recognizing loss across borders: more than meets the … i. overview ii. loss recognition...

TRANSCRIPT

1 1

Recognizing Loss Across Borders:

More than Meets the Eye

Daniel C. White

Philip B. Wright

April 23, 2015 (updated)

St. Louis International Tax Group, Inc.

2

I. Overview

II. Loss Recognition Transactions

A. Insolvent Subsidiary Liquidations – Rev. Rul. 2003-125

B. Sale or Exchange Transactions – Granite Trust

III. General Loss Tax Consequences

IV. Collateral Loss Tax Consequences

V. Examples

Overview

3

A. Insolvent Subsidiaries and Rev. Rul. 2003-125

– Section 332 liquidation “only applies [when] the [controlling

corporate shareholder] receives at least partial payment for the

stock which it owns in the liquidating corporation.”

– Section 332 will not apply and transaction will be taxable under

Section 1001 if:

• Subsidiary is “balance sheet” insolvent. Morton v. Comm’r, 38

B.T.A. 1279 (1938), aff’d 112 F.2d 320 (7th Cir. 1940); or

• Subsidiary has multiple classes of stock and not all classes held by

controlling corporate shareholder receives proceeds in liquidation.

Spaulding Bakeries Inc., 27 T.C. 684 (1957), aff’d 252 F.2d 693(2nd

Cir. 1958); H. K. Porter, 87 T.C. 689 (1986)

– Liquidation of corporation, including by classification election, is

identifiable event. Rev. Rul. 2003-125

II.A Loss Recognition Transactions and

Rev. Rul 2003-125

4

• Section 331 and 336 apply to solvent corporate liquidations not described in Section

332. If a corporation is solvent but does not have one corporate shareholder

“controlling” the subsidiary, Section 332 will not apply. This generally requires full

recognition of gain or loss at the corporate and shareholder level.

– Section 1504(a)(2) defines “control,” generally 80% voting power and 80% value

– Control may be broken in contemplation of the liquidation transaction. Granite Trust Co., 238

F.2d 670 (1st Cir. 1956)

– Pre-liquidation transfers of subsidiary stock may be taxable or tax-free. Compare Sections

1001, 304 with Sections 170, 351(a)

– Nature of the transfer may alter the availability of the loss on the transferred portion. See

Section 267(f)

• Transaction could be a tax-free C reorganization if one corporation acquires

“substantially all properties” of the insolvent corporation, limiting loss recognition.

See Rev. Rul. 69-617 (upstream C reorganization); Treas. Reg. 1.368-2(d)(4)(anti-

Bausch & Lomb regulations); Norman Scott, 48 T.C. 598 (1967)(permitting insolvent

reorganization with affiliated shareholder/creditor)

II.B Loss Recognition Transactions and

Granite Trust

5

A.M. 2011-003 Illustrated

US-X

FS-Y

Debt

FS-Z

80%

20%

FS-Z is balance sheet insolvent

FS-Z changes its entity classification by election

(deemed liquidation)

FS-Z is deemed to distribute its assets subject to its

liabilities in liquidation, which are deemed

contributed to a new partnership

US-X

FS-Y

Debt

FS-Z

80%

20%

After the election, FS-Z is classified as a

partnership for US tax purposes.

6

• AM 2011-003 addresses many of the consequences of an insolvent liquidation of a first tier CFC with multiple owners. – Debt of CFC is not necessarily worthless. Since CFC becomes

partnership, the consolidated return rules do not apply to the FS-Z debt. no deemed satisfaction and reissuance (DSR).

– Under Treas. Reg. 1.1001-3, no transfer has occurred since payment expectations of creditors are not altered by classification change.

– Shareholder takes a cost basis in the assets; but see Est. of Franklin, 544 F.2d 1045 (9th Cir. 1976)(acquisition of assets for non-recourse debt far in excess of value).

– Liabilities assumed by new partnership limited to the value of the assets. Section 752(c).

Collateral Loss Tax Consequences:

Insolvent Subsidiary - Multiple Owners

7

Granite Trust Illustrated

US-X

FS-Y

FS-Y is balance sheet solvent but US-X

has a loss in FS-Y stock.

1. US-X transfers 21% of FS-Y stock to

Trust.

2. FS-Y elects to be changes its

classification by election.

US-X

Debt

79% 21% Trust

After the election, FS-Y is taxed as a

partnership.

