idc vendor assessment

TRANSCRIPT

March 2016, IDC #US41126416

IDC MarketScape

IDC MarketScape: Worldwide Life Science R&D Strategic Consulting Services 2016 Vendor Assessment

Alan S. Louie, Ph.D.

IDC MARKETSCAPE FIGURE

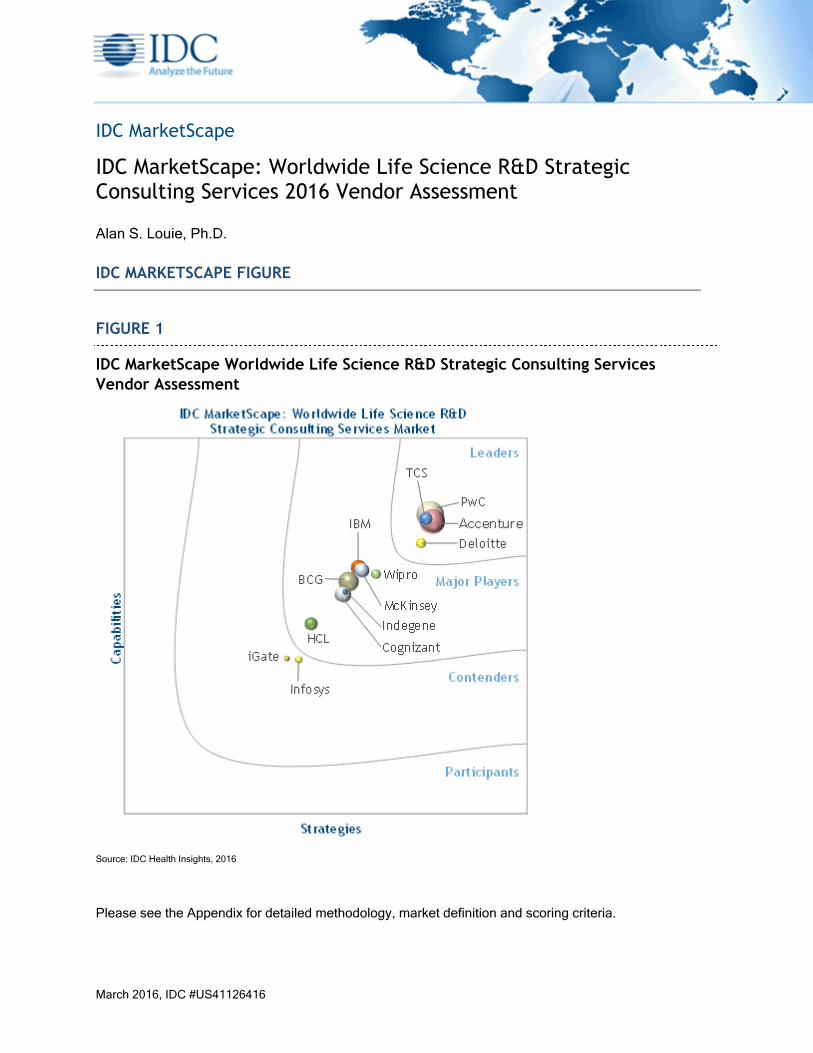

FIGURE 1

IDC MarketScape Worldwide Life Science R&D Strategic Consulting Services

Vendor Assessment

Source: IDC Health Insights, 2016

Please see the Appendix for detailed methodology, market definition and scoring criteria.

©2016 IDC #US41126416 2

IDC OPINION

In our continuing coverage of this space, it is clear that strategic consulting service providers have

continued to grow in both experience and capabilities, resulting in more options for sponsors looking

for competent service providers. In addition, as the industry has focused on externalization strategies

to deliver increased agility and cost savings, preferred service providers are increasingly delivering a

full suite of BPO and ITO solutions in support of strategic consulting efforts. Further, as the boundaries

between the life sciences and healthcare continue to blur, strategic consulting service providers are

increasingly being asked to develop and implement strategies that link or connect data and processes

between the two industries. The demand for strategic consulting services in the life science industry

continues to grow as companies transform themselves in pursuit of long-term sustainability. From a

strategic consulting perspective, transformation initiatives are taking many forms such as traditional

high-level management consulting, organizational transformation, application rationalization,

operations optimization, and infrastructure optimization. Each of these efforts typically requires

strategy development and implementation support from specialist service organizations with relevant

experience. Selecting the right vendor can help organizations efficiently and effectively transform their

organizations, while selecting the wrong vendor often results in wasted resources, lost time, and

potential damage to future success. Like other service areas (i.e., BPO and ITO), strategic consulting

services have experienced double-digit annual growth over the past five years, with significant

expansion beyond traditional service providers as major IT service providers have built industry-

specific expertise and started to expand beyond their IT services strengths to begin to provide more

comprehensive service offerings. Overall, successful strategic consulting service providers are

growing in a variety of ways, including through the expansion of existing client relationships, expanded

offerings (especially through direct support of strategic guidance implementation), and new clients

(especially in expanding the midtier market and with nontraditional entities [e.g., precompetitive

industry consortia]). As expected, premier life science companies routinely engage with a number of

different strategic consulting service providers to most effectively address the diverse strategic

consulting needs present within the organization. Because of the complexity of the life science R&D

market, it is clear that strategic consulting service providers vary widely in the relative strengths of their

offerings. While there are routinely multiple vendors with sufficient experience to compete for RFIs,

RFPs, and other service requests, it is important for companies to shrink the broad list of prospective

vendors to a short list of three to five finalists based on a balanced scorecard that accurately captures

specific company requirements and needs. Successful selection of a single or limited number of

preferred service provider(s) depends on careful consideration of key criteria. Building on contributions

from 13 major life science R&D strategic consulting service providers (including both premier vendors

and the emerging new vendors in this space), this study examines the life science R&D strategic

consulting vendor landscape today with a view toward expected growth over the next three to five

years. This is the third of three documents (BPO, ITO, and strategic consulting) examining services

outsourcing in the life science R&D space. When evaluating vendors, the key criteria that IDC believes

life science companies should consider include:

Breadth of life science R&D strategic consulting services offered; the depth of related platform, project, and/or transformational initiative experience; and the number of prior relatedengagements the vendor has successfully completed

Geographical footprint and global delivery capabilities (typically associated with strategy implementation), level of priority and focus by the vendor on the life science R&D sector, and

the vendor's pace of investment in related life scientific and/or technology-specific areas

©2016 IDC #US41126416 3

Depth of business-related, industry-specific knowledge and the ability to apply this knowledge to improving specific client performance and success

Foundational service capabilities (where applicable), corporate financial stability, and the ability to accommodate different types and sizes of life science clients

Diligent vetting of customer references to examine vendor capabilities surrounding project management, technical skills, account management, and overall value delivery to clients

IDC MARKETSCAPE VENDOR INCLUSION CRITERIA

IDC frequently has unique visibility into vendor selection processes within life science companies

through clients and contacts in the industry. For a vendor to be considered for inclusion in this study,

the vendor's services must have been significantly evaluated for the potential to engage clients within

the target IDC MarketScape space. Further research and due diligence were then conducted to narrow

the list of vendors to only those that IDC views as legitimate contenders for future deals within the

pharmaceutical R&D space. The 13 life science R&D strategic consulting vendors selected to

participate in this study were:

Accenture

Boston Consulting Group (BCG)

Cognizant Technology Solutions

Deloitte

HCL Technologies

IBM

iGate

Indegene

Infosys

McKinsey

PricewaterhouseCoopers (PwC)

Tata Consultancy Services (TCS)

Wipro

Note that BCG, IBM, iGate, and McKinsey declined to respond to the study RFI. As active vendors in

the space, it was decided that the companies should still be included in this study. As a result, the

assessments for these companies were based completely on IDC primary research data, public data

available to IDC, and the best estimates of IDC analysts.

