realignment of financial controlling - building a better ... · pdf filerealignment of...

TRANSCRIPT

Realignment of Financial Controllingin context of implementing current regulatory requirements for financial institutions

Update of the 2012 study — Challenges for Financial Controlling functions in banking.

40 selected financial institutions on the current status of implementation of the regulatory requirements.

3Realignment of Financial Controlling |

In 2012, EY conducted the study “Challenges for Financial Controlling functions in banking” for which around 80 German financial institutions were surveyed on the impact of the financial market crisis on their Financial Controlling function. Closed questions were asked on their management, planning, forecasting and reporting systems and processes.

The participants were also asked about regulatory requirements affecting Financial Controlling, as a variety of new or stricter requirements had been formulated at international level in response to the financial market crisis. These requirements serve to strengthen financial institutions’ capital and liquidity, keep risks at bay (more stringent Risk Management) and optimize existing governance structures.

At the time the original study was conducted, the responses from participants revealed strong pressure to adapt and pointed in particular to the need for the early involvement of the Financial Controlling function in respective implementation projects. The regulatory requirements have since been refined by directives and technical standards, and first implementation projects have also been carried out.

To update the knowledge and insight gained from the 2012 study, 40 selected financial institutions were surveyed on the current status of the involvement and realignment of their Financial Controlling function in the context of implementing the regulatory requirements. The excellent response rate in 2012 was equaled again in this survey.

1.0 Introduction

4 | Realignment of Financial Controlling

1.0 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 03

2.0 Survey results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 06

2.1 Project approach . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 07

2.2 Data model and IT architecture . . . . . . . . . . . . . . . 10

2.3 Implications of Basel III . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

2.4 Implications of FinRep and BSA . . . . . . . . . . . . . . 19

2.5 Capital planning . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

3.0 Outlook . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

Contacts/Imprint . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

Contents

5Realignment of Financial Controlling |

The purpose of the latest EY survey was to evaluate to what extent the new regulatory requirements have already been adopted by the Financial Controlling function and thus have been incorporated into the Controlling framework. Additional aspects include the alignment of the various measurement approaches and the involvement of the Controlling function in regulatory implementation projects.

2.0Survey results

7Realignment of Financial Controlling |

55%46%9%Separate projects dedicated to individual topics

0%Interim/workaround solutions are

being pursued/are planned

45%27%9%9%One overall project with individual subprojects

The new Regulatory Reportingrequirements show a strong trend toward integration and harmonization of finance, risk and controlling functions. Consequently, we wanted to know whether this trend is being taken into account in implementation initiatives currently undertaken by financial institutions. It seems obvious that sometimes complex requirements and their operational impact on IT systems and business processes as well as on refinancing costs and the cost

of capital necessitate a coordinated implementation process that will closely involve Financial Controlling. In this context, we wanted to find out how financial institutions have structured their implementation projects and what role controlling assumed in these projects.

Which project governance has been chosen in your organization to cater to the new Regulatory Reporting requirements (e.g., FinRep/CoRep)?

Current project governance models to address new Regulatory Reporting requirements

Figure 1 60%40%20% 80% 100%0%

■ Controlling function is strongly involved

■ Controlling function is merely a data supplier

■ Controlling function is barely involved/not involved at all

2.1 Project approach

The responses to these questions reveal that around half of the participating financial institutions have launched separate projects, while the other half are focusing on a single overall project. Interim or workaround solutions were not an option for any of the participants.

The Controlling function is strongly involved in the respective projects at only 18% of the financial institutions. Controlling is merely a data supplier at 9% of institutions. The majority of the participants (around 73%) stated that the Controlling function is barely involved or not involved at all in relevant implementation projects.

8 | Realignment of Financial Controlling

Given the advanced stage of the projects and the lack of involvement of Financial Controlling function, we see the

need to review the content of the implementation projects and initiate corresponding follow-up projects.

