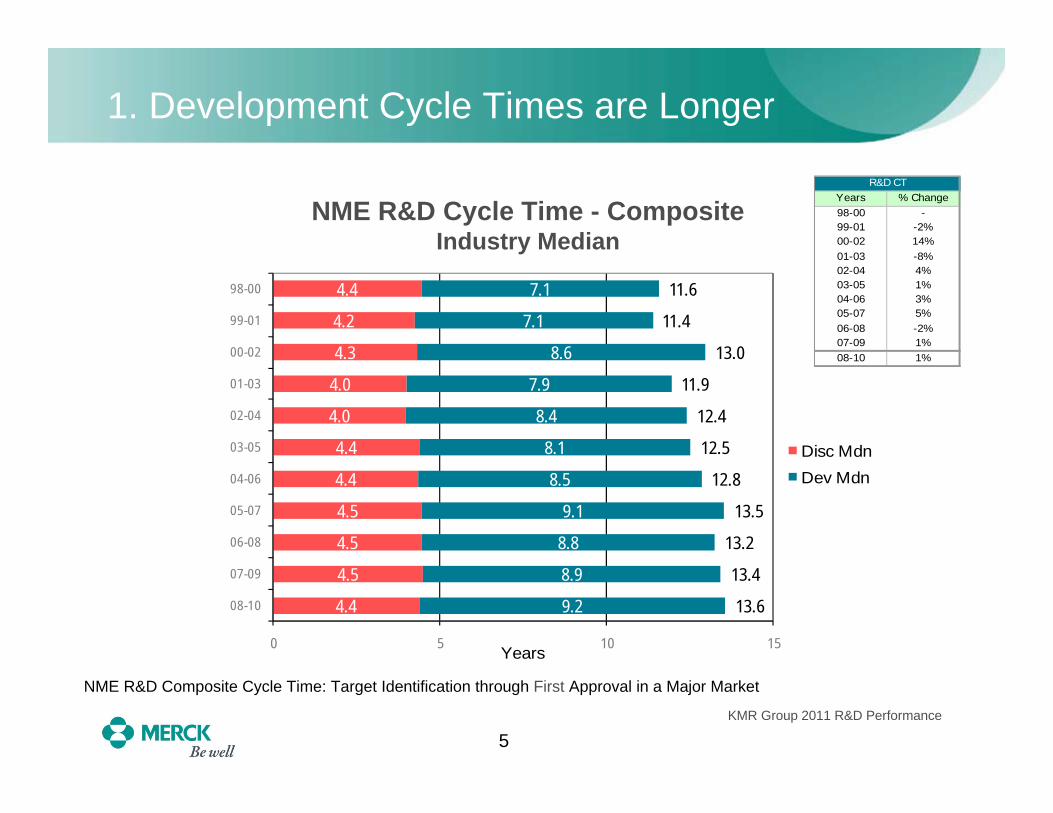

1. Development Cycle Times are Longer

NME R&D Cycle Time - CompositeIndustry Median

NME R&D Composite Cycle Time: Target Identification through First Approval in a Major Market

4.4

4.5

4.5

4.5

4.4

4.4

4.0

4.0

4.3

4.2

4.4

9.2

8.9

8.8

9.1

8.5

8.1

8.4

7.9

8.6

7.1

7.1

13.6

13.4

13.2

13.5

12.8

12.5

12.4

11.9

13.0

11.4

11.6

0 5 10 15

08-10

07-09

06-08

05-07

04-06

03-05

02-04

01-03

00-02

99-01

98-00

Years

Disc MdnDev Mdn

Years % Change98-00 -99-01 -2%00-02 14%01-03 -8%02-04 4%03-05 1%04-06 3%05-07 5%06-08 -2%07-09 1%08-10 1%