ESSENTIAL BUYER GUIDANCE

Strategic consulting services in the life science industry are increasing and expanding in importance as

the life science companies continue to transform themselves in pursuit of long-term sustainability. With

BPO, IT outsourcing, and external partnerships and collaborations increasingly the norm, strategic

consulting services are evolving to incorporate new business best practices and expanding

organizational footprints while concurrently optimizing both cost and organizational agility. While some

general pressures exist for life science companies to consolidate their vendor ecosystem into a limited

number of preferred providers, the high-profile nature of strategic consulting has somewhat limited

©2016 IDC #US41126416 4

consolidation efforts in this area. Where appropriate, savvy IT service providers are actively and

aggressively working to expand their offerings to include strategic consulting capabilities, typically in

areas adjacent to vendor service strengths.

In IDC's view of the strategic consulting ecosystem, key attributes that life science companies are

looking for in their service providers include:

Traditional management consulting expertise and experience

Deep life science industry and/or technology-specific knowledge (where appropriate) in the

area of interest

Practical understanding of application, platform, framework, and infrastructure best practices

where needed

Operational experience in the area of interest as appropriate

Understanding of the life science business at both company and tactical levels

Access to industry-adjacent best practice knowledge where appropriate

The ability to deliver both strategic guidance and direct implementation support for the project

of interest

Strong referenceable clients

At the next level, additional factors that life science companies may consider during their vendor

selection include:

The ability to work effectively with multiple stakeholders (including competing service providers) to drive transformation initiatives, regardless of organizational boundaries

Experience and knowledge from adjacent industries

Internal agreement on the relative importance of quality versus cost in the selection of a

service provider

The ability to deliver a unified service capability over multiple service or geographical areas

The potential to seamlessly expand services delivered across BPO, ITO, and strategicconsulting as part of preferred vendor relationships

Compatible corporate cultures

Historic corporate relationships that could impact vendor selection

VENDOR SUMMARY PROFILES

This section briefly explains IDC's key observations resulting in a vendor's position in the IDC

MarketScape. While every vendor is evaluated against each of the criteria outlined in the Appendix,

the description here provides a summary of each vendor's strengths and challenges.

Accenture

Established in 1989, Accenture has been serving the life science industry for the past 29 years and is

headquartered out of Dublin, Ireland. The company has offices and operations in more than 200 cities

in 55 countries around the world. Although Accenture does not report revenue by industry, IDC

estimates that Accenture derives roughly 5% of its revenue from the life sciences, and we further

estimate that 30% of this revenue comes from R&D-focused engagements. Accenture employs

©2016 IDC #US41126416 5

approximately 373,000 people worldwide, including 13,000 people dedicated to its life science practice

for the fiscal year ending August 31, 2015.

After a close evaluation of Accenture's offerings and capabilities, IDC has positioned the company in

the Leaders category within this IDC MarketScape. The company has a historically strong presence in

life science R&D, including a wide portfolio of BPO, ITO, and strategic consulting service offerings; an

increasingly diverse customer base; and significant success in engaging life science companies.

These capabilities and the company's strong commitment to growing and expanding its capabilities

and experience in this area will routinely position Accenture as a formidable competitor in RFPs and

RFIs it responds to in the strategic consulting and broader R&D IT services market.

Strengths

Accenture has extensive experience working with life science companies across all three sections of

the industry: pharmaceutical, biotech, and medical devices. Building on an aggressive growth and

acquisition strategy, Accenture has diversified significantly beyond its traditional big pharma focus and

has grown its presence among emerging and midtier life science companies in recent years, including

adding significant regulatory compliance services capabilities from its acquisition of Octagon Research

Solutions. Accenture's customer base is well represented across North America, Europe, and

Asia/Pacific. Accenture also has a considerable number of delivery centers located across these three

regions as well as in Latin America. Relative to other vendors discussed in this study and based on

feedback from customer references, Accenture received high marks as a knowledgeable, unbiased,

high-quality service provider willing to work side by side with company teams while asking the right

questions and capably filling project knowledge gaps.

Challenges

Accenture has a strong history of delivering strategic consulting services to the life science industry.

With deep relationships in place and growing capabilities, Accenture is well positioned to continue to

expand its influence in the industry. With outsourced services increasingly available to life science

companies of all sizes and types, Accenture should continue to expand and customize its offerings to

make the company more attractive to companies of all sizes, which should allow the company to

continue to grow its influence in the industry. From a service offering perspective, strategic consulting

services positioned for further development by Accenture should include its predictive modeling,

regulatory compliance, and mobile platform services.

BCG

Founded in 1963, BCG has been serving the life science industry for more than 35 years and is

headquartered out of Boston, Massachusetts. The company has 85 offices in 48 countries around the

world. Although BCG is a private company and does not report revenue by industry, IDC estimates

that the company derives roughly 5% of its revenue from the life sciences, and we further estimate that

30% of this revenue comes from R&D-focused engagements. BCG employs approximately 12,000

people worldwide.

After a close evaluation of BCG's offerings and capabilities, IDC has positioned the company in the

Major Players category within this IDC MarketScape. BCG has been a strategic consulting service

provider to a wide variety of industries worldwide since its inception. The company actively competes

with life science companies for strategic consulting projects as it has particular strengths in both

business strategy and performance optimization. IDC estimates that BCG generates most of its life

science revenue from top-tier life science companies, although the company also works with midtier

©2016 IDC #US41126416 6

companies, nonprofit organizations, and government agencies. In recent years, BCG has expanded its

capabilities beyond its traditional high-level strategic services to deliver more tactical consulting

services, allowing the company to begin to provide a more complete consulting offering. With these

increasingly comprehensive capabilities, BCG is beginning to gain traction in delivering services

beyond its historically strategic focus.

Strengths

BCG has extensive experience working with life science companies across all three sections of the

industry: pharmaceutical, biotech, and medical devices. With separate biopharmaceutical and medical

device practices, BCG has a wealth of traditional strategic consulting capabilities covering the full life

science value chain. BCG continues to be well situated as a key global strategic consulting service

provider with particular strengths in helping to deliver business transformation. Relative to other

vendors discussed in this study, BCG received high marks for its business insights and understanding

of how to effectively expand into new markets and geographies.

Challenges

BCG has a strong legacy of helping senior management create viable strategies in changing business

ecosystems. This continues to be an ongoing challenge in the life science industry today, which should

help BCG continue to grow its presence in the industry. With its added focus on operational support

consulting services, BCG is beginning to face traditional BPO and ITO competitors head on. While

experience and pricing will likely be a differentiator for broader client engagements, BCG is also facing

increased competition from competitors that are increasingly growing their own strategic consulting

capabilities. From a service offering perspective, strategic consulting services positioned for further

development by BCG should include the continuation of expanding its capabilities in helping its clients

to work across traditional industry boundaries to expand business opportunities.

Cognizant

Established in 1994, Cognizant has been serving the life science industry for almost 22 years. The

company, headquartered out of Teaneck, New Jersey, has over 100 delivery and operations centers in

50 countries. IDC estimates that Cognizant derives roughly 30% of its revenue from combined

healthcare and life science efforts, and we estimate that 35% of life science efforts focus on R&D-

related engagements. Cognizant employs more than 219,300 people worldwide, including more than

16,000 people dedicated to its life science practice.