Trust 1

2

FS-Y

8

• Section 1001(a) – “loss shall be the excess of the adjusted basis …over the amount realized”

• Section 165(a) – “There shall be allowed as a deduction any loss sustained during the taxable year and not compensated for by insurance or otherwise” – Closed, completed transaction; fixed by identifiable event. Treas.

Reg 1.165-1(b)

• Section 165(f) – “Losses from sales…of capital assets shall be allowed only to the extent allowed in sections 1211 and 1212”

• Section 267 may limit any loss on a sale or exchange transaction

III. General Loss Tax Consequences

9

• Section 165(g)(1) – “If any security which is a capital asset becomes worthless during the taxable year, the resulting loss shall…be treated as a loss from the sale, on the last day of the taxable year, of a capital asset.”

– A “security” means stock in a corporation, a right to receive stock, or evidence of indebtedness, issued by a corporation… with interest coupons or in registered form.

• Section 165(g)(3) -- any security in a corporation affiliated with a taxpayer which is a domestic corporation shall not be treated as a capital asset. A corporation is treated as affiliated if:

– the taxpayer owns directly stock in such corporation meeting the requirements of section 1504(a)(2) , and

– more than 90 percent of the aggregate of its gross receipts for all taxable years has been from sources other than royalties, rents, dividends, interest, annuities, and gains from sales or exchanges of stocks and securities.

• Timing -- Stock or debt obligation is worthless when it has neither liquidating value nor potential future value. Remember: Identifiable event requirement under Section 165.

III. General Loss Tax Consequences:

Section 165

10

• Treatment of related party debt as equity may prevent insolvency. Classification may be challenged if: – Excessive advances

– Lack of attention to form

– Sweep accounts without clear terms

– Debt arbitrarily created (pushdowns)

– Section 385(c)--Debtor cannot contest its own characterization of the instrument.

• Loss may be permitted if the debt is treated as preferred equity but may be limited to the basis in the common stock. See CCA 200706011 (if debt enforceable under state law and re-classified as “preferred” equity, Spaulding Bakeries applies to claim loss).

• If obligation not respected as enforceable, advances treated as capital contributions. Subsidiary may not be insolvent and could be tax-free. Development Corp. of America Inc., T.C. Memo 1988-127 (1988).

III. Classification of Indebtedness

“True” debt, preferred equity, or “capital”

11

• Section 166(a)(1) – deduction permitted when debt

becomes worthless in a year

– Partial worthlessness permitted as well. Section 166(a)(2)

• Whether debt becomes worthless, in whole or in part, is

a factual determination. Boehm v. Comm’r, 326 U.S. 287

(1946).

• When corporate shareholder holds debt of wholly-owned

subsidiary and subsidiary transfers all of its assets in

partial satisfaction of that debt, corporate shareholder

entitled to both worthless stock loss and partial bad debt

deduction. Rev. Rul. 70-489.

III. General Loss Tax Consequences:

Worthless Indebtedness

12

• Insolvent liquidation is generally a taxable disposition by

debtor corporation of all assets subject to all liabilities.

