stock market special report by epic research 31st july 2014

DESCRIPTION

Epic Research provide specialized nifty future tips to nifty futures intraday traders in which we give nifty levels, nifty calls along with bank nifty tips. Call 07316642300TRANSCRIPT

DAILY REPORT

31st JULY 2014

YOUR MINTVISORY Call us at +91-731-6642300

Global markets at a glance

Asian equities were mixed on Thursday following ro-bust US economic data and as investors braced for Ar-gentina to default on its debt for the second time in twelve years. Shanghai Composite declined 3.50pts to 2,177.74 while Hang Seng rose 5.20pts to 24,737.41 and Nikkei 225 Average advanced 72.17pts to 15,718.40,. STI rose 17.1pts to 0.51% to 3,370.76.

European shares closed lower on Wednesday, as strong U.S. growth failed to offset some weak earnings reports and concern the conflict between Russia and Ukraine will escalate. The FTSEurofirst 300 index closed 0.5% lower at 1,366.52pts after a choppy session.

Wall Street Update

The S&P 500 and Nasdaq ended higher on Wednesday after the Federal Reserve gave a rosier assessment of the US economy while reaffirming that it is in no hurry to raise interest rates. The US central bank also, as ex-pected, reduced its monthly asset purchases to USD 25 billion from USD 35 billion.

The Dow Jones industrial average fell 31.75 points, or 0.19 %, to 16,880.36, the S&P 500 gained 0.12 points, or 0.01 %, to 1,970.07, and Nasdaq Composite added 20.20 points, or 0.45 %, to 4,462.90.

Previous day Roundup

Equity benchmarks bounced back after two-day fall. The 30-share BSE Sensex jumped 96.19 points to close at 26087.42 while the 50-share NSE Nifty rallied 42.70 points to 7791.40 ahead of expiry of July derivative contracts. About 1403 shares have advanced, 1488 shares declined, and 121 shares are unchanged.

Equity benchmarks rebounded in last couple of hours of trade on Wednesday after falling since last Friday. The market saw the third highest turnover at Rs 6.43 lakh crore ahead of expiry of July derivative contracts on Thursday.

Index stats

The Market was very volatile in last session. The sarto-rial indices performed as follow; Consumer Durables [down pts], Capital Goods [down 725.96pts], PSU [up 45.42pts], FMCG [up 24.23pts], Auto [up 99.54pts], Healthcare [up 164.55pts], IT [down 24.28Pts], Metals [up 57.32pts], TECK [up 23.40pts], Oil& Gas [up 44.96pts], Power [up 13.46pts], Realty [up 15.30pts].