After a close evaluation of Cognizant's offerings and capabilities, IDC has positioned the company in

the Major Players category within this IDC MarketScape. The company is particularly strong in

delivering analytics, organizational change management, and process optimization strategic consulting

services. The company's broad portfolio of life science–specific strategic consulting services makes

Cognizant a consistently strong competitor in providing these capabilities to top-tier and midtier life

science companies as an alternative to traditional strategic consulting service providers.

Strengths

Cognizant has extensive experience working with life science companies across all three sections of

the industry: pharmaceutical, biotech, and medical devices. Roughly 90% of Cognizant's life science

customers are large corporations with revenue over $1 billion, and the remaining 10% are primarily

midsize companies. The majority of Cognizant's customer base is spread across North America and

Europe, and the company has a considerable number of delivery and operations centers located

©2016 IDC #US41126416 7

across both of these regions as well as in Asia and Latin America. Relative to other vendors discussed

in this study, Cognizant was recognized for its understanding of its client's business needs, strong

client team leadership, ability to rapidly staff projects to minimize business disruption, and ability to

deliver high-quality services to its clients.

Challenges

While Cognizant has already begun to expand its offerings beyond big pharma, there is a continued

opportunity for the company to grow its client base in the emerging and midtier space. In addition, with

rapid industry growth in Asia/Pacific, Cognizant should be able to leverage its strong R&D services

portfolio to grow its presence in this market. From a service offering perspective, strategic consulting

services positioned for further development by Cognizant should include predictive modeling, mobile

platform development, and translational research strategic support capabilities.

Deloitte

Established in 1845, Deloitte has been serving the life science industry for over 27 years. The

company, headquartered in New York, New York, has offices in more than 150 countries. While IDC

estimates that Deloitte derives approximately 4% of its revenue from the life sciences, we also

estimate that 20% of the company's healthcare and life science revenue comes from R&D-focused

engagements. Deloitte employs more than 210,000 people worldwide, including approximately 5,000

people dedicated to its life science practice.

After a close evaluation of Deloitte's offerings and capabilities, IDC has positioned the company in the

Leaders category within this IDC MarketScape. Within the strategic consulting space, Deloitte is

particularly strong in delivering high-level management consulting, organizational change

management, and R&D operating model design and development for its clients. As one of the

industry's pioneering service providers, Deloitte is consistently a strong competitor in providing

strategic consulting services to a broad spectrum of life science industry clients.

Strengths

Deloitte is an experienced vendor providing its services across all three sections of the industry:

pharmaceutical, biotech, and medical devices. IDC estimates that while more than 60% of Deloitte's

clients are large corporations with revenue over $1 billion, the company has a substantial presence in

the midtier biopharma space and ongoing efforts with smaller biotechs. Deloitte's customers are

spread across North America, Europe, and Asia/Pacific, with North America representing slightly more

than 50% of the company's industry services. Deloitte has a number of delivery centers located around

the world, with major centers in the United States, India, and China. Relative to other vendors

discussed in this study and based on feedback from customer references, Deloitte's deep experience,

strong industry knowledge, transparent methodology, business acumen, and strategic mindset all help

to differentiate the company from its competitors.

Challenges

With its large and highly diversified client base, Deloitte should be able to increase its influence in the

industry by growing its existing client relationships as well as by adding new clients. With its strong life

science R&D service offerings, Deloitte will benefit by expanding its innovation-based, industry-specific

service offerings to expand its presence within client companies. From a service offering perspective,

strategic consulting services positioned for further development by Deloitte should include predictive

©2016 IDC #US41126416 8

modeling, technology-based 3rd Platform (especially mobility), and outsourcing/CRO management

strategic consulting services.

HCL

Established in 1991, HCL has been serving the life science industry for more than 12 years. The

company, headquartered out of Noida, India, has offices in 31 countries. IDC estimates that HCL

derives over 11% of its revenue from the life sciences, roughly 36% of which comes from R&D-focused

engagements. HCL employs more than 103,700 people worldwide, including more than 8,700 people

dedicated to its life science practice.

After a close evaluation of HCL's offerings and capabilities, IDC has positioned the company in the

Major Players category within this IDC MarketScape. Within the life science R&D strategic consulting

space, HCL is particularly strong in delivering analytics, process optimization, and regulatory

compliance strategic support services to its clients. With its targeted focus, HCL is aggressively

growing its services to the industry with the goal of becoming a full service resource to its growing life

science client base.

Strengths

HCL has extensive experience working with life science companies across all three sections of the

industry: pharmaceutical, biotech, and medical devices. Nearly all of HCL's life science customers are

large corporations with revenue over $1 billion, with a significant base of customers spread across

North America, Europe, and Asia/Pacific. HCL also has a considerable number of delivery centers

located across these three regions as well as in Latin America. Relative to other vendors discussed in

this study, HCL was recognized for its industry knowledge, differentiating resources in emerging

regions, and ability to work across the full clinical life cycle.

Challenges

As an experienced global service provider to the life science industry, HCL has historically focused its

efforts on top-tier clients with revenue above $1 billion. As the industry continues to expand through

external collaboration, there is a significant emerging opportunity from the emerging and midtier sector

of the industry. HCL has an opportunity to grow its strategic consulting services by leveraging its

strong ITO client relationships with existing top-tier clients and creating offerings specifically targeted

toward emerging and midtier life science companies. From a service offering perspective, strategic

consulting services positioned for further development by HCL include its predictive modeling and

organizational change management support services.

IBM

Established in 1911, IBM has been serving the life science industry for more than 42 years and is

headquartered out of Armonk, New York. The company has offices and operations in more than 175

countries around the world. Although the company has not reported revenue by industry, IDC

estimates that IBM derives roughly 1% of its revenue from the life sciences, and we further estimate

that 10% of this revenue comes from R&D-focused engagements. IBM employs more than 377,000

people worldwide, including more than 2,500 dedicated to its life science practice.

After a close evaluation of IBM's offerings and capabilities, IDC has positioned the company in the

Major Players category within this IDC MarketScape. IBM's shift away from traditional IT and move

toward Watson and cognitive computing is an important strategic move that remains early in its

adoption in the life sciences. While highly promising, it remains to be seen whether IBM Watson will

©2016 IDC #US41126416 9

deliver to its potential in the life sciences, particularly so in changing how data is handled across the

increasingly growing life science/healthcare ecosystem. If successful, IBM Watson has the potential to

become a foundational presence, requiring strong life science IT service delivery across the industry.

Strengths

IBM has extensive experience working with life science companies across all three sections of the

industry: pharmaceutical, biotech, and medical devices. While IBM's traditionally strong strategic R&D

IT outsourcing services are in decline, the company's development of IBM Watson as a cognitive

computing engine is unmatched in the industry. IBM works with life science customers of all sizes and

has a strong base of customers spread across North America, Europe, and Asia/Pacific. Relative to

other vendors discussed in this study, IBM received high marks as a global thought leader with

foundational technical expertise and a renewed focus on emerging opportunities, including genomics,

cognitive computing, and next-generation IT.

Challenges

With its life science technology and infrastructure-based strategic services in decline, IBM has focused

on Watson and cognitive computing as its growth foundation for the future. With deep relationships in

place, IBM is seeking to grow opportunities with Watson among its existing client base and with new

prospective clients, including supporting collaborations across both life science R&D and healthcare

delivery spaces. While still early, IBM should further develop its Watson-based cognitive innovation

solutions and technology-based analytical frameworks to help both life science and healthcare

companies deliver near-term value to its clients.

iGate

Founded in 1986, iGate has been serving the life science industry for more than 27 years. With

completion of its acquisition by Capgemini in June 2015, iGate has become part of a much larger $14

billion services organization, greatly extends its reach, and positions itself to better compete with its

peers. Because of the acquisition, iGate was unable to directly contribute to this study. Building on

IDC's own models, it is estimated that iGate — a subsidiary of Capgemini — derived roughly 9% of its

revenue from the life sciences, of which 56% comes from R&D-focused engagements. Prior to the

acquisition, iGate employed more than 33,000 people worldwide, including more than 1,200 people

dedicated to its life science practice.