A.M. 2011-003

• Section 61(a)(12) – income includes discharge of

indebtedness

• Section 108(a)(1)(B) -- Gross income does not include

discharge of indebtedness of the taxpayer if the

discharge occurs when the taxpayer is insolvent

III. Loss Tax Consequences:

Subsidiary Tax Consequences

13

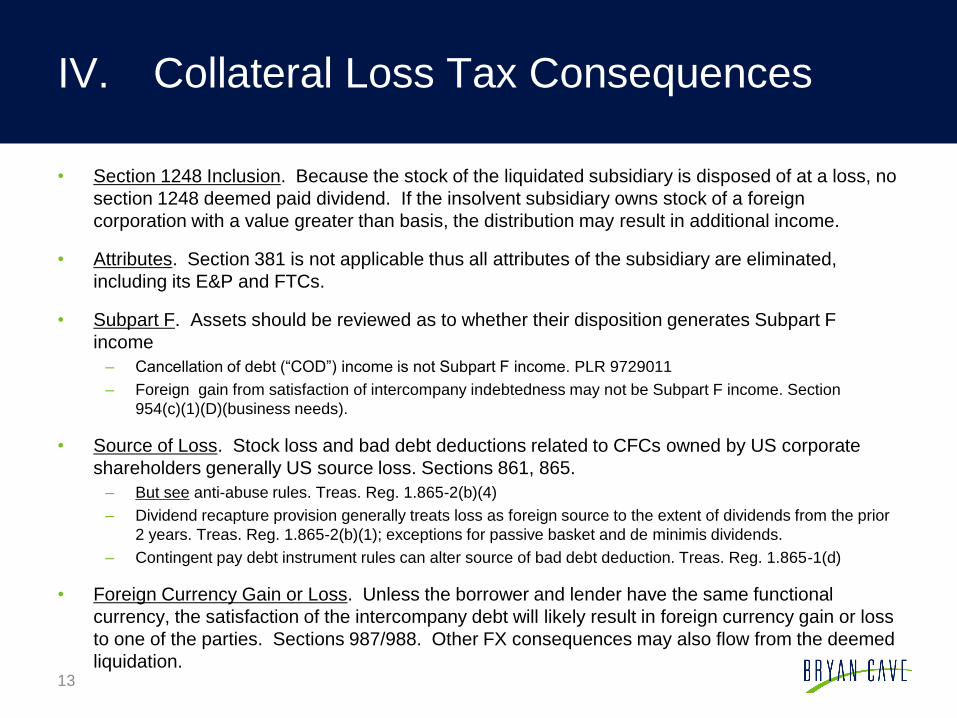

• Section 1248 Inclusion. Because the stock of the liquidated subsidiary is disposed of at a loss, no

section 1248 deemed paid dividend. If the insolvent subsidiary owns stock of a foreign

corporation with a value greater than basis, the distribution may result in additional income.

• Attributes. Section 381 is not applicable thus all attributes of the subsidiary are eliminated,

including its E&P and FTCs.

• Subpart F. Assets should be reviewed as to whether their disposition generates Subpart F

income

– Cancellation of debt (“COD”) income is not Subpart F income. PLR 9729011

– Foreign gain from satisfaction of intercompany indebtedness may not be Subpart F income. Section

954(c)(1)(D)(business needs).

• Source of Loss. Stock loss and bad debt deductions related to CFCs owned by US corporate

shareholders generally US source loss. Sections 861, 865.

– But see anti-abuse rules. Treas. Reg. 1.865-2(b)(4)

– Dividend recapture provision generally treats loss as foreign source to the extent of dividends from the prior

2 years. Treas. Reg. 1.865-2(b)(1); exceptions for passive basket and de minimis dividends.

– Contingent pay debt instrument rules can alter source of bad debt deduction. Treas. Reg. 1.865-1(d)

• Foreign Currency Gain or Loss. Unless the borrower and lender have the same functional

currency, the satisfaction of the intercompany debt will likely result in foreign currency gain or loss

to one of the parties. Sections 987/988. Other FX consequences may also flow from the deemed

liquidation.

IV. Collateral Loss Tax Consequences

14

• If the foreign subsidiary was insolvent, it was likely

operating at a loss. Following the transaction, the losses

of the subsidiary will be earned by the US group and

contribute to the consolidated group.

– Consider how this impacts your ability to use foreign tax credits

going forward

– If you have an overall foreign loss (“OFL”), this will increase the

OFL balance

– If you want to use these losses in the US, consider the dual

consolidated loss limitations under Section 1503(d)

• Consider SRLY implications on domestic use of any such losses

– If subsidiary turns to operating profit, overall domestic loss rule

can apply

IV. Collateral Loss Tax Consequences:

Subsequent to the Loss Recognition

15

• Dual Consolidated Loss (“DCL”) is a net operating loss of a dual resident corporation (“DRC”) or separate unit of a US corporation.

• DRC includes a US corporation subject to tax in a foreign country

• Separate unit includes a branch or hybrid entity.

• DCL cannot be used to offset income of US person if it can be used to offset income of a foreign corporation. Treas. Reg. 1.1503(d)-2, -4.

• But see Domestic use election. Treas. Reg. 1.1503(d)-6(d)

• Recapture of DCL upon disposition (foreign use, disposition of 50+% in the unit in 12 months, DRC leaves consolidated group, failure of annual certification)

IV. Collateral Loss Tax Consequences:

Dual Consolidated Losses

16

• If debt of insolvent subsidiary survives the liquidation of the subsidiary, the owner is member of the consolidated group, and the creditor is a member of the consolidated group, the debt is deemed satisfied and reissued (“DSR”) after joining the group. Treas. Reg. 1.1502-13(g)(5)(i)(A). – DSR has the effect of satisfying the “old” debt at its FMV and

then reissuing “new” debt with an issue price equal to the same price for cash.