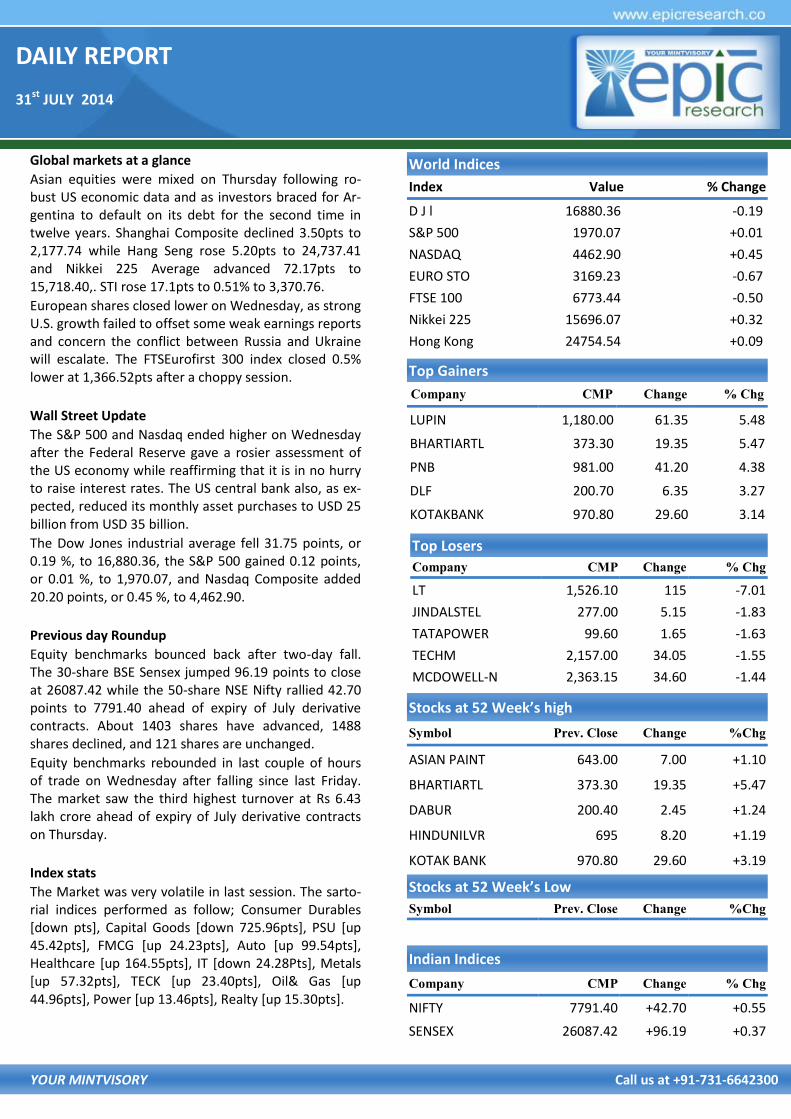

World Indices

Index Value % Change

D J l 16880.36 -0.19

S&P 500 1970.07 +0.01

NASDAQ 4462.90 +0.45

EURO STO 3169.23 -0.67

FTSE 100 6773.44 -0.50

Nikkei 225 15696.07 +0.32

Hong Kong 24754.54 +0.09

Top Gainers

Company CMP Change % Chg

LUPIN 1,180.00 61.35 5.48

BHARTIARTL 373.30 19.35 5.47

PNB 981.00 41.20 4.38

DLF 200.70 6.35 3.27

KOTAKBANK 970.80 29.60 3.14

Top Losers

Company CMP Change % Chg

LT 1,526.10 115 -7.01

JINDALSTEL 277.00 5.15 -1.83

TATAPOWER 99.60 1.65 -1.63

TECHM 2,157.00 34.05 -1.55

MCDOWELL-N 2,363.15 34.60 -1.44

Stocks at 52 Week’s high

Symbol Prev. Close Change %Chg

ASIAN PAINT 643.00 7.00 +1.10

BHARTIARTL 373.30 19.35 +5.47

DABUR 200.40 2.45 +1.24

HINDUNILVR 695 8.20 +1.19

KOTAK BANK 970.80 29.60 +3.19

Indian Indices

Company CMP Change % Chg

NIFTY 7791.40 +42.70 +0.55

SENSEX 26087.42 +96.19 +0.37

Stocks at 52 Week’s Low

Symbol Prev. Close Change %Chg

DAILY REPORT

31st JULY 2014

YOUR MINTVISORY Call us at +91-731-6642300

STOCK RECOMMENDATIONS [FUTURE]

1. TATAMOTOR DVR FUTURE

TATA MOTOR DVR FUTURE is looking strong on charts, long build up has been seen, we may see more upside, if it sus-tains above 300 levels. We advise buying around 296-300 levels with strict stop loss of 290 for the targets of 305-310.

2. HAVELLS FUTURE

HAVELLS FUTURE is looking weak on charts, short build up has been seen, we may see more downside, if it sustains below 1200 levels. We advise selling around 1180-1190 lev-els with strict stop loss of 1220 for the targets of 1150-1120.

EQUITY CASH & FUTURE

STOCK RECOMMENDATION [CASH]

1. INDOCO REMEDIES

INDOCO REMEDIES is looking strong on charts. We advise buying around 210-215 level with strict stop loss 200 for the targets of 225-245

MACRO NEWS

Results Today: ICICI Bank, HCL Tech, Maruti Suzuki, DLF, Tech Mahindra, NTPC, AbanOffshore, HCC, CARE, Castrol India, Cholamandalam Finance, Deepak Fertilizers, HDIL, JM Financial, Mahindra Life, Pantaloons, SPARC, Syndicate Bank, Bajaj Electricals, Greaves Cotton.

Consolidated net profit grew 15.3 % sequentially (up 60.9 % year-on-year) to Rs 1,108.5 crore in the first quarter of current financial year 2014-15 on account of strong op-erational performance and lower forex loss but impacted by Africa operations, tax expenses and exceptional loss.

Lupin sharply beat street expectations on every parame-ter with the net profit growing 56 % year-on-year at Rs 625 crore in the quarter ended June 2014 on account of hefty growth in US and Indian operations but impacted by higher tax expenses. Net profit in the year-ago period was Rs 401 crore.

Cadila Healthcare has reported a 23.2 % growth in con-solidated net profit at Rs 240.2 crore in April-June quarter driven by strong sales growth in the US. Profit in the year-ago period was Rs 195 crore.

Finance Minister to meet CEOs of PSU banks today on fi-nancial inclusion.