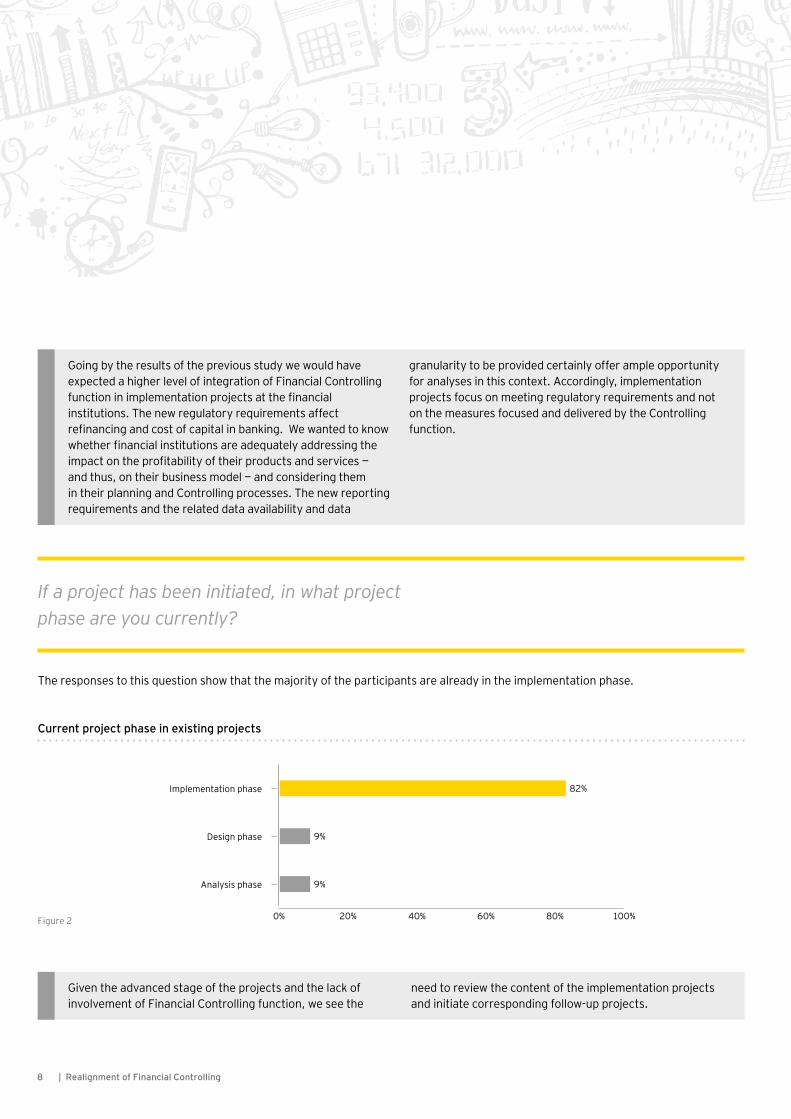

The responses to this question show that the majority of the participants are already in the implementation phase.

If a project has been initiated, in what project phase are you currently?

82%

9%

9%

Current project phase in existing projects

Figure 2

Analysis phase

Design phase

Implementation phase

60%40%20% 80% 100%0%

Going by the results of the previous study we would have expected a higher level of integration of Financial Controlling function in implementation projects at the financial institutions. The new regulatory requirements affect refinancing and cost of capital in banking. We wanted to know whether financial institutions are adequately addressing the impact on the profitability of their products and services — and thus, on their business model — and considering them in their planning and Controlling processes. The new reporting requirements and the related data availability and data

granularity to be provided certainly offer ample opportunity for analyses in this context. Accordingly, implementation projects focus on meeting regulatory requirements and not on the measures focused and delivered by the Controlling function.

9Realignment of Financial Controlling |

Stand-alone (fragmented) IT solutions contrast against an integrated overall solution. Initially, they can frequently be implemented with less time and effort. However,they are usually not commensurate with the medium to long-term objective of a harmonized IT landscape that satisfies the comprehensive set of regulatory requirements. A fragmented infrastructure will usually have difficulties to supply the

requested data in the required quality at short notice or on an ad-hoc basis across reports. Additionally, the opportunity of utilizing the current regulatory requirements implementation to to work toward an integrated overall solution is not being seized. However, this is the only way in which the complex and resource-consuming reconciliations between data sets can be significantly reduced or even eliminated in the future.

The majority of the participants integrate the relevant reporting requirements into existing systems. Merely 14% implement separate IT solutions.

Only around one third are targeting an integrated overall solution. The majority, i.e., around two thirds, work with isolated or stand-alone IT solutions.

If a project has been initiated, how are targeted solutions embedded in your IT architecture?

IT architecture context — Implementation as an interim solution, stand-alone solution or integrated overall solution

IT architecture context — Integration into existing or new systems

Figure 3 Figure 4

■ Mainly interim solutions

■ Mainly isolated, stand-alone IT solutions

■ Mainly integrated overall solutions

■ Financial institutions mainly use existing systems

■ Financial institutions mainly implement new systems

63%

86%

0%

38%

14%

10 | Realignment of Financial Controlling

Usually, the aim of integrated reporting can only be achieved with a comprehensive and reconciled database. Reconciliation of different data sets is possible in theory, but in practice it is generally associated with a great deal of time and effort to ensure data integrity and quality. In the context of the study, we were therefore particularly interested in finding out what databases and IT systems the financial institutions will use to meet the new requirements and to what extent financial institutions will restructure their IT architecture and data models in order to establish a uniform, bank-wide database. In view of the specific

regulatory requirements for IT systems and data, in particular for systemically relevant financial institutions, e.g., BCBS 239 and Asset Quality Review (AQR), even more attention will need to be paid to this topic from now on. Bank-wide risk data aggregation and reporting as well as data quality and data governance are clear objectives of a uniform taxonomy of data fields, which must also take into account Financial Controlling data.

Apart from a few exceptions, the participating financial institutions expect that changes will need to be made in Financial Controlling with regard to (management) methods, processes and systems. The majority (around 64%) of them expect a significant need for change, which will require the introduction of new processes or systems. The remaining participants expect a moderate need for adjustment to existing systems or processes.

Under Basel III (CRR/CRD IV), capital requirements are changing for financial institutions. For the Controlling Function, this necessitates changes to (management) methods, processes and systems. What expectations do you have in this context?

Expectations with regard to the need for change as a result of the amended capital requirements under Basel III

Figure 5

■ Moderate adjustments without significant changes

■ New processes/systems required

■ No need for change

64%

27%

9%

2.2 Data model and IT architecture

Expectations are consistent with the conclusion drawn from the 2012 study, which already indicated change in the Controlling function to be expected.

In our view, the plan or forecast figures will have to become the focus of institutions’ Risk Management under Basel III in order to analyze and anticipate the impact of new capital requirements on their business model. However, it is questionable whether the required processes, IT systems and data are available given the lack of involvement of the Controlling function (see 2.1).

11Realignment of Financial Controlling |

9%Neither FDW nor RDW

18%FDW only

55%FDW and RDW (isolated from one another)

9%RDW only

9%FDW and RDW (integrated/interlinked)

While 55% of the participants have a financial data warehouse and a risk data warehouse (FDW and RDW), these data sets are largely being held separately. The data are not reconciled or linked. Only 9% of the participants have an integrated FDW and RDW.

