real estate market overview -...

TRANSCRIPT

Accelerating success.

Doha, Qatar

REAL ESTATE MARKET OVERVIEW

Q2 2013

2 | Colliers International | Accelerating Success | www.colliers.com

OVERVIEW REPORT | DOHA | REAL ESTATE | SECOND QUARTER | 2013 | INTRODUCTION

Introduction Qatar has become one of the most vibrant economy in the Middle East,

on the back of its hydrocarbon reserves. The World Economic Forum’s

Global Competitiveness Report for 2011-2012, ranked Qatar at No. 14,

on the list of the world’s fastest growing economies, overtaking other

countries in the region including United Arab Emirates (UAE), Bahrain

and Kuwait.

High GDP growth rates, the expected influx of expatriate population,

together with government efforts to diversify the economy, are the

primary drivers of growth in the real estate sector.

Qatar’s hosting of the 2022 World Cup is a further stimulus towards the

country’s infrastructure and transportation networks, creating more

value towards sustainable real estate assets.

A brief synopsis of Doha’s residential, office and retail markets are as

presented below:

• Residential Sector

- Currently an undersupplied market, although depressed consumer

confidence post the global economic downturn have influenced a

downward trend in prices

- An influx of population, supported by economic growth and

employment opportunities continue to remain the key drivers for

residential demand

- Quality units, in terms of build quality, finishes and facilities are

performing significantly better than average units across the

market and have seen early signs of recovery

• Office Sector

- Currently an oversupplied market

- After continuous price declines since 2008, a stabilisation of

rentals, especially within primary grade commercial space has

been observed during 2011- 2012, mainly due to an increase in

market confidence and improved economic opportunities

- There has been notable tenant movement towards central areas

such as West Bay, representing a flight to quality, as rentals have

become more affordable

• Retail Sector

- An undersupplied market, which is likely to move to an oversupply

situation by 2014, provided construction timelines are met

- Going forward, the oversupply will apply potential downward

pressure on rental rates and may result in an increase in vacancy

rates across shopping malls. As an outcome of these two

scenarios, secondary/ less leading malls are likely to reposition

themselves with more tenant favourable terms such as rent free

periods, capital contribution and other softer deals in order to

encourage and/ retain existing tenants

Colliers International Doha Real Estate Overview provides a brief

snapshot of the key factors impacting the Qatar real estate market

and the future outlook of the sectors.

For further information please contact:

Mansoor Ahmed MAS, MSc

Director | Development Solutions

Healthcare | Education | PPP

P.O. Box 71591 | Dubai | UAE

Main: +971 4 453 7400

Mobile: +971 55 899 6091

Duncan Gray BSc (Hons) MRICS MRTPI

Director and Country Manager Qatar

P.O. Box 71591 | Dubai | UAE

Main: +971 4 453 7400

Mobile: +974 3 314 2160 | +971 55 720 0707

482 offices in

62 countries on

6 continents

United States: 140

Canada: 42

Latin America: 20

Asia Pacific: 195

EMEA: 85

• $2.0 billion in revenue

• More than 13,500 employees

• 5,100 brokers

• $71 billion in transaction volume across more than

78,000 sale and lease transactions

• 1.1 billion square feet under management

SERVICES OFFERED BY COLLIERS INTERNATIONAL

• Strategic & Business Planning

• Economic Impact Studies

• Market & Competitive Studies

• Highest & Best Use (HBU) Studies

• Market & Financial Feasibility Studies

• Financial Modelling

• Mergers & Acquisitions Assistance

• Buy side Advisory/Sell side Advisory

• Sale and Leaseback’ Advisory

• Public Private Partnership (PPP) & Privatisation

• Operator Search & Selection and Contract Negotiation

• Land, Property and Business Valuation

• Asset & Performance Management

• Site Selection & Land / Property Acquisition

• Performance Management and Industry Benchmark

Surveys

3 | Colliers International | Accelerating Success | www.colliers.com

2. Residential Sector Overview Exhibit 1: Distribution of Existing Housing Units in

Doha – Qatari Nationals

2.1 SECTOR DEFINITION

Doha’s residential real estate market is represented by an acute housing shortage. This undersupply is primarily due to the influx in expatriate population, which has gradually exerted pressure on the local real estate market.

From a high-density city centre, Doha’s residential market has steadily moved away from the city into areas around the C, D and E Ring Roads. West Bay has now become a sought after location for high-end residential accommodation. The change in preference is the suburban quality of these neighbourhoods and the preference to live in close proximity to both commercial nodes and retail/leisure facilities. Similar to West Bay, the Pearl Qatar, has also gained popularity, especially among high income residents.

2.2 SUPPLY

According to the latest census, Doha’s residential market comprised of 23,185 villas and 74,370 apartments in 2010. The popularity for apartments follow the increasing number of expatiates migrating into Doha for employment (Refer Exhibits 1&2). A more detailed breakdown of apartment statistics reveals that the majority of apartments are two and three bedroom units. There are limited one bedroom and studio units in the existing market (Refer Exhibit 3)

Apartment living is popular only in Doha, and is limited across other municipalities, given the concentration of white collar expatriates in the capital (Refer Exhibit 4)

.