DAILY REPORT

31st JULY 2014

YOUR MINTVISORY Call us at +91-731-6642300

FUTURE & OPTION

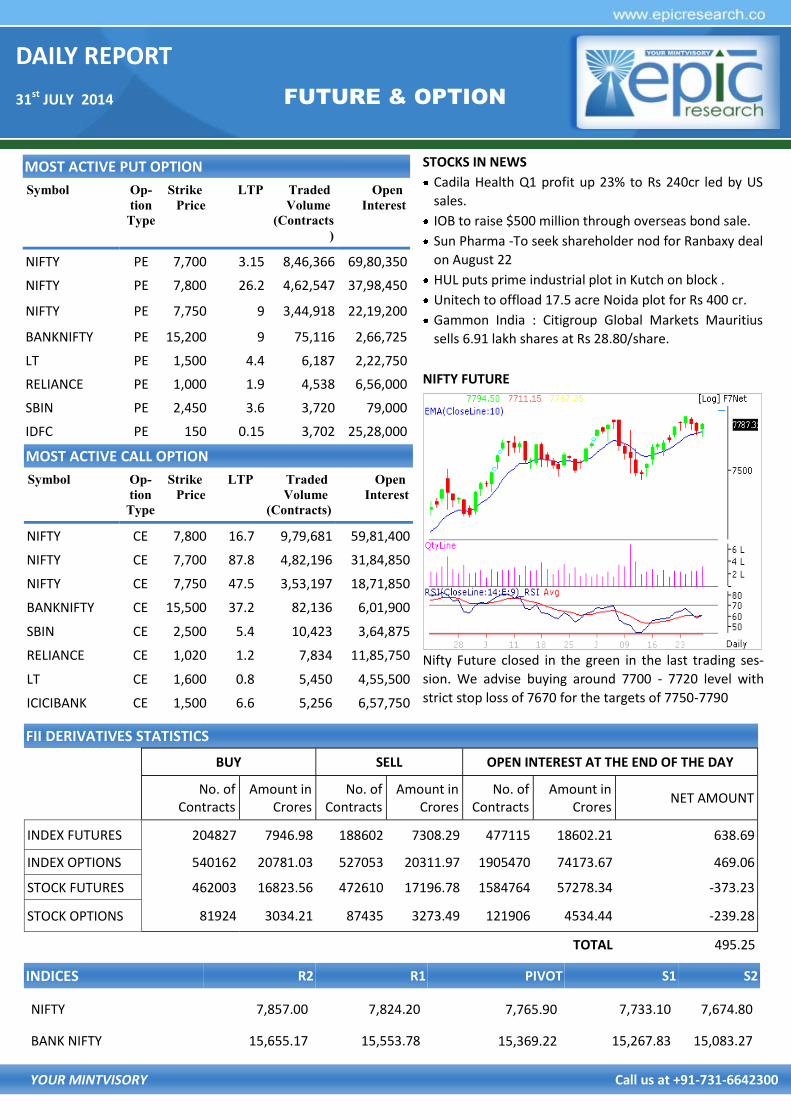

MOST ACTIVE PUT OPTION

Symbol Op-

tion

Type

Strike

Price

LTP Traded

Volume

(Contracts

)

Open

Interest

NIFTY PE 7,700 3.15 8,46,366 69,80,350

NIFTY PE 7,800 26.2 4,62,547 37,98,450

NIFTY PE 7,750 9 3,44,918 22,19,200

BANKNIFTY PE 15,200 9 75,116 2,66,725

LT PE 1,500 4.4 6,187 2,22,750

RELIANCE PE 1,000 1.9 4,538 6,56,000

SBIN PE 2,450 3.6 3,720 79,000

IDFC PE 150 0.15 3,702 25,28,000

MOST ACTIVE CALL OPTION

Symbol Op-

tion

Type

Strike

Price

LTP Traded

Volume

(Contracts)

Open

Interest

NIFTY CE 7,800 16.7 9,79,681 59,81,400

NIFTY CE 7,700 87.8 4,82,196 31,84,850

NIFTY CE 7,750 47.5 3,53,197 18,71,850

BANKNIFTY CE 15,500 37.2 82,136 6,01,900

SBIN CE 2,500 5.4 10,423 3,64,875

RELIANCE CE 1,020 1.2 7,834 11,85,750

LT CE 1,600 0.8 5,450 4,55,500

ICICIBANK CE 1,500 6.6 5,256 6,57,750

FII DERIVATIVES STATISTICS

BUY OPEN INTEREST AT THE END OF THE DAY SELL

No. of

Contracts Amount in

Crores No. of

Contracts Amount in

Crores No. of

Contracts Amount in

Crores NET AMOUNT

INDEX FUTURES 204827 7946.98 188602 7308.29 477115 18602.21 638.69

INDEX OPTIONS 540162 20781.03 527053 20311.97 1905470 74173.67 469.06

STOCK FUTURES 462003 16823.56 472610 17196.78 1584764 57278.34 -373.23

STOCK OPTIONS 81924 3034.21 87435 3273.49 121906 4534.44 -239.28

TOTAL 495.25

INDICES R2 R1 PIVOT S1 S2

NIFTY 7,857.00 7,824.20 7,765.90 7,733.10 7,674.80

BANK NIFTY 15,655.17 15,553.78 15,369.22 15,267.83 15,083.27

STOCKS IN NEWS

Cadila Health Q1 profit up 23% to Rs 240cr led by US

sales.

IOB to raise $500 million through overseas bond sale.

Sun Pharma -To seek shareholder nod for Ranbaxy deal

on August 22

HUL puts prime industrial plot in Kutch on block .

Unitech to offload 17.5 acre Noida plot for Rs 400 cr.

Gammon India : Citigroup Global Markets Mauritius

sells 6.91 lakh shares at Rs 28.80/share.