27% of the participants either have just an FDW or just an RDW. Consequently, 91% of the participants do not have an integrated database linking financial data with risk data.

Which structure best describes the current data architecture at your institution?

Current project phase in existing projects

Figure 6 60%40%20% 80% 100%0%

We believe that significant changes are required here in order to meet the requirements of integrated Controlling. Additionally, BCBS 239, for example, requires systemically relevant financial institutions to reconcile their risk and Accounting data from 2016. The recent Asset Quality Review

also showed that the calculation, linkage and reconcilability of risk and Accounting data posed a major challenge for financial institutions in a number of cases.

12 | Realignment of Financial Controlling

11%No implementation/harmonization planned

11%Yes, using an integrated/linked RDW and FDW

0%Yes, using an RDW

0%Yes, using an isolated RDW and FDW

Yes, using an FDW

A large majority (around 78%) of the participants plan to introduce an integrated database based on the FDW. The FDW would then provide all relevant data for Risk Management, Accounting, Controlling and Regulatory Reporting.

Another 11% view the integration or linkage of FDW and RDW as a solution for a harmonized data landscape, while only 11% are not planning any further harmonization and/or integration.

Do you plan to implement a harmonized data model offering integrated data for the Risk Management, Accounting, Controlling and Regulatory Reporting functions (cf. the EBA’s “Data Point Model”)?

78%

Plans for a harmonized data model with integrated data

Figure 7 60%40%20% 80% 100%0%

The vast majority of almost 90% of respondents have recognized the advantages of integrated and harmonized data and are implementing such a model. In addition to potentially allowing the streamlining of the IT architecture, this approach can also more easily satisfy the Single Point

of Truth principle. Only 11% of the surveyed institutions see no further need for action and plan to meet the new requirements using their existing systems landscape.

13Realignment of Financial Controlling |

65 %

20 %

80 %

… % is directly available in the reporting systems and can be used for Controlling

with little time and effort.

60 %

10 %

25 %… % is only available in the source systems and

cannot be used directly for Controlling.

20 %

50 %

5 %… % is not currently available or not available

in the desired granularity/quality.

The survey results allow us to conclude that, on average, only just over half of all the data that will need to be reported as a result of the new regulatory requirements are already available in the systems and can be used directly by the Controlling

function. The remainder of the required data is distributed fairly equally over the categories “not available” or “only available in the source systems.”

In view of the covered topics : What estimated proportion of data required to meet the new regulatory requirements is already available?

Percentage of data already available to meet the new regulatory requirements

Figure 8 60 %40 %20 % 80 % 100 %0 %

For a significant proportion of the required data, adjustments or data enhancements are required in the systems before the data can be made available for Controlling. This leads to delays in the provision of data and necessitates measures to ensure completeness and transparency — thus tying up

resources. The automated provision of data, viewed as best practice, should therefore be coordinated centrally and ideally addressed and implemented during ongoing projects or follow-up projects.

■ Minimum

■ Median

■ Maximum

14 | Realignment of Financial Controlling

The majority of the participants use the Accounting fair value (55%) or plan to use the Accounting fair value (18%) for Controlling. Only 9% of the participants have access

to both the regulatory fair value as well as the Accounting fair value in Controlling.

In the future, a fair value according to Accounting standards and, at the same time, according to regulatory requirements (see Art. 105 CRR) will have to be determined. Which value is used for performance or which value would you use?

With the Basel III reform package and the Asset Quality Review of the European Central Bank (ECB), the cost of capital for financial institutions can be expected to rise further. In addition, consistent liquidity ratios (LCR, NSFR) and a leverage ratio (LR) are being introduced for the first time, which are expected to affect the financing structure of financial institutions.

For Financial Controlling, these will have significant impact on capital planning, performance measurement and management. In addition, as a result of the reform of Regulatory Reporting requirements under FinRep and CoRep, new data and information have to be collected. They should be checked to determine whether they can be used for Controlling in order to exploit synergies and enhance performance management parameters.

Availability/use for financial controlling: FV under Accounting law vs. FV under regulatory law

Figure 9

■ Accounting FV is available and is used by the Controlling function.

■ Regulatory FV is available and is used by the Controlling function.

■ Both values are available for Controlling and can be used in parallel.

■ Regulatory FV is not available, but is to be used by the Controlling function in the future.

■ Accounting FV is not available, but is to be used by the Controlling function in the future.

■ No value is available and its use is not planned.

FV = Fair Value

55%

0%

9%

18%

9%

9%

2.3 Implications of Basel III

15Realignment of Financial Controlling |

A large majority of the participants intend to establish the new leverage ratio as a metric in Controlling. However, only around 18% of the participants anticipate an impact on product

calculation or plan to implement a further breakdown of the ratio on business unit level.

Due to the introduction of theratios LR, LCR and NSFR, a new taxonomy for leverage must be disclosed for which a limit will also be implemented in the future. In your opinion, what impact does this have on Financial Controlling?

The Controlling functions consider the new leverage ratio to be a key element of the new regulatory requirements.

Impact on Controlling of the future limit for the leverage ratio

Figure 10

■ The Controlling function plans to establish the new leverage ratio as a management metric for use in performance reporting.

■ The Controlling function plans allocation on profit center level.

■ The Controlling function was involved in the introduction.

9%

73%

18%

16 | Realignment of Financial Controlling

Half of the participants reconcile statutory capital and regulatory capital, with the Financial Controlling function being almost always involved in this process.

Those institutions that currently do not have such a reconciliation in place plan to establish such a process during current projects or follow-up projects.

Although 55% of the participants currently reconcile capital figures, 20% do not involve the Financial Controlling in this process, which means that it may not be able to meet its management function in full.

