real time payments - carlo palmers

TRANSCRIPT

RT-RPS – Update – Apr15

Real-Time Retail Payment Systems Update

April 2015

RT-RPS – Update – Apr15

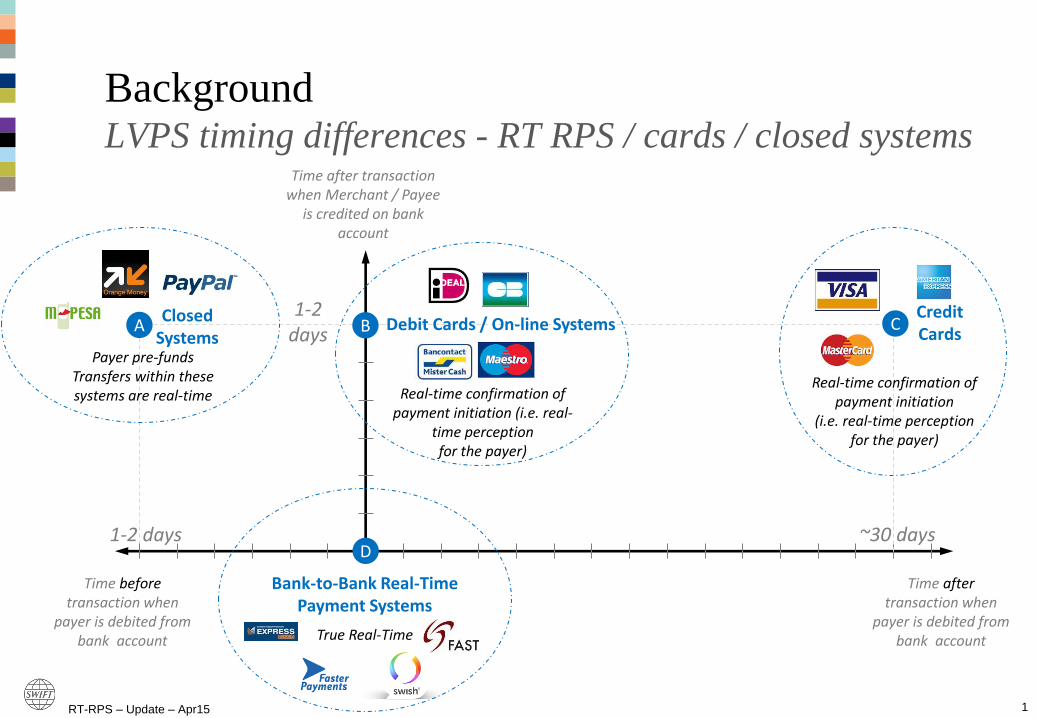

Background LVPS timing differences - RT RPS / cards / closed systems

1

Payer pre-funds Transfers within these systems are real-time

A

1-2 days

Closed Systems

1-2 days

Time after transaction when

payer is debited from bank account

Time before transaction when

payer is debited from bank account

Time after transaction when Merchant / Payee

is credited on bank account

D

Bank-to-Bank Real-Time Payment Systems

True Real-Time

~30 days

Credit Cards

Real-time confirmation of payment initiation

(i.e. real-time perception for the payer)

Debit Cards / On-line Systems

Real-time confirmation of payment initiation (i.e. real-

time perception for the payer)