According to government projections, an additional 60,000 units will be completed by 2020. Considering government projections, along with the actual current construction pipeline in the city, Colliers estimates cumulative residential supply in Doha to reach 138,235 units by the end of 2017 (Refer Exhibit 6).

Source: Statistics Authority – Qatar, 2010, Colliers International 2013

Exhibit 5: Average Apartment Sizes in Doha

Source: Colliers International 2013

Exhibit 3: Distribution of Apartments by the

Number of Rooms in Doha

Source: Statistics Authority – Qatar, 2010, Colliers International 2013

Exhibit 6: Cumulative Residential Supply Estimates

Source: Statistics Authority – Qatar, 2010, Colliers International 2013

Villa 92%

Apartment 8%

Exhibit 2: Distribution of Existing Housing Units in

Doha – Non Qatari Nationals

Source: Statistics Authority – Qatar, 2010, Colliers International 2013

Villa 20%

Apartment 80%

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

Doha

Al R

ayyan

Al W

akra

Um

m S

lal

Al K

hor

and A

lT

hakhira

Al S

ham

al

Al D

ayyanN

o. o

f H

ou

seh

old

s

Apartment Villa

Exhibit 5: Household Persons, by Type of Housing Unit and Municipality

Source: Statistics Authority – Qatar, 2010, Colliers International 2013

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

2010 2011 2012 2013 2014 2015 2016 2017

No

. o

f U

nit

s

CAGR 8%

CAGR 3%

95

141

204

0

50

100

150

200

250

1BR 2BR 3BR

m²

1BR 15%

2BR 44%

3BR 36%

4BR 5%

OVERVIEW REPORT | DOHA | REAL ESTATE | SECOND QUARTER | 2013 | RESIDENTIAL

4 | Colliers International | Accelerating Success | www.colliers.com

2. Residential Sector Overview Contd.

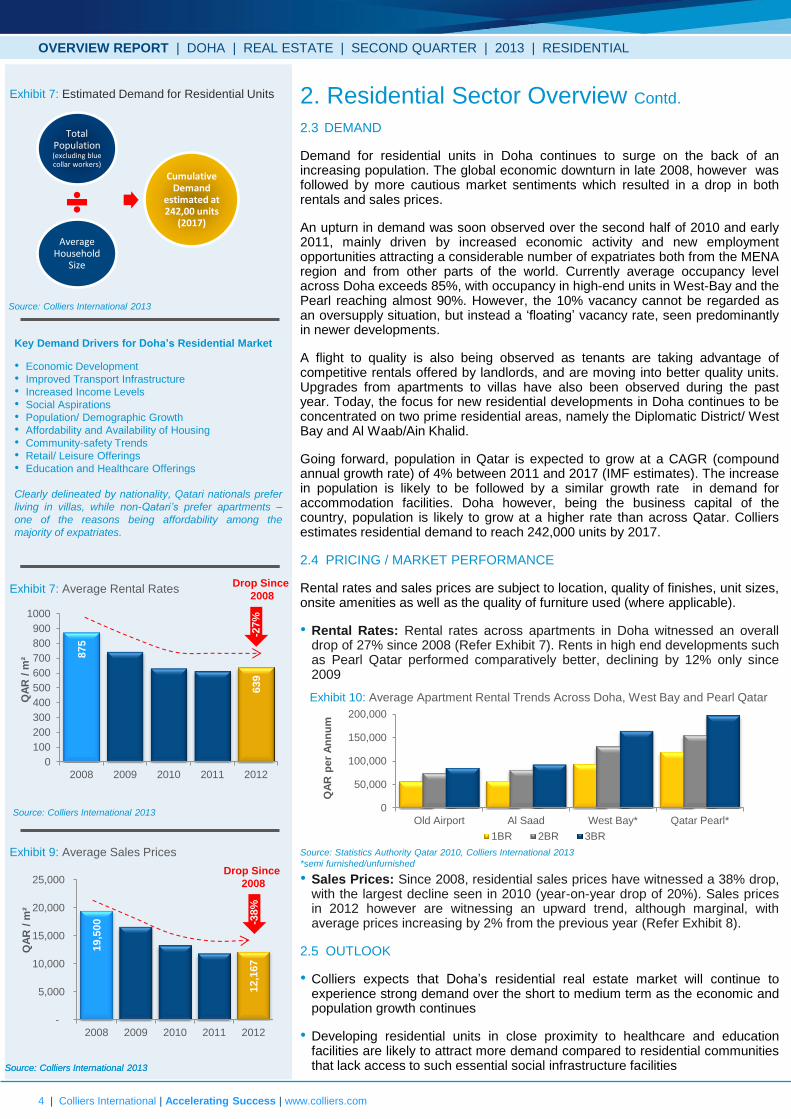

2.3 DEMAND

Demand for residential units in Doha continues to surge on the back of an increasing population. The global economic downturn in late 2008, however was followed by more cautious market sentiments which resulted in a drop in both rentals and sales prices.