– If the face amount of the debt exceeds this issue price (and the note has a maturity greater than 1 year), the note has original issue discount under Section 1273.

– Items taken into account in the DSR are treated as separate not consolidated items. Treas. Reg. 1.1502-13(g)(6)(i)(B).

IV. Collateral Loss Tax Consequences:

Consolidated Intercompany Debt Issues

17

• Shareholder/Lender – Gain/loss on stock

– Character

– Gain/loss on debt (worthlessness)

– FX

– Source

– Basis in Acquired Property

– Other

• Borrower – Gain/loss on assets

– COD income

– Subpart F income

– Attributes (E&P, FTC, etc.)

– FX

– Other

• Ongoing Issues – OFL

– DCL

– FTC utilization group-wide

– Other

V. Example: Base Case

Considerations in Analyzing Examples

18

V. Example: Base Case

FS1 owes USS $100X in debt, its only liability

FS1 owns assets with a fair value of $70X.

Transaction: USS checks-the-box of FS1 (Rev. Rul. 2003-125)

Tax Considerations:

1. Section 165(g)(1), 165(g)(3) for the stock basis in FS1

2. Section 166 loss equal to $30X on debt, extinguished in

transaction

3. COD income of FS1 excluded from Subpart F income

4. Section 304 will not apply to the deemed sale of FS3 to USS

(Rev. Rul. 74-605) but treated as a taxable disposition of stock

in a lower tier CFC

5. Attributes of FS1 such as PTI, FTCs permanently lost

6. Assuming no actual or deemed dividends from FS1 in the last 2

years, stock losses are US source

7. Depending on the currency of the debt, FX gain or loss at either

USS or FS1. Consider whether FX gain at FS1 is Subpart F

income

8. Consider impact of operating losses of FS1 as a branch on tax

credits or OFL balance

9. Consider making domestic use election under DCL regime,

subject to recapture

10. Review credit agreement to see if FS1 as DRE must pledge

100% of its equity or be a guarantor

1

19

V. Example: Base Case - USP Debt

FS1 owes USP $100X in debt, its only liability

FS1 owns assets with a fair value of $70X.

Transaction: USS checks-the-box of FS1

Tax Considerations:

1. Section 165(g)(1), 165(g)(3) for the stock basis in FS1

2. No bad debt deduction under AM 2011-003. Debt subject to DSR

under Treas. Reg. 1.1502-13(g)(5)(ii), potentially creating OID for

future periods (income to USP; deductions to USS)