After a close evaluation of iGate's offerings and capabilities, IDC has positioned the company in the

Contenders category within this IDC MarketScape. Within the life science R&D strategic consulting

space, iGate has continued to build its R&D portfolio of service offerings around its traditional IT

platform and analytics solution strengths while positioning itself as an alternative to the large service

providers. IDC expects that, in combination with Capgemini, iGate's performance in future IDC

MarketScape studies will dramatically improve.

Strengths

iGate has significant experience working with life science companies across all three sections of the

industry: pharmaceutical, biotech, and medical devices. With 30% of its revenue derived from

emerging and midtier life science companies, iGate is well positioned for expected growth in markets

outside of the traditional big pharma. Capgemini's broader size and global footprint should help iGate

to more rapidly build its global presence, building on a strong North American client base and growing

European and Asia/Pacific presence. Relative to other vendors discussed in this study, iGate received

©2016 IDC #US41126416 10

high marks for solid account management and constantly working to improve its client efforts

throughout its engagements.

Challenges

With its highly diversified client base, iGate should be able to increase its influence in the industry by

leveraging its union with Capgemini (including Capgemini's differentiated strategic consulting

capabilities), growing its existing client relationships, and continuing to add new clients. With

continuing globalization of the life science industry overall, iGate along with its newly accessible global

Capgemini capabilities and resources is well positioned to use its strategic consulting capabilities to

compete with the major competitors in the space. From a service offering perspective, iGate needs to

reconcile its strategic consulting offerings with Capgemini's and put forth a unified portfolio offering and

positioning for the market.

Indegene

Established in 1998, Indegene has been serving the life science industry for the past 16 years. The

company, headquartered out of Bangalore, India, has eight delivery centers located in the United

States (three), India (three), and China (two). Although Indegene is privately held, IDC estimates that

Indegene derives 94% of its revenue from the life sciences, with 30% of that revenue coming from

R&D-focused engagements. Indegene employs more than 1,200 employees, all of whom are

dedicated specifically to the life science industry.

After a close evaluation of Indegene's offerings and capabilities, IDC has positioned the company in

the Major Players category within this IDC MarketScape. Indegene has grown its presence

significantly in the R&D strategic consulting space since its positioning as a Contender in IDC MarketScape: Worldwide Life Science R&D Strategic Consulting 2014 Vendor Assessment (IDC

Health Insights #HI246518, February 2014). The company continues to be an emerging service

provider with strengths in analytics, predictive modeling, process optimization, and regulatory

compliance support services. The company's strong technical focus, combined with aggressive

investment for growth, should allow Indegene to continue to grow its presence in the industry over the

foreseeable future.

Strengths

Although a majority of Indegene's customers are large pharmaceutical companies, Indegene has

expanded its presence across all three sections of the industry: pharmaceutical, biotech, and medical

devices. The company has further expanded its focus to include midtier life science companies,

continued to expand geographically, and has added new capabilities through both organic growth and

targeted acquisitions. Relative to other vendors discussed in this study, Indegene's strong technical

team and targeted R&D focus should continue to help differentiate the company from its competitors.

Challenges

With its growing global presence, Indegene should be able to increase its influence in the industry by

both growing its portfolio of strategic consulting offerings and focusing specific efforts toward emerging

and midtier life science companies. With its focused (and expanding) service offerings, Indegene will

also benefit by strengthening its technology-based 3rd Platform and organizational change

management strategic support capabilities. As the company grows, leadership should also consider

expanding the company's technical resources and begin to pursue more emerging industry strategic

areas of focus (e.g., outsourcing, collaboration, and patient engagement support services).

©2016 IDC #US41126416 11

Infosys

Established in 1981, Infosys has been serving the life science industry for more than 13 years. The

company, headquartered out of Bangalore, India, has 85 offices and 100 development centers around

the world. IDC estimates that Infosys derives approximately 6% of its revenue from the life sciences,

roughly 10% of which comes from R&D-focused engagements. Infosys employs more than 193,000

people worldwide, including more than 5,000 people dedicated to its life science practice.

After a close evaluation of Infosys' offerings and capabilities, IDC has positioned the company in the

Contenders category within this IDC MarketScape. Within the life science R&D strategic consulting

space, Infosys is particularly strong in delivering process optimization and R&D supply chain strategic

support services to its clients. With its strong global focus, Infosys is actively growing its strategic

consulting services to strengthen its opportunities within the industry.

Strengths

While continuing to grow its efforts with top-tier pharmaceutical companies, Infosys has developed a

broader industry footprint that appeals to companies of all sizes. In contrast to many of its peers, the

company conducts more of its efforts in Europe than in the United States. With its extensive network of

delivery centers distributed around the world, Infosys is well positioned to provide its customers with

significant flexibility in sourcing their project engagements. Relative to other vendors discussed in this

study, Infosys was recognized for the value it delivers customers relative to cost, quality of its work,

and potential to move beyond tactical support services into more strategic contributions within an

organization.

Challenges

With the strength of its global delivery infrastructure, commitment to grow its life science business, and

breadth of service offerings, Infosys is well positioned to grow its strategic consulting capabilities and

should be competitive in all RFPs that the company competes for. Infosys should continue to gain

more experience in all of its strategic consulting offerings and grow its relationships with its core

clientele. From a service offering perspective, strategic consulting services positioned for further

development by Infosys include analytics, predictive modeling, and technology-based 3rd Platform

support services.

McKinsey

Founded in 1926, McKinsey has been serving in the life science industry for more than 32 years and is

headquartered out of New York, New York. The company has more than 100 offices and operations in

more than 60 countries around the world. Although McKinsey does not report revenue by industry, IDC

estimates that the company derives roughly 5% of its revenue from the life sciences, and we further

estimate that 30% of this comes from R&D-focused engagements. McKinsey employs more than

17,000 people worldwide, including more than 1,700 consultants with life science and/or healthcare

expertise.

After a close evaluation of McKinsey's offerings and capabilities, IDC has positioned the company in

the Major Players category within this IDC MarketScape. As one of the founding management

consulting companies, IDC estimates that McKinsey generates most of its life science revenue from

top-tier life science companies, although the company also works globally with midtier biopharma

companies, nonprofit organizations, and government agencies. These capabilities and the company's

©2016 IDC #US41126416 12

strong reputation in the industry routinely position McKinsey as a strong competitor in high-level,

strategic consulting projects that the company competes for.

Strengths

McKinsey is a strategic consulting service provider to a wide variety of industries worldwide. The

company actively competes with life science companies for strategic consulting projects as it has

particular strengths in both traditional strategy consulting and operations management across the

complete industry life cycle. McKinsey has extensive experience working with life science companies

across all three sections of the industry: pharmaceutical, biotech, and medical devices. With a

presence in more than 60 countries, McKinsey has a strong footprint worldwide and the ability to help

its life science clients expand as the industry becomes increasingly global. Relative to other vendors

discussed in this study and based on feedback from multiple customer references, McKinsey received

high marks as a best-of-breed, high-quality strategic consulting service provider with thought

leadership covering the full product life cycle.

