reardon massachusetts housing institute

TRANSCRIPT

We’re Not as Young as We Used to Be

Tim Reardon

Metropolitan Area Planning Council

Massachusetts Housing Institute

June 14, 2016

And other less self-evident

Observations and Projections

of Demographics and Housing

in Metro Boston

Housing demand:

Population growth is only

half the equation (or less)

Mary’s Household

2000 - 2040

2000,

age 45

2020,

age 65

2040,

age 85

2010,

age 55

3.22

2.84

2.69

2.532.50

2.38

2.31

2.282.20

2.30

2.40

2.50

2.60

2.70

2.80

2.90

3.00

3.10

3.20

3.30

1970 1980 1990 2000 2010 2020 2030 2040

Avera

ge N

um

ber

of

Peop

le p

er

Hou

sehold

Average Household Size, Metro Boston, 1970 - 2040

1990 - 2010 Status Quo Projections

10% drop

projected

2010 - 2040

23% decline

since 1970

Source: Decennial Census,

MAPC Population Projections 2014www.mapc.org/projections

Same number of residents form more

households, need more housing units

2010

2040

250 people =

250 people =

Dozens of communities may see

housing growth + population decline

Housing production is a

prerequisite to long-term

economic growth in Massachusetts

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

15 -19

20 -24

25 -29

30 -34

35 -39

40 -44

45 -49

50 -54

55 -59

60 -64

65 -69

70 -74

75 -79

80 -84

85plus

Age

2040, Status Quo

Baby Boomers

comprise 49% of

MA labor force

1.4 million workers

born before 1970

will retire by 2030

(39% of labor force)

State is not producing

or importing enough

young workers to fill

vacant positions

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

2010

In Labor Force Not In Labor Force

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

2020, Status Quo

Baby

Boomers

Baby

Boomers

Baby

Boomers

Source: MAPC Population Projections 2014

A Stronger Region is Possible

Continued

outmigration

=

no labor force

growth2,543,000

2,509,000

2,526,000

2,400,000

2,450,000

2,500,000

2,550,000

2,600,000

2,650,000

2,700,000

2,750,000

2010 2020 2030 2040

Population in the Labor Force, Metro Boston, 2010 - 2040,

Status Quo vs. Stronger Region

Status Quo

2,543,000

2,509,000

2,526,000

2,515,500

2,616,000

2,643,000

2,690,000

2,400,000

2,450,000

2,500,000

2,550,000

2,600,000

2,650,000

2,700,000

2,750,000

2010 2020 2030 2040

Population in the Labor Force, Metro Boston, 2010 - 2040,

Status Quo vs. Stronger Region

Status Quo

Stronger Region

Net in-migration of

10,000 per year

=

+175,000 workers

by 2040

(7% increase)

Long-term economic growth requires 435,000 new units in Metro Boston,

~500,000 units statewide, by 2040

139,000 155,000

11,000 6,000

53,000

91,000

95,000

178,000

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

Status Quo Stronger Region

Total Net Housing Demand, by Type, Metro Boston, 2010 - 2040

Multi-Family -Rent

Multi-Family -Own

Single Family -Rent

Single Family -Own

Source: MAPC Population Projections, 2014

Baby Boomers will supply more

housing than they demand

Baby Boomers are occupying as many

housing units as they ever will

318,000 383,000 352,000

282,000

165,000

95,000

120,000 132,000

117,000

73,000

140,000

171,000 166,000

170,000

130,000

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

2000 2010 2020 2030 2040

Hou

sing U

nit D

em

and

Baby Boomer (1946 - 1965) Housing Demand, Metro Boston, 2010 - 2040, Stronger Region Scenario