NIFTY FUTURE

Nifty Future closed in the green in the last trading ses-

sion. We advise buying around 7700 - 7720 level with

strict stop loss of 7670 for the targets of 7750-7790

DAILY REPORT

31st JULY 2014

YOUR MINTVISORY Call us at +91-731-6642300

COMMODITY MCX

RECOMMENDATIONS

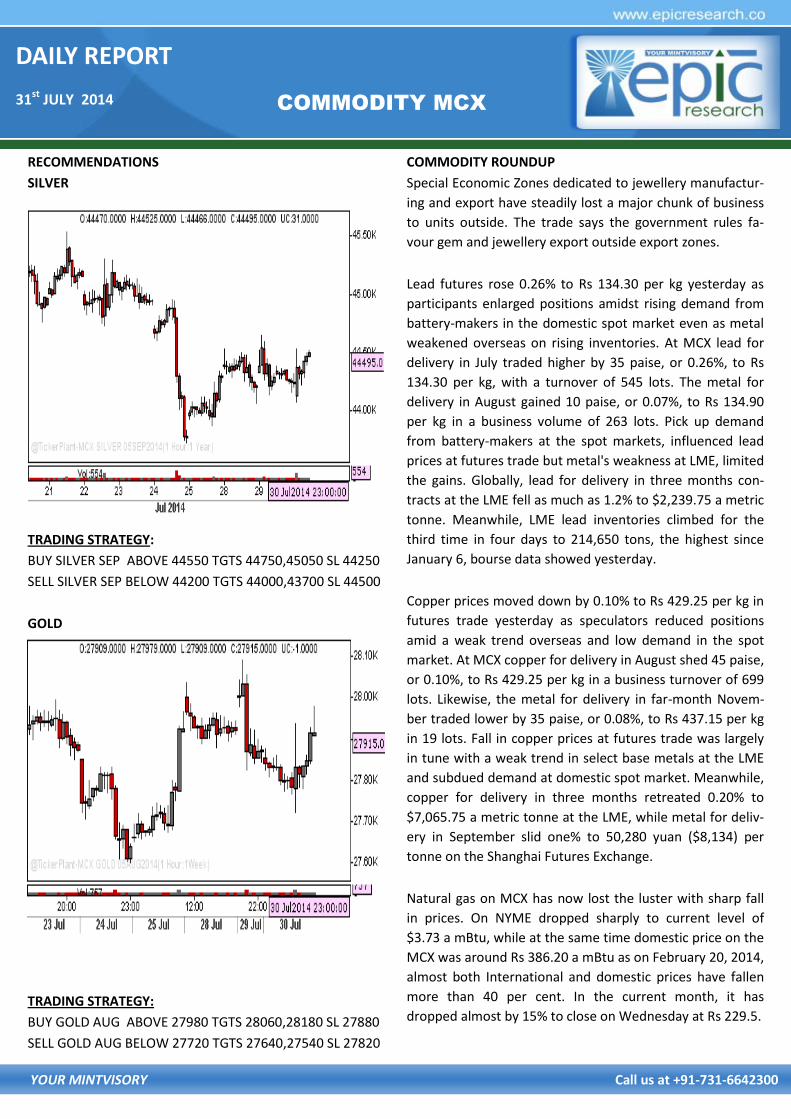

SILVER

TRADING STRATEGY:

BUY SILVER SEP ABOVE 44550 TGTS 44750,45050 SL 44250

SELL SILVER SEP BELOW 44200 TGTS 44000,43700 SL 44500

GOLD

TRADING STRATEGY:

BUY GOLD AUG ABOVE 27980 TGTS 28060,28180 SL 27880

SELL GOLD AUG BELOW 27720 TGTS 27640,27540 SL 27820

COMMODITY ROUNDUP

Special Economic Zones dedicated to jewellery manufactur-

ing and export have steadily lost a major chunk of business

to units outside. The trade says the government rules fa-

vour gem and jewellery export outside export zones.

Lead futures rose 0.26% to Rs 134.30 per kg yesterday as

participants enlarged positions amidst rising demand from

battery-makers in the domestic spot market even as metal

weakened overseas on rising inventories. At MCX lead for

delivery in July traded higher by 35 paise, or 0.26%, to Rs

134.30 per kg, with a turnover of 545 lots. The metal for

delivery in August gained 10 paise, or 0.07%, to Rs 134.90

per kg in a business volume of 263 lots. Pick up demand

from battery-makers at the spot markets, influenced lead

prices at futures trade but metal's weakness at LME, limited

the gains. Globally, lead for delivery in three months con-

tracts at the LME fell as much as 1.2% to $2,239.75 a metric

tonne. Meanwhile, LME lead inventories climbed for the

third time in four days to 214,650 tons, the highest since

January 6, bourse data showed yesterday.

Copper prices moved down by 0.10% to Rs 429.25 per kg in

futures trade yesterday as speculators reduced positions

amid a weak trend overseas and low demand in the spot

market. At MCX copper for delivery in August shed 45 paise,

or 0.10%, to Rs 429.25 per kg in a business turnover of 699

lots. Likewise, the metal for delivery in far-month Novem-

ber traded lower by 35 paise, or 0.08%, to Rs 437.15 per kg

in 19 lots. Fall in copper prices at futures trade was largely

in tune with a weak trend in select base metals at the LME

and subdued demand at domestic spot market. Meanwhile,

copper for delivery in three months retreated 0.20% to

$7,065.75 a metric tonne at the LME, while metal for deliv-

ery in September slid one% to 50,280 yuan ($8,134) per

tonne on the Shanghai Futures Exchange.