Challenges

McKinsey has historically been and continues to be a key advisor to companies worldwide. With the

expansion of strategic consulting to include more industry-specific and technology-centric efforts,

significant competition is continuing to arise from niche and IT-centric service providers within the life

science space. Through either partnerships or M&A, McKinsey should expand its strategic consulting

offerings to be able to deliver more comprehensive transformation solutions to its broad portfolio of life

science clients.

PwC

As one of the foundational players in the industry, headquartered out of New York, New York, PwC

established its pharma management consulting services practice roughly 32 years ago. Overall, the

company has offices and operations in 157 countries around the world. Although PwC does not report

revenue by industry, IDC estimates that the company derives roughly 7% of its revenue from the life

science industry, and we further estimate that 15% of this comes from R&D-focused engagements.

PwC employs more than 195,000 people worldwide, including more than 5,800 dedicated to its life

science practice.

After a close evaluation of PwC's offerings and capabilities, IDC has positioned the company in the

Leaders category within this IDC MarketScape. PwC is among the main service providers of R&D

strategic consulting and carries a legacy of strong strategic consulting services to the industry. The

company has a broad customer base, a strong global footprint, and significant success in engaging

and expanding its relationship with top-tier pharmaceutical companies. PwC is actively growing its

capabilities through an aggressive acquisition strategy and is a formidable competitor in all RFPs and

RFIs it responds to.

Strengths

PwC has extensive experience working with life science companies across all three sections of the

industry: pharmaceutical, biotech, and medical devices. More than 80% of PwC's life science

customers are large corporations with revenue over $1 billion, with a significant base of customers

spread across North America, Europe, and Asia/Pacific. Relative to other vendors discussed in this

study and based on feedback from multiple customer references, PwC continues to receive high marks

©2016 IDC #US41126416 13

for underpromising and overdelivering, bringing industry-specific knowledge (instead of templates) to

engagements, and uniquely understanding industry needs from a business perspective.

Challenges

PwC has a long and deep history of delivering strategic consulting services to the life science industry

and beyond. With deep relationships in place, PwC is well positioned to expand its work both within its

existing client base and with emerging and midtier industry leaders. With industry transformation

increasingly impacting life science companies of all sizes and types, PwC should expand its offerings

to better capture projects with emerging and midtier companies, which should allow the company to

maintain its leadership in the industry. Working from a position of deep experience in delivering a

broad portfolio of comprehensive, industry-specific strategic consulting service offerings, PwC should

look to further expand its technology and therapeutics area-centric process optimization and strategy

capabilities.

TCS

Founded in 1968 as a division of Tata Sons, TCS has been serving the life science industry for the

past 27 years. The company, headquartered out of Mumbai, India, has offices in 46 countries. IDC

estimates that TCS derives roughly 7% of its revenue from its health and life science business unit

(half of which IDC estimates comes from the life sciences), and IDC estimates that roughly 40% of this

revenue comes from R&D-focused engagements. TCS employs more than 319,000 people worldwide,

with IDC estimating more than 10,000 people specifically dedicated to its life science practice.

After a close evaluation of TCS' offerings and capabilities, IDC has positioned the company in the

Leaders category within this IDC MarketScape. Within the life science R&D strategic consulting space,

TCS brings a full spectrum of capabilities, with particular strength in technology-based 3rd Platform

support capabilities and process optimization support services. TCS' strong technical focus, success

with life science companies, and broad service offering make the company a strong partner for

companies seeking a preferred vendor to address their strategic consulting needs.

Strengths

TCS has extensive experience working with life science companies across the three major industry

sectors: pharmaceutical, biotech, and medical devices. Nearly all of TCS' life science customers are

large corporations with revenue over $1 billion, although a small percentage of the company's

customers are midtier life science companies. Most of TCS' customers reside in North America and

Europe, with a few scattered across Asia/Pacific and Latin America. The company also has a

considerable number of delivery centers located across all four of these regions. Relative to other

vendors discussed in this study and based on feedback from multiple customer references, Tata

Consultancy Services received high marks for its foundational technical strengths and its ability to

deliver more strategic consulting and support services (in addition to its core BPO and ITO

capabilities).

Challenges

As an experienced global service provider to the life science industry, TCS has historically focused its

efforts on organizations with revenue above $1 billion. As the industry continues to expand through

external collaboration, there continues to be a significant opportunity to deliver TCS' strong analytical,

process optimization, pharmacovigilance, and regulatory compliance support services beyond the

company's traditional client base. From a service offering perspective, strategic consulting services

©2016 IDC #US41126416 14

positioned for further development by TCS include expanding its predictive modeling, organizational

change management, and outsourcing/CRO strategy support services.

Wipro

Founded in 1945, Wipro has been serving the life science industry for the past 14 years. The company,

headquartered out of Bangalore, India, has offices in 57 countries. Wipro derives roughly 11% of its

revenue from its health and life science business unit (half of which IDC estimates comes from the life

sciences), of which 30% comes from R&D-focused engagements. Wipro employs more than 160,000

people worldwide, including more than 6,300 people dedicated to its life science practice.

After a close evaluation of Wipro's offerings and capabilities, IDC has positioned the company in the

Major Players category within this IDC MarketScape. Within the life science R&D strategic consulting

space, Wipro is particularly strong in delivering analytics, technology-based 3rd Platform, and process

optimization strategic support services, supplemented by a broad portfolio of solid life science R&D

BPO and ITO offerings. The company's global presence, growing portfolio of strategic support

services, aggressive growth strategy, competitive pricing, and strong customer focus have made Wipro

a strong competitor for technology-oriented, strategic consulting services in areas where the company

competes as well as a vendor that should be regularly on the short list in RFPs that the company

participates in.

Strengths

Wipro has extensive experience working with medical device companies, complemented by midlevel

experience with pharmaceutical and biotech companies as well. The vast majority of Wipro's life

science customers are large corporations with revenue over $1 billion, with a smaller contribution from

midtier life science companies. While more than half of its client base is in North America, Wipro does

have a significant client base across all regions of the world, including Europe, Asia, and Latin

America, with multiple delivery centers in each region as well. Relative to other vendors discussed in

this study and based on feedback from multiple customer references, Wipro received high marks for its

strong technical team, ability to deliver high value for the money, willingness to invest in emerging

areas, and collaborative approach to problem solving.

Challenges

As an emerging strategic consulting service provider, Wipro is well positioned for growth. As with other

vendors, Wipro will need to gain additional experience with its existing strategic consulting portfolio of

offerings as well as expand its strategic support capabilities. Wipro has a significant specific

opportunity to grow its strategic consulting services by building on its differentiated medical device

engineering expertise, leveraging its solid BPO and ITO client relationships with existing top-tier

clients, and creating offerings specifically targeted toward emerging and midtier life science

companies. From a service offering perspective, strategic consulting services positioned for further

development by Wipro include organizational change management, technology-based 3rd Platform

development, and outsourcing strategic support services.

APPENDIX

Reading an IDC MarketScape Graph

For the purposes of this analysis, IDC divided potential key measures for success into two primary

categories: capabilities and strategies.

©2016 IDC #US41126416 15

Positioning on the y-axis reflects the vendor's current capabilities and menu of services and how well

aligned the vendor is to customer needs. The capabilities category focuses on the capabilities of the

company and product today, here and now. Under this category, IDC analysts will look at how well a

vendor is building/delivering capabilities that enable it to execute its chosen strategy in the market.

Positioning on the x-axis, or strategies axis, indicates how well the vendor's future strategy aligns with

what customers will require in three to five years. The strategies category focuses on high-level

decisions and underlying assumptions about offerings, customer segments, and business and go-to-

market plans for the next three to five years.