Is a reconciliation between statutory capital and regulatory capital already being performed at your institution? If so, is the Controlling function involved?

Reconciliation between statutory and regulatory capital

If capital figures are being reconciled, the Controlling function is ...

Figure 11 Figure 12

■ Reconciliation is already being conducted.

■ Reconciliation is not planned.

■ Reconciliation is part of the regulatory projects.

■ … involved.

■ … not involved.

■ … responsible.

9%

20%

55%

70%

36%

10%

The existing reconciliation processes provide a basis for the implementation of the new requirements. We conclude that the Controlling Function department should play a

key role in the process, also in order to shed light on the possible capital effects and to be able to fulfill its management function.

17Realignment of Financial Controlling |

The capital buffers planned under Basel III stipulate that financial institutions have to hold additional capital. This can impact capital planning as well as the allocation of capital cost to products and business units. In practice, we believe the challenge lies in particular in combining economic, regulatory, statutory and operational parameters in order to obtain integrated performance indicators.

A large majority of the participants already consider the required capital buffers. Only a small minority see a need for change in order to address the capital buffers.

How are you planning to incorporate the capital buffers proposed under Basel III?

91%

9%

0%

Current project phase in existing projects

Figure 13

Capital buffers taken into account in capital planning process

Capital buffers are not relevant

Enhancement of processes/systems required

60%40%20% 80% 100%0%

18 | Realignment of Financial Controlling

45%

45%

9%

Participation of the performance management function

Figure 14

The Controlling function is heavily involved.

The Controlling function is not involved.

The Controlling function is partially involved.

60%40%20% 80% 100%0%

Incorporating the required capital buffers under Basel III does not entail considerable additional time and effort for the participants. Capital buffers are generally already being taken into account, which means that no further changes are

expected. However, higher volatility of the capital being managed (CRR, IFRSs) is anticipated; there is barely any experience to be leveraged to reliably forecast new deduction items under the CRR or such data still have to be generated.

During the survey, we also asked about the involvement of Financial Controlling in the capital planning process.

The Controlling Function is involved in the planning process in over 90% of cases, thereof 45% of respondents are in the lead.

19Realignment of Financial Controlling |

From 1 July 2014, all systemically relevant financial institutions are required to submit a quarterly FinRep report to the European Banking Authority (EBA). Consequently, the submission of the FinRep report to the EBA will be initially required for the third quarter of 2014.

For the FinRep report, financial institutions have to prepare IFRS consolidated financial statements based on the regulatory scope of consolidation. The information contained in these financial statements is used to complete the various FinRep reporting forms, taking into account the classification requirements of these forms.

The considerably extended information requirements from FinRep compared with the existing Regulatory Reporting requirements pose substantial challenges for financial institutions, mainly due to the very high level of detail of the report. In addition, financial institutions required to submit the report have to ensure that it can be reconciled with various other reportings (e.g., consolidated financial statements, CoRep or LR).

During its Balance Sheet Assessment (BSA), the ECB also requested information from various departments and, by extension, required different sets of information from the financial institutions to be combined. The data requests were already based on the FinRep definitions.

A number of examples are:• Breakdown by product/counterparty group as well as

geographical breakdown• Data on own credit risk• Information on impairments and past due exposures• Data on economic derivative hedging • Loan commitment and collateral data• Information on reconciliations between Accounting (IFRS)

and Regulatory Reporting (CRR)

From the perspective of the Controlling function, the question in this context is to what extent this information required by regulatory requirements should also be used for Financial Controlling.