Natural gas on MCX has now lost the luster with sharp fall

in prices. On NYME dropped sharply to current level of

$3.73 a mBtu, while at the same time domestic price on the

MCX was around Rs 386.20 a mBtu as on February 20, 2014,

almost both International and domestic prices have fallen

more than 40 per cent. In the current month, it has

dropped almost by 15% to close on Wednesday at Rs 229.5.

DAILY REPORT

31st JULY 2014

YOUR MINTVISORY Call us at +91-731-6642300

RECOMMENDATIONS

DHANIYA

BUY DHANIYA AUG ABOVE 11985 TGTS 12015,12065 SL

11935

SELL DHANIYA AUG BELOW 11930 TGTS 11900,11850 SL

11980

GUARSEED

BUY GUARSEED AUG BELOW 5250 TGTS 5280,5330 SL 5200

SELL GUARSEED AUG BELOW 5190 TGTS 5160,5110 SL 5240

NCDEX

NCDEX INDICES

Index Value % Change

Castor Seed 4232 +1.80

Chana 2871 -0.35

Coriander 11962 +0.66

Cotton Seed Oilcake 1665 -0.54

Guarseed 5205 -3.97

Jeera 11265 -1.40

Mustard seed 3599 +0.45

Soy Bean 3632 -0.74

Sugar M Grade 3007 -1.74

Turmeric 6476 +0.90

NCDEX ROUNDUP

Cardamom prices rose 1.06 per cent to Rs 895 per kg in fu-

tures trade yesterday as traders enlarged commitments,

supported by a pick-up in export and domestic demand. At

the MCX, cardamom for delivery in September rose by Rs

9.40, or 1.06 per cent, to Rs 895 per kg, with a business

turnover of 64 lots. The August contract edged up by Rs

8.50, or 0.92 per cent, to Rs 925.20 per kg in 319 lots. Apart

from rising export and domestic demand, tight stocks in the

spot markets following restricted arrivals from growing re-

gions influenced cardamom prices at futures trade here.

Crude palm oil prices marginally up by Rs 1.30 to Rs 522.50

per 10 kg in futures trade yesterday as speculators created

fresh positions on the back of rising spot demand. On the

MCX, crude palm oil for August delivery rose by Rs 1.30, or

0.24%, to Rs 522.50 per kg, with a trading volume of 39 lots.

Similarly, the oil for delivery in July moved up marginally by

0.80 paise, or 0.14%, to Rs 540 per 10 kg, with a business

turnover of 116 lots. Fresh positions built-up by speculators

driven by rising spot demand, mainly led to the rise in crude

palm oil prices at futures market.

Following a steep rise till the third week of July, prices of

vegetables have moderated in the past 10 days due to re-

sumption of monsoon rains, which has brightened the pros-

pects of a recovery in production.