R&D CT

KMR Group 2011 R&D Performance

6

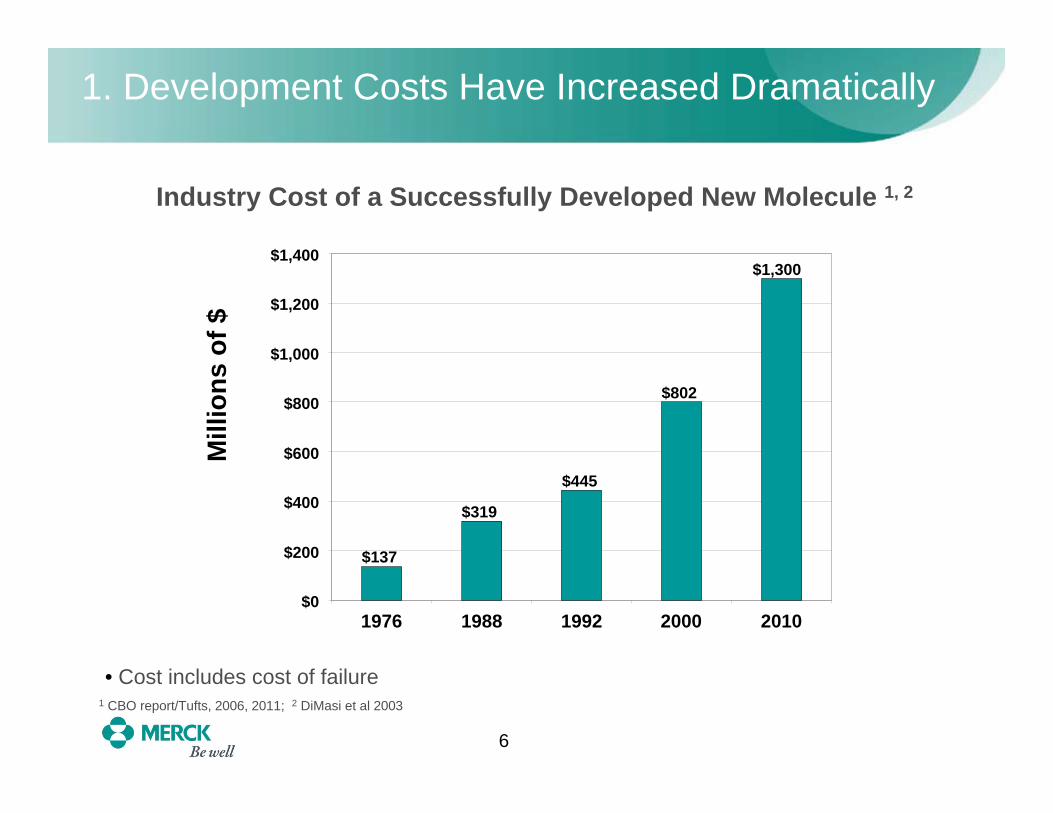

1. Development Costs Have Increased Dramatically

Industry Cost of a Successfully Developed New Molecule 1, 2

• Cost includes cost of failure

$137

$319

$445

$802

$1,300

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

1976 1988 1992 2000 2010

Mill

ions

of $

1 CBO report/Tufts, 2006, 2011; 2 DiMasi et al 2003

7

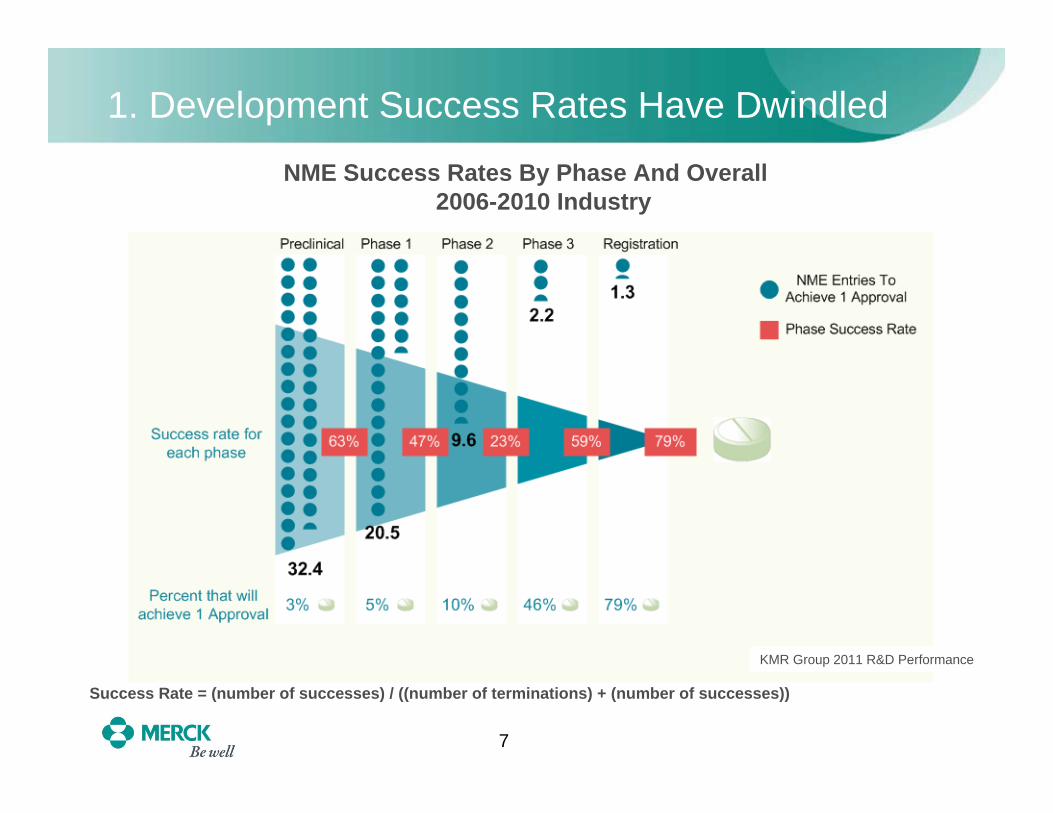

1. Development Success Rates Have Dwindled

NME Success Rates By Phase And Overall2006-2010 Industry

Success Rate = (number of successes) / ((number of terminations) + (number of successes))

KMR Group 2011 R&D Performance

8

2. ROI for R&D in the Pharmaceutical Industry has Turned Negative

Source: Credit Suisse / C. Arnold et al.; published in In Vivo: The Business & Medicine Report, April 2009

R&D Investment as a Percentage of Sales Has Increased, While ROI has Decreased

56

78 8

11 11

13 1314

15 1516 16

9

0

2

4

6

8

10

12

14

16

18

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008

R&

D/S

ales

0.00.20.40.60.81.01.21.41.61.82.02.22.42.62.83.0

Sales/C

apitalized R&

D

Note: The capitalized R&D analysis is Sales for a given year/R&D spend for 11 years (adjusted for inflation).

Sales/Capitalized R&D InvestmentR&D/Sales

9

3. Regulatory Landscape is More Difficult to Navigate

• The regulatory landscape is changing• Outcomes data often requested prior to drug approval

• Greater emphasis on product safety requires extensive data

• Increased post-marketing regulatory requirements

• More requirements to conduct clinical trials in a country as a prelude to registering and marketing a product• Need good interaction with local regulatory agencies for clinical

trial authorization

10

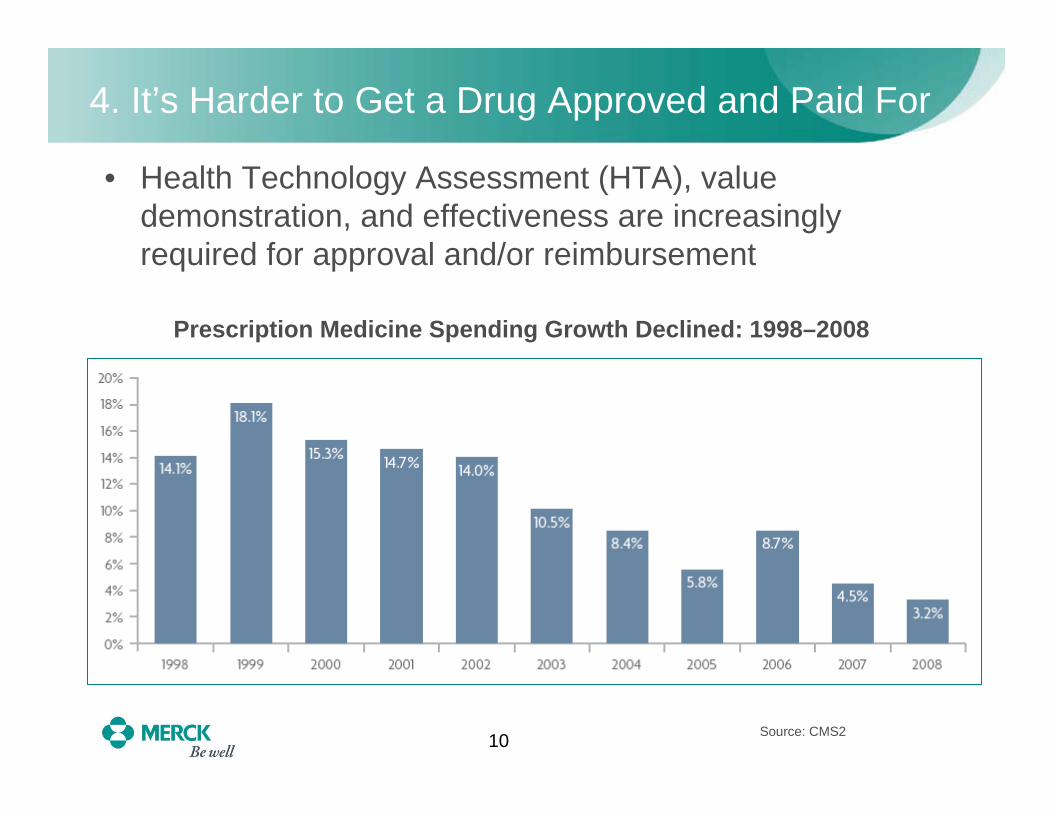

4. It’s Harder to Get a Drug Approved and Paid For

• Health Technology Assessment (HTA), value demonstration, and effectiveness are increasingly required for approval and/or reimbursement