2.4 Implications of FinRep and BSA

20 | Realignment of Financial Controlling

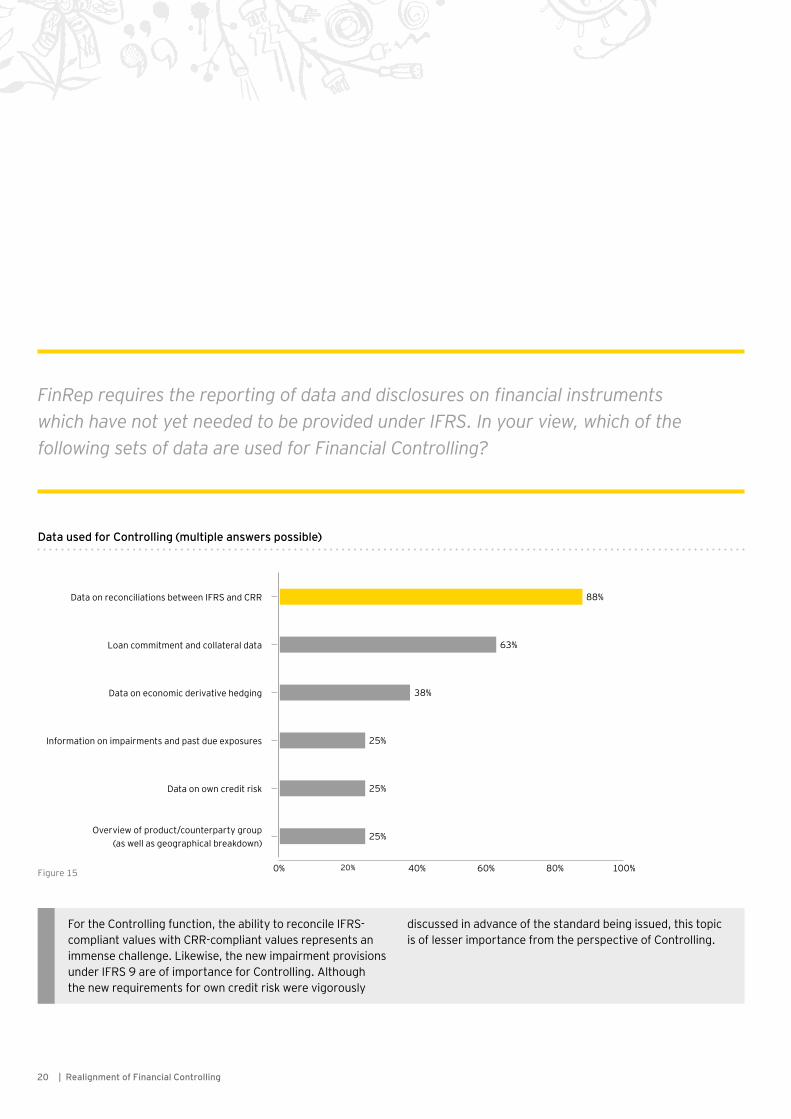

FinRep requires the reporting of data and disclosures on financial instruments which have not yet needed to be provided under IFRS. In your view, which of the following sets of data are used for Financial Controlling?

25%

88%

25%

63%

25%

38%

Data used for Controlling (multiple answers possible)

Figure 15

Information on impairments and past due exposures

Data on reconciliations between IFRS and CRR

Overview of product/counterparty group (as well as geographical breakdown)

Data on economic derivative hedging

Data on own credit risk

Loan commitment and collateral data

60%40%20% 80% 100%0%

For the Controlling function, the ability to reconcile IFRS-compliant values with CRR-compliant values represents an immense challenge. Likewise, the new impairment provisions under IFRS 9 are of importance for Controlling. Although the new requirements for own credit risk were vigorously

discussed in advance of the standard being issued, this topic is of lesser importance from the perspective of Controlling.

21Realignment of Financial Controlling |

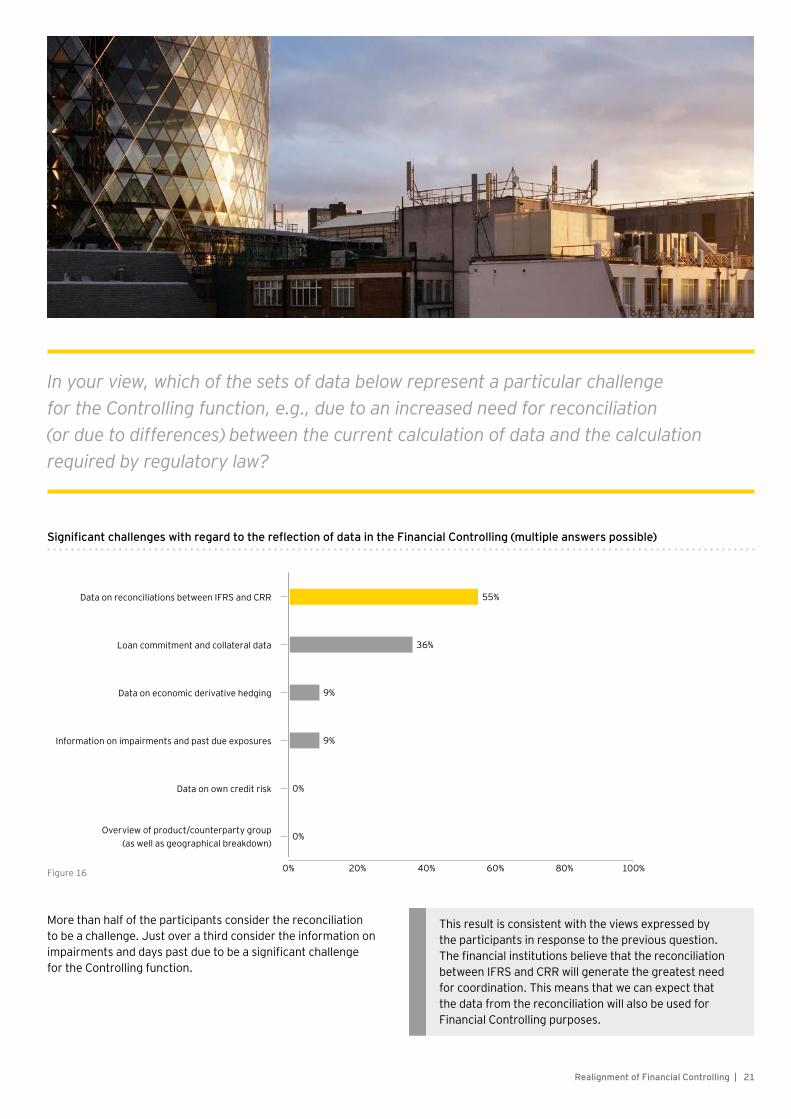

In your view, which of the sets of data below represent a particular challenge for the Controlling function, e.g., due to an increased need for reconciliation (or due to differences) between the current calculation of data and the calculation required by regulatory law?

9%

55%

0%

36%

0%

9%

Significant challenges with regard to the reflection of data in the Financial Controlling (multiple answers possible)

Figure 16

Information on impairments and past due exposures

Data on reconciliations between IFRS and CRR

Overview of product/counterparty group (as well as geographical breakdown)

Data on economic derivative hedging

Data on own credit risk

Loan commitment and collateral data

60%40%20% 80% 100%0%

This result is consistent with the views expressed by the participants in response to the previous question. The financial institutions believe that the reconciliation between IFRS and CRR will generate the greatest need for coordination. This means that we can expect that the data from the reconciliation will also be used for Financial Controlling purposes.

More than half of the participants consider the reconciliation to be a challenge. Just over a third consider the information on impairments and days past due to be a significant challenge for the Controlling function.