DAILY REPORT

31st JULY 2014

YOUR MINTVISORY Call us at +91-731-6642300

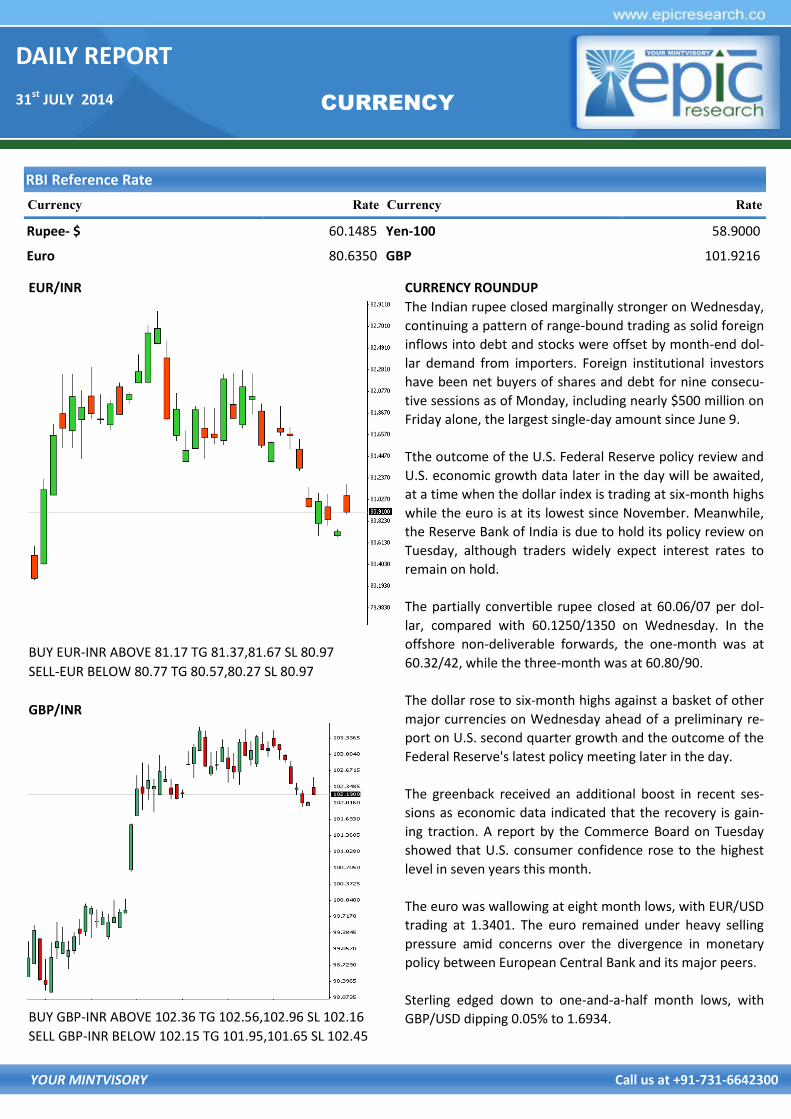

EUR/INR

BUY EUR-INR ABOVE 81.17 TG 81.37,81.67 SL 80.97

SELL-EUR BELOW 80.77 TG 80.57,80.27 SL 80.97

GBP/INR

BUY GBP-INR ABOVE 102.36 TG 102.56,102.96 SL 102.16

SELL GBP-INR BELOW 102.15 TG 101.95,101.65 SL 102.45

CURRENCY ROUNDUP

The Indian rupee closed marginally stronger on Wednesday,

continuing a pattern of range-bound trading as solid foreign

inflows into debt and stocks were offset by month-end dol-

lar demand from importers. Foreign institutional investors

have been net buyers of shares and debt for nine consecu-

tive sessions as of Monday, including nearly $500 million on

Friday alone, the largest single-day amount since June 9.

Tthe outcome of the U.S. Federal Reserve policy review and

U.S. economic growth data later in the day will be awaited,

at a time when the dollar index is trading at six-month highs

while the euro is at its lowest since November. Meanwhile,

the Reserve Bank of India is due to hold its policy review on

Tuesday, although traders widely expect interest rates to

remain on hold.

The partially convertible rupee closed at 60.06/07 per dol-

lar, compared with 60.1250/1350 on Wednesday. In the

offshore non-deliverable forwards, the one-month was at

60.32/42, while the three-month was at 60.80/90.

The dollar rose to six-month highs against a basket of other

major currencies on Wednesday ahead of a preliminary re-

port on U.S. second quarter growth and the outcome of the

Federal Reserve's latest policy meeting later in the day.

The greenback received an additional boost in recent ses-

sions as economic data indicated that the recovery is gain-

ing traction. A report by the Commerce Board on Tuesday

showed that U.S. consumer confidence rose to the highest

level in seven years this month.

The euro was wallowing at eight month lows, with EUR/USD

trading at 1.3401. The euro remained under heavy selling

pressure amid concerns over the divergence in monetary

policy between European Central Bank and its major peers.

Sterling edged down to one-and-a-half month lows, with

GBP/USD dipping 0.05% to 1.6934.