The size of the individual vendor markers in the IDC MarketScape represents the market share of each

individual vendor within the specific market segment being assessed.

IDC MarketScape Methodology

IDC MarketScape criteria selection, weightings, and vendor scores represent well-researched IDC

judgment about the market and specific vendors. IDC analysts tailor the range of standard

characteristics by which vendors are measured through structured discussions, surveys, and

interviews with market leaders, participants, and end users. Market weightings are based on user

interviews, buyer surveys, and the input of a review board of IDC experts in each market. IDC analysts

base individual vendor scores, and ultimately vendor positions on the IDC MarketScape, on detailed

surveys and interviews with the vendors, publicly available information, and end-user experiences in

an effort to provide an accurate and consistent assessment of each vendor's characteristics, behavior,

and capability.

Market Definition

For the purposes of this study, strategic consulting is defined broadly and includes:

High-level management consulting and advisory services (including portfolio and other R&D strategy development, new business model assessments and strategies, and globalization

strategy development and implementation)

Operation and process optimization development and implementation services (including IT

framework development, outsourcing strategies, and organizational change management support)

Technology adoption and implementation strategy development (including mobile, cloud, big data, and social communication strategy development)

Market Overview

The loss of major recurring blockbuster drug revenue to patent expirations has driven the life science

industry to rapidly transform itself over the past several years. Efforts at the forefront include:

Increased focus on targeted therapeutics (niche blockbusters)

Elimination of excess capacity

A complete assessment of operations and processes across the industry life cycle in pursuit of

operational efficiency optimization and process excellence

With significant assistance from external strategic advisors, a major component of life science

company organizational change has been the shift to externalize noncore competencies to external

service providers. While much of this transformation has already been completed, companies are

©2016 IDC #US41126416 16

continuing to optimize and fine-tune their vendor relationships as they further expand the list of

activities that can be effectively performed by partners. This shift has also driven concurrent

consolidation in the service provider ecosystem as companies increasingly look to a small number of

preferred vendors to perform the bulk of their outsourced activities. From the vendor point of view, the

increased outsourcing has created new growth opportunities to offer and provide these same services

to emerging and midtier life science companies.

As part of the drive to change, life science companies have recognized that the current approach to

new drug development will be unable to deliver sufficient new revenue to replace the revenue lost to

patent expirations. While a variety of new business models are being considered and evaluated,

companies are concurrently looking to better exploit both technology innovation and best practices

from outside of the industry. These efforts are being actively supported by strategic consulting service

providers. With a focus on technology, it is clear that this paradigm shift has been long in the making.

IDC's four pillars of technology innovation — IT clouds, big data and analytics, mobile platforms and

solutions, and social and unified communications — will play a major role in industry transformation.

While contributing in different ways, each of the four pillars is expected to directly contribute to both

strategic and tactical initiatives driving organizational change and will have near-term goals,

expectations, and defined ROI. The level of technology adoption varies widely depending on the use

case, with the degree of regulatory oversight, perceived risk, and the willingness to change as key

factors impacting adoption.

Strategic consulting service providers have supported the life science industry for more than 42 years,

delivering BPO, ITO, and strategic consulting services on a regular basis. The shift to externalize

efforts as well as the move to transform supporting infrastructure has provided new opportunities for

these vendors to expand their efforts with life science companies. As a result, life science–focused

service providers are growing rapidly and taking on more responsibility for strategic, IT, and industry-

specific information management activities on behalf of their industry sponsors. While decision-making

and risk-associated activities are expected to remain as core competencies within life science

companies, commoditized, strategic, tactical, and operational activities are rapidly becoming the

domain of a limited number of preferred service provider partners.

While strategic consulting services are well established within the life science R&D and broader life

science industry, there is continuing growth of strategic consulting services based on the ongoing

transformation of the industry from a strategic, operational, and process perspective as well as the

continuing expansion of the industry from both a life-cycle perspective (i.e., closer ties with academic

and peer partners and expansion into the healthcare space) and a geographic perspective. While

initially focused on traditional business transformation, M&A, and operational management, service

providers are extending their reach into both technology and knowledge management areas, with

strong industry-specific and company-specific expertise being brought to the table. With significant

science, technology, and IT knowledge components increasingly becoming part of strategic

engagements, traditional IT service providers are gaining traction in winning strategic consulting

engagements where operational and tactical knowledge and experience is relevant. Key R&D areas

where strategic consulting is expanding include analytics (including predictive model development and

process optimization dashboards), technology adoption and implementation (including mobile, cloud,

big data, and social communication strategies), and globalization and partner strategy and operational

management strategy development and implementation.

©2016 IDC #US41126416 17

Strategies and Capabilities Criteria

Tables 1 and 2 provide key strategy and capability measures for the success of life science R&D

strategic consulting service providers.

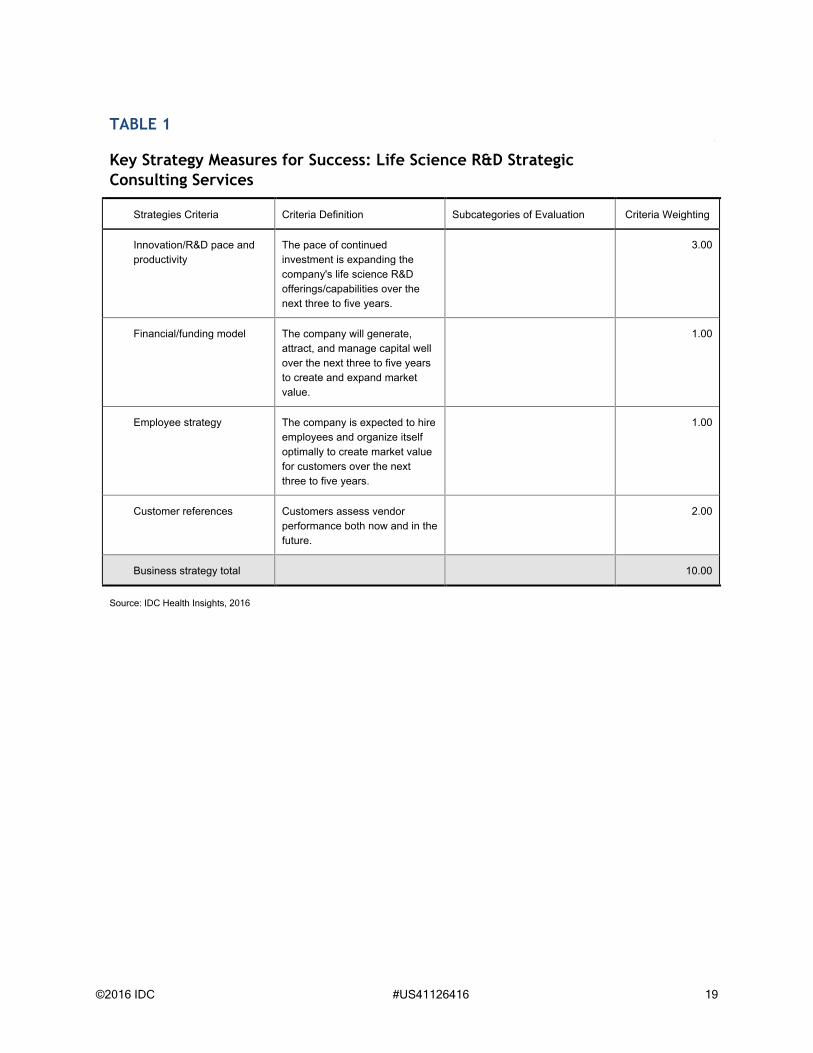

TABLE 1

Key Strategy Measures for Success: Life Science R&D Strategic Consulting Services

Strategies Criteria Criteria Definition Subcategories of Evaluation Criteria Weighting

Offering strategy The vendor's current

development of offerings will be

relevant and attractive to

customers over the next three to

five years.