Prescription Medicine Spending Growth Declined: 1998–2008

Source: CMS2

11

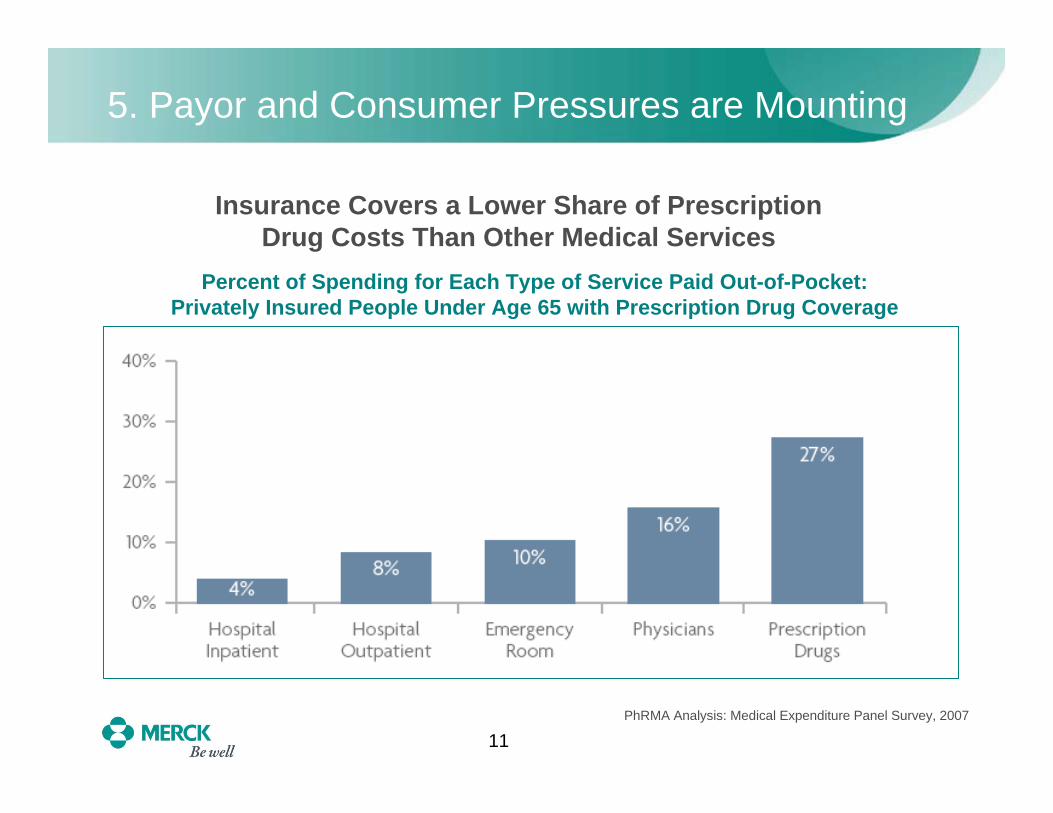

5. Payor and Consumer Pressures are Mounting

Percent of Spending for Each Type of Service Paid Out-of-Pocket: Privately Insured People Under Age 65 with Prescription Drug Coverage

Insurance Covers a Lower Share of PrescriptionDrug Costs Than Other Medical Services

PhRMA Analysis: Medical Expenditure Panel Survey, 2007

12

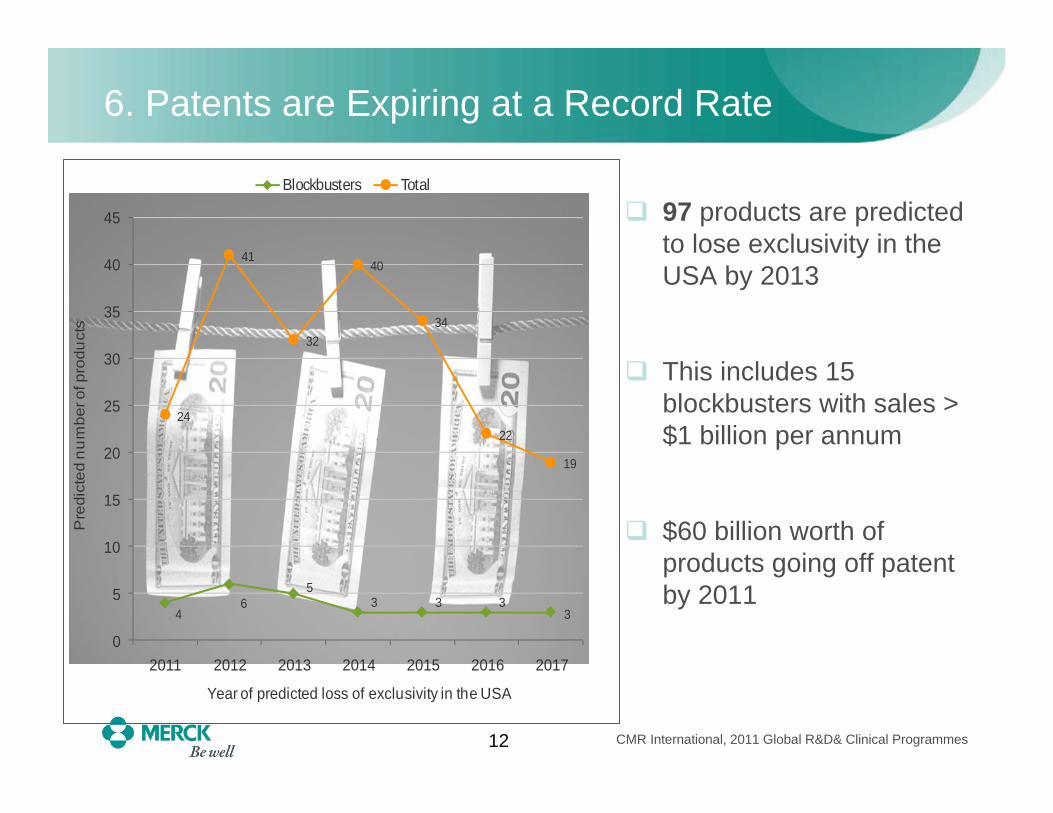

6. Patents are Expiring at a Record Rate

46

53 3 3

3

24

41

32

40

34

22

19

0

5

10

15

20

25

30

35

40

45

2011 2012 2013 2014 2015 2016 2017

Pre

dict

ed n

um

ber o

f pro

duct

s

Year of predicted loss of exclusivity in the USA

Blockbusters Total

97 products are predicted to lose exclusivity in the USA by 2013

This includes 15 blockbusters with sales > $1 billion per annum

$60 billion worth of products going off patent by 2011

CMR International, 2011 Global R&D& Clinical Programmes

13

7. Global Reach is Now an Imperative

• Economies of emerging markets are growing more than twice as fast as the developed world

• Diversified populations must be enrolled in trials• Regulators increasingly want clinical trials to include specific

populations in their own countries / environments / cultures

• Executing global clinical trials is more difficult than ever• Protocols are increasingly complicated• Western European market is increasingly costly• Strong, growing competition in key emerging market countries for

resources, including access to:– Qualified investigators– Patient populations – Vendor partnerships

14

8. Medicines Must Address Changing Needs

• Some major diseases have been partially conquered:• 45% decline in heart attack deaths and heart failure from 1999 to

2005* • U.S. AIDS deaths decreased dramatically following the

introduction of highly active antiretroviral treatment**• Improvements in treatment have helped reduce mortality in

certain cancers by up to 50% or more during 30-year period***

• Aging populations call for emphasis on different therapy areas:• Alzheimer's… Parkinson’s• New ways to manage chronic

conditions: Diabetes… Arthritis

• Innovation is the key to success!