22 | Realignment of Financial Controlling

In your opinion, which of the following new topics/requirements have a direct impact on the Controlling function?

36 %

73 %

9 %

55 %

9 %

55 %

Requirements/topics with future impacts on financial Controlling (multiple answers possible)

Figure 17

Reporting of Asset Encumbrance and Forbearance

Risk Data Aggregation (BCBS 239)

Other

Balance Sheet Assessment

Reporting of Non-Performing Exposures

Asset Quality Review (AQR)

60 %40 %20 % 80 % 100 %0 %

The topic Risk Data Aggregation (BCBS 239) was mentioned most frequently by the participating financial institutions (around 73%). This is not surprising considering that one of the requirements of BCBS 239 is the standardization and aggregation of data for external disclosure and for internal performance management. In fulfilling this requirement, we believe that the Controlling function should not just be an affected party, but rather should play an active role. 55% of

the financial institutions also mentioned the topics Comprehensive Assessment and the Asset Quality Review that the former entails. In our opinion, this is due to the fact that the data requests made in this context not only related to Accounting and regulatory data, but also to planning data, which is the domain of the Financial Controlling function.

According to the participants, many of the topics mentioned in the questionnaire have a direct impact on the Controlling function. The majority of the participants (around 73%) mention

Risk Data Aggregation in particular. Further topics with a high number of mentions are the Balance Sheet Assessment and the Asset Quality Review.

23Realignment of Financial Controlling |

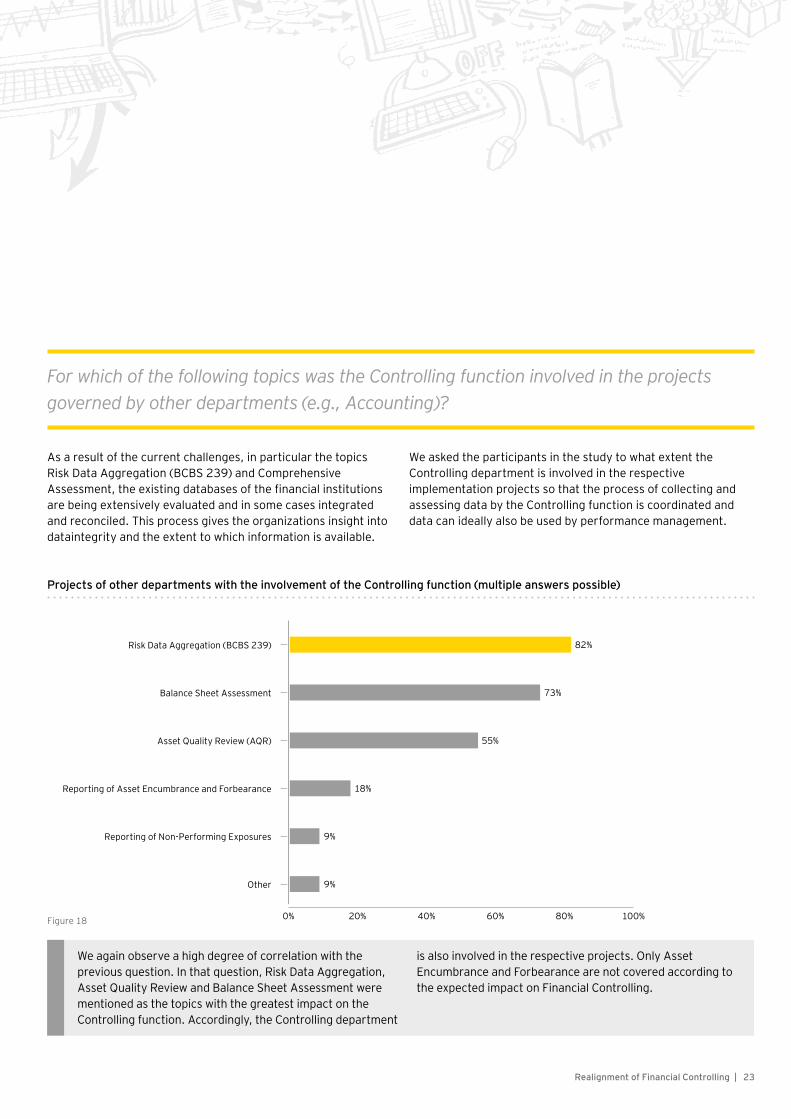

For which of the following topics was the Controlling function involved in the projects governed by other departments (e.g., Accounting)?

18%

82%

9%

73%

9%

55%

Projects of other departments with the involvement of the Controlling function (multiple answers possible)

Figure 18

Reporting of Asset Encumbrance and Forbearance

Risk Data Aggregation (BCBS 239)

Other

Asset Quality Review (AQR)

Reporting of Non-Performing Exposures

Balance Sheet Assessment

60%40%20% 80% 100%0%

We again observe a high degree of correlation with the previous question. In that question, Risk Data Aggregation, Asset Quality Review and Balance Sheet Assessment were mentioned as the topics with the greatest impact on the Controlling function. Accordingly, the Controlling department

is also involved in the respective projects. Only Asset Encumbrance and Forbearance are not covered according to the expected impact on Financial Controlling.

As a result of the current challenges, in particular the topics Risk Data Aggregation (BCBS 239) and Comprehensive Assessment, the existing databases of the financial institutions are being extensively evaluated and in some cases integrated and reconciled. This process gives the organizations insight into dataintegrity and the extent to which information is available.

We asked the participants in the study to what extent the Controlling department is involved in the respective implementation projects so that the process of collecting and assessing data by the Controlling function is coordinated and data can ideally also be used by performance management.