Functionality or offering

road map

Current and planned offerings

are expected to match directly to

the current customer needs to

deliver maximum customer

benefit over the next three to five

years.

Breadth of offering; a range of

industry segments covered

4.00

Delivery model Current and planned offerings

will be delivered in ways that

match customer preferences for

resource allocation, cost agility,

and so forth over the next three

to five years.

Technical focus and appropriate

industry experience available to

effectively deliver services

1.00

Cost management strategy The cost structure for this

offering is competitive, yet

supports the flexibility required to

adjust to the pricing models that

customers will want over the

next three to five years.

Deployment model flexibility 1.00

Portfolio strategy The offering is developed and

delivered in ways specific to

industry-specific/company-

specific current and evolving

needs over the next three to five

years.

Breadth of general and industry-

specific strategic consulting

service offerings

3.00

Customer base The company is expected to

have a substantial customer

base over the next three to five

years.

A number of pharma customers,

a number of biotech customers,

and a number of medical device

customers

1.00

Offering strategy total 10.00

©2016 IDC #US41126416 18

TABLE 1

Key Strategy Measures for Success: Life Science R&D Strategic Consulting Services

Strategies Criteria Criteria Definition Subcategories of Evaluation Criteria Weighting

Go-to-market strategy The vendor's capabilities

maximize the connection

between offerings and

customers, including choosing to

target customer segments that

offer the greatest opportunity

over the next three to five years.

Pricing model The pricing model and the

related pricing options will be

aligned with customers'

preferences over the next three

to five years.

Pricing model and delivery

flexibility

1.00

Sales/distribution strategy The future sales/distribution

structure is aligned with the way

customers, especially those in

high-growth market segments,

want to buy over the next three

to five years.

1.00

Marketing strategy The vendor's marketing

organization is expected to be

aligned with the priority customer

segments and execute well over

the next three to five years.

4.00

Customer service strategy Service options for the vendor's

offerings will be aligned with

priority customer segments'

wants and needs over the next

three to five years.

4.00

Go-to-market strategy total 10.00

Business strategy Strategies to grow the business

are aligned with market trends

and future opportunities over the

next three to five years.

Growth strategy The company is knowledgeable

on the life science industry and

will be well informed on the

current and emerging market

needs and desires over the next

three to five years.

3.00

©2016 IDC #US41126416 19

TABLE 1

Key Strategy Measures for Success: Life Science R&D Strategic Consulting Services

Strategies Criteria Criteria Definition Subcategories of Evaluation Criteria Weighting

Innovation/R&D pace and

productivity

The pace of continued

investment is expanding the

company's life science R&D

offerings/capabilities over the

next three to five years.

3.00

Financial/funding model The company will generate,

attract, and manage capital well

over the next three to five years

to create and expand market

value.

1.00

Employee strategy The company is expected to hire

employees and organize itself

optimally to create market value

for customers over the next

three to five years.

1.00

Customer references Customers assess vendor

performance both now and in the

future.