* Source: K. Fox, et al. Journal of the American Medical Profession 297, 2007**Source: Center of Disease Control, 2009*** Source: D.K. Epsey, et al, Cancer 116, no. 3, 2010

CHOICES

16

Choices: Pharma’s Present—and Future—Path

How are we choosing to:• Respond to economic and investor pressures?• Ensure that we get new products to market?• Gain efficiencies and expedite

clinical trial execution?• Foster Innovation?

CONSOLIDATIONSPORTFOLIO PRIORITIZATION

PARTNERSHIPSOUTSOURCING

EXECUTIONAL EXCELLENCEGLOBALIZATION

INNOVATION …. AND MORE!

17

Responding to Economic and Investor Pressures

• Mergers within the last few years consolidated some major pharmaceutical “powerhouses”• Pfizer /Wyeth; Roche /Genentech; Merck /Schering-Plough

• Integrating companies results in positives and negatives:

CONSOLIDATIONS

That sucking sound? Layoffs draining brains from pharmaAugust 22, 2011

October 25, 2011, 12:38 PM GMT

Job Cuts Hurt, But Will Save Novartis Future Pain

July 8, 2010 1:13 PM

Merck Closing 8 Plants,8 Research Sites

18

New Strategies Rationalizing R&D Spending

• Some companies are slashing R&D spending in response to investor demands

• Others are prioritizing investments based on morecalculated risks / returns• Harder look at early

development programs• Increased willingness to

“kill” programs earlier andmore often

• Changing incentives / rewardsto match changing strategy

PRIORITIZING PORTFOLIOS

19

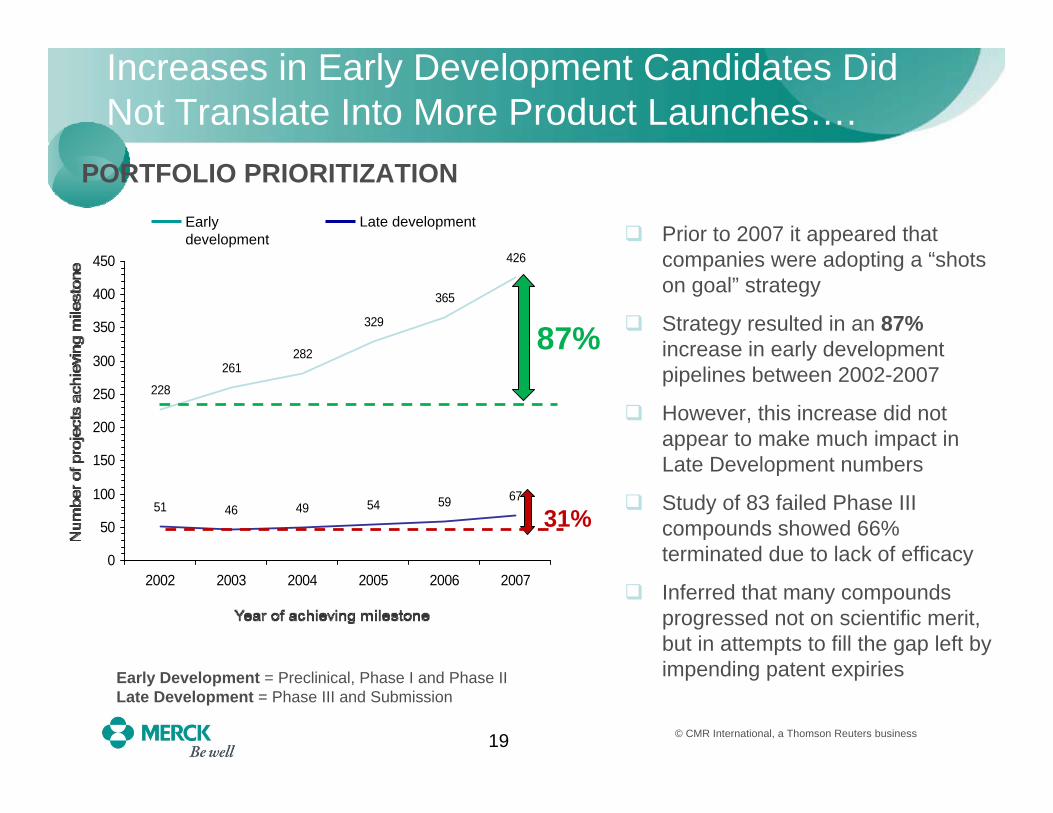

Increases in Early Development Candidates Did Not Translate Into More Product Launches….

228

261282

329

365

426

51 46 49 54 59 67

0

50

100

150

200

250

300

350

400

450

2002 2003 2004 2005 2006 2007

Early development

Late developmentPrior to 2007 it appeared that companies were adopting a “shots on goal” strategy

Strategy resulted in an 87%increase in early development pipelines between 2002-2007

However, this increase did not appear to make much impact in Late Development numbers

Study of 83 failed Phase III compounds showed 66% terminated due to lack of efficacy

Inferred that many compounds progressed not on scientific merit, but in attempts to fill the gap left by impending patent expiries

87%

31%

Early Development = Preclinical, Phase I and Phase IILate Development = Phase III and Submission

© CMR International, a Thomson Reuters business

PORTFOLIO PRIORITIZATION

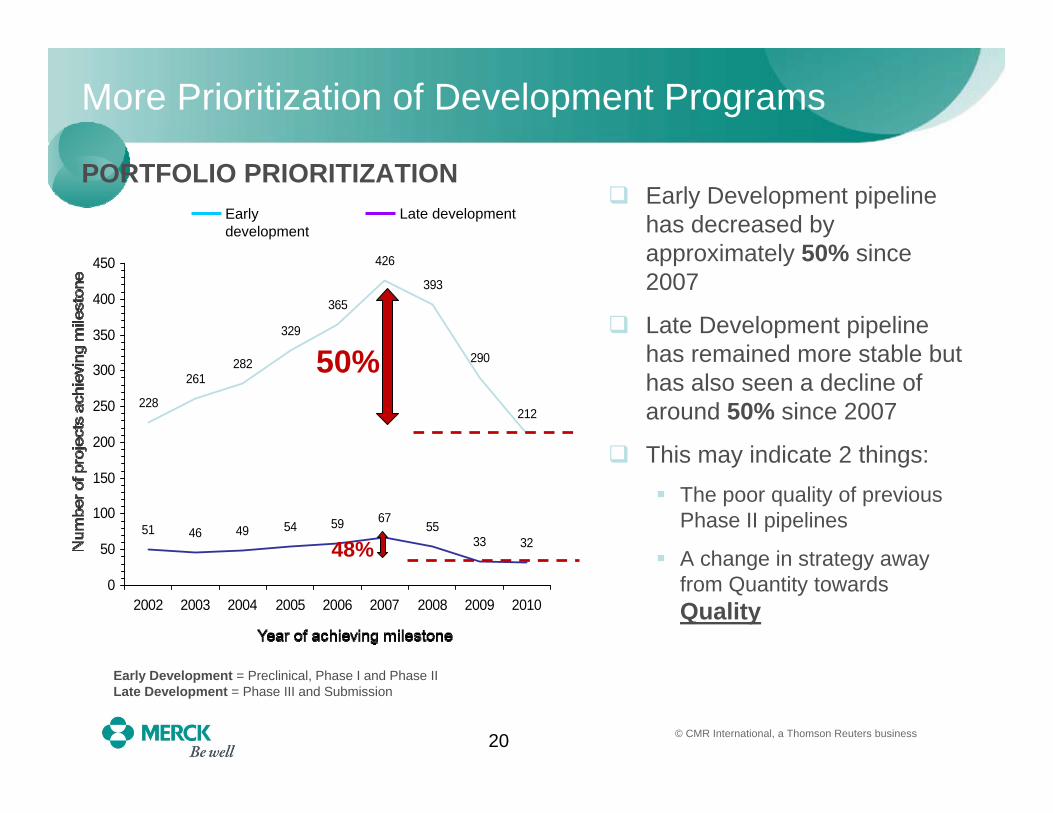

20

228

261282

329

365

426

393

290

212

51 46 49 54 59 6755

33 32

0

50

100

150

200

250

300

350

400

450

2002 2003 2004 2005 2006 2007 2008 2009 2010

More Prioritization of Development Programs

Early development

Late developmentEarly Development pipeline has decreased by approximately 50% since 2007