An upturn in demand was soon observed over the second half of 2010 and early 2011, mainly driven by increased economic activity and new employment opportunities attracting a considerable number of expatriates both from the MENA region and from other parts of the world. Currently average occupancy level across Doha exceeds 85%, with occupancy in high-end units in West-Bay and the Pearl reaching almost 90%. However, the 10% vacancy cannot be regarded as an oversupply situation, but instead a ‘floating’ vacancy rate, seen predominantly in newer developments.

A flight to quality is also being observed as tenants are taking advantage of competitive rentals offered by landlords, and are moving into better quality units. Upgrades from apartments to villas have also been observed during the past year. Today, the focus for new residential developments in Doha continues to be concentrated on two prime residential areas, namely the Diplomatic District/ West Bay and Al Waab/Ain Khalid.

Going forward, population in Qatar is expected to grow at a CAGR (compound annual growth rate) of 4% between 2011 and 2017 (IMF estimates). The increase in population is likely to be followed by a similar growth rate in demand for accommodation facilities. Doha however, being the business capital of the country, population is likely to grow at a higher rate than across Qatar. Colliers estimates residential demand to reach 242,000 units by 2017.

2.4 PRICING / MARKET PERFORMANCE

Rental rates and sales prices are subject to location, quality of finishes, unit sizes, onsite amenities as well as the quality of furniture used (where applicable).

• Rental Rates: Rental rates across apartments in Doha witnessed an overall drop of 27% since 2008 (Refer Exhibit 7). Rents in high end developments such as Pearl Qatar performed comparatively better, declining by 12% only since 2009

• Sales Prices: Since 2008, residential sales prices have witnessed a 38% drop, with the largest decline seen in 2010 (year-on-year drop of 20%). Sales prices in 2012 however are witnessing an upward trend, although marginal, with average prices increasing by 2% from the previous year (Refer Exhibit 8).

2.5 OUTLOOK

• Colliers expects that Doha’s residential real estate market will continue to experience strong demand over the short to medium term as the economic and population growth continues

• Developing residential units in close proximity to healthcare and education facilities are likely to attract more demand compared to residential communities that lack access to such essential social infrastructure facilities

Key Demand Drivers for Doha’s Residential Market

• Economic Development

• Improved Transport Infrastructure

• Increased Income Levels

• Social Aspirations

• Population/ Demographic Growth

• Affordability and Availability of Housing

• Community-safety Trends

• Retail/ Leisure Offerings

• Education and Healthcare Offerings

Clearly delineated by nationality, Qatari nationals prefer

living in villas, while non-Qatari’s prefer apartments –

one of the reasons being affordability among the

majority of expatriates.

Total Population (excluding blue collar workers)

Average Household

Size

Cumulative Demand

estimated at 242,00 units

(2017)

Exhibit 7: Estimated Demand for Residential Units

Source: Colliers International 2013

Source: Colliers International 2013

Exhibit 9: Average Sales Prices

Source: Colliers International 2013

Exhibit 10: Average Apartment Rental Trends Across Doha, West Bay and Pearl Qatar