24 | Realignment of Financial Controlling

In its most recent publication dated February 2014, “A Sound Capital Planning Process: Fundamental Elements,” the Basel Committee on Banking Supervision once again emphasized in light of the financial crisis that the capital planning processes of some financial institutions were “not sufficiently comprehensive,” “not appropriately forward-looking” or “not adequately formalized.”

Against this backdrop, the new requirements of the CRR and of the CRD IV (Basel III), which are applicable for the first time in 2014, still have to prove themselves in practice. In all events, the multiple-year capital planning process, which has also been explicitly required by the MaRisk [“Mindestanforderungen an das Risikomanagement”: Minimum Requirements for Risk Management] since 2013, poses a significant challenge for financial institutions. The numerous and complex new regulations from the Basel III package are also subject to extensive transitional provisions, which extend as far as 2023. The key parameters influencing regulatory capital planning are the

numerous deductions, the new requirements for the prudential filters (in particular the regulatory measurement of fair value), the various capital buffers and the requirements for the eligibility of capital instruments (in particular the regulations on phase-out/in and on grandfathering).

The new requirements indicate that the multiple-year capital planning process will significantly increase in complexity as a result of the CRD IV package. This makes it all the more important to plan and implement this core process of integrated management with all participating organizational units in order to ensure the greatest possible accuracy and efficiency of data gathering and data processing.

2.5 Capital planning

25Realignment of Financial Controlling |

To what extent is your capital planning process coordinated with other departments?

Does the Controlling function coordinate capital planning with other departments?

Integration of the capital planning process in the overall planning process

Figure 19 Figure 20

■ Yes

■ No

■ The capital planning process is an integral part of the overall planning process.

■ The capital planning process is not or is only partially integrated in the overall planning process.

100% 100%

0% 0%

The current survey revealed that capital planning is already being coordinated with the other relevant departments and that the capital planning process is also part of the overall planning process. This result is not surprising. However, we can expect the intensity and frequency of these coordination processes to significantly increase in the future in order to ensure the regular and, by extension, appropriate review and

validation of the enhanced requirements. We can therefore conclude that the overall planning process should be examined for any weaknesses and potential delays and the existing processes aligned with the tasks at hand to ensure that the greater time and effort required in the future does not make the process too cumbersome.

26 | Realignment of Financial Controlling

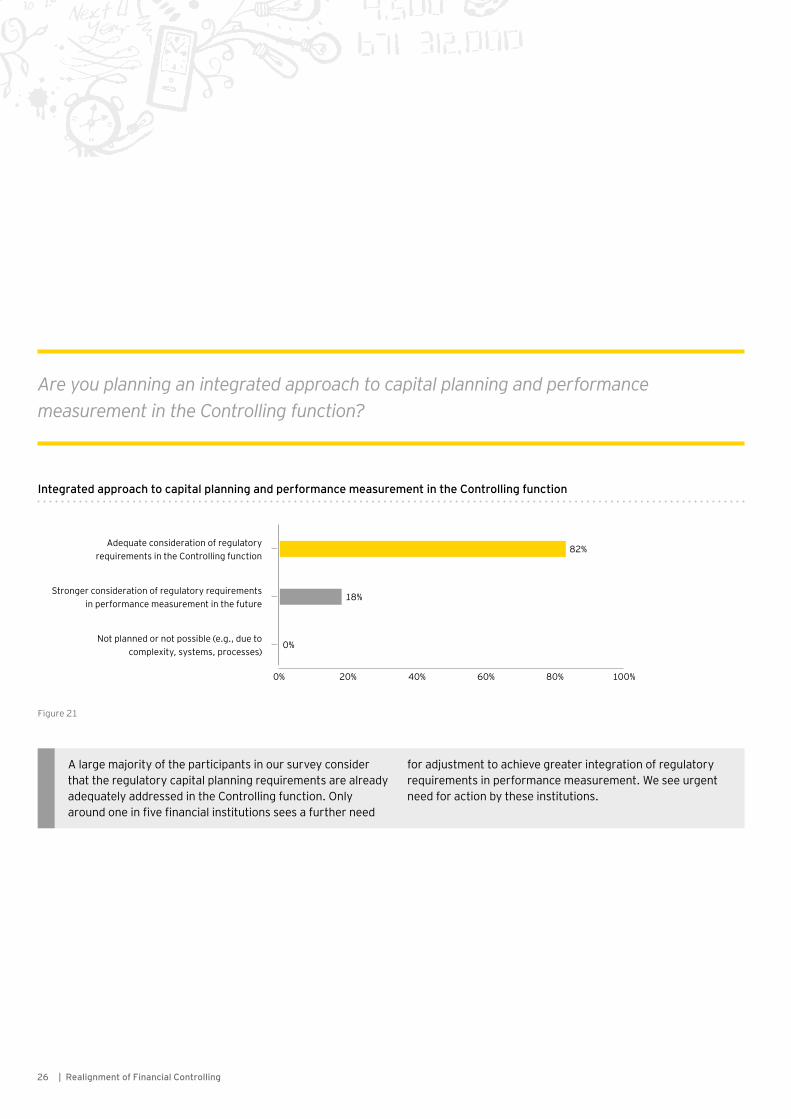

Are you planning an integrated approach to capital planning and performance measurement in the Controlling function?

A large majority of the participants in our survey consider that the regulatory capital planning requirements are already adequately addressed in the Controlling function. Only around one in five financial institutions sees a further need

for adjustment to achieve greater integration of regulatory requirements in performance measurement. We see urgent need for action by these institutions.