Late Development pipeline has remained more stable but has also seen a decline of around 50% since 2007

This may indicate 2 things:The poor quality of previous Phase II pipelines

A change in strategy away from Quantity towards Quality

50%

48%

Early Development = Preclinical, Phase I and Phase IILate Development = Phase III and Submission

© CMR International, a Thomson Reuters business

PORTFOLIO PRIORITIZATION

21

Increased Use of Adaptive Trials

• Companies increasingly choosing to determine a drug's benefit/risk ratio at specific study points in pivotal trials

• Rise in adaptive designs for clinical trials• In adaptive trials, decisions for mid-study changes can be made

at predetermined opportunity points • Decisions based on information available to date

– No waiting for total trial data• Greater use of sophisticated portfolio management

techniques

• Stop the development process sooner, not later if a drug won't prove safe, effective or be approved for sale

PORTFOLIO PRIORITIZATION

22

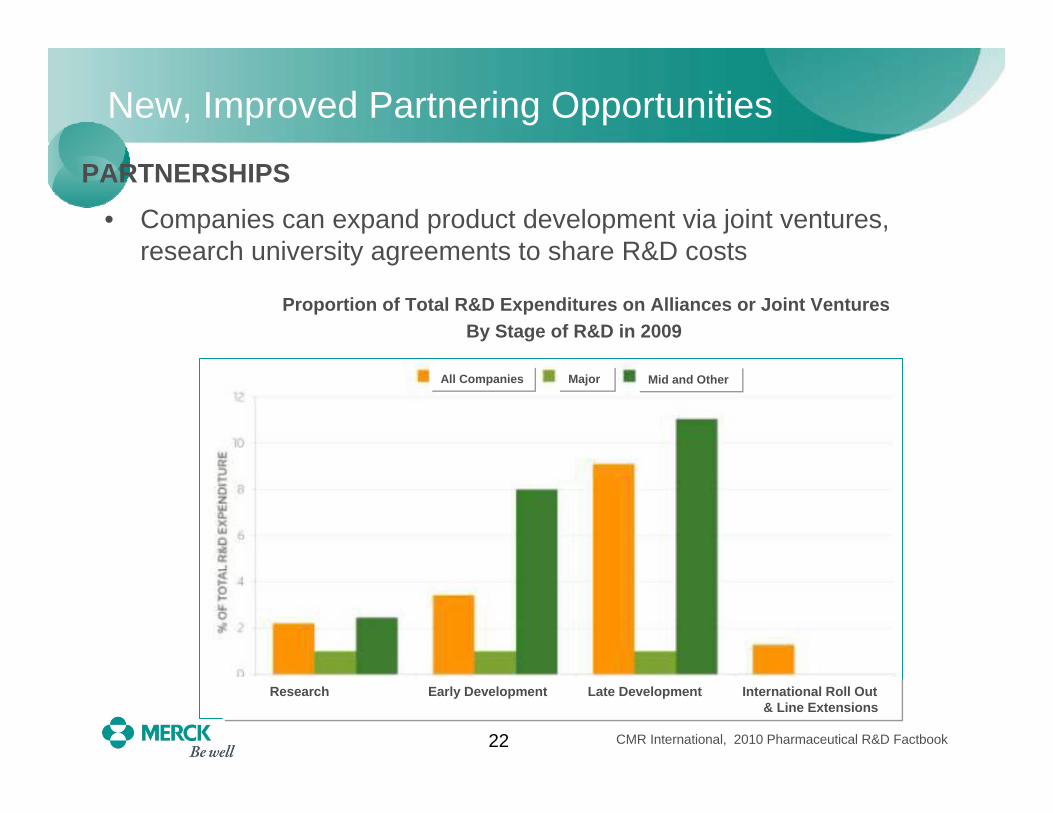

New, Improved Partnering Opportunities

• Companies can expand product development via joint ventures, research university agreements to share R&D costs

Proportion of Total R&D Expenditures on Alliances or Joint VenturesBy Stage of R&D in 2009

CMR International, 2010 Pharmaceutical R&D Factbook

PARTNERSHIPS

Research Early Development Late Development International Roll Out s & Line Extensions

All Companies Major Mid and Other

23

Partnering for Global Reach, Improved Efficiency

• Grow top line by creating new and different partnerships: • Strengthen push into global or emerging markets

• Improve bottom line in other areas:– Manufacturing as well as clinical: Merck and UPS– Outsourcing clinical activities to

Contract Research Organizations (CROs)

PARTNERSHIPS

24

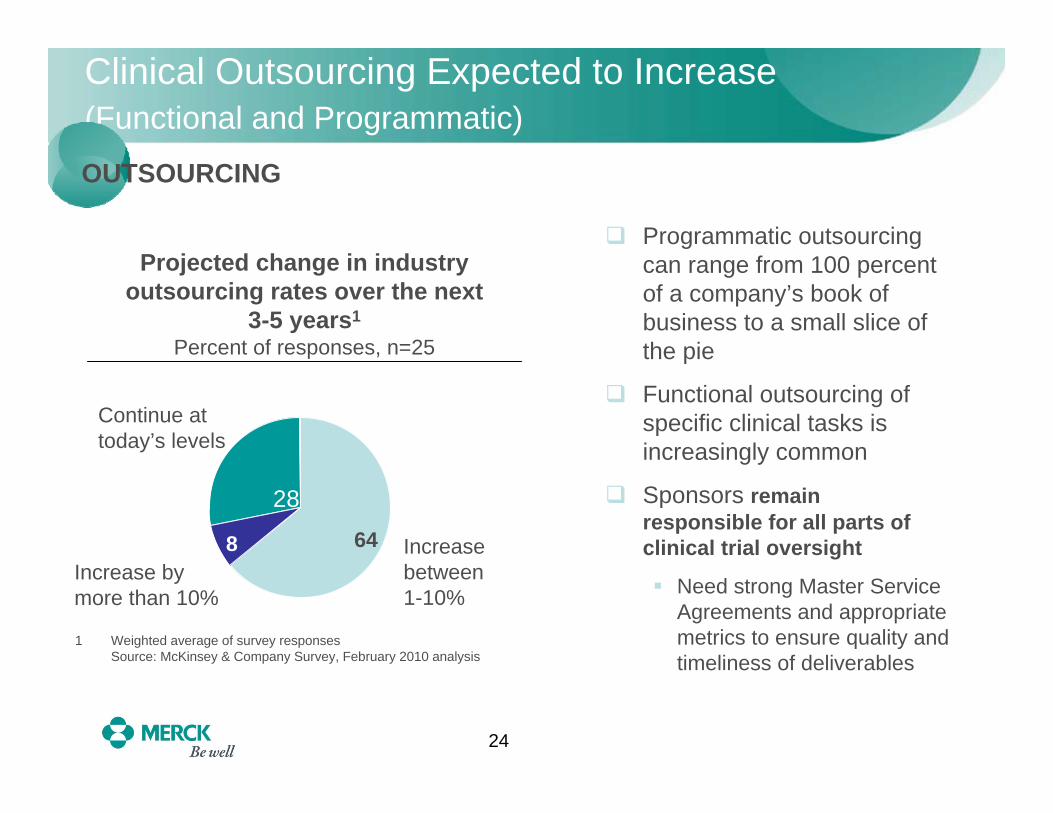

Clinical Outsourcing Expected to Increase(Functional and Programmatic)