Source: Statistics Authority Qatar 2010, Colliers International 2013

*semi furnished/unfurnished

OVERVIEW REPORT | DOHA | REAL ESTATE | SECOND QUARTER | 2013 | RESIDENTIAL

Exhibit 7: Average Rental Rates

875

639

0

100

200

300

400

500

600

700

800

900

1000

2008 2009 2010 2011 2012

QA

R /

m²

-27%

Drop Since

2008

Source: Colliers International 2013

19,5

00

12,1

67

-

5,000

10,000

15,000

20,000

25,000

2008 2009 2010 2011 2012

QA

R /

m²

-38%

Drop Since

2008

0

50,000

100,000

150,000

200,000

Old Airport Al Saad West Bay* Qatar Pearl*

QA

R p

er

An

nu

m

1BR 2BR 3BR

5 | Colliers International | Accelerating Success | www.colliers.com

3. Commercial Sector Overview Exhibit 10: Distribution of Existing Grade A Office

Space in Doha

3.1 SECTOR DEFINITION

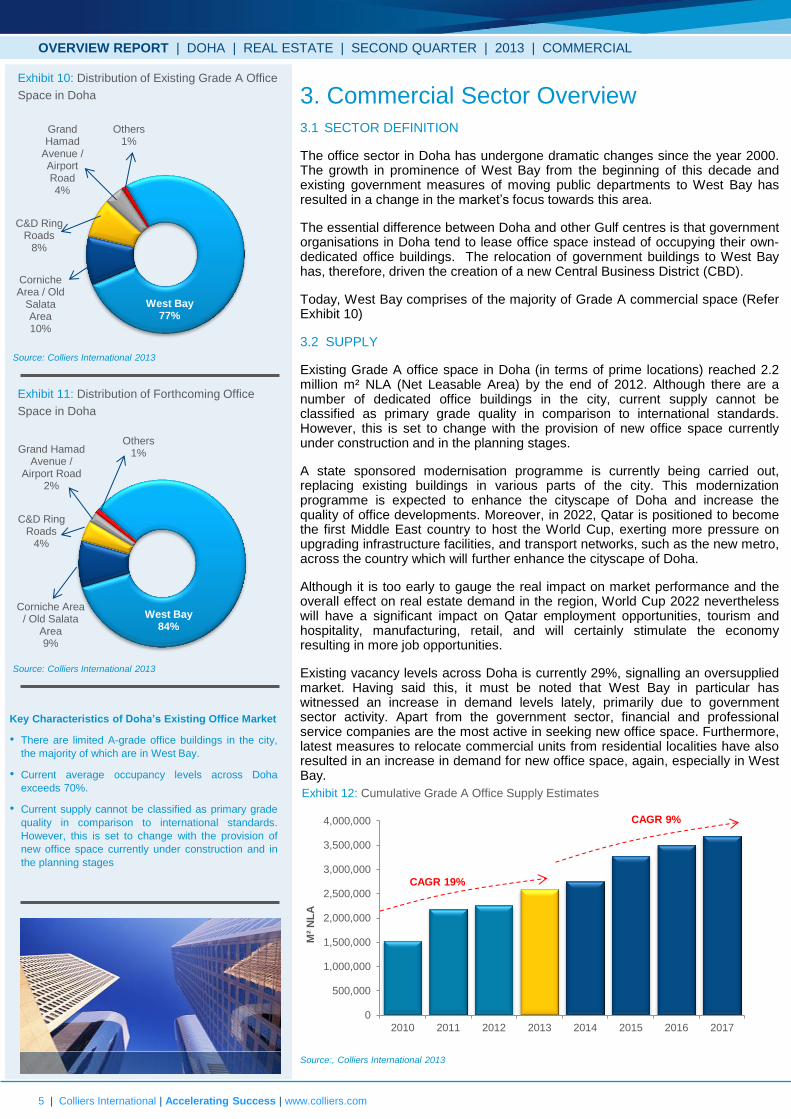

The office sector in Doha has undergone dramatic changes since the year 2000. The growth in prominence of West Bay from the beginning of this decade and existing government measures of moving public departments to West Bay has resulted in a change in the market’s focus towards this area.

The essential difference between Doha and other Gulf centres is that government organisations in Doha tend to lease office space instead of occupying their own-dedicated office buildings. The relocation of government buildings to West Bay has, therefore, driven the creation of a new Central Business District (CBD).

Today, West Bay comprises of the majority of Grade A commercial space (Refer Exhibit 10)

3.2 SUPPLY

Existing Grade A office space in Doha (in terms of prime locations) reached 2.2 million m² NLA (Net Leasable Area) by the end of 2012. Although there are a number of dedicated office buildings in the city, current supply cannot be classified as primary grade quality in comparison to international standards. However, this is set to change with the provision of new office space currently under construction and in the planning stages.

A state sponsored modernisation programme is currently being carried out, replacing existing buildings in various parts of the city. This modernization programme is expected to enhance the cityscape of Doha and increase the quality of office developments. Moreover, in 2022, Qatar is positioned to become the first Middle East country to host the World Cup, exerting more pressure on upgrading infrastructure facilities, and transport networks, such as the new metro, across the country which will further enhance the cityscape of Doha.

Although it is too early to gauge the real impact on market performance and the overall effect on real estate demand in the region, World Cup 2022 nevertheless will have a significant impact on Qatar employment opportunities, tourism and hospitality, manufacturing, retail, and will certainly stimulate the economy resulting in more job opportunities.

Existing vacancy levels across Doha is currently 29%, signalling an oversupplied market. Having said this, it must be noted that West Bay in particular has witnessed an increase in demand levels lately, primarily due to government sector activity. Apart from the government sector, financial and professional service companies are the most active in seeking new office space. Furthermore, latest measures to relocate commercial units from residential localities have also resulted in an increase in demand for new office space, again, especially in West Bay.

Source: Colliers International 2013

West Bay 77%

Corniche Area / Old

Salata Area 10%

C&D Ring Roads

8%

Grand Hamad

Avenue / Airport Road 4%

Others 1%

West Bay 84%

Corniche Area / Old Salata

Area 9%

C&D Ring Roads

4%

Grand Hamad Avenue /

Airport Road 2%

Others 1%

Exhibit 11: Distribution of Forthcoming Office

Space in Doha

Source: Colliers International 2013

Exhibit 12: Cumulative Grade A Office Supply Estimates

Source:, Colliers International 2013

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

2010 2011 2012 2013 2014 2015 2016 2017

M²

NL

A

CAGR 19%

CAGR 9%

Key Characteristics of Doha’s Existing Office Market

• There are limited A-grade office buildings in the city,

the majority of which are in West Bay.

• Current average occupancy levels across Doha

exceeds 70%.

• Current supply cannot be classified as primary grade

quality in comparison to international standards.