3. COD income of FS1 excluded from Subpart F income

4. Section 304 will not apply to the deemed sale of FS3 to USS but treated

as a taxable disposition of stock in a lower tier CFC

5. Attributes of FS1 such as PTI, FTCs permanently lost

6. Assuming no actual or deemed dividends from FS1 in the last 2 years,

stock losses are US source

7. Depending on the currency of the debt, FX gain or loss at either USS or

FS1. Consider whether FX gain at FS1 is Subpart F income. If debt is

not US dollar denominated, FX items become intercompany items

8. Consider impact of operating losses of FS1 as a branch on tax credits

or OFL balance

9. Consider making domestic use election under DCL regime, subject to

recapture

10. Review credit agreement to see if FS1 as DRE must pledge 100% of its

equity or be a guarantor

1

20

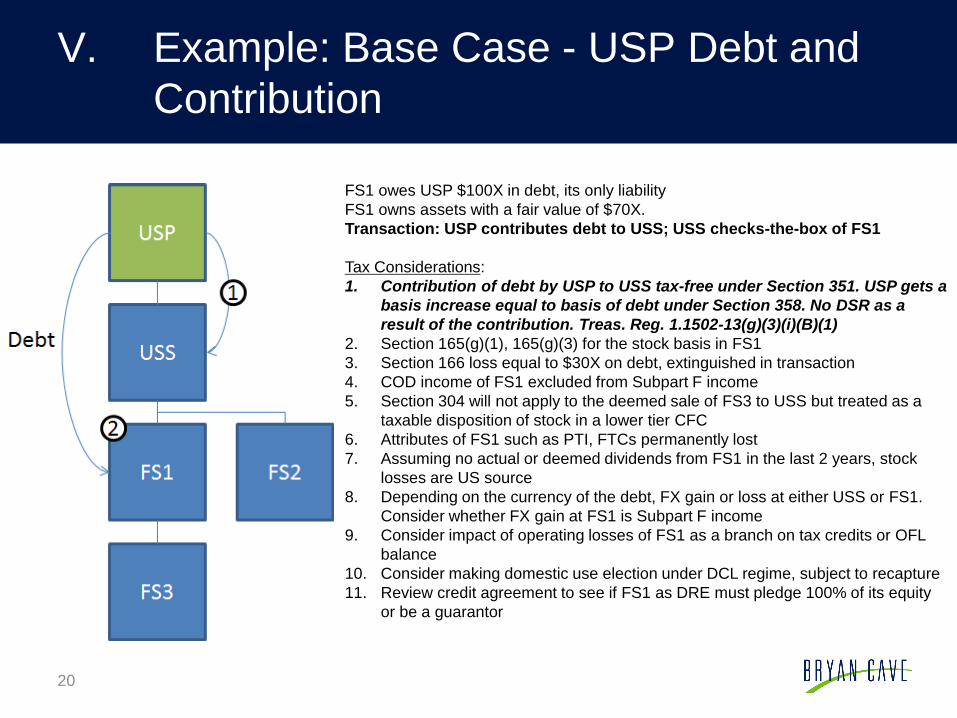

V. Example: Base Case - USP Debt and

Contribution

FS1 owes USP $100X in debt, its only liability

FS1 owns assets with a fair value of $70X.

Transaction: USP contributes debt to USS; USS checks-the-box of FS1

Tax Considerations:

1. Contribution of debt by USP to USS tax-free under Section 351. USP gets a

basis increase equal to basis of debt under Section 358. No DSR as a

result of the contribution. Treas. Reg. 1.1502-13(g)(3)(i)(B)(1)

2. Section 165(g)(1), 165(g)(3) for the stock basis in FS1

3. Section 166 loss equal to $30X on debt, extinguished in transaction

4. COD income of FS1 excluded from Subpart F income

5. Section 304 will not apply to the deemed sale of FS3 to USS but treated as a

taxable disposition of stock in a lower tier CFC

6. Attributes of FS1 such as PTI, FTCs permanently lost

7. Assuming no actual or deemed dividends from FS1 in the last 2 years, stock

losses are US source

8. Depending on the currency of the debt, FX gain or loss at either USS or FS1.

Consider whether FX gain at FS1 is Subpart F income

9. Consider impact of operating losses of FS1 as a branch on tax credits or OFL

balance

10. Consider making domestic use election under DCL regime, subject to recapture

11. Review credit agreement to see if FS1 as DRE must pledge 100% of its equity

or be a guarantor

21

V. Example: Granite Trust - Section 304

Scenario

FS1 owes USS $100X in debt, its only liability

FS1 owns assets with a fair value of $70X.

Transaction: USP sells 25% of FS1 to FS2 for cash; USS checks-the-box of

FS1

Tax Considerations:

1. Sale is described in Section 304(a)(1). Dividend depends on E&P of FS1 and

FS2. Deemed Section 351 results in GRA requirement under Section 367.

Section 362(e)(2) election on where stock loss resides (FS2 stock or FS1

stock)

2. Sections 165(g)(1), 331 for the stock basis in FS1 to USS and FS2. Consider

C reorganization risk

3. No bad debt deduction under AM 2011-003. FS1 as a partnership takes

assets with a basis equal to $100X. Only $70X of debt taken into account

under Section 752(c)