82%

18%

0%

Integrated approach to capital planning and performance measurement in the Controlling function

Figure 21

Not planned or not possible (e.g., due to complexity, systems, processes)

Stronger consideration of regulatory requirements in performance measurement in the future

Adequate consideration of regulatory requirements in the Controlling function

60%40%20% 80% 100%0%

27Neuausrichtung des Financial Controlling |

3.0Outlook

29Realignment of Financial Controlling |

As a result of the new regulatory requirements, the Controlling function may be facing a role change or paradigm shift. In your view, which statements apply to the Risk Management, Accounting, Controlling and Regulatory Reporting functions?

45%

100%

0%

91%

0%

82%

Impacts on functions: As a result of the new regulatory requirements and developments … (multiple answers possible)

Figure 22

... Controlling will provide greater support to the overall business strategy

... the individual finance units will be more closely integrated in terms of the content and focus of their work (more general and overarching expertise will be built up)

... the individual finance units will be segregated more strongly in terms of the content and focus

of their work (greater individual responsibility)

... finance will become more closely integrated overall

... there will be no relevant changes to the content and focus of the finance units’ work

... there will be a stronger focus on Regulatory Reporting

60%40%20% 80% 100%0%

30 | Realignment of Financial Controlling

In the context of the new regulatory requirements, a large majority of the surveyed financial institutions already have advanced projects in the implementation phase, with around half of the participants having launched an overall project and the rest smaller subprojects in order to address the various topics.

Interim solutions did not come into question for any of the participants. It is also apparent that the Controlling department is only responsible in most cases for the supply of the requested data and is not or hardly involved in decisions. This low level of involvement will lead to process and system adjustments further down the track. This will also require the realignment of the role of the Controlling function.

The need for an integrated and harmonized data architecture is also clear to most of the participants, but their awareness of this need is inconsistent with the current implementation projects. When it comes to the overall implementation of the requirements, a large majority of the surveyed financial institutions already have advanced projects in the implementation phase, with most of them implementing new processes rather than focusing on interim solutions. In contrast, it is interesting to note that the related IT support is mostly (63%) provided by interim solutions rather than existing systems (86%), with 64% of the financial institutions identifying a further need to adjust their IT systems, methods and processes. This need is driven by the current regulatory requirements, in particular Risk Data Aggregation (BCBS 239). With regard to the implications of Basel III, FinRep and the new capital adequacy legislation, we observed that 82% of the financial institutions surveyed consider the capital planning process to be mature with the financial control department being appropriately involved, while a fundamental realignment of the process could be necessary according to the remaining 18% in order to meet the new requirements.

The reconciliation between IFRS-compliant (Accounting standards) and CRR-compliant (regulatory requirements) asset values — primarily as a result of the strong need for coordination — is considered to be the greatest challenge. The biggest impact is caused by Risk Data Aggregation

(BCBS 239) — the area which most strongly affects the Controlling function and in which it has the strongest involvement. A large majority (73%) of the participants also plan to implement the new ratios to be reported (LR, LCR and NSFR) as key performance indicators in management reporting.

The results of the study suggest that the target role of the Controlling function has changed. The new regulatory requirements have triggered a new adjustment of methods and processes — driven by new challenges, in particular the convergence of IFRS and regulation, calls for a new, integrated data model and new key performance indicators such as LR, LCR and NSFR. It is also apparent that the Controlling department needs to be more involved in the relevant projects.

Future areas for action include the design, definition and embedding of new functions and areas, with structures across areas and functions to implement and monitor the regulatory requirements from the perspective of the bank as a whole gaining in importance.

Gunther TillmannPartnerPhone +49 6196 996 [email protected]

Thomas GriessPartnerPhone +49 6196 996 [email protected]

Dr. Ute FecklExecutive DirectorPhone +49 6196 996 [email protected]

Istvan SimonSenior ManagerPhone +49 160 939 [email protected]

Contacts

31Realignment of Financial Controlling |

Imprint

PublisherErnst & Young GmbH WirtschaftsprüfungsgesellschaftMergenthalerallee 3–565760 Eschborn/Frankfurt am MainTelefon +49 711 9881 0Telefax +49 711 9881 550

ImagesGetty Images, Thinkstock Images

EY | Assurance | Tax | Transactions | Advisory

About the global EY organizationThe global EY organization is a leader in assurance, tax, transaction and advisory services. We leverage our experience, knowledge and services to help build trust and confidence in the capital markets and in economies the world over. We are ideally equipped for this task – with well trained employees, strong teams, excellent services and outstanding client relations. Our global purpose is to drive progress and make a difference by building a better working world – for our people, for our clients and for our communities.

The global EY organization refers to all member firms of Ernst & Young Global Limited (EYG). Each EYG member firm is a separate legal entity and has no liability for another such entity’s acts or omissions. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information, please visit www.ey.com.

In Germany, EY has 22 locations. In this publication, “EY” and “we” refer to all German member firms of Ernst & Young Global Limited.

© 2014 Ernst & Young GmbH WirtschaftsprüfungsgesellschaftAll Rights Reserved.

BKL 1502-009(14)ED None

In line with EY’s commitment to minimize its impact on the environment, this document has been printed on FSC®-certified paper that consists of 60% recycled fibers.

This publication contains information in summary form and is therefore intended for general guidance only. Although prepared with utmost care this publication is not intended to be a substitute for detailed research or the exercise of professional judgment. Therefore no liability for correctness, completeness and/or currentness will be assumed. It is solely the responsibility of the readers to decide whether and in what form the information made available is relevant for their purposes. Neither Ernst & Young GmbH Wirtschaftsprüfungsgesellschaft nor any other member of the global EY organization can accept any responsibility. On any specific matter, reference should be made to the appropriate advisor.

www.de.ey.com