However, this is set to change with the provision of

new office space currently under construction and in

the planning stages

OVERVIEW REPORT | DOHA | REAL ESTATE | SECOND QUARTER | 2013 | COMMERCIAL

6 | Colliers International | Accelerating Success | www.colliers.com

3. Commercial Sector Overview Contd.

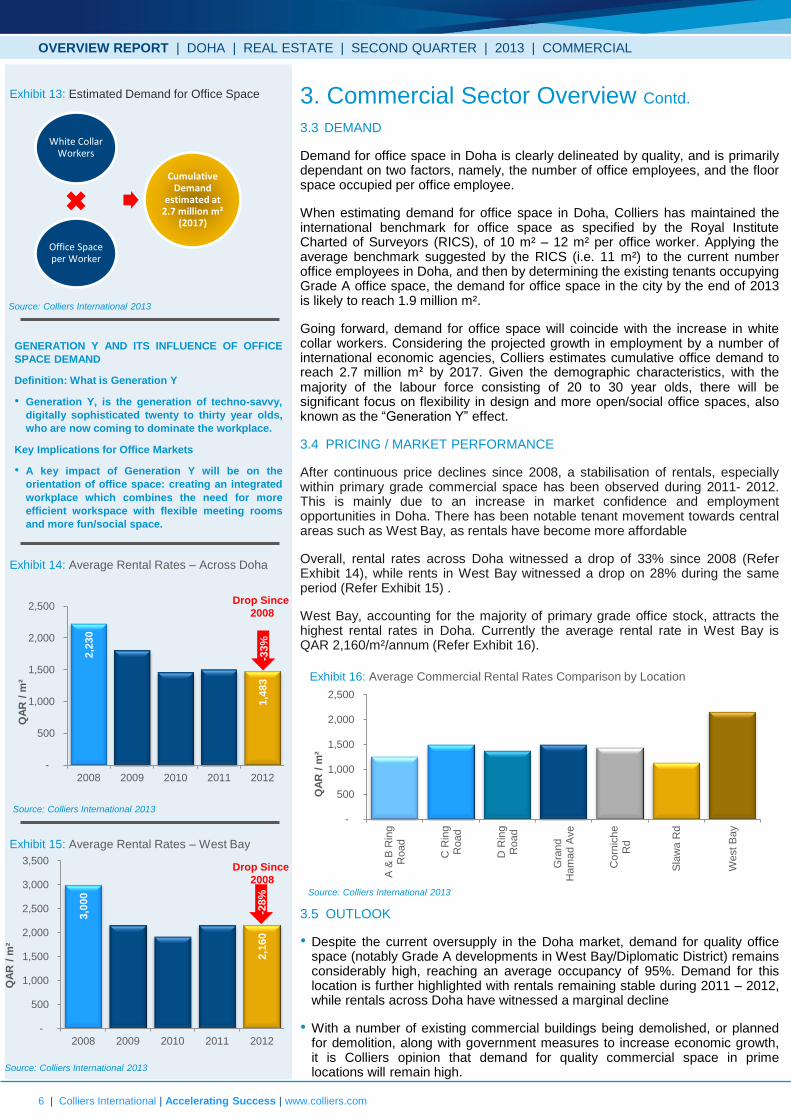

3.3 DEMAND

Demand for office space in Doha is clearly delineated by quality, and is primarily dependant on two factors, namely, the number of office employees, and the floor space occupied per office employee.

When estimating demand for office space in Doha, Colliers has maintained the international benchmark for office space as specified by the Royal Institute Charted of Surveyors (RICS), of 10 m² – 12 m² per office worker. Applying the average benchmark suggested by the RICS (i.e. 11 m²) to the current number office employees in Doha, and then by determining the existing tenants occupying Grade A office space, the demand for office space in the city by the end of 2013 is likely to reach 1.9 million m².

Going forward, demand for office space will coincide with the increase in white collar workers. Considering the projected growth in employment by a number of international economic agencies, Colliers estimates cumulative office demand to reach 2.7 million m² by 2017. Given the demographic characteristics, with the majority of the labour force consisting of 20 to 30 year olds, there will be significant focus on flexibility in design and more open/social office spaces, also known as the “Generation Y” effect.

3.4 PRICING / MARKET PERFORMANCE

After continuous price declines since 2008, a stabilisation of rentals, especially within primary grade commercial space has been observed during 2011- 2012. This is mainly due to an increase in market confidence and employment opportunities in Doha. There has been notable tenant movement towards central areas such as West Bay, as rentals have become more affordable

Overall, rental rates across Doha witnessed a drop of 33% since 2008 (Refer Exhibit 14), while rents in West Bay witnessed a drop on 28% during the same period (Refer Exhibit 15) .

West Bay, accounting for the majority of primary grade office stock, attracts the highest rental rates in Doha. Currently the average rental rate in West Bay is QAR 2,160/m²/annum (Refer Exhibit 16).

3.5 OUTLOOK

• Despite the current oversupply in the Doha market, demand for quality office space (notably Grade A developments in West Bay/Diplomatic District) remains considerably high, reaching an average occupancy of 95%. Demand for this location is further highlighted with rentals remaining stable during 2011 – 2012, while rentals across Doha have witnessed a marginal decline

• With a number of existing commercial buildings being demolished, or planned for demolition, along with government measures to increase economic growth, it is Colliers opinion that demand for quality commercial space in prime locations will remain high.