4. COD income of FS1 excluded from Subpart F income

5. Section 304 will not apply to the deemed sale of FS3, but likely treated as a

taxable disposition of stock in a lower tier CFC

6. Attributes of FS1 such as PTI, FTCs permanently lost

7. Assuming no actual or deemed dividends from FS1 in the last 2 years, stock

losses are US source

8. Depending on the currency of the debt, FX gain or loss at either USS or FS1.

Consider whether FX gain at FS1 is Subpart F income

9. Consider impact of operating losses of on tax credits or OFL balance

10. Review credit agreement to see if FS1 must pledge its equity or be a

guarantor

22

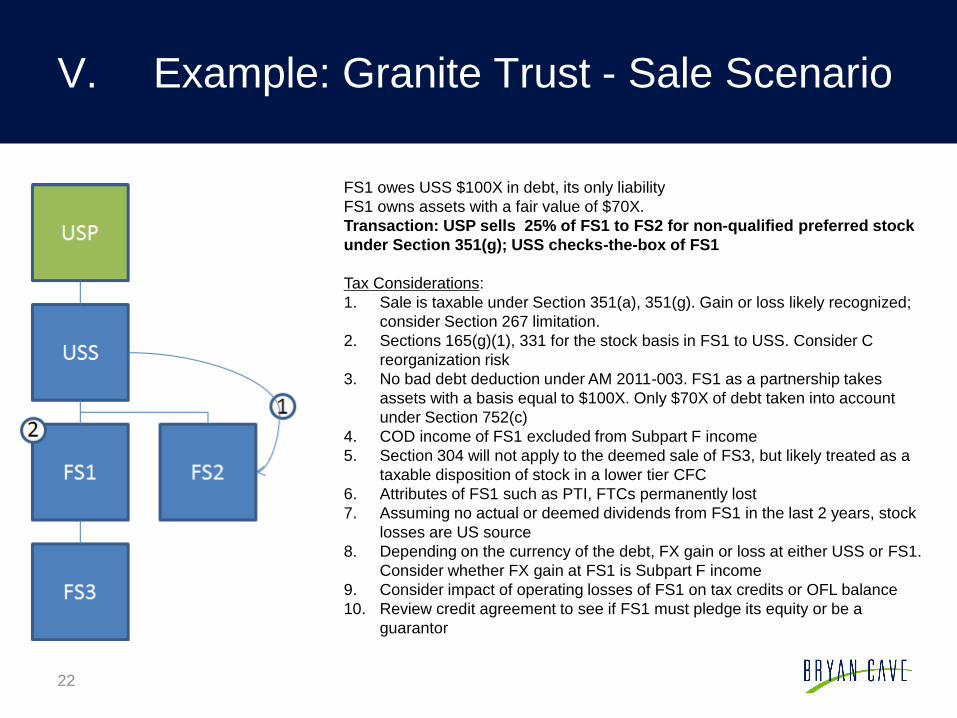

V. Example: Granite Trust - Sale Scenario

FS1 owes USS $100X in debt, its only liability

FS1 owns assets with a fair value of $70X.

Transaction: USP sells 25% of FS1 to FS2 for non-qualified preferred stock

under Section 351(g); USS checks-the-box of FS1

Tax Considerations:

1. Sale is taxable under Section 351(a), 351(g). Gain or loss likely recognized;

consider Section 267 limitation.

2. Sections 165(g)(1), 331 for the stock basis in FS1 to USS. Consider C

reorganization risk

3. No bad debt deduction under AM 2011-003. FS1 as a partnership takes

assets with a basis equal to $100X. Only $70X of debt taken into account

under Section 752(c)

4. COD income of FS1 excluded from Subpart F income

5. Section 304 will not apply to the deemed sale of FS3, but likely treated as a

taxable disposition of stock in a lower tier CFC

6. Attributes of FS1 such as PTI, FTCs permanently lost

7. Assuming no actual or deemed dividends from FS1 in the last 2 years, stock

losses are US source

8. Depending on the currency of the debt, FX gain or loss at either USS or FS1.

Consider whether FX gain at FS1 is Subpart F income

9. Consider impact of operating losses of FS1 on tax credits or OFL balance

10. Review credit agreement to see if FS1 must pledge its equity or be a

guarantor

23

V. Example: Granite Trust – Section 351

Scenario

FS1 owes USS $100X in debt, its only liability

FS1 owns assets with a fair value of $70X.

Transaction: USP contributes 25% of FS1 to FS2; USS checks-the-box of FS1

Tax Considerations:

1. Contribution of FS1 stock should be tax-free under Section 351. Section 367

GRA requirements. Section 362(e)(2) election on where stock loss resides

(FS2 stock or FS1 stock)

2. Section 165(g)(1), 331 for the stock basis in FS1 to USS and FS2; consider C

reorganization risk.

3. No bad debt deduction under AM 2011-003. FS1 as a partnership takes

assets with a basis equal to $100X. Only $70X of debt taken into account

under Section 752(c)

4. Asset gain or loss recognized under Section 336

5. Section 304 will not apply to the deemed sale of FS3 but likely treated as a

taxable disposition of stock in a lower tier CFC

6. Attributes of FS1 such as PTI, FTCs permanently lost

7. Assuming no actual or deemed dividends from FS1 in the last 2 years, stock

loss of USS is US source

8. Depending on the currency of the debt, FX gain or loss at either USS or FS1.

Consider whether FX gain at FS1 is Subpart F income

9. Consider impact of operating losses of FS1 on tax credits or OFL balance

10. Review credit agreement to see if FS1 must pledge its equity or be a

guarantor

24