CURRENCY

RBI Reference Rate

Currency Rate Currency Rate

Rupee- $ 60.1485 Yen-100 58.9000

Euro 80.6350 GBP 101.9216

DAILY REPORT

31st JULY 2014

YOUR MINTVISORY Call us at +91-731-6642300

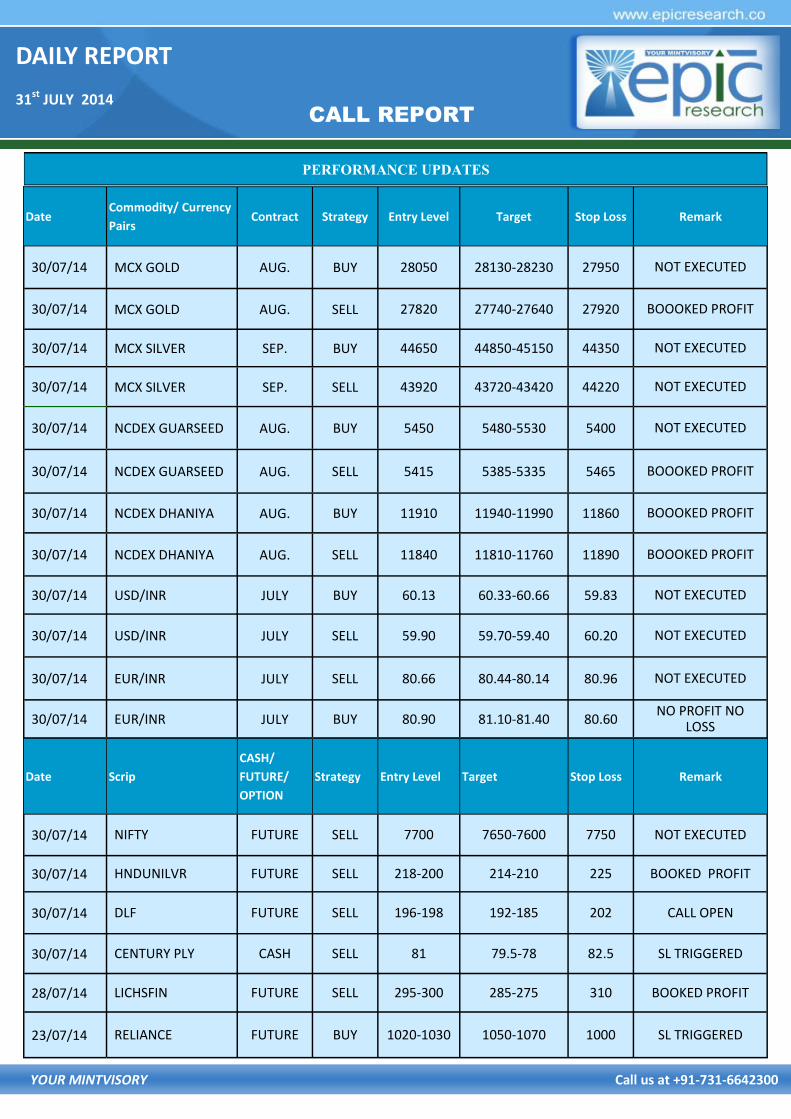

CALL REPORT

PERFORMANCE UPDATES

Date Commodity/ Currency

Pairs Contract Strategy Entry Level Target Stop Loss Remark

30/07/14 MCX GOLD AUG. BUY 28050 28130-28230 27950 NOT EXECUTED

30/07/14 MCX GOLD AUG. SELL 27820 27740-27640 27920 BOOOKED PROFIT

30/07/14 MCX SILVER SEP. BUY 44650 44850-45150 44350 NOT EXECUTED

30/07/14 MCX SILVER SEP. SELL 43920 43720-43420 44220 NOT EXECUTED

30/07/14 NCDEX GUARSEED AUG. BUY 5450 5480-5530 5400 NOT EXECUTED

30/07/14 NCDEX GUARSEED AUG. SELL 5415 5385-5335 5465 BOOOKED PROFIT

30/07/14 NCDEX DHANIYA AUG. BUY 11910 11940-11990 11860 BOOOKED PROFIT

30/07/14 NCDEX DHANIYA AUG. SELL 11840 11810-11760 11890 BOOOKED PROFIT

30/07/14 USD/INR JULY BUY 60.13 60.33-60.66 59.83 NOT EXECUTED

30/07/14 USD/INR JULY SELL 59.90 59.70-59.40 60.20 NOT EXECUTED

30/07/14 EUR/INR JULY SELL 80.66 80.44-80.14 80.96 NOT EXECUTED

30/07/14 EUR/INR JULY BUY 80.90 81.10-81.40 80.60 NO PROFIT NO

LOSS

Date Scrip

CASH/

FUTURE/

OPTION

Strategy Entry Level Target Stop Loss Remark

30/07/14 NIFTY FUTURE SELL 7700 7650-7600 7750 NOT EXECUTED

30/07/14 HNDUNILVR FUTURE SELL 218-200 214-210 225 BOOKED PROFIT

30/07/14 DLF FUTURE SELL 196-198 192-185 202 CALL OPEN

30/07/14 CENTURY PLY CASH SELL 81 79.5-78 82.5 SL TRIGGERED

28/07/14 LICHSFIN FUTURE SELL 295-300 285-275 310 BOOKED PROFIT

23/07/14 RELIANCE FUTURE BUY 1020-1030 1050-1070 1000 SL TRIGGERED

DAILY REPORT

31st JULY 2014

YOUR MINTVISORY Call us at +91-731-6642300

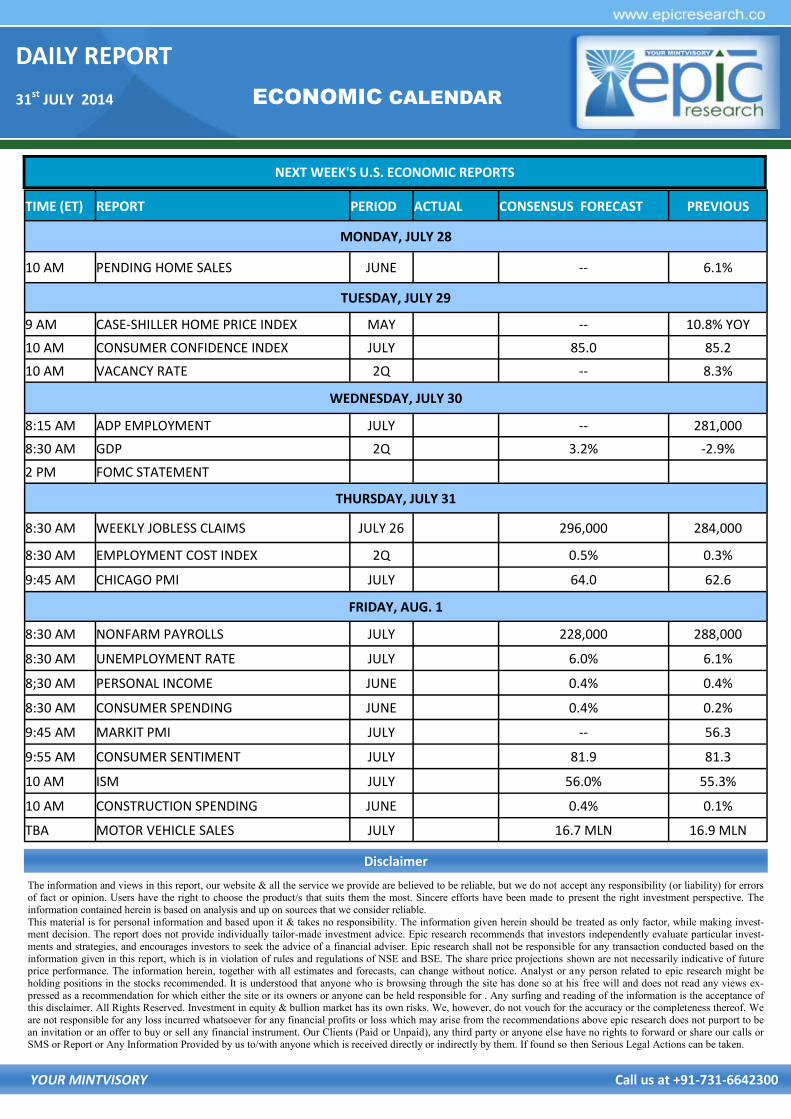

NEXT WEEK'S U.S. ECONOMIC REPORTS

ECONOMIC CALENDAR

The information and views in this report, our website & all the service we provide are believed to be reliable, but we do not accept any responsibility (or liability) for errors of fact or opinion. Users have the right to choose the product/s that suits them the most. Sincere efforts have been made to present the right investment perspective. The

information contained herein is based on analysis and up on sources that we consider reliable.

This material is for personal information and based upon it & takes no responsibility. The information given herein should be treated as only factor, while making invest-ment decision. The report does not provide individually tailor-made investment advice. Epic research recommends that investors independently evaluate particular invest-