B C

RT-RPS – Update – Apr15

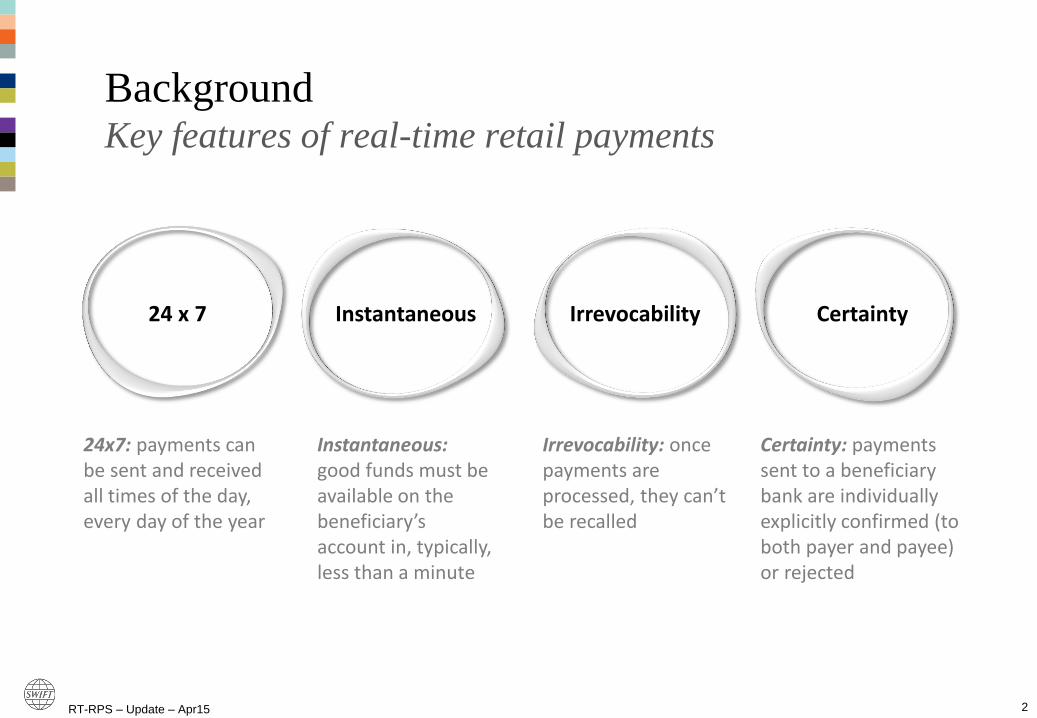

Background Key features of real-time retail payments

2

24x7: payments can be sent and received all times of the day, every day of the year

24 x 7 Instantaneous Irrevocability Certainty

Instantaneous: good funds must be available on the beneficiary’s account in, typically, less than a minute

Irrevocability: once payments are processed, they can’t be recalled

Certainty: payments sent to a beneficiary bank are individually explicitly confirmed (to both payer and payee) or rejected

RT-RPS – Update – Apr15

Background Candidates for RT adoption (from banks’ perspective)

3

Consumer

Business

Consumer

Business

Business

Consumer

4%

51%

18%

7%

80%

20% 20%

Payer Payee Type Share* Confirming Availability Trend Value of RT

Person to Person

Point of Sale (Physical)

Bill Payment**

High Value

E-Commerce

Mobile Commerce

Bulk Payment

Invoice Payment

High Value Order

Primary candidate

Primary candidate

Primary candidate

Secondary candidate

RT Candidate

*share of total non-cash payments worldwide

**including direct debits

Secondary candidate

RT-RPS – Update – Apr15

RT-RPS Characteristics The interbank payment system is only one part of the solution

4

Payee / Beneficiary Customer

Payee Participant Bank

RT Architecture

Applications

Back Office

Infrastructure

Payer Participant Bank

RT Architecture

Applications

Back Office

Infrastructure Payer / Ordering Customer

RT Interbank Payment System

Clearing

Settlement

Agreements Agreements Agreements Agreements Agreements

Three key components required to allow for end-to-end RT-RPS 1. Banks’ infrastructures (front to back) must work in real-time 2. The interbank payment system must work in real-time 3. End-to-end commercial and operational agreements must be in place

3 3 3 3 3

1 1 2

RT-RPS – Update – Apr15

RT-RPS Characteristics But, the approach to clearing and settlement differs

5

Hub Approach RTGS Approach Distributed Approach

Majority of existing RT-RPS’ - UK, SE, SG, PL

CH,MX,CZ AU

• Interactive clearing, where paying bank requests confirmation of payment details

• 24x7x365 (most) • Settlement either via pre-funding or

through deferred net settlement

• No distinction between high and low value

• No interactive clearing as combined with settlement

• No 24x7, but close

• Interactive Bank-to-Bank clearing • Settlement separated from

clearing and performed by CB as a Fast Settlement Service (FSS)

• 24x7

RTGS

Hub Clearing

Settlement

A B

Bank A

Bank B

RTGS A B

Bank A

Bank B

Central Bank

Bank A

Bank B

Clearing

Settlement

A’ B’

A B

FSS

RTGS

Acc

ou

nts

Acc

ou

nts

Acc

ou

nts

A

cco

un

ts

or or

RT-RPS – Update – Apr15

Australian NPP Project SWIFT Solution

Beneficiary Customer

Central Bank

Ordering Customer

Orderer’s Participant Bank

Branch

Mobile

Phone

Internet

Services

Applications

SWIFT Payment Gateway

Beneficiary’s Participant Bank

Branch

Mobile

Phone

Internet

Services

Applications

SWIFT Payment Gateway Clearing / Confirmation

Settlement

Payment Details

Payment Details Confirmation

Domestic Messaging Channel

Settlement

Settlement Confirmation

Settlement Confirmation

1

2

3

4 4

Key Features • Clearing & Settlement - use of a new domestic

point-to-point channel catering for low latency and 24x7 availability

• Leverages ISO 20022 standards • Increased resiliency through a distributed model

SWIFT Payment Gateway

Addressing Database ICS

Overlay services

Thank you