Exhibit 14: Average Rental Rates – Across Doha

GENERATION Y AND ITS INFLUENCE OF OFFICE

SPACE DEMAND

Definition: What is Generation Y

• Generation Y, is the generation of techno-savvy,

digitally sophisticated twenty to thirty year olds,

who are now coming to dominate the workplace.

Key Implications for Office Markets

• A key impact of Generation Y will be on the

orientation of office space: creating an integrated

workplace which combines the need for more

efficient workspace with flexible meeting rooms

and more fun/social space.

White Collar Workers

Office Space per Worker

Cumulative Demand

estimated at 2.7 million m²

(2017)

Exhibit 13: Estimated Demand for Office Space

Source: Colliers International 2013

Source: Colliers International 2013

Exhibit 15: Average Rental Rates – West Bay

Source: Colliers International 2013

Exhibit 16: Average Commercial Rental Rates Comparison by Location

Source: Colliers International 2013

2,2

30

1,4

83

-

500

1,000

1,500

2,000

2,500

2008 2009 2010 2011 2012

QA

R /

m²

-33%

3,0

00

2,1

60

-

500

1,000

1,500

2,000

2,500

3,000

3,500

2008 2009 2010 2011 2012

QA

R /

m²

-28%

-

500

1,000

1,500

2,000

2,500

A &

B R

ing

Road

C R

ing

Road

D R

ing

Road

Gra

nd

Ham

ad A

ve

Corn

iche

Rd

Sla

wa

Rd

West B

ay

QA

R /

m²

Drop Since

2008

Drop Since

2008

OVERVIEW REPORT | DOHA | REAL ESTATE | SECOND QUARTER | 2013 | COMMERCIAL

7 | Colliers International | Accelerating Success | www.colliers.com

4. Retail Sector Overview

4.1 SECTOR DEFINITION

The market is currently dominated by formal retail destinations such as the Villaggio, City Centre and Porto Arabia in the Pearl, which together accounts for the majority of the total organised retail supply in Doha. Established malls such as the City Centre, Landmark and Villaggio are fully occupied, and also have long waiting lists for potential tenants, signalling high demand for the “best” malls in town. Ezdan Mall is the most recent retail development to open in Doha.

Qatar’s relatively high demand for retail facilities is currently maintained by the country’s high per capita income. However, given the magnitude of forthcoming supply, retailers are expressing concern that supply will soon outstrip demand.

4.2 SUPPLY

Organised retail space in Doha reached 504,000 m² GLA (Gross Leasable Area) by the end of 2012 (Refer Exhibit 19). Doha City Centre, Villagio and Porto Arabia alone account for 65% of total retail supply. Analysing total footfall volume alone, Villagio appears to be the most popular shopping mall in Doha, successfully attracting 16.8 million visitors (Refer Exhibit 17). However, when establishing a better comparison between the malls, the footfall per m² of GLA is the highest at The Gate (Refer Exhibit 18).

Additional supply of approximately 1.48 million m² of GLA (provided construction schedules are met) is expected to enter the market between 2013 and 2020, which represents an increase of 294% from the current supply. Ezdan Mall, the most recent to open in Doha, was initially scheduled to open in 2012 but was delayed until 2013. The new mall offers 40,000 m² GLA of retail space, across three floors. Adjacent to Ezdan Mall is Gulf Mall (approximately 80,000 m² GLA), which was also initially scheduled for 2012, but delayed to 2013.