Multifamily Rent

Multifamily Own

Single FamilyRent

Single FamilyOwn

Source: 2000 Census ,

2006 – 2010 American Community Survey,

MAPC Population Projections 2014

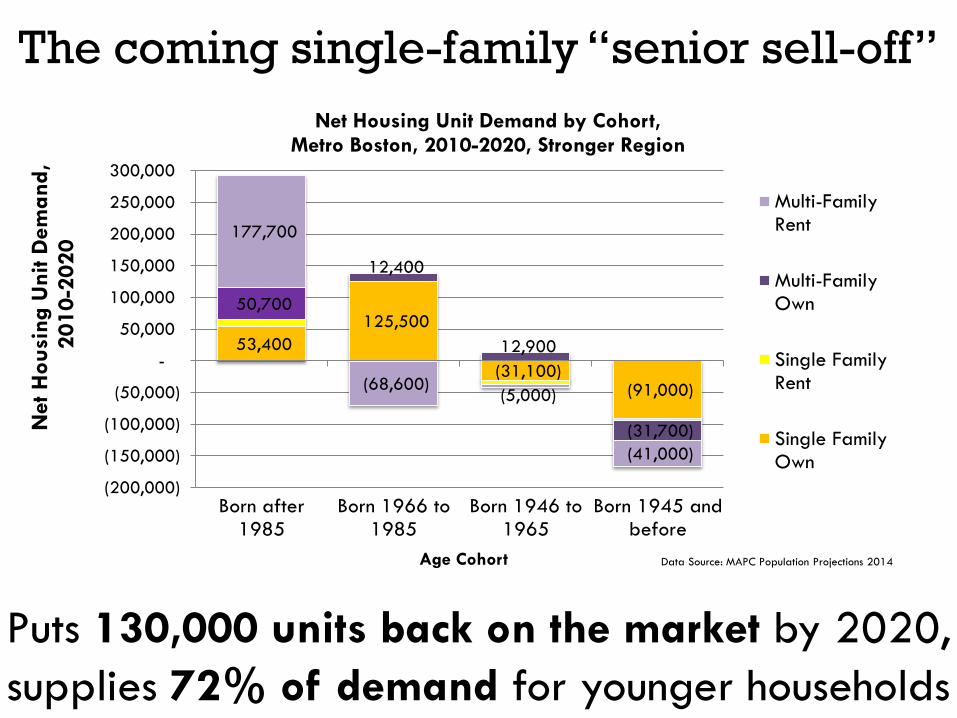

The coming single-family “senior sell-off”

53,400

125,500

(31,100)(91,000)

50,700

12,400

12,900

(31,700)

177,700

(68,600)(5,000)

(41,000)

(200,000)

(150,000)

(100,000)

(50,000)

-

50,000

100,000

150,000

200,000

250,000

300,000

Born after1985

Born 1966 to1985

Born 1946 to1965

Born 1945 andbefore

Net H

ou

sing U

nit D

em

and

,2

01

0-2

02

0

Age Cohort

Net Housing Unit Demand by Cohort, Metro Boston, 2010-2020, Stronger Region

Multi-FamilyRent

Multi-FamilyOwn

Single FamilyRent

Single FamilyOwn

Data Source: MAPC Population Projections 2014

Puts 130,000 units back on the market by 2020,

supplies 72% of demand for younger households

Tastes Are Changing,

Or Are They?

Multifamily occupancy increased for all age groups

Steepest increases among Millennials and Baby BoomersSource: 2006 – 2010 American Community Survey, 2000 Census