2.00

Business strategy total 10.00

Source: IDC Health Insights, 2016

©2016 IDC #US41126416 20

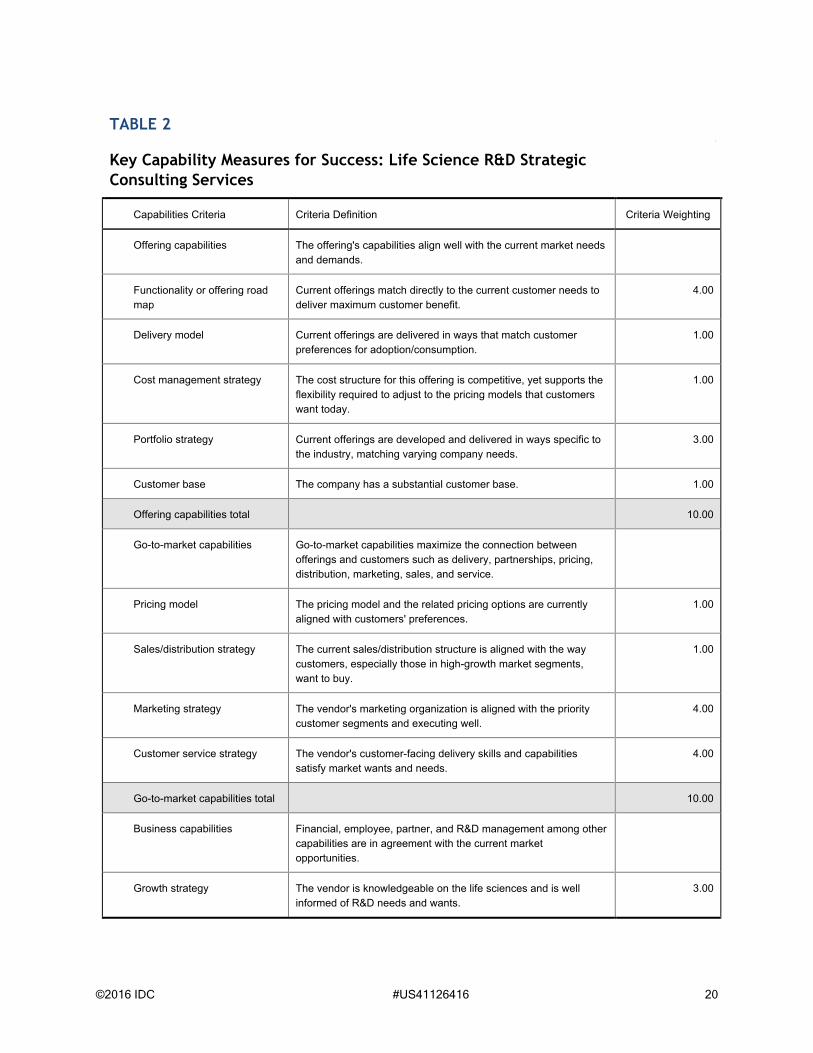

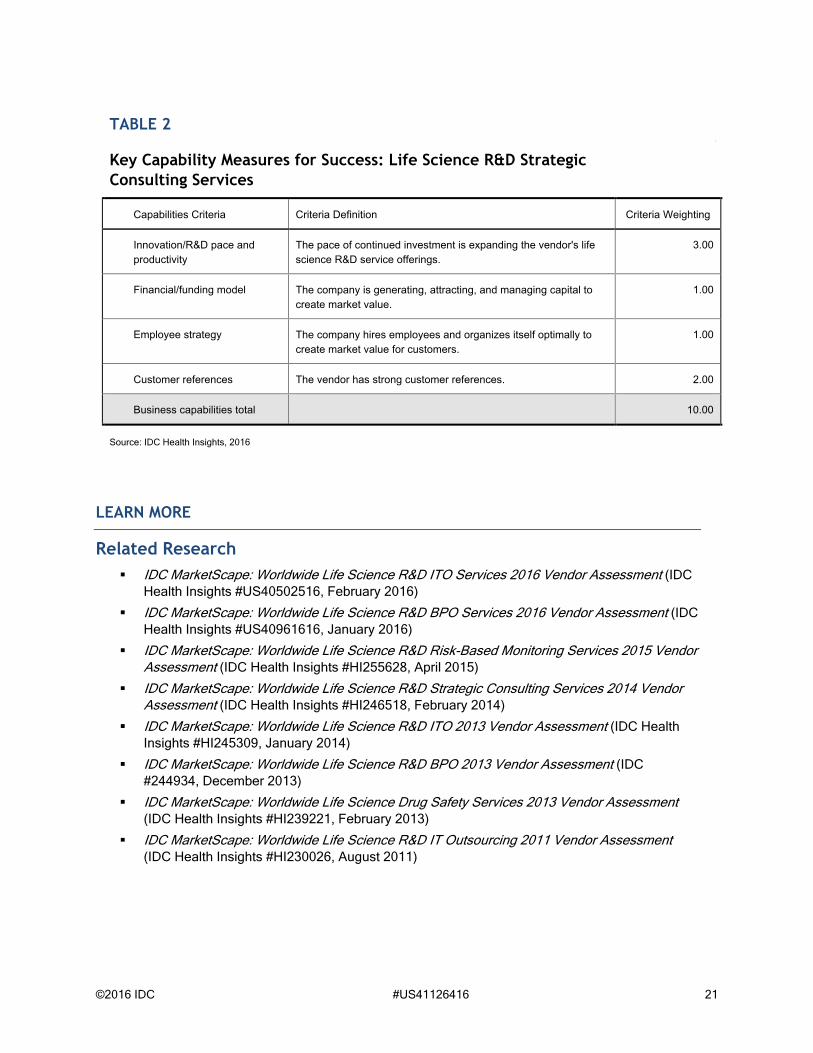

TABLE 2

Key Capability Measures for Success: Life Science R&D Strategic Consulting Services

Capabilities Criteria Criteria Definition Criteria Weighting

Offering capabilities The offering's capabilities align well with the current market needs

and demands.

Functionality or offering road

map

Current offerings match directly to the current customer needs to

deliver maximum customer benefit.

4.00

Delivery model Current offerings are delivered in ways that match customer

preferences for adoption/consumption.

1.00

Cost management strategy The cost structure for this offering is competitive, yet supports the

flexibility required to adjust to the pricing models that customers

want today.

1.00

Portfolio strategy Current offerings are developed and delivered in ways specific to

the industry, matching varying company needs.

3.00

Customer base The company has a substantial customer base. 1.00

Offering capabilities total 10.00

Go-to-market capabilities Go-to-market capabilities maximize the connection between

offerings and customers such as delivery, partnerships, pricing,

distribution, marketing, sales, and service.

Pricing model The pricing model and the related pricing options are currently

aligned with customers' preferences.

1.00

Sales/distribution strategy The current sales/distribution structure is aligned with the way

customers, especially those in high-growth market segments,

want to buy.

1.00

Marketing strategy The vendor's marketing organization is aligned with the priority

customer segments and executing well.

4.00

Customer service strategy The vendor's customer-facing delivery skills and capabilities

satisfy market wants and needs.

4.00

Go-to-market capabilities total 10.00

Business capabilities Financial, employee, partner, and R&D management among other

capabilities are in agreement with the current market

opportunities.

Growth strategy The vendor is knowledgeable on the life sciences and is well

informed of R&D needs and wants.

3.00

©2016 IDC #US41126416 21

TABLE 2

Key Capability Measures for Success: Life Science R&D Strategic Consulting Services

Capabilities Criteria Criteria Definition Criteria Weighting

Innovation/R&D pace and

productivity

The pace of continued investment is expanding the vendor's life

science R&D service offerings.

3.00

Financial/funding model The company is generating, attracting, and managing capital to

create market value.

1.00

Employee strategy The company hires employees and organizes itself optimally to

create market value for customers.

1.00

Customer references The vendor has strong customer references. 2.00

Business capabilities total 10.00

Source: IDC Health Insights, 2016

LEARN MORE

Related Research

IDC MarketScape: Worldwide Life Science R&D ITO Services 2016 Vendor Assessment (IDC Health Insights #US40502516, February 2016)

IDC MarketScape: Worldwide Life Science R&D BPO Services 2016 Vendor Assessment (IDC Health Insights #US40961616, January 2016)

IDC MarketScape: Worldwide Life Science R&D Risk-Based Monitoring Services 2015 Vendor Assessment (IDC Health Insights #HI255628, April 2015)

IDC MarketScape: Worldwide Life Science R&D Strategic Consulting Services 2014 Vendor Assessment (IDC Health Insights #HI246518, February 2014)

IDC MarketScape: Worldwide Life Science R&D ITO 2013 Vendor Assessment (IDC Health Insights #HI245309, January 2014)

IDC MarketScape: Worldwide Life Science R&D BPO 2013 Vendor Assessment (IDC #244934, December 2013)

IDC MarketScape: Worldwide Life Science Drug Safety Services 2013 Vendor Assessment(IDC Health Insights #HI239221, February 2013)

IDC MarketScape: Worldwide Life Science R&D IT Outsourcing 2011 Vendor Assessment(IDC Health Insights #HI230026, August 2011)

©2016 IDC #US41126416 22

Synopsis

This IDC study is the third of a three-part life science R&D IDC MarketScape series focused on IT

outsourcing. With a specific focus on strategic consulting in the life science R&D space, this study

seeks to compare major service providers with each other based on criteria that should be important to

life science companies when considering the selection of a strategic consulting partner to help provide

guidance for strategic, operational, and tactical transformation issues within the R&D space.

Alan Louie, research director of IDC Health Insights' Clinical Development, Strategy and Technology

research, noted, "Strategic consulting in the life sciences is more important than ever as industry

transformation moves forward. Beyond smoothing transitions and optimizing operational and business

performance, companies are actively breaking new ground and extending their world view. Partner

ecosystems are increasingly capable of delivering the complete process life cycle and have become a

critical component of life science corporate strategies for success. The selection of an optimal partner

ecosystem is key to developing and executing these increasingly externalized complex business

strategies. IDC expects that the dependence on external service providers will continue to grow as

organizations seek to navigate through increasingly complex global, regulatory, and operational life

science ecosystems. Leading vendors as preferred partners that understand their sponsor's business

almost as well as their sponsors and have the capacity to deliver superior services will be key to

helping their clients succeed, both now and in the future."

About IDC

International Data Corporation (IDC) is the premier global provider of market intelligence, advisory

services, and events for the information technology, telecommunications and consumer technology

markets. IDC helps IT professionals, business executives, and the investment community make fact-

based decisions on technology purchases and business strategy. More than 1,100 IDC analysts

provide global, regional, and local expertise on technology and industry opportunities and trends in

over 110 countries worldwide. For 50 years, IDC has provided strategic insights to help our clients

achieve their key business objectives. IDC is a subsidiary of IDG, the world's leading technology

media, research, and events company.

Global Headquarters

5 Speen Street

Framingham, MA 01701

USA

508.872.8200

Twitter: @IDC

idc-community.com

www.idc.com

Copyright and Trademark Notice

This IDC research document was published as part of an IDC continuous intelligence service, providing written

research, analyst interactions, telebriefings, and conferences. Visit www.idc.com to learn more about IDC

subscription and consulting services. To view a list of IDC offices worldwide, visit www.idc.com/offices. Please

contact the IDC Hotline at 800.343.4952, ext. 7988 (or +1.508.988.7988) or [email protected] for information on

applying the price of this document toward the purchase of an IDC service or for information on additional copies

or Web rights. IDC and IDC MarketScape are trademarks of International Data Group, Inc.

Copyright 2016 IDC. Reproduction is forbidden unless authorized. All rights reserved.