Exhibit 17: Footfall of Existing Key Shopping Malls

Source: Colliers International 2013

504,0

00

-

100,000

200,000

300,000

400,000

500,000

600,000

Doha C

ity C

en

ter

Vill

agio

Landm

ark

lagoona

Th

e M

all

Po

rto A

rabia

- T

he

Pe

arl

Haytt p

laza

Royal P

laza

Th

e G

ate

To

tal

GL

A/S

qm

Exhibit 19: Existing Shopping Mall Supply - 2012

Source: Colliers International 2013

-

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

2010 2011 2012 2013 2014 2015 2016 2017

m²/

NL

A

CAGR 16%

CAGR 16% Exhibit 20: Cumulative Retail Supply Estimates

Source: Colliers International 2013

210

200 225

200

160

135

175

170

245

0

50

100

150

200

250

Doha C

ity C

en

ter

Vill

agio

Landm

ark

lagoona

Th

e M

all

Po

rto A

rabia

- T

he P

earl

Haytt p

laza

Royal P

laza

Th

e G

ate

QR

/SQ

m/A

nn

um

Exhibit 18: Footfall per m² of GLA

Source: Colliers International 2013

Ezdan Mall – Recently Opened

-

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

16,000,000

18,000,000

Doha C

ity C

en

tre

Vill

agio

Landm

ark

Th

e M

all

Po

rto A

rabia

Haytt P

laza

Th

e G

ate

OVERVIEW REPORT | DOHA | REAL ESTATE | SECOND QUARTER | 2013 | RETAIL

8 | Colliers International | Accelerating Success | www.colliers.com

4. Retail Sector Overview Contd.

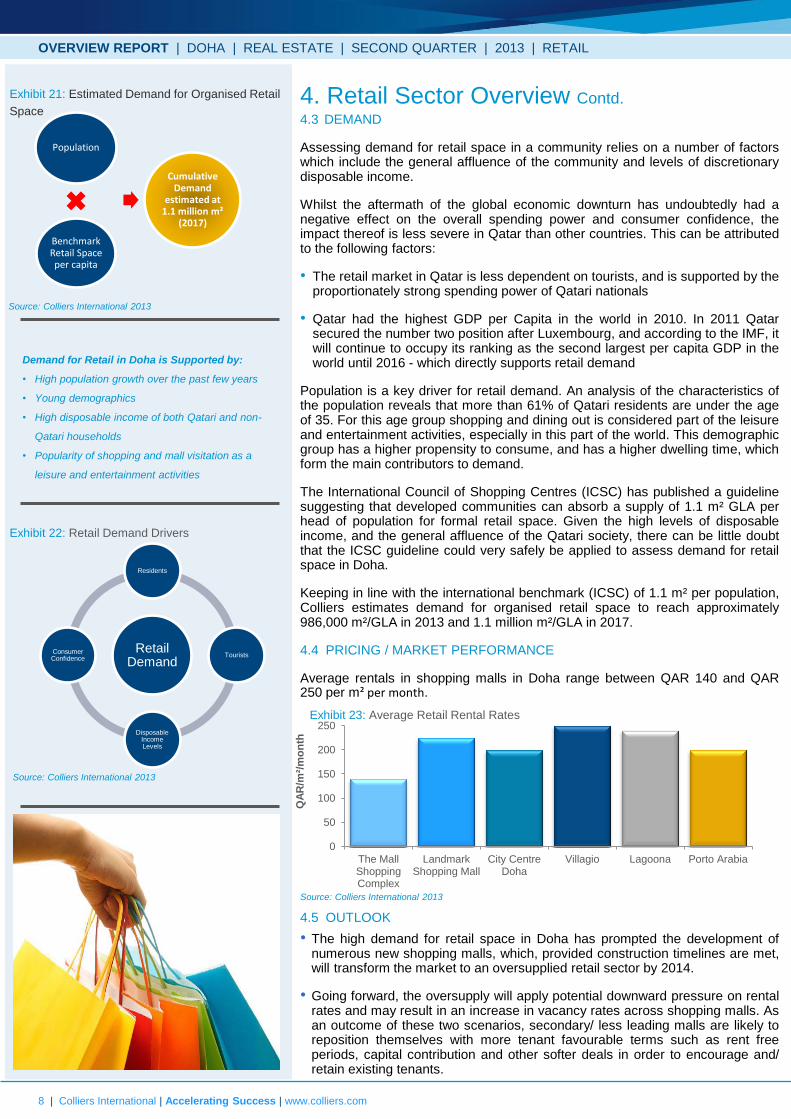

4.3 DEMAND

Assessing demand for retail space in a community relies on a number of factors which include the general affluence of the community and levels of discretionary disposable income.

Whilst the aftermath of the global economic downturn has undoubtedly had a negative effect on the overall spending power and consumer confidence, the impact thereof is less severe in Qatar than other countries. This can be attributed to the following factors:

• The retail market in Qatar is less dependent on tourists, and is supported by the proportionately strong spending power of Qatari nationals

• Qatar had the highest GDP per Capita in the world in 2010. In 2011 Qatar secured the number two position after Luxembourg, and according to the IMF, it will continue to occupy its ranking as the second largest per capita GDP in the world until 2016 - which directly supports retail demand

Population is a key driver for retail demand. An analysis of the characteristics of the population reveals that more than 61% of Qatari residents are under the age of 35. For this age group shopping and dining out is considered part of the leisure and entertainment activities, especially in this part of the world. This demographic group has a higher propensity to consume, and has a higher dwelling time, which form the main contributors to demand.

The International Council of Shopping Centres (ICSC) has published a guideline suggesting that developed communities can absorb a supply of 1.1 m² GLA per head of population for formal retail space. Given the high levels of disposable income, and the general affluence of the Qatari society, there can be little doubt that the ICSC guideline could very safely be applied to assess demand for retail space in Doha.

Keeping in line with the international benchmark (ICSC) of 1.1 m² per population, Colliers estimates demand for organised retail space to reach approximately 986,000 m²/GLA in 2013 and 1.1 million m²/GLA in 2017.

4.4 PRICING / MARKET PERFORMANCE

Average rentals in shopping malls in Doha range between QAR 140 and QAR 250 per m² per month.

4.5 OUTLOOK

• The high demand for retail space in Doha has prompted the development of numerous new shopping malls, which, provided construction timelines are met, will transform the market to an oversupplied retail sector by 2014.