Multifamily Occupancy is Growing

0.2%

7.0%

4.5%

0.8%

2.4% 2.5%

3.8%

0.8% 0.7%

0%

1%

2%

3%

4%

5%

6%

7%

8%

15-24 25-34 35-44 45-54 55-59 60-64 65-69 70-74 75 plus

Ch

an

ge in

Perc

en

t o

f H

ou

seh

old

s in

Multif

am

ily H

ou

sing

Age of Householder

Change in Multifamily Occupancy Rates, 2000 to 2010, Metro Boston

An Urban Resurgence is Underway

-80,000

-60,000

-40,000

-20,000

0

20,000

40,000

60,000

80,000

100,000

0 -4

5 -9

10 -14

15 -19

20 -24

25 -29

30 -34

35 -39

40 -44

45 -49

50 -54

55 -59

60 -64

65 -69

70 -74

75 -79

80 -84

85plus

Net M

igra

nts

in

/(ou

t) in

Pre

vio

us

Deca

de

Age at End of Decade

Net Migration by Age, 1990s and 2000s, Inner Core and Regional Urban Centers

1990 - 2000

2000 - 2010

Source: U.S. Census, MassCHIP, MAPC Analysis

Urban municipalities attracted/retained 30,000

additional residents as compared to the 1990s

A New Lanscape of Housing Demand

Metro Boston will need 435,000 new units by 2040

Most housing demand will be in urban communities

Two-thirds of demand will be for multifamily

21%42%

60% 64%

24%21%

18%

16%

55%

38% 23%

18%

-

20,000

40,000

60,000

80,000

100,000

120,000

Inner Core Regional UrbanCenters

MaturingSuburbs

DevelopingSuburbs

Pro

ject

ed

Hou

sing U

nit D

em

and

, 2

01

0 -

20

30

Housing Unit Demand by Type and Tenure, 2010 - 2030, Stronger Region Scenario

Metro Boston Community Types

Multifamily -Rent

Multifamily -Own

Single Family -Own

75,900

63,201

80,600

108,800

It’s not just a housing problem

25 years of wage polarization

Data Sources: U.S. Census Public Use Microdata Sample 1990 and 2010-14

-100,000-80,000 -60,000 -40,000 -20,000 0 20,000 40,000 60,000 80,000 100,000

Healthcare Practitioners and Technical

Management, Business, Science, and Arts

Education, Training, and Library

Computer and Mathematical

Community and Social Services

Life, Physical, and Social Science

Legal

Protective Service

Personal Care and Service

Food Preparation and Serving

Transportation and Material Moving

Production

Construction and Extraction

Sales and Related

Building and Grounds Maintenance

Healthcare Support

Office and Administrative Support

Farming, Fishing, and Forestry

Architecture and Engineering

Business Operations Specialists

Installation, Maintenance, and Repair

Occupational Group Change by Household Income Category; Metro Boston, 1990 to 2014

Extremely Low-Income Very Low-Income Low-Income Lower Middle-Income Upper Middle-Income High-Income

Decline in “core”

middle income

occupations

Low-income growth,

middle income

decline

Disproportionate

low-income growth

Disproportionate

high-income growth

The Incredible Shrinking Middle Class

126%46%

15%

-1% -4%

33%

(20,000)

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

Working Households by Income CategoryMetro Boston, 1990 - 2014

Extremely Low-Income

Very Low-Income

Low-Income

Lower Middle-Income

Upper Middle-Income

High-Income

Change in number of households

Percent growth

Data Sources: U.S. Census Public Use Microdata Sample 1990 and 2010-14

Middle-Income Working

Households down 3%

Projected New Worker Households

8%

11%

13%

14%

9%

44%

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

500,000

Projected New Worker Households

Metro Boston, 2015 - 2030

High-Income

Upper Middle-Income

Lower Middle-Income

Low-Income

Very Low-Income

Extremely Low-Income

Data Sources: U.S. Census Public Use Microdata Sample 1990 and 2010-14

Over 800,000+ new workers needed by 2030

to fill vacancies left by

retiring Baby Boomers.

These workers will likely

form 492,000 new working

households.

Almost one-third of new

working households will

be low income.

Housing production is an economic imperative for

Massachusetts and its communities

The calculus for assessing the impacts of housing

production is changing radically and rapidly

Boomer downsizing satisfies only a portion of

demand created by younger households

Long-term trends will drive continued demand

for urban & multifamily housing

Sustainable solutions to the affordable housing

crisis require economic policy interventions

Tim Reardon, Director of Data Services

Metropolitan Area Planning Council

www.mapc.org/projections

www.housing.ma