Increase bymore than 10%

Increase between 1-10%

Continue at today’s levels

28

1 Weighted average of survey responsesSource: McKinsey & Company Survey, February 2010 analysis

Projected change in industry outsourcing rates over the next

3-5 years1

Percent of responses, n=25

8 64

28

Programmatic outsourcing can range from 100 percent of a company’s book of business to a small slice of the pie

Functional outsourcing of specific clinical tasks is increasingly common

Sponsors remain responsible for all parts of clinical trial oversight

Need strong Master Service Agreements and appropriate metrics to ensure quality and timeliness of deliverables

OUTSOURCING

25

Strategic Rationale for More Clinical Outsourcing

• Quality and capabilities of major Contract Resource Organizations (CROs) have increased worldwide • Provide more access to global capabilities and infrastructure for

conducting clinical trials

• Improves a pharma company’s flexibility in adjusting to a volatile book of business and associated labor demands• Reduces fixed operating costs• Meets demands for specific job roles while potentially moving

some work to lower-cost geographies with skilled workforces • Reduces risk for “stranded resources” when studies end• Allows companies to focus on core capabilities internally

• Provides performance /cost transparency

OUTSOURCING

26

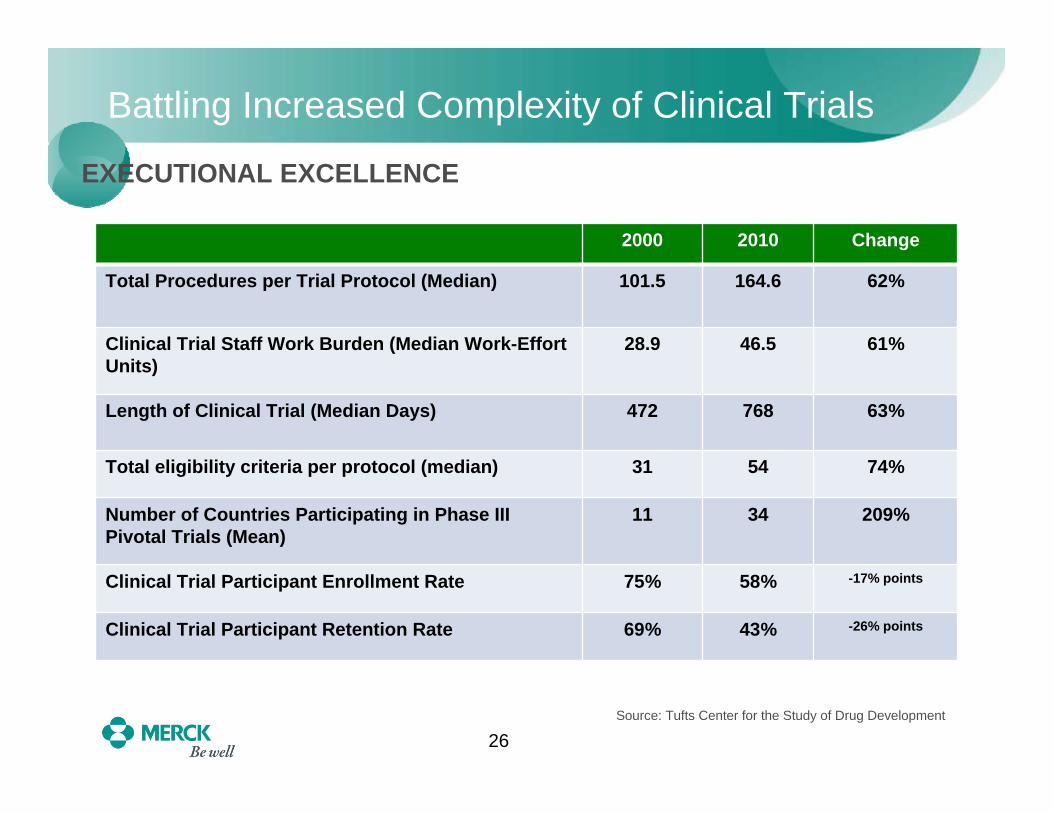

Battling Increased Complexity of Clinical Trials

Changes in Clinical Trials: Resources, Length and Participation

Source: Tufts Center for the Study of Drug Development

EXECUTIONAL EXCELLENCE

2000 2010 Change

Total Procedures per Trial Protocol (Median) 101.5 164.6 62%

Clinical Trial Staff Work Burden (Median Work-Effort Units)

28.9 46.5 61%

Length of Clinical Trial (Median Days) 472 768 63%

Total eligibility criteria per protocol (median) 31 54 74%

Number of Countries Participating in Phase III Pivotal Trials (Mean)

11 34 209%

Clinical Trial Participant Enrollment Rate 75% 58% -17% points

Clinical Trial Participant Retention Rate 69% 43% -26% points

27

• Global clinical trials are very difficult to plan and manage• Need the right protocol… right mix of countries … right

investigators…high-performing Clinical Trial Teams– Including internal and contracted resources globally

• Need sites to initiate on time– With drug on hand and EDC ready to go

• Appropriate monitoring plans must be in place• Review patient enrollment plans• Verify storage conditions for clinical supplies• Review emergency un-blinding procedures• Perform source data verification

• Last but not least: we need patients!

Expediting Clinical Trial ExecutionEXECUTIONAL EXCELLENCE

28

Improving Patient Recruitment

• Variety of patient enrollment factors• Eligibility• Willing participation; good retention rate

• Accurate patient enrollment projections are necessary for success• Under-estimating patient enrollment leads

to too many patients enrolling too soon• Lagging behind enrollment projections

impacts schedule and resources

• Experimenting with new technologies / social media for qualified patient recruitment