• Going forward, the oversupply will apply potential downward pressure on rental rates and may result in an increase in vacancy rates across shopping malls. As an outcome of these two scenarios, secondary/ less leading malls are likely to reposition themselves with more tenant favourable terms such as rent free periods, capital contribution and other softer deals in order to encourage and/ retain existing tenants.

Exhibit 22: Retail Demand Drivers

Population

Benchmark Retail Space per capita

Cumulative Demand

estimated at 1.1 million m²

(2017)

Exhibit 21: Estimated Demand for Organised Retail

Space

Source: Colliers International 2013

Source: Colliers International 2013

Retail Demand

Residents

Tourists

Disposable Income Levels

Consumer Confidence

0

50

100

150

200

250

The MallShoppingComplex

LandmarkShopping Mall

City CentreDoha

Villagio Lagoona Porto Arabia

QA

R/m

²/m

on

th

Demand for Retail in Doha is Supported by:

• High population growth over the past few years

• Young demographics

• High disposable income of both Qatari and non-

Qatari households

• Popularity of shopping and mall visitation as a

leisure and entertainment activities

Exhibit 23: Average Retail Rental Rates

Source: Colliers International 2013

OVERVIEW REPORT | DOHA | REAL ESTATE | SECOND QUARTER | 2013 | RETAIL

9 | Colliers International | Accelerating Success | www.colliers.com

482 offices in

62 countries on

6 continents

United States: 140

Canada: 42

Latin America: 20

Asia Pacific: 195

EMEA: 85

• $2.0 billion in revenue

• More than 13,500 employees

• 5,100 brokers

• $71 billion in transaction volume

across more than 78,000 sale and

lease transactions

• 1.1 billion square feet under

management

SERVICES OFFERED BY COLLIERS

INTERNATIONAL

• Brokerage Sales and Leasing

• Corporate Solutions

• Development Solutions

• Hotel Services

• Healthcare and Education Services

• Investment Services

• Project Management Services

• Real Estate Property Management

Services

• Research Services

• Retail Advisory Services

• Valuation and Advisory Services

SERVICES BY PROPERTY TYPE

• Office

• Retail

• Mixed-Use

• Industrial

• Hotels

• Residential

• Hospitals/Medical Clinics

• Schools / Universities

COLLIERS INTERNATIONAL

Colliers International is a leading global real estate services organisation defined by our spirit of

enterprise. Our 13,500 professionals in 482 offices worldwide are dedicated to creating strategic

partnerships with our clients, providing customised services that transform real estate into a

competitive advantage.

COLLIERS INTERNATIONAL MIDDLE EAST

Colliers International has been providing leading advisory services in the Middle East and North

Africa region since 1996 and in Saudi Arabia since 2004. Regarded as the largest and most

experienced firm in the region, Colliers International’s expertise covers Hospitality, Residential,

Commercial, Retail, Healthcare, Education and PPP sectors together with master planning

solutions, serviced from the five regional offices, i.e., Abu Dhabi, Dubai, Riyadh, Jeddah & Cairo.

Colliers Research Services Group is recognised as a knowledge leader in the industry, providing

clients with valuable market intelligence to support business decisions. Colliers research analysts

provide multi-level support across all property and business types, ranging from data collection to

comprehensive market and competition analysis.

OUR SPECIALISATIONS

The information contained in this document (the “Report”) has been obtained from sources deemed reliable. While every reasonable effort

has been made to ensure its accuracy, we cannot guarantee it. No responsibility is assumed for any inaccuracies. Readers are encouraged

to consult their professional advisors prior to acting on any of the material contained in this report.

Colliers International makes no warranty, representation or undertaking whether expressed or implied, nor does it assume any legal liability,

whether direct or indirect, or responsibility for the accuracy, completeness, or usefulness of any information contained in the Report. It is not

the intention of the Report to be used or deemed as recommendation, option or advice for any action(s) that may take place in the future.

Unless otherwise stated, all information contained in this Report shall not be reproduced, in whole or in part, without the specific written

permission of Colliers International.

Airport Cities & City

Centres

Waterfront

Developments & Ports

Sports &

Entertainment

Healthcare & Life

Sciences

Education & Human

Capital

Infrastructure & Public

Private Partnership

Leisure, Tourism &

Cultural Development

Mixed Use

Developments Hospitality

OVERVIEW REPORT | DOHA | REAL ESTATE | SECOND QUARTER | 2013 | ABOUT COLLIERS INTERNATIONAL

Accelerating success. www.colliers.com

Main +971 4 453 7400 | Fax +971 4 453 7401 | Dubai Main +971 2 619 2460 | Fax +971 2 619 2450 | Abu Dhabi Colliers International P O Box 71591 | Dubai | UAE P O Box 94348 | Abu Dhabi | UAE Cairo | Riyadh | Jeddah

Mansoor Ahmed MAS, MSc Director | Development Solutions Healthcare | Education | Public Private Partnership (PPP) Mobile +971 55 899 6091 [email protected]

Duncan Gray BSc (Hons) MRICS MRTPI Director and Country Manager Qatar Mobile +974 3 314 2160 (Qatar) | +971 55 720 0707 (UAE) [email protected]