ments and strategies, and encourages investors to seek the advice of a financial adviser. Epic research shall not be responsible for any transaction conducted based on the

information given in this report, which is in violation of rules and regulations of NSE and BSE. The share price projections shown are not necessarily indicative of future price performance. The information herein, together with all estimates and forecasts, can change without notice. Analyst or any person related to epic research might be

holding positions in the stocks recommended. It is understood that anyone who is browsing through the site has done so at his free will and does not read any views ex-

pressed as a recommendation for which either the site or its owners or anyone can be held responsible for . Any surfing and reading of the information is the acceptance of this disclaimer. All Rights Reserved. Investment in equity & bullion market has its own risks. We, however, do not vouch for the accuracy or the completeness thereof. We

are not responsible for any loss incurred whatsoever for any financial profits or loss which may arise from the recommendations above epic research does not purport to be

an invitation or an offer to buy or sell any financial instrument. Our Clients (Paid or Unpaid), any third party or anyone else have no rights to forward or share our calls or SMS or Report or Any Information Provided by us to/with anyone which is received directly or indirectly by them. If found so then Serious Legal Actions can be taken.

Disclaimer

TIME (ET) REPORT PERIOD ACTUAL CONSENSUS FORECAST PREVIOUS

MONDAY, JULY 28

10 AM PENDING HOME SALES JUNE -- 6.1%

TUESDAY, JULY 29

9 AM CASE-SHILLER HOME PRICE INDEX MAY -- 10.8% YOY

10 AM CONSUMER CONFIDENCE INDEX JULY 85.0 85.2

10 AM VACANCY RATE 2Q -- 8.3%

WEDNESDAY, JULY 30

8:15 AM ADP EMPLOYMENT JULY -- 281,000

8:30 AM GDP 2Q 3.2% -2.9%

2 PM FOMC STATEMENT

THURSDAY, JULY 31

8:30 AM WEEKLY JOBLESS CLAIMS JULY 26 296,000 284,000

8:30 AM EMPLOYMENT COST INDEX 2Q 0.5% 0.3%

9:45 AM CHICAGO PMI JULY 64.0 62.6

FRIDAY, AUG. 1

8:30 AM NONFARM PAYROLLS JULY 228,000 288,000

8:30 AM UNEMPLOYMENT RATE JULY 6.0% 6.1%

8;30 AM PERSONAL INCOME JUNE 0.4% 0.4%

8:30 AM CONSUMER SPENDING JUNE 0.4% 0.2%

9:45 AM MARKIT PMI JULY -- 56.3

9:55 AM CONSUMER SENTIMENT JULY 81.9 81.3

10 AM ISM JULY 56.0% 55.3%

10 AM CONSTRUCTION SPENDING JUNE 0.4% 0.1%

TBA MOTOR VEHICLE SALES JULY 16.7 MLN 16.9 MLN