EXECUTIONAL EXCELLENCE

29

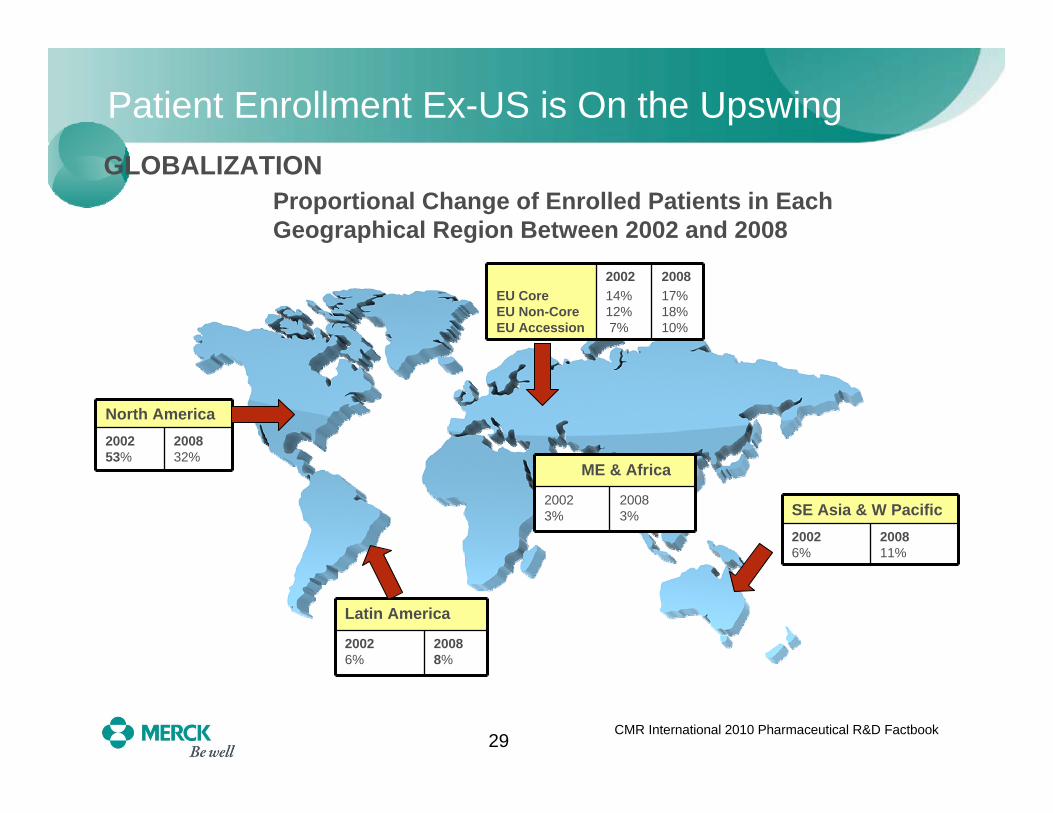

Patient Enrollment Ex-US is On the Upswing

Latin America

20026%

20088%

ME & Africa

20023%

20083%

North America200253%

200832%

GLOBALIZATIONProportional Change of Enrolled Patients in Each Geographical Region Between 2002 and 2008

CMR International 2010 Pharmaceutical R&D Factbook

SE Asia & W Pacific20026%

200811%

EU CoreEU Non-CoreEU Accession

200214%12%7%

200817%18%10%

30

More Emphasis on Country Site Selections

• Appropriate selection of countries for clinical trials, based on: • Good access to patients• Disease state/standard of care compatible with protocol • Quality of available investigators:

– Sufficiently trained staff to manage study procedures– Healthcare professionals who understand clinical trials, ICH / GCPs– Understand local regulatory requirements and healthcare environment

• Adequate facility for evaluating patients and performing study procedures

– Good storage conditions for clinical supplies– Ability to perform source data verification

• Speed of regulatory / Institutional Review Board (IRB) Approvals

• Cost of doing business

GLOBALIZATION

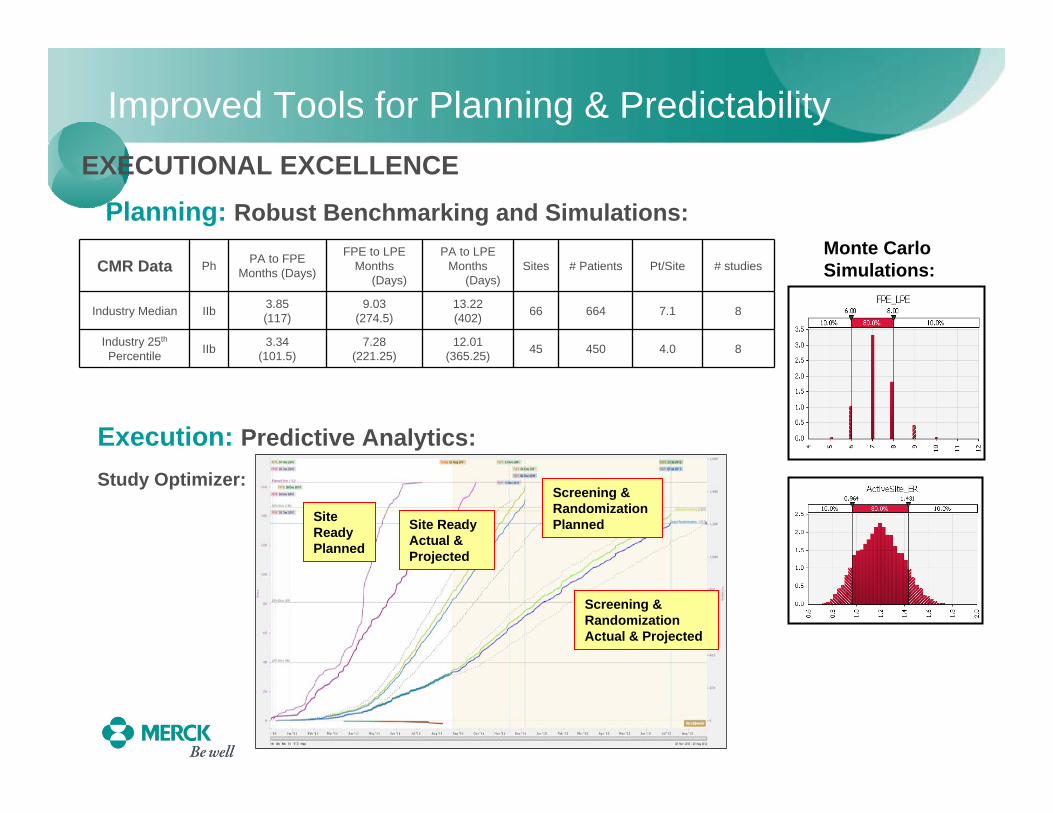

Improved Tools for Planning & Predictability

Planning: Robust Benchmarking and Simulations:

CMR Data Ph PA to FPEMonths (Days)

FPE to LPEMonths

(Days)

PA to LPEMonths

(Days)Sites # Patients Pt/Site # studies

Industry Median IIb 3.85(117)

9.03(274.5)

13.22(402) 66 664 7.1 8

Industry 25th

Percentile IIb 3.34(101.5)

7.28(221.25)

12.01(365.25) 45 450 4.0 8

EXECUTIONAL EXCELLENCE

Execution: Predictive Analytics:

Monte CarloSimulations:

Study Optimizer:

Site Ready Planned

Site Ready Actual & Projected

Screening & Randomization Planned

Screening & Randomization Actual & Projected

32

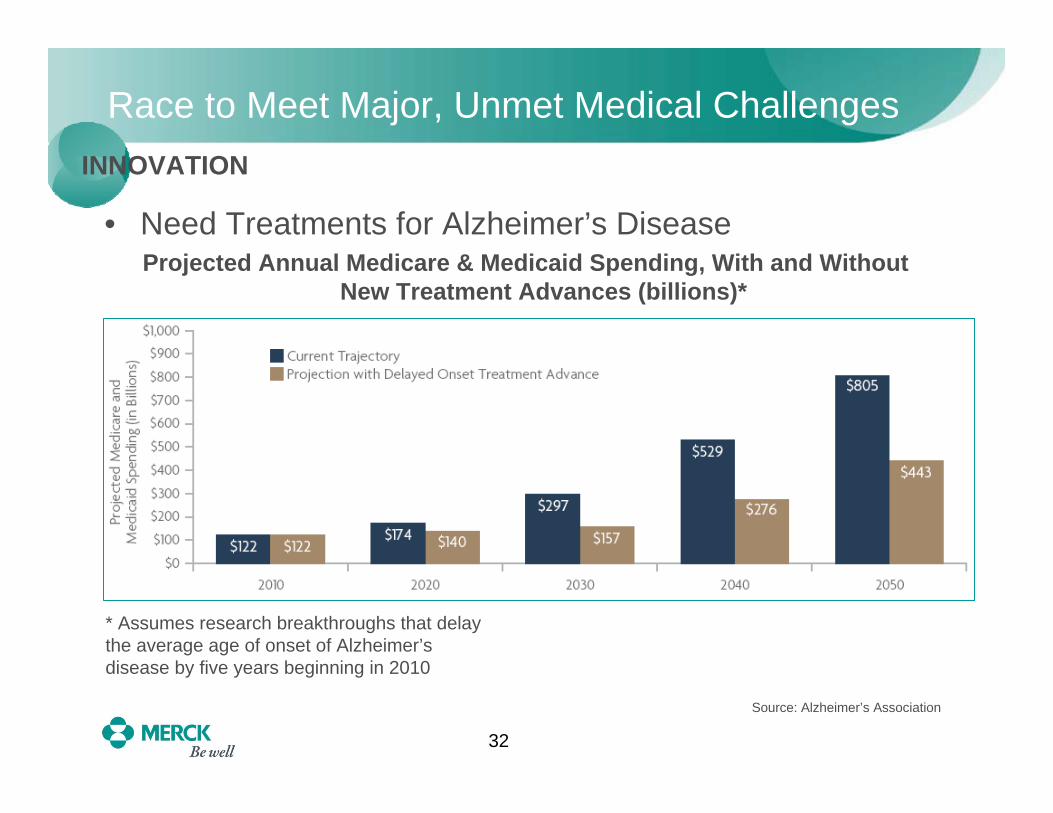

Race to Meet Major, Unmet Medical Challenges

• Need Treatments for Alzheimer’s DiseaseProjected Annual Medicare & Medicaid Spending, With and Without

New Treatment Advances (billions)*

* Assumes research breakthroughs that delay the average age of onset of Alzheimer’s disease by five years beginning in 2010

Source: Alzheimer’s Association

INNOVATION

33

Need New Treatments for Degenerative Disorders

• Parkinson’s Disease Costs Society $27 billion Per Year in Medical Bills and Lost WagesProjected Worldwide Increase in Prevalence of Parkinson’s Disease

INNOVATION

E.R. Dorsey, et al: Neurology 68, no. 5 (2007)

34

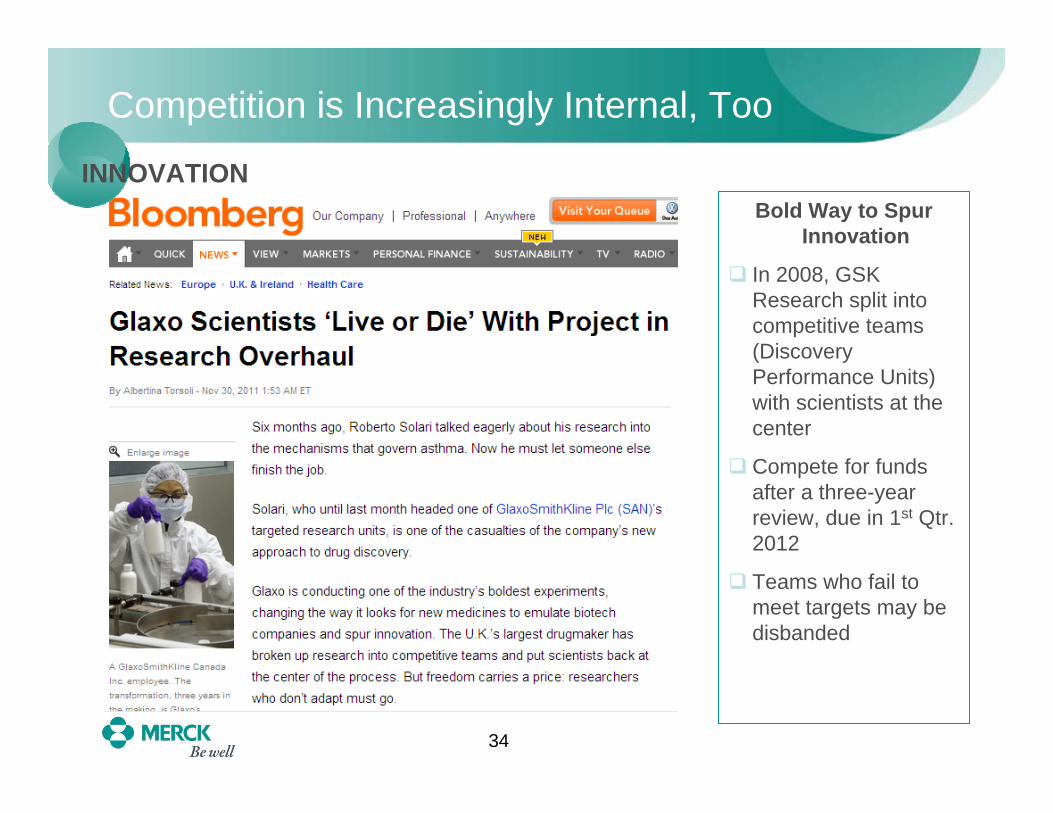

Competition is Increasingly Internal, Too

INNOVATIONBold Way to Spur

Innovation

In 2008, GSK Research split into competitive teams (Discovery Performance Units) with scientists at the center

Compete for funds after a three-year review, due in 1st Qtr. 2012

Teams who fail to meet targets may be disbanded

CHANGES

36

We Must Adapt Behavior, Culture to New Reality

• Work differently to be successful • Changing internal culture and behaviors is not easy• “Big Pharma” had long been a stronghold in the economy

– Viewed as secure, high-quality employers and corporate citizens• Now we are an industry under siege – from payers and

consumers

• Commit to increasing external licensing and research• R&D investment is too costly to always be done alone

• Make globalization work• People need our medicines everywhere• Partnering can help us reach patients

and markets without substantial internal investments

37

What Has to Change in Development for Big Pharma?

• Organizational inertia• Overcome tendency to just keep doing things the way we always have• Build structures that are flexible and adaptable to constant changes in

demography and geography of the development portfolio• Aversion to constant process evolution

• Alleviate concerns that changing something will impact safety orcompliance

• “Not invented here” syndrome• Be willing to partner on innovative therapies and new ways of operating• Cultivate and enhance capabilities in vendor oversight and management

– Without doing their work for them!

• Change attitude that vendors are “just” service providers• Build strong relationships with vendors across all levels of organization• Work collaboratively, as one team• Make vendor oversight and management a core capability

38

Exploring the Ways to “Get it Right”